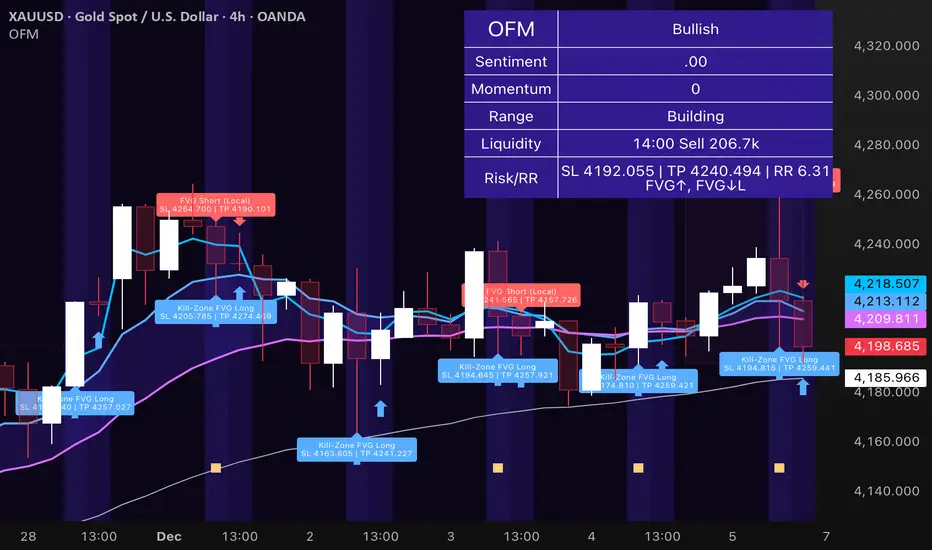

Obsidian Flux Matrix# Obsidian Flux Matrix | JackOfAllTrades

Made with my Senior Level AI Pine Script v6 coding bot for the community!

Narrative Overview

Obsidian Flux Matrix (OFM) is an open-source Pine Script v6 study that fuses social sentiment, higher timeframe trend bias, fair-value-gap detection, liquidity raids, VWAP gravitation, session profiling, and a diagnostic HUD. The layout keeps the obsidian palette so critical overlays stay readable without overwhelming a price chart.

Purpose & Scope

OFM focuses on actionable structure rather than marketing claims. It documents every driver that powers its confluence engine so reviewers understand what triggers each visual.

Core Analytical Pillars

1. Social Pulse Engine

Sentiment Webhook Feed: Accepts normalized scores (-1 to +1). Signals only arm when the EMA-smoothed value exceeds the `sentimentMin` input (0.35 by default).

Volume Confirmation: Requires local volume > 30-bar average × `volSpikeMult` (default 2.0) before sentiment flags.

EMA Cross Validation: Fast EMA 8 crossing above/below slow EMA 21 keeps momentum aligned with flow.

Momentum Alignment: Multi-timeframe momentum composite must agree (positive for longs, negative for shorts).

2. Peer Momentum Heatmap

Multi-Timeframe Blend: RSI + Stoch RSI fetched via request.security() on 1H/4H/1D by default.

Composite Scoring: Each timeframe votes +1/-1/0; totals are clamped between -3 and +3.

Intraday Readability: Configurable band thickness (1-5) so scalpers see context without losing space.

Dynamic Opacity: Stronger agreement boosts column opacity for quick bias checks.

3. Trend & Displacement Framework

Dual EMA Ribbon: Cyan/magenta ribbon highlights immediate posture.

HTF Bias: A higher-timeframe EMA (default 55 on 4H) sets macro direction.

Displacement Score: Body-to-ATR ratio (>1.4 default) detects impulses that seed FVGs or VWAP raids.

ATR Normalization: All thresholds float with volatility so the study adapts to assets and regimes.

4. Intelligent Fair Value Gap (FVG) System

Gap Detection: Three-candle logic (bullish: low > high ; bearish: high < low ) with ATR-sized minimums (0.15 × ATR default).

Overlap Prevention: Price-range checks stop redundant boxes.

Spacing Control: `fvgMinSpacing` (default 5) avoids stacking from the same impulse.

Storage Caps: Max three FVGs per side unless the user widens the limit.

Session Awareness: Kill zone filters keep taps focused on London/NY if desired.

Auto Cleanup: Boxes delete when price closes beyond their invalidation level.

5. VWAP Magnet + Liquidity Raid Engine

Session or Rolling VWAP: Toggle resets to match intraday or rolling preferences.

Equal High/Low Scanner: Looks back 20 bars by default for liquidity pools.

Displacement Filter: ATR multiplier ensures raids represent genuine liquidity sweeps.

Mean Reversion Focus: Signals fire when price displaces back toward VWAP following a raid.

6. Session Range Breakout System

Initial Balance Tracking: First N bars (15 default) define the session box.

Breakout Logic: Requires simultaneous liquidity spikes, nearby FVG activity, and supportive momentum.

Z-Score Volume Filter: >1.5σ by default to filter noisy moves.

7. Lifestyle Liquidity Scanner

Volume Z-Scores: 50-bar baseline highlights statistically significant spikes.

Smart Money Footprints: Bottom-of-chart squares color-code buy vs sell participation.

