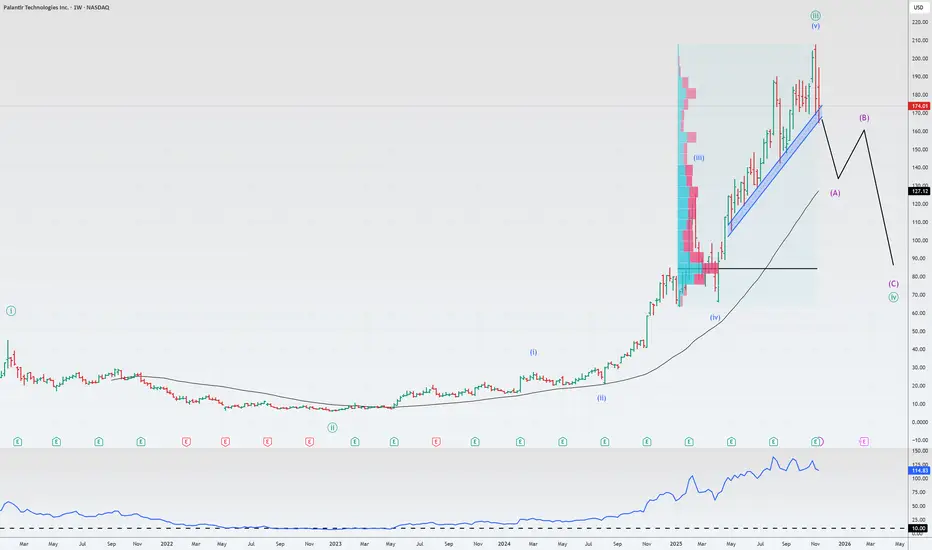

PLTR US🌎Palantir: Rocket Growth vs. Sky-High Valuation. Which Will Outweigh the Other?

The quarterly results are very strong, but investors face significant risks. Let's break it down.

🚀 Strengths:

Explosive revenue: $1.18 billion (+63% YoY), EPS: $0.21. Both metrics beat expectations.

Brighter-than-expected future: Q4 guidance ($1.33 billion) and 2025 guidance (~$4.4 billion) are significantly higher than consensus.

Commercial: 121% YoY growth in the US. This is the company's main driver.

Sales are strong: Closed contracts worth $2.8 billion. The client base grew to 911 companies (+45%).

Super-efficient: Revenue +63%, while headcount is only up 10%. An operating margin of 51% is fantastic.

AI is the fuel: Products like AIP are accelerating adoption, and customers are switching en masse to the Palantir platform.

⚠️ What's scary: Risks and "buts"

The price is sky-high: A P/S ratio of 110+ is nonsense, even for a growing company. Market cap is growing faster than revenue.

The model predicts a collapse: Under optimistic scenarios (40% annual growth), the fair price could be tens of percent lower than the current one.

Share dilution: Share-based compensation (SBC) eats up 24% of revenue—a huge amount. Insiders are actively selling.

Shorted a billion: The legendary Michael Burry bought put options on 5 million shares, betting against PLTR. He believes the AI sector is inflating.

Vulnerability: Business is concentrated in the US, creating regulatory and macro risks. Europe is experiencing stagnation.

A3minvestments

SOBHA IN🌎Sobha is a vertically integrated luxury real estate developer in India.

The company controls the entire value chain, including structural manufacturing, joinery, and finishing, ensuring quality and timeliness.

The company is expected to reduce its dividend payout from 32% to 6.5%, freeing up more capital for reinvestment in growth and potentially increasing ROE to 11% in the future.

P/B 3.6

P/S 3.9

ROE 2.2% 👆

Revenue

2022 | 32.6 B

2023 | 30.3 B

2024 | 40.3 B

Net Profit

2022 | 1.04 B

2023 | 0.49 B

2024 | 0.94 B

We expect revenue and profit growth in the coming years, as well as an increase in FCF

AIMTRON IN (Aimtron Electronics)Aimtron Electronics Limited (NSE: AIMTRON) is an Electronics Technology company specializing in Electronic System Design and Manufacturing (ESDM). It offers a wide range of services including Printed Circuit Board (PCB) design, assembly, and complete electronic system manufacturing ('Box Build').

