Stochastic Oscillator [SystemAlpha]This is a Stochastic Oscillator enhanced with:

- Show Buy and Sell Alert

- Show Regular and Hidden divergence

- Show Divergence Labels

- Generate Alerts: Buy/Sell and Divergence

Search in scripts for "oscillator"

Ehlers Decycler Oscillator [CC]The Decycler Oscillator was created by John Ehlers (Cycle Analytics For Traders pgs 43-44) and it is used to show transitions between uptrends and downtrends. If it rises above the 0 line then this means it has transitioned to an uptrend and it falls below the 0 line then it is in a downtrend. Buy if the indicator line is green and sell when it is red.

This was a custom request so let me know if you would like to see more scripts from me or if you want something custom done!

[astropark] MACD, RSI+, Awesome Oscillator, DMI with ADX//******************************************************************************

// Copyright by astropark v3.1.0

// MACD, RSI+, Awesome Oscillator, DMI, ADX

// 24/10/2018 Added RSI with Center line to have clear glue of current trend

// 10/12/2018 Added MACD

// 13/12/2018 Added multiplier for MACD in order to make it clearly visible over RSI graph

// 11/01/2019 Added Awesome Ascillator (AO)

// 11/01/2019 Added Directional Movement Index (DMI) with ADX

//******************************************************************************

Ehler Bandpass Trigger OscillatorThis is based off of Ehler's Bandpass Filter system (link below slides 15-17). Essentially Ehler runs a band pass with a given period to detrend the price data and highlight a cycle with the given frequency(length). This represents the In phase cycle. Ehler then creates the trigger line by taking the one bar momentum of the In Phase line, multiplying by 2Pi and then using this to create a 60 degree leading signal. The triggers are crossovers of the In Phase and Lead lines. You can also use conservative signals by waiting for the In Phase line to trend in the direction of the trigger crossover as well.

Length represent the cycle period you want to highlight.

Delta represents how much to influence the oscillator by the price (Delta 0 is a perfect wave)

Thanks to HPotter for the BandPass Filter code, which I used as a base for implementing the rest of the system

www.mesasoftware.com

Forecast OscillatorForecast Oscillator indicator script. This indicator was originally developed by Tushar Chande.

[RS]Multiple Majors Currency Basket Power Oscillator V1Power oscillator to discern what currency's are stronger/weaker.

added option to use a smoothed source(close) for pooling the change, giving longer term directional bias, note that this causes lag in the results as MA's turn slower than price.

[RS]Multiple Majors Currency Basket Power Oscillator V0Power oscillator to discern what currency's are stronger/weaker.

Premier RSI Oscillator [LazyBear]This is a modified form of PSO (original idea by Lee Leibfarth), to use RSI as the input.

This provides a quick response to changes in market direction. This highly sensitive indicator allows for early anticipation of price turns and can be used to establish definitive trading zones that identify potential trading opportunities.

Entry/Exit rules are the same as PSO. Enabling bar colors makes it easy to identify the entry/exits too (Refer to my comment below for more points to keep in mind regarding colors)

Here's a comparison against normal RSI.

More info:

PSO:

List of my public indicators: bit.ly

List of my app-store indicators: blog.tradingview.com

UCS_Momentum Oscillator - Version 2This is Version - 2 of the Momentum Oscillator, Like i said on the prior version, This version has an Indicator for Trends.

Marks only Overbought and Oversold Based on the TREND.

The Trend dots are calculated exactly like the Slingshot system trend.

Pivot Detector Oscillator, by Giorgos E. Siligardos The Pivot Detector Oscillator, by Giorgos E. Siligardos

The related article is copyrighted material from Stocks & Commodities 2009 Sep

Klinger Volume Oscillator (KVO) The Klinger Oscillator (KO) was developed by Stephen J. Klinger. Learning

from prior research on volume by such well-known technicians as Joseph Granville,

Larry Williams, and Marc Chaikin, Mr. Klinger set out to develop a volume-based

indicator to help in both short- and long-term analysis.

The KO was developed with two seemingly opposite goals in mind: to be sensitive

enough to signal short-term tops and bottoms, yet accurate enough to reflect the

long-term flow of money into and out of a security.

The KO is based on the following tenets:

Price range (i.e. High - Low) is a measure of movement and volume is the force behind

the movement. The sum of High + Low + Close defines a trend. Accumulation occurs when

today's sum is greater than the previous day's. Conversely, distribution occurs when

today's sum is less than the previous day's. When the sums are equal, the existing trend

is maintained.

