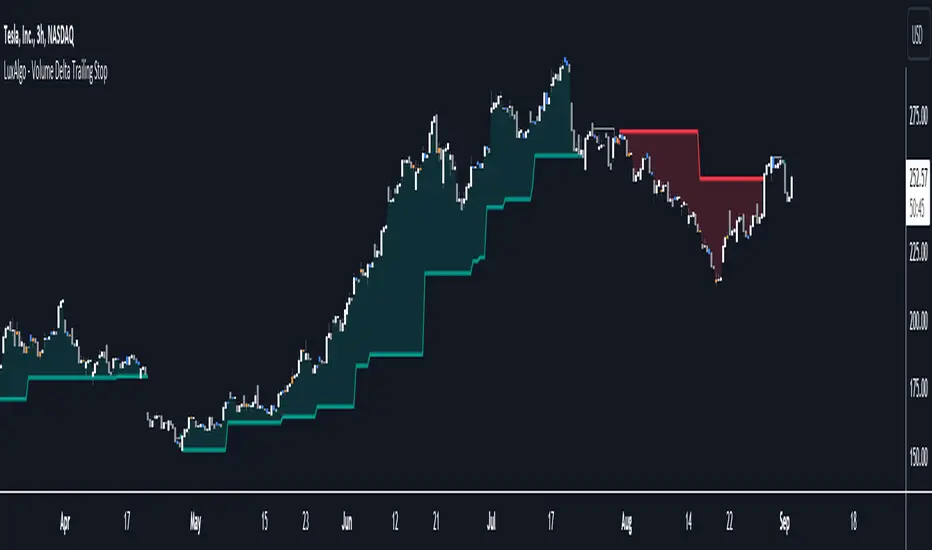

Volume Delta Trailing Stop [LuxAlgo]The ' Volume Delta Trailing Stop ' indicator uses Lower Time Frame (LTF) volume delta data which can provide potential entries together with a Volume-Delta based Trailing Stop-line .

🔶 USAGE

Our 'Volume Delta Trailing Stop' script can show potential entries/Stop Loss lines

A trigger line needs to be broken before a position is taken, after which a Volume Delta-controlled Trailing Stop-line is created:

🔶 DETAILS

🔹 Volume rises when bought or sold

🔹 When the opening price appears on the chart, a buy/sell order has been executed.

If that order is less than the available supply of that particular price, volume will rise, without moving the price.

🔹 When the opening price is the same as the closing price, the volume of that bar can be seen as "neutral volume" (nV); nor "up", nor "down" volume.

Example

A buy order doesn't fill the first available supply in the order book. This price will be the opening price with a certain volume.

When at closing time, price still hasn't moved (the first available supply in the order book isn't filled, or no movement downwards),

the closing price will be equal to the opening price, but with volume. This can be seen as "neutral volume (nV)".

🔹 Delta Volume (ΔV): this is "up volume" minus "down volume"

🔹 Standard volume is colored red when closing price is lower than opening price ( = "down volume").

🔹 Standard volume is colored green when closing price is higher OR equal (nV) than opening price ( = "up volume").

🔹 Neutral Volume

The "Neutral-Volume" is considered "Up-Volume" - setting will dictate whether nV is considered as green 'buy' volume or not.

🔶 EXAMPLE

29 July 10:00 -> 10:05, chart timeframe 5 minutes, open 29311.28, close 29313.89

close > open, so the volume (39.55) is colored green ("up volume").

(The Volume script used in the following examples is the open-source publication Volume Columns w. Alerts (V) from LucF )

Let's zoom to the 1-minute TF:

The same period is now divided into more bars, volume direction (color) is dependable on the difference between open and close.

Counting up and down volume gives a more detailed result, it remains in an upward direction though):

(ΔV = +15.51)

Let's further zoom in to the 1-second TF:

The same period is now divided into even more bars (more possibility for changing direction on each bar)

Here we see several bars that haven't moved in price, but they have volume ("neutral" volume).

(neutral volume is coloured light green here, while up volume is coloured darker green)

When we count all green and red volume bars, the result is quite different:

(ΔV = -0.35)

In total more volume is found when price went downwards, yet price went up in these 5 minutes.

-> This is the heart of our publication, when this divergence occurs, you can see a barcolor changement:

• orange: when price went up, but LTF Volume was mainly in a downward direction.

• blue: when price went down, but LTF Volume was mainly in an upwards direction.

When we split the green "up volume" into "up" and "neutral", the difference is even higher

(here "neutral volume" is colored grey):

(ΔV = -12.76; "up" - "down")

🔶 CONCEPTS

bullishBear = current bar is red but LTF volume is in upward direction -> blue bar

bearishBull = current bar is green but LTF volume is in downward direction -> orange bar

🔹 Potential positioning - forming of Trigger-line

When not in position, the script will wait for a divergence between price and volume direction. When found, a Trigger-line will appear:

• at high when a blue bar appears ( bullishBear ).

• at low when an orange bar appears ( bearishBull ).

Next step is when the Trigger-line is broken by close or high/low (settings: Trigger )

Here, the closing price went under the grey Trigger-line -> bearish position:

🔹 Trailing Stop-line

When the Trigger-line is broken, the Trailing Stop-line (TS-line) will start:

• low when bullish position

• high when bearish position

You can choose (settings -> Trigger -> Close or H/L ) whether close price or high/low should break the Trigger-line

When alerts are enabled ("Any alert() function call"), you'll get the following message:

• ' signal up ' when bullish position

• ' signal down' when bearish position

After that, the TS-line will be adjusted when:

• a blue bullishBear bar appears when in bullish position -> lowest of {low , previous blue bar's high or orange bar's low}

• an orange bearishBull bar appears when in bearish position -> highest of {high, previous blue bar's high or orange bar's low}

When alerts are enabled ("Any alert() function call"), and the TS-line is broken, you'll get the following message:

• ' TS-line broken down ' when out bullish position

• ' TS-line broken up ' when out bearish position

🔹 Reference Point

Default the direction of price will be evaluated by comparing closing price with opening price.

When open and close are the same, you'll get "neutral volume".

You can use "previous close" instead (as in built-in volume indicator) to include gaps.

If close equals open , but close is lower than previous close , it will be regarded as " down volume ",

similar, when close is higher than previous close , it will be regarded as " up volume "

Note, the setting applies for the current timeframe AND Lower timeframe:

Based on: " open " (close - open)

Based on: " previous close " (close - previous close)

🔹 Adjustment

When the TS-line changes, this can be adjusted with a percentage of price , or a multiple of " True Range "

Default (Δ line -> Adjustment - 0)

Δ line -> Adjustment 0.03% (of price)

Δ line -> Mult of TR (10)

🔶 SETTINGS

🔹 LTF: choose your Lower TimeFrame: 1S (seconds), 5S, 10S, 15S, 30S, 1 minute)

🔹 Trigger: Choose the trigger for breaking the Trigger-line ; close or H/L (high when bullish position, low when bearish position)

🔹 Δ line ( Trailing Stop-line ): add/subtract an adjustment when the TS-line changes ( default: Adjustment ):

• Adjustment ( default: 0 ): add/subtract an extra % of price

• Mult of TR : add/subtract a multiple of True Range

🔹 Based on: compare closing price against:

• open

• previous close

🔹 "Neutral-Volume" is considered "Up-Volume" : this setting will dictate whether nV is considered as green 'buy' volume or not.

🔶 CONSIDERATIONS

🔹 The lowest LTF (1S) will give you more detail and will get data close to tick data.

However, a maximum of 100,000 intrabars can be used in calculations .

This means on the daily chart you won't see anything since 1 day ~ 86400 seconds. (just over 1 bar)

-> choose a lower chart timeframe, or choose a higher LTF (5S, 10S, ... 1 minute)

🔹 Always choose a LTF lower than the current chart timeframe.

🔹 Pine Script™ code using this request.security_lower_tf() may calculate differently on historical and real-time bars, leading to repainting .

Search in scripts for "bar"

Volume Profile (Maps) [LuxAlgo]The Pine Script® developers have unleashed "maps"!

Volume Profile (Maps) displays volume, associated with price, above and below the latest price, by using maps

The largest and second-largest volume is highlighted.

🔶 USAGE

The proposed script can highlight more frequent closing prices/prices with the highest volume, potentially highlighting more liquid areas. The prices with the highest associated volume (in red and orange in the indicator) can eventually be used as support/resistance levels.