The company serves global clients in the areas of Industrial Automation, Electric Vehicles, IoT, Medical Devices, Robotics and more

Aimtron focuses on precision engineering and complex electronic systems

The company serves over 500 global customers, including the US, UK, India, Hong Kong, Spain and Mexico markets

Aimtron Electronics successfully completed its IPO in June 2024, wherein 54,04,800 equity shares were issued at a price of Rs 161 per share.

This allowed the company to raise Rs 87.01 crore

The proceeds from the IPO were partially used to increase equity capital.

One of the key objectives of the IPO was to pay off debt.

The company has significantly reduced its debt burden

The shares are trading at a high valuation.

P/E 59

P/S 9.5

👆Such a high valuation is explained by operational and financial performance, and investors are giving a significant premium for such business growth

Revenue over the past year has grown by 71%, and net profit by 89%

ROE is 24.9% This indicates an efficient use of capital.

The company has almost no debt

The main reason for the growth of the shares was strong earnings growth

Aimtron's board of directors has met several times to discuss plans to attract additional capital

The company has already begun expanding its production capacity.

In fiscal 2025, it added a new surface mount (SMT) line, which increased production capabilities

The funds raised will be used for further capital investments in equipment, meeting working capital needs and general corporate purposes, including expanding its international presence

BFH US🌎Bread Financial is a technology-driven financial services company. Its core business is providing data-driven, personalized solutions for payments, loans, and savings. Key areas include:

Own-brand and co-branded credit cards in partnership with retailers.

Installation plans and buy-now-pay-later (BNPL) products.

Direct-to-consumer solutions, such as the Bread Cashback American Express card and Bread Savings products.

Marketing, loyalty, and analytics services that help brands engage customers.

Bread Financial reported adjusted earnings per share (EPS) of $3.14–$3.15 for the second quarter of 2025, significantly exceeding analyst estimates of $1.85–$1.92.

The company has low multiples.

P/E 9.0

P/B 0.8

Dividend yield 1.4%

However, the company pays out only 14% of its earnings as dividends.

Part of the proceeds are being used for share buybacks.

We expect a return on equity (P/B 1.0), which implies growth of approximately 20%.

Xiaomi 1810 HK🌎Xiaomi reports revenue of RMB 111.3 billion in Q1 2025, up 47% YoY

Adjusted net profit up 64% YoY to RMB 10.7 billion

Operating profit margin and net margin improved to 11.8% and 9.6%, respectively

Xiaomi became the leader in China's smartphone market in Q1 2025 with an 18.8% share (up 4.7 p.p. YoY) for the first time in 10 years

Global market share was 14.1%, keeping the company in 3rd place globally

IoT and lifestyle revenue up 59% YoY

EV business posted revenue of RMB 18.6 billion in Q1 2025, while operating loss narrowed to RMB 500 million

New model YU7 launched 2025, which is positioned as a competitor to Tesla Model Y

news in june

Xiaomi unveiled the YU7 electric SUV at a price lower than the Tesla Model Y

Xiaomi: over 200,000 pre-orders in 3 minutes

The launch of the new YU7 model is expected in July 2025, which is positioned as a competitor to Tesla Model Y