Panel Memory: HUD logs the last five raid timestamps, direction, and normalized size.

8. Risk Matrix & Diagnostic HUD

HUD Structure: Table in the top-right summarizes HTF bias, sentiment, momentum, range state, liquidity memory, and current risk references.

Signal Tags: Aggregates SPS, FVG, VWAP, Range, and Liquidity states into a compact string.

Risk Metrics: Swing-based stops (5-bar lookback) + ATR targets (1.5× default) keep risk transparent.

Signal Families & Alerts

Social Pulse (SPS): Volume-confirmed sentiment alignment; triangle markers with “SPS”.

Kill-Zone FVG: Session + HTF alignment + FVG tap; arrow markers plus SL/TP labels.

Local FVG: Captures local reversals when HTF bias has not flipped yet.

VWAP Raid: Equal-high/low raids that snap toward VWAP; “VWAP” label markers.

Range Breakout: Initial balance violations with liquidity and imbalance confirmation; circle markers.

Liquidity Spike: Z-score spikes ≥ threshold; square markers along the baseline.

Visual Design & Customization

Theme Palette: Primary background RGB (12,6,24). Accent shading RGB (26,10,48). Long accents RGB (88,174,255). Short accents RGB (219,109,255).

Stylized Candles: Optional overlay using theme colors.

Signal Toggles: Independently enable markers, heatmap, and diagnostics.

Label Spacing: Auto-spacing enforces ≥4-bar gaps to prevent text overlap.

Customization & Workflow Notes

Adjust ATR/FVG thresholds when volatility shifts.

Re-anchor sentiment to your webhook cadence; EMA smoothing (default 5) dampens noise.

Reposition the HUD by editing the `table.new` coordinates.

Use multiples of the chart timeframe for HTF requests to minimize load.

Session inputs accept exchange-local time; align them to your market.

Performance & Compliance

Pure Pine v6: Single-line statements, no `lookahead_on`.

Resource Safe: Arrays trimmed, boxes limited, `request.security` cached.

Repaint Awareness: Signals confirm on close; alerts mirror on-chart logic.

Runtime Safety: Arrays/loops guard against `na`.

Use Cases

Measure when social sentiment aligns with structure.

Plan ICT-style intraday rebalances around session-specific FVG taps.

Fade VWAP raids when displacement shows exhaustion.

Watch initial balance breaks backed by statistical volume.

Keep risk/target references anchored in ATR logic.

Signal Logic Snapshot

Social Pulse Long/Short: `sentimentEMA` gated by `sentimentMin`, `volSpike`, EMA 8/21 cross, and `momoComposite` sign agreement. Keeps hype tied to structural follow-through.

Kill-Zone FVG Long/Short: Requires session filter, HTF EMA bias alignment, and an active FVG tap (`bullFvgTap` / `bearFvgTap`). Labels include swing stops + ATR targets pulled from `swingLookback` and `liqTargetMultiple`.

Local FVG Long/Short: Uses `localBullish` / `localBearish` heuristics (EMA slope, displacement, sequential closes) to surface intraday reversals even when HTF bias has not flipped.

VWAP Raids: Detect equal-high/equal-low sweeps (`raidHigh`, `raidLow`) that revert toward `sessionVwap` or rolling VWAP when displacement exceeds `vwapAlertDisplace`.

Range Breakouts: Combine `rangeComplete`, breakout confirmation, liquidity spikes, and nearby FVG activity for statistically backed initial balance breaks.

Liquidity Spikes: Volume Z-score > `zScoreThreshold` logs direction, size, and timestamp for the HUD and optional review workflows.

Session Logic & VWAP Handling

Kill zone + NY session inputs use TradingView’s session strings; `f_inSession()` drives both visual shading and whether FVG taps are tradeable when `killZoneOnly` is true.

Session VWAP resets using cumulative price × volume sums that restart when the daily timestamp changes; rolling VWAP falls back to `ta.vwap(hlc3)` for instruments where daily resets are less relevant.

Initial balance box (`rangeBars` input) locks once complete, extends forward, and stays on chart to contextualize later liquidity raids or breakouts.

Parameter Reference

Trend: `emaFastLen`, `emaSlowLen`, `htfResolution`, `htfEmaLen`, `showEmaRibbon`, `showHtfBiasLine`.

Momentum: `tf1`, `tf2`, `tf3`, `rsiLen`, `stochLen`, `stochSmooth`, `heatmapHeight`.

Volume/Liquidity: `volLookback`, `volSpikeMult`, `zScoreLen`, `zScoreThreshold`, `equalLookback`.

VWAP & Sessions: `vwapMode`, `showVwapLine`, `vwapAlertDisplace`, `killSession`, `nySession`, `showSessionShade`, `rangeBars`.

FVG/Risk: `fvgMinTicks`, `fvgLookback`, `fvgMinSpacing`, `killZoneOnly`, `liqTargetMultiple`, `swingLookback`.

Visualization Toggles: `showSignalMarkers`, `showHeatmapBand`, `showInfoPanel`, `showStylizedCandles`.

