Pine Script® indicator

Forecasting

Vicky IndicatorMomentum indicator used for day trading only. Focus on the line. If it crosses below midline then sell options and square off when it crosses midline on the up. Color changes added for better understanding. This is more refined than other indicators and gives better entry and exits

Pine Script® indicator

Final Scalping Strategy - RELAXED ENTRY, jangan gopoh braderEMA Scalping System (MTF) Guide (1HR direction, 15 min entry)

Objective

To capture small, consistent profits by entering trades when 15-minute momentum aligns with the 1-hour trend.

Trades are executed only during high-liquidity London and New York sessions to increase the probability of execution and success.

Strategy Setup

Chart Timeframe (Execution): 15-Minute (M15).

Trend Filter (HTF): 1-Hour (H1) chart data is used for the long-term EMA.

Long-Term Trend Filter: 50-Period EMA (based on H1 data).

Short-Term Momentum Signal: 20-Period EMA (based on M15 data).

Risk

Metric: 14-period ATR for dynamic Stop Loss calculation.

✅ Trading Rules🟢

Long (Buy) Entry Conditions

Session: Must be within the London (0800-1700 GMT) or New York (1300-2200 GMT) sessions.

HTF Trend: Current price must be above the 1-Hour EMA 50.

Momentum Signal: Price crosses above the 15-Minute EMA 20.

Confirmation: The bar immediately following the crossover must close above the 15-Minute EMA 20.

Ent

ry: A market order is executed on the close of the confirmation candle.

🔴 Short (Sell) Entry Conditions

Session: Must be within the London (0800-1700 GMT) or New York (1300-2200 GMT) sessions.

HTF Trend: Current price must be below the 1-Hour EMA 50.

Momentum Signal: Price crosses below the 15-Minute EMA 20.

Confirmation: The bar immediately following the crossover must close below the 15-Minute EMA 20.

Entry: A market order is executed on the close of the confirmation candle.

🛑 Trade Management & Exits

Stop Loss (SL): Placed dynamically at 2.0 times the 14-period ATR distance from the entry candle's low (for Buys) or high (for Sells).

Take Profit (TP): Placed dynamically to achieve a 1.5 Risk-Reward Ratio (RR) (TP distance = 1.5 x SL d

istance).

📊 On-Chart Visuals

Detailed Labels: A box appears on the entry bar showing the action, SL/TP prices, Risk/Reward in Pips, and the exact R:R ratio.

Horizontal Lines: Dashed lines display the calculated SL (Red) and TP (Green) levels while the trade is active.

Background: The chart background is shaded to highlight the active London and New York tradi

ng sessions.

Pine Script® strategy

Ichimoku_RSI_MACD_CleanIchimoku + RSI + MACD. A combination of three indicators. The important thing is that they have a BUY or SELL alert, so it makes it easy to understand the numbers.

Pine Script® indicator

Pine Script® indicator

Ichimoku_RSI_MACDIchimoku cloud + RSI + MACD. Combined indicators with signals, indicating whether it is bullish or bearish (BUY or SELL).

Pine Script® indicator

Ichimoku_RSI_MACD_CleanIchimoku + RSI + MACD indicator. It combines these three indicators. It tells whether the trend is bullish or bearish. Multi-timeframe.

Pine Script® indicator

Supertrend + EMA50 — Signal (no labels) chpolSupertrend + EMA50, best for 15 minutes, Forex, Crypto, XAUUSD.

Pine Script® indicator

Earnings Lines Vertical – All Grey This provides a vertical grey line for prior earnings dates and also for any confirmed (not estimated) future earnings date

Pine Script® indicator

3D Cube Projection - √3 Diagonal3D Cube Projection - √3 Diagonal

OVERVIEW

This indicator implements Bradley F. Cowan's cube projection methodology from his "Four Dimensional Stock Market Structures & Cycles" work. It visualizes a 3D cube projected onto the 2D price-time chart, using the √3 (square root of 3) body diagonal as the primary analytical tool for identifying market structure and potential cycle termination points.

METHODOLOGY

The cube is constructed by selecting two pivot points (A and E) which form the body diagonal - the longest diagonal running through the cube's interior from one corner to the diagonally opposite corner. According to Cowan's geometric approach:

- Point A = Starting pivot (low or high)

- Point E = Ending pivot (opposite extreme)

- Body Diagonal (A→E) = √3 × cube side length

- Face Diagonal (A→C) = √2 × cube side length

The script calculates the cube dimensions by:

1. Measuring the total price range from A to E

2. Dividing by √3 to determine the cube side length in price

3. Distributing the time component across three equal segments

4. Projecting the 3D structure onto the 2D chart plane

FEATURES

✓ Interactive date selection for points A and E

✓ Automatic UPLEG/DOWNLEG detection

✓ All 8 cube vertices labeled (A-H)

✓ All 6 cube faces with independent color/opacity controls

✓ √3 body diagonal (red line by default)

✓ √2 face diagonal (orange line by default)

✓ Customizable cube lines, fills, and labels

✓ Information table showing key measurements

VISUAL CUSTOMIZATION

- Front & Back faces: Box fills for the two square faces

- Side faces: Left and right vertical faces

- Top & Bottom faces: Horizontal connecting faces

- Each group has independent color and opacity settings

- Label size and transparency fully adjustable

- Cube line styles (solid, dashed, dotted) for depth perception

IMPORTANT LIMITATIONS & DISCLOSURES

This indicator works within the inherent constraints of projecting 3D geometry onto a 2D price-time chart:

⚠️ VISUAL APPROXIMATION: This is a visual projection tool, not a mathematically perfect 3D cube. True 3D geometry cannot be accurately represented on a 2D plane without distortion.

