VWAP+SMA+EMAThis is the only indicator combing the results of VWAP + 2 SMAs + 2 EMAs.

This is a free indicator. Enjoy using it.

Kunal Jain

Search in scripts for "vwap"

VWAP - Standard + 3 multi periodThis script combines the standard VWAP with 3 additional period-dependent VWAPs (originally coded by Neolao).

rth vwap and midMidpoint and VWAP are often important inflection points in daytrading. I managed to find a script providing me with a 24 hour session midline by NorthStarDayTrading and a RTH VWAP script by LDBC. So I decided to merge those two to get a RTH mid and vwap.

Rumpy's Donchian Anchored VWAPUses donchian points to anchor VWAPs (start a new VWAP interval). The defaults are set up for a 1H chart, with lookback periods of 1 day, 2 days, 1 week, 2 weeks and 4 weeks for the anchor points.

Green : upper donchian AVWAPs, Red : lower donchian AVWAPS, thin/1day to thickest/4 week.

Option to test whether a new point should be formed from a high or low exceeding the historical high/low over a lookback length or using a closes that exceed the historical high/low.

--------------------------------------

If you find it useful please consider a tip/donation :

BTC - 3BMEXEDyWJ58eXUEALYPadbn1wwWKmf6sA

Percent Difference Between VWAP and Price MTFShows the difference between vwap and price in percent.

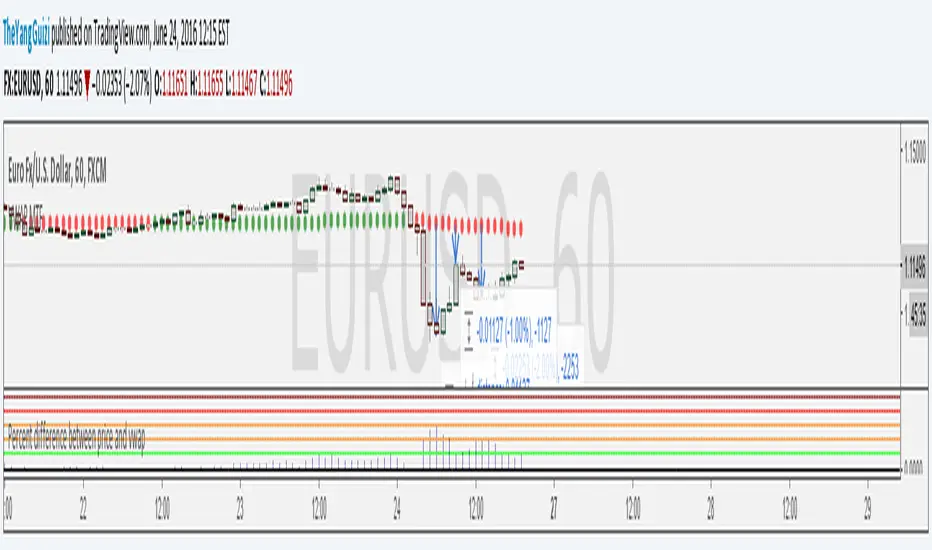

You can can choose between multiple timeframe vwap. Default is normal daily.

The levels on the indicator can be changed to whatever you want to.

In the chart above we can see eurusd reverting up at 3% below monthly vwap, after the brexit dip, It then turns down again at 1% from monthly and lastly it turns up again at 2% from monthly.

Script is a small modification of this:

VWAP Session and NY CashAuto Anchored VWAPs with Label options

Session starts at 1800 EST

Cash Open or NY Session starts 0930 EST

Nic's Anchored VWAP 4Poor mans anchored vwap. Allows you to identified the volume weighted average price from 4 specific points in time.

Best used on key pivot point high's and lows'

Difference % between PRICE and VWAP V2Shows difference between price and daily/weekly/monthly/hourly/whatever VWAP.

In v2:

option to color bars

average percentual difference of custom period

histogram changes color depending on which levels it's at

Levels/period/color etc can be customized.

Use these inputs in the timeframe box:

M - month

W - week

D - day

2D (or 3W or 2M or whatever) = 2 Days (or three week or 2 months and so on)

60= 1 H

240= 4 H

5 = 5 min

and so on.

btw, vaguely remembering reading somewhere that the big players like to make their entry at 4% difference.

Dual Session VWAPs by GK snipervwaps automatically

for london

new york session

easy

will remove automatically next day

VWAP-Anchored MACD [BOSWaves]VWAP-Anchored MACD - Volume-Weighted Momentum Mapping With Zero-Line Filtering

Overview

The VWAP-Anchored MACD delivers a refined momentum model built on volume-weighted price rather than raw closes, giving you a more grounded view of trend strength during sessions, weeks, or months.

Instead of tracking two EMAs of price like a standard MACD, this tool reconstructs the MACD engine using anchored VWAP as the core input. The result is a momentum structure that reacts to real liquidity flow, filters out weak crossovers near the zero line, and visualizes acceleration shifts with clear, high-contrast gradients.

