FVG 9:31–10:00 AM ETFVG 9:31–10:00 AM ET - Script Description

What This Script Does

This indicator finds **Fair Value Gaps (FVGs)** that form during the first 29 minutes of the U.S. stock market (9:31 AM to 10:00 AM Eastern Time). A Fair Value Gap is a price imbalance where there's a gap between candles that often becomes an important support or resistance level.

Key Features:

- **Time Window**: Only looks for FVGs between 9:31-10:00 AM ET (most important opening period)

- **One Per Day**: Finds only the first FVG that forms in this time window each day

- **Visual Display**: Draws a purple box around the gap with a clear "FVG" label

- **Price Tracking**: Monitors when price comes back to test the gap level

- **Alert System**: Sends notifications when price returns to the FVG zone

How FVGs Are Detected:

- **Bullish FVG**: When there's a gap up (low of middle candle is above high of 3rd candle back)

- **Bearish FVG**: When there's a gap down (high of middle candle is below low of 3rd candle back)

The 9:31-10:00 AM window is chosen because this is when institutions and algorithms create their biggest price moves right after market open, making these gaps very reliable.

Customization Options

User Settings

Extend FVG Box (Bars)

- **What it does**: Makes the purple box longer to the right

- **Default**: 0 (box ends right after the gap forms)

- **Options**: Any number from 0 to 100+

- **When to use**:

- Keep at 0 for clean historical view

- Set to 10-20 to track the gap during the current session

- Set higher for longer reference

Code Settings (Can Be Changed)

Time Window

- **Start**: 9:31 AM Eastern Time

- **End**: 10:00 AM Eastern Time

- **Can modify**: Change the hour/minute numbers in the code

Visual Style

- **Color**: Purple with see-through background

- **Label**: Shows "FVG" text in white

- **Can modify**: Change colors and transparency in the code

How to Use:

Setup

Chart Settings

1. Use 1-minute, 5-minute, or 15-minute charts (works best on these timeframes)

2. Apply to liquid markets like ES, NQ, major stocks, or forex pairs

3. Set the "Extend FVG Box" to your preference (start with 0 or 10)

What You'll See

- A purple box appears when an FVG forms during 9:31-10:00 AM

- Box shows the exact price levels of the gap

- "FVG" label appears on the box

- Only one FVG per day will be marked

Trading Strategies

Basic FVG Trading

1. **Wait for Formation**: Let the purple box appear during 9:31-10:00 AM

2. **Watch Price Movement**: See if price moves away from the gap

3. **Enter on Retest**: When price comes back to the purple box area, consider entering

4. **Trade Direction**:

- Bullish FVG = look for long opportunities when price retests

- Bearish FVG = look for short opportunities when price retests

Entry Methods

- **Bounce Play**: Enter when price touches the FVG box and bounces away

- **Break Play**: Enter if price strongly breaks through the FVG box

- **Rejection Play**: Enter opposite direction if price gets rejected at the FVG

Risk Management

Stop Losses

- Place stops just outside the FVG box (a few ticks beyond the gap)

- If trading a bounce, stop goes on opposite side of the gap

- If trading a break, stop goes back inside the gap

Position Sizing

- Start small until you understand how FVGs work in your market

- Bigger gaps = smaller position size (more risk)

- Smaller gaps = can use larger position size

Profit Targets

- Take profits at obvious levels like round numbers, previous highs/lows

- Consider taking half profits at 1:1 risk/reward ratio

- Let some position run if the move is strong

Best Practices

When It Works Best

- High-volume stocks and futures (ES, NQ work great)

- Normal market days without major news during the 9:31-10:00 window

- When there's clear institutional activity in the opening period

When to Be Careful

- Low-volume stocks or markets

- Major economic news releases during the time window

- Market holidays when volume is low

- Very choppy or sideways days

Alert Usage

- The script will alert you when price comes back to test the FVG

- Don't trade the alert blindly - always check the current market situation

- Use the alert as a heads-up to start watching the setup more closely

Tips for Success

- The earlier the FVG forms in the 9:31-10:00 window, often the more significant it is

- FVGs that form with high volume are usually more reliable

- Always consider the overall market direction - don't fight the main trend

- Practice on paper first to understand how FVGs behave in your chosen market

🔗 Works Best With:

✅ Liquidity Levels — Smart Swing Lows: Spot key structural lows that can fuel stop hunts and reversals.

✅ ICT Turtle Soup — Liquidity Reversal: Add a classic reversal pattern to your toolkit to catch fakeouts cleanly.

✅ ICT SMC Liquidity Grabs and OBs- Liquidity Grabs, Order Block Zones, and Fibonacci OTE Levels, allowing traders to identify institutional entry models with clean, rule-based visual signals.

This script is most valuable for day traders who want to catch institutional moves right after market open, but it can also help swing traders identify important intraday levels.

✅ ICT Macro Zones (Grey Box Version)- It tracks real-time highs and lows for each Silver Bullet session.

✅ Weekly Opening Gap (cryptonnnite)

Search in scripts for "track"

Neuracap Gap AnalysisThe Neuracap Gap Analysis indicator is a comprehensive tool designed to identify and track price gaps, special candlestick patterns, and high-volume breakout signals. It combines multiple trading strategies into one powerful indicator for gap trading, pattern recognition, and momentum analysis.

🎯 What This Indicator Does

1. Gap Detection & Tracking

Automatically identifies price gaps (up and down)

Tracks gap fills with visual boxes that extend until closed

Manages gap history with customizable limits

Color-coded visualization (Green = Gap Up, Red = Gap Down)

2. Upside Tasuki Gap Pattern

Identifies the bullish continuation pattern

Colors candles yellow when pattern is detected

Confirms trend continuation signals

3. Episodic Pivot Detection

High-volume breakout identification

EMA filter ensures signals only in uptrends

Strong momentum confirmation

Fuchsia-colored candles with arrow markers

🔍 How to Use for Trading

📈 Gap Trading Strategy

Gap Up Trading:

Wait for gap up (green box appears)

Check volume - Higher volume = stronger signal

Entry options:

Aggressive: Enter at market open

Conservative: Wait for pullback to gap level

Stop loss: Below the gap fill level

Target: Previous resistance or 2:1 risk/reward

Gap Down Trading:

Identify gap down (red box appears)

Look for bounce opportunities

Entry: When price shows reversal signs

Stop: Below recent lows

Target: Gap fill level

💫 Tasuki Gap Strategy

Yellow candle indicates bullish continuation

Confirms uptrend is likely to continue

Entry: On next candle after pattern

Stop: Below the gap low

Target: Next resistance level

🚀 Episodic Pivot Strategy

Fuchsia candle + arrow = High probability breakout

All conditions met:

Price above EMA 20, 50, 200

High volume (2x+ average)

Strong price move (4%+)

Entry: At close or next open

Stop: Below EMA 20 or recent swing low

Target: Measured move or next resistance

📊 Reading the Visual Signals

Gap Boxes

🟢 Green Box: Gap up - potential bullish continuation

🔴 Red Box: Gap down - potential bounce or bearish continuation

Box extends until gap is filled

Box disappears when gap closes

Candle Colors

🟡 Yellow: Tasuki gap pattern (bullish continuation)

🟪 Fuchsia: Episodic pivot (high-volume breakout)

⬜ Normal: No special pattern detected

Arrows & Markers

⬆️ Triangle Arrow: Episodic pivot confirmation

💡 Trading Tips & Best Practices

✅ Do's

Combine with trend analysis - Trade gaps in direction of trend

Check volume - Higher volume = more reliable signals

Use multiple timeframes - Confirm on higher timeframes

Risk management - Always set stop losses

Wait for confirmation - Don't chase, let signals develop

❌ Don'ts

Don't trade all gaps - Focus on high-quality setups

Avoid low volume - Weak volume = unreliable signals

Don't ignore trend - Counter-trend trading is risky

Don't overtrade - Quality over quantity

Don't ignore context - Consider market conditions

⚠️ Risk Management

Position sizing: Risk 1-2% per trade

Stop losses: Always define before entry

Target levels: Set realistic profit targets

Market conditions: Avoid trading in choppy markets

📈 Performance Optimization

For Conservative Traders:

Increase minimum gap size to 1%

Set volume multiplier to 3.0x

Only trade episodic pivots in strong uptrends

Wait for gap fill confirmation

For Aggressive Traders:

Decrease minimum gap size to 0.3%

Set volume multiplier to 1.5x

Trade both gap types

Enter on pattern confirmation

🚨 Alert Setup

The indicator provides alerts for:

Gap Up Detected

Gap Down Detected

Upside Tasuki Gap

Episodic Pivot

Recommended: Enable all alerts and filter manually based on your strategy.