⚠️ TIME DISTRIBUTION: The script divides the time axis into three equal segments (total bars ÷ 3) for practical visualization. This is an approximation that prioritizes visual coherence over strict geometric accuracy.

⚠️ UNIT SCALING: Price and time use different units (dollars vs. bars), making true isometric projection impossible. The cube appears proportional on screen but the dimensions are not directly comparable.

⚠️ 2D CONSTRAINT: We only have X (time) and Y (price) axes available. The Z-axis (depth) is simulated through visual projection techniques (line styles, shading).

INTENDED USE

This tool is designed for traders and analysts who study Bradley Cowan's geometric market analysis methods. It helps visualize:

- Market structure in geometric terms

- Potential support/resistance zones at cube edges

- Cycle timing relationships using √2 and √3 ratios

- Harmonic price-time relationships

The cube projection should be used as one component of a comprehensive analysis approach, combined with other technical tools and fundamental analysis.

MATHEMATICAL FOUNDATION

While the visual representation involves approximations, the core √3 relationship is mathematically sound:

- For any cube, the body diagonal = √3 × side length

- The face diagonal = √2 × side length

- These ratios are preserved in the price dimension calculations

HOW TO USE

1. Select your starting date (Point A) - typically a significant low or high

2. Select your ending date (Point E) - the opposite extreme pivot

3. The indicator automatically constructs the cube geometry

4. Analyze the cube edges, diagonals, and faces for market structure insights

5. Adjust colors and opacity to suit your chart aesthetic

TECHNICAL NOTES

- Works on all timeframes and instruments

- Best viewed on charts with sufficient historical data

- Cube updates in real-time as new bars form

- Range selection is marked with vertical lines and shading

- Calculator table shows Point A, Point E, side length, and bar measurements

ACKNOWLEDGMENT

This indicator is based on the geometric market analysis principles developed by Bradley F. Cowan. Users are encouraged to study Cowan's original works for deeper understanding of the theoretical framework.

DISCLAIMER

This indicator is for educational and analytical purposes only. It does not constitute financial advice. Past performance does not guarantee future results. Always conduct your own research and risk management before making trading decisions.

Pine Script® indicator

Pine Script® indicator

EPS Estimate Profile [SS]This is the EPS Estimate Profile indicator.

What it does

This indicator

Collects all EPS estimates over the course of a lookback and BINS them (sorts them into 10 equal sized categories).

Analyzes the returns from earnings releases based on the EPS estimate and the reaction.

Calculates the number of bullish vs bearish responses that transpired based on the EPS estimate profile.

Calculates the expected Open to High and Open to Low ATR based on the EPS estimate using regression.

Toggle to actual EPS release to compare once earnings results are released.

How to Use it

This indicator can be used to gain insight into whether an earnings release will be received bullishly or bearishly based on the company's EPS estimate.

The indicator allows you to see all historic estimates and how the market generally responded to those estimates, as well as a breakdown of how many times estimates in those ranges produced a bullish response or a bearish response to earnings.

Examples

Let's look at some examples:

Here is MSFT. MSFT's last EPS estimate was 3.672.

If we consult the table, we can see the average return associated with this estimate range is -4%.

Now let's flip to the Daily timeframe and take a look:

MSFT ended the day red and continued to sell into the coming days.

Let's look at another example:

MCDs. Last earnings estimate was 3.327, putting it at the top of the range with an average positive return of 4%.

Let's look on the daily:

We can see that the earnings had a huge, bullish effect on MCD, despite them coming in below their estimates.

If we toggle the indicator to "Actual" EPS release, to see the profile of Actual earnings releases vs response, we get this:

Since MCD under-performed, they were still at the top of the profile; but, we can see that the expected returns are more muted now, though still positive. And indeed, the reaction was still positive.

Distinguishing % Bullish/Bearish to Avg Returns

You will see the profile table displays both the average returns and the percent of bullish/bearish responses. In some cases, you will see that, despite a negative return, the profile reveals more bullish reactions than bearish.

What does this mean?

It means, despite there being more bullish responses, when bearish responses happen they tend to be more severe and profound, vs bullish responses likely are muted.

This can alert you to potential downside risk and help you manage risk accordingly should you elect to trade the earnings release.

ATR Prediction

You will notice in the bottom right corner of the screen a secondary table that lists the predicted open to high ATR and open to low ATR.

This is done using RAW EPS estimates (or raw ACTUAL estimates depending on which you select) and performing a regression to determine the expected ATR.

This is only for reference, the analysis should focus around the historic profile of return estimates and actual return values.

IMPORTANT NOTE: You MUST be on the Monthly timeframe to use this. Otherwise, you will get an error. If, on certain tickers with a huge history, such as MSFT and XOM or OXY, you get an error, you can simply reduce the lookback length to 80 and this will resolve the issue.

Conclusion

And that's the indicator!

A blend of some light math and fundamentals! A real joy honestly.

Hope you enjoy it!

Pine Script® indicator

Moving Average ProjectionDisplays 2-5 moving averages (solid lines) and projects their future trajectory (dashed lines) based on current trend momentum. This helps you anticipate where key MAs are heading and identify potential future support/resistance levels.

