TGS By ShadTGS Levels — Tesla–W.D. Gann Strategy

TGS Levels is a price-geometry indicator designed to map algorithmic decision zones on the chart using principles inspired by W.D. Gann price geometry and Tesla 3-6-9 harmonic structure.

This indicator is not a signal generator.

It provides a structured price map to help traders understand where reactions or breakouts are statistically more likely to occur.

🔹 Core Concept

Markets do not move randomly.

They rotate and expand around harmonic price cycles.

TGS Levels automatically plots a 100-unit price cycle framework (ideal for XAUUSD / Gold) and divides each cycle into hierarchical angles used by institutional and algorithmic trading models.

🔹 Level Hierarchy (Very Important)

TGS uses four types of levels, each with a different purpose:

🔴 SUPER ANGLE (+45)

Primary decision level

Price often shows strong rejection or explosive breakout

Highest importance level

🟥 MAIN ANGLES (+27, +63, +81)

High-probability reaction zones

Used for structured pullbacks, rejections, or continuation confirmation

🟠 SECONDARY ANGLES (+18, +36, +54, +72, +90)

Context & management levels

Expect hesitation, partial profit zones, or stop-tightening areas

Not recommended for direct entries

🟡 MICRO LEVELS (+3, +6, +9)

Liquidity & compression map

Help visualize absorption, stop hunts, and consolidation

For structure awareness only

🔹 What This Indicator Is Used For

✔ Identifying where price is likely to react

✔ Understanding market structure and rotation

✔ Distinguishing rejection vs breakout zones

✔ Improving trade timing when combined with:

Volatility (ATR)

Market structure (HL / LH / BOS)

Session timing (London / New York)

🔹 What This Indicator Is NOT

❌ Not a buy/sell signal

❌ Not a prediction tool

❌ Not based on indicators like RSI or MACD

TGS Levels is a price-first framework, designed to be used with price action, volatility, and structure.

🔹 Best Use Case

Asset: XAUUSD (Gold)

Execution Timeframe: M5

Sessions: London & New York

Style: Scalping / Intraday structure trading

The same logic can be adapted to other instruments by adjusting the cycle size.

🔹 How to Trade With TGS (High-Level)

When volatility is low or falling → expect rejections at main/super angles

When volatility is expanding → expect breakouts through angles

Use oscillators (like Stochastic) only for timing, not direction

Always confirm with price behavior at the level

🔹 Final Note

TGS Levels provides a clean, non-repainting price map that stays aligned when zooming or scrolling the chart.

All levels are calculated automatically and update dynamically with price.

Levels explain behavior — reactions create opportunity.

Search in scripts for "sessions"

TGS by Shad TGS Levels — Tesla–W.D. Gann Strategy

TGS Levels is a price-geometry indicator designed to map algorithmic decision zones on the chart using principles inspired by W.D. Gann price geometry and Tesla 3-6-9 harmonic structure.

This indicator is not a signal generator.

It provides a structured price map to help traders understand where reactions or breakouts are statistically more likely to occur.

🔹 Core Concept

Markets do not move randomly.

They rotate and expand around harmonic price cycles.

TGS Levels automatically plots a 100-unit price cycle framework (ideal for XAUUSD / Gold) and divides each cycle into hierarchical angles used by institutional and algorithmic trading models.

🔹 Level Hierarchy (Very Important)

TGS uses four types of levels, each with a different purpose:

🔴 SUPER ANGLE (+45)

Primary decision level

Price often shows strong rejection or explosive breakout

Highest importance level

🟥 MAIN ANGLES (+27, +63, +81)

High-probability reaction zones

Used for structured pullbacks, rejections, or continuation confirmation

🟠 SECONDARY ANGLES (+18, +36, +54, +72, +90)

Context & management levels

Expect hesitation, partial profit zones, or stop-tightening areas

Not recommended for direct entries

🟡 MICRO LEVELS (+3, +6, +9)

Liquidity & compression map

Help visualize absorption, stop hunts, and consolidation

For structure awareness only

🔹 What This Indicator Is Used For

✔ Identifying where price is likely to react

✔ Understanding market structure and rotation

✔ Distinguishing rejection vs breakout zones

✔ Improving trade timing when combined with:

Volatility (ATR)

Market structure (HL / LH / BOS)

Session timing (London / New York)

🔹 What This Indicator Is NOT

❌ Not a buy/sell signal

❌ Not a prediction tool

❌ Not based on indicators like RSI or MACD

TGS Levels is a price-first framework, designed to be used with price action, volatility, and structure.

🔹 Best Use Case

Asset: XAUUSD (Gold)

Execution Timeframe: M5

Sessions: London & New York

Style: Scalping / Intraday structure trading

The same logic can be adapted to other instruments by adjusting the cycle size.

🔹 How to Trade With TGS (High-Level)

When volatility is low or falling → expect rejections at main/super angles

When volatility is expanding → expect breakouts through angles

Use oscillators (like Stochastic) only for timing, not direction

Always confirm with price behavior at the level

🔹 Final Note

TGS Levels provides a clean, non-repainting price map that stays aligned when zooming or scrolling the chart.

All levels are calculated automatically and update dynamically with price.

Levels explain behavior — reactions create opportunity.

Kabroda BattleBox Command [Renderer]Kabroda BattleBox Command

This is a specialized visualization utility designed to render pre-calculated institutional price levels on your chart. It is intended for traders who utilize the Kabroda Daily Calibration method to define their intraday execution framework.

How it Works: This script does not calculate levels internally. Instead, it serves as a "renderer" for external data.

Input: The user inputs a comma-separated data string (generated daily via their Kabroda Dashboard calibration) into the settings.

Parsing: The script parses this string to extract 6 key price coordinates: Daily Resistance, Breakout Trigger, Breakdown Trigger, Daily Support, and the 30-minute Opening Range High/Low.

Visualizing: It projects these levels forward in time for the current trading session.

Key Features:

Execution Levels: Plots specific Breakout and Breakdown triggers derived from the opening 30-minute volatility.

Liquidity Sessions: Automatically highlights key global trading hours (London Open, NY AM, NY PM, Tokyo, Sydney) based on New York Time, helping traders visualize volume injection points.

Imbalance Zones (Optional): Identifies and highlights market imbalances created by aggressive buying or selling, which often act as magnets for price re-tests.

Usage Guide:

Step 1: Obtain your daily data string.

Step 2: Open Indicator Settings -> "Daily Calibration".

Step 3: Paste the string into the "Paste Data String" field.

Step 4: The script will instantly render the day's battle map.

Disclaimer: This tool is a visualization aid. It requires valid external data to function. Without the daily input string, the chart will remain blank.

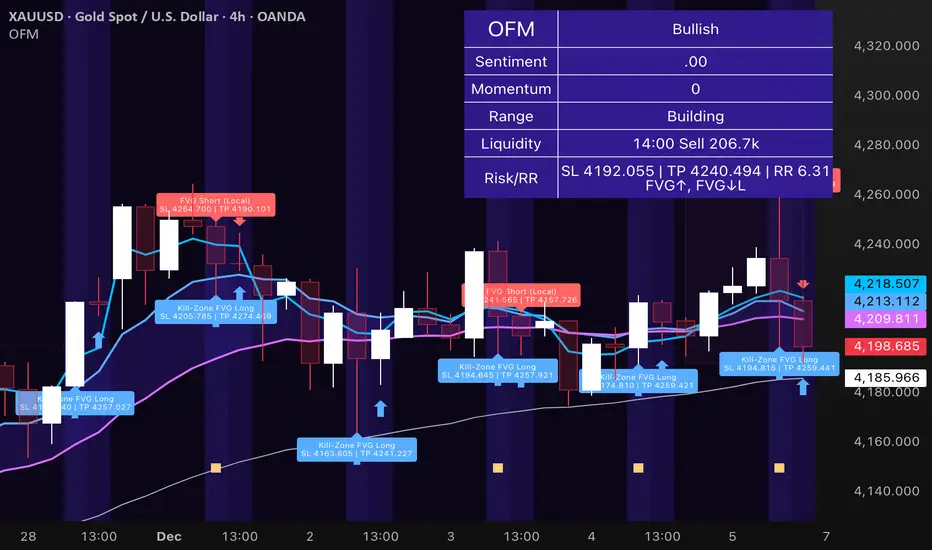

Obsidian Flux Matrix# Obsidian Flux Matrix | JackOfAllTrades

Made with my Senior Level AI Pine Script v6 coding bot for the community!

Narrative Overview

Obsidian Flux Matrix (OFM) is an open-source Pine Script v6 study that fuses social sentiment, higher timeframe trend bias, fair-value-gap detection, liquidity raids, VWAP gravitation, session profiling, and a diagnostic HUD. The layout keeps the obsidian palette so critical overlays stay readable without overwhelming a price chart.

Purpose & Scope

OFM focuses on actionable structure rather than marketing claims. It documents every driver that powers its confluence engine so reviewers understand what triggers each visual.

Core Analytical Pillars

1. Social Pulse Engine

Sentiment Webhook Feed: Accepts normalized scores (-1 to +1). Signals only arm when the EMA-smoothed value exceeds the `sentimentMin` input (0.35 by default).