This indicator acts as a precise momentum map that adapts in real time. You see how weighted price is accelerating, where valid crossovers form, and when trend conviction is strong enough to justify execution.

It uses gradient line coloring to show bullish or bearish momentum, histogram shading to highlight energy shifts, cross dots to mark valid crossovers, optional buy/sell diamonds for execution cues, and candle coloring to display trend strength at a glance.

Theoretical Foundation

Traditional MACD compares the difference between two exponential moving averages of price.

This variant replaces price with anchored VWAP, making the calculation sensitive to actual traded volume across your chosen period (Session, Week, or Month).

Three principles drive the logic:

Anchored VWAP Momentum : Price is weighted by volume and aggregated across the selected anchor. The fast and slow VWAP-EMAs then expose how liquidity-corrected momentum is expanding or contracting.

Zero-Line Distance Filtering : Crossover signals that occur too close to the zero line are removed. This eliminates the common MACD problem of generating weak, directionless signals in choppy phases.

Directional Visualization : MACD line, signal line, histogram, candle colors, and optional diamond markers all react to shifts in VWAP-momentum, giving you a clean structural read on market pressure.

Anchoring VWAP to session, weekly, or monthly resets creates a systematic framework for tracking how capital flow is driving momentum throughout each trading cycle.

How It Works

The core engine processes momentum through several mapped layers:

VWAP Aggregation : Price × volume is accumulated until the anchor resets. This creates a continuous, liquidity-corrected VWAP curve.

MACD Construction : Fast and slow VWAP-EMAs define the MACD line, while a smoothed signal line identifies edges where momentum shifts.

Zero-Line Distance Filter : MACD and signal must both exceed a threshold distance from zero for a crossover to count as valid. This prevents fake crossovers during compression.

Visual Momentum Layers : It uses gradient line coloring to show bullish or bearish momentum, histogram shading to highlight energy shifts, cross dots to mark valid crossovers, optional buy/sell diamonds for execution cues, and candle coloring to display trend strength at a glance.

This layered structure ensures you always know whether momentum is strengthening, fading, or transitioning.

Interpretation

You get a clean, structural understanding of VWAP-based momentum:

Bullish Phases : MACD > Signal, histogram expands, candles turn bullish, and crossovers occur above the threshold.

Bearish Phases : MACD < Signal, histogram drives lower, candles shift bearish, and downward crossovers trigger below the threshold.

Neutral/Compression : Both lines remain near the zero boundary, histogram flattens, and signals are suppressed to avoid noise.

This creates a more disciplined version of MACD momentum reading - less noise, more conviction, and better alignment with liquidity.

Strategy Integration

Trend Continuation : Use VWAP-MACD crossovers that occur far from the zero line as higher-conviction entries.

Zero-Line Rejection : Watch for histogram contractions near zero to anticipate flattening momentum and potential reversal setups.

Session/Week/Month Anchors : Session anchor works best for intraday flows. Weekly or monthly anchor structures create cleaner macro momentum reads for swing trading.

Signal-Only Execution : Optional buy/sell diamonds give you direct points to trigger trades without overanalyzing the chart.

This indicator slots cleanly into any momentum-following system and offers higher signal quality than classic MACD variants due to the volume-weighted core.

Technical Implementation Details

VWAP Reset Logic : Session (D), Week (W), or Month (M)

Dynamic Fast/Slow VWAP EMAs : Fully configurable lengths, smoothing and anchor settings

MACD/Signal Line Framework : Traditional structure with volume-anchored input

Zero-Line Filtering : Adjustable threshold for structural confirmation

Dual Visualization Layers : MACD body + histogram + crosses + candle coloring

Optimized Performance : Lightweight, fast rendering across all timeframes

Optimal Application Parameters

Timeframes:

1- 15 min : Short-term momentum scalping and rapid trend shifts

30- 240 min : Balanced momentum mapping with clear structural filtering

Daily : Macro VWAP regime identification

Suggested Configuration:

Fast Length : 12

Slow Length : 26

Signal Length : 9

Zero Threshold : 200 - 500 depending on asset range

These suggested parameters should be used as a baseline; their effectiveness depends on the asset volatility, liquidity, and preferred entry frequency, so fine-tuning is expected for optimal performance.

Performance Characteristics

High Effectiveness:

Assets with strong intraday or session-based volume cycles

Markets where volume-weighted momentum leads price swings

Trend environments with strong acceleration

Reduced Effectiveness:

Ultra-choppy markets hugging the VWAP axis

Sessions with abnormally low volume

Ranges where MACD naturally compresses

Disclaimer

The VWAP-Anchored MACD is a structural momentum tool designed to enhance directional clarity - not a guaranteed predictor. Performance depends on market regime, volatility, and disciplined execution. Use it alongside broader trend, volume, and structural analysis for optimal results.

