VolumeProfileLibrary "VolumeProfile"

Analyzes volume and price and calculates a volume profile, in particular the Point Of Control and Value Area values.

new(rowSizeInTicks, valueAreaCoverage, startTime)

Constructor method that creates a new Volume Profile

Parameters:

rowSizeInTicks (float) : Internal row size (aka resolution) of the volume profile. Useful for most futures contracts would be '1 / syminfo.mintick'. Default '4'.

valueAreaCoverage (int) : Percentage of total volume that is considered the Value Area. Default '70'

startTime (int) : Start time (unix timestamp in milliseconds) of the Volume Profile. Default 'time'.

Returns: VolumeProfile object

method calculatePOC(vp)

Calculates current Point Of Control of the VP

Namespace types: VolumeProfile

Parameters:

vp (VolumeProfile)

Returns: void

method calculateVA(vp)

Calculates current Value Area High and Low of the VP

Namespace types: VolumeProfile

Parameters:

vp (VolumeProfile)

Returns: void

method update(vp, h, l, v, t)

Processes new chart data and sorts volume into rows. Then calls calculatePOC() and calculateVA() to update the VP. Parameters are usually the output of request.security_lower_tf.

Namespace types: VolumeProfile

Parameters:

vp (VolumeProfile)

h (array) : Array of highs

l (array) : Array of lows

v (array) : Array of volumes

t (array) : Array of candle times

Returns: void

method setSessionHigh(vp, h)

Sets the high of the session the VP is tracking

Namespace types: VolumeProfile

Parameters:

vp (VolumeProfile)

h (float)

Returns: void

method setSessionLow(vp, l)

Sets the low of the session the VP is tracking

Namespace types: VolumeProfile

Parameters:

vp (VolumeProfile)

l (float)

Returns: void

method getPOC(vp)

Gets the current Point Of Control

Namespace types: VolumeProfile

Parameters:

vp (VolumeProfile)

Returns: Point Of Control (float)

method getVAH(vp)

Gets the current Value Area High

Namespace types: VolumeProfile

Parameters:

vp (VolumeProfile)

Returns: Value Area High (float)

method getVAL(vp)

Gets the current Value Area Low

Namespace types: VolumeProfile

Parameters:

vp (VolumeProfile)

Returns: Value Area Low (float)

VolumeProfile

Fields:

rowSizeInTicks (series float)

valueAreaCoverage (series int)

startTime (series int)

valueAreaHigh (series float)

pointOfControl (series float)

valueAreaLow (series float)

sessionHigh (series float)

sessionLow (series float)

volumeByRow (map)

totalVolume (series float)

pocRow (series float)

pocVol (series float)

Techindicator

Request█ OVERVIEW

This library is a tool for Pine Script™ programmers that consolidates access to a wide range of lesser-known data feeds available on TradingView, including metrics from the FRED database, FINRA short sale volume, open interest, and COT data. The functions in this library simplify requests for these data feeds, making them easier to retrieve and use in custom scripts.

█ CONCEPTS

Federal Reserve Economic Data (FRED)

FRED (Federal Reserve Economic Data) is a comprehensive online database curated by the Federal Reserve Bank of St. Louis. It provides free access to extensive economic and financial data from U.S. and international sources. FRED includes numerous economic indicators such as GDP, inflation, employment, and interest rates. Additionally, it provides financial market data, regional statistics, and international metrics such as exchange rates and trade balances.

Sourced from reputable organizations, including U.S. government agencies, international institutions, and other public and private entities, FRED enables users to analyze over 825,000 time series, download their data in various formats, and integrate their information into analytical tools and programming workflows.

On TradingView, FRED data is available from ticker identifiers with the "FRED:" prefix. Users can search for FRED symbols in the "Symbol Search" window, and Pine scripts can retrieve data for these symbols via `request.*()` function calls.

FINRA Short Sale Volume

FINRA (the Financial Industry Regulatory Authority) is a non-governmental organization that supervises and regulates U.S. broker-dealers and securities professionals. Its primary aim is to protect investors and ensure integrity and transparency in financial markets.

FINRA's Short Sale Volume data provides detailed information about daily short-selling activity across U.S. equity markets. This data tracks the volume of short sales reported to FINRA's trade reporting facilities (TRFs), including shares sold on FINRA-regulated Alternative Trading Systems (ATSs) and over-the-counter (OTC) markets, offering transparent access to short-selling information not typically available from exchanges. This data helps market participants, researchers, and regulators monitor trends in short-selling and gain insights into bearish sentiment, hedging strategies, and potential market manipulation. Investors often use this data alongside other metrics to assess stock performance, liquidity, and overall trading activity.

It is important to note that FINRA's Short Sale Volume data does not consolidate short sale information from public exchanges and excludes trading activity that is not publicly disseminated.

TradingView provides ticker identifiers for requesting Short Sale Volume data with the format "FINRA:_SHORT_VOLUME", where "" is a supported U.S. equities symbol (e.g., "AAPL").

Open Interest (OI)

Open interest is a cornerstone indicator of market activity and sentiment in derivatives markets such as options or futures. In contrast to volume, which measures the number of contracts opened or closed within a period, OI measures the number of outstanding contracts that are not yet settled. This distinction makes OI a more robust indicator of how money flows through derivatives, offering meaningful insights into liquidity, market interest, and trends. Many traders and investors analyze OI alongside volume and price action to gain an enhanced perspective on market dynamics and reinforce trading decisions.

TradingView offers many ticker identifiers for requesting OI data with the format "_OI", where "" represents a derivative instrument's ticker ID (e.g., "COMEX:GC1!").

Commitment of Traders (COT)

Commitment of Traders data provides an informative weekly breakdown of the aggregate positions held by various market participants, including commercial hedgers, non-commercial speculators, and small traders, in the U.S. derivative markets. Tallied and managed by the Commodity Futures Trading Commission (CFTC) , these reports provide traders and analysts with detailed insight into an asset's open interest and help them assess the actions of various market players. COT data is valuable for gaining a deeper understanding of market dynamics, sentiment, trends, and liquidity, which helps traders develop informed trading strategies.

TradingView has numerous ticker identifiers that provide access to time series containing data for various COT metrics. To learn about COT ticker IDs and how they work, see our LibraryCOT publication.

█ USING THE LIBRARY

Common function characteristics

• This library's functions construct ticker IDs with valid formats based on their specified parameters, then use them as the `symbol` argument in request.security() to retrieve data from the specified context.

• Most of these functions automatically select the timeframe of a data request because the data feeds are not available for all timeframes.

• All the functions have two overloads. The first overload of each function uses values with the "simple" qualifier to define the requested context, meaning the context does not change after the first script execution. The second accepts "series" values, meaning it can request data from different contexts across executions.

• The `gaps` parameter in most of these functions specifies whether the returned data is `na` when a new value is unavailable for request. By default, its value is `false`, meaning the call returns the last retrieved data when no new data is available.

• The `repaint` parameter in applicable functions determines whether the request can fetch the latest unconfirmed values from a higher timeframe on realtime bars, which might repaint after the script restarts. If `false`, the function only returns confirmed higher-timeframe values to avoid repainting. The default value is `true`.

`fred()`

The `fred()` function retrieves the most recent value of a specified series from the Federal Reserve Economic Data (FRED) database. With this function, programmers can easily fetch macroeconomic indicators, such as GDP and unemployment rates, and use them directly in their scripts.

How it works

The function's `fredCode` parameter accepts a "string" representing the unique identifier of a specific FRED series. Examples include "GDP" for the "Gross Domestic Product" series and "UNRATE" for the "Unemployment Rate" series. Over 825,000 codes are available. To access codes for available series, search the FRED website .

The function adds the "FRED:" prefix to the specified `fredCode` to construct a valid FRED ticker ID (e.g., "FRED:GDP"), which it uses in request.security() to retrieve the series data.

Example Usage

This line of code requests the latest value from the Gross Domestic Product series and assigns the returned value to a `gdpValue` variable:

float gdpValue = fred("GDP")

`finraShortSaleVolume()`

The `finraShortSaleVolume()` function retrieves EOD data from a FINRA Short Sale Volume series. Programmers can call this function to retrieve short-selling information for equities listed on supported exchanges, namely NASDAQ, NYSE, and NYSE ARCA.

