Yatra Online LtdYatra Online Ltd

a) YOL deals in the entire value chain of travel and hospitality, covering B2C and B2B segments.

b) It is the largest Corporate travel services provider, and one of the largest OTAs with ~80,000 domestic hotels and homestays contracted in ~1497 cities.

c) It provides a Real-time and Integrated SaaS Tech Platform which is accessible through the desktop & Mobile apps.

d) The company has a customer base of over 1,300 large corporates with addressable employee base of 9+ million employees.

Service:

The company is one of India’s leading online travel platforms, offering comprehensive corporate travel services to over 850 corporate clients. It facilitates bookings for domestic and international flights, hotels, holiday packages, buses, trains, cabs, homestays, cruises, and local activities. With a network of approximately 108,000 hotels and homestays across 1,500 Indian cities and access to around 2 million hotels globally, it stands as the largest domestic hotel platform in India.

Market Cap: ₹ 1,477 Cr.

Promoter holding: 64.5 %

FII holding: 2.82 %

DII holding: 19.1 %

Public holding: 13.6 %

Debt: ₹ 78.4 Cr.

Debt 3Years back: ₹ 62.8 Cr.

Looks good to buy on every deep, once breakout come it will give good movement.

Fundamental Analysis

Option Chain Terms1. Introduction: What is an Option Chain?

An Option Chain (also called an options matrix) is like a detailed menu for all the available Call and Put options of a particular underlying asset (such as a stock, index, or commodity) for different strike prices and expiry dates.

If you’re a trader, the option chain is where you see all the numbers that decide your trading choices — prices, volumes, open interest, and Greeks.

Think of it as the cockpit of an airplane — lots of data, but if you know what each dial means, you can navigate smoothly.

Example:

If you open the NSE India website and look at the NIFTY Option Chain, you’ll see something like:

Strike Price CALL LTP CALL OI PUT LTP PUT OI

19500 ₹250 1,20,000 ₹15 80,000

19600 ₹180 95,000 ₹25 90,000

This is a simplified snapshot — in reality, there are more columns like bid-ask prices, implied volatility, and Greeks.

2. Core Sections of an Option Chain

An option chain is split into two halves:

Left Side: Call options (bullish contracts)

Right Side: Put options (bearish contracts)

Middle: Strike Prices (common to both)

Here’s how the layout looks visually:

markdown

Copy

Edit

CALL DATA | STRIKE PRICE | PUT DATA

-----------------------------------------------

OI Chg OI LTP IV | 19500 | IV LTP Chg OI OI

OI Chg OI LTP IV | 19600 | IV LTP Chg OI OI

3. Option Chain Key Terms

Let’s go deep into each term one by one.

3.1 Strike Price

The predetermined price at which you can buy (Call) or sell (Put) the underlying asset if you exercise the option.

Every expiry has multiple strike prices — some above the current market price, some below.

Example:

If NIFTY is at 19,500:

19,500 Strike → ATM (At The Money)

19,600 Strike → OTM (Out of The Money) Call, ITM (In The Money) Put

19,400 Strike → ITM Call, OTM Put

3.2 Expiry Date

The last trading day for the option. After this date, the contract expires worthless if not exercised.

In India:

Index options (like NIFTY, BANKNIFTY) → Weekly expiries + Monthly expiries

Stock options → Monthly expiries

3.3 Call Option (CE)

Gives you the right (not obligation) to buy the underlying at the strike price.

Traders buy calls when they expect the price to rise.

3.4 Put Option (PE)

Gives you the right (not obligation) to sell the underlying at the strike price.

Traders buy puts when they expect the price to fall.

3.5 LTP (Last Traded Price)

The most recent price at which the option contract traded.

Reflects the current market value of that option.

3.6 Bid Price & Ask Price

Bid Price: Maximum price buyers are willing to pay.

Ask Price: Minimum price sellers are willing to accept.

The gap between them is called the Bid-Ask Spread.

3.7 Bid Quantity & Ask Quantity

Bid Quantity: Number of contracts buyers want to purchase at the bid price.

Ask Quantity: Number of contracts sellers are offering at the ask price.

3.8 Volume

Total number of contracts traded during the current trading session.

High volume indicates strong interest and liquidity.

3.9 Open Interest (OI)

Total number of outstanding contracts that haven’t been closed or squared off.

Shows market positioning:

High OI in calls → Bearish or range-bound expectation.

High OI in puts → Bullish or range-bound expectation.

3.10 Change in Open Interest (Chg OI)

How much OI has increased or decreased from the previous session.

Used to detect fresh positions or unwinding.

3.11 Implied Volatility (IV)

Market’s expectation of future volatility.

Higher IV → Option premiums become expensive.

Lower IV → Options are cheaper.

3.12 Greeks in the Option Chain

Greeks measure how sensitive the option price is to changes in market factors:

Delta → Price change sensitivity to the underlying asset.

Gamma → Rate of change of Delta.

Theta → Time decay rate of the option price.

Vega → Sensitivity to changes in volatility.

Rho → Sensitivity to interest rate changes.

3.13 ATM, ITM, and OTM

ATM (At The Money): Strike price is equal to the current price.

ITM (In The Money): Option has intrinsic value.

OTM (Out of The Money): Option has no intrinsic value (only time value).

3.14 Premium

The price you pay to buy an option.

Premium = Intrinsic Value + Time Value.

3.15 Break-Even Point

Price level at which your option trade starts becoming profitable.

3.16 PCR (Put-Call Ratio)

Formula: PCR = Put OI / Call OI

High PCR (>1) → Bullish sentiment.

Low PCR (<1) → Bearish sentiment.

4. How to Read the Option Chain

Reading an option chain is about spotting where traders are placing their bets.

Step-by-step:

Identify ATM Strike.

See highest OI in Calls and Puts — this shows resistance and support levels.

Look at Change in OI to spot fresh activity.

Check IV movement for volatility expectations.

Use Greeks for risk assessment.

Example Analysis:

NIFTY at 19,500

Highest Call OI: 19,800 (Resistance)

Highest Put OI: 19,400 (Support)

PCR = 1.2 → Mildly bullish

5. Practical Use Cases

Finding Support & Resistance:

Highest Put OI → Support

Highest Call OI → Resistance

Spotting Breakouts:

Sudden drop in Call OI at resistance → Possible breakout.

Volatility Trading:

High IV → Consider selling options.

Low IV → Consider buying options.

6. Advanced Option Chain Insights

Long Buildup: Price ↑, OI ↑ → Bullish.

Short Buildup: Price ↓, OI ↑ → Bearish.

