PT FinderThis is mostly helpful to find potential price targets for Daytrades on the daily chart (if stronger resistances / supports are too far away).

Shows highs / lows of nearby "pivot" candles (higher high / lower low than both candles around) - depending on expected trade direction. Based on my experience these can be potential (albeit weak) resistance / support.

If it shows values only in the wrong trade direction: set a checkmark at "Invert bullish / bearish price targets" in the indicator settings

Also shows the ADR (blue line = yesterday's close MINUS Average Day Range) - which is helpful for Daytrades to see what price movement you could potentially expect for the day!

As a nice bonus it also shows gaps as yellow areas - in case you maybe missed them because you zoomed in / out too much on your daily chart.

More infos: www.reddit.com

Search in scripts for "gaps"

Smart Money Footprint & Cost Basis Engine [AlgoPoint]Smart Money Footprint & Cost Basis Engine

This indicator is a comprehensive market analysis tool designed to identify the "footprints" of Smart Money (institutions, whales) and pinpoint high-probability reaction zones. Instead of relying on lagging averages, this engine analyzes the very structure of the market to find where large players have shown their hand.

How It Works: The Core Logic

The indicator operates on a multi-stage confirmation process to identify and validate Smart Money zones:

Smart Money Detection (The Trigger): The engine first scans the chart for signs of intense, urgent buying or selling. It does this by identifying Fair Value Gaps (FVGs) created by large, high-volume Displacement Candles. This is our initial Point of Interest (POI).

Cost Basis Calculation (The Average Price): Once a potential Smart Money move is detected, the indicator calculates the Volume-Weighted Average Price (VWAP) for that specific move. This gives us a highly accurate estimate of the average price at which the large players entered their positions.

Historical Confirmation (The "Memory"): This is the indicator's most unique feature. It checks its historical database to see if a similar Smart Money move (in the same direction) has occurred in the same price area in the past. If a match is found, the zone's significance is confirmed.

Verified Cost Basis Zone (The Final Output): A zone that passes all the above checks is drawn on the chart as a high-probability Verified Cost Basis Zone. These are the "memory zones" where the market is likely to react upon a re-visit.

How to Use This Indicator

Cost Basis Zones (The Boxes):

Green Boxes: Bullish zones where Smart Money likely accumulated positions. When the price returns here, a BUY reaction is expected.

Red Boxes: Bearish zones where Smart Money likely distributed positions. When the price returns here, a SELL reaction is expected.

Zone Strength (★★★): Each zone is created with a star rating. More stars indicate a higher-confidence zone (based on factors like volume intensity and historical confirmation).

BUY/SELL Signals: A signal is only generated when the price enters a zone AND the confirmation filters (if enabled in the settings) are passed.

Zone Statuses:

Green/Red: Active and waiting to be tested.

Gray: The zone has been tested, and a signal was produced.

Dark Gray (Invalidated): The zone was broken decisively and is no longer considered valid support/resistance.

Key Settings

Signal Accuracy Filters: You can enable/disable three powerful filters to balance signal quantity and quality:

Momentum Confirmation (Stoch): Waits for momentum to align with the zone's direction.

Candlestick Confirmation (Engulfing): Waits for a strong reversal candle inside the zone.

Lower Timeframe MSS Confirmation: The most advanced filter; waits for a trend shift on a lower timeframe before giving a signal.

Historical Confirmation:

Require Historical Confirmation: Toggle the "Memory" feature on/off. Turn it off to see all potential SM zones.

Tolerance Calculation Method: Choose between a dynamic ATR Multiplier (recommended for all-around use) or a fixed Percentage to define the zone size.

Smart PA Early Entry - Trend StartSmart PA Early Entry Indicator (MACD + FVG + Fibonacci)

This TradingView indicator helps traders spot potential trend reversals early by combining multiple technical tools:

MACD Momentum – Identifies the direction of the trend.

Volume Filter – Confirms strong market participation for reliable signals.

Fair Value Gaps (FVG) – Highlights areas where price may reverse or continue strongly.

Fibonacci Retracement Levels – Pinpoints key support/resistance zones for early entries.

ATR-based Stop Loss – Automatically calculates a dynamic stop-loss based on market volatility.

Trend Start Signals – Alerts only appear on the first candle of a potential trend change to avoid repeated signals.

Visual Labels & Plots – Shows entry price, stop-loss, FVG zones, and Fibonacci levels for easy chart reading.

Ideal for: Intraday and swing traders looking for high-probability entries near trend reversals with clear risk management.

Cnagda Liquidit Trading SystemCnagda Liquidit Trading System helps spot where price is likely to trap traders and reverse, then gives simple, actionable Level to entry, place SL, and take profits with confidence. It blends imbalance zones, trend bias, order blocks, liquidity pools, high-probability fake Signal, and context-aware candle patterns into one clean workflow.

🟩🟥 Imbalance boxes: “Crowd rushed, gaps left”

What it is: Green/red boxes mark fast, one-sided moves where price “skipped” orders—think FVG-like zones that often get revisited.

Why it helps: Price frequently pulls back to “fill” these zones, creating clean retest entries with logical stops.

⏩How to use:

Green box = potential demand retest; Red box = potential supply retest. Enter on pullback into box, not on first impulse. Put stop on far side of box and aim first targets at recent swing points.

↕️ Swing bias (HH/HL vs LH/LL): “Which way is the road?”

What it is: Higher-highs/higher-lows = up-bias; Lower-highs/lower-lows = down-bias. system plots Buy/Sell OB levels aligned with that bias.

Why it helps: Trading with the broader flow reduces “hero trades” against institutions. Bias gives clearer entries and cleaner drawdowns.

⏩How to use:

Up-bias: look for long on Buy OB retests. Down-bias: look for short on Sell OB retests. Wait for a small rejection/engulfing to confirm before triggering.

🧱Order blocks: “Where big players remember”

What it is: last opposite-colored candle before an impulsive move—these zones often hold memory and reaction. system plots these as Buy/Sell OB lines.

Why it helps: Many breakouts pull back to the origin. Good entries often happen on retest, not on the breakout chase.

⏩ How to use:

Let price return into the OB, show wick rejection, and decent volume. Enter with stop beyond OB; define risk-reward before entry.

📊Volume coloring: “How Volume is move?”

What it is: Bar color reflects relative volume; inside bars are black. The dashboard also shows Volume and “Volume vs Prev.”

Why it helps: Patterns without volume often fade; volume validates strength and intent of moves.

⏩ How to use:

Favor entries where imbalance/OB/liquidity-grab coincide with higher volume. If volume is weak, reduce size or skip.

🧲 BSL/SSL liquidity pools: “Fishing for stops”

What it is: Equal highs cluster stops above (BSL); equal lows cluster stops below (SSL). system plots these and highlights the nearest one (“magnet”).

Why it helps: Price often sweeps these pools to trigger stops before reversing. This is a prime trap-reversal location.

⏩ How to use:

Watch nearest BSL/SSL. If price wicks through and closes back inside, anticipate a reversal. Trade reaction, not first poke. When price closes beyond, consider that pool mitigated and move on.

🟢🔴 Advanced liquidity grab: “Catch fakeout”

What it is: Bullish grab = makes a new low beyond a prior low but closes back above it, with a long lower wick, small body, and higher volume. Bearish is mirror. Labeled automatically.

Why it helps: It exposes trap moves (stop hunts) and often precedes true direction.

⏩ How to use:

Best when it aligns with a nearby imbalance/OB and supportive volume. Enter on reversal candle break or on retest. Stop goes beyond sweep wick.

🧠 Smart candlestick patterns (only in right place)

What it is: Engulfing, Hammer, Shooting Star, Hanging Man, Doji (with high volume), Morning/Evening Star, Piercing—but marked “effective” only if context (swing/trend/location) agrees.

Why it helps: same pattern in the wrong place is noise; in the right place, it’s signal.

⏩ How to use:

Location first (BSL/SSL/OB/imbalance), then pattern. Treat pattern as trigger/confirmation—one fresh label shows to keep chart clean.

🧭 Dashboard: “Context in a glance”

⏩ Reversal Level: current swing anchor—expect turns or reactions nearby; great for alerts and planning.

⏩ Volume vs Prev + Volume: Strength meter for signal candle—higher adds conviction.

⏩ Nearest Pool: next “magnet” area—look for sweeps/rejections there.

🧩Step-by-step trading flow (with mindset)

⏩ Set bias: HH/HL = long bias, LH/LL = short bias. Counter-trend only on clean sweeps with strong confirmation.

⏩ Find magnet: Check Nearest Pool (BSL/SSL). Focus attention there; it saves screen time.

