PineStats█ OVERVIEW

PineStats is a comprehensive statistical analysis library for Pine Script v6, providing 104 functions across 6 modules. Built for quantitative traders, researchers, and indicator developers who need professional-grade statistics without reinventing the wheel.

For building mean-reversion strategies, analyzing return distributions, measuring correlations, or testing for market regimes.

█ MODULES

CORE STATISTICS (20 functions)

• Central tendency: mean, median, WMA, EMA

• Dispersion: variance, stdev, MAD, range

• Standardization: z-score, robust z-score, normalize, percentile

• Distribution shape: skewness, kurtosis

PROBABILITY DISTRIBUTIONS (17 functions)

• Normal: PDF, CDF, inverse CDF (quantile function)

• Power-law: Hill estimator, MLE alpha, survival function

• Exponential: PDF, CDF, rate estimation

• Normality testing: Jarque-Bera test

ENTROPY (9 functions)

• Shannon entropy (information theory)

• Tsallis entropy (non-extensive, fat-tail sensitive)

• Permutation entropy (ordinal patterns)

• Approximate entropy (regularity measure)

• Entropy-based regime detection

PROBABILITY (21 functions)

• Win rates and expected value

• First passage time estimation

• TP/SL probability analysis

• Conditional probability and Bayes updates

• Streak and drawdown probabilities

REGRESSION (19 functions)

• Linear regression: slope, intercept, forecast

• Goodness of fit: R², adjusted R², standard error

• Statistical tests: t-statistic, p-value, significance

• Trend analysis: strength, angle, acceleration

• Quadratic regression

CORRELATION (18 functions)

• Pearson, Spearman, Kendall correlation

• Covariance, beta, alpha (Jensen's)

• Rolling correlation analysis

• Autocorrelation and cross-correlation

• Information ratio, tracking error

█ QUICK START

import HenriqueCentieiro/PineStats/1 as stats

// Z-score for mean reversion

z = stats.zscore(close, 20)

// Test if returns are normally distributed

returns = (close - close ) / close

isGaussian = stats.is_normal(returns, 100, 0.05)

// Regression channel

= stats.linreg_channel(close, 50, 2.0)

// Correlation with benchmark

spyReturns = request.security("SPY", timeframe.period, close/close - 1)

beta = stats.beta(returns, spyReturns, 60)

█ USE CASES

✓ Mean Reversion — z-scores, percentiles, Bollinger-style analysis

✓ Regime Detection — entropy measures, correlation regimes

✓ Risk Analysis — drawdown probability, VaR via quantiles

✓ Strategy Evaluation — expected value, win rates, R:R analysis

✓ Distribution Analysis — normality tests, fat-tail detection

✓ Multi-Asset — beta, alpha, correlation, relative strength

█ NOTES

• All functions return `na` on invalid inputs

• Designed for Pine Script v6

• Fully documented in the library header

• Part of the Pine ecosystem: PineStats, PineQuant, PineCriticality, PineWavelet

█ REFERENCES

• Abramowitz & Stegun — Normal CDF approximation

• Acklam's algorithm — Inverse normal CDF

• Hill estimator — Power-law tail estimation

• Tsallis statistics — Non-extensive entropy

Full documentation in the library header.

mean(src, length)

Calculates the arithmetic mean (simple moving average) over a lookback period

Parameters:

src (float) : Source series

length (simple int) : Lookback period (must be >= 1)

Returns: Arithmetic mean of the last `length` values, or `na` if inputs invalid

wma_custom(src, length)

Calculates weighted moving average with linearly decreasing weights

Parameters:

src (float) : Source series

length (simple int) : Lookback period (must be >= 1)

Returns: Weighted moving average, or `na` if inputs invalid

ema_custom(src, length)

Calculates exponential moving average

Parameters:

src (float) : Source series

length (simple int) : Lookback period (must be >= 1)

Returns: Exponential moving average, or `na` if inputs invalid

median(src, length)

Calculates the median value over a lookback period

Parameters:

src (float) : Source series

length (simple int) : Lookback period (must be >= 1)

Returns: Median value, or `na` if inputs invalid

variance(src, length)

Calculates population variance over a lookback period

Parameters:

src (float) : Source series

length (simple int) : Lookback period (must be >= 1)

Returns: Population variance, or `na` if inputs invalid

stdev(src, length)

Calculates population standard deviation over a lookback period

Parameters:

src (float) : Source series

length (simple int) : Lookback period (must be >= 1)

Returns: Population standard deviation, or `na` if inputs invalid

mad(src, length)

Calculates Median Absolute Deviation (MAD) - robust dispersion measure

Parameters:

src (float) : Source series

length (simple int) : Lookback period (must be >= 1)

Returns: MAD value, or `na` if inputs invalid

data_range(src, length)

Calculates the range (highest - lowest) over a lookback period

Parameters:

src (float) : Source series

length (simple int) : Lookback period (must be >= 1)

Returns: Range value, or `na` if inputs invalid

zscore(src, length)

Calculates z-score (number of standard deviations from mean)

Parameters:

src (float) : Source series

length (simple int) : Lookback period for mean and stdev calculation (must be >= 2)

Returns: Z-score, or `na` if inputs invalid or stdev is zero

zscore_robust(src, length)

Calculates robust z-score using median and MAD (resistant to outliers)

Parameters:

src (float) : Source series

length (simple int) : Lookback period (must be >= 2)

Returns: Robust z-score, or `na` if inputs invalid or MAD is zero

normalize(src, length)

Normalizes value to range using min-max scaling

Parameters:

src (float) : Source series

length (simple int) : Lookback period (must be >= 1)

Returns: Normalized value in , or `na` if inputs invalid or range is zero

percentile(src, length)

Calculates percentile rank of current value within lookback window

Parameters:

src (float) : Source series

length (simple int) : Lookback period (must be >= 1)

Returns: Percentile rank (0 to 100), or `na` if inputs invalid

winsorize(src, length, lower_pct, upper_pct)

Winsorizes values by clamping to percentile bounds (reduces outlier impact)

Parameters:

src (float) : Source series

length (simple int) : Lookback period (must be >= 1)

lower_pct (simple float) : Lower percentile bound (0-100, e.g., 5 for 5th percentile)

upper_pct (simple float) : Upper percentile bound (0-100, e.g., 95 for 95th percentile)

Returns: Winsorized value clamped to bounds

skewness(src, length)

Calculates sample skewness (measure of distribution asymmetry)

Parameters:

src (float) : Source series

length (simple int) : Lookback period (must be >= 3)

Returns: Skewness value (negative = left tail, positive = right tail), or `na` if invalid

kurtosis(src, length)

Calculates excess kurtosis (measure of distribution tail heaviness)

Parameters:

src (float) : Source series

length (simple int) : Lookback period (must be >= 4)

Returns: Excess kurtosis (>0 = heavy tails, <0 = light tails), or `na` if invalid

count_valid(src, length)

Counts non-na values in lookback window (useful for data quality checks)

Parameters:

src (float) : Source series

length (simple int) : Lookback period (must be >= 1)

Returns: Count of valid (non-na) values

sum(src, length)

Calculates sum over lookback period

Parameters:

src (float) : Source series

length (simple int) : Lookback period (must be >= 1)

Returns: Sum of values, or `na` if inputs invalid

cumsum(src)

Calculates cumulative sum (running total from first bar)

Parameters:

src (float) : Source series

Returns: Cumulative sum

change(src, length)

Returns the change (difference) from n bars ago

Parameters:

src (float) : Source series

length (simple int) : Number of bars to look back (must be >= 1)

Returns: Current value minus value from `length` bars ago

roc(src, length)

Calculates Rate of Change (percentage change from n bars ago)

Parameters:

src (float) : Source series

length (simple int) : Number of bars to look back (must be >= 1)

Returns: Percentage change as decimal (0.05 = 5%), or `na` if invalid

normal_pdf_standard(x)

Calculates the standard normal probability density function (PDF)

Parameters:

x (float) : The value to evaluate

Returns: PDF value at x for standard normal N(0,1)

normal_pdf(x, mu, sigma)

Calculates the normal probability density function (PDF)

Parameters:

x (float) : The value to evaluate

mu (float) : Mean of the distribution (default: 0)

sigma (float) : Standard deviation (default: 1, must be > 0)

Returns: PDF value at x for normal N(mu, sigma²)

normal_cdf_standard(x)

Calculates the standard normal cumulative distribution function (CDF)

Parameters:

x (float) : The value to evaluate

Returns: Probability P(X <= x) for standard normal N(0,1)

@description Uses Abramowitz & Stegun approximation (formula 7.1.26), accurate to ~1.5e-7

normal_cdf(x, mu, sigma)

Calculates the normal cumulative distribution function (CDF)

Parameters:

x (float) : The value to evaluate

mu (float) : Mean of the distribution (default: 0)

sigma (float) : Standard deviation (default: 1, must be > 0)

