Nifty Intraday Analysis for 11th November 2025NSE:NIFTY

Index has resistance near 25750 – 25800 range and if index crosses and sustains above this level then may reach near 26000 – 26050 range.

Nifty has immediate support near 25400 – 25350 range and if this support is broken then index may tank near 25150 – 25100 range.

Contains image

The Next Big Altcoin Reversal? $CAKE Ready for a Massive Bull RuThe Next Big Altcoin Reversal? NASDAQ:CAKE Ready for a Massive Bull Run

#CAKE is breaking out from a strong falling wedge after a long accumulation phase. Smart money is showing interest as price shifts from bearish to bullish structure.

Support: $2.30 – $2.50

Resistance: $9.30 / $18.70 / $38.40

A weekly close above $3 could trigger a major trend reversal with potential upside of 900%+ in the long term.

SMC & ICT Insights:

Break of Structure confirmed on HTF

FVG support around $2.40–$2.55

Liquidity targets above $9.30 and $18.70

CAKE looks ready for a multi-month bullish run if it holds current levels.

NFA & DYOR

How to Use Candlestick Patterns in TradingA candlestick represents price movement for a given time frame.

It shows:

Open price – where the candle started

Close price – where the candle ended

High price – the top point (shadow or wick)

Low price – the bottom point (shadow or wick)

👉 If the close price > open price, it’s a bullish candle (often green or white).

👉 If the close price < open price, it’s a bearish candle (often red or black).

Understanding The Premium Chart Patterns 1. Hedging: To protect against losses in existing positions.

Example: If you own Nifty stocks but fear a market fall, buying a put option acts as insurance.

2. Speculation: To profit from expected price movements with limited risk.

Example: Buying a call if you expect prices to rise.

3. Income Generation: Selling (writing) options to earn a premium — the price paid by the buyer of the option.

Advanced Option Trading StrategiesHedging and Portfolio Protection Strategies

Options are not just for speculation; they are powerful tools for hedging existing stock portfolios. Hedging means protecting against potential losses due to adverse price moves.

Popular Hedging Techniques:

Protective Put: Buy a put option against long stock holdings to limit downside.

Collar Strategy: Hold stock, sell a call, and buy a put — ideal when you expect limited movement.

Index Options for Portfolio Hedge: Traders holding multiple stocks often hedge using Nifty or Bank Nifty puts instead of individual stock options.

Part 12 Trading Master ClassImportance of Time Decay (Theta)

Another vital concept in options trading is Theta, which measures how much the value of an option decreases as it approaches expiry — this is called time decay.

Buyers of options lose value daily because the time value erodes.

Sellers (writers) benefit from time decay as they collect premium that melts away if the market remains range-bound.

Part 11 Trading Master ClassTaxation and Regulations in India

In India:

Profits from options trading are treated as business income.

Traders must file under F&O income while filing Income Tax.

Options trading is regulated by SEBI and executed through NSE/BSE.

Always ensure you trade only through authorized brokers and maintain proper records for compliance.

Part 9 Trading Master ClassChoosing the Right Strategy

Selecting the right options strategy depends on three factors:

Market Outlook:

Bullish → Long Call, Bull Call Spread, Short Put

Bearish → Long Put, Bear Put Spread, Covered Call

Neutral → Iron Condor, Butterfly, Short Straddle

Volatility:

High volatility → Buy options (Straddle, Strangle)

Low volatility → Sell options (Condor, Credit spreads)

Risk Appetite:

Low-risk → Spreads

Medium-risk → Covered/Protective positions

High-risk → Naked calls/puts

Part 10 Trade Like InstitutionsAdvanced Option Strategies

a) Butterfly Spread

Market View: Very Neutral (Expecting Minimal Movement)

Action: Buy 1 lower strike call + Sell 2 middle strike calls + Buy 1 higher strike call.

It profits if the market remains near the middle strike.

Risk: Limited.

Reward: Limited but high probability of success.

b) Calendar Spread

Market View: Expecting Low Short-Term Volatility but High Long-Term Movement

Action: Sell near-month option + Buy next-month option of same strike.

Used by professional traders to take advantage of time decay differences between expiries.

Part 8 Trading master Class Types of Option Trading Strategies

Options strategies are broadly divided into single-leg and multi-leg strategies.

Single-leg strategies: Involve buying or selling one option.

Multi-leg strategies: Combine two or more options (calls and puts) to create structured trades for specific market conditions.

Let’s discuss each category in detail.