Volume Confirmation: Requires local volume > 30-bar average × `volSpikeMult` (default 2.0) before sentiment flags.

EMA Cross Validation: Fast EMA 8 crossing above/below slow EMA 21 keeps momentum aligned with flow.

Momentum Alignment: Multi-timeframe momentum composite must agree (positive for longs, negative for shorts).

2. Peer Momentum Heatmap

Multi-Timeframe Blend: RSI + Stoch RSI fetched via request.security() on 1H/4H/1D by default.

Composite Scoring: Each timeframe votes +1/-1/0; totals are clamped between -3 and +3.

Intraday Readability: Configurable band thickness (1-5) so scalpers see context without losing space.

Dynamic Opacity: Stronger agreement boosts column opacity for quick bias checks.

3. Trend & Displacement Framework

Dual EMA Ribbon: Cyan/magenta ribbon highlights immediate posture.

HTF Bias: A higher-timeframe EMA (default 55 on 4H) sets macro direction.

Displacement Score: Body-to-ATR ratio (>1.4 default) detects impulses that seed FVGs or VWAP raids.

ATR Normalization: All thresholds float with volatility so the study adapts to assets and regimes.

4. Intelligent Fair Value Gap (FVG) System

Gap Detection: Three-candle logic (bullish: low > high ; bearish: high < low ) with ATR-sized minimums (0.15 × ATR default).

Overlap Prevention: Price-range checks stop redundant boxes.

Spacing Control: `fvgMinSpacing` (default 5) avoids stacking from the same impulse.

Storage Caps: Max three FVGs per side unless the user widens the limit.

Session Awareness: Kill zone filters keep taps focused on London/NY if desired.

Auto Cleanup: Boxes delete when price closes beyond their invalidation level.

5. VWAP Magnet + Liquidity Raid Engine

Session or Rolling VWAP: Toggle resets to match intraday or rolling preferences.

Equal High/Low Scanner: Looks back 20 bars by default for liquidity pools.

Displacement Filter: ATR multiplier ensures raids represent genuine liquidity sweeps.

Mean Reversion Focus: Signals fire when price displaces back toward VWAP following a raid.

6. Session Range Breakout System

Initial Balance Tracking: First N bars (15 default) define the session box.

Breakout Logic: Requires simultaneous liquidity spikes, nearby FVG activity, and supportive momentum.

Z-Score Volume Filter: >1.5σ by default to filter noisy moves.

7. Lifestyle Liquidity Scanner

Volume Z-Scores: 50-bar baseline highlights statistically significant spikes.

Smart Money Footprints: Bottom-of-chart squares color-code buy vs sell participation.

Panel Memory: HUD logs the last five raid timestamps, direction, and normalized size.

8. Risk Matrix & Diagnostic HUD

HUD Structure: Table in the top-right summarizes HTF bias, sentiment, momentum, range state, liquidity memory, and current risk references.

Signal Tags: Aggregates SPS, FVG, VWAP, Range, and Liquidity states into a compact string.

Risk Metrics: Swing-based stops (5-bar lookback) + ATR targets (1.5× default) keep risk transparent.

Signal Families & Alerts

Social Pulse (SPS): Volume-confirmed sentiment alignment; triangle markers with “SPS”.

Kill-Zone FVG: Session + HTF alignment + FVG tap; arrow markers plus SL/TP labels.

Local FVG: Captures local reversals when HTF bias has not flipped yet.

VWAP Raid: Equal-high/low raids that snap toward VWAP; “VWAP” label markers.

Range Breakout: Initial balance violations with liquidity and imbalance confirmation; circle markers.

Liquidity Spike: Z-score spikes ≥ threshold; square markers along the baseline.

Visual Design & Customization

Theme Palette: Primary background RGB (12,6,24). Accent shading RGB (26,10,48). Long accents RGB (88,174,255). Short accents RGB (219,109,255).

Stylized Candles: Optional overlay using theme colors.

Signal Toggles: Independently enable markers, heatmap, and diagnostics.

Label Spacing: Auto-spacing enforces ≥4-bar gaps to prevent text overlap.

Customization & Workflow Notes

Adjust ATR/FVG thresholds when volatility shifts.

Re-anchor sentiment to your webhook cadence; EMA smoothing (default 5) dampens noise.

Reposition the HUD by editing the `table.new` coordinates.

Use multiples of the chart timeframe for HTF requests to minimize load.

Session inputs accept exchange-local time; align them to your market.

Performance & Compliance

Pure Pine v6: Single-line statements, no `lookahead_on`.

Resource Safe: Arrays trimmed, boxes limited, `request.security` cached.

Repaint Awareness: Signals confirm on close; alerts mirror on-chart logic.

Runtime Safety: Arrays/loops guard against `na`.

Use Cases

Measure when social sentiment aligns with structure.

Plan ICT-style intraday rebalances around session-specific FVG taps.

Fade VWAP raids when displacement shows exhaustion.

Watch initial balance breaks backed by statistical volume.

Keep risk/target references anchored in ATR logic.

Signal Logic Snapshot

Social Pulse Long/Short: `sentimentEMA` gated by `sentimentMin`, `volSpike`, EMA 8/21 cross, and `momoComposite` sign agreement. Keeps hype tied to structural follow-through.

Kill-Zone FVG Long/Short: Requires session filter, HTF EMA bias alignment, and an active FVG tap (`bullFvgTap` / `bearFvgTap`). Labels include swing stops + ATR targets pulled from `swingLookback` and `liqTargetMultiple`.

Local FVG Long/Short: Uses `localBullish` / `localBearish` heuristics (EMA slope, displacement, sequential closes) to surface intraday reversals even when HTF bias has not flipped.

VWAP Raids: Detect equal-high/equal-low sweeps (`raidHigh`, `raidLow`) that revert toward `sessionVwap` or rolling VWAP when displacement exceeds `vwapAlertDisplace`.

Range Breakouts: Combine `rangeComplete`, breakout confirmation, liquidity spikes, and nearby FVG activity for statistically backed initial balance breaks.

Liquidity Spikes: Volume Z-score > `zScoreThreshold` logs direction, size, and timestamp for the HUD and optional review workflows.

Session Logic & VWAP Handling

Kill zone + NY session inputs use TradingView’s session strings; `f_inSession()` drives both visual shading and whether FVG taps are tradeable when `killZoneOnly` is true.

Session VWAP resets using cumulative price × volume sums that restart when the daily timestamp changes; rolling VWAP falls back to `ta.vwap(hlc3)` for instruments where daily resets are less relevant.

Initial balance box (`rangeBars` input) locks once complete, extends forward, and stays on chart to contextualize later liquidity raids or breakouts.

Parameter Reference

Trend: `emaFastLen`, `emaSlowLen`, `htfResolution`, `htfEmaLen`, `showEmaRibbon`, `showHtfBiasLine`.

Momentum: `tf1`, `tf2`, `tf3`, `rsiLen`, `stochLen`, `stochSmooth`, `heatmapHeight`.

Volume/Liquidity: `volLookback`, `volSpikeMult`, `zScoreLen`, `zScoreThreshold`, `equalLookback`.

VWAP & Sessions: `vwapMode`, `showVwapLine`, `vwapAlertDisplace`, `killSession`, `nySession`, `showSessionShade`, `rangeBars`.

FVG/Risk: `fvgMinTicks`, `fvgLookback`, `fvgMinSpacing`, `killZoneOnly`, `liqTargetMultiple`, `swingLookback`.

Visualization Toggles: `showSignalMarkers`, `showHeatmapBand`, `showInfoPanel`, `showStylizedCandles`.

Workflow Recipes

Kill-Zone Continuation: During the defined kill session, look for `killFvgLong` or `killFvgShort` arrows that line up with `sentimentValid` and positive `momoComposite`. Use the HUD’s risk readout to confirm SL/TP distances before entering.

VWAP Raid Fade: Outside kill zone, track `raidToVwapLong/Short`. Confirm the candle body exceeds the displacement multiplier, and price crosses back toward VWAP before considering reversions.

Range Break Monitor: After the initial balance locks, mark `rangeBreakLong/Short` circles only when the momentum band is >0 or <0 respectively and a fresh FVG box sits near price.

Liquidity Spike Review: When the HUD shows “Liquidity” timestamps, hover the plotted squares at chart bottom to see whether spikes were buy/sell oriented and if local FVGs formed immediately after.

Metadata

Author: officialjackofalltrades

Platform: TradingView (Pine Script v6)

Category: Sentiment + Liquidity Intelligence

Hope you Enjoy!

Live Session Extremes: Asia / London / NY (5m)This script automatically tracks and plots the live high and low levels of the three major Forex trading sessions:

Asia Session (18:00–03:00) — Teal

London Session (03:00–08:00) — Blue

New York Session (08:00–12:00) — Red

Designed specifically for 5-minute charts, it updates in real time as each session forms new highs or lows.

You always see the most recent session’s levels, cleanly plotted and color-coded on your chart.

