NQ 5x Daily SessionsThis indicator automatically plots horizontal lines for the Daily Open as well as four of the most significant trading milestones of the day (CET/Berlin time). It helps you instantly identify psychological price levels and institutional opening marks directly on your chart.

Features:

Key Time Stamps: Automatic lines for the daily opening price and specific session opens at 08:00 (Frankfurt/Pre-Market), 10:00, 14:00, and 15:30 (NYSE Open).

Fully Customizable:

Control line thickness, label visibility, and the extension of current intraday lines via the settings menu.

Trading Application:

These levels often act as significant Support & Resistance during intraday trading. The 08:00 and 15:30 marks, in particular, frequently represent turning points or the start of strong trends, as trading volume spikes significantly during these windows.

NQ

ATR Levels - Current Candle Close1 of 3 scripts

I use all 3 together to "tell the story"

specifically designed for NQ to watch 4H timeframe.

code is generated by Claude AI so thats why it is free.

ATR Levels - Current Candle Open1 of 3 scripts

I use all 3 together to "tell the story"

specifically designed for NQ to watch 4H timeframe.

code is generated by Claude AI so thats why it is free.

Overnight QQQ/ NQ Auto LevelsUsing QQQ Overnight pricing to have correct levels on the NQ Future Chart.

Vib ORB Range (Free)Vib ORB Range (Free) plots the Opening Range High and Low for the session based on a user-defined start time and duration.

This tool is designed for traders who want a clean, no-noise display of the ORB zone without extra indicators or automation.

Features:

Customizable Opening Range start time

Customizable Opening Range duration

Automatically resets daily

Plots ORB High, ORB Low, and optional ORB Midline

Shaded range zone for improved clarity

Works on all timeframes and markets

How to Use:

Set the ORB start time (default 9:30 New York)

Set the ORB duration (default 15 minutes)

The indicator will draw the ORB zone once the range completes

Use the outlines or shaded zone to visually identify potential breakout areas

This free tool is intended as a simple, reliable ORB visualizer without alerts, filters, or strategy logic.

Micro/Mini P&L [LDT]Overview

Micro/Mini P&L is a risk and P&L visualization tool built primarily for futures traders.

It provides accurate dollar-based calculations for either micros or minis, regardless of which contract type you are currently charting.

The indicator automatically detects your instrument (NQ, MNQ, ES, MES, YM, RTY, CL, GC, etc.) and adjusts point-value data accordingly, allowing you to chart one contract while evaluating risk for another.

This removes the need for manual conversions and keeps your position data consistent at all times.

Although optimized for futures, the tool also works on any other asset for general trade-level visualization.

Features

• Automatic instrument detection for major futures markets including NQ/MNQ, ES/MES, YM/MYM, RTY/M2K, CL/MCL, GC/MGC and others.

Point-value logic adjusts instantly based on the detected symbol ensuring accurate calculations without manual configuration.

• Micro/Mini display toggle, allowing you to calculate dollar values for either contract type regardless of which contract is on your chart.

Useful for traders who prefer charting minis whilst trading micros or the opposite.

• Trade-level visualization, including Entry, Take Profit and Stop Loss levels with automatically drawn lines and optional TP/SL zone shading for clear and structured display on the chart.

• Dynamic P/L calculations, showing both point-based and dollar-based metrics in real time.

This includes TP/SL dollar values, points to target/stop, real-time P/L and an optional risk-reward ratio.

• Adaptive risk table, displaying contract counts from 1 up to your selected maximum, total dollar risk for each row and highlighting your chosen contract size.

This provides a straightforward method for evaluating risk, scaling and position sizing.

• Customizable display options, including color settings, label visibility, extension length, bar offsets and table positioning.

This allows the tool to remain clean, unobtrusive and easy to integrate into any chart layout.

Purpose

This tool is designed to give futures traders a clear, consistent and reliable way to view dollar-accurate risk per contract without performing manual conversions.

Whether you trade micros or minis, the displayed values always align with your selected contract type, even when charting the opposite market.

BOCS Channel Scalper Strategy - Automated Mean Reversion System# BOCS Channel Scalper Strategy - Automated Mean Reversion System

## WHAT THIS STRATEGY DOES:

This is an automated mean reversion trading strategy that identifies consolidation channels through volatility analysis and executes scalp trades when price enters entry zones near channel boundaries. Unlike breakout strategies, this system assumes price will revert to the channel mean, taking profits as price bounces back from extremes. Position sizing is fully customizable with three methods: fixed contracts, percentage of equity, or fixed dollar amount. Stop losses are placed just outside channel boundaries with take profits calculated either as fixed points or as a percentage of channel range.

## KEY DIFFERENCE FROM ORIGINAL BOCS:

**This strategy is designed for traders seeking higher trade frequency.** The original BOCS indicator trades breakouts OUTSIDE channels, waiting for price to escape consolidation before entering. This scalper version trades mean reversion INSIDE channels, entering when price reaches channel extremes and betting on a bounce back to center. The result is significantly more trading opportunities:

- **Original BOCS**: 1-3 signals per channel (only on breakout)

- **Scalper Version**: 5-15+ signals per channel (every touch of entry zones)

- **Trade Style**: Mean reversion vs trend following

- **Hold Time**: Seconds to minutes vs minutes to hours

- **Best Markets**: Ranging/choppy conditions vs trending breakouts

This makes the scalper ideal for active day traders who want continuous opportunities within consolidation zones rather than waiting for breakout confirmation. However, increased trade frequency also means higher commission costs and requires tighter risk management.