⏩ Wait for event: Look for a sweep/grab label, or sharp rejection at pool/OB/imbalance. Avoid FOMO.

⏩ Add confluence: Stack 2–3 of these—imbalance box, OB, contextual pattern, supportive volume.

⏩Plan entry: Bullish: trigger above reversal candle high or take retest of FVG/OB. Stop below sweep wick/zone. Target at least 1:1.5–1:2.

Bearish: mirror above.

⏩Manage smartly: Take partials, move to breakeven or trail thoughtfully. Don’t drag stops inside zone out of emotion.

🎛️ Parameter tuning (to reduce human error)

⏩ swingLen: Smaller = faster but noisier; larger = cleaner but slower. Backtest first, then go live.

⏩ Tolerance (ATR or percent): ATR tolerance adapts to volatility (good for fast markets and lower TFs). Start around 0.15–0.30. In calm markets, try percent 0.05–0.15%.

⏩ minBarsGap: Start with 3–5 so equal highs/lows are truly equal—reduces false pools.

❌Common mistakes → ✅ Better habits

⏩Chasing every breakout → Wait for sweep/rejection, then confirm.

⏩Ignoring volume → Validate strength; cut size or skip on weak volume.

⏩Losing history of pools → If reviewing/backtesting, keep mitigated pools visible (dashed/faded).

⏩Over-tight tolerance/too small swingLen → Increases false signals; backtest to find balance.

📝 checklist (before entry)

⏩ Is there a nearby BSL/SSL and did a sweep/grab happen there?

⏩ Is there a close imbalance/OB that price can retest?

⏩ Do we have an effective pattern plus supportive volume?

⏩Is the stop beyond the wick/zone and RR ≥ 1:1.5?

•?((¯°·._.• 🎀 𝐻𝒶𝓅𝓅𝓎 𝒯𝓇𝒶𝒹𝒾𝓃𝑔 🎀 •._.·°¯((?•

Goldbach Time Indicator🔧 Key Fixes Applied:

1. Time Validation & Bounds Checking:

Hour/Minute Bounds: Ensures hours stay 0-23, minutes stay 0-59

Edge Case Handling: Prevents invalid time calculations from causing missing data

UTC Conversion Safety: Better handling of timezone edge cases

2. Enhanced Value Validation:

NA Checking: Validates all calculated values before using them

Goldbach Detection: Only flags valid, non-NA values as Goldbach hits

Plot Safety: Prevents plotting invalid or NA values that could cause gaps

3. Improved Plot Logic:

Core Level Colors: Blue for core levels (29,35,71,77), yellow/lime/orange for regular hits

Debug Mode Enhanced: Shows all calculations with gray dots when enabled

Better Filtering: Only plots positive, valid values for minus calculations

4. Background vs Dots Issue:

The large green/blue background you see suggests the indicator is detecting Goldbach times correctly, but the dots weren't plotting due to validation issues. This should now be fixed.

HorizonSigma Pro [CHE]HorizonSigma Pro

Disclaimer

Not every timeframe will yield good results . Very short charts are dominated by microstructure noise, spreads, and slippage; signals can flip and the tradable edge shrinks after costs. Very high timeframes adapt more slowly, provide fewer samples, and can lag regime shifts. When you change timeframe, you also change the ratios between horizon, lookbacks, and correlation windows—what works on M5 won’t automatically hold on H1 or D1. Liquidity, session effects (overnight gaps, news bursts), and volatility do not scale linearly with time. Always validate per symbol and timeframe, then retune horizon, z-length, correlation window, and either the neutral band or the z-threshold. On fast charts, “components” mode adapts quicker; on slower charts, “super” reduces noise. Keep prior-shift and calibration enabled, monitor Hit Rate with its confidence interval and the Brier score, and execute only on confirmed (closed-bar) values.

For example, what do “UP 61%” and “DOWN 21%” mean?

“UP 61%” is the model’s estimated probability that the close will be higher after your selected horizon—directional probability, not a price target or profit guarantee. “DOWN 21%” still reports the probability of up; here it’s 21%, which implies 79% for down (a short bias). The label switches to “DOWN” because the probability falls below your short threshold. With a neutral-band policy, for example ±7%, signals are: Long above 57%, Short below 43%, Neutral in between. In z-score mode, fixed z-cutoffs drive the call instead of percentages. The arrow length on the chart is an ATR-scaled projection to visualize reach; treat it as guidance, not a promise.

Part 1 — Scientific description

Objective.

The indicator estimates the probability that price will be higher after a user-defined horizon (a chosen number of bars) and emits long, short, or neutral decisions under explicit thresholds. It combines multi‑feature, z‑normalized inputs, adaptive correlation‑based weighting, a prior‑shifted sigmoid mapping, optional rolling probability calibration, and repaint‑safe confirmation. It also visualizes an ATR‑scaled forward projection and prints a compact statistics panel.

Data and labeling.

For each bar, the target label is whether price increased over the past chosen horizon. Learning is deliberately backward‑looking to avoid look‑ahead: features are associated with outcomes that are only known after that horizon has elapsed.

Feature engineering.

The feature set includes momentum, RSI, stochastic %K, MACD histogram slope, a normalized EMA(20/50) trend spread, ATR as a share of price, Bollinger Band width, and volume normalized by its moving average. All features are standardized over rolling windows. A compressed “super‑feature” is available that aggregates core trend and momentum components while penalizing excessive width (volatility). Users can switch between a “components” mode (weighted sum of individual features) and a “super” mode (single compressed driver).

Weighting and learning.

Weights are the rolling correlations between features (evaluated one horizon ago) and realized directional outcomes, smoothed by an EMA and optionally clamped to a bounded range to stabilize outliers. This produces an adaptive, regime‑aware weighting without explicit machine‑learning libraries.

Scoring and probability mapping.

The raw score is either the weighted component sum or the weighted super‑feature. The score is standardized again and passed through a sigmoid whose steepness is user‑controlled. A “prior shift” moves the sigmoid’s midpoint to the current base rate of up moves, estimated over the evaluation window, so that probabilities remain well‑calibrated when markets drift bullish or bearish. Probabilities and standardized scores are EMA‑smoothed for stability.

Decision policy.

Two modes are supported:

- Neutral band: go long if the probability is above one half plus a user‑set band; go short if it is below one half minus that band; otherwise stay neutral.

- Z‑score thresholds: use symmetric positive/negative cutoffs on the standardized score to trigger long/short.

Repaint protection.

All values used for decisions can be locked to confirmed (closed) bars. Intrabar updates are available as a preview, but confirmed values drive evaluation and stats.

Calibration.

An optional rolling linear calibration maps past confirmed probabilities to realized outcomes over the evaluation window. The mapping is clipped to the unit interval and can be injected back into the decision logic if desired. This improves reliability (probabilities that “mean what they say”) without necessarily improving raw separability.

Evaluation metrics.

The table reports: hit rate on signaled bars; a Wilson confidence interval for that hit rate at a chosen confidence level; Brier score as a measure of probability accuracy; counts of long/short trades; average realized return by side; profit factor; net return; and exposure (signal density). All are computed on rolling windows consistent with the learning scheme.

Visualization.

On the chart, an arrowed projection shows the predicted direction from the current bar to the chosen horizon, with magnitude scaled by ATR (optionally scaled by the square‑root of the horizon). Labels display either the decision probability or the standardized score. Neutral states can display a configurable icon for immediate recognition.

Computational properties.

The design relies on rolling means, standard deviations, correlations, and EMAs. Per‑bar cost is constant with respect to history length, and memory is constant per tracked series. Graphical objects are updated in place to obey platform limits.

Assumptions and limitations.

The method is correlation‑based and will adapt after regime changes, not before them. Calibration improves probability reliability but not necessarily ranking power. Intrabar previews are non‑binding and should not be evaluated as historical performance.

Part 2 — Trader‑facing description

What it does.

This tool tells you how likely price is to be higher after your chosen number of bars and converts that into Long / Short / Neutral calls. It learns, in real time, which components—momentum, trend, volatility, breadth, and volume—matter now, adjusts their weights, and shows you a probability line plus a forward arrow scaled by volatility.

How to set it up.

1) Choose your horizon. Intraday scalps: 5–10 bars. Swings: 10–30 bars. The default of 14 bars is a balanced starting point.

2) Pick a feature mode.

- components: granular and fast to adapt when leadership rotates between signals.

- super: cleaner single driver; less noise, slightly slower to react.

3) Decide how signals are triggered.

- Neutral band (probability based): intuitive and easy to tune. Widen the band for fewer, higher‑quality trades; tighten to catch more moves.