How it works

The `symbol` parameter determines which symbol's short sale volume information is retrieved by the function. If the value is na , the function requests short sale volume data for the chart's symbol. The argument can be the name of the symbol from a supported exchange (e.g., "AAPL") or a ticker ID with an exchange prefix ("NASDAQ:AAPL"). If the `symbol` contains an exchange prefix, it must be one of the following: "NASDAQ", "NYSE", "AMEX", or "BATS".

The function constructs a ticker ID in the format "FINRA:ticker_SHORT_VOLUME", where "ticker" is the symbol name without the exchange prefix (e.g., "AAPL"). It then uses the ticker ID in request.security() to retrieve the available data.

Example Usage

This line of code retrieves short sale volume for the chart's symbol and assigns the result to a `shortVolume` variable:

float shortVolume = finraShortSaleVolume(syminfo.tickerid)

This example requests short sale volume for the "NASDAQ:AAPL" symbol, irrespective of the current chart:

float shortVolume = finraShortSaleVolume("NASDAQ:AAPL")

`openInterestFutures()` and `openInterestCrypto()`

The `openInterestFutures()` function retrieves EOD open interest (OI) data for futures contracts. The `openInterestCrypto()` function provides more granular OI data for cryptocurrency contracts.

How they work

The `openInterestFutures()` function retrieves EOD closing OI information. Its design is focused primarily on retrieving OI data for futures, as only EOD OI data is available for these instruments. If the chart uses an intraday timeframe, the function requests data from the "1D" timeframe. Otherwise, it uses the chart's timeframe.

The `openInterestCrypto()` function retrieves opening, high, low, and closing OI data for a cryptocurrency contract on a specified timeframe. Unlike `openInterest()`, this function can also retrieve granular data from intraday timeframes.

Both functions contain a `symbol` parameter that determines the symbol for which the calls request OI data. The functions construct a valid OI ticker ID from the chosen symbol by appending "_OI" to the end (e.g., "CME:ES1!_OI").

The `openInterestFutures()` function requests and returns a two-element tuple containing the futures instrument's EOD closing OI and a "bool" condition indicating whether OI is rising.

The `openInterestCrypto()` function requests and returns a five-element tuple containing the cryptocurrency contract's opening, high, low, and closing OI, and a "bool" condition indicating whether OI is rising.

Example usage

This code line calls `openInterest()` to retrieve EOD OI and the OI rising condition for a futures symbol on the chart, assigning the values to two variables in a tuple:

= openInterestFutures(syminfo.tickerid)

This line retrieves the EOD OI data for "CME:ES1!", irrespective of the current chart's symbol:

= openInterestFutures("CME:ES1!")

This example uses `openInterestCrypto()` to retrieve OHLC OI data and the OI rising condition for a cryptocurrency contract on the chart, sampled at the chart's timeframe. It assigns the returned values to five variables in a tuple:

= openInterestCrypto(syminfo.tickerid, timeframe.period)

This call retrieves OI OHLC and rising information for "BINANCE:BTCUSDT.P" on the "1D" timeframe:

= openInterestCrypto("BINANCE:BTCUSDT.P", "1D")

`commitmentOfTraders()`

The `commitmentOfTraders()` function retrieves data from the Commitment of Traders (COT) reports published by the Commodity Futures Trading Commission (CFTC). This function significantly simplifies the COT request process, making it easier for programmers to access and utilize the available data.

How It Works

This function's parameters determine different parts of a valid ticker ID for retrieving COT data, offering a streamlined alternative to constructing complex COT ticker IDs manually. The `metricName`, `metricDirection`, and `includeOptions` parameters are required. They specify the name of the reported metric, the direction, and whether it includes information from options contracts.

The function also includes several optional parameters. The `CFTCCode` parameter allows programmers to request data for a specific report code. If unspecified, the function requests data based on the chart symbol's root prefix, base currency, or quoted currency, depending on the `mode` argument. The call can specify the report type ("Legacy", "Disaggregated", or "Financial") and metric type ("All", "Old", or "Other") with the `typeCOT` and `metricType` parameters.

Explore the CFTC website to find valid report codes for specific assets. To find detailed information about the metrics included in the reports and their meanings, see the CFTC's Explanatory Notes .

View the function's documentation below for detailed explanations of its parameters. For in-depth information about COT ticker IDs and more advanced functionality, refer to our previously published COT library .

Available metrics

Different COT report types provide different metrics . The tables below list all available metrics for each type and their applicable directions:

+------------------------------+------------------------+

| Legacy (COT) Metric Names | Directions |

+------------------------------+------------------------+

| Open Interest | No direction |

| Noncommercial Positions | Long, Short, Spreading |

| Commercial Positions | Long, Short |

| Total Reportable Positions | Long, Short |

| Nonreportable Positions | Long, Short |

| Traders Total | No direction |

| Traders Noncommercial | Long, Short, Spreading |

| Traders Commercial | Long, Short |

| Traders Total Reportable | Long, Short |

| Concentration Gross LT 4 TDR | Long, Short |

| Concentration Gross LT 8 TDR | Long, Short |

| Concentration Net LT 4 TDR | Long, Short |

| Concentration Net LT 8 TDR | Long, Short |

+------------------------------+------------------------+

+-----------------------------------+------------------------+

| Disaggregated (COT2) Metric Names | Directions |

+-----------------------------------+------------------------+

| Open Interest | No Direction |

| Producer Merchant Positions | Long, Short |

| Swap Positions | Long, Short, Spreading |

| Managed Money Positions | Long, Short, Spreading |

| Other Reportable Positions | Long, Short, Spreading |

| Total Reportable Positions | Long, Short |

| Nonreportable Positions | Long, Short |

| Traders Total | No Direction |

| Traders Producer Merchant | Long, Short |

| Traders Swap | Long, Short, Spreading |

| Traders Managed Money | Long, Short, Spreading |

| Traders Other Reportable | Long, Short, Spreading |

| Traders Total Reportable | Long, Short |

| Concentration Gross LE 4 TDR | Long, Short |

| Concentration Gross LE 8 TDR | Long, Short |

| Concentration Net LE 4 TDR | Long, Short |

| Concentration Net LE 8 TDR | Long, Short |

+-----------------------------------+------------------------+

+-------------------------------+------------------------+

| Financial (COT3) Metric Names | Directions |

+-------------------------------+------------------------+

| Open Interest | No Direction |

| Dealer Positions | Long, Short, Spreading |

| Asset Manager Positions | Long, Short, Spreading |

| Leveraged Funds Positions | Long, Short, Spreading |

| Other Reportable Positions | Long, Short, Spreading |

| Total Reportable Positions | Long, Short |

| Nonreportable Positions | Long, Short |

| Traders Total | No Direction |

| Traders Dealer | Long, Short, Spreading |

| Traders Asset Manager | Long, Short, Spreading |

| Traders Leveraged Funds | Long, Short, Spreading |

| Traders Other Reportable | Long, Short, Spreading |

| Traders Total Reportable | Long, Short |

| Concentration Gross LE 4 TDR | Long, Short |

| Concentration Gross LE 8 TDR | Long, Short |

| Concentration Net LE 4 TDR | Long, Short |

| Concentration Net LE 8 TDR | Long, Short |

+-------------------------------+------------------------+

Example usage

This code line retrieves "Noncommercial Positions (Long)" data, without options information, from the "Legacy" report for the chart symbol's root, base currency, or quote currency:

float nonCommercialLong = commitmentOfTraders("Noncommercial Positions", "Long", false)

This example retrieves "Managed Money Positions (Short)" data, with options included, from the "Disaggregated" report:

float disaggregatedData = commitmentOfTraders("Managed Money Positions", "Short", true, "", "Disaggregated")

█ NOTES

• This library uses dynamic requests , allowing dynamic ("series") arguments for the parameters defining the context (ticker ID, timeframe, etc.) of a `request.*()` function call. With this feature, a single `request.*()` call instance can flexibly retrieve data from different feeds across historical executions. Additionally, scripts can use such calls in the local scopes of loops, conditional structures, and even exported library functions, as demonstrated in this script. All scripts coded in Pine Script™ v6 have dynamic requests enabled by default. To learn more about the behaviors and limitations of this feature, see the Dynamic requests section of the Pine Script™ User Manual.

• The library's example code offers a simple demonstration of the exported functions. The script retrieves available data using the function specified by the "Series type" input. The code requests a FRED series or COT (Legacy), FINRA Short Sale Volume, or Open Interest series for the chart's symbol with specific parameters, then plots the retrieved data as a step-line with diamond markers.

