Dskyz (DAFE) Aurora Divergence – Quant Master Dskyz (DAFE) Aurora Divergence – Quant Master

Introducing the Dskyz (DAFE) Aurora Divergence – Quant Master , a strategy that’s your secret weapon for mastering futures markets like MNQ, NQ, MES, and ES. Born from the legendary Aurora Divergence indicator, this fully automated system transforms raw divergence signals into a quant-grade trading machine, blending precision, risk management, and cyberpunk DAFE visuals that make your charts glow like a neon skyline. Crafted with care and driven by community passion, this strategy stands out in a sea of generic scripts, offering traders a unique edge to outsmart institutional traps and navigate volatile markets.

The Aurora Divergence indicator was a cult favorite for spotting price-OBV divergences with its aqua and fuchsia orbs, but traders craved a system to act on those signals with discipline and automation. This strategy delivers, layering advanced filters (z-score, ATR, multi-timeframe, session), dynamic risk controls (kill switches, adaptive stops/TPs), and a real-time dashboard to turn insights into profits. Whether you’re a newbie dipping into futures or a pro hunting reversals, this strat’s got your back with a beginner guide, alerts, and visuals that make trading feel like a sci-fi mission. Let’s dive into every detail and see why this original DAFE creation is a must-have.

Why Traders Need This Strategy

Futures markets are a battlefield—fast-paced, volatile, and riddled with institutional games that can wipe out undisciplined traders. From the April 28, 2025 NQ 1k-point drop to sneaky ES slippage, the stakes are high. Meanwhile, platforms are flooded with unoriginal, low-effort scripts that promise the moon but deliver noise. The Aurora Divergence – Quant Master rises above, offering:

Unmatched Originality: A bespoke system built from the ground up, with custom divergence logic, DAFE visuals, and quant filters that set it apart from copycat clutter.

Automation with Precision: Executes trades on divergence signals, eliminating emotional slip-ups and ensuring consistency, even in chaotic sessions.

Quant-Grade Filters: Z-score, ATR, multi-timeframe, and session checks filter out noise, targeting high-probability reversals.

Robust Risk Management: Daily loss and rolling drawdown kill switches, plus ATR-based stops/TPs, protect your capital like a fortress.

Stunning DAFE Visuals: Aqua/fuchsia orbs, aurora bands, and a glowing dashboard make signals intuitive and charts a work of art.

Community-Driven: Evolved from trader feedback, this strat’s a labor of love, not a recycled knockoff.

Traders need this because it’s a complete, original system that blends accessibility, sophistication, and style. It’s your edge to trade smarter, not harder, in a market full of traps and imitators.

1. Divergence Detection (Core Signal Logic)

The strategy’s core is its ability to detect bullish and bearish divergences between price and On-Balance Volume (OBV), pinpointing reversals with surgical accuracy.

How It Works:

Price Slope: Uses linear regression over a lookback (default: 9 bars) to measure price momentum (priceSlope).

OBV Slope: OBV tracks volume flow (+volume if price rises, -volume if falls), with its slope calculated similarly (obvSlope).

Bullish Divergence: Price slope negative (falling), OBV slope positive (rising), and price above 50-bar SMA (trend_ma).

Bearish Divergence: Price slope positive (rising), OBV slope negative (falling), and price below 50-bar SMA.

Smoothing: Requires two consecutive divergence bars (bullDiv2, bearDiv2) to confirm signals, reducing false positives.

Strength: Divergence intensity (divStrength = |priceSlope * obvSlope| * sensitivity) is normalized (0–1, divStrengthNorm) for visuals.

Why It’s Brilliant:

- Divergences catch hidden momentum shifts, often exploited by institutions, giving you an edge on reversals.

- The 50-bar SMA filter aligns signals with the broader trend, avoiding choppy markets.

- Adjustable lookback (min: 3) and sensitivity (default: 1.0) let you tune for different instruments or timeframes.

2. Filters for Precision

Four advanced filters ensure signals are high-probability and market-aligned, cutting through the noise of volatile futures.

Z-Score Filter:

Logic: Calculates z-score ((close - SMA) / stdev) over a lookback (default: 50 bars). Blocks entries if |z-score| > threshold (default: 1.5) unless disabled (useZFilter = false).

Impact: Avoids trades during extreme price moves (e.g., blow-off tops), keeping you in statistically safe zones.

ATR Percentile Volatility Filter:

Logic: Tracks 14-bar ATR in a 100-bar window (default). Requires current ATR > 80th percentile (percATR) to trade (tradeOk).

Impact: Ensures sufficient volatility for meaningful moves, filtering out low-volume chop.

Multi-Timeframe (HTF) Trend Filter:

Logic: Uses a 50-bar SMA on a higher timeframe (default: 60min). Longs require price > HTF MA (bullTrendOK), shorts < HTF MA (bearTrendOK).

Impact: Aligns trades with the bigger trend, reducing counter-trend losses.

US Session Filter:

Logic: Restricts trading to 9:30am–4:00pm ET (default: enabled, useSession = true) using America/New_York timezone.

Impact: Focuses on high-liquidity hours, avoiding overnight spreads and erratic moves.

Evolution:

- These filters create a robust signal pipeline, ensuring trades are timed for optimal conditions.

- Customizable inputs (e.g., zThreshold, atrPercentile) let traders adapt to their style without compromising quality.

3. Risk Management

The strategy’s risk controls are a masterclass in balancing aggression and safety, protecting capital in volatile markets.

Daily Loss Kill Switch:

Logic: Tracks daily loss (dayStartEquity - strategy.equity). Halts trading if loss ≥ $300 (default) and enabled (killSwitch = true, killSwitchActive).

Impact: Caps daily downside, crucial during events like April 27, 2025 ES slippage.

Rolling Drawdown Kill Switch:

Logic: Monitors drawdown (rollingPeak - strategy.equity) over 100 bars (default). Stops trading if > $1000 (rollingKill).

Impact: Prevents prolonged losing streaks, preserving capital for better setups.

Dynamic Stop-Loss and Take-Profit:

Logic: Stops = entry ± ATR * multiplier (default: 1.0x, stopDist). TPs = entry ± ATR * 1.5x (profitDist). Longs: stop below, TP above; shorts: vice versa.

Impact: Adapts to volatility, keeping stops tight but realistic, with TPs targeting 1.5:1 reward/risk.

Max Bars in Trade:

Logic: Closes trades after 8 bars (default) if not already exited.

Impact: Frees capital from stagnant trades, maintaining efficiency.

Kill Switch Buffer Dashboard:

Logic: Shows smallest buffer ($300 - daily loss or $1000 - rolling DD). Displays 0 (red) if kill switch active, else buffer (green).

Impact: Real-time risk visibility, letting traders adjust dynamically.

Why It’s Brilliant:

- Kill switches and ATR-based exits create a safety net, rare in generic scripts.

- Customizable risk inputs (maxDailyLoss, dynamicStopMult) suit different account sizes.

- Buffer metric empowers disciplined trading, a DAFE signature.

4. Trade Entry and Exit Logic

The entry/exit rules are precise, filtered, and adaptive, ensuring trades are deliberate and profitable.

Entry Conditions:

Long Entry: bullDiv2, cooldown passed (canSignal), ATR filter passed (tradeOk), in US session (inSession), no kill switches (not killSwitchActive, not rollingKill), z-score OK (zOk), HTF trend bullish (bullTrendOK), no existing long (lastDirection != 1, position_size <= 0). Closes shorts first.

Short Entry: Same, but for bearDiv2, bearTrendOK, no long (lastDirection != -1, position_size >= 0). Closes longs first.

Adaptive Cooldown: Default 2 bars (cooldownBars). Doubles (up to 10) after a losing trade, resets after wins (dynamicCooldown).

Exit Conditions:

Stop-Loss/Take-Profit: Set per trade (ATR-based). Exits on stop/TP hits.

Other Exits: Closes if maxBarsInTrade reached, ATR filter fails, or kill switch activates.

Position Management: Ensures no conflicting positions, closing opposites before new entries.

Built To Be Reliable and Consistent:

- Multi-filtered entries minimize false signals, a stark contrast to basic scripts.

- Adaptive cooldown prevents overtrading, especially after losses.

- Clean position handling ensures smooth execution, even in fast markets.

5. DAFE Visuals

The visuals are a DAFE hallmark, blending function with clean flair to make signals intuitive and charts stunning.

Aurora Bands:

Display: Bands around price during divergences (bullish: below low, bearish: above high), sized by ATR * bandwidth (default: 0.5).

Colors: Aqua (bullish), fuchsia (bearish), with transparency tied to divStrengthNorm.

Purpose: Highlights divergence zones with a glowing, futuristic vibe.

Divergence Orbs:

Display: Large/small circles (aqua below for bullish, fuchsia above for bearish) when bullDiv2/bearDiv2 and canSignal. Labels show strength (0–1).

Purpose: Pinpoints entries with eye-catching clarity.

