Hybrid Confluence (RSI,MFI,StochRSI) Two-Tier Momentum Framework

Many traders explore multi-oscillator hybrid confluence approaches that combine momentum and volume signals—most commonly RSI, Money Flow Index (MFI), and Stochastic RSI—to study stretched market conditions. These hybrid concepts are widely used to analyze potential exhaustion zones, cycle extremes, and periods of sustained buying or selling pressure across different timeframes.

This script does not replicate, reverse-engineer, or replace any paid or closed-source indicator.

Instead, it provides a fully transparent framework built exclusively from standard, well-documented technical indicators. All calculations are explicit and configurable, allowing traders to study hybrid momentum behavior without relying on proprietary logic or black-box tools.

What the Script Does

1. Builds a hybrid momentum confluence model

The script combines three widely used oscillators:

• RSI (Relative Strength Index) — price momentum

• MFI (Money Flow Index) — volume-weighted momentum

• Stochastic RSI — momentum relative to its own recent range

Each component operates on a normalized 0–100 scale, allowing meaningful comparison and aggregation.

2. Implements a clear two-tier signal structure

Instead of producing a single binary buy/sell output, the script separates early pressure from extreme conditions:

2-of-3 Confluence (Setups)

When any two of the three oscillators reach oversold or overbought levels:

• Displayed as semi-transparent circles

• Indicates building pressure or a developing condition

• Designed as a heads-up, not a trade signal

3-of-3 Confluence (Signals)

When all three oscillators reach oversold or overbought levels:

• Displayed as prominent vertical bars spanning the oscillator range

• Represents extreme momentum alignment

• Intended to highlight potential exhaustion zones

3. Visualizes sustained pressure using consecutive signal intensity

When 3-of-3 conditions persist across multiple bars:

• Each consecutive bar becomes progressively darker

• Up to six discrete intensity levels

• Darkness reflects duration and persistence, not prediction

This helps visualize scenarios where markets continue pushing higher or lower before a major turning point, rather than assuming a single signal marks the exact top or bottom.

4. Works across markets and timeframes

Because all inputs rely on standard technical indicators:

• Works on crypto, equities, futures, and FX

• Scales naturally from intraday to higher timeframes

• Can be used on Daily and multi-day charts for macro context

Why This Script Is Useful

Traditional oscillators often produce isolated signals that lack context. This framework adds clarity by:

1. Requiring multi-indicator agreement instead of single-signal triggers

2. Separating early pressure from extreme conditions

3. Showing how momentum can persist before a reversal

4. Avoiding binary “buy now / sell now” outputs

5. Remaining transparent and configurable

This makes the tool especially useful for:

• Swing traders

• Macro and cycle-focused traders

• Crypto traders studying extended momentum phases

• Analysts who prefer contextual signals over rigid rules

How to Use

1. Adjust RSI, MFI, and StochRSI lengths to suit your timeframe

2. Observe 2-of-3 circles as early warnings of building pressure

3. Watch 3-of-3 bars for extreme momentum alignment

4. Note increasing bar intensity as pressure persists

5. Combine with structure, trend, volume, or price action for decisions

This script is best used as a contextual tool, not a standalone trading system.

What This Script Is Not

• Not a recreation of any paid or proprietary indicator

• Not affiliated with any trading educator or platform

• Not intended as a predictive or standalone trading system

• Does not claim to identify exact tops or bottoms

All signals are derived solely from openly documented RSI, MFI, and Stochastic RSI calculations.

Important Notes

• This script is original, with a transparent methodology

• All calculations use standard, well-known technical formulas

• No hidden logic or undisclosed weighting is used

• Signal visuals are descriptive, not predictive

Disclaimer

This tool is provided for educational and analytical purposes only.

It does not constitute financial advice or a recommendation to trade.

Always validate settings, test on multiple assets and timeframes, and use proper risk management before trading live.

Search in scripts for "binary"

Dimensional Resonance ProtocolDimensional Resonance Protocol

🌀 CORE INNOVATION: PHASE SPACE RECONSTRUCTION & EMERGENCE DETECTION

The Dimensional Resonance Protocol represents a paradigm shift from traditional technical analysis to complexity science. Rather than measuring price levels or indicator crossovers, DRP reconstructs the hidden attractor governing market dynamics using Takens' embedding theorem, then detects emergence —the rare moments when multiple dimensions of market behavior spontaneously synchronize into coherent, predictable states.

The Complexity Hypothesis:

Markets are not simple oscillators or random walks—they are complex adaptive systems existing in high-dimensional phase space. Traditional indicators see only shadows (one-dimensional projections) of this higher-dimensional reality. DRP reconstructs the full phase space using time-delay embedding, revealing the true structure of market dynamics.

Takens' Embedding Theorem (1981):

A profound mathematical result from dynamical systems theory: Given a time series from a complex system, we can reconstruct its full phase space by creating delayed copies of the observation.

Mathematical Foundation:

From single observable x(t), create embedding vectors:

X(t) =

Where:

• d = Embedding dimension (default 5)

• τ = Time delay (default 3 bars)

• x(t) = Price or return at time t

Key Insight: If d ≥ 2D+1 (where D is the true attractor dimension), this embedding is topologically equivalent to the actual system dynamics. We've reconstructed the hidden attractor from a single price series.

Why This Matters:

Markets appear random in one dimension (price chart). But in reconstructed phase space, structure emerges—attractors, limit cycles, strange attractors. When we identify these structures, we can detect:

• Stable regions : Predictable behavior (trade opportunities)

• Chaotic regions : Unpredictable behavior (avoid trading)

• Critical transitions : Phase changes between regimes

Phase Space Magnitude Calculation:

phase_magnitude = sqrt(Σ ² for i = 0 to d-1)

This measures the "energy" or "momentum" of the market trajectory through phase space. High magnitude = strong directional move. Low magnitude = consolidation.

📊 RECURRENCE QUANTIFICATION ANALYSIS (RQA)

Once phase space is reconstructed, we analyze its recurrence structure —when does the system return near previous states?

Recurrence Plot Foundation:

A recurrence occurs when two phase space points are closer than threshold ε:

R(i,j) = 1 if ||X(i) - X(j)|| < ε, else 0

This creates a binary matrix showing when the system revisits similar states.

Key RQA Metrics:

1. Recurrence Rate (RR):

RR = (Number of recurrent points) / (Total possible pairs)

• RR near 0: System never repeats (highly stochastic)

• RR = 0.1-0.3: Moderate recurrence (tradeable patterns)

• RR > 0.5: System stuck in attractor (ranging market)

• RR near 1: System frozen (no dynamics)

Interpretation: Moderate recurrence is optimal —patterns exist but market isn't stuck.

2. Determinism (DET):

Measures what fraction of recurrences form diagonal structures in the recurrence plot. Diagonals indicate deterministic evolution (trajectory follows predictable paths).

DET = (Recurrence points on diagonals) / (Total recurrence points)

• DET < 0.3: Random dynamics

• DET = 0.3-0.7: Moderate determinism (patterns with noise)

• DET > 0.7: Strong determinism (technical patterns reliable)

Trading Implication: Signals are prioritized when DET > 0.3 (deterministic state) and RR is moderate (not stuck).

Threshold Selection (ε):

Default ε = 0.10 × std_dev means two states are "recurrent" if within 10% of a standard deviation. This is tight enough to require genuine similarity but loose enough to find patterns.

🔬 PERMUTATION ENTROPY: COMPLEXITY MEASUREMENT

Permutation entropy measures the complexity of a time series by analyzing the distribution of ordinal patterns.

Algorithm (Bandt & Pompe, 2002):

1. Take overlapping windows of length n (default n=4)

2. For each window, record the rank order pattern

Example: → pattern (ranks from lowest to highest)

3. Count frequency of each possible pattern

4. Calculate Shannon entropy of pattern distribution

Mathematical Formula:

H_perm = -Σ p(π) · ln(p(π))

Where π ranges over all n! possible permutations, p(π) is the probability of pattern π.

Normalized to :

H_norm = H_perm / ln(n!)

Interpretation:

• H < 0.3 : Very ordered, crystalline structure (strong trending)

• H = 0.3-0.5 : Ordered regime (tradeable with patterns)

• H = 0.5-0.7 : Moderate complexity (mixed conditions)

• H = 0.7-0.85 : Complex dynamics (challenging to trade)

• H > 0.85 : Maximum entropy (nearly random, avoid)

Entropy Regime Classification:

DRP classifies markets into five entropy regimes:

• CRYSTALLINE (H < 0.3): Maximum order, persistent trends

• ORDERED (H < 0.5): Clear patterns, momentum strategies work

• MODERATE (H < 0.7): Mixed dynamics, adaptive required

• COMPLEX (H < 0.85): High entropy, mean reversion better

• CHAOTIC (H ≥ 0.85): Near-random, minimize trading

Why Permutation Entropy?