✔ Features

Live updating lines for each session’s high & low

Lines anchored to the exact candles that created the extreme

Auto-cleaning: old session levels are deleted when a new session begins

Clear labeling:

Asia High / Asia Low (Teal)

London High / London Low (Blue)

NY High / NY Low (Red)

Extend-right option for projecting session levels into future price action

Built for precision session-based strategies such as:

Liquidity grabs

Session sweeps

BOS/CHOCH analysis

ICT-style trading

High/low power levels

Cora Combined Suite v1 [JopAlgo]Cora Combined Suite v1 (CCSV1)

This is an 2 in 1 indicator (Overlay & Oscillator) the Cora Combined Suite v1 .

CCSV1 combines a price-pane Overlay for structure/trend with a compact Oscillator for timing/pressure. It’s designed to be clear, beginner-friendly, and largely automatic: you pick a profile (Scalp / Intraday / Swing), choose whether to run as Overlay or Oscillator, and CCSV1 tunes itself in the background.

What’s inside — at a glance

1) Overlay (price pane)

CoRa Wave: a smooth trend line based on a compound-ratio WMA (CRWMA).

Green when the slope rises (bull bias), Red when it falls (bear bias).

Asymmetric ATR Cloud around the CoRa Wave

Width expands more up when buyer pressure dominates and more down when seller pressure dominates.

Fill is intentionally light, so candlesticks remain readable.

Chop Guard (Range-Lock Gate)

When the cloud stays very narrow versus ATR (classic “dead water”), pullback alerts are muted to avoid noise.

Visuals don’t change—only the alerting logic goes quiet.

Typical Overlay reads

Trend: Follow the CoRa color; green favors long setups, red favors shorts.

Value: Pullbacks into/through the cloud in trend direction are higher-quality than chasing breaks far outside it.

Dominance: A visibly asymmetric cloud hints which side is funding the move (buyers vs sellers).

2) Oscillator (subpane or inline preview)

Stretch-Z (columns): how far price is from the CoRa mean (mean-reversion context), clipped to ±clip.

Near 0 = equilibrium; > +2 / < −2 = stretched/extended.

Slope-Z (line): z-score of CoRa’s slope (momentum of the trend line).

Crossing 0 upward = potential bullish impulse; downward = potential bearish impulse.

VPO (stepline): a normalized Volume-Pressure read (positive = buyers funding, negative = sellers).

Rendered as a clean stepline to emphasize state changes.

Event Bands ±2 (subpane): thin reference lines to spot extension/exhaustion zones fast.

Floor/Ceiling lines (optional): quiet boundaries so the panel doesn’t feel “bottomless.”

Inline vs Subpane

Inline (overlay): the oscillator auto-anchors and scales beneath price, so it never crushes the price scale.

Subpane (raw): move to a new pane for the classic ±clip view (with ±2 bands). Recommended for systematic use.

Why traders like it

Two in one: Structure on the chart, timing in the panel—built to complement each other.

Retail-first automation: Choose Scalp / Intraday / Swing and let CCSV1 auto-tune lengths, clips, and pressure windows.

Robust statistics: On fast, spiky markets/timeframes, it prefers outlier-resistant math automatically for steadier signals.

Optional HTF gate: You can require higher-timeframe agreement for oscillator alerts without changing visuals.

Quick start (simple playbook)

Run As

Overlay for structure: assess trend direction, where value is (the cloud), and whether chop guard is active.

Oscillator for timing: move to a subpane to see Stretch-Z, Slope-Z, VPO, and ±2 bands clearly.

Profile

Scalp (1–5m), Intraday (15–60m), or Swing (4H–1D). CCSV1 adjusts length/clip/pressure windows accordingly.

Overlay entries

Trade with CoRa color.

Prefer pullbacks into/through the cloud (trend direction).

If chop guard is active, wait; let the market “breathe” before engaging.

Oscillator timing

Look for Funded Flips: Slope-Z crossing 0 in the direction of VPO (i.e., momentum + funded pressure).

Use ±2 bands to manage risk: stretched conditions can stall or revert—better to scale or wait for a clean reset.

Optional HTF gate

Enable to green-light only those oscillator alerts that align with your chosen higher timeframe.

What each signal means (plain language)

CoRa turns green/red (Overlay): trend bias shift on your chart.

Cloud width tilts asymmetrically: one side (buyers/sellers) is dominating; extensions on that side are more likely.

Stretch-Z near 0: fair value around CoRa; pullback timing zone.

Stretch-Z > +2 / < −2: extended; watch for slowing momentum or scale decisions.

Slope-Z cross up/down: new impulse starting; combine with VPO sign to avoid unfunded crosses.

VPO positive/negative: net buying/selling pressure funding the move.

Alerts included

Overlay

Pullback Long OK

Pullback Short OK

Oscillator

Funded Flip Up / Funded Flip Down (Slope-Z crosses 0 with VPO agreement)

Pullback Long Ready / Pullback Short Ready (near equilibrium with aligned momentum and pressure)

Exhaustion Risk (Long/Short) (Stretch-Z beyond ±2 with weakening momentum or pressure)

Tip: Keep chart alerts concise and use strategy rules (TP/SL/filters) in your trade plan.

Best practices

One glance workflow

Read Overlay for direction + value.

Use Oscillator for trigger + confirmation.

Pairing

Combine with S/R or your preferred execution framework (e.g., your JopAlgo setups).

The suite is neutral: it won’t force trades; it highlights context and quality.

Markets

Works on crypto, indices, FX, and commodities.

Where real volume is available, VPO is strongest; on synthetic volume, treat VPO as a soft filter.

Timeframes

Use the Profile preset closest to your style; feel free to fine-tune later.

For multi-TF trading, enable the HTF gate on the oscillator alerts only.

Inputs you’ll actually use (the rest can stay on Auto)

Run As: Overlay or Oscillator.

Profile: Scalp / Intraday / Swing.

Oscillator Render: “Subpane (raw)” for a classic panel; “Inline (overlay)” only for a quick preview.

HTF gate (optional): require higher-timeframe Slope-Z agreement for oscillator alerts.

Everything else ships with sensible defaults and auto-logic.

Limitations & tips

Not a strategy: CCSV1 is a decision support tool; you still need your entry/exit rules and risk management.

Non-repainting design: Signals finalize on bar close; intrabar graphics can adjust during the bar (Pine standard).

Very flat sessions: If price and volume are extremely quiet, expect fewer alerts; that restraint is intentional.

Who is this for?

Beginners who want one clean overlay for structure and one simple oscillator for timing—without wrestling settings.

Intermediates seeking a coherent trend/pressure framework with HTF confirmation.

Advanced users who appreciate robust stats and clean engineering behind the visuals.

Disclaimer: Educational purposes only. Not financial advice. Trading involves risk. Use at your own discretion.

XAUUSD Family Scalping (5min)🟡 XAUUSD Family Scalping 5-Min — Momentum Precision Indicator

Overview

This indicator is built for XAUUSD (Gold) on the 5-minute timeframe and is designed for short-term momentum scalping.

It helps traders identify early reversal zones, confirm momentum direction, and detect exhaustion points during high-volatility market moves.

Core Concept

The indicator measures momentum strength and price acceleration using a smoothed oscillator.

It features two adjustable thresholds:

Overbought level: 58

Oversold level: -58

When the momentum line crosses above or below these zones, it signals potential trend continuation or reversal opportunities.

Features

Detects short-term momentum shifts on XAUUSD 5M.

Works with EMA-based trend confirmation (optional).

Adaptive smoothing reduces noise and false reversals.

Highlights overbought/oversold areas visually.

Can be combined with price action or other oscillators for confluence.

Usage

Instrument: XAUUSD (Gold)

Best timeframe: 5-minute (scalping setup)

Use case: Detecting momentum exhaustion and reversal entries.

Sessions: London & New York recommended.

Disclaimer

This indicator is for market analysis and educational purposes.

No indicator guarantees profit — use proper risk management and test before live trading.

ICT Macro Time WindowsICT Macro Time Windows - Master institutional market timing with automated 'Macro' trading session tracking.

What are 'Macros'?

In ICT terminology, 'Macros' refer to the key institutional trading windows throughout the day where major banks and liquidity providers are most active. These specific time frames see heightened volatility, liquidity, and strategic positioning.

Perfect Timing Automation:

• 8 Critical Macro Sessions:

London 1: 02:33-03:00 EST

London 2: 04:03-04:30 EST

NY AM1: 08:50-09:10 EST

NY AM2: 09:50-10:10 EST

NY AM3: 10:50-11:10 EST

Lunch: 11:50-12:10 EST

PM: 13:10-13:40 EST

Close: 15:15-15:45 EST

• Fully customizable time zones and session times

• Real-time session detection with visual zones & labels

• Automatic High/Low range tracking within each window

• Boxes, lines, and labels for clear visual reference

• Never miss optimal entry/exit timing again

Trade when institutions trade - stop guessing and start timing your setups with precision during these key liquidity windows! All session times are easily adjustable in settings to match your preferred trading hours.

Perfect for Forex, Futures, and Index traders following ICT concepts and institutional flow analysis.

Europe Session LinesThis simple script marks the start of the European trading sessions:

08:00 a.m. London trading session

09:00 a.m. Frankfurt trading session

The settings of the lines can be changed. (thickness, colour, type).

It can be used on Futures and CFDs for example for FDAX, FTSE100 but also for GOLD, Silver and EURO- and GBP based FX pairs as supply or demand zone with the change of character trading setup.

