EMA Percentile Rank [SS]Hello!

Excited to release my EMA percentile Rank indicator!

What this indicator does

Plots an EMA and colors it by short-term trend.

When price crosses the EMA (up or down) and remains on that side for three subsequent bars, the cross is “confirmed.”

At the moment of the most recent cross, it anchors a reference price to the crossover point to ensure static price targets.

It measures the historical distance between price and the EMA over a lookback window, separately for bars above and below the EMA.

It computes percentile distances (25%, 50%, 85%, 95%, 99%) and draws target bands above/below the anchor.

Essentially what this indicator does, is it converts the raw “distance from EMA” behavior into probabilistic bands and historical hit rates you can use for targets, stop placement, or mean-reversion/continuation decisions.

Indicator Inputs

EMA length: Default is 21 but you can use any EMA you prefer.

Lookback: Default window is 500, this is length that the percentiles are calculated. You can increase or decrease it according to your preference and performance.

Show Accumulation Table: This allows you to see the table that shows the hits/price accumulation of each of the percentile ranges. UCL means upper confidence and LCL means lower confidence (so upper and lower targets).

About Percentiles

A percentile is a way of expressing the position of a value within a dataset relative to all the other values.

It tells you what percentage of the data points fall at or below that value.

For example:

The 25th percentile means 25% of the values are less than or equal to it.

The 50th percentile (also called the median) means half the values are below it and half are above.

The 99th percentile means only 1% of the values are higher.

Percentiles are useful because they turn raw measurements into context — showing how “extreme” or “typical” a value is compared to historical behavior.

In the EMA Percentile Rank indicator, this concept is applied to the distance between price and the EMA. By calculating percentile distances, the script can mark levels that have historically been reached often (low percentiles) or rarely (high percentiles), helping traders gauge whether current price action is stretched or within normal bounds.

Use Cases

The EMA Percentile Rank indicator is best suited for traders who want to quantify how far price has historically moved away from its EMA and use that context to guide decision-making.

One strong use case is target setting after trend shifts: when a confirmed crossover occurs, the percentile bands (25%, 50%, 85%, 95%, 99%) provide statistically grounded levels for scaling out profits or placing stops, based on how often price has historically reached those distances. This makes it valuable for traders who prefer data-driven risk/reward planning instead of arbitrary point targets. Another use case is identifying stretched conditions — if price rapidly tags the 95% or 99% band after a cross, that’s an unusually large move relative to history, which could signal exhaustion and prompt mean-reversion trades or protective actions.

Conversely, if the accumulation table shows price frequently resides in upper bands after bullish crosses, traders may anticipate continuation and hold positions longer . The indicator is also effective as a trend filter when combined with its EMA color-coding : only taking trades in the trend’s direction and using the bands as dynamic profit zones.

Additionally, it can support multi-timeframe confluence (if you align your chart to the timeframes of interest), where higher-timeframe trend direction aligns with lower-timeframe percentile behavior for higher-probability setups. Swing traders can use it to frame pullbacks — entering near lower percentile bands during an uptrend — while intraday traders might use it to fade extremes or ride breakouts past the median band. Because the anchor price resets only on EMA crosses, the indicator preserves a consistent reference for ongoing trades, which is especially helpful for managing swing positions through noise .

Overall, its strength lies in transforming raw EMA distance data into actionable, probability-weighted levels that adapt to the instrument’s own volatility and tendencies .

Summary

This indicator transforms a simple EMA into a distribution-aware framework: it learns how far price tends to travel relative to the EMA on either side, and turns those excursions into percentile bands and historical hit rates anchored to the most recent cross. That makes it a flexible tool for targets, stops, and regime filtering, and a transparent way to reason about “how stretched is stretched?”—with context from your chosen market and timeframe.

I hope you all enjoy!

And as always, safe trades!

Statistics

New Highs - MarkerDescription:

This indicator highlights every bar that sets a new high or matches the previous high.

New Highs (ATH or Lookback Highs) are marked with a green triangle above the candle.

Equal Highs (ties) are marked with an orange triangle above the candle.

You can choose between All-Time Highs (lookback = 0) or rolling lookback highs over a user-defined number of bars.