Look first. Then leap.

█ EXPORTED FUNCTIONS

This library exports the following functions:

fred(fredCode, gaps)

Requests a value from a specified Federal Reserve Economic Data (FRED) series. FRED is a comprehensive source that hosts numerous U.S. economic datasets. To explore available FRED datasets and codes, search for specific categories or keywords at fred.stlouisfed.org Calls to this function count toward a script's `request.*()` call limit.

Parameters:

fredCode (series string) : The unique identifier of the FRED series. The function uses the value to create a valid ticker ID for retrieving FRED data in the format `"FRED:fredCode"`. For example, `"GDP"` refers to the "Gross Domestic Product" series ("FRED:GDP"), and `"GFDEBTN"` refers to the "Federal Debt: Total Public Debt" series ("FRED:GFDEBTN").

gaps (simple bool) : Optional. If `true`, the function returns a non-na value only when a new value is available from the requested context. If `false`, the function returns the latest retrieved value when new data is unavailable. The default is `false`.

Returns: (float) The value from the requested FRED series.

finraShortSaleVolume(symbol, gaps, repaint)

Requests FINRA daily short sale volume data for a specified symbol from one of the following exchanges: NASDAQ, NYSE, NYSE ARCA. If the chart uses an intraday timeframe, the function requests data from the "1D" timeframe. Otherwise, it uses the chart's timeframe. Calls to this function count toward a script's `request.*()` call limit.

Parameters:

symbol (series string) : The symbol for which to request short sale volume data. If the specified value contains an exchange prefix, it must be one of the following: "NASDAQ", "NYSE", "AMEX", "BATS".

gaps (simple bool) : Optional. If `true`, the function returns a non-na value only when a new value is available from the requested context. If `false`, the function returns the latest retrieved value when new data is unavailable. The default is `false`.

repaint (simple bool) : Optional. If `true` and the chart's timeframe is intraday, the value requested on realtime bars may change its time offset after the script restarts its executions. If `false`, the function returns the last confirmed period's values to avoid repainting. The default is `true`.

Returns: (float) The short sale volume for the specified symbol or the chart's symbol.

openInterestFutures(symbol, gaps, repaint)

Requests EOD open interest (OI) and OI rising information for a valid futures symbol. If the chart uses an intraday timeframe, the function requests data from the "1D" timeframe. Otherwise, it uses the chart's timeframe. Calls to this function count toward a script's `request.*()` call limit.

Parameters:

symbol (series string) : The symbol for which to request open interest data.

gaps (simple bool) : Optional. If `true`, the function returns non-na values only when new values are available from the requested context. If `false`, the function returns the latest retrieved values when new data is unavailable. The default is `false`.

repaint (simple bool) : Optional. If `true` and the chart's timeframe is intraday, the value requested on realtime bars may change its time offset after the script restarts its executions. If `false`, the function returns the last confirmed period's values to avoid repainting. The default is `true`.

Returns: ( ) A tuple containing the following values:

- The closing OI value for the symbol.

- `true` if the closing OI is above the previous period's value, `false` otherwise.

openInterestCrypto(symbol, timeframe, gaps, repaint)

Requests opening, high, low, and closing open interest (OI) data and OI rising information for a valid cryptocurrency contract on a specified timeframe. Calls to this function count toward a script's `request.*()` call limit.

Parameters:

symbol (series string) : The symbol for which to request open interest data.

timeframe (series string) : The timeframe of the data request. If the timeframe is lower than the chart's timeframe, it causes a runtime error.

gaps (simple bool) : Optional. If `true`, the function returns non-na values only when new values are available from the requested context. If `false`, the function returns the latest retrieved values when new data is unavailable. The default is `false`.

repaint (simple bool) : Optional. If `true` and the `timeframe` represents a higher timeframe, the function returns unconfirmed values from the timeframe on realtime bars, which repaint when the script restarts its executions. If `false`, it returns only confirmed higher-timeframe values to avoid repainting. The default is `true`.

Returns: ( ) A tuple containing the following values:

- The opening, high, low, and closing OI values for the symbol, respectively.

- `true` if the closing OI is above the previous period's value, `false` otherwise.

commitmentOfTraders(metricName, metricDirection, includeOptions, CFTCCode, typeCOT, mode, metricType)

Requests Commitment of Traders (COT) data with specified parameters. This function provides a simplified way to access CFTC COT data available on TradingView. Calls to this function count toward a script's `request.*()` call limit. For more advanced tools and detailed information about COT data, see TradingView's LibraryCOT library.

Parameters:

metricName (series string) : One of the valid metric names listed in the library's documentation and source code.

metricDirection (series string) : Metric direction. Possible values are: "Long", "Short", "Spreading", and "No direction". Consult the library's documentation or code to see which direction values apply to the specified metric.

includeOptions (series bool) : If `true`, the COT symbol includes options information. Otherwise, it does not.

CFTCCode (series string) : Optional. The CFTC code for the asset. For example, wheat futures (root "ZW") have the code "001602". If one is not specified, the function will attempt to get a valid code for the chart symbol's root, base currency, or main currency.

typeCOT (series string) : Optional. The type of report to request. Possible values are: "Legacy", "Disaggregated", "Financial". The default is "Legacy".

mode (series string) : Optional. Specifies the information the function extracts from a symbol. Possible modes are:

- "Root": The function extracts the futures symbol's root prefix information (e.g., "ES" for "ESH2020").

- "Base currency": The function extracts the first currency from a currency pair (e.g., "EUR" for "EURUSD").

- "Currency": The function extracts the currency of the symbol's quoted values (e.g., "JPY" for "TSE:9984" or "USDJPY").

- "Auto": The function tries the first three modes (Root -> Base currency -> Currency) until it finds a match.

The default is "Auto". If the specified mode is not available for the symbol, it causes a runtime error.

metricType (series string) : Optional. The metric type. Possible values are: "All", "Old", "Other". The default is "All".

Returns: (float) The specified Commitment of Traders data series. If no data is available, it causes a runtime error.

LibraryDivergenceV6LibraryDivergenceV6

Enhance your trading strategies with LibraryDivergenceV6, a comprehensive Pine Script library designed to simplify and optimize the detection of bullish and bearish divergences across multiple technical indicators. Whether you're developing your own indicators or seeking to incorporate robust divergence analysis into your trading systems, this library provides the essential tools and functions to accurately identify potential market reversals and continuations.

Overview

LibraryDivergenceV6 offers a suite of functions that detect divergences between price movements and key technical indicators such as the Relative Strength Index (RSI) and On-Balance Volume (OBV). By automating the complex calculations involved in divergence detection, this library enables traders and developers to implement reliable and customizable divergence strategies with ease.

Key Features

Comprehensive Divergence Detection

Bullish Divergence: Identifies instances where the indicator forms higher lows while the price forms lower lows, signaling potential upward reversals.

Bearish Divergence: Detects situations where the indicator creates lower highs while the price forms higher highs, indicating possible downward reversals.

Overbought and Oversold Conditions: Differentiates between standard and strong divergences by considering overbought and oversold levels, enhancing signal reliability.

Multi-Indicator Support

RSI (Relative Strength Index): Analyze momentum-based divergences to spot potential trend reversals.

OBV (On-Balance Volume): Incorporate volume flow into divergence analysis for a more comprehensive market perspective.

Customizable Parameters

Pivot Points Configuration: Adjust the number of bars to the left and right for pivot detection, allowing fine-tuning based on different timeframes and trading styles.

Range Settings: Define minimum and maximum bar ranges to control the sensitivity of divergence detection, reducing false signals.

Noise Cancellation: Enable or disable noise filtering to focus on significant divergences and minimize minor fluctuations.

Flexible Usage

Exported Functions: Easily integrate divergence detection into your custom indicators or trading strategies with exported functions such as DivergenceBull, DivergenceBear, DivergenceBullOversold, and DivergenceBearOverbought.

Occurrence Handling: Specify which occurrence of a divergence to consider (e.g., most recent, previous) for precise analysis.

Optimized Performance

Efficient Calculations: Designed to handle multiple occurrences and pivot points without compromising script performance.

Line Management: Automatically creates and deletes trend lines based on divergence conditions, ensuring a clean and uncluttered chart display.

