Weekly Regime Filter - Trend + Momentum + Structure (MTF)A multi-timeframe weekly regime indicator that classifies market conditions into BULL , BEAR , or CHOP using three components: trend, momentum, and market structure.

Works on any timeframe while always referencing weekly data — no repainting.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🎯 WHAT IT DOES

Answers one question: What is the weekly regime?

• Trend — EMA hierarchy (Price > EMA Fast > EMA Slow)

• Momentum — DI+ vs DI- with optional ADX filter

• Structure — Break of Structure (BOS) and Change of Character (CHOCH)

BULL = All three bullish

BEAR = All three bearish

CHOP = Mixed signals

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

⚡ KEY FEATURES

• Multi-Timeframe (MTF) — View on 1H, 4H, Daily; regime stays consistent

• Auto-Detect Asset Type — Automatically applies optimized settings for Crypto, Stocks, Forex, Gold, Silver, Oil, Commodities

• BOS/CHOCH Labels — Visual market structure breaks on chart

• Live Status Panel — Shows regime, components, and active parameters

• Non-Repainting — Uses confirmed weekly closes only

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📊 ASSET PRESETS

• Crypto — EMA 50/200, ADX Off, Pivot 2

• Stocks/Indices — EMA 50/200, ADX >20, Pivot 3

• Forex — EMA 30/100, ADX >25, Pivot 2

• Gold — EMA 40/150, ADX >20, Pivot 3

• Silver — EMA 40/150, ADX >22, Pivot 3

• Oil — EMA 30/100, ADX >25, Pivot 2

• Commodities — EMA 40/120, ADX >20, Pivot 3

Select "Custom" to use your own values.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📈 HOW TO USE

For Swing Trading:

• Set chart to Daily

• Use Auto-Detect or select preset

• Long only when BULL, short only when BEAR

• Reduce size or avoid when CHOP

Structure Signals:

• CHOCH ↑ after bear regime = Early reversal signal

• CHOCH ↓ after bull regime = Tighten stops

• BOS in regime direction = Trend continuation

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🔔 ALERTS

• Regime → BULL

• Regime → BEAR

• CHOCH → Bull

• CHOCH → Bear

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

⚙️ SETTINGS

Preset: Auto-Detect, Crypto, Stocks, Forex, Gold, Silver, Oil, Commodities, Custom

Custom Settings (when Custom selected):

• EMA Fast/Slow lengths

• ADX Length & Threshold

• ADX Filter toggle

• Pivot Left/Right

Display:

• Plot Weekly EMAs

• Show BOS/CHOCH Labels

• Show Regime Background

• Background Opacity

• Show Status Label

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📝 NOTES

• Needs ~200 weeks of history for full calculation

• Weekly signals are slower by design — filters noise

• Not a standalone system — combine with entries and risk management

• When using presets, Custom input fields won't visually update (Pine limitation) — status label shows actual values

Search in scripts for "adx"

VIOP Scalping - OriginalVIOP Scalping – Original is a rule-based scalping strategy ported from an original C# logic set. It aims to trade only when trend direction, momentum, and trend strength align, then manages the position using fixed take-profit/stop-loss percentages with an optional trailing mechanism to protect gains during favorable moves.

This strategy is provided for educational and backtesting purposes only. It is not financial advice and does not guarantee profitability. Always test thoroughly before any live usage.

Core Concept

Follow the dominant WMA trend, confirm momentum with EMA separation, filter conditions with RSI + ADX, then exit using fixed TP/SL with trailing behavior after a defined profit threshold.

How the Strategy Works

Trend Direction is defined by WMA: above WMA = long bias, below WMA = short bias.

Momentum is measured via Fast EMA vs Slow EMA and the EMA difference.

Trend Strength is confirmed using ADX (must exceed a threshold).

RSI filters trades to avoid entering when momentum is likely overextended or weak.

A no-trade session blocks entries during a predefined time window (default 09:30–10:05).

Exit logic uses fixed percent TP/SL, with an optional trailing mechanism that activates after a profit threshold.

Inputs and Settings

Trend and Indicator Settings

Main Trend WMA: Determines directional bias (price above = long, price below = short).

Fast EMA / Slow EMA: Used to measure momentum and directional separation.

RSI Period: Filters entries based on RSI range constraints.

ADX Period: Measures trend strength (must exceed threshold to allow entries).

Threshold Settings

EMA Difference Threshold: Minimum EMA separation required to validate momentum.

ADX Threshold: Minimum ADX required to confirm trend strength.

RSI Long Ceiling: RSI must remain below this value for long entries.

RSI Short Floor: RSI must remain above this value for short entries.

Risk Management Settings

Take Profit %: Default TP distance in percent.

Strong Trend Take Profit %: Higher TP used when a “strong trend” condition is detected.

Stop Loss %: Fixed SL distance in percent.

Trailing Activation %: Profit threshold at which trailing starts.

Trailing Distance %: Trailing offset distance used once trailing is active.

Time Filter

No-Trade Hours: Default session is 09:30–10:05. During this window, the strategy does not open new trades.

Entry Logic

No-Trade Time Filter

If the current bar falls inside the no-trade session, entries are blocked.

Long Entry Conditions

Price is above the WMA trend line.

EMA difference is positive and greater than the EMA Difference Threshold.

EMA momentum is increasing (current EMA diff > previous EMA diff).

RSI is within the defined range (RSI > 48 and RSI < RSI Long Ceiling).

Close is higher than the previous close.

ADX is above the ADX Threshold.

Short Entry Conditions

Price is below the WMA trend line.

EMA difference is negative and lower than -EMA Difference Threshold.

Bearish momentum is increasing (current EMA diff < previous EMA diff).

RSI is within the defined range (RSI < 52 and RSI > RSI Short Floor).

Close is lower than the previous close.

ADX is above the ADX Threshold.

Strong Trend Logic (Dynamic TP Selection)

If price is far from the WMA (absolute distance > 20 points) AND EMA separation is strong (absolute EMA diff > 1.5 points), the strategy treats the environment as a strong trend.

In strong trend mode, the strategy uses “Strong Trend Take Profit %” instead of the default “Take Profit %”.

Exit Management (TP/SL + Trailing)

The strategy uses fixed percentage-based TP and SL levels.

Trailing logic is enabled via strategy.exit and activates only after price moves in profit by the defined Trailing Activation %.

Once activated, trailing follows price using the defined Trailing Distance % offset.

This is designed to secure partial gains during extended moves while still allowing room for continuation.

What You See on the Chart

WMA Trend Line (Main Trend Filter).

Fast EMA and Slow EMA (Momentum Confirmation).

Strategy entry/exit markers generated by TradingView.

Recommended Use

Scalping systems that rely on trend-following and momentum confirmation.

Markets where ADX filtering helps avoid choppy conditions.

Traders who want a simple, parameter-driven TP/SL system with trailing after confirmation.

Important Notes

The no-trade session depends on your chart/session settings. Ensure your symbol/session configuration matches your intended market hours.

Percent-based exits scale with price; results will vary across instruments and volatility regimes.

Always validate behavior using bar replay, forward testing, and realistic commission/slippage assumptions.

OpenAI Signal Generator - Enhanced Accuracy# AI-Powered Trading Signal Generator Guide

## Overview

This is an advanced trading signal generator that combines multiple technical indicators using AI-enhanced logic to generate high-accuracy trading signals. The indicator uses a sophisticated combination of RSI, MACD, Bollinger Bands, EMAs, ADX, and volume analysis to provide reliable buy/sell signals with comprehensive market analysis.