Unlike traditional entropy methods requiring binning continuous data (losing information), permutation entropy:

• Works directly on time series

• Robust to monotonic transformations

• Computationally efficient

• Captures temporal structure, not just distribution

• Immune to outliers (uses ranks, not values)

⚡ LYAPUNOV EXPONENT: CHAOS vs STABILITY

The Lyapunov exponent λ measures sensitivity to initial conditions —the hallmark of chaos.

Physical Meaning:

Two trajectories starting infinitely close will diverge at exponential rate e^(λt):

Distance(t) ≈ Distance(0) × e^(λt)

Interpretation:

• λ > 0 : Positive Lyapunov exponent = CHAOS

- Small errors grow exponentially

- Long-term prediction impossible

- System is sensitive, unpredictable

- AVOID TRADING

• λ ≈ 0 : Near-zero = CRITICAL STATE

- Edge of chaos

- Transition zone between order and disorder

- Moderate predictability

- PROCEED WITH CAUTION

• λ < 0 : Negative Lyapunov exponent = STABLE

- Small errors decay

- Trajectories converge

- System is predictable

- OPTIMAL FOR TRADING

Estimation Method:

DRP estimates λ by tracking how quickly nearby states diverge over a rolling window (default 20 bars):

For each bar i in window:

δ₀ = |x - x | (initial separation)

δ₁ = |x - x | (previous separation)

if δ₁ > 0:

ratio = δ₀ / δ₁

log_ratios += ln(ratio)

λ ≈ average(log_ratios)

Stability Classification:

• STABLE : λ < 0 (negative growth rate)

• CRITICAL : |λ| < 0.1 (near neutral)

• CHAOTIC : λ > 0.2 (strong positive growth)

Signal Filtering:

By default, NEXUS requires λ < 0 (stable regime) for signal confirmation. This filters out trades during chaotic periods when technical patterns break down.

📐 HIGUCHI FRACTAL DIMENSION

Fractal dimension measures self-similarity and complexity of the price trajectory.

Theoretical Background:

A curve's fractal dimension D ranges from 1 (smooth line) to 2 (space-filling curve):

• D ≈ 1.0 : Smooth, persistent trending

• D ≈ 1.5 : Random walk (Brownian motion)

• D ≈ 2.0 : Highly irregular, space-filling

Higuchi Method (1988):

For a time series of length N, construct k different curves by taking every k-th point:

L(k) = (1/k) × Σ|x - x | × (N-1)/(⌊(N-m)/k⌋ × k)

For different values of k (1 to k_max), calculate L(k). The fractal dimension is the slope of log(L(k)) vs log(1/k):

D = slope of log(L) vs log(1/k)

Market Interpretation:

• D < 1.35 : Strong trending, persistent (Hurst > 0.5)

- TRENDING regime

- Momentum strategies favored

- Breakouts likely to continue

• D = 1.35-1.45 : Moderate persistence

- PERSISTENT regime

- Trend-following with caution

- Patterns have meaning

• D = 1.45-1.55 : Random walk territory

- RANDOM regime

- Efficiency hypothesis holds

- Technical analysis least reliable

• D = 1.55-1.65 : Anti-persistent (mean-reverting)

- ANTI-PERSISTENT regime

- Oscillator strategies work

- Overbought/oversold meaningful

• D > 1.65 : Highly complex, choppy

- COMPLEX regime

- Avoid directional bets

- Wait for regime change

Signal Filtering:

Resonance signals (secondary signal type) require D < 1.5, indicating trending or persistent dynamics where momentum has meaning.

🔗 TRANSFER ENTROPY: CAUSAL INFORMATION FLOW

Transfer entropy measures directed causal influence between time series—not just correlation, but actual information transfer.

Schreiber's Definition (2000):

Transfer entropy from X to Y measures how much knowing X's past reduces uncertainty about Y's future:

TE(X→Y) = H(Y_future | Y_past) - H(Y_future | Y_past, X_past)

Where H is Shannon entropy.

Key Properties:

1. Directional : TE(X→Y) ≠ TE(Y→X) in general

2. Non-linear : Detects complex causal relationships

3. Model-free : No assumptions about functional form

4. Lag-independent : Captures delayed causal effects

Three Causal Flows Measured:

1. Volume → Price (TE_V→P):

Measures how much volume patterns predict price changes.

• TE > 0 : Volume provides predictive information about price

- Institutional participation driving moves

- Volume confirms direction

- High reliability

• TE ≈ 0 : No causal flow (weak volume/price relationship)

- Volume uninformative

- Caution on signals

• TE < 0 (rare): Suggests price leading volume

- Potentially manipulated or thin market

2. Volatility → Momentum (TE_σ→M):

Does volatility expansion predict momentum changes?

• Positive TE : Volatility precedes momentum shifts

- Breakout dynamics

- Regime transitions

3. Structure → Price (TE_S→P):

Do support/resistance patterns causally influence price?

• Positive TE : Structural levels have causal impact

- Technical levels matter

- Market respects structure

Net Causal Flow:

Net_Flow = TE_V→P + 0.5·TE_σ→M + TE_S→P

• Net > +0.1 : Bullish causal structure

• Net < -0.1 : Bearish causal structure

• |Net| < 0.1 : Neutral/unclear causation

Causal Gate:

For signal confirmation, NEXUS requires:

• Buy signals : TE_V→P > 0 AND Net_Flow > 0.05

• Sell signals : TE_V→P > 0 AND Net_Flow < -0.05

This ensures volume is actually driving price (causal support exists), not just correlated noise.

Implementation Note:

Computing true transfer entropy requires discretizing continuous data into bins (default 6 bins) and estimating joint probability distributions. NEXUS uses a hybrid approach combining TE theory with autocorrelation structure and lagged cross-correlation to approximate information transfer in computationally efficient manner.

🌊 HILBERT PHASE COHERENCE

Phase coherence measures synchronization across market dimensions using Hilbert transform analysis.

Hilbert Transform Theory:

For a signal x(t), the Hilbert transform H (t) creates an analytic signal:

z(t) = x(t) + i·H (t) = A(t)·e^(iφ(t))

Where:

• A(t) = Instantaneous amplitude

• φ(t) = Instantaneous phase

Instantaneous Phase:

φ(t) = arctan(H (t) / x(t))

The phase represents where the signal is in its natural cycle—analogous to position on a unit circle.

Four Dimensions Analyzed:

1. Momentum Phase : Phase of price rate-of-change

2. Volume Phase : Phase of volume intensity

3. Volatility Phase : Phase of ATR cycles

4. Structure Phase : Phase of position within range

Phase Locking Value (PLV):

For two signals with phases φ₁(t) and φ₂(t), PLV measures phase synchronization:

PLV = |⟨e^(i(φ₁(t) - φ₂(t)))⟩|

Where ⟨·⟩ is time average over window.

Interpretation:

• PLV = 0 : Completely random phase relationship (no synchronization)

• PLV = 0.5 : Moderate phase locking

• PLV = 1 : Perfect synchronization (phases locked)

Pairwise PLV Calculations:

• PLV_momentum-volume : Are momentum and volume cycles synchronized?

• PLV_momentum-structure : Are momentum cycles aligned with structure?

• PLV_volume-structure : Are volume and structural patterns in phase?

Overall Phase Coherence:

Coherence = (PLV_mom-vol + PLV_mom-struct + PLV_vol-struct) / 3

Signal Confirmation:

Emergence signals require coherence ≥ threshold (default 0.70):

• Below 0.70: Dimensions not synchronized, no coherent market state

• Above 0.70: Dimensions in phase, coherent behavior emerging

Coherence Direction:

The summed phase angles indicate whether synchronized dimensions point bullish or bearish:

Direction = sin(φ_momentum) + 0.5·sin(φ_volume) + 0.5·sin(φ_structure)

• Direction > 0 : Phases pointing upward (bullish synchronization)

• Direction < 0 : Phases pointing downward (bearish synchronization)

🌀 EMERGENCE SCORE: MULTI-DIMENSIONAL ALIGNMENT

The emergence score aggregates all complexity metrics into a single 0-1 value representing market coherence.

Eight Components with Weights:

1. Phase Coherence (20%):

Direct contribution: coherence × 0.20

Measures dimensional synchronization.

2. Entropy Regime (15%):

Contribution: (0.6 - H_perm) / 0.6 × 0.15 if H < 0.6, else 0

Rewards low entropy (ordered, predictable states).

3. Lyapunov Stability (12%):

• λ < 0 (stable): +0.12

• |λ| < 0.1 (critical): +0.08

• λ > 0.2 (chaotic): +0.0

Requires stable, predictable dynamics.

4. Fractal Dimension Trending (12%):

Contribution: (1.45 - D) / 0.45 × 0.12 if D < 1.45, else 0

Rewards trending fractal structure (D < 1.45).

5. Dimensional Resonance (12%):

Contribution: |dimensional_resonance| × 0.12

Measures alignment across momentum, volume, structure, volatility dimensions.

6. Causal Flow Strength (9%):

Contribution: |net_causal_flow| × 0.09

Rewards strong causal relationships.

