ELC Indicator**ELC Indicator – Enigma Liquidity Concept**

The ELC Indicator is a cutting-edge tool designed for traders who want to leverage price action and liquidity concepts for high-precision trading opportunities. Unlike conventional indicators that rely purely on trend-following or oscillatory methods, ELC incorporates a unique combination of market structure, Fibonacci retracement levels, and dynamic EMA filtering to detect key buy and sell zones. This original approach helps traders capture the most relevant market movements and anticipate potential reversals with higher confidence.

---

### **What the ELC Indicator Does**

The primary goal of the ELC Indicator is to identify liquidity zones and plot Fibonacci-based levels around detected buy or sell signals. It continuously monitors price action to identify instances where significant liquidity grabs occur, signaled by breakouts beyond recent highs or lows. Once a signal is detected, the indicator plots horizontal lines at key Fibonacci ratios (0%, 25%, 50%, 75%, 100%, 120%, and 180%) to give traders a clear visual framework for potential retracement or extension levels.

Additionally, the indicator includes a dynamic EMA filter, which ensures that buy signals are only triggered when the price is above the EMA and sell signals when the price is below the EMA. This filtering mechanism helps reduce false signals in choppy markets and aligns trades with the broader trend direction.

---

### **Key Features**

1. **Buy & Sell Signals**

- Buy signals are generated when a liquidity grab occurs below the previous low, and the closing price is above the candle body midpoint and the EMA.

- Sell signals are triggered when a liquidity grab occurs above the previous high, and the closing price is below the candle body midpoint and the EMA.

- Visual cues are provided via small upward (green) and downward (red) triangles on the chart.

2. **Fibonacci Levels**

- For each buy or sell signal, the indicator plots multiple horizontal lines at key Fibonacci levels. These levels can help traders set realistic profit targets and stop-loss levels.

- The plotted lines can be customized in terms of style (solid, dotted, dashed) and color (buy and sell line colors).

3. **Dynamic EMA Filtering**

- A customizable EMA filter is integrated into the logic to align trades with the prevailing trend.

- The EMA length is adjustable, allowing traders to fine-tune the indicator based on their trading style and market conditions.

4. **Alert System**

- Alerts can be enabled for both buy and sell signals, ensuring traders never miss an opportunity even when away from the screen.

- Alerts are triggered once per bar, ensuring timely notifications without excessive noise.

5. **Customizable Signal Visibility**

- Traders can toggle the visibility of the last 9 buy and sell signals. When this option is disabled, only the most recent signal is displayed, helping to declutter the chart.

---

### **How to Use the ELC Indicator**

- **Trend Following**: The ELC Indicator works well in trending markets by filtering signals based on the EMA direction. Traders can use the plotted Fibonacci levels to enter trades, set profit targets, and manage risk.

- **Reversal Trading**: The liquidity grab detection mechanism allows traders to capture potential market reversals. By waiting for price retracements to key Fibonacci levels after a signal, traders can enter trades with a favorable risk-to-reward ratio.

- **Scalping & Day Trading**: With its ability to plot key intraday levels and generate real-time alerts, the ELC Indicator is particularly useful for scalpers and day traders looking to exploit short-term market inefficiencies.

---

### **Concepts Underlying the Calculations**

1. **Liquidity Grabs**: The ELC Indicator’s core logic is based on detecting instances where the market moves beyond a recent high or low, triggering a liquidity grab. This often signals a potential reversal or continuation, depending on broader market conditions.

2. **Fibonacci Ratios**: Once a signal is detected, key Fibonacci levels are plotted to provide traders with actionable zones for trade entries, profit targets, or stop-loss placements.

3. **EMA Filtering**: The EMA acts as a dynamic trend filter, ensuring that signals are aligned with the dominant market direction. This reduces the likelihood of entering trades against the prevailing trend.

---

### **Why ELC is Unique**

The ELC Indicator stands out by combining multiple powerful trading concepts—liquidity, Fibonacci ratios, and EMA filtering—into a single tool that provides actionable and visually intuitive information. Unlike traditional trend-following indicators that lag behind price action, ELC proactively identifies key market turning points based on liquidity events. Its customizable features, real-time alerts, and comprehensive plotting of Fibonacci levels make it a versatile tool for traders across various styles and timeframes.

Whether you're a scalper looking for intraday opportunities or a swing trader aiming to capture larger moves, the ELC Indicator offers a robust framework for identifying and executing high-probability trades.

---

### **How to Get Started**

1. Add the ELC Indicator to your chart.

2. Customize the EMA length, line colors, and style based on your preference.

3. Enable alerts to receive real-time notifications of buy and sell signals.

4. Use the plotted Fibonacci levels to plan your trade entries, profit targets, and stop-loss levels.

5. Combine the signals from ELC with your existing market analysis for optimal results.

---

This unique approach makes the ELC Indicator a valuable tool for traders seeking precision, clarity, and consistency in their trading decisions.

Search in scripts for "liquidity"

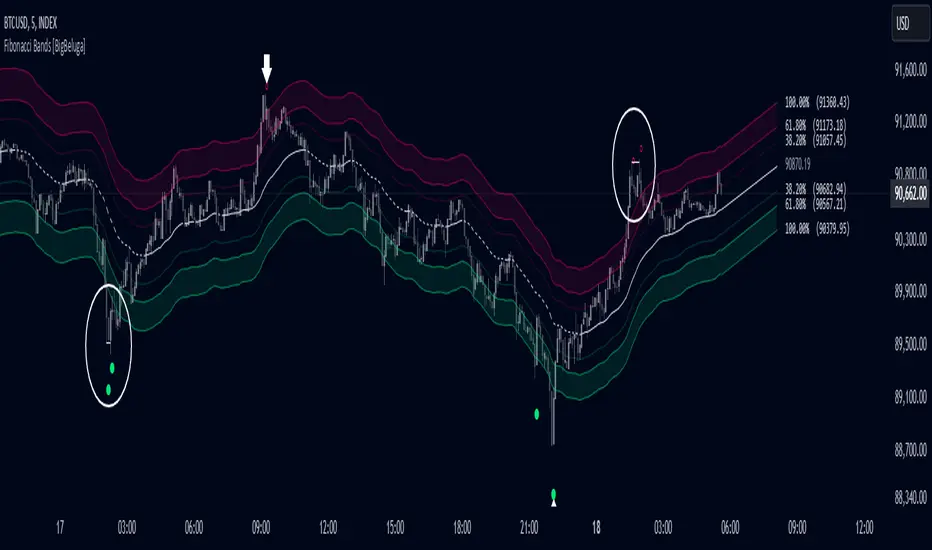

Fibonacci Bands [BigBeluga]The Fibonacci Band indicator is a powerful tool for identifying potential support, resistance, and mean reversion zones based on Fibonacci ratios. It overlays three sets of Fibonacci ratio bands (38.2%, 61.8%, and 100%) around a central trend line, dynamically adapting to price movements. This structure enables traders to track trends, visualize potential liquidity sweep areas, and spot reversal points for strategic entries and exits.

🔵 KEY FEATURES & USAGE

Fibonacci Bands for Support & Resistance:

The Fibonacci Band indicator applies three key Fibonacci ratios (38.2%, 61.8%, and 100%) to construct dynamic bands around a smoothed price. These levels often act as critical support and resistance areas, marked with labels displaying the percentage and corresponding price. The 100% band level is especially crucial, signaling potential liquidity sweep zones and reversal points.

Mean Reversion Signals at 100% Bands:

When price moves above or below the 100% band, the indicator generates mean reversion signals.

Trend Detection with Midline:

The central line acts as a trend-following tool: when solid, it indicates an uptrend, while a dashed line signals a downtrend. This adaptive midline helps traders assess the prevailing market direction while keeping the chart clean and intuitive.

Extended Price Projections:

All Fibonacci bands extend to future bars (default 30) to project potential price levels, providing a forward-looking perspective on where price may encounter support or resistance. This feature helps traders anticipate market structure in advance and set targets accordingly.

Liquidity Sweep:

--

-Liquidity Sweep at Previous Lows:

The price action moves below a previous low, capturing sell-side liquidity (stop-losses from long positions or entries for breakout traders).

The wick suggests that the price quickly reversed, leaving a failed breakout below support.

This is a classic liquidity grab, often indicating a bullish reversal .

-Liquidity Sweep at Previous Highs:

The price spikes above a prior high, sweeping buy-side liquidity (stop-losses from short positions or breakout entries).

The wick signifies rejection, suggesting a failed breakout above resistance.

This is a bearish liquidity sweep , often followed by a mean reversion or a downward move.

Display Customization:

To declutter the chart, traders can choose to hide Fibonacci levels and only display overbought/oversold zones along with the trend-following midline and mean reversion signals. This option enables a clearer focus on key reversal areas without additional distractions.

🔵 CUSTOMIZATION

Period Length: Adjust the length of the smoothed moving average for more reactive or smoother bands.

Channel Width: Customize the width of the Fibonacci channel.

Fibonacci Ratios: Customize the Fibonacci ratios to reflect personal preference or unique market behaviors.

Future Projection Extension: Set the number of bars to extend Fibonacci bands, allowing flexibility in projecting price levels.

Hide Fibonacci Levels: Toggle the visibility of Fibonacci levels for a cleaner chart focused on overbought/oversold regions and midline trend signals.

Liquidity Sweep: Toggle the visibility of Liquidity Sweep points

The Fibonacci Band indicator provides traders with an advanced framework for analyzing market structure, liquidity sweeps, and trend reversals. By integrating Fibonacci-based levels with trend detection and mean reversion signals, this tool offers a robust approach to navigating dynamic price action and finding high-probability trading opportunities.

Engulfing bar detectorHere’s the updated description with the added step about using Fibonacci levels across timeframes for confirmation:

Liquidity Engulfing Bar Detector

The **Liquidity Engulfing Bar Detector** is a powerful tool designed for traders who want to identify high-probability reversal patterns in the market based on liquidity grabbing and price action. This indicator highlights **Bullish Engulfing** and **Bearish Engulfing** bars that fulfill specific liquidity criteria, helping you spot potential trend reversals and trading opportunities.

**Features**:

1. **Bullish Engulfing Bars**:

- The current candle's low dips below the previous candle's low (grabs liquidity).

- The current candle closes above the previous candle's open.

- A green label is plotted above the engulfing bar for easy identification.

2. **Bearish Engulfing Bars**:

- The current candle's high exceeds the previous candle's high (grabs liquidity).

- The current candle closes below the previous candle's open.

- A red label is plotted below the engulfing bar for clear visibility.

3. **Customizable Alerts**:

- Receive instant notifications via TradingView alerts when a bullish or bearish engulfing pattern is detected.

- Alerts are fully customizable, allowing you to stay updated without actively monitoring the chart.

4. **Visual Markers**:

- Clear and intuitive labels make it easy to spot key patterns directly on your chart.

- Fully integrated with any timeframe and market, ensuring versatility for all trading styles.

---

### **How to Use**:

1. **Add the Indicator**:

- Apply the Liquidity Engulfing Bar Detector to your chart to automatically highlight bullish and bearish engulfing bars.

2. **Enable Alerts**:

- Set up TradingView alerts to get notified of potential setups in real-time.

3. **Analyze with Fibonacci Levels**:

- Draw a Fibonacci retracement tool over the identified engulfing bar, from its low to its high (for bullish patterns) or high to low (for bearish patterns).

- Use the following Fibonacci levels as key zones of interest:

- **0.0 (start)**, **0.25**, **0.5 (midpoint)**, **0.75**, and **1.0 (end)**.

- These levels often act as critical support or resistance zones for price action.

4. **Use Multi-Timeframe Confirmation**:

- Validate zones from higher timeframes using lower timeframe candles:

- **1-minute candles** for confirming zones on the **15-minute chart**.

- **5-minute candles** for confirming zones on the **1-hour chart**.

- **15-minute candles** for confirming zones on the **4-hour chart**.

- This approach ensures precision in your entry points and aligns intraday movements with higher timeframe setups.

5. **Integrate with Your Strategy**:

- Combine the indicator with other tools (e.g., trendlines, moving averages, or volume analysis) for confirmation.

- Use proper risk management to maximize your trading edge.

---

### **Why Use This Indicator?**

Liquidity grabs often signal the participation of major market players, which can lead to significant reversals or continuations. By combining liquidity concepts with engulfing bar patterns and Fibonacci analysis, this indicator helps you:

- Identify key market turning points.

- Improve your entries and exits with multi-timeframe precision.

- Enhance your trading strategy with an edge rooted in smart money concepts.

---

**Note**: This indicator is best used with proper risk management and alongside other technical or fundamental analyses.

---

Let me know if there's anything more you'd like to include!

Custom V2 KillZone US / FVG / EMAThis indicator is designed for traders looking to analyze liquidity levels, opportunity zones, and the underlying trend across different trading sessions. Inspired by the ICT methodology, this tool combines analysis of Exponential Moving Averages (EMA), session management, and Fair Value Gap (FVG) detection to provide a structured and disciplined approach to trading effectively.

Indicator Features

Identifying the Underlying Trend with Two EMAs

The indicator uses two EMAs on different, customizable timeframes to define the underlying trend:

EMA1 (default set to a daily timeframe): Represents the primary underlying trend.

EMA2 (default set to a 4-hour timeframe): Helps identify secondary corrections or impulses within the main trend.

These two EMAs allow traders to stay aligned with the market trend by prioritizing trades in the direction of the moving averages. For example, if prices are above both EMAs, the trend is bullish, and long trades are favored.

Analysis of Market Sessions

The indicator divides the day into key trading sessions:

Asian Session

London Session

US Pre-Open Session

Liquidity Kill Session

US Kill Zone Session

Each session is represented by high and low zones as well as mid-lines, allowing traders to visualize liquidity levels reached during these periods. Tracking the price levels in different sessions helps determine whether liquidity levels have been "swept" (taken) or not, which is essential for ICT methodology.

Liquidity Signal ("OK" or "STOP")

A specific signal appears at the end of the "Liquidity Kill" session (just before the "US Kill Zone" session):

"OK" Signal: Indicates that liquidity conditions are favorable for trading the "US Kill Zone" session. This means that liquidity levels have been swept in previous sessions (Asian, London, US Pre-Open), and the market is ready for an opportunity.

"STOP" Signal: Indicates that it is not favorable to trade the "US Kill Zone" session, as certain liquidity conditions have not been met.

The "OK" or "STOP" signal is based on an analysis of the high and low levels from previous sessions, allowing traders to ensure that significant liquidity zones have been reached before considering positions in the "Kill Zone".

Detection of Fair Value Gaps (FVG) in the US Kill Zone Session

When an "OK" signal is displayed, the indicator identifies Fair Value Gaps (FVG) during the "US Kill Zone" session. These FVGs are areas where price may return to fill an "imbalance" in the market, making them potential entry points.

Bullish FVG: Detected when there is a bullish imbalance, providing a buying opportunity if conditions align with the underlying trend.

Bearish FVG: Detected when there is a bearish imbalance, providing a selling opportunity in the trend direction.

FVG detection aligns with the ICT Silver Bullet methodology, where these imbalance zones serve as probable entry points during the "US Kill Zone".

How to Use This Indicator

Check the Underlying Trend

Before trading, observe the two EMAs (daily and 4-hour) to understand the general market trend. Trades will be prioritized in the direction indicated by these EMAs.

Monitor Liquidity Signals After the Asian, London, and US Pre-Open Sessions

The high and low levels of each session help determine if liquidity has already been swept in these areas. At the end of the "Liquidity Kill" session, an "OK" or "STOP" label will appear:

"OK" means you can look for trading opportunities in the "US Kill Zone" session.

"STOP" means it is preferable not to take trades in the "US Kill Zone" session.

Look for Opportunities in the US Kill Zone if the Signal is "OK"

When the "OK" label is present, focus on the "US Kill Zone" session. Use the Fair Value Gaps (FVG) as potential entry points for trades based on the ICT methodology. The identified FVGs will appear as colored boxes (bullish or bearish) during this session.

Use ICT Methodology to Manage Your Trades

Follow the FVGs as potential reversal zones in the direction of the trend, and manage your positions according to your personal strategy and the rules of the ICT Silver Bullet method.

Customizable Settings

The indicator includes several customization options to suit the trader's preferences:

EMA: Length, source (close, open, etc.), and timeframe.

Market Sessions: Ability to enable or disable each session, with color and line width settings.

Liquidity Signals: Customization of colors for the "OK" and "STOP" labels.

FVG: Option to display FVGs or not, with customizable colors for bullish and bearish FVGs, and the number of bars for FVG extension.

-------------------------------------------------------------------------------------------------------------

Cet indicateur est conçu pour les traders souhaitant analyser les niveaux de liquidité, les zones d’opportunité, et la tendance de fond à travers différentes sessions de trading. Inspiré de la méthodologie ICT, cet outil combine l'analyse des moyennes mobiles exponentielles (EMA), la gestion des sessions de marché, et la détection des Fair Value Gaps (FVG), afin de fournir une approche structurée et disciplinée pour trader efficacement.

ICT Master Suite [Trading IQ]Hello Traders!

We’re excited to introduce the ICT Master Suite by TradingIQ, a new tool designed to bring together several ICT concepts and strategies in one place.

The Purpose Behind the ICT Master Suite

There are a few challenges traders often face when using ICT-related indicators:

Many available indicators focus on one or two ICT methods, which can limit traders who apply a broader range of ICT related techniques on their charts.

There aren't many indicators for ICT strategy models, and we couldn't find ICT indicators that allow for testing the strategy models and setting alerts.

Many ICT related concepts exist in the public domain as indicators, not strategies! This makes it difficult to verify that the ICT concept has some utility in the market you're trading and if it's worth trading - it's difficult to know if it's working!

Some users might not have enough chart space to apply numerous ICT related indicators, which can be restrictive for those wanting to use multiple ICT techniques simultaneously.

The ICT Master Suite is designed to offer a comprehensive option for traders who want to apply a variety of ICT methods. By combining several ICT techniques and strategy models into one indicator, it helps users maximize their chart space while accessing multiple tools in a single slot.

Additionally, the ICT Master Suite was developed as a strategy . This means users can backtest various ICT strategy models - including deep backtesting. A primary goal of this indicator is to let traders decide for themselves what markets to trade ICT concepts in and give them the capability to figure out if the strategy models are worth trading!

What Makes the ICT Master Suite Different

There are many ICT-related indicators available on TradingView, each offering valuable insights. What the ICT Master Suite aims to do is bring together a wider selection of these techniques into one tool. This includes both key ICT methods and strategy models, allowing traders to test and activate strategies all within one indicator.

Features

The ICT Master Suite offers:

Multiple ICT strategy models, including the 2022 Strategy Model and Unicorn Model, which can be built, tested, and used for live trading.

Calculation and display of key price areas like Breaker Blocks, Rejection Blocks, Order Blocks, Fair Value Gaps, Equal Levels, and more.

The ability to set alerts based on these ICT strategies and key price areas.

A comprehensive, yet practical, all-inclusive ICT indicator for traders.

Customizable Timeframe - Calculate ICT concepts on off-chart timeframes

Unicorn Strategy Model

2022 Strategy Model

Liquidity Raid Strategy Model

OTE (Optimal Trade Entry) Strategy Model

Silver Bullet Strategy Model

Order blocks

Breaker blocks

Rejection blocks

FVG

Strong highs and lows

Displacements

Liquidity sweeps

Power of 3

ICT Macros

HTF previous bar high and low

Break of Structure indications

Market Structure Shift indications

Equal highs and lows

Swings highs and swing lows

Fibonacci TPs and SLs

Swing level TPs and SLs

Previous day high and low TPs and SLs

And much more! An ongoing project!

How To Use

Many traders will already be familiar with the ICT related concepts listed above, and will find using the ICT Master Suite quite intuitive!

Despite this, let's go over the features of the tool in-depth and how to use the tool!

The image above shows the ICT Master Suite with almost all techniques activated.

ICT 2022 Strategy Model

The ICT Master suite provides the ability to test, set alerts for, and live trade the ICT 2022 Strategy Model.

The image above shows an example of a long position being entered following a complete setup for the 2022 ICT model.

A liquidity sweep occurs prior to an upside breakout. During the upside breakout the model looks for the FVG that is nearest 50% of the setup range. A limit order is placed at this FVG for entry.

The target entry percentage for the range is customizable in the settings. For instance, you can select to enter at an FVG nearest 33% of the range, 20%, 66%, etc.

The profit target for the model generally uses the highest high of the range (100%) for longs and the lowest low of the range (100%) for shorts. Stop losses are generally set at 0% of the range.

The image above shows the short model in action!

Whether you decide to follow the 2022 model diligently or not, you can still set alerts when the entry condition is met.

ICT Unicorn Model

The image above shows an example of a long position being entered following a complete setup for the ICT Unicorn model.

A lower swing low followed by a higher swing high precedes the overlap of an FVG and breaker block formed during the sequence.

During the upside breakout the model looks for an FVG and breaker block that formed during the sequence and overlap each other. A limit order is placed at the nearest overlap point to current price.

The profit target for this example trade is set at the swing high and the stop loss at the swing low. However, both the profit target and stop loss for this model are configurable in the settings.

For Longs, the selectable profit targets are:

Swing High

Fib -0.5

Fib -1

Fib -2

For Longs, the selectable stop losses are:

Swing Low

Bottom of FVG or breaker block

The image above shows the short version of the Unicorn Model in action!

For Shorts, the selectable profit targets are:

Swing Low

Fib -0.5

Fib -1

Fib -2

For Shorts, the selectable stop losses are:

Swing High

Top of FVG or breaker block

The image above shows the profit target and stop loss options in the settings for the Unicorn Model.

Optimal Trade Entry (OTE) Model

The image above shows an example of a long position being entered following a complete setup for the OTE model.

Price retraces either 0.62, 0.705, or 0.79 of an upside move and a trade is entered.

The profit target for this example trade is set at the -0.5 fib level. This is also adjustable in the settings.

For Longs, the selectable profit targets are:

Swing High

Fib -0.5

Fib -1

Fib -2

The image above shows the short version of the OTE Model in action!

For Shorts, the selectable profit targets are:

Swing Low

Fib -0.5

Fib -1

Fib -2

Liquidity Raid Model

The image above shows an example of a long position being entered following a complete setup for the Liquidity Raid Modell.

The user must define the session in the settings (for this example it is 13:30-16:00 NY time).

During the session, the indicator will calculate the session high and session low. Following a “raid” of either the session high or session low (after the session has completed) the script will look for an entry at a recently formed breaker block.

If the session high is raided the script will look for short entries at a bearish breaker block. If the session low is raided the script will look for long entries at a bullish breaker block.

For Longs, the profit target options are:

Swing high

User inputted Lib level

For Longs, the stop loss options are:

Swing low

User inputted Lib level

Breaker block bottom

The image above shows the short version of the Liquidity Raid Model in action!

For Shorts, the profit target options are:

Swing Low

User inputted Lib level

For Shorts, the stop loss options are:

Swing High

User inputted Lib level

Breaker block top

Silver Bullet Model

The image above shows an example of a long position being entered following a complete setup for the Silver Bullet Modell.

During the session, the indicator will determine the higher timeframe bias. If the higher timeframe bias is bullish the strategy will look to enter long at an FVG that forms during the session. If the higher timeframe bias is bearish the indicator will look to enter short at an FVG that forms during the session.

For Longs, the profit target options are:

Nearest Swing High Above Entry

Previous Day High

For Longs, the stop loss options are:

Nearest Swing Low

Previous Day Low

The image above shows the short version of the Silver Bullet Model in action!

For Shorts, the profit target options are:

Nearest Swing Low Below Entry

Previous Day Low

For Shorts, the stop loss options are:

Nearest Swing High

Previous Day High

Order blocks

The image above shows indicator identifying and labeling order blocks.

The color of the order blocks, and how many should be shown, are configurable in the settings!

Breaker Blocks

The image above shows indicator identifying and labeling order blocks.

The color of the breaker blocks, and how many should be shown, are configurable in the settings!

Rejection Blocks

The image above shows indicator identifying and labeling rejection blocks.

The color of the rejection blocks, and how many should be shown, are configurable in the settings!

Fair Value Gaps

The image above shows indicator identifying and labeling fair value gaps.

The color of the fair value gaps, and how many should be shown, are configurable in the settings!

Additionally, you can select to only show fair values gaps that form after a liquidity sweep. Doing so reduces "noisy" FVGs and focuses on identifying FVGs that form after a significant trading event.

The image above shows the feature enabled. A fair value gap that occurred after a liquidity sweep is shown.

Market Structure

The image above shows the ICT Master Suite calculating market structure shots and break of structures!

The color of MSS and BoS, and whether they should be displayed, are configurable in the settings.

Displacements

The images above show indicator identifying and labeling displacements.

The color of the displacements, and how many should be shown, are configurable in the settings!

Equal Price Points

The image above shows the indicator identifying and labeling equal highs and equal lows.

The color of the equal levels, and how many should be shown, are configurable in the settings!

Previous Custom TF High/Low

The image above shows the ICT Master Suite calculating the high and low price for a user-defined timeframe. In this case the previous day’s high and low are calculated.

To illustrate the customizable timeframe function, the image above shows the indicator calculating the previous 4 hour high and low.

Liquidity Sweeps

The image above shows the indicator identifying a liquidity sweep prior to an upside breakout.

The image above shows the indicator identifying a liquidity sweep prior to a downside breakout.

The color and aggressiveness of liquidity sweep identification are adjustable in the settings!

Power Of Three

The image above shows the indicator calculating Po3 for two user-defined higher timeframes!

Macros

The image above shows the ICT Master Suite identifying the ICT macros!

ICT Macros are only displayable on the 5 minute timeframe or less.

Strategy Performance Table

In addition to a full-fledged TradingView backtest for any of the ICT strategy models the indicator offers, a quick-and-easy strategy table exists for the indicator!

The image above shows the strategy performance table in action.

Keep in mind that, because the ICT Master Suite is a strategy script, you can perform fully automatic backtests, deep backtests, easily add commission and portfolio balance and look at pertinent metrics for the ICT strategies you are testing!

Lite Mode

Traders who want the cleanest chart possible can toggle on “Lite Mode”!

In Lite Mode, any neon or “glow” like effects are removed and key levels are marked as strict border boxes. You can also select to remove box borders if that’s what you prefer!

Settings Used For Backtest

For the displayed backtest, a starting balance of $1000 USD was used. A commission of 0.02%, slippage of 2 ticks, a verify price for limit orders of 2 ticks, and 5% of capital investment per order.

A commission of 0.02% was used due to the backtested asset being a perpetual future contract for a crypto currency. The highest commission (lowest-tier VIP) for maker orders on many exchanges is 0.02%. All entered positions take place as maker orders and so do profit target exits. Stop orders exist as stop-market orders.

A slippage of 2 ticks was used to simulate more realistic stop-market orders. A verify limit order settings of 2 ticks was also used. Even though BTCUSDT.P on Binance is liquid, we just want the backtest to be on the safe side. Additionally, the backtest traded 100+ trades over the period. The higher the sample size the better; however, this example test can serve as a starting point for traders interested in ICT concepts.

Community Assistance And Feedback

Given the complexity and idiosyncratic applications of ICT concepts amongst its proponents, the ICT Master Suite’s built-in strategies and level identification methods might not align with everyone's interpretation.

That said, the best we can do is precisely define ICT strategy rules and concepts to a repeatable process, test, and apply them! Whether or not an ICT strategy is trading precisely how you would trade it, seeing the model in action, taking trades, and with performance statistics is immensely helpful in assessing predictive utility.

If you think we missed something, you notice a bug, have an idea for strategy model improvement, please let us know! The ICT Master Suite is an ongoing project that will, ideally, be shaped by the community.

A big thank you to the @PineCoders for their Time Library!

Thank you!

Price Action Analyst [OmegaTools]Price Action Analyst (PAA) is an advanced trading tool designed to assist traders in identifying key price action structures such as order blocks, market structure shifts, liquidity grabs, and imbalances. With its fully customizable settings, the script offers both novice and experienced traders insights into potential market movements by visually highlighting premium/discount zones, breakout signals, and significant price levels.

This script utilizes complex logic to determine significant price action patterns and provides dynamic tools to spot strong market trends, liquidity pools, and imbalances across different timeframes. It also integrates an internal backtesting function to evaluate win rates based on price interactions with supply and demand zones.

The script combines multiple analysis techniques, including market structure shifts, order block detection, fair value gaps (FVG), and ICT bias detection, to provide a comprehensive and holistic market view.

Key Features:

Order Block Detection: Automatically detects order blocks based on price action and strength analysis, highlighting potential support/resistance zones.

Market Structure Analysis: Tracks internal and external market structure changes with gradient color-coded visuals.

Liquidity Grabs & Breakouts: Detects potential liquidity grab and breakout areas with volume confirmation.

Fair Value Gaps (FVG): Identifies bullish and bearish FVGs based on historical price action and threshold calculations.

ICT Bias: Integrates ICT bias analysis, dynamically adjusting based on higher-timeframe analysis.

Supply and Demand Zones: Highlights supply and demand zones using customizable colors and thresholds, adjusting dynamically based on market conditions.

Trend Lines: Automatically draws trend lines based on significant price pivots, extending them dynamically over time.

Backtesting: Internal backtesting engine to calculate the win rate of signals generated within supply and demand zones.

Percentile-Based Pricing: Plots key percentile price levels to visualize premium, fair, and discount pricing zones.

High Customizability: Offers extensive user input options for adjusting zone detection, color schemes, and structure analysis.

User Guide:

Order Blocks: Order blocks are significant support or resistance zones where strong buyers or sellers previously entered the market. These zones are detected based on pivot points and engulfing price action. The strength of each block is determined by momentum, volume, and liquidity confirmations.

Demand Zones: Displayed in shades of blue based on their strength. The darker the color, the stronger the zone.

Supply Zones: Displayed in shades of red based on their strength. These zones highlight potential resistance areas.

The zones will dynamically extend as long as they remain valid. Users can set a maximum number of order blocks to be displayed.

Market Structure: Market structure is classified into internal and external shifts. A bullish or bearish market structure break (MSB) occurs when the price moves past a previous high or low. This script tracks these breaks and plots them using a gradient color scheme:

Internal Structure: Short-term market structure, highlighting smaller movements.

External Structure: Long-term market shifts, typically more significant.

Users can choose how they want the structure to be visualized through the "Market Structure" setting, choosing from different visual methods.

Liquidity Grabs: The script identifies liquidity grabs (false breakouts designed to trap traders) by monitoring price action around highs and lows of previous bars. These are represented by diamond shapes:

Liquidity Buy: Displayed below bars when a liquidity grab occurs near a low.

Liquidity Sell: Displayed above bars when a liquidity grab occurs near a high.

Breakouts: Breakouts are detected based on strong price momentum beyond key levels:

Breakout Buy: Triggered when the price closes above the highest point of the past 20 bars with confirmation from volume and range expansion.

Breakout Sell: Triggered when the price closes below the lowest point of the past 20 bars, again with volume and range confirmation.

Fair Value Gaps (FVG): Fair value gaps (FVGs) are periods where the price moves too quickly, leaving an unbalanced market condition. The script identifies these gaps:

Bullish FVG: When there is a gap between the low of two previous bars and the high of a recent bar.

Bearish FVG: When a gap occurs between the high of two previous bars and the low of the recent bar.

FVGs are color-coded and can be filtered by their size to focus on more significant gaps.

ICT Bias: The script integrates the ICT methodology by offering an auto-calculated higher-timeframe bias:

Long Bias: Suggests the market is in an uptrend based on higher timeframe analysis.

Short Bias: Indicates a downtrend.

Neutral Bias: Suggests no clear directional bias.

Trend Lines: Automatic trend lines are drawn based on significant pivot highs and lows. These lines will dynamically adjust based on price movement. Users can control the number of trend lines displayed and extend them over time to track developing trends.

Percentile Pricing: The script also plots the 25th percentile (discount zone), 75th percentile (premium zone), and a fair value price. This helps identify whether the current price is overbought (premium) or oversold (discount).

Customization:

Zone Strength Filter: Users can set a minimum strength threshold for order blocks to be displayed.

Color Customization: Users can choose colors for demand and supply zones, market structure, breakouts, and FVGs.

Dynamic Zone Management: The script allows zones to be deleted after a certain number of bars or dynamically adjusts zones based on recent price action.

Max Zone Count: Limits the number of supply and demand zones shown on the chart to maintain clarity.

Backtesting & Win Rate: The script includes a backtesting engine to calculate the percentage of respect on the interaction between price and demand/supply zones. Results are displayed in a table at the bottom of the chart, showing the percentage rating for both long and short zones. Please note that this is not a win rate of a simulated strategy, it simply is a measure to understand if the current assets tends to respect more supply or demand zones.

How to Use:

Load the script onto your chart. The default settings are optimized for identifying key price action zones and structure on intraday charts of liquid assets.

Customize the settings according to your strategy. For example, adjust the "Max Orderblocks" and "Strength Filter" to focus on more significant price action areas.

Monitor the liquidity grabs, breakouts, and FVGs for potential trade opportunities.

Use the bias and market structure analysis to align your trades with the prevailing market trend.

Refer to the backtesting win rates to evaluate the effectiveness of the zones in your trading.

Terms & Conditions:

By using this script, you agree to the following terms:

Educational Purposes Only: This script is provided for informational and educational purposes and does not constitute financial advice. Use at your own risk.

No Warranty: The script is provided "as-is" without any guarantees or warranties regarding its accuracy or completeness. The creator is not responsible for any losses incurred from the use of this tool.

Open-Source License: This script is open-source and may be modified or redistributed in accordance with the TradingView open-source license. Proper credit to the original creator, OmegaTools, must be maintained in any derivative works.

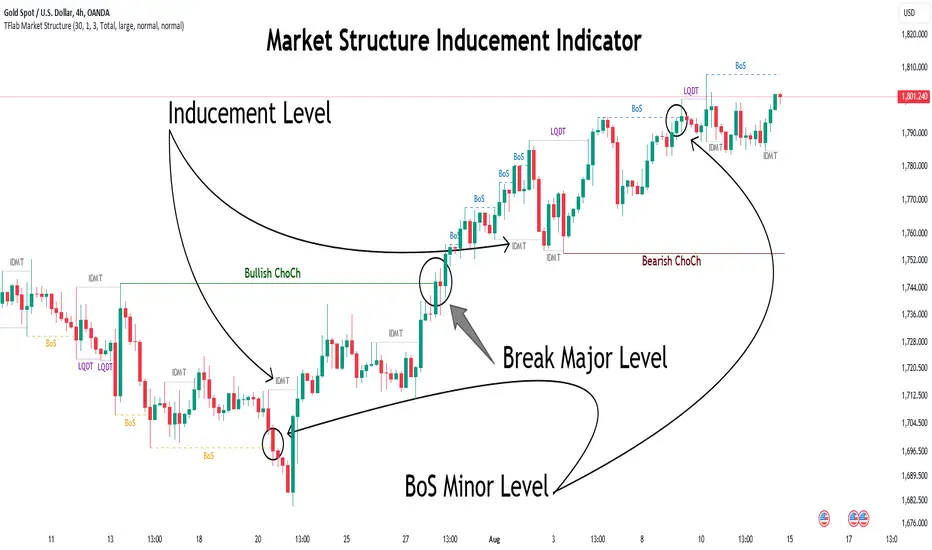

Market Structure Inducements ICT [TradinFinder] CHoch BOS Sweeps🔵 Introduction

Market Structure is the foundation for identifying trends in the market, crucial in technical analysis and strategies like ICT and SMC. Understanding key concepts such as Break of Structure (BOS) and Change of Character (CHOCH) helps traders recognize critical shifts in the market. BOS, referring to a Market Structure Change (BMS), and CHOCH or Market Structure Shift (MSS) signal trend reversals in the market.

Additionally, the concept of Inducement, a vital tool in Smart Money strategies, allows traders to avoid price traps. Identifying valid pullback, valid inducement, POI, and Liquidity Grab helps traders find optimal entry and exit points and leverage Smart Money movements effectively.

Bullish Market Structure :

Bearish Market Structure :

🔵 How to Use

The Market Structure indicator is designed to help traders better understand market structure and detect price traps. By using this indicator, you can identify the right entry and exit points based on structural changes in the market and avoid unprofitable trades. Below, we explain the key concepts and how to apply them in trading.

🟣 Market Structure

Market Structure refers to the overall pattern of price movement in the market. Using this indicator, traders can identify uptrends and downtrends and make better trading decisions based on changes in market structure. The two key concepts here are Break of Structure (BOS) and Change of Character (CHOCH).

Change of Character (CHOCH) : CHOCH occurs when the market shifts from an uptrend to a downtrend or vice versa. These changes typically indicate a broader trend reversal, and the indicator assists you in identifying them accurately.

Break of Structure (BOS) : When the market breaks a key support or resistance level, it signals a change in market structure. This indicator helps you identify these breakouts in time and take advantage of trading opportunities.

🟣 Inducement

Inducement refers to price traps set by Smart Money to trick retail traders into making the wrong trades. This indicator helps you recognize these traps and avoid unprofitable trades.

Valid Inducement : Valid Inducement refers to deliberately created price traps by major market players to gather liquidity from retail traders. Once the market has collected sufficient liquidity, it makes the real move, and professional traders use this moment to enter.

🟣 Valid Pullback

A Valid Pullback refers to a temporary market retracement, indicating a price correction within the main trend. This concept is crucial in technical analysis as it helps traders enter trades at the right time and profit from the continuation of the trend. The Market Structure indicator can identify these valid retracements, allowing traders to enter trades with greater confidence.

🟣 Point of Interest (POI)

Another important concept in market analysis is the Point of Interest (POI), referring to key price areas on the chart. POI includes zones where significant price movements are likely to occur. The Market Structure indicator helps you locate these key points and use them as entry signals for trades.

🟣 Liquidity Grab

Liquidity Grab refers to a scenario where the market intentionally moves to areas where retail traders' stop losses are placed. The goal is to gather liquidity, allowing major players to execute trades at better prices. By using this indicator, you can spot these liquidity grabs and avoid falling into price traps.

🔵 Setting

ChoCh Detector Period : The period of identifying the major market levels that occur when they break ChoCh.

BoS & Liquidity Detector Period : The period of identifying minor levels, which are used to identify BoS and Liquidity levels.

Inducement Detector Period : The period of identification of Inducement levels.

Fast Trend Detector : This feature will help you update the major market structure levels sooner.

Inducement Type Detector : Two modes "Sweeps" and "Total" can be used to identify the levels of Inducement. In "Sweeps" mode only Levels detected by touch shadow. In "Total" mode, all Levels are detected.

🔵 Conclusion

In financial market analysis and forex trading, identifying Market Structure and Inducement is crucial. Market Structure helps you detect uptrends and downtrends, and understand Break of Structure (BOS) and Change of Character (CHOCH). The concept of Inducement also enables traders to spot Smart Money price traps and avoid unprofitable trades.

The Market Structure indicator is a powerful tool that, by analyzing the market structure and concepts like valid pullback and valid inducement, helps you make more precise trade entries. Additionally, by identifying POI and Liquidity Grab, the indicator gives you the ability to spot key market zones and use them to your advantage in trading.

LIT - Timings Fx MartinThe Asia Liquidity Points Indicator is a powerful tool designed for traders to identify key liquidity points during the Asia trading session. This script is tailored specifically to aid traders in capitalizing on the unique characteristics of Asian markets, providing invaluable insights into liquidity zones that can significantly enhance trading decisions.

Key Features:

Asia Session Focus: The indicator focuses exclusively on the Asia trading session, which encompasses the trading activity primarily in the Asian markets such as Tokyo, Hong Kong, Singapore, and others.

Liquidity Zones Identification: The script utilizes advanced algorithms to identify and map out liquidity zones within the Asia trading session. These zones represent areas where significant buying or selling pressure is likely to occur, thus presenting lucrative trading opportunities.

Customizable Parameters: Traders have the flexibility to customize various parameters such as time frame, sensitivity, and display options to suit their trading preferences and strategies.

Visual Alerts: The indicator provides visual alerts on the trading chart, clearly indicating the location and strength of liquidity points. This feature enables traders to quickly identify potential entry or exit points based on the liquidity dynamics in the market.

Real-Time Updates: The script continuously monitors market activity during the Asia session, providing real-time updates on liquidity points as they evolve. This ensures traders stay informed and adaptable to changing market conditions.

Integration with Trading Strategies: The Asia Liquidity Points Indicator seamlessly integrates with various trading strategies, serving as a valuable tool for both discretionary and algorithmic traders. Whether used in isolation or in combination with other technical analysis tools, this indicator can enhance trading performance and profitability.

User-Friendly Interface: The indicator boasts a user-friendly interface, making it accessible to traders of all levels of experience. Whether you are a novice trader or a seasoned professional, you can easily incorporate this tool into your trading arsenal.

In conclusion, the Asia Liquidity Points Indicator offers traders a strategic advantage in navigating the nuances of the Asia trading session. By identifying key liquidity zones and providing real-time insights, this script empowers traders to make informed decisions and capitalize on lucrative trading opportunities in the dynamic Asian markets.

ICT - GAPs and Volume Imbalance

GAPs

Gaps are areas on chart where the price have moved sharply up or down, with no trading in between. Gaps often fill, but they don't have to.

Volume Imbalance

Volume imbalance - determined using 2 candles

Bullish Volume Imbalance - area between the close of 1st candle and the open of 2nd candle

Bearish Volume Imbalance - area between the close of 1st candle and the open of 2nd candle

How to use the indicator:-

When you find imbalance in volume or a GAP in the chart, you may expect price to rebalance it before continuation.

Importantly, GAPs/Imbalances do not always fill. Traders should never assume that a gap/imbalance will fill without understanding the reasons for the gap and monitoring trading activity around the gap.

Pair it with your current bias for better results.

FX Mini-Day/Index Dividers V2This is a combination of the Mini-Day Separator Indicator, timings based off the research by Tom Henstridge/@LiquiditySniper and additional Index KZ delineations, based on ICT's 2022 Youtube Mentorship.

*It borrows some minor code from Enricoamato997 . Credit where it is due!

This is a joint effort by myself, @vbwilkes / Offseason Vince and @Tom_FOREX / TraderTom on the Index/Index Future portion.

Index Future Example

Forex Example

X-Trend Macro Command CenterX-Trend Macro Command Center (MCC) | Institutional Grade Dashboard

📝 Description Body

The Invisible Engine of the Market Revealed.

Traders often focus solely on Price Action, ignoring the massive underwater currents that actually drive trends: Global Liquidity, Inflation, and Central Bank Policy. We created X-Trend Macro Command Center (MCC) to solve this problem.

This is not just an indicator. It is a fundamental heads-up display that bridges the gap between technical charts and macroeconomic reality.

💡 The Idea & Philosophy

Markets don't move in a vacuum. Bull runs are fueled by M2 Money Supply expansion and negative real yields. Crashes are triggered by liquidity crunches and aggressive rate hikes. X-Trend MCC was built to give retail traders the same "Macro Awareness" that institutional desks possess. It aggregates fragmented economic data from Federal Reserve databases (FRED) directly onto your chart in real-time.

🚀 Application & Logic

This tool is designed for Trend Traders, Crypto Investors, and Macro Analysts.

Identify the Regime: Instantly see if the environment is "RISK ON" (High Liquidity, Low Real Rates) or "RISK OFF" (Monetary Tightening).

Validate the Trend: Don't buy the dip if Liquidity (M2) is crashing. Don't short the rally if Real Yields are negative.

Multi-Region Analysis: Switch instantly between economic powerhouses (US, China, Japan) to see where the capital is flowing.

📊 Dashboard Metrics Explained

Every row in the Command Center tells a specific story about the economy:

Interest Rate: The "Gravity" of finance. Higher rates weigh down risk assets (Stocks/Crypto).

Inflation (YoY): The erosion of purchasing power. We calculate this dynamically based on CPI data.

Real Yield (The "Golden" Metric): Calculated as Interest Rate - Inflation.

Green: Real Yield is low/negative. Cash is trash, assets fly.

Red: Real Yield is high. Cash is King, assets struggle.

US Debt & GDP: Fiscal health indicators formatted in Trillions ($T). Watch the Debt-to-GDP ratio—if it spikes >120%, expect currency debasement.

M2 Money Supply: The fuel tank of the market. Tracks the total amount of money in circulation.

↗ Trend: Liquidity is entering the system (Bullish).

↘ Trend: Liquidity is drying up (Bearish).

🧩 The X-Trend Ecosystem

X-Trend MCC is just the tip of the iceberg. This module is part of the larger X-Trend Project — a comprehensive suite of algorithmic tools being developed to quantify market chaos. While our Price Action algorithms (Lite/Pro/Ultra) handle the Micro, the MCC handles the Macro.

Technical Note:

Data Sources: Direct connection to FRED (Federal Reserve Economic Data).

Zero Repainting: Historical data is requested strictly using closed bars to ensure accuracy.

Open Source: We believe in transparency. The code is open for study under MPL 2.0.

Build by Dev0880 | X-Trend © 2025

UK100 London Judas & IFVG SetupUK100 London Judas & IFVG Setup

Overview This indicator is a specialized trading tool designed to automate the ICT Judas Swing strategy specifically for the UK100 (FTSE 100) index during the London Market Open. It combines institutional time-based logic with price action confirmation using Inversion Fair Value Gaps (IFVG) to identify high-probability reversal setups.

How It Works The strategy is based on the concept that the initial move after the London Open is often a "fake-out" (manipulation) designed to trap retail traders and engineer liquidity before the true trend of the day begins.

Session & Opening Price:

The script marks the London Open price (default 09:00 Warsaw / 08:00 London time) with a dashed line.

This serves as the "line in the sand." Prices moving away from this line initially are monitored for manipulation.

Judas Swing (Liquidity Sweep):

If price moves BELOW the open, it is hunting Sell-Side Liquidity (trapping sellers).

If price moves ABOVE the open, it is hunting Buy-Side Liquidity (trapping buyers).

The Entry Trigger: Inversion FVG (IFVG):

The indicator scans for Fair Value Gaps (FVG) created during the manipulation phase.

BUY Signal: The price manipulates lower, creates a Bearish FVG (Red Box), but then aggressively reverses and closes ABOVE that gap. The gap is now "Inverted" (turns Green), acting as support.

SELL Signal: The price manipulates higher, creates a Bullish FVG (Green Box), but then aggressively reverses and closes BELOW that gap. The gap is now "Inverted" (turns Orange), acting as resistance.

Key Features

Automated Pattern Recognition: No need to manually draw gaps. The script detects valid FVG inversions that align with the Judas Swing logic.

Built-in Risk Calculator: The signal labels display the exact Lot Size you should use based on your account balance and risk percentage (default 0.5%). It calculates this dynamically based on the Stop Loss distance.

Institutional Targets: The indicator fetches H1 Fractals (Liquidity) from the 1-hour timeframe and plots them on your 1-minute chart as blue lines. These are your primary Take Profit (TP) levels.

Stop Loss Visualization: Automatically suggests a Stop Loss placement behind the swing high/low of the reversal structure.

How to Use

Timeframe: Set your chart to 1 Minute (1m).

Asset: UK100 (FTSE 100).

Wait: Allow the London session to open. Watch for price to move away from the opening line.

Execute: When a BUY or SELL label appears:

Enter the trade using the Lot Size shown on the label.

Set your Stop Loss at the price shown on the label.

Target the blue H1 Liquidity lines for profit taking.

Settings

Timezone: Set this to your chart/exchange timezone (Default: Europe/Warsaw).

Account Balance: Input your current trading capital (e.g., 100,000) for accurate risk calculations.

Risk Per Trade %: The percentage of your account you are willing to lose if the Stop Loss is hit (Standard: 0.5% - 1.0%).

Contract Size: The value of 1 point movement (Check your broker's specifications. Usually 1 for CFDs).

Alerts You can set a single alert in TradingView to capture all signals. Select the indicator and choose "Any alert() function call". You will receive a notification with the direction (Buy/Sell), Entry Price, and Lot Size.

USDT Market Cap Change [Alpha Extract]A sophisticated stablecoin market analysis tool that tracks USDT market capitalization changes across daily and 60-day periods with statistical normalization and gradient intensity visualization. Utilizing z-score methodology for overbought/oversold detection and dynamic color gradients reflecting change magnitude, this indicator delivers institutional-grade market liquidity assessment through stablecoin flow analysis. The system's dual-timeframe approach combined with statistical normalization provides comprehensive market sentiment measurement based on capital inflows and outflows from the dominant stablecoin.

🔶 Advanced Market Cap Tracking Framework

Implements daily USDT market capitalization monitoring with dual-period change calculations measuring both 1-day and 60-day net capital flows. The system retrieves real-time CRYPTOCAP:USDT data on daily timeframe resolution, calculating absolute dollar changes to quantify stablecoin supply expansion or contraction as primary market liquidity indicator.

// Core Market Cap Analysis

USDT = request.security("CRYPTOCAP:USDT", "D", close)

USDT_60D_Change = USDT - USDT

USDT_1D_Change = USDT - USDT

🔶 Dynamic Gradient Intensity System

Features sophisticated color gradient engine that intensifies visual representation based on change magnitude relative to recent extremes. The system normalizes current 60-day change against configurable lookback period maximum, applying gradient strength calculation to transition colors from neutral tones through progressively intense blues (negative) or reds (positive) based on flow direction and magnitude.

🔶 Statistical Z-Score Normalization Engine

Implements comprehensive z-score calculation framework that normalizes 60-day market cap changes using rolling mean and standard deviation for objective overbought/oversold determination. The system applies statistical normalization over configurable periods, enabling cross-temporal comparison and threshold-based regime identification independent of absolute market cap levels.

// Z-Score Normalization

Change_Mean = ta.sma(USDT_60D_Change, Normalization_Length)

Change_StdDev = ta.stdev(USDT_60D_Change, Normalization_Length)

Z_Score = Change_StdDev > 0 ? (USDT_60D_Change - Change_Mean) / Change_StdDev : 0.0

🔶 Multi-Tier Threshold Detection System

Provides four-level regime classification including standard overbought (+1.5σ), standard oversold (-1.5σ), extreme overbought (+2.5σ), and extreme oversold (-2.5σ) thresholds with configurable adjustment. The system identifies market liquidity extremes when stablecoin inflows or outflows reach statistically significant levels, indicating potential market turning points or trend exhaustion.

🔶 Dual-Timeframe Flow Visualization

Features layered area plots displaying both 60-day strategic flows and 1-day tactical movements with distinct color coding for instant flow direction assessment. The system overlays short-term daily changes on longer-term 60-day trends, enabling traders to identify divergences between tactical and strategic capital flows into or out of stablecoin reserves.

🔶 Gradient Color Psychology Framework

Implements intuitive color scheme where red gradients indicate capital inflow (bullish for crypto as USDT supply expands for buying) and blue gradients show capital outflow (bearish as USDT is redeemed). The intensity progression from pale to vivid colors communicates flow magnitude, with extreme colors signaling statistically significant liquidity events requiring attention.

🔶 Background Zone Highlighting System

Provides subtle background coloring when z-score breaches overbought or oversold thresholds, creating visual alerts without obscuring primary data. The system applies translucent red backgrounds during overbought conditions and blue during oversold states, enabling instant regime recognition across chart timeframes.

🔶 Configurable Normalization Architecture

Features adjustable gradient lookback and statistical normalization periods enabling optimization across different market cycles and trading timeframes. The system allows traders to calibrate sensitivity by modifying the window used for maximum change detection (gradient) and mean/standard deviation calculation (z-score), adapting to volatile or stable market regimes.

🔶 Market Liquidity Interpretation Framework

Tracks USDT supply changes as proxy for overall cryptocurrency market liquidity conditions, where expanding market cap indicates fresh capital entering crypto markets and contracting cap suggests capital flight. The system provides leading indicator properties as large stablecoin inflows often precede major market rallies while outflows may signal distribution phases.

🔶 Why Choose USDT Market Cap Change ?

This indicator delivers sophisticated stablecoin flow analysis through statistical normalization and gradient visualization of USDT market capitalization changes. Unlike traditional market sentiment indicators that rely on price action alone, this tool measures actual capital flows through the dominant stablecoin, providing objective assessment of market liquidity conditions. The combination of dual-timeframe tracking, z-score normalization for overbought/oversold detection, and intensity-based gradient coloring makes it essential for traders seeking macro-level market assessment and regime change detection across cryptocurrency markets. The indicator excels at identifying liquidity extremes that often precede major market reversals or trend accelerations.

Multi-Distribution Volume Profile (Zeiierman)█ Overview

Multi-Distribution Volume Profile (Zeiierman) is a flexible, structure-first volume profile tool that lets you reshape how volume is distributed across price, from classic uniform profiles to advanced statistical curves like Gaussian, Lognormal, Student-t, and more.

Instead of forcing every market into a single "one-size-fits-all" profile, this tool lets you model how volume is likely concentrated inside each bar (body vs wicks, midpoint, tails, center bias, right-skew, heavy tails, etc.) and then stacks that behavior across a whole lookback window to build a rich, multi-distribution map of traded activity.

On top of that, it overlays a dynamic Center Band (value area) and a fade/gradient model that can color each price row by volume, hits, recency, volatility, reversals, or even liquidity voids, turning a plain profile into a multi-dimensional context map.

Highlights

Choose from multiple Profile Build Modes , including uniform, body-only, wick-only, midpoint/close/open, center-weighted, and a suite of probability-style distributions (Gaussian, Lognormal, Weibull, Student-t, etc.)

Flexible anchor layout: draw the profile on Right/Left (horizontal) or Bottom/Top (vertical) to fit any chart layout

Value Area / Center Band computed from volume quantiles around the POC.

Gradient-based Fade Metrics: volume, price hits, freshness (time decay), volatility impact, dwell time, reversal density, compression, and liquidity voids

Separate bullish vs bearish volume at each price row for directional structure insights

█ How It Works

⚪ Profile Construction

The script scans a user-defined Bars Included window and finds the full high–low span of that zone. It then divides this range into a user-controlled number of Price Levels (rows).

For each historical bar within the window:

It measures the candle’s price range, body, and wicks.

It assigns volume to rows according to the selected Profile Build Mode, for example:

* Range Uniform – volume spread evenly across the full high–low range.

* Range Body Only / Range Wick Only – concentrate volume inside the body or wicks only.

* Midpoint / Close / Open Only – allocate volume entirely into one price row (pinpoint modeling).

HL2 / Body Center Weighted – center weights around the middle of the range/body.

Recent-Weighted Volume – amplify newer bars using exponential time decay.

Volume Squared (Hard) – aggressively boost bars with large volume.

Up Bars Only / Down Bars Only – filter volume to only bullish or bearish bars.

For more advanced shapes, the script uses continuous distributions across the bar’s span:

Linear, Triangular, Exponential to High

Cosine Centered, PERT

Gaussian, Lognormal, Cauchy, Laplace

Pareto, Weibull, Logistic, Gumbel

Gamma, Beta, Chi-Square, Student-t, F-Shape

Each distribution produces a weight for each row within the bar’s range, normalized so the total volume remains consistent, but the shape of where that volume lands changes.

⚪ POC & Center Band (Value Area)

Once all rows are accumulated:

The row with the highest total volume becomes the Point of Control (POC)

The script computes cumulative volume and finds the band that wraps a user-defined Center of Profile % (e.g., 68%) around the center of distribution.

This range is displayed as a central band, often treated like a value area where price has spent the most “effort” trading.

⚪ Gradient Fade Engine

Each row also gets a fade metric, chosen in Fade Metric:

Volume – opacity based on relative volume.

Price Hits – how frequently that row was touched.

Blended (Vol+Hits) – average of volume & hits.

Freshness – emphasizes recent activity, controlled by Decay.

Volatility Impact – rows that saw larger ranges contribute more.

Dwell Time – where price “camped” the longest.

Reversal Density – where direction changes cluster.

Compression – tight-range compression zones.

Liquidity Void – inverse of volume (thin liquidity zones).

When Apply Gradient is enabled, the row’s bullish/bearish colors are tinted from faint to strong based on this chosen metric, effectively turning the profile into a heatmap of your chosen structural property.

█ How to Use

⚪ Explore Different Distribution Assumptions

Switch between multiple Profile Build Modes to see how your assumptions about intrabar volume affect structure:

Use Range Uniform for classical profile reading.

Deploy Gaussian, Logistic, or Cosine shapes to emphasize central clustering.

Try Pareto, Lognormal, or F-Shape to focus on tail / extremal activity.

Use Recent-Weighted Volume to prioritize the most recent structural behavior.

This is especially useful for traders who want to test how different modeling assumptions change perceived value areas and levels of interest.

⚪ Identify Value, Acceptance & Rejection Zones

Use the POC and Center of Profile (%) band to distinguish:

High-acceptance zones – wide central band, thick rows, strong gradient → fair value areas

Rejection zones & tails – thin extremes, low dwell time, high volatility or reversal density

These regions can be used as:

Targets and origin zones for mean reversion

Context for breakout validation (leaving value)

Bias reference for intraday rotations or swing rotations

⚪ Read Directional Structure Within the Profile

Because each row is split into bullish vs bearish contributions, you can visually read:

Where buyers dominated a price region (large bullish slice)

Where sellers absorbed or defended (large bearish slice)

Combining this with Fade Metrics like Reversal Density, Dwell Time, or Freshness turns the profile into a structural order-flow map, without needing raw tick-by-tick volume data.

⚪ Use Fade Metrics for Contextual Heatmaps

Each Fade Metric can be used for a different analytical lens:

Volume / Blended – emphasize where volume and activity are concentrated.

Freshness – highlight the most recently active zones that still matter.

Volatility Impact & Compression – spot areas of explosive moves vs coiled ranges.

Reversal Density – locate micro turning points and battle zones.

Liquidity Void – visually pop out thin regions that may act as speedways or magnets.

█ Settings

Profile Build Mode – Selects how each bar’s volume is distributed across its price range (uniform, body/wick, midpoint/close/open, center-weighted, or statistical distribution families).

Bars Included – Number of bars used to build the profile from the current bar backward.

Price Levels – Vertical resolution of the profile: more levels = smoother but heavier.

Anchor Side – Where the profile is drawn on the chart: Right, Left, Bottom, or Top.

Offset (bars) – Horizontal offset from the last bar to the profile when using Right/Left modes.

Apply Gradient – Toggles the fade/heatmap coloring based on the selected metric.

Fade Metric – Chooses the property driving row opacity (Volume, Hits, Freshness, Volatility Impact, Dwell Time, Reversal Density, Compression, Liquidity Void).

Decay – Time-decay factor for Freshness (values close to 1 keep older activity relevant for longer).

Profile Thickness – Relative thickness of the profile along the time axis, as a % of the lookback window.

