Index Funds vs ETFs – Which is Better for Retail Investors?Hello Traders!

When it comes to passive investing, two options always come up, Index Funds and ETFs (Exchange Traded Funds) .

Both track an index like Nifty or Sensex, but the way they work is different.

Let’s break them down so you know which one suits you better.

1. What are Index Funds?

Index funds are mutual funds that replicate a market index like Nifty 50.

You can invest directly through SIP or lump sum, just like other mutual funds.

They don’t trade on the stock exchange; instead, you buy/sell via the fund house.

NAV is calculated once a day, you get units at that day’s NAV.

2. What are ETFs?

ETFs also track an index like Nifty or BankNifty, but they trade like stocks on the exchange.

You need a demat account to buy/sell ETFs.

You can trade them intraday, just like shares.

Price changes throughout the day as they trade live in the market.

3. Key Differences You Must Know

Liquidity: ETFs depend on exchange volumes. Index funds are more stable since you transact with the AMC.

Ease of Use: Index funds are simpler for beginners (no demat needed). ETFs suit traders who want flexibility.

Costs: ETFs usually have lower expense ratios, but you pay brokerage. Index funds may have slightly higher costs but no brokerage.

Investment Style: Index funds are great for long-term SIPs. ETFs are better for those who want intraday liquidity or tactical entries.

Rahul’s Tip:

If you’re just starting and prefer SIPs without worrying about trading, go for index funds.

If you’re comfortable with demat and want real-time flexibility, ETFs give you more control.

Conclusion:

Index funds and ETFs both are powerful tools for retail investors.

The “better” choice depends on your style, simple and steady with index funds, or flexible and active with ETFs.

This educational idea By @TraderRahulPal (TradingView Moderator) | More analysis & educational content on my profile

If this post made the difference clear for you, like it, drop your choice in comments, and follow for more simple investing insights!

Mutualfunds

Flexi Cap Funds vs Multi Cap Funds – What’s the Difference?Hello Traders!

When it comes to equity mutual funds, many investors get confused between Flexi Cap and Multi Cap funds. Both invest across large, mid, and small-cap stocks, but there’s a key difference in how they are managed. Let’s break it down in simple words.

What are Multi Cap Funds?

Multi Cap Funds are required by SEBI rules to invest a minimum of 25% each in large-cap, mid-cap, and small-cap stocks.

This means:

They are compulsory diversified .

Even if small caps are risky at the moment, the fund manager must still hold at least 25% exposure.

Good for investors who want fixed diversification across all categories.

What are Flexi Cap Funds?

Flexi Cap Funds, as the name suggests, have full flexibility. The fund manager can invest in large, mid, or small-cap in any proportion, depending on market conditions.

This means:

No fixed rule for allocation.

The fund manager can go 70% large-cap in volatile times or shift more to small/mid-caps when opportunities are strong.

Good for investors who trust the fund manager’s judgment.

Key Differences You Should Know

Flexibility: Multi Cap = fixed allocation, Flexi Cap = flexible allocation.

Risk Level: Multi Cap has balanced risk due to compulsory exposure. Flexi Cap risk depends on manager’s calls.

Return Potential: Flexi Cap may deliver better returns in the hands of a skilled manager, but also comes with higher dependency on their decisions.

Investor Type: Multi Cap suits investors wanting rule-based diversification. Flexi Cap suits investors comfortable with dynamic allocation.

Rahul’s Tip:

If you want steady exposure across all market caps, Multi Cap funds are safer. But if you believe in the fund manager’s ability and want more flexibility, Flexi Cap funds can give you better opportunities.

Conclusion:

Both categories have their place in a portfolio. The choice depends on your risk appetite and trust in active fund management.

Remember, what matters most is not just category, but consistent performance and fund manager track record.

If this post cleared your confusion, like it, share your view in the comments, and follow for more simple investing insights!

How to Create Your Own Pension with Mutual Funds (SWP Explained)Hello Everyone,

For most people, retirement planning starts with the question – “How will I get monthly income once I stop working?”

The answer is – Systematic Withdrawal Plan (SWP). With SWP, you can actually create your own pension and enjoy a stress-free retirement.

What is SWP?

A Systematic Withdrawal Plan allows you to invest a lump sum amount in a mutual fund and withdraw a fixed sum every month (or quarter/year). It’s just like receiving a pension or salary, while your remaining money continues to stay invested and grow.

Why SWP Works Like a Pension

Steady Cash Flow: You can set up regular monthly withdrawals, which creates a reliable income stream for your retirement needs.

Inflation Protection: Unlike traditional pensions or FDs where income is fixed, in SWP you can increase your withdrawal every year. This way, your monthly income grows in line with rising living costs.

Wealth Preservation: Even though you withdraw regularly, your remaining corpus is invested and keeps compounding. Over long periods, this can multiply your wealth.

Tax Efficiency: Compared to interest income from FDs, SWPs are more tax-friendly as withdrawals are treated as capital gains. This means potentially lower taxes and higher take-home income.