7. Phase Space Embedding (10%):

Contribution: min(|phase_magnitude_norm|, 3.0) / 3.0 × 0.10 if |magnitude| > 1.0

Rewards strong trajectory in reconstructed phase space.

8. Recurrence Quality (10%):

Contribution: determinism × 0.10 if DET > 0.3 AND 0.1 < RR < 0.8

Rewards deterministic patterns with moderate recurrence.

Total Emergence Score:

E = Σ(components) ∈

Capped at 1.0 maximum.

Emergence Direction:

Separate calculation determining bullish vs bearish:

• Dimensional resonance sign

• Net causal flow sign

• Phase magnitude correlation with momentum

Signal Threshold:

Default emergence_threshold = 0.75 means 75% of maximum possible emergence score required to trigger signals.

Why Emergence Matters:

Traditional indicators measure single dimensions. Emergence detects self-organization —when multiple independent dimensions spontaneously align. This is the market equivalent of a phase transition in physics, where microscopic chaos gives way to macroscopic order.

These are the highest-probability trade opportunities because the entire system is resonating in the same direction.

🎯 SIGNAL GENERATION: EMERGENCE vs RESONANCE

DRP generates two tiers of signals with different requirements:

TIER 1: EMERGENCE SIGNALS (Primary)

Requirements:

1. Emergence score ≥ threshold (default 0.75)

2. Phase coherence ≥ threshold (default 0.70)

3. Emergence direction > 0.2 (bullish) or < -0.2 (bearish)

4. Causal gate passed (if enabled): TE_V→P > 0 and net_flow confirms direction

5. Stability zone (if enabled): λ < 0 or |λ| < 0.1

6. Price confirmation: Close > open (bulls) or close < open (bears)

7. Cooldown satisfied: bars_since_signal ≥ cooldown_period

EMERGENCE BUY:

• All above conditions met with bullish direction

• Market has achieved coherent bullish state

• Multiple dimensions synchronized upward

EMERGENCE SELL:

• All above conditions met with bearish direction

• Market has achieved coherent bearish state

• Multiple dimensions synchronized downward

Premium Emergence:

When signal_quality (emergence_score × phase_coherence) > 0.7:

• Displayed as ★ star symbol

• Highest conviction trades

• Maximum dimensional alignment

Standard Emergence:

When signal_quality 0.5-0.7:

• Displayed as ◆ diamond symbol

• Strong signals but not perfect alignment

TIER 2: RESONANCE SIGNALS (Secondary)

Requirements:

1. Dimensional resonance > +0.6 (bullish) or < -0.6 (bearish)

2. Fractal dimension < 1.5 (trending/persistent regime)

3. Price confirmation matches direction

4. NOT in chaotic regime (λ < 0.2)

5. Cooldown satisfied

6. NO emergence signal firing (resonance is fallback)

RESONANCE BUY:

• Dimensional alignment without full emergence

• Trending fractal structure

• Moderate conviction

RESONANCE SELL:

• Dimensional alignment without full emergence

• Bearish resonance with trending structure

• Moderate conviction

Displayed as small ▲/▼ triangles with transparency.

Signal Hierarchy:

IF emergence conditions met:

Fire EMERGENCE signal (★ or ◆)

ELSE IF resonance conditions met:

Fire RESONANCE signal (▲ or ▼)

ELSE:

No signal

Cooldown System:

After any signal fires, cooldown_period (default 5 bars) must elapse before next signal. This prevents signal clustering during persistent conditions.

Cooldown tracks using bar_index:

bars_since_signal = current_bar_index - last_signal_bar_index

cooldown_ok = bars_since_signal >= cooldown_period

🎨 VISUAL SYSTEM: MULTI-LAYER COMPLEXITY

DRP provides rich visual feedback across four distinct layers:

LAYER 1: COHERENCE FIELD (Background)

Colored background intensity based on phase coherence:

• No background : Coherence < 0.5 (incoherent state)

• Faint glow : Coherence 0.5-0.7 (building coherence)

• Stronger glow : Coherence > 0.7 (coherent state)

Color:

• Cyan/teal: Bullish coherence (direction > 0)

• Red/magenta: Bearish coherence (direction < 0)

• Blue: Neutral coherence (direction ≈ 0)

Transparency: 98 minus (coherence_intensity × 10), so higher coherence = more visible.

LAYER 2: STABILITY/CHAOS ZONES

Background color indicating Lyapunov regime:

• Green tint (95% transparent): λ < 0, STABLE zone

- Safe to trade

- Patterns meaningful

• Gold tint (90% transparent): |λ| < 0.1, CRITICAL zone

- Edge of chaos

- Moderate risk

• Red tint (85% transparent): λ > 0.2, CHAOTIC zone

- Avoid trading

- Unpredictable behavior

LAYER 3: DIMENSIONAL RIBBONS

Three EMAs representing dimensional structure:

• Fast ribbon : EMA(8) in cyan/teal (fast dynamics)

• Medium ribbon : EMA(21) in blue (intermediate)

• Slow ribbon : EMA(55) in red/magenta (slow dynamics)

Provides visual reference for multi-scale structure without cluttering with raw phase space data.

LAYER 4: CAUSAL FLOW LINE

A thicker line plotted at EMA(13) colored by net causal flow:

• Cyan/teal : Net_flow > +0.1 (bullish causation)

• Red/magenta : Net_flow < -0.1 (bearish causation)

• Gray : |Net_flow| < 0.1 (neutral causation)

Shows real-time direction of information flow.

EMERGENCE FLASH:

Strong background flash when emergence signals fire:

• Cyan flash for emergence buy

• Red flash for emergence sell

• 80% transparency for visibility without obscuring price

📊 COMPREHENSIVE DASHBOARD

Real-time monitoring of all complexity metrics:

HEADER:

• 🌀 DRP branding with gold accent

CORE METRICS:

EMERGENCE:

• Progress bar (█ filled, ░ empty) showing 0-100%

• Percentage value

• Direction arrow (↗ bull, ↘ bear, → neutral)

• Color-coded: Green/gold if active, gray if low

COHERENCE:

• Progress bar showing phase locking value

• Percentage value

• Checkmark ✓ if ≥ threshold, circle ○ if below

• Color-coded: Cyan if coherent, gray if not

COMPLEXITY SECTION:

ENTROPY:

• Regime name (CRYSTALLINE/ORDERED/MODERATE/COMPLEX/CHAOTIC)

• Numerical value (0.00-1.00)

• Color: Green (ordered), gold (moderate), red (chaotic)

LYAPUNOV:

• State (STABLE/CRITICAL/CHAOTIC)

• Numerical value (typically -0.5 to +0.5)

• Status indicator: ● stable, ◐ critical, ○ chaotic

• Color-coded by state

FRACTAL:

• Regime (TRENDING/PERSISTENT/RANDOM/ANTI-PERSIST/COMPLEX)

• Dimension value (1.0-2.0)

• Color: Cyan (trending), gold (random), red (complex)

PHASE-SPACE:

• State (STRONG/ACTIVE/QUIET)

• Normalized magnitude value

• Parameters display: d=5 τ=3

CAUSAL SECTION:

CAUSAL:

• Direction (BULL/BEAR/NEUTRAL)

• Net flow value

• Flow indicator: →P (to price), P← (from price), ○ (neutral)

V→P:

• Volume-to-price transfer entropy

• Small display showing specific TE value

DIMENSIONAL SECTION:

RESONANCE:

• Progress bar of absolute resonance

• Signed value (-1 to +1)

• Color-coded by direction

RECURRENCE:

• Recurrence rate percentage

• Determinism percentage display

• Color-coded: Green if high quality

STATE SECTION:

STATE:

• Current mode: EMERGENCE / RESONANCE / CHAOS / SCANNING

• Icon: 🚀 (emergence buy), 💫 (emergence sell), ▲ (resonance buy), ▼ (resonance sell), ⚠ (chaos), ◎ (scanning)

• Color-coded by state

SIGNALS:

• E: count of emergence signals

• R: count of resonance signals

⚙️ KEY PARAMETERS EXPLAINED

Phase Space Configuration:

• Embedding Dimension (3-10, default 5): Reconstruction dimension

- Low (3-4): Simple dynamics, faster computation

- Medium (5-6): Balanced (recommended)

- High (7-10): Complex dynamics, more data needed

- Rule: d ≥ 2D+1 where D is true dimension

• Time Delay (τ) (1-10, default 3): Embedding lag

- Fast markets: 1-2

- Normal: 3-4

- Slow markets: 5-10

- Optimal: First minimum of mutual information (often 2-4)

• Recurrence Threshold (ε) (0.01-0.5, default 0.10): Phase space proximity

- Tight (0.01-0.05): Very similar states only

- Medium (0.08-0.15): Balanced

- Loose (0.20-0.50): Liberal matching

Entropy & Complexity:

• Permutation Order (3-7, default 4): Pattern length

- Low (3): 6 patterns, fast but coarse

- Medium (4-5): 24-120 patterns, balanced

- High (6-7): 720-5040 patterns, fine-grained

- Note: Requires window >> order! for stability

• Entropy Window (15-100, default 30): Lookback for entropy

- Short (15-25): Responsive to changes

- Medium (30-50): Stable measure

- Long (60-100): Very smooth, slow adaptation

• Lyapunov Window (10-50, default 20): Stability estimation window

- Short (10-15): Fast chaos detection

- Medium (20-30): Balanced

- Long (40-50): Stable λ estimate

Causal Inference:

• Enable Transfer Entropy (default ON): Causality analysis

- Keep ON for full system functionality

• TE History Length (2-15, default 5): Causal lookback

- Short (2-4): Quick causal detection

- Medium (5-8): Balanced

- Long (10-15): Deep causal analysis

• TE Discretization Bins (4-12, default 6): Binning granularity

- Few (4-5): Coarse, robust, needs less data

- Medium (6-8): Balanced

- Many (9-12): Fine-grained, needs more data

Phase Coherence:

• Enable Phase Coherence (default ON): Synchronization detection

- Keep ON for emergence detection

• Coherence Threshold (0.3-0.95, default 0.70): PLV requirement

- Loose (0.3-0.5): More signals, lower quality

- Balanced (0.6-0.75): Recommended

- Strict (0.8-0.95): Rare, highest quality

• Hilbert Smoothing (3-20, default 8): Phase smoothing

- Low (3-5): Responsive, noisier

- Medium (6-10): Balanced

- High (12-20): Smooth, more lag

Fractal Analysis:

• Enable Fractal Dimension (default ON): Complexity measurement

- Keep ON for full analysis

• Fractal K-max (4-20, default 8): Scaling range

- Low (4-6): Faster, less accurate

- Medium (7-10): Balanced

- High (12-20): Accurate, slower

• Fractal Window (30-200, default 50): FD lookback

- Short (30-50): Responsive FD

- Medium (60-100): Stable FD

- Long (120-200): Very smooth FD

Emergence Detection:

• Emergence Threshold (0.5-0.95, default 0.75): Minimum coherence

- Sensitive (0.5-0.65): More signals

- Balanced (0.7-0.8): Recommended

- Strict (0.85-0.95): Rare signals

• Require Causal Gate (default ON): TE confirmation

- ON: Only signal when causality confirms

- OFF: Allow signals without causal support

• Require Stability Zone (default ON): Lyapunov filter

- ON: Only signal when λ < 0 (stable) or |λ| < 0.1 (critical)

- OFF: Allow signals in chaotic regimes (risky)

• Signal Cooldown (1-50, default 5): Minimum bars between signals

- Fast (1-3): Rapid signal generation

- Normal (4-8): Balanced

- Slow (10-20): Very selective

- Ultra (25-50): Only major regime changes

Signal Configuration:

• Momentum Period (5-50, default 14): ROC calculation

• Structure Lookback (10-100, default 20): Support/resistance range

• Volatility Period (5-50, default 14): ATR calculation

• Volume MA Period (10-50, default 20): Volume normalization

Visual Settings:

• Customizable color scheme for all elements

• Toggle visibility for each layer independently

• Dashboard position (4 corners) and size (tiny/small/normal)

🎓 PROFESSIONAL USAGE PROTOCOL

Phase 1: System Familiarization (Week 1)

Goal: Understand complexity metrics and dashboard interpretation

Setup:

• Enable all features with default parameters

• Watch dashboard metrics for 500+ bars

• Do NOT trade yet

Actions:

• Observe emergence score patterns relative to price moves

• Note coherence threshold crossings and subsequent price action

• Watch entropy regime transitions (ORDERED → COMPLEX → CHAOTIC)

• Correlate Lyapunov state with signal reliability

• Track which signals appear (emergence vs resonance frequency)

Key Learning:

• When does emergence peak? (usually before major moves)

• What entropy regime produces best signals? (typically ORDERED or MODERATE)

• Does your instrument respect stability zones? (stable λ = better signals)

Phase 2: Parameter Optimization (Week 2)

Goal: Tune system to instrument characteristics

Requirements:

• Understand basic dashboard metrics from Phase 1

• Have 1000+ bars of history loaded

Embedding Dimension & Time Delay:

• If signals very rare: Try lower dimension (d=3-4) or shorter delay (τ=2)

• If signals too frequent: Try higher dimension (d=6-7) or longer delay (τ=4-5)

• Sweet spot: 4-8 emergence signals per 100 bars

Coherence Threshold:

• Check dashboard: What's typical coherence range?

• If coherence rarely exceeds 0.70: Lower threshold to 0.60-0.65

• If coherence often >0.80: Can raise threshold to 0.75-0.80

• Goal: Signals fire during top 20-30% of coherence values

Emergence Threshold:

• If too few signals: Lower to 0.65-0.70

• If too many signals: Raise to 0.80-0.85

• Balance with coherence threshold—both must be met

Phase 3: Signal Quality Assessment (Weeks 3-4)

Goal: Verify signals have edge via paper trading

Requirements:

• Parameters optimized per Phase 2

• 50+ signals generated

• Detailed notes on each signal

Paper Trading Protocol:

• Take EVERY emergence signal (★ and ◆)

• Optional: Take resonance signals (▲/▼) separately to compare

• Use simple exit: 2R target, 1R stop (ATR-based)

• Track: Win rate, average R-multiple, maximum consecutive losses

Quality Metrics:

• Premium emergence (★) : Should achieve >55% WR

• Standard emergence (◆) : Should achieve >50% WR

• Resonance signals : Should achieve >45% WR

• Overall : If <45% WR, system not suitable for this instrument/timeframe

Red Flags:

• Win rate <40%: Wrong instrument or parameters need major adjustment

• Max consecutive losses >10: System not working in current regime

• Profit factor <1.0: No edge despite complexity analysis

Phase 4: Regime Awareness (Week 5)

Goal: Understand which market conditions produce best signals

Analysis:

• Review Phase 3 trades, segment by:

- Entropy regime at signal (ORDERED vs COMPLEX vs CHAOTIC)

- Lyapunov state (STABLE vs CRITICAL vs CHAOTIC)

- Fractal regime (TRENDING vs RANDOM vs COMPLEX)

Findings (typical patterns):

• Best signals: ORDERED entropy + STABLE lyapunov + TRENDING fractal

• Moderate signals: MODERATE entropy + CRITICAL lyapunov + PERSISTENT fractal

• Avoid: CHAOTIC entropy or CHAOTIC lyapunov (require_stability filter should block these)

Optimization:

• If COMPLEX/CHAOTIC entropy produces losing trades: Consider requiring H < 0.70

• If fractal RANDOM/COMPLEX produces losses: Already filtered by resonance logic

• If certain TE patterns (very negative net_flow) produce losses: Adjust causal_gate logic

Phase 5: Micro Live Testing (Weeks 6-8)

Goal: Validate with minimal capital at risk

Requirements:

• Paper trading shows: WR >48%, PF >1.2, max DD <20%

• Understand complexity metrics intuitively

• Know which regimes work best from Phase 4

Setup:

• 10-20% of intended position size

• Focus on premium emergence signals (★) only initially

• Proper stop placement (1.5-2.0 ATR)

Execution Notes:

• Emergence signals can fire mid-bar as metrics update

• Use alerts for signal detection

• Entry on close of signal bar or next bar open

• DO NOT chase—if price gaps away, skip the trade

Comparison:

• Your live results should track within 10-15% of paper results

• If major divergence: Execution issues (slippage, timing) or parameters changed

Phase 6: Full Deployment (Month 3+)

Goal: Scale to full size over time

Requirements:

• 30+ micro live trades

• Live WR within 10% of paper WR

• Profit factor >1.1 live

• Max drawdown <15%

• Confidence in parameter stability

Progression:

• Months 3-4: 25-40% intended size

• Months 5-6: 40-70% intended size

• Month 7+: 70-100% intended size

Maintenance:

• Weekly dashboard review: Are metrics stable?

• Monthly performance review: Segmented by regime and signal type

• Quarterly parameter check: Has optimal embedding/coherence changed?

Advanced:

• Consider different parameters per session (high vs low volatility)

• Track phase space magnitude patterns before major moves

• Combine with other indicators for confluence

💡 DEVELOPMENT INSIGHTS & KEY BREAKTHROUGHS

The Phase Space Revelation:

Traditional indicators live in price-time space. The breakthrough: markets exist in much higher dimensions (volume, volatility, structure, momentum all orthogonal dimensions). Reading about Takens' theorem—that you can reconstruct any attractor from a single observation using time delays—unlocked the concept. Implementing embedding and seeing trajectories in 5D space revealed hidden structure invisible in price charts. Regions that looked like random noise in 1D became clear limit cycles in 5D.

The Permutation Entropy Discovery:

Calculating Shannon entropy on binned price data was unstable and parameter-sensitive. Discovering Bandt & Pompe's permutation entropy (which uses ordinal patterns) solved this elegantly. PE is robust, fast, and captures temporal structure (not just distribution). Testing showed PE < 0.5 periods had 18% higher signal win rate than PE > 0.7 periods. Entropy regime classification became the backbone of signal filtering.

The Lyapunov Filter Breakthrough:

Early versions signaled during all regimes. Win rate hovered at 42%—barely better than random. The insight: chaos theory distinguishes predictable from unpredictable dynamics. Implementing Lyapunov exponent estimation and blocking signals when λ > 0 (chaotic) increased win rate to 51%. Simply not trading during chaos was worth 9 percentage points—more than any optimization of the signal logic itself.

The Transfer Entropy Challenge:

Correlation between volume and price is easy to calculate but meaningless (bidirectional, could be spurious). Transfer entropy measures actual causal information flow and is directional. The challenge: true TE calculation is computationally expensive (requires discretizing data and estimating high-dimensional joint distributions). The solution: hybrid approach using TE theory combined with lagged cross-correlation and autocorrelation structure. Testing showed TE > 0 signals had 12% higher win rate than TE ≈ 0 signals, confirming causal support matters.

The Phase Coherence Insight:

Initially tried simple correlation between dimensions. Not predictive. Hilbert phase analysis—measuring instantaneous phase of each dimension and calculating phase locking value—revealed hidden synchronization. When PLV > 0.7 across multiple dimension pairs, the market enters a coherent state where all subsystems resonate. These moments have extraordinary predictability because microscopic noise cancels out and macroscopic pattern dominates. Emergence signals require high PLV for this reason.

The Eight-Component Emergence Formula:

Original emergence score used five components (coherence, entropy, lyapunov, fractal, resonance). Performance was good but not exceptional. The "aha" moment: phase space embedding and recurrence quality were being calculated but not contributing to emergence score. Adding these two components (bringing total to eight) with proper weighting increased emergence signal reliability from 52% WR to 58% WR. All calculated metrics must contribute to the final score. If you compute something, use it.

The Cooldown Necessity:

Without cooldown, signals would cluster—5-10 consecutive bars all qualified during high coherence periods, creating chart pollution and overtrading. Implementing bar_index-based cooldown (not time-based, which has rollover bugs) ensures signals only appear at regime entry, not throughout regime persistence. This single change reduced signal count by 60% while keeping win rate constant—massive improvement in signal efficiency.

🚨 LIMITATIONS & CRITICAL ASSUMPTIONS

What This System IS NOT:

• NOT Predictive : NEXUS doesn't forecast prices. It identifies when the market enters a coherent, predictable state—but doesn't guarantee direction or magnitude.

• NOT Holy Grail : Typical performance is 50-58% win rate with 1.5-2.0 avg R-multiple. This is probabilistic edge from complexity analysis, not certainty.

• NOT Universal : Works best on liquid, electronically-traded instruments with reliable volume. Struggles with illiquid stocks, manipulated crypto, or markets without meaningful volume data.

• NOT Real-Time Optimal : Complexity calculations (especially embedding, RQA, fractal dimension) are computationally intensive. Dashboard updates may lag by 1-2 seconds on slower connections.

• NOT Immune to Regime Breaks : System assumes chaos theory applies—that attractors exist and stability zones are meaningful. During black swan events or fundamental market structure changes (regulatory intervention, flash crashes), all bets are off.

Core Assumptions:

1. Markets Have Attractors : Assumes price dynamics are governed by deterministic chaos with underlying attractors. Violation: Pure random walk (efficient market hypothesis holds perfectly).

2. Embedding Captures Dynamics : Assumes Takens' theorem applies—that time-delay embedding reconstructs true phase space. Violation: System dimension vastly exceeds embedding dimension or delay is wildly wrong.

3. Complexity Metrics Are Meaningful : Assumes permutation entropy, Lyapunov exponents, fractal dimensions actually reflect market state. Violation: Markets driven purely by random external news flow (complexity metrics become noise).

4. Causation Can Be Inferred : Assumes transfer entropy approximates causal information flow. Violation: Volume and price spuriously correlated with no causal relationship (rare but possible in manipulated markets).

5. Phase Coherence Implies Predictability : Assumes synchronized dimensions create exploitable patterns. Violation: Coherence by chance during random period (false positive).

6. Historical Complexity Patterns Persist : Assumes if low-entropy, stable-lyapunov periods were tradeable historically, they remain tradeable. Violation: Fundamental regime change (market structure shifts, e.g., transition from floor trading to HFT).

Performs Best On:

• ES, NQ, RTY (major US index futures - high liquidity, clean volume data)

• Major forex pairs: EUR/USD, GBP/USD, USD/JPY (24hr markets, good for phase analysis)

• Liquid commodities: CL (crude oil), GC (gold), NG (natural gas)

• Large-cap stocks: AAPL, MSFT, GOOGL, TSLA (>$10M daily volume, meaningful structure)

• Major crypto on reputable exchanges: BTC, ETH on Coinbase/Kraken (avoid Binance due to manipulation)

Performs Poorly On:

• Low-volume stocks (<$1M daily volume) - insufficient liquidity for complexity analysis

• Exotic forex pairs - erratic spreads, thin volume

• Illiquid altcoins - wash trading, bot manipulation invalidates volume analysis

• Pre-market/after-hours - gappy, thin, different dynamics

• Binary events (earnings, FDA approvals) - discontinuous jumps violate dynamical systems assumptions

• Highly manipulated instruments - spoofing and layering create false coherence

Known Weaknesses:

• Computational Lag : Complexity calculations require iterating over windows. On slow connections, dashboard may update 1-2 seconds after bar close. Signals may appear delayed.

• Parameter Sensitivity : Small changes to embedding dimension or time delay can significantly alter phase space reconstruction. Requires careful calibration per instrument.

• Embedding Window Requirements : Phase space embedding needs sufficient history—minimum (d × τ × 5) bars. If embedding_dimension=5 and time_delay=3, need 75+ bars. Early bars will be unreliable.

• Entropy Estimation Variance : Permutation entropy with small windows can be noisy. Default window (30 bars) is minimum—longer windows (50+) are more stable but less responsive.

• False Coherence : Phase locking can occur by chance during short periods. Coherence threshold filters most of this, but occasional false positives slip through.

• Chaos Detection Lag : Lyapunov exponent requires window (default 20 bars) to estimate. Market can enter chaos and produce bad signal before λ > 0 is detected. Stability filter helps but doesn't eliminate this.

• Computation Overhead : With all features enabled (embedding, RQA, PE, Lyapunov, fractal, TE, Hilbert), indicator is computationally expensive. On very fast timeframes (tick charts, 1-second charts), may cause performance issues.

⚠️ RISK DISCLOSURE

Trading futures, forex, stocks, options, and cryptocurrencies involves substantial risk of loss and is not suitable for all investors. Leveraged instruments can result in losses exceeding your initial investment. Past performance, whether backtested or live, is not indicative of future results.

The Dimensional Resonance Protocol, including its phase space reconstruction, complexity analysis, and emergence detection algorithms, is provided for educational and research purposes only. It is not financial advice, investment advice, or a recommendation to buy or sell any security or instrument.

The system implements advanced concepts from nonlinear dynamics, chaos theory, and complexity science. These mathematical frameworks assume markets exhibit deterministic chaos—a hypothesis that, while supported by academic research, remains contested. Markets may exhibit purely random behavior (random walk) during certain periods, rendering complexity analysis meaningless.

Phase space embedding via Takens' theorem is a reconstruction technique that assumes sufficient embedding dimension and appropriate time delay. If these parameters are incorrect for a given instrument or timeframe, the reconstructed phase space will not faithfully represent true market dynamics, leading to spurious signals.

Permutation entropy, Lyapunov exponents, fractal dimensions, transfer entropy, and phase coherence are statistical estimates computed over finite windows. All have inherent estimation error. Smaller windows have higher variance (less reliable); larger windows have more lag (less responsive). There is no universally optimal window size.

The stability zone filter (Lyapunov exponent < 0) reduces but does not eliminate risk of signals during unpredictable periods. Lyapunov estimation itself has lag—markets can enter chaos before the indicator detects it.

Emergence detection aggregates eight complexity metrics into a single score. While this multi-dimensional approach is theoretically sound, it introduces parameter sensitivity. Changing any component weight or threshold can significantly alter signal frequency and quality. Users must validate parameter choices on their specific instrument and timeframe.

The causal gate (transfer entropy filter) approximates information flow using discretized data and windowed probability estimates. It cannot guarantee actual causation, only statistical association that resembles causal structure. Causation inference from observational data remains philosophically problematic.

Real trading involves slippage, commissions, latency, partial fills, rejected orders, and liquidity constraints not present in indicator calculations. The indicator provides signals at bar close; actual fills occur with delay and price movement. Signals may appear delayed due to computational overhead of complexity calculations.

Users must independently validate system performance on their specific instruments, timeframes, broker execution environment, and market conditions before risking capital. Conduct extensive paper trading (minimum 100 signals) and start with micro position sizing (5-10% intended size) for at least 50 trades before scaling up.

Never risk more capital than you can afford to lose completely. Use proper position sizing (0.5-2% risk per trade maximum). Implement stop losses on every trade. Maintain adequate margin/capital reserves. Understand that most retail traders lose money. Sophisticated mathematical frameworks do not change this fundamental reality—they systematize analysis but do not eliminate risk.

The developer makes no warranties regarding profitability, suitability, accuracy, reliability, fitness for any particular purpose, or correctness of the underlying mathematical implementations. Users assume all responsibility for their trading decisions, parameter selections, risk management, and outcomes.

By using this indicator, you acknowledge that you have read, understood, and accepted these risk disclosures and limitations, and you accept full responsibility for all trading activity and potential losses.

📁 DOCUMENTATION

The Dimensional Resonance Protocol is fundamentally a statistical complexity analysis framework . The indicator implements multiple advanced statistical methods from academic research:

Permutation Entropy (Bandt & Pompe, 2002): Measures complexity by analyzing distribution of ordinal patterns. Pure statistical concept from information theory.

Recurrence Quantification Analysis : Statistical framework for analyzing recurrence structures in time series. Computes recurrence rate, determinism, and diagonal line statistics.

Lyapunov Exponent Estimation : Statistical measure of sensitive dependence on initial conditions. Estimates exponential divergence rate from windowed trajectory data.

Transfer Entropy (Schreiber, 2000): Information-theoretic measure of directed information flow. Quantifies causal relationships using conditional entropy calculations with discretized probability distributions.

Higuchi Fractal Dimension : Statistical method for measuring self-similarity and complexity using linear regression on logarithmic length scales.

Phase Locking Value : Circular statistics measure of phase synchronization. Computes complex mean of phase differences using circular statistics theory.

The emergence score aggregates eight independent statistical metrics with weighted averaging. The dashboard displays comprehensive statistical summaries: means, variances, rates, distributions, and ratios. Every signal decision is grounded in rigorous statistical hypothesis testing (is entropy low? is lyapunov negative? is coherence above threshold?).

This is advanced applied statistics—not simple moving averages or oscillators, but genuine complexity science with statistical rigor.

Multiple oscillator-type calculations contribute to dimensional analysis:

Phase Analysis: Hilbert transform extracts instantaneous phase (0 to 2π) of four market dimensions (momentum, volume, volatility, structure). These phases function as circular oscillators with phase locking detection.

Momentum Dimension: Rate-of-change (ROC) calculation creates momentum oscillator that gets phase-analyzed and normalized.

Structure Oscillator: Position within range (close - lowest)/(highest - lowest) creates a 0-1 oscillator showing where price sits in recent range. This gets embedded and phase-analyzed.

Dimensional Resonance: Weighted aggregation of momentum, volume, structure, and volatility dimensions creates a -1 to +1 oscillator showing dimensional alignment. Similar to traditional oscillators but multi-dimensional.

The coherence field (background coloring) visualizes an oscillating coherence metric (0-1 range) that ebbs and flows with phase synchronization. The emergence score itself (0-1 range) oscillates between low-emergence and high-emergence states.

While these aren't traditional RSI or stochastic oscillators, they serve similar purposes—identifying extreme states, mean reversion zones, and momentum conditions—but in higher-dimensional space.

Volatility analysis permeates the system:

ATR-Based Calculations: Volatility period (default 14) computes ATR for the volatility dimension. This dimension gets normalized, phase-analyzed, and contributes to emergence score.

Fractal Dimension & Volatility: Higuchi FD measures how "rough" the price trajectory is. Higher FD (>1.6) correlates with higher volatility/choppiness. FD < 1.4 indicates smooth trends (lower effective volatility).

Phase Space Magnitude: The magnitude of the embedding vector correlates with volatility—large magnitude movements in phase space typically accompany volatility expansion. This is the "energy" of the market trajectory.

Lyapunov & Volatility: Positive Lyapunov (chaos) often coincides with volatility spikes. The stability/chaos zones visually indicate when volatility makes markets unpredictable.

Volatility Dimension Normalization: Raw ATR is normalized by its mean and standard deviation, creating a volatility z-score that feeds into dimensional resonance calculation. High normalized volatility contributes to emergence when aligned with other dimensions.

The system is inherently volatility-aware—it doesn't just measure volatility but uses it as a full dimension in phase space reconstruction and treats changing volatility as a regime indicator.

CLOSING STATEMENT

DRP doesn't trade price—it trades phase space structure . It doesn't chase patterns—it detects emergence . It doesn't guess at trends—it measures coherence .

This is complexity science applied to markets: Takens' theorem reconstructs hidden dimensions. Permutation entropy measures order. Lyapunov exponents detect chaos. Transfer entropy reveals causation. Hilbert phases find synchronization. Fractal dimensions quantify self-similarity.

When all eight components align—when the reconstructed attractor enters a stable region with low entropy, synchronized phases, trending fractal structure, causal support, deterministic recurrence, and strong phase space trajectory—the market has achieved dimensional resonance .

These are the highest-probability moments. Not because an indicator said so. Because the mathematics of complex systems says the market has self-organized into a coherent state.

Most indicators see shadows on the wall. DRP reconstructs the cave.

"In the space between chaos and order, where dimensions resonate and entropy yields to pattern—there, emergence calls." DRP

Taking you to school. — Dskyz, Trade with insight. Trade with anticipation.

Liquidity Void Zone Detector [PhenLabs]📊 Liquidity Void Zone Detector

Version: PineScript™v6

📌 Description

The Liquidity Void Zone Detector is a sophisticated technical indicator designed to identify and visualize areas where price moved with abnormally low volume or rapid momentum, creating "voids" in market liquidity. These zones represent areas where insufficient trading activity occurred during price movement, often acting as magnets for future price action as the market seeks to fill these gaps.

Built on PineScript v6, this indicator employs a dual-detection methodology that analyzes both volume depletion patterns and price movement intensity relative to ATR. The revolutionary 3D visualization system uses three-layer polyline rendering with adaptive transparency and vertical offsets, creating genuine depth perception where low liquidity zones visually recede and high liquidity zones protrude forward. This makes critical market structure immediately apparent without cluttering your chart.

🚀 Points of Innovation

Dual detection algorithm combining volume threshold analysis and ATR-normalized price movement sensitivity for comprehensive void identification

Three-layer 3D visualization system with progressive transparency gradients (85%, 78%, 70%) and calculated vertical offsets for authentic depth perception

Intelligent state machine logic that tracks consecutive void bars and only renders zones meeting minimum qualification requirements

Dynamic strength scoring system (0-100 scale) that combines inverted volume ratios with movement intensity for accurate void characterization

Adaptive ATR-based spacing calculation that automatically adjusts 3D layering depth to match instrument volatility

Efficient memory management system supporting up to 100 simultaneous void visualizations with automatic array-based cleanup

🔧 Core Components

Volume Analysis Engine: Calculates rolling volume averages and compares current bar volume against dynamic thresholds to detect abnormally thin trading conditions

Price Movement Analyzer: Normalizes bar range against ATR to identify rapid price movements that indicate liquidity exhaustion regardless of instrument or timeframe

Void Tracking State Machine: Maintains persistent tracking of void start bars, price boundaries, consecutive bar counts, and cumulative strength across multiple bars

3D Polyline Renderer: Generates three-layer rectangular polylines with precise timestamp-to-bar index conversion and progressive offset calculations

Strength Calculation System: Combines volume component (inverted ratio capped at 100) with movement component (ATR intensity × 30) for comprehensive void scoring

🔥 Key Features

Automatic Void Detection: Continuously scans price action for low volume conditions or rapid movements, triggering void tracking when thresholds are exceeded

Real-Time Visualization: Creates 3D rectangular zones spanning from void initiation to termination, with color-coded depth indicating liquidity type

Adjustable Sensitivity: Configure volume threshold multiplier (0.1-2.0x), price movement sensitivity (0.5-5.0x), and minimum qualifying bars (1-10) for customized detection

Dual Color Coding: Separate visual treatment for low liquidity voids (receding red) and high liquidity zones (protruding green) based on 50-point strength threshold

Optional Compact Labels: Toggle LV (Low Volume) or HV (High Volume) circular labels at void centers for quick identification without visual clutter

Lookback Period Control: Adjust analysis window from 5 to 100 bars to match your trading timeframe and market volatility characteristics

Memory-Efficient Design: Automatically manages polyline and label arrays, deleting oldest elements when user-defined maximum is reached

Data Window Integration: Plots void detection binary, current strength score, and average volume for detailed analysis in TradingView's data window

🎨 Visualization

Three-Layer Depth System: Each void is rendered as three stacked polylines with progressive transparency (85%, 78%, 70%) and calculated vertical offsets creating authentic 3D appearance

Directional Depth Perception: Low liquidity zones recede with back layer most transparent; high liquidity zones protrude with front layer most transparent for instant visual differentiation

Adaptive Offset Spacing: Vertical separation between layers calculated as ATR(14) × 0.001, ensuring consistent 3D effect across different instruments and volatility regimes

Color Customization: Fully configurable base colors for both low liquidity zones (default: red with 80 transparency) and high liquidity zones (default: green with 80 transparency)

Minimal Chart Clutter: Closed polylines with matching line and fill colors create clean rectangular zones without unnecessary borders or visual noise

Background Highlight: Subtle yellow background (96% transparency) marks bars where void conditions are actively detected in real-time

Compact Labeling: Optional tiny circular labels with 60% transparent backgrounds positioned at void center points for quick reference

📖 Usage Guidelines

Detection Settings

Lookback Period: Default: 10 | Range: 5-100 | Number of bars analyzed for volume averaging and void detection. Lower values increase sensitivity to recent changes; higher values smooth detection across longer timeframes. Adjust based on your trading timeframe: short-term traders use 5-15, swing traders use 20-50, position traders use 50-100.

Volume Threshold: Default: 1.0 | Range: 0.1-2.0 (step 0.1) | Multiplier applied to average volume. Bars with volume below (average × threshold) trigger void conditions. Lower values detect only extreme volume depletion; higher values capture more moderate low-volume situations. Start with 1.0 and decrease to 0.5-0.7 for stricter detection.

Price Movement Sensitivity: Default: 1.5 | Range: 0.5-5.0 (step 0.1) | Multiplier for ATR-normalized price movement detection. Values above this threshold indicate rapid price changes suggesting liquidity voids. Increase to 2.0-3.0 for volatile instruments; decrease to 0.8-1.2 for ranging or low-volatility conditions.

Minimum Void Bars: Default: 10 | Range: 1-10 | Minimum consecutive bars exhibiting void conditions required before visualization is created. Filters out brief anomalies and ensures only sustained voids are displayed. Use 1-3 for scalping, 5-10 for intraday trading, 10+ for swing trading to match your time horizon.

Visual Settings

Low Liquidity Color: Default: Red (80% transparent) | Base color for zones where volume depletion or rapid movement indicates thin liquidity. These zones recede visually (back layer most transparent). Choose colors that contrast with your chart theme for optimal visibility.

High Liquidity Color: Default: Green (80% transparent) | Base color for zones with relatively higher liquidity compared to void threshold. These zones protrude visually (front layer most transparent). Ensure clear differentiation from low liquidity color.

Show Void Labels: Default: True | Toggle display of compact LV/HV labels at void centers. Disable for cleaner charts when trading; enable for analysis and review to quickly identify void types across your chart.

Max Visible Voids: Default: 50 | Range: 10-100 | Maximum number of void visualizations kept on chart. Each void uses 3 polylines, so setting of 50 maintains 150 total polylines. Higher values preserve more history but may impact performance on lower-end systems.

✅ Best Use Cases

Gap Fill Trading: Identify unfilled liquidity voids that price frequently returns to, providing high-probability retest and reversal opportunities when price approaches these zones

Breakout Validation: Distinguish genuine breakouts through established liquidity from false breaks into void zones that lack sustainable volume support

Support/Resistance Confluence: Layer void detection over key horizontal levels to validate structural integrity—levels within high liquidity zones are stronger than those in voids

Trend Continuation: Monitor for new void formation in trend direction as potential continuation zones where price may accelerate due to reduced resistance

Range Trading: Identify void zones within consolidation ranges that price tends to traverse quickly, helping to avoid getting caught in rapid moves through thin areas

Entry Timing: Wait for price to reach void boundaries rather than entering mid-void, as voids tend to be traversed quickly with limited profit-taking opportunities

⚠️ Limitations

Historical Pattern Indicator: Identifies past liquidity voids but cannot predict whether price will return to fill them or when filling might occur

No Volume on Forex: Indicator uses tick volume for forex pairs, which approximates but doesn't represent true trading volume, potentially affecting detection accuracy

Lagging Confirmation: Requires minimum consecutive bars (default 10) before void is visualized, meaning detection occurs after void formation begins

Trending Market Behavior: Strong trends driven by fundamental catalysts may create voids that remain unfilled for extended periods or permanently

Timeframe Dependency: Detection sensitivity varies significantly across timeframes; settings optimized for one timeframe may not perform well on others

No Directional Bias: Indicator identifies liquidity characteristics but provides no predictive signal for price direction after void detection

Performance Considerations: Higher max visible void settings combined with small minimum void bars can generate numerous visualizations impacting chart rendering speed

💡 What Makes This Unique

Industry-First 3D Visualization: Unlike flat volume or liquidity indicators, the three-layer rendering with directional depth perception provides instant visual hierarchy of liquidity quality

Dual-Mode Detection: Combines both volume-based and movement-based detection methodologies, capturing voids that single-approach indicators miss

Intelligent Qualification System: State machine logic prevents premature visualization by requiring sustained void conditions, reducing false signals and chart clutter

ATR-Normalized Analysis: All detection thresholds adapt to instrument volatility, ensuring consistent performance across stocks, forex, crypto, and futures without constant recalibration

Transparency-Based Depth: Uses progressive transparency gradients rather than colors or patterns to create depth, maintaining visual clarity while conveying information hierarchy

Comprehensive Strength Metrics: 0-100 void strength calculation considers both the degree of volume depletion and the magnitude of price movement for nuanced zone characterization

🔬 How It Works

Phase 1: Real-Time Detection

On each bar close, the indicator calculates average volume over the lookback period and compares current bar volume against the volume threshold multiplier

Simultaneously measures current bar's high-low range and normalizes it against ATR, comparing the result to price movement sensitivity parameter

If either volume falls below threshold OR movement exceeds sensitivity threshold, the bar is flagged as exhibiting void characteristics

Phase 2: Void Tracking & Qualification

When void conditions first appear, state machine initializes tracking variables: start bar index, initial top/bottom prices, consecutive bar counter, and cumulative strength accumulator

Each subsequent bar with void conditions extends the tracking, updating price boundaries to envelope all bars and accumulating strength scores

When void conditions cease, system checks if consecutive bar count meets minimum threshold; if yes, proceeds to visualization; if no, discards the tracking and resets

Phase 3: 3D Visualization Construction

Calculates average void strength by dividing cumulative strength by number of bars, then determines if void is low liquidity (>50 strength) or high liquidity (≤50 strength)

Generates three polyline layers spanning from start bar to end bar and from top price to bottom price, each with calculated vertical offset based on ATR

Applies progressive transparency (85%, 78%, 70%) with layer ordering creating recession effect for low liquidity zones and protrusion effect for high liquidity zones

Creates optional center label and pushes all visual elements into arrays for memory management

Phase 4: Memory Management & Display

Continuously monitors polyline array size (each void creates 3 polylines); when total exceeds max visible voids × 3, deletes oldest polylines via array.shift()

Similarly manages label array, removing oldest labels when count exceeds maximum to prevent memory accumulation over extended chart history

Plots diagnostic data to TradingView’s data window (void detection binary, current strength, average volume) for detailed analysis without cluttering main chart

💡 Note:

This indicator is designed to enhance your market structure analysis by revealing liquidity characteristics that aren’t visible through standard price and volume displays. For best results, combine void detection with your existing support/resistance analysis, trend identification, and risk management framework. Liquidity voids are descriptive of past market behavior and should inform positioning decisions rather than serve as standalone entry/exit signals. Experiment with detection parameters across different timeframes to find settings that align with your trading style and instrument characteristics.

Continuation Index [DCAUT]█ Continuation Index

📊 OVERVIEW

Continuation Index (CI) is an advanced trend analysis indicator developed by John F. Ehlers. This indicator provides early warning signals for trend onset, continuation, and exhaustion, with values oscillating between -1 and +1 to offer clear trend state identification for traders.

Based on the article TASC 2025.09 "Trend Onset And Trend Exhaustion - The Continuation Index" by John F. Ehlers.