Important: Projections show where MAs would move IF the current trend continues—they're not predictions. Market conditions change, so use projections as planning tools, not trading signals.

General Settings

Number of MAs (2-5) controls how many moving averages display on your chart. Start with 2-3 to avoid clutter. Projection Bars (1-100) determines how far into the future to project—use 10-20 for intraday charts and 20-40 for daily charts. Lookback for Slope (2-100) sets the number of bars used to calculate trend slope, where shorter lookbacks are more responsive and longer ones are smoother. The default of 20 works well for most situations.

Individual MA Settings (MA 1-5)

Each MA has four settings: Length sets the period for the MA (common values are 9, 20, 50, 100, and 200), Type lets you choose between SMA, EMA, WMA, HMA, VWMA, or RMA (EMA is most popular), Color sets the historical MA line color, and Projection Color sets the projected line color (usually a lighter or transparent version of the main color).

MA Types Quick Reference: EMA is most popular and responsive to recent prices. SMA gives equal weight to all periods and is the smoothest. HMA is very responsive with low lag. VWMA incorporates volume data.

Quick Setup Examples

Day Trading: 3 MAs (9/21/50 EMA), 10-15 projection bars, 10-15 lookback

Swing Trading: 2 MAs (50/200 EMA), 20-30 projection bars, 20 lookback

Scalping: 2 MAs (9/20 EMA), 5-10 projection bars, 5-10 lookback

How to Use

Trend Identification: An uptrend shows price above rising MAs with projections pointing up. A downtrend shows price below falling MAs with projections pointing down. Consolidation appears as flat MAs with horizontal projections.

Support & Resistance: Rising MA projections act as future dynamic support levels, while falling MA projections act as future dynamic resistance levels.

Anticipating Changes: Watch for projected MA crossovers before they happen. When projections converge, expect volatility or consolidation. Steep projections suggest unsustainable trends, so be cautious. Flat projections indicate ranging markets.

Trade Planning: Check the current trend using MA alignment, then look at projections to gauge trend continuation likelihood. Use projected MA levels for potential targets or stop placement.

Important Tips

When Projections Work Best: Projections are most reliable in stable trending markets with consistent momentum, low volatility environments, and away from major news events.

When to Be Cautious: Use caution during high volatility or choppy price action, around major economic releases, when projections show extreme or parabolic angles, and during trend transitions.

Combine With Other Analysis: Don't trade projections alone. Use them alongside price action, volume, support and resistance levels, and other indicators for confirmation.

Best Practices

Start with 2-3 MAs to avoid chart clutter. Match your projection and lookback bars to your trading timeframe. Use consistent color schemes for quick interpretation. Adjust settings as market conditions change. Always use proper risk management—projections are planning tools, not guarantees.

Troubleshooting

Projections not showing: Check that Projection Bars > 0 and you're viewing the most recent bar

Chart too cluttered: Reduce number of MAs or increase projection color transparency

Projections too volatile: Increase lookback bars or switch to EMA/SMA from HMA

Can't see certain MAs: Verify "Number of MAs" setting includes them (MA 3 won't show if set to 2)

Pine Script® indicator

Level LinesThis indicator displays levels in close proximity to the current price, enabling users to identify psychological levels on charts that serve as support/resistance zones or key reference points for price action.

In the settings, you can customize the number of lines shown above and below the current price, along with the interval size for rendering them.

As the price moves higher or lower, the lines dynamically adjust to reflect the most relevant levels.

In settings you can fully customize the style of lines (color, width, style) with separate settings available for lines above & below the current price.

Pine Script® indicator

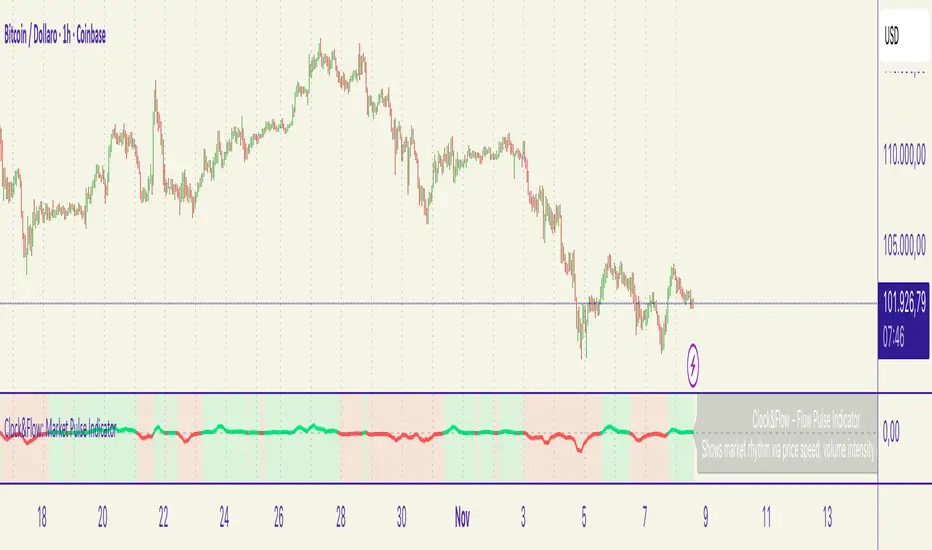

Clock&Flow – Market Pulse IndicatorClock&Flow – Market Pulse Indicator

1) General Purpose

The Market Pulse Indicator is designed to visualize the strength and direction of market flow in a clear, intuitive way.