Gradient Background:

Display: Green (bullish), red (bearish), or gray (neutral), 90–95% transparent.

Purpose: Sets the market mood without clutter.

Strategy Plots:

- Stop/TP Lines: Red (stops), green (TPs) for active trades.

- HTF MA: Yellow line for trend context.

- Z-Score: Blue step-line (if enabled).

- Kill Switch Warning: Red background flash when active.

What Makes This Next-Level?:

- Visuals make complex signals (divergences, filters) instantly clear, even for beginners.

- DAFE’s unique aesthetic (orbs, bands) sets it apart from generic scripts, reinforcing originality.

- Functional plots (stops, TPs) enhance trade management.

6. Metrics Dashboard

The top-right dashboard (2x8 table) is your command center, delivering real-time insights.

Metrics:

Daily Loss ($): Current loss vs. day’s start, red if > $300.

Rolling DD ($): Drawdown vs. 100-bar peak, red if > $1000.

ATR Threshold: Current percATR, green if ATR exceeds, red if not.

Z-Score: Current value, green if within threshold, red if not.

Signal: “Bullish Div” (aqua), “Bearish Div” (fuchsia), or “None” (gray).

Action: “Consider Buying”/“Consider Selling” (signal color) or “Wait” (gray).

Kill Switch Buffer ($): Smallest buffer to kill switch, green if > 0, red if 0.

Why This Is Important?:

- Consolidates critical data, making decisions effortless.

- Color-coded metrics guide beginners (e.g., green action = go).

- Buffer metric adds transparency, rare in off-the-shelf scripts.

7. Beginner Guide

Beginner Guide: Middle-right table (shown once on chart load), explains aqua orbs (bullish, buy) and fuchsia orbs (bearish, sell).

Key Features:

Futures-Optimized: Tailored for MNQ, NQ, MES, ES with point-value adjustments.

Highly Customizable: Inputs for lookback, sensitivity, filters, and risk settings.

Real-Time Insights: Dashboard and visuals update every bar.

Backtest-Ready: Fixed qty and tick calc for accurate historical testing.

User-Friendly: Guide, visuals, and dashboard make it accessible yet powerful.

Original Design: DAFE’s unique logic and visuals stand out from generic scripts.

How to Use

Add to Chart: Load on a 5min MNQ/ES chart in TradingView.

Configure Inputs: Adjust instrument, filters, or risk (defaults optimized for MNQ).

Monitor Dashboard: Watch signals, actions, and risk metrics (top-right).

Backtest: Run in strategy tester to evaluate performance.

Live Trade: Connect to a broker (e.g., Tradovate) for automation. Watch for slippage (e.g., April 27, 2025 ES issues).

Replay Test: Use bar replay (e.g., April 28, 2025 NQ drop) to test volatility handling.

Disclaimer

Trading futures involves significant risk of loss and is not suitable for all investors. Past performance is not indicative of future results. Backtest results may not reflect live trading due to slippage, fees, or market conditions. Use this strategy at your own risk, and consult a financial advisor before trading. Dskyz (DAFE) Trading Systems is not responsible for any losses incurred.

Backtesting:

Frame: 2023-09-20 - 2025-04-29

Fee Typical Range (per side, per contract)

CME Exchange $1.14 – $1.20

Clearing $0.10 – $0.30

NFA Regulatory $0.02

Firm/Broker Commis. $0.25 – $0.80 (retail prop)

TOTAL $1.60 – $2.30 per side

Round Turn: (enter+exit) = $3.20 – $4.60 per contract

Final Notes

The Dskyz (DAFE) Aurora Divergence – Quant Master isn’t just a strategy—it’s a movement. Crafted with originality and driven by community passion, it rises above the flood of generic scripts to deliver a system that’s as powerful as it is beautiful. With its quant-grade logic, DAFE visuals, and robust risk controls, it empowers traders to tackle futures with confidence and style. Join the DAFE crew, light up your charts, and let’s outsmart the markets together!

(This publishing will most likely be taken down do to some miscellaneous rule about properly displaying charting symbols, or whatever. Once I've identified what part of the publishing they want to pick on, I'll adjust and repost.)

Use it with discipline. Use it with clarity. Trade smarter.

**I will continue to release incredible strategies and indicators until I turn this into a brand or until someone offers me a contract.

Created by Dskyz, powered by DAFE Trading Systems. Trade fast, trade bold.

Search in scripts for "Futures"

Adaptivity: Measures of Dominant Cycles and Price Trend [Loxx]Adaptivity: Measures of Dominant Cycles and Price Trend is an indicator that outputs adaptive lengths using various methods for dominant cycle and price trend timeframe adaptivity. While the information output from this indicator might be useful for the average trader in one off circumstances, this indicator is really meant for those need a quick comparison of dynamic length outputs who wish to fine turn algorithms and/or create adaptive indicators.

This indicator compares adaptive output lengths of all publicly known adaptive measures. Additional adaptive measures will be added as they are discovered and made public.

The first released of this indicator includes 6 measures. An additional three measures will be added with updates. Please check back regularly for new measures.

Ehers:

Autocorrelation Periodogram

Band-pass

Instantaneous Cycle

Hilbert Transformer

Dual Differentiator

Phase Accumulation (future release)

Homodyne (future release)

Jurik:

Composite Fractal Behavior (CFB)

Adam White:

Veritical Horizontal Filter (VHF) (future release)

What is an adaptive cycle, and what is Ehlers Autocorrelation Periodogram Algorithm?

From his Ehlers' book Cycle Analytics for Traders Advanced Technical Trading Concepts by John F. Ehlers , 2013, page 135:

"Adaptive filters can have several different meanings. For example, Perry Kaufman's adaptive moving average (KAMA) and Tushar Chande's variable index dynamic average (VIDYA) adapt to changes in volatility . By definition, these filters are reactive to price changes, and therefore they close the barn door after the horse is gone.The adaptive filters discussed in this chapter are the familiar Stochastic , relative strength index (RSI), commodity channel index (CCI), and band-pass filter.The key parameter in each case is the look-back period used to calculate the indicator. This look-back period is commonly a fixed value. However, since the measured cycle period is changing, it makes sense to adapt these indicators to the measured cycle period. When tradable market cycles are observed, they tend to persist for a short while.Therefore, by tuning the indicators to the measure cycle period they are optimized for current conditions and can even have predictive characteristics.

The dominant cycle period is measured using the Autocorrelation Periodogram Algorithm. That dominant cycle dynamically sets the look-back period for the indicators. I employ my own streamlined computation for the indicators that provide smoother and easier to interpret outputs than traditional methods. Further, the indicator codes have been modified to remove the effects of spectral dilation.This basically creates a whole new set of indicators for your trading arsenal."

What is this Hilbert Transformer?

An analytic signal allows for time-variable parameters and is a generalization of the phasor concept, which is restricted to time-invariant amplitude, phase, and frequency. The analytic representation of a real-valued function or signal facilitates many mathematical manipulations of the signal. For example, computing the phase of a signal or the power in the wave is much simpler using analytic signals.

The Hilbert transformer is the technique to create an analytic signal from a real one. The conventional Hilbert transformer is theoretically an infinite-length FIR filter. Even when the filter length is truncated to a useful but finite length, the induced lag is far too large to make the transformer useful for trading.

From his Ehlers' book Cycle Analytics for Traders Advanced Technical Trading Concepts by John F. Ehlers , 2013, pages 186-187:

"I want to emphasize that the only reason for including this section is for completeness. Unless you are interested in research, I suggest you skip this section entirely. To further emphasize my point, do not use the code for trading. A vastly superior approach to compute the dominant cycle in the price data is the autocorrelation periodogram. The code is included because the reader may be able to capitalize on the algorithms in a way that I do not see. All the algorithms encapsulated in the code operate reasonably well on theoretical waveforms that have no noise component. My conjecture at this time is that the sample-to-sample noise simply swamps the computation of the rate change of phase, and therefore the resulting calculations to find the dominant cycle are basically worthless.The imaginary component of the Hilbert transformer cannot be smoothed as was done in the Hilbert transformer indicator because the smoothing destroys the orthogonality of the imaginary component."

What is the Dual Differentiator, a subset of Hilbert Transformer?

From his Ehlers' book Cycle Analytics for Traders Advanced Technical Trading Concepts by John F. Ehlers , 2013, page 187:

"The first algorithm to compute the dominant cycle is called the dual differentiator. In this case, the phase angle is computed from the analytic signal as the arctangent of the ratio of the imaginary component to the real component. Further, the angular frequency is defined as the rate change of phase. We can use these facts to derive the cycle period."

What is the Phase Accumulation, a subset of Hilbert Transformer?