Voids within the volume profile can highlight large price displacements (volatile variations).

🔶 CONCEPTS

🔹 Maps

A map object is a collection that consists of key - value pairs

Each key is unique and can only appear once. When adding a new value with a key that the map already contains, that value replaces the old value associated with the key .

You can change the value of a particular key though, for example adding volume (value) at the same price (key), the latter technique is used in this script.

Volume is added to the map, associated with a particular price (default close, can be set at high, low, open,...)

When the map already contains the same price (key), the value (volume) is added to the existing volume at the associated price.

A map can contain maximum 50K values, which is more than enough to hold 20K bars (Basic 5K - Premium plan 20K), so the whole history can be put into a map.

🔹 Visible line/box limit

We can only display maximum 500 line.new() though.

The code locates the current (last) close, and displays volume values around this price, using lines, for example 250 lines above and 250 lines below current price.

If one side contains fewer values, the other side can show more lines, taking the maximum out of the 500 visible line limitation.

Example (max. 500 lines visible)

• 100 values below close

• 2000 values above close

-> 100 values will be displayed below close

-> 400 remaining -> 400 values will be displayed above close

Pushing the limits even further, when ' Amount of bars ' is set higher than 500, boxes - box.new() - will be used as well.

These have a limit of 500 as well, bringing the total limit to 1000.

Note that there are visual differences when boxes overlap against lines.

If this is confusing, please keep ' Amount of bars ' at max. 500 (then only lines will be used).

🔹 Rounding function

This publication contains 2 round functions, which can be used to widen the Volume Profile

Round

• "Round" set at zero -> nothing changes to the source number

• "Round" set below zero -> x digit(s) after the decimal point, starting from the right side, and rounded.

• "Round" set above zero -> x digit(s) before the decimal point, starting from the right side, and rounded.

Example: 123456.789

0->123456.789

1->123456.79

2->123456.8

3->123457

-1->123460

-2->123500

Step

Another option is custom steps.

After setting "Round" to "Step", choose the desired steps in price,

Examples

• 2 -> 1234.00, 1236.00, 1238.00, 1240.00

• 5 -> 1230.00, 1235.00, 1240.00, 1245.00

• 100 -> 1200.00, 1300.00, 1400.00, 1500.00

• 0.05 -> 1234.00, 1234.05, 1234.10, 1234.15

•••

🔶 FEATURES

🔹 Adjust position & width

🔹 Table

The table shows the details:

• Size originalMap : amount of elements in original map

• # higher: amount of elements, higher than last "close" (source)

• index "close" : index of last "close" (source), or # element, lower than source

• Size newMap : amount of elements in new map (used for display lines)

• # higher : amount of elements in newMap, higher than last "close" (source)

• # lower : amount of elements in newMap, lower than last "close" (source)

🔹 Volume * currency

Let's take as example BTCUSD, relative to USD, 10 volume at a price of 100 BTCUSD will be very different than 10 volume at a price of 30000 (1K vs. 300K)

If you want volume to be associated with USD, enable Volume * currency . Volume will then be multiplied by the price:

• 10 volume, 1 BTC = 100 -> 1000

• 10 volume, 1 BTC = 30K -> 300K

Disabled

Enabled

🔶 DETAILS

🔹 Put

When the map doesn't contain a price, it will be added, using map.put(id, key, value)

In our code:

map.put(originalMap, price, volume)

or

originalMap.put(price, volume)

A key (price) is now associated with a value (volume) -> key : value

Since all keys are unique, we don't have to know its position to extract the value, we just need to know the key -> map.get(id, key)

We use map.get() when a certain key already exists in the map, and we want to add volume with that value.

if originalMap.contains(price)

originalMap.put(price, originalMap.get(price) + volume)

-> At the last bar, all prices (source) are now associated with volume.

🔹 Copy & sort

Next, every key of the map is copied and sorted (array of keys), after which the index (idx) is retrieved of last (current) price.

copyK = originalMap.keys().copy()

copyK.sort()

idx = copyK.binary_search_leftmost(src)

Then left and right side of idx is investigated to show a maximum amount of lines at both sides of last price.

🔹 New map & display

The keys (from sorted array of copied keys) that will be displayed are put in a new map, with the associated volume values from the original map.

newMap = map.new()

🔹 Re-cap

• put in original amp (price key, volume value)

• copy & sort

• find index of last price

• fetch relevant keys left/right from that index

• put keys in new map and fetch volume associated with these keys (from original map)

Simple example (only show 5 lines)

bar 0, price = 2, volume = 23

bar 1, price = 4, volume = 3

bar 2, price = 8, volume = 21

bar 3, price = 6, volume = 7

bar 4, price = 9, volume = 13

bar 5, price = 5, volume = 85

bar 6, price = 3, volume = 13

bar 7, price = 1, volume = 4

bar 8, price = 7, volume = 9

Original map:

Copied keys array:

Sorted:

-> 5 keys around last price (7) are fetched (5, 6, 7, 8, 9)

-> keys are placed into new map + volume values from original map

Lastly, these values are displayed.

🔶 SETTINGS

Source : Set source of choice; default close , can be set as high , low , open , ...

Volume & currency : Enable to multiply volume with price (see Features )

Amount of bars : Set amount of bars which you want to include in the Volume Profile

Max lines : maximum 1000 (if you want to use only lines, and no boxes -> max. 500, see Concepts )

🔹 Round -> ' Round/Step '

Round -> see Concepts

Step -> see Concepts

🔹 Display Volume Profile

Offset: shifts the Volume Profile (max. 500 bars to the right of last bar, see Features )

Max width Volume Profile: largest volume will be x bars wide, the rest is displayed as a ratio against largest volume (see Features )

Show table : Show details (see Features )

🔶 LIMITATIONS

• Lines won't go further than first bar (coded).

• The Volume Profile can be placed maximum 500 bar to the right of last price.

• Maximum 500 lines/boxes can be displayed

Developing Market Profile / TPO [Honestcowboy]The Developing Market Profile Indicator aims to broaden the horizon of Market Profile / TPO research and trading. While standard Market Profiles aim is to show where PRICE is in relation to TIME on a previous session (usually a day). Developing Market Profile will change bar by bar and display PRICE in relation to TIME for a user specified number of past bars.

What is a market profile?

"Market Profile is an intra-day charting technique (price vertical, time/activity horizontal) devised by J. Peter Steidlmayer. Steidlmayer was seeking a way to determine and to evaluate market value as it developed in the day time frame. The concept was to display price on a vertical axis against time on the horizontal, and the ensuing graphic generally is a bell shape--fatter at the middle prices, with activity trailing off and volume diminished at the extreme higher and lower prices."

For education on market profiles I recommend you search the net and study some profitable traders who use it.

Key Differences

Does not have a value area but distinguishes each column in relation to the biggest column in percentage terms.

Updates bar by bar

Does not take sessions into account

Shows historical values for each bar

While there is an entire education system build around Market Profiles they usually focus on a daily profile and in some cases how the value area develops during the day (there are indicators showing the developing value area).

The idea of trading based on a developing value area is what inspired me to build the Developing Market Profile.

🟦 CALCULATION

Think of this Developing Market Profile the same way as you would think of a moving average. On each bar it will lookback 200 bars (or as user specified) and calculate a Market Profile from those bars (range).

🔹Market Profile gets calculated using these steps:

Get the highest high and lowest low of the price range.

Separate that range into user specified amount of price zones (all spaced evenly)

Loop through the ranges bars and on each bar check in which price zones price was, then add +1 to the zones price was in (we do this using the OccurenceArray)

After it looped through all bars in the range it will draw columns for each price zone (using boxes) and make them as wide as the OccurenceArray dictates in number of bars

🔹Coloring each column:

The script will find the biggest column in the Profile and use that as a reference for all other columns. It will then decide for each column individually how big it is in % compared to the biggest column. It will use that percentage to decide which color to give it, top 20% will be red, top 40% purple, top 60% blue, top 80% green and all the rest yellow. The user is able to adjust these numbers for further customisation.

The historical display of the profiles uses plotchar() and will not only use the color of the column at that time but the % rating will also decide transparancy for further detail when analysing how the profiles developed over time. Each of those historical profiles is calculated using its own 200 past bars. This makes the script very heavy and that is why it includes optimisation settings, more info below.

🟦 USAGE

My general idea of the markets is that they are ever changing and that in studying that changing behaviour a good trader is able to distinguish new behaviour from old behaviour and adapt his approach before losing traders "weak hands" do.