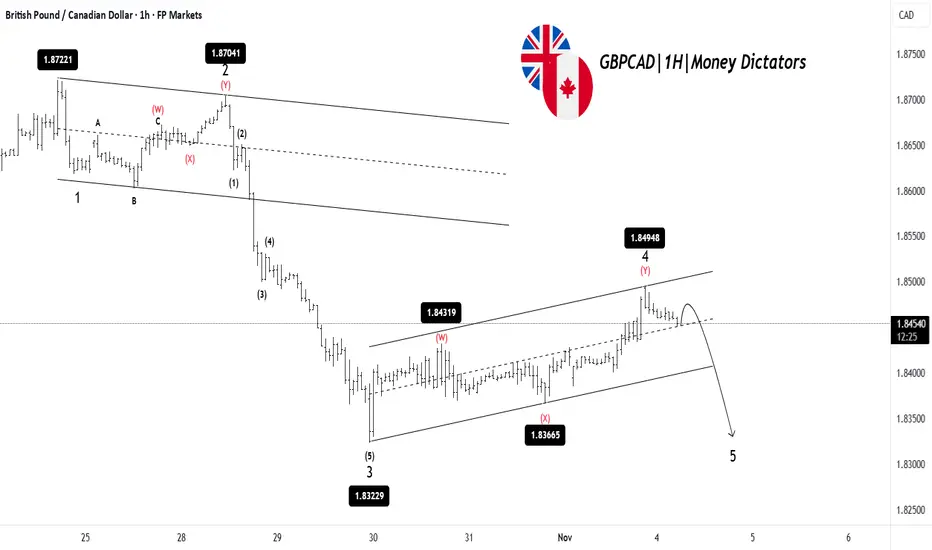

GBPCAD: Bears Ready to Push Into Wave 5GBPCAD has completed a clear 1-2-3 move to the downside, followed by a corrective Wave 4 that has pushed the price higher inside a rising channel. This correction now looks nearly complete, as the price is struggling to break above the resistance. Once Wave 4 is finished, the chart suggests a final drop into Wave 5 toward the lower support zone. That would complete the overall bearish structure before any larger reversal can happen. In simple terms: correction is almost done → one more leg down expected.

Stay tuned!

@Money_Dictators

Thank you :)

Technical Analysis and Chart PatternsIntroduction

Technical analysis is a cornerstone of modern trading and investing. It involves studying price charts and market data to forecast future price movements. Unlike fundamental analysis, which focuses on financial statements, earnings, and economic indicators, technical analysis revolves around price action, volume, and market psychology. It assumes that all relevant information is already reflected in the price, and history tends to repeat itself through recognizable chart patterns and trends.

Core Principles of Technical Analysis

Technical analysis operates on three main principles:

Price Discounts Everything:

All known information—economic data, earnings, market sentiment, or political events—is already factored into the stock price. Therefore, analyzing price action alone can reveal the collective behavior of market participants.

Price Moves in Trends:

Markets rarely move randomly. Prices tend to move in identifiable trends—upward, downward, or sideways. Recognizing these trends early allows traders to position themselves advantageously.

History Repeats Itself:

Human psychology drives markets—fear, greed, hope, and panic repeat across generations. Therefore, patterns formed in the past tend to recur, providing clues about future price action.

Types of Technical Charts

Before identifying patterns, one must understand chart types used in technical analysis:

Line Chart:

It connects closing prices over a specific period, providing a simple view of the trend.

Bar Chart:

Each bar represents the open, high, low, and close (OHLC) for a given period. It gives more insight than a line chart.

Candlestick Chart:

The most popular chart among traders, candlesticks visually show market psychology. A bullish candle (close > open) is often green or white, while a bearish candle (close < open) is red or black.

Candlestick formations help identify reversals and continuations in price.

Trend Analysis

A trend is the general direction of price movement. It can be classified as:

Uptrend: Series of higher highs and higher lows.

Downtrend: Series of lower highs and lower lows.

Sideways/Range: Prices oscillate between support and resistance.

Traders use trendlines and channels to visualize and trade along the trend. The saying “Trend is your friend” highlights the importance of trading with the prevailing direction rather than against it.

Key Tools in Technical Analysis

Support and Resistance Levels:

Support: A price level where buying pressure prevents further decline.

Resistance: A level where selling pressure halts price advances.

When a resistance is broken, it can turn into new support and vice versa.

Moving Averages:

They smooth out price data to identify trend direction.

Simple Moving Average (SMA) – average of closing prices over a period.

Exponential Moving Average (EMA) – gives more weight to recent prices.

Common crossovers like the Golden Cross (short-term MA crosses above long-term MA) and Death Cross (short-term MA crosses below long-term MA) indicate trend reversals.

Volume Analysis:

Volume measures market participation. Increasing volume confirms the strength of a trend, while declining volume may signal weakening momentum.

Indicators and Oscillators:

Tools like Relative Strength Index (RSI), Moving Average Convergence Divergence (MACD), Bollinger Bands, and Stochastic Oscillator help identify overbought/oversold conditions, momentum shifts, and trend confirmation.

Chart Patterns in Technical Analysis

Chart patterns are visual formations created by price movements. They represent the psychological struggle between buyers and sellers and help traders predict potential outcomes.

Patterns are generally divided into reversal patterns and continuation patterns.

1. Reversal Patterns

These indicate that a current trend is likely to change direction.

a. Head and Shoulders

One of the most reliable reversal patterns.

Appears at the end of an uptrend.

Consists of three peaks: a higher middle peak (head) between two smaller ones (shoulders).

Neckline break confirms a bearish reversal.

Inverse Head and Shoulders appears at the bottom of a downtrend and signals a bullish reversal.

b. Double Top and Double Bottom

Double Top: Price hits a resistance twice, forming an “M” shape, signaling a bearish reversal.

Double Bottom: Price touches support twice, forming a “W” shape, indicating a bullish reversal.

c. Triple Top and Triple Bottom

Similar to double patterns but with three peaks or troughs. They confirm stronger reversals after multiple failed attempts to break support/resistance.

d. Rounding Bottom (Saucer Bottom)

Indicates a gradual shift from bearish to bullish sentiment over time. Common in long-term trend reversals.

e. Falling and Rising Wedges

Falling Wedge: Occurs during a downtrend and signals a bullish reversal.

Rising Wedge: Forms during an uptrend and signals a bearish reversal.