📝 Summary

This indicator excels at identifying high-probability trading opportunities through gap analysis, pattern recognition, and momentum confirmation. Use it as part of a complete trading system with proper risk management for best results.

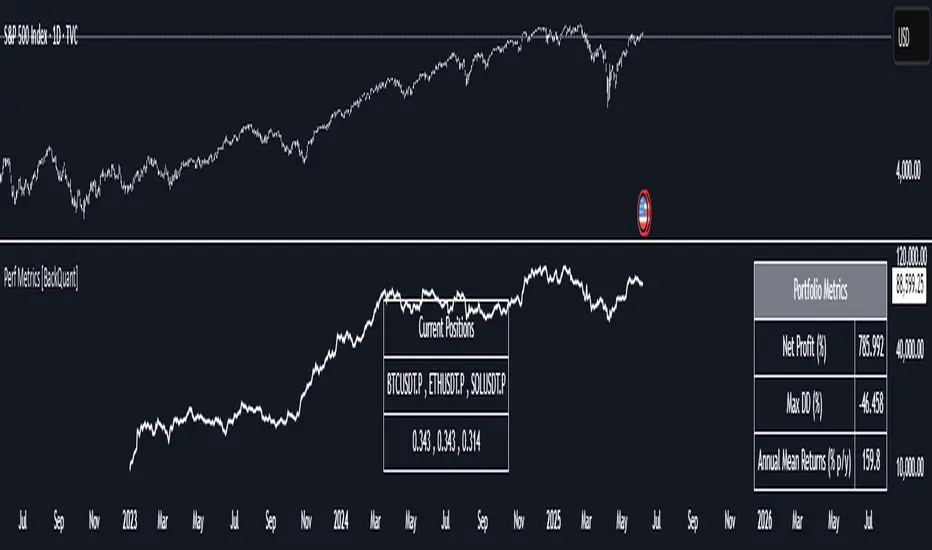

Performance Metrics With Bracketed Rebalacing [BackQuant]Performance Metrics With Bracketed Rebalancing

The Performance Metrics With Bracketed Rebalancing script offers a robust method for assessing portfolio performance, integrating advanced portfolio metrics with different rebalancing strategies. With a focus on adaptability, the script allows traders to monitor and adjust portfolio weights, equity, and other key financial metrics dynamically. This script provides a versatile approach for evaluating different trading strategies, considering factors like risk-adjusted returns, volatility, and the impact of portfolio rebalancing.

Please take the time to read the following:

Key Features and Benefits of Portfolio Methods

Bracketed Rebalancing:

Bracketed Rebalancing is an advanced strategy designed to trigger portfolio adjustments when an asset's weight surpasses a predefined threshold. This approach minimizes overexposure to any single asset while maintaining flexibility in response to market changes. The strategy is particularly beneficial for mitigating risks that arise from significant asset weight fluctuations. The following image illustrates how this method reacts when asset weights cross the threshold:

Daily Rebalancing:

Unlike the bracketed method, Daily Rebalancing adjusts portfolio weights every trading day, ensuring consistent asset allocation. This method aims for a more even distribution of portfolio weights, making it a suitable option for traders who prefer less sensitivity to individual asset volatility. Here's an example of Daily Rebalancing in action:

No Rebalancing:

For traders who prefer a passive approach, the "No Rebalancing" option allows the portfolio to remain static, without any adjustments to asset weights. This method may appeal to long-term investors or those who believe in the inherent stability of their selected assets. Here’s how the portfolio looks when no rebalancing is applied:

Portfolio Weights Visualization:

One of the standout features of this script is the visual representation of portfolio weights. With adjustable settings, users can track the current allocation of assets in real-time, making it easier to analyze shifts and trends. The following image shows the real-time weight distribution across three assets:

Rolling Drawdown Plot:

Managing drawdown risk is a critical aspect of portfolio management. The Rolling Drawdown Plot visually tracks the drawdown over time, helping traders monitor the risk exposure and performance relative to the peak equity levels. This feature is essential for assessing the portfolio's resilience during market downturns:

Daily Portfolio Returns:

Tracking daily returns is crucial for evaluating the short-term performance of the portfolio. The script allows users to plot daily portfolio returns to gain insights into daily profit or loss, helping traders stay updated on their portfolio’s progress:

Performance Metrics

Net Profit (%):

This metric represents the total return on investment as a percentage of the initial capital. A positive net profit indicates that the portfolio has gained value over the evaluation period, while a negative value suggests a loss. It's a fundamental indicator of overall portfolio performance.

Maximum Drawdown (Max DD):

Maximum Drawdown measures the largest peak-to-trough decline in portfolio value during a specified period. It quantifies the most significant loss an investor would have experienced if they had invested at the highest point and sold at the lowest point within the timeframe. A smaller Max DD indicates better risk management and less exposure to significant losses.

Annual Mean Returns (% p/y):

This metric calculates the average annual return of the portfolio over the evaluation period. It provides insight into the portfolio's ability to generate returns on an annual basis, aiding in performance comparison with other investment opportunities.

Annual Standard Deviation of Returns (% p/y):

This measure indicates the volatility of the portfolio's returns on an annual basis. A higher standard deviation signifies greater variability in returns, implying higher risk, while a lower value suggests more stable returns.

Variance:

Variance is the square of the standard deviation and provides a measure of the dispersion of returns. It helps in understanding the degree of risk associated with the portfolio's returns.

Sortino Ratio:

The Sortino Ratio is a variation of the Sharpe Ratio that only considers downside risk, focusing on negative volatility. It is calculated as the difference between the portfolio's return and the minimum acceptable return (MAR), divided by the downside deviation. A higher Sortino Ratio indicates better risk-adjusted performance, emphasizing the importance of avoiding negative returns.

Sharpe Ratio:

The Sharpe Ratio measures the portfolio's excess return per unit of total risk, as represented by standard deviation. It is calculated by subtracting the risk-free rate from the portfolio's return and dividing by the standard deviation of the portfolio's excess return. A higher Sharpe Ratio indicates more favorable risk-adjusted returns.

Omega Ratio:

The Omega Ratio evaluates the probability of achieving returns above a certain threshold relative to the probability of experiencing returns below that threshold. It is calculated by dividing the cumulative probability of positive returns by the cumulative probability of negative returns. An Omega Ratio greater than 1 indicates a higher likelihood of achieving favorable returns.

Gain-to-Pain Ratio:

The Gain-to-Pain Ratio measures the return per unit of risk, focusing on the magnitude of gains relative to the severity of losses. It is calculated by dividing the total gains by the total losses experienced during the evaluation period. A higher ratio suggests a more favorable balance between reward and risk.

www.linkedin.com

Compound Annual Growth Rate (CAGR) (% p/y):

CAGR represents the mean annual growth rate of the portfolio over a specified period, assuming the investment has been compounding over that time. It provides a smoothed annual rate of growth, eliminating the effects of volatility and offering a clearer picture of long-term performance.

Portfolio Alpha (% p/y):

Portfolio Alpha measures the portfolio's performance relative to a benchmark index, adjusting for risk. It is calculated using the Capital Asset Pricing Model (CAPM) and represents the excess return of the portfolio over the expected return based on its beta and the benchmark's performance. A positive alpha indicates outperformance, while a negative alpha suggests underperformance.

Portfolio Beta:

Portfolio Beta assesses the portfolio's sensitivity to market movements, indicating its exposure to systematic risk. A beta greater than 1 suggests the portfolio is more volatile than the market, while a beta less than 1 indicates lower volatility. Beta is used to understand the portfolio's potential for gains or losses in relation to market fluctuations.

Skewness of Returns:

Skewness measures the asymmetry of the return distribution. A positive skew indicates a distribution with a long right tail, suggesting more frequent small losses and fewer large gains. A negative skew indicates a long left tail, implying more frequent small gains and fewer large losses. Understanding skewness helps in assessing the likelihood of extreme outcomes.

Value at Risk (VaR) 95th Percentile:

VaR at the 95th percentile estimates the maximum potential loss over a specified period, given a 95% confidence level. It provides a threshold value such that there is a 95% probability that the portfolio will not experience a loss greater than this amount.