## TECHNICAL METHODOLOGY:

### Price Normalization Process:

The strategy normalizes price data to create consistent volatility measurements across different instruments and price levels. It calculates the highest high and lowest low over a user-defined lookback period (default 100 bars). Current close price is normalized using: (close - lowest_low) / (highest_high - lowest_low), producing values between 0 and 1 for standardized volatility analysis.

### Volatility Detection:

A 14-period standard deviation is applied to the normalized price series to measure price deviation from the mean. Higher standard deviation values indicate volatility expansion; lower values indicate consolidation. The strategy uses ta.highestbars() and ta.lowestbars() to identify when volatility peaks and troughs occur over the detection period (default 14 bars).

### Channel Formation Logic:

When volatility crosses from a high level to a low level (ta.crossover(upper, lower)), a consolidation phase begins. The strategy tracks the highest and lowest prices during this period, which become the channel boundaries. Minimum duration of 10+ bars is required to filter out brief volatility spikes. Channels are rendered as box objects with defined upper and lower boundaries, with colored zones indicating entry areas.

### Entry Signal Generation:

The strategy uses immediate touch-based entry logic. Entry zones are defined as a percentage from channel edges (default 20%):

- **Long Entry Zone**: Bottom 20% of channel (bottomBound + channelRange × 0.2)

- **Short Entry Zone**: Top 20% of channel (topBound - channelRange × 0.2)

Long signals trigger when candle low touches or enters the long entry zone. Short signals trigger when candle high touches or enters the short entry zone. This captures mean reversion opportunities as price reaches channel extremes.

### Cooldown Filter:

An optional cooldown period (measured in bars) prevents signal spam by enforcing minimum spacing between consecutive signals. If cooldown is set to 3 bars, no new long signal will fire until 3 bars after the previous long signal. Long and short cooldowns are tracked independently, allowing both directions to signal within the same period.

### ATR Volatility Filter:

The strategy includes a multi-timeframe ATR filter to avoid trading during low-volatility conditions. Using request.security(), it fetches ATR values from a specified timeframe (e.g., 1-minute ATR while trading on 5-minute charts). The filter compares current ATR to a user-defined minimum threshold:

- If ATR ≥ threshold: Trading enabled

- If ATR < threshold: No signals fire

This prevents entries during dead zones where mean reversion is unreliable due to insufficient price movement.

### Take Profit Calculation:

Two TP methods are available:

**Fixed Points Mode**:

- Long TP = Entry + (TP_Ticks × syminfo.mintick)

- Short TP = Entry - (TP_Ticks × syminfo.mintick)

**Channel Percentage Mode**:

- Long TP = Entry + (ChannelRange × TP_Percent)

- Short TP = Entry - (ChannelRange × TP_Percent)

Default 50% targets the channel midline, a natural mean reversion target. Larger percentages aim for opposite channel edge.

### Stop Loss Placement:

Stop losses are placed just outside the channel boundary by a user-defined tick offset:

- Long SL = ChannelBottom - (SL_Offset_Ticks × syminfo.mintick)

- Short SL = ChannelTop + (SL_Offset_Ticks × syminfo.mintick)

This logic assumes channel breaks invalidate the mean reversion thesis. If price breaks through, the range is no longer valid and position exits.

### Trade Execution Logic:

When entry conditions are met (price in zone, cooldown satisfied, ATR filter passed, no existing position):

1. Calculate entry price at zone boundary

2. Calculate TP and SL based on selected method

3. Execute strategy.entry() with calculated position size

4. Place strategy.exit() with TP limit and SL stop orders

5. Update info table with active trade details

The strategy enforces one position at a time by checking strategy.position_size == 0 before entry.

### Channel Breakout Management:

Channels are removed when price closes more than 10 ticks outside boundaries. This tolerance prevents premature channel deletion from minor breaks or wicks, allowing the mean reversion setup to persist through small boundary violations.

### Position Sizing System:

Three methods calculate position size:

**Fixed Contracts**:

- Uses exact contract quantity specified in settings

- Best for futures traders (e.g., "trade 2 NQ contracts")

**Percentage of Equity**:

- position_size = (strategy.equity × equity_pct / 100) / close

- Dynamically scales with account growth

**Cash Amount**:

- position_size = cash_amount / close

- Maintains consistent dollar exposure regardless of price

## INPUT PARAMETERS:

### Position Sizing:

- **Position Size Type**: Choose Fixed Contracts, % of Equity, or Cash Amount

- **Number of Contracts**: Fixed quantity per trade (1-1000)

- **% of Equity**: Percentage of account to allocate (1-100%)

- **Cash Amount**: Dollar value per position ($100+)