- Z‑score thresholds: consistent numeric cutoffs that ignore base‑rate drift.

4) Keep reliability helpers on. Leave prior shift and calibration enabled to stabilize probabilities across bullish/bearish regimes.

5) Smoothing. A short EMA on the probability or score reduces whipsaws while preserving turns.

6) Overlay. The arrow shows the call and a volatility‑scaled reach for the next horizon. Treat it as guidance, not a promise.

Reading the stats table.

- Hit Rate with a confidence interval: your recent accuracy with an uncertainty range; trust the range, not only the point.

- Brier Score: lower is better; it checks whether a stated “70%” really behaves like 70% over time.

- Profit Factor, Net Return, Exposure: quick triage of tradability and signal density.

- Average Return by Side: sanity‑check that the long and short calls each pull their weight.

Typical adjustments.

- Too many trades? Increase the neutral band or raise the z‑threshold.

- Missing the move? Tighten the band, or switch to components mode to react faster.

- Choppy timeframe? Lengthen the z‑score and correlation windows; keep calibration on.

- Volatility regime change? Revisit the ATR multiplier and enable square‑root scaling of horizon.

Execution and risk.

- Size positions by volatility (ATR‑based sizing works well).

- Enter on confirmed values; use intrabar previews only as early signals.

- Combine with your market structure (levels, liquidity zones). This model is statistical, not clairvoyant.

What it is not.

Not a black‑box machine‑learning model. It is transparent, correlation‑weighted technical analysis with strong attention to probability reliability and repaint safety.

Suggested defaults (robust starting point).

- Horizon 14; components mode; weight EMA 10; correlation window 500; z‑length 200.

- Neutral band around seven percentage points, or z‑threshold around one‑third of a standard deviation.

- Prior shift ON, Calibration ON, Use calibrated for decisions OFF to start.

- ATR multiplier 1.0; square‑root horizon scaling ON; EMA smoothing 3.

- Confidence setting equivalent to about 95%.

Disclaimer

No indicator guarantees profits. HorizonSigma Pro is a decision aid; always combine with solid risk management and your own judgment. Backtest, forward test, and size responsibly.

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Enhance your trading precision and confidence 🚀

Best regards

Chervolino

OB/FVG Precision Overlap ZonesThis indicator highlights only the zones where Order Blocks (OBs) and Fair Value Gaps (FVGs) overlap, filtering out weaker signals. By focusing on these confluence areas, it helps identify higher-probability entries and cleaner risk to reward setups.

Volumetric Support and Resistance [BackQuant]Volumetric Support and Resistance

What this is

This Overlay locates price levels where both structure and participation have been meaningful. It combines classical swing points with a volume filter, then manages those levels on the chart as price evolves. Each level carries:

• A reference price (support or resistance)

• An estimate of the volume that traded around that price

• A touch counter that updates when price retests it

• A visual box whose thickness is scaled by volatility

The result is a concise map of candidate support and resistance that is informed by both price location and how much trading occurred there.

How levels are built

Find structural pivots uses ta.pivothigh and ta.pivotlow with a user set sensitivity. Larger sensitivity looks for broader swings. Smaller sensitivity captures tighter turns.

Require meaningful volume computes an average volume over a lookback period and forms a volume ratio for the current bar. A pivot only becomes a level when the ratio is at least the volume significance multiplier.

Avoid clustering checks a minimum level distance (as a percent of price). If a candidate is too close to an existing level, it is skipped to keep the map readable.

Attach a volume strength to the level estimates volume strength by averaging the volume of recent bars whose high to low range spans that price. Levels with unusually high strength are flagged as high volume.

Store and draw levels are kept in an array with fields for price, type, volume, touches, creation bar, and a box handle. On the last bar, each level is drawn as a horizontal box centered at the price with a vertical thickness scaled by ATR. Borders are thicker when the level is marked high volume. Boxes can extend into the future.

How levels evolve over time

• Aging and pruning : levels are removed if they are too old relative to the lookback or if you exceed the maximum active levels.

• Break detection : a level can be removed when price closes through it by more than a break threshold set as a fraction of ATR. Toggle with Remove Broken Levels.

• Touches : when price approaches within the break threshold, the level’s touch counter increments.

Visual encoding

• Boxes : support boxes are green, resistance boxes are red. Box height uses an ATR based thickness so tolerance scales with volatility. Transparency is fixed in this version. Borders are thicker on high volume levels.

• Volume annotation : show the estimated volume inside the box or as a label at the right. If a level has more than one touch, a suffix like “(2x)” is appended.

• Extension : boxes can extend a fixed number of bars into the future and can be set to extend right.

• High volume bar tint : bars with volume above average × multiplier are tinted green if up and red if down.

Inputs at a glance

Core Settings

• Level Detection Sensitivity — pivot window for swing detection

• Volume Significance Multiplier — minimum volume ratio to accept a pivot

• Lookback Period — window for average volume and maintenance rules

Level Management

• Maximum Active Levels — cap on concurrently drawn levels

• Minimum Level Distance (%) — required spacing between level prices

Visual Settings

• Remove Broken Levels — drop a level once price closes decisively through it

• Show Volume Information on Levels — annotate volume and touches

• Extend Levels to Right — carry boxes forward

Enhanced Visual Settings

• Show Volume Text Inside Box — text placement option

• Volume Based Transparency and Volume Based Border Thickness — helper logic provided; current draw block fixes transparency and increases border width on high volume levels

Colors

• Separate colors for support, resistance, and their high volume variants

How it can be used

• Trade planning : use the most recent support and resistance as reference zones for entries, profit taking, or stop placement. ATR scaled thickness provides a practical buffer.

• Context for patterns : combine with breakouts, pullbacks, or candle patterns. A breakout through a high volume resistance carries more informational weight than one through a thin level.

• Prioritization : when multiple levels are nearby, prefer high volume or higher touch counts.

• Regime adaptation : widen sensitivity and increase minimum distance in fast regimes to avoid clutter. Tighten them in calm regimes to capture more granularity.

Why volume support and resistance is used in trading

Support and resistance relate to willingness to transact at certain prices. Volume measures participation. When many contracts change hands near a price:

• More market players hold inventory there, often creating responsive behavior on retests

• Order flow can concentrate again to defend or to exit

• Breaks can be cleaner as trapped inventory rebalances

Conditioning level detection on above average activity focuses attention on prices that mattered to more participants.

Alerts

• New Support Level Created

• New Resistance Level Created

• Level Touch Alert

• Level Break Alert

Strengths

• Dual filter of structure and participation, reducing trivial swing points

• Self cleaning map that retires old or invalid levels

• Volatility aware presentation using ATR based thickness

• Touch counting for persistence assessment

• Tunable inputs for instrument and timeframe

Limitations and caveats

• Volume strength is an approximation based on bars spanning the price, not true per price volume

• Pivots confirm after the sensitivity window completes, so new levels appear with a delay

• Narrow ranges can still cluster levels unless minimum distance is increased

• Large gaps may jump past levels and immediately trigger break conditions

Practical tuning guide

• If the chart is crowded: increase sensitivity, increase minimum level distance, or reduce maximum active levels

• If useful levels are missed: reduce volume multiplier or sensitivity

• If you want stricter break removal: increase the ATR based break threshold in code

• For instruments with session patterns: tailor the lookback period to a representative window

Interpreting touches and breaks

• First touch after creation is a validation test

• Multiple shallow touches suggest absorption; a later break may then travel farther

• Breaks on high current volume merit extra attention

Multi timeframe usage

Levels are computed on the active chart timeframe. A common workflow is to keep a higher timeframe instance for structure and a lower timeframe instance for execution. Align trades with higher timeframe levels where possible.

Final Thoughts

This indicator builds a lightweight, self updating map of support and resistance grounded in swings and participation. It is not a full market profile, but it captures much of the practical benefit with modest complexity. Treat levels as context and decision zones, not guarantees. Combine with your entry logic and risk controls.

X FocusDesigned to help traders reduce distractions by de-emphasizing specific time ranges on the chart. Instead of highlighting high-activity zones, this tool intentionally applies a muted overlay to selected sessions, allowing traders to concentrate on price action that occurs outside those designated ranges.

Core Purpose

The primary goal of this indicator is to combat the “noise” that often arises during certain periods, such as overnight sessions or pre-market trading. By visually softening those areas, traders can focus on the more relevant trading windows WITHOUT losing any time-based context. Unlike traditional tools that remove data entirely, X Focus preserves all candlestick and price information—ensuring that key levels, gaps, or reference values are still visible.

Key Features

Custom Session Filtering

Users can define up to three time ranges depending on preference. This flexibility allows for tailoring the indicator to different market strategies.

