Search in scripts for "backtest"

✅ BACKTEST: UT Bot + RSIRSI levels widened (60/40) — more signals.

Removed ATR volatility filter (to let trades fire).

Added inputs for TP and SL using ATR — fully dynamic.

Cleaned up conditions to ensure alignment with market structure.

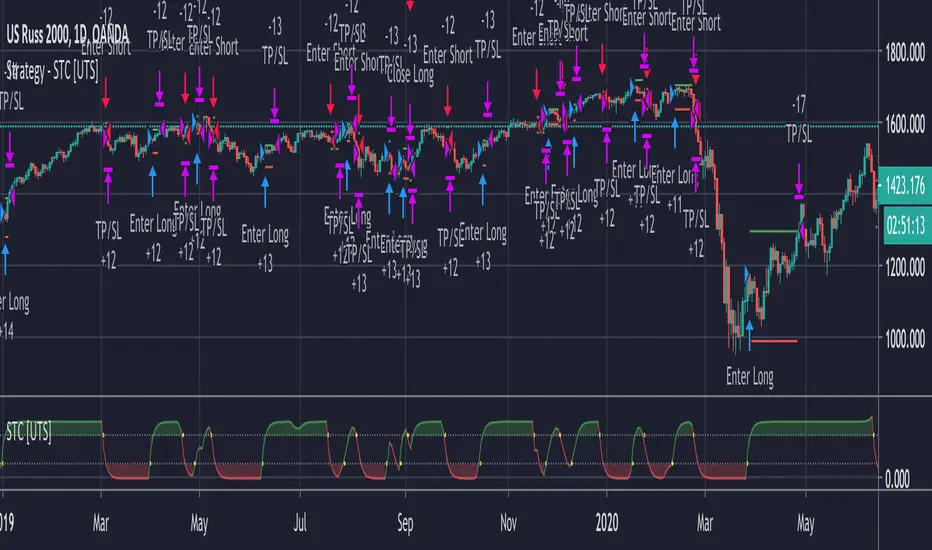

Strategy - Uber STC - Schaff Trend Cycle [UTS]Backtesting of Uber STC - Schaff Trend Cycle

Backtest with focus win/loss profitability.

Formula: profitability = win / (win+loss)

Default equity 100k USD

Default 2% Risk per trade

Default currency USD

Define backtest interval precisely by month, year, day

LONG and SHORT positions

Visualize SL and TP on chart

ATR (len: 14, smooth: SMA)

ATR based Stop-Loss, if hit trade will be closed and considered as loss

ATR based Take-Profit, if hit trade will be closed and considered as win

On TP or SL hit the trade is closed and marked as win/loss

Laguerre RSI by KivancOzbilgic STRATEGYBacktesting.

" Laguerre RSI is based on John EHLERS' Laguerre Filter to avoid the noise of RSI .

Change alpha coefficient to increase/decrease lag and smoothness.

Buy when Laguerre RSI crosses upwards above 20.

Sell when Laguerre RSI crosses down below 80.

While indicator runs flat above 80 level, it means that an uptrend is strong.

While indicator runs flat below 20 level, it means that a downtrend is strong. "