VWAP Momentum Oscillator How It Works

Core Calculation Method

The oscillator combines four key market measurements into a single, normalized reading:

1. Price-VWAP Deviation: `(Close - VWAP) / VWAP × 100`

2. VWAP-MA Momentum: `(VWAP - MovingAverage) / MovingAverage × 100`

3. Anchored VWAP Strength: Average of high/low anchor deviations from rolling VWAP

4. Range Position: `(Close - PeriodLow) / (PeriodHigh - PeriodLow) × 100 - 50`

Dynamic Signal Line

The signal line uses an EMA that automatically adjusts its length based on your chart timeframe:

- Futures: Always covers 23 hours of trading (1,380 minutes)

- Stocks: Always covers 6.5 hours of trading (390 minutes)

- Examples: 276 periods on 5-min futures chart, 1,380 periods on 1-min futures chart

Trading Signals

🟢 Buy Signals

- Condition: Main oscillator crosses above signal line while below zero

- Logic: Momentum turning bullish from oversold conditions

- Visual: Green "BUY" label below price action

🔴 Sell Signals

- Condition: Main oscillator crosses below signal line while above zero

- Logic: Momentum turning bearish from overbought conditions

- Visual: Red "SELL" label above price action

⚠️ Extreme Warnings

- Extreme Overbought: Red triangle when oscillator crosses above +4.0

- Extreme Oversold: Green triangle when oscillator crosses below -4.0

- Purpose: Risk management alerts, not entry/exit signals

Oscillator Zones

Interpretation Guide

- Above +2.0: Strong bullish momentum zone (green background)

- 0 to +2.0: Mild bullish territory

- 0 to -2.0: Mild bearish territory

- Below -2.0: Strong bearish momentum zone (red background)

- Above +4.0: Extreme overbought (caution advised)

- Below -4.0: Extreme oversold (potential reversal zone)

Customization Options

Moving Average Settings

- EMA/SMA Toggle: Choose between exponential or simple moving average

- Color Customization: Adjust MA line color and width

Visual Controls

- Bullish/Bearish Colors: Customize momentum zone colors

- Signal Line: Toggle visibility and adjust color

- Line Widths: Control thickness of all plot lines

Anchor Modes

- NY Session Only: Anchors reset at NY market open (9:30 AM ET)

- 24H NY Day: Anchors reset at NY calendar day change (midnight ET)

Best Practices

Timeframe Selection

- Scalping: 1-5 minute charts for quick momentum changes

- Day Trading: 5-15 minute charts for clearer trend signals

- Swing Trading: 1-4 hour charts for major momentum shifts

Signal Confirmation

- Wait for crossovers: Don't trade on oscillator position alone

- Respect extreme levels: Exercise caution above +4 or below -4

- Use with price action: Combine with support/resistance levels

Risk Management

- Extreme zones: Reduce position size when oscillator is extended

- Failed signals: Exit quickly if momentum doesn't follow through

- Market context: Consider overall trend direction and market volatility

Technical Specifications

Calculation Components

- Base Length: 1,380 periods (futures) / 390 periods (stocks)

- Signal Line: Dynamic EMA covering one full trading day

- Smoothing: 3-period SMA on raw oscillator (adjustable)

- Update Frequency: Real-time on every price tick

Performance Notes

- Resource Efficient: Optimized calculations minimize CPU usage

- Memory Friendly: Uses incremental VWAP calculations

- Fast Loading: Minimal historical data requirements

Version History & Development

This oscillator evolved from advanced VWAP overlay strategies, transforming complex multi-line analysis into a single, actionable momentum gauge. The indicator maintains the sophistication of institutional VWAP analysis while providing the clarity needed for retail trading decisions.

Core Philosophy

Traditional VWAP indicators show where price is relative to volume-weighted averages, but they don't quantify momentum or provide clear entry/exit signals. This oscillator solves that problem by normalizing all VWAP relationships into a single, bounded indicator that works consistently across all timeframes and asset classes.

---

Open Source License: This indicator is provided free for the TradingView community. Feel free to modify and enhance according to your trading needs.

Dynamic Swing Anchored VWAP STRAT (Zeiierman/PineIndicators)Dynamic Swing Anchored VWAP STRATEGY — Zeiierman × PineIndicators (Pine Script v6)

A pivot-to-pivot Anchored VWAP strategy that adapts to volatility, enters long on bullish structure, and closes on bearish structure. Built for TradingView in Pine Script v6.

Full credits to zeiierman.

Repainting notice: The original indicator logic is repainting. Swing labels (HH/HL/LH/LL) are finalized after enough bars have printed, so labels do not occur in real time. It is not possible to execute at historical label points. Treat results as educational and validate with Bar Replay and paper trading before considering any discretionary use.

Concept

The script identifies swing highs/lows over a user-defined lookback ( Swing Period ). When structure flips (most recent swing low is newer than the most recent swing high, or vice versa), a new regime begins.

At each confirmed pivot, a fresh Anchored VWAP segment is started and updated bar-by-bar using an EWMA-style decay on price×volume and volume.

Responsiveness is controlled by Adaptive Price Tracking (APT) . Optionally, APT auto-adjusts with an ATR ratio so that high volatility accelerates responsiveness and low volatility smooths it.

Longs are opened/held in bullish regimes and closed when the regime turns bearish. No short positions are taken by design.