### Channel Settings:

- **Nested Channels**: Allow multiple overlapping channels vs single channel

- **Normalization Length**: Lookback for high/low calculation (1-500, default 100)

- **Box Detection Length**: Period for volatility detection (1-100, default 14)

### Scalping Settings:

- **Enable Long Scalps**: Toggle long entries on/off

- **Enable Short Scalps**: Toggle short entries on/off

- **Entry Zone % from Edge**: Size of entry zone (5-50%, default 20%)

- **SL Offset (Ticks)**: Distance beyond channel for stop (1+, default 5)

- **Cooldown Period (Bars)**: Minimum spacing between signals (0 = no cooldown)

### ATR Filter:

- **Enable ATR Filter**: Toggle volatility filter on/off

- **ATR Timeframe**: Source timeframe for ATR (1, 5, 15, 60 min, etc.)

- **ATR Length**: Smoothing period (1-100, default 14)

- **Min ATR Value**: Threshold for trade enablement (0.1+, default 10.0)

### Take Profit Settings:

- **TP Method**: Choose Fixed Points or % of Channel

- **TP Fixed (Ticks)**: Static distance in ticks (1+, default 30)

- **TP % of Channel**: Dynamic target as channel percentage (10-100%, default 50%)

### Appearance:

- **Show Entry Zones**: Toggle zone labels on channels

- **Show Info Table**: Display real-time strategy status

- **Table Position**: Corner placement (Top Left/Right, Bottom Left/Right)

- **Color Settings**: Customize long/short/TP/SL colors

## VISUAL INDICATORS:

- **Channel boxes** with semi-transparent fill showing consolidation zones

- **Colored entry zones** labeled "LONG ZONE ▲" and "SHORT ZONE ▼"

- **Entry signal arrows** below/above bars marking long/short entries

- **Active TP/SL lines** with emoji labels (⊕ Entry, 🎯 TP, 🛑 SL)

- **Info table** showing position status, channel state, last signal, entry/TP/SL prices, and ATR status

## HOW TO USE:

### For 1-3 Minute Scalping (NQ/ES):

- ATR Timeframe: "1" (1-minute)

- ATR Min Value: 10.0 (for NQ), adjust per instrument

- Entry Zone %: 20-25%

- TP Method: Fixed Points, 20-40 ticks

- SL Offset: 5-10 ticks

- Cooldown: 2-3 bars

- Position Size: 1-2 contracts

### For 5-15 Minute Day Trading:

- ATR Timeframe: "5" or match chart

- ATR Min Value: Adjust to instrument (test 8-15 for NQ)

- Entry Zone %: 20-30%

- TP Method: % of Channel, 40-60%

- SL Offset: 5-10 ticks

- Cooldown: 3-5 bars

- Position Size: Fixed contracts or 5-10% equity

### For 30-60 Minute Swing Scalping:

- ATR Timeframe: "15" or "30"

- ATR Min Value: Lower threshold for broader market

- Entry Zone %: 25-35%

- TP Method: % of Channel, 50-70%

- SL Offset: 10-15 ticks

- Cooldown: 5+ bars or disable

- Position Size: % of equity recommended

## BACKTEST CONSIDERATIONS:

- Strategy performs best in ranging, mean-reverting markets

- Strong trending markets produce more stop losses as price breaks channels

- ATR filter significantly reduces trade count but improves quality during low volatility

- Cooldown period trades signal quantity for signal quality

- Commission and slippage materially impact sub-5-minute timeframe performance

- Shorter timeframes require tighter entry zones (15-20%) to catch quick reversions

- % of Channel TP adapts better to varying channel sizes than fixed points

- Fixed contract sizing recommended for consistent risk per trade in futures

**Backtesting Parameters Used**: This strategy was developed and tested using realistic commission and slippage values to provide accurate performance expectations. Recommended settings: Commission of $1.40 per side (typical for NQ futures through discount brokers), slippage of 2 ticks to account for execution delays on fast-moving scalp entries. These values reflect real-world trading costs that active scalpers will encounter. Backtest results without proper cost simulation will significantly overstate profitability.

## COMPATIBLE MARKETS:

Works on any instrument with price data including stock indices (NQ, ES, YM, RTY), individual stocks, forex pairs (EUR/USD, GBP/USD), cryptocurrency (BTC, ETH), and commodities. Volume-based features require data feed with volume information but are optional for core functionality.

## KNOWN LIMITATIONS:

- Immediate touch entry can fire multiple times in choppy zones without adequate cooldown

- Channel deletion at 10-tick breaks may be too aggressive or lenient depending on instrument tick size

- ATR filter from lower timeframes requires higher-tier TradingView subscription (request.security limitation)

- Mean reversion logic fails in strong breakout scenarios leading to stop loss hits

- Position sizing via % of equity or cash amount calculates based on close price, may differ from actual fill price

- No partial closing capability - full position exits at TP or SL only

- Strategy does not account for gap openings or overnight holds

## RISK DISCLOSURE:

Trading involves substantial risk of loss. Past performance does not guarantee future results. This strategy is for educational purposes and backtesting only. Mean reversion strategies can experience extended drawdowns during trending markets. Stop losses may not fill at intended levels during extreme volatility or gaps. Thoroughly test on historical data and paper trade before risking real capital. Use appropriate position sizing and never risk more than you can afford to lose. Consider consulting a licensed financial advisor before making trading decisions. Automated trading systems can malfunction - monitor all live positions actively.