Workflow Recipes

Kill-Zone Continuation: During the defined kill session, look for `killFvgLong` or `killFvgShort` arrows that line up with `sentimentValid` and positive `momoComposite`. Use the HUD’s risk readout to confirm SL/TP distances before entering.

VWAP Raid Fade: Outside kill zone, track `raidToVwapLong/Short`. Confirm the candle body exceeds the displacement multiplier, and price crosses back toward VWAP before considering reversions.

Range Break Monitor: After the initial balance locks, mark `rangeBreakLong/Short` circles only when the momentum band is >0 or <0 respectively and a fresh FVG box sits near price.

Liquidity Spike Review: When the HUD shows “Liquidity” timestamps, hover the plotted squares at chart bottom to see whether spikes were buy/sell oriented and if local FVGs formed immediately after.

Metadata

Author: officialjackofalltrades

Platform: TradingView (Pine Script v6)

Category: Sentiment + Liquidity Intelligence

Hope you Enjoy!

Artificialintelligence

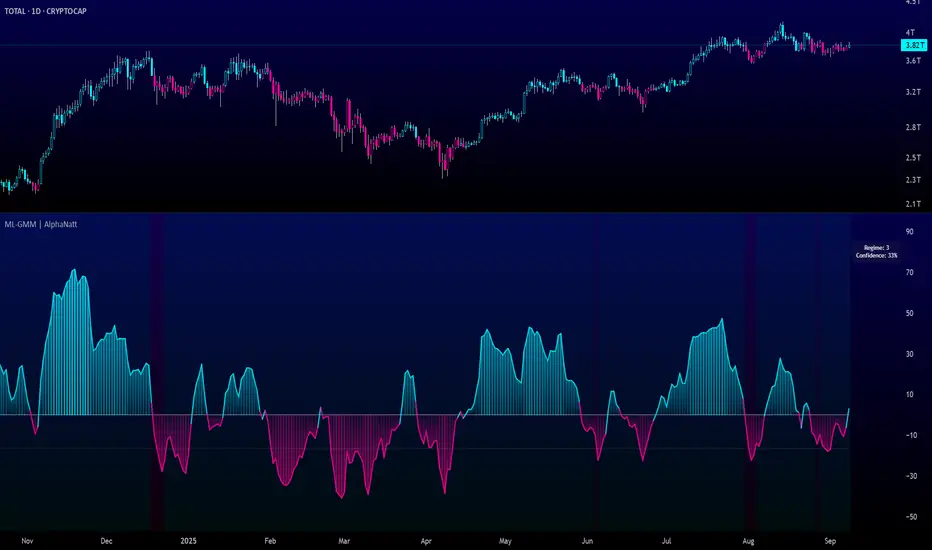

Machine Learning Gaussian Mixture Model | AlphaNattMachine Learning Gaussian Mixture Model | AlphaNatt

A revolutionary oscillator that uses Gaussian Mixture Models (GMM) with unsupervised machine learning to identify market regimes and automatically adapt momentum calculations - bringing statistical pattern recognition techniques to trading.

"Markets don't follow a single distribution - they're a mixture of different regimes. This oscillator identifies which regime we're in and adapts accordingly."

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🤖 THE MACHINE LEARNING

Gaussian Mixture Models (GMM):

Unlike K-means clustering which assigns hard boundaries, GMM uses probabilistic clustering :

Models data as coming from multiple Gaussian distributions

Each market regime is a different Gaussian component

Provides probability of belonging to each regime

More sophisticated than simple clustering

Expectation-Maximization Algorithm:

The indicator continuously learns and adapts using the E-M algorithm:

E-step: Calculate probability of current market belonging to each regime

M-step: Update regime parameters based on new data

Continuous learning without repainting

Adapts to changing market conditions

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🎯 THREE MARKET REGIMES

The GMM identifies three distinct market states:

Regime 1 - Low Volatility:

Quiet, ranging markets

Uses RSI-based momentum calculation

Reduces false signals in choppy conditions

Background: Pink tint

Regime 2 - Normal Market:

Standard trending conditions

Uses Rate of Change momentum

Balanced sensitivity

Background: Gray tint

Regime 3 - High Volatility:

Strong trends or volatility events

Uses Z-score based momentum

Captures extreme moves

Background: Cyan tint

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

💡 KEY INNOVATIONS

1. Probabilistic Regime Detection:

Instead of binary regime assignment, provides probabilities:

30% Regime 1, 60% Regime 2, 10% Regime 3

Smooth transitions between regimes

No sudden indicator jumps

2. Weighted Momentum Calculation:

Combines three different momentum formulas

Weights based on regime probabilities

Automatically adapts to market conditions

3. Confidence Indicator:

Shows how certain the model is (white line)

High confidence = strong regime identification

Low confidence = transitional market state

Line transparency changes with confidence

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

⚙️ PARAMETER OPTIMIZATION

Training Period (50-500):

50-100: Quick adaptation to recent conditions

100: Balanced (default)

200-500: Stable regime identification

Number of Components (2-5):

2: Simple bull/bear regimes

3: Low/Normal/High volatility (default)

4-5: More granular regime detection

Learning Rate (0.1-1.0):

0.1-0.3: Slow, stable learning

0.3: Balanced (default)

0.5-1.0: Fast adaptation

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📊 TRADING STRATEGIES

Visual Signals:

Cyan gradient: Bullish momentum

Magenta gradient: Bearish momentum

Background color: Current regime

Confidence line: Model certainty

1. Regime-Based Trading:

Regime 1 (pink): Expect mean reversion

Regime 2 (gray): Standard trend following

Regime 3 (cyan): Strong momentum trades

2. Confidence-Filtered Signals:

Only trade when confidence > 70%

High confidence = clearer market state

Avoid transitions (low confidence)

3. Adaptive Position Sizing:

Regime 1: Smaller positions (choppy)

Regime 2: Normal positions

Regime 3: Larger positions (trending)

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🚀 ADVANTAGES OVER OTHER ML INDICATORS

vs K-Means Clustering:

Soft clustering (probabilities) vs hard boundaries

Captures uncertainty and transitions

More mathematically robust

vs KNN (K-Nearest Neighbors):

Unsupervised learning (no historical labels needed)

Continuous adaptation

Lower computational complexity

vs Neural Networks:

Interpretable (know what each regime means)

No overfitting issues

Works with limited data

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📈 PERFORMANCE CHARACTERISTICS

Best Market Conditions:

Markets with clear regime shifts

Volatile to trending transitions

Multi-timeframe analysis

Cryptocurrency markets (high regime variation)

Key Strengths:

Automatically adapts to market changes

No manual parameter adjustment needed

Smooth transitions between regimes

Probabilistic confidence measure

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🔬 TECHNICAL BACKGROUND

Gaussian Mixture Models are used extensively in:

Speech recognition (Google Assistant)

Computer vision (facial recognition)

Astronomy (galaxy classification)

Genomics (gene expression analysis)

Finance (risk modeling at investment banks)

The E-M algorithm was developed at Stanford in 1977 and is one of the most important algorithms in unsupervised machine learning.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

💡 PRO TIPS

Watch regime transitions: Best opportunities often occur when regimes change

Combine with volume: High volume + regime change = strong signal

Use confidence filter: Avoid low confidence periods

Multi-timeframe: Compare regimes across timeframes

Adjust position size: Scale based on identified regime

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

⚠️ IMPORTANT NOTES

Machine learning adapts but doesn't predict the future

Best used with other confirmation indicators

Allow time for model to learn (100+ bars)

Not financial advice - educational purposes

Backtest thoroughly on your instruments

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🏆 CONCLUSION

The GMM Momentum Oscillator brings institutional-grade machine learning to retail trading. By identifying market regimes probabilistically and adapting momentum calculations accordingly, it provides:

Automatic adaptation to market conditions

Clear regime identification with confidence levels

Smooth, professional signal generation

True unsupervised machine learning

This isn't just another indicator with "ML" in the name - it's a genuine implementation of Gaussian Mixture Models with the Expectation-Maximization algorithm, the same technology used in:

Google's speech recognition

Tesla's computer vision

NASA's data analysis

Wall Street risk models

"Let the machine learn the market regimes. Trade with statistical confidence."

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

Developed by AlphaNatt | Machine Learning Trading Systems

Version: 1.0

Algorithm: Gaussian Mixture Model with E-M

Classification: Unsupervised Learning Oscillator

Not financial advice. Always DYOR.

CNN Statistical Trading System [PhenLabs]📌 DESCRIPTION

An advanced pattern recognition system utilizing Convolutional Neural Network (CNN) principles to identify statistically significant market patterns and generate high-probability trading signals.

CNN Statistical Trading System transforms traditional technical analysis by applying machine learning concepts directly to price action. Through six specialized convolution kernels, it detects momentum shifts, reversal patterns, consolidation phases, and breakout setups simultaneously. The system combines these pattern detections using adaptive weighting based on market volatility and trend strength, creating a sophisticated composite score that provides both directional bias and signal confidence on a normalized -1 to +1 scale.

🚀 CONCEPTS

• Built on Convolutional Neural Network pattern recognition methodology adapted for financial markets

• Six specialized kernels detect distinct price patterns: upward/downward momentum, peak/trough formations, consolidation, and breakout setups

• Activation functions create non-linear responses with tanh-like behavior, mimicking neural network layers

• Adaptive weighting system adjusts pattern importance based on current market regime (volatility < 2% and trend strength)

• Multi-confirmation signals require CNN threshold breach (±0.65), RSI boundaries, and volume confirmation above 120% of 20-period average

🔧 FEATURES

Six-Kernel Pattern Detection:

Simultaneous analysis of upward momentum, downward momentum, peak/resistance, trough/support, consolidation, and breakout patterns using mathematically optimized convolution kernels.

Adaptive Neural Architecture:

Dynamic weight adjustment based on market volatility (ATR/Price) and trend strength (EMA differential), ensuring optimal performance across different market conditions.

Professional Visual Themes:

Four sophisticated color palettes (Professional, Ocean, Sunset, Monochrome) with cohesive design language. Default Monochrome theme provides clean, distraction-free analysis.

Confidence Band System:

Upper and lower confidence zones at 150% of threshold values (±0.975) help identify high-probability signal areas and potential exhaustion zones.

Real-Time Information Panel:

Live display of CNN score, market state with emoji indicators, net momentum, confidence percentage, and RSI confirmation with dynamic color coding based on signal strength.