How it works (under the hood)

Swing detection: Uses ta.highestbars / ta.lowestbars over prd to update swing highs (ph) and lows (pl), plus their bar indices (phL, plL).

Regime logic: If phL > plL → bullish regime; else → bearish regime. A change in this condition triggers a re-anchor of the VWAP at the newest pivot.

Adaptive VWAP math: APT is converted to an exponential decay factor ( alphaFromAPT ), then applied to running sums of price×volume and volume, producing the current VWAP estimate.

Rendering: Each pivot-anchored VWAP segment is drawn as a polyline and color-coded by regime. Optional structure labels (HH/HL/LH/LL) annotate the swing character.

Orders: On bullish flips, strategy.entry("L") opens/maintains a long; on bearish flips, strategy.close("L") exits.

Inputs & controls

Swing Period (prd) — Higher values identify larger, slower swings; lower values catch more frequent pivots but add noise.

Adaptive Price Tracking (APT) — Governs the VWAP’s “half-life.” Smaller APT → faster/closer to price; larger APT → smoother/stabler.

Adapt APT by ATR ratio — When enabled, APT scales with volatility so the VWAP speeds up in turbulent markets and slows down in quiet markets.

Volatility Bias — Tunes the strength of APT’s response to volatility (above 1 = stronger effect; below 1 = milder).

Style settings — Colors for swing labels and VWAP segments, plus line width for visibility.

Trade logic summary

Entry: Long when the swing structure turns bullish (latest swing low is more recent than the last swing high).

Exit: Close the long when structure turns bearish.

Position size: qty = strategy.equity / close × 5 (dynamic sizing; scales with account equity and instrument price). Consider reducing the multiplier for a more conservative profile.

Recommended workflow

Apply to instruments with reliable volume (equities, futures, crypto; FX tick volume can work but varies by broker).

Start on your preferred timeframe. Intraday often benefits from smaller APT (more reactive); higher timeframes may prefer larger APT (smoother).

Begin with defaults ( prd=50, APT=20 ); then toggle “Adapt by ATR” and vary Volatility Bias to observe how segments tighten/loosen.

Use Bar Replay to watch how pivots confirm and how the strategy re-anchors VWAP at those confirmations.

Layer your own risk rules (stops/targets, max position cap, session filters) before any discretionary use.

Practical tips

Context filter: Consider combining with a higher-timeframe bias (e.g., daily trend) and using this strategy as an entry timing layer.

First pivot preference: Some traders prefer only the first bullish pivot after a bearish regime (and vice versa) to reduce whipsaw in choppy ranges.

Deviations: You can add VWAP deviation bands to pre-plan partial exits or re-entries on mean-reversion pulls.

Sessions: Session-based filters (RTH vs. ETH) can materially change behavior on futures and equities.

Extending the script (ideas)

Add stops/targets (e.g., ATR stop below last swing low; partial profits at k×VWAP deviation).

Introduce mirrored short logic for two-sided testing.

Include alert conditions for regime flips or for price-VWAP interactions.

Incorporate HTF confirmation (e.g., only long when daily VWAP slope ≥ 0).

Throttle entries (e.g., once per regime flip) to avoid over-trading in ranges.

Known limitations

Repainting: Swing labels and pivot confirmations depend on future bars; historical labels can look “perfect.” Treat them as annotations, not executable signals.

Execution realism: Strategy includes commission and slippage fields, yet actual fills differ by venue/liquidity.

No guarantees: Past behavior does not imply future results. This publication is for research/education only and not financial advice.

Defaults (backtest environment)

Initial capital: 10,000

Commission value: 0.01

Slippage: 1

Overlay: true

Max bars back: 5000; Max labels/polylines set for deep swing histories

Quick checklist

Add to chart and verify that the instrument has volume.

Use defaults, then tune APT and Volatility Bias with/without ATR adaptation.

Observe how each pivot re-anchors VWAP and how regime flips drive entries/exits.

Paper trade across several symbols/timeframes before any discretionary decisions.

Attribution & license

Original indicator concept and logic: Zeiierman — please credit the author.

Strategy wrapper and publication: PineIndicators .

License: CC BY-NC-SA 4.0 (Attribution-NonCommercial-ShareAlike). Respect the license when forking or publishing derivatives.

Anchored VWAP by Fin VirajSimple Anchored VWAP with Directional Colors

📊 Overview

A clean and efficient Anchored VWAP (Volume Weighted Average Price) indicator with dynamic directional coloring. This indicator provides traders with a reliable reference point for price action analysis based on volume-weighted calculations from specific anchor points.

