Enhanced Forex IndicatorDescription of the "Enhanced Forex Indicator"

The "Enhanced Forex Indicator" is designed for traders who want a comprehensive technical analysis tool on the TradingView platform. This script integrates Exponential Moving Averages (EMAs), support and resistance zones, and candlestick pattern recognition to provide actionable trading signals, particularly useful for Forex and other financial markets. The script is suitable for intraday trading and swing trading.

Components of the Indicator

Exponential Moving Averages (EMAs):

Short EMA (Blue Line): Faster responding average, good for identifying recent trend changes.

Long EMA (Red Line): Slower moving average, helps in confirming longer-term trends.

Support and Resistance Zones:

Resistance Zone (Red): Area where potential selling pressure could overcome buying pressure, halting price increases temporarily or reversing them.

Support Zone (Green): Area where potential buying pressure could overcome selling pressure, supporting prices and preventing them from falling further.

Candlestick Patterns:

Bullish Engulfing Pattern (Green Triangle Up 'BE'): Suggests a potential upward reversal or start of a bullish trend.

Bearish Engulfing Pattern (Red Triangle Down 'BE'): Indicates a potential downward reversal or start of a bearish trend.

Buy/Sell Signals:

Buy Signal (Green Label 'BUY'): Triggered when the price is above both EMAs and a bullish engulfing pattern is detected.

Sell Signal (Red Label 'SELL'): Triggered when the price is below both EMAs and a bearish engulfing pattern is detected.

Trading Setup:

Entry: Consider entering a buy position when the 'BUY' signal appears, indicating bullish conditions. Enter a sell position when the 'SELL' signal appears, indicating bearish conditions.

Exit: Look for closing signals opposite your entry or use predefined take profit and stop loss levels. For instance, exit a buy position on a 'SELL' signal or when the price drops below the support zone.

Risk Management:

Set stop losses just below the support zone for buy orders and above the resistance zone for sell orders to protect against significant losses.

Adjust position sizes according to your risk tolerance and account balance.

Considerations:

Use this indicator in conjunction with other analysis tools and fundamental data to confirm signals and strengthen your trading strategy.

Periodically backtest the strategy based on this indicator to ensure its effectiveness in current market conditions.

Optimization:

Adjust the lengths of the EMAs and the buffer size of the support and resistance zones to better fit the asset's volatility and your trading timeframe.

Search in scripts for "pattern"

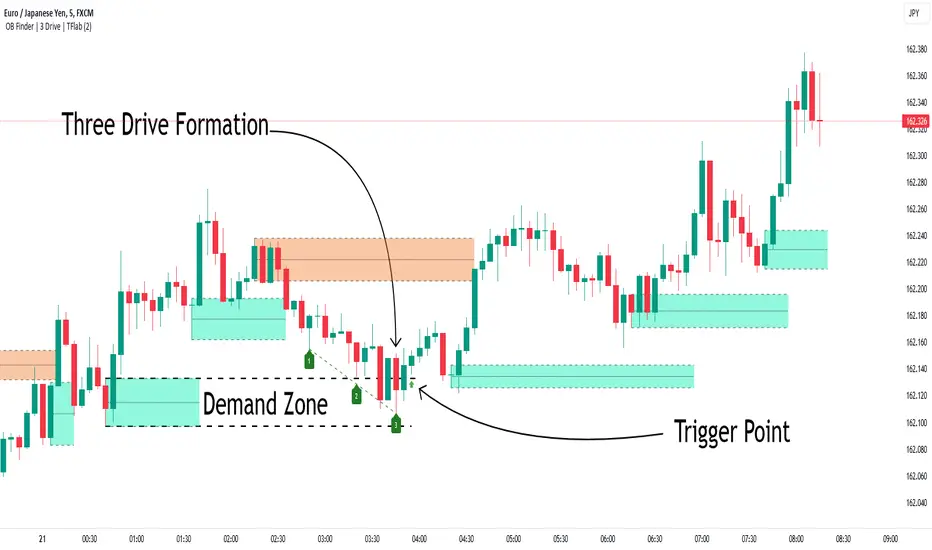

Smart Money Setup 04 [TradingFinder] Three Drive (Harmonic) + OB🔵 Introduction

The "Three Drive" pattern is a well-known formation in technical analysis, recognized for its ability to signal potential trend reversals in price action. Within the realm of trading, particularly in the context of "Reversal Patterns," the Three Drive pattern holds significance as a reliable indicator of shifts in market sentiment.

🟣 Bullish 3 Drive

This pattern typically manifests at a price bottom, where a sequence of lower lows suggests a prevailing negative trend. However, within the structure of the Three Drive pattern, a notable occurrence unfolds.

The second low breaches the range of the first low, followed by the third low surpassing the range of the second low. These penetrations signify a diminishing selling pressure and an emerging buying interest.

Traders often await the confirmation of the third low surpassing the second low as an entry point, with price targets set at the highs formed within the Three Drive pattern.

🟣 Bearish 3 Drive

Conversely, the Bearish Three Drive pattern emerges at a price top, characterized by a sequence of higher highs indicating an upward trend. Yet, amidst this apparent bullish momentum, a shift occurs.

The second high breaks beyond the range of the first high, succeeded by the third high exceeding the range of the second high. These breaches signify a waning buying strength and a resurgence in selling pressure.

Entry into a trade is often executed after the confirmation of the third high surpassing the second high, with targets set at the lows formed within the Three Drive pattern.

Importance :

Understanding the Three Drive pattern's significance extends beyond mere technical analysis. It bears resemblance to other established patterns, such as the Harmonic Pattern and Ending Diagonal within the Elliott Wave Theory.

Recognizing these parallels aids traders in comprehending broader market dynamics and potential price movements.

🔵 Formation of 3 Drive in Order Block Zone

The convergence of the Three Drive pattern with the concept of the Order Block Zone introduces a nuanced layer to traders' analytical approach.

In "Price Action" methodology, Order Blocks represent areas on the price chart where significant market players, such as institutional traders, have executed notable orders.

These zones often act as barriers, with price encountering resistance or support upon reaching them.

When the Three Drive pattern forms within an Order Block Zone, it signifies a confluence of market dynamics.

The completion of the pattern within this zone suggests a potential reversal in the prevailing trend, augmented by the presence of significant institutional orders.

Traders incorporate these Order Blocks into their analysis to identify probable levels where price may change direction, enhancing the reliability of their trading decisions.

🔵 How to Use :

To effectively utilize the Three Drive pattern within the Order Block Zone, traders seek alignment between the completion of the pattern and the presence of significant Order Blocks.

This convergence enhances the reliability of the pattern's signals, increasing the likelihood of successful trade outcomes.

Bullish Three Drive in Demand Zone :

Bearish Three Drive in Supply Zone :

Settings :

You can set your desired "Pivot Period" via settings for the indicator to identify setups based on it.

Engulfing Box & LinesThe "Engulfing Box & Lines" indicator aims to spot and highlight Engulfing candlestick patterns within a trend. These patterns can provide valuable indications of a possible trend reversal, and the indicator underlines them through the use of colored rectangles and horizontal lines. To fully understand the functioning and use of this indicator, let's explore its key elements and associated strategies.

Identification of Engulfing Patterns:

The indicator focuses on detecting two types of Engulfing candles:

Bullish Engulfing: Occurs when a bullish candle (open lower than close) completely encloses the body of the previous bearish candle. This could indicate a possible upside reversal.

Bearish Engulfing: Occurs when a bearish candle (opening higher than closing) entirely engulfs the body of the previous bullish candle. This could signal a potential bearish reversal.

Using the EMA 200:

The indicator uses the 200-period Exponential Moving Average (EMA) as a reference to determine the position of the candles with respect to the long-term trend. When the price is above the 200 EMA, the bullish Engulfing candles are highlighted with a green box, while below the 200 EMA, red boxes are shown for the bearish Engulfing candles.

Size of Boxes and Lines:

The colored boxes represent the size of the body of the candle that caused the Engulfing. Additionally, a horizontal line is drawn close to the body of the candle, serving as the fulcrum of the indicator.

Trading Strategies:

This indicator can be used for different trading strategies:

Trend Continuation: During a positive trend, the onset of an engulfing pattern suggests a possible continuation of the trend. The horizontal lines represent potential support areas, where the price could bounce. Traders might consider buying during such bounces.