Individual Feature Analysis:

Optional display of all six kernel outputs with distinct visual styles (step lines, circles, crosses, area fills) for advanced pattern component analysis.

User Guide

• Monitor CNN Score crossing above +0.65 for long signals or below -0.65 for short signals with volume confirmation

• Use confidence bands to identify optimal entry zones - signals within confidence bands carry higher probability

• Background intensity reflects signal strength - darker backgrounds indicate stronger conviction

• Enter long positions when blue circles appear above oscillator with RSI < 75 and volume > 120% average

• Enter short positions when dark circles appear below oscillator with RSI > 25 and volume confirmation

• Information panel provides real-time confidence percentage and momentum direction for position sizing decisions

• Individual feature plots allow granular analysis of specific pattern components for strategy refinement

💡Conclusion

CNN Statistical Trading System represents the evolution of technical analysis, combining institutional-grade pattern recognition with retail accessibility. The six-kernel architecture provides comprehensive market pattern coverage while adaptive weighting ensures relevance across all market conditions. Whether you’re seeking systematic entry signals or advanced pattern confirmation, this indicator delivers mathematically rigorous analysis with intuitive visual presentation.

Professional MSTI+ Trading Indicator"Professional MSTI+ Trading Indicator" is a comprehensive technical analysis tool that combines over 20 indicators to generate high-quality trading signals and assess market sentiment. The script integrates standard indicators (MACD, RSI, Bollinger Bands, Stochastic, Simple Moving Averages, and Volume Analysis) with advanced components (Squeeze Momentum, Fisher Transform, True Strength Index, Heikin-Ashi, Laguerre RSI, Hull MA) and further includes metrics such as ADX, Chaikin Money Flow, Williams %R, VWAP, and EMA for in-depth market analysis.

Key Features:

Multiple Presets for Different Trading Styles:

Choose from optimal configurations like Professional, Swing Trading, Day Trading, Scalping, or Reversal Hunter. Note that the presets may not work perfectly on all pairs, and manual calibration might be required. This flexibility allows you to fine-tune the settings to align with your unique strategies and signals.

Multi-Layered Signal Filtering:

Filters based on trend, volume, and volatility help eliminate false signals, enhancing the accuracy of market entries.

Comprehensive Fear & Greed Index:

The indicator aggregates data from RSI, volatility, momentum, trend, and volume to gauge overall market sentiment, providing an additional layer of market context.

Dynamic Information Panel:

Displays detailed status updates for each component (e.g., MACD, RSI, Laguerre RSI, TSI, Fisher Transform, Squeeze, Hull MA, etc.) along with a visual strength bar that represents the intensity of the trading signal.

Signal Generation:

Buy and sell signals are generated when a predefined number of conditions are met and confirmed over multiple bars. These signals are clearly displayed on the chart with arrows, making it easier to spot potential entry and exit points.

Alert Setup:

Built-in alert conditions allow you to receive real-time notifications when trading signals are generated, helping you stay on top of market movements.

"Professional MSTI+ Trading Indicator" is designed to enhance your trading strategy by providing a multi-faceted market analysis and an intuitive visual interface. While the presets offer a robust starting point, they may require manual calibration on certain pairs, giving you the flexibility to configure your own unique strategies and signals.

AI Adaptive Oscillator [PhenLabs]📊 Algorithmic Adaptive Oscillator

Version: PineScript™ v6

📌 Description

The AI Adaptive Oscillator is a sophisticated technical indicator that employs ensemble learning and adaptive weighting techniques to analyze market conditions. This innovative oscillator combines multiple traditional technical indicators through an AI-driven approach that continuously evaluates and adjusts component weights based on historical performance. By integrating statistical modeling with machine learning principles, the indicator adapts to changing market dynamics, providing traders with a responsive and reliable tool for market analysis.

🚀 Points of Innovation:

Ensemble learning framework with adaptive component weighting

Performance-based scoring system using directional accuracy

Dynamic volatility-adjusted smoothing mechanism

Intelligent signal filtering with cooldown and magnitude requirements

Signal confidence levels based on multi-factor analysis

🔧 Core Components

Ensemble Framework : Combines up to five technical indicators with performance-weighted integration

Adaptive Weighting : Continuous performance evaluation with automated weight adjustment

Volatility-Based Smoothing : Adapts sensitivity based on current market volatility

Pattern Recognition : Identifies potential reversal patterns with signal qualification criteria

Dynamic Visualization : Professional color schemes with gradient intensity representation

Signal Confidence : Three-tiered confidence assessment for trading signals

🔥 Key Features

The indicator provides comprehensive market analysis through:

Multi-Component Ensemble : Integrates RSI, CCI, Stochastic, MACD, and Volume-weighted momentum

Performance Scoring : Evaluates each component based on directional prediction accuracy

Adaptive Smoothing : Automatically adjusts based on market volatility

Pattern Detection : Identifies potential reversal patterns in overbought/oversold conditions

Signal Filtering : Prevents excessive signals through cooldown periods and minimum change requirements

Confidence Assessment : Displays signal strength through intuitive confidence indicators (average, above average, excellent)

🎨 Visualization

Gradient-Filled Oscillator : Color intensity reflects strength of market movement

Clear Signal Markers : Distinct bullish and bearish pattern signals with confidence indicators

Range Visualization : Clean representation of oscillator values from -6 to 6

Zero Line : Clear demarcation between bullish and bearish territory

Customizable Colors : Color schemes that can be adjusted to match your chart style

Confidence Symbols : Intuitive display of signal confidence (no symbol, +, or ++) alongside direction markers

📖 Usage Guidelines

⚙️ Settings Guide

Color Settings

Bullish Color

Default: #2b62fa (Blue)

This setting controls the color representation for bullish movements in the oscillator. The color appears when the oscillator value is positive (above zero), with intensity indicating the strength of the bullish momentum. A brighter shade indicates stronger bullish pressure.