De-Emphasis by Design

Instead of masking or deleting data, the indicator overlays a semi-transparent shading box over the chosen sessions. This ensures traders remain aware of the data while maintaining visual focus on the price action outside of the selected time blocks.

Dual Utility – Highlight or Suppress

While built on the principle of minimizing distractions, the same framework can also be used in reverse to highlight specific areas of interest. This versatility makes it suitable for both noise-reduction and spotlighting critical ranges.

Dark Mode / Light Mode

Adjustable color schemes allow seamless integration into any chart setup, whether the user prefers dark or light backgrounds.

Non-Intrusive Visualization

The shading effect is applied without altering price bars, indicators, or other overlays. This ensures compatibility with existing technical tools and strategies.

Use Case

Traders who find themselves reacting too strongly to inconsequential movements during certain times (such as after-hours or low-volume sessions) can benefit from the X Focus indicator. It helps maintain clarity and discipline by visually guiding attention toward the periods that matter most—without erasing or ignoring potentially useful price references.

Infinite EMA with Alpha Control♾️ Infinite EMA with Alpha Control

What Makes This EMA "Infinite"?

Unlike traditional EMA indicators that are limited to typical periods (1-5000), this Infinite EMA breaks all boundaries. You can create EMAs with periods of 1,000, 10,000, or even 1,000,000 bars - that's why it's called "infinite"! Also Infinite EMA starts working immediately from the very first bar on your chart

Why This EMA is "Infinite":

1. Mathematically: When N → ∞, alpha → 0, meaning infinitely long "memory"

2. Practically: You can set any period - even 100,000 bars

3. Flexibility: Alpha allows precise control over the "forgetting speed"

How Does It Work?

The magic lies in the Alpha parameter. While regular EMAs use fixed formulas, this indicator gives you direct control over the EMA's "memory" through Alpha values:

• High Alpha (0.1-0.2): Fast reaction, short memory

• Medium Alpha (0.01-0.05): Balanced response

• Low Alpha (0.0001-0.001): Extremely slow reaction, very long memory

• Ultra-low Alpha (0.000001): Almost frozen in time

The Mathematical Formula:

Alpha = 2 / (Period + 1)

This means you can achieve any EMA period by adjusting Alpha, giving you infinite flexibility!

Expanded "Infinite EMA" Table:

Period EMA (N) - Alpha (Rounded) - Alpha (Exact) - Description

10 - 0.1818 - 0.181818... - Fast EMA

20 - 0.0952 - 0.095238... - Short-term

50 - 0.0392 - 0.039215... - Medium-term

100 - 0.0198 - 0.019801... - Long-term

200 - 0.0100 - 0.009950... - Standard long-term

500 - 0.0040 - 0.003996... - Very long-term

1,000 - 0.0020 - 0.001998... - Super long-term

2,000 - 0.0010 - 0.000999... - Ultra long-term

5,000 - 0.0004 - 0.000399... - Mega long-term

10,000 - 0.0002 - 0.000199... - Giga long-term

25,000 - 0.00008 - 0.000079... - Century-scale EMA

50,000 - 0.00004 - 0.000039... - Practically motionless

100,000 - 0.00002 - 0.000019... - "Glacial" EMA

500,000 - 0.000004 - 0.000003... - Geological timescale

1,000,000 - 0.000002 - 0.000001... - Approaching constant

5,000,000 - 0.0000004 - 0.0000003... - Virtually static

10,000,000 - 0.0000002 - 0.0000001... - Nearly flat line

100,000,000 - 0.00000002 - 0.00000001... - Mathematical infinity

Formula: Alpha = 2/(N+1) where N is the EMA period

Key Features:

Dual EMA System: Run fast and slow EMAs simultaneously

Crossover Signals: Automatic buy/sell signals with customizable alerts

Alpha Control: Direct mathematical control over EMA behavior

Infinite Periods: From 1 to 100,000,000+ bars

Visual Customization: Colors, fills, backgrounds, signal sizes

Instant Start: Works accurately from the very first bar

Update Intervals: Control calculation frequency for noise reduction

Why Choose Infinite EMA?

1. Unlimited Flexibility: Any period you can imagine

2. Mathematical Precision: Direct alpha control for exact behavior

3. Professional Grade: Suitable for all trading styles

4. Easy to Use: Simple settings with powerful results

5. No Warm-up Period: Accurate values from bar #1

Simple Explanation:

Think of EMA as a "memory system":

• High Alpha = Short memory (forgets quickly, reacts fast)

• Low Alpha = Long memory (remembers everything, moves slowly)

With Infinite EMA, you can set the "memory length" to anything from seconds to centuries!

⚡ Instant Start Feature - EMA from First Bar

Immediate Calculation from Bar #1

Unlike traditional EMA indicators that require a "warm-up period" of N bars before showing accurate values, Infinite EMA starts working immediately from the very first bar on your chart.

How It Works:

Traditional EMA Problem:

• Standard 200-period EMA: Needs 200+ bars to become accurate

• First 200 bars: Shows incorrect/unstable values

• Result: Large portions of historical data are unusable

Infinite EMA Solution:

Bar #1: EMA = Current Price (perfect starting point)

Bar #2: EMA = Alpha × Price + (1-Alpha) × Previous EMA

Bar #3: EMA = Alpha × Price + (1-Alpha) × Previous EMA

...and so on

Key Benefits:

No Warm-up Period: Start trading signals from day one

Full Chart Coverage: Every bar has a valid EMA value

Historical Accuracy: Backtesting works on entire dataset

New Markets: Works perfectly on newly listed assets

Short Datasets: Effective even with limited historical data

Practical Impact:

Scenario Traditional EMA Infinite EMA

New cryptocurrency Unusable for first 200 days ✅ Works from day 1

Limited data (< 200 bars) Inaccurate values ✅ Fully functional

Backtesting Must skip first 200 bars ✅ Test entire history

Real-time trading Wait for stabilization ✅ Trade immediately

Technical Implementation:

if barstate.isfirst

EMA := currentPrice // Perfect initialization

else

EMA := alpha × currentPrice + (1-alpha) × previousEMA

This smart initialization ensures mathematical accuracy from the very first calculation, eliminating the traditional EMA "ramp-up" problem.

Why This Matters:

For Backesters: Use 100% of available data

For Live Trading: Get signals immediately on any timeframe

For Researchers: Analyze complete datasets without gaps

Bottom Line: Infinite EMA is ready to work the moment you add it to your chart - no waiting, no warm-up, no exceptions!

Unlike traditional EMAs that require a "warm-up period" of 200+ bars before showing accurate values, Infinite EMA starts working immediately from bar #1.

This breakthrough eliminates the common problem where the first portion of your chart shows unreliable EMA data. Whether you're analyzing a newly listed cryptocurrency, working with limited historical data, or backtesting strategies, every single bar provides mathematically accurate EMA values.

No more waiting periods, no more unusable data sections - just instant, reliable trend analysis from the moment you apply the indicator to any chart.

🔄 Update Interval Bars Feature

The Update Interval feature allows you to control how frequently the EMA recalculates, providing flexible noise filtering without changing the core mathematics.

Set to 1 for standard behavior (updates every bar), or increase to 5-10 for smoother signals that update less frequently. Higher intervals reduce market noise and false signals but introduce slightly more lag. This is particularly useful on volatile timeframes where you want the EMA's directional bias without every minor price fluctuation affecting the calculation.

Perfect for swing traders who prefer cleaner, more stable trend lines over hyper-responsive indicators.

Conclusion

The Infinite EMA transforms the traditional EMA from a fixed-period tool into a precision instrument with unlimited flexibility. By understanding the Alpha-Period relationship, traders can create custom EMAs that perfectly match their trading style, timeframe, and market conditions.

The "infinite" nature comes from the ability to set any period imaginable - from ultra-fast 2-bar EMAs to glacially slow 10-million-bar EMAs, all controlled through a single Alpha parameter.

________________________________________

Whether you're a beginner looking for simple trend following or a professional researcher analyzing century-long patterns, Infinite EMA adapts to your needs. The power of infinite periods is now in your hands! 🚀

Go forward to the horizon. When you reach it, a new one will open up.

- J. P. Morgan

BPS Multi-MA 5 — 22/30, SMA/WMA/EMA# Multi-MA 5 — 22/30 base, SMA/WMA/EMA

**What it is**

A lightweight 5-line moving-average ribbon for fast visual bias and trend/mean-reversion reads. You can switch the MA type (SMA/WMA/EMA) and choose between two ways of setting lengths: by monthly “session-based” base (22 or 30) with multipliers, or by entering exact lengths manually. An optional info table shows the effective settings in real time.