Short Covering: Price ↑, OI ↓ → Bullish reversal.

Long Unwinding: Price ↓, OI ↓ → Bearish reversal.

7. Common Mistakes to Avoid

Ignoring IV before entering trades.

Reading OI without considering price movement.

Not adjusting for upcoming news or events.

Trading illiquid strikes with wide bid-ask spreads.

8. Conclusion

An option chain is not just a table of numbers — it’s a real-time X-ray of trader sentiment.

By understanding every term — from LTP to IV, from Delta to PCR — you can turn raw data into actionable insights.

Mastering the Art of Risk Management in Trading 1. Introduction: Why Risk Management is the Heart of Trading

Trading is not about making big profits quickly — it’s about staying in the game long enough to let your edge work for you.

Think of trading like a professional sport. Skill matters, but survival matters more. Even the world’s best traders lose trades; what separates them from amateurs is how they manage those losses.

In simple terms:

Good trading without risk management = gambling.

Average trading with strong risk management = long-term success.

Warren Buffett’s famous rules apply perfectly here:

Don’t lose money.

Never forget rule #1.

2. Core Principles of Risk Management

Before we go deep into strategies, let’s lock in the foundation.

2.1 Risk is Inevitable

Every trade carries risk. The goal is not to avoid it but to control its size and impact.

2.2 Asymmetry in Trading

A 50% loss requires a 100% gain to break even. This means avoiding large drawdowns is far more important than chasing big wins.

Loss % Required Gain to Recover

10% 11.1%

25% 33.3%

50% 100%

75% 300%

2.3 Risk per Trade

Most professional traders risk 0.5%–2% of their account per trade.

This ensures no single bad trade can destroy the account.

3. The Psychology of Risk

Risk management is not just math — it’s deeply psychological.

Loss Aversion Bias: Humans feel losses twice as strongly as gains. This can push traders into revenge trading.

Overconfidence Bias: Winning streaks can lead to oversized positions.

Fear of Missing Out (FOMO): Chasing trades without proper entry rules increases risk.

A great risk management system removes emotional decision-making by setting clear, mechanical rules.

4. Position Sizing: The Risk Control Lever

Position sizing determines how much capital to put into a trade. Even if your strategy is perfect, bad sizing can blow up your account.

4.1 Fixed Fractional Method

Risk a fixed % of capital per trade.

Example: If account = ₹10,00,000 and risk = 1% → Risk per trade = ₹10,000.

If Stop Loss = ₹50 away from entry, position size = ₹10,000 ÷ ₹50 = 200 shares.

4.2 Volatility-Based Position Sizing

Adjust position size according to the volatility of the asset (ATR – Average True Range).

If ATR = ₹25 and your risk budget = ₹5,000, position size = ₹5,000 ÷ ₹25 = 200 shares.

4.3 Kelly Criterion (Advanced)

Maximizes capital growth based on win rate & reward/risk ratio.

Formula: K% = W – (1 – W) / R

Where:

W = Win probability

R = Reward/Risk ratio

Caution: Kelly is aggressive; use fractional Kelly for real trading.

5. Stop Loss Strategies: Your Safety Net

A stop loss is not a sign of weakness — it’s a shield.

5.1 Fixed Stop Loss

Predefined point in price where you exit.

5.2 Volatility Stop Loss

Adjust stop distance using ATR to account for market noise.

5.3 Time-Based Stop

Exit after a fixed time if the trade hasn’t moved in your favor.

5.4 Trailing Stop

Moves with price in your favor to lock in profits.

Golden Rule: Place stops based on market structure, not emotions.

6. Reward-to-Risk Ratio (RRR)

The RRR tells you how much you stand to gain for every unit you risk.

Example:

Risk: ₹1000

Reward: ₹3000

RRR = 3:1 → Even a 40% win rate is profitable.

High RRR trades allow more losers than winners while staying profitable.

7. Diversification & Correlation Risk

7.1 Asset Diversification

Avoid putting all capital into one asset or sector.

7.2 Correlation Risk

If you buy Nifty futures and Bank Nifty futures, you’re effectively doubling your risk because they move together.

8. Risk Management for Different Trading Styles

8.1 Day Trading

Keep daily loss limits (e.g., 3% of capital).

Avoid revenge trading after a loss.

8.2 Swing Trading

Use wider stops to allow for multi-day fluctuations.

Position sizing becomes even more critical.

8.3 Options Trading

Risk can be higher due to leverage.

Always calculate max loss before entering.

9. Risk Management Tools

ATR Indicator – For volatility-based stops.

Position Size Calculators – To control exposure.

Heat Maps & Correlation Tools – To avoid overexposure.

Journaling Software – To track mistakes.

10. Risk-Adjusted Performance Metrics

Professional traders measure performance relative to risk taken.

Sharpe Ratio – Risk-adjusted returns.

Sortino Ratio – Focuses on downside volatility.

Max Drawdown – Largest account drop during a period.

11. Building a Personal Risk Management Plan

Your plan should cover:

Max % of capital risked per trade.

Max daily/weekly loss limit.

Position sizing rules.

Stop loss & target placement method.

Diversification guidelines.

Rules for scaling in/out.

Plan for handling drawdowns.

12. Advanced Concepts

12.1 Portfolio Heat

Sum of all open trade risks; keep it below a set % of account.

12.2 Value at Risk (VaR)

Estimates the max expected loss over a time frame.

12.3 Stress Testing

Simulate worst-case scenarios (e.g., gap downs, black swans).

Conclusion: Risk Management is Your Superpower

In trading, capital is ammunition. Risk management ensures you never run out of bullets before the big opportunities arrive.

Mastering it is not optional — it’s the difference between a short-lived hobby and a long-term career.

Intraday Trading vs Swing Trading1. Introduction to the Two Trading Styles

1.1 What is Intraday Trading?

Intraday trading, often called day trading, involves buying and selling a stock (or any tradable asset) within the same trading day.

The key points are:

Positions are never held overnight.

The goal is to capitalize on short-term price movements.

Traders often make multiple trades in a single day.

Requires continuous monitoring of charts and price action.

For example:

If the market opens at 9:15 AM and closes at 3:30 PM (in India), an intraday trader will enter and exit all trades during that time frame.

1.2 What is Swing Trading?

Swing trading focuses on capturing price swings that can last from a few days to several weeks.

The key points are:

Positions are held overnight and sometimes for weeks.

Aims to profit from medium-term trends.

Fewer trades compared to intraday trading.

Allows more flexibility — you don’t have to watch the screen all day.

For example:

A swing trader might buy a stock on Monday based on a bullish chart setup and hold it until the next Thursday when it hits their target.