PseudoPlotLibrary "PseudoPlot"

PseudoPlot: behave like plot and fill using polyline

This library enables line plotting by polyline like plot() and fill().

The core of polyline() is array of chart.point array, polyline() is called in its method.

Moreover, plotarea() makes a box in main chart, plotting data within the box is enabled.

It works so slowy to manage array of chart.point, so limit the target to visible area of the chart.

Due to polyline specifications, na and expression can not be used for colors.

1. pseudoplot

pseudoplot() behaves like plot().

//use plot()

plot(close)

//use pseudoplot()

pseudoplot(close)

Pseudoplot has label. Label is enabled when title argument is set.

In the example bellow, "close value" label is shown with line.

The label is shown at right of the line when recent bar is visible.

It is shown at 15% from the left of visible area when recent bar is not visible.

Just set "" if you don't need label.

//use plot()

plot(close,"close value")

//use pseudoplot

pseudoplot(close, "close value")

Arguments are designed in an order as similar as possible to plot.

plot(series, title, color, linewidth, style, trackprice, histbase, offset, join, editable, show_last, display, format, precision, force_overlay) → plot

pseudoplot(series, title, ,linecolor ,linewidth, linestyle, labelbg, labeltext, labelsize, shorttitle, format, xpos_from_left, overlay) → pseudo_plot

2. pseudofill

pseudofill() behaves like fill().

The label is shown(text only) at right of the line when recent bar is visible.

It is shown at 10% from the left of visible area when recent bar is not visible.

Just set "" if you don't need label.

//use plot() and fill()

p1=plot(open)

p2=plot(close)

fill(p1,p2)

//use pseudofill()

pseudofill(open,close)

Arguments are designed in an order as similar as possible to fill.

fill(hline1, hline2, color, title, editable, fillgaps, display) → void

pseudofill(series1, series2, fillcolor, title, linecolor, linewidth, linestyle, labeltext, labelsize, shorttitle, format, xpos_from_left, overlay) → pseudo_plot

3. plotarea and its methods

plotarea() makes a box in main chart. You can set the box position to top or bottom, and

the box height in percentage of the range of visible high and low prices.

x-coordinate of the box is from chart.left_visible_bar_time to chart.right_visible_bar_time,

y-coordinate is highest and lowest price of visible bars.

pseudoplot() and pseudofill() work as method of plotarea(box).

Usage is almost same as the function version, just set min and max value, y-coodinate is remapped automatically.

hline() is also available. The y-coordinate of hline is specified as a percentage from the bottom.

plotarea() and its associated methods are overlay=true as default.

Depending on the drawing order of the objects, plot may become invisible, so the bgcolor of plotarea should be na or tranceparent.

//1. make a plotarea

// bgcolor should be na or transparent color.

area=plotarea("bottom",30,"plotarea",bgcolor=na)

//2. plot in a plotarea

//(min=0, max=100 is omitted as it is the default.)

area.pseudoplot(ta.rsi(close,14))

//3. draw hlines

area.hline(30,linestyle="dotted",linewidth=2)

area.hline(70,linestyle="dotted",linewidth=2)

4. Data structure and sub methods

Array management is most imporant part of using polyline.

I don't know the proper way to handle array, so it is managed by array and array as intermediate data.

(type xy_arrays to manage bar_time and price as independent arrays.)

method cparray() pack arrays to array, when array includes both chart.left_visible_bar_time and chart.right_visible_bar.time.

Calling polyline is implemented as methods of array of chart.point.

Method creates polyline object if array is not empty.

method polyline(linecolor, linewidth, linestyle, overlay) → series polyline

method polyline_fill(fillcolor, linecolor, linewidth, linestyle, overlay) → series polyline

Also calling label is implemented as methods of array of chart.point.

Method creates label ofject if array is not empty.

Label is located at right edge of the chart when recent bar is visible, located at left side when recent bar is invisible.

label(title, labelbg, labeltext, labelsize, format, shorttitle, xpos_from_left, overlay) → series label

label_for_fill(title, labeltext, labelsize, format, shorttitle, xpos_from_left, overlay) → series label

visible_xyInit(series)

make arrays of visible x(bar_time) and y(price/value).

Parameters:

series (float) : (float) series variable

Returns: (xy_arrays)

method remap(this, bottom, top, min, max)

Namespace types: xy_arrays

Parameters:

this (xy_arrays)

bottom (float) : (float) bottom price to ajust.

top (float) : (float) top price to ajust.

min (float) : (float) min of src value.

max (float) : (float) max of src value.

Returns: (xy_arrays)

method polyline(this, linecolor, linewidth, linestyle, overlay)

Namespace types: array

Parameters:

this (array)

linecolor (color) : (color) color of polyline.

linewidth (int) : (int) width of polyline.

linestyle (string) : (string) linestyle of polyline. default is line.style_solid("solid"), others line.style_dashed("dashed"), line.style_dotted("dotted").

overlay (bool) : (bool) force_overlay of polyline. default is false.

Returns: (polyline)

method polyline_fill(this, fillcolor, linecolor, linewidth, linestyle, overlay)

Namespace types: array

Parameters:

this (array)

fillcolor (color)

linecolor (color) : (color) color of polyline.

linewidth (int) : (int) width of polyline.

linestyle (string) : (string) linestyle of polyline. default is line.style_solid("solid"), others line.style_dashed("dashed"), line.style_dotted("dotted").

overlay (bool) : (bool) force_overlay of polyline. default is false.

Returns: (polyline)

method label(this, title, labelbg, labeltext, labelsize, format, shorttitle, xpos_from_left, overlay)

Namespace types: array

Parameters:

this (array)

title (string) : (string) label text.

labelbg (color) : (color) color of label bg.

labeltext (color) : (color) color of label text.

labelsize (int) : (int) size of label.

format (string) : (string) textformat of label. default is text.format_none("none"). others text.format_bold("bold"), text.format_italic("italic"), text.format_bold+text.format_italic("bold+italic").

shorttitle (string) : (string) another label text for recent bar is not visible.

xpos_from_left (int) : (int) another label x-position(percentage from left of chart width), when recent bar is not visible. default is 15%.

overlay (bool) : (bool) force_overlay of label. default is false.

Returns: (label)

method label_for_fill(this, title, labeltext, labelsize, format, shorttitle, xpos_from_left, overlay)

Namespace types: array

Parameters:

this (array)

title (string) : (string) label text.

labeltext (color) : (color) color of label text.

labelsize (int) : (int) size of label.

format (string) : (string) textformat of label. default is text.format_none("none"). others text.format_bold("bold"), text.format_italic("italic"), text.format_bold+text.format_italic("bold+italic").

shorttitle (string) : (string) another label text for recent bar is not visible.

xpos_from_left (int) : (int) another label x-position(percentage from left of chart width), when recent bar is not visible. default is 10%.

overlay (bool) : (bool) force_overlay of label. default is false.

Returns: (label)

pseudoplot(series, title, linecolor, linewidth, linestyle, labelbg, labeltext, labelsize, shorttitle, format, xpos_from_left, overlay)

polyline like plot with label

Parameters:

series (float) : (float) series variable to plot.

title (string) : (string) title if need label. default value is ""(disable label).

linecolor (color) : (color) color of line.

linewidth (int) : (int) width of line.

linestyle (string) : (string) style of plotting line. default is "solid", others "dashed", "dotted".

labelbg (color) : (color) color of label bg.

labeltext (color) : (color) color of label text.

labelsize (int) : (int) size of label text.

shorttitle (string) : (string) another label text for recent bar is not visible.

format (string) : (string) textformat of label. default is text.format_none("none"). others text.format_bold("bold"), text.format_italic("italic"), text.format_bold+text.format_italic("bold+italic").

xpos_from_left (int) : (int) another label x-position(percentage from left of chart width), when recent bar is not visible. default is 15%.

overlay (bool) : (bool) force_overlay of polyline and label.