Bearish Color

Default: #ce9851 (Amber)

This setting determines the color representation for bearish movements in the oscillator. The color appears when the oscillator value is negative (below zero), with intensity reflecting the strength of the bearish momentum. A more saturated shade indicates stronger bearish pressure.

Signal Settings

Signal Cooldown (bars)

Default: 10

Range: 1-50

This parameter sets the minimum number of bars that must pass before a new signal of the same type can be generated. Higher values reduce signal frequency and help prevent overtrading during choppy market conditions. Lower values increase signal sensitivity but may generate more false positives.

Min Change For New Signal

Default: 1.5

Range: 0.5-3.0

This setting defines the minimum required change in oscillator value between consecutive signals of the same type. It ensures that new signals represent meaningful changes in market conditions rather than minor fluctuations. Higher values produce fewer but potentially higher-quality signals, while lower values increase signal frequency.

AI Core Settings

Base Length

Default: 14

Minimum: 2

This fundamental setting determines the primary calculation period for all technical components in the ensemble (RSI, CCI, Stochastic, etc.). It represents the lookback window for each component’s base calculation. Shorter periods create a more responsive but potentially noisier oscillator, while longer periods produce smoother signals with potential lag.

Adaptive Speed

Default: 0.1

Range: 0.01-0.3

Controls how quickly the oscillator adapts to new market conditions through its volatility-adjusted smoothing mechanism. Higher values make the oscillator more responsive to recent price action but potentially more erratic. Lower values create smoother transitions but may lag during rapid market changes. This parameter directly influences the indicator’s adaptiveness to market volatility.

Learning Lookback Period

Default: 150

Minimum: 10

Determines the historical data range used to evaluate each ensemble component’s performance and calculate adaptive weights. This setting controls how far back the AI “learns” from past performance to optimize current signals. Longer periods provide more stable weight distribution but may be slower to adapt to regime changes. Shorter periods adapt more quickly but may overreact to recent anomalies.

Ensemble Size

Default: 5

Range: 2-5

Specifies how many technical components to include in the ensemble calculation.

Understanding The Interaction Between Settings

Base Length and Learning Lookback : The base length determines the reactivity of individual components, while the lookback period determines how their weights are adjusted. These should be balanced according to your timeframe - shorter timeframes benefit from shorter base lengths, while the lookback should generally be 10-15 times the base length for optimal learning.

Adaptive Speed and Signal Cooldown : These settings control sensitivity from different angles. Increasing adaptive speed makes the oscillator more responsive, while reducing signal cooldown increases signal frequency. For conservative trading, keep adaptive speed low and cooldown high; for aggressive trading, do the opposite.

Ensemble Size and Min Change : Larger ensembles provide more stable signals, allowing for a lower minimum change threshold. Smaller ensembles might benefit from a higher threshold to filter out noise.

Understanding Signal Confidence Levels

The indicator provides three distinct confidence levels for both bullish and bearish signals:

Average Confidence (▲ or ▼) : Basic signal that meets the minimum pattern and filtering criteria. These signals indicate potential reversals but with moderate confidence in the prediction. Consider using these as initial alerts that may require additional confirmation.

Above Average Confidence (▲+ or ▼+) : Higher reliability signal with stronger underlying metrics. These signals demonstrate greater consensus among the ensemble components and/or stronger historical performance. They offer increased probability of successful reversals and can be traded with less additional confirmation.

Excellent Confidence (▲++ or ▼++) : Highest quality signals with exceptional underlying metrics. These signals show strong agreement across oscillator components, excellent historical performance, and optimal signal strength. These represent the indicator’s highest conviction trade opportunities and can be prioritized in your trading decisions.