## ACKNOWLEDGMENT & CREDITS:

This strategy is built upon the channel detection methodology created by **AlgoAlpha** in the "Smart Money Breakout Channels" indicator. Full credit and appreciation to AlgoAlpha for pioneering the normalized volatility approach to identifying consolidation patterns. The core channel formation logic using normalized price standard deviation is AlgoAlpha's original contribution to the TradingView community.

Enhancements to the original concept include: mean reversion entry logic (vs breakout), immediate touch-based signals, multi-timeframe ATR volatility filtering, flexible position sizing (fixed/percentage/cash), cooldown period filtering, dual TP methods (fixed points vs channel percentage), automated strategy execution with exit management, and real-time position monitoring table.

NDX Ladder → Adjusted to Active Ticker (5s & 10s)This indicator allows you to a grid of NDX levels directly on the NQ! (E-mini NASDAQ 100 Futures) chart, automatically adjusting for the spread between NDX and NQ1!. This is particularly useful for traders who perform technical analysis on SPX but execute trades on NQ1!.

Features:

Renders every 5 and 10 points steps of the NDX in your current chart.

The script adjusts these levels in real-time based on the current spread between NDX and NQ / MNQ

Plots updated horizontal lines that move with the spread

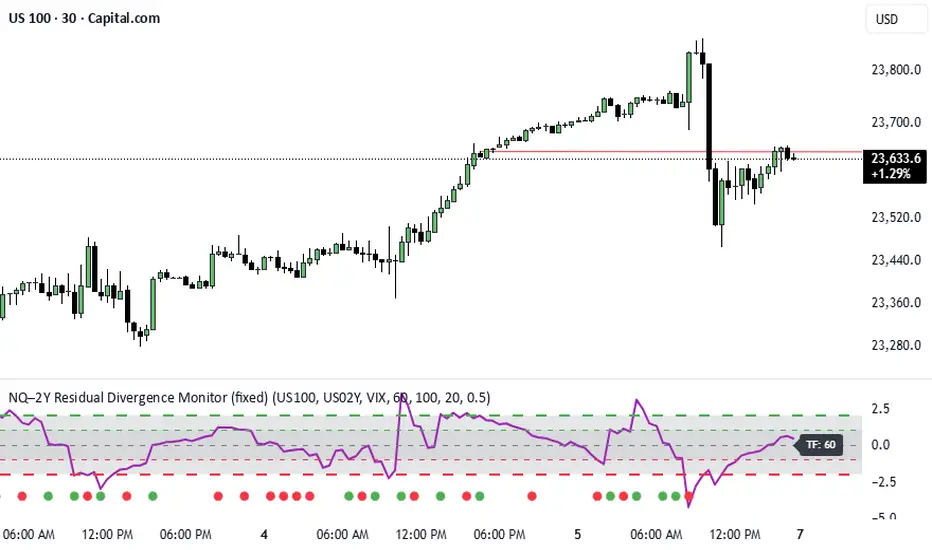

NQ–2Y CorrelationThis indicator tracks the relationship between the Nasdaq futures (NQ) and the US 2-Year Treasury yield (US02Y). The two typically move in opposite directions. This tool highlights when that relationship breaks down, and when moves become stretched to extremes. This can be useful for traders to find inflection points in price representing either overbought or oversold extremes.

Key Features

Residual Z-Score: Shows how far NQ’s returns deviate from what would be expected given moves in the 2Y. Useful for spotting stretched conditions (+/- 2σ bands).

Correlation Tracking: Fast and slow correlations between NQ and inverted 2Y returns. Helps identify regime shifts in the relationship.

Same-Direction Signals: Green dots mark when NQ and 2Y both move strongly in the same direction (rare alignment). Red dots mark strong opposing moves.

Alerts: Triggers available for residual stretches, correlation flips, and significant same-direction or opposite moves.

Usage

Monitor Z-Score to identify when the equity–rates linkage is stretched beyond typical bounds. I typically use this on the H1 or H4 timeframe.

Watch for correlation regime shifts to spot changing market dynamics. Typically price falling into support or moving into resistance as there is a false correlation or a flip.

Same-direction dots help flag unusual synchronized moves between risk assets and yields - these are especially useful for identifying false moves.

Minimalist RSI - Nasdaq (14) with Volume Filter and AlertsDescription:

This indicator shows the standard RSI (period 14) adapted for Nasdaq, with a clean and minimalist design. It adds visual levels for overbought (75) and oversold (25), plus an optional centerline 50 to better interpret momentum.

It incorporates a high volume visual filter to confirm signals and avoid false entries in low-interest conditions. Buy and sell signals are based on RSI crosses in extreme zones, optionally filtered by volume to improve reliability.

You can enable automatic alerts to receive notifications when important signals occur.

How to use:

Watch the RSI and its position relative to overbought/oversold zones and the 50 line.