A Market Profile can visually show a trader what kind of market environment we currently are in. In training this visual feedback helps traders remember past market environments and how the market behaved during these times.

Use the history shown using plotchars in colors to get an idea of how the Market Profile looked at each bar of the chart.

This history will help in studying how price moves at different stages of the Market Profile development.

I'm in no way an expert in trading Market Profiles so take this information with a grain of salt. Below an idea of how I would trade using this indicator:

🟦 SETTINGS

🔹MARKET PROFILING

Lookback: The amount of bars the Market Profile will look in the past to calculate where price has been the most in that range

Resolution: This is the amount of columns the Market Profile will have. These columns are calculated using the highest and lowest point price has been for the lookback period

Resolution is limited to a maximum of 32 because of pinescript plotting limits (64). Each plotchar() because of using variable colors takes up 2 of these slots

🔹VISUAL SETTINGS

Profile Distance From Chart: The amount of bars the market profile will be offset from the current bar

Border width (MP): The line thickness of the Market Profile column borders

Character: This is the character the history will use to show past profiles, default is a square.

Color theme: You can pick 5 colors from biggest column of the Profile to smallest column of the profile.

Numbers: these are for % to decide column color. So on default top 20% will be red, top 40% purple... Always use these in descending order

Show Market Profile: This setting will enable/disable the current Market Profile (columns on right side of current bar)

Show Profile History: This setting will enable/disable the Profile History which are the colored characters you see on each bar

🔹OPTIMISATION AND DEBUGGING

Calculate from here: The Market Profile will only start to calculate bar by bar from this point. Setting is needed to optimise loading time and quite frankly without it the script would probably exceed tradingview loading time limits.

Min Size: This setting is there to avoid visual bugs in the script. Scaling the chart there can be issues where the Market Profile extends all the way to 0. To avoid this use a minimum size bigger than the bugged bottom box

LNL Scalper ArrowsLNL Scalper Arrows

The indicator consist of various different types of candlestick patterns that are truly time tested by multiple veteran traders. These arrows are a combination of short-term scalping strategies taught by Linda Raschke & a trader that goes by name Quant Trade Edge. These strategies/patterns occur regularly within the markets. They offer high probability quick moves during the trending days. These four patterns are based on pure price action, no oscillators, no trend, no momentum indicators involved. Trend (ema) is there just as a simple trend gauge.

LNL Scalper Arrows were designed specifically for intra-day trading. Mostly useful for the futures but also stocks as well. These arrows can work anywhere between the fast-moving 512 or 1600 tick charts to a 1min, 2min and up to 5min or 10min charts.

Trend Gauge (Exponential Moving Average)

Nothing fancy just a classic EMA that can guide the direction of the short-term trend. I have added a custom coloring of the EMA that is based on a simple RSI filter. That should help to visualize the non-directional moments within the trend. Although the length is adjustable, for scalping it is better to focus on smaller periods such as 9, 13 or 20 or 34 but anything above 50 loses its purpose as a short-term trend gauge. Again, this is a scalping tool not a trend tool, you are not going to get rid of the fakeouts by increasing the period of the trend.

Tail Arrows (Eat the Tail Pattern)

Tail is a candlestick that is either a price rejection spike, or a flag continuation pattern on a lower time frame. A failed action. It is basically a candle with much bigger wick (shadow) of the candle than the actual body. Such candles are usually telling us about strong participation from the other side of the market. Eat the tail pattern occurs whenever the low of the Tail candle is immediately broken on a following candle "the tail is eaten alive". Such a breaks occurs in a most aggressive types of markets with a strong momentum. DO NOT try to trade this in a low volume or a ranging market. Tail Arrows are the most aggressive arrows & should be only used on the highest volume or a parabolic momentum markets.

Scalp Arrows (Scallop Pattern)

Known as Scallops or minor lows or highs, these patterns are the most common within the all scalper arrows. They occur regularly on 1min & 5min charts - basically everyday. Scallops provide the best possible risk to reward entry within the trend without the need of any indicators or oscillators. The Scallop Up 3 bar pattern consist of a high that is lower that the previous high but also low that is lower than the previous low. Scallop Up or a minor low triggers when the last high is broken, creating a three bar mountain or a peak within the 5 bar span.

Hoagie Arrows (Hoagie Pattern)

Hoagies occur way less often than any other scalping patterns. Hoagies represent two (or more) inside candles within the shadow of a first candle. Such a formation is creating a small compression or a range that sooner or later breaks out. The hoagie is triggered whenever the high or low of the shadow (first) candle is broken. The great thing about the hoagies is that they can work either way despite the trend direction. Although this indicator is coded for the 2 bar hoagies, there are no limitations on how much inside bars can hoagie include.

Umbrella Arrows (Umbrella Pattern)

Another really awesome 3 bar pattern that is really fun to trade. Umbrella occurs when the candle before the previous candle is a pin bar or a tail bar and the body of the previous candle is within the shadow or a wick of the candle before. The umbrella is triggered once the high or low of the previous bar is broken. Umbrellas are more frequent than Hoagies but occur much less than the Scallops.

Outside Bar Wedges (Outside Bar Pattern)

Pretty much self-explanatory candlestick pattern. Outside Bar is basically any bar that peaks outside of the both ends of the previous candle. So the range of the candle is higher & it looked beyond the high and beyond the low of the previous candle. These candles are signalizing the potenial momentum change. Ouside Bars usually occur at the tops or bottoms of the moves. I decided to add them because they can serve as a great addition to these scalping patterns.

Signal vs. SignalBreak Mode

The trigger can be viewed in two different ways:

1. Signal: Plots the trigger before the trigger bar, basically right when the pattern is formed but NOT YET triggered. The signal is triggered once the next candle break the high or low of the current candle.

2. SignalBrake: Plots the trigger after the break of the high or low of the actual pattern. It is basically a candle after the signal candle. (Signal is better for trading because it gives you time to prepare for the actual break of the high or low = the actual signal. SignalBrake is great for looking back in history only for the patterns that actually traded).

Pin Bar BTW Ratio

Pin Bar (Body-To-Wick) Ratio represents the size of the body of a pin bar candle for Eat the Tail and Umbrella patterns. Pin Bar BTW Ratio measures the ratio between the wick & the body of the candle. Ref. interval is 2.0 - 5.0 (ideal pin bar is 2.0 - 3.0 = the wick or a shadow is 2x - 3x bigger than the body of the candle)

ATR Stop & Target Labels

I also created three simple labels (tables) that can show you the ideal target & stop as well as the current ATR. Since LNL Scalper Arrows consist of high probability scalping patterns, a good rule of thumb to follow is to use a half of the current ATR as a target and a current ATR as a stop (or two times the target). So if the current 7 period ATR is 30 the target would be 15 pts. and a stop around 30 pts. With such a risk management you should aim for a win rate 70% or higher. Obviously you can adjust the risk management in the settings to your personal preference.

Low Range vs. High Range Markets

There are two major downsides with the Scalper Arrows:

1. You need volume and a volatility. These patterns really do struggle in ranging "boring" sideways action. It is absolutely crucial to recognize the current market environment and really stay cautions and (or completely out) in case the chop continues. Adding something like DMI can help you recognize the potential flat markets.

2. Not only do you need volume & momentum, you also need a decent range. This indicator works better on a rangy market such as NQ futures or YM. But are much tougher to trade on lower range markets such as some stocks or ZB futures or basically any other lower range market.

Hope it helps.

libhs.log.DEMO◼ Overview

This is a demonstration of dual logging library I have ported from my personal use for public use. Please start bar replay from Bar#4, and progress automatically slowly or manually.You would need to go through 450+ bars to see the full capability.

Logger=A dual logging library for developers. Tradingview lacks logging capability. This library provided logging while developing your scripts and is to be used by developers when developing and debugging their scripts.

Using this library would potentially slow down you scripts. Hence, use this for debugging only. Once your code is as you would like it to be, remove the logging code.

◼︎ Usage (Console):

Console = A sleek single cell logging with a limit of 4096 characters. When you dont need a large logging capability.

//@version=5

indicator("demo.Console", overlay=true)

plot(na)

import GETpacman/log/2 as logger

var console = logger.log.new()

console.init() // init() should be called as first line after variable declaration

console.FrameColor:=color.green

console.log('\n')

console.log('\n')

console.log('Hello World')

console.log('\n')

console.log('\n')

console.ShowStatusBar:=true

console.StatusBarAtBottom:=true

console.FrameColor:=color.blue //settings can be changed anytime before show method is called. Even twice. The last call will set the final value

console.ShowHeader:=false //this wont throw error but is not used for console

console.show(position=position.bottom_right) //this should be the last line of your code, after all methods and settings have been dealt with.