2. Core Differences at a Glance

Aspect Intraday Trading Swing Trading

Holding Period Minutes to hours, same day only Days to weeks

Trading Frequency High (multiple trades/day) Low (few trades/week)

Capital Requirement Can be lower due to leverage (but higher risk) Moderate; less leverage

Market Monitoring Continuous, real-time Periodic (once/twice a day)

Stress Level High Moderate

Profit Potential Small profits per trade, cumulative gains Larger profits per trade

Risk Higher due to volatility & leverage Lower per trade but still significant

Technical Analysis Very short-term indicators Medium-term trends, chart patterns

Best for Quick decision-makers, active traders Patient traders, part-time market participants

3. Time Commitment and Lifestyle Fit

One of the biggest differences between the two is time commitment.

3.1 Intraday Trading Lifestyle

Requires full-time attention during market hours.

You need a dedicated trading setup with a fast internet connection, live charts, and possibly multiple monitors.

Ideal for those who enjoy fast decision-making and thrive under pressure.

No overnight market risk — but very sensitive to intraday volatility.

3.2 Swing Trading Lifestyle

Can be managed alongside a job or business.

You may only need to check charts once or twice daily.

Not as dependent on split-second execution.

Overnight gaps can cause gains or losses, but this is part of the strategy.

4. Analytical Approach and Tools

Both styles use technical analysis, but the indicators, timeframes, and patterns differ.

4.1 Intraday Trading Tools

Timeframes: 1-min, 5-min, 15-min, and 1-hour charts.

Indicators:

Moving Averages (5 EMA, 20 EMA)

VWAP (Volume Weighted Average Price)

RSI (Relative Strength Index)

MACD

Volume Profile

Strategies:

Breakout Trading

Scalping

Momentum Trading

Reversal Trading

Example:

An intraday trader may look for a breakout above a resistance level on a 5-minute chart and ride the move for 30 minutes.

4.2 Swing Trading Tools

Timeframes: 1-hour, daily, and weekly charts.

Indicators:

50-day and 200-day Moving Averages

RSI (14-period)

MACD (slower settings)

Fibonacci retracement

Strategies:

Trend-following

Pullback entries

Chart pattern breakouts (Cup & Handle, Flag, Head & Shoulders)

Example:

A swing trader might spot a bullish flag pattern on a daily chart and hold the stock for 7–10 days until the trend completes.

5. Risk and Money Management

Risk management is non-negotiable in both.

5.1 Intraday Trading Risk Profile

Typically risk 0.5%–1% of capital per trade.

Use of tight stop-losses (0.5%–2% price move).

Leverage can magnify profits — but also losses.

High risk of overtrading due to frequent opportunities.

5.2 Swing Trading Risk Profile

Typically risk 1%–3% of capital per trade.

Stop-losses are wider (5%–10%) due to longer holding periods.

Leverage is less common.

Lower chance of overtrading but more exposure to overnight news events.

6. Psychological Factors

The psychology of trading is often underestimated — but it’s the hidden battlefield.

6.1 Intraday Trading Mindset

Requires quick thinking and emotional control.

Must accept being wrong quickly and exit trades.

High adrenaline; mistakes can happen if overexcited.

Pressure is intense — small distractions can be costly.

6.2 Swing Trading Mindset

Requires patience and discipline.

Must tolerate overnight volatility.

Less pressure from immediate decision-making.

Risk of “holding and hoping” if the trade goes wrong.

7. Costs and Infrastructure

7.1 Intraday Trading Costs

Higher brokerage fees due to frequent trades.

Need a high-speed internet connection.

Possibly premium data feeds and charting software.

7.2 Swing Trading Costs

Lower brokerage costs (fewer trades).

Basic trading platforms are enough.

No need for ultra-fast execution speed.

8. Pros and Cons of Each Style

8.1 Intraday Trading Pros

Quick results — profit/loss is realized the same day.

No overnight risk.

Many opportunities daily.

Intraday Cons:

High stress and mental fatigue.

Requires constant attention.

Overtrading temptation.

8.2 Swing Trading Pros

Less time-intensive.

Larger moves per trade possible.

Easier for people with other commitments.

Swing Cons:

Overnight gaps can hurt.

Slower feedback loop.

Can miss fast intraday moves.

9. Which is More Profitable?

This is a trick question — profitability depends more on the trader’s skill, discipline, and consistency than the style itself.

Intraday traders often make many small profits; compounding them can lead to large gains, but losses can pile up fast.

Swing traders aim for fewer but larger profits, which can be less stressful but require more patience.

10. Deciding Which Style Suits You

Ask yourself:

Can you sit in front of a screen for hours without losing focus? (Yes → Intraday)

Do you prefer analyzing charts once a day? (Yes → Swing)

Are you comfortable with overnight risk? (Yes → Swing)

Do you want to avoid holding positions overnight? (Yes → Intraday)

Do you thrive under pressure? (Yes → Intraday)

Are you patient enough to wait days for a trade to work? (Yes → Swing)

Final Thoughts

There’s no universal “better” option between intraday trading and swing trading — only the option that’s better for you.

Both can be profitable if approached with:

Solid strategy

Risk management

Psychological discipline

Continuous learning

Whether you enjoy the fast-paced, high-energy environment of intraday trading or the patient, trend-focused approach of swing trading, the real key lies in execution and discipline.

BUY TODAY SELL TOMORROW for 5%DON’T HAVE TIME TO MANAGE YOUR TRADES?

- Take BTST trades at 3:25 pm every day

- Try to exit by taking 4-7% profit of each trade

- SL can also be maintained as closing below the low of the breakout candle

Now, why do I prefer BTST over swing trades? The primary reason is that I have observed that 90% of the stocks give most of the movement in just 1-2 days and the rest of the time they either consolidate or fall

Trendline Breakout in STARCEMENT

BUY TODAY SELL TOMORROW for 5%

Support Breakdown is excepted in SOLUSDSOLUSD has breached a key support zone around the $178–$179 level, turning the area into potential resistance. Price action shows repeated rejections near this zone, followed by a decisive breakdown on strong bearish momentum.

If sellers maintain pressure below this level, further downside towards $175 and $171 could be on the cards. A sustained recovery back above $179 would be needed to invalidate the bearish outlook.

📉 Bias: Bearish below $179

🎯 Targets: $175 – $171

Buy GoldLet it go down and buy from there. Buy with small lot size and while managing your funds

Target 3351,3368,3375,3380,3390,3405,3430

Gold LongEntry- 3355-3352

SL- 3349

Target- 3368, 3370, 3375

Reason- Gold has broken out of a falling trendline in 1hr TF with a strong candle. News is also there that trump is not going to put tariff on gold bars.