The breakout direction typically opposes the wedge slope.

2. Continuation Patterns

These suggest that the existing trend will continue after a brief pause or consolidation.

a. Triangles

Ascending Triangle: Horizontal resistance with rising support. Usually bullish.

Descending Triangle: Horizontal support with falling resistance. Usually bearish.

Symmetrical Triangle: Converging trendlines; breakout can occur in either direction.

b. Flags and Pennants

Flags: Small rectangular consolidations that form after a sharp move (flagpole). Breakout in the same direction resumes the prior trend.

Pennants: Similar to flags but shaped like small symmetrical triangles.

c. Rectangles (Price Channels)

When price oscillates between parallel support and resistance lines, it indicates accumulation or distribution. A breakout determines the next direction.

d. Cup and Handle

Looks like a tea cup: a rounded “cup” followed by a small “handle” consolidation. A breakout above the handle signals bullish continuation.

Candlestick Patterns

In addition to chart patterns, candlestick patterns offer short-term trading signals:

Bullish Engulfing: Large bullish candle engulfs the previous bearish candle—signals buying momentum.

Bearish Engulfing: Large bearish candle engulfs the previous bullish one—signals selling pressure.

Doji: Open and close prices are nearly equal, indicating indecision.

Hammer & Inverted Hammer: Found at bottoms, indicating potential reversals.

Shooting Star: Appears at tops, suggesting bearish reversal.

Combining Patterns with Indicators

Professional traders often combine chart patterns with technical indicators for confirmation.

Example:

A head and shoulders pattern confirmed by falling RSI strengthens the bearish outlook.

A cup and handle confirmed by rising volume adds validity to a bullish move.

This multi-factor approach reduces false signals and increases accuracy.

Advantages of Technical Analysis

Quick Decision-Making: Real-time charts provide instant trading opportunities.

Universal Application: Works across stocks, forex, commodities, and crypto.

Captures Market Psychology: Reflects fear and greed through patterns.

Supports Short-Term Trading: Ideal for day traders and swing traders.

Limitations of Technical Analysis

Subjectivity: Two traders may interpret the same chart differently.

False Breakouts: Patterns may fail, especially in volatile markets.

Lagging Indicators: Some tools like moving averages react after price changes.

No Fundamental Insight: It ignores earnings, news, and macroeconomic data.

Conclusion

Technical analysis is both an art and a science. By studying chart patterns, trends, and indicators, traders can anticipate potential price moves with greater confidence. However, success in technical analysis demands discipline, patience, and risk management. Patterns don’t guarantee results; they only increase probabilities. Combining chart patterns with volume analysis, market context, and proper stop-loss strategies creates a strong foundation for consistent profitability.

Ultimately, mastering technical analysis means understanding how market psychology shapes price movements—and using that knowledge to stay one step ahead of the crowd.

Private vs Public Banks in the Indian Market1. Ownership and Management Structure

The fundamental difference between public and private banks lies in ownership.

Public Sector Banks (PSBs) are majority-owned by the Government of India, which holds more than 50% of their equity. The government plays a key role in appointing top executives and formulating policy directions. Examples include State Bank of India (SBI), Punjab National Bank (PNB), Bank of Baroda (BoB), and Canara Bank.

Private Sector Banks (PVBs), on the other hand, are owned and managed by private entities or individuals, with the government having little or no control. The management is typically professional, and boards are accountable to private shareholders. Major private banks include HDFC Bank, ICICI Bank, Axis Bank, Kotak Mahindra Bank, and IndusInd Bank.

This difference in ownership affects how both types of banks operate, their decision-making processes, and their responsiveness to market conditions.

2. Historical Background

Public sector banks form the backbone of India’s traditional banking system. They gained prominence after bank nationalization in 1969 and 1980, which brought 20 major banks under government control. The aim was to ensure that banking services reached rural and underbanked areas, supporting agriculture, small industries, and social development.

Private banks, however, emerged in two waves:

The first phase included old private banks such as Karur Vysya Bank, South Indian Bank, and Federal Bank, which were regional and limited in scale.

The second phase, or the “new generation” private banks, began after the economic liberalization of 1991, when the Reserve Bank of India (RBI) allowed new private players to enter. Banks like HDFC Bank, ICICI Bank, and Axis Bank brought innovation, technology, and competition to the market.

3. Operational Efficiency and Technology

Private sector banks are widely recognized for their efficiency and technological advancement. They were pioneers in introducing digital banking, internet and mobile apps, ATMs, 24/7 customer service, and AI-based financial solutions. Their focus on automation and quick service appeals especially to urban customers.

Public banks, though initially slower to adopt technology, have made significant progress in recent years. Initiatives like YONO by SBI, Bank of Baroda’s digital transformation, and PSB Alliance have modernized public banking. However, public banks still face challenges due to their vast legacy systems and bureaucratic procedures.

4. Customer Service and Experience

Private banks are often perceived as offering superior customer service, with faster processing times, personalized products, and proactive relationship management. Their staff is trained to focus on efficiency and customer satisfaction.

Public banks, however, have traditionally been known for longer processing times and formal procedures. Yet, they provide an essential service to a larger section of society, especially in rural and semi-urban areas where private banks may not have strong penetration. PSBs are more committed to social welfare schemes such as Jan Dhan Yojana, Mudra loans, and agricultural credit programs.

