Trend SuggestionsThis brings together a number of variables to produce trend predictions that could be utilized as decision-making tools.

Uses the aforementioned price and volume derivatives

- A moving average and three weighted moving averages (WMA1, WMA2, WMA3)

- Super Trend Line (ST)

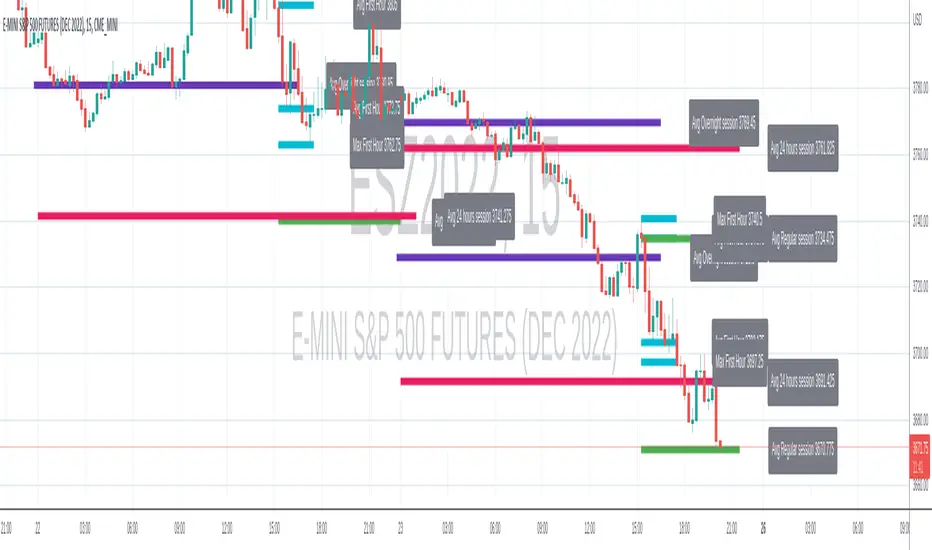

- Opening Range Breakout on Five Minutes, Resistance Bands Pocket pivots, support, and price volume

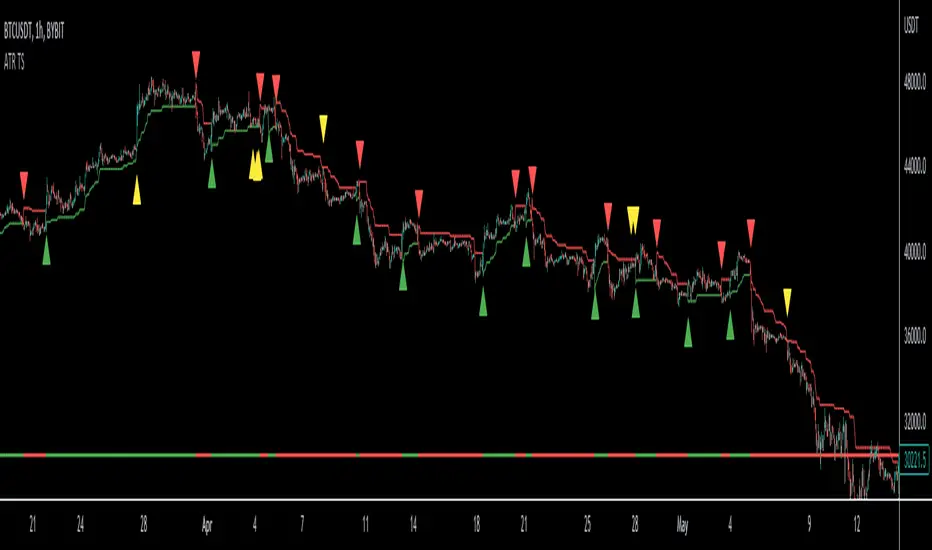

he Direction is determined by the High and Low Bands of WMAs and the Supertrend Line, which are used to determine the Upper and Lower Lines around the Price. When the price passes below the lower boundary of the band, a downtrend is said to have begun.

Similarly, for an uptrend, this continues until the price passes over the upper edge of the band. Teal for an uptrend and fuchsia for a downturn area shared by the band to identify the trend.

The first five minutes of the breakout lines have a tiny buffer augmentation of 11% applied to them.

Based on what has been observed, support and resistance zones have been somewhat changed from the figures that are often utilized (might work other markets as well)

The markings that may be seen are as follows:

- Blue Triangle indicates a pocket pivot with an upward bias;

- Maroon Triangle indicates a pocket pivot with a downward bias;

- Teal colored Diamonds indicate price upthrusts and potential trend confirmation locations, depending on success or failure.

- Similar backdrop color changes that look as vertical shading are also used to identify them.

- Fuchsia-colored diamonds indicate price declines and a potential trend, depending on whether it persists or fails.

- Dark green and maroon square boxes indicate potential price reversals in the support and resistance bands, respectively.

It goes without saying that this work is derived from numerous other open-source community initiatives.

Feel free to adjust anything you'd like, and we appreciate any feedback.

Pine Script® indicator