Developer: John EHLERS

Author: KivancOzbilgic

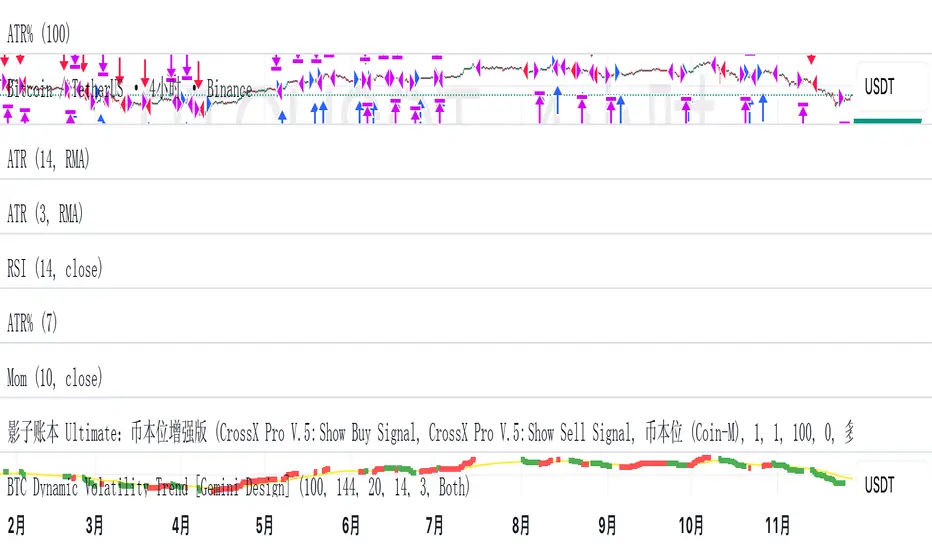

BTC Dynamic Volatility Trend Backtested from 2017 to present, this strategy has delivered a staggering 7100%+ cumulative return. It doesn't just track the market; it dominates it. By capturing major trends and strictly limiting drawdowns, it has significantly outperformed the standard 'Buy & Hold' BTC strategy, proving its ability to generate massive alpha across multiple bull and bear cycles.

自 2017 年至今,本策略实现了惊人的 7100%+ 累计收益率。它不仅仅是跟随市场,更是超越了市场。通过精准捕捉主升浪并严格控制回撤,该策略在穿越多轮牛熊周期后,大幅度跑赢了比特币‘买入持有’(Buy & Hold)的基准收益,展现了极致的阿尔法(Alpha)捕捉能力。"

Introduction :Simplicity is the ultimate sophistication. This strategy is designed specifically for Bitcoin (BTC), capturing its unique characteristics: high volatility, frequent fakeouts, and massive trend persistence. It abandons complex indicators in favor of a robust logic: "Follow the Trend, Filter the Noise, Let Profits Run."

Core Logic

Trend Filter (Fibonacci EMA 144): We use the 144-period Exponential Moving Average as the baseline. Longs are only taken above this line, and shorts only below. This keeps you on the right side of the major trend.

Volatility Breakout (Donchian Channel 20): Entries are triggered only when price breaks the 20-day high (for longs) or low (for shorts). This confirms momentum and avoids trading in chop.

Dynamic Risk Management (ATR Chandelier Exit):

Instead of fixed % stops, we use Average True Range (ATR) to calculate stop losses.

The Ratchet Mechanism: The stop loss moves up with the price but never moves down (for longs). This locks in profits automatically as the trend develops and exits immediately when volatility turns against you.

Why Use This Strategy?

Zero Repainting: All signals are confirmed.

No Curve Fitting: Uses classic parameters (144, 20) that have worked for decades.

Mental Peace: The strategy handles the exit. You don't need to guess where to sell. It holds through minor corrections and exits only when the trend truly reverses.

Settings

Leverage %: Adjust your position size based on equity (default 100% = 1x).

Timeframe: Recommended for 4H charts.

中文版 (Chinese Version)

简介 :大道至简。本策略专为 比特币 (BTC) 设计,针对其高波动、假突破多但趋势爆发力强的特点,摒弃了复杂的过度拟合指标,回归交易本质:“顺大势,滤噪音,截断亏损,让利润奔跑”。

核心逻辑

趋势过滤器 (斐波那契 EMA 144): 使用 144 周期指数移动平均线作为多空分水岭。价格在均线之上只做多,之下只做空。这能有效过滤掉大部分震荡市的噪音。

波动率突破 (唐奇安通道 20): 只有当价格突破过去 20 根 K 线的最高价(做多)或最低价(做空)时才进场。这确保了我们只在趋势确立的瞬间入场。

动态风控 (ATR 吊灯止损):

拒绝固定点数止损,使用 ATR(平均真实波幅)根据市场热度动态计算安全距离。

棘轮机制: 止损线会跟随价格上涨而上移,但绝不会下移(做多时)。这实现了自动化的“利润锁定”,既能扛住正常的波动回调,又能在大势反转时果断离场。

策略优势

绝不重绘: 所有信号均为收盘确认或实时触价。

拒绝拟合: 使用经过数十年市场验证的经典参数组合。

心态管理: 策略全自动管理出场。你不需要纠结何时止盈,它会帮你吃到完整的鱼身,直到趋势结束。

使用建议

资金管理: 可通过参数调整仓位占比(默认 100% = 1倍杠杆)。

推荐周期: 建议在4小时 图表上运行效果最佳。

Backtest - Ichimoku CloudThis script find the entry position on a chart using Ichimoku clud conditions.

and also exit condition based on base line & price close w.r.t to Ichi cloud.