5. Market Reach and Financial Inclusion

In terms of reach, public sector banks hold a dominant position. They have thousands of branches across rural India, ensuring that even remote populations have access to banking facilities. For instance, SBI alone accounts for more than 20% of India’s total banking network.

Private banks, conversely, focus primarily on urban and metropolitan regions where customers demand faster, technology-driven services. However, they are now expanding into Tier 2 and Tier 3 cities to capture a growing middle-class market.

6. Profitability and Performance

Private banks usually exhibit higher profitability, better asset quality, and more stable returns. Their operational flexibility, low non-performing asset (NPA) ratios, and efficiency in cost management contribute to superior financial performance. For instance, banks like HDFC and ICICI consistently report high return on assets (ROA) and return on equity (ROE).

Public banks, due to their social obligations and exposure to priority sectors, often face higher NPAs and lower profitability. Lending to agriculture, infrastructure, and small enterprises—though socially vital—sometimes leads to defaults. However, government support through recapitalization and mergers (like SBI with its associate banks) helps maintain their financial stability.

7. Lending Patterns and Risk Management

Public banks prioritize social and developmental objectives, lending to priority sectors such as agriculture, small industries, and low-income groups. They are also instrumental in implementing government schemes like PMEGP, Stand-Up India, and PM Kisan.

Private banks focus more on profitable segments such as retail loans, home loans, credit cards, and wealth management. They employ advanced risk assessment tools, AI-driven credit scoring, and market-based pricing, which help reduce bad loans and maintain better credit discipline.

8. Employment and Work Culture

Public sector banks provide job security, stable career paths, and government-linked benefits. They attract candidates through national-level exams conducted by IBPS or SBI. However, the work culture can be bureaucratic, hierarchical, and slower in decision-making.

Private banks offer performance-based incentives, faster promotions, and modern work environments, but job security is lower. They emphasize productivity, targets, and results, often leading to higher stress levels but better pay for top performers.

9. Regulatory Environment

Both public and private banks are regulated by the Reserve Bank of India (RBI) and governed by the Banking Regulation Act, 1949. However, PSBs are also accountable to the Ministry of Finance and the Parliament of India, which increases oversight but sometimes limits autonomy. Private banks enjoy greater independence in policy decisions but must adhere strictly to RBI norms.

10. Public Trust and Perception

Public banks enjoy a high level of trust among citizens, especially older generations and rural populations, because of government backing. Depositors believe their money is safe, even if the bank faces trouble, as the government is expected to intervene.

Private banks are viewed as modern, efficient, and customer-friendly, but public confidence fluctuates based on market performance. However, strong brands like HDFC Bank and ICICI Bank have built reputations rivaling public banks in reliability.

11. Future Trends and Outlook

The future of India’s banking sector lies in coexistence and collaboration between public and private players.

Public banks are likely to focus on financial inclusion, rural expansion, and implementation of government initiatives.

Private banks will continue to drive technological innovation, digital lending, and customer-centric growth.

Additionally, the rise of fintech companies, digital payments platforms (like Paytm and PhonePe), and neo-banks is pushing both sectors toward modernization and customer-focused strategies.

Government-led reforms such as bank mergers, recapitalization packages, and privatization plans indicate an evolving structure aimed at improving competitiveness and efficiency. As India’s economy grows, both public and private banks will play complementary roles in supporting national development and financial stability.

Conclusion

In summary, public sector banks represent the traditional, inclusive, and socially driven side of Indian banking, while private sector banks symbolize innovation, efficiency, and profit-oriented growth. Each has its strengths: public banks bring trust, accessibility, and social responsibility, while private banks bring technology, speed, and superior service quality.

The Indian market thrives on this balance — where government-backed institutions ensure inclusive development and private banks drive modernization and competition. Together, they form a robust dual system that continues to evolve, reflecting the dynamic needs of a rapidly developing economy.

Relative Strength Index (RSI) Indicator Secrets1. The Hidden Meaning Behind RSI Levels

Most traders use the 70/30 rule blindly. In reality, RSI levels are relative, not absolute. For instance:

In a strong uptrend, RSI can remain above 70 for a long period — this does not mean the market will immediately reverse. It often indicates strong bullish momentum.

In a downtrend, RSI can stay below 30 for an extended time — signaling strong bearish pressure, not necessarily an immediate bounce.

Secret Tip:

Adjust your RSI levels based on market conditions:

Bullish market: Use RSI zones of 40–80 (support around 40, resistance around 80).

Bearish market: Use RSI zones of 20–60 (resistance around 60, support around 20).

By doing this, you interpret RSI in the context of trend strength rather than treating it as an isolated signal.

2. RSI as a Trend Identifier

One of the most overlooked uses of RSI is trend confirmation. Traders often rely on moving averages or price patterns to identify trends, but RSI can do this more efficiently.

In uptrends, RSI tends to stay above 40 and frequently reach 70–80.

In downtrends, RSI remains below 60 and often hits 20–30.

Secret Insight:

If RSI repeatedly bounces from the 40–50 zone during a price pullback, it suggests that the uptrend is healthy. Conversely, if RSI fails to move above 60 during rallies, it signals weakness in the market.

This method helps traders stay with the trend longer, instead of prematurely exiting a position when RSI crosses traditional overbought or oversold levels.

3. RSI Divergence – The Ultimate Reversal Signal

RSI divergence is one of the strongest signals for trend reversal. It occurs when the price makes a new high or low that isn’t confirmed by the RSI.