◼︎ Usage (Logx):

Logx = Multiple columns logging with a limit of 4096 characters each message. When you need to log large number of messages.

//@version=5

indicator("demo.Logx", overlay=true)

plot(na)

import GETpacman/log/2 as logger

var logx = logger.log.new()

logx.init() // init() should be called as first line after variable declaration

logx.FrameColor:=color.green

logx.log('\n')

logx.log('\n')

logx.log('Hello World')

logx.log('\n')

logx.log('\n')

logx.ShowStatusBar:=true

logx.StatusBarAtBottom:=true

logx.ShowQ3:=false

logx.ShowQ4:=false

logx.ShowQ5:=false

logx.ShowQ6:=false

logx.FrameColor:=color.olive //settings can be changed anytime before show method is called. Even twice. The last call will set the final value

logx.show(position=position.top_right) //this should be the last line of your code, after all methods and settings have been dealt with.

◼︎ Fields (with default settings)

▶︎ IsConsole = True Log will act as Console if true, otherwise it will act as Logx

▶︎ ShowHeader = True (Log only) Will show a header at top or bottom of logx.

▶︎ HeaderAtTop = True (Log only) Will show the header at the top, or bottom if false, if ShowHeader is true.

▶︎ ShowStatusBar = True Will show a status bar at the bottom

▶︎ StatusBarAtBottom = True Will show the status bar at the bottom, or top if false, if ShowHeader is true.

▶︎ ShowMetaStatus = True Will show the meta info within status bar (Current Bar, characters left in console, Paging On Every Bar, Console dumped data etc)

▶︎ ShowBarIndex = True Logx will show column for Bar Index when the message was logged. Console will add Bar index at the front of logged messages

▶︎ ShowDateTime = True Logx will show column for Date/Time passed with the logged message logged. Console will add Date/Time at the front of logged messages

▶︎ ShowLogLevels = True Logx will show column for Log levels corresponding to error codes. Console will log levels in the status bar

▶︎ ReplaceWithErrorCodes = True (Log only) Logx will show error codes instead of log levels, if ShowLogLevels is switched on

▶︎ RestrictLevelsToKey7 = True Log levels will be restricted to Ley 7 codes - TRACE, DEBUG, INFO, WARNING, ERROR, CRITICAL, FATAL

▶︎ ShowQ1 = True (Log only) Show the column for Q1

▶︎ ShowQ2 = True (Log only) Show the column for Q2

▶︎ ShowQ3 = True (Log only) Show the column for Q3

▶︎ ShowQ4 = True (Log only) Show the column for Q4

▶︎ ShowQ5 = True (Log only) Show the column for Q5

▶︎ ShowQ6 = True (Log only) Show the column for Q6

▶︎ ColorText = True Log/Console will color text as per error codes

▶︎ HighlightText = True Log/Console will highlight text (like denoting) as per error codes

▶︎ AutoMerge = True (Log only) Merge the queues towards the right if there is no data in those queues.

▶︎ PageOnEveryBar = True Clear data from previous bars on each new bar, in conjuction with PageHistory setting.

▶︎ MoveLogUp = True Move log in up direction. Setting to false will push logs down.

▶︎ MarkNewBar = True On each change of bar, add a marker to show the bar has changed

▶︎ PrefixLogLevel = True (Console only) Prefix all messages with the log level corresponding to error code.

▶︎ MinWidth = 40 Set the minimum width needed to be seen. Prevents logx/console shrinking below these number of characters.

▶︎ TabSizeQ1 = 0 If set to more than one, the messages on Q1 or Console messages will indent by this size based on error code (Max 4 used)

▶︎ TabSizeQ2 = 0 If set to more than one, the messages on Q2 will indent by this size based on error code (Max 4 used)

▶︎ TabSizeQ3 = 0 If set to more than one, the messages on Q2 will indent by this size based on error code (Max 4 used)

▶︎ TabSizeQ4 = 0 If set to more than one, the messages on Q2 will indent by this size based on error code (Max 4 used)

▶︎ TabSizeQ5 = 0 If set to more than one, the messages on Q2 will indent by this size based on error code (Max 4 used)

▶︎ TabSizeQ6 = 0 If set to more than one, the messages on Q2 will indent by this size based on error code (Max 4 used)

▶︎ PageHistory = 0 Used with PageOnEveryBar. Determines how many historial pages to keep.

▶︎ HeaderQbarIndex = 'Bar#' (Logx only) The header to show for Bar Index

▶︎ HeaderQdateTime = 'Date' (Logx only) The header to show for Date/Time

▶︎ HeaderQerrorCode = 'eCode' (Logx only) The header to show for Error Codes

▶︎ HeaderQlogLevel = 'State' (Logx only) The header to show for Log Level

▶︎ HeaderQ1 = 'h.Q1' (Logx only) The header to show for Q1

▶︎ HeaderQ2 = 'h.Q2' (Logx only) The header to show for Q2

▶︎ HeaderQ3 = 'h.Q3' (Logx only) The header to show for Q3

▶︎ HeaderQ4 = 'h.Q4' (Logx only) The header to show for Q4

▶︎ HeaderQ5 = 'h.Q5' (Logx only) The header to show for Q5

▶︎ HeaderQ6 = 'h.Q6' (Logx only) The header to show for Q6

▶︎ Status = '' Set the status to this text.

▶︎ HeaderColor Set the color for the header

▶︎ HeaderColorBG Set the background color for the header

▶︎ StatusColor Set the color for the status bar

▶︎ StatusColorBG Set the background color for the status bar

▶︎ TextColor Set the color for the text used without error code or code 0.

▶︎ TextColorBG Set the background color for the text used without error code or code 0.

▶︎ FrameColor Set the color for the frame around Logx/Console

▶︎ FrameSize = 1 Set the size of the frame around Logx/Console

▶︎ CellBorderSize = 0 Set the size of the border around cells.

▶︎ CellBorderColor Set the color for the border around cells within Logx/Console

▶︎ SeparatorColor = gray Set the color of separate in between Console/Logx Attachment

◼︎ Methods (summary)

● init ▶︎ Initialise the log

● log ▶︎ Log the messages. Use method show to display the messages

● page ▶︎ Clear messages from previous bar while logging messages on this bar.

● show ▶︎ Shows a table displaying the logged messages

● clear ▶︎ Clears the log of all messages

● resize ▶︎ Resizes the log. If size is for reduction then oldest messages are lost first.

● turnPage ▶︎ When called, all messages marked with previous page, or from start are cleared

● dateTimeFormat ▶︎ Sets the date time format to be used when displaying date/time info.

● resetTextColor ▶︎ Reset Text Color to library default

● resetTextBGcolor ▶︎ Reset Text BG Color to library default

● resetHeaderColor ▶︎ Reset Header Color to library default

● resetHeaderBGcolor ▶︎ Reset Header BG Color to library default

● resetStatusColor ▶︎ Reset Status Color to library default

● resetStatusBGcolor ▶︎ Reset Status BG Color to library default

● setColors ▶︎ Sets the colors to be used for corresponding error codes

● setColorsBG ▶︎ Sets the background colors to be used for corresponding error codes. If not match of error code, then text color used.

● setColorsHC ▶︎ Sets the highlight colors to be used for corresponding error codes.If not match of error code, then text bg color used.

● resetColors ▶︎ Reset the colors to library default (Total 36, not including error code 0)

● resetColorsBG ▶︎ Reset the background colors to library default

● resetColorsHC ▶︎ Reset the highlight colors to library default

● setLevelNames ▶︎ Set the log level names to be used for corresponding error codes. If not match of error code, then empty string used.

● resetLevelNames ▶︎ Reset the log level names to library default. (Total 36) 1=TRACE, 2=DEBUG, 3=INFO, 4=WARNING, 5=ERROR, 6=CRITICAL, 7=FATAL

● attach ▶︎ Attaches a console to an existing Logx, allowing to have dual logging system independent of each other

● detach ▶︎ Detaches an already attached console from Logx

Orion:SagittaSagitta

Sagitta is an indicator the works to assist in the validation of potential long entries and to place stop-loss orders. Sagitta is not a "golden indicator" but more of a confirmation indicator of what prices might be suggesting.