Retracements and Entries: Lines can act as support or resistance zones, depending on the trend. When the price approaches a line, a retracement could occur. Traders might move to a lower timeframe to spot entry signals, using the line as a reference.

Closing Positions: Lines could also be used to define exit levels. For example, a trader might decide to exit a position when the price approaches a resistance line.

Confirmations with Other Indicators: The indicator could be used in conjunction with other technical tools, such as oscillators or candlestick analysis, to confirm signals and improve the accuracy of trading decisions.

RSI Primed [ChartPrime]

RSI Primed combines candlesticks, patterns, and the classic RSI indicator for advanced market trend indications

Introduction

Technical traders are always looking for innovative methods to pinpoint potential entry and exit points in the market. The RSI Prime indicator provides such traders with an enhanced view of market conditions by combining various charting styles and the Relative Strength Index (RSI). It offers users a unique perspective on the market trends and price momentum, enabling them to make better-informed decisions and stay ahead of the market curve.

The RSI Primed is a versatile indicator that combines different charting styles with the Relative Strength Index (RSI) to help traders analyze market trends and price momentum. It offers multiple visualization modes that serve specific purposes and provide unique insights into market performance:

Regular Candlesticks

Candlesticks with Patterns

Heikin Ashi Candles

Line Style

Regular Candlestick Mode

The Regular Candlestick Mode in RSI Primed depicts traditional Japanese candlesticks that most traders are familiar with. This mode bypasses any smoothing or modified calculations, representing real-price movements. Regular candlesticks offer a clear and straightforward way to visualize market trends and price action.

Candlestick with Patterns Mode

The Candlestick with Patterns Mode focuses on identifying high-probability candlestick patterns while incorporating RSI values. By leveraging the information captured by the RSI, this mode allows traders to spot significant market reversals or continuation patterns that could signal potential trading opportunities. Some recognizable patterns include engulfing bullish, engulfing bearish, morning star bullish, and evening star bearish patterns.

Heikin Ashi Candles Mode

The Heikin Ashi Candles Mode presents an advanced candlestick charting technique known for its excellent trend-following capabilities. Heikin Ashi Candles filter out noise in the market and provide a clear representation of market trends. In this mode, candlesticks are plotted based on RSI values of the open, high, low, and close prices, helping traders understand and utilize market trends effectively.

Line Style Mode

The Line Style Mode offers a simpler and minimalistic representation of the RSI values by using a line instead of candlesticks to visualize market trends. This mode helps traders focus on the overall trend direction and eliminates potential distractions caused by the complexity of candlestick patterns.

Candle Color Overlay Mode

The Candle Color Overlay Mode is a unique feature in the RSI Primed indicator that allows traders to visualize the RSI values on the chart's candles as a heat gradient. This mode adds a color overlay to the candlesticks, representing the RSI values in relation to the candlesticks' price action.

By displaying the RSI as a color gradient, traders can quickly assess market momentum and identify overbought or oversold conditions without having to switch between different modes or charts. The gradient ranges from cool colors (blue and green) for lower RSI values, indicating oversold conditions, to warm colors (orange and red) for higher RSI values, signifying overbought situations.

To enable the Candle Color Overlay Mode, traders can toggle the "Color Candles" option in the indicator settings. Once enabled, the color gradient will be applied to the candlesticks on the chart, providing a visually striking and informative representation of the RSI values in relation to price action. This mode can be used in tandem with any of the other charting styles, allowing traders to gain even more insights into market trends and momentum.

RSI Primed Implementation

The RSI Primed indicator combines the benefits of various charting styles with the RSI to help traders gain a comprehensive view of market trends and price momentum. It incorporates the Heikin Ashi and RSI values as inputs to generate several visualization modes, enabling traders to select the one that best suits their needs.

Chebyshev Digital Audio Filter in RSI Primed Indicator

A unique feature of the RSI Primed Indicator is the incorporation of the Chebyshev Digital Audio Filter, a powerful tool that significantly influences the indicator's accuracy and responsiveness. This signal processing method brings several benefits to the context of the RSI indicator, improving its performance and capabilities.

1. Improved Signal Filtering

The Chebyshev filter excels in its ability to remove high-frequency noise and unwanted signals from the RSI data. While other filtering techniques might introduce unwanted side effects or distort the RSI data, the Chebyshev filter accurately retains the main signal components, enhancing the RSI Primed's overall accuracy and reliability.

2. Faster Response Time

The Chebyshev filter offers a faster response time than most other filtering techniques. In the context of the RSI Primed Indicator, this means that the filtering process is quicker and more efficient, allowing traders to act swiftly during rapidly changing market conditions.

3. Enhanced Trend Detection

By effectively removing noise from the RSI data, the Chebyshev filter contributes to the enhanced detection of underlying market trends. This feature helps traders identify potential entry and exit points more accurately, improving their overall trading strategy and performance.

How to Use RSI Primed

Traders can choose from different visualization modes to suit their preferences while using the RSI Primed indicator. By closely monitoring the chosen visualization mode and the position of the moving average, traders can make informed decisions about market trends.

Green candlesticks or an upward line slope indicate a bullish trend, and red candlesticks or a downward line slope suggest a bearish trend. If the candles or line are above the moving average, it could signify an uptrend, whereas a position below the moving average may indicate a downtrend.

The RSI Primed indicator offers a unique and comprehensive perspective on market trends and price momentum by combining various charting styles with the RSI. Traders can choose from different visualization modes and make well-informed decisions to capitalize on market opportunities. This innovative indicator provides a clear and concise view of the market, enabling traders to make swift decisions and enhance their trading results.

Quinn-Fernandes Fourier Transform of Filtered Price [Loxx]Down the Rabbit Hole We Go: A Deep Dive into the Mysteries of Quinn-Fernandes Fast Fourier Transform and Hodrick-Prescott Filtering

In the ever-evolving landscape of financial markets, the ability to accurately identify and exploit underlying market patterns is of paramount importance. As market participants continuously search for innovative tools to gain an edge in their trading and investment strategies, advanced mathematical techniques, such as the Quinn-Fernandes Fourier Transform and the Hodrick-Prescott Filter, have emerged as powerful analytical tools. This comprehensive analysis aims to delve into the rich history and theoretical foundations of these techniques, exploring their applications in financial time series analysis, particularly in the context of a sophisticated trading indicator. Furthermore, we will critically assess the limitations and challenges associated with these transformative tools, while offering practical insights and recommendations for overcoming these hurdles to maximize their potential in the financial domain.

Our investigation will begin with a comprehensive examination of the origins and development of both the Quinn-Fernandes Fourier Transform and the Hodrick-Prescott Filter. We will trace their roots from classical Fourier analysis and time series smoothing to their modern-day adaptive iterations. We will elucidate the key concepts and mathematical underpinnings of these techniques and demonstrate how they are synergistically used in the context of the trading indicator under study.

As we progress, we will carefully consider the potential drawbacks and challenges associated with using the Quinn-Fernandes Fourier Transform and the Hodrick-Prescott Filter as integral components of a trading indicator. By providing a critical evaluation of their computational complexity, sensitivity to input parameters, assumptions about data stationarity, performance in noisy environments, and their nature as lagging indicators, we aim to offer a balanced and comprehensive understanding of these powerful analytical tools.

In conclusion, this in-depth analysis of the Quinn-Fernandes Fourier Transform and the Hodrick-Prescott Filter aims to provide a solid foundation for financial market participants seeking to harness the potential of these advanced techniques in their trading and investment strategies. By shedding light on their history, applications, and limitations, we hope to equip traders and investors with the knowledge and insights necessary to make informed decisions and, ultimately, achieve greater success in the highly competitive world of finance.

█ Fourier Transform and Hodrick-Prescott Filter in Financial Time Series Analysis

Financial time series analysis plays a crucial role in making informed decisions about investments and trading strategies. Among the various methods used in this domain, the Fourier Transform and the Hodrick-Prescott (HP) Filter have emerged as powerful techniques for processing and analyzing financial data. This section aims to provide a comprehensive understanding of these two methodologies, their significance in financial time series analysis, and their combined application to enhance trading strategies.