Bullish Divergence: Price makes a lower low, but RSI makes a higher low — signaling potential upward reversal.

Bearish Divergence: Price makes a higher high, but RSI makes a lower high — indicating possible downward reversal.

Secret Tip:

For divergence to be effective, it must occur after a strong trend and be confirmed by volume or candlestick patterns (like Doji, hammer, or engulfing). Many traders lose money by trading every small divergence — patience is key.

Additionally, hidden divergence can predict trend continuation:

Hidden Bullish Divergence: RSI makes a lower low, but price makes a higher low → continuation of uptrend.

Hidden Bearish Divergence: RSI makes a higher high, but price makes a lower high → continuation of downtrend.

Combining regular and hidden divergences can give traders early entry signals and improve accuracy.

4. RSI Swing Rejections: The Secret Entry Technique

Welles Wilder’s original writings described an advanced RSI technique called “Swing Rejection”, which most traders overlook.

A bullish swing rejection occurs when:

RSI drops below 30 (oversold zone).

It rises above 30.

Pulls back but stays above 30.

Then breaks its previous high.

This pattern signals a strong bullish reversal — often before the price fully turns up.

A bearish swing rejection is the opposite:

RSI rises above 70.

Falls below 70.

Rebounds but fails to cross 70 again.

Then breaks its prior low — confirming weakness.

Secret Insight:

Swing rejections filter out false overbought/oversold signals and identify high-probability turning points in the market.

5. RSI with Multiple Time Frames

Professional traders rarely rely on a single RSI setting or timeframe. Instead, they confirm RSI signals across multiple timeframes.

For example:

If the daily RSI is oversold but the weekly RSI is still in a downtrend, the bounce may be short-lived.

When both daily and weekly RSI align in the same direction, it indicates a powerful trend reversal or continuation.

Secret Tip:

Use RSI(14) on higher timeframes (daily/weekly) for trend bias, and RSI(7) or RSI(9) on lower timeframes (hourly or 4-hour) for precise entries.

6. RSI and Moving Averages – A Smart Combination

Combining RSI with moving averages creates a more reliable trading system. For example:

Use a 50-period moving average to determine the trend direction.

Trade RSI signals only in the direction of the moving average.

Example:

If the price is above the 50-MA and RSI bounces from 40 → it’s a strong buy signal.

If the price is below the 50-MA and RSI drops from 60 → it’s a strong sell signal.

This combination filters out false signals and aligns trades with the dominant market trend.

7. RSI Range Shifts – The Professional Secret

A rarely discussed RSI secret is the concept of range shifts. In a strong uptrend, RSI tends to move between 40–80 instead of 30–70. In a strong downtrend, it shifts between 20–60. Recognizing this range shift early helps traders identify when the market transitions from sideways to trending behavior.

When RSI consistently fails to fall below 40 and pushes above 70, it confirms that bulls control the market. Conversely, when RSI struggles to rise above 60 and keeps hitting 30, bears dominate.

Spotting a range shift early can help you enter trends sooner and ride them longer.

8. Customizing RSI Periods for Different Assets

Most traders use the default 14-period RSI. However, adjusting the period can dramatically change its responsiveness:

Shorter RSI (5 or 7): More sensitive, gives early signals but more noise.

Longer RSI (20 or 30): Smoother, fewer false signals but more lag.

Secret Tip:

For volatile instruments like cryptocurrencies or small-cap stocks, use a shorter RSI (7–10).

For stable assets like large-cap stocks or indices, use longer RSI (14–21).

Customizing RSI settings according to volatility improves accuracy and reduces whipsaws.

9. Psychological Secrets of RSI

At its core, RSI reflects market psychology — the tug-of-war between buyers and sellers. When RSI rises above 70, it shows traders’ greed; when it falls below 30, it reveals fear. Understanding this helps you trade in the opposite direction of crowd emotions.

The best traders use RSI not just as a technical tool, but as a window into trader sentiment. Combining RSI readings with support/resistance zones or volume analysis offers a powerful edge.

10. Conclusion

The RSI indicator is far more than a simple overbought/oversold tool. Its true strength lies in understanding context, trend structure, divergence, and range behavior. By mastering RSI’s hidden secrets — such as swing rejections, range shifts, and multiple timeframe confirmations — traders can dramatically improve accuracy and timing.

When used intelligently, RSI reveals the rhythm of market momentum and helps traders ride trends, spot reversals, and stay on the right side of price action. Like all tools, it works best when combined with sound risk management, patience, and discipline — the true secrets behind profitable trading.

Artificial Intelligence (AI) has Revolutionized1. Introduction to AI in Trading

AI refers to the simulation of human intelligence through machines that can analyze data, learn from it, and make decisions with minimal human intervention. In trading, AI systems are designed to interpret large volumes of market data, recognize patterns, and execute trades based on pre-defined strategies or learned behaviors. These systems use techniques like machine learning, deep learning, and natural language processing (NLP) to improve performance over time.

Before the AI era, traders relied on intuition, experience, and manual technical analysis. They studied indicators like moving averages, RSI, and MACD, spending hours identifying potential entry and exit points. Today, AI can perform the same analysis within seconds — and with greater precision.

2. How AI Simplifies Trading

AI simplifies trading in multiple ways — from data analysis to strategy automation and risk management. Let’s break it down:

a. Data Processing Power

Markets generate massive amounts of data every second — stock prices, trading volumes, economic indicators, and news headlines. Humans can’t process such data in real time, but AI systems can. They analyze historical and live data simultaneously to identify trends, correlations, and anomalies.