The company's debt is completely covered by the money on the balance sheet

The company's balance sheet is growing steadily every year

🚀We expect continued growth in revenue, profit, OCF, FCF🚀

A great company with a growing business

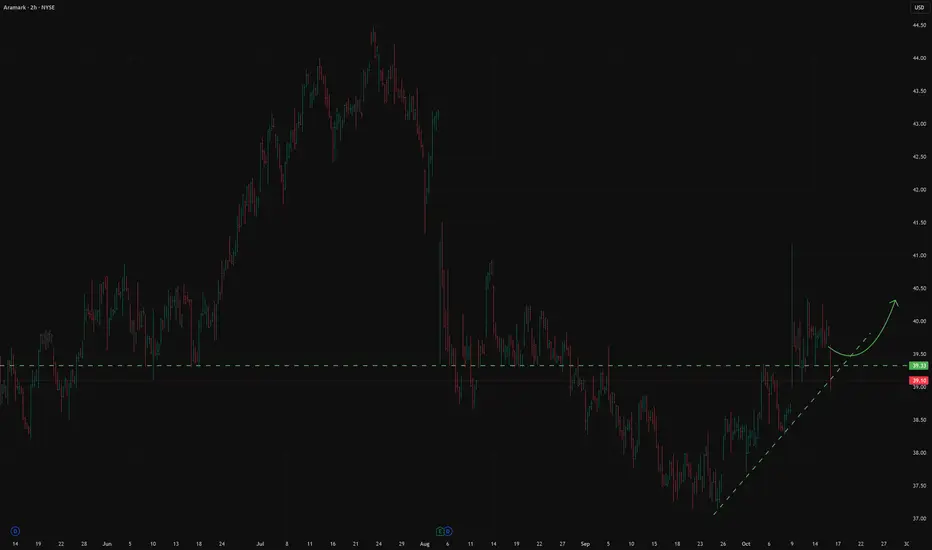

ARMK US🌎Aramark operates in two primary reporting segments:

Food and Service Services in the U.S.

Food and Service Services International

Foodservice Services: Food service, catering, food service management, and convenience-focused retail services

Healthcare Services: Non-healthcare food and related services, including patient nutrition, retail food services, environmental services, and procurement services.

Facility Management Services: Building operations and maintenance, cleaning and housekeeping services, energy management, groundskeeping, and capital project management.

In September 2024, Aramark announced the launch of Avendra International, the international expansion of its procurement division.

In December 2024, Aramark announced that Avendra International had acquired the Spanish procurement consultancy Quantum Cost Consultancy Group. This acquisition is aimed at accelerating Avendra's international expansion.

Customer retention >97% in the US and International FSS segments.

The company has been systematically deleveraging since mid-2020. Debt has decreased from 9.25% to 6.25%.

The upcoming rate cuts will only contribute to balance sheet recovery.

Cash flows are stable and positive.

We expect continued systematic profit growth.

Dividend yield of 1.1%, distributing 1/3 of profits.

LTCUSDT (Crypto) Long🌎Litecoin (LTC) is a decentralized peer-to-peer cryptocurrency created in 2011 as an alternative to Bitcoin. It was designed to provide faster and cheaper transactions, positioning itself as "digital silver" to Bitcoin's "digital gold."

The primary goal of Litecoin's creation was to become a more efficient means of instant payments and transfers than Bitcoin.

Litecoin operates on the Proof-of-Work principle, like Bitcoin, but uses the Scrypt algorithm.

The Scrypt algorithm was initially chosen to counter specialized mining hardware (ASICs), keeping mining more decentralized. Although ASICs for Scrypt have been developed over time, this algorithm still requires more memory than SHA-256, which is used in Bitcoin.

The Litecoin network has successfully implemented important upgrades such as Segregated Witness (SegWit) and the Lightning Network, which increase throughput and enable instant microtransactions.

Litecoin has a stated maximum supply of 84 million LTC, four times greater than Bitcoin.

Litecoin block times and transactions are confirmed significantly faster than Bitcoin. This, along with a less congested network, results in very low fees.

A growing number of merchants accepting LTC and integration with payment systems (such as the partnership with Spend)

Litecoin's partnership with the Spend platform (also known as SPEDN by Flexa) was part of a broader integration aimed at making spending Litecoin and other cryptocurrencies in everyday life simple and instant.

This partnership was a joint effort between several parties: the Litecoin Foundation, Nexus Wallet, and the Flexa payment network, which operates the SPEDN app.

At the peak of the partnership, the Flexa network included over 41,000 merchants, primarily in North America, where SPEDN payments were accepted. Here are some well-known companies that accepted payments through this system:

Lowe's, Petco, GameStop, Bed Bath & Beyond, Nordstrom

Why this partnership was important:

It directly linked digital currency to real goods and services.

It also clearly demonstrated Litecoin's advantages—speed (2.5 minutes per block) and low fees.