Conditional Value at Risk (CVaR):

CVaR, also known as Expected Shortfall, measures the average loss exceeding the VaR threshold. It provides insight into the tail risk of the portfolio, indicating the expected loss in the worst-case scenarios beyond the VaR level.

These metrics collectively offer a comprehensive view of the portfolio's performance, risk exposure, and efficiency. By analyzing these indicators, investors can make informed decisions, balancing potential returns with acceptable levels of risk.

Conclusion

The Performance Metrics With Bracketed Rebalancing script provides a comprehensive framework for evaluating and optimizing portfolio performance. By integrating advanced metrics, adaptive rebalancing strategies, and visual analytics, it empowers traders to make informed decisions in managing their investment portfolios. However, it's crucial to consider the implications of rebalancing strategies, as academic research indicates that predictable rebalancing can lead to market impact costs. Therefore, adopting flexible and less predictable rebalancing approaches may enhance portfolio performance and reduce associated costs.

Ergodic Market Divergence (EMD)Ergodic Market Divergence (EMD)

Bridging Statistical Physics and Market Dynamics Through Ensemble Analysis

The Revolutionary Concept: When Physics Meets Trading

After months of research into ergodic theory—a fundamental principle in statistical mechanics—I've developed a trading system that identifies when markets transition between predictable and unpredictable states. This indicator doesn't just follow price; it analyzes whether current market behavior will persist or revert, giving traders a scientific edge in timing entries and exits.

The Core Innovation: Ergodic Theory Applied to Markets

What Makes Markets Ergodic or Non-Ergodic?

In statistical physics, ergodicity determines whether a system's future resembles its past. Applied to trading:

Ergodic Markets (Mean-Reverting)

- Time averages equal ensemble averages

- Historical patterns repeat reliably

- Price oscillates around equilibrium

- Traditional indicators work well

Non-Ergodic Markets (Trending)

- Path dependency dominates

- History doesn't predict future

- Price creates new equilibrium levels

- Momentum strategies excel

The Mathematical Framework

The Ergodic Score combines three critical divergences:

Ergodic Score = (Price Divergence × Market Stress + Return Divergence × 1000 + Volatility Divergence × 50) / 3

Where:

Price Divergence: How far current price deviates from market consensus

Return Divergence: Momentum differential between instrument and market

Volatility Divergence: Volatility regime misalignment

Market Stress: Adaptive multiplier based on current conditions

The Ensemble Analysis Revolution

Beyond Single-Instrument Analysis

Traditional indicators analyze one chart in isolation. EMD monitors multiple correlated markets simultaneously (SPY, QQQ, IWM, DIA) to detect systemic regime changes. This ensemble approach:

Reveals Hidden Divergences: Individual stocks may diverge from market consensus before major moves

Filters False Signals: Requires broader market confirmation

Identifies Regime Shifts: Detects when entire market structure changes

Provides Context: Shows if moves are isolated or systemic

Dynamic Threshold Adaptation

Unlike fixed-threshold systems, EMD's boundaries evolve with market conditions:

Base Threshold = SMA(Ergodic Score, Lookback × 3)

Adaptive Component = StDev(Ergodic Score, Lookback × 2) × Sensitivity

Final Threshold = Smoothed(Base + Adaptive)

This creates context-aware signals that remain effective across different market environments.

The Confidence Engine: Know Your Signal Quality

Multi-Factor Confidence Scoring

Every signal receives a confidence score based on:

Signal Clarity (0-35%): How decisively the ergodic threshold is crossed

Momentum Strength (0-25%): Rate of ergodic change

Volatility Alignment (0-20%): Whether volatility supports the signal

Market Quality (0-20%): Price convergence and path dependency factors

Real-Time Confidence Updates

The Live Confidence metric continuously updates, showing:

- Current opportunity quality

- Market state clarity

- Historical performance influence

- Signal recency boost

- Visual Intelligence System

Adaptive Ergodic Field Bands

Dynamic bands that expand and contract based on market state:

Primary Color: Ergodic state (mean-reverting)

Danger Color: Non-ergodic state (trending)

Band Width: Expected price movement range

Squeeze Indicators: Volatility compression warnings

Quantum Wave Ribbons

Triple EMA system (8, 21, 55) revealing market flow:

Compressed Ribbons: Consolidation imminent

Expanding Ribbons: Directional move developing

Color Coding: Matches current ergodic state

Phase Transition Signals

Clear entry/exit markers at regime changes:

Bull Signals: Ergodic restoration (mean reversion opportunity)

Bear Signals: Ergodic break (trend following opportunity)

Confidence Labels: Percentage showing signal quality

Visual Intensity: Stronger signals = deeper colors

Professional Dashboard Suite

Main Analytics Panel (Top Right)

Market State Monitor

- Current regime (Ergodic/Non-Ergodic)

- Ergodic score with threshold

- Path dependency strength

- Quantum coherence percentage

Divergence Metrics

- Price divergence with severity

- Volatility regime classification

- Strategy mode recommendation

- Signal strength indicator

Live Intelligence

- Real-time confidence score

- Color-coded risk levels

- Dynamic strategy suggestions

Performance Tracking (Left Panel)

Signal Analytics

- Total historical signals

- Win rate with W/L breakdown

- Current streak tracking

- Closed trade counter

Regime Analysis

- Current market behavior

- Bars since last signal

- Recommended actions

- Average confidence trends

Strategy Command Center (Bottom Right)

Adaptive Recommendations

- Active strategy mode

- Primary approach (mean reversion/momentum)

- Suggested indicators ("weapons")

- Entry/exit methodology

- Risk management guidance

- Comprehensive Input Guide

Core Algorithm Parameters

Analysis Period (10-100 bars)

Scalping (10-15): Ultra-responsive, more signals, higher noise

Day Trading (20-30): Balanced sensitivity and stability

Swing Trading (40-100): Smooth signals, major moves only Default: 20 - optimal for most timeframes

Divergence Threshold (0.5-5.0)

Hair Trigger (0.5-1.0): Catches every wiggle, many false signals

Balanced (1.5-2.5): Good signal-to-noise ratio

Conservative (3.0-5.0): Only extreme divergences Default: 1.5 - best risk/reward balance

Path Memory (20-200 bars)

Short Memory (20-50): Recent behavior focus, quick adaptation

Medium Memory (50-100): Balanced historical context

Long Memory (100-200): Emphasizes established patterns Default: 50 - captures sufficient history without lag

Signal Spacing (5-50 bars)

Aggressive (5-10): Allows rapid-fire signals

Normal (15-25): Prevents clustering, maintains flow

Conservative (30-50): Major setups only Default: 15 - optimal trade frequency

Ensemble Configuration

Select markets for consensus analysis:

SPY: Broad market sentiment

QQQ: Technology leadership

IWM: Small-cap risk appetite

DIA: Blue-chip stability

More instruments = stronger consensus but potentially diluted signals

Visual Customization

Color Themes (6 professional options):

Quantum: Cyan/Pink - Modern trading aesthetic

Matrix: Green/Red - Classic terminal look

Heat: Blue/Red - Temperature metaphor

Neon: Cyan/Magenta - High contrast

Ocean: Turquoise/Coral - Calming palette

Sunset: Red-orange/Teal - Warm gradients

Display Controls:

- Toggle each visual component

- Adjust transparency levels

- Scale dashboard text

- Show/hide confidence scores

- Trading Strategies by Market State

- Ergodic State Strategy (Primary Color Bands)

Market Characteristics

- Price oscillates predictably

- Support/resistance hold

- Volume patterns repeat

- Mean reversion dominates

Optimal Approach

Entry: Fade moves at band extremes

Target: Middle band (equilibrium)

Stop: Just beyond outer bands

Size: Full confidence-based position

Recommended Tools

- RSI for oversold/overbought

- Bollinger Bands for extremes

- Volume profile for levels

- Non-Ergodic State Strategy (Danger Color Bands)

Market Characteristics

- Price trends persistently

- Levels break decisively

- Volume confirms direction

- Momentum accelerates

Optimal Approach

Entry: Breakout from bands

Target: Trail with expanding bands

Stop: Inside opposite band

Size: Scale in with trend

Recommended Tools

- Moving average alignment

- ADX for trend strength

- MACD for momentum

- Advanced Features Explained

Quantum Coherence Metric

Measures phase alignment between individual and ensemble behavior:

80-100%: Perfect sync - strong mean reversion setup

50-80%: Moderate alignment - mixed signals

0-50%: Decoherence - trending behavior likely

Path Dependency Analysis

Quantifies how much history influences current price:

Low (<30%): Technical patterns reliable

Medium (30-50%): Mixed influences

High (>50%): Fundamental shift occurring

Volatility Regime Classification

Contextualizes current volatility:

Normal: Standard strategies apply

Elevated: Widen stops, reduce size

Extreme: Defensive mode required

Signal Strength Indicator

Real-time opportunity quality:

- Distance from threshold

- Momentum acceleration

- Cross-validation factors

Risk Management Framework

Position Sizing by Confidence

90%+ confidence = 100% position size

70-90% confidence = 75% position size

50-70% confidence = 50% position size

<50% confidence = 25% or skip

Dynamic Stop Placement

Ergodic State: ATR × 1.0 from entry

Non-Ergodic State: ATR × 2.0 from entry

Volatility Adjustment: Multiply by current regime

Multi-Timeframe Alignment

- Check higher timeframe regime

- Confirm ensemble consensus

- Verify volume participation

- Align with major levels

What Makes EMD Unique

Original Contributions

First Ergodic Theory Trading Application: Transforms abstract physics into practical signals

Ensemble Market Analysis: Revolutionary multi-market divergence system

Adaptive Confidence Engine: Institutional-grade signal quality metrics

Quantum Coherence: Novel market alignment measurement

Smart Signal Management: Prevents clustering while maintaining responsiveness

Technical Innovations

Dynamic Threshold Adaptation: Self-adjusting sensitivity

Path Memory Integration: Historical dependency weighting

Stress-Adjusted Scoring: Market condition normalization

Real-Time Performance Tracking: Built-in strategy analytics

Optimization Guidelines

By Timeframe

Scalping (1-5 min)

Period: 10-15

Threshold: 0.5-1.0

Memory: 20-30

Spacing: 5-10

Day Trading (5-60 min)

Period: 20-30

Threshold: 1.5-2.5

Memory: 40-60

Spacing: 15-20

Swing Trading (1H-1D)

Period: 40-60

Threshold: 2.0-3.0

Memory: 80-120

Spacing: 25-35

Position Trading (1D-1W)

Period: 60-100

Threshold: 3.0-5.0

Memory: 100-200

Spacing: 40-50

By Market Condition

Trending Markets

- Increase threshold

- Extend memory

- Focus on breaks

Ranging Markets

- Decrease threshold

- Shorten memory

- Focus on restores

Volatile Markets

- Increase spacing

- Raise confidence requirement

- Reduce position size

- Integration with Other Analysis

- Complementary Indicators

For Ergodic States

- RSI divergences

- Bollinger Band squeezes

- Volume profile nodes

- Support/resistance levels

For Non-Ergodic States

- Moving average ribbons

- Trend strength indicators

- Momentum oscillators

- Breakout patterns

- Fundamental Alignment

- Check economic calendar

- Monitor sector rotation

- Consider market themes

- Evaluate risk sentiment

Troubleshooting Guide

Too Many Signals:

- Increase threshold

- Extend signal spacing

- Raise confidence minimum

Missing Opportunities

- Decrease threshold

- Reduce signal spacing

- Check ensemble settings

Poor Win Rate

- Verify timeframe alignment

- Confirm volume participation

- Review risk management

Disclaimer

This indicator is for educational and informational purposes only. It does not constitute financial advice. Trading involves substantial risk of loss and is not suitable for all investors. Past performance does not guarantee future results.

The ergodic framework provides unique market insights but cannot predict future price movements with certainty. Always use proper risk management, conduct your own analysis, and never risk more than you can afford to lose.

This tool should complement, not replace, comprehensive trading strategies and sound judgment. Markets remain inherently unpredictable despite advanced analysis techniques.

Transform market chaos into trading clarity with Ergodic Market Divergence.

Created with passion for the TradingView community

Trade with insight. Trade with anticipation.

— Dskyz , for DAFE Trading Systems

Aftershock by Session [SAKANE]■ Background & Motivation

In 24/7 markets like crypto, not all participants react simultaneously to major events.

Instead, reactions unfold across different regional trading sessions — Asia (APAC), Europe (EU), and the United States (US) — each with its own tempo and sentiment.

This indicator is designed to visualize which session drives the market after a key event — capturing the "aftershock" effect that ripples through time zones.

■ Key Features

Tracks price return (open → close) for each session: APAC / EU / US

Cumulative session returns are calculated and visualized

Smoothing options: SMA, EMA, or Ehlers SuperSmoother

Optimized for daily charts to highlight structural momentum shifts

Toggle visibility of each session independently

■ Why “Aftershock”?

Take April 2, 2025 — the day of the “Trump Tariff Opening.”

That policy announcement triggered a market-wide response. But:

Which session reacted first?

Which session truly moved the market?

This indicator is named “Aftershock” because it helps you see the ripple effect of such events — when and where momentum followed.

■ How to Use

Search for “Aftershock by Session ” on TradingView

Add it to your chart (use Daily timeframe)

Customize sessions and smoothing options via settings

You can also bookmark it for quick access.

■ Insights & Use Cases

Detect which session initiated or led market moves after news events

Understand geo-temporal dynamics — did the move start in Asia, Europe, or the US?

For example, on April 2, 2025, the day Trump’s tariff pivot was announced:

You can instantly see which session took the lead —

the APAC session hesitated, while the US session drove the trend.

This insight becomes visually obvious with the cumulative lines.

■ Unique Value

Unlike typical indicators based on raw price action,

Aftershock analyzes market movement through a session-based structural lens.

It captures where capital actually moved — and when.

A tool not just for technical analysis, but for event-driven, macro-aware market reading.

■ Final Thoughts

To truly understand market mechanics, we must look beyond candles and trends.

Aftershock by Session breaks down the 24-hour cycle into meaningful regional flows,

allowing you to track the true drivers behind price momentum.

Whether you're trading, researching, or tracking macro catalysts,

this tool helps answer the key question:

“Who moved the market — and when?”

Machine Learning | Adaptive Trend Signals [Bitwardex]⚙️🧠Machine Learning | Adaptive Trend Signals

🔷Overview

Machine Learning | Adaptive Trend Signals is a Pine Script™ v6 indicator designed to visualize market trends and generate signals through a combination of volatility clustering, Gaussian smoothing, and adaptive trend calculations. Built as an overlay indicator, it integrates advanced techniques inspired by machine learning concepts, such as K-Means clustering, to adapt to changing market conditions. The script is highly customizable, includes a backtesting module, and supports alert conditions, making it suitable for traders exploring trend-based strategies and developers studying volatility-driven indicator design.

🔷Functionality

The indicator performs the following core functions:

• Volatility Clustering: Uses K-Means clustering to categorize market volatility into high, medium, and low states, adjusting trend sensitivity accordingly.

• Trend Calculation: Computes adaptive trend lines (SmartTrend) based on volatility-adjusted standard deviation, smoothed RSI, and ADX filters.

• Signal Generation: Identifies potential buy and sell points through trend line crossovers and directional confirmation.

• Backtesting Module: Tracks trade outcomes based on the SmartTrend3 value, displaying win rate and total trades.

• Visualization: Plots trend lines with gradient colors and optional signal markers (bullish 🐮 and bearish 🐻).

• Alerts: Provides configurable alerts for trend shifts and volatility state changes.

🔷Technical Methodology

Volatility Clustering with K-Means

The indicator employs a K-Means clustering algorithm to classify market volatility, measured via the Average True Range (ATR), into three distinct clusters:

• Data Collection: Gathers ATR values over a user-defined training period (default: 100 bars).

• Centroid Initialization: Sets initial centroids at the highest, lowest, and midpoint ATR values within the training period.

• Iterative Clustering: Assigns ATR data points to the nearest centroid, recalculates centroid means, and repeats until convergence.

• Dynamic Adjustment: Assigns a volatility state (high, medium, or low) based on the closest centroid, adjusting the trend factor (e.g., tighter for high volatility, wider for low volatility).

This approach allows the indicator to adapt its sensitivity to varying market conditions, providing a data-driven foundation for trend calculations.

🔷Gaussian Smoothing

To enhance signal clarity and reduce noise, the indicator applies Gaussian kernel smoothing to:

• RSI: Smooths the Relative Strength Index (calculated from OHLC4) to filter short-term fluctuations.

• SmartTrend: Smooths the primary trend line for a more stable output.