The concept is that while stocks can turn in one bar, it usually takes two bars or more to signal a turn. So, using a measurement of two bars help determine the potential turning of prices.

Behind the scenes, Sagitta is nothing more than a 2 period stochastic which has had its values divided into five specific zones.

Dividing the range of the two bars in five sections, the High is equal to 100 and the Low is equal to 0.

The zones are:

20 = bearish (red) – This is when the close is the lower 20% of the two bars

40 = bearish (orange) – This is when the close is between the lower 20% and 40% of the two bars.

60 = neutral (yellow) – This is when the close is between the middle 40% - 60% of the two bars.

80 = bullish (blue) – This is when the close is between the upper 60% - 80% of the two bars.

100 = bullish (green) – This is when the close is above the upper 80% of the bar.

The general confirmation concept works as such:

When the following bar is of a higher value than the previous bar, there is potential for further upward price movement. Conversely when the following bar is lower than the previous bar, there is potential for further downward movement.

Going from a red bar to orange bar Might be an indication of a positive turn in direction of prices.

Going from a green bar to an orange bar would also be considered a negative directional turn of prices.

When the follow on bar decreases (ie, green to blue, blue to yellow, etc) placing a stop-loss would be prudent.

Maroon lines in the middle of a bar is an indication that prices are currently caught in consolidation.

Silver/Gray bars indicate that a high potential exists for a strong upward turn in prices exists.

Consolidation is calculated by determining if the close of one bar is between the high and low of another bar. This then establishes the range high and low. As long as closes continue with this range, the high and low of the range can expand. When the close is outside of the range, the consolidation is reset.

Signals in areas of consolidation (maroon center bar) should be looked upon as if the prices are going to challenge the high of the consolidation range and not necessarily break through.

The entry technique used is:

The greater of the following two calculations:

High of signal bar * 1.002 or High of signal bar + .03

The stop-loss technique used is:

The lesser of the following two calculations:

Low of signal bar * .998 or Low of signal bar - .03

IF an entry signal is generated and the price doesn’t reach the entry calculation. It is considered a failed entry and is not considered a negative or that you missed out on something. This has saved you from losing money since the prices are not ready to commit to the direction.

When placing a stop-loss, it is never suggested that you lower the value of a stop-loss. Always move your stop-losses higher in order to lock in profit in case of a negative turn.

Strat Dashboard [TFO]The Strat Dashboard tracks up to 10 signals while highlighting common strat reversal patterns, the SSS 50% rule, timeframe continuity, and some additional criteria with VWAP and moving averages.

With the strat, all price action bars/candles are simplified into 3 total possibilities: 1 (inside bar), 2 (a bar that takes the previous bar's high OR low), and 3 (outside bar). The first table column for Last X Candles shows the most recent candles according to this notation, for example, 1 - 2D - 2U. This would mean we had an inside bar, followed by a bar that took the previous bar's low, followed then by a bar that took the previous bar's high. Note that the colors in this column are set according to whether the current bar's close exceeds the previous bar's high/low. By default, these colors are green if above the previous bar's highs, or red if below the previous bar's lows. If the current close is in between the previous candle's high and low (even after already taking the prior high or low), no color will be applied.

The SSS 50% column shows a yes or no value for whether the current bar aligns with the SSS 50% rule, where a bar has taken either the previous high or low, and has since reversed to at least the midway point of the previous bar's height - essentially anticipating a 2 that may become a 3 (outside bar).

Timeframe continuity (TFC) shows a yes or no value for when the current candle on multiple timeframes are all green or red (above the open price or below the open price, respectively). For example, if you were looking at the current 15m, 1h, and 1D bars, and they were all above the open price, you could say there's TFC between all three timeframes. As of the initial release, you can select up to 3 different timeframes. The table values will only be true when all selected timeframes are in alignment. When setting alerts, first deselect the timeframes if you don't want TFC logic to impact alerts.

The "Last" column shows the last strat reversal pattern that was confirmed (after the last bar closes). Waiting for a candle close is the safer option since a 2 can turn into a 3; however for higher timeframes, it may be beneficial to make an update to this indicator in which you can have live alerts as well (not waiting for a candle close). You can select which strat reversals you want to be shown from the settings. Various strat reversals may be selected for alerts of type "Any"; for example, if setting up an alert for "Any" strat reversal on Symbol 1, then this alert will go off when any of the *selected* strat reversals occur for that specific symbol. Deselect any strat reversals that you don't want to be included in these alerts.

Lastly, the EMA and VWAP columns simply show whether price is above or below said value. This tracks the current candle close, and may repaint/change several times if the current bar is oscillating above and below these values.

Swing Levels and Liquidity - By LeviathanThis script will plot pivot points (swing highs and lows) in the form of lines, boxes or labels to help you identify market structure, “liquidity” areas, swing failure patterns, etc. You are also able to see the volume traded at each pivot point, which will help you compare their significance.

Bars Left-Right

A pivot high (swing high) is a bar in a series of bars that has a higher value than the bars around it and a pivot low (swing low) is a bar in a series of bars that has a lower value than the bars surrounding it. The Bars Left and Bars Right parameters are used to define the number of bars on the left and right sides of a pivot point that the function should consider when identifying pivot highs and lows in a time series. For example, if Bars Left is set to 5 and Bars Right is set to 6, the function will look for a pivot point by comparing the value of the current bar with the values of the 5 bars to its left and the 6 bars to its right. If the value of the current bar is higher than all of these bars, it is considered a pivot high point. These parameter can be used to adjust the sensitivity of the script (lowering the Bars Left and Bars Right parameters will give you more swing points and increasing the Bars Left and Bars Right parameters will give you fewer swing points).

”Show Boxes” - This will draw a box above the swing high and a box below the swing low to help you visualise a large area of interest around swing points. Additional box types and the width of the box can be adjusted in Appearance settings below.

”Show Lines” - This will draw a horizontal line at the level of each swing high and swing low.

”Show Labels” - This will plot a circle at the high point of each swing high and at the low point of each swing low.

”Show Volume” - This will display the amount of volume traded in a given swing point candle. It can help you identify the significance of a given swing point by comparing it to the volumes of other swing points.

”Extend Until Filled” - This will extend the swing point levels until they are mitigated by the price. Turning it off will continue plotting the levels just a few more bars after a swing point occurs.

”Appearance” - You can show/hide swing points, choose the colors of labels, lines and boxes, choose the size and positioning of the text, choose line and box appearance (adjust the Box Width when switching between timeframes!) and more.

More updates coming soon (MTF, more data…)

Simple STRAT Tool by nnamWhat this Indicator Does

This indicator is a very simple tool created specifically for experienced Straters. It was created for those Straters who fully understand the 1-2-3 Strat Scenarios, are in need of an easy to use tool, and do not want or need a lot of messy markings on their chart.

The indicator simply allows the user to color code the Strat 1, 2 ,3 (Inside /Outside /Up / Down) Bars as desired and by default extends lines to the right of the chart from the Highs and Lows of the previous 2 Bars giving the user a simple reference for Strat scenario structure breaks.

As shown above, the bars are color coded, but the original bar color is maintained via the border and wick.

If a bar is an Outside Bar or an Inside Bar, it is still easy to identify whether or not the bar was a Bullish or Bearish 1 or 3.

The same goes for 2UP and 2Down Bars - It is easy to identify Bullish or Bearish UP or DOWN Bars.

Optionally, as show in the screenshot below, the user can extend the lines in both directions to get an "at a glance" better understanding of where price is currently vs previous support and resistance areas.

For Straters that prefer to trade only INSIDE BAR BREAKOUTS there is an optional input setting labeled "Trade Inside Bars ONLY".

This setting turns OFF the lines that extend from the 2nd previous bar back and only displays and extend lines from the previous bar IF and ONLY IF the current bar is an INSIDE (one) bar. .

The User Input settings allow for the following customizations:

1. Custom Outside Bar Color

2. Custom Inside Bar Color

3. Custom 2 Up Bar Color

4. Custom 2 Down Bar Color

5. Turn ON or OFF color coded bars

6. Trade only INSIDE Bar Breakouts

7. Extend Lines Both Directions

8. Hide all Lines

The customizable settings above allow the user to hide all lines and turn OFF color coding without having to fully remove the indicator from the chart. This is convenient when the user has another indicator that uses color coded bars or the lines conflict with another indicator and they need to be temporarily disabled.