Unlike common volume or momentum indicators, it blends three essential dimensions — price velocity, normalized volume, and volatility (ATR) — to highlight when market pressure is truly meaningful.

It helps identify genuine liquidity inflows/outflows, potential exhaustion zones, and moments of compression or expansion within the price structure.

2) Data Sources

All data is directly taken from the current chart’s feed on TradingView:

Price (close): to measure relative price change.

Volume: to detect the intensity of market participation (normalized to average).

ATR (Average True Range): to evaluate volatility relative to price levels.

No external data or off-platform sources are used.

3) Logic and Calculation Steps

Price Velocity: calculates the percentage change between the current close and the close N bars ago.

priceChange = (close - close ) / close

Normalized Volume: compares current volume to its moving average over the same period.

volNorm = volume / sma(volume, length)

Normalized Volatility: ATR divided by price to adjust for instrument scale.

atrNorm = atr(length) / close

Combination : multiplies the three components into one raw value that represents market pulse intensity.

rawPulse = priceChange * volNorm * (1 + atrNorm)

Smoothing: a moving average (smoothLen) is applied to create a cleaner and more readable oscillator line.

flowPulse = sma(rawPulse * multiplier, smoothLen)

4) Parameters (Default Settings)

length (20): analysis period for price change, volume, and ATR.

smoothLen (5): smoothing factor; higher values reduce noise.

multiplier (100): scales the output for readability; adjust to fit chart scale.

5) How to Read the Indicator

Market Pulse > 0 (green): net inflow of liquidity; buying pressure dominates.

Market Pulse < 0 (red): net outflow of liquidity; selling pressure dominates.

Near 0: neutral phase; market balance or consolidation.

Sudden peaks: strong bursts of flow — often coincide with news releases or session overlaps.

Confirmations: use as a second-level filter before entering trades or to confirm momentum behind a breakout.

6) Divergences

Divergences between price and Market Pulse are key signals of weakening flow strength:

Bullish divergence: price forms lower lows while Market Pulse forms higher lows → selling pressure is fading; potential reversal or bounce.

Bearish divergence: price forms higher highs while Market Pulse fails to confirm → buying momentum is losing strength; potential correction ahead.

For reliability, look for divergences on higher timeframes (H4, Daily).

On lower timeframes, treat them as early warnings.

7) Typical Use Cases

Breakout confirmation: price breaks resistance with a rising Market Pulse → confirms genuine participation.

False signal filter: price breaks a level but Market Pulse remains flat/negative → likely fake breakout.

Pullback entry: after a breakout, wait for a short retracement and a new positive pulse → safer entry point.

Exit signal: if you’re long and Market Pulse suddenly turns negative with strong volume → consider partial exit or tighter stops.

8) Recommended Timeframes

Intraday / Scalping: 5–30 min charts with length 10–14, smoothLen 3–5.

Swing trading: 1h–4h charts with length 20–50.

Position trading: Daily charts with larger length (50–100) for smoother data.

Always optimize parameters to the specific asset — there are no universal settings.

9) Limitations

This indicator is not a trading system — it’s a decision-support tool.

Results depend on the quality of the volume data available for the symbol.

Performance and sensitivity are influenced by length, smoothing, and multiplier values — always test before live trading.

Use alongside sound risk and money management.

10) Disclaimer

This script is provided for educational purposes only and does not constitute financial advice.

Trading and investing involve significant risk, including the potential loss of capital.

Always test indicators in simulation environments and make independent decisions based on your own analysis and risk tolerance.

Italiano

1) Scopo generale

Flow Pulse è un oscillatore pensato per visualizzare la forza e la direzione del flusso di mercato in modo immediato. Non è un semplice indicatore di volume né una copia di RSI/MACD: combina tre dimensioni fondamentali — variazione di prezzo, volume normalizzato e volatilità — per mettere in evidenza i momenti in cui la pressione dei partecipanti è realmente significativa.

È ideale per identificare: entrate guidate da flussi reali, potenziali esaurimenti, momenti di compressione/espansione del movimento e segnali di conferma per breakout o rimbalzi.

2) Dati utilizzati

L’indicatore usa esclusivamente dati disponibili sulla piattaforma TradingView del grafico corrente:

price (close) — per calcolare la variazione percentuale del prezzo;

volume per misurare l’intensità degli scambi (normalizzato su media);

ATR (Average True Range) — per normalizzare la volatilità rispetto al prezzo;

Tutti i feed (prezzo e volume) sono quelli forniti dall’exchange/fornitore dati collegato al simbolo sul grafico.

3) Logica e passaggi di calcolo

Velocità del prezzo: calcolo della variazione percentuale tra la chiusura corrente e la chiusura N barre fa:

priceChange = (close - close ) / close

— misura la direzione e magnitudine del movimento in termine relativo.

Volume normalizzato: rapporto tra il volume corrente e la media mobile semplice del volume su length barre:

volNorm = volume / sma(volume, length)

— evidenzia volumi anomali rispetto alla media.

Volatilità normalizzata (ATR): rapporto ATR/close per rendere la volatilità comparabile across price levels:

atrNorm = atr(length) / close

Combinazione: il prodotto di questi fattori (con un piccolo offset su ATR) genera un valore grezzo:

rawPulse = priceChange * volNorm * (1 + atrNorm)

— se priceChange e volNorm sono positivi e l’ATR è presente, il rawPulse sarà significativamente positivo.