Confidence assessment is calculated through a multi-factor analysis including:

Historical performance of ensemble components

Degree of agreement between different oscillator components

Relative strength of the signal compared to historical thresholds

✅ Best Use Cases:

Identify potential market reversals through oscillator extremes

Filter trade signals based on AI-evaluated component weights

Monitor changing market conditions through oscillator direction and intensity

Confirm trade signals from other indicators with adaptive ensemble validation

Detect early momentum shifts through pattern recognition

Prioritize trading opportunities based on signal confidence levels

Adjust position sizing according to signal confidence (larger for ++ signals, smaller for standard signals)

⚠️ Limitations

Requires sufficient historical data for accurate performance scoring

Ensemble weights may lag during dramatic market condition changes

Higher ensemble sizes require more computational resources

Performance evaluation quality depends on the learning lookback period length

Even high confidence signals should be considered within broader market context

💡 What Makes This Unique

Adaptive Intelligence : Continuously adjusts component weights based on actual performance

Ensemble Methodology : Combines strength of multiple indicators while minimizing individual weaknesses

Volatility-Adjusted Smoothing : Provides appropriate sensitivity across different market conditions

Performance-Based Learning : Utilizes historical accuracy to improve future predictions

Intelligent Signal Filtering : Reduces noise and false signals through sophisticated filtering criteria

Multi-Level Confidence Assessment : Delivers nuanced signal quality information for optimized trading decisions

🔬 How It Works

The indicator processes market data through five main components:

Ensemble Component Calculation :

Normalizes traditional indicators to consistent scale

Includes RSI, CCI, Stochastic, MACD, and volume components

Adapts based on the selected ensemble size

Performance Evaluation :

Analyzes directional accuracy of each component

Calculates continuous performance scores

Determines adaptive component weights

Oscillator Integration :

Combines weighted components into unified oscillator

Applies volatility-based adaptive smoothing

Scales final values to -6 to 6 range

Signal Generation :

Detects potential reversal patterns

Applies cooldown and magnitude filters

Generates clear visual markers for qualified signals

Confidence Assessment :

Evaluates component agreement, historical accuracy, and signal strength

Classifies signals into three confidence tiers (average, above average, excellent)

Displays intuitive confidence indicators (no symbol, +, ++) alongside direction markers

💡 Note:

The AI Adaptive Oscillator performs optimally when used with appropriate timeframe selection and complementary indicators. Its adaptive nature makes it particularly valuable during changing market conditions, where traditional fixed-weight indicators often lose effectiveness. The ensemble approach provides a more robust analysis by leveraging the collective intelligence of multiple technical methodologies. Pay special attention to the signal confidence indicators to optimize your trading decisions - excellent (++) signals often represent the most reliable trade opportunities.

QT RSI [ W.ARITAS ]The QT RSI is an innovative technical analysis indicator designed to enhance precision in market trend identification and decision-making. Developed using advanced concepts in quantum mechanics, machine learning (LSTM), and signal processing, this indicator provides actionable insights for traders across multiple asset classes, including stocks, crypto, and forex.

Key Features:

Dynamic Color Gradient: Visualizes market conditions for intuitive interpretation:

Green: Strong buy signal indicating bullish momentum.

Blue: Neutral or observation zone, suggesting caution or lack of a clear trend.

Red: Strong sell signal indicating bearish momentum.

Quantum-Enhanced RSI: Integrates adaptive energy levels, dynamic smoothing, and quantum oscillators for precise trend detection.

Hybrid Machine Learning Model: Combines LSTM neural networks and wavelet transforms for accurate prediction and signal refinement.

Customizable Settings: Includes advanced parameters for dynamic thresholds, sensitivity adjustment, and noise reduction using Kalman and Jurik filters.

How to Use:

Interpret the Color Gradient:

Green Zone: Indicates bullish conditions and potential buy opportunities. Look for upward momentum in the RSI plot.

Blue Zone: Represents a neutral or consolidation phase. Monitor the market for trend confirmation.

Red Zone: Indicates bearish conditions and potential sell opportunities. Look for downward momentum in the RSI plot.

Follow Overbought/Oversold Boundaries:

Use the upper and lower RSI boundaries to identify overbought and oversold conditions.

Leverage Advanced Filtering:

The smoothed signals and quantum oscillator provide a robust framework for filtering false signals, making it suitable for volatile markets.

Application: Ideal for traders and analysts seeking high-precision tools for:

Identifying entry and exit points.

Detecting market reversals and momentum shifts.

Enhancing algorithmic trading strategies with cutting-edge analytics.

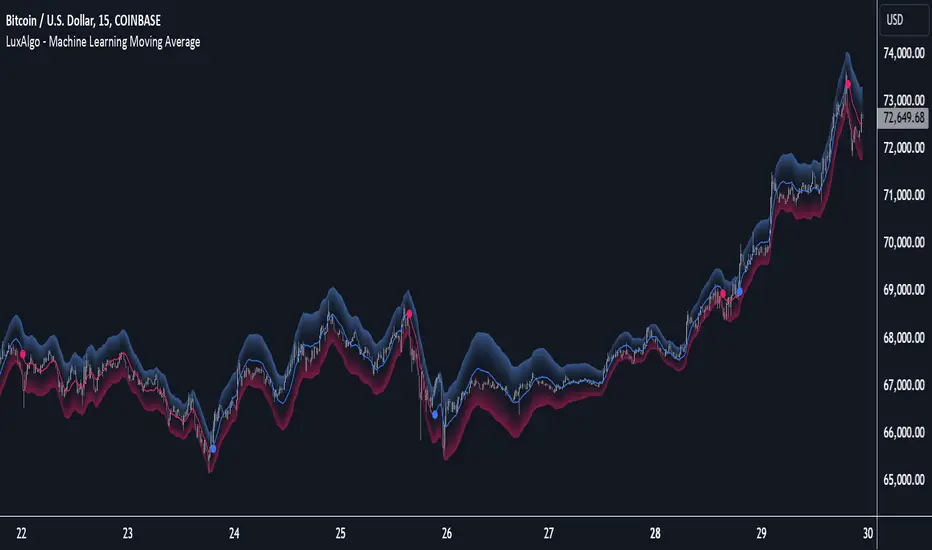

Machine Learning Moving Average [LuxAlgo]The Machine Learning Moving Average (MLMA) is a responsive moving average making use of the weighting function obtained Gaussian Process Regression method. Characteristic such as responsiveness and smoothness can be adjusted by the user from the settings.