Alerts are included for both new highs and equal highs.

Use this tool to quickly spot breakouts or double-top style patterns as they form.

Break Point Record Table — GSK-VIZAG-AP-INDIA "Break Point Record Table — GSK-VIZAG-AP-INDIA" indicator captures key break points during each trading session and presents a clear, color-coded table overlay on the chart for quick visual reference. Specifically, it logs sessions' open price and monitors subsequent price action for notable breaks in the session high or low prices. Each break event is recorded with the time, price, and percentage change from the previous break, helping traders identify significant price movements within the session at a glance.

Key Features:

Records the session start time and opening price for context.

Tracks every intraday break above the previous session high or below the previous session low.

Calculates and displays the percentage change at each break event.

Highlights breaks with descriptive text including break time and values to aid trade decision-making.

Displays a table with columns for Time, Open, High, Low, and a Description of the event.

Uses color-coded cells to differentiate between session start, highs, lows, and break descriptions for better readability.

Maintains performance and readability by limiting the table to the latest 30 break events.

Usage & Benefits:

This indicator is ideal for intraday traders who want reliable visual cues to monitor momentum shifts and breakout/breakdown points during the trading day. By capturing these break points as discrete events and organizing the data into an easily accessible, visually intuitive table, it improves situational awareness and supports timely trading decisions.

SE – RSI Divergence Scanner (BOTH on 1h & 15m) – v6Screenar svenska mid/large cap bolag som har divergenser i 15 min och 1h timeframe samtidigt.

Relative Strength Heat [InvestorUnknown]The Relative Strength Heat (RSH) indicator is a relative strength of an asset across multiple RSI periods through a dynamic heatmap and provides smoothed signals for overbought and oversold conditions. The indicator is highly customizable, allowing traders to adjust RSI periods, smoothing methods, and visual settings to suit their trading strategies.

The RSH indicator is particularly useful for identifying momentum shifts and potential reversal points by aggregating RSI data across a range of periods. It presents this data in a visually intuitive heatmap, with color-coded bands indicating overbought (red), oversold (green), or neutral (gray) conditions. Additionally, it includes signal lines for overbought and oversold indices, which can be smoothed using RAW, SMA, or EMA methods, and a table displaying the current index values.

Features

Dynamic RSI Periods: Calculates RSI across 31 periods, starting from a user-defined base period and incrementing by a specified step.

Heatmap Visualization: Displays RSI strength as a color-coded heatmap, with red for overbought, green for oversold, and gray for neutral zones.

Customizable Smoothing: Offers RAW, SMA, or EMA smoothing for overbought and oversold signals.

Signal Lines: Plots scaled overbought (purple) and oversold (yellow) signal lines with a midline for reference.

Information Table: Displays real-time overbought and oversold index values in a table at the top-right of the chart.

User-Friendly Inputs: Allows customization of RSI source, period ranges, smoothing length, and colors.

How It Works

The RSH indicator aggregates RSI calculations across 31 periods, starting from the user-defined Starting Period and incrementing by the Period Increment. For each period, it computes the RSI and determines whether the asset is overbought (RSI > threshold_ob) or oversold (RSI < threshold_os). These states are stored in arrays (ob_array for overbought, os_array for oversold) and used to generate the following outputs:

Heatmap: The indicator plots 31 horizontal bands, each representing an RSI period. The color of each band is determined by the f_col function:

Red if the RSI for that period is overbought (>threshold_ob).

Green if the RSI is oversold (

Candle Range Theory 4H Blocks (New York Time)This is a script to those who mess up the CRT, Candle Range Theory, times to trade Forex and CFDs. It is simple and effective.

Average Daily Range TrackerAverage Daily Range Tracker

This indicator helps you measure volatility in real time by tracking the Average Daily Range (ADR) and comparing it to the current day’s price action.

🔑 Features

Calculates the ADR over a user-defined lookback period (default = 14 days).

Displays today’s developing range (High–Low) as the session unfolds.

Shows what % of the ADR has already been consumed intraday.

Visual progress bar makes it easy to see how close today is to its historical average range.