## Key Features

### 1. Multi-Indicator Analysis

- **RSI (Relative Strength Index)**

- Length: 14 periods (default)

- Overbought: 70 (default)

- Oversold: 30 (default)

- Used for identifying overbought/oversold conditions

- **MACD (Moving Average Convergence Divergence)**

- Fast Length: 12 (default)

- Slow Length: 26 (default)

- Signal Length: 9 (default)

- Identifies trend direction and momentum

- **Bollinger Bands**

- Length: 20 periods (default)

- Multiplier: 2.0 (default)

- Measures volatility and potential reversal points

- **EMAs (Exponential Moving Averages)**

- Fast EMA: 9 periods (default)

- Slow EMA: 21 periods (default)

- Used for trend confirmation

- **ADX (Average Directional Index)**

- Length: 14 periods (default)

- Threshold: 25 (default)

- Measures trend strength

- **Volume Analysis**

- MA Length: 20 periods (default)

- Threshold: 1.5x average (default)

- Confirms signal strength

### 2. Advanced Features

- **Customizable Signal Frequency**

- Daily

- Weekly

- 4-Hour

- Hourly

- On Every Close

- **Enhanced Filtering**

- EMA crossover confirmation

- ADX trend strength filter

- Volume confirmation

- ATR-based volatility filter

- **Comprehensive Alert System**

- JSON-formatted alerts

- Detailed technical analysis

- Multiple timeframe analysis

- Customizable alert frequency

## How to Use

### 1. Initial Setup

1. Open TradingView and create a new chart

2. Select your preferred trading pair

3. Choose an appropriate timeframe

4. Apply the indicator to your chart

### 2. Configuration

#### Basic Settings

- **Signal Frequency**: Choose how often signals are generated

- Daily: Signals at the start of each day

- Weekly: Signals at the start of each week

- 4-Hour: Signals every 4 hours

- Hourly: Signals every hour

- On Every Close: Signals on every candle close

- **Enable Signals**: Toggle signal generation on/off

- **Include Volume**: Toggle volume analysis on/off

#### Technical Parameters

##### RSI Settings

- Adjust `rsi_length` (default: 14)

- Modify `rsi_overbought` (default: 70)

- Modify `rsi_oversold` (default: 30)

##### EMA Settings

- Fast EMA Length (default: 9)

- Slow EMA Length (default: 21)

##### MACD Settings

- Fast Length (default: 12)

- Slow Length (default: 26)

- Signal Length (default: 9)

##### Bollinger Bands

- Length (default: 20)

- Multiplier (default: 2.0)

##### Enhanced Filters

- ADX Length (default: 14)

- ADX Threshold (default: 25)

- Volume MA Length (default: 20)

- Volume Threshold (default: 1.5)

- ATR Length (default: 14)

- ATR Multiplier (default: 1.5)

### 3. Signal Interpretation

#### Buy Signal Requirements

1. RSI crosses above oversold level (30)

2. Price below lower Bollinger Band

3. MACD histogram increasing

4. Fast EMA above Slow EMA

5. ADX above threshold (25)

6. Volume above threshold (if enabled)

7. Market volatility check (if enabled)

#### Sell Signal Requirements

1. RSI crosses below overbought level (70)

2. Price above upper Bollinger Band

3. MACD histogram decreasing

4. Fast EMA below Slow EMA

5. ADX above threshold (25)

6. Volume above threshold (if enabled)

7. Market volatility check (if enabled)

### 4. Visual Indicators

#### Chart Elements

- **Moving Averages**

- SMA (Blue line)

- Fast EMA (Yellow line)

- Slow EMA (Purple line)

- **Bollinger Bands**

- Upper Band (Green line)

- Middle Band (Orange line)

- Lower Band (Green line)

- **Signal Markers**

- Buy Signals: Green triangles below bars

- Sell Signals: Red triangles above bars

- **Background Colors**

- Light green: Buy signal period

- Light red: Sell signal period

### 5. Alert System

#### Alert Types

1. **Signal Alerts**

- Generated when buy/sell conditions are met

- Includes comprehensive technical analysis

- JSON-formatted for easy integration

2. **Frequency-Based Alerts**

- Daily/Weekly/4-Hour/Hourly/Every Close

- Includes current market conditions

- Technical indicator values

#### Alert Message Format

```json

{

"symbol": "TICKER",

"side": "BUY/SELL/NONE",

"rsi": "value",

"macd": "value",

"signal": "value",

"adx": "value",

"bb_upper": "value",

"bb_middle": "value",

"bb_lower": "value",

"ema_fast": "value",

"ema_slow": "value",

"volume": "value",

"vol_ma": "value",

"atr": "value",

"leverage": 10,

"stop_loss_percent": 2,

"take_profit_percent": 5

}

```

## Best Practices

### 1. Signal Confirmation

- Wait for multiple confirmations

- Consider market conditions

- Check volume confirmation

- Verify trend strength with ADX

### 2. Risk Management

- Use appropriate position sizing

- Implement stop losses (default 2%)

- Set take profit levels (default 5%)

- Monitor market volatility

### 3. Optimization

- Adjust parameters based on:

- Trading pair volatility

- Market conditions

- Timeframe

- Trading style

### 4. Common Mistakes to Avoid

1. Trading without volume confirmation

2. Ignoring ADX trend strength

3. Trading against the trend

4. Not considering market volatility

5. Overtrading on weak signals

## Performance Monitoring

Regularly review:

1. Signal accuracy

2. Win rate

3. Average profit per trade

4. False signal frequency

5. Performance in different market conditions

## Disclaimer

This indicator is for educational purposes only. Past performance is not indicative of future results. Always use proper risk management and trade responsibly. Trading involves significant risk of loss and is not suitable for all investors.

Advanced Candlestick Pattern DetectorWhat Does This Indicator Do?

This indicator looks at the way price moves in the market using candlesticks (those red and green bars you see on charts). It tries to find special patterns like Bullish Engulfing, Hammer, Doji, and others. When one of these patterns shows up, the indicator checks a bunch of filters to decide if the pattern is strong enough to be a signal to buy or sell.

The Main Parts of the Indicator

1. Candlestick Pattern Detection

Bullish Engulfing:

Imagine you see a small down candle (red) and then a big up candle (green) that completely “covers” the red one. That’s a bullish engulfing pattern. It can signal that buyers are taking over.

Bearish Engulfing:

The opposite of bullish engulfing. A small up candle (green) is followed by a big down candle (red) that covers the previous candle. This suggests sellers might be in control.

Hammer & Shooting Star:

Hammer: A candle with a very short body and a long shadow at the bottom. It shows that buyers stepped in after a drop.

Shooting Star:

Similar to the hammer but with a long shadow on top. It can indicate that sellers are starting to push the price down.

Doji:

A candle with almost no body. This means the opening and closing prices are very close. It shows indecision in the market.

Harami Patterns (Bullish & Bearish):

These are two-candle patterns where the second candle is completely inside the body of the first candle. They signal that the previous trend might be about to change.

Morning Star & Evening Star:

These are three-candle patterns.

Morning Star:

Often seen at the bottom of a downtrend, it can signal a reversal to an uptrend.

Evening Star:

Seen at the top of an uptrend, it can signal that the price may soon go down.

2. Filters: Making the Signals Smarter

The indicator doesn’t just rely on patterns. It uses several “filters” to decide if a pattern is strong enough to trade on. Here’s what each filter does:

a. Adaptive Thresholds (ATR-Based)

What It Is:

The indicator uses something called ATR (Average True Range) to see how much the price is moving (volatility).

How It Works:

Instead of using fixed numbers to decide if a candle is a Hammer or a Doji, it adjusts these numbers based on current market activity.

User Settings:

Use Adaptive Thresholds: Turn this on to let the indicator adjust automatically.

Body Factor, Shadow Factor, Doji Factor: These numbers are multipliers that decide how small or big the body and shadows of the candle should be. You can change them if you want the indicator to be more or less sensitive.

b. Volume Filter

What It Is:

Volume shows how many trades are happening.

How It Works:

The filter checks if the current volume is higher than the average volume (multiplied by a set factor). This helps ensure that the signal isn’t coming from a very quiet market.

User Settings:

Use Volume Filter: Turn this on if you want to ignore signals when there’s not much trading.

Volume MA Period & Volume Multiplier: These settings determine what “normal” volume is and how much higher the current volume must be to count.

c. Multi-Timeframe Trend Filter

What It Is:

This filter looks at a bigger picture by using a moving average (MA) from a higher timeframe (for example, daily charts).

How It Works:

For a bullish (buy) signal, the indicator checks if the price is above this MA.

For a bearish (sell) signal, the price must be below the MA.

User Settings:

Use Multi-Timeframe Trend Filter: Enable or disable this filter.

Higher Timeframe for Trend: Choose which timeframe (like Daily) to use.

Trend MA Type (SMA or EMA) & Trend MA Period: Choose the type of moving average and how many candles to average.

d. Additional Trend Filters (ADX & RSI)

ADX Filter:

What It Is:

ADX stands for Average Directional Index. It measures how strong a trend is.

How It Works:

If the ADX is above a certain threshold, it means the trend is strong.

User Setting:

ADX Threshold: Set the minimum strength the trend should have.

RSI Filter:

What It Is:

RSI (Relative Strength Index) tells you if the price is overbought (too high) or oversold (too low).

How It Works:

For a buy signal, RSI should be low (under a set threshold).

For a sell signal, RSI should be high (above a set threshold).

User Settings:

RSI Buy Threshold & RSI Sell Threshold: These set the levels for buying or selling.

3. How the Final Signal Is Determined

For a signal (buy or sell) to be generated, the indicator first checks if one of the candlestick patterns is present. Then it goes through all these filters (trend, volume, ADX, RSI). Only if everything is in line will it show:

A BUY signal when all bullish conditions are met.

A SELL signal when all bearish conditions are met.