Trend-Strong Candle - 3 EMAs with Filters# Trend-Strong Candle - Professional Trading Indicator

## 📊 What It Does

Identifies high-probability entries by combining triple EMA trend analysis with strong candle detection. Only signals when all conditions align for maximum accuracy.

## 🎯 Core Features

- Triple EMA System: Fast (20) / Medium (50) / Slow (200) for trend confirmation

- Strong Candle Filter: ATR-based sizing ensures genuine momentum

- Advanced Filters: EMA close validation + trend stability checks

- Live Alerts: Instant notifications for real-time signals

- Session Filter: Trade only during active EU/US market hours

## ⚡ Quick Setup

Scalping (1-5min): Default settings + enable session filter

Day Trading (15-60min): Default settings work perfectly

Swing Trading (4H+): Increase ATR multiplier to 0.8-1.0

## 📈 Trading Rules

Long Signals: Green triangle below candle

- Strong bullish candle during confirmed uptrend

- All EMAs properly aligned (Fast > Medium > Slow)

Short Signals: Red triangle above candle

- Strong bearish candle during confirmed downtrend

- All EMAs properly aligned (Fast < Medium < Slow)

## ⚠️ Critical Success Factors

1. Always Verify the Trend Yourself

The indicator helps identify signals, but YOU must confirm the larger trend context. Check higher timeframes and overall market structure before entering.

2. Understand the "Big Players"

Strong candles in trend direction usually come from institutional money (banks, funds, algorithms). These create the momentum that retail traders can follow. The indicator catches these institutional moves.

3. Distance to Next Value Level

NEVER enter if price is too close to major resistance/support levels:

- Check distance to round numbers (1.1000, 1.1050, etc.)

- Ensure at least 20-30 pips room to next key level

- You need space for profit - tight levels = limited upside

4. Risk Management

- Stop Loss: 1-2 ATR from entry

- Take Profit: 2-3 ATR target (minimum 1:2 R/R)

- Position Size: Risk max 1-2% per trade

## 💡 Pro Tips

- Best Sessions: London open (8-12 UTC) and NY open (13-17 UTC)

- Avoid: Major news, low liquidity periods, choppy markets

- Multiple Timeframes: Confirm signals on higher timeframe

- Value Levels: Always check daily/weekly support/resistance before entering

## 🎯 Success Formula

Trend Confirmation + Strong Institutional Candle + Distance to Value Levels = High Probability Trade

*

Remember: The indicator finds the signals, but successful trading requires your analysis of trend context and value level positioning. Trade smart, not just frequent.

Dynamic Swing Anchored VWAP STRAT (Zeiierman/PineIndicators)Dynamic Swing Anchored VWAP STRATEGY — Zeiierman × PineIndicators (Pine Script v6)

A pivot-to-pivot Anchored VWAP strategy that adapts to volatility, enters long on bullish structure, and closes on bearish structure. Built for TradingView in Pine Script v6.

Full credits to zeiierman.

Repainting notice: The original indicator logic is repainting. Swing labels (HH/HL/LH/LL) are finalized after enough bars have printed, so labels do not occur in real time. It is not possible to execute at historical label points. Treat results as educational and validate with Bar Replay and paper trading before considering any discretionary use.

Concept

The script identifies swing highs/lows over a user-defined lookback ( Swing Period ). When structure flips (most recent swing low is newer than the most recent swing high, or vice versa), a new regime begins.

At each confirmed pivot, a fresh Anchored VWAP segment is started and updated bar-by-bar using an EWMA-style decay on price×volume and volume.

Responsiveness is controlled by Adaptive Price Tracking (APT) . Optionally, APT auto-adjusts with an ATR ratio so that high volatility accelerates responsiveness and low volatility smooths it.

Longs are opened/held in bullish regimes and closed when the regime turns bearish. No short positions are taken by design.

How it works (under the hood)

Swing detection: Uses ta.highestbars / ta.lowestbars over prd to update swing highs (ph) and lows (pl), plus their bar indices (phL, plL).

Regime logic: If phL > plL → bullish regime; else → bearish regime. A change in this condition triggers a re-anchor of the VWAP at the newest pivot.

Adaptive VWAP math: APT is converted to an exponential decay factor ( alphaFromAPT ), then applied to running sums of price×volume and volume, producing the current VWAP estimate.

Rendering: Each pivot-anchored VWAP segment is drawn as a polyline and color-coded by regime. Optional structure labels (HH/HL/LH/LL) annotate the swing character.

Orders: On bullish flips, strategy.entry("L") opens/maintains a long; on bearish flips, strategy.close("L") exits.

Inputs & controls

Swing Period (prd) — Higher values identify larger, slower swings; lower values catch more frequent pivots but add noise.

Adaptive Price Tracking (APT) — Governs the VWAP’s “half-life.” Smaller APT → faster/closer to price; larger APT → smoother/stabler.

Adapt APT by ATR ratio — When enabled, APT scales with volatility so the VWAP speeds up in turbulent markets and slows down in quiet markets.

Volatility Bias — Tunes the strength of APT’s response to volatility (above 1 = stronger effect; below 1 = milder).

Style settings — Colors for swing labels and VWAP segments, plus line width for visibility.

Trade logic summary

Entry: Long when the swing structure turns bullish (latest swing low is more recent than the last swing high).

Exit: Close the long when structure turns bearish.

Position size: qty = strategy.equity / close × 5 (dynamic sizing; scales with account equity and instrument price). Consider reducing the multiplier for a more conservative profile.

Recommended workflow

Apply to instruments with reliable volume (equities, futures, crypto; FX tick volume can work but varies by broker).

Start on your preferred timeframe. Intraday often benefits from smaller APT (more reactive); higher timeframes may prefer larger APT (smoother).

Begin with defaults ( prd=50, APT=20 ); then toggle “Adapt by ATR” and vary Volatility Bias to observe how segments tighten/loosen.

Use Bar Replay to watch how pivots confirm and how the strategy re-anchors VWAP at those confirmations.

Layer your own risk rules (stops/targets, max position cap, session filters) before any discretionary use.

Practical tips

Context filter: Consider combining with a higher-timeframe bias (e.g., daily trend) and using this strategy as an entry timing layer.

First pivot preference: Some traders prefer only the first bullish pivot after a bearish regime (and vice versa) to reduce whipsaw in choppy ranges.

Deviations: You can add VWAP deviation bands to pre-plan partial exits or re-entries on mean-reversion pulls.

Sessions: Session-based filters (RTH vs. ETH) can materially change behavior on futures and equities.

Extending the script (ideas)

Add stops/targets (e.g., ATR stop below last swing low; partial profits at k×VWAP deviation).

Introduce mirrored short logic for two-sided testing.

Include alert conditions for regime flips or for price-VWAP interactions.

Incorporate HTF confirmation (e.g., only long when daily VWAP slope ≥ 0).

Throttle entries (e.g., once per regime flip) to avoid over-trading in ranges.

Known limitations

Repainting: Swing labels and pivot confirmations depend on future bars; historical labels can look “perfect.” Treat them as annotations, not executable signals.

Execution realism: Strategy includes commission and slippage fields, yet actual fills differ by venue/liquidity.

No guarantees: Past behavior does not imply future results. This publication is for research/education only and not financial advice.

Defaults (backtest environment)

Initial capital: 10,000

Commission value: 0.01

Slippage: 1

Overlay: true

Max bars back: 5000; Max labels/polylines set for deep swing histories

Quick checklist

Add to chart and verify that the instrument has volume.

Use defaults, then tune APT and Volatility Bias with/without ATR adaptation.

Observe how each pivot re-anchors VWAP and how regime flips drive entries/exits.

Paper trade across several symbols/timeframes before any discretionary decisions.

Attribution & license

Original indicator concept and logic: Zeiierman — please credit the author.

Strategy wrapper and publication: PineIndicators .

License: CC BY-NC-SA 4.0 (Attribution-NonCommercial-ShareAlike). Respect the license when forking or publishing derivatives.

MACROFLOW 200 — Bias & Triggersstephtradez model

MACROFLOW 200 — at a glance (the elevator pitch)

Trade direction = Macro Bias + 1H 200 EMA filter + DXY confirm.

Locations = 1H supply/demand zones.

Triggers (15m): (T1) Retest rejection, (T2) Liquidity sweep + BOS/CHOCH, (T3) Momentum break + shallow pullback.

Stops: structure‑based beyond zone with ATR buffer.

Targets: 2R base, scale at 1.5R, trail to next HTF zone.

Sessions: 7–10 pm ET and 9:30–10:30 am ET.

Risk: tight, prop‑friendly max 1% per session

GeeksDoByte 15m & 30m ORB + Prev Day High/LowCME_MINI:NQ1!

How It Works

Opening Ranges

At 9:30 ET, the script begins tracking the high & low.

It uses two fixed sessions:

15 min from 09:30 to 09:45

30 min from 09:30 to 10:00

On the very first bar of each session it initializes the range, then continuously updates the high/low on each new intraday bar.

Dashed lines are drawn when the session opens and extended horizontally across subsequent bars.

Previous Day’s Levels

Independently, it fetches yesterday’s high and low via a daily security call.

