[SM-021] Gaussian Trend System [Optimized]This script is a comprehensive trend-following strategy centered around a Gaussian Channel. It is designed to capture significant market movements while filtering out noise during consolidation phases. This version (v2) introduces code optimizations using Pine Script v6 Arrays and a new Intraday Time Control feature.

1. Core Methodology & Math

The foundation of this strategy is the Gaussian Filter, originally conceptualized by @DonovanWall.

Gaussian Poles: Unlike standard moving averages (SMA/EMA), this filter uses "poles" (referencing signal processing logic) to reduce lag while maintaining smoothness.

Array Optimization: In this specific iteration, the f_pole function has been refactored to utilize Pine Script Arrays. This improves calculation efficiency and rendering speed compared to recursive variable calls, especially when calculating deep historical data.

Channel Logic: The strategy calculates a "Filtered True Range" to create High and Low bands around the main Gaussian line.

Long Entry: Price closes above the High Band.

Short Entry: Price closes below the Low Band.

2. Signal Filtering (Confluence)

To reduce false signals common in trend-following systems, the strategy employs a "confluence" approach using three additional layers:

Baseline Filter: A 200-period (customizable) EMA or SMA acts as a regime filter. Longs are only taken above the baseline; Shorts only below.

ADX Filter (Volatility): The Average Directional Index (ADX) is used to measure trend strength. If the ADX is below a user-defined threshold (default: 20), the market is considered "choppy," and new entries are blocked.

Momentum Check: A Stochastic RSI check ensures that momentum aligns with the breakout direction.

3. NEW: Intraday Session Filter

Per user requests, a time-based filter has been added to restrict trading activity to specific market sessions (e.g., the New York Open).

How it works: Users can toggle a checkbox to enable/disable the filter.

Configuration: You can define a specific time range (Default: 09:30 - 16:00) and a specific Timezone (Default: New York).

Logic: The strategy longCondition and shortCondition now check if the current bar's timestamp falls within this window. If outside the window, no new entries are generated, though existing trades are managed normally.

4. Risk Management

The strategy relies on volatility-based exits rather than fixed percentage stops:

ATR Stop Loss: A multiple of the Average True Range (ATR) is calculated at the moment of entry to set a dynamic Stop Loss.

ATR Take Profit: An optional Reward-to-Risk (RR) ratio can be set to place a Take Profit target relative to the Stop Loss distance.

Band Exit: If the trend reverses and price crosses the opposite band, the trade is closed immediately to prevent large drawdowns.

Credits & Attribution

Original Gaussian Logic: Developed by @DonovanWalll. This script utilizes his mathematical formula for the pole filters.

Strategy Wrapper & Array Refactor: Developed by @sebamarghella.

Community Request: The Intraday Session Filter was added to assist traders focusing on specific liquidity windows.

Disclaimer: This strategy is for educational purposes. Past performance is not indicative of future results. Please use the settings menu to adjust the Session Time and Risk parameters to fit your specific asset class.

ATR

Hash Ratings EngineHash Ratings Engine - Technical Consensus Strategy

A systematic trading strategy that harnesses TradingView's Technical Ratings to generate high-conviction entries with institutional-grade risk management.

What It Does

This strategy aggregates the consensus of 26+ technical indicators (RSI, MACD, Stochastics, multiple Moving Averages, etc.) into a single actionable signal. When enough indicators align bullish or bearish, the engine triggers an entry. Built-in trend filtering and ATR-based exits keep you on the right side of the market.

Key Features

Trend Filter - Only takes longs in uptrends, shorts in downtrends. This single filter typically improves results by 20-40% by avoiding counter-trend trades.

ATR-Based Risk Management - Stop loss and trailing stops adapt to current market volatility. Tight stops in calm markets, wider stops in volatile conditions.

Cooldown System - After a losing trade, the strategy waits before re-entering. This prevents the consecutive loss streaks that destroy accounts.

Clean Visuals - Fluorescent entry/exit signals with price level references. See exactly where you got in and out.

Settings Guide

Indicator Timeframe: Leave blank for current chart. Use higher timeframe for fewer, higher-quality signals.

Rating Source: "All" for balanced approach. "MAs" for trend-following. "Oscillators" for mean-reversion.

Entry Thresholds

Strong Signal Threshold: Higher = fewer trades but better conviction. Start at 0.5, test 0.4-0.6.

Risk Management

ATR Period: 12 is responsive, 14 is standard, 20+ is smoother.

Stop Loss: 2-3x ATR for tight stops, 3.5-4x for moderate, 5x+ for wide.

Trail Activation: How far price must move in profit before trailing begins.

Trail Offset: How closely the trail follows price.

Trend Filter

EMA Length: 150 works well on 4H charts. Use 100 for lower timeframes, 200 for daily.

Trade Timing

Cooldown: Keep enabled. 5 bars is a good starting point.