From his Ehlers' book Cycle Analytics for Traders Advanced Technical Trading Concepts by John F. Ehlers , 2013, page 189:

"The next algorithm to compute the dominant cycle is the phase accumulation method. The phase accumulation method of computing the dominant cycle is perhaps the easiest to comprehend. In this technique, we measure the phase at each sample by taking the arctangent of the ratio of the quadrature component to the in-phase component. A delta phase is generated by taking the difference of the phase between successive samples. At each sample we can then look backwards, adding up the delta phases.When the sum of the delta phases reaches 360 degrees, we must have passed through one full cycle, on average.The process is repeated for each new sample.

The phase accumulation method of cycle measurement always uses one full cycle's worth of historical data.This is both an advantage and a disadvantage.The advantage is the lag in obtaining the answer scales directly with the cycle period.That is, the measurement of a short cycle period has less lag than the measurement of a longer cycle period. However, the number of samples used in making the measurement means the averaging period is variable with cycle period. longer averaging reduces the noise level compared to the signal.Therefore, shorter cycle periods necessarily have a higher out- put signal-to-noise ratio."

What is the Homodyne, a subset of Hilbert Transformer?

From his Ehlers' book Cycle Analytics for Traders Advanced Technical Trading Concepts by John F. Ehlers , 2013, page 192:

"The third algorithm for computing the dominant cycle is the homodyne approach. Homodyne means the signal is multiplied by itself. More precisely, we want to multiply the signal of the current bar with the complex value of the signal one bar ago. The complex conjugate is, by definition, a complex number whose sign of the imaginary component has been reversed."

What is the Instantaneous Cycle?

The Instantaneous Cycle Period Measurement was authored by John Ehlers; it is built upon his Hilbert Transform Indicator.

From his Ehlers' book Cybernetic Analysis for Stocks and Futures: Cutting-Edge DSP Technology to Improve Your Trading by John F. Ehlers, 2004, page 107:

"It is obvious that cycles exist in the market. They can be found on any chart by the most casual observer. What is not so clear is how to identify those cycles in real time and how to take advantage of their existence. When Welles Wilder first introduced the relative strength index (rsi), I was curious as to why he selected 14 bars as the basis of his calculations. I reasoned that if i knew the correct market conditions, then i could make indicators such as the rsi adaptive to those conditions. Cycles were the answer. I knew cycles could be measured. Once i had the cyclic measurement, a host of automatically adaptive indicators could follow.

Measurement of market cycles is not easy. The signal-to-noise ratio is often very low, making measurement difficult even using a good measurement technique. Additionally, the measurements theoretically involve simultaneously solving a triple infinity of parameter values. The parameters required for the general solutions were frequency, amplitude, and phase. Some standard engineering tools, like fast fourier transforms (ffs), are simply not appropriate for measuring market cycles because ffts cannot simultaneously meet the stationarity constraints and produce results with reasonable resolution. Therefore i introduced maximum entropy spectral analysis (mesa) for the measurement of market cycles. This approach, originally developed to interpret seismographic information for oil exploration, produces high-resolution outputs with an exceptionally short amount of information. A short data length improves the probability of having nearly stationary data. Stationary data means that frequency and amplitude are constant over the length of the data. I noticed over the years that the cycles were ephemeral. Their periods would be continuously increasing and decreasing. Their amplitudes also were changing, giving variable signal-to-noise ratio conditions. Although all this is going on with the cyclic components, the enduring characteristic is that generally only one tradable cycle at a time is present for the data set being used. I prefer the term dominant cycle to denote that one component. The assumption that there is only one cycle in the data collapses the difficulty of the measurement process dramatically."

What is the Band-pass Cycle?

From his Ehlers' book Cycle Analytics for Traders Advanced Technical Trading Concepts by John F. Ehlers , 2013, page 47:

"Perhaps the least appreciated and most underutilized filter in technical analysis is the band-pass filter. The band-pass filter simultaneously diminishes the amplitude at low frequencies, qualifying it as a detrender, and diminishes the amplitude at high frequencies, qualifying it as a data smoother. It passes only those frequency components from input to output in which the trader is interested. The filtering produced by a band-pass filter is superior because the rejection in the stop bands is related to its bandwidth. The degree of rejection of undesired frequency components is called selectivity. The band-stop filter is the dual of the band-pass filter. It rejects a band of frequency components as a notch at the output and passes all other frequency components virtually unattenuated. Since the bandwidth of the deep rejection in the notch is relatively narrow and since the spectrum of market cycles is relatively broad due to systemic noise, the band-stop filter has little application in trading."

From his Ehlers' book Cycle Analytics for Traders Advanced Technical Trading Concepts by John F. Ehlers , 2013, page 59:

"The band-pass filter can be used as a relatively simple measurement of the dominant cycle. A cycle is complete when the waveform crosses zero two times from the last zero crossing. Therefore, each successive zero crossing of the indicator marks a half cycle period. We can establish the dominant cycle period as twice the spacing between successive zero crossings."

What is Composite Fractal Behavior (CFB)?

All around you mechanisms adjust themselves to their environment. From simple thermostats that react to air temperature to computer chips in modern cars that respond to changes in engine temperature, r.p.m.'s, torque, and throttle position. It was only a matter of time before fast desktop computers applied the mathematics of self-adjustment to systems that trade the financial markets.

Unlike basic systems with fixed formulas, an adaptive system adjusts its own equations. For example, start with a basic channel breakout system that uses the highest closing price of the last N bars as a threshold for detecting breakouts on the up side. An adaptive and improved version of this system would adjust N according to market conditions, such as momentum, price volatility or acceleration.

Since many systems are based directly or indirectly on cycles, another useful measure of market condition is the periodic length of a price chart's dominant cycle, (DC), that cycle with the greatest influence on price action.

The utility of this new DC measure was noted by author Murray Ruggiero in the January '96 issue of Futures Magazine. In it. Mr. Ruggiero used it to adaptive adjust the value of N in a channel breakout system. He then simulated trading 15 years of D-Mark futures in order to compare its performance to a similar system that had a fixed optimal value of N. The adaptive version produced 20% more profit!

This DC index utilized the popular MESA algorithm (a formulation by John Ehlers adapted from Burg's maximum entropy algorithm, MEM). Unfortunately, the DC approach is problematic when the market has no real dominant cycle momentum, because the mathematics will produce a value whether or not one actually exists! Therefore, we developed a proprietary indicator that does not presuppose the presence of market cycles. It's called CFB (Composite Fractal Behavior) and it works well whether or not the market is cyclic.

CFB examines price action for a particular fractal pattern, categorizes them by size, and then outputs a composite fractal size index. This index is smooth, timely and accurate

Essentially, CFB reveals the length of the market's trending action time frame. Long trending activity produces a large CFB index and short choppy action produces a small index value. Investors have found many applications for CFB which involve scaling other existing technical indicators adaptively, on a bar-to-bar basis.

What is VHF Adaptive Cycle?

Vertical Horizontal Filter (VHF) was created by Adam White to identify trending and ranging markets. VHF measures the level of trend activity, similar to ADX DI. Vertical Horizontal Filter does not, itself, generate trading signals, but determines whether signals are taken from trend or momentum indicators. Using this trend information, one is then able to derive an average cycle length.

Is it Time for a Pullback? Check Bars Since MA TestAn old market adage declares that “prices never move in a straight line.” Dips occur even in bullish markets. But how can traders know when prices may be due for a pullback?

Today’s script tries to answer that question by asking how many bars have passed since a stock, index or other symbol has tested a given moving average. Long periods of time without touching a line such as the 50-day simple moving average, for example, could prompt traders to be more patient.

Bars Since MA Test counts how many bars have passed since prices touched or crossed the MA in question. The resulting value is plotted in a simple histogram. Users can set the MA length and type. By default, it uses the 50-day simple moving average (SMA).

The chart above applies Bars Since MA Test to the S&P 500. It shows that the index has gone 129 bars without testing its 50-day SMA. That’s the longest since a 146-bar stretch between July 2006 and February 2007.

Other longer runs include January-August 1995 (156 bars), November 1960-June 1961 (144 bars) and April-November 1958 (158 bars).

Given the small number of comparable readings, could traders suspect the current advance is getting long in the tooth?

TradeStation has, for decades, advanced the trading industry, providing access to stocks, options and futures. If you're born to trade, we could be for you. See our Overview for more.

Past performance, whether actual or indicated by historical tests of strategies, is no guarantee of future performance or success. There is a possibility that you may sustain a loss equal to or greater than your entire investment regardless of which asset class you trade (equities, options or futures); therefore, you should not invest or risk money that you cannot afford to lose. Online trading is not suitable for all investors. View the document titled Characteristics and Risks of Standardized Options at www.TradeStation.com . Before trading any asset class, customers must read the relevant risk disclosure statements on www.TradeStation.com . System access and trade placement and execution may be delayed or fail due to market volatility and volume, quote delays, system and software errors, Internet traffic, outages and other factors.

Securities and futures trading is offered to self-directed customers by TradeStation Securities, Inc., a broker-dealer registered with the Securities and Exchange Commission and a futures commission merchant licensed with the Commodity Futures Trading Commission). TradeStation Securities is a member of the Financial Industry Regulatory Authority, the National Futures Association, and a number of exchanges.