4. Visual Elements on the Chart

Trend MA Line:

A blue line is drawn on your chart showing the moving average from the higher timeframe (if you enable the trend filter). This helps you see the overall direction of the market.

Labels on the Chart:

When a signal is detected, you’ll see:

A BUY label below the candle (green).

A SELL label above the candle (red).

Background Colors:

The chart background might change slightly (green for bullish and red for bearish) to give you a quick visual cue.

Histogram:

At the bottom, there is a histogram that shows +1 for bullish signals, -1 for bearish signals, and 0 when there’s no clear signal.

5. Alerts

Alerts are built into the indicator so you can get a notification when a signal appears. The alert messages are fixed strings, meaning they always say something like “BUY signal on at price .” You can set up these alerts in TradingView to be notified via sound, email, or pop-up.

How to Use and Adjust the Filters

Deciding on Patterns:

You can choose which candlestick patterns you want to detect by toggling the options (e.g., Bullish Engulfing, Hammer, etc.).

Adjusting Adaptive Thresholds:

If you feel that the indicator is too sensitive (or not sensitive enough) during volatile times, adjust the Body Factor, Shadow Factor, and Doji Factor. These change how the indicator recognizes different candle shapes based on market movement.

Volume Filter Settings:

Use Volume Filter:

Turn this on if you want to ignore signals when there’s not enough trading activity.

Adjust the Volume MA Period and Volume Multiplier to change what “normal” volume is for your chart.

Multi-Timeframe Trend Filter Settings:

Choose a higher timeframe (like Daily) to see the bigger picture trend. Select the type of moving average (SMA or EMA) and its period. This filter ensures you only trade in the direction of the overall trend.

ADX & RSI Filters:

ADX:

Adjust the ADX Threshold if you want to change the minimum strength of the trend needed for a signal.

RSI:

Set the RSI Buy Threshold (for oversold conditions) and RSI Sell Threshold (for overbought conditions) to refine when a signal is valid.

Summary

This indicator is like having a smart assistant that not only looks for specific price patterns (candlesticks) but also checks if the overall market conditions are right using several filters. By combining:

Pattern Detection

Adaptive thresholds (based on ATR)

Volume Checks

Multi-Timeframe Trend Analysis

Additional Trend Strength and Overbought/Oversold Indicators (ADX & RSI)

...it helps you decide if it might be a good time to buy or sell. You can customize each part to fit your trading style, and with the built-in alerts, you can be notified when everything lines up.

Feel free to adjust the settings to see how each filter changes the signals on your chart. Experimenting with these will help you learn how the market behaves and how you can best use the indicator for your own strategy!

Crypto Scanner v4This guide explains a version 6 Pine Script that scans a user-provided list of cryptocurrency tokens to identify high probability tradable opportunities using several technical indicators. The script combines trend, momentum, and volume-based analyses to generate potential buying or selling signals, and it displays the results in a neatly formatted table with alerts for trading setups. Below is a detailed walkthrough of the script’s design, how traders can interpret its outputs, and recommendations for optimizing indicator inputs across different timeframes.

## Overview and Key Components

The script is designed to help traders assess multiple tokens by calculating several indicators for each one. The key components include:

- **Input Settings:**

- A comma-separated list of symbols to scan.

- Adjustable parameters for technical indicators such as ADX, RSI, MFI, and a custom Wave Trend indicator.

- Options to enable alerts and set update frequencies.

- **Indicator Calculations:**

- **ADX (Average Directional Index):** Measures trend strength. A value above the provided threshold indicates a strong trend, which is essential for validating momentum before entering a trade.

- **RSI (Relative Strength Index):** Helps determine overbought or oversold conditions. When the RSI is below the oversold level, it may present a buying opportunity, while an overbought condition (not explicitly part of this setup) could suggest selling.

- **MFI (Money Flow Index):** Similar in concept to RSI but incorporates volume, thus assessing buying and selling pressure. Values below the designated oversold threshold indicate potential undervaluation.

- **Wave Trend:** A custom indicator that calculates two components (WT1 and WT2); a crossover where WT1 moves from below to above WT2 (particularly near oversold levels) may signal a reversal and a potential entry point.

- **Scanning and Trading Zone:**

- The script identifies a *bullish setup* when the following conditions are met for a token:

- ADX exceeds the threshold (strong trend).

- Both RSI and MFI are below their oversold levels (indicating potential buying opportunities).

- A Wave Trend crossover confirms near-term reversal dynamics.

- A *trading zone* condition is also defined by specific ranges for ADX, RSI, MFI, and a limited difference between WT1 and WT2. This zone suggests that the token might be in a consolidation phase where even small moves may be significant.

- **Alerts and Table Reporting:**

- A table is generated, with each row corresponding to a token. The table contains columns for the symbol, ADX, RSI, MFI, WT1, WT2, and the trading zone status.

- Visual cues—such as different background colors—highlight tokens with a bullish setup or that are within the trading zone.

- Alerts are issued based on the detection of a bullish setup or entry into a trading zone. These alerts are limited per bar to avoid flooding the trader with notifications.

## How to Interpret the Indicator Outputs

Traders should use the indicator values as guidance, verifying them against their own analysis before making any trading decision. Here’s how to assess each output:

- **ADX:**

- **High values (above threshold):** Indicate strong trends. If other indicators confirm an oversold condition, a trader may consider a long position for a corrective reversal.

- **Low values:** Suggest that the market is not trending strongly, and caution should be taken when considering entry.

- **RSI and MFI:**

- **Below oversold levels:** These conditions are traditionally seen as signals that an asset is undervalued, potentially triggering a bounce.

- **Above typical resistance levels (not explicitly used here):** Would normally caution a trader against entering a long position.

- **Wave Trend (WT1 and WT2):**

- A crossover where WT1 moves upward above WT2 in an oversold environment can signal the beginning of a recovery or reversal, thereby reinforcing buy signals.

- **Trading Zone:**

- Being “in zone” means that the asset’s current values for ADX, RSI, MFI, and the closeness of the Wave Trend lines indicate a period of consolidation. This scenario might be suitable for both short-term scalping or as an early exit indicator, depending on further market analysis.

## Timeframe Optimization Input Table

Traders can optimize indicator inputs depending on the timeframe they use. The following table provides a set of recommended input values for various timeframes. These values are suggestions and should be adjusted based on market conditions and individual trading styles.

Timeframe ADX RSI MFI ADX RSI MFI WT Channel WT Average

5-min 10 10 10 20 30 20 7 15

15-min 12 12 12 22 30 20 9 18

1-hour 14 14 14 25 30 20 10 21

4-hour 16 16 16 27 30 20 12 24

1-day 18 18 18 30 30 20 14 28

Adjust these parameters directly in the script’s input settings to match the selected timeframe. For shorter timeframes (e.g., 5-min or 15-min), the shorter lengths help filter high-frequency noise. For longer timeframes (e.g., 1-day), longer input values may reduce false signals and capture more significant trends.

## Best Practices and Usage Tips

- **Token Limit:**

- Limit the number of tokens scanned to 10 per query line. If you need to scan more tokens, initiate a new query line. This helps manage screen real estate and ensures the table remains legible.

- **Confirming Signals:**

- Use this script as a starting point for identifying high potential trades. Each indicator’s output should be used to confirm your trading decision. Always cross-reference with additional technical analysis tools or market context.

- **Regular Review:**

- Since the script updates the table every few bars (as defined by the update frequency), review the table and alerts regularly. Market conditions change rapidly, so timely decisions are crucial.

## Conclusion

This Pine Script provides a comprehensive approach for scanning multiple cryptocurrencies using a combination of trend strength (ADX), momentum (RSI and MFI), and reversal signals (Wave Trend). By using the provided recommendation table for different timeframes and limiting the tokens to 20 per query line (with a maximum of four query lines), traders can streamline their scanning process and more effectively identify high probability tradable tokens. Ultimately, the outputs should be critically evaluated and combined with additional market research before executing any trades.

Johnny's Machine Learning Moving Average (MLMA) w/ Trend Alerts📖 Overview

Johnny's Machine Learning Moving Average (MLMA) w/ Trend Alerts is a powerful adaptive moving average indicator designed to capture market trends dynamically. Unlike traditional moving averages (e.g., SMA, EMA, WMA), this indicator incorporates volatility-based trend detection, Bollinger Bands, ADX, and RSI, offering a comprehensive view of market conditions.

The MLMA is "machine learning-inspired" because it adapts dynamically to market conditions using ATR-based windowing and integrates multiple trend strength indicators (ADX, RSI, and volatility bands) to provide an intelligent moving average calculation that learns from recent price action rather than being static.

🛠 How It Works

1️⃣ Adaptive Moving Average Selection

The MLMA automatically selects one of four different moving averages:

📊 EMA (Exponential Moving Average) – Reacts quickly to price changes.