Smoothing: media mobile semplice (SMA) applicata al rawPulse e moltiplicazione per un fattore scalare (multiplier) per portare il range su livelli leggibili:

flowPulse = sma(rawPulse * multiplier, smoothLen)

4) Parametri esposti (default consigliati)

length (periodo analisi) — default 20: influenza calcolo Δ% e media volumi; allunga la finestra storica.

smoothLen (smussamento) — default 5: smoothing del segnale per ridurre rumore.

multiplier — default 100: fattore di scala per rendere l’oscillatore più leggibile.

5) Interpretazione pratica dei valori

FlowPulse > 0 (verde): predominanza di flusso d’ingresso — pressione d’acquisto. Maggiore il valore, più forte la convinzione (volume + movimento + volatilità).

FlowPulse < 0 (rosso): predominanza di flusso in uscita — pressione di vendita.

Vicino a 0: assenza di flussi netti chiari; mercato piatto o bilanciato.

Picchi repentini: indicano accelerate di flusso — spesso coincidono con rotture, open/close session, news.

Sostegno al trade: usa FlowPulse come conferma prima di entrare su breakout o come avviso di attenzione su esaurimenti.

6) Divergenze (come leggerle)

Le divergenze tra prezzo e FlowPulse sono segnali importanti:

Divergenza rialzista (bullish divergence): prezzo fa nuovi minimi mentre FlowPulse non fa nuovi minimi (o forma minimo relativo più alto) → indica che la spinta di vendita non è supportata da volume/volatilità, possibile inversione/rimbalzo.

Divergenza ribassista (bearish divergence): prezzo fa nuovi massimi mentre FlowPulse non li conferma (o forma massimo relativo più basso) → la spinta d’acquisto è “debole”, possibile esaurimento e inversione.

Note pratiche: cercare divergenze su timeframe maggiori (H4, D) per maggiore attendibilità; sui timeframe minori prendere solo come early warning.

7) Esempi d’uso operativo

Conferma breakout: prezzo rompe resistenza + FlowPulse positivo e crescente → breakout più probabile e con volumi reali.

Filtro per falsi segnali: prezzo rompe ma FlowPulse è piatto/negativo → alto rischio di false breakout.

Entrata per pullback: dopo breakout, attendere un pullback con FlowPulse che torna positivo → ingresso più prudente.

Gestione delle uscite: se sei long e FlowPulse improvvisamente si inverte in negativo su volumi elevati → considerare riduzione posizione o stop.

8) Timeframe consigliati

Intraday / Scalping: M5–M30 con length ridotto (es. 10–14) e smoothLen piccolo.

Swing trading: H1–H4 con length 20–50.

Position trading: D1 con length maggiore per filtrare rumore.

Testa i parametri sul tuo asset e timeframe; nessun parametro è universale.

9) Limitazioni e avvertenze

L’indicatore non è un sistema di trading completo: è un tool di informazione e timing.

Dipende dalla qualità dei dati di volume del simbolo: su alcuni titoli/mercati (es. alcuni ETF, Forex su certi broker) il volume può essere parziale o non rappresentativo.

I valori di margine/multiplier e smoothing influenzano sensibilmente sensibilità e falsi segnali: backtest e ottimizzazione sono raccomandati.

Non usare il solo FlowPulse per entrare su leva elevata senza gestione del rischio12) Disclaimer da inserire

Disclaimer: Questo indicatore è fornito solo a scopo didattico e non costituisce consulenza finanziaria. L’uso comporta rischi: valuta sempre la gestione del rischio e testa su conto demo prima dell’applicazione in reale.

Pine Script® indicator

Indicator Overview主力籌碼預判買賣力道 (JUMBO)Pro+ 2.0主力預判買賣力道 Pro+ 是一個先進的多維度交易分析系統,專為台灣股市投資者設計。本指標整合了趨勢、成交量、動量、價格位置和波動率五大維度,通過加權評分系統生成綜合的「Power指標」,精準預判主力資金動向。

🔧 核心技術架構

1. 多維度評分系統

趨勢維度 (30%):雙EMA系統 + MACD + ADX趨勢強度

成交量維度 (25%):OBV能量潮 + 成交量比率分析

動量維度 (20%):RSI + MFI資金流量指標

價格位置維度 (20%):VWAP + 布林通道位置分析

波動率維度 (5%):ATR波動率調整

2. 多重確認機制

趨勢確認:EMA金叉/死叉 + 超級趨勢方向

成交量確認:成交量脈衝檢測 + OBV趨勢確認

動量確認:RSI超買超賣 + MFI資金流向

位置確認:布林通道位置 + VWAP相對位置

📊 主要功能特色

訊號系統

主力佈局訊號 🟥

趨勢多頭確認 + Power > 35

成交量放大 + 動量指標多頭

RSI未超買 + 價格突破基準

主力出貨訊號 🟩

趨勢空頭確認 + Power < -35

成交量異常 + 動量指標空頭

RSI未超賣 + 價格跌破基準

Power交叉訊號 🟠🔵

黃金交叉:Power線向上穿越Power MA線

死亡交叉:Power線向下穿越Power MA線

視覺化系統

台灣股市顏色標準:紅色上漲/多頭,綠色下跌/空頭

多層級K線著色:強力訊號→普通訊號→偏多偏空→盤整

智能資訊面板:實時顯示8大關鍵指標狀態

⚙️ 參數設定說明

主要參數

EMA週期:13/55(短期/長期)

Power閾值:35(靈敏度調整)