TradeStation Securities, Inc. and TradeStation Technologies, Inc. are each wholly owned subsidiaries of TradeStation Group, Inc., both operating, and providing products and services, under the TradeStation brand and trademark. When applying for, or purchasing, accounts, subscriptions, products and services, it is important that you know which company you will be dealing with. Visit www.TradeStation.com for further important information explaining what this means.

Breakdown or Buyable Dip? Pullback Depth Can HelpAs a common adage says, “the market doesn’t move in a straight line.” But when prices have fallen, it’s not always clear whether buying makes sense. That’s where today’s script may help.

Most traditional indicators judge movement based on price. That’s obviously important, but time can also be helpful. After all, there’s a big difference between probing a low from 2-3 weeks ago versus a low from months or even years in the past.

Pullback Depth clearly illustrates this by answering the question: “Today’s low is the lowest in how many bars?”

The resulting integer is plotted in a simple histogram. Values are always negative because bars with higher absolute values (meaning more negative, or further below zero) are potentially more bearish.

The study also has a maximum lookback period to avoid overwhelming the study with too many bars. Its default setting of 125 bars includes enough history to illustrate the trend.

The stock market’s recent run has seen only shallow pullbacks. Most dips have probed 1-2 weeks in the past, while Friday’s selloff only turned back the clock a month.

Consider two other previous moments.

First, the great bull run of 1995 saw only shallow pullbacks. (None exceeded 50 days.):

In contrast, early 2022 saw the S&P 500 test levels more than 100 candles into the past. It soon fell into an official “bear market:”

TradeStation has, for decades, advanced the trading industry, providing access to stocks, options and futures. If you're born to trade, we could be for you. See our Overview for more.

Past performance, whether actual or indicated by historical tests of strategies, is no guarantee of future performance or success. There is a possibility that you may sustain a loss equal to or greater than your entire investment regardless of which asset class you trade (equities, options or futures); therefore, you should not invest or risk money that you cannot afford to lose. Online trading is not suitable for all investors. View the document titled Characteristics and Risks of Standardized Options at www.TradeStation.com . Before trading any asset class, customers must read the relevant risk disclosure statements on www.TradeStation.com . System access and trade placement and execution may be delayed or fail due to market volatility and volume, quote delays, system and software errors, Internet traffic, outages and other factors.

Securities and futures trading is offered to self-directed customers by TradeStation Securities, Inc., a broker-dealer registered with the Securities and Exchange Commission and a futures commission merchant licensed with the Commodity Futures Trading Commission). TradeStation Securities is a member of the Financial Industry Regulatory Authority, the National Futures Association, and a number of exchanges.

TradeStation Securities, Inc. and TradeStation Technologies, Inc. are each wholly owned subsidiaries of TradeStation Group, Inc., both operating, and providing products and services, under the TradeStation brand and trademark. When applying for, or purchasing, accounts, subscriptions, products and services, it is important that you know which company you will be dealing with. Visit www.TradeStation.com for further important information explaining what this means.

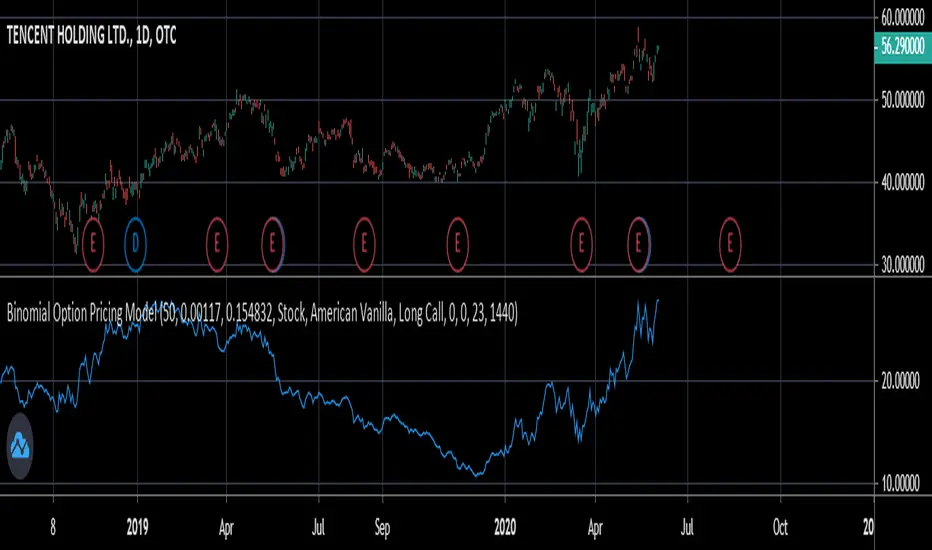

Binomial Option Pricing ModelA binomial option pricing model is an option pricing model that calculates an option's price using binomial trees. The BOPM method of calculating option prices is different from the Black-Scholes Model because it provides more flexibility in the type of options you want to price. The BOPM, unlike the BS model typically used for European style options, allows you to price options which have the ability to exercise early, such as American or Bermudan options. Although you can use the BOPM for any option style.

This specific model allows you to price both American and European vanilla options.

The way the BOPM calculates option prices is by:

First, dividing up the time until expiry into equal parts called steps. This specific model presented only uses 2 steps. For example, say you have an option with an expiry of 60 days, and your binomial tree has only two steps. Then each step will contain 30 days.

Second, the model will project the expected price of the underlying at the end of each step, called a node. The expected price is calculated by using the underlying's volatility and projecting what the price of the underlying would be if it were to rise and fall. This step is repeated until the terminal node, aka the end of the tree, is reached.

Third, once the terminal node's expected underlying prices are calculated, their expected option prices must be calculated.

Finally, after calculating the terminal option prices, backwards induction must be used to calculate the option prices at the previous nodes, until you reach Node 0, aka the current option price.

In order to use this model:

1st. Enter your option's strike price.

2nd. Enter the risk-free-rate of the currency the option is based in.

3rd. Enter the dividend yield of the underlying if it's a stock, or the foreign risk-free-rate if it's an FX option.

*For example, if you were trading an AAPL stock option, in the risk-free-rate box mentioned in step 2, you would enter the US risk-free-rate because AAPL options are traded in US dollars. In the dividend yield box mentioned in step 3, you would enter the stock's dividend yield, which for AAPL is 0.82.

*If you were, for example, trading an option on the EUR/JPY currency pair, the risk-free-rate mentioned in step 2, would be the Japanese risk-free-rate. Then in the the dividend yield box from step 3, you'd input the Eurozone risk-free-rate.

*If you were trading an options on futures contract, the risk-free-rate mentioned in step 2, would be the risk-free-rate for whatever currency the futures contract is denominated in. For example EUR futures are denominated in USD, so you would input the US risk-free-rate. Meanwhile, something like FTSE futures are denominated in GBP, so you would input the British risk-free-rate. As for the dividend yield box mentioned in step 3, for all options on futures, enter 0.

4th. Pick what type of underlying the option is based on: stock, FX, or futures.

5th. Pick the style of option: American or European.

6th. Pick the type of option: Long Call or Long Put.

7th. Input your time until expiry. You can express this in terms of days, hours, and minutes.

8th. Lastly, input your chart time-frame in term of minutes. For example, if you're using the 1 min time-frame enter 1, 4hr time-frame enter 480, daily time-frame enter 1440.

*Disclaimer, because this particular model only uses 2 steps, it won't work on stocks with high prices (over $100). If you want to use this on stocks with prices greater than $100, you would need to add more steps to the code, shown below. The model in its current form should work for stocks below $100.

cephxs / New X Opening Gaps [Pro +]NWOG & NDOG - OPENING GAPS

Smart Gap Detection with Intelligent Filtering

Visualizes New Week Opening Gaps (NWOGs) and New Day Opening Gaps (NDOGs) with built-in intelligence to show you only what matters. No more cluttered charts with gaps from 3 months ago that price will never revisit.

THE PROBLEM WITH GAP INDICATORS

Most gap indicators dump every single gap on your chart and call it a day. You end up with 50 boxes cluttering your screen, half of which are miles away from current price and the other half are so tiny they're basically noise.

This one's different and I explain why below.

SMART FILTERING (THE GOOD STUFF)

Two filters work together to keep your chart clean:

Size Filter: Uses ATR-based detection to filter out insignificant gaps, dynamic with less volatile time periods

- Filter None: Show everything (if you really want chaos)

- Filter Insignificant: Hide the micro-gaps that don't matter

- Juicy Gaps Only: Only show gaps worth paying attention to

Distance Filter: Only displays gaps within range of current price

- Really Close: 0.5 ATR - tight focus on immediate levels

- Balanced: 1 ATR - sweet spot for most traders

- Slightly Far: 3 ATR - wider view for swing traders

Cleanup Interval: Controls how quickly out-of-range gaps disappear

- Immediately: Gaps hide/show every bar as price moves

- 5 / 15 / 30 Minutes: Gaps only update visibility at interval boundaries - reduces visual noise during choppy price action

The magic: gaps appear and disappear as price moves toward or away from them. Old gaps that price has left behind fade out, and gaps that become relevant fade back in. Use delayed cleanup intervals if you want gaps to "stick around" a bit longer before disappearing.