🔵 HMA (Hull Moving Average) – Smooth and fast, reducing lag.

🟡 WMA (Weighted Moving Average) – Gives recent prices more importance.

🔴 VWAP (Volume Weighted Average Price) – Accounts for volume impact.

The user can select which moving average type to use, making the indicator customizable based on their strategy.

2️⃣ Dynamic Trend Detection

ATR-Based Adaptive Window 📏

The Average True Range (ATR) determines the window size dynamically.

When volatility is high, the moving average window expands, making the MLMA more stable.

When volatility is low, the window shrinks, making the MLMA more responsive.

Trend Strength Filters 📊

ADX (Average Directional Index) > 25 → Indicates a strong trend.

RSI (Relative Strength Index) > 70 or < 30 → Identifies overbought/oversold conditions.

Price Position Relative to Upper/Lower Bands → Determines bullish vs. bearish momentum.

3️⃣ Volatility Bands & Dynamic Support/Resistance

Bollinger Bands (BB) 📉

Uses standard deviation-based bands around the MLMA to detect overbought and oversold zones.

Upper Band = Resistance, Lower Band = Support.

Helps traders identify breakout potential.

Adaptive Trend Bands 🔵🔴

The MLMA has built-in trend envelopes.

When price breaks the upper band, bullish momentum is confirmed.

When price breaks the lower band, bearish momentum is confirmed.

4️⃣ Visual Enhancements

Dynamic Gradient Fills 🌈

The trend strength (ADX-based) determines the gradient intensity.

Stronger trends = More vivid colors.

Weaker trends = Lighter colors.

Trend Reversal Arrows 🔄

🔼 Green Up Arrow: Bullish reversal signal.

🔽 Red Down Arrow: Bearish reversal signal.

Trend Table Overlay 🖥

Displays ADX, RSI, and Trend State dynamically on the chart.

📢 Trading Signals & How to Use It

1️⃣ Bullish Signals 📈

✅ Conditions for a Long (Buy) Trade:

The MLMA crosses above the lower band.

The ADX is above 25 (confirming trend strength).

RSI is above 55, indicating positive momentum.

Green trend reversal arrow appears (confirmation of a bullish reversal).

🔹 How to Trade It:

Enter a long trade when the MLMA turns bullish.

Set stop-loss below the lower Bollinger Band.

Target previous resistance levels or use the upper band as take-profit.

2️⃣ Bearish Signals 📉

✅ Conditions for a Short (Sell) Trade:

The MLMA crosses below the upper band.

The ADX is above 25 (confirming trend strength).

RSI is below 45, indicating bearish pressure.

Red trend reversal arrow appears (confirmation of a bearish reversal).

🔹 How to Trade It:

Enter a short trade when the MLMA turns bearish.

Set stop-loss above the upper Bollinger Band.

Target the lower band as take-profit.

💡 What Makes This a Machine Learning Moving Average?

📍 1️⃣ Adaptive & Self-Tuning

Unlike static moving averages that rely on fixed parameters, this MLMA automatically adjusts its sensitivity to market conditions using:

ATR-based dynamic windowing 📏 (Expands/contracts based on volatility).

Adaptive smoothing using EMA, HMA, WMA, or VWAP 📊.

Multi-indicator confirmation (ADX, RSI, Volatility Bands) 🏆.

📍 2️⃣ Intelligent Trend Confirmation

The MLMA "learns" from recent price movements instead of blindly following a fixed-length average.

It incorporates ADX & RSI trend filtering to reduce noise & false signals.

📍 3️⃣ Dynamic Color-Coding for Trend Strength

Strong trends trigger more vivid colors, mimicking confidence levels in machine learning models.

Weaker trends appear faded, suggesting uncertainty.

🎯 Why Use the MLMA?

✅ Pros

✔ Combines multiple trend indicators (MA, ADX, RSI, BB).

✔ Automatically adjusts to market conditions.

✔ Filters out weak trends, making it more reliable.

✔ Visually intuitive (gradient colors & reversal arrows).

✔ Works across all timeframes and assets.

⚠️ Cons

❌ Not a standalone strategy → Best used with volume confirmation or candlestick analysis.

❌ Can lag slightly in fast-moving markets (due to smoothing).

Strength Measurement -HTStrength Measurement -HT

This indicator provides a comprehensive view of trend strength by calculating the average ADX (Average Directional Index) across multiple timeframes. It helps traders identify strong trends, potential reversals, and confirm signals from other indicators.

Key Features:

Multi-Timeframe Analysis: Analyze trend strength across different timeframes. Choose which timeframes to include in the calculation (5 min, 15 min, 30 min, 1 hour, 4 hour).

Customizable ADX Parameters: Adjust the ADX smoothing (adxlen) and DI length (dilen) parameters to fine-tune the indicator to your preferred settings.

Smoothed Average ADX: The average ADX is smoothed using a Simple Moving Average to reduce noise and provide a clearer picture of the overall trend.

Color-Coded Visualization: The histogram clearly indicates trend direction and strength:

Green: Uptrend

Red: Downtrend

Darker shades: Stronger trend

Lighter shades: Weaker trend

Reference Levels: Includes horizontal lines at 25, 50, and 75 to provide benchmarks for trend strength classification.

Alerts: Set alerts for strong trend up (ADX crossing above 50) and weakening trend (ADX crossing below 25).

How to Use:

Select Timeframes: Choose the timeframes you want to include in the average ADX calculation.

Adjust ADX Parameters: Fine-tune the adxlen and dilen values based on your trading style and the timeframe of the chart.

Identify Strong Trends: Look for histogram bars with darker green or red colors, indicating a strong trend.

Spot Potential Reversals: Watch for changes in histogram color and height, which may suggest a weakening trend or a potential reversal.

Combine with Other Indicators: Use this indicator with other technical analysis tools to confirm trading signals.

Note: This indicator is based on the ADX, which is a lagging indicator.

DMI Delta by 0xjcfOverview

This indicator integrates the Directional Movement Index (DMI), Average Directional Index (ADX), and volume analysis into an Oscillator designed to help traders identify divergence-based trading signals. Unlike typical volume or momentum indicators, this combination provides insight into directional momentum and volume intensity, allowing traders to make well-informed decisions based on multiple facets of market behavior.

Purpose and How Components Work Together

By combining DMI and ADX with volume analysis, this indicator helps traders detect when momentum diverges from price action—a common precursor to potential reversals or significant moves. The ADX filter enhances this by distinguishing trending from range-bound conditions, while volume analysis highlights moments of extreme sentiment, such as solid buying or selling. Together, these elements provide traders with a comprehensive view of market strength, directional bias, and volume surges, which help filter out weaker signals.

Key Features

DMI Delta and Oscillator: The DMI indicator measures directional movement by comparing DI+ and DI- values. This difference (DMI Delta) is calculated and displayed as a histogram, visualizing changes in directional bias. When combined with ADX filtering, this histogram helps traders gauge the strength of momentum and spot directional shifts early. For instance, a rising histogram in a bearish price trend might signal a potential bullish reversal.

Volume Analysis with Extremes: Volume is monitored to reveal when market participation is unusually high, using a customizable multiplier to highlight significant volume spikes. These extreme levels are color-coded directly on the histogram, providing visual cues on whether buying or selling interest is particularly strong. Volume analysis adds depth to the directional insights from DMI, allowing traders to differentiate between regular and powerful moves.

ADX Trending Filter: The ADX component filters trends by measuring the overall strength of a price move, with a default threshold of 25. When ADX is above this level, it suggests that the market is trending strongly, making the DMI Delta readings more reliable. Below this threshold, the market is likely range-bound, cautioning traders that signals might not have as much follow-through.

Using the Indicator in Divergence Strategies

This indicator excels in divergence strategies by highlighting moments when price action diverges from directional momentum. Here’s how it aids in decision-making:

Bullish Divergence: If the price is falling to new lows while the DMI Delta histogram rises, it can indicate weakening bearish momentum and signal a potential price reversal to the upside.

Bearish Divergence: Conversely, if prices are climbing but the DMI Delta histogram falls, it may point to waning bullish momentum, suggesting a bearish reversal.

Visual Cues and Customization

The color-coded output enhances usability:

Bright Green/Red: Extreme volume with strong bullish or bearish signals, often at points of high potential for trend continuation or reversal.

Green/Red Shades: These shades reflect trending conditions (bullish or bearish) based on ADX, factoring in volume. Green signals a bullish trend, and red is a bearish trend.

Blue/Orange Shades: Indicates non-trending or weaker conditions, suggesting a more cautious approach in range-bound markets.