Returns: Probability P(X <= x) for normal N(mu, sigma²)

normal_inv_standard(p)

Calculates the inverse standard normal CDF (quantile function)

Parameters:

p (float) : Probability value (must be in (0, 1))

Returns: x such that P(X <= x) = p for standard normal N(0,1)

@description Uses Acklam's algorithm, accurate to ~1.15e-9

normal_inv(p, mu, sigma)

Calculates the inverse normal CDF (quantile function)

Parameters:

p (float) : Probability value (must be in (0, 1))

mu (float) : Mean of the distribution

sigma (float) : Standard deviation (must be > 0)

Returns: x such that P(X <= x) = p for normal N(mu, sigma²)

power_law_alpha(src, length, tail_pct)

Estimates power-law exponent (alpha) using Hill estimator

Parameters:

src (float) : Source series (typically absolute returns or drawdowns)

length (simple int) : Lookback period (must be >= 10 for reliable estimates)

tail_pct (simple float) : Percentage of data to use for tail estimation (default: 0.1 = top 10%)

Returns: Estimated alpha (tail index), typically 2-4 for financial data

@description Alpha < 2 indicates infinite variance (very heavy tails)

@description Alpha < 3 indicates infinite kurtosis

@description Alpha > 4 suggests near-Gaussian behavior

power_law_alpha_mle(src, length, x_min)

Estimates power-law alpha using maximum likelihood (Clauset method)

Parameters:

src (float) : Source series (positive values expected)

length (simple int) : Lookback period (must be >= 20)

x_min (float) : Minimum threshold for power-law behavior

Returns: Estimated alpha using MLE

power_law_pdf(x, alpha, x_min)

Calculates power-law probability density (Pareto Type I)

Parameters:

x (float) : Value to evaluate (must be >= x_min)

alpha (float) : Power-law exponent (must be > 1)

x_min (float) : Minimum value / scale parameter (must be > 0)

Returns: PDF value

power_law_survival(x, alpha, x_min)

Calculates power-law survival function P(X > x)

Parameters:

x (float) : Value to evaluate (must be >= x_min)

alpha (float) : Power-law exponent (must be > 1)

x_min (float) : Minimum value / scale parameter (must be > 0)

Returns: Probability of exceeding x

power_law_ks(src, length, alpha, x_min)

Tests if data follows power-law using simplified Kolmogorov-Smirnov

Parameters:

src (float) : Source series

length (simple int) : Lookback period

alpha (float) : Estimated alpha from power_law_alpha()

x_min (float) : Threshold value

Returns: KS statistic (lower = better fit, typically < 0.1 for good fit)

is_power_law(src, length, tail_pct, ks_threshold)

Simple test if distribution appears to follow power-law

Parameters:

src (float) : Source series

length (simple int) : Lookback period

tail_pct (simple float) : Tail percentage for alpha estimation

ks_threshold (simple float) : Maximum KS statistic for acceptance (default: 0.1)

Returns: true if KS test suggests power-law fit

exp_pdf(x, lambda)

Calculates exponential probability density function

Parameters:

x (float) : Value to evaluate (must be >= 0)

lambda (float) : Rate parameter (must be > 0)

Returns: PDF value

exp_cdf(x, lambda)

Calculates exponential cumulative distribution function

Parameters:

x (float) : Value to evaluate (must be >= 0)

lambda (float) : Rate parameter (must be > 0)

Returns: Probability P(X <= x)

exp_lambda(src, length)

Estimates exponential rate parameter (lambda) using MLE

Parameters:

src (float) : Source series (positive values)

length (simple int) : Lookback period

Returns: Estimated lambda (1/mean)

jarque_bera(src, length)

Calculates Jarque-Bera test statistic for normality

Parameters:

src (float) : Source series

length (simple int) : Lookback period (must be >= 10)

Returns: JB statistic (higher = more deviation from normality)

@description Under normality, JB ~ chi-squared(2). JB > 6 suggests non-normality at 5% level

is_normal(src, length, significance)

Tests if distribution is approximately normal

Parameters:

src (float) : Source series

length (simple int) : Lookback period

significance (simple float) : Significance level (default: 0.05)

Returns: true if Jarque-Bera test does not reject normality

shannon_entropy(src, length, n_bins)

Calculates Shannon entropy from a probability distribution

Parameters:

src (float) : Source series

length (simple int) : Lookback period (must be >= 10)

n_bins (simple int) : Number of histogram bins for discretization (default: 10)

Returns: Shannon entropy in bits (log base 2)

@description Higher entropy = more randomness/uncertainty, lower = more predictability

shannon_entropy_norm(src, length, n_bins)

Calculates normalized Shannon entropy

Parameters:

src (float) : Source series

length (simple int) : Lookback period

n_bins (simple int) : Number of histogram bins

Returns: Normalized entropy where 0 = perfectly predictable, 1 = maximum randomness

tsallis_entropy(src, length, q, n_bins)

Calculates Tsallis entropy with q-parameter

Parameters:

src (float) : Source series

length (simple int) : Lookback period (must be >= 10)

q (float) : Entropic index (q=1 recovers Shannon entropy)

n_bins (simple int) : Number of histogram bins

Returns: Tsallis entropy value

@description q < 1: emphasizes rare events (fat tails)

@description q = 1: equivalent to Shannon entropy

@description q > 1: emphasizes common events

optimal_q(src, length)

Estimates optimal q parameter from kurtosis

Parameters:

src (float) : Source series

length (simple int) : Lookback period

Returns: Estimated q value that best captures the distribution's tail behavior

@description Uses relationship: q ≈ (5 + kurtosis) / (3 + kurtosis) for kurtosis > 0

tsallis_q_gaussian(x, q, beta)

Calculates Tsallis q-Gaussian probability density

Parameters:

x (float) : Value to evaluate

q (float) : Tsallis q parameter (must be < 3)

beta (float) : Width parameter (inverse temperature, must be > 0)

Returns: q-Gaussian PDF value

@description q=1 recovers standard Gaussian

permutation_entropy(src, length, order)

Calculates permutation entropy (ordinal pattern complexity)

Parameters:

src (float) : Source series

length (simple int) : Lookback period (must be >= 20)

order (simple int) : Embedding dimension / pattern length (2-5, default: 3)

Returns: Normalized permutation entropy

@description Measures complexity of temporal ordering patterns

@description 0 = perfectly predictable sequence, 1 = random

approx_entropy(src, length, m, r)

Calculates Approximate Entropy (ApEn) - regularity measure

Parameters:

src (float) : Source series

length (simple int) : Lookback period (must be >= 50)

m (simple int) : Embedding dimension (default: 2)

r (simple float) : Tolerance as fraction of stdev (default: 0.2)

Returns: Approximate entropy value (higher = more irregular/complex)

@description Lower ApEn indicates more self-similarity and predictability

entropy_regime(src, length, q, n_bins)

Detects market regime based on entropy level

Parameters:

src (float) : Source series (typically returns)

length (simple int) : Lookback period

q (float) : Tsallis q parameter (use optimal_q() or default 1.5)

n_bins (simple int) : Number of histogram bins

Returns: Regime indicator: -1 = trending (low entropy), 0 = transition, 1 = ranging (high entropy)

entropy_risk(src, length)

Calculates entropy-based risk indicator

Parameters:

src (float) : Source series (typically returns)

length (simple int) : Lookback period

Returns: Risk score where 1 = maximum divergence from Gaussian 1

hit_rate(src, length)

Calculates hit rate (probability of positive outcome) over lookback

Parameters:

src (float) : Source series (positive values count as hits)

length (simple int) : Lookback period

Returns: Hit rate as decimal

hit_rate_cond(condition, length)

Calculates hit rate for custom condition over lookback

Parameters:

condition (bool) : Boolean series (true = hit)

length (simple int) : Lookback period

Returns: Hit rate as decimal

expected_value(src, length)

Calculates expected value of a series

Parameters:

src (float) : Source series

length (simple int) : Lookback period

Returns: Expected value (mean)

expected_value_trade(win_prob, take_profit, stop_loss)

Calculates expected value for a trade with TP and SL levels

Parameters:

win_prob (float) : Probability of hitting TP (0-1)

take_profit (float) : Take profit in price units or %

stop_loss (float) : Stop loss in price units or % (positive value)

Returns: Expected value per trade

@description EV = (win_prob * TP) - ((1 - win_prob) * SL)

breakeven_winrate(take_profit, stop_loss)

Calculates breakeven win rate for given TP/SL ratio

Parameters:

take_profit (float) : Take profit distance

stop_loss (float) : Stop loss distance

Returns: Required win rate for breakeven (EV = 0)

reward_risk_ratio(take_profit, stop_loss)

Calculates the reward-to-risk ratio

Parameters:

take_profit (float) : Take profit distance

stop_loss (float) : Stop loss distance

Returns: R:R ratio

fpt_probability(src, length, target, max_bars)