Best Practices

Start with default settings and backtest on your preferred instrument. Adjust the Strong Signal Threshold first - this has the biggest impact on trade frequency. Then tune the EMA length to match your timeframe. Finally, optimize the ATR multipliers for your risk tolerance.

Works on any liquid market - crypto, forex, stocks, futures. Higher timeframes (4H, Daily) tend to produce cleaner signals than lower timeframes.

Disclaimer

Past performance does not guarantee future results. Always backtest thoroughly and use proper position sizing. This strategy is for educational purposes - trade at your own risk.

DEMA ATR Strategy [PrimeAutomation]⯁ OVERVIEW

The DEMA ATR Strategy combines trend-following logic with adaptive volatility filters to identify strong momentum phases and manage trades dynamically.

It uses a Double Exponential Moving Average (DEMA) anchored to ATR volatility bands, creating a self-adjusting trend baseline.

When the adjusted DEMA shifts direction, the strategy enters positions and scales out profit in phases based on ATR-driven targets.

This system adapts to volatility, filters noise, and seeks sustained directional moves.

⯁ KEY FEATURES

DEMA-Volatility Hybrid Filter

Uses Double EMA with ATR expansion/compression logic to form a dynamic trend baseline.

Directional Shift Entries

Entries occur when the adjusted DEMA flips trend (bullish crossover or bearish crossunder vs its past value).

Noise Reduction Mechanism

ATR range caps extreme moves and prevents false flips during choppy volatility spikes.

Multi-Level Take Profits

Targets scale out positions at 1×, 2×, and 3× ATR multiples in the trade direction.

Volatility-Adaptive Targets

ATR multiplier ensures profit targets expand/contract based on market conditions.

Single-Direction Exposure

No pyramiding; the strategy flips position only when trend shifts.

Automated Trade Finalization

When all profit targets trigger, the position is fully closed.

⯁ STRATEGY LOGIC

Trend Direction:

DEMA baseline is modified using ATR upper/lower envelopes.

• If the adjusted DEMA rises above previous value → Bullish

• If it falls below previous value → Bearish

Entry Rules:

• Enter Long when bullish shift occurs and no long position exists

• Enter Short when bearish shift occurs and no short position exists

Take Profit Logic:

3 partial exits for each trade based on ATR:

• TP1 = ±1× ATR

• TP2 = ±2× ATR

• TP3 = ±3× ATR

Profit distribution: 30% / 30% / 40%

Exit Conditions:

• Exit when all TPs hit (full scale-out if sum of all TPs 100%)

• Opposite trend signal closes current trade and opens new one

⯁ WHEN TO USE

Trending environments

Medium–high volatility phases

Swing trading and intraday trend plays

Markets that respect momentum continuation (crypto, indices, FX majors)

⯁ CONCLUSION

This strategy blends DEMA trend recognition with ATR-based volatility adaptation to generate cleaner directional entries and structured take-profit exits. It is designed to capture momentum phases while avoiding noise-driven false signals, delivering a disciplined and scalable trend-following approach.

Safe Supertrend Strategy (No Repaint)Overview

The Safe Supertrend is a repaint-free version of the popular Supertrend trend-following indicator.

Most Supertrend indicators appear perfect on historical charts because they flip intrabar and then repaint after the candle closes.

This version fixes that by using close-of-bar confirmation only, making every trend flip 100% stable, safe, and non-repainting.

Why This Supertrend Doesn’t Repaint

Most Supertrend indicators calculate their trend direction using the current bar’s data.

But during a live candle:

ATR expands and contracts

The upper/lower bands move

Price moves above/below the band temporarily

A false flip appears → then disappears when the candle closes

That is classic repainting.

This indicator avoids all of that by using:

close > upper

close < lower

This means:

Trend direction flips only based on the previous candle,

No intrabar calculations,

No flickering signals,

No “perfect but fake” historical performance.

Every signal you see on the chart is exactly what was available in real-time.

How It Works

Calculates ATR (Average True Range) and SMA centerline

Builds upper and lower volatility bands

Confirms trend flips only after the previous bar closes

Plots clear bull and bear reversal signals

Works on all markets (crypto, stocks, forex, indices)

No repainting, no recalc, no misleading flips.

Bullish Signal (Trend Up)

A bullish trend begins only when:

The previous candle closes above the upper ATR band,

And this flip is fully confirmed.

A green triangle marks the start of a new uptrend.

Bearish Signal (Trend Down)

A bearish trend begins only when:

The previous candle closes below the lower ATR band,

And the downtrend is confirmed.

A red triangle signals the start of a new downtrend.

Inputs

ATR Length - default 10

ATR Multiplier - default 3.0

Works on all timeframes and market

Simple, but powerful.

Why Use This Version Instead of a Regular Supertrend?