These historic levels are plotted as simple horizontal lines for daily context.

How to Use

Breakout Entries

A close above the 15 min ORB high can signal an early breakout; a further push above the 30 min ORB high confirms extended momentum.

Conversely, breaks below the respective lows can indicate short setups.

Support & Resistance

Yesterday’s high/low often act as magnet levels. If price is near the previous high when the opening ranges break, you get a confluence zone worth watching.

Trade Management

Combine the two opening-range levels to tier your stops or scale in.

For example, you might place an initial stop below the 15 min low and a wider stop below the 30 min low.

LilSpecCodes1. Killzone Background Highlighting:

It highlights 4 key market sessions:

Killzone Time (EST) Color

Silver Bullet 9:30 AM – 12:00 PM Light Blue

London Killzone 2:00 AM – 5:00 AM Light Green

NY PM Killzone 1:30 PM – 4:00 PM Light Purple

Asia Open 7:00 PM – 11:00 PM Light Red

These are meant to help you focus during high-probability trading times.

__________________________________________________

2. Previous Day High/Low (PDH/PDL):

Plots green line = PDH

Plots red line = PDL

Tracks the current day’s session high/low and sets it as PDH/PDL on a new trading day

CHANGES WITH ETH/RTH

3. Inside Bar Marker:

Plots a small black triangle under bars where the high is lower than the previous bar’s high and the low is higher than the previous bar’s low (inside bars)

Useful for spotting potential breakout or continuation setups

4. Vertical Time Markers (White Dashed Lines)

Time (EST) Label

4:00 AM End of London Silver Bullet

9:30 AM NYSE Open

10:00 AM Start of NY Silver Bullet

11:00 AM End of NY Silver Bullet

11:30 AM (Customizable Input)

3:00 PM PM Killzone Ends

3:15 PM Futures Market Close

7:15 PM Asia Session Watch

Recent Session High Low Marker - SimpleDescription:

This Pine Script marks the high and low points of the most recent trading sessions: Asian, London, and New York.

Asian Session: From 19:00 to 21:00 New York time (UTC-4).

London Session: From 02:00 to 05:00 New York time (UTC-4).

New York Session: From 07:00 to 10:00 New York time (UTC-4).

For each session, the script draws two lines:

One for the high of the session.

One for the low of the session.

The lines are drawn horizontally across the chart, making them easy to spot. Each session is marked by two lines with specific colors:

Orange for the Asian session.

Blue for the London session.

Purple for the New York session.

The lines are dynamically updated during the active session, and they will reset when the next session begins. The width of the lines is set to 2 to ensure they are visible without being too thick.

Credits:

Script created by Jdv.

ORB-HL1. Opening Range Detection

Automatically calculates the high and low of the first 15 minutes after the selected session opens.

Supported sessions:

New York (Futures): 08:30–08:45 EST

New York (Equities): 09:30–09:45 EST

London: 03:00–03:15 GMT

Asia: 19:00–19:15 JST

Plots ORB high/low lines for the rest of the day.

2. Breakout Signals

Highlights the first valid breakout above or below the ORB range on the:

5-minute timeframe

15-minute timeframe

Green arrows = breakout up (long)

Red arrows = breakout down (short)

3. 1-Minute Projection

When a breakout is confirmed on a higher timeframe (5m or 15m), a projection label (e.g., "5m", "15m") appears on the 1-minute chart.

Purple label = 5m breakout

Teal label = 15m breakout

Helps you confirm momentum in real time while on the 1-minute chart.

4. Trailing Stop System

Uses ATR to create an adaptive trailing stop after breakout.

Turns green when price is above stop (bullish), red when below (bearish).

Optional Buy / Sell signal labels appear on crossover events.

5. Session High/Low Visualization

Tracks and displays the previous session’s High and Low for:

Tokyo

London

New York

Lines extend into the current session to act as S/R reference.

Labels like "NY High", "Asia Low" are placed at the end of each line.

6. Alerts

Built-in alerts for:

First 5m or 15m breakout (long/short)

Trailing stop Buy/Sell crossover

7. Customization Options

Turn session H/L lines on/off per session

Customize projection visibility

Adjust ATR period and sensitivity

Set how far each session line extends using bar offsets

Enhanced Volume Trend Indicator with BB SqueezeEnhanced Volume Trend Indicator with BB Squeeze: Comprehensive Explanation

The visualization system allows traders to quickly scan multiple securities to identify high-probability setups without detailed analysis of each chart. The progression from squeeze to breakout, supported by volume trend confirmation, offers a systematic approach to identifying trading opportunities.

The script combines multiple technical analysis approaches into a comprehensive dashboard that helps traders make informed decisions by identifying high-probability setups while filtering out noise through its sophisticated confirmation requirements. It combines multiple technical analysis approaches into an integrated visual system that helps traders identify potential trading opportunities while filtering out false signals.

Core Features

1. Volume Analysis Dashboard

The indicator displays various volume-related metrics in customizable tables:

AVOL (After Hours + Pre-Market Volume): Shows extended hours volume as a percentage of the 21-day average volume with color coding for buying/selling pressure. Green indicates buying pressure and red indicates selling pressure.

Volume Metrics: Includes regular volume (VOL), dollar volume ($VOL), relative volume compared to 21-day average (RVOL), and relative volume compared to 90-day average (RVOL90D).

Pre-Market Data: Optional display of pre-market volume (PVOL), pre-market dollar volume (P$VOL), pre-market relative volume (PRVOL), and pre-market price change percentage (PCHG%).

2. Enhanced Volume Trend (VTR) Analysis

The Volume Trend indicator uses adaptive analysis to evaluate buying and selling pressure, combining multiple factors:

MACD (Moving Average Convergence Divergence) components

Volume-to-SMA (Simple Moving Average) ratio

Price direction and market conditions

Volume change rates and momentum

EMA (Exponential Moving Average) alignment and crossovers

Volatility filtering

VTR Visual Indicators

The VTR score ranges from 0-100, with values above 50 indicating bullish conditions and below 50 indicating bearish conditions. This is visually represented by colored circles:

"●" (Filled Circle):

Green: Strong bullish trend (VTR ≥ 80)

Red: Strong bearish trend (VTR ≤ 20)

"◯" (Hollow Circle):

Green: Moderate bullish trend (VTR 65-79)

Red: Moderate bearish trend (VTR 21-35)

"·" (Small Dot):

Green: Weak bullish trend (VTR 55-64)

Red: Weak bearish trend (VTR 36-45)

"○" (Medium Hollow Circle): Neutral conditions (VTR 46-54), shown in gray

In "Both" display mode, the VTR shows both the numerical score (0-100) alongside the appropriate circle symbol.

Enhanced VTR Settings

The Enhanced Volume Trend component offers several advanced customization options:

Adaptive Volume Analysis (volTrendAdaptive):

When enabled, dynamically adjusts volume thresholds based on recent market volatility

Higher volatility periods require proportionally higher volume to generate significant signals

Helps prevent false signals during highly volatile markets

Keep enabled for most trading conditions, especially in volatile markets

Speed of Change Weight (volTrendSpeedWeight, range 0-1):

Controls emphasis on volume acceleration/deceleration rather than absolute levels

Higher values (0.7-1.0): More responsive to new volume trends, better for momentum trading

Lower values (0.2-0.5): Less responsive, better for trend following

Helps identify early volume trends before they fully develop

Momentum Period (volTrendMomentumPeriod, range 2-10):

Defines lookback period for volume change rate calculations

Lower values (2-3): More responsive to recent changes, better for short timeframes

Higher values (7-10): Smoother, better for daily/weekly charts

Directly affects how quickly the indicator responds to new volume patterns

Volatility Filter (volTrendVolatilityFilter):

Adjusts significance of volume by factoring in current price volatility

High volume during high volatility receives less weight

High volume during low volatility receives more weight

Helps distinguish between genuine volume-driven moves and volatility-driven moves

EMA Alignment Weight (volTrendEmaWeight, range 0-1):

Controls importance of EMA alignments in final VTR calculation

Analyzes multiple EMA relationships (5, 10, 21 period)

Higher values (0.7-1.0): Greater emphasis on trend structure

Lower values (0.2-0.5): More focus on pure volume patterns

Display Mode (volTrendDisplayMode):

"Value": Shows only numerical score (0-100)

"Strength": Shows only symbolic representation

"Both": Shows numerical score and symbol together

3. Bollinger Band Squeeze Detection (SQZ)

The BB Squeeze indicator identifies periods of low volatility when Bollinger Bands contract inside Keltner Channels, often preceding significant price movements.