Estimates probability of price reaching target within N bars

Parameters:

src (float) : Source series (typically returns)

length (simple int) : Lookback for volatility estimation

target (float) : Target move (in same units as src, e.g., % return)

max_bars (simple int) : Maximum bars to consider

Returns: Probability of reaching target within max_bars

@description Based on random walk with drift approximation

fpt_mean(src, length, target)

Estimates mean first passage time to target level

Parameters:

src (float) : Source series (typically returns)

length (simple int) : Lookback for volatility estimation

target (float) : Target move

Returns: Expected number of bars to reach target (can be infinite)

fpt_historical(src, length, target)

Counts historical bars to reach target from each point

Parameters:

src (float) : Source series (typically price or returns)

length (simple int) : Lookback period

target (float) : Target move from each starting point

Returns: Array of first passage times (na if target not reached within lookback)

tp_probability(src, length, tp_distance, sl_distance)

Estimates probability of hitting TP before SL

Parameters:

src (float) : Source series (typically returns)

length (simple int) : Lookback for estimation

tp_distance (float) : Take profit distance (positive)

sl_distance (float) : Stop loss distance (positive)

Returns: Probability of TP being hit first

trade_probability(src, length, tp_pct, sl_pct)

Calculates complete trade probability and EV analysis

Parameters:

src (float) : Source series (typically returns)

length (simple int) : Lookback period

tp_pct (float) : Take profit percentage

sl_pct (float) : Stop loss percentage

Returns: Tuple:

cond_prob(condition_a, condition_b, length)

Calculates conditional probability P(B|A) from historical data

Parameters:

condition_a (bool) : Condition A (the given condition)

condition_b (bool) : Condition B (the outcome)

length (simple int) : Lookback period

Returns: P(B|A) = P(A and B) / P(A)

bayes_update(prior, likelihood, false_positive)

Updates probability using Bayes' theorem

Parameters:

prior (float) : Prior probability P(H)

likelihood (float) : P(E|H) - probability of evidence given hypothesis

false_positive (float) : P(E|~H) - probability of evidence given hypothesis is false

Returns: Posterior probability P(H|E)

streak_prob(win_rate, streak_length)

Calculates probability of N consecutive wins given win rate

Parameters:

win_rate (float) : Single-trade win probability

streak_length (simple int) : Number of consecutive wins

Returns: Probability of streak

losing_streak_prob(win_rate, streak_length)

Calculates probability of experiencing N consecutive losses

Parameters:

win_rate (float) : Single-trade win probability

streak_length (simple int) : Number of consecutive losses

Returns: Probability of losing streak

drawdown_prob(src, length, dd_threshold)

Estimates probability of drawdown exceeding threshold

Parameters:

src (float) : Source series (returns)

length (simple int) : Lookback period

dd_threshold (float) : Drawdown threshold (as positive decimal, e.g., 0.10 = 10%)

Returns: Historical probability of exceeding drawdown threshold

prob_to_odds(prob)

Calculates odds from probability

Parameters:

prob (float) : Probability (0-1)

Returns: Odds (prob / (1 - prob))

odds_to_prob(odds)

Calculates probability from odds

Parameters:

odds (float) : Odds ratio

Returns: Probability (0-1)

implied_prob(decimal_odds)

Calculates implied probability from decimal odds (betting)

Parameters:

decimal_odds (float) : Decimal odds (e.g., 2.5 means $2.50 return per $1 bet)

Returns: Implied probability

logit(prob)

Calculates log-odds (logit) from probability

Parameters:

prob (float) : Probability (must be in (0, 1))

Returns: Log-odds

inv_logit(log_odds)

Calculates probability from log-odds (inverse logit / sigmoid)

Parameters:

log_odds (float) : Log-odds value

Returns: Probability (0-1)

linreg_slope(src, length)

Calculates linear regression slope

Parameters:

src (float) : Source series

length (simple int) : Lookback period (must be >= 2)

Returns: Slope coefficient (change per bar)

linreg_intercept(src, length)

Calculates linear regression intercept

Parameters:

src (float) : Source series

length (simple int) : Lookback period (must be >= 2)

Returns: Intercept (predicted value at oldest bar in window)

linreg_value(src, length)

Calculates predicted value at current bar using linear regression

Parameters:

src (float) : Source series

length (simple int) : Lookback period

Returns: Predicted value at current bar (end of regression line)

linreg_forecast(src, length, offset)

Forecasts value N bars ahead using linear regression

Parameters:

src (float) : Source series

length (simple int) : Lookback period for regression

offset (simple int) : Bars ahead to forecast (positive = future)

Returns: Forecasted value

linreg_channel(src, length, mult)

Calculates linear regression channel with bands

Parameters:

src (float) : Source series

length (simple int) : Lookback period

mult (simple float) : Standard deviation multiplier for bands

Returns: Tuple:

r_squared(src, length)

Calculates R-squared (coefficient of determination)

Parameters:

src (float) : Source series

length (simple int) : Lookback period

Returns: R² value where 1 = perfect linear fit

adj_r_squared(src, length)

Calculates adjusted R-squared (accounts for sample size)

Parameters:

src (float) : Source series

length (simple int) : Lookback period

Returns: Adjusted R² value

std_error(src, length)

Calculates standard error of estimate (residual standard deviation)

Parameters:

src (float) : Source series

length (simple int) : Lookback period

Returns: Standard error

residual(src, length)

Calculates residual at current bar

Parameters:

src (float) : Source series

length (simple int) : Lookback period

Returns: Residual (actual - predicted)

residuals(src, length)

Returns array of all residuals in lookback window

Parameters:

src (float) : Source series

length (simple int) : Lookback period

Returns: Array of residuals

t_statistic(src, length)

Calculates t-statistic for slope coefficient

Parameters:

src (float) : Source series

length (simple int) : Lookback period

Returns: T-statistic (slope / standard error of slope)

slope_pvalue(src, length)

Approximates p-value for slope t-test (two-tailed)

Parameters:

src (float) : Source series

length (simple int) : Lookback period

Returns: Approximate p-value

is_significant(src, length, alpha)

Tests if regression slope is statistically significant

Parameters:

src (float) : Source series

length (simple int) : Lookback period

alpha (simple float) : Significance level (default: 0.05)

Returns: true if slope is significant at alpha level

trend_strength(src, length)

Calculates normalized trend strength based on R² and slope

Parameters:

src (float) : Source series

length (simple int) : Lookback period

Returns: Trend strength where sign indicates direction

trend_angle(src, length)

Calculates trend angle in degrees

Parameters:

src (float) : Source series

length (simple int) : Lookback period

Returns: Angle in degrees (positive = uptrend, negative = downtrend)

linreg_acceleration(src, length)

Calculates trend acceleration (second derivative)

Parameters:

src (float) : Source series

length (simple int) : Lookback period for each regression

Returns: Acceleration (change in slope)

linreg_deviation(src, length)

Calculates deviation from regression line in standard error units

Parameters:

src (float) : Source series

length (simple int) : Lookback period

Returns: Deviation in standard error units (like z-score)

quadreg_coefficients(src, length)

Fits quadratic regression and returns coefficients

Parameters:

src (float) : Source series

length (simple int) : Lookback period (must be >= 4)

Returns: Tuple: for y = a*x² + b*x + c

quadreg_value(src, length)

Calculates quadratic regression value at current bar

Parameters:

src (float) : Source series

length (simple int) : Lookback period

Returns: Predicted value from quadratic fit

correlation(x, y, length)

Calculates Pearson correlation coefficient between two series

Parameters:

x (float) : First series

y (float) : Second series

length (simple int) : Lookback period (must be >= 3)

Returns: Correlation coefficient

covariance(x, y, length)

Calculates sample covariance between two series

Parameters:

x (float) : First series

y (float) : Second series

length (simple int) : Lookback period (must be >= 2)

Returns: Covariance value

beta(asset, benchmark, length)

Calculates beta coefficient (slope of regression of y on x)

Parameters:

asset (float) : Asset returns series

benchmark (float) : Benchmark returns series

length (simple int) : Lookback period

Returns: Beta coefficient

@description Beta = Cov(asset, benchmark) / Var(benchmark)

alpha(asset, benchmark, length, risk_free)

Calculates alpha (Jensen's alpha / intercept)

Parameters:

asset (float) : Asset returns series

benchmark (float) : Benchmark returns series

length (simple int) : Lookback period

risk_free (float) : Risk-free rate (default: 0)

Returns: Alpha value (excess return not explained by beta)

spearman(x, y, length)

Calculates Spearman rank correlation coefficient

Parameters:

x (float) : First series

y (float) : Second series

length (simple int) : Lookback period (must be >= 3)

Returns: Spearman correlation

@description More robust to outliers than Pearson correlation

kendall_tau(x, y, length)