GAP TYPES EXPLAINED

New Week Opening Gaps (NWOGs):

The gap between Friday's close and Monday's open. These form over the weekend when markets are closed and often act as significant support/resistance.

Two classifications:

Void Gaps: Gap direction aligns with Friday's candle direction (continuation)

Overlap Gaps: Gap direction conflicts with Friday's candle (potential reversal)

New Day Opening Gaps (NDOGs):

The gap between one day's close and the next day's open. Smaller but frequent - useful for intraday traders looking for fill targets.

FEATURES

Automatic Week/Day Detection: Handles forex (17:00 ET open) and futures (18:00 ET open) correctly

DST-Aware: Uses New York timezone with automatic daylight saving adjustments

50% Equilibrium Line: Marks the midpoint of each gap - key level for entries

Days Ago Labels: Shows how old each gap is at a glance

Extension Modes: Choose between live-extending boxes or fixed-width boxes

Separate Color Schemes: Different colors for void vs overlap NWOGs, bullish vs bearish NDOGs

INPUTS

NWOG Display

Show NWOGs: Master toggle

Extension Mode: "Extend Live" or "Extend to Week Close"

Maximum NWOGs: Limit displayed gaps (1-50)

Show Void/Overlap Gaps: Toggle each type independently

Show NWOG Labels: Toggle gap labels

NDOG Display

Show NDOGs: Master toggle

Extension Mode: "Extend Live" or "Extend to Day Close"

Maximum NDOGs: Limit displayed gaps (1-50)

Show NDOG Labels: Toggle gap labels

Filter Settings

Size Filter: Filter None / Filter Insignificant / Juicy Gaps Only

Only Show Near Price: Enable/disable distance filtering

Distance Filter: Really Close / Balanced / Slightly Far

Cleanup Interval: Immediately / 5 Minutes / 15 Minutes / 30 Minutes - controls how often gaps update visibility

ATR Period: Period for ATR calculation (default: 14)

Right Edge Offset: How many bars ahead boxes extend

Styling

Box Transparency: Fill and border opacity

Midline Style: Solid / Dotted / Dashed

Label Style: Simple ("NWOG, 5d ago") or Descriptive ("NWOG (Void Bull), 5d ago")

Label Size: Tiny / Small / Normal / Large

RECOMMENDED SETTINGS

For intraday (1m-15m):

Size Filter: Filter Insignificant

Distance Filter: Really Close or Balanced

Show NDOGs: On

Maximum NDOGs: 5-10

For swing trading (1H-4H):

Size Filter: Juicy Gaps Only

Distance Filter: Balanced or Slightly Far

Show NWOGs: On

Maximum NWOGs: 10-20

TIMEFRAME NOTES

Works on daily timeframe and below. Above daily, the indicator disables itself since NWOG/NDOG gap detection requires daily open/close data.

ASSET SUPPORT

Automatically handles different market open times:

Forex: Week opens Sunday 17:00 ET, closes Friday 17:00 ET

Futures: Week opens Sunday 18:00 ET, closes Friday 16:15 ET

Stocks/Other: Uses session-based detection

FAQ

Why do gaps appear and disappear?

That's the distance filter working. As price moves, gaps that were far away become relevant and appear. Gaps that price leaves behind disappear. This keeps your chart focused on actionable levels.

What's the difference between void and overlap gaps?

Void gaps continue Friday's direction (trend continuation). Overlap gaps conflict with Friday's direction (potential reversal setup). Different traders prefer different types.

Why can't I see any gaps?

Check your filter settings. "Juicy Gaps Only" with "Really Close" distance filter is very selective. Try "Filter Insignificant" with "Balanced" for more gaps.

DISCLAIMER

This indicator is for educational purposes only. Opening gaps are one tool among many - they don't guarantee fills or reversals. Always use proper risk management and never trade based on a single indicator. Past gap fills don't guarantee future performance. Do your own analysis.

CHANGELOG

Pro +: Added smart size/distance filtering, void/overlap classification, NDOG support, DST-aware timezone handling

Base: Initial NWOG visualization

Made with ❤️ by fstarlabs

HA Trend Reclaim Daily Structure Pullback🔹 HA Trend Reclaim — Daily Structure Pullback System

HA Trend Reclaim is a professional-grade trend continuation indicator designed to highlight high-probability LONG and SHORT setups using a combination of:

Heikin Ashi candle structure

EMA trend alignment (9 & 50 EMA)

Daily High / Low market structure

Pullback → momentum reclaim logic

This indicator is built for traders who want clarity, discipline, and structure, not noise or over-signaling.

It focuses on trading with the dominant trend, entering only after price pulls back and confirms strength via momentum reclaim.

🔑 What Makes This Different

✔ No counter-trend signals

✔ No breakout chasing

✔ Built-in structure awareness

✔ Clear visual entries & risk levels

✔ Works across stocks, crypto, and futures

This script is ideal for traders who prefer fewer, higher-quality trades rather than constant signals.

2️⃣ HOW TO USE (FEATURED-FRIENDLY VERSION)

🟢 LONG Conditions

A LONG signal appears when:

EMA 9 is above EMA 50

Price is above EMA 50

Price pulls back into the EMA zone

Price reclaims EMA 9 upward

Heikin Ashi candle closes bullish (not a doji)

🔴 SHORT Conditions

A SHORT signal appears when:

EMA 9 is below EMA 50

Price is below EMA 50

Price pulls back into the EMA zone

Price reclaims EMA 9 downward

Heikin Ashi candle closes bearish (not a doji)

📦 Daily Structure Boxes

The indicator highlights the daily high–low range:

Green box → bullish daily bias

Red box → bearish daily bias

These boxes help traders avoid:

Mid-range chop

Late entries

Trading against daily momentum

3️⃣ BEST SETTINGS (VERY IMPORTANT FOR USERS)

Recommended Timeframes

Stocks: 5m, 15m, 1H

Crypto: 15m, 1H, 4H

Futures: 5m, 15m

Recommended Inputs

Setting Value

EMA Fast 9

EMA Slow 50

Swing Lookback 15

Runner RR 2.0

Heikin Ashi Enabled

Show Daily Boxes Enabled

Notes

Higher timeframes = fewer, stronger signals

Avoid low-liquidity instruments

Best used during active sessions (London / NY)

CVD Zones & Divergence [Pro]# CVD Zones & Divergence

**Complete CVD order flow toolkit** - Divergences, POC, Profile, and Supply/Demand zones all in one professional indicator.

## 🎯 What It Does

Combines **four powerful order flow tools** into a single, cohesive indicator:

1. **CVD Divergences** - Early warnings + confirmed signals

2. **Point of Control (POC)** - Fair value equilibrium line

3. **CVD Profile** - Visual distribution histogram

4. **Supply/Demand Zones** - Real absorption-based S/R levels

All based on **Cumulative Volume Delta (CVD)** - actual buying/selling pressure, not approximations.

## ✨ Key Features

### 🔄 CVD Divergences (Dual Mode)

**Confirmed Divergences** (High Accuracy)

- Solid lines (customizable colors)

- 🔻 Bear / 🔺 Bull labels

- Win rate: ~70-80%

- Best for swing traders

**Early Warning Mode** ⚡ (Fast Signals)

- Dashed lines (default purple)

- ⚠️ Early Bear / ⚠️ Early Bull labels

- Fires 6+ bars earlier

- Win rate: ~55-65%

- Best for scalpers/day traders

### 🎯 Point of Control (POC)

- **Independent lookback** (300 bars default)

- Yellow line showing fair value

- Where most CVD activity occurred

- Acts as dynamic support/resistance

- Resets and recalculates continuously

### 📊 CVD Profile Histogram

- **Visual CVD distribution** over lookback period

- **Split buy/sell** (blue/orange bars)

- **Value Area** (70% CVD zone highlighted)

- Position: Right/Left/Current (your choice)

- Shows where actual order flow happened

### 📦 Supply/Demand Zones

- **Absorption-based** detection (not guesses!)