█ The Quinn-Fernandes Fourier Transform: History, Applications, and Use in Financial Time Series Analysis

The Quinn-Fernandes Fourier Transform is an advanced spectral estimation technique developed by John J. Quinn and Mauricio A. Fernandes in the early 1990s. It builds upon the classical Fourier Transform by introducing an adaptive approach that improves the identification of dominant frequencies in noisy signals. This section will explore the history of the Quinn-Fernandes Fourier Transform, its applications in various domains, and its specific use in financial time series analysis.

History of the Quinn-Fernandes Fourier Transform

The Quinn-Fernandes Fourier Transform was introduced in a 1993 paper titled "The Application of Adaptive Estimation to the Interpolation of Missing Values in Noisy Signals." In this paper, Quinn and Fernandes developed an adaptive spectral estimation algorithm to address the limitations of the classical Fourier Transform when analyzing noisy signals.

The classical Fourier Transform is a powerful mathematical tool that decomposes a function or a time series into a sum of sinusoids, making it easier to identify underlying patterns and trends. However, its performance can be negatively impacted by noise and missing data points, leading to inaccurate frequency identification.

Quinn and Fernandes sought to address these issues by developing an adaptive algorithm that could more accurately identify the dominant frequencies in a noisy signal, even when data points were missing. This adaptive algorithm, now known as the Quinn-Fernandes Fourier Transform, employs an iterative approach to refine the frequency estimates, ultimately resulting in improved spectral estimation.

Applications of the Quinn-Fernandes Fourier Transform

The Quinn-Fernandes Fourier Transform has found applications in various fields, including signal processing, telecommunications, geophysics, and biomedical engineering. Its ability to accurately identify dominant frequencies in noisy signals makes it a valuable tool for analyzing and interpreting data in these domains.

For example, in telecommunications, the Quinn-Fernandes Fourier Transform can be used to analyze the performance of communication systems and identify interference patterns. In geophysics, it can help detect and analyze seismic signals and vibrations, leading to improved understanding of geological processes. In biomedical engineering, the technique can be employed to analyze physiological signals, such as electrocardiograms, leading to more accurate diagnoses and better patient care.

Use of the Quinn-Fernandes Fourier Transform in Financial Time Series Analysis

In financial time series analysis, the Quinn-Fernandes Fourier Transform can be a powerful tool for isolating the dominant cycles and frequencies in asset price data. By more accurately identifying these critical cycles, traders can better understand the underlying dynamics of financial markets and develop more effective trading strategies.

The Quinn-Fernandes Fourier Transform is used in conjunction with the Hodrick-Prescott Filter, a technique that separates the underlying trend from the cyclical component in a time series. By first applying the Hodrick-Prescott Filter to the financial data, short-term fluctuations and noise are removed, resulting in a smoothed representation of the underlying trend. This smoothed data is then subjected to the Quinn-Fernandes Fourier Transform, allowing for more accurate identification of the dominant cycles and frequencies in the asset price data.

By employing the Quinn-Fernandes Fourier Transform in this manner, traders can gain a deeper understanding of the underlying dynamics of financial time series and develop more effective trading strategies. The enhanced knowledge of market cycles and frequencies can lead to improved risk management and ultimately, better investment performance.

The Quinn-Fernandes Fourier Transform is an advanced spectral estimation technique that has proven valuable in various domains, including financial time series analysis. Its adaptive approach to frequency identification addresses the limitations of the classical Fourier Transform when analyzing noisy signals, leading to more accurate and reliable analysis. By employing the Quinn-Fernandes Fourier Transform in financial time series analysis, traders can gain a deeper understanding of the underlying financial instrument.

Drawbacks to the Quinn-Fernandes algorithm

While the Quinn-Fernandes Fourier Transform is an effective tool for identifying dominant cycles and frequencies in financial time series, it is not without its drawbacks. Some of the limitations and challenges associated with this indicator include:

1. Computational complexity: The adaptive nature of the Quinn-Fernandes Fourier Transform requires iterative calculations, which can lead to increased computational complexity. This can be particularly challenging when analyzing large datasets or when the indicator is used in real-time trading environments.

2. Sensitivity to input parameters: The performance of the Quinn-Fernandes Fourier Transform is dependent on the choice of input parameters, such as the number of harmonic periods, frequency tolerance, and Hodrick-Prescott filter settings. Choosing inappropriate parameter values can lead to inaccurate frequency identification or reduced performance. Finding the optimal parameter settings can be challenging, and may require trial and error or a more sophisticated optimization process.

3. Assumption of stationary data: The Quinn-Fernandes Fourier Transform assumes that the underlying data is stationary, meaning that its statistical properties do not change over time. However, financial time series data is often non-stationary, with changing trends and volatility. This can limit the effectiveness of the indicator and may require additional preprocessing steps, such as detrending or differencing, to ensure the data meets the assumptions of the algorithm.

4. Limitations in noisy environments: Although the Quinn-Fernandes Fourier Transform is designed to handle noisy signals, its performance may still be negatively impacted by significant noise levels. In such cases, the identification of dominant frequencies may become less reliable, leading to suboptimal trading signals or strategies.

5. Lagging indicator: As with many technical analysis tools, the Quinn-Fernandes Fourier Transform is a lagging indicator, meaning that it is based on past data. While it can provide valuable insights into historical market dynamics, its ability to predict future price movements may be limited. This can result in false signals or late entries and exits, potentially reducing the effectiveness of trading strategies based on this indicator.

Despite these drawbacks, the Quinn-Fernandes Fourier Transform remains a valuable tool for financial time series analysis when used appropriately. By being aware of its limitations and adjusting input parameters or preprocessing steps as needed, traders can still benefit from its ability to identify dominant cycles and frequencies in financial data, and use this information to inform their trading strategies.

█ Deep-dive into the Hodrick-Prescott Fitler

The Hodrick-Prescott (HP) filter is a statistical tool used in economics and finance to separate a time series into two components: a trend component and a cyclical component. It is a powerful tool for identifying long-term trends in economic and financial data and is widely used by economists, central banks, and financial institutions around the world.

The HP filter was first introduced in the 1990s by economists Robert Hodrick and Edward Prescott. It is a simple, two-parameter filter that separates a time series into a trend component and a cyclical component. The trend component represents the long-term behavior of the data, while the cyclical component captures the shorter-term fluctuations around the trend.

The HP filter works by minimizing the following objective function:

Minimize: (Sum of Squared Deviations) + λ (Sum of Squared Second Differences)

Where:

1. The first term represents the deviation of the data from the trend.

2. The second term represents the smoothness of the trend.

3. λ is a smoothing parameter that determines the degree of smoothness of the trend.

The smoothing parameter λ is typically set to a value between 100 and 1600, depending on the frequency of the data. Higher values of λ lead to a smoother trend, while lower values lead to a more volatile trend.

The HP filter has several advantages over other smoothing techniques. It is a non-parametric method, meaning that it does not make any assumptions about the underlying distribution of the data. It also allows for easy comparison of trends across different time series and can be used with data of any frequency.

Another significant advantage of the HP Filter is its ability to adapt to changes in the underlying trend. This feature makes it particularly well-suited for analyzing financial time series, which often exhibit non-stationary behavior. By employing the HP Filter to smooth financial data, traders can more accurately identify and analyze the long-term trends that drive asset prices, ultimately leading to better-informed investment decisions.

However, the HP filter also has some limitations. It assumes that the trend is a smooth function, which may not be the case in some situations. It can also be sensitive to changes in the smoothing parameter λ, which may result in different trends for the same data. Additionally, the filter may produce unrealistic trends for very short time series.

Despite these limitations, the HP filter remains a valuable tool for analyzing economic and financial data. It is widely used by central banks and financial institutions to monitor long-term trends in the economy, and it can be used to identify turning points in the business cycle. The filter can also be used to analyze asset prices, exchange rates, and other financial variables.

The Hodrick-Prescott filter is a powerful tool for analyzing economic and financial data. It separates a time series into a trend component and a cyclical component, allowing for easy identification of long-term trends and turning points in the business cycle. While it has some limitations, it remains a valuable tool for economists, central banks, and financial institutions around the world.

█ Combined Application of Fourier Transform and Hodrick-Prescott Filter

The integration of the Fourier Transform and the Hodrick-Prescott Filter in financial time series analysis can offer several benefits. By first applying the HP Filter to the financial data, traders can remove short-term fluctuations and noise, effectively isolating the underlying trend. This smoothed data can then be subjected to the Fourier Transform, allowing for the identification of dominant cycles and frequencies with greater precision.