Disclaimer- This is just for educational purposes please take advice before making any decision.

Jai Shree Ram.

SUZLON swing tradeSuzlon Energy for Swing Trading (Initiating Tomorrow)

Current Status & Technical View:

* Suzlon is seen as being in a consolidation phase after a significant rally. This is viewed by some as a healthy base-building period before a potential upward move.

* It has shown a strong rally of 19% over the last three months, but has seen a slight pullback in the past month (down 4.7%) and week (down 4%).

* Technically, the stock is still viewed within a bullish medium-term setup, with key support noted near ₹61-₹62. The NSE shows the previous close at ₹64.21.

* Key resistance is identified around ₹68-₹70, and a decisive breakout above ₹68.30 could lead to targets of ₹73.50 and potentially ₹86.50.

* Crucially, Suzlon is scheduled to announce its Q1 results tomorrow, August 12th, 2025. This could be a significant catalyst for the stock price. Brokerages are expecting strong year-on-year growth in both PAT (55-58%) and revenue (around 60%).

Action Plan for Buying Tomorrow:

1. Monitor the Opening & Initial Price Action: The stock's reaction to the market opening and the release of Q1 results will be crucial.

* Strong Opening with Positive Results: If the Q1 results are positive and the stock opens strong, consider an entry around the current levels, or near the breakout level of ₹68-₹70 if it approaches that with good volume.

* Negative Reaction or Weak Opening: If the Q1 results are disappointing or the market reacts negatively, the stock could see a sharp decline. In such a scenario, it might be wiser to wait for the volatility to settle and for the stock to find support before considering an entry.

2. Entry Point:

* Conservative Entry: If the stock corrects after a potentially positive reaction to earnings, look for a bounce from support levels. The previous swing low at ₹59.80, which aligns with the 50-week EMA, could be a potential entry point if the stock finds strong support there.

* Breakout Entry: If the stock shows strong upward momentum and breaks above the ₹68-₹70 resistance zone with good volume, you could consider an entry on confirmation of the breakout.

3. Stop-Loss: To manage risk effectively, set a clear stop-loss order.

* Recommended Stop-Loss: Based on technical analysis, placing a stop-loss below ₹59.80 (the 50-week EMA) is a sound strategy to limit potential losses if the trade goes against you.

* Tighter Stop-Loss: If your risk appetite is lower, you could consider a tighter stop-loss near recent support levels, but ensure it's not too tight to get stopped out prematurely.

4. Selling Targets:

* Short-Term Targets: Target levels in the range of ₹74-₹80 in the near term.

* Medium-Term Target: An extended target of ₹86.50 is also suggested if the momentum continues.

5. Risk Management:

* Volatility: Be prepared for potential volatility tomorrow, especially around the Q1 earnings announcement.

* Don't Over-Leverage: Avoid over-leveraging your position, especially since Suzlon is considered a higher-beta stock.

* Market Sentiment: Keep an eye on the overall market sentiment, as it can influence the stock's performance.

I am not SEBI registered, please do your own research.

How to Read a Balance Sheet – Simple Breakdown for Traders!Hello Traders!

Most traders ignore the balance sheet because it looks “too accounting-heavy.”

But understanding just the basics can give you an edge, especially when you want to know if a company is financially healthy.

Today, let’s simplify the balance sheet so you can read it with confidence.

What is a Balance Sheet?

A balance sheet is a snapshot of a company’s financial position at a specific point in time.

It tells you what the company owns, what it owes, and what’s left for shareholders.

Three Main Sections You Must Know

Assets:

Everything the company owns that has value, cash, buildings, machinery, inventory, and money owed to it.

Assets show the company’s ability to generate future income.

Liabilities:

Everything the company owes to others, loans, unpaid bills, and other obligations.

High liabilities compared to assets can be a warning sign.

Shareholder’s Equity:

The value left for shareholders after liabilities are subtracted from assets.

It’s like the “net worth” of the company.

Key Ratios to Look At

Debt-to-Equity Ratio:

Shows how much of the company is funded by debt versus shareholder capital. Lower is generally better.

Current Ratio:

Compares current assets to current liabilities. If it’s above 1, the company can likely pay short-term debts.

Return on Equity (ROE):

Measures how efficiently management is using shareholder funds to generate profit.

Rahul’s Tip:

You don’t need to be an accountant to read a balance sheet.

Focus on big-picture numbers, assets, liabilities, and equity, and see if the business is stable, growing, and not overloaded with debt.

Conclusion:

A balance sheet tells you if the company can survive tough times and fund future growth.

Once you understand it, you’ll never look at a stock the same way again.

If this helped you, like the post, share your view in the comments, and follow for more practical investing insights!

CHENNAI PETRO-BLEND OF TECHNOFUNDABuy CHENNAI PETRO 680 TILL 610 FOR target of 740 and 850. Classic blend of fundamental a technical analysis. Bullish flag and inverse head & shoulder breakout happening at 630 levels.

Also available near P to B/V with dividend yield above 8%.

view invalid below 580.

Awaiting the BreakDown or a Snap Back to Resistance?XAUUSD – Game of Patience: Awaiting the BreakDown or a Snap Back to Resistance? | MMFlow Trading

1. Market Context

The week opened with a sharp sell-off in Gold — driven by profit-taking and stop-loss hunting on late-week FOMO BUY positions.

Buying momentum is fading, while sellers are lurking at the ascending channel’s support.

Price is currently reacting at KeyLevel 336x–337x, with H1 candles showing lower wicks → signs of indecision.

2. Technical Outlook

Overall structure: Still within an H1-H4 uptrend channel, but BUY momentum is weakening.

No clear SELL confirmation yet → need a BreakDown from the channel to confirm seller dominance.

Scenario 1: Break the channel → target 335x & 333x zones.

Scenario 2: No break → price may rebound to retest 339x – 340x – 342x resistance levels.

3. Fundamental & Macro View

This week brings major USD economic data: CPI & PPI.

Forecasts lean positive for USD, which could increase downward pressure on Gold.

However, expect false breakouts before/after news releases — risk management is key.

4. MMFlow Trading Plan

BUY SCALP

Entry: 3353 – 3351

SL: 3345

TP: 3358 – 3362 – 3366 – 3370 – 3375 – 3380

BUY ZONE

Entry: 3332 – 3330

SL: 3325

TP: 3336 – 3340 – 3345 – 3350 – 3360 – 3370 – 3380

SELL SCALP

Entry: 3394 – 3396

SL: 3400

TP: 3390 – 3385 – 3380 – 3370 – 3360

SELL ZONE

Entry: 3425 – 3427

SL: 3430

TP: 3420 – 3415 – 3410 – 3405 – 3400 – 3390 – 3380

5. Risk Management

Avoid FOMO — wait for clear candle confirmations before entering.