Customizable for Diverse Trading Styles

This indicator allows users to adjust settings like the ADX threshold and volume multiplier to optimize performance for various timeframes and strategies. Whether a trader prefers swing trading or intraday scalping, these parameters enable fine-tuning to enhance signal reliability across different market contexts.

Practical Usage Tips

Entry and Exit Signals: Use this indicator in conjunction with price action. Divergences between the price and DMI Delta histogram can reinforce entry or exit decisions.

Adjust Thresholds: Based on backtesting, customize the ADX Trending Threshold and Volume Multiplier to ensure optimal performance on different timeframes or trading styles.

In summary, this indicator is tailored for traders seeking a multi-dimensional approach to market analysis. It blends momentum, trend strength, and volume insights to support divergence-based strategies, helping traders confidently make informed decisions. Remember to validate signals through backtesting and use it alongside price action for the best results.

Previous Day High Low Strategy only for LongWelcome to the "Previous Day High Low Strategy only for Long"!.

This strategy aims to identify potential long trading opportunities based on the previous day's high and low prices, along with certain market strength conditions.

Key Features:

Entry Conditions: The strategy triggers a long position when the current day's closing price crosses above the previous day's high or low.

Market Strength Filter: The strategy incorporates a market strength filter using the Average Directional Index (ADX). It only takes long positions when the ADX value is above a specific threshold and when there is a predominance of upward movement.

Trade Timing: The strategy operates within a specified trade window, starting at 09:30 and ending at 15:10. Positions are closed at 15:15 if still active.

Risk Management: The strategy employs dynamic stop-loss and profit-taking levels based on a user-defined Max Profit value. It has three profit targets (T1, T2, T3) and a stop-loss level to manage risk effectively.

Rules:

Ensure that the strategy idea is clearly understandable. Provide an easy-to-read title and a thoughtful description explaining the reasoning behind the strategy.

All content should be ad-free. Avoid any form of promotion, advertising, or solicitation.

No fundraising requests or money solicitation is allowed on TradingView.

Publish in the same language as the TradingView subdomain you're on, except for script titles, which must be in English.

Don't plagiarize. Create and share only unique content, and always give credit when using someone else's work.

Be respectful, kind, and constructive when engaging with others.

Zero tolerance for contentious political discourse, defamatory, threatening, or discriminatory remarks.

Avoid sharing harmful, misleading, or inappropriate content.

Respect the moderators' work and address complaints privately.

Use only your original account and avoid creating duplicate or fake accounts.

Do not attempt to manipulate the reputation system or engage in like-for-like schemes.

Explanation of how the strategy works

1. Previous Day's High and Low (HH, LL):

In this strategy, we start by obtaining the high and low prices of the previous day (not the current day) using the request.security function. This function allows us to access historical data for a specific time frame. The high and low prices are stored in the variables HH and LL, respectively.

2. Entry Conditions:

The strategy uses two conditions to trigger a long position:

Condition 1 (Long Condition 1): If the closing price of the current day crosses above the previous day's high (HH), it generates a long signal. This is achieved using the ta.crossover function, which detects when a crossover occurs.

Condition 2 (Long Condition 2): Similarly, if the closing price of the current day crosses above the previous day's low (LL), it also generates a long signal.

Combined Condition: To take long positions, the strategy combines both long conditions using the logical OR operator (or). This means that if either of the two conditions is met, a long position will be initiated.

3. Market Strength Filter:

The strategy also includes a filter based on the Average Directional Index (ADX) to gauge the market's strength before taking long positions. The ADX measures the strength of a trend in the market. The higher the ADX value, the stronger the trend.

Calculation of ADX: The ADX is calculated using the adx function, which takes two parameters: LWdilength (DMI Length) and LWadxlength (ADX period).

Strength Condition (strength_up): The strategy requires that the ADX value should be above a threshold (11 in this case) and that there is a predominance of upward movement (up > down) before initiating a long position. The LWADX value is multiplied by 2.5 and compared to the highest value of LWADX from the last 4 periods using ta.highest(LWADX , 4). If these conditions are met, the variable strength_up is set to true.

Combined Condition: The strength_up condition is then combined with the long conditions using the logical AND operator (and). This means that the strategy will only take a long position if both the long conditions and the market strength condition are met.

4. Trade Timing:

The strategy sets a specific trade window between 09:30 and 15:10. It will only execute trades within this time frame (TradeTime).

5. Risk Management:

The strategy implements dynamic stop-loss (SL) and profit-taking levels (T1, T2, T3) based on a user-defined Max Profit value. The stop-loss is set as a percentage of the Max Profit value. As the position moves in favor of the trader, the profit targets are adjusted accordingly.

6. Position Management:

The strategy uses the strategy.entry function to enter long positions based on the combined entry conditions. Once a position is open, the script uses strategy.exit to define the exit condition when either the profit target or stop-loss level is hit. The strategy.close function is used to close any open position at the end of the trade window (15:15).

7. Plotting:

The strategy uses the plot function to visualize the previous day's high and low prices, as well as the stop-loss (SL) and profit-taking (T1, T2, T3) levels on the chart.

Overall, the "Previous Day High Low Strategy only for Long" aims to identify potential long trading opportunities based on the previous day's price action and market strength conditions. However, as with any trading strategy, it's essential to thoroughly test it and consider risk management before applying it to real-world trading scenarios.

Disclaimer:

The information presented by this strategy is for educational purposes only and should not be considered as investment advice. The strategy is not designed for qualified investors. Always conduct your own research and consult with a financial advisor before making any trading decisions.

Remember, the success of any trading strategy depends on various factors, including market conditions, risk management, and individual trading skills. Past performance is not indicative of future results.

Trend Strength Matrix [JOAT]Trend Strength Matrix — Multi-Timeframe Confluence Analysis System

This indicator addresses a specific analytical challenge: how to efficiently compare multiple technical measurements across different timeframes while accounting for their varying scales and interpretations. Rather than managing separate indicator windows with different scales, this tool normalizes four distinct analytical approaches to a common -1 to +1 scale and presents them in a unified matrix format.

Why This Combination Adds Value

The core problem this indicator solves is analytical fragmentation. Traders often use multiple indicators but struggle with:

1. **Scale Inconsistency**: RSI ranges 0-100, MACD has no fixed range, ADX ranges 0-100 but measures strength not direction

2. **Timeframe Coordination**: Checking multiple timeframes requires switching between charts or cramming multiple indicators

3. **Cognitive Load**: Processing different indicator types simultaneously creates mental overhead

4. **Confluence Assessment**: Determining when multiple approaches agree requires manual comparison

This indicator specifically addresses these issues by creating a standardized analytical framework where different measurement approaches can be directly compared both within and across timeframes.

Originality and Technical Innovation

While the individual components (RSI, MACD, ADX, Moving Average) are standard, the originality lies in:

1. **Unified Normalization System**: Each component is mathematically transformed to a -1 to +1 scale using component-specific normalization that preserves the indicator's core characteristics

2. **Multi-Timeframe Weighting Algorithm**: Higher timeframes receive proportionally more weight (40% current, 25% next, 20% third, 15% fourth) based on the principle that longer timeframes provide more significant context

3. **Real-Time Confluence Scoring**: The composite calculation provides an instant assessment of how much the different analytical approaches agree

4. **Adaptive Visual Encoding**: The heatmap format allows immediate pattern recognition of agreement/disagreement across both indicators and timeframes

How the Components Work Together

Each component measures a different aspect of market behavior, and their combination provides a more complete analytical picture:

**Momentum Component (RSI-based)**: Measures the velocity of price changes by comparing average gains to losses

**Trend Component (MACD-based)**: Measures the relationship between fast and slow moving averages, indicating trend acceleration/deceleration

**Strength Component (ADX-based)**: Measures trend strength regardless of direction, then applies directional bias

**Position Component (MA-based)**: Measures price position relative to a reference average

The mathematical relationship between these components creates a comprehensive view:

- When all four agree (similar colors), it suggests multiple analytical approaches are aligned

- When they disagree (mixed colors), it highlights analytical uncertainty or transition periods

- The composite score quantifies the degree of agreement numerically

Detailed Component Analysis

**1. Momentum Oscillator Component**

This component transforms RSI into a centered oscillator by subtracting 50 and dividing by 50, creating a -1 to +1 range where 0 represents equilibrium between buying and selling pressure.

// Momentum calculation normalized to -1 to +1 scale

float rsi = ta.rsi(close, rsiLength)

float rsiScore = (rsi - 50) / 50

// Result: 0 at equilibrium, +1 at extreme overbought, -1 at extreme oversold

**2. Moving Average Convergence Component**

MACD is normalized by its own volatility (standard deviation) to create a bounded oscillator. This prevents the unbounded nature of MACD from dominating the composite calculation.