Wait for high volume confirmation for greater reliability (you can disable this filter if preferred).

Use buy and sell signals alongside your price action and overall context analysis to make decisions.

Set alerts to not miss opportunities.

Important Notice:

This indicator is a support tool, not a complete strategy. Trading involves risks and no guarantees. Always use risk management and test the indicator on a demo before using it live.

Personal note:

This is my first script and I would love to receive constructive feedback to improve and offer better tools to the community. Thanks for trying it!

Motivational phrase:

“No risk, no reward.”

NQ Position Size CalculatorNQ Position Size Line Calculator is designed specifically for Nasdaq 100 futures (NQ) and micro futures (MNQ) traders who want to maintain disciplined risk management. This visual tool eliminates the guesswork from position sizing by displaying distance lines and contract calculations directly on your chart.

The indicator creates horizontal lines at 10-tick intervals from your stop loss level, showing you exactly how many contracts to trade at each distance to maintain your predetermined risk amount. Whether you're trading regular NQ contracts or micro MNQ contracts, this calculator ensures you never risk more than intended while providing instant visual feedback for optimal position sizing decisions.

How to Use the Indicator

Step 1: Configure Your Settings

Stop Loss Price: Enter your exact stop loss level (e.g., 20000.00)

Risk Amount ($): Set your maximum dollar risk per trade (e.g., $500)

Contract Type: Choose between:

NQ (Regular): $5 per tick - for larger accounts

MNQ (Micro): $0.50 per tick - for smaller accounts or conservative sizing

Display Options:

Max Lines: Number of distance lines to show (default: 30)

Show Labels: Toggle tick distance and contract count labels

Line Color: Customize the color of distance lines

Label Size: Choose tiny, small, or normal label sizes

Step 2: Read the Visual Display

Once configured, the indicator displays:

Stop Loss Line:

Thick yellow line marking your exact stop loss level

Yellow label showing the stop loss price

Distance Lines:

Dashed red lines at 10-tick intervals above and below your stop loss

Lines appear on both sides for long and short position planning

Labels (if enabled):

Green labels (right side): For long positions above your stop loss

Red labels (left side): For short positions below your stop loss

Format: "20T 5x" means 20 ticks distance, 5 contracts maximum

Step 3: Use the Information Tables

The indicator provides two helpful tables:

Position Size Table (top-right):

Shows common tick distances (10, 20, 40, 80, 160 ticks)

Displays risk per contract at each distance

Contract count for your specified risk amount

Total risk with rounded contract numbers

Settings Table (bottom-right):

Confirms your current risk amount

Shows selected contract type

Displays current settings for quick reference

Step 4: Apply to Your Trading

For Long Positions:

Look at the green labels on the right side of your chart

Find your desired entry level

Read the label to see: distance in ticks and maximum contracts

Example: "30T 8x" = 30 ticks from stop, buy 8 contracts maximum

For Short Positions:

Look at the red labels on the left side of your chart

Find your desired entry level

Read the label for tick distance and contract count

Example: "40T 6x" = 40 ticks from stop, sell 6 contracts maximum

Step 5: Trading Execution

Before Entering a Trade:

Identify your stop loss level and input it into the indicator

Choose your entry point by looking at the distance lines

Note the contract count from the corresponding label

Verify the risk amount matches your trading plan

Execute your trade with the calculated position size

Risk Management Features:

Contract rounding: All position sizes are rounded down (never up) to ensure you don't exceed your risk limit

Zero position filtering: Lines only show where position size is at least 1 contract

Dual-sided display: Plan both long and short opportunities simultaneously

Cumulative Intraday Volume with Long/Short LabelsThis indicator calculates a running total of volume for each trading day, then shows on the price chart when that total crosses levels you choose. Every day at 6:00 PM Eastern Time, the total goes back to zero so it always reflects only the current day’s activity. From that moment on, each time a new candle appears the indicator looks at whether the candle closed higher than it opened or lower. If it closed higher, the candle’s volume is added to the running total; if it closed lower, the same volume amount is subtracted. As a result, the total becomes positive when buyers have dominated so far today and negative when sellers have dominated.

Because futures markets close at 6 PM ET, the running total resets exactly then, mirroring the way most intraday traders think in terms of a single session. Throughout the day, you will see this running total move up or down according to whether more volume is happening on green or red candles. Once the total goes above a number you specify (for example, one hundred thousand contracts), the indicator will place a small “Long” label at that candle on the main price chart to let you know buying pressure has reached that level. Similarly, once the total goes below a negative number you choose (for example, minus one hundred thousand), a “Short” label will appear at that candle to signal that selling pressure has reached your chosen threshold. You can set these threshold numbers to whatever makes sense for your trading style or the market you follow.

Because raw volume alone never turns negative, this design uses candle direction as a sign. Green candles (where the close is higher than the open) add volume, and red candles (where the close is lower than the open) subtract volume. Summing those signed volume values tells you in a single number whether buying or selling has been stronger so far today. That number resets every evening, so it does not carry over any buying or selling from previous sessions.