SQZ Visual Indicators

"●" (Filled Circle): Strong squeeze - high probability setup for an impending breakout

Green: Strong squeeze with bullish bias (likely upward breakout)

Red: Strong squeeze with bearish bias (likely downward breakout)

Orange: Strong squeeze with unclear direction

"◯" (Hollow Circle): Moderate squeeze - medium probability setup

Green: With bullish EMA alignment

Red: With bearish EMA alignment

Orange: Without clear directional bias

"-" (Dash): Gray dash indicates no squeeze condition (normal volatility)

The script identifies squeeze conditions through multiple methods:

Bollinger Bands contracting inside Keltner Channels

BB width falling to bottom 20% of recent range (BB width percentile)

Very narrow Keltner Channel (less than 5% of basis price)

Tracking squeeze duration in consecutive bars

Different squeeze strengths are detected:

Strong Squeeze: BB inside KC with tight BB width and narrow KC

Moderate Squeeze: BB inside KC with either tight BB width or narrow KC

No Squeeze: Normal market conditions

4. Breakout Detection System

The script includes two breakout indicators working in sequence:

4.1 Pre-Breakout (PBK) Indicator

Detects potential upcoming breakouts by analyzing multiple factors:

Squeeze conditions lasting 2-3 bars or more

Significant price ranges

Strong volume confirmation

EMA/MACD crossovers

Consistent price direction

PBK Visual Indicators

"●" (Filled Circle): Detected pre-breakout condition

Green: Likely upward breakout (bullish)

Red: Likely downward breakout (bearish)

Orange: Direction not yet clear, but breakout likely

"-" (Dash): Gray dash indicates no pre-breakout condition

The PBK uses sophisticated conditions to reduce false signals including minimum squeeze length, significant price movement, and technical confirmations.

4.2 Breakout (BK) Indicator

Confirms actual breakouts in progress by identifying:

End of squeeze or strong expansion of Bollinger Bands

Volume expansion

Price moving outside Bollinger Bands

EMA crossovers with volume confirmation

MACD crossovers with significant price range

BK Visual Indicators

"●" (Filled Circle): Confirmed breakout in progress

Green: Upward breakout (bullish)

Red: Downward breakout (bearish)

Orange: Unusual breakout pattern without clear direction

"◆" (Diamond): Special breakout conditions (meets some but not all criteria)

"-" (Dash): Gray dash indicates no breakout detected

The BK indicator uses advanced filters for confirmation:

Requires consecutive breakout signals to reduce false positives

Strong volume confirmation requirements (40% above average)

Significant price movement thresholds

Consistency checks between price action and indicators

5. Market Metrics and Analysis

Price Change Percentage (CHG%)

Displays the current percentage change relative to the previous day's close, color-coded green for positive changes and red for negative changes.

Average Daily Range (ADR%)

Calculates the average daily percentage range over a specified period (default 20 days), helping traders gauge volatility and set appropriate price targets.

Average True Range (ATR)

Shows the Average True Range value, a volatility indicator developed by J. Welles Wilder that measures market volatility by decomposing the entire range of an asset price for that period.

Relative Strength Index (RSI)

Displays the standard 14-period RSI, a momentum oscillator that measures the speed and change of price movements on a scale from 0 to 100.

6. External Market Indicators

QQQ Change

Shows the percentage change in the Invesco QQQ Trust (tracking the Nasdaq-100 Index), useful for understanding broader tech market trends.

UVIX Change

Displays the percentage change in UVIX, a volatility index, providing insight into market fear and potential hedging activity.

BTC-USD

Shows the current Bitcoin price from Coinbase, useful for traders monitoring crypto correlation with equities.

Market Breadth (BRD)

Calculates the percentage difference between ATHI.US and ATLO.US (high vs. low securities), indicating overall market direction and strength.

7. Session Analysis and Volume Direction

Session Detection

The script accurately identifies different market sessions:

Pre-market: 4:00 AM to 9:30 AM

Regular market: 9:30 AM to 4:00 PM

After-hours: 4:00 PM to 8:00 PM

Closed: Outside trading hours

This detection works on any timeframe through careful calculation of current time in seconds.

Buy/Sell Volume Direction

The script analyzes buying and selling pressure by:

Counting up volume when close > open

Counting down volume when close < open

Tracking accumulated volume within the day

Calculating intraday pressure (up volume minus down volume)

Enhanced AVOL Calculation

The improved AVOL calculation works in all timeframes by:

Estimating typical pre-market and after-hours volume percentages

Combining yesterday's after-hours with today's pre-market volume

Calculating this as a percentage of the 21-day average volume

Determining buying/selling pressure by analyzing after-hours and pre-market price changes

Color-coding results: green for buying pressure, red for selling pressure

This calculation is particularly valuable because it works consistently across any timeframe.

Customization Options

Display Settings

The dashboard has two customizable tables: Volume Table and Metrics Table, with positions selectable as bottom_left or bottom_right.

All metrics can be individually toggled on/off:

Pre-market data (PVOL, P$VOL, PRVOL, PCHG%)

Volume data (AVOL, RVOL Day, RVOL 90D, Volume, SEED_YASHALGO_NSE_BREADTH:VOLUME )

Price metrics (ADR%, ATR, RSI, Price Change%)

Market indicators (QQQ, UVIX, Breadth, BTC-USD)

Analysis indicators (Volume Trend, BB Squeeze, Pre-Breakout, Breakout)

These toggle options allow traders to customize the dashboard to show only the metrics they find most valuable for their trading style.

Table and Text Customization

The dashboard's appearance can be customized:

Table background color via tableBgColor

Text color (White or Black) via textColorOption

The indicator uses smart formatting for volume and price values, automatically adding appropriate suffixes (K, M, B) for readability.

MACD Configuration for VTR

The Volume Trend calculation incorporates MACD with customizable parameters:

Fast Length: Controls the period for the fast EMA (default 3)

Slow Length: Controls the period for the slow EMA (default 9)

Signal Length: Controls the period for the signal line EMA (default 5)

MACD Weight: Controls how much influence MACD has on the volume trend score (default 0.3)

These settings allow traders to fine-tune how momentum is factored into the volume trend analysis.

Bollinger Bands and Keltner Channel Settings

The Bollinger Bands and Keltner Channels used for squeeze detection have preset (hidden) parameters:

BB Length: 20 periods

BB Multiplier: 2.0 standard deviations

Keltner Length: 20 periods

Keltner Multiplier: 1.5 ATR

These settings follow standard practice for squeeze detection while maintaining simplicity in the user interface.

Practical Trading Applications

Complete Trading Strategies

1. Squeeze Breakout Strategy

This strategy combines multiple components of the indicator:

Wait for a strong squeeze (SQZ showing ●)

Look for pre-breakout confirmation (PBK showing ● in green or red)

Enter when breakout is confirmed (BK showing ● in same direction)

Use VTR to confirm volume supports the move (VTR ≥ 65 for bullish or ≤ 35 for bearish)

Set profit targets based on ADR (Average Daily Range)

Exit when VTR begins to weaken or changes direction

2. Volume Divergence Strategy

This strategy focuses on the volume trend relative to price:

Identify when price makes a new high but VTR fails to confirm (divergence)

Look for VTR to show weakening trend (● changing to ◯ or ·)

Prepare for potential reversal when SQZ begins to form

Enter counter-trend position when PBK confirms reversal direction

Use external indicators (QQQ, BTC, Breadth) to confirm broader market support

3. Pre-Market Edge Strategy

This strategy leverages pre-market data:

Monitor AVOL for unusual pre-market activity (significantly above 100%)

Check pre-market price change direction (PCHG%)

Enter position at market open if VTR confirms direction

Use SQZ to determine if volatility is likely to expand

Exit based on RVOL declining or price reaching +/- ADR for the day

Market Context Integration

The indicator provides valuable context for trading decisions:

QQQ change shows tech market direction

BTC price shows crypto market correlation

UVIX change indicates volatility expectations

Breadth measurement shows market internals

This context helps traders avoid fighting the broader market and align trades with overall market direction.

Timeframe Optimization

The indicator is designed to work across different timeframes:

For day trading: Focus on AVOL, VTR, PBK/BK, and use shorter momentum periods

For swing trading: Focus on SQZ duration, VTR strength, and broader market indicators

For position trading: Focus on larger VTR trends and use EMA alignment weight

Advanced Analytical Components

Enhanced Volume Trend Score Calculation

The VTR score calculation is sophisticated, with the base score starting at 50 and adjusting for:

Price direction (up/down)

Volume relative to average (high/normal/low)

Volume acceleration/deceleration

Market conditions (bull/bear)

Additional factors are then applied, including:

MACD influence weighted by strength and direction

Volume change rate influence (speed)

Price/volume divergence effects

EMA alignment scores

Volatility adjustments

Breakout strength factors

Price action confirmations

The final score is clamped between 0-100, with values above 50 indicating bullish conditions and below 50 indicating bearish conditions.

Anti-False Signal Filters

The indicator employs multiple techniques to reduce false signals:

Requiring significant price range (minimum percentage movement)

Demanding strong volume confirmation (significantly above average)

Checking for consistent direction across multiple indicators

Requiring prior bar consistency (consecutive bars moving in same direction)

Counting consecutive signals to filter out noise

These filters help eliminate noise and focus on high-probability setups.