// MACD normalized by its historical volatility

= ta.macd(close, macdFast, macdSlow, macdSignal)

float macdStdev = ta.stdev(macdLine, 100)

float macdScore = macdStdev != 0 ? math.max(-1, math.min(1, macdLine / (macdStdev * 2))) : 0

**3. Directional Movement Component**

This combines ADX (strength) with directional movement (+DI vs -DI) to create a directional strength measurement. ADX alone shows strength but not direction; this component adds directional context.

// ADX-based directional strength

= calcADX(adxLength)

float adxStrength = math.min(adx / 50, 1) // Normalize ADX to 0-1

float adxDirection = plusDI > minusDI ? 1 : -1 // Direction bias

float adxScore = adxStrength * adxDirection // Combine strength and direction

**4. Price Position Component**

This measures price deviation from a moving average, weighted by the magnitude of deviation to distinguish between minor and significant displacements.

// Price position relative to moving average

float ma = ta.sma(close, maLength)

float maDirection = close > ma ? 1 : -1

float maDeviation = math.abs(close - ma) / ma * 10 // Percentage deviation scaled

float maScore = math.max(-1, math.min(1, maDirection * math.min(maDeviation, 1)))

Multi-Timeframe Integration Logic

The multi-timeframe system uses a weighted average that gives more influence to higher timeframes:

// Timeframe weighting system

float currentTF = composite * 0.40 // Current timeframe: 40%

float higherTF1 = composite_tf2 * 0.25 // Next higher: 25%

float higherTF2 = composite_tf3 * 0.20 // Third higher: 20%

float higherTF3 = composite_tf4 * 0.15 // Fourth higher: 15%

float multiTFComposite = currentTF + higherTF1 + higherTF2 + higherTF3

This weighting reflects the principle that higher timeframes provide more significant context for market direction, while lower timeframes provide timing precision.

What the Dashboard Shows

The heatmap displays a grid where:

Each row represents a timeframe

Each column shows one component's normalized reading

Colors indicate the value: green shades for positive, red shades for negative, gray for neutral

The rightmost column shows the composite average for that timeframe

Visual Elements

Moving Average Line — A simple moving average plotted on the price chart

Background Tint — Subtle coloring based on the composite score

Shift Labels — Markers when the composite crosses threshold values

Dashboard Table — The main heatmap display

Inputs

Calculation Parameters:

Momentum Length (default: 14)

MACD Fast/Slow/Signal (default: 12/26/9)

Directional Movement Length (default: 14)

Moving Average Length (default: 50)

Timeframe Settings:

Enable/disable multi-timeframe analysis

Select additional timeframes to display

How to Read the Display

Similar colors across a row indicate the components are showing similar readings

Mixed colors indicate the components are showing different readings

The composite percentage shows the average of all four components

Alerts

Composite crossed above/below threshold values

Strong readings (above 50% or below -50%)

Important Limitations and Realistic Expectations

This indicator displays current analytical conditions—it does not predict future price movements

Agreement between components indicates current analytical alignment, not future price direction

All four components are based on historical price data and inherently lag price action

Market conditions can change rapidly, making current readings irrelevant

Different parameter settings will produce different readings and interpretations

No combination of technical indicators can reliably predict future market behavior

Strong readings in one direction do not guarantee continued movement in that direction

The composite score reflects mathematical relationships, not market fundamentals or sentiment

This tool should be used as one input among many in a comprehensive analytical approach

Appropriate Use Cases

This indicator is designed for:

- Analytical organization and efficiency

- Multi-timeframe confluence assessment

- Pattern recognition in indicator relationships

- Educational study of how different analytical approaches relate

- Supplementary analysis alongside other methods

This indicator is NOT designed for:

- Standalone trading signals

- Guaranteed profit generation

- Market timing precision

- Replacement of fundamental analysis

- Automated trading systems

— Made with passion by officialjackofalltrades

PRO Scalper(EN)

## What it is

**PRO Scalper** is an intraday price–action and liquidity map that helps you see where the market is likely to move **now**, not just where it has been.

It combines five building blocks that professional scalpers often watch together:

1. **Session Volume-Weighted Average Price (VWAP)** — the intraday “fair value” anchor.

2. **Opening Range** — the first minutes of the session that set the day’s balance.

3. **Trend filter** — higher-timeframe bias using **Exponential Moving Averages (EMA)** and optional **Average Directional Index (ADX)** strength.

4. **Two independent Supply/Demand zone engines** — zones are drawn from confirmed swing pivots, with midlines and **touch counters**.

5. **Order-flow style visuals**:

* **Delta bubbles** (green/red circles) show where buying or selling pressure was unusually strong, using a safe **delta proxy** (no external feeds).

* **Liquidity densities** (subtle rectangular bands) highlight clusters of large activity that often act as magnets or barriers and disappear when “eaten” by strong moves.

This mix gives you a **complete intraday picture**: the mean (VWAP), the day’s initial balance (Opening Range), the higher-timeframe push (trend filter), the nearby fuel or brakes (zones), and the live pressure points (bubbles and densities).

---

## Why these components

* **VWAP** tracks where the bulk of traded value sits. Price tends to rotate around it or accelerate away from it — a perfect compass for scalps.

* **Opening Range** frames the early auction. Many intraday breaks, fades and retests start at its boundaries.

* **EMA bias + ADX strength** separates trending conditions from chop, so you can keep only the zones that agree with the bigger push.

* **Pivot-based zones (two pairs at once)** are simple, objective and fast. Midlines help with confirmations; touch counters quantify how many times the zone was tested.

* **Bubbles and densities** add the “effort” layer: where the push appeared and where liquidity is concentrated. You see **where** a move is likely to continue or fail.

Together they reduce ambiguity: **context + level + effort** — all on one screen.

---

## How it works (plain language)

* **VWAP** resets each day and is calculated as the cumulative sum of typical price multiplied by volume divided by total volume.

* **Opening Range** is either automatic (a multiple of your chart timeframe) or a manual number of minutes. While it is forming, the highest high and lowest low are captured and plotted as the range.

* **Trend filter**

* **EMA Fast** and **EMA Slow** define directional bias.

* **ADX (optional)** adds “trend strength”: only when the Average Directional Index is above the chosen threshold do we treat the move as strong. You can source this from a higher timeframe.

* **Zones**

* There are **two independent pairs** of pivots at the same time (for example 10-left 10-right and 5-left 5-right).

* Each detected pivot creates a **Supply** (from a swing high) or **Demand** (from a swing low) box. Box depth = **zone depth × Average True Range** for adaptive sizing; the boxes **extend forward**.

* Midline (optional dashed line inside the box) is the “balance” of the zone.

* **“Only in trend”** mode can hide boxes that go against the higher-timeframe bias.

* The **touch counter** increases when price revisits the box. Labels show the pair name and the number of touches.

* **Bubbles**

* A safe **delta proxy** measures bar pressure (for example, range-weighted close vs open).

* A **quantile filter** shows only unusually large pressure: choose lookback and percentile, and the script draws a circle sized by intensity (green = bullish pressure, red = bearish).

* **Densities**

* The script marks heavy activity clusters as **subtle bands** around price (depth = fraction of Average True Range).

* If price **breaks** a density with volume above its moving average, the band **disappears** (“eaten”), which often precedes continuation.

---

## How to use — practical playbooks

> Recommended chart: crypto or index futures, one to five minutes. Use **one hour** or **fifteen minutes** for the higher-timeframe bias.

### 1) Trend pullback scalp (continuation)

1. Enable **Only in trend** zones.

2. In an uptrend: wait for a pullback into a **Demand** zone that overlaps with VWAP or sits just below the Opening Range midpoint.

3. Look for **green bubbles** near the zone’s bottom or a fresh **density** under price.

4. Enter on a candle closing **back above the zone midline**.

5. Stop-loss: below the bottom of the zone or a small multiple of Average True Range.

6. Targets: previous swing high, Opening Range high, fixed risk multiples, or VWAP.

Mirror the logic for downtrends using Supply zones, red bubbles and densities above price.

### 2) Reversion with liquidity sweep (fade)

1. Bias neutral or countertrend allowed.

2. Price **wicks through** a zone boundary (or an Opening Range line) and **closes back inside** the zone.

3. The bubble color often flips (absorption).

4. Enter toward the **inside** of the zone; stop beyond the sweep wick; first target = zone midline, second = opposite side of the zone or VWAP.

### 3) Opening Range break and retest

1. Wait for the Opening Range to complete.

2. A break with a large bubble suggests intent.

3. Look for a **retest** into a nearby zone aligned with VWAP.

4. Trade continuation toward the next zone or the session extremes.

### 4) Density “eaten” continuation

1. When a density band **disappears** on high volume, it often means the resting liquidity was consumed.

2. Trade in the direction of the break, toward the nearest opposing zone.

---

## Settings — quick guide

**Core**

* *ATR Length* — used for zone and density depths.