Once you have this indicator on your chart, you simply watch the “summed volume” line as it moves throughout the day. If it climbs past your long threshold, you know buyers are firmly in control and a long entry might make sense. If it falls past your short threshold, you know sellers are firmly in control and a short entry might make sense. In quieter markets or times of low volume, you might use a smaller threshold so that even modest buying or selling pressure will trigger a label. During very active periods, a larger threshold will prevent too many signals when volume spikes frequently.

This approach is straightforward but can be surprisingly powerful. It does not rely on complex formulas or hidden statistical measures. Instead, it simply adds and subtracts daily volume based on candle color, then alerts you when that total reaches levels you care about. Over several years of historical testing, this formula has shown an ability to highlight moments when intraday sentiment shifts decisively from buyers to sellers or vice versa. Because the indicator resets every day at 6 PM, it always reflects only today’s sentiment and remains easy to interpret without carrying over past data. You can use it on any intraday timeframe, but it works especially well on five-minute or fifteen-minute charts for futures contracts.

If you want a clear gauge of whether buyers or sellers are dominating in real time, and you prefer a rule-based method rather than a complex model, this indicator gives you exactly that. It shows net buying or selling pressure at a glance, resets each session like most intraday traders do, and marks the moments when that pressure crosses the levels you decide are important. By combining a daily reset with signed volume, you get a single number that tells you precisely what the crowd is doing at any given moment, without any of the guesswork or hidden calculations that more complicated indicators often carry.

MACD & Bollinger Bands Overbought OversoldMACD & Bollinger Bands Reversal Detector

This indicator combines the power of MACD divergence analysis with Bollinger Bands to help traders identify potential reversal points in the market.

Key Features:

MACD Calculation & Divergence:

The script calculates the standard MACD components (MACD line, Signal line, and Histogram) using configurable fast, slow, and signal lengths. It includes a simplified divergence detection mechanism that flags potential bearish divergence—when the price makes a new swing high but the MACD fails to confirm the move. This divergence can serve as an early warning that the bullish momentum is waning.

Bollinger Bands:

A 20-period simple moving average (SMA) is used as the basis, with upper and lower bands drawn at 2 standard deviations. These bands help visualize overbought and oversold conditions. For example, a close at or above the upper band suggests the market may be overextended (overbought), while a close at or below the lower band may indicate oversold conditions.

Visual Alerts:

The indicator plots the Bollinger Bands on the chart along with labels marking overbought and oversold conditions. Additionally, it marks potential bearish divergence with a downward triangle, providing a quick visual cue to traders.

Usage Suggestions:

Confluence with Other Signals:

Use the divergence signals and Bollinger Band conditions as filters. For example, even if another indicator suggests a long entry, you might avoid it if the price is overbought or if MACD divergence warns of weakening momentum.

Customization:

All key parameters, such as the MACD lengths, Bollinger Band period, and multiplier, are fully configurable. This flexibility allows you to adjust the indicator to suit different markets or trading styles.

Disclaimer:

This script is provided for educational purposes only. Always perform your own analysis and backtesting before trading with live capital.

QQQ and SPY Price Levels [MW]Introduction:

Don’t let SPY and QQQ resistance levels hurt your futures trading anymore. The QQQ and SPY Price Levels indicator automagically provides easily accessible QQQ price levels for NASDAQ-related charts such as QQQ, /NQ and /MNQ futures, and leveraged ETFs such as TQQQ and SQQQ as well as for SPY price levels for S&P 500-related charts such as SPY, /ES and /MES futures, SPX, and leveraged ETFs such as UPRO and SPXU. If you’ve ever traded futures, or anything QQQ- or SPY-related and wanted to know at what price would the corresponding asset reach a key whole number level of QQQ or SPY, like 400, 440, 445, or even 447.50, this tool is for you. Key 10x, 5x, and even 2.5x multiples of QQQ and SPY can act as support or resistance for other related-assets. Until now, there hasn’t been an indicator that can serve as an easy visual cue to know exactly when that is about to happen across assets.

This indicator is a fork of the original SPY Price Levels indicator, which only considered SPY-related assets.

Settings:

QQQ/SPY 2.5x: Show closest levels above and below that are multiples of 2.5 on QQQ

QQQ/SPY 5x: Show closest levels above and below that are multiples of 5 on QQQ

QQQ/SPY 10x: Show closest levels above and below that are multiples of 10 on QQQ

Show QQQ/SPY Price Label: Show the current QQQ/SPY price

Extend lines to the left: Extend label lines for each price level to the beginning of the chart

Calculations:

This indicator defines the ratio between the price of QQQ/SPY and another NASDAQ/S&P-related asset and uses that multiplier once the user-defined price increments are defined. For example, if /MNQ is at 19000 and QQQ is at 465, then the ratio would be 40.8.

The incremental QQQ levels that are above and below the QQQ price are calculated using the following equations:

qqqLevelUp = _multiplier * math.ceil(_qqqClose / _multiplier)

qqqLevelDown = _multiplier * math.floor(_qqqClose / _multiplier)

The conversion ratio is then multiplied by that amount to get the final estimated corresponding price using the calculation:

levelUp := _conversion * qqqLevelUp

levelDown := _conversion * qqqLevelDown

For leveraged assets, the conversion must be used on the difference between the current QQQ price and the incremental upper and lower levels.

