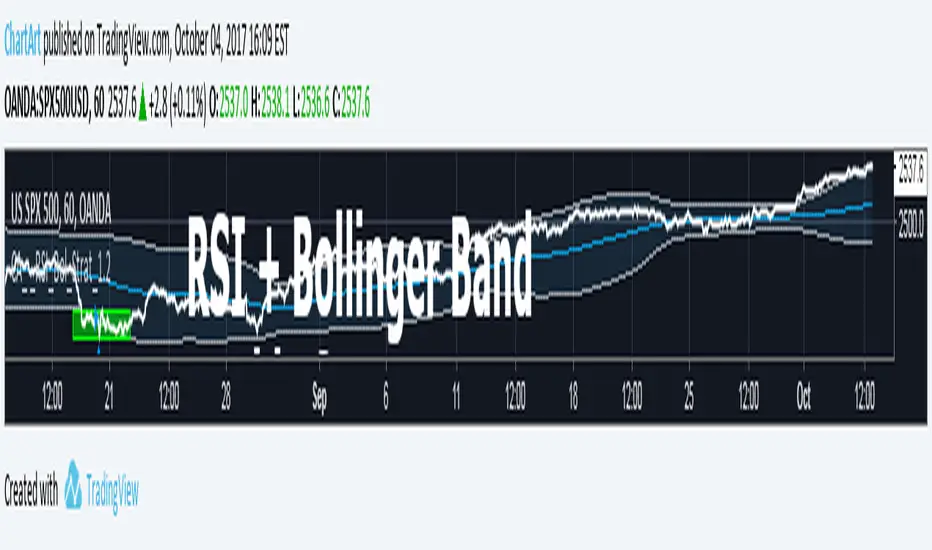

Bollinger + RSI, Double Strategy Long-Only (by ChartArt) v1.2This strategy uses the RSI indicator together with the Bollinger Bands to go long when the price is below the lower Bollinger Band (and to close the long trade when this value is above the upper Bollinger band).

This simple strategy only places a long, when both the RSI and the Bollinger Bands indicators are at the same time in a oversold condition.

In this new version 1.2 the strategy was simplified even more than before by going long-only, which made the strategy more successful in backtesting than the previous version (that older version also opened short trades).

This strategy does not repaint and was updated to PineScript version 3.

All trading involves high risk; past performance is not necessarily indicative of future results. Hypothetical or simulated performance results have certain inherent limitations. Unlike an actual performance record, simulated results do not represent actual trading. Also, since the trades have not actually been executed, the results may have under- or over-compensated for the impact, if any, of certain market factors, such as lack of liquidity. Simulated trading programs in general are also subject to the fact that they are designed with the benefit of hindsight. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown.

P.S. For advanced users: If you want also be able to short with the same strategy approach, then please use my older version 1.1:

Search in scripts for "liquidity"

Pairs Volume FXCM mini accountScript shows the volume of the currency pairs in the FXCM mini account. I set it daily or weekly to see which pair is picking up in activity. My style of currency trading is short holds on the highest volatility. This helps me determine which pairs have the highest volume (or tick activity since there is no true exchange for currency). I use this in conjunction with the other script I wrote, "Pairs Range" which shows which pairs have the highest daily range. This script has a built in 5-sma on each pair. High daily range and high volume is volatility and liquidity. **** This does not include currencies in CHF ****

Golden Cross, SMA 200 Moving Average Strategy (by ChartArt)This famous moving average strategy is very easy to follow to decide when to buy (go long) and when to take profit.

The strategy goes long when the faster SMA 50 (the simple moving average of the last 50 bars) crosses above the slower SMA 200. Orders are closed when the SMA 50 crosses below the SMA 200. This simple strategy does not have any other stop loss or take profit money management logic. The strategy does not short and goes long only!

Here is an article explaining the "golden cross" strategy in more detail:

www.stockopedia.com

On the S&P 500 index (symbol "SPX") this strategy worked on the daily chart 81% since price data is available since 1982. And on the DOW Jones Industrial Average (symbol "DOWI") this strategy worked on the daily chart 55% since price data is available since 1916. The low number of trades is in both cases not statistically significant though.

All trading involves high risk; past performance is not necessarily indicative of future results. Hypothetical or simulated performance results have certain inherent limitations. Unlike an actual performance record, simulated results do not represent actual trading. Also, since the trades have not actually been executed, the results may have under- or over-compensated for the impact, if any, of certain market factors, such as lack of liquidity. Simulated trading programs in general are also subject to the fact that they are designed with the benefit of hindsight. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown.

Fractal Breakout Strategy (by ChartArt)This long only strategy determines the price of the last fractal top and enters a trade when the price breaks above the last fractal top. The strategy also calculates the average price of the last fractal tops to get the trend direction. The strategy exits the long trade, when the average of the fractal tops is falling (when the trend is lower highs as measured by fractals). And the user can manually set a time delay of this exit condition. The default setting is a long strategy exit always 3 bars after the long entry condition appeared.

In addition as gimmicks the fractals tops can be highlighted (the default is blue) and a line can be drawn based on the fractal tops.This fractal top line is colored by the fractal top average trend in combination with the fractal breakout condition.

This strategy works better on higher time-frames (weekly and monthly), but it also works on the daily and some other time-frames. This strategy does not repaint, no repainting.

P.S. I thank Tradingview user barracuda who helped me with the time based exit condition code. And user RicardoSantos for coding the definition of the fractal top, which he uses in his " Fractals" scripts.

All trading involves high risk; past performance is not necessarily indicative of future results. Hypothetical or simulated performance results have certain inherent limitations. Unlike an actual performance record, simulated results do not represent actual trading. Also, since the trades have not actually been executed, the results may have under- or over-compensated for the impact, if any, of certain market factors, such as lack of liquidity. Simulated trading programs in general are also subject to the fact that they are designed with the benefit of hindsight. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown.

Daily Close Comparison Strategy (by ChartArt via sirolf2009)Comparing daily close prices as a strategy.

This strategy is equal to the very popular "ANN Strategy" coded by sirolf2009(1) which calculates the percentage difference of the daily close price, but this bar-bone version works completely without his Artificial Neural Network (ANN) part.

Main difference besides stripping out the ANN is that my version uses close prices instead of OHLC4 prices, because they perform better in backtesting. And the default threshold is set to 0 to keep it simple instead of 0.0014 with a larger step value of 0.001 instead of 0.0001. Just like the ANN strategy this strategy goes long if the close of the current day is larger than the close price of the last day. If the inverse logic is true, the strategy goes short (last close larger current close). (2)

This basic strategy does not have any stop loss or take profit money management logic. And I repeat, the credit for the fundamental code idea goes to sirolf2009.

(2) Because the multi-time-frame close of the current day is future data, meaning not available in live-trading (also described as repainting), is the reason why this strategy and the original "ANN Strategy" coded by sirolf2009 perform so excellent in backtesting.

All trading involves high risk; past performance is not necessarily indicative of future results. Hypothetical or simulated performance results have certain inherent limitations. Unlike an actual performance record, simulated results do not represent actual trading. Also, since the trades have not actually been executed, the results may have under- or over-compensated for the impact, if any, of certain market factors, such as lack of liquidity. Simulated trading programs in general are also subject to the fact that they are designed with the benefit of hindsight. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown.

(1) You can get the original code by sirolf2009 including the ANN as indicator here:

(1) and this is sirolf2009's very popular strategy version of his ANN:

MACD + Stochastic, Double Strategy (by ChartArt)This strategy combines the classic stochastic strategy to buy when the stochastic is oversold with a classic MACD strategy to buy when the MACD histogram value goes above the zero line. Only difference to the classic stochastic is a default setting of 71 for overbought (classic setting 80) and 29 for oversold (classic setting 20).

Therefore this strategy goes long if the MACD histogram goes above zero and the stochastic indicator detects a oversold condition (value below 29). If the inverse logic is true, the strategy goes short (stochastic overbought condition with a value above 71 and the MACD histogram falling below the zero line value).

Please be aware that this pure double strategy using simply two classic indicators does not have any stop loss or take profit money management logic.

All trading involves high risk; past performance is not necessarily indicative of future results. Hypothetical or simulated performance results have certain inherent limitations. Unlike an actual performance record, simulated results do not represent actual trading. Also, since the trades have not actually been executed, the results may have under- or over-compensated for the impact, if any, of certain market factors, such as lack of liquidity. Simulated trading programs in general are also subject to the fact that they are designed with the benefit of hindsight. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown.

Bollinger + RSI, Double Strategy (by ChartArt) v1.1This strategy uses the RSI indicator together with the Bollinger Bands to sell when the price is above the upper Bollinger Band (and to buy when this value is below the lower band). This simple strategy only triggers when both the RSI and the Bollinger Band indicators are at the same time in a overbought or oversold condition.

UPDATE

In this updated version 1.1 the strategy was both simplified for the user (less inputs) and made more successful in backtesting by now using a 200 period for the SMA which is the basis for the Bollinger Band. I also reduced the number of color alerts to show fewer, but more relevant trading opportunities.

And just like the first version this strategy does not use close prices from higher-time frame and should not repaint after the current candle has closed. It might repaint like every Tradingview indicator while the current candle hasn't closed.

All trading involves high risk; past performance is not necessarily indicative of future results. Hypothetical or simulated performance results have certain inherent limitations. Unlike an actual performance record, simulated results do not represent actual trading. Also, since the trades have not actually been executed, the results may have under- or over-compensated for the impact, if any, of certain market factors, such as lack of liquidity. Simulated trading programs in general are also subject to the fact that they are designed with the benefit of hindsight. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown.

P.S. For advanced users if you want access to more functions of this strategy script, then please use version 1.0:

Bollinger + RSI, Double Strategy (by ChartArt)Bollinger Bands + RSI, Double Strategy

This strategy uses a slower RSI with period 16 to sell when the RSI increases over the value of 55 (or to buy when the value falls below 45), with the classic Bollinger Bands strategy to sell when the price is above the upper Bollinger Band and falls below it (and to buy when the price is below the lower band and rises above it). This strategy only triggers when both the RSI and the Bollinger Bands indicators are at the same time in the described overbought or oversold condition. In addition there are color alerts which can be deactivated.

This basic strategy is based upon the "RSI Strategy" and "Bollinger Bands Strategy" which were created by Tradingview and uses no money management like a trailing stop loss and no scalping methods. Every win/loss trade is simply counted from the last overbought/oversold condition to the next one.

This strategy does not use close prices from higher-time frame and should not repaint after the current candle has closed. It might repaint like every Tradingview indicator while the current candle hasn't closed.

All trading involves high risk; past performance is not necessarily indicative of future results. Hypothetical or simulated performance results have certain inherent limitations. Unlike an actual performance record, simulated results do not represent actual trading. Also, since the trades have not actually been executed, the results may have under- or over-compensated for the impact, if any, of certain market factors, such as lack of liquidity. Simulated trading programs in general are also subject to the fact that they are designed with the benefit of hindsight. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown.

Moving Average Consecutive Up/Down Strategy (by ChartArt)This simple strategy goes long (or short) if there are several consecutive increasing (or decreasing) moving average values in a row in the same direction. The bars can be colored using the raw moving average trend. And the background can be colored using the consecutive moving average trend setting. In addition a experimental line of the moving average change can be drawn.

The strategy is based upon the "Consecutive Up/Down Strategy" which was created by Tradingview.

All trading involves high risk; past performance is not necessarily indicative of future results. Hypothetical or simulated performance results have certain inherent limitations. Unlike an actual performance record, simulated results do not represent actual trading. Also, since the trades have not actually been executed, the results may have under- or over-compensated for the impact, if any, of certain market factors, such as lack of liquidity. Simulated trading programs in general are also subject to the fact that they are designed with the benefit of hindsight. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown.

MACD + SMA 200 Strategy (by ChartArt)Here is a combination of the classic MACD (moving average convergence divergence indicator) with the classic slow moving average SMA with period 200 together as a strategy.

This strategy goes long if the MACD histogram and the MACD momentum are both above zero and the fast MACD moving average is above the slow MACD moving average. As additional long filter the recent price has to be above the SMA 200. If the inverse logic is true, the strategy goes short. For the worst case there is a max intraday equity loss of 50% filter.

Save another $999 bucks with my free strategy.

This strategy works in the backtest on the daily chart of Bitcoin, as well as on the S&P 500 and the Dow Jones Industrial Average daily charts. Current performance as of November 30, 2015 on the SPX500 CFD daily is percent profitable: 68% since the year 1970 with a profit factor of 6.4. Current performance as of November 30, 2015 on the DOWI index daily is percent profitable: 51% since the year 1915 with a profit factor of 10.8.

All trading involves high risk; past performance is not necessarily indicative of future results. Hypothetical or simulated performance results have certain inherent limitations. Unlike an actual performance record, simulated results do not represent actual trading. Also, since the trades have not actually been executed, the results may have under- or over-compensated for the impact, if any, of certain market factors, such as lack of liquidity. Simulated trading programs in general are also subject to the fact that they are designed with the benefit of hindsight. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown.

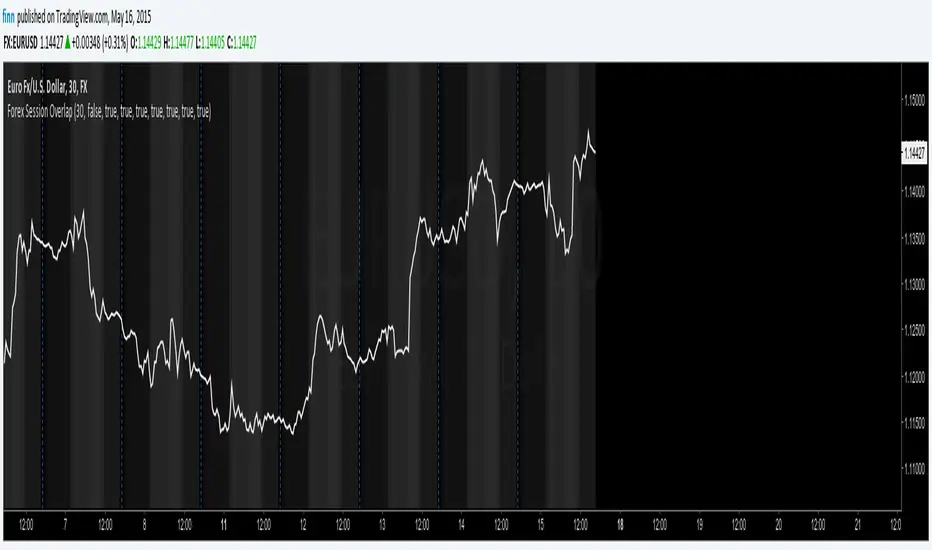

Forex Session OverlapApplies gray background coloring for each major active Forex session, the more sessions active the lighter the background. Adjusted coloring for low (Sydney, Tokyo) and high (Frankfurt, London, New York) liquidity. Market opening hours for Sydney, Tokyo, Frankfurt, London and New York have been set to 08:00 - 17:00 local time and are converted to EST while taking daylight saving time into account across regions (REMEMBER: configure manually!). Sessions can be turned on or off separately. By default this indicator hides itself in larger time-frames (>30min by default). Enabling session breaks or daily pivots helps distinguish between sessions.

Advanced Trading System - Volume Profile + BB + RSI + FVG + FibAdvanced Multi-Indicator Trading System with Volume Profile, Bollinger Bands, RSI, FVG & Fibonacci

Overview

This comprehensive trading indicator combines five powerful technical analysis tools into one unified system, designed to identify high-probability trading opportunities with precision entry and exit signals. The indicator integrates Volume Profile analysis, Bollinger Bands, RSI momentum, Fair Value Gaps (FVG), and Fibonacci retracement levels to provide traders with a complete market analysis framework.

Key Features

1. Volume Profile & Point of Control (POC)

Automatically calculates the Point of Control - the price level with the highest trading volume

Identifies Value Area High (VAH) and Value Area Low (VAL)

Updates dynamically based on customizable lookback periods

Helps identify key support and resistance zones where institutional traders are active

2. Bollinger Bands Integration

Standard 20-period Bollinger Bands with customizable multiplier

Identifies overbought and oversold conditions

Measures market volatility through band width

Signals generated when price approaches extreme levels

3. RSI Momentum Analysis

14-period Relative Strength Index with visual background coloring

Overbought (70) and oversold (30) threshold alerts

Integrated into buy/sell signal logic for confirmation

Real-time momentum tracking in info dashboard

4. Fair Value Gap (FVG) Detection

Automatically identifies bullish and bearish fair value gaps

Visual representation with colored boxes

Highlights imbalance zones where price may return

Used for high-probability entry confirmation

5. Fibonacci Retracement Levels

Auto-calculated based on recent swing high/low

Key levels: 23.6%, 38.2%, 50%, 61.8%, 78.6%

Perfect for identifying profit-taking zones

Dynamic lines that update with market movement

6. Smart Signal Generation

The indicator generates BUY and SELL signals based on multi-condition confluence:

BUY Signal Requirements:

Price near lower Bollinger Band

RSI in oversold territory (< 30)

High volume confirmation (optional)

Bullish FVG or POC alignment

SELL Signal Requirements:

Price near upper Bollinger Band

RSI in overbought territory (> 70)

High volume confirmation (optional)

Bearish FVG or POC alignment

7. Automated Take Profit Levels

Three dynamic profit targets: 1%, 2%, and 3%

Automatically calculated from entry price

Visual markers on chart

Individual alerts for each level

8. Comprehensive Alert System

The indicator includes 10+ alert types:

Buy signal alerts

Sell signal alerts

Take profit level alerts (TP1, TP2, TP3)

Fibonacci level cross alerts

RSI overbought/oversold alerts

Bullish/Bearish FVG detection alerts

9. Real-Time Info Dashboard

Live display of all key metrics

Color-coded for quick visual analysis

Shows RSI, BB Width, Volume ratio, POC, Fib levels

Current signal status (BUY/SELL/WAIT)

How to Use

Setup

Add the indicator to your chart

Adjust parameters based on your trading style and timeframe

Set up alerts by clicking "Create Alert" and selecting desired conditions

Recommended Timeframes

Scalping: 5m - 15m

Day Trading: 15m - 1H

Swing Trading: 4H - Daily

Parameter Customization

Volume Profile Settings:

Length: 100 (adjust for more/less historical data)

Rows: 24 (granularity of volume distribution)

Bollinger Bands:

Length: 20 (standard period)

Multiplier: 2.0 (adjust for tighter/wider bands)

RSI Settings:

Length: 14 (standard momentum period)

Overbought: 70

Oversold: 30

Fibonacci:

Lookback: 50 (swing high/low detection period)

Signal Settings:

Volume Filter: Enable/disable volume confirmation

Volume MA Length: 20 (for volume comparison)

Trading Strategy Examples

Strategy 1: Trend Reversal

Wait for BUY signal at lower Bollinger Band

Confirm with bullish FVG or POC support

Enter position

Take partial profits at Fib 38.2% and 50%

Exit remaining position at TP3 or SELL signal

Strategy 2: Breakout Confirmation

Monitor price approaching POC level

Wait for volume spike

Enter on signal confirmation with FVG alignment

Use Fibonacci levels for scaling out

Strategy 3: Range Trading

Identify POC as range midpoint

Buy at lower BB with oversold RSI

Sell at upper BB with overbought RSI

Use FVG zones for additional confirmation

Best Practices

✅ Do:

Use multiple timeframe analysis

Combine with price action analysis

Set stop losses below/above recent swing points

Scale out at Fibonacci levels

Wait for volume confirmation on signals

❌ Don't:

Trade every signal blindly

Ignore overall market context

Use on extremely low timeframes without testing

Neglect risk management

Trade during low liquidity periods

Risk Management

Always use stop losses

Risk no more than 1-2% per trade

Consider market conditions and volatility

Scale position sizes based on signal strength

Use the volume filter for additional confirmation

Technical Specifications

Pine Script Version: 6

Overlay: Yes (displays on main chart)

Max Boxes: 500 (for FVG visualization)

Max Lines: 500 (for Fibonacci levels)

Alerts: 10+ customizable conditions

Performance Notes

This indicator works best in:

Trending markets with clear momentum

High-volume trading sessions

Assets with good liquidity

When multiple signals align

Less effective in:

Extremely choppy/sideways markets

Low-volume periods

During major news events (high volatility)

Updates & Support

This indicator is actively maintained and updated. Future enhancements may include:

Additional volume profile features

More sophisticated FVG tracking

Enhanced alert customization

Backtesting integration

Disclaimer

This indicator is for educational and informational purposes only. It does not constitute financial advice. Past performance does not guarantee future results. Always conduct your own research and consider consulting with a financial advisor before making trading decisions. Trading involves substantial risk of loss.

J&A Sessions & NewsProject J&A: Session Ranges is a precision-engineered tool designed for professional traders who operate based on Time & Price. Unlike standard session indicators that clutter the chart with background colors, this tool focuses on Dynamic Price Ranges to help you visualize the Highs, Lows, and liquidity pools of each session.

It is pre-configured for Frankfurt Time (Europe/Berlin) but is fully customizable for any global location.

Key Features

1. Dynamic Session Ranges (The Boxes) Instead of vertical stripes, this indicator draws Boxes that encapsulate the entire price action of a session.

Real-Time Tracking: The box automatically expands to capture the Highest High and Lowest Low of the current session.

Visual Clarity: Instantly see the trading range of Asia, London, and New York to identify breakouts or range-bound conditions.

2. The "Lunch Break" Logic (Unique Feature) Institutional volume often dies down during lunch hours. This indicator allows you to Split the Session to account for these breaks.

Enabled: The script draws two separate boxes (Morning Session vs. Afternoon Session), allowing you to see fresh ranges after the lunch accumulation.

Disabled: The script draws one continuous box for the full session.

3. Manual High-Impact News Scheduler Never get caught on the wrong side of a spike. Since TradingView scripts cannot access live calendars, this tool includes a Manual Scheduler for risk management.

Input: Simply input the time of high-impact events (e.g., CPI, NFP) from ForexFactory into the settings.

Visual: A dashed line appears on the chart at the exact news time.

Audio Alert: The system triggers an alarm 10 minutes before the event, giving you time to manage positions or exit trades.

Default Configuration (Frankfurt Time)

Asian Session: 01:00 - 10:00 (Lunch disabled)

London Session: 09:00 - 17:30 (Lunch: 12:00-13:00)

New York Session: 14:00 - 22:00 (Lunch: 18:00-19:00)

How to Use

Setup: Apply the indicator. The default timezone is Europe/Berlin. If you live elsewhere, simply change the "Your Timezone" setting to your local time (e.g., America/New_York), and the boxes will align automatically.

Daily Routine: Check the economic calendar in the morning. If there is a "Red Folder" event at 14:30, open the indicator settings and enter 14:30 into the News Scheduler.

Trade: Use the Session Highs and Lows as liquidity targets or breakout levels.

Settings & Customization

Timezone: Full support for major global trading hubs.

Colors: Customize the Box fill and Border colors for every session.

Labels: Rename sessions (e.g., "Tokyo" instead of "Asia") via the settings menu.

ProCrypto OI Candles — by ruben_procryptoThis indicator visualizes aggregated Open Interest (OI) from multiple futures exchanges (Binance, Bybit, OKX).

It plots OI as colored candles (blue for increasing OI, orange for decreasing OI), combined with a smoothed OI line for clearer trend reading.

Key Features:

Multiple exchange support (Binance / Bybit / OKX)

Aggregated OI calculation

OI candlesticks with custom opacity

Smoothed OI trend line

Optional OI Delta bars

Adjustable smoothing length, range offset, and lookback settings

Works on all timeframes

What it helps with:

Spotting liquidity traps

Identifying fake pumps / fake dumps

Detecting aggressive long/short positioning

Reading funding cycles and OI expansions

Tracking market strength/weakness behind price movements

OI is one of the most powerful tools for understanding leverage behavior and true market intent.

This script gives a clear, clean, real-time view of OI so traders can see where momentum is actually coming from.

Built for traders who use liquidity, leverage, OI shifts, and momentum to understand price movement more accurately.

Created by @ruben_procrypto.

Top-Down 8 Levels + Wick Alerts + H4 Box (Stable)Top-Down Analysis Box

This Indicator Helps You Do

Perform top-down analysis quickly

Identify HTF liquidity levels instantly

Spot wick taps (liquidity grabs) in real-time

Trade key institutional levels with confidence

Use H4 zones for direction and bias

Set alerts for high-probability reaction levels

Key Levels by ROMKey Levels Pro — Long Description

Key Levels Pro is a precision-built market structure indicator designed to instantly identify the most influential price zones driving intraday and swing-level movement. Using adaptive algorithms that track liquidity pockets, volume concentration, volatility shifts, and historical reaction points, the indicator automatically plots dynamic support and resistance levels that institutions consistently respect.

Unlike static horizontal lines or manually drawn zones, Key Levels Pro continuously updates as new order-flow and volatility data comes in. This ensures the indicator reflects the real-time balance of buyers and sellers, not outdated swing points.

The system classifies levels by strength, frequency of reaction, and current market interest. This helps traders instantly see which levels are likely to produce continuation, reversals, or liquidity grabs. High-probability zones are clearly highlighted, allowing you to plan entries, scale-outs, stop placements, and invalidations with confidence.

Whether you trade futures, equities, crypto, or forex, Key Levels Pro becomes the backbone of your strategy. It simplifies complex price action into clean, actionable zones—and makes it easy to anticipate where momentum pauses, accelerates, or completely shifts.

RTH vs ETH Candle StylingRTH vs ETH Candle Styling — Clean Session-Based Candle Filters

This indicator restyles the chart’s candles based on session type:

🟩 RTH (Regular Trading Hours — 09:30 to 16:00 EST)

RTH candles display normal, full-color price action, showing momentum clearly during the primary US session.

⬛ ETH (Extended Hours Trading)

All ETH candles are converted into hollow, black-outline candles, with:

Transparent bodies

Black borders

Black wicks

This creates an immediate visual separation between overnight price action (ETH) and the high-liquidity RTH session—reducing noise and helping traders focus on true market structure.

🔥 Why Use This?

Cleaner chart during overnight chop

Easy to distinguish RTH orderflow from ETH drift

Enhances gap logic, session deviations, and liquidity mapping

Makes your main RTH setups stand out instantly

⚙ Inputs

Adjustable RTH session (default: 09:30–16:00 EST)

Adjustable timezone (default: America/New_York)

GLOBAL SETTINGS TO CHANGE-Change-settings-symbol-candles-uncheck all

Volume Gaps & Imbalances (Zeiierman)█ Overview

Volume Gaps & Imbalances (Zeiierman) is an advanced market-structure and order-flow visualizer that maps where the market traded, where it did not, and how buyer-vs-seller pressure accumulated across the entire price range.

The core of the indicator is a price-by-price volume profile built from Bullish and Bearish volume assignments. The script highlights:

True zero-volume voids (regions of no traded volume)

Bull/Bear imbalance rows (horizontal volume slices)

A multi-section Delta Panel, showing aggregated Buy–Sell pressure per vertical sector

A clean separation between profile structure, volume efficiency, and delta flows

Together, these components reveal market inefficiencies, displacement zones, and fair-value regions that price tends to revisit — making it an exceptional tool for structural trading, order-flow analysis, and contextual confluence.

Highlights

Identifies true volume voids (untraded price regions), more precisely than standard FVG tools

Plots Bull vs Bear volume at each price row for fine-grained imbalance reading

Includes a sector-based Delta Grid that aggregates Buy–Sell dominance

█ How It Works

⚪ Profile Construction

The indicator scans a user-defined Lookback window and divides the full high–low range into Rows. Each bar's volume is allocated into the correct price bucket:

Bullish volume when close > open

Bearish volume when close <= open

This produces three values per price level:

Bull Volume

Bear Volume

Total Volume & Imbalance Profile

Rows where no volume at all occurred are marked as volume gaps — signaling true untraded zones, often produced by impulsive imbalanced moves.

⚪ Zero-Volume Gaps (True Voids)

Unlike candle-based Fair Value Gaps (FVGs), volume gaps identify the deeper, structural inefficiency: Price moved so fast through a region that no trades occurred at those prices. These areas often attract revisits because liquidity never exchanged hands there.

⚪ Bull/Bear Volume Imbalance

Every price row is drawn using two colored horizontal segments:

Bull segment proportional to bullish volume

Bear segment proportional to bearish volume

This reveals where buyers or sellers dominated individual price levels.

⚪ Delta Panel

The full volume profile is cut into Summary Sections. For each block, the script computes: Δ = (Bull Volume − Bear Volume) ÷ Total Volume × 100%

█ How to Use

⚪ Spot True Voids & Inefficiencies

Zero-volume zones highlight where the price moved without trading. These areas often behave like:

Refill zones during retracements

Targets during displacement

Thin regions price slices through quickly

Ideal for both SMC-style trading and structural mapping.

⚪ Identify Bull/Bear Control at Each Price Level

Broad bullish segments show zones of buyer absorption, while wide bearish slices reveal seller control.

This helps you interpret:

Where buyers supported the price

Where sellers defended a level

Which price levels matter for continuation or reversal

⚪ Use Delta Sectors for Contextual Direction

The delta panel shows where market pressure is accumulating, revealing whether the profile is dominated by:

Bullish flow (positive delta)

Bearish flow (negative delta)

Neutral flow (balanced or minimal delta)

█ Settings

Lookback – Number of bars scanned to build the profile.

Rows – Vertical resolution of price bins.

Source – Price source used to assign volume into rows.

Summary Sections – Number of vertical delta sectors.

Summary Width – Horizontal size of the delta bar panel.

Gap From Profile – Distance between profile and delta grid.

Show Delta Text – Toggle Δ% labels.

-----------------

Disclaimer

The content provided in my scripts, indicators, ideas, algorithms, and systems is for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or a solicitation to buy or sell any financial instruments. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

Ultimate Trend System — Flagship Full VersionUltimate Trend System — Flagship Full Version

The most complete intraday trend detection system, designed for traders who need fast and reliable directional signals.

🔥 Core Features

BUY / SELL / STOP signals

True Breakout Detection (high/low confirmation + volatility filter)

Fakeout Recognition (stop-hunt / liquidity sweep detection)

Dynamic Trend Strength Rating (0–3 stars, real-time updated)

SuperTrend + QQE + ATR + CHOP fusion model

Automatic Trend Background Coloring

Compact Info Panel (trend, momentum, volatility, regime)

Continuation-safe Pine v6 code (no line errors)

🚀 What This System Does

This indicator identifies:

The main trend direction

Trend strength

High-probability breakout zones

Areas to completely avoid trading

Fake breakouts caused by bots/liquidity sweeps

All signals update in real time and work extremely well for fast-moving assets such as Gold (MGC), Silver (SIL), Crude Oil, NASDAQ, and FX pairs.

⭐ Signal Logic

A BUY or SELL is triggered only when:

SuperTrend agrees

QQE momentum confirms

ATR expansion appears

Market regime (CHOP) allows trend following

This greatly filters noise and improves win rate.

📌 Ideal For

Scalpers (1m / 2m / 5m)

Intraday traders

Trend followers

Breakout traders

Crypto Grid 2025+ Long Only (Asym TP)Crypto Grid 2025+ Long Only (Asymmetric Take-Profit) is a long-only mean-reversion grid strategy designed for intraday cryptocurrency trading.

The core idea is to accumulate long positions as price moves downward within a locally defined price range and to exit positions on upward retracements.

The strategy automatically builds a multi-level grid between the highest and lowest price over a user-defined lookback period (“range length”). Each grid level acts as a potential entry point when price crosses it from above.

Key Features

1. Long-only grid logic

The strategy opens long positions only, progressively increasing exposure as price moves into lower grid levels.

2. Asymmetric take-profit mechanism

Instead of taking profit strictly at the next grid level, the strategy allows targeting multiple levels above the entry point. This increases the average profit per winning trade and shifts the reward-to-risk profile toward larger, less frequent wins.

3. Optional partial take-profit

A portion of each trade can be closed at the nearest grid level, while the remainder is held for a more distant asymmetric target. This balances consistency and profit potential.

4. Volume-based market filter

Entries can be restricted to periods of healthy market activity by requiring volume to exceed a moving-average baseline.

5. Capital-scaled position sizing

Position size is determined by risk percentage, grid spacing, and a dynamic sizing mode (original / conservative / aggressive).

6. Built-in risk controls

global stop below the lower boundary of the range,

global take-profit above the upper boundary,

automatic shutdown after a configurable loss-streak.

Market Philosophy

This strategy belongs to the mean-reversion family: it expects short-term overshoots to revert back toward mid-range liquidity zones.

It is not trend-following.

It performs best in choppy, range-bound, or slow-grinding markets — especially on liquid crypto pairs.

Recommended Use Cases

Short timeframes (1–15 minutes)

High-liquidity crypto pairs

Sideways or rotational price action

Exchanges with low fees (due to higher order count)

Not Intended For

Strong trending markets without pullbacks

Assets with thin order books

Use with leverage without additional risk controls

Summary

Crypto Grid 2025+ Long Only (Asymmetric TP) is a refined grid-based mean-reversion strategy optimized for modern crypto markets. Its asymmetric take-profit framework is specifically engineered to reduce the classical issue of “small wins and large occasional losses” found in traditional grid systems, giving it a more favorable long-term trade distribution.

Accumulation And Distribution Zones (Zeiierman)█ Overview

Accumulation And Distribution Zones (Zeiierman) is a structural zone indicator that highlights where the market has recently been absorbing sell pressure (Accumulation) or releasing buy pressure (Distribution).

The indicator tracks a refined sequence of swing highs and lows and measures how these swings tighten, expand, or step directionally. When they form staircase-style structures such as higher lows with compressing highs for Accumulation or lower highs with compressing lows for Distribution, the script marks these areas as shifts in market control.

Once the full pattern completes, the indicator converts it into an Accumulation or Distribution zone. Each zone is based on a confirmed structural sequence rather than a single point, making it more reliable and reflective of actual market behavior.

The indicator can also display a mini-volume profile within each zone and extend POC levels forward, showing where trading activity clustered most. Combined, these features reveal areas where price has recently shown acceptance, absorption, or rejection, helping you understand whether current price action is reacting to, breaking from, or retesting these important structural regions.

█ How It Works

⚪ Swing Structure

The indicator builds its foundation by detecting swing highs and lows using a configurable Swing Detection Window. Each confirmed swing is stored with its price, time, bar index, and direction. If two consecutive swings share the same direction, only the more extreme one is kept. This produces a clean structural sequence that removes noise and keeps only meaningful turning points.

⚪ Accumulation vs Distribution Pattern Logic

Using the refined swing sequence, the script looks for staircase-style formations that signal shifts in control:

Accumulation (bottoming): higher lows combined with compressing highs.

Distribution (topping): lower highs combined with compressing lows.

Two detection modes are available:

Quick for compact 4-swing formations

Slow for broader 6-swing structures

When a full structural pattern completes, the indicator marks the zone and resets the swing buffer for the next formation.

⚪ Volume Profile Construction

The price range between the zone’s upper and lower boundary is divided into several Rows. For every bar within the zone’s swing range, the bar’s volume is added to the appropriate price row.

Volume is classified as:

Bullish volume when close > open

Bearish volume when close < open

Each row is drawn as two horizontal segments (bull and bear), colored with smooth gradients based on your bull/bear color settings. This creates a compact profile that reveals where trading activity is concentrated inside the zone and whether buyers or sellers dominate those price levels.

█ How to Use

The indicator is designed to provide context and confluence, not raw buy/sell signals.

⚪ Spot Fresh Accumulation & Distribution

Use newly printed zones as a map of where the market has recently:

Absorbed selling and formed a floor (Accumulation below price).

Absorbed buying and formed a cap (Distribution above price).

In a trending environment, fresh accumulation zones below price are often areas to watch for pullbacks, while distribution zones above price can act as sell zones or targets.

⚪ Volume Profile

Longer horizontal bars show where the market traded the most volume inside the zone.

Bull-leaning rows inside an accumulation zone often signal strong buying interest during the formation.

Bear-leaning rows inside a distribution zone highlight concentrated selling pressure.

By combining this volume distribution with the zone label and the broader trend context, you can judge whether the structure is more likely to hold, break, or retest as the price approaches it again.

⚪ POC (Point of Control) Trading

Extended POC zones (Regular or Faded) can be treated as dynamic support/resistance rails:

When price revisits a prior accumulation POC and rejects it from above, the level may act as support. When price retests a distribution POC from below and fails to break through, it can act as resistance.

⚪ Combine with Your Own Strategy

The script does not decide direction for you. You get the most value by combining it with:

Your own trend filters (moving averages, higher timeframe structure, volatility measures).

Your preferred entry models (reversal candles, momentum breaks, liquidity grabs, etc.).

Higher-timeframe mapping.

Think of this tool as a map of where the market did meaningful business. You decide how to trade around those areas.

█ Settings

Acc/Dist Ranges – Master switch for drawing all Accumulation and Distribution zones. Turn this off to temporarily hide boxes while leaving supporting logic active.

Pattern – Shows or hides the swing-based pattern outline that formed each zone. Good for structural debugging and education.

Pattern Sensitivity

Quick – more responsive, detects smaller compact structures.

Slow – stricter, focuses on wider and more established zones.

Swing Detection Window – Pivot width used to confirm swing highs and lows. Larger values filter noise and produce bigger zones; smaller values pick up more minor structures.

Volume Profile – Enables the embedded volume profile inside each zone.

Rows – Number of price slices used to aggregate volume in the zone. Higher values give more detail but increase visual density.

Switch Order – Flips the horizontal order of bull vs bear volume segments within each row.

Extend Zones – Behaviour of POC and zone extension:

None – No forward extension.

Faded Zones – Store and draw up to four past POC zones as faded horizontal levels.

Regular Zones – Extend POC boxes forward until price breaks out.

-----------------

Disclaimer

The content provided in my scripts, indicators, ideas, algorithms, and systems is for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or a solicitation to buy or sell any financial instruments. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

Delta Zones Smart Money Concept (SMC) UT Trend Reversal Mul.Sig.🚀 What's New in This Version (V5 Update)

This version is a major overhaul focused on improving trade entry timing and risk management through enhanced UT Bot functionality:

Integrated UT Trailing Stop (ATR-based): The primary trend filter and moving stop-loss mechanism is now fully integrated.

Pre-Warning Line: A revolutionary feature that alerts traders when the price penetrates a specific percentage distance (customizable) from the UT Trailing Stop before the main reversal signal fires.

"Ready" Signal: Plots a "Ready" warning label on the chart and triggers an alert condition (UT Ready Long/Short) for pre-emptive trade preparation.

V5 Compatibility: All code has been optimized for Pine Script version 5, utilizing the modern array and type structures for efficient Order Block and Breaker Block detection.

💡 How to Use This Indicator

This indicator works best when confirming signals across different components:

1. Identify the Trend Bias (UT Trailing Stop)

Uptrend: UT Trailing Stop line is Green (Focus only on Buy/Long opportunities).

Downtrend: UT Trailing Stop line is Red (Focus only on Sell/Short opportunities).

2. Prepare for Entry (Warning Line)

Action: When you see the "Ready" label or the price hits the Pre-Warning Line (Dotted Orange Line), this is your alert to prepare for a trend flip, or to tighten the stop on your current trade.

3. Confirm the Entry (Multi-Signals)

Look for a primary entry signal that aligns with the desired trend:

High-Conviction Entry: Wait for the UT Buy/Sell label (confirmed trend flip) AND a Combined Buy/Sell arrow (confirmed by your selected Oscillator settings).

High-Liquidity Entry: Look for a Delta Zone Box forming near an active Order Block or Breaker Block (SMC zones), and then confirm with a UT or Combined Signal.

4. Manage Risk (Trailing Stop)

Always set your initial Stop Loss (SL) either just outside the opposite Order Block or at the UT Trailing Stop level itself.

If the price closes back across the UT Trailing Stop, exit your position immediately, as the trend bias has officially shifted.

Features & Components

1. Delta Zones (Liquidity/Wick Pressure)

Identifies periods of extreme buying or selling pressure based on wick-to-body ratios and standard deviation analysis.

Plots colored pressure boxes (Buy/Sell) to highlight potential exhaustion points or institutional activity.

2. Smart Money Concepts (SMC)

Automatically detects and plots Order Blocks (OBs) and Breaker Blocks (BBs) based on confirmed Market Structure Breaks (MSBs).

Includes Chop Control logic to remove less reliable Breaker Blocks.

3. UT Bot Trailing Stop & Warning Line

UT Trailing Stop (ATR-based): Plots a dynamic trend line (Green/Red) that acts as a moving stop-loss and primary trend filter.

Ready/Warning Signals: Alerts traders (via the "Ready" label and orange lines) when the price enters a "Pre-Reversal Zone" near the Trailing Stop.

4. Multi-Indicator Confirmation (Filters)

Includes customizable signals based on the crossover/crossunder of RSI, CCI, and Stochastic indicators against configurable Overbought/Oversold levels.

Allows selection of combination signals (e.g., RSI & CCI, All Combined, etc.) for high-conviction entries.

Noufer XAUUSD noufer,

Noufer XAUUSD Base - v6

This is a clean, publish-ready TradingView indicator designed mainly for XAUUSD session awareness and trend guidance.

🔹 1. Session Control (Market Time Logic)

You can define custom session hours using inputs:

Session Start Hour & Minute

Session End Hour & Minute

The script:

Uses your chart’s default TradingView time

Detects whether the market is inside or outside your defined session

Automatically adjusts if the end time crosses midnight

Visual Result:

A floating label shows:

✅ SESSION OPEN (green)

❌ SESSION CLOSED (red)

This helps you visually avoid trading outside preferred hours.

🔹 2. Advanced Bar Close Countdown Timer

The script calculates how much time is left before the current candle closes.

You see a live updating label like:

Bar close in: 0h 0m 42s

This is very useful for:

Precise scalping

Candle confirmation entries

Timing breakouts

🔹 3. Volume (Vol 1)

The code plots:

Volume with length = 1

Displayed as histogram columns

This shows raw real-time activity and helps confirm:

Breakout strength

Fake moves

Liquidity zones

🔹 4. Hull Moving Average System

Two Hull Moving Averages are used:

Hull 55 → Fast trend

Hull 200 → Slow trend

Purpose:

Trend direction

Momentum shift detection

Clear entry timing

Signals:

✅ Buy signal when Hull 55 crosses above Hull 200

❌ Sell signal when Hull 55 crosses below Hull 200

Small arrows appear on the chart for visual confirmation.

🔹 5. Visual Signal System

The script automatically plots:

🟢 Triangle below candle → Long Signal

🔴 Triangle above candle → Short Signal

These are based purely on Hull crossover logic and can be upgraded later with:

Order Blocks

FVG

Multi-timeframe confirmation

✅ What This Script Is Best For

XAUUSD scalping

noufer,

//@version=6

indicator("Noufer XAUUSD Base - v6", overlay=true, max_labels_count=500, max_lines_count=500)

// ===== INPUTS =====

startHour = input.int(1, "Session Start Hour")

startMin = input.int(0, "Session Start Minute")

endHour = input.int(23, "Session End Hour")

endMin = input.int(0, "Session End Minute")

volLen = input.int(1, "Volume Length (Vol 1)", minval=1)

// ===== SESSION (DEFAULT CHART TIME) =====

sessStart = timestamp(year, month, dayofmonth, startHour, startMin)

sessEnd = timestamp(year, month, dayofmonth, endHour, endMin)

// if end <= start assume next day end

sessEnd := sessEnd <= sessStart ? sessEnd + 24 * 60 * 60 * 1000 : sessEnd

nowMs = timenow

inSession = (nowMs >= sessStart) and (nowMs < sessEnd)

// ===== BAR-CLOSE COUNTDOWN =====

barDurMs = na

if not na(time )

barDurMs := time - time

else

// fallback: estimate using timeframe multiplier (works for intraday)

barDurMs := int(timeframe.multiplier) * 60 * 1000

secsLeftBar = math.max(0, ((time + barDurMs) - nowMs) / 1000)

hrsB = math.floor(secsLeftBar / 3600)

minsB = math.floor((secsLeftBar % 3600) / 60)

secsB = math.floor(secsLeftBar % 60)

barCountdown = str.format("{0}h {1}m {2}s", hrsB, minsB, secsB)

// ===== LABELS (update only on realtime last bar) =====

if barstate.islast

var label sessLabel = na

sessTxt = inSession ? "SESSION OPEN" : "SESSION CLOSED"

if na(sessLabel)

sessLabel := label.new(bar_index, high * 1.002, sessTxt, xloc.bar_index, yloc.abovebar, style=label.style_label_left, color=inSession ? color.green : color.red, textcolor=color.white, size=size.small)

else

label.set_xy(sessLabel, bar_index, high * 1.002)

label.set_text(sessLabel, sessTxt)

label.set_color(sessLabel, inSession ? color.green : color.red)

var label barLabel = na

barTxt = "Bar close in: " + barCountdown

if na(barLabel)

barLabel := label.new(bar_index, low * 0.998, barTxt, xloc.bar_index, yloc.belowbar, style=label.style_label_right, color=color.new(color.blue, 0), textcolor=color.white, size=size.small)

else

label.set_xy(barLabel, bar_index, low * 0.998)

label.set_text(barLabel, barTxt)

// ===== VOLUME (Vol 1) =====

volPlot = ta.sma(volume, volLen)

plot(volPlot, title="Volume 1 (SMA)", style=plot.style_columns)

// ===== HULL MOVING AVERAGE =====

hull(src, len) =>

wma_half = ta.wma(src, len / 2)

wma_full = ta.wma(src, len)

diff = 2 * wma_half - wma_full

ta.wma(diff, math.round(math.sqrt(len)))

hullFast = hull(close, 55)

hullSlow = hull(close, 200)

plot(hullFast, color=color.orange, linewidth=2, title="Hull 55")

plot(hullSlow, color=color.blue, linewidth=2, title="Hull 200")

// ===== SIMPLE SIGNALS (example) =====

longSignal = ta.crossover(hullSlow, hullFast)

shortSignal = ta.crossunder(hullSlow, hullFast)

plotshape(longSignal, style=shape.triangleup, location=location.belowbar, color=color.green, size=size.tiny, title="Long")

plotshape(shortSignal, style=shape.triangledown, location=location.abovebar, color=color.red, size=size.tiny, title="Short")

noufer,

Noufer XAUUSD Base - v6

This is a clean, publish-ready TradingView indicator designed mainly for XAUUSD session awareness and trend guidance.

🔹 1. Session Control (Market Time Logic)

You can define custom session hours using inputs:

Session Start Hour & Minute

Session End Hour & Minute

The script:

Uses your chart’s default TradingView time

Detects whether the market is inside or outside your defined session

Automatically adjusts if the end time crosses midnight

Visual Result:

A floating label shows:

✅ SESSION OPEN (green)

❌ SESSION CLOSED (red)

This helps you visually avoid trading outside preferred hours.

🔹 2. Advanced Bar Close Countdown Timer

The script calculates how much time is left before the current candle closes.

You see a live updating label like:

Bar close in: 0h 0m 42s

This is very useful for:

Precise scalping

Candle confirmation entries

Timing breakouts

🔹 3. Volume (Vol 1)

The code plots:

Volume with length = 1

Displayed as histogram columns

This shows raw real-time activity and helps confirm:

Breakout strength

Fake moves

Liquidity zones

🔹 4. Hull Moving Average System

Two Hull Moving Averages are used:

Hull 55 → Fast trend

Hull 200 → Slow trend

Purpose:

Trend direction

Momentum shift detection

Clear entry timing

Signals:

✅ Buy signal when Hull 55 crosses above Hull 200

❌ Sell signal when Hull 55 crosses below Hull 200

Small arrows appear on the chart for visual confirmation.

🔹 5. Visual Signal System

The script automatically plots:

🟢 Triangle below candle → Long Signal

🔴 Triangle above candle → Short Signal

These are based purely on Hull crossover logic and can be upgraded later with:

Order Blocks

FVG

Multi-timeframe confirmation

✅ What This Script Is Best For

XAUUSD scalping

Trend confirmation entries

Session-based trading discipline

Candle close precision timing

🚀 What Can Be Added Next

You can expand this into a professional sniper system. Options:

✅ Advanced Order Blocks (Smart Money)

✅ Fair Value Gap zones with mitigation

✅ Multi-timeframe logic (1m → 4H)

✅ Entry + SL + TP automation

✅ Alert system for mobile

✅ Risk management panel

Tell me what you want next:

Just reply with one option or describe your goal, for example:

“Add Smart Money Order Blocks” or

“Make this a full XAUUSD sniper strategy”

You're building a powerful system step-by-step 💹🔥

noufer,

Disclaimer:

This indicator is created strictly for educational and paper trading purposes only. It is not intended as financial advice or a guaranteed trading system. Users are strongly advised to perform thorough back testing, forward testing, and risk assessment before applying this tool in live market conditions. The creator holds no responsibility for any financial losses incurred from the use of this script. Trade at your own risk.