MACD Enhancement and Integration

The indicator enhances standard MACD analysis:

Calculating MACD relative strength compared to recent history

Normalizing MACD slope relative to volatility

Detecting MACD acceleration for stronger signals

Integrating MACD crossovers with other confirmation factors

EMA Analysis System

The indicator uses a comprehensive EMA analysis system:

Calculating multiple EMAs (5, 10, 21 periods)

Detecting golden cross (10 EMA crosses above 21 EMA)

Detecting death cross (10 EMA crosses below 21 EMA)

Assessing price position relative to EMAs

Measuring EMA separation percentage

Recent Enhancements and Evolution

Version 5.2 includes several improvements:

Enhanced AVOL to show buying/selling direction through color coding

Improved VTR with adaptive analysis based on market conditions

AVOL display now works in all timeframes through sophisticated estimation

Removed animal symbols and streamlined code with bright colors for better visibility

Improved anti-false signal filters throughout the system

Optimizing Indicator Settings

For Different Market Types

Range-Bound Markets:

Lower EMA Alignment Weight (0.2-0.4)

Higher Speed of Change Weight (0.8-1.0)

Focus on SQZ and PBK signals for breakout potential

Trending Markets:

Higher EMA Alignment Weight (0.7-1.0)

Moderate Speed of Change Weight (0.4-0.6)

Focus on VTR strength and BK confirmations

Volatile Markets:

Enable Volatility Filter

Enable Adaptive Volume Analysis

Lower Momentum Period (2-3)

Focus on strong volume confirmation (VTR ≥ 80 or ≤ 20)

For Different Asset Classes

Equities:

Standard settings work well

Pay attention to AVOL for gap potential

Monitor QQQ correlation

Futures:

Consider higher Volume/RVOL weight

Reduce MACD weight slightly

Pay close attention to SQZ duration

Crypto:

Higher volatility thresholds may be needed

Monitor BTC price for correlation

Focus on stronger confirmation signals

Integrated Visual System for Trading Decisions

The colored circle indicators create an intuitive visual system for quick market assessment:

Progression Sequence: SQZ (Squeeze) → PBK (Pre-Breakout) → BK (Breakout)

This sequence often occurs in order, with the squeeze leading to pre-breakout conditions, followed by an actual breakout.

VTR (Volume Trend): Provides context about the volume supporting these movements.

Color Coding: Green for bullish conditions, red for bearish conditions, and orange/gray for neutral or undefined conditions.

Session Highs and Lows IndicatorSession Highs and Lows Indicator

This indicator automatically tracks and displays the High and Low prices for major trading sessions:

London

New York

Asia

New York Close

For each session, it plots:

A label at the highest and lowest price point reached during the session.

A dashed line showing the high and low levels extended to the right (until the current bar), helping traders visualize key support/resistance zones.

You can toggle visibility for each session individually through the settings panel.

Session times are set in GMT+8, but you can adjust them in the code if needed.

Color code:

London: Blue

New York: Red

Asia: Green

New York Close: Orange

All lines and labels are semi-transparent to avoid chart clutter.

Ideal for intraday and session-based trading strategies.

Timezone Highlight v1.0Features Explained:

Customizable Time Settings:

Easily adjust the opening and closing times for each session to fit your local time zone or trading preferences.

Color-Coded Sessions:

New York : Blue

London : Yellow

Tokyo : Red

Sydney : Green

You can modify the colors or transparency in the script.

Dynamic Highlighting:

Automatically highlights the active trading session based on the current time.

This Pine Script is user-friendly and designed to provide immediate visual insights into global market activity. Let me know if you need further enhancements!

Its my first script so please don't be too strict!

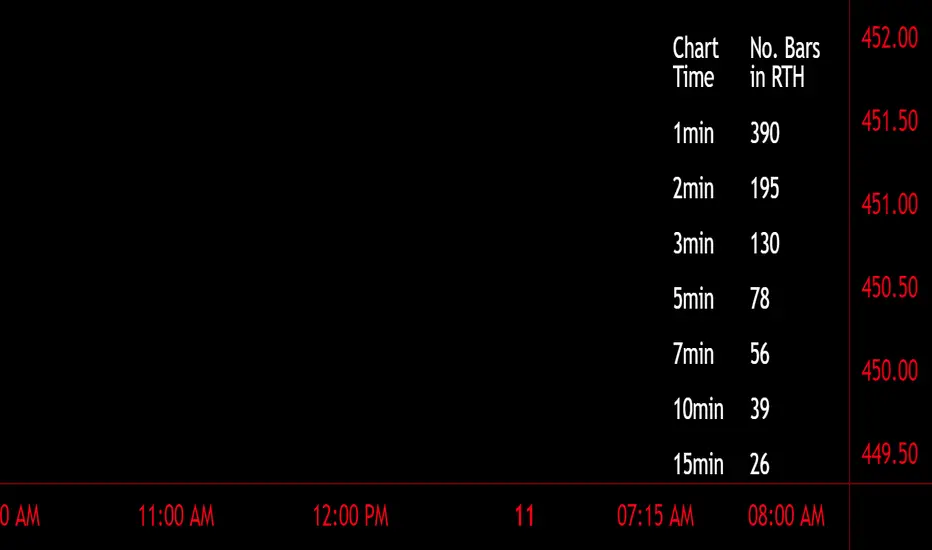

Number of Bars CheatSheetA regular trading day on the New York Stock Exchange (NYSE) consists of two main sessions: the Opening Auction and the Closing Auction, separated by a continuous trading session. Here's a breakdown of the trading day:

1. **Pre-Opening Session**: This session starts at 4:00 AM Eastern Time (ET) and lasts until 9:30 AM ET. During this time, there is limited trading activity, and orders can be entered and canceled. However, most of the trading activity doesn't occur until the regular trading session begins.

2. **Regular Trading Session**: The regular trading session on the NYSE starts at 9:30 AM ET and lasts until 4:00 PM ET. This is the primary trading session where the majority of price bars are formed.

3. **Closing Auction**: After the regular trading session ends at 4:00 PM ET, there is a closing auction period that typically lasts until 4:10 PM ET. During this time, there is a final price discovery process where orders are matched to determine the closing price for each security.

So, during the regular trading session, which is the main focus for most traders and investors, there are a total of 6.5 hours of trading. Trading occurs continuously during this time, with price bars being formed based on the time frame you're looking at. The most common time frames for price bars are one minute, five minutes, 15 minutes, 30 minutes, and one hour, among others. Therefore, the number of price bars in a regular trading day on the NYSE will depend on the time frame you are using for your analysis. For example, if you are using one-minute bars, there will be 6.5 x 60 = 390 price bars in a regular trading day.

Default Strategy Inputs (Forex / Crypto)The code in this post contains a set of default strategy inputs I use in new projects / backtests in Tradingview.

Full code commentary is available on the Backtest-Rookies website. To comply with house rules, I cannot post the direct link here.

Features

Trade Direction: So that you can limit the strategy for long only, short only or trade in both directions. It is important to note that when you select “Long Only”, you will still see Short signals on the chart. However, they are only used to close a position rather than reverse it. This is the default behaviour for strategies. The same applies to “Short Only”.

Date Ranges: So that you can isolate backtesting to specific periods of interest such as bull or bear markets.

Sessions: So you can easily get an idea of the expected results during your own session. You may also notice that performance of the strategy varies depending on which session it is deployed in.

Some example stop losses: It is not an exhaustive list but it should be enough to provide some inspiration for different types of stops that you can experiment with.

Happy Scripting. I hope the community finds it useful.

AlphaTrend++ offset labelsAlphaTrend++

Overview

The AlphaTrend++ is an advanced Pine Script indicator designed to help traders identify buy and sell opportunities in trending and volatile markets. Building on trend-following principles, it uses a modified Average True Range (ATR) calculation combined with volume or momentum data to plot a dynamic trend line. The indicator overlays on the price chart, displaying a colored trend line, a filled trend zone, buy/sell signals, and optional stop-loss tick labels, making it ideal for day trading or swing trading, particularly in markets like futures (e.g., MES).

What It Does

This indicator generates buy and sell signals based on the direction and momentum of a custom trend line, filtered by optional time restrictions and signal frequency logic. The trend line adapts to price action and volatility, with a filled zone highlighting trend strength. Buy/sell signals are plotted as labels, and stop-loss distances are displayed in ticks (customizable for instruments like MES). The indicator supports standard chart types for realistic signal generation.

How It Works

The indicator employs the following components:

Trend Line Calculation: A dynamic trend line is calculated using ATR adjusted by a user-defined multiplier, combined with either Money Flow Index (MFI) or Relative Strength Index (RSI) depending on volume availability. The line tracks price movements, adjusting upward or downward based on trend direction and volatility.

Trend Zone: The area between the current trend line and its value two bars prior is filled, colored green for bullish trends (upward movement) or red for bearish trends (downward movement), providing a visual cue of trend strength.

Signal Generation: Buy signals occur when the trend line crosses above its value two bars ago, and sell signals occur when it crosses below, with optional filtering to reduce signal noise (based on bar timing logic). Signals can be restricted to a 9:00–15:00 UTC trading window.

Stop-Loss Ticks: For each signal, the indicator calculates the distance to the trend line (acting as a stop-loss level) in ticks, using a user-defined tick size (default 0.25 for MES). These are displayed as labels below/above the signal.

Time Filter: An optional filter limits signals to 9:00–15:00 UTC, aligning with active trading sessions like the US market open.

The indicator ensures compatibility with standard chart types (e.g., candlestick or bar charts) to avoid unrealistic results associated with non-standard types like Heikin Ashi or Renko.

How to Use It

Add to Chart: Apply the indicator to a candlestick or bar chart on TradingView.