For example, the calculation for the next level up looks like the following:

levelUpDelta := math.abs(_qqqClose - qqqLevelUp)

levelUp := close + _conversion * (levelUpDelta * _leverage)

This logic is identical for SPY-related assets.

How to Use:

The QQQ and SPY Price Levels indicator aims to be as unobtrusive as possible. The default view shows 3 labels and 2 lines that are all aligned to the right of the main chart, so that it interferes as little as possible with any other indicators. It can be added to any /NQ or /MNQ futures chart, SQQQ, TQQQ, and, of course, QQQ as well as any /ES /MES futures chart, SPXU, UPRO, SPX, and of course SPY. The most immediate price levels for each multiplier appears above and below the current price along with the price of QQQ/SPY.

For example, MNQU2024 is currently at 19594. By looking at the indicator the next QQQ increment below is at 475, or 19556 on the MNQU2024 chart. This potential support is marked with a green label that shows both prices. The next increment above is at QQQ 477.50, or 19659 on the MESU2024 chart. And the QQQ price itself, is also shown (and can be removed) at 475.92.

QQQ and SPY price increments of 2.5, 5, and 10 tend to consistently act at the very least as emotional support and resistance levels. Weak, or weakening volume and/or momentum when these levels are hit can trigger a strong rejection, and can sometimes precipitate lengthy consolidation periods at those levels. Watching an NASDAQ- and S&P 500-related asset come to a halt, fall off a cliff, or react in some other unintuitive way could very well be the result of a QQQ/SPY level being reached. Even though many of us know that this relationship exists, it’s easy to forget. So, this indicator helps to ensure that its users keep that relationship front and center.

By extending the lines into the past on QQQ/SPY and their related assets, you can see what reactions happened at these key levels.

Other Usage Notes and Limitations:

The calculations used only provide an estimated relationship or a close approximation, and are not exact.

It's important for traders to be aware of the limitations of any indicator and to use them as part of a broader, well-rounded trading strategy that includes risk management, fundamental analysis, and other tools that can help with reducing false signals, determining trend direction, and providing additional confirmation for a trade decision. Diversifying strategies and not relying solely on one type of indicator or analysis can help mitigate some of these risks.

Bull Flag DetectionThe FuturesGod bull flag indicator aims to identify the occurrence of bull flags.

Bull flags are a popular trading pattern that allows users to gauge long entries into a given market. Flags consist of a pole that is followed by either a downward or sideways consolidation period.

This script can be used on any market but was intended for futures (NQ, ES) trading on the intraday timeframe.

The script does the following:

1. Identifies the occurrence of a flag pole. This is based on a lookback period and percentage threshold decided by the user.

2. Marks the consolidation area after the pole occurrence using swing highs and swing lows.

3. Visually the above is represented by a shaded green area.

4. When a pole is detected, it is marked by a downward off-white triangle. Note that if the percentage threshold is reached several times on the same upward climb, the script will continue to identify points where the threshold for pole detection is met.

5. Also visualized are the 20, 50 and 200 period exponential moving averages. The area between the 20 and 50 EMAs are shaded to provide traders a visual of a possible support area.

High/Low of week: Stats & Day of Week tendencies// Purpose:

-To show High of Week (HoW) day and Low of week (LoW) day frequencies/percentages for an asset.

-To further analyze Day of Week (DoW) tendencies based on averaged data from all various custom weeks. Giving a more reliable measure of DoW tendencies ('Meta Averages').

-To backtest day-of-week tendencies: across all asset history or across custom user input periods (i.e. consolidation vs trending periods).

-Education: to see how how data from a 'hard-defined-week' may be misleading when seeking statistical evidence of DoW tendencies.

// Notes & Tips:

-Only designed for use on DAILY timeframe.

-Verification table is to make sure HoW / LoW DAY (referencing previous finished week) is printing correctly and therefore the stats table is populating correctly.

-Generally, leaving Timezone input set to "America/New_York" is best, regardless of your asset or your chart timezone. But if misaligned by 1 day =>> tweak this timezone input to correct

-If you want to use manual backtesting period (e.g. for testing consolidation periods vs trending periods): toggle these settings on, then click the indicator display line three dots >> 'Reset Points' to quickly set start & end dates.

// On custom week start days:

-For assets like BTC which trade 7 days a week, this is quite simple. Pick custom start day, use verification table to check all is well. See the start week day & time in said verification table.

-For traditional assets like S&P which trade only 5 days a week and suffer from occasional Holidays, this is a bit more complicated. If the custom start day input is a bank holiday, its custom 'week' will be discounted from the data set. E.g.1: if you choose 'use custom start day' and set it to Monday, then bank holiday Monday weeks will be discounted from the data set. E.g.2: If you choose 'use custom start day' and set it to Thursday, then the Holiday Thursday custom week (e.g Thanksgiving Thursday >> following Weds) would be discounted from the data set.