Calculates Kendall's tau rank correlation (simplified)

Parameters:

x (float) : First series

y (float) : Second series

length (simple int) : Lookback period (must be >= 3)

Returns: Kendall's tau

correlation_change(x, y, length, change_period)

Calculates change in correlation over time

Parameters:

x (float) : First series

y (float) : Second series

length (simple int) : Lookback period for correlation

change_period (simple int) : Period over which to measure change

Returns: Change in correlation

correlation_regime(x, y, length, ma_length)

Detects correlation regime based on level and stability

Parameters:

x (float) : First series

y (float) : Second series

length (simple int) : Lookback period for correlation

ma_length (simple int) : Moving average length for smoothing

Returns: Regime: -1 = negative, 0 = uncorrelated, 1 = positive

correlation_stability(x, y, length, stability_length)

Calculates correlation stability (inverse of volatility)

Parameters:

x (float) : First series

y (float) : Second series

length (simple int) : Lookback for correlation

stability_length (simple int) : Lookback for stability calculation

Returns: Stability score where 1 = perfectly stable

relative_strength(asset, benchmark, length)

Calculates relative strength of asset vs benchmark

Parameters:

asset (float) : Asset price series

benchmark (float) : Benchmark price series

length (simple int) : Smoothing period

Returns: Relative strength ratio (normalized)

tracking_error(asset, benchmark, length)

Calculates tracking error (standard deviation of excess returns)

Parameters:

asset (float) : Asset returns

benchmark (float) : Benchmark returns

length (simple int) : Lookback period

Returns: Tracking error (annualize by multiplying by sqrt(252) for daily data)

information_ratio(asset, benchmark, length)

Calculates information ratio (risk-adjusted excess return)

Parameters:

asset (float) : Asset returns

benchmark (float) : Benchmark returns

length (simple int) : Lookback period

Returns: Information ratio

capture_ratio(asset, benchmark, length, up_capture)

Calculates up/down capture ratio

Parameters:

asset (float) : Asset returns

benchmark (float) : Benchmark returns

length (simple int) : Lookback period

up_capture (simple bool) : If true, calculate up capture; if false, down capture

Returns: Capture ratio

autocorrelation(src, length, lag)

Calculates autocorrelation at specified lag

Parameters:

src (float) : Source series

length (simple int) : Lookback period

lag (simple int) : Lag for autocorrelation (default: 1)

Returns: Autocorrelation at specified lag

partial_autocorr(src, length)

Calculates partial autocorrelation at lag 1

Parameters:

src (float) : Source series

length (simple int) : Lookback period

Returns: PACF at lag 1 (equals ACF at lag 1)

autocorr_test(src, length, max_lag)

Tests for significant autocorrelation (Ljung-Box inspired)

Parameters:

src (float) : Source series

length (simple int) : Lookback period

max_lag (simple int) : Maximum lag to test

Returns: Sum of squared autocorrelations (higher = more autocorrelation)

cross_correlation(x, y, length, lag)

Calculates cross-correlation at specified lag

Parameters:

x (float) : First series

y (float) : Second series (lagged)

length (simple int) : Lookback period

lag (simple int) : Lag to apply to y (positive = y leads x)

Returns: Cross-correlation at specified lag

cross_correlation_peak(x, y, length, max_lag)

Finds lag with maximum cross-correlation

Parameters:

x (float) : First series

y (float) : Second series

length (simple int) : Lookback period

max_lag (simple int) : Maximum lag to search (both directions)

Returns: Tuple:

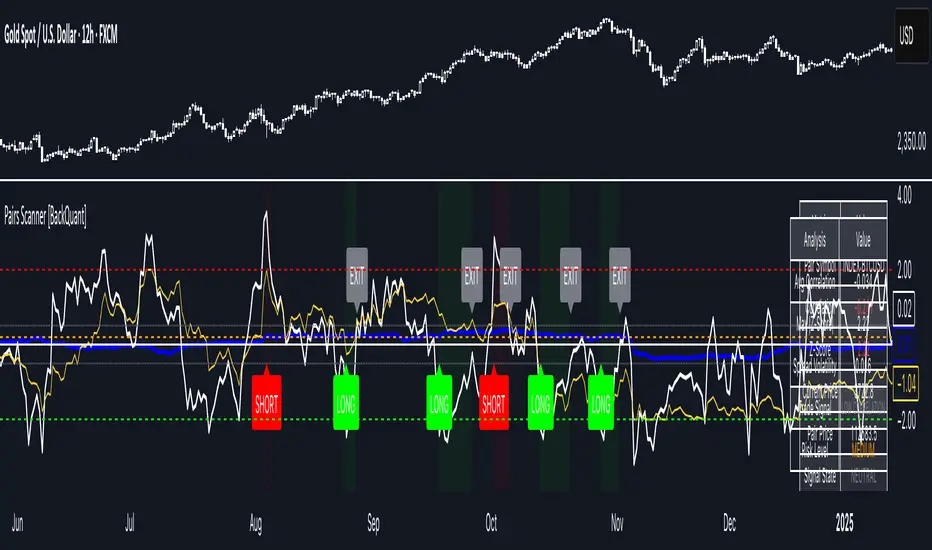

Correlation

Gold Inverse Correlation TrackerGold Inverse Correlation Tracker - Professional Multi-Asset Analysis

What This Indicator Does:

This indicator monitors the real-time correlation between Gold and five key financial assets that historically move inversely (opposite) to gold prices. It displays these relationships across three different timeframes simultaneously, giving you both short-term trading signals and long-term trend confirmation.

The indicator tracks:

US Dollar Index (DXY) - Historical correlation: -0.63

Real Interest Rates (TIPS) - Historical correlation: -0.82 (strongest inverse relationship)

10-Year Treasury Yield - Nominal interest rate proxy

S&P 500 (SPX) - Equity market sentiment (variable correlation)

VIX - Volatility index (optional, flight-to-safety indicator)

Why Inverse Correlations Matter for Gold Trading:

Understanding inverse correlations is critical for gold traders because:

Predictive Power - When assets move opposite to gold consistently, you can use their strength/weakness to predict gold's next move

Hedging Opportunities - Strong inverse correlations let you hedge gold positions by trading the inverse asset

Regime Detection - When correlations break down, it signals a market regime change or increased uncertainty

Confirmation Signals - Multiple strong inverse correlations validate your gold trade thesis

Risk Management - Knowing what moves against gold helps you understand your portfolio's true exposure

The Science Behind the Numbers:

Real interest rates have the strongest inverse correlation to gold (approximately -0.82) because:

Gold pays no yield or dividend

When real rates rise, the opportunity cost of holding gold increases

Investors shift to interest-bearing assets when they offer positive real returns

When real rates go negative, gold becomes relatively more attractive

The US Dollar shows strong inverse correlation (approximately -0.63) because:

Gold is priced in US dollars globally

A stronger dollar makes gold more expensive for foreign buyers, reducing demand

A weaker dollar makes gold cheaper internationally, increasing demand

Both compete as reserve assets and stores of value

Why the Indicator is Weighted This Way:

Three Timeframe Approach:

Short-term (20 periods) - Captures recent correlation shifts for day trading and swing trading

Medium-term (50 periods) - The primary signal - balances noise reduction with responsiveness

Long-term (100 periods) - Confirms structural correlation trends for position trading

Correlation Thresholds:

Strong Inverse (<-0.7) - Statistically significant inverse relationship; highest confidence for inverse trades

Moderate Inverse (<-0.3) - Meaningful inverse relationship; still useful but less reliable

Weak Inverse (<0.0) - Slight inverse tendency; correlation may be breaking down

Positive (>0.0) - Assets moving together; inverse relationship has failed

How to Use This Indicator:

For Inverse Trading Strategies:

When DXY shows RED correlation (<-0.7), consider shorting DXY when gold is strong

When Real Rates show RED correlation, rising rates = falling gold (and vice versa)

When multiple assets show strong inverse correlation, confidence is highest

For Regime Detection:

All RED = Classic gold market behavior; correlations intact

Mixed colors = Transitional market; be cautious

All GREEN/GRAY = Correlation breakdown; paradigm shift occurring

For Hedging:

Use assets with strong inverse correlation to hedge gold positions

When correlation weakens, reduce hedge size

When correlation strengthens, increase hedge effectiveness

Alert System:

The indicator includes built-in alerts for:

Individual assets crossing strong inverse threshold

Multiple assets simultaneously showing strong inverse correlation (highest probability setup)

Correlation breakdowns that may signal regime changes

Color Guide:

RED - Strong inverse correlation (<-0.7) - Best inverse trading opportunity

ORANGE - Moderate inverse (<-0.3) - Useful but less reliable

YELLOW - Weak inverse (<0.0) - Correlation weakening

GRAY - Weak positive (0.0 to 0.7) - Assets moving together

GREEN - Strong positive (>0.7) - Inverse relationship broken

Recommended Settings:

Day Trading (1H-4H charts):

Short: 14 periods

Medium: 30 periods

Long: 60 periods

Swing Trading (Daily charts):

Short: 20 periods (default)

Medium: 50 periods (default)

Long: 100 periods (default)

Position Trading (Weekly charts):

Short: 10 periods

Medium: 20 periods

Long: 50 periods

Pro Tips:

Watch for divergences - when gold moves but correlations don't confirm

Correlation breakdowns often precede major trend reversals

The Medium-term (50p) correlation is plotted on the chart as your primary reference

Use the Status column for quick assessment of each asset's relationship

Set alerts for "Multiple Strong Inverse" to catch highest-probability setups

Important Notes:

This indicator is designed for Gold charts only (XAUUSD, GLD, GC1!, etc.)