Returns: (pseudo_plot)

method pseudoplot(this, series, title, linecolor, linewidth, linestyle, labelbg, labeltext, labelsize, shorttitle, format, xpos_from_left, min, max, overlay)

Namespace types: series box

Parameters:

this (box)

series (float) : (float) series variable to plot.

title (string) : (string) title if need label. default value is ""(disable label).

linecolor (color) : (color) color of line.

linewidth (int) : (int) width of line.

linestyle (string) : (string) style of plotting line. default is "solid", others "dashed", "dotted".

labelbg (color) : (color) color of label bg.

labeltext (color) : (color) color of label text.

labelsize (int) : (int) size of label text.

shorttitle (string) : (string) another label text for recent bar is not visible.

format (string) : (string) textformat of label. default is text.format_none("none"). others text.format_bold("bold"), text.format_italic("italic"), text.format_bold+text.format_italic("bold+italic").

xpos_from_left (int) : (int) another label x-position(percentage from left of chart width), when recent bar is not visible. default is 15%.

min (float)

max (float)

overlay (bool) : (bool) force_overlay of polyline and label.

Returns: (pseudo_plot)

pseudofill(series1, series2, fillcolor, title, linecolor, linewidth, linestyle, labeltext, labelsize, shorttitle, format, xpos_from_left, overlay)

fill by polyline

Parameters:

series1 (float) : (float) series variable to plot.

series2 (float) : (float) series variable to plot.

fillcolor (color) : (color) color of fill.

title (string)

linecolor (color) : (color) color of line.

linewidth (int) : (int) width of line.

linestyle (string) : (string) style of plotting line. default is "solid", others "dashed", "dotted".

labeltext (color)

labelsize (int)

shorttitle (string)

format (string) : (string) textformat of label. default is text.format_none("none"). others text.format_bold("bold"), text.format_italic("italic"), text.format_bold+text.format_italic("bold+italic").

xpos_from_left (int) : (int) another label x-position(percentage from left of chart width), when recent bar is not visible. default is 15%.

overlay (bool) : (bool) force_overlay of polyline and label.

Returns: (pseudoplot)

method pseudofill(this, series1, series2, fillcolor, title, linecolor, linewidth, linestyle, labeltext, labelsize, shorttitle, format, xpos_from_left, min, max, overlay)

Namespace types: series box

Parameters:

this (box)

series1 (float) : (float) series variable to plot.

series2 (float) : (float) series variable to plot.

fillcolor (color) : (color) color of fill.

title (string)

linecolor (color) : (color) color of line.

linewidth (int) : (int) width of line.

linestyle (string) : (string) style of plotting line. default is "solid", others "dashed", "dotted".

labeltext (color)

labelsize (int)

shorttitle (string)

format (string) : (string) textformat of label. default is text.format_none("none"). others text.format_bold("bold"), text.format_italic("italic"), text.format_bold+text.format_italic("bold+italic").

xpos_from_left (int) : (int) another label x-position(percentage from left of chart width), when recent bar is not visible. default is 15%.

min (float)

max (float)

overlay (bool) : (bool) force_overlay of polyline and label.

Returns: (pseudo_plot)

plotarea(pos, height, title, bordercolor, borderwidth, bgcolor, textsize, textcolor, format, overlay)

subplot area in main chart

Parameters:

pos (string) : (string) position of subplot area, bottom or top.

height (int) : (float) percentage of visible chart heght.

title (string) : (string) text of area box.

bordercolor (color) : (color) color of border.

borderwidth (int) : (int) width of border.

bgcolor (color) : (string) color of area bg.

textsize (int)

textcolor (color)

format (string)

overlay (bool) : (bool) force_overlay of polyline and label.

Returns: (box)

method hline(this, ypos_from_bottom, linecolor, linestyle, linewidth, overlay)

Namespace types: series box

Parameters:

this (box)

ypos_from_bottom (float) : (float) percentage of box height from the bottom of box.(bottom is 0%, top is 100%).

linecolor (color) : (color) color of line.

linestyle (string) : (string) style of line.

linewidth (int) : (int) width of line.

overlay (bool) : (bool) force_overlay of polyline and label.

Returns: (line)

pseudo_plot

polyline and label.

Fields:

p (series polyline)

l (series label)

xy_arrays

x(bartime) and y(price or value) arrays.

Fields:

t (array)

p (array)

DynamicPeriodPublicDynamic Period Calculation Library

This library provides tools for adaptive period determination, useful for creating indicators or strategies that automatically adjust to market conditions.

Overview

The Dynamic Period Library calculates adaptive periods based on pivot points, enabling the creation of responsive indicators and strategies that adjust to market volatility.

Key Features

Dynamic Periods: Computes periods using distances between pivot highs and lows.

Customizable Parameters: Users can adjust detection settings and period constraints.

Robust Handling: Includes fallback mechanisms for cases with insufficient pivot data.

Use Cases

Adaptive Indicators: Build tools that respond to market volatility by adjusting their periods dynamically.

Dynamic Strategies: Enhance trading strategies by integrating pivot-based period adjustments.

Function: `dynamic_period`

Description

Calculates a dynamic period based on the average distances between pivot highs and lows.

Parameters

`left` (default: 5): Number of left-hand bars for pivot detection.

`right` (default: 5): Number of right-hand bars for pivot detection.

`numPivots` (default: 5): Minimum pivots required for calculation.

`minPeriod` (default: 2): Minimum allowed period.

`maxPeriod` (default: 50): Maximum allowed period.

`defaultPeriod` (default: 14): Fallback period if no pivots are found.

Returns

A dynamic period calculated based on pivot distances, constrained by `minPeriod` and `maxPeriod`.

Example

//@version=6

import CrimsonVault/DynamicPeriodPublic/1

left = input.int(5, "Left bars", minval = 1)

right = input.int(5, "Right bars", minval = 1)

numPivots = input.int(5, "Number of Pivots", minval = 2)

period = DynamicPeriodPublic.dynamic_period(left, right, numPivots)

plot(period, title = "Dynamic Period", color = color.blue)

Implementation Notes

Pivot Detection: Requires sufficient historical data to identify pivots accurately.

Edge Cases: Ensures a default period is applied when pivots are insufficient.

Constraints: Limits period values to a user-defined range for stability.

IndicatorsLibrary "Indicators"

cmf(lookback, n_to_smooth)

Calculates the Chaikin's Money Flow.

Parameters:

lookback (simple int)

n_to_smooth (simple int)

Returns: float The Money Flow value.

cmma(lookback, atr_length)

Calculates the CMMA (Close Minus Moving Average) indicator.

Parameters:

lookback (simple int)

atr_length (simple int)

Returns: float The CMMA value.

macd(fast_length, slow_length, n_to_smooth)

Calculates the normalized and scaled MACD.

Parameters:

fast_length (simple int)

slow_length (simple int)

n_to_smooth (simple int)

Returns: A tuple containing .

stochK(length, n_to_smooth)

Calculates a simplified Stochastic Oscillator.

Uses: 100 * ta.sma((close - lowest_low) / (highest_high - lowest_low), n_to_smooth)

Parameters:

length (simple int)

n_to_smooth (simple int)

Returns: float The Stochastic %K value.

williamsR(length)

Calculates the Williams %R using the stochK function.

Uses: -1 * (100 - stoch(length, 1))

Parameters:

length (simple int)

Returns: float The Williams %R value.

supertrendLibrary "supertrend"

supertrend : Library dedicated to different variations of supertrend

supertrend_atr(length, multiplier, atrMaType, source, highSource, lowSource, waitForClose, delayed)

supertrend_atr: Simple supertrend based on atr but also takes into consideration of custom MA Type, sources

Parameters:

length (simple int) : : ATR Length

multiplier (simple float) : : ATR Multiplier

atrMaType (simple string) : : Moving Average type for ATR calculation. This can be sma, ema, hma, rma, wma, vwma, swma

source (float) : : Default is close. Can Chose custom source

highSource (float) : : Default is high. Can also use close price for both high and low source

lowSource (float) : : Default is low. Can also use close price for both high and low source

waitForClose (simple bool) : : Considers source for direction change crossover if checked. Else, uses highSource and lowSource.

delayed (simple bool) : : if set to true lags supertrend atr stop based on target levels.