Optional ADR plot available in a separate pane.

📈 How traders use it

Spot when a market has already made its “typical” daily move.

Adjust intraday trade expectations: avoid chasing after the bulk of the move is done.

Use % of ADR consumed as a volatility filter for setups.

Combine with support/resistance to identify exhaustion zones.

⚙️ Customization

Lookback length for ADR calculation.

Progress bar size and color.

Optional toggle to plot ADR in its own panel.

Future 8 AM MarkerThis simple script marks the 8:00 AM New York open on the chart each day. It’s especially useful in Replay Mode to track price reactions and practice setups around this key time.

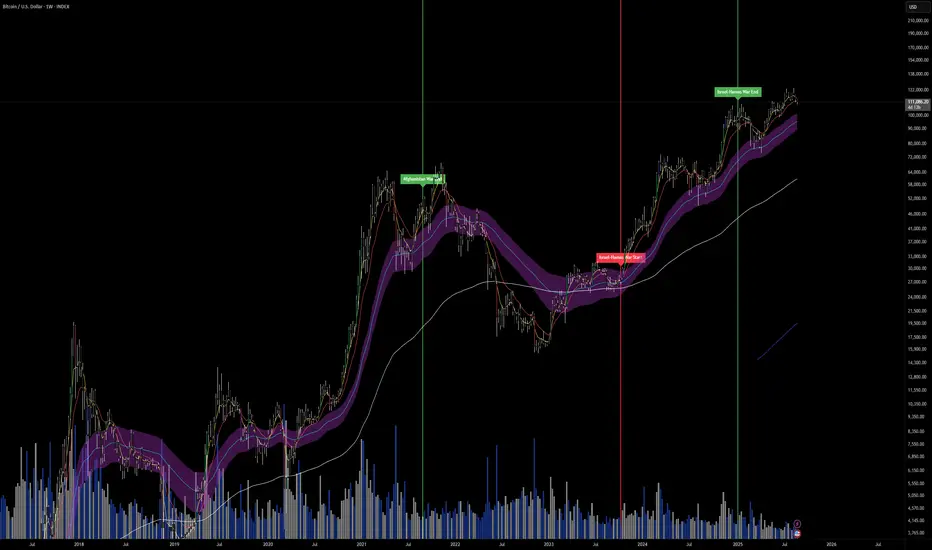

Major & Modern Wars TimelineDescription:

This indicator overlays vertical lines and labels on your chart to mark the start and end dates of major global wars and modern conflicts.

Features:

Displays start (red line + label) and end (green line + label) for each war.

Covers 20th century wars (World War I, World War II, Korean War, Vietnam War, Gulf War, Afghanistan, Iraq).

Includes modern conflicts: Syrian Civil War, Ukraine War, and Israel–Hamas War.

For ongoing conflicts, the end date is set to 2025 for timeline visualization.

Customizable: label position (above/below bar), line width.

Works on any chart timeframe, overlaying events on financial data.

Use case:

Useful for historical market analysis (e.g., gold, oil, S&P 500), helping traders and researchers see how wars and conflicts align with market movements.

Trading Stats BarSimple statistics bar designed to give important values for swing trading

Most of the values are self explanatory

Float Grade

Combines float and float % designed to give a sense if the stock has the potential to move quickly. If the float is less than 20 million and float % less than 50, this has a high potential to make fast moves.

Volume Run Rate

Concept is to focus on the opening x minutes and average this value over the previous y days

Timeframe Shift AlertIf the higher timeframe flips bullish, you’ll get a notification like:

“✅ Higher TF (240) just flipped from Bearish → Bullish”

• If it flips bearish, you’ll get:

“❌ Higher TF (240) just flipped from Bullish → Bearish”

Weekly pecentage tracker by PRIVATE

Settings Picture below this link: 👇

i.ibb.co

What it is

A lightweight “Weekly % Tracker” overlay that lets you manually enter weekly performance (in percent) for XAUUSD + up to 10 FX pairs, then shows:

a small table panel with each enabled symbol and its % result

one TOTAL row (Sum / Average / Compounded across all enabled symbols)

an optional mini badge showing the % for a single selected symbol

Nothing is auto-calculated from price—you type the % yourself.