---

## How it works

* Calculates five moving averages from the selected price source.

* Lengths are either:

* **Multipliers mode:** `Base × Multiplier` (e.g., base 22 → 22/44/66/88/110), or

* **Manual mode:** any five exact lengths (e.g., 10/22/50/100/200).

* Plots five lines with fixed legend titles (MA1…MA5); the **info table** displays the actual type and lengths.

---

## Inputs

**Length Mode**

* **Multipliers** — choose a **Base** of **22** (≈ trading sessions per month) or **30** (calendar-style, smoother) and set **×1…×5** multipliers.

* **Manual** — enter **Len1…Len5** directly.

**MA Settings**

* **MA Type:** SMA / WMA / EMA

* **Source:** any series (e.g., `close`, `hlc3`, etc.)

* **Use true close (ignore Heikin Ashi):** when enabled, the MA is computed from the underlying instrument’s real `close`, not HA candles.

* **Show info table:** toggles the on-chart table with the current mode, type, base, and lengths.

---

## Quick start

1. Add the indicator to your chart.

2. Pick **MA Type** (e.g., **WMA** for faster response, **SMA** for smoother).

3. Choose **Length Mode**:

* **Multipliers:** set **Base = 22** for session-based monthly lengths (stocks/FX), or **30** for heavier smoothing.

* **Manual:** enter your exact lengths (e.g., 10/22/50/100/200).

4. (Optional) On **Heikin Ashi** charts, enable **Use true close** if you want the lines based on the instrument’s real close.

---

## Tips & notes

* **1 month ≈ 21–22 sessions.** Using 30 as “monthly” yields a smoother, more delayed curve.

* **WMA** reacts faster than **SMA** at the same length; expect earlier signals but more whipsaws in chop.

* **Len = 1** makes the MA track the chosen source (e.g., `close`) almost exactly.

* If changing lengths doesn’t move the lines, ensure you’re editing fields for the **active Length Mode** (Multipliers vs Manual).

* For clean comparisons, use the **same timeframe**. If you later wrap this in MTF logic, keep `lookahead_off` and handle gaps appropriately.

---

## Use cases

* Trend ribbon and dynamic bias zones

* Pullback entries to the mid/slow lines

* Crossovers (fast vs slow) for confirmation

* Volatility filtering by spreading lengths (e.g., 22/44/88/132/176)

---

**Credits:** Built for clarity and speed; designed around session-based “monthly” lengths (22) or smoother calendar-style (30).

NQ FVG + MSS ChecklistThe NQ FVG + MSS Quick Checklist is a simple yet powerful visual tool for traders focusing on the Nasdaq 100 (NQ) futures. It provides a step-by-step checklist to assess trade setups based on key market concepts like Fair Value Gaps (FVG), Market Structure Shifts (MSS), session highs/lows, and previous day levels.

This indicator helps you quickly see which elements of your trading plan are met before entering a trade. Each checklist item can be manually toggled, and a cumulative Trade Score provides a quick visual guide to setup strength.

Key Features:

Step-by-step checklist for NQ trading setups

Track levels: Session highs/lows & Previous Day High/Low

Spot 5M FVG and Retests

Identify MSS on 1M and find 1M FVG inside MSS

Manual SL & TP guidance

Trade Score for quick setup strength assessment

Fully visible table overlay on top of the chart

How to Use:

Mark session & previous day levels

Observe reaction at key levels (Sweep or Continue)

Identify 5M FVG and any retests

Spot 1M MSS and 1M FVG inside MSS

Set SL/TP based on FVG extremes and next session levels

Check the cumulative Trade Score for setup confirmation

Note: This indicator is manual input-based, letting traders tick off items as they analyze the chart, making it a lightweight trading checklist HUD that stays on top of all chart elements.

Advanced Price Ranges ICTThis indicator automatically divides price into fixed ranges (configurable in points or pips) and plots important reference levels such as the high, low, 50% midpoint, and 25%/75% quarters. It is designed to help traders visualize structured price movement, spot confluence zones, and frame their trading bias around clean range-based levels.

🔹 Key Features

Custom Range Size: Define ranges in points (e.g., 100, 50, 25, 10) or in Forex pips.

Forex Mode: Automatically adapts pip size (0.0001 or 0.01 for JPY pairs).

Dynamic Anchoring: Price ranges automatically align to the current price, snapping into blocks.

Multiple Ranges: Option to extend visualization above and below the current active block for a complete grid.

Level Types:

High / Low of the range

50% midpoint

25% and 75% quarters

Custom Styling: Adjustable line colors and widths for each level type.

Labels: Optional right-edge labels showing level type and exact price.

Alerts: Built-in alerts for when price crosses the range high, low, or 50% midpoint.

🔹 Use Cases

Quickly map out 100/50/25/10 point structures like Zeussy’s advanced price range method.

Identify key reaction levels where liquidity is often built or swept.

Support ICT-style concepts like range-based bias, fair value gaps, and liquidity pools.

Works for indices, futures, crypto, and forex.

🔹 Customization

Range increments can be set to any size (default 100).

Toggle which levels are shown (High/Low, Midpoint, Quarters).

Adjustable line widths, colors, and label visibility.

Extend ranges above and below for broader market context.

SCTI-D1SCTI-D1 Indicator Introduction / 指标简介

The SCTI-D1 (Smart Composite Trading Indicator - Daily) is a comprehensive, multi-feature trading tool designed for serious traders who demand depth, flexibility, and clarity in their market analysis. This indicator combines several powerful concepts into one seamless workflow, including:

Multiple EMA Systems with customizable lengths and visibility

PMA (Projected Moving Average) with fill options between lines

VWAP with configurable anchors and deviation bands

Divergence Detection for MACD and Histogram

Volume Profile with node detection (peaks, troughs, highs, lows)

Smart Money Concepts including order blocks, fair value gaps, equal highs/lows, and market structure shifts

Whether you trade stocks, forex, or cryptocurrencies, the SCTI-D1 helps you identify key levels, track institutional activity, and spot high-probability reversal signals—all in one clean, customizable interface.

SCTI-D1 指标简介

SCTI-D1(智能综合交易指标 - 日线版)是一款功能全面的交易工具,专为需要深度、灵活性和清晰市场分析的专业交易者设计。该指标将多种强大概念融合在一个流畅的工作流程中,包括:

多组EMA系统,可自定义长度和显示

PMA(投影移动平均线),支持均线间填充色

VWAP,可配置锚定周期和偏差带

背离检测,支持MACD和柱状图

成交量分布,支持节点检测(峰值、谷值、最高、最低)

聪明钱概念,包括订单块、公允价值缺口、等高/等低和市场结构转换

无论您交易股票、外汇还是加密货币,SCTI-D1 都能帮助您识别关键水平、跟踪机构资金动向并发现高概率反转信号——所有功能均集成在一个清晰可定制的界面中。

ICT Structure Levels (ST/IT/LT) - v7 (by Jonas E)ICT Structure Levels (ST/IT/LT) – Neighbor-Wick Pivots

This indicator is designed for traders following ICT-style market structure analysis. It identifies Short-Term (ST), Intermediary (IT), and Long-Term (LT) swing highs and lows, but with a stricter filter that reduces false signals.

Unlike standard pivot indicators, this script requires not only that a bar makes a structural high/low, but also that the neighboring bars’ extremes are formed by wicks rather than flat-bodied candles. This wick condition helps confirm that the level is a true liquidity sweep and not just random price action.

How it works (conceptual):

Detects pivots based on user-defined left/right bars.

Validates that extremes on both sides of the pivot are wick-driven (high > body for highs, low < body for lows).

Marks valid STH/STL, ITH/ITL, and LTH/LTL directly on the chart with optional price labels.

Uses ATR offset for better label readability.

Alerts can be enabled to notify when a new structural level is confirmed.

How to use it:

Map market structure across multiple layers (ST/IT/LT).

Identify true liquidity grabs and avoid false highs/lows.

Integrate with Break of Structure (BOS) and Change of Character (CHoCH) strategies.

Combine with other ICT concepts (Order Blocks, Fair Value Gaps, Liquidity Pools).

What makes it unique:

Most pivot indicators mark every high/low indiscriminately. This script filters pivots using wick validation, which significantly reduces noise and focuses only on the levels most relevant to liquidity-based trading strategies.

Smarter Money Concepts - Wyckoff Springs & Upthrusts [PhenLabs]📊Smarter Money Concepts - Wyckoff Springs & Upthrusts

Version: PineScript™v6

📌Description

Discover institutional manipulation in real-time with this advanced Wyckoff indicator that detects Springs (accumulation phases) and Upthrusts (distribution phases). It identifies when price tests support or resistance on high volume, followed by a strong recovery, signaling potential reversals where smart money accumulates or distributes positions. This tool solves the common problem of missing these subtle phase transitions, helping traders anticipate trend changes and avoid traps in volatile markets.