- Green = Demand (buyers absorbed 2:1+)

- Red = Supply (sellers absorbed 2:1+)

- Shows **real** institutional levels

- Auto-sorted by strength

- Displays top 8 zones

## 📊 What You See on Chart

```

Your Chart:

├─ 🔴 Red lines (bearish divergences)

├─ 🟢 Green lines (bullish divergences)

├─ 🟣 Purple dashed (early warnings)

├─ 🟡 Yellow POC line (fair value)

├─ 📊 Blue/Orange profile (right side)

├─ 🟢 Green boxes (demand zones)

└─ 🔴 Red boxes (supply zones)

```

## ⚙️ Recommended Settings

### 15m Day Trading (Most Popular)

```

📊 Profile:

- Lookback: 150 bars

- Profile Rows: 24

- Position: Right

🎯 POC:

- POC Lookback: 300 bars

- Show POC: ON

📦 Zones:

- Min Absorption Ratio: 2.0

- HVN Threshold: 1.5

- Max Zones: 8

🔄 Divergences:

- Pivot L/R: 9

- Early Warning: ON

- Early Right Bars: 3

- Min Bars Between: 40

- Min CVD Diff: 5%

```

### 5m Scalping

```

Profile Lookback: 100

POC Lookback: 200

Pivot L/R: 7

Early Warning Right: 2

Min Bars Between: 60

```

### 1H Swing Trading

```

Profile Lookback: 200

POC Lookback: 400-500

Pivot L/R: 12-14

Early Warning Right: 4-5

Min Bars Between: 30

Min CVD Diff: 8%

```

## 💡 How to Trade

### Setup 1: Divergence at Zone ⭐ (BEST - 75%+ win rate)

**Entry:**

- Price hits demand/supply zone

- Divergence appears (early or confirmed)

- Double confluence = high probability

**Example (Long):**

```

1. Price drops into green demand zone

2. ⚠️ Early bullish divergence fires

3. Enter long with tight stop below zone

4. Target: POC or next supply zone

```

**Risk/Reward:** 1:3 to 1:5

---

### Setup 2: POC Bounce/Rejection

**Entry:**

- Price approaches POC line

- Wait for reaction (bounce or rejection)

- Enter in direction of reaction

**Long Setup:**

```

1. Price pulls back to POC from above

2. POC acts as support

3. Bullish divergence appears (confirmation)

4. Enter long, stop below POC

```

**Short Setup:**

```

1. Price rallies to POC from below

2. POC acts as resistance

3. Bearish divergence appears

4. Enter short, stop above POC

```

**Risk/Reward:** 1:2 to 1:4

---

### Setup 3: Zone + Profile Confluence

**Entry:**

- Supply/demand zone aligns with thick profile bar

- Shows high CVD activity at that level

- Triple confluence = very high probability

**Example:**

```

1. Supply zone at 26,100

2. Profile shows heavy selling at 26,100

3. Price rallies to 26,100

4. Bearish divergence appears

5. Enter short

```

**Risk/Reward:** 1:4 to 1:6

---

### Setup 4: Early Warning Scalp ⚡

**Entry (Aggressive):**

- ⚠️ Early warning fires

- Price at zone or POC

- Enter immediately

- Tight stop (1-2 ATR)

**Management:**

```

- Take 50% profit at 1:1

- Move stop to breakeven

- 🔻 Confirmed signal → Trail stop

- Exit rest at target

```

**Risk/Reward:** 1:1.5 to 1:2

**Trades/day:** 3-8

---

### Setup 5: Multi-Timeframe (Advanced)

**Confirmation Required:**

```

Higher TF (1H):

- Confirmed divergence

- At major POC or zone

Lower TF (15m):

- Early warning triggers

- Entry with better timing

```

**Benefits:**

- HTF gives direction

- LTF gives entry

- Best of both worlds

**Risk/Reward:** 1:3 to 1:5

---

## 📊 Component Details

### CVD Profile

**What the colors mean:**

- **Blue bars** = Buying CVD (demand)

- **Orange bars** = Selling CVD (supply)

- **Lighter shade** = Value Area (70% CVD)

- **Thicker bar** = More volume at that price

**How to use:**

- Thick bars = Support/Resistance

- Profile shape shows market structure

- Balanced profile = range

- Skewed profile = trend

---

### Supply/Demand Zones

**How they're detected:**

1. High Volume Node (1.5x average)

2. CVD buy/sell ratio calculated

3. Ratio ≥ 2.0 → Zone created

4. Sorted by strength (top 8 shown)

**Zone labels show:**

- Type: "Demand" or "Supply"

- Ratio: "2.8:1" = strength

**Not like other indicators:**

- ❌ Other tools use price action alone

- ✅ This uses actual CVD absorption

- Shows WHERE limit orders defended levels

---

### Point of Control (POC)

**What it shows:**

- Price with highest CVD activity

- Market's "fair value"

- Dynamic S/R level

**How to use:**

- Price above POC = bullish bias

- Price below POC = bearish bias

- POC retest = trading opportunity

- POC cross = trend change signal

**Independent lookback:**

- Profile: 150 bars (short-term)

- POC: 300 bars (longer-term context)

- Gives stable, relevant POC

---

## 🔧 Settings Explained

### 📊 Profile Settings

**Lookback Bars** (150 default)

- How many bars for profile calculation

- Lower = more recent, reactive

- Higher = more historical, stable

**Profile Rows** (24 default)

- Granularity of distribution

- Lower = coarser (faster)

- Higher = finer detail (slower)

**Profile Position**

- Right: After current price

- Left: Before lookback period

- Current: At lookback start

**Value Area** (70% default)

- Highlights main CVD concentration

- 70% is standard

- Higher % = wider zone

---

### 🎯 POC Settings

**POC Lookback** (300 default)

- Independent from profile

- Longer = more stable POC

- Shorter = more reactive POC

**Show POC Line/Label**

- Toggle visibility

- Customize color/width

---

### 📦 Zone Settings

**Min Absorption Ratio** (2.0 default)

- Buy/Sell threshold for zones

- 2.0 = 2:1 ratio minimum

- Higher = fewer, stronger zones

**HVN Threshold** (1.5 default)

- Volume must be 1.5x average

- Higher = stricter filtering

- Lower = more zones

**Max Zones** (8 default)

- Limits display clutter

- Shows strongest N zones only

---

### 🔄 Divergence Settings

**Pivot Left/Right** (9/9 default)

- Bars to confirm pivot

- Higher = slower, more confirmed

- Lower = faster, less confirmed

**Early Warning**

- ON = Show early signals

- Early Right Bars (3 default)

- 3 = 6 bars faster than confirmed

**Filters:**

- Min Bars Between (40): Prevents spam

- Min CVD Diff % (5): Filters weak signals

**Visual:**

- Line styles: Solid/Dashed/Dotted

- Colors: Customize all 4 types

- Labels: Toggle ON/OFF

---

## 🎨 Color Customization

**Divergences:**

- Bullish Confirmed: Green (default)

- Bearish Confirmed: Red (default)

- Early Bullish: Purple (default)

- Early Bearish: Purple (default)

**Zones & Profile:**

- Bull/Demand: Green

- Bear/Supply: Red

- Buy CVD Profile: Blue

- Sell CVD Profile: Orange

- Value Area Up/Down: Lighter blue/orange

**POC:**

- POC Color: Yellow (default)

All customizable to your preference!

---

## 🔔 Alerts Available

**6 Alert Types:**

1. 🔻 Bearish Divergence (confirmed)

2. 🔺 Bullish Divergence (confirmed)

3. ⚠️ Early Bearish Warning

4. ⚠️ Early Bullish Warning

5. (Manual: POC cross)

6. (Manual: Zone touch)

**Setup:**

1. Click Alert (⏰)

2. Choose "CVD Zones & Divergence"

3. Select alert type

4. Configure notification

5. Create!

---

## 💎 Pro Tips

### From Experienced Traders:

**"Use zones with divergences for best setups"**

- Zone alone: 60% win rate

- Divergence alone: 65% win rate

- Both together: 75%+ win rate

**"POC is your friend"**

- Price tends to revert to POC

- Great target for counter-trend trades

- POC cross = potential trend change

**"Profile tells the story"**

- Thick bars = institutional levels

- Balanced profile = range-bound

- Skewed high = distribution (top)

- Skewed low = accumulation (bottom)

**"Early warnings for entries, confirmed for confidence"**

- Early = better entry price

- Confirmed = validation

- Use both in scale-in strategy

**"Filter by timeframe"**

- 1m-5m: Very fast, many signals

- 15m: Sweet spot for most traders

- 1H-4H: High quality, fewer signals

---

## 🔧 Tuning Guide

### Too Cluttered?

**Simplify:**

```

✅ Show Divergences: ON

✅ Show POC: ON

❌ Show Zones: OFF (or reduce to 4-5)

❌ Show Value Area: OFF

❌ Divergence Labels: OFF

→ Clean chart with just lines + POC

```

### Missing Opportunities?

**More Signals:**

```

↓ Pivot Right: 6-7

↓ Early Warning Right: 2

↓ Min Bars Between: 25-30

↓ Min CVD Diff: 2-3%

↓ Min Absorption Ratio: 1.8

```

### Too Many False Signals?

**Stricter Filters:**

```

↑ Pivot Right: 12-15

↑ Min Bars Between: 60

↑ Min CVD Diff: 8-10%

↑ Min Absorption Ratio: 2.5

↓ Max Zones: 4-5

```

### POC Not Making Sense?

**Adjust POC Lookback:**

```

If too high: Increase to 400-500

If too low: Increase to 400-500

If jumping around: Increase to 500+

→ Longer lookback = more stable POC

```

---

## ❓ FAQ

**Q: Difference from CVD Divergence (standalone)?**

A: This is the **complete package**:

- Divergence tool = divergences only

- This = divergences + POC + profile + zones

- Use divergence tool for clean charts

- Use this for full analysis

**Q: Too slow/laggy?**

A: Reduce computational load:

```

Profile Rows: 18 (from 24)

Lookback: 100 (from 150)

Max Zones: 5 (from 8)

```

**Q: No volume data error?**

A: Symbol has no volume

- Works: Futures, stocks, crypto

- Maybe: Forex (broker-dependent)

- Doesn't work: Some forex pairs

**Q: Can I use just some features?**

A: Absolutely! Toggle what you want:

```

Zones only: Turn off divergences + POC

POC only: Turn off zones + divergences

Divergences only: Turn off zones + POC + profile

Mix and match as needed!