Center of Profile (%) – Volume percentage used to define the central band (value area) around the POC.

-----------------

Disclaimer

The content provided in my scripts, indicators, ideas, algorithms, and systems is for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or a solicitation to buy or sell any financial instruments. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

Session Highs and Lows🔑 Key Levels: Session Liquidity & Structure Mapper

The Key Levels indicator is an essential tool for traders as it automatically plots and projects critical Highs and Lows established during key trading sessions. These levels represent major liquidity pools and define the current market structure, serving as high-probability targets, support, or resistance for the remainder of the trading day.

⚙️ Core Functionality

The indicator operates in two distinct modes, tailored for different asset classes:

1. Asset Class Mode (Toggle)

You can switch between two predefined setups depending on the asset you are trading:

Stock Mode (RTH/ETH): Designed for US stocks and futures (e.g., NQ, ES, YM). It tracks and projects levels for Regular Trading Hours (RTH) (09:30-16:00) and Extended Hours (ETH) (16:00-09:30).

Forex/Default Mode (Asia/London/NY): Designed for global markets (e.g., currency pairs). It tracks and projects levels for the three major liquidity sessions: Asia (19:00-03:00), London (03:00-09:30), and New York (09:30-16:00).

🗺️ Key Levels Mapped

The script continuously tracks and plots the most significant structural levels:

Current Session High/Low: The running high and low of the currently active session.

Previous Session High/Low: The confirmed high and low from the most recently completed session. These are often targeted by market makers.

Previous Day High/Low (PDH/PDL): The high and low of the prior 24-hour day, acting as major structural boundaries and a crucial macro market filter.

🎛️ Advanced Liquidity Management

The indicator is built with specific controls for high-level liquidity analysis:

Extend Through Sweeps (Critical Setting):

OFF (Recommended): The projected line is automatically stopped or deleted the moment the price candle wicks or closes past it. This visually confirms that the liquidity at that level has been "swept" or "mitigated."

ON: The line extends indefinitely, treating the level as simple support/resistance, regardless of interaction.

Previous vs. Current View: You can select a checkbox (e.g., Use PREVIOUS London Level) to hide the current session's running levels and only display the static, confirmed high/low from the prior completed session. This helps declutter the chart and focus only on the confirmed structural levels.

Show Older History: Toggle to keep lines from prior days visible, allowing you to track multi-day structural context.

🎯 Trading Application

The lines plotted by the Key Levels indicator provide immediate, actionable information:

Bias Filter: Use the PDH/PDL to determine the overall market context. Trading above the PDH suggests a bullish bias, while trading below the PDL suggests a bearish bias.

Manipulation/Entry: Wait for price to aggressively sweep a Previous Session High/Low (line stops extending). This often signals a liquidity grab or "manipulation" phase. Look for entries in the opposite direction for the main move (Distribution).

Targets: Key levels (especially unmitigated ones) serve as excellent, objective take-profit targets for active trades.

Trend Gazer: Unified ICT Trading System with Signals# Trend Gazer User Guide (English)

## 📖 Table of Contents

1. (#about-this-indicator)

2. (#quick-start-guide-3-steps)

3. (#detailed-usage)

4. (#settings-customization)

5. (#why-combine-multiple-features)

6. (#faq)

---

## About This Indicator

**Trend Gazer** is an integrated trading system designed to read institutional order flow like professional traders.

### 🎯 3 Problems This Indicator Solves

#### ❌ Problem 1: Too Many Indicators = Information Overload

```

Normal: RSI + MACD + Moving Average + Bollinger Bands... → Cluttered chart

Solution: All integrated into ONE indicator → Clean & Clear

```

#### ❌ Problem 2: Single Indicators Give False Signals

```

Normal: Enter based on RSI alone → Frequent stop-outs

Solution: Structure × Zone × Momentum multi-angle confirmation → Higher win rate

```

#### ❌ Problem 3: Unclear Entry Timing

```

Normal: Know the trend but don't know WHERE to enter

Solution: LS Bounce Signal shows EXACT entry points

```

---

## Quick Start Guide (3 Steps)

### 🚀 STEP 1: Confirm Trend Direction

**Look for CHoCH (Change of Character)**

```

📍 (1.CHoCH) label = Uptrend starting

📍 (a.CHoCH) label = Downtrend starting

```

**Important**: Wait for CHoCH! No direction without it.

---

### 🎯 STEP 2: Find Entry Points

**Wait for LS Bounce Signal (green/red labels)**

```

🟢 "Long@ HL only" label → LONG (buy) candidate

🔴 "Short@ LH only" label → SHORT (sell) candidate

```

**Label text color meaning**:

- **White text**: Clean trend (high confidence)

- **Yellow text**: Trend transition (moderate caution)

---

### 🛡️ STEP 3: Final Confirmation with Bar Color

**Bar color shows market state**

```

🔴 Red bar: BUY zone (buying is favored)

🟢 Green bar: SELL zone (selling is favored)

⚪ White bar: Neutral (wait and see)

```

---

## Detailed Usage

### 📊 Understanding the Chart

#### 1. Labels (Market Structure Changes)

```

(1.CHoCH) / (a.CHoCH) : Trend reversal

(2.SiMS) / (b.SiMS) : Momentum confirmation

(3.BoMS) / (c.BoMS) : Trend continuation

```

#### 2. Boxes (Institutional Order Zones)

```

📦 Blue boxes: Bullish OB (buy orders accumulated)

📦 Red boxes: Bearish OB (sell orders accumulated)

📦 Black transparent boxes: Liquidity Sweep

```

**How to use Order Blocks**:

- Function as support/resistance

- Signals within OB have higher reliability

- Use for stop-loss placement

#### 3. Lines (Trends and Support/Resistance)

```

━━━ Red lines: EMA20, EMA50, EMA100 (short to mid-term trends)

━━━ Blue lines: 60min NPR/BB bands (support/resistance)

```

#### 4. Bar Colors (Filter 6)

```

Bar color = Real-time market state

🔴 Red: Buying is favored

🟢 Green: Selling is favored

⚪ White: Neutral

```

---

### 🎯 Practical Trading Flow

#### 📍 Preparation Phase

```

1. Open chart (recommended: 5min or 15min)

2. Add Trend Gazer to chart

3. Start in observation mode (don't enter yet)

```

#### 📍 Entry Decision

```

✅ CHoCH confirms direction → Uptrend starting

✅ LS Bounce Signal "Long@ HL only" appears

→ Entry point candidate

✅ Bar turns red → Market supports buying

→ Entry decision 🎯

✅ Place stop below nearest Order Block (blue box)

```

#### 📍 Exit Decision

```

🔴 Opposite LS Bounce Signal "Short@ LH only" appears

→ Consider taking profit

🔴 Bar turns green

→ Potential trend reversal, review position

🔴 Stop loss hit

→ Exit with loss

```

---

### 💡 Tips for Higher Win Rate

#### ✅ DO's

```

1. Enter AFTER CHoCH appears

2. Prioritize white-text LS Bounce Signals

3. Check higher timeframe (1H or Daily) trend

4. Emphasize signals within Order Blocks

5. Use bar color as final confirmation

```

#### ❌ DON'Ts

```

1. Enter before CHoCH → No clear direction

2. Enter only on yellow text → Unstable transition period

3. Ignore bar color → Trading against market state

4. Don't check Order Blocks → Unclear support/resistance

5. Enter same direction consecutively → Overtrading

```

---

## Settings Customization

### 🔧 How to Open Settings

```

1. Right-click on indicator name on chart

2. Select "Settings..."

3. Settings panel opens

```

---

### 📋 Recommended Setting Profiles

#### 🔰 Beginner Settings (Simple)

**Goal**: Reduce noise, show only important signals

```

【FILTERS】

✅ Bonus Filter: ON

✅ Filter 6 (OB/BB/NPR Zone Filter): ON

❌ Direction Filter: OFF

❌ Liquidation Reversal Filter: OFF

❌ ICT Market Structure Filter: OFF

❌ EMA Trend Filter: OFF

❌ OB/FVG Filter 1: OFF

❌ OB/FVG Filter 2: OFF

【SIGNALS】

✅ Signal 0 (Bonus): ON

✅ Signal 1 (VWC Change): ON

✅ Signal 2 (Liq Rev): ON

❌ Signal 3 (LS): OFF (complex alone)

❌ Signal 4 (LS Break): OFF

❌ Signal 5 (OB+LS NPR): OFF

❌ Signal 6 (OB+LS EMA): OFF

【LS BOUNCE SIGNAL】

✅ Exclude EMA50 from touch detection: OFF

❌ Only show when EMA fills are mixed: OFF

```