成交量濾波:1.2倍(異常成交量檢測)

超級趨勢:10週期/3倍數(趨勢過濾)

進階參數

布林通道:20週期/2倍標準差

波動率設定:14週期ATR

動量指標:14週期RSI/MFI

🎯 交易應用策略

進場時機

強力買入:🔥標記 + Power黃金交叉

常規買入:紅色向上箭頭 + Power > 35

確認買入:多重條件同時滿足

出場時機

強力賣出:💧標記 + Power死亡交叉

常規賣出:綠色向下箭頭 + Power < -35

風險控制:趨勢反轉 + 動量減弱

風險管理

止損設定:ATR波動率參考

倉位控制:Power數值強度分級

訊號過濾:ADX趨勢強度確認

📈 指標優勢

高準確率:多重條件過濾,減少假訊號

及時性:領先指標預判主力動向

完整性:涵蓋技術分析主要維度

用戶友好:直觀的視覺化設計

自定義:參數可調適應不同交易風格

🎯 Indicator Overview

Main Force Prediction Buying/Selling Strength Pro+ is an advanced multi-dimensional trading analysis system specifically designed for Taiwan stock market investors. This indicator integrates five key dimensions: trend, volume, momentum, price position, and volatility, generating a comprehensive "Power Indicator" through a weighted scoring system to accurately predict institutional fund movements.

🔧 Core Technical Architecture

1. Multi-Dimensional Scoring System

Trend Dimension (30%): Dual EMA system + MACD + ADX trend strength

Volume Dimension (25%): OBV accumulation + Volume ratio analysis

Momentum Dimension (20%): RSI + MFI money flow index

Price Position Dimension (20%): VWAP + Bollinger Bands position analysis

Volatility Dimension (5%): ATR volatility adjustment

2. Multi-Confirmation Mechanism

Trend Confirmation: EMA golden/death cross + SuperTrend direction

Volume Confirmation: Volume spike detection + OBV trend confirmation

Momentum Confirmation: RSI overbought/oversold + MFI money flow

Position Confirmation: Bollinger Bands position + VWAP relative position

📊 Key Features

Signal System

Institutional Accumulation Signals 🟥

Bullish trend confirmation + Power > 35

Volume expansion + Momentum indicators bullish

RSI not overbought + Price breakthrough baseline

Institutional Distribution Signals 🟩

Bearish trend confirmation + Power < -35

Abnormal volume + Momentum indicators bearish

RSI not oversold + Price breakdown below baseline

Power Cross Signals 🟠🔵

Golden Cross: Power line crosses above Power MA line

Death Cross: Power line crosses below Power MA line

Visualization System

Taiwan Market Color Standard: Red for uptrend/bullish, Green for downtrend/bearish

Multi-level Candlestick Coloring: Strong signals → Regular signals → Bias signals → Consolidation

Smart Info Panel: Real-time display of 8 key indicator statuses

⚙️ Parameter Settings

Main Parameters

EMA Periods: 13/55 (Short-term/Long-term)

Power Threshold: 35 (Sensitivity adjustment)

Volume Filter: 1.2x (Abnormal volume detection)

SuperTrend: 10 period/3 multiplier (Trend filtering)

Advanced Parameters

Bollinger Bands: 20 period/2 standard deviations

Volatility Settings: 14 period ATR

Momentum Indicators: 14 period RSI/MFI

🎯 Trading Application Strategies

Entry Timing

Strong Buy: 🔥 Mark + Power Golden Cross

Regular Buy: Red upward arrow + Power > 35

Confirmed Buy: Multiple conditions simultaneously met

Exit Timing

Strong Sell: 💧 Mark + Power Death Cross

Regular Sell: Green downward arrow + Power < -35

Risk Control: Trend reversal + Momentum weakening

Risk Management

Stop Loss Setting: ATR volatility reference

Position Sizing: Power value strength grading

Signal Filtering: ADX trend strength confirmation

📈 Indicator Advantages

High Accuracy: Multiple condition filtering reduces false signals

Timeliness: Leading indicators predict institutional movements

Completeness: Covers main dimensions of technical analysis

User-Friendly: Intuitive visualization design

Customizable: Adjustable parameters adapt to different trading styles

🔍 Professional Usage Tips

Trend Confirmation: Use in conjunction with major trend direction

Volume Validation: Ensure volume confirms price movements

Risk Management: Always use appropriate position sizing

Timeframe Analysis: Apply across multiple timeframes for confirmation

Market Context: Consider overall market conditions and sector rotation

版本: Pro+ 2.0

適用市場: 台股、亞股、全球股市

最佳時間框架: 日線、4小時線、1小時線

開發者: JUMBO Trading System

更新日期: 2025版本

Pine Script® indicator

Paste Horizontal LinesThis script automictically will draw horizontal line for previous key Price Action levels. I created this script to facilitate line drawing process. I receive key price targets from a trading service for a few stocks every morning. I needed a fast way to lay them out. I copy and past and BAM! Unique situation I know, so you may or may have a need. So if you do it works perfectly. If you want changes let me know.

Pine Script® indicator

Pearson SL/TP📘 Description

Pearson SL/TP — Advanced Correlation-Based Strategy with Full Risk Management

The Pearson SL/TP indicator is an advanced market analysis tool that combines Pearson correlation, volatility-based stop/target levels, and dynamic signal strength evaluation.

It is designed for traders who want to visualize potential momentum shifts and risk/reward zones in a single, integrated chart.