By combining volume spike detection, ATR-normalized recovery strength, and a sigmoid probability model, it filters out weak signals and highlights only high-confidence setups. Whether you’re swing trading or day trading, this indicator provides clear visual cues to align with institutional flows, improving entry timing and risk management.

🚀Points of Innovation

Sigmoid-based probability threshold for signal filtering, ensuring only statistically significant Wyckoff patterns trigger alerts

ATR-normalized recovery measurement that adapts to market volatility, unlike static recovery checks in traditional indicators

Customizable volume spike multiplier to distinguish institutional volume from retail noise

Integrated dashboard legend with position and size options for personalized chart visualization

Hidden probability plots for advanced users to analyze underlying math without chart clutter

🔧Core Components

Support/Resistance Calculator: Scans a user-defined lookback period to establish dynamic levels for Spring and Upthrust detection

Volume Spike Detector: Compares current volume to a 10-period SMA, multiplied by a configurable factor to identify significant surges

Recovery Strength Analyzer: Uses ATR to measure price recovery after breaks, normalizing for different market conditions

Probability Model: Applies sigmoid function to combine volume and recovery data, generating a confidence score for each potential signal

🔥Key Features

Spring Detection: Spots accumulation when price dips below support but recovers strongly, helping traders enter longs at potential bottoms

Upthrust Detection: Identifies distribution when price spikes above resistance but falls back, alerting to possible short opportunities at tops

Customizable Inputs: Adjust lookback, volume multiplier, ATR period, and probability threshold to match your trading style and market

Visual Signals: Clear + (green) and - (red) labels on charts for instant recognition of accumulation and distribution phases

Alert System: Triggers notifications for signals and probability thresholds, keeping you informed without constant monitoring

🎨Visualization

Spring Signal: Green upward label (+) below the bar, indicating strong recovery after support break for accumulation

Upthrust Signal: Red downward label (-) above the bar, showing failed breakout above resistance for distribution

Dashboard Legend: Customizable table explaining signals, positioned anywhere on the chart for quick reference

📖Usage Guidelines

Core Settings

Support/Resistance Lookback

Default: 20

Range: 5-50

Description: Sets bars back for S/R levels; lower for recent sensitivity, higher for stable long-term zones – ideal for spotting Wyckoff phases

Volume Spike Multiplier

Default: 1.5

Range: 1.0-3.0

Description: Multiplies 10-period volume SMA; higher values filter to significant spikes, confirming institutional involvement in patterns

ATR for Recovery Measurement

Default: 5

Range: 2-20

Description: ATR period for recovery strength; shorter for volatile markets, longer for smoother analysis of post-break recoveries

Phase Transition Probability Threshold

Default: 0.9

Range: 0.5-0.99

Description: Minimum sigmoid probability for signals; higher for strict filtering, ensuring only high-confidence Wyckoff setups

Display Settings

Dashboard Position

Default: Top Right

Range: Various positions

Description: Places legend table on chart; choose based on layout to avoid overlapping price action

Dashboard Text Size

Default: Normal

Range: Auto to Huge

Description: Adjusts legend text; larger for visibility, smaller for minimal space use

✅Best Use Cases

Swing Trading: Identify Springs for long entries in downtrends turning to accumulation

Day Trading: Catch Upthrusts for short scalps during intraday distribution at resistance

Trend Reversal Confirmation: Use in conjunction with other indicators to validate phase shifts in ranging markets

Volatility Plays: Spot signals in high-volume environments like news events for quick reversals

⚠️Limitations

May produce false signals in low-volume or sideways markets where volume spikes are unreliable

Depends on historical data, so performance varies in unprecedented market conditions or gaps

Probability model is statistical, not predictive, and cannot account for external factors like news

💡What Makes This Unique

Probability-Driven Filtering: Sigmoid model combines multiple factors for superior signal quality over basic Wyckoff detectors

Adaptive Recovery: ATR normalization ensures reliability across assets and timeframes, unlike fixed-threshold tools

User-Centric Design: Tooltips, customizable dashboard, and alerts make it accessible yet powerful for all trader levels

🔬How It Works

Calculate S/R Levels:

Uses the highest high and the lowest low over the lookback period to set dynamic zones

Establishes baseline for detecting breaks in Wyckoff patterns

Detect Breaks and Recovery:

Checks for price breaking support/resistance, then recovering on volume

Measures recovery strength via ATR for volatility adjustment

Apply Probability Model:

Combines volume spike and recovery into a sigmoid function for confidence score

Triggers signal only if above threshold, plotting visuals and alerts

💡Note:

For optimal results, combine with price action analysis and test settings on historical charts. Remember, Wyckoff patterns are most effective in trending markets – use lower probability thresholds for practice, then increase for live trading to focus on high-quality setups.

MMA, Mid-Price Moving Averages (Open + Close Based MAs)📝 Script Description

This script introduces a custom set of moving averages based on the mid-price, calculated as the average of the open and close prices:

Mid Price = (Open + Close) / 2

Instead of traditional close-based MAs, this approach reflects the average sentiment throughout the trading session, offering a smoother and more realistic view of price action.

🔍 Key Features:

✅ Gap-aware smoothing

Captures opening gaps, offering a better representation of intraday shifts.

✅ Reduced noise

Less vulnerable to sharp closing moves or one-off spikes, making it easier to identify true trend breaks or supports.

✅ Closer to actual flow

Reflects a more natural midline of price movement, ideal for traders who prioritize clean, sustained trends.

✅ Better support/resistance alignment

Especially useful for identifying stable uptrends and minimizing false breakout signals.

📐 Included Moving Averages:

MA 5

MA 10

MA 20

MA 60

MA 120

MA 200

(All based on mid-price, not close)

🎯 Recommended For:

Traders seeking smoother and more reliable trendlines

Those who want a more realistic depiction of support and resistance

Ideal for filtering out noisy movements while focusing on clean, straight-moving charts

Imbalance RSI Divergence Strategy# Imbalance RSI Divergence Strategy - User Guide

## What is This Strategy?

This strategy identifies **imbalance** zones in the market and combines them with **RSI divergence** to generate trading signals. It aims to capitalize on price gaps left by institutional investors and large volume movements.

### Main Settings

- **RSI Period (14)**: Period used for RSI calculation. Lower values = more sensitive, higher values = more stable signals.

- **ATR Period (10)**: Period for volatility measurement using Average True Range.

- **ATR Stop Loss Multiplier (2.0)**: How many ATR units to use for stop loss calculation.

- **Risk:Reward Ratio (4.0)**: Risk-reward ratio. 2.0 = 2 units of reward for 1 unit of risk.

- **Use RSI Divergence Filter (true)**: Enables/disables the RSI divergence filter.

### Imbalance Filters

- **Minimum Imbalance Size (ATR) (0.3)**: Minimum imbalance size in ATR units to filter out small imbalances.

- **Enable Lookback Limit (false)**: Activates historical lookback limitations.

- **Maximum Lookback Bars (300)**: Maximum number of bars to look back.

### Visual Settings

- **Show Imbalance Size**: Displays imbalance size in ATR units.

- **Show RSI Divergence Lines**: Shows/hides divergence lines.

- **Divergence Line Colors**: Colors for bullish/bearish divergence lines.