If you have any questions regarding this indicator please let me know. If you have any suggestions for minor tweaks to the indicator do not hesitate to ask for them.

I hope you enjoy this indicator and get some usefulness from it... HAPPY TRADING!!

Signs of the Times [LucF]█ OVERVIEW

This oscillator calculates the directional strength of bars using a primitive weighing mechanism based on a small number of what I consider to be fundamental properties of a bar. It does not consider the amplitude of price movements, so can be used as a complement to momentum-based oscillators. It thus belongs to the same family of indicators as my Bar Balance , Volume Ticks , Efficient work , Volume Buoyancy or my Delta Volume indicators.

█ CONCEPTS

The calculations underlying Signs of the Times (SOTT) use a simple, oft-explored concept: measure bar attributes, assign a weight to them, and aggregate results to provide an evaluation of a bar's directional strength. Bull and bear weights are added independently, then subtracted and divided by the maximum possible weight, so the final calculation looks like this:

(up - dn) / weightRange

SOTT has a zero centerline and oscillates between +1 and -1. Ten elementary properties are evaluated. Most carry a weight of one, a few are doubly weighted. All properties are evaluated using only the current bar's values or by comparing its values to those of the preceding bar. The bull conditions follow; their inverse applies to bear conditions:

Weight of 1

• Bar's close is greater than the bar's open (bar is considered to be of "up" polarity)

• Rising open

• Rising high

• Rising low

• Rising close

• Bar is up and its body size is greater than that of the previous bar

• Bar is up and its body size is greater than the combined size of wicks

Weight of 2

• Gap to the upside

• Efficient Work when it is positive

• Bar is up and volume is greater than that of the previous bar (this only kicks in if volume is actually available on the chart's data feed)

Except for the Efficient Work weight, which is a +1 to -1 float value multiplied by 2, all weights are discrete; either zero or the full weight of 1 or 2 is generated. This will cause any gap, for example, to generate a weight of +2 or -2, regardless of the gap's size. That is the reason why the oscillator is oblivious to the amplitude of price movements.

You can see the code used to calculate SOTT in my ta library 's `sott()` function.

█ HOW TO USE THE INDICATOR

No videos explain this indicator and none are planned; reading this description or the script's code is the only way to understand what Signs of the Times does.

Load the indicator on an active chart (see here if you don't know how).

The default configuration displays:

• An Arnaud-Legoux moving average of length 20 of the instant SOTT value. This is the signal line.

• A fill between the MA and the centerline.

• Levels at arbitrary values of +0.3 and -0.3.

• A channel between the signal line and its MA (a simple MA of length 20), which can be one of four colors:

• Bull (green): The signal line is above its MA.

• Strong bull (lime): The bull condition is fulfilled and the signal line is above the centerline.

• Bear (red): The signal line is below its MA.

• Strong bear (pink): The bear condition is fulfilled and the signal line is below the centerline.

The script's "Inputs" tab allows you to:

• Choose a higher timeframe to calculate the indicator's values. This can be useful to get a wider perspective of the indicator's values.

If you elect to use a higher timeframe, make sure that your chart's timeframe is always lower than the higher timeframe you specified,

as calculating on a timeframe lower than the chart's does not make much sense because the indicator is then displaying only the value of the last intrabar in the chart bar.

• Specify the type of MA used to produce the signal line. Use a length of 1 or the Data Window to see the instant value of SOTT. It is quite noisy, thus the need to average it.

• Specify the type of MA applied to the signal line. The idea here is to provide context to the signal.

• Control the display and colors of the lines and fills.

The first pane of this publication's chart shows the default setup. The second one shows only a monochrome signal line.

Using the "Style" tab of the indicator's settings, you can change the type and width of the lines, and the level values.

█ INTERPRETATION

Remember that Signs of the Times evaluates directional bar strength — not price movement. Its highs and lows do not reflect price, but the strength of chart bars. The fact that SOTT knows nothing of how far price moves or of trends is easy to forget. As such, I think SOTT is best used as a confirmation tool. Chart movements may appear to be easy to read when looking at historical bars, but when you have to make go-no-go decisions on the last bar, the landscape often becomes murkier. By providing a quantitative evaluation of the strength of the last few bars, which is not always easily discernible by simply looking at them, SOTT aims to help you decide if the short-term past favors the bets you are considering. Can SOTT predict the future? Of course not.

While SOTT uses completely different calculations than classical momentum oscillators, its profile shares many of their characteristics. This could lead one to infer that directional bar strength correlates with price movement, which could in turn lead one to conclude that indicators such as this one are useless, or that they can be useful tools to confirm momentum oscillators or other models of price movement. The call is, of course, up to you. You can try, for example, to compare a Wilder MA of SOTT to an RSI of the same length.

One key difference with momentum oscillators is that SOTT is much less sensitive to large price movements. The default Arnaud-Legoux MA used for the signal line makes it quite active; you can use a more quiet SMA or EMA if you prefer to tone it down.

In systems where it can be useful to only enter or exit on short-term strength, an average of SOTT values over the last 3 to 5 bars can be used as a more quiet filter than a momentum oscillator would.

█ NOTES

My publications often go through a long gestation period where I use them on my charts or in systems before deciding if they are worth a publication. With an incubation period of more than three years, Signs of the Times holds the record. The properties SOTT currently evaluates result from the systematic elimination of contaminants over that lengthy period of time. It was long because of my usual, slow gear, but also because I had to try countless combinations of conditions before realizing that, contrary to my intuition, best results were achieved by:

• Keeping the number of evaluated properties to the absolute minimum.

• Limiting the evaluation's scope to the current and preceding bar.

• Choosing properties that, in my view, were unmistakably indicative of bullish/bearish conditions.

Repainting

As most oscillators, the indicator provides live realtime values that will recalculate with chart updates. It will thus repaint in real time, but not on historical values. To learn more about repainting, see the Pine Script™ User Manual's page on the subject .

Impactful pattern and candles pattern AlertThe Alertion indicator!

impactful pattern:

pattern that happen near the zone or in the zone at lower timeframe and give us entry and stop limit price.

It is helpful for price action traders and those who want to decrease their risk.

There are 3 IP patterns:

Quasimodo

Head and shoulder

whipsaw engulfing

These patterns may occur near the zone or may not occur but by them, you can decrease your trading risk for example you can

trade with half lot before IP pattern and enter with other half after pattern.

how to use?

for example:

you find zone at 1h timeframe for short position

when price enter to your zone

you run this indicator and choose your lower timeframe, for example 15m and click on short position.

Then make the alert by right-click on your chart and choose the add alert and at condition box choose the impactful pattern and then click on create

now wait for message :)

Candles pattern:

like reversal bar, key reversal bar, exhaustion bar, pin bar, two-bar reversal, tree-bar reversal, inside bar, outside bar

these occur when the trend turn, so it is usable when the price enter to your zone or near your zone.

This pattern can decrease your risk.

Inside bar and outside bar:

if this pattern engulf up, it is bullish pattern and if engulf down, it is bearish pattern.

what does this indicator do?

this indicator is for making alert

it helps you to decrease your risk and failure.

You optimize it to alert you when IP pattern happen or candle pattern happen or inside bar or outside bar engulfing or all of them.

For IP pattern, it will message you entry and stop limit price.

It works at 2 different timeframes, so you can make alert for example in 1h TF for candles pattern and 15m TF for IP pattern.

Indicator will alert you for candles pattern at your chart timeframe and for IP pattern at timeframe you've chosen when you run the indicator, and it is changeable

in setting.

setting options

TIMEFRAME

IP: select the timeframe for IP patterns it means when IP pattern happen at that timeframe the indicator will alert you

example = your TF is 1h, you found the supply zone and want to trade, note that IP pattern happen in lower TF, so you select 15m TF or TF lower than 1h.

Short position: select it if you want to make short position.

BUFFERING

indicator send you entry and stop limit price

you can change it by amount of percent

it is your strategy to change your entry and stop loss or not

example= in head and shoulder pattern at short position, the stop limit is high price of head in pattern

so the indicator will message you the exact price but if you want to put

your stop limit 5 percent upper than exact price you can enter 5 in front of stop loss

or you want to enter 5 percent lower than exact high price of shoulder, you can optimize it.

ALERTION

you choose what alert you want

IP alert or candle alert or inside and outside bar alert

type your text for alert

you can write additional text for your message

ADVANCE

IP alert frequency option:

1. Once per bar : indicator will alert you for IP pattern once at your chat timeframe bar, and you should wait til next bar for next alert.