Volume produces continuous intra-day changes in price reflecting buying and selling pressure.

The KO quantifies the difference between the number of shares being accumulated and distributed

each day as "volume force". A strong, rising volume force should accompany an uptrend and then

gradually contract over time during the latter stages of the uptrend and the early stages of

the following downtrend. This should be followed by a rising volume force reflecting some

accumulation before a bottom develops.

Money Flow Indicator (Chaikin Oscillator) Indicator plots Money Flow Indicator (Chaikin). This indicator looks

to improve on Larry William's Accumulation Distribution formula that

compared the closing price with the opening price. In the early 1970's,

opening prices for stocks stopped being transmitted by the exchanges.

This made it difficult to calculate Williams' formula. The Chaikin

Oscillator uses the average price of the bar calculated as follows

(High + Low) /2 instead of the Open.

The indicator subtracts a 10 period exponential moving average of the

AccumDist function from a 3 period exponential moving average of the

AccumDist function.

CMO Oscillator with FilterHi

Let me introduce my CMO Oscillator with Filter script.

This indicator plots a CMO which ignores price changes which are less

than a threshold value. CMO was developed by Tushar Chande. A scientist,

an inventor, and a respected trading system developer, Mr. Chande developed

the CMO to capture what he calls "pure momentum". For more definitive

information on the CMO and other indicators we recommend the book The New

Technical Trader by Tushar Chande and Stanley Kroll.

The CMO is closely related to, yet unique from, other momentum oriented

indicators such as Relative Strength Index, Stochastic, Rate-of-Change, etc.

It is most closely related to Welles Wilder`s RSI, yet it differs in several ways:

- It uses data for both up days and down days in the numerator, thereby directly

measuring momentum;

- The calculations are applied on unsmoothed data. Therefore, short-term extreme

movements in price are not hidden. Once calculated, smoothing can be applied to the

CMO, if desired;

- The scale is bounded between +100 and -100, thereby allowing you to clearly see

changes in net momentum using the 0 level. The bounded scale also allows you to

conveniently compare values across different securities.

CMO & WMA Oscillator This indicator plots Chandre Momentum Oscillator and its WMA on the

same chart. This indicator plots the absolute value of CMO. CMO was

developed by Tushar Chande. A scientist, an inventor, and a respected

trading system developer, Mr. Chande developed the CMO to capture what

he calls ?pure momentum". For more definitive information on the CMO and

other indicators we recommend the book The New Technical Trader by Tushar

Chande and Stanley Kroll.

The CMO is closely related to, yet unique from, other momentum oriented

indicators such as Relative Strength Index, Stochastic, Rate-of-Change,

etc. It is most closely related to Welles Wilder?s RSI, yet it differs

in several ways:

- It uses data for both up days and down days in the numerator, thereby

directly measuring momentum;

- The calculations are applied on unsmoothed data. Therefore, short-term

extreme movements in price are not hidden. Once calculated, smoothing

can be applied to the CMO, if desired;

- The scale is bounded between +100 and -100, thereby allowing you to clearly

see changes in net momentum using the 0 level. The bounded scale also allows

you to conveniently compare values across different securities.

CMOabs OscillatorHi

Let me introduce my CMOabs Oscillator script.

This indicator plots the absolute value of CMO. CMO was developed by Tushar

Chande. A scientist, an inventor, and a respected trading system developer,

Mr. Chande developed the CMO to capture what he calls "pure momentum". For

more definitive information on the CMO and other indicators we recommend the

book The New Technical Trader by Tushar Chande and Stanley Kroll.

The CMO is closely related to, yet unique from, other momentum oriented indicators

such as Relative Strength Index, Stochastic, Rate-of-Change, etc. It is most closely

related to Welles Wilder`s RSI, yet it differs in several ways:

- It uses data for both up days and down days in the numerator, thereby directly

measuring momentum;

- The calculations are applied on unsmoothed data. Therefore, short-term extreme

movements in price are not hidden. Once calculated, smoothing can be applied to

the CMO, if desired;

- The scale is bounded between +100 and -100, thereby allowing you to clearly see

changes in net momentum using the 0 level. The bounded scale also allows you to

conveniently compare values across different securities.

TurboVWAPoscilOscillator based on VWAP and its standard deviations. It will display VWAP as a zero line and then an indicator line showing where price is in relation to VWAP expressed as Standard Deviation units.