✨ Key Features

🎯 Multiple Anchor Types

Session: Anchors to daily trading session start

Day: Resets at the beginning of each trading day

Week: Weekly anchor points for swing trading

Month: Monthly anchors for longer-term analysis

Manual Date: Set custom anchor date for specific events

🌈 Directional Color System

🟢 Green: Price above VWAP with upward momentum

🔴 Red: Price below VWAP with downward momentum

🔵 Blue: Neutral/transitional conditions

📏 Standard Deviation Bands

Customizable multipliers (default: 1.0 and 2.0)

Toggle on/off as needed

Support and resistance levels based on statistical deviation

Filled area between bands for better visualization

🔧 Settings & Customization

Input Parameters

Anchor Type: Choose from 5 different anchor methods

Manual Anchor Date: Set specific date for manual anchoring

Reset Anchor Point: Manual reset button

Show Standard Deviation Bands: Toggle bands visibility

Band Multipliers: Adjust band distance (1σ and 2σ)

VWAP Line Width: Customize line thickness (1-4)

Color Customization

Bullish Color: Customize uptrend color

Bearish Color: Customize downtrend color

Neutral Color: Customize neutral state color

Band Color: Customize standard deviation bands color

📈 How to Use

For Day Trading

Set anchor type to "Session" or "Day"

Use VWAP as dynamic support/resistance

Green color = bullish bias, Red color = bearish bias

For Swing Trading

Set anchor type to "Week" or "Month"

Longer-term VWAP acts as major S/R level

Standard deviation bands show potential reversal zones

For Event-Based Analysis

Set anchor type to "Manual Date"

Choose significant event date (earnings, news, etc.)

Analyze price behavior relative to that anchor point

🎨 Visual Interpretation

VWAP Line Colors

Bright Green: Strong bullish momentum (price above rising VWAP)

Bright Red: Strong bearish momentum (price below falling VWAP)

Blue: Neutral conditions or transitional phase

Standard Deviation Bands

Upper Bands: Potential resistance levels

Lower Bands: Potential support levels

Band Touches: Often indicate reversal or continuation points

💡 Trading Applications

Support & Resistance

VWAP acts as dynamic support in uptrends

VWAP acts as dynamic resistance in downtrends

Standard deviation bands provide additional S/R levels

Trend Analysis

Price consistently above VWAP = bullish trend

Price consistently below VWAP = bearish trend

Color changes help identify trend shifts

Entry & Exit Points

Use VWAP reclaims for potential long entries

Use VWAP breaks for potential short entries

Standard deviation bands for profit-taking levels

⚙️ Technical Details

Pine Script Version: v6

Overlay: Yes (plots on price chart)

Calculation: Volume-weighted average price from anchor point

Standard Deviation: Statistical measure of price dispersion

Performance: Optimized for real-time calculation

🔄 Anchor Reset Logic

The indicator automatically resets based on selected anchor type:

Session/Day: Resets at market open

Week: Resets at week start

Month: Resets at month start

Manual: Resets from chosen date

Manual Reset: Override button for immediate reset

📋 Best Practices

Choose appropriate timeframe for your anchor type

Combine with volume analysis for better confirmation

Use multiple timeframes for comprehensive analysis

Consider market context when interpreting signals

Test on demo before live trading

⚠️ Disclaimer

This indicator is for educational and informational purposes only. Always conduct your own analysis and risk management before making trading decisions.

VWAP Periodic Close [LuxAlgo]The VWAP Periodic Close script offers an advanced tool for analyzing the Volume Weighted Average Price (VWAP) across various timeframes.

This tool enables traders to visualize VWAP close levels for daily, weekly, monthly, quarterly, and yearly periods, offering a comprehensive view of price behavior across different time frames. It helps in identifying key levels where the VWAP closes at the end of each specified period.

🔶 USAGE

This script is designed to enhance your trading strategy by plotting VWAP close levels on your chart for different time periods. This helps traders easily identify historical VWAP levels and analyze price action relative to these levels, particularly useful for identifying key support and resistance levels providing insights into potential future price behavior.

Supports VWAP closes for multiple timeframes, including historical periods (e.g., 3 months back, 3 quarters back, 3 years back). The labels provide context and detailed information about the VWAP close at a specific point in time and enhance the clarity and usefulness of the VWAP data presented on the chart.

Users can toggle the display of VWAP lines for different periods and customize the colors for each timeframe (e.g., distinct colors for monthly, quarterly, and yearly closes).

🔶 SETTINGS

The script offers a range of customizable settings to tailor the analysis to your trading needs.

🔹 Volume Weighted Average Price (VWAP)

VWAP Close Level: Toggle the display of VWAP levels at the end of each period (daily, weekly, monthly, quarterly, yearly).

VWAP Origin: Toggle the display of the VWAP line for each period.

VWAP Source: Choose the data source for VWAP calculations (default is HLC3).

Historical Closes: Define the number of historical VWAP levels to plot.

Line/Label Offset: Adjust the offset for positioning lines and labels on the chart.

🔹 Themes

Theme Selection: Choose between "Day," "Night," or "Custom" themes to adjust the color scheme of VWAP lines and labels.

Neural Adaptive VWAPNeural Adaptive VWAP with ML Features is an advanced trading indicator that enhances traditional Volume Weighted Average Price (VWAP) calculations through machine learning-inspired adaptive algorithms and predictive volume modeling.