Momentum Breakout StrategyBacktest a strategy where, when a candlestick on a timeframe rises more than a certain %, it enters a trade.

RSI-VWAPBacktest script based on the previous RSI-VWAP indicator:

It's the popular RSI indicator with VWAP as a source instead of close:

- RSI_VWAP = rsi(vwap(close), RSI_VWAP_length)

What is the Volume Weighted Average Price ( VWAP )?

VWAP is calculated by adding up the dollars traded for every transaction (price multiplied by the number of shares traded) and then dividing by the total shares traded.

Trades are laddered to improve the average entry price and each entry is increased, improving the entry but increasing the risk of being liquidated.

It can be easily converted to study (alerts)

Settings for BINANCE:BTCUSDT at 30m

Simple Price Momentum - How To Create A Simple Trading StrategyThis script was built using a logical approach to trading systems. All the details can be found in a step by step guide below. I hope you enjoy it. I am really glad to be part of this community. Thank you all. I hope you not only succeed on your trading career but also enjoy it.

docs.google.com

[Strategy]TB!Just an Indicator [EWO& Guppy Made Easy]]Backtesting for TB! Just an Indicator + the merger of EWO & Guppy

Moving Averages Cross - MTF - StrategyBacktesting Script for the following strategy

Strategy Injector Source: github.com

Tryhard bitmex strategy - SMA+RSI, no repaint, no trailing stopBacktest for 2017-2018, with x1 leverage.

3MA for trend detection, fast RSI for counter-trend elements.

The strategy contains many parameters that are not optimal now, the results can be much better

4H CCI Strategy 1.5Included adaptive lot size based on ATR, and also ATR based stop and take profit levels.

Risk/reward increased to 1:2 and should work in all ranging FX pairs as long as they are not trending.

Once the market starts trending it'll eat this bot alive.

Cheers,

Ivan Labrie

Time at Mode FX

[STRATEGY] Adaptive Multi Factor Trend TradingDaily Filters

Close vs. short/long daily SMAs (customizable) defines directional priority.

Use the daily Short Long MA spread (or ATR‑normalized) to filter out range‑bound conditions and reduce false breakouts.

30‑Minute Entry Logic

Buy

Daily bullish regime confirmed

High breaks above the trend

Protected by trailing take‑profit and fixed stop‑loss.

Sell #1

Daily bearish regime confirmed

Low breaks below the trend

Long MA slope must be strong (trend‑quality filter).

Sell #2

Day‑session only, limited to high‑probability hours

Triggered by an aggregated bear score (multi‑factor stack) + a downward linear‑regression slope

Friday uses special thresholds/intervals (event‑risk control).

Multi‑Factor Framework

MACD, RSI, Stoch (KD), Ichimoku, CCI, PSAR, Williams %R, Heikin Ashi, Bias, Force Index, plus regression‑slope.

Signals are stacked into bull/bear totals and used as filters or weights—no single indicator dominance.

Risk & Position Management

Fixed TP/SL + trailing TP across entry types

Position size adapts to recent performance (loss‑streak counter) and slope state

Auto pause when the loss streak hits the threshold (configurable duration).

Trading‑Day Controls

Optional pre‑holiday blackout list

Date‑range limiter for backtests or deployment windows.

Design Intent

The goal is to keep net P&L stable while lifting win rate.

In strong‑trend environments, the system leans into trend signals (Sell #1 / Buy).

In short‑term chop, Sell #2 timing and the slope filter reduce noise and avoid low‑quality entries.