By combining these two powerful techniques, traders can gain a more comprehensive understanding of the underlying dynamics of financial time series. This enhanced knowledge can lead to the development of more effective trading strategies, better risk management, and ultimately, improved investment performance.

The Fourier Transform and the Hodrick-Prescott Filter are powerful tools for financial time series analysis. Each technique offers unique benefits, with the Fourier Transform being adept at identifying dominant cycles and frequencies, and the HP Filter excelling at isolating long-term trends from short-term noise. By combining these methodologies, traders can develop a deeper understanding of the underlying dynamics of financial time series, leading to more informed investment decisions and improved trading strategies. As the financial markets continue to evolve, the combined application of these techniques will undoubtedly remain an essential aspect of modern financial analysis.

█ Features

Endpointed and Non-repainting

This is an endpointed and non-repainting indicator. These are crucial factors that contribute to its usefulness and reliability in trading and investment strategies. Let us break down these concepts and discuss why they matter in the context of a financial indicator.

1. Endpoint nature: An endpoint indicator uses the most recent data points to calculate its values, ensuring that the output is timely and reflective of the current market conditions. This is in contrast to non-endpoint indicators, which may use earlier data points in their calculations, potentially leading to less timely or less relevant results. By utilizing the most recent data available, the endpoint nature of this indicator ensures that it remains up-to-date and relevant, providing traders and investors with valuable and actionable insights into the market dynamics.

2. Non-repainting characteristic: A non-repainting indicator is one that does not change its values or signals after they have been generated. This means that once a signal or a value has been plotted on the chart, it will remain there, and future data will not affect it. This is crucial for traders and investors, as it offers a sense of consistency and certainty when making decisions based on the indicator's output.

Repainting indicators, on the other hand, can change their values or signals as new data comes in, effectively "repainting" the past. This can be problematic for several reasons:

a. Misleading results: Repainting indicators can create the illusion of a highly accurate or successful trading system when backtesting, as the indicator may adapt its past signals to fit the historical price data. This can lead to overly optimistic performance results that may not hold up in real-time trading.

b. Decision-making uncertainty: When an indicator repaints, it becomes challenging for traders and investors to trust its signals, as the signal that prompted a trade may change or disappear after the fact. This can create confusion and indecision, making it difficult to execute a consistent trading strategy.

The endpoint and non-repainting characteristics of this indicator contribute to its overall reliability and effectiveness as a tool for trading and investment decision-making. By providing timely and consistent information, this indicator helps traders and investors make well-informed decisions that are less likely to be influenced by misleading or shifting data.

Inputs

Source: This input determines the source of the price data to be used for the calculations. Users can select from options like closing price, opening price, high, low, etc., based on their preferences. Changing the source of the price data (e.g., from closing price to opening price) will alter the base data used for calculations, which may lead to different patterns and cycles being identified.

Calculation Bars: This input represents the number of past bars used for the calculation. A higher value will use more historical data for the analysis, while a lower value will focus on more recent price data. Increasing the number of past bars used for calculation will incorporate more historical data into the analysis. This may lead to a more comprehensive understanding of long-term trends but could also result in a slower response to recent price changes. Decreasing this value will focus more on recent data, potentially making the indicator more responsive to short-term fluctuations.

Harmonic Period: This input represents the harmonic period, which is the number of harmonics used in the Fourier Transform. A higher value will result in more harmonics being used, potentially capturing more complex cycles in the price data. Increasing the harmonic period will include more harmonics in the Fourier Transform, potentially capturing more complex cycles in the price data. However, this may also introduce more noise and make it harder to identify clear patterns. Decreasing this value will focus on simpler cycles and may make the analysis clearer, but it might miss out on more complex patterns.

Frequency Tolerance: This input represents the frequency tolerance, which determines how close the frequencies of the harmonics must be to be considered part of the same cycle. A higher value will allow for more variation between harmonics, while a lower value will require the frequencies to be more similar. Increasing the frequency tolerance will allow for more variation between harmonics, potentially capturing a broader range of cycles. However, this may also introduce noise and make it more difficult to identify clear patterns. Decreasing this value will require the frequencies to be more similar, potentially making the analysis clearer, but it might miss out on some cycles.

Number of Bars to Render: This input determines the number of bars to render on the chart. A higher value will result in more historical data being displayed, but it may also slow down the computation due to the increased amount of data being processed. Increasing the number of bars to render on the chart will display more historical data, providing a broader context for the analysis. However, this may also slow down the computation due to the increased amount of data being processed. Decreasing this value will speed up the computation, but it will provide less historical context for the analysis.

Smoothing Mode: This input allows the user to choose between two smoothing modes for the source price data: no smoothing or Hodrick-Prescott (HP) smoothing. The choice depends on the user's preference for how the price data should be processed before the Fourier Transform is applied. Choosing between no smoothing and Hodrick-Prescott (HP) smoothing will affect the preprocessing of the price data. Using HP smoothing will remove some of the short-term fluctuations from the data, potentially making the analysis clearer and more focused on longer-term trends. Not using smoothing will retain the original price fluctuations, which may provide more detail but also introduce noise into the analysis.

Hodrick-Prescott Filter Period: This input represents the Hodrick-Prescott filter period, which is used if the user chooses to apply HP smoothing to the price data. A higher value will result in a smoother curve, while a lower value will retain more of the original price fluctuations. Increasing the Hodrick-Prescott filter period will result in a smoother curve for the price data, emphasizing longer-term trends and minimizing short-term fluctuations. Decreasing this value will retain more of the original price fluctuations, potentially providing more detail but also introducing noise into the analysis.

Alets and signals

This indicator featues alerts, signals and bar coloring. You have to option to turn these on/off in the settings menu.

Maximum Bars Restriction

This indicator requires a large amount of processing power to render on the chart. To reduce overhead, the setting "Number of Bars to Render" is set to 500 bars. You can adjust this to you liking.

█ Related Indicators and Libraries

Goertzel Cycle Composite Wave

Goertzel Browser

Fourier Spectrometer of Price w/ Extrapolation Forecast

Fourier Extrapolator of 'Caterpillar' SSA of Price

Normalized, Variety, Fast Fourier Transform Explorer

Real-Fast Fourier Transform of Price Oscillator

Real-Fast Fourier Transform of Price w/ Linear Regression

Fourier Extrapolation of Variety Moving Averages

Fourier Extrapolator of Variety RSI w/ Bollinger Bands

Fourier Extrapolator of Price w/ Projection Forecast

Fourier Extrapolator of Price

STD-Stepped Fast Cosine Transform Moving Average

Variety RSI of Fast Discrete Cosine Transform

loxfft

Custom XABCD Validation and Backtesting ToolOverview:

We hear a lot about Gartleys, bats, crabs and the rest of the barnyard crew, but have you ever wondered what other creatures might be lurking out there yet to be discovered? Well wonder no longer, it's time to find out for yourself! The Custom XABCD Validation and Backtesting Tool allows you to define retracement ratios and targets for your very own patterns.

Tips:

(1) Adjust the patterns entry/stop/target configuration and see how it affects the pattern's backtesting results.

(2) Adjust the weights of pattern score components (% error, PRZ confluence, Point D/PRZ confluence), along with the entry minimum score requirements ('If score is above'), and see how it affects the patterns' results.

Pattern Scoring:

The pattern's score is an attempt to represent the quality of a pattern with a single metric. This is one of the most powerful aspects of the tool because it can quickly tell you whether a trade is worth entering. The score is based on 3 components:

(1) Retracement % Accuracy - this measures how closely a pattern's retracement ratios match your defined theoretical values. You can change the "Allowed ratio error %" in Settings to be more or less inclusive.

(2) PRZ Level Confluence - Potential Reversal Zone levels are retracements of the XA, BC, and/or XC legs. These levels indicate where a potential reversal might occur (i.e. pivot point D). The PRZ Level Confluence component measures the closeness of the two closest PRZ levels, relative to the height of the of the XA leg.

(3) Point D / PRZ Confluence - this measures the closeness of point D to either of the two closest PRZ levels (identified in the PRZ Level Confluence component above), relative to the height of the XA leg. In theory, the closer together these levels are, the higher the probability of a reversal.