The Gaussian kernel uses a sigma value derived from the user-defined smoothing length, ensuring mathematically consistent noise reduction.

🔷SmartTrend Calculation

The pineSmartTrend function is the core of the indicator, producing three trend lines:

• SmartTrend: The primary trend line, calculated using a volatility-adjusted standard deviation, smoothed RSI, and ADX conditions.

• SmartTrend2: A secondary trend line with a wider factor (base factor * 1.382) for signal confirmation.

SmartTrend3: The average of SmartTrend and SmartTrend2, used for plotting and backtesting.

Key components of the calculation include:

• Dynamic Standard Deviation: Scales based on ATR relative to its 50-period smoothed average, with multipliers (1.0 to 1.4) applied according to volatility thresholds.

• RSI and ADX Filters: Requires RSI > 50 for bullish trends or < 50 for bearish trends, alongside ADX > 15 and rising to confirm trend strength.

Volatility-Adjusted Bands: Constructs upper and lower bands around price action, adjusted by the volatility cluster’s dynamic factor.

🔷Signal Generation

The generate_signals function generates signals as follows:

• Buy Signal: Triggered when SmartTrend crosses above SmartTrend2 and the price is above SmartTrend, with directional confirmation.

• Sell Signal: Triggered when SmartTrend crosses below SmartTrend2 and the price is below SmartTrend, with directional confirmation.

Directional Logic: Tracks trend direction to filter out conflicting signals, ensuring alignment with the broader market context.

Signals are visualized as small circles with bullish (🐮) or bearish (🐻) emojis, with an option to toggle visibility.

🔷Backtesting

The get_backtest function evaluates signal outcomes using the SmartTrend3 value (rather than closing prices) to align with the trend-based methodology.

It tracks:

• Total Trades: Counts completed long and short trades.

• Win Rate: Calculates the percentage of trades where SmartTrend3 moves favorably (higher for longs, lower for shorts).

Position Management: Closes opposite positions before opening new ones, simulating a single-position trading system.

Results are displayed in a table at the top-right of the chart, showing win rate and total trades. Note that backtest results reflect the indicator’s internal logic and should not be interpreted as predictive of real-world performance.

🔷Visualization and Alerts

• Trend Lines: SmartTrend3 is plotted with gradient colors reflecting trend direction and volatility cluster, accompanied by a secondary line for visual clarity.

• Signal Markers: Optional buy/sell signals are plotted as small circles with customizable colors.

• Alerts: Supports alerts for:

• Bullish and bearish trend shifts (confirmed on bar close).

Transitions to high, medium, or low volatility states.

🔷Input Parameters

• ATR Length (default: 14): Period for ATR calculation, used in volatility clustering.

• Period (default: 21): Common period for RSI, ADX, and standard deviation calculations.

• Base SmartTrend Factor (default: 2.0): Base multiplier for volatility-adjusted bands.

• SmartTrend Smoothing Length (default: 10): Length for Gaussian smoothing of the trend line.

• Show Buy/Sell Signals? (default: true): Enables/disables signal markers.

• Bullish/Bearish Color: Customizable colors for trend lines and signals.

🔷Usage Instructions

• Apply to Chart: Add the indicator to any TradingView chart.

• Configure Inputs: Adjust parameters to align with your trading style or market conditions (e.g., shorter ATR length for faster markets).

• Interpret Output:

• Trend Lines: Use SmartTrend3’s direction and color to gauge market bias.

• Signals: Monitor bullish (🐮) and bearish (🐻) markers for potential entry/exit points.

• Backtest Table: Review win rate and total trades to understand the indicator’s behavior in historical data.

• Set Alerts: Configure alerts for trend shifts or volatility changes to support manual or automated trading workflows.

• Combine with Analysis: Use the indicator alongside other tools or market context, as it is designed to complement, not replace, comprehensive analysis.

🔷Technical Notes

• Data Requirements: Requires at least 100 bars for accurate volatility clustering. Ensure sufficient historical data is loaded.

• Market Suitability: The indicator is designed for trend detection and may perform differently in ranging or volatile markets due to its reliance on RSI and ADX filters.

• Backtesting Scope: The backtest module uses SmartTrend3 values, which may differ from price-based outcomes. Results are for informational purposes only.

• Computational Intensity: The K-Means clustering and Gaussian smoothing may increase processing time on lower timeframes or with large datasets.

🔷For Developers

The script is modular, well-commented, encouraging reuse and modification with proper attribution.

Key functions include:

• gaussianSmooth: Applies Gaussian kernel smoothing to any data series.

• pineSmartTrend: Computes adaptive trend lines with volatility and momentum filters.

• getDynamicFactor: Adjusts trend sensitivity based on volatility clusters.

• get_backtest: Evaluates signal performance using SmartTrend3.

Developers can extend these functions for custom indicators or strategies, leveraging the volatility clustering and smoothing methodologies. The K-Means implementation is particularly useful for adaptive volatility analysis.

🔷Limitations

• The indicator is not predictive and should be used as part of a broader trading strategy.

• Performance varies by market, timeframe, and parameter settings, requiring user experimentation.

• Backtest results are based on historical data and internal logic, not real-world trading conditions.

• Volatility clustering assumes sufficient historical data; incomplete data may affect accuracy.

🔷Acknowledgments

Developed by Bitwardex, inspired by machine learning concepts and adaptive trading methodologies. Community feedback is welcome via TradingView’s platform.

🔷 Risk Disclaimer

Trading involves significant risks, and most traders may incur losses. Bitwardex AI Algo is provided for informational and educational purposes only and does not constitute financial advice or a recommendation to buy or sell any financial instrument . The signals, metrics, and features are tools for analysis and do not guarantee profits or specific outcomes. Past performance is not indicative of future results. Always conduct your own due diligence and consult a financial advisor before making trading decisions.

M2 Liqudity WaveGlobal Liquidity Wave Indicator (M2-Based)

The Global Liquidity Wave Indicator is designed to track and visualize the impact of global M2 liquidity on risk assets—especially those highly correlated to monetary expansion, like Bitcoin, MSTR, and other macro-sensitive equities.

Key features include:

Leading Signal: Historically leads Bitcoin price action by approximately 70 days, offering traders and analysts a forward-looking edge.

Wave-Based Projection: Visualizes a "probability cloud"—a smoothed band representing the most likely trajectory for Bitcoin based on changes in global liquidity.

Min/Max Offset Controls: Adjustable offsets let you define the range of lookahead windows to shape the wave and better capture liquidity-driven inflection points.

Explicit Offset Visualization: Option to manually specify an exact offset to fine-tune the overlay, ideal for testing hypotheses or aligning with macro narratives.

Macro Alignment: Particularly effective for assets with high sensitivity to global monetary policy and liquidity cycles.

This tool is not just a chart overlay—it's a lens into the liquidity engine behind the market, helping anticipate directional bias in advance of price moves.

How to use?

- Enable the indicator for BTCUSD.

- Set Offset Range Start and End to 70 and 115 days

- Set Specific Offset to 78 days (this can change so you'll need to play around)

FAQ

Why a global liquidity wave?

The global liquidity wave accounts for variability in how much global liquidity affects an underlying asset. Think of the Global Liquidity Wave as an area that tracks the most probable path of Bitcoin, MSTR, etc. based on the total global liquidity.

Why the offset?

Global liquidity takes time to make its way into assets such as #Bitcoin, Strategy, etc. and there can be many reasons for that. It's never a specific number of days of offset, which is why a global liquidity wave is helpful in tracking probable paths for highly correlated risk assets.

Day’s Open ForecastOverview

This Pine Script indicator combines two primary components:

1. Day’s Open Forecast:

o Tracks historical daily moves (up and down) from the day’s open.

o Calculates average up and down moves over a user-defined lookback period.

o Optionally includes standard deviation adjustments to forecast potential intraday levels.

o Plots lines on the chart for the forecasted up and down moves from the current day's open.

2. Session VWAP:

o Allows you to specify a custom trading session (by time range and UTC offset).

o Calculates and plots a Volume-Weighted Average Price (VWAP) during that session.

By combining these two features, you can gauge potential intraday moves relative to historical behavior from the open, while also tracking a session-specific VWAP that can act as a dynamic support/resistance reference.

How the Code Works

1. Collect Daily Moves

o The script detects when a new day starts using time("D").

o Once a new day is detected, it stores the previous day’s up-move (dayHigh - dayOpen) and down-move (dayOpen - dayLow) into arrays.

o These arrays keep track of the last N days (default: 126) of up/down move data.