Returns: dir : Supertrend direction

supertrend : BuyStop if direction is 1 else SellStop

supertrend_bands(bandType, maType, length, multiplier, source, highSource, lowSource, waitForClose, useTrueRange, useAlternateSource, alternateSource, sticky)

supertrend_bands: Simple supertrend based on atr but also takes into consideration of custom MA Type, sources

Parameters:

bandType (simple string) : : Type of band used - can be bb, kc or dc

maType (simple string) : : Moving Average type for Bands. This can be sma, ema, hma, rma, wma, vwma, swma

length (simple int) : : Band Length

multiplier (float) : : Std deviation or ATR multiplier for Bollinger Bands and Keltner Channel

source (float) : : Default is close. Can Chose custom source

highSource (float) : : Default is high. Can also use close price for both high and low source

lowSource (float) : : Default is low. Can also use close price for both high and low source

waitForClose (simple bool) : : Considers source for direction change crossover if checked. Else, uses highSource and lowSource.

useTrueRange (simple bool) : : Used for Keltner channel. If set to false, then high-low is used as range instead of true range

useAlternateSource (simple bool) : - Custom source is used for Donchian Chanbel only if useAlternateSource is set to true

alternateSource (float) : - Custom source for Donchian channel

sticky (simple bool) : : if set to true borders change only when price is beyond borders.

Returns: dir : Supertrend direction

supertrend : BuyStop if direction is 1 else SellStop

supertrend_zigzag(length, history, useAlternativeSource, alternativeSource, source, highSource, lowSource, waitForClose, atrlength, multiplier, atrMaType)

supertrend_zigzag: Zigzag pivot based supertrend

Parameters:

length (simple int) : : Zigzag Length

history (simple int) : : number of historical pivots to consider

useAlternativeSource (simple bool)

alternativeSource (float)

source (float) : : Default is close. Can Chose custom source

highSource (float) : : Default is high. Can also use close price for both high and low source

lowSource (float) : : Default is low. Can also use close price for both high and low source

waitForClose (simple bool) : : Considers source for direction change crossover if checked. Else, uses highSource and lowSource.

atrlength (simple int) : : ATR Length

multiplier (simple float) : : ATR Multiplier

atrMaType (simple string) : : Moving Average type for ATR calculation. This can be sma, ema, hma, rma, wma, vwma, swma

Returns: dir : Supertrend direction

supertrend : BuyStop if direction is 1 else SellStop

zupertrend(length, history, useAlternativeSource, alternativeSource, source, highSource, lowSource, waitForClose, atrlength, multiplier, atrMaType)

zupertrend: Zigzag pivot based supertrend

Parameters:

length (simple int) : : Zigzag Length

history (simple int) : : number of historical pivots to consider

useAlternativeSource (simple bool)

alternativeSource (float)

source (float) : : Default is close. Can Chose custom source

highSource (float) : : Default is high. Can also use close price for both high and low source

lowSource (float) : : Default is low. Can also use close price for both high and low source

waitForClose (simple bool) : : Considers source for direction change crossover if checked. Else, uses highSource and lowSource.

atrlength (simple int) : : ATR Length

multiplier (simple float) : : ATR Multiplier

atrMaType (simple string) : : Moving Average type for ATR calculation. This can be sma, ema, hma, rma, wma, vwma, swma

Returns: dir : Supertrend direction

supertrend : BuyStop if direction is 1 else SellStop

zsupertrend(zigzagpivots, history, source, highSource, lowSource, waitForClose, atrMaType, atrlength, multiplier)

zsupertrend: Same as zigzag supertrend. But, works on already calculated array rather than Calculating fresh zigzag

Parameters:

zigzagpivots (array) : : Precalculated zigzag pivots

history (simple int) : : number of historical pivots to consider

source (float) : : Default is close. Can Chose custom source

highSource (float) : : Default is high. Can also use close price for both high and low source

lowSource (float) : : Default is low. Can also use close price for both high and low source

waitForClose (simple bool) : : Considers source for direction change crossover if checked. Else, uses highSource and lowSource.

atrMaType (simple string) : : Moving Average type for ATR calculation. This can be sma, ema, hma, rma, wma, vwma, swma

atrlength (simple int) : : ATR Length

multiplier (simple float) : : ATR Multiplier

Returns: dir : Supertrend direction

supertrend : BuyStop if direction is 1 else SellStop

taLibrary "ta"

Collection of all custom and enhanced TA indicators

ma(source, maType, length)

returns custom moving averages

Parameters:

source (float) : Moving Average Source

maType (simple string) : Moving Average Type : Can be sma, ema, hma, rma, wma, vwma, swma, highlow, linreg, median

length (simple int) : Moving Average Length

Returns: moving average for the given type and length

atr(maType, length)

returns ATR with custom moving average

Parameters:

maType (simple string) : Moving Average Type : Can be sma, ema, hma, rma, wma, vwma, swma, highlow, linreg, median

length (simple int) : Moving Average Length

Returns: ATR for the given moving average type and length

atrpercent(maType, length)

returns ATR as percentage of close price

Parameters:

maType (simple string) : Moving Average Type : Can be sma, ema, hma, rma, wma, vwma, swma, highlow, linreg, median

length (simple int) : Moving Average Length

Returns: ATR as percentage of close price for the given moving average type and length

bb(source, maType, length, multiplier, sticky)

returns Bollinger band for custom moving average

Parameters:

source (float) : Moving Average Source

maType (simple string) : Moving Average Type : Can be sma, ema, hma, rma, wma, vwma, swma, highlow, linreg, median

length (simple int) : Moving Average Length

multiplier (float) : Standard Deviation multiplier

sticky (simple bool) : - sticky boundaries which will only change when value is outside boundary.

Returns: Bollinger band with custom moving average for given source, length and multiplier

bbw(source, maType, length, multiplier, sticky)

returns Bollinger bandwidth for custom moving average

Parameters:

source (float) : Moving Average Source

maType (simple string) : Moving Average Type : Can be sma, ema, hma, rma, wma, vwma, swma, highlow, linreg, median

length (simple int) : Moving Average Length

multiplier (float) : Standard Deviation multiplier

sticky (simple bool) : - sticky boundaries which will only change when value is outside boundary.

Returns: Bollinger Bandwidth for custom moving average for given source, length and multiplier

bpercentb(source, maType, length, multiplier, sticky)

returns Bollinger Percent B for custom moving average

Parameters:

source (float) : Moving Average Source

maType (simple string) : Moving Average Type : Can be sma, ema, hma, rma, wma, vwma, swma, highlow, linreg, median

length (simple int) : Moving Average Length

multiplier (float) : Standard Deviation multiplier

sticky (simple bool) : - sticky boundaries which will only change when value is outside boundary.

Returns: Bollinger Percent B for custom moving average for given source, length and multiplier

kc(source, maType, length, multiplier, useTrueRange, sticky)

returns Keltner Channel for custom moving average

Parameters:

source (float) : Moving Average Source

maType (simple string) : Moving Average Type : Can be sma, ema, hma, rma, wma, vwma, swma, highlow, linreg, median

length (simple int) : Moving Average Length

multiplier (float) : Standard Deviation multiplier

useTrueRange (simple bool) : - if set to false, uses high-low.

sticky (simple bool) : - sticky boundaries which will only change when value is outside boundary.

Returns: Keltner Channel for custom moving average for given souce, length and multiplier

kcw(source, maType, length, multiplier, useTrueRange, sticky)

returns Keltner Channel Width with custom moving average

Parameters:

source (float) : Moving Average Source

maType (simple string) : Moving Average Type : Can be sma, ema, hma, rma, wma, vwma, swma, highlow, linreg, median

length (simple int) : Moving Average Length

multiplier (float) : Standard Deviation multiplier

useTrueRange (simple bool) : - if set to false, uses high-low.

sticky (simple bool) : - sticky boundaries which will only change when value is outside boundary.

Returns: Keltner Channel Width for custom moving average

kpercentk(source, maType, length, multiplier, useTrueRange, sticky)

returns Keltner Channel Percent K Width with custom moving average

Parameters:

source (float) : Moving Average Source

maType (simple string) : Moving Average Type : Can be sma, ema, hma, rma, wma, vwma, swma, highlow, linreg, median

length (simple int) : Moving Average Length

multiplier (float) : Standard Deviation multiplier

useTrueRange (simple bool) : - if set to false, uses high-low.

sticky (simple bool) : - sticky boundaries which will only change when value is outside boundary.

Returns: Keltner Percent K for given moving average, source, length and multiplier

dc(length, useAlternateSource, alternateSource, sticky)

returns Custom Donchian Channel

Parameters:

length (simple int) : - donchian channel length

useAlternateSource (simple bool) : - Custom source is used only if useAlternateSource is set to true

alternateSource (float) : - Custom source

sticky (simple bool) : - sticky boundaries which will only change when value is outside boundary.