Configure Settings:

Multiplier: Adjust the ATR multiplier (default 1.0) to control trend line sensitivity. Higher values widen the stop-loss distance.

Common Period: Set the ATR and MFI/RSI period (default 14) for trend calculations.

No Volume Data: Enable if volume data is unavailable (e.g., for certain forex pairs), switching from MFI to RSI.

Tick Size: Set the tick size for stop-loss calculations (default 0.25 for MES futures).

Show Buy/Sell Signals: Toggle signal labels (default enabled).

Show Stop Loss Ticks: Toggle stop-loss tick labels (default enabled).

Use Time Filter: Restrict signals to 9:00–15:00 UTC (default disabled).

Use Filtered Signals: Enable to reduce signal frequency using bar timing logic (default enabled).

Interpret Signals:

Buy Signal: A blue “BUY” label below the bar indicates a potential long entry (trend line crossover, passing filters).

Sell Signal: A red “SELL” label above the bar indicates a potential short entry (trend line crossunder, passing filters).

Trend Zone: Green fill suggests bullish momentum; red fill suggests bearish momentum.

Stop-Loss Ticks: Gray labels show the stop-loss distance in ticks, helping with risk management.

Monitor Context: Use the trend line and filled zone to confirm the market’s direction before acting on signals.

Unique Features

Adaptive Trend Line: Combines ATR with MFI or RSI to create a responsive trend line that adjusts to volatility and market conditions.

Tick-Based Stop-Loss: Displays stop-loss distances in ticks, customizable for specific instruments, aiding precise risk management.

Signal Filtering: Optional bar timing logic reduces false signals, improving reliability in choppy markets.

Trend Zone Visualization: The filled zone between trend line values enhances trend clarity, making it easier to assess momentum.

Time-Restricted Trading: Optional 9:00–15:00 UTC filter aligns signals with high-liquidity sessions.

Notes

Use on standard candlestick or bar charts to ensure accurate signals.

Test the indicator on a demo account to optimize settings for your market and timeframe.

Combine with other analysis (e.g., support/resistance, volume spikes) for better decision-making.

The indicator is not a standalone system; use it as part of a broader trading strategy.

Limitations

Signals may lag in highly volatile or low-liquidity markets due to ATR-based calculations.

The 9:00–15:00 UTC time filter may not suit all markets; disable it for 24-hour assets like forex or crypto.

Stop-loss tick calculations assume consistent tick sizes; verify compatibility with your instrument.

This indicator is designed for traders seeking a robust, trend-following tool with customizable risk management and signal filtering, optimized for active trading sessions.

This update enhances label customization, clarity, and signal usability while preserving all existing AlphaTrend++ logic. The goal is to improve readability during live trading and allow traders to personalize the visual footprint of entries and stop-loss levels.

Improvements

• Cleaner Label Placement

Labels now maintain consistent spacing from the candle, regardless of volatility or ATR expansion.

• Enhanced Visual Structure

BUY/SELL signals remain bold and clear, while SL ticks use a more compact and optional sizing scheme.

• Better User Control

New UI inputs:

Entry Label Size

SL Label Size

SL Label Offset (Ticks)nces.

Hash Momentum Strategy# Hash Momentum Strategy

## 📊 Overview

The **Hash Momentum Strategy** is a professional-grade momentum trading system designed to capture strong directional price movements with precision timing and intelligent risk management. Unlike traditional EMA crossover strategies, this system uses momentum acceleration as its primary signal, resulting in earlier entries and better risk-to-reward ratios.

---

## ⚡ What Makes This Strategy Unique

### 1. Momentum-Based Entry System

Most strategies rely on lagging indicators like moving average crossovers. This strategy captures momentum *acceleration* - entering when price movement is gaining strength, not after the move has already happened.

### 2. Programmable Risk-to-Reward

Set your exact R:R ratio (1:2, 1:2.5, 1:3, etc.) and the strategy automatically calculates stop loss and take profit levels. No more guessing or manual calculations.

### 3. Smart Partial Profit Taking

Lock in profits at multiple stages:

- **First TP**: Take 50% off at 2R

- **Second TP**: Take 40% off at 2.5R

- **Final TP**: Let 10% ride to maximum target

This approach locks in gains while letting winners run.

### 4. Dynamic Momentum Threshold

Uses ATR (Average True Range) multiplied by your threshold setting to adapt to market volatility. Volatile markets = higher threshold. Quiet markets = lower threshold.

### 5. Trade Cooldown System

Prevents overtrading and revenge trading by enforcing a cooldown period between trades. Configurable from 1-24 bars.

### 6. Optional Session & Weekend Filters

Filter trades by Tokyo, London, and New York sessions. Optional weekend-off toggle to avoid low-liquidity periods.

---

## 🎯 How It Works

### Signal Generation

**STEP 1: Calculate Momentum**

- Momentum = Current Price - Price

- Check if Momentum > ATR × Threshold Multiplier

- Momentum must be accelerating (positive change in momentum)

**STEP 2: Confirm with EMA Trend Filter**

- Long: Price must be above EMA

- Short: Price must be below EMA

**STEP 3: Check Filters**

- Not in cooldown period

- Valid session (if enabled)

- Not weekend (if enabled)

**STEP 4: ENTRY SIGNAL TRIGGERED**

### Risk Management Example

**Example Long Trade:**

- Entry: $100

- Stop Loss: $97.80 (2.2% risk)

- Risk Amount: $2.20

**Take Profit Levels:**

- TP1: $104.40 (2R = $4.40) → Close 50%

- TP2: $105.50 (2.5R = $5.50) → Close 40%

- Final: $105.50 (2.5R) → Close remaining 10%

---

## ⚙️ Settings Guide

### Core Strategy

**Momentum Length** (Default: 13)

Number of bars for momentum calculation. Higher = stronger but fewer signals.

**Momentum Threshold** (Default: 2.25)

ATR multiplier. Higher = only trade biggest moves.

**Use EMA Trend Filter** (Default: ON)

Only long above EMA, short below EMA.

**EMA Length** (Default: 28)

Period for trend-confirming EMA.

### Filters

**Use Trading Session Filter** (Default: OFF)

Restrict trading to specific sessions.

**Tokyo Session** (Default: OFF)

Trade during Asian hours (00:00-09:00 JST).

**London Session** (Default: OFF)

Trade during European hours (08:00-17:00 GMT).

**New York Session** (Default: OFF)

Trade during US hours (08:00-17:00 EST).

**Weekend Off** (Default: OFF)

Disable trading on Saturdays and Sundays.

### Risk Management

**Stop Loss %** (Default: 2.2)

Fixed percentage stop loss from entry.

**Risk:Reward Ratio** (Default: 2.5)

Your target reward as multiple of risk.

**Use Partial Profit Taking** (Default: ON)

Take profits in stages.

**First TP R:R** (Default: 2.0)

First target as multiple of risk.

**First TP Size %** (Default: 50)

Percentage of position to close at TP1.

**Second TP R:R** (Default: 2.5)

Second target as multiple of risk.

**Second TP Size %** (Default: 40)

Percentage of position to close at TP2.

### Trade Management

**Use Trade Cooldown** (Default: ON)

Prevent overtrading.

**Cooldown Bars** (Default: 6)

Bars to wait after closing a trade.

---

## 🎨 Visual Elements

### Chart Indicators

🟢 **Green Dot** (below bar) = Long entry signal

🔴 **Red Dot** (above bar) = Short entry signal

🔵 **Blue X** (above bar) = Long position closed

🟠 **Orange X** (below bar) = Short position closed

**EMA Line** = Trend direction (green when bullish, red when bearish)

**White Line** = Entry price

**Red Line** = Stop loss level

**Green Lines** = Take profit levels (TP1, TP2, Final)

### Dashboard

When not in real-time mode, a dashboard displays:

- Current position (LONG/SHORT/FLAT)

- Entry price

- Stop loss price

- Take profit price

- R:R ratio

- Current momentum strength

- Total trades

- Win rate

- Net profit %

---

## 📈 Recommended Settings by Timeframe

### 1-Hour Timeframe (Default)

- Momentum Length: 13

- Momentum Threshold: 2.25

- EMA Length: 28

- Stop Loss: 2.2%

- R:R Ratio: 2.5

- Cooldown: 6 bars

### 4-Hour Timeframe

- Momentum Length: 24-36

- Momentum Threshold: 2.5

- EMA Length: 50

- Stop Loss: 3-4%

- R:R Ratio: 2.0-2.5

- Cooldown: 6-8 bars

### 15-Minute Timeframe

- Momentum Length: 8-10

- Momentum Threshold: 2.0

- EMA Length: 20

- Stop Loss: 1.5-2%

- R:R Ratio: 2.0

- Cooldown: 4-6 bars

---

## 🔧 Optimization Tips

### Want More Trades?

- Decrease Momentum Threshold (2.0 instead of 2.25)

- Decrease Momentum Length (10 instead of 13)

- Decrease Cooldown Bars (4 instead of 6)

### Want Higher Quality Trades?

- Increase Momentum Threshold (2.5-3.0)

- Increase Momentum Length (18-24)

- Increase Cooldown Bars (8-10)

### Want Lower Drawdown?

- Increase Cooldown Bars

- Use tighter stop loss