For example, an AI algorithm can scan millions of trades across multiple exchanges to find a small arbitrage opportunity — something no human could do manually.

b. Automated Trading Systems

AI-powered bots can execute trades automatically based on predefined rules or predictive models. These algorithmic trading systems remove emotional decision-making — a common pitfall for human traders.

Once trained, an AI system can:

Identify potential trade setups

Execute buy/sell orders instantly

Adjust position sizes based on risk

Manage stop-loss and take-profit levels

This automation makes trading faster, more efficient, and less stressful.

c. Predictive Analysis

AI’s ability to learn from historical data helps forecast future price movements. Machine learning models use techniques like regression analysis, neural networks, or reinforcement learning to predict market direction.

For example, an AI might recognize that when a specific stock’s moving average crosses above its long-term average and news sentiment is positive, prices tend to rise. The AI can then act on this pattern automatically.

d. Sentiment Analysis

Markets are heavily influenced by news, social media, and global events. AI systems equipped with NLP can scan thousands of news articles, tweets, and financial reports to gauge market sentiment.

If the AI detects positive sentiment around a company, it might increase buying positions. Conversely, negative news or uncertainty could trigger sell orders. This allows traders to act before the broader market reacts.

e. Risk Management

AI doesn’t just trade — it also protects capital. Advanced systems monitor volatility, exposure, and portfolio balance. If risk levels exceed predefined limits, the AI can adjust trades automatically to minimize losses.

For instance, during sudden market crashes, AI can liquidate risky positions or shift funds into safer assets — all within milliseconds.

3. Types of AI-Based Trading Strategies

AI simplifies different trading styles, whether you’re a short-term day trader or a long-term investor.

a. Algorithmic Trading

Algorithms follow structured rules based on price, timing, and quantity. AI enhances these algorithms with adaptive learning, meaning strategies evolve with changing market conditions.

b. High-Frequency Trading (HFT)

HFT uses AI to execute thousands of trades per second to profit from minute price discrepancies. Only AI systems can operate at such speed and accuracy.

c. Quantitative Trading

Quant traders rely on mathematical models. AI refines these models using machine learning, improving accuracy with each trade.

d. Sentiment-Based Trading

AI reads emotions in the market using NLP, helping traders anticipate how public perception affects asset prices.

e. Portfolio Optimization

AI continuously assesses the risk-reward ratio of assets in a portfolio, rebalancing positions for optimal returns.

4. Benefits of AI in Trading

AI provides several clear advantages that make trading easier, smarter, and more profitable:

a. Speed and Efficiency

AI can process information faster than any human, allowing near-instant trade execution — a critical advantage in fast-moving markets.

b. Accuracy and Consistency

Unlike humans, AI doesn’t tire, panic, or act emotionally. It follows logic and data, ensuring consistent execution of strategies.

c. Learning and Improvement

Through machine learning, AI systems continuously adapt to new patterns. Each trade provides more data for the AI to learn from and refine its decisions.

d. Accessibility for Retail Traders

Previously, algorithmic and quantitative trading were available only to institutions. Today, retail traders can access AI-powered tools through trading platforms like Zerodha Streak, Tradetron, 5paisa Algo, or MetaTrader with AI plugins. These platforms make automation simple — no coding required.

e. 24/7 Trading

AI can monitor global markets around the clock — from U.S. stocks to Indian derivatives to cryptocurrency exchanges — ensuring no opportunity is missed.

5. AI Tools That Make Trading Easy

Several user-friendly AI tools are making trading accessible to everyone:

ChatGPT-style analysis bots: Help traders analyze stocks, news, or sentiment instantly.

TradingView AI scripts: Generate automatic signals based on customized indicators.

Zerodha Streak / Tradetron: Allow non-programmers to create and deploy AI trading strategies visually.

MetaTrader Expert Advisors (EAs): Automate forex and stock trading using AI-driven rules.

AI-Powered Analytics: Platforms like TrendSpider, Tickeron, and Kavout provide AI-based pattern recognition and predictions.

These platforms simplify trading so that even beginners can participate confidently without deep technical knowledge.

6. Challenges and Limitations

While AI makes trading easier, it’s not foolproof. Traders must understand its limitations:

Data Dependency: Poor data leads to poor predictions. AI is only as good as the information it’s trained on.

Overfitting: Some AI models may “overlearn” historical data, performing well in backtests but failing in real markets.

Market Volatility: Sudden geopolitical or economic shocks can render even advanced AI models temporarily ineffective.

Ethical and Technical Risks: Over-reliance on automation can cause flash crashes if many algorithms react simultaneously.

Cost and Complexity: Some advanced AI systems are expensive to build and maintain.

Thus, AI is a tool — not a guarantee of profit. Successful traders combine AI insights with human judgment.

7. The Future of AI Trading

The future of trading will be increasingly dominated by AI. Advancements like quantum computing, reinforcement learning, and hybrid human-AI systems will make trading even faster, more adaptive, and more personalized.

AI-driven systems will soon:

Understand market psychology better than human traders

Simulate millions of possible future scenarios in seconds

Provide real-time personalized trading advice

Detect global correlations across stocks, commodities, and currencies

In India, for example, AI-based algorithmic trading is growing rapidly, supported by SEBI regulations and broker integration. Retail traders are adopting automation tools to gain institutional-level efficiency.