The moving average also includes bands, used to highlight possible reversals.

🔶 USAGE

The Machine Learning Moving Average smooths out noisy variations from the price, directly estimating the underlying trend in the price.

A higher "Window" setting will return a longer-term moving average while increasing the "Forecast" setting will affect the responsiveness and smoothness of the moving average, with higher positive values returning a more responsive moving average and negative values returning a smoother but less responsive moving average.

Do note that an excessively high "Forecast" setting will result in overshoots, with the moving average having a poor fit with the price.

The moving average color is determined according to the estimated trend direction based on the bands described below, shifting to blue (default) in an uptrend and fushia (default) in downtrends.

The upper and lower extremities represent the range within which price movements likely fluctuate.

Signals are generated when the price crosses above or below the band extremities, with turning points being highlighted by colored circles on the chart.

🔶 SETTINGS

Window: Calculation period of the moving average. Higher values yield a smoother average, emphasizing long-term trends and filtering out short-term fluctuations.

Forecast: Sets the projection horizon for Gaussian Process Regression. Higher values create a more responsive moving average but will result in more overshoots, potentially worsening the fit with the price. Negative values will result in a smoother moving average.

Sigma: Controls the standard deviation of the Gaussian kernel, influencing weight distribution. Higher Sigma values return a longer-term moving average.

Multiplicative Factor: Adjusts the upper and lower extremity bounds, with higher values widening the bands and lowering the amount of returned turning points.

🔶 RELATED SCRIPTS

Machine-Learning-Gaussian-Process-Regression

SuperTrend-AI-Clustering

Machine Learning using Neural Networks | EducationalThe script provided is a comprehensive illustration of how to implement and execute a simplistic Neural Network (NN) on TradingView using PineScript.

It encompasses the entire workflow from data input, weight initialization, implicit neuron calculation, feedforward computation, backpropagation for weight adjustments, generating predictions, to visualizing the Mean Squared Error (MSE) Loss Curve for monitoring the training phase.

In the visual example above, you can see that the prediction is not aligned with the actual value. This is intentional for demonstrative purposes, and by incrementing the Epochs or Learning Rate, you will see these two values converge as the accuracy increases.

Hyperparameters:

Learning Rate, Epochs, and the choice between Simple Backpropagation and a verbose version are declared as script inputs, allowing users to tailor the training process.

Initialization:

Random initialization of weight matrices (w1, w2) is performed to ensure asymmetry, promoting effective gradient updates. A seed is added for reproducibility.

Utility Functions:

Functions for matrix randomization, sigmoid activation, MSE loss calculation, data normalization, and standardization are defined to streamline the computation process.

Neural Network Computation:

The feedforward function computes the hidden and output layer values given the input.

Two variants of the backpropagation function are provided for weight adjustment, with one offering a more verbose step-by-step computation of gradients.

A wrapper train_nn function iterates through epochs, performing feedforward, loss computation, and backpropagation in each epoch while logging and collecting loss values.

Training Invocation:

The input data is prepared by normalizing it to a value between 0 and 1 using the maximum standardized value, and the training process is invoked only on the last confirmed bar to preserve computational resources.

Output Forecasting and Visualization:

Post training, the NN's output (predicted price) is computed, standardized and visualized alongside the actual price on the chart.

The MSE loss between the predicted and actual prices is visualized, providing insight into the prediction accuracy.

Optionally, the MSE Loss Curve is plotted on the chart, illustrating the loss trajectory through epochs, assisting in understanding the training performance.

Customizable Visualization:

Various inputs control visualization aspects like Chart Scaling, Chart Horizontal Offset, and Chart Vertical Offset, allowing users to adapt the visualization to their preference.

-------------------------------------------------------

The following is this Neural Network structure, consisting of one hidden layer, with two hidden neurons.

Through understanding the steps outlined in my code, one should be able to scale the NN in any way they like, such as changing the input / output data and layers to fit their strategy ideas.

Additionally, one could forgo the backpropagation function, and load their own trained weights into the w1 and w2 matrices, to have this code run purely for inference.

-------------------------------------------------------

While this demonstration does create a “prediction”, it is on historical data. The purpose here is educational, rather than providing a ready tool for non-programmer consumers.

Normally in Machine Learning projects, the training process would be split into two segments, the Training and the Validation parts. For the purpose of conveying the core concept in a concise and non-repetitive way, I have foregone the Validation part. However, it is merely the application of your trained network on new data (feedforward), and monitoring the loss curve.

Essentially, checking the accuracy on “unseen” data, while training it on “seen” data.

-------------------------------------------------------

I hope that this code will help developers create interesting machine learning applications within the Tradingview ecosystem.