// On 'Meta Averages':

-The idea is to try and mitigate out the 'continuation bias' that comes from having a fixed week start/end time: i.e. sometimes a market is trending through the week start/end time, so the start/end day stats are over-weighted if one is trying to tease out typical weekly profile tendencies or typical DoW tendencies. You'll notice this if you compare the stats with various custom start days ('bookend' start/end days are always more heavily weighted). I wanted to try to mitigate out this 'bias' by cycling through all the possible new week start/end days and taking an average of the results. i.e. on BTC/USD the 'meta average' for Tuesday would be the average of the Tuesday HoW frequencies from the set of all 7 possible custom weeks(Mon-Sun, Tues-Mon, Weds-Tues, etc etc).

// User Inputs:

~Week Start:

-use custom week start day (default toggled OFF); Choose custom week start day

-show Meta Averages (default toggled ON)

~Verification Table:

-show table, show new week lines, number of new week lines to show

-table formatting options (position, color, size)

-timezone (only for tweaking if printed DoW is misaligned by 1 day)

~Statistics Table:

-show table, table formatting options (position, color, size)

~Manual Backtesting:

-Use start date (default toggled OFF), choose start date, choose vline color

-Use end date (defautl toggled OFF), choose end date, choose vline color

// Demo charts:

NQ1! (Nasdaq), Full History, Traditional week (Mon>>Friday) stats. And Meta Averages. Annotations in purple:

NQ1! (Nasdaq), Full History, Custom week (custom start day = Wednesday). And Meta Averages. Annotations in purple:

QQQ NDX NQ Price Converter [Pt]A must have tool for QQQ NDX NQ traders~!!!

Description

The QQQ NDX NQ Price Converter is a powerful and easy-to-use tool that allows traders to view corresponding price levels for linked instruments in real-time. This includes QQQ, NDX, NQ, and NAS100USD. Although these instruments often move in sync, differences in price movements, volume, and trading hours can create unique key levels and support/resistance areas for each. By mapping these levels on the same chart, traders can more easily spot trading opportunities and improve their chances of success.

Customizable features

- multiplier from the closest whole number price level

- line color

- line style

- label position / size

- # of levels to display

- toggle current price display table

Convert ETF to Futures/IndexThis indicator is used to automatically map an ETF's VWAP and 10 levels above and below the strike of your choice, to the futures or index instrument currently being viewed/traded. This works very well when using both SPY to ES/MES/SPX or QQQ to NQ/MNQ/NDX to plot the ETF strikes and can lead to some incredible trades, especially when trading level to level. Since SPY, QQQ, IWM, and DIA have the same price action as their futures iteration, there seems to be a direct correlation between their levels and VWAP . This indicator is made to easily map these key levels to the appropriate futures instrument. If you have a way to measure GEX centered around a certain level, I recommend color coding the lines to help indicate whether the level will have strong positive or negative gamma hedging associated with it.

SPY to ES or QQQ to NQThis indicator is used to automatically map SPY VWAP and 10 levels of your choice to ES / MES or map QQQ VWAP and 10 levels of your choice to NQ / MNQ . Since SPY and QQQ have the same price action as their futures iteration, there seems to a direct correlation between their levels and VWAP. This indicator is made to easily map the key levels of your choice to the appropriate futures instrument.

Cowabunga System from babypips.comPlease do read the information below as well, especially if you are new to Forex.

The Cowabunga System is a type of Mechanical Trading System that filters trades based on the trend of the 4 hour chart with EMAs and some other familiar indicators (RSI, Stochastics and MACD) while entering trades base on 15 minute chart.

I have coded (quite amateurishly) the basic system onto a 15 minute chart (the 4 hour settings are coded as well). The author says the system is to be traded off the 15 minute chart with the 4 hour chart only as a reference for trend direction.

4 Hour Chart Settings

5 EMA

10 EMA

Stochastics (10,3,3)

RSI (9)

Then we move onto the 15 minute chart, where he gives us the trade entry rules.

15 Minute Chart Settings

5 EMA

10 EMA

Stochastics (10,3,3)

RSI (9)

MACD (12,26,9)

Entry Rules - long entry rules used, obviously reverse these for shorting.

1. EMA must cross above the 10 EMA.

2. RSI must be greater than 50 and not overbought.

3. Stochastic must be headed up and not be in overbought territory.

4. MACD histogram must go from negative to positive OR be negative and start to increase in value.

What I did.

1. Set the RSI and Stochastic levels to avoid entries when they indicate overbought conditions for long and oversold conditions for short (80 and 20 levels).

2. Users can input specific times they want to backtest.

3. User's can configure profit targets, trailing stops and stops. Default is set it to was 100 pips profit target with a 40 pip trailing stop. (Note, when you are changing these values, please note that each pip is worth 10, so 100 pips is entered as 1000.)

The Cowabunga System from babypips.com is another popular and active system. The author, Pip Surfer, continues to post wins and losses with this system. It shows there is a lot of honesty and integrity with this system if the author keeps up to date even 10 years later and is not afraid of sharing the times the system causes losses.

As an example of this, here is post he shared just last week . It's almost like a journal, he gives specific times and reasons why he entered, lets the readers know when he was stopped out, etc. I think that what he does is equally important as his system.

To read more about this system, visit the thread on babypips.com, click here.