Correlations are not static - they change over time based on market conditions

A correlation of -0.82 means 82% of gold's price movements can be explained by real interest rates

Always combine with other technical analysis and fundamental factors

Past correlations do not guarantee future relationships

Based on Research:

The correlation coefficients used in this indicator are based on peer-reviewed research:

Erb & Harvey (1997-2012): Real rates to gold correlation of -0.82

World Gold Council (2024): US Dollar to gold correlation of -0.63

Multiple academic studies confirming gold's inverse relationship with opportunity cost assets

Use this indicator to trade smarter, hedge better, and understand the macro forces driving gold prices.

Gold Projection DivergenceGOLD PROJECTION DIVERGENCE

Oscillator Companion for the Gold Macro Projection Model

OVERVIEW

The Gold Projection Divergence oscillator quantifies how far gold is trading from its projected fair value. While the main indicator shows where gold should be, this oscillator shows how extreme the mispricing is—providing precise timing signals for entries and exits.

HOW IT WORKS

The oscillator calculates the difference between actual gold price and the projected value, then normalizes it as a Z-score . This statistical measure shows how many standard deviations gold is trading away from its projected fair value.

Z > +2 — Gold is 2+ standard deviations above fair value (extremely overvalued)

Z > +1 — Gold is moderately overvalued

Z = 0 — Gold is trading at projected fair value

Z < -1 — Gold is moderately undervalued

Z < -2 — Gold is 2+ standard deviations below fair value (extremely undervalued)

VISUAL ELEMENTS

Histogram — Color-coded divergence magnitude

Yellow Line — Smoothed Z-score

Dashed Lines — +2 and -2 standard deviation levels

Dotted Lines — +1 and -1 standard deviation levels

Triangle Markers — Extreme crossover signals

Circle Markers — Zero-line crossings

HISTOGRAM COLORS

Dark Red — Z > +2 (extreme overvaluation)

Orange — Z between +1 and +2

Light Orange — Z between 0 and +1

Light Green — Z between -1 and 0

Green — Z between -2 and -1

Lime — Z < -2 (extreme undervaluation)

COMPONENT TABLE

The breakdown table shows divergence from each individual factor:

Silver — Is gold over/undervalued relative to silver?

M2 — Is gold over/undervalued relative to money supply?

DXY — Is gold over/undervalued relative to dollar strength?

Equity — Is gold over/undervalued relative to stocks?

TIPS — Is gold over/undervalued relative to real rates?

TRADING APPLICATIONS

Mean Reversion Strategy

Enter LONG when Z < -2 and begins rising

Enter SHORT when Z > +2 and begins falling

Use zero-line crossings for trend confirmation

Trend Following Filter

Only take long trades when Z < 0 (undervalued)

Only take short trades when Z > 0 (overvalued)

Divergence Confirmation

Bearish: Price makes new highs while Z-score makes lower highs

Bullish: Price makes new lows while Z-score makes higher lows

ALERTS

Extreme Undervaluation — Z crosses below -2

Extreme Overvaluation — Z crosses above +2

Moderate Undervaluation — Z crosses below -1

Moderate Overvaluation — Z crosses above +1

Divergence Turned Positive — Crossed above zero

Divergence Turned Negative — Crossed below zero

COMBINED USAGE

For best results, use both indicators together :

Main Indicator — Visual context of actual vs. projected on price chart

Divergence Oscillator — Precise measurement for timing decisions

The main indicator shows where gold should be; the oscillator shows how extreme the mispricing is and when to act.

Disclaimer: This indicator is for educational purposes only. Past correlations do not guarantee future relationships. Market conditions can alter historical relationships. Always use proper risk management.

Gold Macro Projection ModelGOLD MACRO PROJECTION MODEL

Multi-Factor Fair Value Estimation for Gold

OVERVIEW

The Gold Macro Projection Model estimates gold's fair value based on its historical relationships with key macroeconomic drivers. By synthesizing data from silver , M2 money supply , the US Dollar Index , TIPS (real rates proxy) , and major equity indices , this indicator projects where gold should theoretically be trading—helping traders identify potential overvaluation and undervaluation conditions.

HOW IT WORKS

This indicator employs three complementary projection methodologies :

Correlation-Weighted Z-Score Composite (50% weight)

Calculates rolling correlations between gold and each input factor. Factors with stronger correlations receive more influence. Each factor is normalized to a z-score, combined into a composite, then converted back to gold's price scale.

Silver/Gold Ratio Mean Reversion (35% weight)

The silver/gold ratio historically exhibits mean-reverting behavior. This component projects gold's implied price based on current silver prices and the historical average ratio.

M2 Money Supply Relationship (15% weight)

Gold tracks monetary expansion over long time horizons. This anchors the projection to the fundamental relationship between gold and the monetary base.

INPUT FACTORS

Silver — Strong positive correlation; precious metals move together

M2 Money Supply — Positive correlation; gold as inflation hedge

US Dollar Index (DXY) — Typically negative correlation; inverse relationship

TIPS ETF — Real interest rate proxy; gold responds to real yields

Equity Indices — Variable correlation; risk-on/risk-off dynamics

VISUAL ELEMENTS

Yellow Line — Actual gold price

Aqua Line — Projected fair value

Green Fill — Gold trading below projection (potentially undervalued)

Red Fill — Gold trading above projection (potentially overvalued)

Aqua Bands — Standard deviation envelope around projection

INFO TABLE

The indicator displays a real-time information panel showing:

Current actual vs. projected price

Divergence percentage and Z-score

Rolling correlations for each factor

Dynamic weight allocation

Buy/Sell signal based on divergence extremes

SIGNAL INTERPRETATION

STRONG BUY — Z-score below -2 (extremely undervalued)

BUY — Z-score between -2 and -1 (moderately undervalued)

NEUTRAL — Z-score between -1 and +1 (fairly valued)

SELL — Z-score between +1 and +2 (moderately overvalued)

STRONG SELL — Z-score above +2 (extremely overvalued)

SETTINGS

Correlation Period — Lookback for correlation calculations (default: 60)

Regression Period — Lookback for mean/standard deviation (default: 120)

Smoothing Period — EMA smoothing for projection line (default: 10)

Auto Weights — Toggle between correlation-based or manual weights

Band Multiplier — Standard deviation multiplier for bands (default: 1.5)

ALERTS

Gold Extremely Undervalued — Z crosses below -2

Gold Extremely Overvalued — Z crosses above +2

Gold Crossed Above Projection

Gold Crossed Below Projection

BEST PRACTICES

Use on daily timeframe for most reliable signals

Combine with the companion Gold Divergence Oscillator for timing

Disclaimer: This indicator is for educational purposes only. Past correlations do not guarantee future relationships. Always use proper risk management.

Global Macro Scanner & Relative PerformanceDescription: This indicator is an all-in-one Macro Dashboard that allows traders to track money flow across major global asset classes in real-time. It combines a floating data table with a normalized percentage-performance chart.

Features:

Macro Dashboard (Table): Displays the current value, daily % change, and status (Inflow/Outflow) for 9 key economic sectors:

US M2 Supply: Tracks monetary inflation/tightening.

DXY (US Dollar): Currency strength.

Bonds (AGG): US Aggregate Bond market.

Stocks (VT): Total World Stock Index.

Real Estate (VNQ): Vanguard Real Estate ETF.

Commodities: Oil (WTI), Gold, and Silver.

Crypto: Total Crypto Market Cap.

Relative Performance Chart (Lines): Instead of plotting raw prices (which have vastly different scales), this script plots the Percentage Return relative to a baseline.

Lookback Period: You can set a lookback (default 100 bars). The script sets the price 100 bars ago as "0%" and plots how much each asset has gained or lost since then.

Comparison: This allows you to visually see which assets are outperforming or underperforming relative to each other over the same time period.

Visual Aids:

Dynamic Labels: Each line is tagged with a label at the current candle so you can identify assets without needing a legend.

Colors: Each asset has a distinct, fixed color for consistency between the table and the chart.

How to use:

Add the script to your chart.

