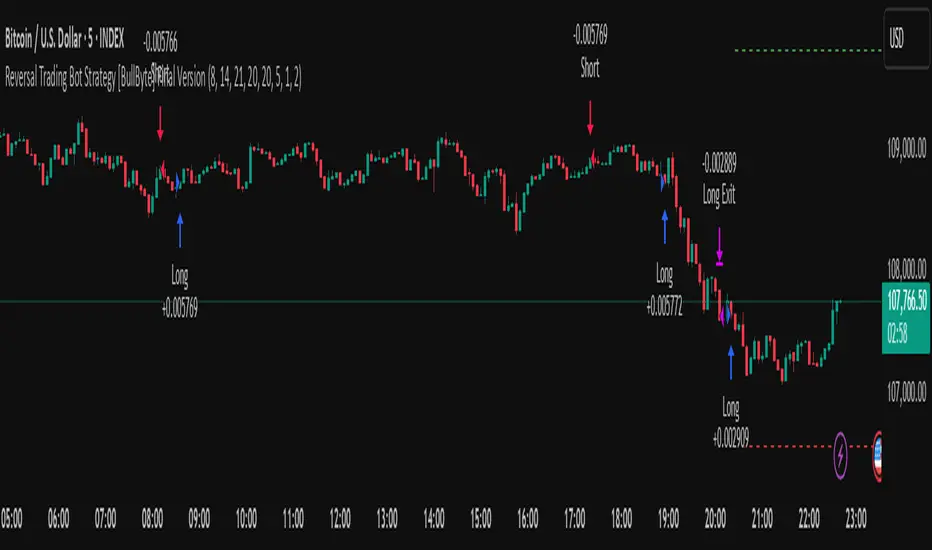

CNN Fear and Greed StrategyAdaptation of the CNN Fear and Greed Index Indicator (Original by EdgeTools)

The following changes have been implemented:

Put/Call Ratio Data Source: The data source for the Put/Call Ratio has been updated.

Bond Data Source: The data sources for the bond components (Safe Haven Demand and Junk Bond Demand) have been updated.

Normalization Adjustment: The normalization method has been adjusted to allow the CNN Fear and Greed Index to display over a longer historical period, optimizing it for backtesting purposes.

Style Modification: The display style has been modified for a simpler and cleaner appearance.

Strategy Logic Addition: Added a new strategy entry condition: index >= 25 AND index crosses over its 5-period Simple Moving Average (SMA), and a corresponding exit condition of holding the position for 252 bars (days).

CNN Fear & Greed Backtest Strategy (Adapted)

This script is an adaptation of the popular CNN Fear & Greed Index, originally created by EdgeTools, with significant modifications to optimize it for long-term backtesting on the TradingView platform.

The core function of the Fear & Greed Index is to measure the current emotional state of the stock market, ranging from 0 (Extreme Fear) to 100 (Extreme Greed). It operates on the principle that excessive fear drives prices too low (a potential buying opportunity), and excessive greed drives them too high (a potential selling opportunity).

Key Components of the Index (7 Factors)

The composite index is calculated as a weighted average of seven market indicators, each normalized to a score between 0 and 100:

Market Momentum: S&P 500's current level vs. its 125-day Moving Average.

Stock Price Strength: Stocks hitting 52-week highs vs. those hitting 52-week lows.

Stock Price Breadth: Measured by the McClellan Volume Summation Index (or similar volume/breadth metric).

Put/Call Ratio: The relationship between volume of put options (bearish bets) and call options (bullish bets).

Market Volatility: The CBOE VIX Index relative to its 50-day Moving Average.

Safe Haven Demand: The relative performance of stocks (S&P 500) vs. bonds.

Junk Bond Demand: The spread between high-yield (junk) bonds and U.S. Treasury yields.

Critical Adaptations for Backtesting

To improve the index's utility for quantitative analysis, the following changes were made:

Long-Term Normalization: The original normalization method (ta.stdev over a short LENGTH) has been replaced or adjusted to use longer historical data. This change ensures the index generates consistent and comparable sentiment scores across decades of market history, which is crucial for reliable backtesting results.

Updated Data Sources: Specific ticker requests for the Put/Call Ratio and Bond components (Safe Haven and Junk Bond Demand) have been updated to use the most reliable and long-running data available on TradingView, reducing data gaps and improving chart continuity.

Simplified Visuals: The chart display is streamlined, focusing only on the final Fear & Greed Index line and key threshold levels (25, 50, 75) for quick visual assessment.

Integrated Trading Strategy

This script also includes a simple, rules-based strategy designed to test the counter-trend philosophy of the index:

Entry Logic (Long Position): A long position is initiated when the market shows increasing fear, specifically when the index score is less than or equal to the configurable FEAR_LEVEL (default 25) and the index crosses above its own short-term 5-period Simple Moving Average (SMA). This crossover acts as a confirmation that sentiment may be starting to turn around from peak fear.

Exit Logic (Time-Based): All positions are subject to a time-based exit after holding for 252 trading days (approximately one year). This fixed holding period aims to capture the typical duration of a cyclical market recovery following a major panic event.

Search in scripts for "momentum"

Macketings 1min ScalpingThis is a hyper-reactive scalping strategy designed for the 1-minute chart. It utilizes a strict four-EMA hierarchy (80/90/340/500) to ensure trades are only taken in the strongest aligned market trend. The strategy is built to be extremely tight on risk and focuses on capturing the immediate, high-momentum swing that follows a confirmed EMA retest or breakout.

Key Mechanics (How it Works):

Strict Trend Alignment: Entry is only permitted when the faster EMA band (80/90) and the price action are correctly aligned with the slow trend (340/500).

Long: EMA 80/90 must be above EMA 340/500, AND EMA 340 must be above EMA 500. (And vice-versa for Short.)

Expanded Retest Entry: The strategy waits for the price to retest or briefly enter the 80/90 band, then immediately enters upon the confirmed momentum breakout from that band.

Dynamic Risk Management (Tight Ride): The strategy is engineered to ride the wave aggressively while protecting capital immediately:

Extremely Tight Initial Stop Loss (0.2% default): Limits initial risk instantly.

Break-Even Security: Once profit hits 0.3%, the Stop Loss is automatically trailed to secure 0.2% profit (a risk-free trade).

Aggressive Exit Logic: Positions are closed not only upon hitting the Take Profit target (2.5%) but also immediately if the 80/90 EMA band crosses the 340 EMA, signaling a critical loss of momentum.

Disclaimer:

This strategy requires high-liquidity instruments and is best used on low timeframes (1-minute) due to its dependency on fast momentum shifts and tight stops. Backtesting and forward testing are crucial before deployment.

Rasta Long/Short — StrategyThe Rasta Long/Short Strategy is a visual and educational framework designed to help traders study momentum shifts that appear when a fast EMA interacts with a slower smoothed baseline.

It is not a signal service. Instead, it is a research tool that helps you observe transitions, structure, and behavior across different market conditions and smoothing contexts.

The script plots:

A primary EMA line (fast reaction wave).

A Smoothed line (your chosen smoothing method).

Color-coded fog regions showing directional bias.

Optional DNA rung connections between the two lines for structural comparison.

Together, these allow a deeper study of how momentum pushes, volatility compression, expansions, and drift emerge around fast/slow EMA interactions.

✦ Core Idea

The Rasta Long/Short mechanism studies how price behaves when the fast EMA crosses above or below a smoothed anchor.

Rather than predicting price, it reveals where transitions occur across different structures, timeframes, and smoothing techniques.

The Long/Short logic simply highlights flips in directional structure.

It is not intended for real-time signals or automated execution; it is intended for understanding market movement.

✦ Smoothing Types (Explained)

The strategy allows experimenting with several smoothing families to observe how they transform the fast EMA:

SMA (Simple Moving Average)

Averaged, slower response. Good for stability comparisons.

EMA (Exponential)

Faster reaction, more responsive, smoother behavior during momentum.

RMA (Wilder’s)

Used in RSI calculations; steady, well-balanced response.

WMA (Weighted)

More weight to recent bars; bridges SMA and EMA dynamics.

None

Raw EMA vs EMA interaction with no secondary smoothing.

Each smoothing type provides unique structural information and can lead to different interpretations.

✦ Modes of Study

Designed for multi-timeframe research:

1H / 4H — Momentum flow mapping and structural identification.

Daily / Weekly — Higher-timeframe rotations, macro structure transitions.

1–15m — Microstructure studies, noise vs trend emergence.

Use the built-in Strategy Tester to explore entry/exit context, but treat results as research, not predictive performance.

✦ Components (Visual Study Tools)

EMA Line (Fast)

Primary reactive wave. Shows fast directional shifts.

Smoothed Line (Slow)

Trend baseline / reference structure.

Fog Region

Highlights fast-vs-smoothed directional alignment.

DNA Rungs (Optional)

Structural “bridges” showing the exact relationship between waves on each bar.

Useful for studying separation, compression, and expansions.

✦ Educational Insights

This strategy helps illuminate:

How fast and slow EMAs interact dynamically.

How structure changes precede trend emergence.

Where volatility compresses before expansion.

How noise, drift, and clean reversals differ.

How different smoothers alter the interpretation of the same price data.

The goal is clarity — not prediction.

✦ How to Use

Apply to any timeframe or instrument.

Enable or disable fog depending on preferred visibility.

Use DNA rungs for close structural comparison.

Observe long/short flips as educational reference points — not signals.

Study transitions visually, then backtest using the Strategy Tester for pattern research.

✦ Disclaimer

This script is provided for educational and research purposes only.

It does not provide trading signals, financial advice, or recommendations.

Past behavior does not indicate future performance.

Always practice risk-aware study and consult qualified financial professionals when needed.

✦ Author

Michael Culpepper (mikeyc747)

Creator of the Rasta framework and related market structure studies.

CongTrader Strategy V1📈 CongTrader Strategy V1 — Official Overview

CongTrader Strategy V1 is a precision-built algorithm designed for intraday and swing traders who want a structured, rules-driven approach to capturing directional momentum while avoiding low-quality market conditions.

This strategy combines volatility-based logic, trend confirmation filters, and a market-conditioning engine to produce high-probability long and short signals with strictly candle-close confirmed entries (no intrabar repainting).

🔍 Core Philosophy

Modern markets move in bursts of volatility that are often preceded by subtle shifts in momentum and structure.

CongTrader V1 is engineered to:

identify emerging directional pressure early

filter out noise, consolidation, and choppy environments

only execute when multiple conditions align

maintain consistent, disciplined trade management

The result is a strategy that aims to trade quality over quantity, focusing on clear, structured setups rather than impulsive, intrabar signals.

🧠 Key Components (High-Level Explanation)

1️⃣ Directional Signal Engine (Trigger System)

The strategy uses a custom momentum-oscillation model to detect potential turning points and trend continuations.

This engine smooths price action, measures pressure extremes, and generates trigger crossovers that signal potential long or short opportunities.

(The exact formula and coefficients are proprietary and not displayed.)

2️⃣ ATR-Based Risk Management

Each trade is automatically paired with:

a volatility-adaptive stop loss, and

a volatility-adaptive profit target

This allows the strategy to adjust position management dynamically based on current market movement rather than fixed pip or dollar distances.

3️⃣ Trend Confirmation Filter (EMA)

A long-term EMA trend filter prevents counter-trend entries by ensuring:

Long positions trade only above trend

Short positions trade only below trend

This keeps signals aligned with higher-timeframe momentum.

4️⃣ VWAP Institutional Bias Filter

VWAP is used as a dynamic market fair-value reference.

The strategy only trades when price action shows favorable positioning relative to VWAP—helping avoid false moves and mean-reversion traps.

5️⃣ Range & Volatility Filter

A volatility/range filter avoids entering during tight consolidations.

If the market is not moving or lacks range expansion, the strategy waits patiently.

This significantly reduces chop and whipsaw trades.

6️⃣ RTH (Regular Trading Hours) Protection

Optionally limits trades to regular exchange hours for traders who avoid low-liquidity overnight sessions.

⏳ Candle-Close Entry Confirmation (No Repainting)

All entries are strictly confirmed after the bar closes, which means:

No intrabar fakeouts

No signal disappearance

No repainting

Cleaner, more realistic backtesting

This ensures the strategy behaves the same in backtests and in live charts.

🎯 Trade Logic Summary

A trade is only taken when:

✔ A directional trigger signal occurs

✔ Price meets VWAP bias conditions

✔ Price aligns with the long-term trend

✔ Sufficient volatility/range is present

✔ (Optional) Within regular trading hours

✔ The candle has fully confirmed

Every trade is managed automatically with ATR-based stop loss and take profit placement.

📊 Who This Strategy Is For

CongTrader V1 works well for:

Intraday traders (1–15m)

Swing traders (30m–4h)

Momentum and trend-followers

Algorithmic traders looking for disciplined, rules-based entries

Traders who want cleaner signals and less noise

Anyone who wants to avoid low-quality, choppy markets

🔔 Alerts Included

Built-in alerts notify you instantly when conditions for long or short entries are met, making it suitable for:

Manual execution

Automated trading systems

Signal services

🧩 Important Note

This strategy is designed for educational purposes and is not financial advice. Performance may vary depending on market conditions, broker feed, and instrument volatility. Always backtest thoroughly and use risk management.

RSI + MACD Multi-Timeframe StrategyThis strategy combines the Relative Strength Index (RSI) from the daily timeframe with the Moving Average Convergence Divergence (MACD) from the 4-hour timeframe to generate precise long entry and exit signals.

The system uses a multi-timeframe approach to align longer-term trend conditions with shorter-term momentum shifts — allowing traders to catch dips with confirmation and exit before reversals.

🧠 Strategy Logic

✅ Long Entry Condition:

- RSI on the daily (1D) timeframe is oversold (below your defined threshold)

- MACD on the 4H timeframe crosses above the signal line

→ A long trade is opened when these two align

✅ Long Exit Condition:

- RSI on the daily timeframe is overbought

- MACD on the 4H timeframe crosses below the signal line

→ The long trade is closed when these two conditions are met

💡 This strategy currently supports long entries only. Short logic can be added if needed.

📊 Indicator Components

🔹 RSI (Relative Strength Index):

- A momentum oscillator that measures the speed and magnitude of price changes.

- Helps identify overbought (potential sell) and oversold (potential buy) conditions.

- Applied on the 1D timeframe (by default) to reflect broader market trend or exhaustion levels.

🔹 MACD (Moving Average Convergence Divergence):

- A trend-following momentum indicator based on moving averages.

- The MACD Line (fast EMA - slow EMA) crossing above the Signal Line indicates bullish momentum.

- Used here on the 4-hour timeframe (by default) for shorter-term momentum confirmation.

🔹 Multi-Timeframe (MTF) Logic:

- Uses request.security() to pull higher timeframe data (1D for RSI, 4H for MACD).

- Ensures no repainting, as it only uses closed candles from the higher timeframe.

- Aligns longer-term signals with shorter-term entries, reducing false signals.

📈 Plotting Options

The script includes a plot selector input allowing you to toggle between:

- RSI Plot (with overbought/oversold lines)

- MACD Plot (MACD line and signal line)

- This helps visualize signal conditions clearly on your chart.

🛠 Customization

- RSI & MACD settings are fully configurable

- RSI and MACD timeframes can be adjusted independently

⚠️ Disclaimer

This strategy is provided for educational and informational purposes only.

It is not financial advice or a recommendation to buy or sell any asset.

Past performance does not guarantee future results. Always test strategies in a simulated environment before live use, and consult with a licensed financial advisor for investment decisions.

W%R Pullback+EMA Trend [TS_Indie]🔰 Core Concept of the Strategy

The main idea is “Trend-Following with Momentum Pullback.”

This means trading in the direction of the main trend (defined by EMA) while using Williams %R to identify pullback entries (buying the dip or selling the rally) where momentum returns to the trend direction.

📊 Indicators Used

1. EMA Fast – Defines the short-term trend.

2. EMA Slow – Defines the long-term trend (used as a trend filter).

3. Williams %R

• Overbought zone: above -20

• Oversold zone: below -80

⚙️ Entry Rules

🔹 Buy Setup

1. EMA Fast > EMA Slow → Uptrend condition.

2. Williams %R on the previous candle dropped below -80, and on the current candle, it crosses back above -80 → indicates momentum returning to the upside.

3. Current close is above EMA Fast.

4. Entry Buy at the close of the candle where %R crosses above -80.

🎯 Entry, Stop Loss, and Take Profit

1. Entry : At the candle close where the signal occurs.

2. Stop Loss : At the lowest low between the current and previous candles.

3. Take Profit : Calculated based on entry price and stop loss distance multiplied by the Risk/Reward Ratio.

🔹 Sell Setup

1. EMA Fast < EMA Slow → Downtrend condition.

2. Williams %R on the previous candle went above -20, and on the current candle, it crosses back below -20 → indicates renewed selling momentum.

3. Current price is below EMA Fast.

4. Entry Sell at the close of the candle where %R crosses below -20.

🎯 Entry, Stop Loss, and Take Profit

1. Entry : At the candle close where the signal occurs.

2. Stop Loss : At the highest high between the current and previous candles.

3. Take Profit : Calculated based on entry price and stop loss distance multiplied by the Risk/Reward Ratio.

⚙️ Optional Parameters

• Custom Risk/Reward Ratio for Take Profit.

• Option to add ATR buffer to Stop Loss.

• Adjustable EMA Fast period.

• Adjustable EMA Slow period.

• Adjustable Williams %R period.

• Option to enable Long only / Short only positions.

• Customizable Backtest start and end date.

• Customizable trading session time.

⏰ Alert Function

Alerts display:

• Entry price

• Stop Loss price

• Take Profit price

Guys, try adjusting the parameters yourselves!

I’ve been tweaking the settings for several days and managed to get great results on XAU/USD in the 5-minute timeframe.

I think this strategy is quite interesting and could potentially deliver good results on other instruments as well.

⚠️ Disclaimer

This indicator is designed for educational and research purposes only.

It does not guarantee profits and should not be considered financial advice.

Trading in financial markets involves significant risk, including the potential loss of capital.

Turtles StrategyBorn from the 1980s "Turtle" experiment, this method of trading captures breakouts and places or closes trades with intrabar entries or exits and realized-equity risk controls.

How It Works

The strategy buys/sells on breakouts from recent highs/lows, using ATR for volatility-adjusted stops and sizing. It risks a fixed % (default 1%) of realized equity per trade—initial capital plus closed P&L, ignoring open positions for conservatism. Drawdown protection auto-reduces risk by 20% at 10% drops (up to three times), resetting only on full peak recovery. Single positions only, with 1-tick slippage simulated for realistic fills. Best for trending assets like forex,commodities, crypto, stocks. Backtest for optimal parameters.

Main Operations

The strategy works on any timeframe but it's meant to be used on daily charts.

Entry Signals:

Long: Buy-stop 1 tick above 20-bar high (default "Entry Period") when no position—enters intrabar on breakout.

Short: Sell-stop 1 tick below 20-bar low. OCA cancels opposites.

Size: (Realized equity × adjusted risk %) ÷ (2× ATR stop distance), scaled by point value.

Exit Signals:

Longs: Stop at tighter of (entry - 2× ATR) or (10-bar low - 1 tick trailing, default "Exit Period").

Shorts: Stop at tighter of (entry + 2× ATR) or (10-bar high + 1 tick trailing).

Locks profits in trends, exits fast on fades.

Risk Controls:

Tracks realized equity peak.

10% drawdown: Risk ×0.8; 20%/30%: Further ×0.8 (max 3x).

Full reset above peak—preserves capital in slumps.

Gold 15m: Trend + S/R + Liquidity Sweep (RR 1:2)This strategy is designed for short-term trading on XAUUSD (Gold) using the 15-minute timeframe. It combines trend direction, support/resistance pivots, liquidity sweep detection, and momentum confirmation to identify high-probability reversal setups in line with the dominant market trend.

⚙️ Core Logic:

Trend Filter (EMA 200):

The strategy only takes long positions when price is above the 200 EMA and short positions when price is below it.

Support/Resistance via Pivots:

Dynamic swing highs and lows are identified using pivot points. These act as local supply and demand levels where liquidity is likely to accumulate.

Liquidity Sweep Detection:

A bullish liquidity sweep occurs when price briefly breaks below the last pivot low (grabbing liquidity) and then closes back above it.

A bearish sweep occurs when price breaks above the last pivot high and then closes back below.

Momentum & Candle Strength:

The strategy filters signals based on candle range and body size to ensure entries occur during strong price reactions, not weak retracements.

Risk Management (1:2 RR):

Stop-loss is placed slightly beyond the last pivot level using ATR-based buffers, and take-profit is set at 2× the risk distance, maintaining a reward-to-risk ratio of 1:2.

💼 Trade Logic Summary:

Long Entry:

After a bullish liquidity sweep & reclaim, momentum confirmation, and trend alignment (above EMA 200).

Short Entry:

After a bearish sweep & reclaim, momentum confirmation, and trend alignment (below EMA 200).

Exit:

Automated via ATR-based Stop Loss and Take Profit targets.

📊 Customization Options:

Adjustable EMA length, pivot settings, ATR multipliers, and RR ratio.

Option to enable/disable trend filter.

Toggle display of S/R zones on chart.

🧠 Best Use:

Works best during London and New York sessions when Gold shows strong momentum.

Can be adapted for forex pairs and indices by tuning ATR and pivot parameters.

VWAP Retest + EMA9 Cross + Candle Pattern V2📈 VWAP Retest + EMA9 Cross + Candle Pattern Strategy_V2

Setup: This intraday momentum strategy combines 3 core elements:

• VWAP Retest: Price retests VWAP within a small buffer zone

• EMA9 Crossover: EMA9 crosses above VWAP within the last 3 bars

• Bullish Candle Pattern: At least one bullish signal — Hammer, Engulfing, or Momentum candle

A trade is triggered only during the US morning session (9:30–12:30 EST) and only if price is above yesterday’s high, suggesting strong momentum.

⚙️ Strategy Settings

• Initial Capital: $100,000

• Position Sizing: 10% of equity per trade

• Commission: 0.03% per trade

• Slippage: 1 tick

• Take Profit: +3% from entry

• Stop Loss: 0.5% below VWAP at entry

• Forced Exit: 1:00 PM EST

📊 Strategy Logic

• VWAP Retest Filter ensures entry is near a value zone.

• EMA9 Cross Confirmation aligns short-term momentum with volume-weighted price.

• Bullish Candle Patterns provide price action confirmation:

○ ✅ Hammer

○ ✅ Bullish Engulfing

○ ✅ Large momentum body

• Above Yesterday’s High (YH) acts as a bullish bias filter.

🧪 Backtest Results (Jan 2023 – Oct 2025)

• Total Trades: 120

• Win Rate: 52.5%

• Profit Factor: 1.18

• Max Drawdown: 1.22%

• Net P&L: +$1,064 (+1.06%)

Due to chart data limits, only part of the period may be visible on publication charts.

🔍 Chart Visuals

This strategy plots:

• VWAP (white) and EMA9 (orange)

• Candle pattern markers:

○ “H” = Hammer

○ “BE” = Bullish Engulfing

○ “M” = Momentum Candle

• “SETUP” label when all conditions are met

• YH/YL labels for context — previous day’s high/low

💡 Use Case

This setup is designed for intraday momentum scalping, ideal for traders who:

• Trade morning breakouts

• Use VWAP as a dynamic support/resistance

• Want clear, rule-based entries based on both trend and price action

Educational and research use - not financial advice.

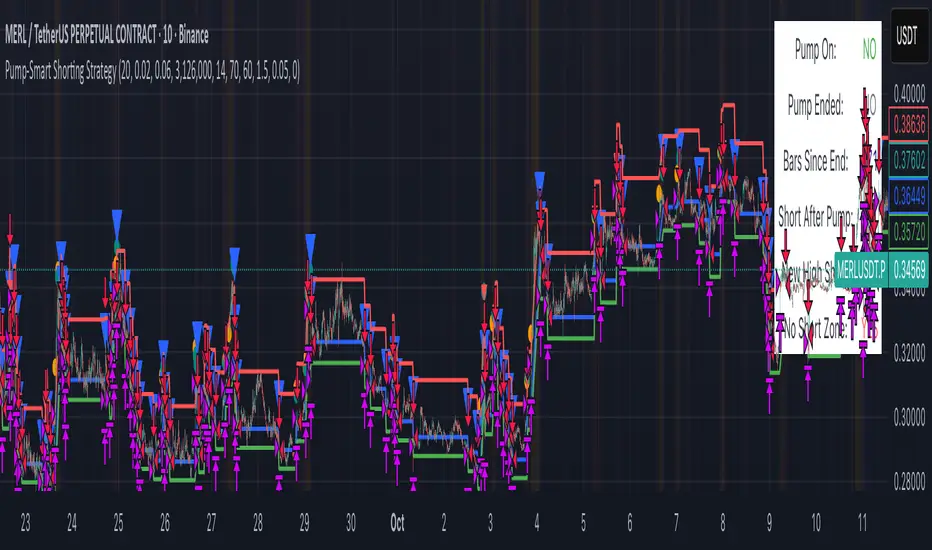

Pump-Smart Shorting StrategyThis strategy is built to keep your portfolio hedged as much as possible while maximizing profitability. Shorts are opened after pumps cool off and on new highs (when safe), and closed quickly during strong upward moves or if stop loss/profit targets are hit. It uses visual overlays to clearly show when hedging is on, off, or blocked due to momentum, ensuring you’re protected in most market conditions but never short against the pump. Fast re-entry keeps the hedge active with minimal downtime.

Pump Detection:

RSI (Relative Strength Index): Calculated over a custom period (default 14 bars). If RSI rises above a threshold (default 70), the strategy considers the market to be in a pump (strong upward momentum).

Volume Spike: The current volume is compared to a 20-bar simple moving average of volume. If it exceeds the average by 1.5× and price increases at least 5% in one bar, pump conditions are triggered.

Price Jump: Measured by (close - close ) / close . A single-bar change > 5% helps confirm rapid momentum.

Pump Zone (No Short): If any of these conditions is true, an orange or red background is shown and shorts are blocked.

Cooldown and Re-Entry:

Cooldown Detection: After the pump ends, RSI must fall below a set value (default ≤ 60), and either volume returns towards average or price momentum is less than half the original spike (oneBarUp <= pctUp/2).

barsWait Parameter: You can specify a waiting period after cooldown before a short is allowed.

Short Entry After Pump/Cooldown: When these cooldown conditions are met, and no short is active, a blue background is shown and a short position is opened at the next signal.

New High Entry:

Lookback New High: If the current high is greater than the highest high in the last N bars (default 20), and pump is NOT active, a short can be opened.

Take Profit (TP) & Stop Loss (SL):

Take Profit: Short is closed if price falls to a threshold below the entry (minProfitPerc, default 2%).

Stop Loss: Short is closed if price rises to a threshold above the entry (stopLossPerc, default 6%).

Preemptive Exit:

Any time a pump is detected while a short position is open, the strategy closes the short immediately to avoid losses.

Visual Feedback:

Orange Background: Market is pumping, do not short.

Red Background: Other conditions block shorts (cooldown or waiting).

Blue Background: Shorts allowed.

Triangles/Circles: Mark entries, pump start/end, for clear trading signals.

BTC 5-MA Multi Cross Strategy By Hardik Prajapati Ai TradelabThis strategy is built around the five most powerful and commonly used moving averages in crypto trading — 5, 20, 50, 100, and 200-period SMAs (Simple Moving Averages) — applied on a 1-hour Bitcoin chart.

Core Idea:

The strategy aims to identify strong bullish trends by confirming when the price action crosses above all key moving averages. This alignment of multiple MAs indicates momentum shift and helps filter out false breakouts.

⸻

⚙️ How It Works:

1. Calculates 5 Moving Averages:

• 5 MA → Short-term momentum (fastest signal)

• 20 MA → Near-term trend confirmation

• 50 MA → Mid-term trend filter

• 100 MA → Long-term trend foundation

• 200 MA → Macro-trend direction (strongest support/resistance)

2. Buy Condition (Entry):

• A Buy is triggered when:

• The price crosses above the 5 MA, and

• The closing price remains above all other MAs (20, 50, 100, 200)

This signals that momentum is aligned across all time horizons — a strong uptrend confirmation.

3. Sell Condition (Exit):

• The position is closed when price crosses below the 20 MA, showing weakness in short-term momentum.

4. Visual Signals:

• 🟢 BUY triangle below candles → Entry signal

• 🔴 SELL triangle above candles → Exit signal

• Colored MAs plotted for trend clarity.

⸻

📈 Recommended Usage:

• Chart: BTC/USDT

• Timeframe: 1 Hour

• Type: Trend-following crossover strategy

• Ideal for: Identifying major breakout moves and confirming trend reversals.

⸻

⚠️ Notes:

• This script is meant for educational and backtesting purposes only.

• Always apply additional confirmation tools (like RSI, Volume, or VIX-style filters) before live trading.

• Works best during trending markets; may produce whipsaws in sideways zones.

AVWAP+RSI Confluence — 1R TesterRSI + 1R ATR - Monthly P\&L (v4)

WHAT THIS STRATEGY DOES (OVERVIEW)

* Pine strategy (v4) that combines a simple momentum trigger with a symmetric 1R ATR risk model and an on-chart Monthly/Yearly P\&L table.

* Momentum filter: trades only when RSI crosses its own SMA in the direction of the trend (price vs Trend EMA).

* Risk engine: exits use fixed 1R ATR brackets captured at entry (no drifting targets/stops).

* Accounting: the table aggregates percentage returns by month and year using strategy equity.

ENTRY LOGIC (LONGS & OPTIONAL SHORTS)

Indicators used:

* RSI(rsiLen) and its SMA: SMA(RSI, rsiMaLen)

* Trend filter: EMA(emaTrendLen) on price

Longs:

1. RSI crosses above its RSI SMA

2. RSI > rsiBuyThr (filters weak momentum)

3. Close > EMA(emaTrendLen)

Shorts (optional via enableShort):

1. RSI crosses below its RSI SMA

2. RSI < rsiSellThr

3. Close < EMA(emaTrendLen)

EXIT LOGIC AND RISK MODEL (1R ATR)

* On entry, snapshot ATR(atrLen) into atrAtEntry and the average fill price into entryPx.

* Longs: stop = entryPx - ATR \* atrMult; target = entryPx + ATR \* atrMult

* Shorts: mirrored.

* Stops and targets are posted immediately and remain fixed for the life of the trade.

POSITION SIZING AND COSTS

* Default position size: 25% of equity per trade (adjustable in Properties/inputs).

* Commission percent and a small slippage are set in strategy() so backtests include friction by default.

MONTHLY / YEARLY P\&L TABLE (HOW IT WORKS)

* Uses strategy equity to compute bar returns: equity / equity\ - 1.

* Compounds bar returns into current month and current year; commits each finished period at month/year change (or last bar).

* Renders rows as years; columns Jan..Dec plus a Year total column.

* Cells colored by sign; precision and maximum rows are controlled by inputs.

* Values represent percentage returns, not currency P\&L.

VISUAL AIDS

* Two pivot trails (pivot high/low) are plotted for context only; they do not affect entries or exits.

CUSTOMIZATION TIPS

* Raise rsiBuyThr (long) or lower rsiSellThr (short) to filter weak momentum.

* Increase emaTrendLen to tighten trend alignment.

* Adjust atrLen and atrMult to fit your timeframe/instrument volatility.

* Leave enableShort = false if you prefer long-only behavior or shorting is constrained.

NON-REPAINTING AND BACKTEST NOTES

* Signals use bar-close crosses of built-in indicators (RSI, EMA, ATR); no future bars are referenced.

* calc\_on\_every\_tick = true for responsive visuals; Strategy Tester evaluates on bar close in history.

* Backtest stop/limit fills are simulated and may differ from live execution/liquidity.

DISCLAIMERS

* Educational use only. This is not financial advice. Markets involve risk. Past performance does not guarantee future results.

INPUTS (QUICK REFERENCE)

* rsiLen, rsiMaLen, rsiBuyThr, rsiSellThr

* emaTrendLen

* atrLen, atrMult, enableShort

* leftBars, rightBars, prec, showTable, maxYearsRows

SHORT TAGLINE

RSI momentum with 1R ATR brackets and a built-in Monthly/Yearly P\&L table.

TAGS

strategy, RSI, ATR, trend, risk-management, backtest, Pine-v4

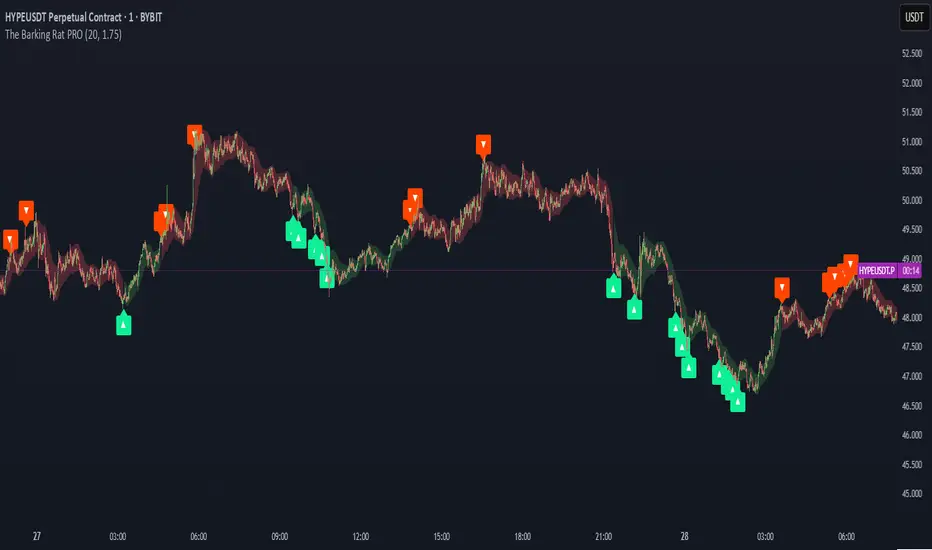

The Barking Rat PROThe Barking Rat PRO is designed around high/low pivot structure to capture meaningful market reversals. It intelligently identifies turning points by combining higher high/lower low (HH/LL) pivot detection, Fair Value Gap (FVG) confirmation, volatility-aware filters, and momentum checks. Unique features, such as a one-bar flip handler and a contextual ribbon overlay, provide traders with both clarity and precision. These tools help isolate high-probability setups while filtering out low-conviction signals, making trade opportunities easier to spot and act upon.

🧠 Core Logic: Structure-First, Filtered Reversals

The strategy takes a methodical, disciplined approach, prioritizing structural pivots over random signals. By layering multiple validation checks—structural pivots, gap confirmation, volatility filters, and momentum alignment—it highlights trades with high conviction while reducing exposure to noisy market conditions. The result is a clear, repeatable framework for reversal trading that can be applied across timeframes.

HH/LL Pivot Framework

Trades are triggered based on simple structural pivots: higher highs (HH) and lower lows (LL). When a structure flip occurs, the strategy either opens a new position or executes a one-bar delayed flip if an opposing position already exists. This ensures smooth transitions and avoids premature entries on minor market swings, keeping trading decisions focused on meaningful trend shifts.

Volatility & Distance Filters

To avoid low-quality trades, entries are validated against relative volatility, ensuring that pivots represent significant market movement. Trades must also be sufficiently spaced from previous entries and separated by a minimum number of bars, which prevents overtrading and clustered signals that can dilute performance.

Momentum Filter (RSI)

The strategy optionally aligns entries with momentum conditions using RSI. Long trades are favored when RSI is relatively low, suggesting potential exhaustion on the downside, while short trades are favored when RSI is relatively high, indicating potential overextension on the upside. This additional layer improves timing, helping traders avoid entering against strong, ongoing momentum.

Background Ribbon (Contextual Visuals)

A translucent ribbon overlays the chart to provide visual context of active trades. The ribbon displays volatility envelopes and position direction: green for long trades, red for short trades. It enhances clarity by giving traders a quick visual reference of the market environment without cluttering the chart.

Why These Parameters Were Chosen

The strategy focuses only on structurally meaningful pivots to ensure high-conviction trades.

Volatility filters confirm that trade signals are significant relative to recent price action, while FVG confirmation captures institutional-style imbalances.

Momentum and spacing rules prevent low-quality entries and overtrading, while the one-bar flip handler ensures seamless transitions when the structure reverses.

Ribbon overlays provide intuitive, real-time visualization of active trades and market context.

📈 Chart Visuals: Clear & Intuitive

- Green “▲” below a candle: Long entry triggered on LL → HH structure flip

- Red “▼” above a candle: Short entry triggered on HH → LL structure flip

- Translucent Ribbon: Green when long, Red when short

🔔 Alerts: Stay Notified Without Watching

The strategy supports real-time alerts on candle close, ensuring that only fully confirmed signals trigger notifications.

You must manually configure alerts within your TradingView account. Once set up, a single alert per instrument covers all relevant entries and exits, making hands-free monitoring simple and efficient.

⚙️ Strategy Report Properties

Position size: 25% of equity per trade

Initial capital: 10,000.00 USDT

Pyramiding: 25 entries per direction

Slippage: 2 ticks

Commission: 0.055% per side

Backtest timeframe: 1-minute

Backtest instrument: HYPEUSDT

Backtesting range: Aug 11, 2025 — Aug 28, 2025

💡Why 25% Equity Per Trade?

While it's always best to size positions based on personal risk tolerance, we defaulted to 25% equity per trade in the backtesting data — and here’s why:

Backtests using this sizing show manageable drawdowns even under volatile periods

The strategy generates a sizeable number of trades, reducing reliance on a single outcome

Combined with conservative filters, the 25% setting offers a balance between aggression and control

Users are strongly encouraged to customize this to suit their risk profile.

🔍 What Makes This Strategy Unique?

HH/LL Pivot Focus: Trades pivot structure flips instead of relying on generic indicators.

Fair Value Gap Confirmation: Only pivots supported by FVGs are acted upon, reducing noise.

One-Bar Flip Handler: Ensures clean transitions when the structure reverses, avoiding same-bar conflicts.

Volatility & Spacing Filters: Trades require sufficient movement from prior entries and minimum bar spacing to maintain quality.

Momentum-Aware Entries: RSI alignment favors entries near potential exhaustion points, improving signal reliability.

Contextual Ribbon Overlay: Visualizes volatility and active positions clearly, without cluttering the chart.

The Barking Rat LiteMomentum & FVG Reversion Strategy

The Barking Rat Lite is a disciplined, short-term mean-reversion strategy that combines RSI momentum filtering, EMA bands, and Fair Value Gap (FVG) detection to identify short-term reversal points. Designed for practical use on volatile markets, it focuses on precise entries and ATR-based take profit management to balance opportunity and risk.

Core Concept

This strategy seeks potential reversals when short-term price action shows exhaustion outside an EMA band, confirmed by momentum and FVG signals:

EMA Bands:

Parameters used: A 20-period EMA (fast) and 100-period EMA (slow).

Why chosen:

- The 20 EMA is sensitive to short-term moves and reflects immediate momentum.

- The 100 EMA provides a slower, structural anchor.

When price trades outside both bands, it often signals overextension relative to both short-term and medium-term trends.

Application in strategy:

- Long entries are only considered when price dips below both EMAs, identifying potential undervaluation.

- Short entries are only considered when price rises above both EMAs, identifying potential overvaluation.

This dual-band filter avoids counter-trend signals that would occur if only a single EMA was used, making entries more selective..

Fair Value Gap Detection (FVG):

Parameters used: The script checks for dislocations using a 12-bar lookback (i.e. comparing current highs/lows with values 12 candles back).

Why chosen:

- A 12-bar displacement highlights significant inefficiencies in price structure while filtering out micro-gaps that appear every few bars in high-volatility markets.

- By aligning FVG signals with candle direction (bullish = close > open, bearish = close < open), the strategy avoids random gaps and instead targets ones that suggest exhaustion.

Application in strategy:

- Bullish FVGs form when earlier lows sit above current highs, hinting at downward over-extension.

- Bearish FVGs form when earlier highs sit below current lows, hinting at upward over-extension.

This gives the strategy a structural filter beyond simple oscillators, ensuring signals have price-dislocation context.

RSI Momentum Filter:

Parameters used: 14-period RSI with thresholds of 80 (overbought) and 20 (oversold).

Why chosen:

- RSI(14) is a widely recognized momentum measure that balances responsiveness with stability.

- The thresholds are intentionally extreme (80/20 vs. the more common 70/30), so the strategy only engages at genuine exhaustion points rather than frequent minor corrections.

Application in strategy:

- Longs trigger when RSI < 20, suggesting oversold exhaustion.

- Shorts trigger when RSI > 80, suggesting overbought exhaustion.

This ensures entries are not just technically valid but also backed by momentum extremes, raising conviction.

ATR-Based Take Profit:

Parameters used: 14-period ATR, with a default multiplier of 4.

Why chosen:

- ATR(14) reflects the prevailing volatility environment without reacting too much to outliers.

- A multiplier of 4 is a pragmatic compromise: wide enough to let trades breathe in volatile conditions, but tight enough to enforce disciplined exits before mean reversion fades.

Application in strategy:

- At entry, a fixed target is set = Entry Price ± (ATR × 4).

- This target scales automatically with volatility: narrower in calm periods, wider in explosive markets.

By avoiding discretionary exits, the system maintains rule-based discipline.

Visual Signals on Chart

Blue “▲” below candle: Potential long entry

Orange/Yellow “▼” above candle: Potential short entry

Green “✔️”: Trade closed at ATR take profit

Blue (20 EMA) & Orange (100 EMA) lines: Dynamic channel reference

⚙️Strategy report properties

Position size: 25% equity per trade

Initial capital: 10,000.00 USDT

Pyramiding: 10 entries per direction

Slippage: 2 ticks

Commission: 0.055% per side

Backtest timeframe: 1-minute

Backtest instrument: HYPEUSDT

Backtesting range: Jul 28, 2025 — Aug 17, 2025

Note on Sample Size:

You’ll notice the report displays fewer than the ideal 100 trades in the strategy report above. This is intentional. The goal of the script is to isolate high-quality, short-term reversal opportunities while filtering out low-conviction setups. This means that the Barking Rat Lite strategy is very selective, filtering out over 90% of market noise. The brief timeframe shown in the strategy report here illustrates its filtering logic over a short window — not its full capabilities. As a result, even on lower timeframes like the 1-minute chart, signals are deliberately sparse — each one must pass all criteria before triggering.

For a larger dataset:

Once the strategy is applied to your chart, users are encouraged to expand the lookback range or apply the strategy to other volatile pairs to view a full sample.

💡Why 25% Equity Per Trade?

While it's always best to size positions based on personal risk tolerance, we defaulted to 25% equity per trade in the backtesting data — and here’s why:

Backtests using this sizing show manageable drawdowns even under volatile periods.

The strategy generates a sizeable number of trades, reducing reliance on a single outcome.

Combined with conservative filters, the 25% setting offers a balance between aggression and control.

Users are strongly encouraged to customize this to suit their risk profile.

What makes Barking Rat Lite valuable

Combines multiple layers of confirmation: EMA bands + FVG + RSI

Adaptive to volatility: ATR-based exits scale with market conditions

Clear, actionable visuals: Easy to monitor and manage trades

The Barking Rat PercentilesPercentile Reversion with Multi-Layered Smoothing

The Barking Rat Percentiles is a multi-tiered reversion strategy based on fixed percentage movements away from the mean, designed to capture price extremes through a structured, practical approach. It combines statistically derived percentile bands, RSI momentum filtering, and ATR-driven exits to identify potential turning points while managing opportunity with precision. The aim is to isolate high-quality reversal opportunities at progressively deeper extremes while avoiding noise and low-conviction setups.

At its core, the strategy measures the current market position relative to long-term percentile thresholds. When price moves significantly beyond these smoothed levels and momentum shows signs of exhaustion, staged entries are triggered. Exits are managed using independent ATR-based take profit and stop loss logic to adapt to varying volatility conditions.

🧠 Core Logic: Tiered Extremes & Structured Management

This strategy is intentionally methodical, layering multiple thresholds and validation checks before highlighting potential setups. By combining percentile-based extremes with momentum confirmation and adaptive trade management, it offers a disciplined and repeatable framework for mean reversion trading.

1. Percentile Thresholds as the Primary Framework

The script calculates the highest high and lowest low over a long lookback period of more than 1000 candles to define the overall price range. It then derives upper and lower percentile thresholds to determine extreme price levels. These thresholds are smoothed using a simple moving average to filter out short-term noise, ensuring that only statistically significant deviations from the mean are considered for potential trades.

2. Multi-Tier Entry Levels

Based on the percentile distance away from the mean, the script plots and references five discrete trigger levels beyond the primary thresholds for both long and short positions. Each tier represents progressively deeper extremes, typically 1–3% beyond the smoothed threshold, balancing the benefits of early entries with the safety of more confirmed extremes. Custom logic ensures only one signal is generated per threshold level, avoiding duplicate entries in the same zone.

3. RSI Momentum Filter

A 14-period RSI filter is applied to prevent entering trades against strong momentum. Long trades are only triggered when RSI falls below 30 (oversold), and short trades only when RSI rises above 70 (overbought). This helps align entries with potential exhaustion points, reducing the risk of entering prematurely into a strong ongoing trend.

4. ATR-Based Trade Management

For each trade sequence, the strategy will exit on the first exit condition met: either the take profit (TP) or the stop loss (SL). Because the TP uses a smaller ATR multiplier, it’s generally closer to the entry price, so most trades will hit the TP before reaching the SL. The SL is intentionally set with a larger ATR multiplier to give the trade room to develop, acting as a protective fallback rather than a frequent exit.

So in practice, you’ll usually see the TP executed for a trade, and the SL only triggers in cases where price moves further against the position than expected.

5. Position Reset Logic

Once price returns to the smoothed threshold region, all entry tiers in that direction are reset. This allows the system to prepare for new opportunities if the market revisits extreme levels, without triggering duplicate trades at the same threshold.

Why These Parameters Were Chosen

Multi-tier thresholds ensure that only meaningful extremes are acted upon, while the long-range SMA provides historical context and filters out noise. The staged entry logic per level balances the desire for early participation with the discipline of risk management. ATR-based TP and SL levels adapt to changing volatility, while the RSI filter improves timing by aligning trades with potential exhaustion points. Together, these elements create a balanced, structured, and repeatable approach to mean reversion trading.

📈 Chart Visuals: Clear & Intuitive

Green “▲” below a candle: Potential long entry

Red “▼” above a candle: Potential short entry

Blue “✔️”: Exit when ATR take profit is hit

Orange “✘”: Exit when ATR stop loss is hit

Tier threshold lines (smoothed upper/lower bounds)

🔔Alerts: Stay Notified Without Watching

The strategy supports real-time alerts on candle close, ensuring that signals are only triggered once fully confirmed.

You must manually set up alerts within your TradingView account. Once configured, you’ll be able to set up one alert per instrument. This one alert covers all relevant signals and exits — ideal for hands-free monitoring.

⚙️Strategy report properties

Position size: 25% equity per trade

Initial capital: 10,000.00 USDT

Pyramiding: 10 entries per direction

Slippage: 2 ticks

Commission: 0.055% per side

Backtest timeframe: 1-minute

Backtest instrument: SOLUSDT

Backtesting range: Jul 28, 2025 — Aug 14, 2025

Note on Sample Size:

You’ll notice the report displays fewer than the ideal 100 trades in the strategy report above. This is intentional. The goal of the script is to isolate high-quality, short-term reversal opportunities while filtering out low-conviction setups. This means that the Barking Rat Percentiles strategy is ultra-selective, filtering out over 90% of market noise by enforcing multiple validation layers. The brief timeframe shown in the strategy report here illustrates its filtering logic over a short window — not its full capabilities. As a result, even on lower timeframes like the 1-minute chart, signals are deliberately sparse — each one must pass all criteria before triggering.

For a larger dataset:

Once the strategy is applied to your chart, users are encouraged to expand the lookback range or apply the strategy to other volatile pairs to view a full sample.

💡Why 25% Equity Per Trade?

While it's always best to size positions based on personal risk tolerance, we defaulted to 25% equity per trade in the backtesting data — and here’s why:

Backtests using this sizing show manageable drawdowns even under volatile periods

The strategy generates a sizeable number of trades, reducing reliance on a single outcome

Combined with conservative filters, the 25% setting offers a balance between aggression and control

Users are strongly encouraged to customize this to suit their risk profile.

🔍 What Makes This Strategy Unique?

Multi-Tier Percentile Triggers – Instead of relying on a single overbought/oversold zone, this strategy uses five distinct entry tiers per direction, allowing for staged, precision entries at progressively deeper extremes.

Long-Term Percentile Smoothing – By calculating extremes over a 1000+ candle range and smoothing them with a moving average, the strategy focuses only on statistically significant deviations.

Custom One-Signal-Per-Tier Logic – Prevents duplicate trades at the same threshold level, reducing overtrading and noise.

Dual ATR Exit System – Independent TP and SL levels adapt to volatility. TP uses a smaller ATR multiplier for realistic, achievable exits and generally executes first, while the SL has a larger ATR multiplier to provide protective breathing room if the trade moves further against the position.

Momentum-Aware Filtering – A 14-period RSI filter ensures trades are only taken when momentum is likely exhausted, avoiding entries into strong trends.

Automatic Position Reset – Once price normalizes, tiers reset, allowing for fresh entries without interference from previous trades.

Commander Sparks | 1:1 Daily Core (Prop-Mode Overnight)Features

Trend Filter: EMA50 > EMA200 (long bias), EMA50 < EMA200 (short bias).

VWAP Filter: Only buys above VWAP, sells below VWAP.

Bollinger Band Filter: Avoids chop — enters only when price is outside BB midline in trend direction.

MACD Momentum: Entry only when MACD line crosses signal line in trend direction.

Risk Control: ATR-based stop, exactly 1:1 target, fixed full exit.

Time Filter: Trades 24/5 — including overnight & Sunday reopen.

No pyramiding — 1 trade per signal.

Entries allowed: 6:00 PM → 3:55 PM ET (1800-1555)

Auto-flat: 3:55–4:00 PM ET (so you’re flat before the 4:00 PM cutoff)

Toggle Prop Mode OFF anytime to trade 24/5 with no time limits.

Dskyz (DAFE) GENESIS Dskyz (DAFE) GENESIS: Adaptive Quant, Real Regime Power

Let’s be honest: Most published strategies on TradingView look nearly identical—copy-paste “open-source quant,” generic “adaptive” buzzwords, the same shallow explanations. I’ve even fallen into this trap with my own previously posted strategies. Not this time.

What Makes This Unique

GENESIS is not a black-box mashup or a pre-built template. It’s the culmination of DAFE’s own adaptive, multi-factor, regime-aware quant engine—built to outperform, survive, and visualize live edge in anything from NQ/MNQ to stocks and crypto.

True multi-factor core: Volume/price imbalances, trend shifts, volatility compression/expansion, and RSI all interlock for signal creation.

Adaptive regime logic: Trades only in healthy, actionable conditions—no “one-size-fits-all” signals.

Momentum normalization: Uses rolling, percentile-based fast/slow EMA differentials, ALWAYS normalized, ALWAYS relevant—no “is it working?” ambiguity.

Position sizing that adapts: Not fixed-lot, not naive—not a loophole for revenge trading.

No hidden DCA or pyramiding—what you see is what you trade.

Dashboard and visual system: Directly connected to internal logic. If it’s shown, it’s used—and nothing cosmetic is presented on your chart that isn’t quantifiable.

📊 Inputs and What They Mean (Read Carefully)

Maximum Raw Score: How many distinct factors can contribute to regime/trade confidence (default 4). If you extend the quant logic, increase this.

RSI Length / Min RSI for Shorts / Max RSI for Longs: Fine-tunes how “overbought/oversold” matters; increase the length for smoother swings, tighten floors/ceilings for more extreme signals.

⚡ Regime & Momentum Gates

Min Normed Momentum/Score (Conf): Raise to demand only the strongest trends—your filter to avoid algorithmic chop.

🕒 Volatility & Session

ATR Lookback, ATR Low/High Percentile: These control your system’s awareness of when the market is dead or ultra-volatile. All sizing and filter logic adapts in real time.

Trading Session (hours): Easy filter for when entries are allowed; default is regular trading hours—no surprise overnight fills.

📊 Sizing & Risk

Max Dollar Risk / Base-Max Contracts: All sizing is adaptive, based on live regime and volatility state—never static or “just 1 contract.” Control your max exposures and real $ risk. ATR will effect losses in high volatility times.

🔄 Exits & Scaling

Stop/Trail/Scale multipliers: You choose how dynamic/flexible risk controls and profit-taking need to be. ATR-based, so everything auto-adjusts to the current market mode.

Visuals That Actually Matter

Dashboard (Top Right): Shows only live, relevant stats: scoring, status, position size, win %, win streak, total wins—all from actual trade engine state (not “simulated”).

Watermark (Bottom Right): Momentum bar visual is always-on, regime-aware, reflecting live regime confidence and momentum normalization. If the bar is empty, you’re truly in no-momentum. If it glows lime, you’re riding the strongest possible edge.

*No cosmetics, no hidden code distractions.

Backtest Settings

Initial capital: $10,000

Commission: Conservative, realistic roundtrip cost:

15–20 per contract (including slippage per side) I set this to $25

Slippage: 3 ticks per trade

Symbol: CME_MINI:NQ1!

Timeframe: 1 min (but works on all timeframes)

Order size: Adaptive, 1–3 contracts

No pyramiding, no hidden DCA

Why these settings?

These settings are intentionally strict and realistic, reflecting the true costs and risks of live trading. The 10,000 account size is accessible for most retail traders. 25/contract including 3 ticks of slippage are on the high side for NQ, ensuring the strategy is not curve-fit to perfect fills. If it works here, it will work in real conditions.

Why It Wins

While others put out “AI-powered” strategies with little logic or soul, GENESIS is ruthlessly practical. It is built around what keeps traders alive:

- Context-aware signals, not just patterns

- Tight, transparent risk

- Inputs that adapt, not confuse

- Visuals that clarify, not distract

- Code that runs clean, efficient, and with minimal overfitting risk (try it on QQQ, AMD, SOL, etc. out of the box)

Disclaimer (for TradingView compliance):

Trading is risky. Futures, stocks, and crypto can result in significant losses. Do not trade with funds you cannot afford to lose. This is for educational and informational purposes only. Use in simulation/backtest mode before live trading. No past performance is indicative of future results. Always understand your risk and ownership of your trades.

This will not be my last—my goal is to keep raising the bar until DAFE is a brand or I’m forced to take this private.

Use with discipline, use with clarity, and always trade smarter.

— Dskyz , powered by DAFE Trading Systems.

Dskyz (DAFE) Adaptive Regime - Quant Machine ProDskyz (DAFE) Adaptive Regime - Quant Machine Pro:

Buckle up for the Dskyz (DAFE) Adaptive Regime - Quant Machine Pro, is a strategy that’s your ultimate edge for conquering futures markets like ES, MES, NQ, and MNQ. This isn’t just another script—it’s a quant-grade powerhouse, crafted with precision to adapt to market regimes, deliver multi-factor signals, and protect your capital with futures-tuned risk management. With its shimmering DAFE visuals, dual dashboards, and glowing watermark, it turns your charts into a cyberpunk command center, making trading as thrilling as it is profitable.

Unlike generic scripts clogging up the space, the Adaptive Regime is a DAFE original, built from the ground up to tackle the chaos of futures trading. It identifies market regimes (Trending, Range, Volatile, Quiet) using ADX, Bollinger Bands, and HTF indicators, then fires trades based on a weighted scoring system that blends candlestick patterns, RSI, MACD, and more. Add in dynamic stops, trailing exits, and a 5% drawdown circuit breaker, and you’ve got a system that’s as safe as it is aggressive. Whether you’re a newbie or a prop desk pro, this strat’s your ticket to outsmarting the markets. Let’s break down every detail and see why it’s a must-have.

Why Traders Need This Strategy

Futures markets are a gauntlet—fast moves, volatility spikes (like the April 28, 2025 NQ 1k-point drop), and institutional traps that punish the unprepared. Meanwhile, platforms are flooded with low-effort scripts that recycle old ideas with zero innovation. The Adaptive Regime stands tall, offering:

Adaptive Intelligence: Detects market regimes (Trending, Range, Volatile, Quiet) to optimize signals, unlike one-size-fits-all scripts.

Multi-Factor Precision: Combines candlestick patterns, MA trends, RSI, MACD, volume, and HTF confirmation for high-probability trades.

Futures-Optimized Risk: Calculates position sizes based on $ risk (default: $300), with ATR or fixed stops/TPs tailored for ES/MES.

Bulletproof Safety: 5% daily drawdown circuit breaker and trailing stops keep your account intact, even in chaos.

DAFE Visual Mastery: Pulsing Bollinger Band fills, dynamic SL/TP lines, and dual dashboards (metrics + position) make signals crystal-clear and charts a work of art.

Original Craftsmanship: A DAFE creation, built with community passion, not a rehashed clone of generic code.

Traders need this because it’s a complete, adaptive system that blends quant smarts, user-friendly design, and DAFE flair. It’s your edge to trade with confidence, cut through market noise, and leave the copycats in the dust.

Strategy Components

1. Market Regime Detection

The strategy’s brain is its ability to classify market conditions into five regimes, ensuring signals match the environment.

How It Works:

Trending (Regime 1): ADX > 20, fast/slow EMA spread > 0.3x ATR, HTF RSI > 50 or MACD bullish (htf_trend_bull/bear).

Range (Regime 2): ADX < 25, price range < 3% of close, no HTF trend.

Volatile (Regime 3): BB width > 1.5x avg, ATR > 1.2x avg, HTF RSI overbought/oversold.

Quiet (Regime 4): BB width < 0.8x avg, ATR < 0.9x avg.

Other (Regime 5): Default for unclear conditions.

Indicators: ADX (14), BB width (20), ATR (14, 50-bar SMA), HTF RSI (14, daily default), HTF MACD (12,26,9).

Why It’s Brilliant:

Regime detection adapts signals to market context, boosting win rates in trending or volatile conditions.

HTF RSI/MACD add a big-picture filter, rare in basic scripts.

Visualized via gradient background (green for Trending, orange for Range, red for Volatile, gray for Quiet, navy for Other).

2. Multi-Factor Signal Scoring

Entries are driven by a weighted scoring system that combines candlestick patterns, trend, momentum, and volume for robust signals.

Candlestick Patterns:

Bullish: Engulfing (0.5), hammer (0.4 in Range, 0.2 else), morning star (0.2), piercing (0.2), double bottom (0.3 in Volatile, 0.15 else). Must be near support (low ≤ 1.01x 20-bar low) with volume spike (>1.5x 20-bar avg).

Bearish: Engulfing (0.5), shooting star (0.4 in Range, 0.2 else), evening star (0.2), dark cloud (0.2), double top (0.3 in Volatile, 0.15 else). Must be near resistance (high ≥ 0.99x 20-bar high) with volume spike.

Logic: Patterns are weighted higher in specific regimes (e.g., hammer in Range, double bottom in Volatile).

Additional Factors:

Trend: Fast EMA (20) > slow EMA (50) + 0.5x ATR (trend_bull, +0.2); opposite for trend_bear.

RSI: RSI (14) < 30 (rsi_bull, +0.15); > 70 (rsi_bear, +0.15).

MACD: MACD line > signal (12,26,9, macd_bull, +0.15); opposite for macd_bear.

Volume: ATR > 1.2x 50-bar avg (vol_expansion, +0.1).

HTF Confirmation: HTF RSI < 70 and MACD bullish (htf_bull_confirm, +0.2); RSI > 30 and MACD bearish (htf_bear_confirm, +0.2).

Scoring:

bull_score = sum of bullish factors; bear_score = sum of bearish. Entry requires score ≥ 1.0.

Example: Bullish engulfing (0.5) + trend_bull (0.2) + rsi_bull (0.15) + htf_bull_confirm (0.2) = 1.05, triggers long.

Why It’s Brilliant:

Multi-factor scoring ensures signals are confirmed by multiple market dynamics, reducing false positives.

Regime-specific weights make patterns more relevant (e.g., hammers shine in Range markets).

HTF confirmation aligns with the big picture, a quant edge over simplistic scripts.

3. Futures-Tuned Risk Management

The risk system is built for futures, calculating position sizes based on $ risk and offering flexible stops/TPs.

Position Sizing:

Logic: Risk per trade (default: $300) ÷ (stop distance in points * point value) = contracts, capped at max_contracts (default: 5). Point value = tick value (e.g., $12.5 for ES) * ticks per point (4) * contract multiplier (1 for ES, 0.1 for MES).

Example: $300 risk, 8-point stop, ES ($50/point) → 0.75 contracts, rounded to 1.

Impact: Precise sizing prevents over-leverage, critical for micro contracts like MES.

Stops and Take-Profits:

Fixed: Default stop = 8 points, TP = 16 points (2:1 reward/risk).

ATR-Based: Stop = 1.5x ATR (default), TP = 3x ATR, enabled via use_atr_for_stops.

Logic: Stops set at swing low/high ± stop distance; TPs at 2x stop distance from entry.

Impact: ATR stops adapt to volatility, while fixed stops suit stable markets.

Trailing Stops:

Logic: Activates at 50% of TP distance. Trails at close ± 1.5x ATR (atr_multiplier). Longs: max(trail_stop_long, close - ATR * 1.5); shorts: min(trail_stop_short, close + ATR * 1.5).

Impact: Locks in profits during trends, a game-changer in volatile sessions.

Circuit Breaker:

Logic: Pauses trading if daily drawdown > 5% (daily_drawdown = (max_equity - equity) / max_equity).

Impact: Protects capital during black swan events (e.g., April 27, 2025 ES slippage).

Why It’s Brilliant:

Futures-specific inputs (tick value, multiplier) make it plug-and-play for ES/MES.

Trailing stops and circuit breaker add pro-level safety, rare in off-the-shelf scripts.

Flexible stops (ATR or fixed) suit different trading styles.

4. Trade Entry and Exit Logic

Entries and exits are precise, driven by bull_score/bear_score and protected by drawdown checks.

Entry Conditions:

Long: bull_score ≥ 1.0, no position (position_size <= 0), drawdown < 5% (not pause_trading). Calculates contracts, sets stop at swing low - stop points, TP at 2x stop distance.

Short: bear_score ≥ 1.0, position_size >= 0, drawdown < 5%. Stop at swing high + stop points, TP at 2x stop distance.

Logic: Tracks entry_regime for PNL arrays. Closes opposite positions before entering.

Exit Conditions:

Stop-Loss/Take-Profit: Hits stop or TP (strategy.exit).

Trailing Stop: Activates at 50% TP, trails by ATR * 1.5.

Emergency Exit: Closes if price breaches stop (close < long_stop_price or close > short_stop_price).

Reset: Clears stop/TP prices when flat (position_size = 0).

Why It’s Brilliant:

Score-based entries ensure multi-factor confirmation, filtering out weak signals.

Trailing stops maximize profits in trends, unlike static exits in basic scripts.

Emergency exits add an extra safety layer, critical for futures volatility.

5. DAFE Visuals

The visuals are pure DAFE magic, blending function with cyberpunk flair to make signals intuitive and charts stunning.

Shimmering Bollinger Band Fill:

Display: BB basis (20, white), upper/lower (green/red, 45% transparent). Fill pulses (30–50 alpha) by regime, with glow (60–95 alpha) near bands (close ≥ 0.995x upper or ≤ 1.005x lower).

Purpose: Highlights volatility and key levels with a futuristic glow.

Visuals make complex regimes and signals instantly clear, even for newbies.

Pulsing effects and regime-specific colors add a DAFE signature, setting it apart from generic scripts.

BB glow emphasizes tradeable levels, enhancing decision-making.

Chart Background (Regime Heatmap):

Green — Trending Market: Strong, sustained price movement in one direction. The market is in a trend phase—momentum follows through.

Orange — Range-Bound: Market is consolidating or moving sideways, with no clear up/down trend. Great for mean reversion setups.

Red — Volatile Regime: High volatility, heightened risk, and larger/faster price swings—trade with caution.

Gray — Quiet/Low Volatility: Market is calm and inactive, with small moves—often poor conditions for most strategies.

Navy — Other/Neutral: Regime is uncertain or mixed; signals may be less reliable.

Bollinger Bands Glow (Dynamic Fill):

Neon Red Glow — Warning!: Price is near or breaking above the upper band; momentum is overstretched, watch for overbought conditions or reversals.

Bright Green Glow — Opportunity!: Price is near or breaking below the lower band; market could be oversold, prime for bounce or reversal.

Trend Green Fill — Trending Regime: Fills between bands with green when the market is trending, showing clear momentum.

Gold/Yellow Fill — Range Regime: Fills with gold/aqua in range conditions, showing the market is sideways/oscillating.

Magenta/Red Fill — Volatility Spike: Fills with vivid magenta/red during highly volatile regimes.

Blue Fill — Neutral/Quiet: A soft blue glow for other or uncertain market states.

Moving Averages:

Display: Blue fast EMA (20), red slow EMA (50), 2px.

Purpose: Shows trend direction, with trend_dir requiring ATR-scaled spread.

Dynamic SL/TP Lines:

Display: Pulsing colors (red SL, green TP for Trending; yellow/orange for Range, etc.), 3px, with pulse_alpha for shimmer.

Purpose: Tracks stops/TPs in real-time, color-coded by regime.

6. Dual Dashboards

Two dashboards deliver real-time insights, making the strat a quant command center.

Bottom-Left Metrics Dashboard (2x13):

Metrics: Mode (Active/Paused), trend (Bullish/Bearish/Neutral), ATR, ATR avg, volume spike (YES/NO), RSI (value + Oversold/Overbought/Neutral), HTF RSI, HTF trend, last signal (Buy/Sell/None), regime, bull score.

Display: Black (29% transparent), purple title, color-coded (green for bullish, red for bearish).

Purpose: Consolidates market context and signal strength.

Top-Right Position Dashboard (2x7):

Metrics: Regime, position side (Long/Short/None), position PNL ($), SL, TP, daily PNL ($).

Display: Black (29% transparent), purple title, color-coded (lime for Long, red for Short).

Purpose: Tracks live trades and profitability.

Why It’s Brilliant:

Dual dashboards cover market context and trade status, a rare feature.

Color-coding and concise metrics guide beginners (e.g., green “Buy” = go).

Real-time PNL and SL/TP visibility empower disciplined trading.

7. Performance Tracking

Logic: Arrays (regime_pnl_long/short, regime_win/loss_long/short) track PNL and win/loss by regime (1–5). Updated on trade close (barstate.isconfirmed).

Purpose: Prepares for future adaptive thresholds (e.g., adjust bull_score min based on regime performance).

Why It’s Brilliant: Lays the groundwork for self-optimizing logic, a quant edge over static scripts.

Key Features

Regime-Adaptive: Optimizes signals for Trending, Range, Volatile, Quiet markets.

Futures-Optimized: Precise sizing for ES/MES with tick-based risk inputs.

Multi-Factor Signals: Candlestick patterns, RSI, MACD, and HTF confirmation for robust entries.

Dynamic Exits: ATR/fixed stops, 2:1 TPs, and trailing stops maximize profits.

Safe and Smart: 5% drawdown breaker and emergency exits protect capital.

DAFE Visuals: Shimmering BB fill, pulsing SL/TP, and dual dashboards.

Backtest-Ready: Fixed qty and tick calc for accurate historical testing.

How to Use

Add to Chart: Load on a 5min ES/MES chart in TradingView.

Configure Inputs: Set instrument (ES/MES), tick value ($12.5/$1.25), multiplier (1/0.1), risk ($300 default). Enable ATR stops for volatility.

Monitor Dashboards: Bottom-left for regime/signals, top-right for position/PNL.

Backtest: Run in strategy tester to compare regimes.

Live Trade: Connect to Tradovate or similar. Watch for slippage (e.g., April 27, 2025 ES issues).

Replay Test: Try April 28, 2025 NQ drop to see regime shifts and stops.

Disclaimer

Trading futures involves significant risk of loss and is not suitable for all investors. Past performance does not guarantee future results. Backtest results may differ from live trading due to slippage, fees, or market conditions. Use this strategy at your own risk, and consult a financial advisor before trading. Dskyz (DAFE) Trading Systems is not responsible for any losses incurred.

Backtesting:

Frame: 2023-09-20 - 2025-04-29

Slippage: 3

Fee Typical Range (per side, per contract)

CME Exchange $1.14 – $1.20

Clearing $0.10 – $0.30

NFA Regulatory $0.02

Firm/Broker Commis. $0.25 – $0.80 (retail prop)

TOTAL $1.60 – $2.30 per side

Round Turn: (enter+exit) = $3.20 – $4.60 per contract

Final Notes

The Dskyz (DAFE) Adaptive Regime - Quant Machine Pro is more than a strategy—it’s a revolution. Crafted with DAFE’s signature precision, it rises above generic scripts with adaptive regimes, quant-grade signals, and visuals that make trading a thrill. Whether you’re scalping MES or swinging ES, this system empowers you to navigate markets with confidence and style. Join the DAFE crew, light up your charts, and let’s dominate the futures game!

(This publishing will most likely be taken down do to some miscellaneous rule about properly displaying charting symbols, or whatever. Once I've identified what part of the publishing they want to pick on, I'll adjust and repost.)

Use it with discipline. Use it with clarity. Trade smarter.

**I will continue to release incredible strategies and indicators until I turn this into a brand or until someone offers me a contract.

Created by Dskyz, powered by DAFE Trading Systems. Trade smart, trade bold.

Dskyz (DAFE) Quantum Sentiment Flux - Beginners Dskyz (DAFE) Quantum Sentiment Flux - Beginners:

Welcome to the Dskyz (DAFE) Quantum Sentiment Flux - Beginners , a strategy and concept that’s your ultimate wingman for trading futures like MNQ, NQ, MES, and ES. This gem combines lightning-fast momentum signals, market sentiment smarts, and bulletproof risk management into a system so intuitive, even newbies can trade like pros. With clean DAFE visuals, preset modes for every vibe, and a revamped dashboard that’s basically a market GPS, this strategy makes futures trading feel like a high-octane sci-fi mission.

Built on the Dskyz (DAFE) legacy of Aurora Divergence, the Quantum Sentiment Flux is designed to empower beginners while giving seasoned traders a lean, sentiment-driven edge. It uses fast/slow EMA crossovers for entries, filters trades with VIX, SPX trends, and sector breadth, and keeps your account safe with adaptive stops and cooldowns. Tuned for more action with faster signals and a slick bottom-left dashboard, this updated version is ready to light up your charts and outsmart institutional traps. Let’s dive into why this strat’s a must-have and break down its brilliance.

Why Traders Need This Strategy

Futures markets are a wild ride—fast moves, volatility spikes (like the April 28, 2025 NQ 1k-point drop), and institutional games that can wreck unprepared traders. Beginners often get lost in complex systems or burned by impulsive trades. The Quantum Sentiment Flux is the antidote, offering:

Dead-Simple Setup: Preset modes (Aggressive, Balanced, Conservative) auto-tune signals, risk, and sizing, so you can trade without a quant degree.

Sentiment Superpower: VIX filter, SPX trend, and sector breadth visuals keep you aligned with market health, dodging chop and riding trends.

Ironclad Safety: Tighter ATR-based stops, 2:1 take-profits, and preset cooldowns protect your capital, even in chaotic sessions.

Next-Level Visuals: Green/red entry triangles, vibrant EMAs, a sector breadth background, and a beefed-up dashboard make signals and context pop.

DAFE Swagger: The clean aesthetics, sleek dashboard—ties it to Dskyz’s elite brand, making your charts a work of art.

Traders need this because it’s a plug-and-play system that blends beginner-friendly simplicity with pro-level market awareness. Whether you’re just starting or scalping 5min MNQ, this strat’s your key to trading with confidence and style.

Strategy Components

1. Core Signal Logic (High-Speed Momentum)

The strategy’s engine is a momentum-based system using fast and slow Exponential Moving Averages (EMAs), now tuned for faster, more frequent trades.

How It Works:

Fast/Slow EMAs: Fast EMA (Aggressive: 5, Balanced: 7, Conservative: 9 bars) and slow EMA (12/14/18 bars) track short-term vs. longer-term momentum.

Crossover Signals:

Buy: Fast EMA crosses above slow EMA, and trend_dir = 1 (fast EMA > slow EMA + ATR * strength threshold).

Sell: Fast EMA crosses below slow EMA, and trend_dir = -1 (fast EMA < slow EMA - ATR * strength threshold).

Strength Filter: ma_strength = fast EMA - slow EMA must exceed an ATR-scaled threshold (Aggressive: 0.15, Balanced: 0.18, Conservative: 0.25) for robust signals.

Trend Direction: trend_dir confirms momentum, filtering out weak crossovers in choppy markets.

Evolution:

Faster EMAs (down from 7–10/21–50) catch short-term trends, perfect for active futures markets.

Lower strength thresholds (0.15–0.25 vs. 0.3–0.5) make signals more sensitive, boosting trade frequency without sacrificing quality.

Preset tuning ensures beginners get optimized settings, while pros can tweak via mode selection.

2. Market Sentiment Filters

The strategy leans hard into market sentiment with a VIX filter, SPX trend analysis, and sector breadth visuals, keeping trades aligned with the big picture.

VIX Filter:

Logic: Blocks long entries if VIX > threshold (default: 20, can_long = vix_close < vix_limit). Shorts are always allowed (can_short = true).

Impact: Prevents longs during high-fear markets (e.g., VIX spikes in crashes), while allowing shorts to capitalize on downturns.

SPX Trend Filter:

Logic: Compares S&P 500 (SPX) close to its SMA (Aggressive: 5, Balanced: 8, Conservative: 12 bars). spx_trend = 1 (UP) if close > SMA, -1 (DOWN) if < SMA, 0 (FLAT) if neutral.

Impact: Provides dashboard context, encouraging trades that align with market direction (e.g., longs in UP trend).

Sector Breadth (Visual):

Logic: Tracks 10 sector ETFs (XLK, XLF, XLE, etc.) vs. their SMAs (same lengths as SPX). Each sector scores +1 (bullish), -1 (bearish), or 0 (neutral), summed as breadth (-10 to +10).

Display: Green background if breadth > 4, red if breadth < -4, else neutral. Dashboard shows sector trends (↑/↓/-).

Impact: Faster SMA lengths make breadth more responsive, reflecting sector rotations (e.g., tech surging, energy lagging).

Why It’s Brilliant:

- VIX filter adds pro-level volatility awareness, saving beginners from panic-driven losses.

- SPX and sector breadth give a 360° view of market health, boosting signal confidence (e.g., green BG + buy signal = high-probability trade).

- Shorter SMAs make sentiment visuals react faster, perfect for 5min charts.

3. Risk Management