Reduce position size ahead of CPI/PPI events.

Focus on pre-defined key levels, avoid trading in noise zones.

Part11 Trading Master ClassRatio Spread

When to Use: Expect limited move in one direction.

How It Works: Buy 1 option, sell multiple options at different strikes.

Risk: Unlimited on one side if not hedged.

Diagonal Spread

When to Use: Expect gradual move over time.

How It Works: Buy long-term option at one strike, sell short-term option at different strike.

Risk Management in Options

Even though options can limit loss, traders often misuse them and blow accounts.

Key risk tips:

Never risk more than 2–3% of capital on one trade.

Understand implied volatility — high IV inflates premiums.

Avoid selling naked options without sufficient margin.

Always set stop-loss rules.

Part12 Trading Master ClassAdvanced Options Strategies

Butterfly Spread

When to Use: Expect stock to stay near a specific price.

How It Works: Buy 1 ITM option, sell 2 ATM options, buy 1 OTM option.

Risk: Limited.

Reward: Highest if stock ends at middle strike.

Example: Stock ₹100, buy call ₹95, sell 2 calls ₹100, buy call ₹105.

Calendar Spread

When to Use: Expect low short-term volatility but possible long-term move.

How It Works: Sell short-term option, buy long-term option at same strike.

Risk: Limited to net premium.

Reward: Comes from time decay of short option.

Ambuja Cements – Breakout on Record FY25 Performance📈Technical Analysis

Over the last decade, Ambuja steadily climbed from below ₹50 to peak around ₹700 by mid-2024, before slipping to ₹450.

Since then, it formed higher lows and faced resistance around ₹580. With strong FY25 results, it convincingly broke above ₹580, climbed to ₹620, and is now retesting that level.

If ₹580 holds as support with bullish candle confirmation, the next upside targets are:

🎯Target 1: ₹620

🎯Target 2: ₹650

🎯Target 3: ₹680–700

Stop Loss: Below ₹560. If it fails to act as support, the bullish thesis is negated.

💰FY25 Financial Highlights (vs FY24 & FY23)

Total Income: ₹35,045 Cr (↑ +6% vs ₹33,160 Cr; ↓ –10% vs ₹38,937 Cr)

Total Expenses: ₹29,074 Cr (↑ +9% vs ₹26,760 Cr; ↓ –14% vs ₹33,815 Cr)

Financing Profit: ₹5,971 Cr (↓ –7% vs ₹6,400 Cr; ↑ +17% vs ₹5,122 Cr)

Profit Before Tax: ₹5,922 Cr (↑ +0.4% vs ₹5,896 Cr; ↑ +59% vs ₹3,729 Cr)

Profit After Tax: ₹5,158 Cr (↑ +9% vs ₹4,735 Cr; ↑ +70% vs ₹3,024 Cr)

Diluted EPS: ₹16.92 (↑ from ₹16.26; ↑ from ₹13.01)

Key Takeaway: Ambuja delivered its highest-ever annual PAT of ₹5,158 Cr, complemented by record volumes (65.2 MT) and operational efficiencies. The company also crossed 100 MTPA cement capacity, establishing a strong foundation for future growth.

🧠Fundamental Analysis

Outstanding Q1 FY26 Performance

Ambuja delivered a substantial 24% YoY increase in net profit, posting ₹970 crore pushed by record quarterly sales and strong operational efficiency

Cost and Margin Improvements

EBITDA reached an all-time high of ₹1,961 crore with margins expanding to 19.1%, supported by better pricing and cost optimization

Bottom Line

Ambuja Cements has broken a long-term resistance level at ₹580, supported by stellar FY25 performance. A successful retest could propel the stock towards ₹700. Watch near-term support closely—break below ₹560 could derail the bullish setup.

Disclaimer: lnkd.in

Torrent Pharma – Steady Growth with Strong Margins📈Technical Analysis

The stock has shown a powerful uptrend over the past 5–6 years, with a sharp rally from ₹1,000 to ₹3,500. For the past year, the ₹3,500–₹3,600 zone stood strong as resistance. With the release of the positive Q1 FY26 results, Torrent has decisively broken above this supply zone accompanied by higher volumes—something not seen earlier this year.

After the breakout, prices rose to ₹3,800 and then retested the broken zone, which now appears to be offering support. Provided this zone continues to hold and is followed by bullish candlestick confirmation, the stock looks set for further upside.

Targets:

🎯 ₹3,800 (Target 1)

🎯 ₹3,900 (Target 2)

🎯 ₹4,000 (Target 3)

Stop Loss: Below the support zone at ₹3,400. If prices fall below this, bullish outlook is invalidated.

💰Q1 FY26 Financial Highlights (vs Q4 FY25 & Q1 FY25)

Total Income: ₹3,178 Cr (↑ +7.4% QoQ vs ₹2,959 Cr; ↑ +11.2% YoY vs ₹2,859 Cr)

Total Expenses: ₹2,146 Cr (↑ +7.6% QoQ vs ₹1,995 Cr; ↑ +9.8% YoY vs ₹1,955 Cr)

Operating Profit: ₹1,032 Cr (↑ +7.0% QoQ vs ₹964 Cr; ↑ +14.2% YoY vs ₹904 Cr)

Profit Before Tax: ₹738 Cr (↑ +11.0% QoQ vs ₹665 Cr; ↑ +12.5% YoY vs ₹656 Cr)

Profit After Tax: ₹548 Cr (↑ +10.0% QoQ vs ₹498 Cr; ↑ +19.9% YoY vs ₹457 Cr)

Diluted EPS: ₹16.19 (↑ +10.1% QoQ vs ₹14.71; ↑ +19.9% YoY vs ₹13.50)

This performance reflects robust execution across both domestic and international markets.

🧠Fundamentals & Strategic Highlights

Domestic Market Strength: India revenues grew ~11%, driven by outperforming chronic therapies (13% growth vs 9% IPM growth)

Global Growth:

US business expanded by ~19%

Brazil saw 11% growth

Analyst Sentiment: Citi raised its target price to ₹4,380, citing sustained margin expansion and branded portfolio gains

M&A Plans: Torrent is acquiring a majority stake in JB Chemicals for ₹18,000–₹19,500 Cr, positioning the company among India’s top five pharma giants

✅Conclusion

Torrent Pharma’s technical breakout, backed by a wholesome Q1 performance and strategic M&A moves, positions it favorably for renewed upside. A failure to hold above ₹3,500 would challenge this view.