Adjust the "Lookback" setting in the inputs to change the starting point of the comparison (e.g., set it to the start of the year to see Year-to-Date performance).

Use the dashboard to spot daily money flow rotation (e.g., Money moving out of Stocks and into Gold).

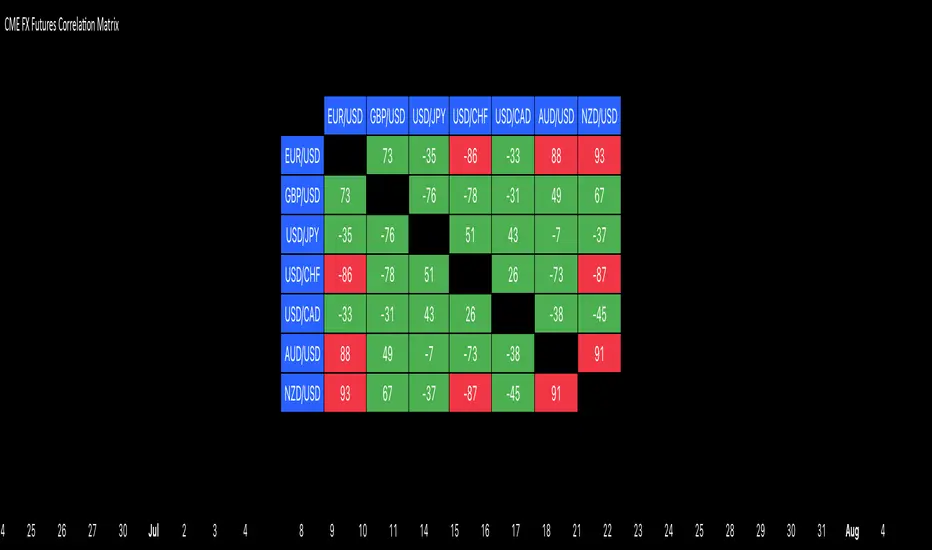

QuantLabs MASM Correlation TableThe Market is a graph. See the flows:

The QuantLabs MASM is not a standard correlation table. It is an Alpha-Grade Scanner architected to reveal the hidden "hydraulic" relationships between global macro assets in real-time.

Rebuilt from the ground up for Version 3, this engine pushes the absolute limits of the Pine Script™ runtime. It utilizes a proprietary Logarithmic Math Engine, Symmetric Compute Optimization, and a futuristic "Ghost Mode" interface to deliver a 15x15 real-time correlation matrix with zero lag.

Under the Hood: The Quant Architecture

We stripped away standard libraries to build a lean, high-performance engine designed for institutional-grade accuracy.

1. Alpha Math Engine (Logarithmic Returns) Most tools calculate correlation based on Price, which generates spurious signals (e.g., "Everything is correlated in a bull run").

The Solution: Our engine computes Logarithmic Returns (log(close/close )) by default. This measures the correlation of change (Velocity & Vector), not price levels.

The Result: A mathematically rigorous view of statistical relationships that filters out the noise of general market drift.

Dual-Core: Toggle seamlessly between "Alpha Mode" (Log Returns) for verified stats and "Visual Mode" (Price) for trend alignment.

Calculation Modes: Pearson (Standard), Euclidean (Distance), Cosine (Vector), Manhattan (Grid).

2. Symmetric Compute Optimization Calculating a 15x15 matrix requires evaluating 225 unique relationships per bar, which often crashes memory limits.

The Fix: The V3 Engine utilizes Symmetric Logic, recognizing that Correlation(A, B) == Correlation(B, A).

The Gain: By computing only the lower triangle of the matrix and mirroring pointers to the upper triangle, we reduced computational load by 50%, ensuring a lightning-fast data feed even on lower timeframes.

3. Context-Aware "Ghost Mode" The UI is designed for professional traders who need focus, not clutter.

Smart Detection: The matrix automatically detects your current chart's Ticker ID. If you are trading QQQ, the matrix will visually highlight the Nas100 row and column, making them opaque and bright while dimming the rest.

Dynamic Transparency: Irrelevant data ("Noise" < 0.3 correlation) fades into the background. Only significant "Alpha Signals" (> 0.7) glow with full Neon Saturation.

Key Features

Dominant Flow Scanner: The matrix scans all 105 unique pairs every tick and prints the #1 Strongest Correlation at the bottom of the pane (e.g., DOMINANT FLOW: Bitcoin ↔ Nas100 ).

Streak Counter: A "Stubbornness" metric that tracks how many consecutive days a strong correlation has persisted. Instantly identify if a move is a "flash event" or a "structural trend."

Neon Palette: Proprietary color mapping using Electric Blue (+1.0) for lockstep correlation and Deep Red (-1.0) for inverse hedging.

Usage Guide

Placement: Best viewed in a bottom pane (Footer).

Assets: Pre-loaded with the Essential 15 Macro Drivers (Indices, BTC, Gold, Oil, Rates, FX, Key Sectors). Fully editable via settings (Ticker|Name).

Reading the Grid:

🔵 Bright Blue: Assets moving in lockstep (Risk-On).

🔴 Bright Red: Assets moving perfectly opposite (Hedge/Risk-Off).

⚫ Faded/Black: No statistical relationship (Decoupled).

Key Improvements Made:

Formatting: Added clear bullet points and bolding to make it scannable.

Clarity: Clarified the "Logarithmic Returns" section to explain why it matters (Velocity vs. Price Levels).

Tone: Maintained the "high-tech/quant" vibe but removed slightly clunky phrases like "spurious signals" (unless you prefer that academic tone, in which case I left it in as it fits the persona).

Structure: Grouped the "Modes" under the Math Engine for better logic.

Created and designed by QuantLabs

SMT Divergence [Kodexius]SMT Divergence is a correlation-based divergence detector built around the Smart Money Technique concept: when two normally correlated instruments should be making similar swing progress, but one prints a new extreme while the other fails to confirm it. This “disagreement” can be a valuable contextual signal around liquidity runs, distribution phases, and potential reversal or continuation points.

The script compares the chart symbol (primary) with a user-selected comparison symbol (for example BTC vs ETH, ES vs NQ, EUR/USD vs GBP/USD) and automatically scans both instruments for confirmed swing highs and swing lows using pivot logic. Once swings are established, it checks for classic SMT conditions:

Primary makes a new swing extreme while the comparison symbol forms a non-confirming swing .

To support a wider range of markets, the indicator includes an Inverse Correlation option for pairs that typically move opposite to each other (for example DXY vs EUR/USD). With this enabled, the divergence rules are logically flipped so that the script still detects “non-confirmation” in a way that is consistent with the pair’s relationship.

The indicator is designed to be readable and actionable. It can draw divergence labels directly on the main chart, connect the relevant swing points with lines, show a compact information table with the last signal and settings, and optionally render the comparison symbol as a mini candle chart in the indicator pane for quick visual validation.

🔹 Features

🔸 Two-Symbol SMT Analysis (Primary vs Compare)

Select any comparison symbol to evaluate correlation structure and divergence. The script fetches the comparison OHLC data using the current chart timeframe to keep both series aligned for analysis.

🔸 Inverse Correlation Mode

For inversely correlated pairs, enable “Inverse Correlation” so the script interprets confirmation appropriately (for example, a higher low on the comparison instrument might be expected to correspond to a lower low on the primary, depending on the relationship). This helps avoid false conclusions when the pair naturally moves opposite.

🔸 Pivot-Based Swing with Adjustable Sensitivity

Swings are detected using confirmed pivots (left bars and right bars). This provides cleaner structural swing points compared with raw candle-to-candle comparisons, and it lets you control sensitivity for different market conditions and timeframes. The script also limits stored swing history to keep performance stable.

🔸 Flexible Detection Mode: Time Matched or Independent Swings

You can choose how swings are paired across instruments:

Time Matched searches for a comparison swing that occurred at the same pivot time as the primary swing.

Independent Swings compares each symbol’s own last two swings without requiring an exact time match.

🔸 Range Control and Noise Filtering

To reduce weak or irrelevant signals:

“Max Bars Between Swings” ensures the two swings being compared are close enough in structure to be meaningful.

“Min Price Diff (%)” can require a minimum percentage change between the primary’s last two swing prices to confirm the move is significant.

🔸 Clear Visual Output with Tooltips

When a divergence is detected, the script can print a label (“SMT”) with bullish or bearish styling and a tooltip that includes the symbol pair and the primary swing price for quick context.

🔸 Divergence Lines for Context

Optional lines connect the relevant swing points, making it easier to see the exact structure that triggered the signal. One line can be drawn on the main chart and another in the indicator pane for the comparison series.

🔸 Info Table (At a Glance)

A compact table can display the active symbols, correlation mode, total divergences stored, and the most recent signal type.

🔸 Alerts Included

Built-in alert conditions are provided for bullish SMT, bearish SMT, and any SMT event so you can automate notifications without editing the code.