Key settings

Panel: show/hide, position, number of decimals, colors (background, text, green/red).

Total mode:

Sum – adds percentages

Average – mean of enabled rows

Compounded –

(

∏

(

1

+

𝑝

/

100

)

−

1

)

×

100

(∏(1+p/100)−1)×100

Symbols:

XAUUSD (toggle + label + % input)

10 FX pairs (each has On/Off, label text, % input). You can rename labels to any symbol text you want.

Mini badge: show/hide, position, and symbol to display.

How it works

Overlay indicator: overlay=true; just draws UI on the chart (no plots).

Arrays (syms, vals, ons) collect the row data in order: XAU first, then FX1…FX10.

Helpers:

posFrom() converts a position string (e.g., “Top Right”) into a position.* constant.

wp_col() picks green/red/neutral based on the sign of the %.

wp_round() rounds values to the selected decimals.

calc_total() computes the TOTAL with the chosen mode over enabled rows only.

Table creation logic:

Counts how many rows are enabled.

If none enabled or panel is off: the panel table is deleted, so no box/background is visible.

If enabled and on: the panel is (re)created at the chosen position.

On each last bar (barstate.islast), it clears the table to transparent (bgcolor=na) and then fills one row per enabled symbol, followed by a single TOTAL row.

Mini badge:

Always (re)created on position change.

Shows selected symbol’s % (or “-” if that symbol isn’t enabled or has no value).

Colors text green/red by sign.

Notes & limits

It’s manual input—the script doesn’t read trades or P/L from price.

You can rename each row’s label to match any symbol name you want.

When no rows are enabled, the panel disappears entirely (no empty background).

Designed to be light: only draws tables; no heavy plotting.

If you want the TOTAL row to be optional, or different color thresholds, or CSV-style export/import of the values, say the word and I’ll add it.

Daily Weekly Monthly HLC (بهداد)خطوط مهم روزانه هفتگی ماهانه This is an indicator that shows the closing lines and the highest and lowest prices for daily, weekly and monthly periods. In addition, we can divide the entire weekly period into several parts.

Androlog DailyWeeklyMonthlyAndrologLevel — Daily / Weekly / Monthly Levels

This indicator visualizes the Daily, Weekly, and Monthly key levels introduced by Daniel. It’s intentionally minimal and fast, focused on clean higher‑timeframe references for intraday and daily trading.

What it shows:

Daily open and prior‑day high/low

Weekly and Monthly “open”-based levels

Optional labels for quick price readouts

Controls

Show only new levels or keep/extend old ones

Choose whether levels extend to the right

Alerts

Optional alert conditions for level touches (per your settings)

Uses confirmed higher‑timeframe bars; no historical repaint

Lunar calendar day Crypto Trading StrategyLunar calendar day Crypto Trading Strategy

This strategy explores the potential impact of the lunar calendar on cryptocurrency price cycles.

It implements a simple but unconventional rule:

Buy on the 5th day of each lunar month

Sell on the 26th day of the lunar month

No trades between January 1 (solar) and Lunar New Year’s Day (holiday buffer period)

Research background

Several academic studies have investigated the influence of lunar cycles on financial markets. Their findings suggest:

Returns tend to be higher around the full moon compared to the new moon.

Periods between the full moon and the waning phase often show stronger average returns than the waxing phase.

This strategy combines those observations into a practical implementation by testing fixed entry (lunar day 5) and exit (lunar day 26) points, while excluding the transition period from solar New Year to Lunar New Year, effectively capturing mid-month lunar effects.

How it works

The script includes a custom lunar date calculation function, reconstructing lunar months and days for each year (2020–2026).

On lunar day 5, the strategy opens a long position with 100% of equity.

On lunar day 26, the strategy closes the position.

No trades are executed between Jan 1 and Lunar New Year’s Day.

All trades include:

Commission: 0.1%

Slippage: 3 ticks

Position sizing uses the entire equity (100%) for simplicity, but this is not recommended for live trading.

Why this is original

Unlike mashups of built-in indicators, this script:

Implements a full lunar calendar system inside Pine Script.