2. Once per bar close : alert you when your chart timeframe bar closed and next alert will happen when next bar is closed.

3. All: alert you all the times IP pattern happen

pivot left and right bars: lower will find smaller pattern

at the END:

this indicator is not strategy

it is part of your strategy that help you to increase your winning rate.

It is helpful for scalping and candle patterns finding.

After you make an alert, you can delete the indicator or change your timeframe or make another alert, your previous alert won’t change.

Thank you all.

Poly Cycle [Loxx]This is an example of what can be done by combining Legendre polynomials and analytic signals. I get a way of determining a smooth period and relative adaptive strength indicator without adding time lag.

This indicator displays the following:

The Least Squares fit of a polynomial to a DC subtracted time series - a best fit to a cycle.

The normalized analytic signal of the cycle (signal and quadrature).

The Phase shift of the analytic signal per bar.

The Period and HalfPeriod lengths, in bars of the current cycle.

A relative strength indicator of the time series over the cycle length. That is, adaptive relative strength over the cycle length.

The Relative Strength Indicator, is adaptive to the time series, and it can be smoothed by increasing the length of decreasing the number of degrees of freedom.

Other adaptive indicators based upon the period and can be similarly constructed.

There is some new math here, so I have broken the story up into 5 Parts:

Part 1:

Any time series can be decomposed into a orthogonal set of polynomials .

This is just math and here are some good references:

Legendre polynomials - Wikipedia, the free encyclopedia

Peter Seffen, "On Digital Smoothing Filters: A Brief Review of Closed Form Solutions and Two New Filter Approaches", Circuits Systems Signal Process, Vol. 5, No 2, 1986

I gave some thought to what should be done with this and came to the conclusion that they can be used for basic smoothing of time series. For the analysis below, I decompose a time series into a low number of degrees of freedom and discard the zero mode to introduce smoothing.

That is:

time series => c_1 t + c_2 t^2 ... c_Max t^Max

This is the cycle. By construction, the cycle does not have a zero mode and more physically, I am defining the "Trend" to be the zero mode.

The data for the cycle and the fit of the cycle can be viewed by setting

ShowDataAndFit = TRUE;

There, you will see the fit of the last bar as well as the time series of the leading edge of the fits. If you don't know what I mean by the "leading edge", please see some of the postings in . The leading edges are in grayscale, and the fit of the last bar is in color.

I have chosen Length = 17 and Degree = 4 as the default. I am simply making sure by eye that the fit is reasonably good and degree 4 is the lowest polynomial that can represent a sine-like wave, and 17 is the smallest length that lets me calculate the Phase Shift (Part 3 below) using the Hilbert Transform of width=7 (Part 2 below).

Depending upon the fit you make, you will capture different cycles in the data. A fit that is too "smooth" will not see the smaller cycles, and a fit that is too "choppy" will not see the longer ones. The idea is to use the fit to try to suppress the smaller noise cycles while keeping larger signal cycles.

Part 2:

Every time series has an Analytic Signal, defined by applying the Hilbert Transform to it. You can think of the original time series as amplitude * cosine(theta) and the transformed series, called the quadrature, can be thought of as amplitude * sine(theta). By taking the ratio, you can get the angle theta, and this is exactly what was done by John Ehlers in . It lets you get a frequency out of the time series under consideration.

Amazon.com: Rocket Science for Traders: Digital Signal Processing Applications (9780471405672): John F. Ehlers: Books

It helps to have more references to understand this. There is a nice article on Wikipedia on it.

Read the part about the discrete Hilbert Transform:

en.wikipedia.org

If you really want to understand how to go from continuous to discrete, look up this article written by Richard Lyons:

www.dspguru.com

In the indicator below, I am calculating the normalized analytic signal, which can be written as:

s + i h where i is the imagery number, and s^2 + h^2 = 1;

s= signal = cosine(theta)

h = Hilbert transformed signal = quadrature = sine(theta)

The angle is therefore given by theta = arctan(h/s);

The analytic signal leading edge and the fit of the last bar of the cycle can be viewed by setting

ShowAnalyticSignal = TRUE;

The leading edges are in grayscale fit to the last bar is in color. Light (yellow) is the s term, and Dark (orange) is the quadrature (hilbert transform). Note that for every bar, s^2 + h^2 = 1 , by construction.

I am using a width = 7 Hilbert transform, just like Ehlers. (But you can adjust it if you want.) This transform has a 7 bar lag. I have put the lag into the plot statements, so the cycle info should be quite good at displaying minima and maxima (extrema).

Part 3:

The Phase shift is the amount of phase change from bar to bar.

It is a discrete unitary transformation that takes s + i h to s + i h

explicitly, T = (s+ih)*(s -ih ) , since s *s + h *h = 1.

writing it out, we find that T = T1 + iT2

where T1 = s*s + h*h and T2 = s*h -h*s

and the phase shift is given by PhaseShift = arctan(T2/T1);

Alas, I have no reference for this, all I doing is finding the rotation what takes the analytic signal at bar to the analytic signal at bar . T is the transfer matrix.

Of interest is the PhaseShift from the closest two bars to the present, given by the bar and bar since I am using a width=7 Hilbert transform, bar is the earliest bar with an analytic signal.

I store the phase shift from bar to bar as a time series called PhaseShift. It basically gives you the (7-bar delayed) leading edge the amount of phase angle change in the series.

You can see it by setting

ShowPhaseShift=TRUE

The green points are positive phase shifts and red points are negative phase shifts.

On most charts, I have looked at, the indicator is mostly green, but occasionally, the stock "retrogrades" and red appears. This happens when the cycle is "broken" and the cycle length starts to expand as a trend occurs.

Part 4:

The Period:

The Period is the number of bars required to generate a sum of PhaseShifts equal to 360 degrees.

The Half-period is the number of bars required to generate a sum of phase shifts equal to 180 degrees. It is usually not equal to 1/2 of the period.

You can see the Period and Half-period by setting

ShowPeriod=TRUE

The code is very simple here:

Value1=0;

Value2=0;

while Value1 < bar_index and math.abs(Value2) < 360 begin

Value2 = Value2 + PhaseShift ;

Value1 = Value1 + 1;

end;

Period = Value1;

The period is sensitive to the input length and degree values but not overly so. Any insight on this would be appreciated.

Part 5:

The Relative Strength indicator:

The Relative Strength is just the current value of the series minus the minimum over the last cycle divided by the maximum - minimum over the last cycle, normalized between +1 and -1.

RelativeStrength = -1 + 2*(Series-Min)/(Max-Min);

It therefore tells you where the current bar is relative to the cycle. If you want to smooth the indicator, then extend the period and/or reduce the polynomial degree.

In code:

NewLength = floor(Period + HilbertWidth+1);

Max = highest(Series,NewLength);

Min = lowest(Series,NewLength);

if Max>Min then

Note that the variable NewLength includes the lag that comes from the Hilbert transform, (HilbertWidth=7 by default).

Conclusion:

This is an example of what can be done by combining Legendre polynomials and analytic signals to determine a smooth period without adding time lag.

________________________________

Changes in this one : instead of using true/false options for every single way to display, use Type parameter as following :

1. The Least Squares fit of a polynomial to a DC subtracted time series - a best fit to a cycle.

2. The normalized analytic signal of the cycle (signal and quadrature).

3. The Phase shift of the analytic signal per bar.

4. The Period and HalfPeriod lengths, in bars of the current cycle.

5. A relative strength indicator of the time series over the cycle length. That is, adaptive relative strength over the cycle length.

statisticsLibrary "statistics"

General statistics library.

erf(x) The "error function" encountered in integrating the normal

distribution (which is a normalized form of the Gaussian function).

Parameters:

x : The input series.

Returns: The Error Function evaluated for each element of x.

erfc(x)

Parameters:

x : The input series

Returns: The Complementary Error Function evaluated for each alement of x.

sumOfReciprocals(src, len) Calculates the sum of the reciprocals of the series.

For each element 'elem' in the series:

sum += 1/elem

Should the element be 0, the reciprocal value of 0 is used instead

of NA.

Parameters:

src : The input series.

len : The length for the sum.

Returns: The sum of the resciprocals of 'src' for 'len' bars back.

mean(src, len) The mean of the series.

(wrapper around ta.sma).

Parameters:

src : The input series.

len : The length for the mean.

Returns: The mean of 'src' for 'len' bars back.

average(src, len) The mean of the series.