Disclaimer: lnkd.in

Inflation & Interest Rate Impact on Markets 1. Introduction – Why This Topic Matters

Inflation and interest rates are like the heartbeat and blood pressure of the global economy. When they rise or fall, every financial market — from stocks and bonds to commodities and currencies — reacts. These two forces can determine:

The cost of money (borrowing/lending rates)

The value of assets (how much investors are willing to pay for future earnings)

Consumer spending power (how much people can buy with their money)

Investment flows (where capital moves globally)

Understanding how they interact is crucial for traders, investors, policymakers, and even businesses planning budgets.

2. Understanding Inflation

Inflation is the general rise in prices over time, which reduces the purchasing power of money.

2.1 Types of Inflation

Demand-Pull Inflation

Driven by strong consumer demand outpacing supply.

Example: Post-pandemic reopening in 2021–2022 led to huge spending surges and price hikes.

Cost-Push Inflation

Driven by rising production costs (wages, raw materials, energy).

Example: Oil price spike due to geopolitical tensions.

Built-In Inflation

When workers demand higher wages to keep up with prices, which increases costs for businesses, causing more inflation — the wage-price spiral.

Hyperinflation

Extreme, rapid price increases (often 50%+ per month).

Example: Zimbabwe in the 2000s, Venezuela in the 2010s.

2.2 Measuring Inflation

CPI (Consumer Price Index) — Measures average price change for a basket of goods/services.

PPI (Producer Price Index) — Measures wholesale/production cost changes.

Core Inflation — CPI without volatile food & energy prices (better for long-term trends).

PCE (Personal Consumption Expenditures) — The Fed’s preferred measure in the U.S.

2.3 Causes of Inflation Surges

Supply chain disruptions (COVID-19 impact)

Commodity shocks (oil, metals, food)

Loose monetary policy (low interest rates, money printing)

Fiscal stimulus (government spending boosts demand)

3. Understanding Interest Rates

Interest rates represent the cost of borrowing money, usually set by central banks for short-term lending.

3.1 Types of Rates

Policy Rate

Set by central banks (e.g., U.S. Fed Funds Rate, RBI Repo Rate in India).

Market Rates

Determined by supply/demand in bond markets (long-term yields like the 10-year Treasury).

Real vs. Nominal Rates

Nominal rate = stated rate

Real rate = nominal rate − inflation rate

Example: If interest rate = 5% and inflation = 6%, the real rate is −1% (losing purchasing power).

3.2 Why Central Banks Adjust Rates

To fight inflation — raise rates to cool spending.

To boost growth — cut rates to encourage borrowing.

To stabilize currency — higher rates attract foreign capital, strengthening the currency.

4. The Inflation–Interest Rate Relationship

The two are deeply linked.

High inflation → central banks raise interest rates to slow the economy.

Low inflation or deflation → central banks cut rates to stimulate demand.

This relationship is central to monetary policy.

4.1 The Lag Effect

Interest rate changes take 6–18 months to fully impact inflation and growth. This delay means policymakers act based on forecasts, not current numbers.

4.2 The Risk of Over-Tightening or Under-Tightening

Over-tightening: Raising rates too much can cause recession.

Under-tightening: Keeping rates low for too long can cause runaway inflation.

5. Impact on Financial Markets

5.1 Stock Markets

High Inflation + Rising Rates

Bad for growth stocks (tech, startups) because future earnings are discounted more heavily.

Sectors like utilities, real estate, and consumer discretionary may underperform.

Moderate Inflation + Stable Rates

Can support equities, especially cyclical sectors (industrials, consumer goods).

Low Inflation + Low Rates

Great for growth stocks and speculative investments.

Historical Example:

In 2022, the U.S. Fed hiked rates aggressively to fight 40-year-high inflation. The S&P 500 dropped ~19% for the year, with tech-heavy Nasdaq falling ~33%.

5.2 Bond Markets

When rates rise → bond prices fall (inverse relationship).

Inflation erodes fixed returns from bonds.

TIPS (Treasury Inflation-Protected Securities) outperform during high inflation because they adjust payouts to CPI.

5.3 Currency Markets (Forex)

Higher rates → stronger currency (capital inflows).

Lower rates → weaker currency.

Inflation can weaken a currency if it erodes trust in stability.

Example: The U.S. dollar index (DXY) surged in 2022 due to aggressive Fed hikes.

5.4 Commodities

Inflation often boosts commodity prices (oil, gold, agricultural products).

Gold performs well in high inflation but can underperform when rates rise sharply (due to higher opportunity cost of holding non-yielding assets).

5.5 Real Estate

Higher rates → higher mortgage costs → cooling housing demand.

Inflation in construction materials → higher building costs.

6. Sector-by-Sector Effects

Sector High Inflation Impact High Interest Rate Impact

Technology Negative Very Negative

Energy Positive Neutral to Positive

Consumer Staples Neutral to Positive Neutral

Consumer Discretionary Negative Negative

Financials Positive (loan demand) Positive (better margins)

Real Estate Negative (costs up) Negative (loan cost high)

7. Historical Case Studies

7.1 1970s Stagflation

Inflation above 10%, slow growth, oil shocks.

Fed raised rates to 20% in early 1980s to crush inflation.

Stocks suffered, gold surged.

7.2 2008 Global Financial Crisis

Low inflation but collapsing growth.

Central banks cut rates to near-zero.

Stock markets rebounded post-2009.

7.3 2021–2023 Post-COVID Inflation Surge

Supply chain bottlenecks, stimulus, and energy shocks.

Fed and ECB hiked rates fastest in decades.

Equity valuations compressed, bonds sold off, dollar strengthened.

8. Trading & Investment Strategies

8.1 For High Inflation Environments

Favor real assets (commodities, real estate, infrastructure).

Use inflation-protected bonds.

Short-duration fixed income instead of long bonds.

8.2 For Rising Interest Rates

Reduce exposure to long-duration assets.

Consider value stocks over growth stocks.

Use currency carry trades in favor of higher-rate countries.

8.3 For Falling Rates

Increase equity exposure, especially growth sectors.

Extend bond duration to lock in higher yields before they drop.

Real estate investment can rebound.

9. The Psychology of Markets

Inflation and rate hikes affect sentiment — fear of recession, optimism in easing cycles.

Expectation management by central banks is as important as actual moves.

Markets often price in changes before they happen.

10. Key Takeaways

Inflation and interest rates are interconnected — one drives changes in the other.