2. Compute Statistics

o The script computes the average (f_average()) of up-moves and down-moves over the stored period.

o It also computes the standard deviation (f_stddev()) of up/down moves for optional “forecast bands.”

3. Forecast Lines

o Plots the current day’s open.

o Plots the average forecast lines above and below the open (Avg Up Move Level and Avg Down Move Level).

o If standard deviation is enabled, plots additional lines (Avg+StdDev Up and Avg+StdDev Down).

4. Session VWAP

o The script detects the start of a user-defined session (via input.session) and resets accumulation of volume and the numerator for VWAP.

o As each bar in the session updates, it accumulates volume (vwapCumulativeVolume) and a price-volume product (vwapCumulativeNumerator).

o The session VWAP is then calculated as (vwapCumulativeNumerator / vwapCumulativeVolume) and plotted.

5. Visualization Options

o Users can toggle standard deviation usage, historical up/down moves plotting, and whether to show the forecast “bands.”

o The vwapSession and vwapUtc inputs let you adjust which session (and time zone offset) the VWAP is calculated for.

________________________________________

How to Use This Indicator on TradingView

1. Create a New Script

o Open TradingView, then navigate to Pine Editor (usually found at the bottom of the chart).

o Copy and paste the entire code into the editor.

2. Save and Add to Chart

o Click Save (give it a relevant title if you wish), then click Add to chart.

o The indicator will appear on your chart with the forecast lines and VWAP.

o By default, it is overlayed on the price chart (because of overlay=true).

3. Customize Inputs

o In the indicator’s settings, you can:

Change lookback days (default: 126).

Enable or disable standard deviation (Include Standard Deviation in Forecast?).

Adjust the standard deviation multiplier.

Choose whether to plot bands (Plot Bands with Averages/StdDev?).

Plot historical moves if desired (Plot Historical Up/Down Moves for Reference?).

Set your custom session and UTC offset for the VWAP calculation.

4. Interpretation

o “Current Day Open” is simply today’s open price on your chart.

o Up/Down Move Lines: Indicate a potential forecast based on historical averages.

If standard deviation is enabled, the second set of lines acts as an extended range.

o VWAP: Helpful for determining intraday price equilibrium over the specified session.

Important Notes / Best Practices

• The script only updates the historical up/down move data once per day (when a new day starts).

• The VWAP portion resets at the start of the specified session each day.

• Standard deviation multiplies the average up/down range, giving you a sense of “volatility range” around the day’s open.

• Adjust the lookback length (dayCount) to balance how many days of data you want to average. More days = smoother but possibly slower to adapt; fewer days = more reactive but potentially less reliable historically.

Educational & Liability Disclaimers

1. Educational Disclaimer

o The information provided by this indicator is for educational and informational purposes only. It is a technical analysis tool intended to demonstrate how to use historical data and basic statistics in Pine Script.

2. No Financial Advice

o This script does not constitute financial or investment advice. All examples and explanations are solely illustrative. You should always do your own analysis before making any investment decisions.

3. No Liability

o The author of this script is not liable for any losses or damages—monetary or otherwise—that may occur from the application of this script.

o Past performance does not guarantee future results, and you should never invest money you cannot afford to lose.

By adding this indicator to your TradingView chart, you acknowledge and accept that you alone are responsible for your own trading decisions.

Enjoy using the “Day’s Open Forecast” and Session VWAP for better market insights!

Liquidity Depth [AlgoAlpha]OVERVIEW

This script visualizes market liquidity by identifying key price levels where significant volume has transacted. It highlights zones of high buying and selling interest, helping traders understand where liquidity is accumulating and how price may respond to these areas. By dynamically tracking volume at highs and lows, the script builds a real-time liquidity profile, making it a powerful tool for identifying potential support and resistance levels.

CONCEPTS

Liquidity depth analysis helps traders determine how price interacts with supply and demand at different levels. The script processes historical volume data to distinguish between high-liquidity and low-liquidity zones. It assigns transparency levels to plotted lines , ensuring that more relevant liquidity areas stand out visually. The script adds a profile to show the depth of liquidity (derived from historical volume data) for levels above and below the current price

FEATURES

Liquidity Levels: Tracks liquidity levels based on volume concentration at price high and lows.

Volume-Based Transparency: More significant liquidity levels are displayed with higher visibility, showing their significance.

Interpolation: interpolates the bullish and bearish liquidity depth at a user defined range away from the price, helping in comparing the liquidity amounts between bullish and bearish.

Depth Profile: Allows traders to visualize depth of liquidity in a more quantitative and clearer way than the liquidity levels/list]

USAGE

This indicator is best used to track liquidity levels and potential price reaction areas. Traders can adjust the Liquidity Lookback setting to analyze past liquidity levels over different historical periods. The Profile Resolution setting controls the granularity of liquidity depth visualization, with higher values providing more detail. The script can be applied across different timeframes, from intraday scalping to swing trading analysis. The plotted liquidity zones provide traders with insights into where price may encounter strong support, resistance, or potential liquidity-driven reversals.

Stock Sector ETF with IndicatorsThe Stock Sector ETF with Indicators is a versatile tool designed to track the performance of sector-specific ETFs relative to the current asset. It automatically identifies the sector of the underlying symbol and displays the corresponding ETF’s price action alongside key technical indicators. This helps traders analyze sector trends and correlations in real time.

---

Key Features

Automatic Sector Detection:

Fetches the sector of the current asset (e.g., "Technology" for AAPL).

Maps the sector to a user-defined ETF (default: SPDR sector ETFs) .

Technical Indicators:

Simple Moving Average (SMA): Tracks the ETF’s trend.

Bollinger Bands: Highlights volatility and potential reversals.

Donchian High (52-Week High): Identifies long-term resistance levels.

Customizable Inputs:

Adjust indicator parameters (length, visibility).

Override default ETFs for specific sectors.

Informative Table:

Displays the current sector and ETF symbol in the bottom-right corner.

---

Input Settings

SMA Settings

SMA Length: Period for calculating the Simple Moving Average (default: 200).

Show SMA: Toggle visibility of the SMA line.

Bollinger Bands Settings

BB Length: Period for Bollinger Bands calculation (default: 20).

BB Multiplier: Standard deviation multiplier (default: 2.0).

Show Bollinger Bands: Toggle visibility of the bands.

Donchian High (52-Week High)

Daily High Length: Days used to calculate the high (default: 252, approx. 1 year).

Show High: Toggle visibility of the 52-week high line.

Sector Selections

Customize ETFs for each sector (e.g., replace XLU with another utilities ETF).

---

Example Use Cases

Trend Analysis: Compare a stock’s price action to its sector ETF’s SMA for trend confirmation.

Volatility Signals: Use Bollinger Bands to spot ETF price squeezes or breakouts.

Sector Strength: Monitor if the ETF is approaching its 52-week high to gauge sector momentum.

Enjoy tracking sector trends with ease! 🚀

PT Least Squares Moving AveragePT LSMA Multi-Period Indicator

The PT Least Squares Moving Average (LSMA) Multi-Period Indicator is a powerful tool designed for investors who want to track market trends across multiple time horizons in a single, convenient indicator. This indicator calculates the LSMA for four different periods— 25 bars, 50 bars, 450 bars, and 500 bars providing a comprehensive view of short-term and long-term market movements.

Key Features:

- Multi-Timeframe Trend Analysis: Tracks both short-term (25 & 50 bars) and long-term (450 & 500 bars) market trends, helping investors make informed decisions.

- Smoothing Capability: The LSMA reduces noise by fitting a linear regression line to past price data, offering a clearer trend direction compared to traditional moving averages.

- One-Indicator Solution: Combines multiple LSMA periods into a single chart, reducing clutter and enhancing visual clarity.

- Versatile Applications: Suitable for trend identification, market timing, and spotting potential reversals across different timeframes.

- Customizable Styling: Allows users to customize colors and line styles for each period to suit their preferences.

How to Use:

1. Short-Term Trends (25 & 50 bars):Ideal for identifying recent price movements and short-term trade opportunities.

2. Long-Term Trends (450 & 500 bars): Helps investors gauge broader market sentiment and position themselves accordingly for longer holding periods.

3. Trend Confirmation: When shorter LSMA periods cross above longer ones, it may signal bullish momentum, whereas the opposite may indicate bearish sentiment.

4. Support and Resistance: The LSMA lines can act as dynamic support and resistance levels during trending markets.

Best For:

- Long-term investors looking to align their positions with dominant market trends.