Today, the SPEDN app is no longer available, but the Flexa payment network itself continues to operate and develop other solutions. Litecoin remains available for spending—through other services, such as BitPay (crypto debit cards and gift cards) or directly at a growing number of online and offline merchants.

In investing and trading, we treat cryptocurrencies as an asset class tied to a risk-on/risk-off regime, only with added variance, like on steroids, so to speak.

Currently, the markets are in risk-on mode, and number of factors point to the beginning of altcoin season.

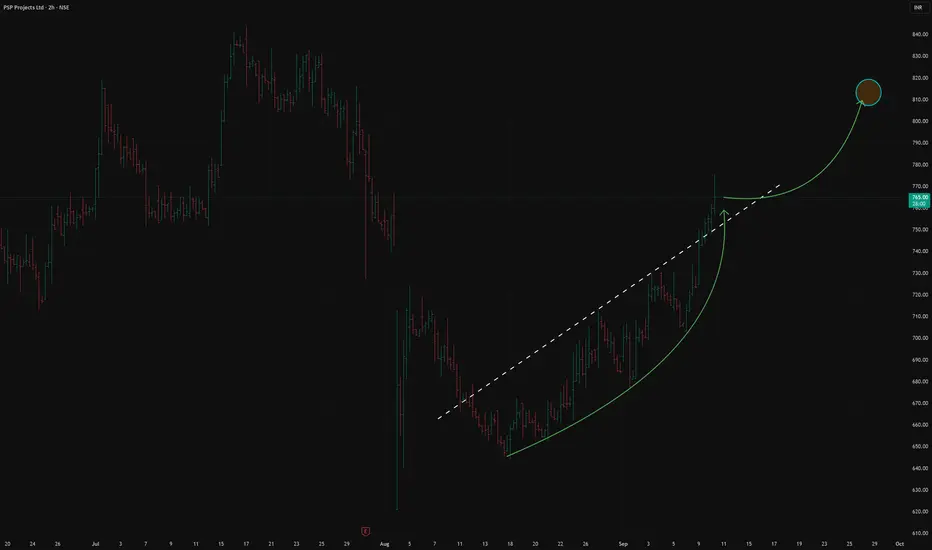

PSPPROJECT IN Long#Invest #PSPPROJECT #India

The company provides services in all stages of construction: from planning and design to construction and post-construction activities, including mechanical, electrical and plumbing works

PSP Projects has a strong position in the engineering and construction sector

The company is working on major projects in the infrastructure and construction sector.

The company is currently building the largest office complex in the world (Surat Diamond Bourse)

Revenue is expected to reach INR 47.566 billion by 2028

EPS is expected to increase by 61.1% annually

The company has shown improvement in operating cash flow generation in the last reporting periods

The stock is breaking upwards from an ascending channel, which gives a chance for acceleration

DATAPATTNS IN (Data Patterns) Long#Invest #India #Datapattns

Data Patterns is involved in defence projects such as Light Combat Aircraft (LCA), BrahMos missile programme, and supplies to ISRO and DRDO

Government of India is aggressively promoting indigenous defence manufacturing through the Atmanirbhar Bharat policy

India's defence budget is increasing, with a focus on domestically produced equipment

The company has shown robust financial performance with a net profit of Rs 221.81 crore for 2025 and revenue growth

EPS (TTM) is Rs 38.32 crore and ROE is 15.66%

The company's revenue is expected to reach Rs 1.36 billion in the next quarter, with long-term price targets of Rs 38,930 by 2040

The company is virtually debt-free

Expansion into global export markets and development of new product segments (e.g., satellite technology, electronic warfare)

Expected to continue revenue and profit growth. Entering the positive FCF area.

EPS will show growth in the future, which will also support growth

MIDHANI IN (Mishra Dhatu Nigam) Long 🌎

The company specializes in the production of specialty metals.

Primary products: nickel-, cobalt-, and iron-based superalloys, titanium alloys, specialty steels, and soft magnetic alloys.

The company's products are of strategic importance and are supplied to the defense, aerospace, and energy sectors (including nuclear).