🌟 Key Features:

🧠 Machine Learning-Inspired Adaptation

Dynamic weight adjustment system that learns from prediction errors

Multi-feature volume prediction using time-of-day patterns, price momentum, and volatility

Adaptive learning mechanism that improves accuracy over time

📊 Enhanced VWAP Calculation

Combines actual and predicted volume for forward-looking VWAP computation

Session-based reset with proper daily anchoring

Confidence bands based on rolling standard deviation for dynamic support/resistance

🎯 Advanced Signal Generation

Volume-confirmed crossover signals to reduce false entries

Color-coded candle visualization based on VWAP position

Multi-level strength indicators (strong/weak bullish/bearish zones)

⚙️ Intelligent Feature Engineering

Normalized volume analysis with statistical z-score

Time-series pattern recognition for intraday volume cycles

Price momentum and volatility integration

Sigmoid activation functions for realistic predictions

📈 How It Works:

The indicator employs a sophisticated feature engineering approach that extracts meaningful patterns from:

Volume Patterns: Normalized volume analysis and historical comparisons

Temporal Features: Time-of-day and minute-based cyclical patterns

Market Dynamics: Price momentum, volatility, and rate of change

Adaptive Learning: Error-based weight adjustment similar to neural network training

Unlike static VWAP indicators, this system continuously adapts its calculation methodology based on real-time market feedback, making it more responsive to changing market conditions while maintaining the reliability of traditional VWAP analysis.

🔧 Customizable Parameters:

VWAP Length (1-200 bars)

Volume Pattern Lookback (5-50 periods)

Learning Rate (0.001-0.1) for adaptation speed

Prediction Horizon (1-10 bars ahead)

Adaptation Period for weight updates

📊 Visual Elements:

Blue Line: Adaptive VWAP with predictive elements

Red/Green Bands: Dynamic confidence zones

Colored Candles: Position-based strength visualization

Signal Arrows: Volume-confirmed entry points

Info Table: Real-time performance metrics and weight distribution

🎯 Best Use Cases:

Intraday Trading: Enhanced execution timing with volume prediction

Institutional-Style Execution: Improved VWAP-based order placement

Trend Following: Adaptive trend identification with confidence zones

Support/Resistance Trading: Dynamic levels that adjust to market conditions

VWAP Direction HistogramThe ** VWAP Direction Histogram ** indicator is a powerful tool for traders looking to gauge the directional bias of the Volume Weighted Average Price (VWAP). VWAP is a critical metric that combines price and volume to provide a weighted average price, often used to identify institutional trading activity and support/resistance levels. This indicator builds upon the traditional VWAP by calculating its directional changes over a customizable lookback period, providing clear visual cues to traders through a color-coded histogram.

By identifying whether VWAP is rising or falling over the specified lookback period, this indicator helps traders determine the prevailing trend bias in the market. A positive VWAP direction suggests upward momentum and a bullish trend bias, while a negative direction indicates downward momentum and bearish sentiment. This information is further reinforced by coloring the chart candles based on the VWAP trend, enabling quick visual analysis and enhancing decision-making for trend-following strategies. Whether you're trading intraday or longer-term, the ** VWAP Direction Histogram ** offers an intuitive and effective way to align your trades with market trends.

Distance from Vwap// How it Works \\

Measuring the distance of the close price from a higher timeframe VWAP - Volume Weighted Average Price

There is a threshold which is calculated by looking back at the previous x amount of bars and storing the highest/lowest values

If the distance from the vwap stretches above that threshold, the histogram will go green if price is above VWAP and red if its below the vwap

If the distance from the vwap reaches below the low threshold you will see the histogram flashes orange

// Settings \\

In the settings you have the ability to change what timeframe the indicator is calculated on, as well as this you can change the timeframe the VWAP is calculated on.

I always recommend using a higher timeframe vwap as they tend to me more respected

e.g on the hourly timeframe, I use the weekly VWAP, on 1 minute timeframe you may want to use 4 hour timeframe but obviously feel free to experiment

// Use Case \\

When histogram is flashing green, prices is pulling far away from the vwap, obviously you don't want to be buying a falling knife but if you have levels of confluence this can help spot reversals.

I personally wait until the first candle after its been green to get confirmation of the fall weakening. Vica versa for reds and shorts/sells.

When you see orange flashes, this shows that price has been consolidating and the price is very close to the higher time frame VWAP which could be considered a safe entry point as they tend to lead to a big move to follow

// Suggestions \\

Happy for anyone to make any suggestions on changes which could improve the script,

// Terms \\

Feel free to use the script, If you do use the script could you please just tag me as I am interested to see how people are using it. Good Luck!

VWAP Multiple [Huntersull]This is a VWAP/Price multiple analysis, in the same vein as something like the Mayer multiple.

It finds the VWAP of price and volume starting at the bar you choose when initiating the script (You can also drag the starting point line on the chart to change it later), and calculates the running VWAP total for every following bar until the current bar.

It then takes the hlc3 of price for each bar and divides it by the VWAP value of that bar, giving a multiple over VWAP price.

This is then charted with your choice of an SMA, EMA, or WMA using VWAP as the source, and a default length of 200, which is also modifiable.