### Volatility-Based Adjustments

- **Low volatility markets**:

- Minimum Imbalance Size: 0.2-0.4 ATR

- ATR Stop Loss Multiplier: 1.5-2.0

- **High volatility markets**:

- Minimum Imbalance Size: 0.5-1.0 ATR

- ATR Stop Loss Multiplier: 2.5-3.5

### Risk Tolerance

- **Conservative approach**:

- Risk:Reward Ratio: 2.0-3.0

- RSI Divergence Filter: Enabled

- Minimum Imbalance Size: Higher (0.5+ ATR)

- **Aggressive approach**:

- Risk:Reward Ratio: 4.0-6.0

- Minimum Imbalance Size: Lower (0.2-0.3 ATR)

###Market Conditions

- **Trending markets**: Higher RSI Period (21-28)

- **Sideways markets**: Lower RSI Period (10-14)

- **Volatile markets**: Higher ATR Multiplier

## Recommended Testing Procedure

1. **Start with default settings** and backtest on 3-6 months of historical data

2. **Adjust RSI Period** to see which value produces better results

3. **Optimize ATR Multiplier** for stop loss levels

4. **Test different Risk:Reward ratios** comparatively

5. **Fine-tune Minimum Imbalance Size** to improve signal quality

## Important Considerations

- **False positive signals**: Imbalances may be less reliable during low volatility periods

- **Market openings**: First hours often produce more imbalances but can be riskier

- **News events**: Consider disabling strategy during major news releases

- **Backtesting**: Test across different market conditions (trending, sideways, volatile)

## Recommended Settings for Beginners

**Safe settings for new users:**

- RSI Period: 14

- ATR Period: 14

- ATR Stop Loss Multiplier: 2.5

- Risk:Reward Ratio: 3.0

- Minimum Imbalance Size: 0.5 ATR

- RSI Divergence Filter: Enabled

## Advanced Tips

### Signal Quality Improvement

- **Combine with market structure**: Look for imbalances near key support/resistance levels

- **Volume confirmation**: Higher volume during imbalance formation increases reliability

- **Multiple timeframe analysis**: Confirm signals on higher timeframes

### Risk Management

- **Position sizing**: Never risk more than 1-2% of account per trade

- **Maximum drawdown**: Set overall stop loss for the strategy

- **Market hours**: Consider avoiding low liquidity periods

### Performance Monitoring

- **Win rate**: Track percentage of profitable trades

- **Average R:R**: Monitor actual risk-reward achieved vs. target

- **Maximum consecutive losses**: Set alerts for strategy review

This strategy works best when combined with proper risk management and market analysis. Always backtest thoroughly before using real money and adjust parameters based on your specific market and trading style.

Seasonality Monte Carlo Forecaster [BackQuant]Seasonality Monte Carlo Forecaster

Plain-English overview

This tool projects a cone of plausible future prices by combining two ideas that traders already use intuitively: seasonality and uncertainty. It watches how your market typically behaves around this calendar date, turns that seasonal tendency into a small daily “drift,” then runs many randomized price paths forward to estimate where price could land tomorrow, next week, or a month from now. The result is a probability cone with a clear expected path, plus optional overlays that show how past years tended to move from this point on the calendar. It is a planning tool, not a crystal ball: the goal is to quantify ranges and odds so you can size, place stops, set targets, and time entries with more realism.

What Monte Carlo is and why quants rely on it

• Definition . Monte Carlo simulation is a way to answer “what might happen next?” when there is randomness in the system. Instead of producing a single forecast, it generates thousands of alternate futures by repeatedly sampling random shocks and adding them to a model of how prices evolve.

• Why it is used . Markets are noisy. A single point forecast hides risk. Monte Carlo gives a distribution of outcomes so you can reason in probabilities: the median path, the 68% band, the 95% band, tail risks, and the chance of hitting a specific level within a horizon.

• Core strengths in quant finance .

– Path-dependent questions : “What is the probability we touch a stop before a target?” “What is the expected drawdown on the way to my objective?”

– Pricing and risk : Useful for path-dependent options, Value-at-Risk (VaR), expected shortfall (CVaR), stress paths, and scenario analysis when closed-form formulas are unrealistic.

– Planning under uncertainty : Portfolio construction and rebalancing rules can be tested against a cloud of plausible futures rather than a single guess.

• Why it fits trading workflows . It turns gut feel like “seasonality is supportive here” into quantitative ranges: “median path suggests +X% with a 68% band of ±Y%; stop at Z has only ~16% odds of being tagged in N days.”

How this indicator builds its probability cone

1) Seasonal pattern discovery

The script builds two day-of-year maps as new data arrives:

• A return map where each calendar day stores an exponentially smoothed average of that day’s log return (yesterday→today). The smoothing (90% old, 10% new) behaves like an EWMA, letting older seasons matter while adapting to new information.

• A volatility map that tracks the typical absolute return for the same calendar day.

It calculates the day-of-year carefully (with leap-year adjustment) and indexes into a 365-slot seasonal array so “March 18” is compared with past March 18ths. This becomes the seasonal bias that gently nudges simulations up or down on each forecast day.

2) Choice of randomness engine

You can pick how the future shocks are generated:

• Daily mode uses a Gaussian draw with the seasonal bias as the mean and a volatility that comes from realized returns, scaled down to avoid over-fitting. It relies on the Box–Muller transform internally to turn two uniform random numbers into one normal shock.

• Weekly mode uses bootstrap sampling from the seasonal return history (resampling actual historical daily drifts and then blending in a fraction of the seasonal bias). Bootstrapping is robust when the empirical distribution has asymmetry or fatter tails than a normal distribution.

Both modes seed their random draws deterministically per path and day, which makes plots reproducible bar-to-bar and avoids flickering bands.

3) Volatility scaling to current conditions

Markets do not always live in average volatility. The engine computes a simple volatility factor from ATR(20)/price and scales the simulated shocks up or down within sensible bounds (clamped between 0.5× and 2.0×). When the current regime is quiet, the cone narrows; when ranges expand, the cone widens. This prevents the classic mistake of projecting calm markets into a storm or vice versa.

4) Many futures, summarized by percentiles

The model generates a matrix of price paths (capped at 100 runs for performance inside TradingView), each path stepping forward for your selected horizon. For each forecast day it sorts the simulated prices and pulls key percentiles:

• 5th and 95th → approximate 95% band (outer cone).

• 16th and 84th → approximate 68% band (inner cone).

• 50th → the median or “expected path.”

These are drawn as polylines so you can immediately see central tendency and dispersion.

5) A historical overlay (optional)

Turn on the overlay to sketch a dotted path of what a purely seasonal projection would look like for the next ~30 days using only the return map, no randomness. This is not a forecast; it is a visual reminder of the seasonal drift you are biasing toward.

Inputs you control and how to think about them

Monte Carlo Simulation

• Price Series for Calculation . The source series, typically close.

• Enable Probability Forecasts . Master switch for simulation and drawing.

• Simulation Iterations . Requested number of paths to run. Internally capped at 100 to protect performance, which is generally enough to estimate the percentiles for a trading chart. If you need ultra-smooth bands, shorten the horizon.

• Forecast Days Ahead . The length of the cone. Longer horizons dilute seasonal signal and widen uncertainty.

• Probability Bands . Draw all bands, just 95%, just 68%, or a custom level (display logic remains 68/95 internally; the custom number is for labeling and color choice).

• Pattern Resolution . Daily leans on day-of-year effects like “turn-of-month” or holiday patterns. Weekly biases toward day-of-week tendencies and bootstraps from history.

• Volatility Scaling . On by default so the cone respects today’s range context.

Plotting & UI

• Probability Cone . Plots the outer and inner percentile envelopes.

• Expected Path . Plots the median line through the cone.

• Historical Overlay . Dotted seasonal-only projection for context.

• Band Transparency/Colors . Customize primary (outer) and secondary (inner) band colors and the mean path color. Use higher transparency for cleaner charts.

What appears on your chart

• A cone starting at the most recent bar, fanning outward. The outer lines are the ~95% band; the inner lines are the ~68% band.

• A median path (default blue) running through the center of the cone.

• An info panel on the final historical bar that summarizes simulation count, forecast days, number of seasonal patterns learned, the current day-of-year, expected percentage return to the median, and the approximate 95% half-range in percent.

• Optional historical seasonal path drawn as dotted segments for the next 30 bars.

How to use it in trading

1) Position sizing and stop logic

The cone translates “volatility plus seasonality” into distances.

• Put stops outside the inner band if you want only ~16% odds of a stop-out due to noise before your thesis can play.

• Size positions so that a test of the inner band is survivable and a test of the outer band is rare but acceptable.

• If your target sits inside the 68% band at your horizon, the payoff is likely modest; outside the 68% but inside the 95% can justify “one-good-push” trades; beyond the 95% band is a low-probability flyer—consider scaling plans or optionality.

2) Entry timing with seasonal bias

When the median path slopes up from this calendar date and the cone is relatively narrow, a pullback toward the lower inner band can be a high-quality entry with a tight invalidation. If the median slopes down, fade rallies toward the upper band or step aside if it clashes with your system.

3) Target selection

Project your time horizon to N bars ahead, then pick targets around the median or the opposite inner band depending on your style. You can also anchor dynamic take-profits to the moving median as new bars arrive.

4) Scenario planning & “what-ifs”

Before events, glance at the cone: if the 95% band already spans a huge range, trade smaller, expect whips, and avoid placing stops at obvious band edges. If the cone is unusually tight, consider breakout tactics and be ready to add if volatility expands beyond the inner band with follow-through.

5) Options and vol tactics

• When the cone is tight : Prefer long gamma structures (debit spreads) only if you expect a regime shift; otherwise premium selling may dominate.