Translates academic findings on lunar effects into an applied backtest.

Adds a realistic trading filter (holiday gap) based on cultural/seasonal calendar rules.

Provides researchers and traders with a framework to explore non-traditional, time-based signals.

Notes

This is an experimental, research-oriented strategy, not financial advice.

Results are highly dependent on the chosen period (2020–2026).

Using 100% equity per trade is for simplification only and is not a viable money management practice.

The purpose is to investigate whether cyclical patterns linked to lunar time can provide any statistical edge in ETHUSDT.

Parabolic CCI Pro — Long & Short + ATR Risk — [AlphaFinansData]English Description (Enhanced)

🔹 CCI + Parabolic SAR Strategy (Long & Short, Smart Risk Management)

This indicator combines the power of CCI (Commodity Channel Index) and Parabolic SAR, creating a highly reliable trading system that adapts to market conditions.

🚀 How It Works:

Trend Hunting: CCI detects weakening momentum and potential reversal zones.

Confirmation: Parabolic SAR confirms the trend direction, reducing false signals.

Smart Risk Management: Offers both fixed-percentage and ATR-based dynamic Stop Loss & Take Profit, adjusting to volatility automatically.

Performance Dashboard: Tracks win rate, average profit/loss, max drawdown, and winning/losing streaks for deeper strategy insights.

⚡ Who Is It For?

Day traders looking for quick entries and exits,

Swing traders seeking to capture trend reversals,

Risk-conscious investors who want disciplined SL/TP management.

💡 More than just a signal generator, this indicator provides traders with a structured trading framework that helps maintain consistency and discipline.

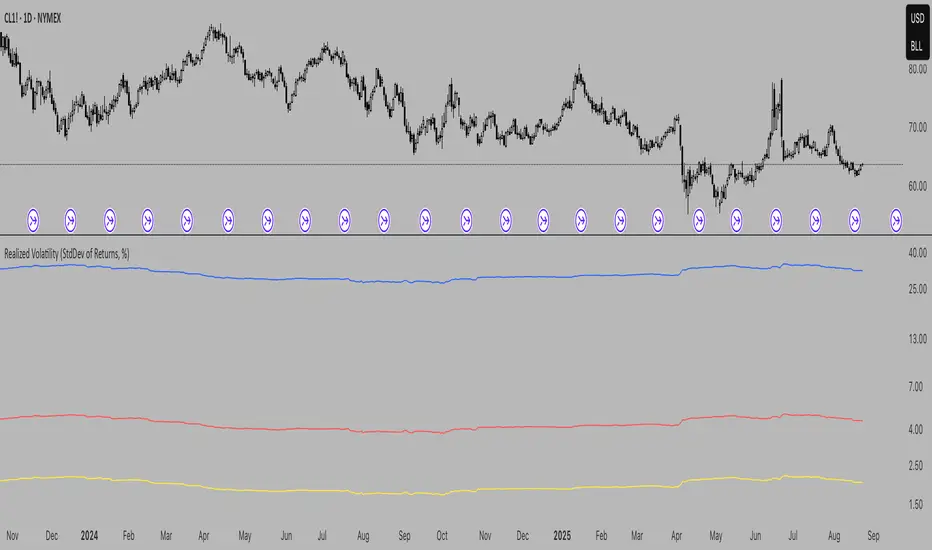

Realized Volatility (StdDev of Returns, %)Realized Volatility (StdDev of Returns, %)

This indicator measures realized (historical) volatility by calculating the standard deviation of log returns over a user-defined lookback period. It helps traders and analysts observe how much the price has varied in the past, expressed as a percentage.

How it works:

Computes close-to-close logarithmic returns.

Calculates the standard deviation of these returns over the selected lookback window.

Provides three volatility measures:

Daily Volatility (%): Standard deviation over the chosen period.

Annualized Volatility (%): Scaled using the square root of the number of trading days per year (default = 250).

Horizon Volatility (%): Scaled to a custom horizon (default = 5 days, useful for short-term views).

Inputs:

Lookback Period: Number of bars used for volatility calculation.

Trading Days per Year: Used for annualizing volatility.