8. Conclusion

Trading with AI is indeed easy — not because markets are simple, but because AI simplifies the process. It processes data, executes trades, manages risk, and learns continuously, allowing traders to focus on strategy rather than mechanics. Whether you’re a beginner or a professional, AI empowers you to trade smarter, faster, and more confidently.

However, while AI can make trading easier, it cannot eliminate risk entirely. Success still requires discipline, sound risk management, and an understanding of the technology behind the system. In the evolving world of finance, AI is not replacing traders — it is transforming them into more efficient and informed decision-makers.

In essence, AI doesn’t make trading effortless — it makes it intelligent. And with the right tools, anyone can harness its power to trade effectively in today’s digital markets.

Styles of Trading in the Indian Market1. Intraday Trading

Definition:

Intraday trading, also known as day trading, involves buying and selling financial instruments within the same trading day. The goal is to capitalize on short-term price movements without holding positions overnight.

Characteristics:

Positions are squared off before market close.

Traders rely heavily on technical analysis and price charts.

High liquidity stocks such as Reliance Industries, HDFC Bank, and Infosys are commonly traded.

Traders use tools like candlestick patterns, moving averages, RSI, MACD, and VWAP to identify entry and exit points.

Advantages:

Quick profits within a single day.

No overnight risk from news or global events.

Risks:

Requires constant attention and discipline.

High exposure to market volatility can lead to significant losses if risk management is weak.

In India, intraday trading is highly popular among retail traders because of its low capital requirement and the ability to use margin provided by brokers. However, success depends on speed, precision, and market understanding.

2. Swing Trading

Definition:

Swing trading involves holding positions for a few days to weeks to profit from short- to medium-term market “swings” or trends.

Characteristics:

Combines both technical and fundamental analysis.

Traders identify trend reversals, breakouts, and pullbacks.

Ideal for traders who cannot monitor markets all day but still seek active participation.

Advantages:

Less stressful than intraday trading.

Captures larger price movements.

Suitable for those with moderate risk tolerance.

Risks:

Overnight and weekend risks due to unexpected market news.

Requires patience and a good understanding of trend dynamics.

In the Indian context, swing trading is common among part-time traders and professionals who use stock screeners to identify stocks showing strong price momentum or technical patterns like cup-and-handle, flag, or triangle breakouts.

3. Positional Trading

Definition:

Positional trading focuses on capturing long-term market trends by holding positions for weeks, months, or even years. It lies between investing and active trading.

Characteristics:

Traders rely heavily on fundamental analysis and macroeconomic trends.

Technical indicators such as moving averages and Fibonacci retracements help identify entry points.

Patience and capital stability are key.

Advantages:

Lower transaction costs compared to frequent trading.

Less time-intensive.

Allows traders to ride major market moves.

Risks:

Exposure to long-term volatility, corporate announcements, or global crises.

In India, positional trading suits those who understand company fundamentals, earnings reports, and sector performance. Many long-term investors use this style to hold blue-chip stocks or sector leaders during growth phases.

4. Scalping

Definition:

Scalping is a high-frequency trading style where traders make multiple trades per day to capture very small price changes.

Characteristics:

Trades last from seconds to minutes.

Relies on high liquidity and tight bid-ask spreads.

Requires fast execution and strict risk management.

Advantages:

Low exposure to market-wide risks.

Frequent small profits can accumulate into significant returns.

Risks:

Requires advanced technology and quick decision-making.

Brokerage and transaction costs can reduce profits.

In India, scalping is often done in the derivatives or currency segment where liquidity is high. Professional traders and proprietary trading firms use advanced algorithms and trading terminals like NSE NOW or ODIN for execution.

5. Arbitrage Trading

Definition:

Arbitrage trading involves exploiting price differences of the same or related assets across different markets or instruments.

Types of Arbitrage in India:

Cash and Futures Arbitrage: Buying in the cash market and selling in the futures market when futures are overpriced.

Index Arbitrage: Taking advantage of the price gap between an index and its underlying stocks.

Cross-Exchange Arbitrage: Profiting from price differences of the same stock listed on NSE and BSE.

Advantages:

Low risk since trades are based on price inefficiencies.

Works well in highly liquid markets.

Risks:

Opportunities last for very short periods.

High capital and technology required for quick execution.

In the Indian market, institutional players and hedge funds dominate arbitrage trading. They employ automated systems that can identify and execute trades in milliseconds.

6. Momentum Trading

Definition:

Momentum trading focuses on identifying stocks showing strong upward or downward price momentum and riding that trend until it loses strength.

Characteristics:

Traders look for stocks with high volume and strong relative strength.

Uses indicators like RSI, MACD, and Moving Average Crossover.

The goal is to “buy high and sell higher” or “sell low and buy lower.”

Advantages:

Potential for high returns during trending markets.

Combines elements of both technical and sentiment analysis.

Risks:

Sharp reversals can lead to losses.

Highly dependent on timing and market psychology.

In India, momentum trading gained popularity with digital trading platforms and algorithmic systems. Traders often focus on mid-cap and small-cap stocks that move rapidly due to news, earnings results, or market sentiment.

7. Algorithmic and Quantitative Trading

Definition:

Algorithmic trading (algo trading) uses computer programs and mathematical models to execute trades based on predefined strategies without human intervention.

Characteristics:

Involves back-tested data and high-speed execution.

Strategies include arbitrage, momentum, statistical, and mean-reversion trading.