🔍 Core Concept

This script measures the **Pearson correlation coefficient between recent price movements and time progression, highlighting potential trend exhaustion or momentum reversals when the correlation reaches extreme values.

* High positive correlation (near +1) → price moving steadily upward → possible overbought condition.

* High negative correlation (near -1) → price moving steadily downward → possible oversold condition.

When these extremes are reached, and confirmed by several internal filters, the script generates LONG or SHORT signals with fully calculated Stop Loss and Take Profit levels.

⚙️ Main Features

📈 Signal Generation

* Uses Pearson correlation as a primary indicator of trend intensity.

* Detects potential reversal zones when correlation crosses user-defined thresholds.

* Optional divergence confirmation enhances signal reliability.

💰 Risk Management

* Stop Loss (SL) and Take Profits (TP1 & TP2) automatically adapt to volatility using the ATR (Average True Range).

* Dynamic risk/reward ratios help assess trade quality.

* Adjustable multipliers let you fine-tune your risk parameters.

🧠 Signal Strength Analysis

Each signal is graded from Weak to Very Strong based on four factors:

1. Volume activity

2. Trend alignment

3. Pearson momentum

4. Correlation change intensity

🎨 Visualization

* Overbought / Oversold background zones

* Signal arrows (LONG / SHORT)

* SL / TP** price levels and labels

* Interactive dashboard** displaying:

* Current Pearson value

* Market state (Overbought / Oversold / Neutral)

* Signal strength

* Latest trade data (Entry, SL, TP1, TP2, Risk:Reward)

🔔 Alerts

Built-in alerts for:

* Confirmed LONG / SHORT signals

* Bullish / Bearish divergences

🧩 Customization

All major parameters — including **Pearson length, thresholds, ATR multipliers, and visual options — are fully customizable.

This allows you to adapt the indicator to any market, timeframe, or trading style.

Pine Script® indicator

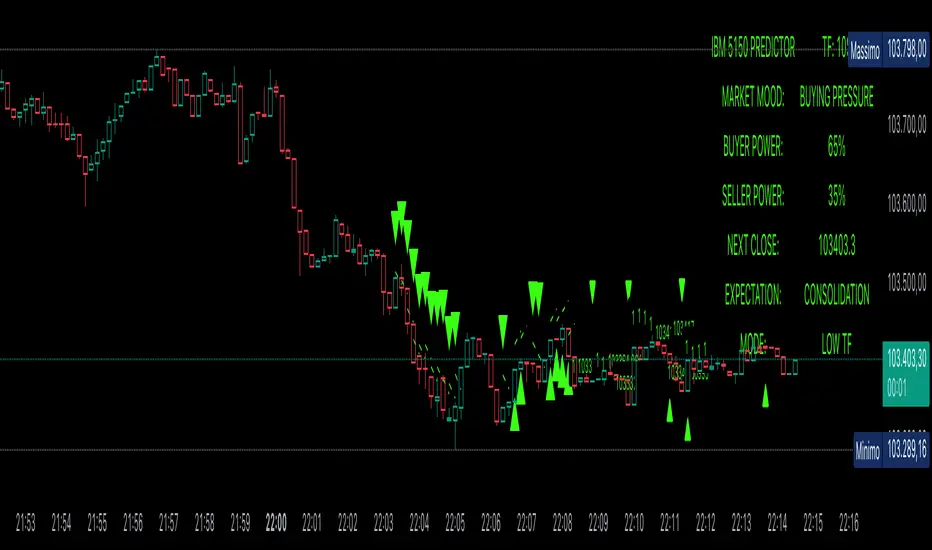

Power Balance ForecasterHey trader buddy! Remember the old IBM 5150 on Wall Street back in the 80s? :) Well, I wanted to pay tribute to it with this retro-style code when MS DOS and CRT screens were the cutting edge of technology...

Analysis of the balance of power between buyers and sellers with price predictions

What This Indicator Does

The Power Balance Forecaster indicator analyzes the relationship between buyer and seller strength to predict future price movements. Here's what it does in detail:

Main Features:

Power Balance Analysis: Calculates real-time percentage of buyer power vs seller power

Price Predictions: Estimates next closing level based on current momentum

Market State Detection: Identifies 5 different market conditions

Visual Signals: Shows directional arrows and price targets

How the Trading Logic Works

Power Balance Calculation:

Analyzes Consecutive Bars - Counts consecutive bullish and bearish bars

Calculates Momentum - Uses ATR-normalized momentum to measure trend strength

Determines Market State - Assigns one of 5 market states based on conditions

Market States:

Bull Control: Strong uptrend (75% buyer power)

Bear Control: Strong downtrend (75% seller power)

Buying Pressure: Bullish pressure (65% buyer power)

Selling Pressure: Bearish pressure (65% seller power)

Balance Area: Market in equilibrium (50/50)

Prediction System:

Bullish Condition: Buyer power > 55% + Positive momentum = Bullish prediction

Bearish Condition: Seller power > 55% + Negative momentum = Bearish prediction

Price Target: Based on ATR multiplied by timeframe factor

Configurable Parameters:

Analysis Sensitivity (5-50): Controls how responsive the indicator is

Low values (5-15): More sensitive, ideal for scalping

High values (30-50): More stable, ideal for swing trading

Table Position: Choose from 9 positions to display the data table

Trading Signals:

Green Triangle ▲: Bullish signal, price expected to increase

Green Triangle ▼: Bearish signal, price expected to decrease

Dashed Line: Shows the price target projection

Label: Displays the exact target value

Recommended Timeframes:

Lower Timeframes (1-15 minutes):

Sensitivity: 10-20

Automatic Low TF mode

Higher Timeframes (1 hour - 1 day):

Sensitivity: 25-40

Automatic High TF mode

Important Notes:

Always use this indicator in combination with:

Market context analysis

Proper risk management

Confirmation from other indicators

Mandatory stop losses

The indicator works best in trending markets and may be less effective during extreme consolidation periods.