* *Show VWAP / Show Opening Range*.

* *Opening Range*: Auto (multiple of timeframe minutes) or Manual minutes.

**Trend Filter**

* *Mode*: Off, EMA only, or EMA with ADX strength.

* *Use higher timeframe* and its value.

* *EMA Fast / EMA Slow*, *ADX Length*, *ADX threshold*.

* *Plot EMA filter* to display the moving averages.

**Zones (two pairs)**

* *Pivot A Left / Right* and *Pivot B Left / Right*.

* *Zone depth × ATR*, *Extend bars*.

* *Show zone midline*, *Only in trend zones*.

* Labels automatically show the touch counters.

**Bubbles**

* *Show Bubbles*.

* *Quantile lookback* and *Quantile percent* (higher percent = stricter filter, fewer bubbles).

**Densities**

* *Metric*: absolute delta proxy or raw volume.

* *Quantile lookback / percent*.

* *Depth × ATR*, *Extend bars*, *Merge distance* (in ATR),

* *Break condition*: volume moving average length and multiplier,

* *Midline for densities* (optional dashed line).

---

## Tips and risk management

* This script **does not use external order-flow feeds**. Delta is a **proxy** suitable for TradingView; tune quantiles per symbol and timeframe.

* Do not trade every bubble. Combine **context (trend + VWAP + Opening Range)** with **level (zone)** and **effort (bubble/density)**.

* Set stop-losses beyond the zone or at a fraction of Average True Range. Predefine risk per trade.

* Backtest your rules with a strategy script before using real funds.

* Markets differ. Parameters that work on Bitcoin may not transfer to low-liquidity altcoins or stocks.

* Nothing here is financial advice. Scalping is high-risk; slippage and over-trading can quickly damage your account.

---

## What makes PRO Scalper unique

* Two **independent** zone engines run in parallel, so you can see both **larger structure** and **fine intraday levels** at the same time.

* Clean **“only in trend” rendering** — zones and midlines against the bias can be hidden, reducing clutter and hesitation.

* **Touch counters** convert “feel” into numbers.

* **Self-contained order-flow visuals** (bubbles and densities) that require no extra data sources.

* Careful defaults: subtle colors for densities, clearer zones, and responsive auto Opening Range.

---

(RU)

## Что это такое

**PRO Scalper** — это индикатор для внутридневной торговли, который показывает **контекст и ликвидность прямо сейчас**.

Он объединяет пять модулей, которыми профессиональные скальперы пользуются вместе:

1. **VWAP** — средневзвешенная по объему цена за сессию, «справедливая стоимость» дня.

2. **Opening Range** — первая часть сессии, задающая баланс дня.

3. **Фильтр тренда** — направление старшего таймфрейма по **экспоненциальным средним** и при желании по силе тренда **Average Directional Index**.

4. **Две независимые системы зон спроса/предложения** — зоны строятся от подтвержденных экстремумов (пивотов), имеют **среднюю линию** и **счетчик касаний**.

5. **Визуализация «ордер-флоу»**:

* **Пузыри дельты** (зеленые/красные круги) — места повышенного покупательного/продажного давления, рассчитанные через безопасный **прокси-дельты**.

* **Плотности ликвидности** (ненавязчивые прямоугольные ленты) — скопления объема, которые нередко притягивают цену или удерживают ее и исчезают, когда «разъедаются» сильным движением.

Итог — **полная картинка момента**: среднее (VWAP), баланс дня (Opening Range), старшая сила (фильтр тренда), ближайшие уровни топлива/тормозов (зоны), текущие точки усилия (пузыри и плотности).

---

## Почему именно эти элементы

* **VWAP** показывает, где сосредоточена стоимость; цена либо вращается вокруг него, либо быстро уходит — идеальный ориентир скальпера.

* **Opening Range** фиксирует ранний аукцион — от его границ часто начинаются пробои, возвраты и ретесты.

* **EMA + ADX** отделяют тренд от «пилы», позволяя оставлять на графике только зоны по направлению старшего таймфрейма.

* **Зоны от пивотов** просты, объективны и быстры; средняя линия помогает подтверждать разворот, счетчик касаний переводит субъективность в цифры.

* **Пузыри и плотности** добавляют слой «усилия»: где именно возник толчок и где сконцентрирована ликвидность.

Комбинация **контекста + уровня + усилия** уменьшает двусмысленность и ускоряет принятие решения.

---

## Как это работает (простыми словами)

* **VWAP** каждый день стартует заново: сумма «типичной цены × объем» делится на суммарный объем.

* **Opening Range** — автоматический (кратный минутам вашего таймфрейма) или вручную заданный период; пока он формируется, фиксируются максимум и минимум.

* **Фильтр тренда**

* Две экспоненциальные средние задают направление.

* **ADX** (по желанию) добавляет «силу». Источник можно взять со старшего таймфрейма.

* **Зоны**

* Одновременно работает **две пары** пивотов (например 10-лево 10-право и 5-лево 5-право).

* От пивота строится зона **предложения** (от максимума) или **спроса** (от минимума). Глубина зоны = **коэффициент × Average True Range**; зона тянется вперед.

* Внутри рисуется **средняя линия** (по желанию).

* Режим **«только по тренду»** скрывает зоны против старшего направления.

* **Счетчик касаний** увеличивается, когда цена снова входит в зону; подпись показывает пару и количество касаний.

* **Пузыри**

* Используется безопасный **прокси-дельты** — измерение «напряжения» внутри свечи.

* Через **квантильный фильтр** выводятся только необычно сильные места: настраиваются окно и процент квантиля; размер кружка — сила, цвет: зеленый покупатели, красный продавцы.

* **Плотности**

* Крупные активности отмечаются **ненавязчивыми прямоугольниками** (глубина — доля Average True Range).

* Если плотность **пробивается** объемом выше среднего, она **исчезает** — часто это предвещает продолжение.

---

## Как пользоваться — практические схемы

> Рекомендация: крипто или фьючерсы, таймфрейм 1–5 минут. Для старшего фильтра удобно взять **1 час** или **15 минут**.

### 1) Скальп на откат по тренду

1. Включите **«только по тренду»**.

2. В восходящем тренде дождитесь отката в **зону спроса**, желательно рядом с **VWAP** или серединой **Opening Range**.

3. Подтверждение — **зеленые пузыри** у нижней границы зоны или свежая **плотность** под ценой.

4. Вход после закрытия свечи **выше средней линии** зоны.

5. Стоп-лосс: за нижнюю границу зоны или небольшой множитель Average True Range.

6. Цели: предыдущий максимум, верх Opening Range, фиксированные R-множители, либо VWAP.

Для нисходящего тренда зеркально: зоны предложения, красные пузыри и плотности над ценой.

### 2) Контрдвижение с «выбиванием ликвидности»

1. Нейтральный или контртрендовый режим.

2. Цена **выносит хвостом** границу зоны (или линию Opening Range) и **закрывается обратно внутри**.

3. Цвет пузыря часто меняется (поглощение).

4. Вход внутрь зоны; стоп — за хвост выбивания; цели: средняя линия, противоположная граница зоны или VWAP.

### 3) Пробой Opening Range + ретест

1. Дождитесь завершения диапазона.

2. Сильный пробой с крупным пузырем — признак намерения.

3. Ищите **ретест** в зоне по тренду рядом с линией диапазона и VWAP.

4. Торгуйте продолжение к следующей зоне.

### 4) Продолжение после «съеденной» плотности

1. Когда прямоугольник плотности **исчезает** на повышенном объеме, это значит, что ликвидность поглощена.

2. Торгуйте в сторону пробоя к ближайшей противоположной зоне.

---

## Настройки — краткая шпаргалка

**Core**

— Длина Average True Range (для размеров зон и плотностей).

— Включение VWAP и Opening Range.

— Длина Opening Range: автоматическая (кратная минутам ТФ) или ручная.

**Trend Filter**

— Режим: выкл., только средние, либо средние + ADX.

— Источник со старшего таймфрейма и его значение.

— Длины средних, длина ADX и порог силы.

— Показать/скрыть линий средних.

**Zones (две пары одновременно)**

— Пара A: лев/прав; Пара B: лев/прав.

— Глубина зоны × Average True Range, продление по барам.

— Средняя линия, режим **«только по тренду»**.

— Подписи со счетчиком касаний.

**Bubbles**

— Вкл./выкл., окно поиска и процент квантиля (чем выше процент — тем реже пузыри).

**Densities**

— Метрика: абсолютная прокси-дельты или чистый объем.