Horizon (days): Adjusts volatility to a shorter or longer time frame.

Notes:

This is a statistical measure of past volatility, not a forecasting tool.

If you change the scale to logarithmic, the indicator readibility improves.

It should be used for analysis in combination with other tools and not as a standalone signal.

Crypto Position Size CalculatorPosition Size Calculator for Crypto.

This indicator uses the current price and a selected stop loss to calculate your position size without having to work it out elsewhere!

Simply set your account size, desired risk percentage and stop loss level and it will work out how many lots and the dollar value of your desired position.

Hope you enjoy!

Calculadora de posicion)Position Size Calculator is a simple tool that helps traders instantly know how many contracts or lots to use based on their risk.

Just set your account size, risk percentage, and stop loss distance — the calculator does the rest.

Stay disciplined, control your risk, and trade with confidence.

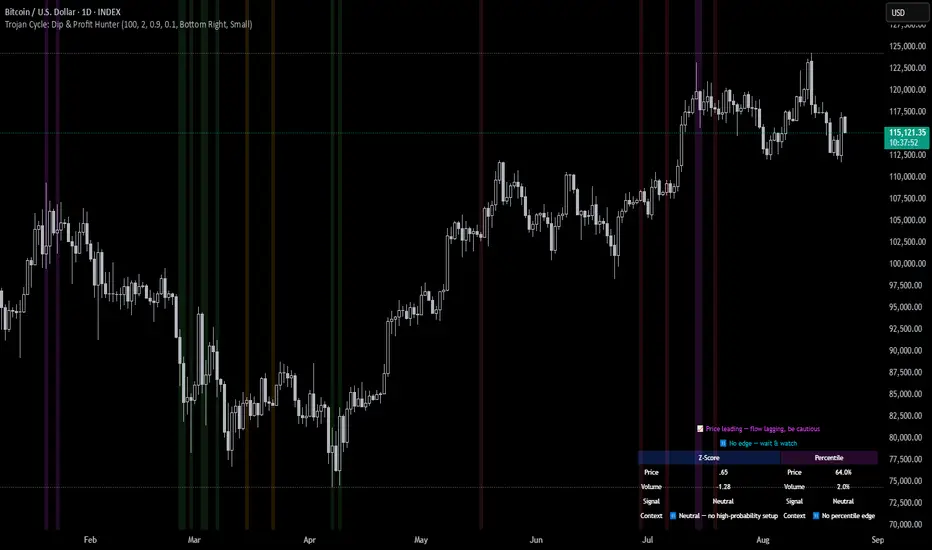

Trojan Cycle: Dip & Profit Hunter📉 Crypto is changing. Your signals should too.

This script doesn’t try to outguess price — it helps you track capital rotation and flow behavior in alignment with the evolving macro structure of the digital asset market.

Trojan Cycle: Dip & Profit Hunter is a signal engine built to support and validate the capital rotation models outlined in the Trojan Cycle and Synthetic Rotation theses — available via RWCS_LTD’s published charts

It is not a classic “buy low, sell high” tool. It is a structural filter that uses price/volume statistics to surface accumulation zones, synthetic traps, and macro context shifts — all aligned with the institutionalization of crypto post-2024.

🧠 Purpose & Value

Crypto no longer follows the retail-led, halving-driven pattern of 2017 or 2021.

Instead, institutional infrastructure, regulatory filters, and equity-market Trojan horses define the new path of capital.

This tool helps you visualize that path by interpreting behavior through statistical imbalances and real-time momentum signals.

Use it to:

Track where capital is accumulating or exiting

Identify signals consistent with true cycle rotation (vs. synthetic traps)

Validate your macro view with real-time statistical context

🔍 How It Works

The engine combines four signal layers:

1. Z-Score Logic

- Measures how far price and volume have deviated from their mean

- Detects dips, blowoffs, and exhaustion zones

2. Percentile Logic

- Compares current price and volume to historical rank distribution

- Flags statistically rare conditions (e.g. bottom 10% price, top 90% volume)

3. Combined Context Engine

- Integrates both models to generate one of 36 unique output states

- Each state provides a labeled market context (e.g., 🟢 Confluent Buy, 🔴 Confluent Sell, 🧨 Synthetic Trap )