When VWAP is over the moving average, it is filled green. When VWAP is below the moving average, it is filled red.

--------------------------------------------

This is not meant to be a trading indicator, but a tool for general bull/bear market and trend analysis. Use at your own risk.

Multiple Anchored VWAP [Morty]The Anchored VWAP (aVWAP) indicator ties VWAP calculations to a specific price bar chosen by the trader. Anchored VWAP allows you to specify the price bar where calculations begin, making it easy to see whether the bulls or bears have been in charge since a very specific point in time. The starting price bar that is chosen generally marks a shift in market psychology, such as a significant high or low, earnings, news, or other announcements. The Anchored VWAP line is charted using price and volume data from that significant event onward.

This indicator plots up to 4 aVWAP lines in the chart.

Features:

- plot up to 4 aVWAP lines

- custom start date of aVWAP

- custom line color

- optional label of starting price bar

- optional custom resolution

----------------------------------------------------

锚定VWAP(aVWAP)指标将VWAP的计算与交易者选择的特定价格柱联系起来。锚定VWAP允许你指定计算开始的价格柱,使你很容易看到自一个非常具体的时间点以来,是牛市还是熊市在起作用。所选择的起始价格条通常标志着市场心理的转变,如一个重要的高点或低点、收益、新闻或其他公告。锚定VWAP线是使用从该重大事件开始的价格和成交量数据绘制的。

该指标在图表中最多绘制了4条aVWAP线。

特色:

- 绘制多达4条aVWAP线

- 自定义aVWAP的开始日期

- 自定义线的颜色

- 可选的起始价格条的标签

- 可选的自定义分辨率

VWAP BB Breakout + DMI MomentumI decided to code a single indicator that has some of my most used indicators.

I encourage that you have read up on VWAP, Bollinger Bands, ADX/DMI to understand how they function.

VWAP + Bollinger 1σ Breakout + DMI/ADX Scalping Strategy (NASDAQ)

This strategy is designed for single-chart, intraday scalping on the NASDAQ, focusing on volatility expansion in the direction of market control. It avoids higher-timeframe confirmation to eliminate lag and reacts only when price shows acceptance and momentum.

Core Concepts

VWAP defines market control and trade direction

Bollinger Bands (20, 1σ) identify early volatility expansion

DMI/ADX (10 / 5) confirms directional momentum and strength

The strategy trades breakouts that are supported by both bias and momentum, filtering out low-quality moves and chop.

Trade Rules

Long Setup

Price is above VWAP

Candle closes above the upper Bollinger 1σ band

+DI > –DI

ADX rising or above strength threshold

Short Setup

Price is below VWAP

Candle closes below the lower Bollinger 1σ band

–DI > +DI

ADX rising or above strength threshold

Trades are taken only on candle close to confirm acceptance.

Risk & Trade Management

Trades are avoided near VWAP to reduce chop

Stops are placed just inside the Bollinger 20 SMA or beyond the breakout candle

Partial profits can be taken at the 2σ band

Exits are considered when ADX flattens or DMI flips

Market Conditions

Best suited for:

High-liquidity sessions (NY open and main session)

Trending or expanding volatility environments

Avoid during:

Flat VWAP conditions

Bollinger Band compression

Low ADX / range-bound markets

Strategy Philosophy

This is a reactive momentum strategy, not predictive.

It waits for price to prove direction and strength, then participates in the move rather than anticipating it.

Moving VWAP-KAMA CloudMoving VWAP-KAMA Cloud

Overview

The Moving VWAP-KAMA Cloud is a high-conviction trend filter designed to solve a major problem with standard indicators: Noise. By combining a smoothed Volume Weighted Average Price (MVWAP) with Kaufman’s Adaptive Moving Average (KAMA), this indicator creates a "Value Zone" that identifies the true structural trend while ignoring choppy price action.

Unlike brittle lines that break constantly, this cloud is "slow" by design—making it exceptionally powerful for spotting genuine trend reversals and filtering out fakeouts.

How It Works

This script uses a unique "Double Smoothing" architecture:

The Anchor (MVWAP): We take the standard VWAP and smooth it with a 30-period EMA. This represents the "Fair Value" baseline where volume has supported price over time.

The Filter (KAMA): We apply Kaufman's Adaptive Moving Average to the already smoothed MVWAP. KAMA is unique because it flattens out during low-volatility (choppy) periods and speeds up during high-momentum trends.

The Cloud:

Green/Teal Cloud: Bullish Structure (MVWAP > KAMA)

Purple Cloud: Bearish Structure (MVWAP < KAMA)

🔥 The "Reversal Slingshot" Strategy

Backtests reveal a powerful behavior during major trend changes, particularly after long bear markets:

The Resistance Phase: During a long-term downtrend, price will repeatedly rally into the Purple Cloud and get rejected. The flattened KAMA line acts as a "concrete ceiling," keeping the bearish trend intact.

The Breakout & Flip: When price finally breaks above the cloud with conviction, and the cloud flips Green, it signals a structural regime change.