Trades are triggered by signals generated from real-time data.

Advantages:

Emotion-free and consistent trading.

Ability to process massive data and execute instantly.

Efficient in spotting opportunities invisible to manual traders.

Risks:

System errors or poor coding can cause losses.

Requires strong technical knowledge and infrastructure.

In India, algo trading has grown rapidly after SEBI allowed direct market access for institutional and retail traders. Many brokers now offer APIs to automate strategies through platforms like Zerodha’s Kite Connect and Upstox API.

8. Options and Derivatives Trading

Definition:

This style involves trading derivatives such as futures and options to speculate, hedge, or arbitrage.

Characteristics:

Traders use strategies like call/put buying, writing, straddles, spreads, and iron condors.

Derivatives magnify both profits and losses due to leverage.

Advantages:

Flexibility to profit in bullish, bearish, or neutral markets.

Useful for hedging portfolio risks.

Risks:

Requires deep understanding of volatility, time decay, and market direction.

High leverage can amplify losses.

In India, derivatives trading dominates the NSE market, with NIFTY and BANKNIFTY options being the most popular instruments among traders.

Conclusion

The Indian market offers multiple trading styles suited to various trader profiles — from short-term intraday players to long-term positional investors. Choosing the right style depends on one’s risk appetite, capital, time availability, and market knowledge. While intraday and swing trading attract active participants, positional and algorithmic trading are gaining ground due to technological advancements and increased financial literacy.

Successful traders in India understand that no single style guarantees consistent profits. The key lies in discipline, risk management, back-testing strategies, and continuous learning. As India’s financial ecosystem matures with innovations like algo trading, mobile platforms, and regulatory clarity, traders have unprecedented opportunities to participate effectively in the nation’s evolving markets.

Part 7 Trading Master Class Basics of Options in India

An option is a derivative contract that gives the holder the right but not the obligation to buy or sell an underlying asset (like Nifty, Bank Nifty, or a stock) at a predetermined price (called the strike price) before or on a specified date (expiry).

Call Option (CE): Gives the right to buy.

Put Option (PE): Gives the right to sell.

Traders use options for:

Hedging (protecting portfolio losses)

Speculation (betting on price movements)

Income generation (using premium decay)

In India, options are traded on exchanges like NSE and BSE, primarily on indices (Nifty, Bank Nifty, FinNifty) and individual stocks.

Possible Long Setup Scenarios in Indus Tower LimitedWe are analyzing the combination of the Mother and Child patterns in the technical chart of Indus Towers Limited.

Since its listing in 2012, the stock has been moving sideways, forming a large symmetrical triangle (the Mother pattern). A breakout occurred with high volume, followed by a retest in 2024. Currently, the stock is forming a smaller symmetrical triangle (the Child pattern) while retesting the boundaries of the larger Mother pattern.

The Mother pattern indicates strong potential for a long-term upward move, during which several smaller Child patterns may form.

On the daily chart, the Child pattern is still developing. The stock may either:

face rejection from resistance and pull back to take support before completing the pattern, or

break out and then retest the breakout level.

In both cases, key levels to watch are:

₹405 after a breakout, and

₹325 as a support level for possible accumulation.

There are no exact levels, stock can easily oscillate 5-10 points any direction.

The target is ₹430+, with a logical stop-loss applied in both scenarios for capital protection.

"Mother pattern is Showcased in the captioned image".

Nifty Intraday Analysis for 10th November 2025NSE:NIFTY

Index has resistance near 25650 – 25700 range and if index crosses and sustains above this level then may reach near 25875 – 25925 range.

Nifty has immediate support near 25350 – 25300 range and if this support is broken then index may tank near 25150 – 25100 range.

The market is expected to be range-bound for the next couple of days, with a decisive move on either side anticipated after the Bihar Election result outcome which is scheduled on Friday.

Premium Chart Knowledge Strategy and Leverage

Option trading allows traders to speculate on price movements or hedge positions with limited capital, offering leverage and flexibility through calls (buy) and puts (sell) contracts.

Risk and Reward

Options carry high profit potential but significant risk due to time decay and volatility. Successful trading requires analysis, discipline, and understanding of premium pricing and expiry.

US Dollar Weakness Likely After Final Push UpDXY has completed a complex corrective W–X–Y pattern, with the final leg (Y) recently topping near the 100.50 zone. Price has failed to break above the invalidation level, suggesting the uptrend is losing strength. This signals that the dollar may have finished its corrective phase and could now start a fresh bearish wave targeting lower zones near 97–98. The overall structure indicates that momentum is shifting from bullish to bearish. In simple terms: rally is likely over → downside move toward new lows expected next.

Stay tuned!

@Money_Dictators

Thank you :)

Candle Pattern Explained There are two primary types of options: Call Options and Put Options. A Call Option gives the buyer the right to purchase an underlying asset at a specific price (called the strike price) before or on a certain date (known as the expiry date). Traders buy calls when they expect the price of the asset to rise. Conversely, a Put Option gives the buyer the right to sell the asset at the strike price within a specific period. Traders buy puts when they anticipate the asset’s price will fall.

Part 6 Institutional Trading Option Trading in India

In India, option trading is available on major exchanges like NSE and BSE, primarily for:

Equity Options (Stocks)

Index Options (NIFTY, BANK NIFTY, FINNIFTY)

Contracts are settled in cash, and trading happens in defined lot sizes. Most retail traders prefer index options due to liquidity and low margin requirements.