Their effects ripple through stocks, bonds, commodities, currencies, and real estate.

Different sectors and asset classes respond differently.

Historical patterns offer guidance but each cycle has unique triggers.

Traders can position based on anticipated shifts rather than reacting late.

Smart Money Concepts1. Introduction: What is Smart Money Concepts?

Smart Money Concepts (SMC) is a modern price action trading methodology that focuses on how big players — institutions, hedge funds, banks, and market makers — move the market.

The core belief: price is manipulated by "smart money" to accumulate positions before large moves, and if you can track their footprints, you can ride their moves instead of getting trapped like retail traders.

In SMC, you don’t rely on indicators that lag behind price. Instead, you learn to read the raw story of price action: where liquidity lies, where stop hunts happen, and where imbalances push price.

Think of it like this:

Retail trading is reacting to price.

SMC trading is predicting what price will want to do, based on smart money’s needs.

2. Core Principles of SMC

SMC builds around a few non-negotiable principles:

2.1 Market Structure

Price moves in waves (higher highs, higher lows in an uptrend, or lower highs, lower lows in a downtrend).

Smart money manipulates these structures:

Break of Structure (BOS): When price breaks a significant swing point in the direction of the trend.

Change of Character (ChoCH): A shift in market bias — often the first sign of trend reversal.

Example:

If we’re in an uptrend and suddenly a major low is broken, this isn’t “random selling.” It’s likely a smart money signal that distribution has started.

2.2 Liquidity

Smart money hunts liquidity pools — areas where retail traders have stop-loss orders:

Above recent highs → stop-losses of short sellers.

Below recent lows → stop-losses of long traders.

Why? Because triggering these stops provides the volume big players need to enter large positions without causing huge slippage.

2.3 Order Blocks

An Order Block is the last opposite candle before a strong impulsive move.

For example:

In an uptrend: the last bearish candle before a strong bullish push.

In a downtrend: the last bullish candle before a strong bearish push.

Order blocks are institutional footprints — zones where smart money likely placed big orders.

2.4 Imbalance & Fair Value Gap (FVG)

Sometimes price moves so fast in one direction that it leaves a gap between candles’ wicks — meaning no trades happened in that range.

Price often revisits these Fair Value Gaps to “rebalance” the market before continuing.

2.5 Premium & Discount Zones

Using Fibonacci retracement, the 50% level divides the market into:

Premium (above 50%) → expensive zone for buying, better for selling.

Discount (below 50%) → cheap zone for buying, better for selling.

Smart money often buys at a discount and sells at a premium.

3. How Smart Money Operates

Retail traders believe price moves randomly — smart money knows better.

3.1 Accumulation & Distribution

Markets cycle through:

Accumulation → Smart money quietly builds positions at low prices.

Manipulation → Stop hunts and fake breakouts to mislead retail traders.

Distribution → Price moves explosively in their intended direction.

3.2 Stop Hunts

Smart money deliberately pushes price to known liquidity areas:

Looks like a breakout to retail traders → but reverses right after.

This traps breakout traders and activates their stops, providing liquidity.

3.3 Inducement

Before moving toward the main liquidity pool, smart money creates a “bait” level to attract retail orders. This induces traders to place stops exactly where smart money wants.

4. SMC Tools & Key Components

4.1 Market Structure Tools

Swing highs/lows

BOS (Break of Structure)

ChoCH (Change of Character)

4.2 Liquidity Identification

Equal highs/lows (double tops/bottoms)

Trendline liquidity (breakouts)

Session highs/lows (London, New York, Asia)

4.3 Order Blocks

Bullish OB → for buys

Bearish OB → for sells

Refined OB → using lower timeframes for precision

4.4 Fair Value Gaps

Look for large impulse moves leaving gaps between candle wicks.

4.5 Fibonacci Levels

Use 50% as a bias divider, 61.8% & 78.6% for sniper entries.

5. The SMC Trading Process

Here’s a step-by-step method to apply SMC:

Step 1: Higher Timeframe Bias

Start from daily (D1) or 4H charts.

Identify market structure (uptrend, downtrend, or range).

Mark major BOS and ChoCH points.

Step 2: Identify Liquidity Pools

Look for equal highs/lows, trendlines, swing points.

Mark where retail traders are likely trapped.

Step 3: Locate Order Blocks

Find the last opposite candle before a strong move.

Confirm it aligns with your higher timeframe bias.

Step 4: Watch for Imbalance

Mark Fair Value Gaps for potential retracements.

Step 5: Entry Execution

Drop to lower timeframes (5M, 1M) for refined entries.

Wait for a lower timeframe BOS in the direction of your trade.

Step 6: Risk Management

Stop-loss just beyond the order block or liquidity sweep point.

Risk 1–2% per trade.

6. Example Trade Setup

Imagine EUR/USD is in an uptrend on 4H:

4H BOS confirmed bullish bias.

Liquidity found below equal lows at 1.0750.

Bullish order block spotted just below 1.0750.

Fair Value Gap in that same area.

On 5M chart → price sweeps liquidity, taps OB, breaks minor high.

Entry after BOS → SL below OB → TP at previous high.

7. SMC vs Traditional Technical Analysis

Aspect Traditional TA SMC

Indicators Uses RSI, MACD, Moving Averages Pure price action

Focus Patterns (Head & Shoulders, etc.) Liquidity, order flow

Timing Often late entries Precision entries

Mindset Follow trend Follow smart money

8. Common Mistakes in SMC Trading

Over-marking charts → clutter leads to confusion.

Forcing trades without waiting for confirmation.

Ignoring higher timeframe bias.

Not managing risk — precision doesn’t mean perfection.

9. Psychology of SMC Trading

SMC can give very high RR trades (1:5, 1:10), but the patience required can be tough.

You need:

Discipline to wait for setups.

Emotional detachment from market noise.

Confidence to enter when it feels counterintuitive.

10. Final Thoughts: Why SMC Works

SMC works because it aligns your trading with the actual drivers of price — the big money.

Instead of being prey, you become a shadow of the predator.

Key takeaways:

Market is a liquidity game.

Learn where smart money is likely to act.

Trade less, but with sniper precision.

Gold Breakouts 3368 then Sell GoldGold Strategy

Gold Breakouts 3368 then sell side activate

Target 🎯 3361,3351,3325,3300

Daily chart 📉 is bearish side

But Deep only buy don't sell

TCS Oversold — Eyeing a Short-Term ReboundTata Consultancy Services (TCS) is approaching oversold territory on the daily chart with RSI near 30, signaling potential for a short-term bounce. Price action is testing support, and risk is well-defined with a 1:1+ risk-reward setup. While the broader IT sector remains under watch, this setup offers an attractive opportunity for swing or short-term traders.