The company operates a full production cycle—from smelting to the production of finished forged, rolled, and drawn products.

Specializing in strategically important alloys for the defense and aerospace industries creates high barriers to entry and ensures stable demand.

74% of shares are state-owned.

EV/EBITDA 31.2

P/B 4.9

Debt/Equity 0.25

Revenue

2023 | 872

2024 | 1,073

2025 | 1,074

Net Profit

2023 | 156

2024 | 91

2025 | 110

NBCC IN Long🇮🇳 #nbcc #invest

NBCC (India) Limited is an Indian state-owned company and a leader in the construction sector.

The company's operations are divided into three main segments:

Project Management and Consulting (PMC): This segment accounts for approximately 92% of revenue. This includes the redevelopment of old government quarters, project management in the institutional, residential, and industrial sectors, as well as infrastructure projects abroad (Mauritius, Maldives, Seychelles, and Dubai).

Engineering, Procurement, and Construction (EPC)

Real Estate Development

For the fiscal year ending March 2024, revenue was INR 106.67 billion, up 19.03% year-on-year.

The company has been debt-free for the past five years.

High multiples:

P/E 51

P/B 11

EV/EBITDA 28

OCF, FCF positive

We expect profit and revenue to continue to grow.

Dividend yield 0.6%

Formation of the second shoulder in the Inverted H&STo dot miss the next idea Follow Us

Supreme Petrochem Limited manufactures and sells polystyrene, expandable polystyrene, masterbatches and compounds of styrenics and other polymers, and extruded polystyrene insulation board in India and internationally.

The company has a high return on equity (ROE) of 18.38% and return on capital employed (ROCE) of 23.94%

Strong Balance sheet

Recorded growth in foreign institutional investor (FII) ownership

Management plans to increase export share from 9% to 14%

Capacity utilisation is expected to exceed 80% by the end of the year

Start-up of ABS plastics production may open up new opportunities in the long term

We are waiting for the end of the technical correction, the completion of the right shoulder in the inverted head and shoulders figure.

price target 850

Zydus Wellness split 1:5The chart in TradingView shows the stock falling 80% and a huge gap.

This is a 1:5 split. If you previously owned one share, you will now own five shares.

The chart in TradingView will be updated over time.

Good luck.

COCHINSHIP IN (Cochin Shipyard) LongCSL is the largest shipbuilder and ship repairer in India

The company recently bagged a contract with Adani Ports and SEZ for the construction of eight tugboats worth about $54 million through its subsidiary Udupi Cochin Shipyard Limited

The conclusion of the Master Ship Repair Agreement (MSRA) with the US Navy for the repair of USNS ships opens up a significant new source of revenue

The company showed an impressive 38.51% YoY revenue growth in the last quarter, reaching INR 106.86 billion

From a technical perspective

-There was an ascending trend line

-Breakout up and then retest of the descending line.

-The correction is ending

-Expect a breakout of the resistance and an increase in quotes

SINDHUTRAD IN ( Sindhu Trade Links Limited) Long#Invest #India #SINDHUTRAD

🇮🇳

Sindhu Trade Links is an Indian company operating in the logistics and transportation services sector

SINDHUTRAD is involved in key infrastructure projects in India

The logistics sector in India is expected to grow by 15% in the next 12 months. SINDHUTRAD, with its current growth rate, can beat this growth

The company plans to expand its presence in new regions, which can increase its market share

The company's revenue has increased by 70% in the last three years, significantly exceeding the industry average

The company's P/S is 2.4, which is higher than the industry average of 0.6. This indicates investor expectations for future growth

___________________________

Invest Ideas and Analytics on Global Markets

Palladium Long#Invest #Palladium #PALL #PA #XPDUSD

A weaker dollar after soft US inflation data has increased expectations for a Fed rate cut

US President Trump's announcement of tariffs of up to 100% on India and China to pressure Russia is increasing demand for safe haven assets, including palladium

Palladium prices have lagged behind other precious metals

Palladium production is gradually declining due to the depletion of deposits in South Africa, the US and Canada.