(wrapper around ta.sma).

Parameters:

src : The input series.

len : The length for the average.

Returns: The average of 'src' for 'len' bars back.

geometricMean(src, len) The Geometric Mean of the series.

The geometric mean is most important when using data representing

percentages, ratios, or rates of change. It cannot be used for

negative numbers

Since the pure mathematical implementation generates a very large

intermediate result, we performed the calculation in log space.

Parameters:

src : The input series.

len : The length for the geometricMean.

Returns: The geometric mean of 'src' for 'len' bars back.

harmonicMean(src, len) The Harmonic Mean of the series.

The harmonic mean is most applicable to time changes and, along

with the geometric mean, has been used in economics for price

analysis. It is more difficult to calculate; therefore, it is less

popular than eiter of the other averages.

0 values are ignored in the calculation.

Parameters:

src : The input series.

len : The length for the harmonicMean.

Returns: The harmonic mean of 'src' for 'len' bars back.

median(src, len) The median of the series.

(a wrapper around ta.median)

Parameters:

src : The input series.

len : The length for the median.

Returns: The median of 'src' for 'len' bars back.

variance(src, len, biased) The variance of the series.

Parameters:

src : The input series.

len : The length for the variance.

biased : Wether to use the biased calculation (for a population), or the

unbiased calculation (for a sample set). .

Returns: The variance of 'src' for 'len' bars back.

stdev(src, len, biased) The standard deviation of the series.

Parameters:

src : The input series.

len : The length for the stdev.

biased : Wether to use the biased calculation (for a population), or the

unbiased calculation (for a sample set). .

Returns: The standard deviation of 'src' for 'len' bars back.

skewness(src, len) The skew of the series.

Skewness measures the amount of distortion from a symmetric

distribution, making the curve appear to be short on the left

(lower prices) and extended to the right (higher prices). The

extended side, either left or right is called the tail, and a

longer tail to the right is called positive skewness. Negative

skewness has the tail extending towards the left.

Parameters:

src : The input series.

len : The length for the skewness.

Returns: The skewness of 'src' for 'len' bars back.

kurtosis(src, len) The kurtosis of the series.

Kurtosis describes the peakedness or flatness of a distribution.

This can be used as an unbiased assessment of whether prices are

trending or moving sideways. Trending prices will ocver a wider

range and thus a flatter distribution (kurtosis < 3; negative

kurtosis). If prices are range-bound, there will be a clustering

around the mean and we have positive kurtosis (kurtosis > 3)

Parameters:

src : The input series.

len : The length for the kurtosis.

Returns: The kurtosis of 'src' for 'len' bars back.

excessKurtosis(src, len) The normalized kurtosis of the series.

kurtosis > 0 --> positive kurtosis --> trending

kurtosis < 0 --> negative krutosis --> range-bound

Parameters:

src : The input series.

len : The length for the excessKurtosis.

Returns: The excessKurtosis of 'src' for 'len' bars back.

normDist(src, len, value) Calculates the probability mass for the value according to the

src and length. It calculates the probability for value to be

present in the normal distribution calculated for src and length.

Parameters:

src : The input series.

len : The length for the normDist.

value : The series of values to calculate the normal distance for

Returns: The normal distance of 'value' to 'src' for 'len' bars back.

normDistCumulative(src, len, value) Calculates the cumulative probability mass for the value according

to the src and length. It calculates the cumulative probability for

value to be present in the normal distribution calculated for src

and length.

Parameters:

src : The input series.

len : The length for the normDistCumulative.

value : The series of values to calculate the cumulative normal distance

for

Returns: The cumulative normal distance of 'value' to 'src' for 'len' bars

back.

zScore(src, len, value) Returns then z-score of objective to the series src.

It returns the number of stdev's the objective is away from the

mean(src, len)

Parameters:

src : The input series.

len : The length for the zScore.

value : The series of values to calculate the cumulative normal distance

for

Returns: The z-score of objectiv with respect to src and len.

er(src, len) Calculates the efficiency ratio of the series.

It measures the noise of the series. The lower the number, the

higher the noise.

Parameters:

src : The input series.

len : The length for the efficiency ratio.

Returns: The efficiency ratio of 'src' for 'len' bars back.

efficiencyRatio(src, len) Calculates the efficiency ratio of the series.

It measures the noise of the series. The lower the number, the

higher the noise.

Parameters:

src : The input series.

len : The length for the efficiency ratio.

Returns: The efficiency ratio of 'src' for 'len' bars back.

fractalEfficiency(src, len) Calculates the efficiency ratio of the series.

It measures the noise of the series. The lower the number, the

higher the noise.

Parameters:

src : The input series.

len : The length for the efficiency ratio.

Returns: The efficiency ratio of 'src' for 'len' bars back.

mse(src, len) Calculates the Mean Squared Error of the series.

Parameters:

src : The input series.

len : The length for the mean squared error.

Returns: The mean squared error of 'src' for 'len' bars back.

meanSquaredError(src, len) Calculates the Mean Squared Error of the series.

Parameters:

src : The input series.

len : The length for the mean squared error.

Returns: The mean squared error of 'src' for 'len' bars back.

rmse(src, len) Calculates the Root Mean Squared Error of the series.

Parameters:

src : The input series.

len : The length for the root mean squared error.

Returns: The root mean squared error of 'src' for 'len' bars back.

rootMeanSquaredError(src, len) Calculates the Root Mean Squared Error of the series.

Parameters:

src : The input series.

len : The length for the root mean squared error.

Returns: The root mean squared error of 'src' for 'len' bars back.

mae(src, len) Calculates the Mean Absolute Error of the series.

Parameters:

src : The input series.

len : The length for the mean absolute error.

Returns: The mean absolute error of 'src' for 'len' bars back.

meanAbsoluteError(src, len) Calculates the Mean Absolute Error of the series.

Parameters:

src : The input series.

len : The length for the mean absolute error.

Returns: The mean absolute error of 'src' for 'len' bars back.

BE_CustomFx_LibraryLibrary "BE_CustomFx_Library"

A handful collection of regular functions, Custom Tools & Utility Functions could be used in regular Scripts. hope these functions can be understood by a non programmer like me too.

G_TextValOfNumber(ValueToConvert, RequiredDecimalPlaces, BeginingChar, EndChar) Function to return the String Value of Number with decimal precision with the prefix and suffix characters provided

Parameters:

ValueToConvert : = Number to Convert

RequiredDecimalPlaces : = No of Decimal values Required. supports to a max of 5 decimals else defaults to 2

BeginingChar : = Prefix character which is needed.

EndChar : = Suffix character which is needed.

Returns: Returns Out put with formated value of Given Number for the specified deicimal values with Prefix and suffix string

G_TradableValue(ValueToConvert, NeedCustomization, RequiredDecimalPlaces) Function to return the Tradable Value of Number

Parameters:

ValueToConvert : = Number to Convert

NeedCustomization : = set to 1 if you want to customize the decimal percision values. default is No customization needed, which provides output equalent to round_to_mintick

RequiredDecimalPlaces : = if NeedCustomization is set to 1 mention the decimal percision value required. max supported decimal is 5 else defaults to 2

Returns: Returns Out put with formated value of Given Number

G_TxtSizeForLables(SizeValue) Function to Get size Value for text values used in Lables

Parameters:

SizeValue : = auto, tiny, small, normal, large, huge. specify either of these values or default value Normal will be displayed as output

Returns: Returns Respective Text size

G_Reg_LineType(LineType) Function to Get Line Style Value for text values used in Lines

Parameters:

LineType : = 'solid (─)', 'dotted (┈)', 'dashed (╌)', 'arrow left (←)', 'arrow right (→)', 'arrows both (↔)' or default line style 'dotted (┈)' will be the output

Returns: Returns Respective Line style

G_ShapeTypeForLables(ShapeType) Function to Get Shape Style Value for text values used in plot shapes

Parameters:

ShapeType : = 'XCross', 'Cross', 'Triangle Up', 'Triangle Down', 'Flag', 'Circle','Arrow Up', 'Arrow Down','Lable Up', 'Lable Down' or default shpae style Triangle Up will be the output

Returns: Returns Respective Shape style

G_Indicator_Val(string, float, int, int) Gets Output of the technical analyis indicator which has length Parameter. RSI, ATR, EMA, SMA, HMA, WMA, VWMA, 'CMO', 'MOM', 'ROC','VWAP'

Parameters: