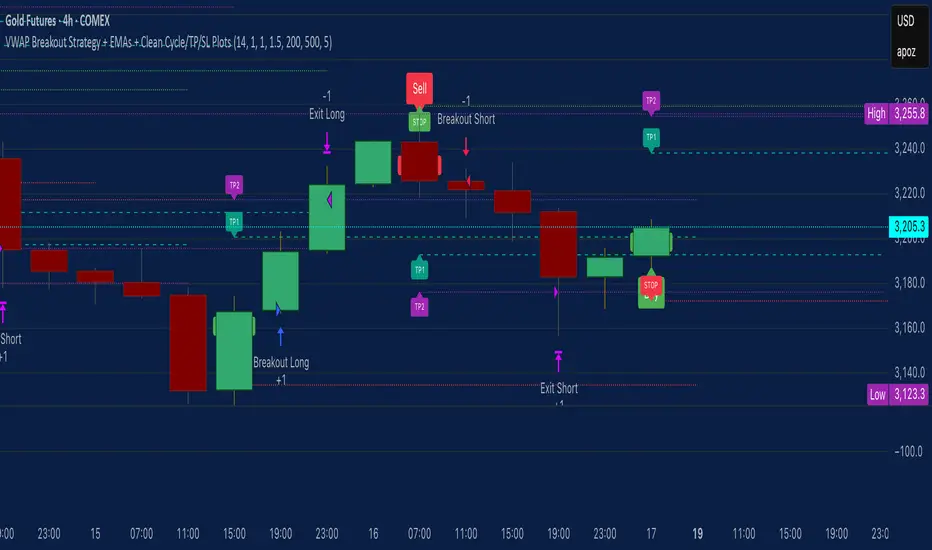

VWAP Breakout Strategy + EMAs + Clean Cycle/TP/SL PlotsHere’s a quick user-guide to get you up and running with your “VWAP Breakout Strategy + EMAs + Clean Cycle/TP/SL Plots” script in TradingView:

⸻

1. Installing the Script

1. Open TradingView, go to Pine Editor (bottom panel).

2. Paste in your full Pine-v6 code and hit Add to chart.

3. Save it (“Save as…”): give it a memorable name (e.g. “VWAP Breakout+EMAs”).

⸻

2. Configuring Your Inputs

Once it’s on the chart, click the ⚙️ Settings icon to tune:

Setting Default What it does

ATR Length 14 Period for average true range (volatility measure)

ATR Multiplier for Stop 1.5 How many ATRs away your stop-loss sits

TP1 / TP2 Multipliers (ATR) 1.0 / 2.0 Distance of TP1 and TP2 in ATR multiples

Show VWAP / EMAs On Toggles the blue VWAP line & EMAs (100/34/5)

Full Cycle Range Points 200 Height of the shaded “cycle zone”

Pivot Lookback 5 How many bars back to detect a pivot low

Round Number Step 500 Spacing of your dotted horizontal lines

Show TP/SL Labels On Toggles all the “ENTRY”, “TP1”, “TP2”, “STOP” tags

Feel free to adjust ATR multipliers and cycle-zone size based on the instrument’s typical range.

⸻

3. Reading the Signals

• Long Entry:

• Trigger: price crosses above VWAP

• You’ll see a green “Buy” tag at the low of the signal bar, plus an “ENTRY (Long)” label at the close.

• Stop is plotted as a red dashed line below (ATR × 1.5), and TP1/TP2 as teal and purple lines above.

• Short Entry:

• Trigger: price crosses below VWAP

• A red “Sell” tag appears at the high, with “ENTRY (Short)” at the close.

• Stop is the green line above; TP1/TP2 are dashed teal/purple lines below.

⸻

4. Full Cycle Zone

Whenever a new pivot low is detected (using your Pivot Lookback), the script deletes the old box and draws a shaded yellow rectangle from that low up by “Full Cycle Range Points.”

• Use this to visualize the “maximum expected swing” from your pivot.

• You can quickly see whether price is still traveling within a normal cycle or has overstretched.

⸻

5. Round-Number Levels

With Show Round Number Levels enabled, you’ll always get horizontal dotted lines at the nearest multiples of your “Round Number Step” (e.g. every 500 points).

• These often act as psychological support/resistance.

• Handy to see confluence with VWAP or cycle-zone edges.

⸻

6. Tips & Best-Practices

• Timeframes: Apply on any intraday chart (5 min, 15 min, H1…), but match your ATR length & cycle-points to the timeframe’s typical range.

• Backtest first: Use the Strategy Tester tab to review performance, tweak ATR multipliers or cycle size, then optimize.

• Combine with context: Don’t trade VWAP breakouts blindly—look for confluence (e.g. support/resistance zones, higher-timeframe trend).

• Label clutter: If too many labels build up, you can toggle Show TP/SL Labels off and rely just on the lines.

⸻

That’s it! Once you’ve added it to your chart and dialed in the inputs, your entries, exits, cycle ranges, and key levels will all be plotted automatically. Feel free to experiment with the ATR multipliers and cycle-zone size until it fits your instrument’s personality. Happy trading!

Search in scripts for "entry"

RCI Strategy [PineIndicators]RCI Strategy

This strategy leverages the Rank Correlation Index (RCI) — a statistical oscillator that measures the relationship between time and price rank — combined with a configurable moving average filter. It offers clean, rule-based entries and exits, and visually enhanced trade tracking via labeled markers and boxes on the chart.

The RCI Strategy is well-suited for momentum traders looking to capture directional shifts with confirmation through RCI smoothing.

Core Logic

1. Rank Correlation Index (RCI)

Measures how closely price changes correlate with time rankings.

Values range between -100 and +100.

Thresholds at ±80 help identify potential reversals or extremes.

2. RCI Smoothing via Moving Average

A moving average (MA) is applied to the RCI to smooth out fluctuations.

Supported MA types:

SMA

EMA

SMMA (RMA)

WMA

VWMA

Users can disable the smoothing by selecting "None".

Trade Entry Logic

Long Entry: RCI crosses above the selected moving average.

Short Entry: RCI crosses below the moving average.

Entries are restricted by trade direction settings:

Long Only

Short Only

Long & Short

Visual Features

RCI Panel Display

Plots RCI line and its moving average in a separate pane.

Horizontal guide lines at 0, +80, and -80 help visualize signal zones.

Trade Labels on Chart

Buy Label: Plotted when a long entry is executed.

Close Label: Plotted when any position is closed.

Triangle markers for visual emphasis on direction change.

Trade Visualization Boxes

A colored box is drawn between entry and exit prices.

Green = profitable trade; Red = losing trade.

Two horizontal lines connect entry and exit prices for reference.

Customization Parameters

RCI Source: Select input price for the RCI (default: close).

RCI Length: Set sensitivity of the oscillator.

MA Type and Length: Choose and configure the smoothing filter.

Trade Direction Mode: Define whether to allow Long, Short, or both.

Use Cases

Swing traders who want to trade directional reversals with statistical backing.

Traders seeking a clean and visual strategy based on rank momentum.

Environments where both trend and range dynamics occur.

Conclusion

The RCI Strategy is a non-repainting, rule-based trading model that combines rank correlation momentum with smoothed trend logic. Its clean visual markers, labeled trades, and flexible MA filters make it a valuable tool for discretionary and systematic traders alike.

Parabolic RSI Strategy [ChartPrime × PineIndicators]This strategy combines the strengths of the Relative Strength Index (RSI) with a Parabolic SAR logic applied directly to RSI values.

Full credit to ChartPrime for the original concept and indicator, licensed under the MPL 2.0.

It provides clear momentum-based trade signals using an innovative method that tracks RSI trend reversals via a customized Parabolic SAR, enhancing traditional oscillator strategies with dynamic trend confirmation.

How It Works

The system overlays a Parabolic SAR on the RSI, detecting trend shifts in RSI itself rather than on price, offering early reversal insight with visual and algorithmic clarity.

Core Components

1. RSI-Based Trend Detection

Calculates RSI using a customizable length (default: 14).

Uses upper and lower thresholds (default: 70/30) for overbought/oversold zones.

2. Parabolic SAR Applied to RSI

A custom Parabolic SAR function tracks momentum within the RSI, not price.

This allows the system to capture RSI trend reversals more responsively.

Configurable SAR parameters: Start, Increment, and Maximum acceleration.

3. Signal Generation

Long Entry: Triggered when the SAR flips below the RSI line.

Short Entry: Triggered when the SAR flips above the RSI line.

Optional RSI filter ensures that:

Long entries only occur above a minimum RSI (e.g. 50).

Short entries only occur below a maximum RSI.

Built-in logic prevents new positions from being opened against trend without prior exit.

Trade Modes & Controls

Choose from:

Long Only

Short Only

Long & Short

Optional setting to reverse positions on opposite signal (instead of waiting for a flat close).

Visual Features

1. RSI Plotting with Thresholds

RSI is displayed in a dedicated pane with overbought/oversold fill zones.

Custom horizontal lines mark threshold boundaries.

2. Parabolic SAR Overlay on RSI

SAR dots color-coded for trend direction.

Visible only when enabled by user input.

3. Entry & Exit Markers

Diamonds: Mark entry points (above for shorts, below for longs).

Crosses: Mark exit points.

Strategy Strengths

Provides early momentum reversal entries without relying on price candles.

Combines oscillator and trend logic without repainting.

Works well in both trending and mean-reverting markets.

Easy to configure with fine-tuned filter options.

Recommended Use Cases

Intraday or swing traders who want to catch RSI-based reversals early.

Traders seeking smoother signals than price-based Parabolic SAR entries.

Users of RSI looking to reduce false positives via trend tracking.

Customization Options

RSI Length and Thresholds.

SAR Start, Increment, and Maximum values.

Trade Direction Mode (Long, Short, Both).

Optional RSI filter and reverse-on-signal settings.

SAR dot color customization.

Conclusion

The Parabolic RSI Strategy is an innovative, non-repainting momentum strategy that enhances RSI-based systems with trend-confirming logic using Parabolic SAR. By applying SAR logic to RSI values, this strategy offers early, visualized, and filtered entries and exits that adapt to market dynamics.

Credit to ChartPrime for the original methodology, published under MPL-2.0.

HMA 200 + EMA 20 Crossover StrategyThis strategy combines a long-term trend filter using the Hull Moving Average (HMA 200) with a short-term entry trigger using the Exponential Moving Average (EMA 20).

📈 Entry Logic:

Buy Entry: When price is above the HMA 200 and crosses above the EMA 20.

Sell Entry: When price is below the HMA 200 and crosses below the EMA 20.

The strategy closes the current position and reverses on the opposite signal.

⚙️ Strategy Settings (Backtest Configuration):

Position size: 10% of equity per trade

Commission: 0.1% per trade (to simulate broker fees)

Slippage: 2 ticks (to reflect realistic fill conditions)

✅ Purpose:

This script is designed to identify high-probability trades in the direction of the overall trend, avoiding whipsaw conditions. It is useful for traders looking for a dynamic crossover-based system that filters trades based on longer-term momentum.

🔎 Make sure to test across multiple assets and timeframes. For best results, apply this strategy to liquid trending markets like major FX pairs, indices, or high-cap stocks.

ADX and DI - Trader FelipeADX and DI - Trader Felipe

This indicator combines the Average Directional Index (ADX) and the Directional Indicators (DI+ and DI-) to help traders assess market trends and their strength. It is designed to provide a clear view of whether the market is in a trending phase (either bullish or bearish) and helps identify potential entry and exit points.

What is ADX and DI?

DI+ (Green Line):

DI+ measures the strength of upward (bullish) price movements. When DI+ is above DI-, it signals that the market is experiencing upward momentum.

DI- (Red Line):

DI- measures the strength of downward (bearish) price movements. When DI- is above DI+, it suggests that the market is in a bearish phase, with downward momentum.

ADX (Blue Line):

ADX quantifies the strength of the trend, irrespective of whether it is bullish or bearish. The higher the ADX, the stronger the trend:

ADX > 20: Indicates a trending market (either up or down).

ADX < 20: Indicates a weak or sideways market with no clear trend.

Threshold Line (Gray Line):

This horizontal line, typically set at 20, represents the threshold for identifying whether the market is trending or not. If ADX is above 20, the market is considered to be in a trend. If ADX is below 20, it suggests that the market is not trending and is likely in a consolidation phase.

Summary of How to Use the Indicator:

Trend Confirmation: Use ADX > 20 to confirm a trending market. If ADX is below 20, avoid trading.

Long Entry: Enter a long position when DI+ > DI- and ADX > 20.

Short Entry: Enter a short position when DI- > DI+ and ADX > 20.

Avoid Sideways Markets: Do not trade when ADX is below 20. Look for other strategies for consolidation phases.

Exit Strategy: Exit the trade if ADX starts to decline or if the DI lines cross in the opposite direction.

Combine with Other Indicators: Use additional indicators like RSI, moving averages, or support/resistance to filter and confirm signals.

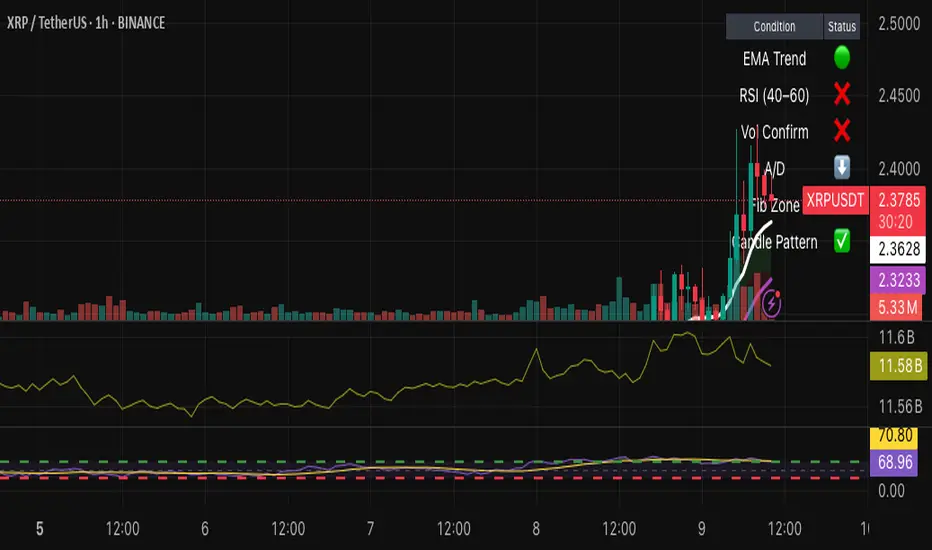

Hybrid Swing/Day Alert System - PLATINUM EditionThis indicator is a complete trading assistant designed for crypto swing and day traders, built to identify high-probability long and short setups based on a multi-confirmation system.

Strategy Logic

The system scans and confirms entries only when 6 major confluences align:

1. EMA Trend: Price is above or below the EMA 9, 21, and 200 (bullish or bearish trend).

2. RSI Zone: RSI(14) is between 40-60 (ideal reversal zone).

3. Volume Confirmation: Volume is declining on pullback and then spikes.

4. Accumulation/Distribution: A/D line rising (for longs) or falling (for shorts).

5. Fibonacci Pullback Zone: Automatic detection of swing high/low and checks if price is inside the golden zone (0.5-0.618).

Built-In Alerts

- Long Setup Confirmed - Short Setup Confirmed - Setup Forming: Monitor

Conclusion

This script is ideal for disciplined traders who value confluence-based entries, risk/reward logic, and trend-aligned trades. Perfect for semi-automated trading via alerts or manual execution.6. Candle Pattern: Bullish (hammer, doji, engulfing) or Bearish (rejection wick, engulfing, doji).

Visual Features

- Long Entry: Green square

- Short Entry: Red triangle

- Pre-Signal Alert: Blue circle (confluence forming)

- Dynamic Table: Displays all 6 confirmations in real time

- Fibonacci Zones: Auto-plotted long/short retracement zones

- Customizable: Turn on/off alerts, overlays, and direction filters

Best Use Cases

- 4H/Daily: Trend confirmation

- 1H: Entry execution

- 15min: Scalping (use cautiously)

- Works great with BTC, ETH, SOL, XAU, and meme coins

Ceres Trader Simple Trend & Momentum SignalsCeres Trader – Simple Trend & Momentum Signals

Description:

Cut through chart noise with a lightweight, two-factor signal system that combines a classic trend filter (200 EMA) with momentum confirmation (smoothed RSI as a QQE proxy). This indicator plots clean entry arrows—no background shading, no clutter—so you can trade only in the high-probability regime:

Trend Filter: 200-period exponential moving average

Momentum Filter: RSI(14) smoothed over N bars, offset by 50 to create a zero-line

Long Entry: Price above the 200 EMA and the smoothed RSI crosses up through zero → green up-arrow below bar

Short Entry: Price below the 200 EMA and the smoothed RSI crosses down through zero → red down-arrow above bar

Key Features:

Minimalist display: only the 200 EMA and entry arrows

Customizable inputs: EMA length, RSI length, RSI smoothing period

Ultra-low CPU load: suitable for lower timeframes (e.g. 1 min gold futures)

Yellow label text: for optimal visibility on dark or light chart backgrounds

How to Use:

Add the script to your TradingView chart.

Choose your timeframe and adjust inputs as needed.

Take only the long signals when price is above the EMA, and only the short signals when price is below.

Place stops just beyond the EMA; targets can be measured swings or fixed R-multiples.

Notes:

Designed as a regime-based entry filter—no exits or background fills included.

Feel free to combine with your own stop-loss, take-profit, and money-management rules.

Trade smarter, not harder—let the market tell you only when both trend and momentum align.

Timeframe StrategyThis is a multi-timeframe trading strategy inspired by Ross Cameron's style, optimized for scalping and trend-following across various timeframes (1m, 5m, 15m, 1h, and 1D). The strategy integrates a comprehensive set of technical indicators, dynamic risk management, and visual tools.

Core Features

Dynamic Take Profit, Stop Loss & Trailing Stop

> Separate settings per timeframe for:

-TP% (Take Profit)

-SL% (Stop Loss)

-Trailing Stop %

-Cooldown bars

> Configurable via UI inputs.

>Smart Entry Conditions

Bullish entry: EMA9 crossover EMA20 and EMA50 > EMA200

Bearish entry: EMA9 crossunder EMA20 and EMA50 < EMA200

>Additional confirmation filters:

-Volume Filter (enabled/disabled via UI)

-Time Filter (e.g., only between 15:00–20:00 UTC)

-Spike Filter: rejects high-volatility candles

-RSI Filter: above/below 50 for trend confirmation

-ADX Filter (only applied on 1m, e.g., ADX > 15)

-Micro-Volatility Filter: minimum range percentage (1m only)

-Trend Filter (1m only): price must be above/below EMA200

>Trailing Stop Logic

-Configurable for each timeframe.

- Optional via toggle (use_trailing).

>Trade Cooldown Logic

-Prevents consecutive trades within X bars, configurable per timeframe.

>Technical Indicators Used

-EMA 9 / 20 / 50 / 200

-VWAP

-RSI (14)

-ATR (14) for volatility-based spike filtering

-Custom-calculated ADX (14) (manually implemented)

>Visual Elements

🔼/🔽 Entry signals (long/short) plotted on the chart.

📉 Table in bottom-left:

Displays current values of EMA/VWAP/volume/ATR/ADX.

> Optional "Tab info" panel in top-right (toggleable):

-Timeframe & strategy settings

-Live status of filters (volume, time, cooldown, spike, RSI, ADX, range, trend)

-Uses emoji (✅ / ❌) for quick diagnostics.

>User Customization

-Inputs per timeframe for all key parameters.

-Toggle switches for:

-Trailing stop

-Volume filter

-Info table visibility

This strategy is designed for active traders seeking a balance between momentum entry, risk control, and adaptability across timeframes. It's ideal for backtesting quick reversals or breakout setups in fast markets, especially at lower timeframes like 1m or 5m.

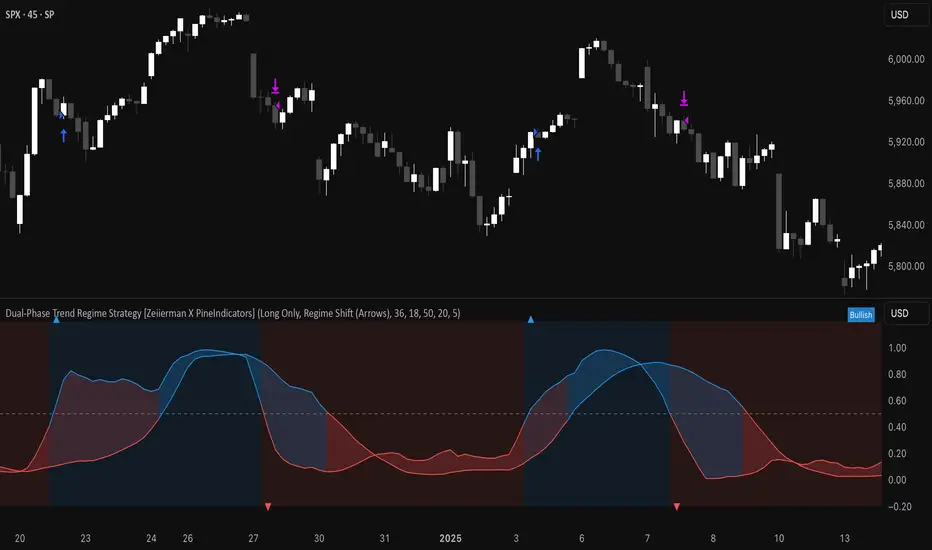

Dual-Phase Trend Regime Strategy [Zeiierman X PineIndicators]This strategy is based on the Dual-Phase Trend Regime Indicator by Zeiierman.

Full credit for the original concept and logic goes to Zeiierman.

This non-repainting strategy dynamically switches between fast and slow oscillators based on market volatility, providing adaptive entries and exits with high clarity and reliability.

Core Concepts

1. Adaptive Dual Oscillator Logic

The system uses two oscillators:

Fast Oscillator: Activated in high-volatility phases for quick reaction.

Slow Oscillator: Used during low-volatility phases to reduce noise.

The system automatically selects the appropriate oscillator depending on the market's volatility regime.

2. Volatility Regime Detection

Volatility is calculated using the standard deviation of returns. A median-split algorithm clusters volatility into:

Low Volatility Cluster

High Volatility Cluster

The current volatility is then compared to these clusters to determine whether the regime is low or high volatility.

3. Trend Regime Identification

Based on the active oscillator:

Bullish Trend: Oscillator > 0.5

Bearish Trend: Oscillator < 0.5

Neutral Trend: Oscillator = 0.5

The strategy reacts to changes in this trend regime.

4. Signal Source Options

You can choose between:

Regime Shift (Arrows): Trade based on oscillator value changes (from bullish to bearish and vice versa).

Oscillator Cross: Trade based on crossovers between the fast and slow oscillators.

Trade Logic

Trade Direction Options

Long Only

Short Only

Long & Short

Entry Conditions

Long Entry: Triggered on bullish regime shift or fast crossing above slow.

Short Entry: Triggered on bearish regime shift or fast crossing below slow.

Exit Conditions

Long Exit: Triggered on bearish shift or fast crossing below slow.

Short Exit: Triggered on bullish shift or fast crossing above slow.

The strategy closes opposing positions before opening new ones.

Visual Features

Oscillator Bands: Plots fast and slow oscillators, colored by trend.

Background Highlight: Indicates current trend regime.

Signal Markers: Triangle shapes show bullish/bearish shifts.

Dashboard Table: Displays live trend status ("Bullish", "Bearish", "Neutral") in the chart’s corner.

Inputs & Customization

Oscillator Periods – Fast and slow lengths.

Refit Interval – How often volatility clusters update.

Volatility Lookback & Smoothing

Color Settings – Choose your own bullish/bearish colors.

Signal Mode – Regime shift or oscillator crossover.

Trade Direction Mode

Use Cases

Swing Trading: Take entries based on adaptive regime shifts.

Trend Following: Follow the active trend using filtered oscillator logic.

Volatility-Responsive Systems: Adjust your trade behavior depending on market volatility.

Clean Exit Management: Automatically closes positions on opposite signal.

Conclusion

The Dual-Phase Trend Regime Strategy is a smart, adaptive, non-repainting system that:

Automatically switches between fast and slow trend logic.

Responds dynamically to changes in volatility.

Provides clean and visual entry/exit signals.

Supports both momentum and reversal trading logic.

This strategy is ideal for traders seeking a volatility-aware, trend-sensitive tool across any market or timeframe.

Full credit to Zeiierman.

Dskyz (DAFE) Aurora Divergence – Quant Master Dskyz (DAFE) Aurora Divergence – Quant Master

Introducing the Dskyz (DAFE) Aurora Divergence – Quant Master , a strategy that’s your secret weapon for mastering futures markets like MNQ, NQ, MES, and ES. Born from the legendary Aurora Divergence indicator, this fully automated system transforms raw divergence signals into a quant-grade trading machine, blending precision, risk management, and cyberpunk DAFE visuals that make your charts glow like a neon skyline. Crafted with care and driven by community passion, this strategy stands out in a sea of generic scripts, offering traders a unique edge to outsmart institutional traps and navigate volatile markets.

The Aurora Divergence indicator was a cult favorite for spotting price-OBV divergences with its aqua and fuchsia orbs, but traders craved a system to act on those signals with discipline and automation. This strategy delivers, layering advanced filters (z-score, ATR, multi-timeframe, session), dynamic risk controls (kill switches, adaptive stops/TPs), and a real-time dashboard to turn insights into profits. Whether you’re a newbie dipping into futures or a pro hunting reversals, this strat’s got your back with a beginner guide, alerts, and visuals that make trading feel like a sci-fi mission. Let’s dive into every detail and see why this original DAFE creation is a must-have.

Why Traders Need This Strategy

Futures markets are a battlefield—fast-paced, volatile, and riddled with institutional games that can wipe out undisciplined traders. From the April 28, 2025 NQ 1k-point drop to sneaky ES slippage, the stakes are high. Meanwhile, platforms are flooded with unoriginal, low-effort scripts that promise the moon but deliver noise. The Aurora Divergence – Quant Master rises above, offering:

Unmatched Originality: A bespoke system built from the ground up, with custom divergence logic, DAFE visuals, and quant filters that set it apart from copycat clutter.

Automation with Precision: Executes trades on divergence signals, eliminating emotional slip-ups and ensuring consistency, even in chaotic sessions.

Quant-Grade Filters: Z-score, ATR, multi-timeframe, and session checks filter out noise, targeting high-probability reversals.

Robust Risk Management: Daily loss and rolling drawdown kill switches, plus ATR-based stops/TPs, protect your capital like a fortress.

Stunning DAFE Visuals: Aqua/fuchsia orbs, aurora bands, and a glowing dashboard make signals intuitive and charts a work of art.

Community-Driven: Evolved from trader feedback, this strat’s a labor of love, not a recycled knockoff.

Traders need this because it’s a complete, original system that blends accessibility, sophistication, and style. It’s your edge to trade smarter, not harder, in a market full of traps and imitators.

1. Divergence Detection (Core Signal Logic)

The strategy’s core is its ability to detect bullish and bearish divergences between price and On-Balance Volume (OBV), pinpointing reversals with surgical accuracy.

How It Works:

Price Slope: Uses linear regression over a lookback (default: 9 bars) to measure price momentum (priceSlope).

OBV Slope: OBV tracks volume flow (+volume if price rises, -volume if falls), with its slope calculated similarly (obvSlope).

Bullish Divergence: Price slope negative (falling), OBV slope positive (rising), and price above 50-bar SMA (trend_ma).

Bearish Divergence: Price slope positive (rising), OBV slope negative (falling), and price below 50-bar SMA.

Smoothing: Requires two consecutive divergence bars (bullDiv2, bearDiv2) to confirm signals, reducing false positives.

Strength: Divergence intensity (divStrength = |priceSlope * obvSlope| * sensitivity) is normalized (0–1, divStrengthNorm) for visuals.

Why It’s Brilliant:

- Divergences catch hidden momentum shifts, often exploited by institutions, giving you an edge on reversals.

- The 50-bar SMA filter aligns signals with the broader trend, avoiding choppy markets.

- Adjustable lookback (min: 3) and sensitivity (default: 1.0) let you tune for different instruments or timeframes.

2. Filters for Precision

Four advanced filters ensure signals are high-probability and market-aligned, cutting through the noise of volatile futures.

Z-Score Filter:

Logic: Calculates z-score ((close - SMA) / stdev) over a lookback (default: 50 bars). Blocks entries if |z-score| > threshold (default: 1.5) unless disabled (useZFilter = false).

Impact: Avoids trades during extreme price moves (e.g., blow-off tops), keeping you in statistically safe zones.

ATR Percentile Volatility Filter:

Logic: Tracks 14-bar ATR in a 100-bar window (default). Requires current ATR > 80th percentile (percATR) to trade (tradeOk).

Impact: Ensures sufficient volatility for meaningful moves, filtering out low-volume chop.

Multi-Timeframe (HTF) Trend Filter:

Logic: Uses a 50-bar SMA on a higher timeframe (default: 60min). Longs require price > HTF MA (bullTrendOK), shorts < HTF MA (bearTrendOK).

Impact: Aligns trades with the bigger trend, reducing counter-trend losses.

US Session Filter:

Logic: Restricts trading to 9:30am–4:00pm ET (default: enabled, useSession = true) using America/New_York timezone.

Impact: Focuses on high-liquidity hours, avoiding overnight spreads and erratic moves.

Evolution:

- These filters create a robust signal pipeline, ensuring trades are timed for optimal conditions.

- Customizable inputs (e.g., zThreshold, atrPercentile) let traders adapt to their style without compromising quality.

3. Risk Management

The strategy’s risk controls are a masterclass in balancing aggression and safety, protecting capital in volatile markets.

Daily Loss Kill Switch:

Logic: Tracks daily loss (dayStartEquity - strategy.equity). Halts trading if loss ≥ $300 (default) and enabled (killSwitch = true, killSwitchActive).

Impact: Caps daily downside, crucial during events like April 27, 2025 ES slippage.

Rolling Drawdown Kill Switch:

Logic: Monitors drawdown (rollingPeak - strategy.equity) over 100 bars (default). Stops trading if > $1000 (rollingKill).

Impact: Prevents prolonged losing streaks, preserving capital for better setups.

Dynamic Stop-Loss and Take-Profit:

Logic: Stops = entry ± ATR * multiplier (default: 1.0x, stopDist). TPs = entry ± ATR * 1.5x (profitDist). Longs: stop below, TP above; shorts: vice versa.

Impact: Adapts to volatility, keeping stops tight but realistic, with TPs targeting 1.5:1 reward/risk.

Max Bars in Trade:

Logic: Closes trades after 8 bars (default) if not already exited.

Impact: Frees capital from stagnant trades, maintaining efficiency.

Kill Switch Buffer Dashboard:

Logic: Shows smallest buffer ($300 - daily loss or $1000 - rolling DD). Displays 0 (red) if kill switch active, else buffer (green).

Impact: Real-time risk visibility, letting traders adjust dynamically.

Why It’s Brilliant:

- Kill switches and ATR-based exits create a safety net, rare in generic scripts.

- Customizable risk inputs (maxDailyLoss, dynamicStopMult) suit different account sizes.

- Buffer metric empowers disciplined trading, a DAFE signature.

4. Trade Entry and Exit Logic

The entry/exit rules are precise, filtered, and adaptive, ensuring trades are deliberate and profitable.

Entry Conditions:

Long Entry: bullDiv2, cooldown passed (canSignal), ATR filter passed (tradeOk), in US session (inSession), no kill switches (not killSwitchActive, not rollingKill), z-score OK (zOk), HTF trend bullish (bullTrendOK), no existing long (lastDirection != 1, position_size <= 0). Closes shorts first.

Short Entry: Same, but for bearDiv2, bearTrendOK, no long (lastDirection != -1, position_size >= 0). Closes longs first.

Adaptive Cooldown: Default 2 bars (cooldownBars). Doubles (up to 10) after a losing trade, resets after wins (dynamicCooldown).

Exit Conditions:

Stop-Loss/Take-Profit: Set per trade (ATR-based). Exits on stop/TP hits.

Other Exits: Closes if maxBarsInTrade reached, ATR filter fails, or kill switch activates.

Position Management: Ensures no conflicting positions, closing opposites before new entries.

Built To Be Reliable and Consistent:

- Multi-filtered entries minimize false signals, a stark contrast to basic scripts.

- Adaptive cooldown prevents overtrading, especially after losses.

- Clean position handling ensures smooth execution, even in fast markets.

5. DAFE Visuals

The visuals are a DAFE hallmark, blending function with clean flair to make signals intuitive and charts stunning.

Aurora Bands:

Display: Bands around price during divergences (bullish: below low, bearish: above high), sized by ATR * bandwidth (default: 0.5).

Colors: Aqua (bullish), fuchsia (bearish), with transparency tied to divStrengthNorm.

Purpose: Highlights divergence zones with a glowing, futuristic vibe.

Divergence Orbs:

Display: Large/small circles (aqua below for bullish, fuchsia above for bearish) when bullDiv2/bearDiv2 and canSignal. Labels show strength (0–1).

Purpose: Pinpoints entries with eye-catching clarity.

Gradient Background:

Display: Green (bullish), red (bearish), or gray (neutral), 90–95% transparent.

Purpose: Sets the market mood without clutter.

Strategy Plots:

- Stop/TP Lines: Red (stops), green (TPs) for active trades.

- HTF MA: Yellow line for trend context.

- Z-Score: Blue step-line (if enabled).

- Kill Switch Warning: Red background flash when active.

What Makes This Next-Level?:

- Visuals make complex signals (divergences, filters) instantly clear, even for beginners.

- DAFE’s unique aesthetic (orbs, bands) sets it apart from generic scripts, reinforcing originality.

- Functional plots (stops, TPs) enhance trade management.

6. Metrics Dashboard

The top-right dashboard (2x8 table) is your command center, delivering real-time insights.

Metrics:

Daily Loss ($): Current loss vs. day’s start, red if > $300.

Rolling DD ($): Drawdown vs. 100-bar peak, red if > $1000.

ATR Threshold: Current percATR, green if ATR exceeds, red if not.

Z-Score: Current value, green if within threshold, red if not.

Signal: “Bullish Div” (aqua), “Bearish Div” (fuchsia), or “None” (gray).

Action: “Consider Buying”/“Consider Selling” (signal color) or “Wait” (gray).

Kill Switch Buffer ($): Smallest buffer to kill switch, green if > 0, red if 0.

Why This Is Important?:

- Consolidates critical data, making decisions effortless.

- Color-coded metrics guide beginners (e.g., green action = go).

- Buffer metric adds transparency, rare in off-the-shelf scripts.

7. Beginner Guide

Beginner Guide: Middle-right table (shown once on chart load), explains aqua orbs (bullish, buy) and fuchsia orbs (bearish, sell).

Key Features:

Futures-Optimized: Tailored for MNQ, NQ, MES, ES with point-value adjustments.

Highly Customizable: Inputs for lookback, sensitivity, filters, and risk settings.

Real-Time Insights: Dashboard and visuals update every bar.

Backtest-Ready: Fixed qty and tick calc for accurate historical testing.

User-Friendly: Guide, visuals, and dashboard make it accessible yet powerful.

Original Design: DAFE’s unique logic and visuals stand out from generic scripts.

How to Use

Add to Chart: Load on a 5min MNQ/ES chart in TradingView.

Configure Inputs: Adjust instrument, filters, or risk (defaults optimized for MNQ).

Monitor Dashboard: Watch signals, actions, and risk metrics (top-right).

Backtest: Run in strategy tester to evaluate performance.

Live Trade: Connect to a broker (e.g., Tradovate) for automation. Watch for slippage (e.g., April 27, 2025 ES issues).

Replay Test: Use bar replay (e.g., April 28, 2025 NQ drop) to test volatility handling.

Disclaimer

Trading futures involves significant risk of loss and is not suitable for all investors. Past performance is not indicative of future results. Backtest results may not reflect live trading due to slippage, fees, or market conditions. Use this strategy at your own risk, and consult a financial advisor before trading. Dskyz (DAFE) Trading Systems is not responsible for any losses incurred.

Backtesting:

Frame: 2023-09-20 - 2025-04-29

Fee Typical Range (per side, per contract)

CME Exchange $1.14 – $1.20

Clearing $0.10 – $0.30

NFA Regulatory $0.02

Firm/Broker Commis. $0.25 – $0.80 (retail prop)

TOTAL $1.60 – $2.30 per side

Round Turn: (enter+exit) = $3.20 – $4.60 per contract

Final Notes

The Dskyz (DAFE) Aurora Divergence – Quant Master isn’t just a strategy—it’s a movement. Crafted with originality and driven by community passion, it rises above the flood of generic scripts to deliver a system that’s as powerful as it is beautiful. With its quant-grade logic, DAFE visuals, and robust risk controls, it empowers traders to tackle futures with confidence and style. Join the DAFE crew, light up your charts, and let’s outsmart the markets together!

(This publishing will most likely be taken down do to some miscellaneous rule about properly displaying charting symbols, or whatever. Once I've identified what part of the publishing they want to pick on, I'll adjust and repost.)

Use it with discipline. Use it with clarity. Trade smarter.

**I will continue to release incredible strategies and indicators until I turn this into a brand or until someone offers me a contract.

Created by Dskyz, powered by DAFE Trading Systems. Trade fast, trade bold.

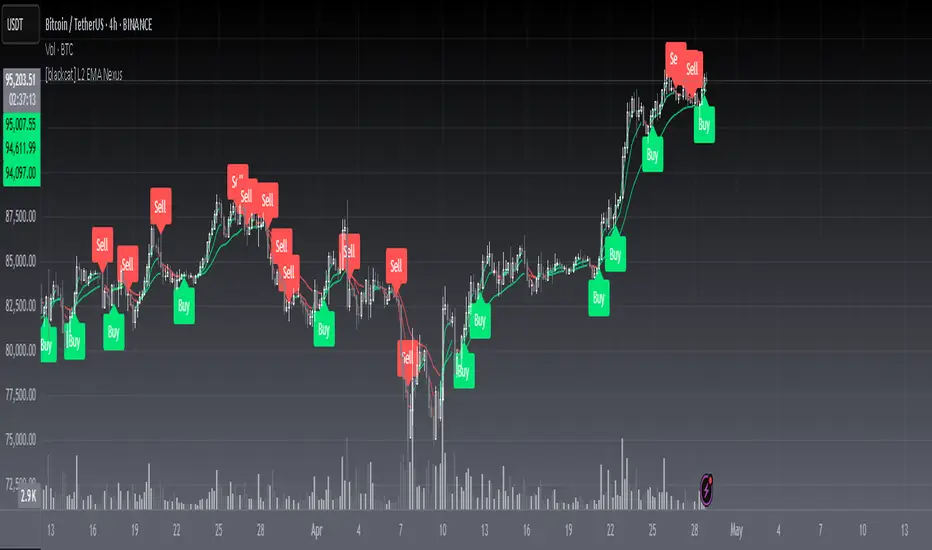

[blackcat] L2 EMA NexusOVERVIEW

The L2 EMA Nexus is a comprehensive trading indicator that utilizes a three-tiered Exponential Moving Average (EMA) system to identify potential trading opportunities. This script combines technical analysis with robust risk management features to help traders make informed decisions.

KEY FEATURES

• Triple EMA Analysis:

Customizable source inputs for each EMA

Adjustable length parameters (3, 8, 21 periods)

Dynamic color coding based on trend direction

Real-time price action monitoring

• Advanced Entry Signals:

High-low price action verification

EMA cross-overs and cross-unders

Multi-timeframe trend confirmation

Dynamic position sizing limits

• Risk Management:

Configurable Take Profit levels

Flexible Stop Loss settings

Optional TP/SL activation

Clear visual indicators for levels

HOW TO USE

Setup Initial Parameters:

Configure EMA lengths for your timeframe

Set Take Profit percentage (default 25%)

Define Stop Loss percentage (default 2.5%)

Adjust pyramiding limit as needed

Enable/Disable Features:

Toggle TP/SL settings based on strategy

Customize alert conditions

Modify visual labels for clarity

Monitor Trading Signals:

Watch for buy/sell labels

Track TP/SL levels

Monitor position status

TRADE MANAGEMENT

• Entry Conditions:

Long Entry: Higher high with rising EMA1 and stable EMA3

Short Entry: Lower low with falling EMA1 and stable EMA2

• Exit Conditions:

Take Profit: Price reaches defined percentage above/below entry

Stop Loss: Price reaches defined percentage below/above entry

• Position Control:

Limited to specified number of positions

Automatic position tracking

Clear visual indication of current trades

TECHNICAL DETAILS

• EMA Calculation:

Uses Exponential Moving Average for trend following

Color-coded based on 2-bar trend direction

Multiple timeframe compatibility

• Label System:

Clear buy/sell markers

Take Profit and Stop Loss indicators

Real-time position status updates

• Alert Configuration:

Customizable alert messages

Multiple alert conditions

Option to enable/disable specific alerts

LIMITATIONS

⚠️ Important Considerations:

Results may vary across different market conditions

Historical performance does not guarantee future results

Always backtest strategy before live trading

Consider complementing with additional analysis tools

BEST PRACTICES

• Recommended Timeframes:

Daily charts for long-term strategies

4-hour charts for swing trading

1-hour charts for short-term trading

• Risk Management Tips:

Start with small position sizes

Always use TP/SL in live trading

Monitor market volatility before entering trades

TROUBLESHOOTING

• Common Issues:

Ensure proper chart resolution

Verify alert conditions are enabled

Check for conflicting indicators

• Performance Optimization:

Use appropriate timeframe for your strategy

Adjust indicator parameters based on market conditions

Monitor for potential overfitting

SMT SwiftEdge PowerhouseSMT SwiftEdge Powerhouse: Precision Trading with Divergence, Liquidity Grabs, and OTE Zones

The SMT SwiftEdge Powerhouse is a powerful trading tool designed to help traders identify high-probability entry points during the most active market sessions—London and New York. By combining Smart Money Technique (SMT) Divergence, Liquidity Grabs, and Optimal Trade Entry (OTE) Zones, this script provides a unique and cohesive strategy for capturing market reversals with precision. Whether you're a scalper or a swing trader, this indicator offers clear visual signals to enhance your trading decisions on any timeframe.

What Does This Script Do?

This script integrates three key concepts to identify potential trading opportunities:

SMT Divergence:

SMT Divergence compares the price action of two correlated assets (e.g., Nasdaq and S&P 500 futures) to detect hidden market reversals. When one asset makes a higher high while the other makes a lower high (bearish divergence), or one makes a lower low while the other makes a higher low (bullish divergence), it signals a potential reversal. This technique leverages institutional "smart money" behavior to anticipate market shifts.

Liquidity Grabs:

Liquidity Grabs occur when price breaks above recent highs or below recent lows on higher timeframes (5m and 15m), often triggering stop-loss orders from retail traders. These breakouts are identified using pivot points and confirm institutional activity, setting the stage for a reversal. The script focuses on liquidity grabs during the London and New York sessions for maximum market activity.

Optimal Trade Entry (OTE) Zones:

OTE Zones are Fibonacci-based retracement areas (e.g., 61.8%) calculated after a liquidity grab. These zones highlight where price is likely to retrace before continuing in the direction of the reversal, offering a high-probability entry point. The script adjusts the width of these zones using the Average True Range (ATR) to adapt to market volatility.

By combining these components, the script identifies when institutional activity (liquidity grabs) aligns with market reversals (SMT divergence) and pinpoints precise entry points (OTE zones) during high-liquidity sessions.

Why Combine These Components?

The integration of SMT Divergence, Liquidity Grabs, and OTE Zones creates a robust trading system for several reasons:

Synergy of Institutional Signals: SMT Divergence and Liquidity Grabs both reflect "smart money" behavior—divergence shows hidden reversals, while liquidity grabs confirm institutional intent to trap retail traders. Together, they provide a strong foundation for identifying high-probability setups.

Session-Based Precision: Focusing on the London and New York sessions ensures signals occur during periods of high volatility and liquidity, increasing their reliability.

Precision Entries with OTE: After confirming a setup with divergence and liquidity grabs, OTE zones provide a clear entry area, reducing guesswork and improving trade accuracy.

Adaptability: The script works on any timeframe, with adjustable settings for signal sensitivity, session times, and Fibonacci levels, making it versatile for different trading styles.

This combination makes the script unique by aligning institutional insights with actionable entry points, tailored to the most active market hours.

How to Use the Script

Setup:

Add the script to your chart (works on any timeframe, e.g., 1m, 5m, 15m).

Configure the settings in the indicator's inputs:

Session Settings: Adjust the start/end times for London and New York sessions (default: London 8-11 UTC, New York 13-16 UTC). You can disable session restrictions if desired.

Asset Settings: Set the primary and secondary assets for SMT Divergence (default: NQ1! and ES1!). Ensure the assets are correlated.

Signal Settings: Adjust the lookback period, ATR period, and signal sensitivity (Low/Medium/High) to control the frequency of signals.

OTE Settings: Choose the Fibonacci level for OTE zones (default: 61.8%).

Visual Settings: Enable/disable OTE zones, SMT labels, and debug labels for troubleshooting.

Interpreting Signals:

Blue Circles: Indicate a liquidity grab (price breaking a 5m or 15m pivot high/low), marking the start of a potential setup.

Blue OTE Zones: Appear after a liquidity grab, showing the retracement area (e.g., 61.8% Fibonacci level) where price is likely to enter for a reversal trade. The label "OTE Trigger 5m/15m" confirms the direction (Short/Long) and session.

Green/Red Entry Boxes: Mark precise entry points when price enters the OTE zone and confirms the SMT Divergence. Green boxes indicate a long entry, red boxes a short entry.

Trading Example:

On a 1m chart, a blue circle appears when price breaks a 5m pivot high during the London session.

A blue OTE zone forms, showing a retracement area (e.g., 61.8% Fibonacci level) with the label "OTE Trigger 5m/15m (Short, London)".

Price retraces into the OTE zone, and a red "Short Entry" box appears, confirming a bearish SMT Divergence.

Enter a short trade at the red box, with a stop-loss above the OTE zone and a take-profit at the next support level.

Originality and Utility

The SMT SwiftEdge Powerhouse stands out by merging SMT Divergence, Liquidity Grabs, and OTE Zones into a single, session-focused indicator. Unlike traditional indicators that focus on one aspect of price action, this script combines institutional reversal signals with precise entry zones, tailored to the most active market hours. Its adaptability across timeframes, customizable settings, and clear visual cues make it a versatile tool for traders seeking to capitalize on smart money movements with confidence.

Tips for Best Results

Use on correlated assets like NQ1! (Nasdaq futures) and ES1! (S&P 500 futures) for accurate SMT Divergence.

Test on lower timeframes (1m, 5m) for scalping or higher timeframes (15m, 1H) for swing trading.

Adjust the "Signal Sensitivity" to "High" for more signals or "Low" for fewer, high-quality setups.

Enable "Show Debug Labels" if signals are not appearing as expected, to troubleshoot pivot points and liquidity grabs.

HL2 Moving Average with BandsThis indicator is designed to assist traders in identifying potential trade entries and exits for S&P 500 (ES) and Nasdaq-100 (NQ) futures. It calculates a Simple Moving Average (SMA) based on the HL2 value (average of high and low prices) of the current candle over a user-defined lookback period (default: 200 periods). The indicator plots this SMA as a blue line, providing a smoothed reference for price trends.

Additionally, it includes upper and lower bands calculated as a percentage (default: 0.5%) above and below the SMA, plotted as green and red lines, respectively. These bands act as dynamic thresholds to identify overbought or oversold conditions. The indicator generates trade signals based on price action relative to these bands:

Long Entry: A green upward triangle is plotted below the candle when the close crosses above the upper band, signaling a potential buy.

Close Long: A red square is plotted above the candle when the close crosses back below the upper band, indicating an exit for the long position.

Short Entry: A red downward triangle is plotted above the candle when the close crosses below the lower band, signaling a potential sell.

Close Short: A green square is plotted below the candle when the close crosses back above the lower band, indicating an exit for the short position.

The script is customizable, allowing users to adjust the SMA length and band percentage to suit their trading style or market conditions. It is plotted as an overlay on the price chart for easy integration with other technical analysis tools.

Recommended Time Frame and Settings for Trading S&P 500 and Nasdaq-100 Futures

Based on research and market dynamics for S&P 500 (ES) and Nasdaq-100 (NQ) futures, the 5-minute chart is recommended as the optimal time frame for day trading with this indicator. This time frame strikes a balance between capturing intraday trends and filtering out excessive noise, which is critical for futures trading due to their high volatility and leverage. The 5-minute chart aligns well with periods of high liquidity and volatility, such as the U.S. market open (9:30 AM–11:00 AM EST) and the afternoon session (2:00 PM–4:00 PM EST), when institutional traders are most active.

Why 5-minute? It allows traders to react to short-term price movements while avoiding the rapid fluctuations of 1-minute charts, which can be prone to false signals in choppy markets. It also provides enough data points to make the SMA and bands meaningful without the lag associated with longer time frames like 15-minute or hourly charts.

Recommended Settings

SMA Length: Set to 200 periods. This longer lookback period smooths the HL2 data, reducing noise and providing a reliable trend reference for the 5-minute chart. A 200-period SMA helps identify significant trend shifts without being overly sensitive to minor price fluctuations.

Band Percentage: 0.5% is more suitable for the volatility of ES and NQ futures on a 5-minute chart, as it generates fewer but higher-probability signals. Wider bands (e.g., 1%) may miss short-term opportunities, while narrower bands (e.g., 0.1%) may produce excessive false signals.

Trading Session Recommendations

Futures markets for ES and NQ are open nearly 24 hours (Sunday 6:00 PM EST to Friday 5:00 PM EST, with a daily break from 4:00 PM–5:00 PM EST), but not all hours are equally optimal due to varying liquidity and volatility. The best times to trade with this indicator are:

U.S. Market Open (9:30 AM–11:00 AM EST): This period is characterized by high volume and volatility, driven by the opening of U.S. equity markets and economic data releases (e.g., 8:30 AM EST reports like CPI or GDP). The indicator’s signals are more reliable during this window due to strong order flow and price momentum.

Afternoon Session (2:00 PM–4:00 PM EST): After the lunchtime lull, volume picks up as institutional traders return, and news or FOMC announcements often drive price action. The indicator can capture breakout moves as prices test the upper or lower bands.

Pre-Market (7:30 AM–9:30 AM EST): For traders comfortable with lower liquidity, this period can offer opportunities, especially around 8:30 AM EST economic releases. However, use tighter risk management due to wider spreads and potential volatility spikes.

Additional Tips

Avoid Low-Volume Periods: Steer clear of trading during low-liquidity hours, such as the overnight session (11:00 PM–3:00 AM EST), when spreads widen and price movements can be erratic, leading to false signals from the indicator.

Combine with Other Tools: Enhance the indicator’s effectiveness by pairing it with support/resistance levels, Fibonacci retracements, or volume analysis to confirm signals. For example, a long entry signal above the upper band is stronger if it coincides with a breakout above a key resistance level.

Risk Management: Given the leverage in futures (e.g., Micro E-mini contracts require ~$1,200 margin for ES), use tight stop-losses (e.g., below the lower band for longs or above the upper band for shorts) to manage risk. Aim for a risk-reward ratio of at least 1:2.

Test Settings: Backtest the indicator on a demo account to optimize the SMA length and band percentage for your specific trading style and risk tolerance. Micro E-mini contracts (MES for S&P 500, MNQ for Nasdaq-100) are ideal for testing due to their lower capital requirements.

Why These Settings and Time Frame?

The 5-minute chart with a 200-period SMA and 0.5% bands is tailored for the volatility and liquidity of ES and NQ futures during peak trading hours. The longer SMA period ensures the indicator captures meaningful trends, while the 0.5% bands are tight enough to signal actionable breakouts but wide enough to avoid excessive whipsaws. Trading during high-volume sessions maximizes the likelihood of valid signals, as institutional participation drives clearer price action.

By focusing on these settings and time frames, traders can leverage the indicator to capitalize on the dynamic price movements of S&P 500 and Nasdaq-100 futures while managing the inherent risks of these markets.

DEMA Trend Oscillator Strategy📌 Overview

The DEMA Trend Oscillator Strategy is a dynamic trend-following approach based on the Normalized DEMA Oscillator SD.

It adapts in real-time to market volatility with the goal of improving entry accuracy and optimizing risk management.

⚠️ This strategy is provided for educational and research purposes only.

Past performance does not guarantee future results.

🎯 Strategy Objectives

The main goal of this strategy is to respond quickly to sudden price movements and trend reversals,

by combining momentum-based signals with volatility filters.

It is designed to be user-friendly for traders of all experience levels.

✨ Key Features

Normalized DEMA Oscillator: A momentum indicator that normalizes DEMA values on a 0–100 scale, allowing intuitive identification of trend strength

Two-Bar Confirmation Filter: Requires two consecutive bullish or bearish candles to reduce noise and enhance entry reliability

ATR x2 Trailing Stop: In addition to fixed stop-loss levels, a trailing stop based on 2× ATR is used to maximize profits during strong trends

📊 Trading Rules

Long Entry:

Normalized DEMA > 55 (strong upward momentum)

Candle low is above the upper SD band

Two consecutive bullish candles appear

Short Entry:

Normalized DEMA < 45 (downward momentum)

Candle high is below the lower SD band

Two consecutive bearish candles appear

Exit Conditions:

Take-profit at a risk-reward ratio of 1.5

Stop-loss triggered if price breaks below (long) or above (short) the SD band

Trailing stop activated based on 2× ATR to secure and extend profits

💰 Risk Management Parameters

Symbol & Timeframe: Any (AUDUSD 5M example)

Account size (virtual): $3000

Commission: 0.4PIPS(0.0004)

Slippage: 2 pips

Risk per trade: 5%

Number of trades (backtest):534

All parameters can be adjusted based on broker specifications and individual trading profiles.

⚙️ Trading Parameters & Considerations

Indicator: Normalized DEMA Oscillator SD

Parameter settings:

DEMA Period (len_dema): 40

Base Length: 20

Long Threshold: 55

Short Threshold: 45

Risk-Reward Ratio: 1.5

ATR Multiplier for Trailing Stop: 2.0

🖼 Visual Support

The chart displays the following visual elements:

Upper and lower SD bands (±2 standard deviations)

Entry signals shown as directional arrows

🔧 Strategy Improvements & Uniqueness

This strategy is inspired by “Normalized DEMA Oscillator SD” by QuantEdgeB,

but introduces enhancements such as a two-bar confirmation filter and an ATR-based trailing stop.

Compared to conventional trend-following strategies, it offers superior noise filtering and profit optimization.

✅ Summary

The DEMA Trend Oscillator Strategy is a responsive and practical trend-following method

that combines momentum detection with adaptive risk management.

Its visual clarity and logical structure make it a powerful and repeatable tool

for traders seeking consistent performance in trending markets.

⚠️ Always apply appropriate risk management. This strategy is based on historical data and does not guarantee future results.

Pivot Levels with EMA Trend📌 Trend Change Levels with EMA Trend

✨ Description:

This TradingView script identifies clean trend change levels based on 1-hour structure shifts and filters them to keep only those not invalidated. It follows the "Jake Ricci" method, each level is printed at the beginning of the candle that changes the trend, on a 1 hour chart. For precision, make sure to exclude after/pre market and only use the levels on regular hours charts.

It includes dynamic EMAs (9, 50, 200), intraday VWAP, the daily open level printed, and a visual trend label based on EMA(9) slope.

Designed for intermediate traders, it helps build bias, manage entries, and avoid false setups by focusing on clean, reactive levels that the market respects.

🔧 Core Logic:

On the 1H chart, the script compares current and previous closes to detect trend direction. If the trend flips (e.g., up to down), the open of the candle that caused the flip becomes a candidate level.

Only levels that remain untouched by future candle closes are plotted — this filters out “weak” levels that price already violated (which means, a candle closes after passing through the level).

These levels become key S/R zones and often act as reaction points during pullbacks, traps, and liquidity sweeps.

The idea is to check how the price reacts to those levels. Usually there's a clean retest of the level. After that, if the price continues in that direction, it tends to reach the following level.

🔹 Included Tools:

🟣 Trend Change Levels (1H):

Fixed horizontal lines based on confirmed shifts in trend, shown only when not broken.

📉 EMAs (9 / 50 / 200):

Visibility can be set per timeframe. Use for trend context.

📍 EMA Trend Label:

Shows \"UP\", \"DOWN\", or \"RANGE\" based on EMA(9) slope.

🔵 VWAP (Intraday Reset):

Real-time volume-weighted average price that resets daily. Useful for fair value zones and reversion plays.

🟠 Daily Open Line:

Plot of the current day’s open. Used for intraday directional bias. Usually: DO NOT take longs below the Open Print, DO NOT take shorts above it.

📊 ATR Table:

Displays current ATR multiplier on the chart. It's useful to understand if the market is expanding or not.

📈 How to Use It (Strategy):

1. Start on the 1H chart to generate levels.

Only the open of candles that reversed trend are considered — and only if future candles didn’t close through them. I suggest manually adding horizontal lines to mark again the levels, so that they stick to all the timeframes.

2. Use the trend label to decide your bias — \"UP\" for long setups, \"DOWN\" for shorts. Avoid trading against the slope.

3. Switch to the 5m chart and wait for price to approach a plotted level. These are often used for manipulation, retests, or clean reversals.

4. Look for confirmation: rejection candles, break-and-retest, strong engulfing candles, or traps above/below the level. ALWAYS check the price action around the level, along with the volume.

5. Check if VWAP or an EMA is near the level. If yes, the confluence strengthens the trade idea.

6. Use the ATR value to understand if the market is expanding (candles are bigger than the ATR). You don't want to stay in a slow and ranging trade.

✅ Example Entry Flow:

1. On the 1H chart, note a trend change level printed recently.

2. Check the current trend label — if it says \"UP,\" prefer longs.

3. Wait for price to retrace toward the level.

4. On the 5m, look for a bullish engulfing candle or trap setup at the level.

5. Check if VWAP and EMA(50) are near. If yes, execute the trade.

6. Set stop just under the low of the candle prior to your entry. Ideally, a retracing candle.

To be clear: imaging to be LONG, you wait for a retracement that should touch your level. You wait for a candle that resumes the LONG trend, enter when it breaks the high of the previous candle (sill in retracement), you place your stop under the candle prior to your entry.

Notes:

No repainting — levels only show up after confirmed shifts.

Removes broken levels for chart clarity and reliability.

Helps spot high-probability pullback zones and fakeouts.

Perfect confluence tool to support price action, SMC, or EMA strategies.

Works across multiple timeframes with customizable inputs.

👤 Ideal For:

Intraday traders looking for reactive entry points and direction confirmation.

Swing traders wanting to pinpoint continuation zones or reversal pivots.

🚨 Final Note: This indicator doesn’t generate buy/sell signals. It improves your trade filtering by identifying areas the market already respected and reacting to them with price action. Combine it with your own system , test it in replay, and use screenshots to document setups.

📌 If used with discipline, this becomes a precision tool — not a signal generator.

Daily Bollinger Band StrategyOverview of the Daily Bollinger Band Strategy

1. Strategy Overview and Features

This strategy is a tool for backtesting a trading method that uses Bollinger Bands. It is *not* a tool for automated trading.

1-1. Main Display Items

The main chart displays the Bollinger Bands and the 200-day moving average.

It also shows the entry and exit points along with the position size (in units of 100 shares).

1-2. Summary of Trading Rules

For long (buy) strategies, the trade enters when the price crosses above the +1σ line of the Bollinger Bands, aiming to ride an upward trend. The position is exited when the price crosses below the middle band.

For short (sell) strategies, the trade enters when the price crosses below the -1σ line of the Bollinger Bands, aiming to ride a downward trend. The position is exited when the price crosses above the middle band.

1-3. Strategic Enhancements

The strategy uses the slope of the 200-day moving average to determine the trend direction and enter trades accordingly. This improves the win rate and payoff ratio.

Additionally, to reduce the probability of ruin, the risk per trade is limited to 1.0% of capital, and position sizing is adjusted using ATR (a volatility indicator).

2. Trading Rules

2-1. Chart Type

Only daily charts are used.

2-2. Indicators Used

(1) Bollinger Bands** (used for entry and exit signals)

- Period: Fixed at 80 days

- Upper and lower bands: Fixed at ±1σ

(2) Moving Average** (used to determine trend direction)

- Period: Fixed at 200 days

- Trend direction is judged based on whether the difference from the previous day is positive (upward) or negative (downward)

2-3. Buy Rules

Setup:

- Price crosses above the +1σ line from below

- Both the middle band and 200-day moving average are upward sloping

Entry:

- Buy at the next day’s market open using a market order

Exit:

- If the price crosses below the middle band, sell at the next day’s open using a market order

2-4. Sell Rules

Setup:

- Price crosses below the -1σ line from above

- Both the middle band and 200-day moving average are downward sloping

Entry:

- Sell at the next day’s market open using a market order

Exit:

- If the price crosses above the middle band, buy back at the next day’s open using a market order

2-5. Risk Management Rules

- Risk per trade: 1.0% of total capital (acceptable loss = capital × 1.0%)

- Position size: Acceptable loss ÷ 2ATR (rounded down to the nearest unit of 100 shares)

2-6. Other Notes

- No brokerage fees

- No pyramiding

- No partial exits

- No reverse positions (no “stop-and-reverse” trades)

3. Strategy Parameters

The following settings can be specified:

3-1. Period Settings

- Start date: Set the start date for the backtest period

- Stop date: Set the end date for the backtest period

3-2. Display of Trend and Signals

- Show trend: When checked, the background color of the bars is light red for an uptrend and light blue for a downtrend

- Show signal: When checked, entry and exit signals are displayed (note: signals are executed at the next day’s open, so there is a one-day lag in the display)

3-3. Capital Management Settings

- Funds: Capital available for trading (in JPY)

- Risk rate: Specify what percentage of the capital to risk per trade

Settings in the “Properties” tab are not used in this strategy.

4. Backtest Results (Example)

Here are the backtest results conducted by the author:

- Target Stocks: All components of the Nikkei 225

- Test Period: January 4, 2000 – December 30, 2024

- Data Points: 12,886

- Win Rate: 33.45%

- Net Profit: ¥82,132,380

- Payoff Ratio: 2.450

- Expected Value: ¥6,373.8

- Risk Rate: 1.0%

- Probability of Ruin: 0.00%

---

デイリー・ボリンジャーバンド・ストラテジーの概要

1. ストラテジーの概要と特徴

このストラテジーは、ボリンジャーバンドを使ったトレード手法のバックテストを行うツールです。自動売買を行うツールではありません。

1-1. 主な表示項目

メインチャートにボリンジャーバンドと 200日移動平均線を表示します。

また、エントリーと手仕舞いのタイミングと数量(100株単位)も表示されます。

1-2. トレードルールの概要

買い戦略の場合、ボリンジャーバンドの +1σ 超えでエントリーして上昇トレンドに乗り、ミドルバンドを割ったら決済します。

売り戦略の場合、ボリンジャーバンドの -1σ 割りでエントリーして下降トレンドに乗り、ミドルバンドを上抜けたら決済します。

1-3. ストラテジーの工夫点

200日移動平均線の傾きを見てトレンド方向にエントリーをしています。こうして勝率とペイオフレシオの成績を向上しています。

また、破産確率を抑えるために、リスク資金比率を 1.0% にして、ATR(ボラティリティ指標) を使って注文数を調整しています。

2. 売買ルール

2-1. 使用するチャート

日足チャートに限定します

2-2. 使用する指標

(1) ボリンジャーバンド(仕掛けと手仕舞いのシグナルに使用)

期間は80日に固定

上下バンドは ±1σ に固定

(2) 移動平均線(トレンドの方向を見るために使用)

期間は200日に固定

移動平均の値の前日との差がプラスのとき上向き、マイナスのとき下向きと判断

2-3. 買いのルール

セットアップ:ボリンジャーバンドの +1σ を価格が下から上に交差 かつ ミドルバンドと 200日移動平均線が上向き

仕掛け:翌日の寄り付きに成行で買う

手仕舞い:ボリンジャーバンドのミドルバンドを価格が上から下に交差したら、翌日の寄り付きに成行で売る

2-4. 売りのルール

セットアップ:ボリンジャーバンドの -1σ を価格が上から下に交差 かつ ミドルバンドと 200日移動平均線が下向き

仕掛け:翌日の寄り付きに成行で売る

手仕舞い:ボリンジャーバンドのミドルバンドを価格が下から上に交差したら、翌日の寄り付きに成行で買い戻す

2-5. 資金管理のルール

リスク資金比率:資産の 1.0%(許容損失 = 資産 × 1.0%)

注文数:許容損失 ÷ 2ATR(単元株数未満は切り捨て)

2-6. その他

仲介手数料:なし

ピラミッディング:なし

分割決済:なし

ドテン:しない

3. ストラテジーのパラメーター

次の項目が指定できます。

3-1. 期間の設定

Staer date : バックテストの検証期間の開始日を指定します

Stop date : バックテストの検証期間の終了日を指定します

3-2. トレンドとシグナルの表示

Show trend : チェックを入れると、バーの背景色が、トレンドが上昇のときは薄い赤で、下落のときは薄い青で表示されます

Show signal : チェックを入れると、エントリーと手仕舞いのシグナルを表示します(シグナルの出た翌日の寄り付きに売買をするので表示に1日のずれがあります)

3-3. 資金管理用の設定

Funds : トレード用の資金(円)

Risk rate : 許容損失を資金の何%にするかで指定します

「プロパティタブ」で設定する値は、このストラテジーでは有効ではありません。

4. バックテストの結果(例)

作者がバックテストを実施した結果をお知らせします。

対象銘柄:日経225構成銘柄すべて

対象期間:2000年1月4日~2024年12月30日

データ件数:12,886

勝率:33.45%

純利益:82,132,380

ペイオフレシオ:2.450

期待値:6,373.8

リスク資金比率:1.0%

破産確率:0.00%

DM Support / Resistance (USA Session)This indicator is specifically designed for use on the 4-hour time frame and helps traders identify key support and resistance levels during the USA trading session (9:30 AM to 4:00 PM Eastern Time). The indicator calculates important price levels to assist in making well-informed entry and exit decisions, particularly for those focusing on swing trades or longer-term intraday strategies. It also includes a feature to skip setups when relevant fundamental news is scheduled, ensuring you avoid trading during periods of high volatility.

Key Features:

Support and Resistance Levels (S1 & R1):

The indicator calculates and displays Support 1 (S1) and Resistance 1 (R1) levels, which act as key barriers for price action and help traders spot potential reversal or breakout zones on the chart.

Pivot Point (PP):

The Pivot Point (PP) is calculated as the average of the previous period's high, low, and close. It serves as a central reference point for market direction, allowing traders to evaluate whether the market is in a bullish or bearish trend.

Market Bias:

The Bias is shown as a histogram that helps traders assess the strength of the market trend. A positive bias suggests bullish sentiment, while a negative bias signals bearish conditions. This can be used to confirm the overall trend direction.

4-Hour Time Frame:

The indicator is optimized for the 4-hour time frame, making it suitable for traders looking for swing trades or those who wish to capture longer-term trends within the USA session. The key support, resistance, and pivot levels are recalculated dynamically to reflect price action over 4-hour periods.

Dynamic Plotting and Alerts:

Support and resistance levels are drawn as dashed horizontal lines, updating in real-time to reflect the most current market data during the USA session. Alerts can be set for significant price movements crossing these levels.

Stop-Loss Strategy Based on 15-Minute Time Frame:

A unique feature of this indicator is its stop-loss strategy, which uses 15-minute time frame support and resistance levels. When a long or short entry is triggered on the 4-hour chart, traders should place their stop-loss according to the relevant 15-minute support or resistance level.

If the price closes above the 15-minute support for a long entry, or closes below the 15-minute resistance for a short entry, it signals the need to exit or adjust your position based on these levels.

Fundamental News Filter:

To avoid unnecessary risk, the indicator incorporates a fundamental news filter. If there is relevant news scheduled during the USA session, such as high-impact economic data or central bank announcements, the indicator will skip the setup for that period. This prevents traders from entering positions during times of elevated volatility caused by news events, which could result in unpredictable price movements.

How to Use:

Long Entry: When the Bias is positive and the price breaks above Support 1 (S1), this signals a potential bullish move. Consider entering a long position at this point.

Stop-Loss Strategy: Set your stop-loss at the respective 15-minute support level. If the price closes below this level, it could signal a reversal, prompting you to exit the trade.

Short Entry: When the Bias is negative and the price breaks below Resistance 1 (R1), this signals a potential bearish move. Enter a short position at this point.

Stop-Loss Strategy: Set your stop-loss at the respective 15-minute resistance level. If the price closes above this level, exit the short trade as it could indicate a bullish reversal.

Pivot Point (PP): The Pivot Point serves as a reference level to gauge potential price reversals. A move above the PP suggests a bullish bias, while trading below the PP suggests a bearish outlook.

Bias Histogram: The Bias Histogram helps confirm trend direction. A positive bias confirms long positions, while a negative bias reinforces short trades.

Avoid Trading During High-Impact News: If there is significant economic news or fundamental events scheduled during the USA session, the indicator will automatically skip any potential setup. This feature ensures you avoid entering trades that might be affected by unexpected news-driven volatility, keeping your trading strategy safer and more reliable.

Why Use This Indicator:

The 4-hour time frame is ideal for traders who prefer swing trading or those looking to capture longer-term trends in a structured manner. This indicator provides crucial insights into market direction, support/resistance levels, and potential entry/exit points.

The stop-loss management based on the 15-minute support and resistance levels helps traders protect their positions from sudden price reversals, ensuring more precise risk management.

The fundamental news filter is particularly useful for avoidance of high-risk periods. By skipping setups during high-impact news events, traders can avoid entering trades when price volatility could be unpredictable.

Overall, this indicator is a powerful tool for traders who want to make data-driven decisions based on technical analysis while ensuring that their positions are managed responsibly and avoiding news-driven risk.

Scalping 15min: EMA + MACD + RSI + ATR-based SL/TP📈 Strategy: 15-Minute Scalping — EMA + MACD + RSI + ATR-based SL/TP

This scalping strategy is designed for 15-minute charts and combines trend-following and momentum confirmation with dynamic stop loss and take profit levels based on volatility.

🔧 Indicators Used:

EMA 50 — identifies the main trend

MACD Histogram — confirms momentum direction

RSI (14) — filters overbought/oversold conditions

ATR (14) — dynamically sets SL and TP based on market volatility

📊 Entry Conditions:

Long Entry:

Price is above EMA 50

MACD histogram is positive

RSI is above 50 but below 70

Short Entry:

Price is below EMA 50

MACD histogram is negative

RSI is below 50 but above 30

🛑 Risk Management:

Stop Loss: 1×ATR (user-configurable)

Take Profit: 2×ATR (user-configurable)

These values can be adjusted in the script inputs depending on your risk/reward preference or market conditions.

⚠️ Notes:

Strategy is optimized for scalping fast-moving pairs (e.g. crypto, forex).

Works best in trending markets.

Use backtesting and forward testing before live trading.

TrendSync Pro (SMC)📊 TrendSync Pro (SMC) – Advanced Trend-Following Strategy with HTF Alignment

Created by Shubham Singh

🔍 Strategy Overview

TrendSync Pro (SMC) is a precision-based smart trend-following strategy inspired by Smart Money Concepts (SMC). It combines: Real-time pivot-based trendline detection

Higher Time Frame (HTF) filtering to align trades with dominant trend

Risk management via adjustable Stop Loss (SL) and Take Profit (TP)

Directional control — trade only bullish, bearish, or both setups

Realistic backtesting using commissions and slippage

Pre-optimized profiles for scalpers, intraday, swing, and long-term traders

🧠 How It Works:

🔧 Strategy Settings Image:

beeimg.com

The strategy dynamically identifies trend direction by using swing high/low pivots. When a new pivot forms: It draws a trendline from the last significant pivot

Detects whether the trend is up (based on pivot lows) or down (based on pivot highs)

Waits for price to break above/below the trendline

Confirms with HTF price direction (HTF close > previous HTF close = bullish)

Only then it triggers a long or short trade

It exits either at TP, SL, or a manual trendline break

🛠️ Adjustable Parameters:

Trend Period: Length for pivot detection (affects sensitivity of trendlines)

HTF Timeframe: Aligns lower timeframe entries with higher timeframe direction

SL% and TP%: Customize your risk-reward profile

Commission & Slippage: Make backtests more realistic

Trade Direction: Choose to trade: Long only, Short only, or Both

🎛️ Trade Direction Control:

In settings, you can choose: Bullish Only: Executes only long entries

Bearish Only: Executes only short entries

Both: Executes both long and short entries when conditions are met

This allows you to align trades with your own market bias or external analysis.

📈 Entry Logic: Long Entry:

• Price crosses above trendline

• HTF is bullish (HTF close > previous close)

• Latest pivot is a low (trend is considered up)

Short Entry:

• Price crosses below trendline

• HTF is bearish (HTF close < previous close)

• Latest pivot is a high (trend is considered down)

📉 Exit Logic: Hit Take Profit or Stop Loss

Manual trendline invalidation: If price crosses opposite of the trend direction

⏰ Best Timeframes & Recommended Settings:

Scalping (1m to 5m):

HTF = 15m | Trend Period = 7

SL = 0.5% | TP = 1% to 2%

Intraday (15m to 30m):

HTF = 1H | Trend Period = 10–14

SL = 0.75% | TP = 2% to 3%

6 Hour Trading (30m to 1H):

HTF = 4H | Trend Period = 20

SL = 1% | TP = 4% to 6%

Swing Trading (4H to 1D):

HTF = 1D | Trend Period = 35

SL = 2% | TP = 8% to 12%

Long-Term Investing (1D+):

HTF = 1W | Trend Period = 50

SL = 3% | TP = 15%+

Note: These are recommended base settings. Adjust based on volatility, asset class, or personal trading style.

📸 Testing Note:

beeimg.com

TradingView limits test length to 20k bars (~40 trades on smaller timeframes). To show long-term results: Test on higher timeframes (e.g., 1H, 4H, 1D)

Share images of backtest result in description

Host longer test result screenshots on Imgur or any public drive

📍 Asset Behavior Insight:

This strategy works on multiple assets, including BTC, ETH, etc.

Performance varies by trend strength:

Sometimes BTC performs better than ETH

Other times ETH gives better results

That’s normal as both assets follow different volatility and trend behavior

It’s a trend-following setup. Longer and clearer the trend → better the results.

✅ Best Practices: Avoid ranging markets

Use proper SL/TP for each timeframe

Use directional filter if you already have a directional bias

Always forward test before going live

⚠️ Trading Disclaimer:

This script is for educational and backtesting purposes only. Trading involves risk. Always use risk management and never invest more than you can afford to lose.

Smart Grid Scalping (Pullback) Strategy[BullByte]The Smart Grid Scalping (Pullback) Strategy is a high-frequency trading strategy designed for short-term traders who seek to capitalize on market pullbacks. This strategy utilizes a dynamic ATR-based grid system to define optimal entry points, ensuring precise trade execution. It integrates volatility filtering and an RSI-based confirmation mechanism to enhance signal accuracy and reduce false entries.

This strategy is specifically optimized for scalping by dynamically adjusting trade levels based on current market conditions. The grid-based system helps capture retracement opportunities while maintaining strict trade management through predefined profit targets and trailing stop-loss mechanisms.

Key Features :

1. ATR-Based Grid System :

- Uses a 10-period ATR to dynamically calculate grid levels for entry points.

- Prevents chasing trades by ensuring price has reached key levels before executing entries.

2. No Trade Zone Protection :

- Avoids low-volatility zones where price action is indecisive.

- Ensures only high-momentum trades are executed to improve success rate.

3. RSI-Based Entry Confirmation :

- Long trades are triggered when RSI is below 30 (oversold) and price is in the lower grid zone.

- Short trades are triggered when RSI is above 70 (overbought) and price is in the upper grid zone.

4. Automated Trade Execution :

- Long Entry: Triggered when price drops below the first grid level with sufficient volatility.

- Short Entry: Triggered when price exceeds the highest grid level with sufficient volatility.

5. Take Profit & Trailing Stop :

- Profit target set at a customizable percentage (default 0.2%).

- Adaptive trailing stop mechanism using ATR to lock in profits while minimizing premature exits.

6. Visual Trade Annotations :

- Clearly labeled "LONG" and "SHORT" markers appear at trade entries for better visualization.

- Grid levels are plotted dynamically to aid decision-making.

Strategy Logic :