OPEN-SOURCE SCRIPT

Updated VWAP Market Session Anchored

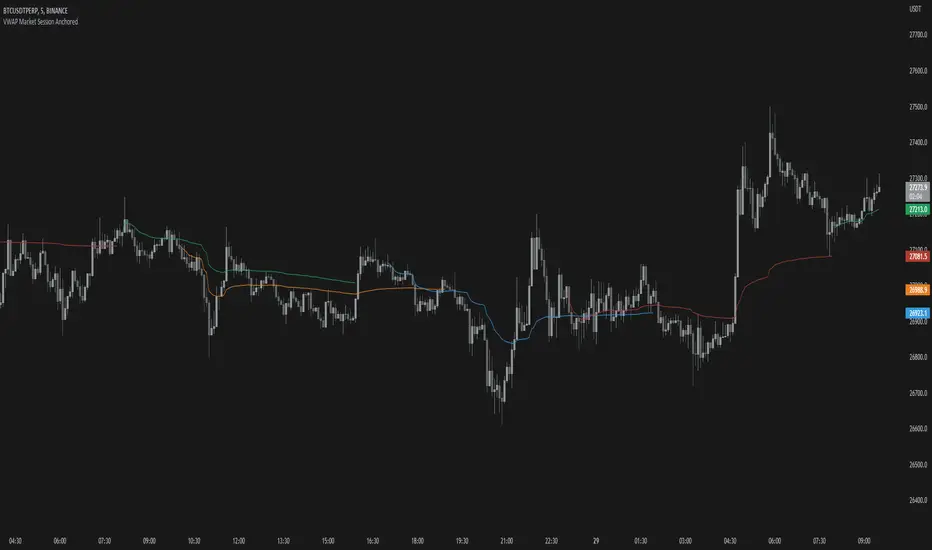

VWAP Market Session Anchored differs from the traditional VWAP or VWAP Auto Anchored indicator in that the Volume Weighted Average Price calculation is automatically anchored to four major market session starts: Sydney, London, Tokyo, New York.

Settings

Usage

Similar to the traditional VWAP, VWAP Market Session Anchored is a technical analysis tool used to measure the average price weighted by volume. VWAP Market Session Anchored can be used to identify the trend during a specific market session.

Limitations

When setting a custom session, be mindful that calculations are based off of the Coordinated Universal Time (UTC) time, you must convert your local time zone to UTC in order to have an accurate representation of your custom session.

It is not recommended to use this indicator on timeframes above 1 hour as market sessions only last a few hours.

Settings

- Source: the source for the VWAP calculation.

- Offset: changing this number will move the VWAP either Forwards or Backwards, relative to the current market. Zero is the default.

- Band: enabling this will show Standard Deviation bands.

- Band Multiplier: the value the Standard Deviation bands will be multiplied by before being plotted on the chart.

- Sessions: enabling the sessions will plot the respective anchored VWAP on chart.

- Custom: enabling this will show a custom user-defined session.

- Custom UTC: the custom session is defined by a starting UTC hour followed by the ending UTC hour.

Usage

Similar to the traditional VWAP, VWAP Market Session Anchored is a technical analysis tool used to measure the average price weighted by volume. VWAP Market Session Anchored can be used to identify the trend during a specific market session.

Limitations

When setting a custom session, be mindful that calculations are based off of the Coordinated Universal Time (UTC) time, you must convert your local time zone to UTC in order to have an accurate representation of your custom session.

It is not recommended to use this indicator on timeframes above 1 hour as market sessions only last a few hours.

Release Notes

- Updated colors

- Updated chart

Open-source script

In true TradingView spirit, the creator of this script has made it open-source, so that traders can review and verify its functionality. Kudos to the author! While you can use it for free, remember that republishing the code is subject to our House Rules.

Disclaimer

The information and publications are not meant to be, and do not constitute, financial, investment, trading, or other types of advice or recommendations supplied or endorsed by TradingView. Read more in the Terms of Use.

Open-source script

In true TradingView spirit, the creator of this script has made it open-source, so that traders can review and verify its functionality. Kudos to the author! While you can use it for free, remember that republishing the code is subject to our House Rules.

Disclaimer

The information and publications are not meant to be, and do not constitute, financial, investment, trading, or other types of advice or recommendations supplied or endorsed by TradingView. Read more in the Terms of Use.