- Swing traders seeking confirmation from multiple time horizons.

- Portfolio managers tracking price momentum across various investment durations.

This LSMA Multi-Period Indicator equips investors with a well-rounded perspective on price movements, offering a strategic edge in navigating market cycles with confidence.

Created by Prince Thomas

FTD & DD AnalyzerFTD & DD Analyzer

A comprehensive tool for identifying Follow-Through Days (FTDs) and Distribution Days (DDs) to analyze market conditions and potential trend changes, based on William J. O'Neil's proven methodology.

About the Methodology

This indicator implements the market analysis techniques developed by William J. O'Neil, founder of Investor's Business Daily and author of "How to Make Money in Stocks." O'Neil's research, spanning market data back to the 1880s, has successfully identified major market turns throughout history. His FTD and DD concepts remain crucial tools for institutional investors and serious traders.

Overview

This indicator helps traders identify two critical market conditions:

Distribution Days (DDs) - days of institutional selling pressure

Follow-Through Days (FTDs) - confirmation of potential market bottoms and new uptrends

The combination of these signals provides valuable insight into market health and potential trend changes.

Key Features

Distribution Day detection with customizable criteria

Follow-Through Day identification based on classical methodology

Market bottom detection using EMA analysis

Dynamic warning system for accumulated Distribution Days

Visual alerts with customizable labels

Advanced debug mode for detailed analysis

Flexible display options for different trading styles

Distribution Days Analysis

What is a Distribution Day?

A Distribution Day occurs when:

The price closes lower by a specified percentage (default -0.2%)

Volume is higher than the previous day

DD Settings

Price Threshold: Minimum price decline to qualify (default -0.2%)

Lookback Period: Number of days to analyze for DD accumulation (default 25)

Warning Levels:

First warning at 4 DDs

Severe warning (SOS - Sign of Strength) at 6 DDs

Display Options:

Show/hide DD count

Show/hide DD labels

Choose between showing all DDs or only within lookback period

Follow-Through Day Detection

What is a Follow-Through Day?

Following O'Neil's research, a Follow-Through Day confirms a potential market bottom when:

Occurs between day 4 and 13 after a bottom formation (optimal: days 4-7)

Shows significant price gain (default 1.5%)

Accompanied by higher volume than the previous day

Key Statistics:

FTDs followed by distribution on days 1-2 fail 95% of the time

Distribution on day 3 leads to 70% failure rate

Later distribution (days 4-5) shows only 30% failure rate

FTD Settings

Minimum Price Gain: Required percentage gain (default 1.5%)

Valid Window: Day 4 to Day 13 after bottom

Quality Rating:

🚀 for FTDs occurring within 7 days (historically most reliable)

⭐ for later FTDs

Market Bottom Detection

The indicator uses a sophisticated approach to identify potential market bottoms:

EMA Analysis:

Tracks 8 and 21-period EMAs

Monitors EMA alignment and momentum

Customizable tolerance levels

Price Action:

Looks for lower lows within specified lookback period

Confirms bottom with subsequent price action

Reset mechanism to prevent false signals

Visual Indicators

Label Types

📉 Distribution Days

⬇️ Market Bottoms

🚀/⭐ Follow-Through Days

⚠️ DD Warning Levels

Customization Options

Label size: Tiny, Small, Normal, Large

Label style: Default, Arrows, Triangles

Background colors for different signals

Dynamic positioning using ATR multiplier

Practical Usage

1. Monitor DD Accumulation:

Watch for increasing number of Distribution Days

Pay attention to warning levels (4 and 6 DDs)

Consider reducing exposure when warnings appear

2. Bottom Recognition:

Look for potential bottom formations

Monitor EMA alignment and price action

Wait for confirmation signals

3. FTD Confirmation:

Track days after potential bottom

Watch for strong price/volume action in valid window

Note FTD quality rating for additional context

Alert System

Built-in alerts for:

New Distribution Days

Follow-Through Day signals

High DD accumulation warnings

Tips for Best Results

Use multiple timeframes for confirmation

Combine with other market health indicators

Pay attention to sector rotation and market leadership

Monitor volume patterns for confirmation

Consider market context and external factors

Technical Notes

The indicator uses advanced array handling for DD tracking

Dynamic calculations ensure accurate signal generation

Debug mode available for detailed analysis

Optimized for real-time and historical analysis

Additional Information

Compatible with all markets and timeframes

Best suited for daily charts

Regular updates and maintenance

Based on O'Neil's time-tested market analysis principles

Conclusion

The FTD & DD Analyzer provides a systematic approach to market analysis, combining O'Neil's proven methodologies with modern technical analysis. It helps traders identify potential market turns while monitoring institutional participation through volume analysis.

Remember that no indicator is perfect - always use in conjunction with other analysis tools and proper risk management.

Drawdown from All-Time High (Line)This Pine Script is a **Drawdown Indicator from All-Time High** for TradingView. It calculates and plots the percentage drawdown from the highest price the asset has ever reached (the all-time high). Here's a breakdown of what this script does:

### Description:

- **Drawdown Calculation**:

- The drawdown is calculated as the difference between the current price (`close`) and the all-time high, divided by the all-time high, and multiplied by 100 to express it as a percentage.

- If the current price is higher than the previous all-time high, the all-time high is updated to the current price.

- **All-Time High Tracking**:

- The script tracks the highest price (`allTimeHigh`) that the asset has ever reached. Each time a new high is reached, the `allTimeHigh` value is updated.

- **Line Plot**:

- The drawdown percentage is then plotted as a line on the chart, with a color of **blue** for easy visualization.

- The line shows how much the price has dropped relative to its all-time high.

- **Zero Line**:

- A horizontal line is added at the **0%** level to act as a reference point, which is helpful to identify when the asset has fully recovered to its all-time high.

### Key Features:

- **Track Drawdown**: The indicator helps visualize how far the current price has fallen from its highest point, which is useful for understanding the depth of losses (drawdowns) during a period.

- **Update All-Time High**: The indicator automatically updates the all-time high whenever a new high is detected.

- **Visual Reference**: The 0% horizontal line provides a clear indication of when the asset is at its all-time high, and the drawdown is at 0%.

### How it Works:

- If the current price surpasses the all-time high, the script will reset the all-time high to the new price.

- The drawdown percentage is calculated from the current price relative to this all-time high, and it is displayed as a line on the chart.

### Visuals:

- **Drawdown Line**: Plots the percentage of the drawdown, which is the drop from the all-time high.

- **Zero Line**: A dotted horizontal line at 0% marks the level of the all-time high.

This indicator is valuable for understanding the extent of price corrections and potential recoveries relative to the historical peak of the asset. It is especially useful for traders and investors who want to assess the risk of drawdowns in relation to the highest price achieved by the asset.

B-Xtrender By Neal inspired from @PuppytherapyThanks to @puppytherapy for creating the original B-Xtrender indicator, available at this link: B-Xtrender by @QuantTherapy

I played around the code to have entry and exit condition. The B-Xtrender @QuantTherapy

indicator is a momentum-based tool designed to help traders identify potential trade opportunities by tracking shifts in market momentum. Using a smoothed momentum oscillator, it detects changes in trend direction and provides clear signals for entry and exit points.

Features

Momentum Detection:

Tracks market momentum using the BX-Trender Oscillator.

Green bars indicate bullish momentum, while red bars indicate bearish momentum.

Lighter shades of green/red reflect weakening momentum.

Entry and Exit Signals:

Entry Condition: A long trade is triggered when the oscillator changes from red to green .

Exit Condition: A long trade exit is triggered when the oscillator changes from green to red .

Dynamic PnL Calculation:

Automatically calculates profit or loss in percentage (%) when a trade is exited.

Positive PnL values are prefixed with `+`, and negative values are shown as `-`.

Clear Visualization:

Bar chart-style oscillator in a separate pane for better trend visualization.

Trade labels on the main price chart for clear entry and exit points.

Inputs

Short-Term Momentum Parameters:

Short - L1: Length of the first EMA for short-term momentum calculations.

Short - L2: Length of the second EMA for short-term momentum calculations.

Short - L3: RSI smoothing period applied to the short-term momentum.

Long-Term Momentum Parameters:

Long - L1: Length of the EMA for long-term momentum calculations.

Long - L2: RSI smoothing period applied to the long-term momentum.

Entry and Exit Logic

Entry Condition:

A long trade is triggered when:

The BX-Trender Oscillator changes from red to green .