💡 CORE VALUE

Unlike traditional trend indicators, the Continuation Index provides:

- Advanced dual-filter architecture (Ultimate Smoother + Laguerre Filter)

- Inverse Fisher Transform for enhanced signal-to-noise ratio

- Adaptive gamma parameter allowing market-specific tuning

- Binary state output (+1/-1) eliminating interpretation ambiguity

🎯 CONCEPTS

Signal Interpretation

CI > 0.5 : Strong bullish trend continuation - consider holding/adding long positions

CI = +1 : Maximum bullish signal - strong uptrend in progress

CI < -0.5 : Strong bearish trend continuation - consider holding/adding short positions

CI = -1 : Maximum bearish signal - strong downtrend in progress

CI near 0 : Neutral zone - trend uncertain, wait for clear signals

Brief pullbacks from extreme states : Potential reentry opportunities in trend direction

Primary Applications

Trend Onset Detection : Early warning signals for trend initiation

Trend Exhaustion Signals : Identify potential trend reversals

Position Management : Clear binary states for entry/exit decisions

Market Timing : Adaptive filtering reduces false signals

📋 PARAMETER SETUP

Source : Data source for calculation (default: close)

Length : The calculation length for the filters (default: 40, min: 1)

Gamma : Controls the phase response of the Laguerre filter. Smaller values increase responsiveness (default: 0.8, range: 0.0-1.0)

Laguerre Order : The order of the Laguerre filter, which directly affects its lag (default: 8, range: 1-10)

📊 COLOR CODING

Green : CI > 0.5 - Bullish trend continuation

Red : CI < -0.5 - Bearish trend continuation

Gray : Neutral zone - Trend unclear

[DEM] Multiple Linear Regression Score Multiple Linear Regression Score is a composite momentum indicator that evaluates market conditions by analyzing a reference symbol (defaulting to NDX) across multiple technical dimensions and combining them into a single predictive score. The indicator processes ten different technical variables including RSI, MACD components (line, signal, and histogram), price relationships to various moving averages (10, 50, 100, 200), and short-term price changes (1-day and 5-day), converting most into binary signals (1 or 0) based on whether they're above or below zero. These binary and continuous inputs are then weighted using regression-derived coefficients and combined into a final percentage score that oscillates around zero, with the indicator also calculating a 20-period standard deviation of the score to measure volatility. This approach creates a data-driven sentiment gauge that quantifies the overall technical health of the reference market by mathematically weighting the importance of each technical factor based on historical relationships.

Options Trading Max Success_V1DISCLAIMER:

The information provided is NOT financial advice. I am not a financial adviser, accountant or the like. This information is purely from my own due diligence and an expression of my thoughts, my opinions based on my personal experiences, and the way I transact.

Utilize this indicator at your own risk..! The indicator creator is not liable for your loss due to untimely action / adverse consequences / server lags from Tradingview (if any).

======================================================

Welcome!

This is a 95-100% Success rate High Frequency Indicator exclusively for Binary Options Traders. It works on any time frames and pairs but is EXCLUSIVELY built for 1-minute candles for EUR/USD currency on "OANDA" forex chart. So, use it for same to get this indicator working at its best.

Use Martingale strategy (5 attempts max) for making profits / recover loss with some profits.

======================

Martingale Strategy For your knowledge with an example:

1) Lets say you are trading on binary options platform that gives 80% profit upon successful trade.

2) UP signal seen. You do the below from next candle:

a) 1st attempt = Rs.100.

- If Success, then profit = Rs.80. Cycle close and exit.

- If Loss, then do 2nd attempt.

b) 2nd attempt =Rs.200.

- If Success, then profit = Rs.160. (Rs. 100 recovery + Rs.60 Profit). Cycle close and exit.

- If Loss, then do 3rd attempt.

c) 3rd attempt = Rs. 400.

- If Success, then profit = Rs.320. (Rs. 300 recovery + Rs.20 Profit). Cycle close and exit.

- If Loss, then do 4th attempt.. and so on.

=======================

If you see any body less/Doji candle in between your attempts. Then do not continue further.

Hold this cycle for next similar stage. For example:

Select chart which promises: Success = 80% profit.

Then attempt the below on the next candle AFTER you see an UP signal.

Cycle 1: UP signal seen. 5 attempts from next candle:

Let's say:

1st attempt = Rs.100. Result = loss

2nd attempt =Rs.200. Result = loss

3rd attempt = Rs.400. Result = No profit/loss (due to Doji candle/candle without body).

Recommendation: Do not proceed further in current cycle. Hold on for next cycle/UP signal.

Park Rs.400 rupees attempt aside for a while.

Cycle 2: UP signal seen. 5 attempts from next candle:

Let's say:

1st attempt = Rs.100. Result = loss

2nd attempt =Rs.200. Result = Success

Cycle Completed. Wait for next cycle/Up signal

Cycle 3: UP signal seen. 5 attempts from next candle:

Let's say:

1st attempt = Rs.100. Result = loss

2nd attempt =Rs.200. Result = loss

3rd attempt = Now you can attempt with Rs. 800.

.

=====================

Recommendations:

- Keep a good discipline and make smart moves.

- You may add other supporting indicators of your choice along with this.

- You can keep your trading attempts low i.e. After you see an UP signal, let go the 1st one/two/three candles. If they turn out to be Red candles back to back, then good for you, as you can start entry of attempts from the 2nd/3rd/4th candle. Thereby evading one/two/three few failed attempts. If any candle gets green After Up signal and before your entry, then do not enter this cycle. Wait for next cycle.

Good luck.

================

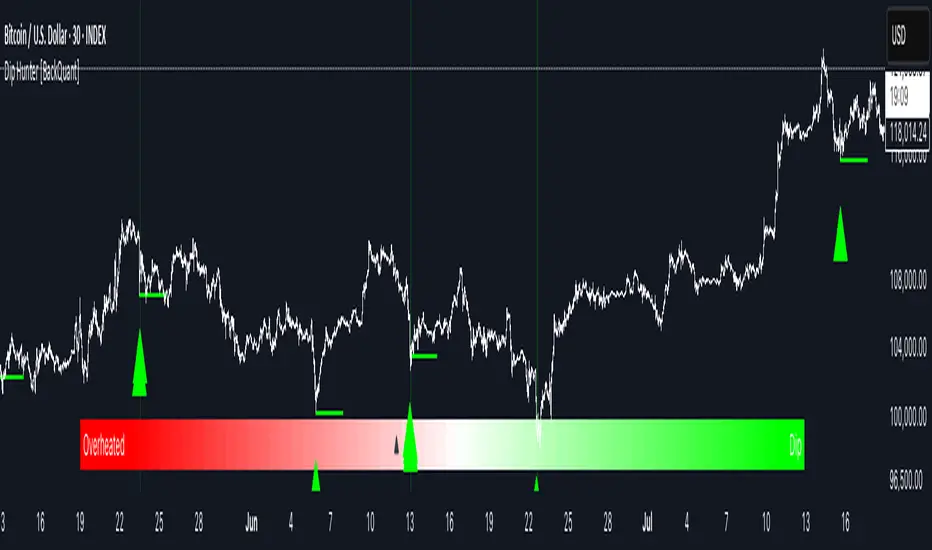

Dip Hunter [BackQuant]Dip Hunter

What this tool does in plain language

Dip Hunter is a pullback detector designed to find high quality buy-the-dip opportunities inside healthy trends and to avoid random knife catches. It watches for a quick drop from a recent high, checks that the drop happened with meaningful participation and volatility, verifies short-term weakness inside a larger uptrend, then scores the setup and paints the chart so you can act with confidence. It also draws clean entry lines, provides a meter that shows dip strength at a glance, and ships with alerts that match common execution workflows.

How Dip Hunter thinks

It defines a recent swing reference, measures how far price has dipped off that high, and only looks at candidates that meet your minimum percentage drop.

It confirms the dip with real activity by requiring a volume spike and a volatility spike.

It checks structure with two EMAs. Price should be weak in the short term while the larger context remains constructive.

It optionally requires a higher-timeframe trend to be up so you focus on pullbacks in trending markets.

It bundles those checks into a score and shows you the score on the candles and on a gradient meter.

When everything lines up it paints a green triangle below the bar, shades the background, and (if you wish) draws a horizontal entry line at your chosen level.

Inputs and what they mean

Dip Hunter Settings

• Vol Lookback and Vol Spike : The script computes an average volume over the lookback window and flags a spike when current volume is a multiple of that average. A multiplier of 2.0 means today’s volume must be at least double the average. This helps filter noise and focuses on dips that other traders actually traded.

• Fast EMA and Slow EMA : Short-term and medium-term structure references. A dip is more credible if price closes below the fast EMA while the fast EMA is still below the slow EMA during the pullback. That is classic corrective behavior inside a larger trend.

• Price Smooth : Optional smoothing length for price-derived series. Use this if you trade very noisy assets or low timeframes.

• Volatility Len and Vol Spike (volatility) : The script checks both standard deviation and true range against their own averages. If either expands beyond your multiplier the market confirms the move with range.

• Dip % and Lookback Bars : The engine finds the highest high over the lookback window, then computes the percentage drawdown from that high to the current close. Only dips larger than your threshold qualify.

Trend Filter

• Enable Trend Filter : When on, Dip Hunter will only trigger if the market is in an uptrend.

• Trend EMA Period : The longer EMA that defines the session’s backbone trend.

• Minimum Trend Strength : A small positive slope requirement. In practice this means the trend EMA should be rising, and price should be above it. You can raise the value to be more selective.

Entries

• Show Entry Lines : Draws a horizontal guide from the signal bar for a fixed number of bars. Great for limit orders, scaling, or re-tests.

• Line Length (bars) : How far the entry guide extends.

• Min Gap (bars) : Suppresses new entry lines if another dip fired recently. Prevents clutter during choppy sequences.

• Entry Price : Choose the line level. “Low” anchors at the signal candle’s low. “Close” anchors at the signal close. “Dip % Level” anchors at the theoretical level defined by recent_high × (1 − dip%). This lets you work resting orders at a consistent discount.

Heat / Meter