While the score is percentage-based, it should not be confused with a probability. A score of 96% does not imply a 96% chance of success. It simply represents the average of the three components mentioned above, weighted according to the defined weight parameters. A score of 100% would mean that (1) all leg retracements match the defined theoretical retracement ratios exactly, (2) all PRZ retracement levels are exactly the same value, and (3) pivot point D occurred exactly at the confluent PRZ level.

Pattern scoring research has been ongoing since I introduced the concept with my Harmonic Pattern Detection, Prediction and Backtesting Tool (see below). So the way that the score is calculated is subject to change based on the results of that research.

Stock Tech Bot One ViewTechnical indicators are not limited. Hence, here is another indicator with the combination of OBV, RSI, and MACD along with support, and resistance that follows the price while honoring the moving average of 200, 90 & 50.

The default lookback period of this indicator is 21 though it is changeable as per the user's desire.

The highest high and lowest low for the last 21 days lookback period proven to be the perfect Support & Resistance as the price of particular stock values are decided by market psychology. The support and resistance lines are very important to understand the market psychology which is very well proven with price action patterns and the lines are drawn based on,

Lower Extreme = 0.1 (Changeable)

Maximum Range = 21 days highest high - 21 days lowest low.

Support Line = 21 days lowest low + (Maximum Range * Lower Extreme)

Resistance Line = 21 days highest high - (Maximum Range * Lower Extreme)

RSI - Relative strength indicator is very famous to find the market momentum within the range of 0 - 100. Though the lookback period is changeable, the 14 days lookback period is the perfect match as the momentum of market movement for the last 3 weeks will always assist to identify the market regime. Here the momentum is just to highlight the indication (green up arrow under the candle for long and red down arrow above the candle for short) of market movement though it is not very important to consider if the price of the stock respect the support & resistance lines along with volume indicator (* = violet color).

OBV - Momentum:

The on-balance volume is always going indicator on any kind of tickers, which helps to identify the buying interest. Now, applying momentum on OBV with the positive movement for at least two consecutive days gives perfect confirmation for entry. A combination of the price along with this momentum(OBV) in the chart will help us to know the whipsaw in the price.

The Symbol "*" on top of each bar shows the market interest in that particular stock. If your ticker is fundamentally strong then you can see this "*" even when the market falls.

MACD:

One of the favorites and simple indicators widely used, where the thump of the rule is not to change the length even if it is allowed. It's OK to believe blindly in certain indicator and consider it while trading. That's why the indicator changes the bar color by following the MACD histogram.

Volume:

It may be the OBV works based on the open price and close price along with volume movement, it is wise to have the volume that is plotted along with price movement that should help you to decide whether the market is greedy or fearful.

The symbol "-" on top of each bar tells you a lot and don't ignore it.

Moving Average:

Moving average is a very good trend indicator as everyone considers seeing along with the price in the chart which is not omitted while we gauge the price movement alone with volume in this indicator. The 200, 90 & 50 MA's are everyone's favorite, and the same is plotted on the chart.

As explained above, the combination of all four indicators with price movement will give us very good confidence to take entry.

Candlestick Pattern:

You should admire the techniques of the candlestick pattern as you navigate the chart from right to left. Though there are a lot of patterns that exist, it is easy to enable and disable to view the signal as the label.

Further, last but not least, the exit always depends on individual conviction and how often the individual watch the price movement, if your conviction is strong then follow the down arrow red indication. If not, then exit with a trailing stop that indicates the bar with orange color.

Happy investing

Note: It is just a combination of multiple indicators and patterns to get one holistic view. So, the credit goes to all wise developers who publically published.

Regression Channel Alternative MTF█ OVERVIEW

This indicator displays 3 timeframes of parallel channel using linear regression calculation to assist manual drawing of chart patterns.

This indicator is not true Multi Timeframe (MTF) but considered as Alternative MTF which calculate 100 bars for Primary MTF, can be refer from provided line helper.

The timeframe scenarios are defined based on Position, Swing and Intraday Trader.

█ INSPIRATIONS

These timeframe scenarios are defined based on Harmonic Trading : Volume Three written by Scott M Carney.

By applying channel on each timeframe, MW or ABCD patterns can be easily identified manually.

This can also be applied on other chart patterns.

█ CREDITS

Scott M Carney, Harmonic Trading : Volume Three (Reaction vs. Reversal)

█ TIMEFRAME EXPLAINED

Higher / Distal : The (next) longer or larger comparative timeframe after primary pattern has been identified.

Primary / Clear : Timeframe that possess the clearest pattern structure.

Lower / Proximate : The (next) shorter timeframe after primary pattern has been identified.

Lowest : Check primary timeframe as main reference.

█ EXAMPLE OF USAGE / EXPLAINATION

Head & Shoulders S/R RegularThis is my take in Head & Shoulders (regular H&S)

The script will wait until a valid point E is found, which means A, C and E are alined

Then it will find the highest point between C - E -> Head (= D),

together with the highest point between A - C -> Left Shoulder (= B)

After this, the pattern is drawn, together with a 'trigger' area (E-G - E'-G' ~ 'Right shoulder area')

ONLY in this field, when a close is higher than E'-G', the figure will turn green, if lower than E-G, it will turn red, else, it will be blue

Settings:

Date range filtering

Here you can filter the patterns by setting the date period (for E)

Pivot Points -> Leftbars - Rightbars

min/max retrace AD -> E

Set the retracement for E (retracement A -> D -> E, here between 1.4 & 1.5)

% tolerance

Tolerance of Right shoulder height against Left shoulder height

0% (= the same relative height):

85% (-> now close isn't higher than E'-G' -> blue coloured):

min/max %

Sets the desired B height against D (here B is between 35-45% of D):

width R shoulder = L shoulder + x%

Sets the width of Right shoulder against Left shoulder

0% (nothing extra, just the same width as Left shoulder)

100% (Right shoulder area is double as large as the Left shoulder):

-70% (Right shoulder area much narrower than Left shoulder):

maximum visible patterns:

Set the maximum visible amount of patterns

This script uses one of the latest fantastic Pinescript features:

linefill and for ... in loop

Cheers!

Price Action [Morty]This price action indicator uses the higher timeframe SSL channel to identify trends.

The long entry signal is a bullish candlestick pattern when the price retraces to EMA20 in an uptrend.

The short entry signal is a bearish candlestick pattern when the price retraces to the EMA20 in a downrend.

Currently, this indicator shows engulfing patterns, pin bar patterns, 2 bar reversal patterns and harami patterns.

It also shows a volatility squeeze signal when the Bollinger bands is within the Kelter channels.

The buy and sell signal can also be filter by the ADX indicator greater than a threshold.

You can set your stoploss to the previous low/high when you go long/short.

The risk/reward ratio could be 1 to 1.5.

This indicator can be used in any market.

Tweezers and Kangaroo TailHello Traders,

Here Tweezers and Kangaroo Tail script is in your service. The script searches for Tweezer / Kangaroo Tail candlestick patterns and shows them as T (Tweezer) and K (Kangaroo Tail). Thanks to RorschachT who game me the idea and some details while working on this script.

What are these candlestick patterns?

Tweezers :

- A tweezers pattern occurs when the highs/Lows of two candlesticks occur at almost exactly the same level

- Both candles must have wicks

- Bigger Wick / Smaller Wick rate should not be greater than 150% ( 150% by default and you have option to change it)

- First Candle must be highest/lowest for last 5 candles (5 by default and you have option to change it)

- The level of High for Top, Low for Bottom must be almost lower than 20% of the bigger wick of tweezer candles (20% by default and you have option to change it)

- The Candles can be right next to each other or apart but not more than 12 candles apart (12 by default and you have option to change it)

- You will see that Tweezers pattern occurs frequently

Kangaroo Tail:

- Looks almost like a Hammer or Inverted Hammer candle

- They have both its open and close in the top or bottom third of the candle

- There must be some space/room on the left of the kangaroo tail

- The open and close of the Kangaroo Tail candle must be inside the range of the previous candlestick

- The next candle should create a new high or new low

- You have several options to set details about the "Room" that should be on the left and also options for Wick/Body rates

- You can see example below

You have option to enable/disable any of these patterns.

as far as I have tested they are strong reversal patterns but none of the indicators or patterns may not be enough alone. so you should confirm the signals using other indicators or tools

If you need more information you can find a lot of info on the net ;)

Example: Tweezers - Aparted

Example: Kangaroo Tail - Bullish

Enjoy!