• When the cone is wide : Debit structures benefit from range; credit spreads need wider wings or smaller size. Align with your separate IV metrics.

Reading the probability cone like a pro

• Cone slope = seasonal drift. Upward slope means the calendar has historically favored positive drift from this date, downward slope the opposite.

• Cone width = regime volatility. A widening fan tells you that uncertainty grows fast; a narrow cone says the market typically stays contained.

• Mean vs. price gap . If spot trades well above the median path and the upper band, mean-reversion risk is high. If spot presses the lower inner band in an up-sloping cone, you are in the “buy fear” zone.

• Touches and pierces . Touching the inner band is common noise; piercing it with momentum signals potential regime change; the outer band should be rare and often brings snap-backs unless there is a structural catalyst.

Methodological notes (what the code actually does)

• Log returns are used for additivity and better statistical behavior: sim_ret is applied via exp(sim_ret) to evolve price.

• Seasonal arrays are updated online with EWMA (90/10) so the model keeps learning as each bar arrives.

• Leap years are handled; indexing still normalizes into a 365-slot map so the seasonal pattern remains stable.

• Gaussian engine (Daily mode) centers shocks on the seasonal bias with a conservative standard deviation.

• Bootstrap engine (Weekly mode) resamples from observed seasonal returns and adds a fraction of the bias, which captures skew and fat tails better.

• Volatility adjustment multiplies each daily shock by a factor derived from ATR(20)/price, clamped between 0.5 and 2.0 to avoid extreme cones.

• Performance guardrails : simulations are capped at 100 paths; the probability cone uses polylines (no heavy fills) and only draws on the last confirmed bar to keep charts responsive.

• Prerequisite data : at least ~30 seasonal entries are required before the model will draw a cone; otherwise it waits for more history.

Strengths and limitations

• Strengths :

– Probabilistic thinking replaces single-point guessing.

– Seasonality adds a small but meaningful directional bias that many markets exhibit.

– Volatility scaling adapts to the current regime so the cone stays realistic.

• Limitations :

– Seasonality can break around structural changes, policy shifts, or one-off events.

– The number of paths is performance-limited; percentile estimates are good for trading, not for academic precision.

– The model assumes tomorrow’s randomness resembles recent randomness; if regime shifts violently, the cone will lag until the EWMA adapts.

– Holidays and missing sessions can thin the seasonal sample for some assets; be cautious with very short histories.

Tuning guide

• Horizon : 10–20 bars for tactical trades; 30+ for swing planning when you care more about broad ranges than precise targets.

• Iterations : The default 100 is enough for stable 5/16/50/84/95 percentiles. If you crave smoother lines, shorten the horizon or run on higher timeframes.

• Daily vs. Weekly : Daily for equities and crypto where month-end and turn-of-month effects matter; Weekly for futures and FX where day-of-week behavior is strong.

• Volatility scaling : Keep it on. Turn off only when you intentionally want a “pure seasonality” cone unaffected by current turbulence.

Workflow examples

• Swing continuation : Cone slopes up, price pulls into the lower inner band, your system fires. Enter near the band, stop just outside the outer line for the next 3–5 bars, target near the median or the opposite inner band.

• Fade extremes : Cone is flat or down, price gaps to the upper outer band on news, then stalls. Favor mean-reversion toward the median, size small if volatility scaling is elevated.

• Event play : Before CPI or earnings on a proxy index, check cone width. If the inner band is already wide, cut size or prefer options structures that benefit from range.

Good habits

• Pair the cone with your entry engine (breakout, pullback, order flow). Let Monte Carlo do range math; let your system do signal quality.

• Do not anchor blindly to the median; recalc after each bar. When the cone’s slope flips or width jumps, the plan should adapt.

• Validate seasonality for your symbol and timeframe; not every market has strong calendar effects.

Summary

The Seasonality Monte Carlo Forecaster wraps institutional risk planning into a single overlay: a data-driven seasonal drift, realistic volatility scaling, and a probabilistic cone that answers “where could we be, with what odds?” within your trading horizon. Use it to place stops where randomness is less likely to take you out, to set targets aligned with realistic travel, and to size positions with confidence born from distributions rather than hunches. It will not predict the future, but it will keep your decisions anchored to probabilities—the language markets actually speak.

US Macro Cycle (Z-Score Model)US Macro Cycle (Z-Score Model)

This indicator tracks the US economic cycle in real time using a weighted composite of seven macro and market-based indicators, each converted into a rolling Z-score for comparability. The model identifies the current phase of the cycle — Expansion, Peak, Contraction, or Recovery — and suggests sector tilts based on historical performance in each phase.

Core Components:

Yield Curve (10y–2y): Positive & steepening = growth; inverted = slowdown risk.

Credit Spreads (HYG/LQD): Tightening = risk-on; widening = risk-off.

Sector Leadership (Cyclicals vs. Defensives): Measures market leadership regime.

Copper/Gold Ratio: Higher copper = growth signal; higher gold = defensive.

SPY vs. 200-day MA: Equity trend strength.

SPY/IEF Ratio: Stocks vs. bonds relative strength.

VIX (Inverted): Low/falling volatility = supportive; high/rising = risk-off.

Methodology:

Each series is transformed into a rolling Z-score over the selected lookback period (optionally using median/MAD for robustness and winsorization to clip outliers).

Z-scores are combined using user-defined weights and normalized.

The smoothed composite is compared against phase thresholds to classify the macro environment.

Features:

Customizable Weights: Emphasize the indicators most relevant to your strategy.

Adjustable Thresholds: Fine-tune cycle phase definitions.

Background Coloring: Visual cue for the current phase.

Summary Table: Displays composite Z, confidence %, and individual Z-scores.

Alerts: Trigger when the phase changes, with details on the composite score and recommended tilt.

Use Cases:

Align sector rotation or relative strength strategies with the macro backdrop.

Identify favorable or defensive phases for tactical allocation.

Monitor macro turning points to manage portfolio risk.

It's doesn't fill nan gaps so there is quite a bit of zeroes, non-repainting.

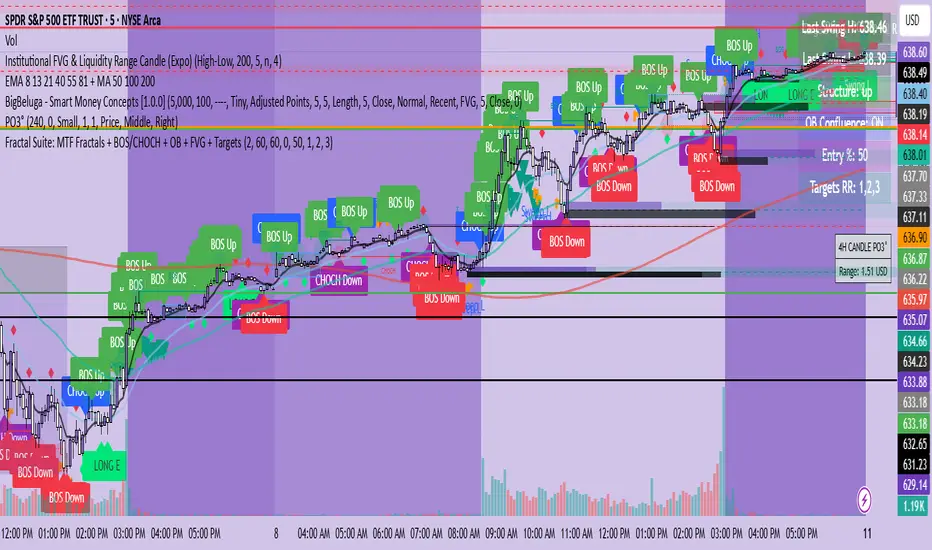

Fractal Suite: MTF Fractals + BOS/CHOCH + OB + FVG + Targets Kese Way

Fractals (Multi-Timeframe): Automatically detects both current-timeframe and higher-timeframe Bill Williams fractals, with customizable left/right bar settings.

Break of Structure (BOS) & CHoCH: Marks structural breaks and changes of character in real time.

Liquidity Sweeps: Identifies sweep patterns where price takes out a previous swing high/low but closes back within range.

Order Blocks (OB): Highlights the last opposite candle before a BOS, with customizable extension bars.

Fair Value Gaps (FVG): Finds 3-bar inefficiencies with a minimum size filter.

Confluence Zones: Optionally require OB–FVG overlap for high-probability setups.

Entry, Stop, and Targets: Automatically calculates entry price, stop loss, and up to three take-profit targets based on risk-reward ratios.

Visual Dashboard: Mini on-chart table summarizing structure, last swing points, and settings.

Alerts: Set alerts for new fractals, BOS events, and confluence-based trade setups.