Recycling from old cars only partially compensates for the deficit

Despite the growth of electric vehicles, hybrid vehicles with internal combustion engines retain market share, and this supports demand for palladium for catalysts

New areas of demand:

China and India invest in hydrogen infrastructure. Palladium is used to purify hydrogen

Innovative technologies for using palladium to synthesize ammonia without CO₂ emissions

Supply reduction:

Producers Anglo American, Wesizwe Platinum and others are cutting investments due to low prices

Production in Russia is stable, but growth is only possible with the launch of the Chernogorsk deposit in 2026

Palladium is attractive as an alternative to gold due to its growth potential

From a technical point of view

-formation of a double bottom.

-There was already an exit, a false exit upward.

-Now a cup with a handle is being drawn.

How to participate in the growth?

-Buying a futures contract (US NYMEX ticker PA)

-buying through an ETF (for the US, ticker PALL).

*The ticker may be different on the stock exchange in your country

You can also look at companies with exposure to palladium

Norilsk Nickel, Sibanye-Stillwater and Anglo American

BEML IN ( BEML Limited) LongBEML is the second largest manufacturer of earthmoving equipment in Asia

BEML manufactures a wide range of products including:

Earthmoving Equipment: Bulldozers, Excavators, Dump Trucks, Motor Graders.

Mining Equipment: Underground Mining Machines, Road Headers.

Rail: Metro Coaches, Electric Multiple Units, Vande Bharat Trains.

Defence Equipment: High Mobility Vehicles, Missile Systems, Aerospace Equipment

Since the Government of India holds 54% stake in the company, BEML receives significant support from the government, especially in the defence and infrastructure sector. This provides the company with stability and access to large government contracts

The company recently received an order for LHB coaches worth and an order for High Mobility Vehicles worth from the Ministry of Defence.

The company's current order book is over INR 16,700 crore, which provides visibility of earnings for the coming years

The company pays out about 30% of its profits as dividends. The dividend yield is small and can be considered as an additional bonus to the growing business. The dividend growth will continue in the coming years

The defense complex will be in great demand in the country in the next decade

The company's profit has been growing at an average rate of 35.7% per annum over the past five years. We expect the positive dynamics in this parameter to continue.

In terms of the Technical picture, the price is testing the support level of the ascending trend line, and a double bottom is also visible so far.

Stock Market is in Risk OnThe US market, as well as some assets, is in a risk-on mode.

Most assets have their own seasonality.

The chart above shows one of them:

In recent years, in the period July-September, a correction began on the US market.

A number of macro indicators also speak in favor of a correction and that it is overdue.

Risk appetite according to Morgan Stanley research has reached a historical maximum

Although seasonality does not guarantee a correction right here and now, but at least it gives reason to think about reducing long positions

We are not positive about TeslaThe impact of tariffs and expiring EV credits is expected to pressure future US deliveries and regulatory credit revenue in the near term

Elon Musk: Well, we're in this weird transition period where we will lose a lot of incentives in the US. Slab incentives actually in many other parts of the world. But we'll lose them in the US. Across all of it at the relatively early stages of autonomy. On the other hand, autonomy is most advanced and most available from a regulatory standpoint in the US. Does that mean we could have a few rough quarters? Yeah. We probably could have a few rough quarters. I'm not saying that we will, but we could. Q4, Q1, maybe Q2.

Revenue -12% y/y ( decline for the first time in 10 years)!!!

EPS 0,27 $ agj vs 0,39 $ estimated

FCF -89% y/y but still positive ( just 146 M$)

CAPEX for 2025 increased

EBITDA dropped by 7.8%.

Price to Sales 12,7

P/B 14

Expensive

We expect declining of the stock price to 210 $

And, yes, many still regard Tesla as a car manufacturer, but this is not a correct view of the company. Later in our blog we will touch on the question of how to correctly look at the brainchild of Elon Musk.

Oswal Agro Mills 12% upsideFollow Us and Don't miss a next Idea

The company's activities are divided between trade, real estate and investments

The company has almost no debt

Over the past 5 years, CAGR is 28.4%

In recent quarters, there has been significant growth in revenue and operating profit

Low P/E 8.4

P/B 1.1

Target Price 89