Flexibility: You can change the withdrawal amount, frequency, or even stop the SWP anytime depending on your needs. No traditional pension gives this much flexibility.

Why Multi-Asset Funds Work Best for SWP

SWP is most effective when your investment is diversified across equity, debt, and gold – which is exactly what multi-asset funds offer.

Equity portion helps your wealth grow faster.

Debt portion provides stability and regular income.

Gold acts as a hedge during uncertain times.

That’s why multi-asset funds are often considered the best option for long-term SWPs.

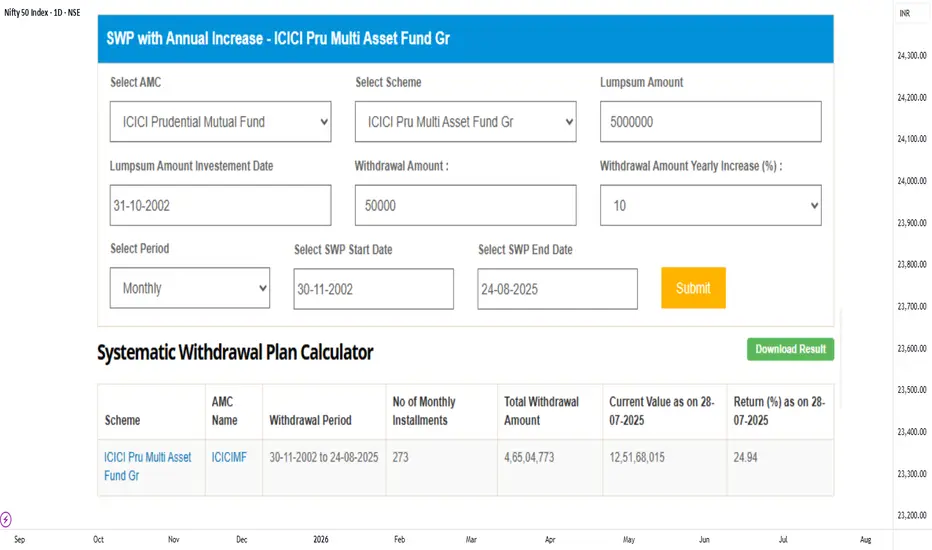

Real Example (Past Data)

Suppose an investor invested ₹50 lakh in 2002 in a multi-asset fund.

He started withdrawing ₹50,000 per month, increasing it by 10% every year.

By 2025, he had already withdrawn ₹4.65 crore (like a monthly pension).

Yet, his remaining corpus grew to around ₹12.5 crore.

Note: This is based on past returns. Future results may differ. Returns are never guaranteed in markets.

But just think of it this way – if 2002 was your starting point, and today was 2025, this is the power of SWP you would have experienced.

Rahul’s Tip

SIP helps you build wealth .

SWP helps you enjoy wealth .

If you want financial independence after retirement, don’t wait for government or company pensions. Create your own with SWPs in multi-asset funds.

If this helped, like/follow/comment.

The Ultimate Guide to Building Wealth Through Smart Investing!Hello Traders & Investors!

Are you wondering which investment method can build the largest corpus over the long term? With so many options— Stocks, ETFs, Mutual Funds, Gold, Bonds, Fixed Deposits, and even Options Writing, it’s crucial to know which one offers the best returns while managing risk effectively. Let’s dive into a detailed comparison to find the best strategy for long-term wealth creation!

1. Equity (Stocks) – The Ultimate Wealth Creator

Average Returns: 12-18% CAGR (historically for strong companies).

Why It’s Powerful: Equity investments compound over time and provide the highest long-term returns.

Best For: Investors who can handle volatility and have a long investment horizon.

Pros:

✔ Compounding Effect – Small investments grow into massive wealth over time.

✔ Beats Inflation – Equity is the best asset class for long-term wealth preservation.

Cons:

❌ High volatility in the short term.

❌ Requires research & patience.

2. ETFs & Mutual Funds – Passive Investing for Consistency

Average Returns: 10-15% CAGR (depending on market performance).

Why It’s Powerful: Diversification and professional management make it a safer alternative to direct stock investing.

Best For: Investors who want steady returns without active stock picking.

Pros:

✔ Low Risk Compared to Stocks – Reduces exposure to single-stock failures.

✔ Great for Long-Term Investors – Set & forget approach.

Cons:

❌ Returns are slightly lower than individual stocks.

❌ Expense ratios reduce overall profitability.

3. Gold – The Safe-Haven Asset

Average Returns: 8-12% CAGR (historically).

Why It’s Powerful: Gold holds value during market crashes and economic uncertainty.

Best For: Investors looking for portfolio diversification and inflation protection.

Pros:

✔ Hedge Against Inflation & Crashes.

✔ Highly Liquid – Easily Buy & Sell.

Cons:

❌ Lower long-term returns than stocks & ETFs.

❌ No compounding effect.

4. Bonds & Fixed Deposits – Safety but Low Growth

Average Returns: 6-8% CAGR (historically).

Why It’s Powerful: Provides stability and guaranteed returns, making it a good option for conservative investors.