[RS]ZigZag PA V1ZigZag Based on price oscilation.

added pattern recognition, also added recognition of head and shoulders and contracting/expanding triangles to previous list of patterns :p

Use Alt Timeframe: enables optional timeframes, use higher timeframes to reduce noise.

Timeframe: said Alt Timeframe.

Show Patterns: toggles Pattern Recognition on.

First presented FVG (w/stats) w/statistical hourly ranges & biasOverview

This indicator identifies the first Fair Value Gap (FVG) that forms during each hourly session and provides comprehensive statistical analysis based on 12 years of historical NASDAQ (NQ) data. It combines price action analysis with probability-based statistics to help traders make informed decisions.

⚠️ IMPORTANT - Compatibility

Market: This indicator is designed exclusively for NASDAQ futures (NQ/MNQ)

Timeframe: Statistical data is based on FVGs formed on the 5-minute timeframe

FVG Detection: Works on any timeframe, but use 5-minute for accuracy matching the statistical analysis

All hardcoded statistics are derived from 12 years of NQ historical data

What It Does

1. FVG Detection & Visualization

Automatically detects the first FVG (bullish or bearish) that forms each hour

Draws colored boxes around FVGs:

Blue boxes = Bullish FVG (gap up)

Red boxes = Bearish FVG (gap down)

FVG boxes extend to the end of the hour

Optional midpoint lines show the center of each FVG

Uses volume imbalance logic (outside prints) to refine FVG boundaries

2. Hourly Reference Lines

Vertical Delimiter: Marks the start of each hour

Hourly Open Line: Shows where the current hour opened

Expected Range Lines: Projects the anticipated high/low based on historical data

Choose between Mean (average) or Median (middle value) statistics

Upper range line (teal/green)

Lower range line (red)

All lines span exactly one hour from the moment it opens

Optional labels show price values at line ends

3. Real-Time Statistics Table

The table displays live data for the current hour only:

Hour: Current hour in 12-hour format (AM/PM)

FVG Status: Shows if a Bull FVG, Bear FVG, or no FVG has formed yet

Green background = Bullish FVG detected

Red background = Bearish FVG detected

1st 15min: Direction of the first 15 minutes (Bullish/Bearish/Neutral/Pending)

Continuation %: Historical probability that the hour continues in the first 15-minute direction

Color-coded: Green for bullish, red for bearish

Avg Range %: Expected percentage range for the current hour (based on 12-year mean)

FVG Effect %: Historical probability that FVG direction predicts hourly close direction

Shows BISI→Bull % for bullish FVGs

Shows SIBI→Bear % for bearish FVGs

Blank if no FVG has formed yet

Time Left: Countdown timer showing MM:SS remaining in the hour (updates in real-time)

Hourly Bias: Historical directional tendency (bullish % or bearish %)

H Open: Current hour's opening price

Exp Range: Projected price range (Low - High) based on historical average

Customization Options

Detection Settings:

Lower Timeframe Selection (15S, 1min, 5min) - controls FVG detection granularity

Display Settings:

FVG box colors (bullish/bearish)

Midpoint lines (show/hide, color, style)

Table Settings:

Position (9 locations: corners, edges, center)

Text size (Tiny, Small, Normal, Large)

Hourly Lines:

Toggle each line type on/off

Hour delimiter (color, width)

Open line (color, width, style)

Range lines (color, width, style)

Choose Mean or Median statistics for range calculation

Show/hide labels with customizable text size

How to Use

Apply to NQ futures chart (NQ1! or MNQ1!)

Set chart to 5-minute timeframe for optimal FVG detection matching the statistical data

Watch for the first FVG to form each hour

Reference the table for probability-based decision support:

High continuation % = strong directional bias

FVG Effect % shows reliability of the FVG signal

Time Left helps manage entries/exits within the hour

Use range lines as potential targets or reversal zones

Statistical Foundation

All statistics are derived from:

12 years of NASDAQ (NQ) historical data

Hourly analysis of FVG formation patterns

First 15-minute directional analysis

Mean and Median calculations for range expectations

Data encompasses 2,400+ samples per hour

Best Practices

✅ Use on NQ/MNQ futures only

✅ Best on 5-minute charts (matches statistical data)

✅ Combine FVG signals with continuation probabilities

✅ Use range lines as potential profit targets

✅ Watch the countdown timer for hour-end setups

❌ Do not use on other markets (statistics won't apply)

❌ Avoid using during low-liquidity hours (5PM ET has minimal data)

Technical Notes

Timezone: America/New_York (EST/EDT)

Weekend filtering: Automatically hides data during market closure

Updates in real-time on live bars

Maximum 500 boxes/lines for performance

FVG detection includes volume imbalance (body gap) refinement

Credits

Statistical analysis based on 12 years of NASDAQ historical data. FVG detection methodology follows ICT concepts with volume imbalance refinement.

Disclaimer: This indicator provides statistical analysis based on historical data. Past performance does not guarantee future results. Always use proper risk management.

Would you like me to adjust any section or add/remove anything?6-9 Session & Levels - Customizable Range Analysis Indicator

Description:

This indicator provides comprehensive session-based range analysis designed for intraday traders. It calculates and displays key levels based on a customizable session period (default 6:00-9:00 AM ET).

Core Features:

Sespastedthis is a summary for another indicator- i was hoping for something more like this in terms of content etc22:23Architected comprehensive indicator summary matching professional documentation style.The user wants me to rewrite the summary for their FVG indicator in a similar style to the example provided. The example is more structured, detailed, and professional. Let me create a comprehensive summary that follows that format:

Clear title

Description/Overview

Core Features (broken down into sections)

Input Settings Explained (detailed breakdown of all customization options)

How It Works section

Use Case

Note/Disclaimer

Let me make it thorough and match the style while being accurate to their indicator's functionality.Here's a detailed summary in that format:

Every Hour 1st FVG with Statistical Analysis - NASDAQ Hourly Trading Intelligence

Description:

This indicator identifies the first Fair Value Gap (FVG) that forms during each hourly session and provides comprehensive probability-based statistical analysis derived from 12 years of NASDAQ (NQ) historical data. It combines real-time FVG detection with hardcoded statistical probabilities to help intraday traders make informed decisions based on historical patterns and hourly price action dynamics.

IMPORTANT: This indicator is specifically calibrated for NASDAQ futures (NQ/MNQ) only. All statistical data is derived from 12 years of NQ historical analysis with FVGs detected on the 5-minute timeframe. Using this indicator on other markets will produce invalid statistical results.

Core Features:

FVG Detection & Visualization

Automatically detects and displays the first Fair Value Gap (bullish or bearish) that forms within each hourly session

Color-coded boxes mark FVG zones: Blue for bullish FVGs (gap up), Red for bearish FVGs (gap down)

FVG boxes extend precisely to the end of the hour boundary

Optional midpoint lines show the center point of each FVG

Uses volume imbalance logic (outside prints) to refine FVG boundaries beyond simple wick-to-wick gaps

Supports both chart timeframe detection and lower timeframe detection via request.security_lower_tf

Hourly Reference Lines

Vertical Hour Delimiter: Marks the exact start of each new hour with an extendable vertical line

Hourly Open Line: Displays the opening price of the current hour

Expected Range Lines: Projects anticipated high and low levels based on 12 years of statistical data

Choose between Mean (average) or Median (middle value) calculations

Upper range line shows expected high

Lower range line shows expected low

All lines span exactly one hour from open to close

Optional labels display exact price values at the end of each line

Real-Time Statistics Table

Displays comprehensive live data for the current hour only:

Hour: Current hour in 12-hour format (e.g., "9AM", "2PM")

FVG Status: Shows detection state with color coding

"None Yet" (white background) - No FVG detected

"Bull FVG" (green background) - Bullish FVG identified

"Bear FVG" (red background) - Bearish FVG identified

1st 15min: Direction of first 15 minutes (Bullish/Bearish/Neutral/Pending)

Continuation %: Historical probability that the hour closes in the direction of the first 15 minutes