🔸 Optional Comparison Candle Panel

If enabled, the indicator can plot the comparison symbol as candles in the indicator pane. This is useful for confirming whether the divergence is happening around major levels, consolidations, or impulsive legs on the secondary instrument.

🔹 Calculations

This section summarizes the core logic used by the script.

1. Data Synchronization (Comparison Symbol)

The comparison instrument is requested on the chart’s current timeframe so swing calculations are performed consistently:

=

request.security(compareSymbolInput, timeframe.period, )

This ensures pivots and swing times are derived from the same bar cadence as the primary chart.

2. Swing Detection via Confirmed Pivots

Swings are detected using pivot logic with user-defined left and right bars:

primaryPivotHigh = ta.pivothigh(high, pivotLeftBars, pivotRightBars)

primaryPivotLow = ta.pivotlow(low, pivotLeftBars, pivotRightBars)

Because pivots are confirmed only after the “right bars” have closed, the script stores each swing using an offset so the swing’s bar index and time reflect where the pivot actually occurred, not where it was confirmed.

3. Swing Storage and Retrieval

Both symbols maintain arrays of SwingPoint objects. Each new swing is pushed into the array, and older swings are dropped once the array exceeds the configured maximum. This makes the divergence engine predictable and prevents uncontrolled memory growth.

The script then retrieves the last and previous swing highs and lows (per symbol) to evaluate structure.

4. Matching Logic (Time Matched vs Independent)

When “Time Matched” is selected, the script searches the comparison swing array for a pivot that occurred at the exact same timestamp as the primary swing. When “Independent Swings” is selected, it simply uses the comparison symbol’s last two swings of the same type.

5. Bullish SMT Condition (LL vs HL)

A bullish SMT event is defined as:

Primary forms a lower low (last low < previous low)

Comparison forms a higher low (last low > previous low)

If inverse correlation is enabled, the comparison condition flips to maintain logical confirmation rules

The two primary swings must be within the configured bar distance window

Optional minimum percentage difference must be satisfied

A simple anti duplication rule prevents repeated triggers on the same structure

These checks are implemented directly in the bullish detection block.

6. Bearish SMT Condition (HH vs LH)

A bearish SMT event is defined as:

Primary forms a higher high (last high > previous high)

Comparison forms a lower high (last high < previous high)

Inverse correlation flips the comparison rule

Range checks, minimum difference filtering, and duplicate protection apply similarly

These checks are implemented in the bearish detection block.

7. Percentage Difference Filter

The optional “Min Price Diff (%)” filter measures the relative distance between the last two primary swing prices. This prevents very small structural changes from being treated as valid SMT signals.

priceDiffPerc = math.abs(lastSwing.price - prevSwing.price) / prevSwing.price * 100.0

The divergence condition is only allowed to trigger if this value exceeds the user defined threshold.

priceOk = priceDiffPerc >= minPriceDiff

This filter is especially useful on higher timeframes or during low volatility conditions, where micro structure noise can otherwise produce misleading signals.

8. Visualization and Output

When a divergence is confirmed, the script:

Stores the event in a divergence array (limited by “Max Divergences to Display”)

Draws a directional SMT label with a tooltip (optional)

Draws connecting lines using time based coordinates for clean alignment (optional)

It also updates an information table on the last bar only, and exposes alertconditions for automation workflows.

Pair Correlation Master [Macro]The Main Idea

Trading represents a constant battle between Systemic Flows (the whole market moving together) and Idiosyncratic Moves (one specific asset moving on its own).

This tool allows you to monitor a "basket" of 4 assets simultaneously (e.g., the major USD pairs). It answers the most important question in forex and multi-asset trading: "Is this move happening because the Dollar is weak, or because the Euro is strong?"

It separates the "Signal" (the unique move) from the "Noise" (the herd movement).

1. The Chart Lines: The "Race" (Macro Trend)

Think of the lines on your chart as a long-distance race. They visualize the performance of all 4 assets over the last 200 candles (adjustable).

- Bunched Together: If all lines are moving in the same direction, the market is highly correlated. (e.g., "The Dollar is selling off everywhere").

- Fanning Out: If the lines are spreading apart, specific currencies are outperforming others.

- The Zero Line: This is the starting line.

--- Above 0: The pair is in a macro uptrend.

--- Below 0: The pair is in a macro downtrend.

2. The Dashboard: The "Health Check" (Micro Data)

The table in the top right gives you the immediate statistics for right now.

- A. The Z-Score (The Rubber Band)

This measures how "stretched" price is compared to its normal behavior.

- White (< 2.0): Normal trading activity.

- Orange (> 2.0): The price is stretching. Warning sign.

- Red (> 3.0): Critical Stretch. The rubber band is pulled to its limit. Statistically, a pullback or pause is highly likely.

B. The Star (★)

The script automatically calculates the average behavior of your group. If one asset is behaving completely differently from the rest, it marks it with a Star (★).

- Example: EURUSD, GBPUSD, and NZDUSD are flat, but AUDUSD is rallying hard. AUDUSD gets the ★. This is where the unique opportunity lies.

🎯 Best Uses: 4H & Daily Timeframes

This indicator is tuned for "Macro" analysis. It works best on the "4-Hour" and "Daily" charts to filter out intraday noise and capture swing trading moves.

- Strategy 1: The "Rubber Band" Snap (Mean Reversion)

- Setup: Look for a Z-Score in the RED (> 3.0) on the Daily timeframe.

- Action: This indicates an unsustainable move. Look for reversals or exhaustion patterns to trade against the trend back toward the mean.

- Strategy 2: The "Lone Wolf" (Trend Following)

- Setup: Look for the asset with the Star (★).

- Action: If the whole basket is flat (Balanced), but the Star asset is breaking out, that creates a high-quality trend trade because that specific currency has its own catalyst (News/Earnings).

- Strategy 3: Systemic Flows (Basket Trading)

- Setup: The dashboard footer says "⚠️ SYSTEMIC MOVE."

- Action: This means everything is moving together (e.g., a massive USD crash). Don't look for unique setups; just join the trend on the strongest pair.

Dashboard Footer Key

The bottom of the table summarizes the current state of the market for you:

- Balanced / Rangebound: The market is quiet. Good for range trading.

- Focus: : Trade this specific pair. It is moving independently.

- Systemic Move: The whole basket is moving violently. Trade the momentum.

p.s. Suggestion - apply and use on the chart rather than an oscillator.

RCV Essentials════════════════════════════════════════════

RCV ESSENTIALS - MULTI-TIMEFRAME & SESSION ANALYSIS TOOL

════════════════════════════════════════════

📊 WHAT THIS INDICATOR DOES

This professional-grade indicator combines two powerful analysis modules:

1. TRADING SESSION TRACKER - Visualizes high/low ranges for major global market sessions (NY Open, London Open, Asian Session, etc.)

2. MULTI-TIMEFRAME CANDLE DISPLAY - Shows up to 8 higher timeframes simultaneously on your chart (15m, 30m, 1H, 4H, 1D, 1W, 1M, 3M)

════════════════════════════════════════════

🎯 KEY FEATURES

════════════════════════════════════════════

TRADING SESSIONS MODULE:

✓ Track up to 6 custom trading sessions simultaneously

✓ Real-time high/low range detection during active sessions

✓ Pre-configured for NYO (7-9am), LNO (2-3am), Asian Session (4:30pm-12am)

✓ 60+ global timezone options

✓ Customizable colors, labels, and transparency

✓ Daily divider lines (optional Sunday skip for traditional markets)

✓ Only displays on ≤30m timeframes for optimal clarity

MULTI-TIMEFRAME CANDLES MODULE:

✓ Display 1-8 higher timeframes with up to 10 candles each

✓ Real-time candle updates (non-repainting)

✓ Fully customizable colors (separate bullish/bearish for body/border/wick)

✓ Adjustable candle width, spacing, and positioning

✓ Smart label system (top/bottom/both, aligned or follow candles)

✓ Automatic timeframe validation (only shows TFs higher than chart)

✓ Memory-optimized with automatic cleanup

════════════════════════════════════════════

🔧 HOW IT WORKS

════════════════════════════════════════════

TECHNICAL IMPLEMENTATION:

Session Tracking Algorithm:

• Detects session start/end using time() function with timezone support

• Continuously monitors and updates high/low during active session

• Finalizes range when session ends using var persistence

• Draws boxes using real-time bar_index positioning

• Maintains session ranges across multiple days for reference

Multi-Timeframe System:

• Uses ta.change(time()) detection to identify new MTF candle formation

• Constructs candles using custom Type definitions (Candle, CandleSet, Config)

• Stores OHLC data in arrays with automatic size management

• Renders using box objects (bodies) and line objects (wicks)

• Updates current candle every tick; historical candles remain static

• Calculates dynamic positioning based on user settings (offset, spacing, width)

Object-Oriented Architecture:

• Custom Type "Candle" - Stores OHLC values, timestamps, visual elements

• Custom Type "CandleSet" - Manages arrays of candles + settings per timeframe

• Custom Type "Config" - Centralizes all display configuration

• Efficient memory management via unshift() for new candles, pop() for old

Performance Optimizations:

• var declarations minimize recalculation overhead

• Conditional execution (sessions only on short timeframes)

• Maximum display limits prevent excessive object creation

• Timeframe validation at barstate.isfirst reduces redundant checks

════════════════════════════════════════════

📈 HOW TO USE

════════════════════════════════════════════

SETUP:

1. Add indicator to chart (works best on 1m-30m timeframes)

2. Open Settings → "Trading Sessions" group

- Enable desired sessions (NYO, LNO, AS, or custom)

- Select your timezone from 60+ options

- Adjust colors and transparency

3. Open Settings → "Multi-TF Candles" group

- Enable timeframes (TF1-TF8)

- Configure each timeframe and display count

- Customize colors and layout

READING THE CHART:

• Session boxes show high/low ranges during active sessions

• MTF candles display to the right of current price

• Labels identify each timeframe (15m, 1H, 4H, etc.)