```

**Q: Best timeframe?**

A:

- **1m-5m**: Scalping (busy, many signals)

- **15m**: Day trading ⭐ (recommended)

- **1H-4H**: Swing trading (quality signals)

- **Daily**: Position trading (very selective)

**Q: Works on crypto/forex/stocks?**

A:

- ✅ Futures: Excellent

- ✅ Stocks: Excellent

- ✅ Crypto: Very good (major pairs)

- ⚠️ Forex: Depends on broker volume

---

## 📈 Performance Expectations

### Realistic Win Rates

| Strategy | Win Rate | Avg R/R | Trades/Week |

|----------|----------|---------|-------------|

| Early warnings only | 55-65% | 1:1.5 | 15-30 |

| Confirmed only | 70-80% | 1:2 | 8-15 |

| Divergence + Zone | 75-85% | 1:3 | 5-12 |

| Full confluence (all 4) | 80-90% | 1:4+ | 3-8 |

**Keys to success:**

- Don't trade every signal

- Wait for confluence

- Proper risk management

- Trade what you see, not what you think

---

## 🚀 Quick Start

**New User (5 minutes):**

1. ✅ Add to 15m chart

2. ✅ Default settings work well

3. ✅ Watch for 1 week (don't trade yet!)

4. ✅ Note which setups work best

5. ✅ Backtest on 50+ signals

6. ✅ Start with small size

7. ✅ Scale up slowly

**First Trade Checklist:**

- Divergence + Zone/POC = confluence

- Clear S/R level nearby

- Risk/reward minimum 1:2

- Position size = 1% risk max

- Stop loss placed

- Target identified

- Journal entry ready

---

## 📊 What Makes This Special?

**Most indicators:**

- Use RSI/MACD divergences (lagging)

- Guess at S/R zones (subjective)

- Don't show actual order flow

**This indicator:**

- Uses real CVD (actual volume delta)

- Absorption-based zones (real orders)

- Profile shows distribution (real activity)

- POC shows equilibrium (real fair value)

- All from one data source (coherent)

**Result:**

- Everything aligns

- No conflicting signals

- True order flow analysis

- Professional-grade toolkit

---

## 🎯 Trading Philosophy

**Remember:**

- Indicator shows you WHERE to look

- YOU decide whether to trade

- Quality over quantity always

- Risk management is #1

- Patience beats aggression

**Best trades have:**

- ✅ Multiple confluences

- ✅ Clear risk/reward

- ✅ Obvious invalidation point

- ✅ Aligned with trend/context

**Worst trades have:**

- ❌ Single signal only

- ❌ Poor location (middle of nowhere)

- ❌ Unclear stop placement

- ❌ Counter to all context

---

## ⚠️ Risk Disclaimer

**Important:**

- Past performance ≠ future results

- All trading involves risk

- Only risk what you can afford to lose

- This is a tool, not financial advice

- Use proper position sizing

- Keep a trading journal

- Consider professional advice

**Your responsibility:**

- Which setups to trade

- Position size

- Entry/exit timing

- Risk management

- Emotional control

**Success = Tool + Strategy + Discipline + Risk Management**

---

## 📝 Version History

**v1.0** - Current Release

- CVD divergences (confirmed + early warning)

- Point of Control (independent lookback)

- CVD profile histogram

- Supply/demand absorption zones

- Value area visualization

- 6 alert types

- Full customization

---

## 💬 Community

**Questions?** Drop a comment below

**Success story?** Share with the community

**Feature request?** Let me know

**Bug report?** Provide details in comments

---

**Happy Trading! 🚀📊**

*Professional order flow analysis in one indicator.*

**Like this?** ⭐ Follow for more quality tools!

Trading Volatility Clock⏰ TRADING VOLATILITY CLOCK - Know When the Action Happens (Anywhere in the World)

A real-time session tracker with multi-timezone support for active traders who need to know when US market volatility strikes - no matter where they are in the world. Perfect for day traders, scalpers, and anyone trading liquid US markets.

══════════════════════════════════════════════════════

📊 WHAT IT DOES

This indicator displays a live clock showing:

- Current time in YOUR selected timezone (10 major timezones supported)

- Active US market session with color-coded volatility levels

- Countdown timer showing time remaining in current session

- Preview of the next upcoming session

- Optional alerts when entering high-volatility periods

══════════════════════════════════════════════════════

🌍 MULTI-TIMEZONE SUPPORT

SESSIONS ALWAYS TRACK US MARKET HOURS (Eastern Time):

No matter which timezone you select, the sessions always trigger at the correct US market times. Perfect for international traders who want to:

• See their local time while tracking US market sessions

• Know exactly when US volatility hits in their timezone

• Plan their trading day around US market hours

SUPPORTED TIMEZONES:

• America/New_York (ET) - Eastern Time

• America/Chicago (CT) - Central Time

• America/Los_Angeles (PT) - Pacific Time

• Europe/London (GMT) - Greenwich Mean Time

• Europe/Berlin (CET) - Central European Time

• Asia/Tokyo (JST) - Japan Standard Time

• Asia/Shanghai (CST) - China Standard Time

• Asia/Hong_Kong (HKT) - Hong Kong Time

• Australia/Sydney (AEDT) - Australian Eastern Time

• UTC - Coordinated Universal Time

EXAMPLE: A trader in Tokyo selects "Asia/Tokyo"

• Clock shows: 11:30 PM JST

• Session shows: "Opening Drive" 🔥 HIGH

• They know: US market just opened (9:30 AM ET in New York)

══════════════════════════════════════════════════════

🎯 WHY IT'S USEFUL

Whether you trade futures, high-volume stocks, or ETFs, volatility isn't constant throughout the day. Knowing WHEN to expect movement is critical:

🔥 HIGH VOLATILITY (Red):

• Opening Drive (9:30-10:30 AM ET) - Highest volume of the day

• Power Hour (3:00-4:00 PM ET) - Second-highest volume, final push

⚡ MEDIUM VOLATILITY (Yellow):

• Pre-Market (8:00-9:30 AM ET) - Building momentum

• Lunch Return (1:00-2:00 PM ET) - Traders returning

• Afternoon Session (2:00-3:00 PM ET) - Trend continuation

• After Hours (4:00-5:00 PM ET) - News reactions

💤 LOW VOLATILITY (Gray):

• Overnight Grind (12:00-8:00 AM ET) - Thin volume

• Mid-Morning Chop (10:30-11:30 AM ET) - Ranges form

• Lunch Hour (11:30 AM-1:00 PM ET) - Dead zone

• Evening Fade (5:00-8:00 PM ET) - Volume dropping

══════════════════════════════════════════════════════

⚙️ CUSTOMIZATION OPTIONS

TIMEZONE SETTINGS:

• Select from 10 major timezones worldwide

• Clock automatically displays in your local time

• Sessions remain locked to US market hours

SESSION TIME CUSTOMIZATION:

• Every session boundary is adjustable (in minutes from midnight ET)

• Perfect for traders who define sessions differently

• Advanced users can create custom volatility schedules

DISPLAY OPTIONS:

• Toggle next session preview on/off

• Enable/disable high volatility alerts

• Clean, unobtrusive table display in top-right corner

══════════════════════════════════════════════════════

💡 HOW TO USE

1. Add indicator to any chart (works on all timeframes)

2. Select your timezone in Settings → Timezone Settings

3. Set your chart to 1-minute timeframe for real-time updates

4. Customize session times if needed (Settings → Session Time Customization)

5. Watch the top-right corner for live session tracking

TRADING APPLICATIONS:

• Avoid trading during dead zones (lunch hour, mid-morning chop)

• Increase position size during high volatility windows

• Set alerts for Opening Drive and Power Hour

• Plan your trading day around US market volatility schedule

• International traders can track US sessions in their local time

══════════════════════════════════════════════════════

🎓 EDUCATIONAL VALUE

This indicator teaches traders:

• Market microstructure and volume patterns

• Why certain times produce better opportunities

• How institutional flows create intraday patterns

• The importance of timing in active trading

• How to adapt US market trading to any timezone

══════════════════════════════════════════════════════

⚠️ IMPORTANT NOTES

- Works best on 1-minute charts for frequent updates

- Sessions are ALWAYS based on US Eastern Time (ET)

- Timezone selection only changes the clock display

- Clock updates when new bar closes (not tick-by-tick)

- Alerts trigger once per bar when enabled

- Perfect for international traders tracking US markets

══════════════════════════════════════════════════════

📈 BEST USED WITH

- High-volume US stocks: TSLA, NVDA, AAPL, AMD, META

- Major US ETFs: SPY, QQQ, IWM, DIA

- US Futures: ES, NQ, RTY, YM, MES, MNQ

- Any liquid US instrument with clear intraday volume patterns

══════════════════════════════════════════════════════

🌏 FOR INTERNATIONAL TRADERS

This tool is specifically designed for traders outside the US who need to:

• Track US market sessions in their local timezone

• Know when to be at their desk for US volatility

• Avoid waking up for low-volatility periods

• Maximize trading efficiency around US market hours

No more timezone confusion. No more missing the opening bell. Just set your timezone and trade with confidence.