Debt-Free Companies – Hidden Gold for Long-Term Investors!Hello Traders!

In the stock market, stability often beats speed. And one of the biggest signs of a stable company is having little to no debt.

Debt-free companies might not always be flashy, but they quietly build wealth for patient investors.

Today, let’s explore why companies without debt can be hidden gold for long-term portfolios.

Why Debt-Free Matters

More Profits Stay with Shareholders:

When there’s no debt, the company doesn’t have to pay interest. That means more of the profits are available for reinvestment or dividends.

Better Financial Stability:

Debt-free companies can survive economic slowdowns better since they have fewer fixed obligations to meet.

Flexibility for Growth:

With no debt burden, management can focus on expanding, innovating, or entering new markets without worrying about repayment schedules.

Lower Risk for Investors:

Less debt means lower bankruptcy risk. Even in bad market cycles, these companies have a safety cushion.

But Remember…

Debt is Not Always Bad:

Some companies use debt smartly to fuel growth. Being debt-free is great, but also check if they are missing growth opportunities.

Check Other Fundamentals:

A debt-free company with falling sales or poor management is still a bad investment. Always look at revenue trends, ROE, and industry position.

Rahul’s Tip:

Debt-free companies are like a strong foundation, they give you peace of mind. But don’t just chase “zero debt” blindly. Combine it with consistent earnings growth and a competitive edge for the best long-term bets.

Conclusion:

In the hunt for multibaggers, debt-free businesses can be the silent wealth creators. They’re not always in the spotlight, but their strength shows over time.

If you found this helpful, like the post, drop your thoughts in the comments, and follow for more investing insights you can actually use.

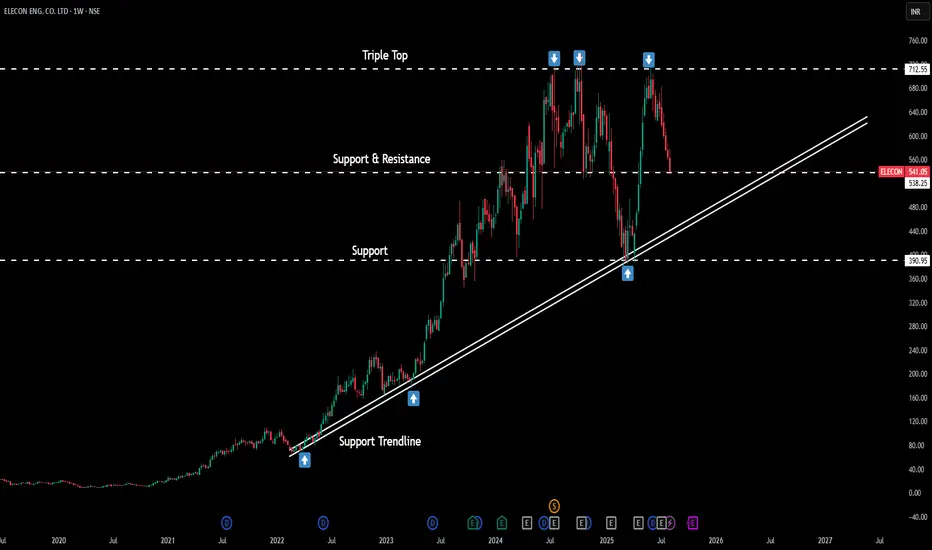

Elecon Engineering Company LtdDate 10.08.2025

Elecon Engineering

Timeframe : Weekly Chart

About :

Company manufactures and sells power transmission and material handling equipment in India and internationally. In addition, it engages in the steel and non-ferrous foundry business.

Business Segment :

(1) Gear Division 72%

(2) Bulk Material Handling Equipment Solutions 28%

Products & Projects :

(1) Coal Handling Plants

(2) Stockyard machines

(3) Wagon Tipplers

(4) Over 2,000 Crushers/Feeders

(5) Pipe Conveyors and specialised belt conveyor systems

(6) Feeders

Foundry Division:

It caters to the machining and foundry needs of Elecon Engineering, providing casting and machining services to several companies other than the Elecon group.

Capacity of 8400 MTPA

Market Position :

Market Share for Industrial gear in India at ~39%

Geographical Revenue Split

India - 77%

Outside India - 23%

Clientele :

Ultratech cement, British Steel, HAYLEY, Tetra Pak, adani, LT, NMDC,SAIL, BHEL etc.

Order Book :

New order intake for FY25 is 2,380 crores

Valuations :

(1) Roce = 28.5%

(2) Roe = 23%

(3) Book Value = 6X

(4) Pe Ratio = 27

(5) Opm = 25%

(6) Promoter Holding = 60%

(7) Sales Growth = 20% (YoY last 3 years)

Regards,

Ankur Singh

What is ROE and Why It’s the True Test of Management Efficiency!Hello Traders!

When it comes to judging how well a company is run, one ratio quietly reveals the truth, ROE (Return on Equity) .

It’s not just a number; it’s a measure of how effectively management uses shareholders’ money to generate profits.

Today, let’s understand what ROE is, why it matters, and how to use it the right way.

What is ROE?

Return on Equity:

ROE shows how much profit a company generates for every ₹1 of shareholder equity.

Example: An ROE of 18% means the company earns ₹0.18 for every ₹1 invested by shareholders.

Formula:

ROE = (Net Profit ÷ Shareholder Equity) × 100

The Higher, The Better, But…:

A high ROE often signals strong management and efficient use of resources, but it’s important to check how that ROE is achieved.

Why ROE is the True Test of Management Efficiency

Measures Profitability from Shareholder’s View:

ROE focuses on returns that actually belong to shareholders, not just overall profits.

Reveals How Capital is Used:

High ROE means the company is using its capital effectively to grow the business.

Filters Out Average Management:

Companies with consistently high ROE often have skilled leaders and a solid strategy.

Exposes Debt-Driven Illusions:

Sometimes ROE looks high only because the company is taking on huge debt. Always check debt-to-equity ratio alongside ROE.

Rahul’s Tip:

Don’t look at ROE in isolation. Compare it with peers in the same industry, and check if it’s consistent over several years.

A one-time spike in ROE doesn’t mean management has suddenly become brilliant.

Conclusion:

ROE is a powerful tool to judge management’s efficiency, but only when used with other checks.

Look for companies with steady, high ROE and reasonable debt.

That’s where strong management and sustainable growth usually go hand in hand.

If you found this useful, like the post, share your view in the comments, and follow for more easy investing insights!