Returns: Donchian channel

dcw(length, useAlternateSource, alternateSource, sticky)

returns Donchian Channel Width

Parameters:

length (simple int) : - donchian channel length

useAlternateSource (simple bool) : - Custom source is used only if useAlternateSource is set to true

alternateSource (float) : - Custom source

sticky (simple bool) : - sticky boundaries which will only change when value is outside boundary.

Returns: Donchian channel width

dpercentd(length, useAlternateSource, alternateSource, sticky)

returns Donchian Channel Percent of price

Parameters:

length (simple int) : - donchian channel length

useAlternateSource (simple bool) : - Custom source is used only if useAlternateSource is set to true

alternateSource (float) : - Custom source

sticky (simple bool) : - sticky boundaries which will only change when value is outside boundary.

Returns: Donchian channel Percent D

oscillatorRange(source, method, highlowLength, rangeLength, sticky)

oscillatorRange - returns Custom overbought/oversold areas for an oscillator input

Parameters:

source (float) : - Osillator source such as RSI, COG etc.

method (simple string) : - Valid values for method are : sma, ema, hma, rma, wma, vwma, swma, highlow, linreg, median

highlowLength (simple int) : - length on which highlow of the oscillator is calculated

rangeLength (simple int) : - length used for calculating oversold/overbought range - usually same as oscillator length

sticky (simple bool) : - overbought, oversold levels won't change unless crossed

Returns: Dynamic overbought and oversold range for oscillator input

oscillator(type, length, shortLength, longLength, source, highSource, lowSource, method, highlowLength, sticky)

oscillator - returns Choice of oscillator with custom overbought/oversold range

Parameters:

type (simple string) : - oscillator type. Valid values : cci, cmo, cog, mfi, roc, rsi, stoch, tsi, wpr

length (simple int) : - Oscillator length - not used for TSI

shortLength (simple int) : - shortLength only used for TSI

longLength (simple int) : - longLength only used for TSI

source (float) : - custom source if required

highSource (float) : - custom high source for stochastic oscillator

lowSource (float) : - custom low source for stochastic oscillator

method (simple string) : - Valid values for method are : sma, ema, hma, rma, wma, vwma, swma, highlow, linreg, median

highlowLength (simple int) : - length on which highlow of the oscillator is calculated

sticky (simple bool) : - overbought, oversold levels won't change unless crossed

Returns: Oscillator value along with dynamic overbought and oversold range for oscillator input

PitchforkLibrary "Pitchfork"

Pitchfork class

method tostring(this)

Converts PitchforkTypes/Fork object to string representation

Namespace types: Fork

Parameters:

this (Fork) : PitchforkTypes/Fork object

Returns: string representation of PitchforkTypes/Fork

method tostring(this)

Converts Array of PitchforkTypes/Fork object to string representation

Namespace types: array

Parameters:

this (array) : Array of PitchforkTypes/Fork object

Returns: string representation of PitchforkTypes/Fork array

method tostring(this, sortKeys, sortOrder)

Converts PitchforkTypes/PitchforkProperties object to string representation

Namespace types: PitchforkProperties

Parameters:

this (PitchforkProperties) : PitchforkTypes/PitchforkProperties object

sortKeys (bool) : If set to true, string output is sorted by keys.

sortOrder (int) : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

Returns: string representation of PitchforkTypes/PitchforkProperties

method tostring(this, sortKeys, sortOrder)

Converts PitchforkTypes/PitchforkDrawingProperties object to string representation

Namespace types: PitchforkDrawingProperties

Parameters:

this (PitchforkDrawingProperties) : PitchforkTypes/PitchforkDrawingProperties object

sortKeys (bool) : If set to true, string output is sorted by keys.

sortOrder (int) : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

Returns: string representation of PitchforkTypes/PitchforkDrawingProperties

method tostring(this, sortKeys, sortOrder)

Converts PitchforkTypes/Pitchfork object to string representation

Namespace types: Pitchfork

Parameters:

this (Pitchfork) : PitchforkTypes/Pitchfork object

sortKeys (bool) : If set to true, string output is sorted by keys.

sortOrder (int) : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

Returns: string representation of PitchforkTypes/Pitchfork

method createDrawing(this)

Creates PitchforkTypes/PitchforkDrawing from PitchforkTypes/Pitchfork object

Namespace types: Pitchfork

Parameters:

this (Pitchfork) : PitchforkTypes/Pitchfork object

Returns: PitchforkTypes/PitchforkDrawing object created

method createDrawing(this)

Creates PitchforkTypes/PitchforkDrawing array from PitchforkTypes/Pitchfork array of objects

Namespace types: array

Parameters:

this (array) : array of PitchforkTypes/Pitchfork object

Returns: array of PitchforkTypes/PitchforkDrawing object created

method draw(this)

draws from PitchforkTypes/PitchforkDrawing object

Namespace types: PitchforkDrawing

Parameters:

this (PitchforkDrawing) : PitchforkTypes/PitchforkDrawing object

Returns: PitchforkTypes/PitchforkDrawing object drawn

method delete(this)

deletes PitchforkTypes/PitchforkDrawing object

Namespace types: PitchforkDrawing

Parameters:

this (PitchforkDrawing) : PitchforkTypes/PitchforkDrawing object

Returns: PitchforkTypes/PitchforkDrawing object deleted

method delete(this)

deletes underlying drawing of PitchforkTypes/Pitchfork object

Namespace types: Pitchfork

Parameters:

this (Pitchfork) : PitchforkTypes/Pitchfork object

Returns: PitchforkTypes/Pitchfork object deleted

method delete(this)

deletes array of PitchforkTypes/PitchforkDrawing objects

Namespace types: array

Parameters:

this (array) : Array of PitchforkTypes/PitchforkDrawing object

Returns: Array of PitchforkTypes/PitchforkDrawing object deleted

method delete(this)

deletes underlying drawing in array of PitchforkTypes/Pitchfork objects

Namespace types: array

Parameters:

this (array) : Array of PitchforkTypes/Pitchfork object

Returns: Array of PitchforkTypes/Pitchfork object deleted

method clear(this)

deletes array of PitchforkTypes/PitchforkDrawing objects and clears the array

Namespace types: array

Parameters:

this (array) : Array of PitchforkTypes/PitchforkDrawing object

Returns: void

method clear(this)

deletes array of PitchforkTypes/Pitchfork objects and clears the array

Namespace types: array

Parameters:

this (array) : Array of Pitchfork/Pitchfork object

Returns: void

PitchforkDrawingProperties

Pitchfork Drawing Properties object

Fields:

extend (series bool) : If set to true, forks are extended towards right. Default is true

fill (series bool) : Fill forklines with transparent color. Default is true

fillTransparency (series int) : Transparency at which fills are made. Only considered when fill is set. Default is 80

forceCommonColor (series bool) : Force use of common color for forks and fills. Default is false

commonColor (series color) : common fill color. Used only if ratio specific fill colors are not available or if forceCommonColor is set to true.

PitchforkDrawing

Pitchfork drawing components

Fields:

medianLine (Line type from Trendoscope/Drawing/2) : Median line of the pitchfork

baseLine (Line type from Trendoscope/Drawing/2) : Base line of the pitchfork

forkLines (array type from Trendoscope/Drawing/2) : fork lines of the pitchfork

linefills (array type from Trendoscope/Drawing/2) : Linefills between forks

Fork

Fork object property

Fields:

ratio (series float) : Fork ratio

forkColor (series color) : color of fork. Default is blue

include (series bool) : flag to include the fork in drawing. Default is true

PitchforkProperties

Pitchfork Properties

Fields:

forks (array) : Array of Fork objects

type (series string) : Pitchfork type. Supported values are "regular", "schiff", "mschiff", Default is regular

inside (series bool) : Flag to identify if to draw inside fork. If set to true, inside fork will be drawn

Pitchfork

Pitchfork object

Fields:

a (chart.point) : Pivot Point A of pitchfork

b (chart.point) : Pivot Point B of pitchfork

c (chart.point) : Pivot Point C of pitchfork

properties (PitchforkProperties) : PitchforkProperties object which determines type and composition of pitchfork

dProperties (PitchforkDrawingProperties) : Drawing properties for pitchfork

lProperties (LineProperties type from Trendoscope/Drawing/2) : Common line properties for Pitchfork lines

drawing (PitchforkDrawing) : PitchforkDrawing object

SnowdexUtilsLibrary "SnowdexUtils"

the various function that often use when create a strategy trading.

f_backtesting_date(train_start_date, train_end_date, test_date, deploy_date)

Backtesting within a specific window based on deployment and testing dates.