Green background with up arrow (↑) for bullish continuation probability

Red background with down arrow (↓) for bearish continuation probability

Avg Range %: Expected percentage range for the current hour based on 12-year mean

FVG Effect %: Historical effectiveness of FVG directional prediction

Shows "BISI→Bull %" for bullish FVGs (gap up predicting bullish hourly close)

Shows "SIBI→Bear %" for bearish FVGs (gap down predicting bearish hourly close)

Displays blank if no FVG has formed yet

Time Left: Real-time countdown timer showing minutes and seconds remaining in the hour (MM:SS format)

Hourly Bias: Historical directional tendency showing bullish or bearish percentage bias

H Open: Current hour's opening price

Exp Range: Projected price range showing "Low - High" based on selected statistic (mean or median)

Input Settings Explained:

Detection Settings

Lower Timeframe: Select the base timeframe for FVG detection

Options: 15S (15 seconds), 1 (1 minute), 5 (5 minutes)

Recommendation: Use 5-minute to match the statistical data sample

The indicator uses this timeframe to scan for FVG patterns even when viewing higher timeframes

Display Settings

Bullish FVG Color: Set the color and transparency for bullish (upward) FVG boxes

Bearish FVG Color: Set the color and transparency for bearish (downward) FVG boxes

Show Midpoint Lines: Toggle horizontal lines at the center of each FVG box

Midpoint Line Color: Customize the midpoint line color

Midpoint Line Style: Choose between Solid, Dotted, or Dashed line styles

Table Settings

Table Position: Choose from 9 locations:

Top: Left, Center, Right

Middle: Left, Center, Right

Bottom: Left, Center, Right

Table Text Size: Select from Tiny, Small, Normal, or Large for readability on different screen sizes

Hourly Lines Settings

Show Hourly Lines: Master toggle for all hourly reference lines

Show Hour Delimiter: Toggle the vertical line marking each hour's start

Delimiter Color: Customize color and transparency

Delimiter Width: Set line thickness (1-5)

Show Hourly Open: Toggle the horizontal line at the hour's opening price

Open Line Color: Customize color

Open Line Width: Set thickness (1-5)

Open Line Style: Choose Solid, Dashed, or Dotted

Show Range Lines: Toggle the expected high/low projection lines

Range Statistic: Choose "Mean" (12-year average) or "Median" (12-year middle value)

Range High Color: Customize upper range line color and transparency

Range Low Color: Customize lower range line color and transparency

Range Line Width: Set thickness (1-5)

Range Line Style: Choose Solid, Dashed, or Dotted

Show Line Labels: Toggle price labels at the end of all horizontal lines

Label Text Size: Choose Tiny, Small, or Normal

How It Works:

FVG Detection Logic:

The indicator scans price action on the selected lower timeframe (default: 1-minute) looking for Fair Value Gaps using a 3-candle pattern:

Bullish FVG: Formed when candle 's high is below candle 's low, creating an upward gap

Bearish FVG: Formed when candle 's low is above candle 's high, creating a downward gap

The detection is refined using volume imbalance logic by checking for body gaps (outside prints) on both sides of the middle candle. This narrows the FVG zone to areas where bodies don't touch, indicating stronger imbalances.

Only the first FVG that forms during each hour is displayed. If a bullish FVG forms first, it takes priority. The FVG box is drawn from the formation time through to the end of the hour.

Statistical Analysis:

All probability statistics are hardcoded from 12 years (2,400+ samples per hour) of NASDAQ futures analysis:

First 15-Minute Direction: At 15 minutes into each hour, the indicator determines if price closed above, below, or equal to the hour's opening price

Continuation Probability: Historical analysis shows the likelihood that the hour closes in the same direction as the first 15 minutes

Example: If 9AM's first 15 minutes are bullish, there's a 60.1% chance the entire 9AM hour closes bullish (lowest continuation hour)

4PM shows the highest continuation at 86.1% for bullish first 15 minutes

FVG Effectiveness: Tracks how often the first FVG's direction correctly predicts the hourly close direction

BISI (Bullish Imbalance/Sell-side Inefficiency) → Bullish close probability

SIBI (Bearish Imbalance/Buy-side Inefficiency) → Bearish close probability

Range Expectations: Mean and median values represent typical price movement percentage for each hour

9AM and 10AM show the largest ranges (~0.6%)

5PM shows minimal range (~0.06%) due to low liquidity

Hourly Reference Lines:

When each new hour begins:

Vertical delimiter marks the hour's start

Hourly open line plots at the first bar's opening price

Range projection lines calculate expected high/low:

Upper Range = Hourly Open + (Range% / 100 × Hourly Open)

Lower Range = Hourly Open - (Range% / 100 × Hourly Open)

Lines extend exactly to the hour's end time

Labels appear at line endpoints showing exact prices

Real-Time Updates:

FVG Status: Updates immediately when the first FVG forms

First 15min Direction: Locked in at the 15-minute mark

Countdown Timer: Uses timenow to update every second

Table Statistics: Refresh on every bar close

Timezone Handling:

All times are in America/New_York (Eastern Time)

Automatically filters weekend periods (Saturday and Sunday before 6PM)

Hour detection accounts for daylight saving time changes

Use Cases:

Intraday Trading Strategy Development:

FVG Entry Signals: Use the first hourly FVG as a directional bias

Bullish FVG + High continuation % = Strong long setup

Bearish FVG + High continuation % = Strong short setup

First 15-Minute Breakout: Combine first 15-min direction with continuation probabilities

Wait for first 15 minutes to complete

If continuation % is above 70%, trade in that direction

Example: 4PM bullish first 15 min = 86.1% chance hour closes bullish

Range Targeting: Use expected high/low lines as profit targets or reversal zones

Price approaching mean high = potential resistance

Price approaching mean low = potential support

Compare mean vs median for different risk tolerance (median is more conservative)

Hour Selection: Focus trading on hours with:

High FVG effectiveness (11AM: 81.5% BISI→Bull)

High continuation rates (4PM: 86.1% bull continuation)

Avoid low-continuation hours like 9AM (60.1%)

Time Management: Use the countdown timer to:

Enter early in the hour when FVG forms

Exit before hour-end if no follow-through

Avoid late-hour entries with <15 minutes remaining

Statistical Edge Identification:

Compare current hour's FVG against historical effectiveness

Identify when first 15-min direction contradicts FVG direction (conflict = caution)

Use hourly bias to confirm or contradict FVG signals

Monitor if price stays within expected range or breaks out (outlier moves)

Risk Management:

Expected range lines provide logical stop-loss placement

FVG Effect % helps size positions (higher % = larger position)

Time Left countdown aids in time-based stop management

Avoid trading hours with neutral bias or low continuation rates

Statistical Foundation:

All embedded statistics are derived from:

12 years of NASDAQ futures (NQ) continuous contract data

5-minute timeframe FVG detection methodology

24 hours per day analysis (excluding weekends)

2,400+ samples per hour for robust statistical validity

America/New_York timezone for session alignment

Data includes:

Hourly range analysis (mean, median, standard deviation)

First 15-minute directional analysis

FVG formation frequency and effectiveness

Continuation probability matrices

Bullish/bearish bias percentages

Best Practices:

✅ Do:

Use exclusively on NASDAQ futures (NQ1! or MNQ1!)

Apply on 5-minute charts for optimal FVG detection matching statistical samples

Wait for first 15 minutes to complete before acting on continuation probabilities

Combine FVG signals with continuation % and FVG Effect % for confluence

Use expected range lines as initial profit targets

Monitor the countdown timer for time-based trade management

Focus on hours with high statistical edges (4PM, 11AM, 10AM)

❌ Don't:

Use on other markets (ES, RTY, YM, stocks, forex, crypto) - statistics will be invalid

Rely solely on FVG without confirming with continuation probabilities

Trade during low-liquidity hours (5PM shows only 0.06% average range)

Ignore the first 15-minute direction when it conflicts with FVG direction

Apply to timeframes significantly different from 5-minute for FVG detection

Use median range expectations aggressively (they're conservative)

Technical Implementation Notes:

Timezone: Fixed to America/New_York with automatic DST adjustment

Weekend Filtering: Automatically hides data Saturday and Sunday before 6PM ET

Performance: Maximum 500 boxes and 500 lines for optimal chart rendering

Update Frequency: Table updates on every bar close; timer updates every second using timenow

FVG Priority: Bullish FVGs take precedence when both form simultaneously

Lower Timeframe Detection: Uses request.security_lower_tf for accurate sub-chart-timeframe FVG detection

Precision: All price labels use format.mintick for appropriate decimal precision

Big thanks to @Trades-Dont-Lie for the FPFVG code in his excellent indicator that I've used here

Elliott Wave Full Fractal System v2.0Elliott Wave Full Fractal System v2.0 – Q.C. FINAL (Guaranteed R/R)

Elliott Wave Full Fractal System is a multi-timeframe wave engine that automatically labels Elliott impulses and ABC corrections, then builds a rule-based, ATR-driven risk/reward framework around the “W3–W4–W5” leg.