Best For: Those seeking low-risk, fixed returns over time.

Pros:

✔ Principal Protection – No Market Risk.

✔ Fixed Income Source.

Cons:

❌ Returns barely beat inflation.

❌ Not ideal for wealth creation.

5. Option Writing – High Risk, High Reward

Average Returns: 15-30% CAGR (if done correctly).

Why It’s Powerful: Generates consistent income through premium collection.

Best For: Experienced traders who understand risk management and capital allocation.

Pros:

✔ Consistent Income Through Premiums.

✔ Can Profit in Any Market Condition.

Cons:

❌ High capital requirement.

❌ Risk of significant losses in volatile markets.

6. The Best Long-Term Investment Strategy?

For Maximum Growth: Equity (Stocks) + ETFs – The best for compounding wealth.

For Balanced Growth & Safety: Equity + ETFs + Gold – A mix of high returns & stability.

For Conservative Investors: ETFs + Bonds + Fixed Deposits – Low risk, but lower returns.

For Passive Income Seekers: Dividend Stocks + Bonds – Steady returns with income.

For Experienced Traders: Stocks + ETFs + Option Writing – High returns, requires skill.

Conclusion

There’s no single best investment, but if you want huge wealth creation, equities & ETFs outperform all other asset classes in the long run. Add gold & bonds for stability, and if experienced, option writing can generate extra income.

What’s your preferred investment strategy for long-term wealth creation? Let’s discuss below! 👇

Equity Mutual FundsEquity mutual funds have emerged as one of India’s most popular investment options, attracting new and seasoned investors. This article will delve into the various aspects of equity mutual funds, from their investment strategies to their impact on wealth creation.

Equity mutual funds have emerged as one of India’s most popular investment options, attracting new and seasoned investors. This section will delve into the different types of equity mutual funds and their investment strategies.

Mutual Funds investment mistakes in IndiaIntroduction

Investing in mutual funds has become popular for many Indian investors in recent years. It provides an opportunity to invest in a diversified portfolio of assets managed by experienced professionals, with potentially higher returns than traditional investment options such as fixed deposits or savings accounts. Mutual funds also offer flexibility, liquidity, and tax benefits, making them an attractive option for investors seeking financial stability and growth.

15 Mutual Fund Investment Checklist IndiaIntroduction:

A mutual fund is a professionally managed investment vehicle that pools multiple investors’ money to invest in securities such as stocks, bonds, and money market instruments. Investors purchase units of the mutual fund, representing a portion of the holdings in the fund’s portfolio. Mutual funds are managed by asset management companies (AMCs), which charge a fee for their services.

Investing in mutual funds can be an excellent way for individuals to participate in the stock market without picking individual stocks. Mutual funds offer diversification, which means spreading the investment across multiple securities to reduce the risk of losses. Moreover, mutual funds are managed by professional fund managers with the expertise to research and select securities, which can result in better returns. Additionally, mutual funds offer liquidity, meaning investors can easily buy and sell units based on their investment needs.

The purpose of this article is to provide a comprehensive guide to the basic parameters to consider before investing in mutual funds. We will explore the various factors that can impact the performance of mutual funds, such as ratings, NAV, expense ratio, entry load, exit load, AMC, AUM, benchmark, fund manager, holdings, launch date, lock-in period, returns, risk, and SIP minimum. By the end of this article, readers will have a clear understanding of how to evaluate mutual funds and make informed investment decisions.

Guide to Asset Allocation and Investment Planning in IndiaIntroduction to Asset Allocation:

Asset allocation is a crucial process in investment management, where an individual divides their investment portfolio among different asset classes, such as equities, debt, and cash. It is the process of deciding how to distribute your investment portfolio across various asset classes to achieve optimal returns for a given level of risk.

Asset allocation has become increasingly popular as people seek to diversify their portfolios and minimize risk. According to a survey conducted by ICICI Securities, 73% of Indian investors prefer mutual funds as an investment option due to their potential for higher returns and diversification benefits.

Asset allocation balances risk and reward, considering an individual’s investment goals, risk tolerance, and time horizon. For example, someone with a high-risk tolerance and a long-term investment horizon might invest more in equities. In contrast, someone with a lower risk tolerance and a shorter investment horizon might choose to invest more in debt securities.

Factors influencing asset allocation include an individual’s investment goals, financial situation, risk tolerance, and time horizon. It is crucial to consider these factors before making any investment decisions.

25/04/2022 Research Report For ABSLAMCDisclaimer:

I am not SEBI registered person and this is not an investment advice and also please note this is only for education purpose. Also note we can use this research in my own portfolios. So don't influence yourself by this research. Please note before investing according to this educational research, please do own research and also do take advice from your financial adviser. Your any profits and loss are totally your liability. No one is liable for that. Also, please note we will not never compensate your any loss. So before investing any single rupee, please do your own research according to your risk taking capacity and after that do invest and book profits on right time.

Buy @ C.M.P (Current Market Price)

Target 1: More Then 1100

Compare ABSLAMC's Chart With UTIAMC's This Chart