This shift indicates bullish momentum.

Exit Condition:

A long trade exit is triggered when:

The BX-Trender Oscillator changes from green to red .

This shift indicates a loss of bullish momentum or the start of bearish momentum.

PnL Calculation:

When exiting a trade, the indicator calculates the profit or loss as a percentage of the entry price.

Example:

A profit is displayed as +5.67% .

A loss is displayed as -3.21% .

Visualization

Oscillator Bars:

Green Bars: Represent increasing bullish momentum.

Light Green Bars: Represent weakening bullish momentum.

Red Bars: Represent increasing bearish momentum.

Light Red Bars: Represent weakening bearish momentum.

Just make sure that you checked off the B-Xtrend oscillator off from the style so chart can be active

Trade Labels:

Entry Labels: Displayed below the candle with the text Entry, long .

Exit Labels: Displayed above the candle with the text Exit .

Bar Chart Pane:

The oscillator is displayed in a separate pane for clear trend visualization.

Default Style

Oscillator Colors:

Green for bullish momentum.

Red for bearish momentum.

Light green and light red for weaker momentum.

Trade Labels:

Green labels for entries.

Red labels for exits, with percentage PnL displayed.

Use Cases

Momentum-Based Entries:

Detects shifts in momentum from bearish to bullish for precise trade entry points.

Trend Reversal Detection:

Identifies when bullish momentum weakens, signaling an exit opportunity.

Visual Simplicity:

Offers an intuitive way to track trends with its bar chart-style oscillator and clear trade labels.

This indicator doesn't indicate that it will work perfectly. More updates on the way.

Hull MA with Alerts and LabelsThis script is designed to help traders visually track market trends using various types of moving averages (MAs) and to receive alerts when certain conditions are met. Here’s a detailed breakdown of how the script works:

1. User Inputs and Customization:

MA Length: Traders can define the length of the moving average (default is 100).

Confirmation Candles: The trader can specify how many candles must confirm a trend before the script triggers a signal (default is 1).

MA Variation: The trader can choose between different moving average types: Simple Moving Average (SMA), Exponential Moving Average (EMA), Weighted Moving Average (WMA), or Hull Moving Average (HMA).

Source: Traders select the price source for the moving average calculation (e.g., close price).

Ribbon Transparency: Allows control over the transparency level of the ribbon plotted between the moving averages.

Bullish/Bearish Ribbon Colors: The user can choose the colors for bullish and bearish trends.

2. Moving Average Calculations:

The script provides multiple options for calculating moving averages:

SMA (Simple Moving Average)

EMA (Exponential Moving Average)

WMA (Weighted Moving Average)

HMA (Hull Moving Average)

For the Hull Moving Average (HMA), it uses a specific formula that smoothens the movement and reduces lag, which is helpful for more reactive trend detection.

3. Plotting Moving Averages and Trend Ribbon:

The script calculates two key moving averages:

MHULL: The main moving average, selected based on the user’s chosen MA variation and source.

SHULL: A shifted version of the MHULL to help compare trends (shifted by 2 bars).

These two moving averages are plotted on the chart for visualization. MHULL is plotted in green (or another color if changed), while SHULL is plotted in red. A ribbon is drawn between MHULL and SHULL to indicate trends visually. The ribbon changes color depending on whether the trend is bullish (MHULL > SHULL) or bearish (MHULL < SHULL). The ribbon’s transparency can be adjusted for visual clarity.

4. Trend Detection:

Bullish Trend: The script checks if the price has closed above MHULL for the defined number of confirmation candles. If confirmed, a bullish trend is detected.

Bearish Trend: Similarly, the script checks if the price has closed below SHULL for the confirmation period, indicating a bearish trend.

The script tracks whether the market is in a bullish or bearish trend and prevents repeated signals by remembering the current trend state.

5. Alerts and Labels:

Bullish Alerts and Labels: When a confirmed bullish trend is detected (i.e., price closes above MHULL for the entire confirmation period and MHULL > SHULL), the script triggers an alert notifying the trader of the bullish condition. A "BULLISH" label is placed on the chart near the low of the candle where the trend was confirmed.

Bearish Alerts and Labels: If a confirmed bearish trend is detected (i.e., price closes below SHULL for the confirmation period and MHULL < SHULL), the script triggers an alert for the bearish condition. A "BEARISH" label is placed on the chart near the high of the candle where the trend was confirmed.

These alerts and labels help traders act quickly on trend changes and align their trading strategy with market conditions.

6. Practical Use for Traders:

For traders, this script offers:

Customizability : It allows traders to define the length and type of moving averages, choose price sources, and control how signals are confirmed.

Visual Trend Representation : The plotted MA lines and colored ribbons help traders easily see market direction.

Early Warnings : With alerts and labels, the script gives traders early signals when trends are shifting, allowing them to adjust positions accordingly.

Trend Confirmation : The script waits for a user-defined number of confirmation candles before signaling a new trend, reducing false signals.

Overall, the script helps traders automate their strategy by tracking moving averages and alerting them when key trend conditions are met.

Sharpe and Sortino Ratios█ OVERVIEW

This indicator calculates the Sharpe and Sortino ratios using a chart symbol's periodic price returns, offering insights into the symbol's risk-adjusted performance. It features the option to calculate these ratios by comparing the periodic returns to a fixed annual rate of return or the returns from another selected symbol's context.

█ CONCEPTS

Returns, risk, and volatility

The return on an investment is the relative gain or loss over a period, often expressed as a percentage. Investment returns can originate from several sources, including capital gains, dividends, and interest income. Many investors seek the highest returns possible in the quest for profit. However, prudent investing and trading entails evaluating such returns against the associated risks (i.e., the uncertainty of returns and the potential for financial losses) for a clearer perspective on overall performance and sustainability.

The profitability of an investment typically comes at the cost of enduring market swings, noise, and general uncertainty. To navigate these turbulent waters, investors and portfolio managers often utilize volatility , a measure of the statistical dispersion of historical returns, as a foundational element in their risk assessments because it provides a tangible way to gauge the uncertainty in returns. High volatility suggests increased uncertainty and, consequently, higher risk, whereas low volatility suggests more stable returns with minimal fluctuations, implying lower risk. These concepts are integral components in several risk-adjusted performance metrics, including the Sharpe and Sortino ratios calculated by this indicator.

Risk-free rate

The risk-free rate represents the rate of return on a hypothetical investment carrying no risk of financial loss. This theoretical rate provides a benchmark for comparing the returns on a risky investment and evaluating whether its excess returns justify the risks. If an investment's returns are at or below the theoretical risk-free rate or the risk premium is below a desired amount, it may suggest that the returns do not compensate for the extra risk, which might be a call to reassess the investment.

Since the risk-free rate is a theoretical concept, investors often utilize proxies for the rate in practice, such as Treasury bills and other government bonds. Conventionally, analysts consider such instruments "risk-free" for a domestic holder, as they are a form of government obligation with a low perceived likelihood of default.

The average yield on short-term Treasury bills, influenced by economic conditions, monetary policies, and inflation expectations, has historically hovered around 2-3% over the long term. This range also aligns with central banks' inflation targets. As such, one may interpret a value within this range as a minimum proxy for the risk-free rate, as it may correspond to the minimum rate required to maintain purchasing power over time. This indicator uses a default value of 2% as the risk-free rate in its Sharpe and Sortino ratio calculations. Users can adjust this value from the "Risk-free rate of return" input in the "Settings/Inputs" tab.

Sharpe and Sortino ratios

The Sharpe and Sortino ratios are two of the most widely used metrics that offer insight into an investment's risk-adjusted performance . They provide a standardized framework to compare the effectiveness of investments relative to their perceived risks. These metrics can help investors determine whether the returns justify the risks taken to achieve them, promoting more informed investment decisions.

Both metrics measure risk-adjusted performance similarly. However, they have some differences in their formulas and their interpretation:

1. Sharpe ratio

The Sharpe ratio , developed by Nobel laureate William F. Sharpe, measures the performance of an investment compared to a theoretically risk-free asset, adjusted for the investment risk. The ratio uses the following formula:

Sharpe Ratio = (𝑅𝑎 − 𝑅𝑓) / 𝜎𝑎

Where:

• 𝑅𝑎 = Average return of the investment

• 𝑅𝑓 = Theoretical risk-free rate of return

• 𝜎𝑎 = Standard deviation of the investment's returns (volatility)