══════════════════════════════════════════════════════

This is an open-source educational tool. Feel free to modify and adapt to your trading style!

Happy Trading! 🚀

Predicted Funding RatesOverview

The Predicted Funding Rates indicator calculates real-time funding rate estimates for perpetual futures contracts on Binance. It uses triangular weighting algorithms on multiple different timeframes to ensure an accurate prediction.

Funding rates are periodic payments between long and short position holders in perpetual futures markets

If positive, longs pay shorts (usually bullish)

If negative, shorts pay longs (usually bearish)

This is a prediction. Actual funding rates depend on the instantaneous premium index, derived from bid/ask impacts of futures. So whilst it may imitate it similarly, it won't be completely accurate.

This only applies currently to Binance funding rates, as HyperLiquid premium data isn't available. Other Exchanges may be added if their premium data is uploaded.

Methods

Method 1: Collects premium 1-minunute data using triangular weighing over 8 hours. This granular method fills in predicted funding for 4h and less recent data

Method 2: Multi-time frame approach. Daily uses 1 hour data in the calculation, 4h + timeframes use 15M data. This dynamic method fills in higher timeframes and parts where there's unavailable premium data on the 1min.

How it works

1) Premium data is collected across multiple timeframes (depending on the timeframe)

2) Triangular weighing is applied to emphasize recent data points linearly

Tri_Weighing = (data *1 + data *2 + data *3 + data *4) / (1+2+3+4)

3) Finally, the funding rate is calculated

FundingRate = Premium + clamp(interest rate - Premium, -0.05, 0.05)

where the interest rate is 0.01% as per Binance

Triangular weighting is calculated on collected premium data, where recent data receives progressively higher weight (1, 2, 3, 4...). This linear weighting scheme provides responsiveness to recent market conditions while maintaining stability, similar to an exponential moving average but with predictable, linear characteristics

A visual representation:

Data points: ──────────────>

Weights: 1 2 3 4 5

Importance: ▂ ▃ ▅ ▆ █

How to use it

For futures traders:

If funding is trending up, the market can be interpreted as being in a bull market

If trending down, the market can be interpreted as being in a bear market

Even used simply, it allows you to gauge roughly how well the market is performing per funding. It can basically be gauged as a sentiment indicator too

For funding rate traders:

If funding is up, it can indicate a long on implied APR values

If funding is down, it can indicate a short on implied APR values

It also includes an underlying APR, which is the annualized funding rate. For Binance, it is current funding * (24/8) * 365

For Position Traders: Monitor predicted funding rates before entering large positions. Extremely high positive rates (>0.05% for 8-hour periods) suggest overleveraged longs and potential reversal risk. Conversely, extreme negative rates indicate shorts dominance

Table:

Funding rate: Gives the predicted funding rate as a percentage

Current premium: Displays the current premium (difference between perpetual futures price and the underlying spot) as a percentage

Funding period: You can choose between 1 hour funding (HyperLiquid usually) and 8 hour funding (Binance)

APR: Underlying annualized funding rate

What makes it original

Whilst some predicted funding scripts exist, some aren't as accurate or have gaps in data. And seeing as funding values are generally missing from TV tickers, this gives traders accessibility to the script when they would have to use other platforms

Notes

Currently only compatible with symbols that have Binance USDT premium indices

Optimal accuracy is found on timeframes that are 4H or less. On higher timeframes, the accuracy drops off

Actual funding rates may differ

Inputs

Funding Period: Choose between "8 Hour" (standard Binance cycle) or "1 Hour" (divides the 8-hour rate by 8 for granular comparison)

Plot Type: Display as "Funding Rate" (percentage per interval) or "APR" (annualized rate calculated as 8-hour rate × 3 × 365)

Table: Toggle the information table showing current funding rate, premium, funding period, and APR in the top-right corner

Positive Colour: Sets the colour for positive funding rates where longs pay shorts (default: #00ffbb turquoise)

Negative Colour: Sets the colour for negative funding rates where shorts pay longs (default: red)

Table Background: Controls the background colour and transparency of the information table (default: transparent dark blue)

Table Text Colour: Sets the colour for all text labels in the information table (default: white)

Table Text Size: Controls font size with options from Tiny to Huge, with Small as the default balance of readability and space

TimeMapTimeMap is a visual price-reference indicator designed to help traders rapidly visualize how current price levels relate to significant historical closing prices. It overlays your chart with reference lines representing past weekly, monthly, quarterly (3-month), semi-annual (6-month), and annual closing prices. By clearly plotting these historical price references, TimeMap helps traders quickly gauge price position relative to historical market structure, aiding in the identification of trends, support/resistance levels, and potential reversals.

How it Works:

The indicator calculates the precise number of historical bars corresponding to weekly, monthly, quarterly, semi-annual, and annual intervals, dynamically adjusting according to your chart’s timeframe (intraday, daily, weekly, monthly) and chosen market type (Stocks US, Crypto, Forex, or Futures). Historical closing prices from these periods are plotted directly on your chart as horizontal reference lines.

For intraday traders, the script accurately calculates historical offsets considering regular and extended trading sessions (e.g., pre-market and after-hours sessions for US stocks), ensuring correct positioning of historical lines.

User-Configurable Inputs Explained in Detail:

Market Type:

Allows you to specify your trading instrument type, automatically adjusting calculations for:

- Stocks US (default): 390 minutes per regular session (780 minutes if extended hours enabled), 5 trading days/week.

- Crypto: 1440 minutes/day, 7 trading days/week.

- Forex: 1440 minutes/day, 5 trading days/week.

- Futures: 1320 minutes/day, 5 trading days/week.

Show Weekly Close:

When enabled, plots a line at the exact closing price from one week ago. Provides short-term context and helps identify recent price momentum.

Show Monthly Close:

When enabled, plots a line at the exact closing price from one month ago. Helpful for evaluating medium-term price positioning and monthly trend strength.

Show 3-Month Close:

When enabled, plots a line at the exact closing price from three months ago. Useful for assessing quarterly market shifts, intermediate trend changes, and broader market sentiment.

Show 6-Month Close:

When enabled, plots a line at the exact closing price from six months ago. Useful for identifying semi-annual trends, significant price pivots, and longer-term support/resistance levels.

Show 1-Year Close:

When enabled, plots a line at the exact closing price from one year ago. Excellent for assessing long-term market direction and key annual price levels.

Enable Smoothing:

Activates a Simple Moving Average (SMA) smoothing of historical reference lines, reducing volatility and providing clearer visual references. Recommended for traders preferring less volatile reference levels.

Smoothing Length:

Determines the number of bars used in calculating the SMA smoothing of historical lines. Higher values result in smoother but slightly delayed reference lines; lower values offer more immediate yet more volatile levels.

Use Extended Hours (Intraday Only):

When enabled (only applicable for Stocks US), it accounts for pre-market and after-hours trading sessions, providing accurate intraday historical line calculations based on extended sessions (typically 780 minutes/day total).

Important Notes and Compliance:

- This indicator does not provide trading signals, recommendations, or predictions. It serves purely as a visual analytical tool to supplement traders’ existing methods.

- Historical lines plotted are strictly based on past available price data; the indicator never accesses future data or data outside the scope of Pine Script’s standard capabilities.

- The script incorporates built-in logic to avoid runtime errors if insufficient historical data exists for a selected timeframe, ensuring robustness even with limited historical bars.

- TimeMap is original work developed exclusively by Julien Eche (@Julien_Eche). It does not reuse or replicate third-party or existing open-source scripts.

Recommended Best Practices:

- Use TimeMap as a complementary analytical reference, not as a standalone strategy or trade decision-making tool.

- Adapt displayed historical periods and smoothing settings based on your trading style and market approach.