This indicator is based on my awesome indicator TurboVWAP, so it shares most of its features:

- you can select whether you want a rolling or an anchored VWAP as basis.

- the VWAP will auto-set itself depending on the chart timeframe, so that it will be calculated based on the period you really want, not number of bars or similar.

- you can set the indicator to auto-set session start and end times for the session-anchored VWAP depending on the futures contract selected, so you don't need to mess with times.

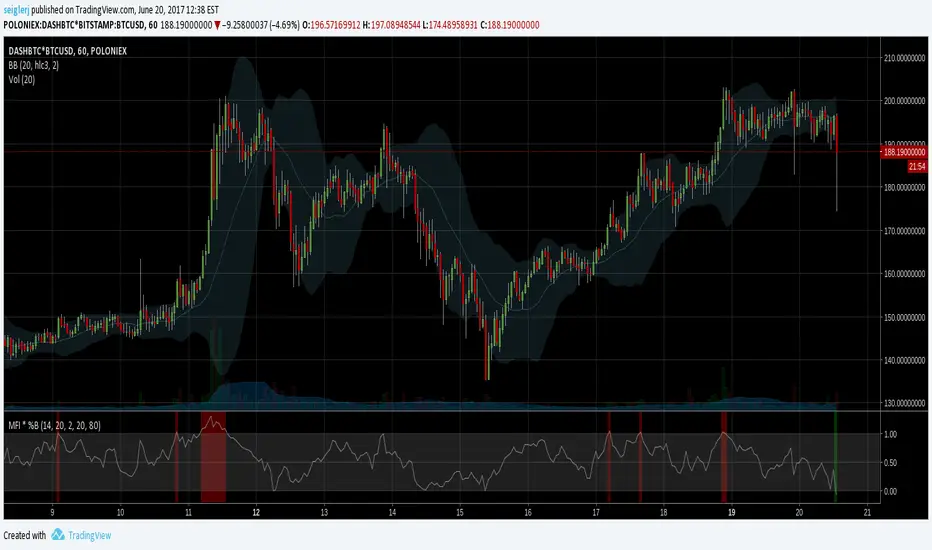

MFI * %B [seiglerj]Oscillator averaging Money Flow Index and Bollinger Bands' %B

Colored bars indicate buy or sell signals

I have no idea if this is the right way to combine these two, but I'm gonna try it and see what happens

(mab) Williams %R, RSI, Stochastic and Stochastic RSIThis indicator can display a Williams %R and a second oscillator at the same time. RSI , Stochastic or Stochastic RSI can be displayed as second oscillator. Williams %R is configured with 21 length by default and adds a 13 EMA on it (like used by TRI ). There is an option to display divergences on the oscillators.

OscillatorPivotsLibrary "OscillatorPivots"

Measures pivots in an oscillator and flags if they are above a configurable size. Uses absolute size rather than just highest/lowest in a candle range.

f_osc_Pivots()

Uses the total change in the Y axis, instead of a simple Williams pivot over a defined number of bars. In other words, it measures the size of the actual pivot, not just whether it happens to be the highest/lowest value in a range.

Measures the absolute, cumulative change both before and after the pivot, to avoid flagging mere kinks in trends.

The advantage is that absolute pivot size is, in some cases, precisely what we care about. A disadvantage is that it can take an arbitrary, perhaps long, time to confirm.

You can configure the threshold size of the pivot so that it finds large or small pivots.

Always returns a pivot high after a pivot low, then another pivot high and so on, in order. It never returns a high followed by a high, which simple indicators based on the ta.pivot() function can do.

@param chart_H_1 This must always be set to 1, unless you are using my HighTimeframeTiming library, in which case set it to the output of the function for a _HTF_H of 1.

@param chart_H_2 This must always be set to 2, unless you are using my HighTimeframeTiming library, in which case set it to the output of the function for a _HTF_H of 2.

@param _osc This is the oscillator float value.

@param _oscPivotSize This is the user setting for what counts as a big enough change to be a pivot.

@returns Information about the pivot that is likely to be useful in further calculations:

confirmPeak, confirmDip - whether the pivot was confirmed this bar

peakBarsBack, dipBarsBack - how many bars ago the actual peak or dip was

peakPrice, dipPrice - the value of the oscillator at the peak/dip

It also returns some internal variables, which are plotted in this library only for an understanding of how the function works.

debug_peakStartLevel, debug_dipStartLevel - The level of the currently active peak/dip