“Guaranteed R/R” here means every order is placed with a predefined stop-loss and take-profit that respect a minimum Reward:Risk ratio – it does not mean guaranteed profits.

Core Idea

This strategy turns a full fractal Elliott Wave labelling engine into a systematic trading model.

It scans fractal pivots on three wave degrees (Primary, Intermediate, Minor) to detect 5-wave impulses and ABC corrections.

A separate “Trading Degree” pivot stream, filtered by a 200-EMA trend filter and ATR-based dynamic pivots, is then used to find W4 pullback entries with a minimum, user-defined Reward:Risk ratio.

Default Properties & Risk Assumptions

The backtest uses realistic but conservative defaults:

// Default properties used for backtesting

strategy(

"Elliott Wave Full Fractal System - Q.C. FINAL (Guaranteed R/R)",

overlay = true,

initial_capital = 10000, // realistic account size

default_qty_type = strategy.percent_of_equity,

default_qty_value = 1, // 1% risk per trade

commission_type = strategy.commission.cash_per_contract,

commission_value = 0.005, // example stock commission

slippage = 0 // see notes below

)

Account size: 10,000 (can be changed to match your own account).

Position sizing: 1% of equity per trade to keep risk per idea sustainable and aligned with TradingView’s recommendations.

Commission: 0.005 cash per contract/share as a realistic example for stock trading.

Slippage: set to 0 in code for clarity of “pure logic” backtesting. Real-life trading will experience slippage, so users should adjust this according to their market and broker.

Always re-run the backtest after changing any of these values, and avoid using high risk fractions (5–10%+) as that is rarely sustainable.

1. Full Fractal Wave Engine

The script builds and maintains four pivot streams using ATR-adaptive fractals:

Primary Degree (Macro Trend):

Captures the large swings that define the major trend. Labels ①–⑤ and ⒶⒷⒸ using blue “Circle” labels and thicker lines.

Intermediate Degree (Trading Degree):

Captures the medium swings (swing-trading horizon). Uses teal labels ( (1)…(5), (A)(B)(C) ).

Minor Degree (Micro Structure):

Tracks short-term swings inside the larger waves. Uses red roman numerals (i…v, a b c).

ABC Corrections (Optional):

When enabled, the engine tries to detect standard A–B–C corrective structures that follow a completed 5-wave impulse and plots them with dashed lines.

Each degree uses a dynamic pivot lookback that expands when ATR is above its EMA, so the system naturally requires “stronger” pivots in volatile environments and reacts faster in quiet conditions.

2. Theory Rules & Strict Mode

Normal Mode: More permissive detection. Designed to show more wave structures for educational / exploratory use.

Strict Mode: Enforces key Elliott constraints:

Wave 3 not shorter than waves 1 and 5.

No invalid W4 overlap with W1 (for standard impulses).

ABC Logic: After a confirmed bullish impulse, the script expects a down-up-down corrective pattern (A,B,C). After a bearish impulse, it looks for up-down-up.

3. Trend Filter & Pivots

EMA Trend Filter: A configurable EMA (default 200) is used as a non-wave trend filter.

Price above EMA → Only long setups are considered.

Price below EMA → Only short setups are considered.

ATR-Adaptive Pivots: The pivot engine scales its left/right bars based on current ATR vs ATR EMA, making waves and trading pivots more robust in volatile regimes.

4. Dynamic Risk Management (Guaranteed R/R Engine)

The trading engine is designed around risk, not just pattern recognition:

ATR-Based Stop:

Stop-loss is placed at:

Entry ± ATR × Multiplier (user-configurable, default 2.0).

This anchors risk to current volatility.

Minimum Reward:Risk Ratio:

For each setup, the script:

Computes the distance from entry to stop (risk).

Projects a take-profit target at risk × min_rr_ratio away from entry.

Only accepts the setup if risk is positive and the required R:R ratio is achievable.

Result: Every order is created with both TP and SL at a predefined distance, so each trade starts with a known, minimum Reward:Risk profile by design.

“Guaranteed R/R” refers exclusively to this order placement logic (TP/SL geometry), not to win-rate or profitability.

5. Trading Logic – W3–W4–W5 Pattern

The Trading pivot stream (separate from visual wave degrees) looks for a simple but powerful pattern:

Bullish structure:

Sequence of pivots forms a higher-high / higher-low pattern.

Price is above the EMA trend filter.

A strong “W3” leg is confirmed with structure rules (optionally stricter in Strict mode).

Entry (Long – W4 Pullback):

The “height” of W3 is measured.

Entry is placed at a configurable Fibonacci pullback (default 50%) inside that leg.

ATR-based stop is placed below entry.

Take-profit is projected to satisfy min Reward:Risk.

Bearish structure:

Mirrored logic (lower highs/lows, price below EMA, W3 down, W4 retrace up, W5 continuation down).

Once a valid setup is found, the script draws a colored box around the entry zone and a label describing the type of signal (“LONG SETUP” or “SHORT SETUP”) with the suggested limit price.

6. Orders & Execution

Entry Orders: The strategy uses limit orders at the computed W4 level (“Sniper Long” or “Sniper Short”).

Exits: A single strategy.exit() is attached to each entry with:

Take-profit at the projected minimum R:R target.

Stop-loss at ATR-based level.

One Trade at a Time: New setups are only used when there is no open position (strategy.opentrades == 0) to keep the logic clear and risk contained.

7. Visual Guide on the Chart

Wave Labels:

Primary: ①,②,③,④,⑤, ⒶⒷⒸ

Intermediate: (1)…(5), (A)(B)(C)

Minor: i…v, a b c

Trend EMA: Single blue EMA showing the dominant trend.

Setup Boxes:

Green transparent box → long entry zone.

Red transparent box → short entry zone.

Labels: “LONG SETUP / SHORT SETUP” labels mark the proposed limit entry with price.

8. How to Use This Strategy

Attach the strategy to your chart

Choose your market (stocks, indices, FX, crypto, futures, etc.) and timeframe (for example 1h, 4h, or Daily). Then add the strategy to the chart from your Scripts list.

Start with the default settings

Leave all inputs on their defaults first. This lets you see the “intended” behaviour and the exact properties used for the published backtest (account size, 1% risk, commission, etc.).

Study the wave map

Zoom in and out and look at the three wave degrees:

Blue circles → Primary degree (big picture trend).

Teal (1)…(5) → Intermediate degree (swing structure).

Red i…v → Minor degree (micro waves).

Use this to understand how the engine is interpreting the Elliott structure on your symbol.

Watch for valid setups

Look for the coloured boxes and labels:

Green box + “LONG SETUP” label → potential W4 pullback long in an uptrend.

Red box + “SHORT SETUP” label → potential W4 pullback short in a downtrend.

Only trades in the direction of the EMA trend filter are allowed by the strategy.

Check the Reward:Risk of each idea

For each setup, inspect:

Limit entry price.

ATR-based stop level.

Projected take-profit level.

Make sure the minimum Reward:Risk ratio matches your own rules before you consider trading it.

Backtest and evaluate

Open the Strategy Tester:

Verify you have a decent sample size (ideally 100+ trades).

Check drawdowns, average trade, win-rate and R:R distribution.

Change markets and timeframes to see where the logic behaves best.

Adapt to your own risk profile

If you plan to use it live:

Set Initial Capital to your real account size.

Adjust default_qty_value to a risk level you are comfortable with (often 0.5–2% per trade).

Set commission and slippage to realistic broker values.

Re-run the backtest after every major change.

Use as a framework, not a signal machine