Parameters:

train_start_date (int) : the start date for training the strategy.

train_end_date (int) : the end date for training the strategy.

test_date (bool) : if true, backtests within the period from `train_end_date` to the current time.

deploy_date (bool) : if true, the strategy backtests up to the current time.

Returns: given time falls within the specified window for backtesting.

f_init_ma(ma_type, source, length)

Initializes a moving average based on the specified type.

Parameters:

ma_type (simple string) : the type of moving average (e.g., "RMA", "EMA", "SMA", "WMA").

source (float) : the input series for the moving average calculation.

length (simple int) : the length of the moving average window.

Returns: the calculated moving average value.

f_init_tp(side, entry_price, rr, sl_open_position)

Calculates the target profit based on entry price, risk-reward ratio, and stop loss. The formula is `tp = entry price + (rr * (entry price - stop loss))`.

Parameters:

side (bool) : the trading side (true for long, false for short).

entry_price (float) : the entry price of the position.

rr (float) : the risk-reward ratio.

sl_open_position (float) : the stop loss price for the open position.

Returns: the calculated target profit value.

f_round_up(number, decimals)

Rounds up a number to a specified number of decimals.

Parameters:

number (float)

decimals (int)

Returns: The rounded-up number.

f_get_pip_size()

Calculates the pip size for the current instrument.

Returns: Pip size adjusted for Forex instruments or 1 for others.

f_table_get_position(value)

Maps a string to a table position constant.

Parameters:

value (string) : String representing the desired position (e.g., "Top Right").

Returns: The corresponding position constant or `na` for invalid values.

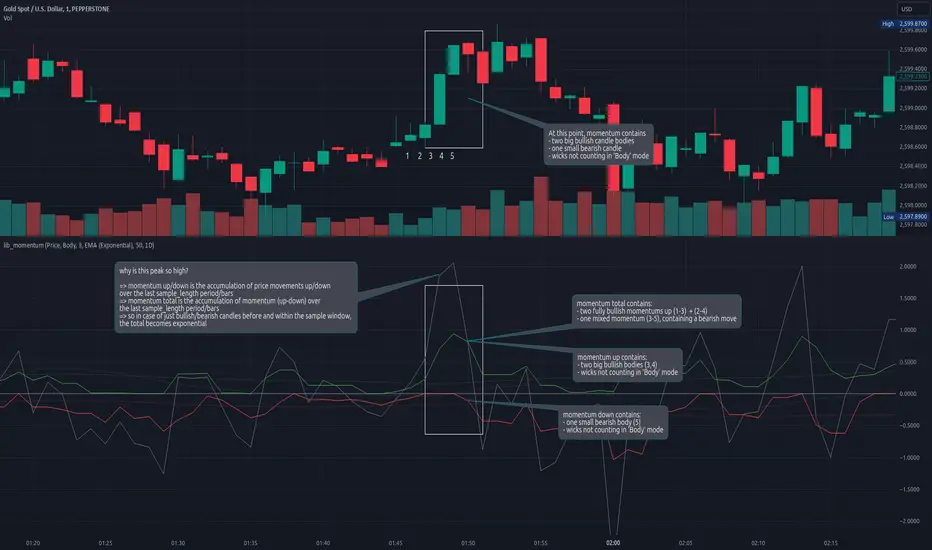

lib_momentumLibrary "lib_momentum"

This library calculates the momentum, derived from a sample range of prior candles. Depending on set MomentumType it either deduces the momentum from the price, volume, or a product of both. If price/product are selected, you can choose from SampleType if only candle body, full range from high to low or a combination of both (body counts full, wicks half for each direction) should be used. Optional: You can choose to normalize the results, dividing each value by its average (normalization_ma_length, normalization_ma). This will allow comparison between different instruments. For the normalization Moving Average you can choose any currently supported in my lib_no_delay.

get_momentum(momentum_type, sample_type, sample_length, normalization_ma_length, normalization_ma)

Parameters:

momentum_type (series MomentumType) : select one of MomentumType. to sample the price, volume or a product of both

sample_type (series SampleType) : select one of SampleType. to sample the body, total range from high to low or a combination of both (body count full, wicks half for each direction)

sample_length (simple int) : how many candles should be sampled (including the current)

normalization_ma_length (simple int) : if you want to normalize results (momentum / momentum average) this sets the period for the average. (default = 0 => no normalization)

normalization_ma (simple MovingAverage enum from robbatt/lib_no_delay/9) : is the type of moving average to normalize / compare with

Returns: returns the current momentum where the total line is not just (up - down) but also sampled over the sample_length and can therefore be used as trend indicator. If up/down fail to reach total's level it's a sign of decreasing momentum, if up/down exceed total the trend it's a sign of increasing momentum.

RawCuts_01Library "RawCuts_01"

A collection of functions by:

mutantdog

The majority of these are used within published projects, some useful variants have been included here aswell.

This is volume one consisting mainly of smaller functions, predominantly the filters and standard deviations from Weight Gain 4000.

Also included at the bottom are various snippets of related code for demonstration. These can be copied and adjusted according to your needs.

A full up-to-date table of contents is located at the top of the main script.

WEIGHT GAIN FILTERS

A collection of moving average type filters with adjustable volume weighting.

Based upon the two most common methods of volume weighting.

'Simple' uses the standard method in which a basic VWMA is analogous to SMA.

'Elastic' uses exponential method found in EVWMA which is analogous to RMA.

Volume weighting is applied according to an exponent multiplier of input volume.

0 >> volume^0 (unweighted), 1 >> volume^1 (fully weighted), use float values for intermediate weighting.

Additional volume filter switch for smoothing of outlier events.

DIVA MODULAR DEVIATIONS

A small collection of standard and absolute deviations.

Includes the weightgain functionality as above.

Basic modular functionality for more creative uses.

Optional input (ct) for external central tendency (aka: estimator).

Can be assigned to alternative filter or any float value. Will default to internal filter when no ct input is received.

Some other useful or related functions included at the bottom along with basic demonstration use.

weightgain_sma(src, len, xVol, fVol)

Simple Moving Average (SMA): Weight Gain (Simple Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

Returns: Standard Simple Moving Average with Simple Weight Gain applied.

weightgain_hsma(src, len, xVol, fVol)

Harmonic Simple Moving Average (hSMA): Weight Gain (Simple Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

Returns: Harmonic Simple Moving Average with Simple Weight Gain applied.

weightgain_gsma(src, len, xVol, fVol)

Geometric Simple Moving Average (gSMA): Weight Gain (Simple Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

Returns: Geometric Simple Moving Average with Simple Weight Gain applied.

weightgain_wma(src, len, xVol, fVol)

Linear Weighted Moving Average (WMA): Weight Gain (Simple Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

Returns: Basic Linear Weighted Moving Average with Simple Weight Gain applied.

weightgain_hma(src, len, xVol, fVol)

Hull Moving Average (HMA): Weight Gain (Simple Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

Returns: Basic Hull Moving Average with Simple Weight Gain applied.

diva_sd_sma(src, len, xVol, fVol, ct)

Standard Deviation (SD SMA): Diva / Weight Gain (Simple Volume)

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

ct (float) : Central tendency (optional, na = bypass). Internal: weightgain_sma().

Returns:

diva_sd_wma(src, len, xVol, fVol, ct)

Standard Deviation (SD WMA): Diva / Weight Gain (Simple Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

ct (float) : Central tendency (optional, na = bypass). Internal: weightgain_wma().

Returns:

diva_aad_sma(src, len, xVol, fVol, ct)

Average Absolute Deviation (AAD SMA): Diva / Weight Gain (Simple Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

ct (float) : Central tendency (optional, na = bypass). Internal: weightgain_sma().

Returns:

diva_aad_wma(src, len, xVol, fVol, ct)

Average Absolute Deviation (AAD WMA): Diva / Weight Gain (Simple Volume) .

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

ct (float) : Central tendency (optional, na = bypass). Internal: weightgain_wma().

Returns:

weightgain_ema(src, len, xVol, fVol)

Exponential Moving Average (EMA): Weight Gain (Elastic Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

Returns: Exponential Moving Average with Elastic Weight Gain applied.