4. Momentum Spread & Divergence

- Measures whether price is leading volume (trap risk) or volume is leading price (accumulation)

- Outputs intuitive momentum context with emoji-coded alerts

📋 What You See

🧠 Contextual Table UI with key Z-Scores, percentiles, signals, and market commentary

🎯 Emoji-coded signals to quickly grasp high-probability setups or risk zones

🌊 Optional overlays: price/volume divergence, momentum spread

🎨 Visual table customization (size, position) and chart highlights for signal clarity

🔔 Alert System

✅ Single dynamic alert using alert() that only fires when signal context changes

Prevents alert fatigue and allows clean webhook/automation integration

🧭 Use Cases

For macro cycle traders: Track where we are in the Trojan Cycle using statistical context

For thesis explorers: Use the 36-output signal map to match against your rotation thesis

For capital rotation watchers: Identify structural setups consistent with ETF-driven or compliance-filtered flow

For narrative skeptics: Avoid synthetic altseason traps where volume lags or flow dries up

🧪 Suggested Pairing for Thesis Validation

To use this tool as part of a thesis-confirmation framework , pair it with:

BTC.D — Bitcoin Dominance

ETH/BTC — Ethereum strength vs. Bitcoin

TOTALE100/ETH — Altcoin strength relative to ETH

RWCS_LTD’s published charts and macro cycle models

🏁 Final Note

Crypto has matured. So should your signals.

This tool doesn’t try to game the next 2 candles. It helps you understand the current phase in a compliance-filtered, institutionalized rotation model.

It’s not built for hype — it’s built for conviction.

Explore the thesis → Validate the structure → Trade with clarity.

🚨 Disclaimer

This script is not financial advice. It is an analytical tool designed to support market structure research and rotation thesis validation. Use this as part of a broader framework including technical structure, dominance charts, and macro data.

ATR by Session Library [1CG]Library "ATRxSession"

This library shows you how big the bars usually are during a trading session. It looks only at the times you choose (like New York or London hours), measures the “true range” of every bar in that session, then finds the average for that session. It keeps the last N sessions and gives you their overall average, so you can quickly see how much the market typically moves per bar during your chosen session.

Call getSessionAtr(timezone, session, sessionCount) from your script, and it will return a single number: the average per-bar volatility during the chosen session, based on the last N completed sessions. This makes it easy to plug session-specific volatility into your own indicators or strategies.

getSessionAtr(_timezone, _session, _sessionCount)

getSessionAtr - Computes a session-aware ATR over completed sessions.

Parameters:

_timezone (string) : (string) - Timezone string to evaluate session timing.

_session (string) : (string) - Session time range string (e.g., "0930-1600").

_sessionCount (int) : (int) - Number of past completed sessions to include in the rolling average.

Returns: (float) - The average ATR across the last N completed sessions, or na if not enough data.

Size & LeverageSize and Leverage calculator for trading, using market orders. It will calculate maximum possible leverage by default in order to prioritize capital efficiency. If you wish to use manual leverage you need to manually enter it in the settings. The script rounds both auto leverage and size to your liking. Entry price is always last price. Size is the actual size you need to input, adjusted to your leverage, cost means the margin required to open the trade. I made this indicator as a binance futures user.

AndrologQuartileAndrologQuartile

This indicator is based on the assumption that if a candle closes in the upper or lower quartile of its range, the next candle often tends to take out the high or low of that candle.

The script does two things:

It calculates and displays live statistics on how often this condition occurs and how often it is successful.

It highlights candles that meet the quartile condition so you can track them in real time.

It is most meaningful to use this indicator on higher timeframes (from 1h upwards).

You can also set an alert: once configured, the alert will always trigger for the timeframe that was active at the moment of setup.

Usage tip:

Click the statistics panel in the top right corner to adjust settings and alerts.

Adjustable parameters:

Quartiles: Default values are 25% and 75%.

Min Distance: Defines how far the high/low must be from the candle’s close (in %) to be considered relevant. A smaller value is applied automatically on intraday timeframes under 5 minutes.