The "Slingshot" Retest: Often, immediately after this flip, price will drop back into the top of the cloud. This is the "Slingshot" moment. The old resistance becomes new, hardened support.

The Rally: From this support bounce, stocks often launch into a sustained, multi-month bull run. This setup has been observed repeatedly at the bottom of major corrections.

How to Use This Indicator

1. Dynamic Support & Resistance

The KAMA Wall: When price retraces into the cloud, the KAMA line often flattens out, acting as a hard "floor" or "wall." A break of this wall usually signals a genuine trend change, not just a stop hunt.

2. Trend Confirmation (Regime Filter)

Bullish Regime: If price is holding above the cloud, only look for Long setups.

Bearish Regime: If price is holding below the cloud, only look for Short setups.

No-Trade Zone: If price is stuck inside the cloud, the market is traversing fair value. Stand aside until a clear winner emerges.

3. Multi-Timeframe Versatility

While designed for trend confirmation on higher timeframes (4H, Daily), this indicator adapts beautifully to lower timeframes (5m, 15m) for intraday scalping.

On Lower Timeframes: The cloud reacts much faster, acting as a dynamic "VWAP Band" that helps intraday traders stay on the right side of momentum during the session.

Settings

Moving VWAP Period (30): The lookback period for the base VWAP smoothing.

KAMA Settings (10, 10, 30): Controls the sensitivity of the adaptive filter.

Cloud Transparency: Adjust to keep your chart clean.

Alerts Included

Price Cross Over/Under MVWAP

Price Cross Over/Under KAMA

Cloud Flip (Bullish/Bearish Trend Change)

Tip for Traders

This is not a signal entry indicator. It is a Trend Conviction tool. Use it to filter your entries from faster indicators (like RSI or MACD). If your fast indicator signals "Buy" but the cloud is Purple, the probability is low. Wait for the Cloud Flip

Simple VWAP + BandsSimple VWAP + Bands

A clean and customizable VWAP (Volume Weighted Average Price) indicator with standard deviation bands and RTH (Regular Trading Hours) session support.

Features:

- VWAP Line: Volume-weighted average price calculation

- Three Standard Deviation Bands: Configurable bands at 1σ, 2σ, and 3σ levels (above and below VWAP)

- RTH Session Support: Option to calculate VWAP only during regular trading hours

- Customizable Session Times: Configure your own trading session hours and timezone

- Clean Visualization: Line breaks between sessions prevent messy connections across non-trading periods

- Toggle Bands: Show/hide individual standard deviation bands as needed

Use Cases:

- Identify overbought/oversold conditions relative to volume-weighted price

- Track price deviation from VWAP during trading sessions

- Support and resistance levels based on standard deviations

- Mean reversion trading strategies

Kalman Based VWAP [EdgeTerminal]Kalman VWAP is a different take on volume-weighted average price (VWAP) indicator where we enhance the results with Kalman filtering and dynamic wave visualization for a more smooth and improved trend identification and volatility analysis.

A little bit about Kalman Filter:

Kalman filtering (also known as linear quadratic estimation) is an algorithm that uses a series of measurements observed over time, including statistical noise and other inaccuracies, to produce estimates of unknown variables that tend to be more accurate than those based on a single measurement, by estimating a joint probability distribution over the variables for each time-step. The filter is constructed as a mean squared error minimiser, but an alternative derivation of the filter is also provided showing how the filter relates to maximum likelihood statistics

This indicator combines:

Volume-Weighted Average Price (VWAP) for institutional price levels

Kalman filtering for noise reduction and trend smoothing

Dynamic wave visualization for volatility zones

This creates a robust indicator that helps traders identify trends, support/resistance zones, and potential reversal points with high precision.

What makes this even more special is the fact that we use open price as a data source instead of usual close price. This allows you to tune the indicator more accurately when back testing it and generally get results that are closer to real time market data.

The math:

In case if you're interested in the math of this indicator, the indicator employs a state-space Kalman filter model:

State Equation: x_t = x_{t-1} + w_t

Measurement Equation: z_t = x_t + v_t

x_t is the filtered VWAP state

w_t is process noise ~ N(0, Q)

v_t is measurement noise ~ N(0, R)

z_t is the traditional VWAP measurement

The Kalman filter recursively updates through:

Prediction: x̂_t|t-1 = x̂_{t-1}

Update: x̂_t = x̂_t|t-1 + K_t(z_t - x̂_t|t-1)

Where K_t is the Kalman gain, optimally balancing between prediction and measurement.

Input Parameters

Measurement Noise: Controls signal smoothing (0.0001 to 1.0)

Process Noise: Adjusts trend responsiveness (0.0001 to 1.0)

Wave Size: Multiplier for volatility bands (0.1 to 5.0)

Trend Lookback: Period for trend determination (1 to 100)

Bull/Bear Colors: Customizable color schemes

Application:

I recommend using this along other indicators. This is best used for assets that don't have a close time, such as BTC but can be used with anything as long as the data is there.

With default settings, this works better for swing trades but you can adjust it for day trading as well, by adjusting the lookback and also process noise.