• Real-time updates on the most recent MTF candle

TRADING APPLICATIONS:

Session Breakout Strategy:

→ Identify session high/low (e.g., Asian session 16:30-00:00)

→ Wait for break above/below range

→ Confirm with higher timeframe candle close

→ Enter in breakout direction, stop at opposite side of range

Multi-Timeframe Confirmation:

→ Spot setup on primary chart (e.g., 5m)

→ Verify 15m, 1H, 4H candles align with trade direction

→ Only take trades where higher TFs confirm

→ Exit when higher TF candles show reversal

Combined Session + MTF:

→ Asian session establishes range overnight

→ London Open breaks Asian high

→ Confirm with bullish 15m + 1H candles

→ Enter long with stop below Asian high

════════════════════════════════════════════

🎨 ORIGINALITY & INNOVATION

════════════════════════════════════════════

What makes this indicator original:

1. INTEGRATED DUAL-MODULE DESIGN

Unlike separate session or MTF indicators, this combines both in a single performance-optimized script, enabling powerful correlation analysis between session behavior and timeframe structure.

2. ADVANCED RENDERING SYSTEM

Uses custom Pine Script v5 Types with dynamic box/line object management instead of basic plot functions. This enables:

• Precise visual control over positioning and spacing

• Real-time updates without repainting

• Efficient memory handling via automatic cleanup

• Support for 8 simultaneous timeframes with independent settings

3. INTELLIGENT SESSION TRACKING

The algorithm continuously recalculates ranges bar-by-bar during active sessions, then preserves the final range. This differs from static zone indicators that simply draw fixed boxes at predefined levels.

4. MODULAR ARCHITECTURE

Custom Type definitions (Candle, CandleSet, Config) create extensible, maintainable code structure while supporting complex multi-timeframe operations with minimal performance impact.

5. PROFESSIONAL FLEXIBILITY

Extensive customization: 6 configurable sessions, 8 timeframe slots, 60+ timezones, granular color/sizing/spacing controls, multiple label positioning modes—adaptable to any market or trading style.

6. SMART VISUAL DESIGN

Automatic timeframe validation, dynamic label alignment options, and intelligent spacing calculations ensure clarity even with multiple timeframes displayed simultaneously.

════════════════════════════════════════════

⚙️ CONFIGURATION OPTIONS

════════════════════════════════════════════

TRADING SESSIONS:

• Session 1-6: On/Off toggles

• Time Ranges: Custom start-end times

• Labels: Custom text for each session

• Colors: Individual color per session

• Timezone: 60+ options (Americas, Europe, Asia, Pacific, Africa)

• Range Transparency: 0-100%

• Outline: Optional border

• Label Display: Show/hide session names

• Daily Divider: Dotted lines at day changes

• Skip Sunday: For traditional markets vs 24/7 crypto

MULTI-TF CANDLES:

• Timeframes 1-8: Enable/disable individually

• Timeframe Selection: Any TF (seconds to months)

• Display Count: 1-10 candles per timeframe

• Bullish Colors: Body/Border/Wick (independent)

• Bearish Colors: Body/Border/Wick (independent)

• Candle Width: 1-10+ bars

• Right Margin: 0-200+ bars from edge

• TF Spacing: Gap between timeframe groups

• Label Color: Any color

• Label Size: Tiny/Small/Normal/Large/Huge

• Label Position: Top/Bottom/Both

• Label Alignment: Follow Candles or Align

════════════════════════════════════════════

📋 TECHNICAL SPECIFICATIONS

════════════════════════════════════════════

• Pine Script Version: v5

• Chart Overlay: True

• Max Boxes: 500

• Max Lines: 500

• Max Labels: 500

• Max Bars Back: 5000

• Update Frequency: Real-time (every tick)

• Timeframe Compatibility: Chart TF must be lower than selected MTFs

• Session Display: Activates only on ≤30 minute timeframes

• Memory Management: Automatic cleanup via array operations

Omega Correlation [OmegaTools]Omega Correlation (Ω CRR) is a cross-asset analytics tool designed to quantify both the strength of the relationship between two instruments and the tendency of one to move ahead of the other. It is intended for traders who work with indices, futures, FX, commodities, equities and ETFs, and who require something more robust than a simple linear correlation line.

The indicator operates in two distinct modes, selected via the “Show” parameter: Correlation and Anticipation. In Correlation mode, the script focuses on how tightly the current chart and the chosen second asset move together. In Anticipation mode, it shifts to a lead–lag perspective and estimates whether the second asset tends to behave as a leader or a follower relative to the symbol on the chart.

In both modes, the core inputs are the chart symbol and a user-selected second symbol. Internally, both assets are transformed into normalized log-returns: the script computes logarithmic returns, removes short-term mean and scales by realized volatility, then clips extreme values. This normalisation allows the tool to compare behaviour across assets with different price levels and volatility profiles.

In Correlation mode, the indicator computes a composite correlation score that typically ranges between –1 and +1. Values near +1 indicate strong and persistent positive co-movement, values near zero indicate an unstable or weak link, and values near –1 indicate a stable anti-correlation regime. The composite score is constructed from three components.

The first component is a normalized return co-movement measure. After transforming both instruments into normalized returns, the script evaluates how similar those returns are bar by bar. When the two assets consistently deliver returns of similar sign and magnitude, this component is high and positive. When they frequently diverge or move in opposite directions, it becomes negative. This captures short-term co-movement in a volatility-adjusted way.

The second component focuses on high–low swing alignment. Rather than looking only at closes, it examines the direction of changes in highs and lows for each bar. If both instruments are printing higher highs and higher lows together, or lower highs and lower lows together, the swing structure is considered aligned. Persistent alignment contributes positively to the correlation score, while repeated mismatches between the swing directions reduce it. This helps differentiate between superficial price noise and structural similarity in trend behaviour.

The third component is a classical Pearson correlation on closing prices, computed over a longer lookback. This serves as a stabilising backbone that summarises general co-movement over a broader window. By combining normalized return co-movement, swing alignment and standard price correlation with calibrated weights, the Correlation mode provides a richer view than a single linear measure, capturing both short-term dynamic interaction and longer-term structural linkage.

In Anticipation mode, Omega Correlation estimates whether the second asset tends to lead or lag the current chart. The output is again a continuous score around the range. Positive values suggest that the second asset is acting more as a leader, with its past moves bearing informative value for subsequent moves of the chart symbol. Negative values indicate that the second asset behaves more like a laggard or follower. Values near zero suggest that no stable lead–lag structure can be identified.

The anticipation score is built from four elements inspired by quantitative lead–lag and price discovery analysis. The first element is a residual lead correlation, conceptually similar to Granger-style logic. The script first measures how much of the chart symbol’s normalized returns can be explained by its own lagged values. It then removes that component and studies the correlation between the residuals and lagged returns of the second asset. If the second asset’s past returns consistently explain what the chart symbol does beyond its own autoregressive behaviour, this residual correlation becomes significantly positive.

The second element is an asymmetric lead–lag structure measure. It compares the strength of relationships in both directions across multiple lags: the correlation of the current symbol with lagged versions of the second asset (candidate leader) versus the correlation of lagged values of the current symbol with the present values of the second asset. If the forward direction (second asset leading the first) is systematically stronger than the backward direction, the structure is skewed toward genuine leadership of the second asset.

The third element is a relative price discovery score, constructed by building a dynamic hedge ratio between the two prices and defining a spread. The indicator looks at how changes in each asset contribute to correcting deviations in this spread over time. When the chart symbol tends to do most of the adjustment while the second asset remains relatively stable, it suggests that the second asset is taking a greater role in determining the equilibrium price and the chart symbol is adjusting to it. The difference in adjustment intensity between the two instruments is summarised into a single score.