Pine Script® indicator

Seasonality Range Marker For better Seasonality Analysation. To see Seasionality patterns in the chart.

Pine Script® indicator

Inter-symmetric Forecast (ISF)Concept:

The Inter-Symmetric Forecast (ISF) is a physics-inspired price projection tool that visualizes both trend-continuation and mean-reversion scenarios in one dynamic structure. It extends the classic ADAM Projection by introducing a regime-sensitive weighting based on the Market Reynolds Number (Reₘ), a dimensionless ratio of market momentum × liquidity to volatility-derived “viscosity.”

Mechanism:

ISF mirrors past price action around the current close (the continuation path) while also forward-pasting the same pattern unreflected (the anti-trend path). It then blends these paths bar-by-bar using time-reflected Reₘ values — meaning the liquidity-momentum regime of each past segment determines how much its future mirror leans toward continuation or reversion.

Interpretation:

High Reₘ → strong inertia/liquidity, favors trend continuation.

Low Reₘ → high friction/volatility, favors mean reversion.

The yellow blended forecast shows the regime-weighted midpoint between both outcomes.

Use:

ISF offers traders a visual probability corridor rather than a fixed prediction — illustrating how far a move might extend if momentum persists, or fade if conditions become viscous. It’s best used as a contextual forecasting overlay for discretionary or systematic analysis.

Pine Script® indicator

Hybrid Linear Regression Channel with Fibonacci LevelsHow to Use the LRC Fib Hybrid Indicator (Detailed Guide)

1. Read the Trend

2.The thick blue line is the linear regression midline.

If it’s sloping upward → uptrend (favor longs).

If sloping downward → downtrend (favor shorts).

The gray channel bounds are ±2 standard deviations (adjustable).

3. Understand Fibonacci Levels

Fib lines are projected parallel to the regression slope using the channel width as 100%:

Red dashed lines (0.0 to 0.786): Support zones in uptrends.

Blue dashed line (0.5): Midline/neutral.

Green dashed lines (1.0 to 2.618): Resistance zones in downtrends.

Strongest levels: 0.618 (support) and 1.618 (resistance).

4. Buy Signal (Long Entry)

Triggered when:

Midline is rising (uptrend confirmed).

Price crosses above a red Fib level (0.0–0.786).

Volume > 20-period average (if confirmation enabled).

Action:

Enter long on the green triangle (▲).

Stop Loss: Below the lower gray channel or recent swing low.

Take Profit: At 1.0, 1.272, or 1.618 green Fibs.

5. Sell Signal (Short Entry)

Triggered when:

Midline is falling (downtrend).

Price crosses below a green Fib level (1.272–2.618).

Volume > average.

Action:

Enter short on the red triangle (▼).

Stop Loss: Above the upper gray channel.

Take Profit: At 1.0, 0.786, or 0.618 red Fibs.

6. Use the Info Table (Bottom-Right)

Shows live prices of all Fib levels, current trend ("Up"/"Down"), and signal status ("BUY"/"SELL"/"None").

7. Customize via Settings (Gear Icon)

Regression Length: 50–200 (shorter = faster response).

Std Dev Multiplier: 1.5–3.0 (tighter/wider channel).

Toggle Fibs: Hide unused levels to declutter.

Volume Confirmation: Turn off for pure price action.

8. Set Alerts

Right-click chart → Add Alert → Select "Buy Signal" or "Sell Signal" → Enable popup/email/webhook.

9. Best Practices

Best in trending markets (avoid chop).

Wait for volume spike on bounce.

Combine with higher timeframe bias.

Use 0.618/1.618 as primary reversal zones.

This indicator gives you adaptive trend, precise entries, volume filter, and dynamic targets — all in one clean overlay.

Pine Script® indicator

Predicta Futures – Scalping Predictor with Confidence FilterPredicta Futures is an advanced short-term forecasting indicator that combines historical pattern similarity analysis with weighted technical signals to predict price movements 1–10 minutes ahead.

**Core Functionality**

The script scans up to 5,000 historical bars to identify structurally similar price patterns. It aggregates forward outcomes from matched patterns and integrates real-time signals from RSI, MACD, Bollinger Bands, volume momentum, and volatility. A composite confidence score filters signals, displaying only those meeting the user-defined threshold (default ≥68%).

**Key Outputs**

- Buy/sell triangles with text labels

- Dashed projection line to predicted price

- Dotted target and ATR-based stop lines

- Info panel showing forecast direction, confidence %, expected move %, pattern count, order book status, and data access details

**Customization & Performance**

- Execution modes: Fast, Balanced, Accurate

- Adaptive sampling with recency bias option

- Filters for volatility and market hours

- Adjustable weights, lookback period, and prediction horizon

**Use Cases**

Scalping, intraday trading, futures, cryptocurrencies, equities.

*Order book metrics are simulated (platform limitation). Technical analysis tool; not financial advice.*

Pine Script® indicator