— Окно/квантиль, глубина × Average True Range, продление,

— Порог объединения (в Average True Range),

— Условие «разъедания» по объему,

— Средняя линия плотности (по желанию).

---

## Советы и риски

* Индикатор **не использует внешние потоки ордер-флоу**. Дельта — **прокси**, подходящая для TradingView; подбирайте квантили под инструмент и таймфрейм.

* Не торгуйте каждый пузырь. Склейте **контекст (тренд + VWAP + Opening Range)** с **уровнем (зона)** и **усилием (пузырь/плотность)**.

* Стоп-лосс — за границей зоны или по Average True Range. Риск на сделку задавайте заранее.

* Перед реальными деньгами протестируйте правила в стратегии.

* Разные рынки ведут себя по-разному; настройки из Биткоина могут не подойти малоликвидным альткоинам или акциям.

* Это не инвестиционная рекомендация. Скальпинг — высокий риск; проскальзывание и переизбыток сделок быстро наносят ущерб капиталу.

---

## Чем уникален PRO Scalper

* Две **одновременные** системы зон показывают и **крупную структуру**, и **точные локальные уровни**.

* Режим **«только по тренду»** чистит экран от лишних уровней и ускоряет решение.

* **Счетчики касаний** дают количественную опору.

* **Самодостаточные визуализации усилия** (пузыри и плотности) — без сторонних источников данных.

* Аккуратная цветовая схема: плотности — мягко, зоны — ясно; Opening Range — адаптивный.

Пусть он станет вашей «картой местности» для быстрых и дисциплинированных решений внутри дня.

sideways market for strangleThis Pine Script is designed to identify **sideways or range-bound markets**, which are often ideal conditions for trading **options strangle strategies**. Here's a breakdown of what the script does:

---

### 🛠 **Purpose:**

To **detect low-volatility, sideways market conditions** where price is not trending strongly in either direction — suitable for **neutral options strategies like short strangles**.

---

### 📌 **Key Components:**

#### 1. **Inputs:**

- `RSI Length`: Default 14 — used for calculating the Relative Strength Index (RSI).

- `ADX Length`: Default 14 — used for calculating the Average Directional Index (ADX), DI+ (positive directional movement), and DI- (negative directional movement).

#### 2. **RSI Calculation:**

- `rsiValue` is calculated using the built-in `ta.rsi(close, rsiLength)`.

- A **sideways market** is expected when RSI is in the **40–60 range**, indicating lack of strong momentum.

#### 3. **ADX and Directional Indicators (DI+ and DI-):**

- `diPlus` and `diMinus` are calculated based on recent price movements and the True Range.

- `dx` (Directional Index) measures the strength of trend direction using the difference between DI+ and DI-.

- `adx` is a smoothed version of `dx` and represents **overall trend strength**.

#### 4. **Sideways Market Conditions:**

- **RSI Condition**: RSI is between 40 and 60.

- **ADX Condition**:

- `adx <= 25` → Weak or no trend.

- `adx < diPlus` and `adx < diMinus` → Confirms ADX is lower than directional components, reducing likelihood of a trending market.

#### 5. **Signal Plot:**

- A **green label below the bar** (`shape.labelup`) is plotted when both conditions are met.

- Indicates potential sideways market conditions.

---

### ✅ **Use Case:**

- This signal can help identify **low-volatility zones** suitable for **short strangles** or **iron condors**, where you profit from time decay while expecting the price to stay within a range.

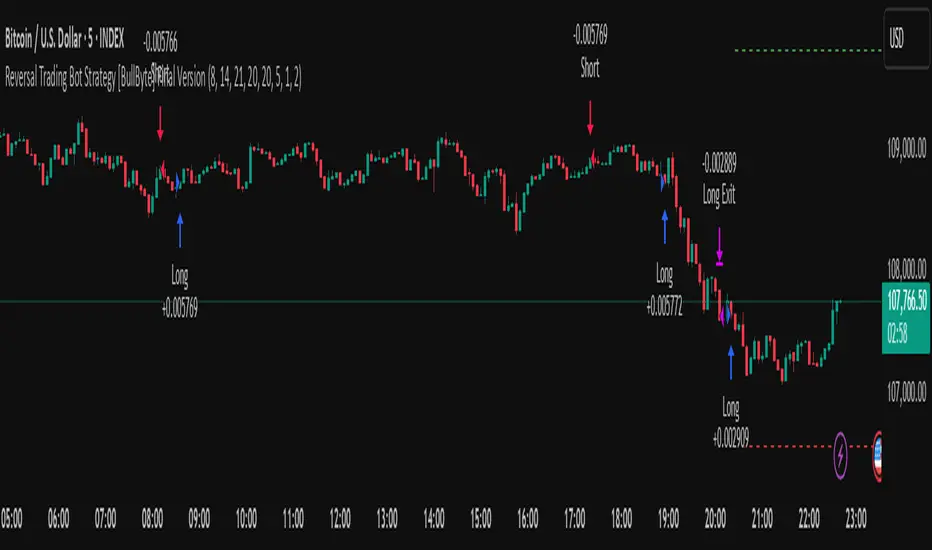

Reversal Trading Bot Strategy[BullByte]Overview :

The indicator Reversal Trading Bot Strategy is crafted to capture potential market reversal points by combining momentum, volatility, and trend alignment filters. It uses a blend of technical indicators to identify both bullish and bearish reversal setups, ensuring that multiple market conditions are met before entering a trade.

Core Components :

Technical Indicators Used :

RSI (Relative Strength Index) :

Purpose : Detects divergence conditions by comparing recent lows/highs in price with the RSI.

Parameter : Length of 8.

Bollinger Bands (BB) :

Purpose : Measures volatility and identifies price levels that are statistically extreme.

Parameter : Length of 20 and a 2-standard deviation multiplier.

ADX (Average Directional Index) & DMI (Directional Movement Index) :

Purpose : Quantifies the strength of the trend. The ADX threshold is set at 20, and additional filters check for the alignment of the directional indicators (DI+ and DI–).

ATR (Average True Range) :

Purpose : Provides a volatility measure used to set stop levels and determine risk through trailing stops.

Volume SMA (Simple Moving Average of Volume ):

Purpose : Helps confirm strength by comparing the current volume against a 20-period average, with an optional filter to ensure volume is at least twice the SMA.

User-Defined Toggle Filters :

Volume Filter : Confirms that the volume is above average (or twice the SMA) before taking trades.

ADX Trend Alignment Filter : Checks that the ADX’s directional indicators support the trade direction.

BB Close Confirmation : Optionally refines the entry by requiring price to be beyond the upper or lower Bollinger Band rather than just above or below.

RSI Divergence Exit : Allows the script to close positions if RSI divergence is detected.

BB Mean Reversion Exit : Closes positions if the price reverts to the Bollinger Bands’ middle line.

Risk/Reward Filter : Ensures that the potential reward is at least twice the risk by comparing the distance to the Bollinger Band with the ATR.

Candle Movement Filter : Optional filter to require a minimum percentage move in the candle to confirm momentum.

ADX Trend Exit : Closes positions if the ADX falls below the threshold and the directional indicators reverse.

Entry Conditions :

Bullish Entry :

RSI Divergence : Checks if the current close is lower than a previous low while the RSI is above the previous low, suggesting bullish divergence.

Bollinger Confirmation : Requires that the price is above the lower (or upper if confirmation is toggled) Bollinger Band.

Volume & Trend Filters : Combines volume condition, ADX strength, and an optional candle momentum condition.

Risk/Reward Check : Validates that the trade meets a favorable risk-to-reward ratio.

Bearish Entry :

Uses a mirror logic of the bullish entry by checking for bearish divergence, ensuring the price is below the appropriate Bollinger level, and confirming volume, trend strength, candle pattern, and risk/reward criteria.

Trade Execution and Exit Strateg y:

Trade Execution :

Upon meeting the entry conditions, the strategy initiates a long or short position.

Stop Loss & Trailing Stops :

A stop-loss is dynamically set using the ATR value, and trailing stops are implemented as a percentage of the close price.

Exit Conditions :

Additional exit filters can trigger early closures based on RSI divergence, mean reversion (via the middle Bollinger Band), or a weakening trend as signaled by ADX falling below its threshold.

This multi-layered exit strategy is designed to lock in gains or minimize losses if the market begins to reverse unexpectedly.

How the Strategy Works in Different Market Conditions :

Trending Markets :

The ADX filter ensures that trades are only taken when the trend is strong. When the market is trending, the directional movement indicators help confirm the momentum, making the reversal signal more reliable.

Ranging Markets :

In choppy markets, the Bollinger Bands expand and contract, while the RSI divergence can highlight potential turning points. The optional filters can be adjusted to avoid false signals in low-volume or low-volatility conditions.

Volatility Management :