Most Supertrends:

Look great historically

But repaint continuously on live charts

Give false trend flips intrabar

Cannot be reliably used in strategies

This version:

Uses strict previous-bar logic

Never repaints trend direction

Works perfectly in live trading

Backtests accurately

Is ideal for algorithmic strategies

Ideal For:

Trend-following strategies

Breakout trading

Algo trading systems

Reversal detection

Filtering market noise

Swing trading & scalping

Final Note

This is a safer, more reliable Supertrend designed for real-world use — not perfect-looking repaint illusions.

If you use Supertrend in your trading system, this no-repaint version ensures your signals are trustworthy and consistent.

Safe Supertrend Strategy (No Repaint)Overview

The Safe Supertrend is a repaint-free version of the popular Supertrend trend-following indicator.

Most Supertrend indicators appear perfect on historical charts because they flip intrabar and then repaint after the candle closes.

This version fixes that by using close-of-bar confirmation only, making every trend flip 100% stable, safe, and non-repainting.

Why This Supertrend Doesn’t Repaint

Most Supertrend indicators calculate their trend direction using the current bar’s data.

But during a live candle:

ATR expands and contracts

The upper/lower bands move

Price moves above/below the band temporarily

A false flip appears → then disappears when the candle closes

That is classic repainting.

This indicator avoids all of that by using:

close > upper

close < lower

This means:

Trend direction flips only based on the previous candle,

No intrabar calculations,

No flickering signals,

No “perfect but fake” historical performance.

Every signal you see on the chart is exactly what was available in real-time.

How It Works

Calculates ATR (Average True Range) and SMA centerline

Builds upper and lower volatility bands

Confirms trend flips only after the previous bar closes

Plots clear bull and bear reversal signals

Works on all markets (crypto, stocks, forex, indices)

No repainting, no recalc, no misleading flips.

Bullish Signal (Trend Up)

A bullish trend begins only when:

The previous candle closes above the upper ATR band,

And this flip is fully confirmed.

A green triangle marks the start of a new uptrend.

Bearish Signal (Trend Down)

A bearish trend begins only when:

The previous candle closes below the lower ATR band,

And the downtrend is confirmed.

A red triangle signals the start of a new downtrend.

Inputs

ATR Length - default 10

ATR Multiplier - default 3.0

Works on all timeframes and market

Simple, but powerful.

Why Use This Version Instead of a Regular Supertrend?

Most Supertrends:

Look great historically

But repaint continuously on live charts

Give false trend flips intrabar

Cannot be reliably used in strategies

This version:

Uses strict previous-bar logic

Never repaints trend direction

Works perfectly in live trading

Backtests accurately

Is ideal for algorithmic strategies

Ideal For:

Trend-following strategies

Breakout trading

Algo trading systems

Reversal detection

Filtering market noise

Swing trading & scalping

Final Note

This is a safer, more reliable Supertrend designed for real-world use — not perfect-looking repaint illusions.

If you use Supertrend in your trading system, this no-repaint version ensures your signals are trustworthy and consistent.

Hash Supertrend [Hash Capital Research]Hash Supertrend Strategy by Hash Capital Research

Overview

Hash Supertrend is a professional-grade trend-following strategy that combines the proven Supertrend indicator with institutional visual design and flexible time filtering.

The strategy uses ATR-based volatility bands to identify trend direction and executes position reversals when the trend flips.This implementation features a distinctive fluorescent color system with customizable glow effects, making trend changes immediately visible while maintaining the clean, professional aesthetic expected in quantitative trading environments.

Entry Signals:

Long Entry: Price crosses above the Supertrend line (trend flips bullish)

Short Entry: Price crosses below the Supertrend line (trend flips bearish)

Controls the lookback period for volatility calculation

Lower values (7-10): More sensitive to price changes, generates more signals

Higher values (12-14): Smoother response, fewer signals but potentially delayed entries

Recommended range: 7-14 depending on market volatility

Factor (Default: 3.0)

Restricts trading to specific hours

Useful for avoiding low-liquidity sessions, overnight gaps, or known choppy periods

When disabled, strategy trades 24/7

Start Hour (Default: 9) & Start Minute (Default: 30)

Define when the trading session begins

Uses exchange timezone in 24-hour format

Example: 9:30 = 9:30 AM

End Hour (Default: 16) & End Minute (Default: 0)

Controls the vibrancy of the fluorescent color system

1-3: Subtle, muted colors

4-6: Balanced, moderate saturation

7-10: Bright, highly saturated fluorescent appearance

Affects both the Supertrend line and trend zones

Glow Effect (Default: On)

Adds luminous halo around the Supertrend line

Creates a multi-layered visual with depth

Particularly effective during strong trends

Glow Intensity (Default: 5.0)

Displays tiny fluorescent dots at entry points

Green dot below bar: Long entry

Red dot above bar: Short entry

Provides clear visual confirmation of executed trades

Show Trend Zone (Default: On)

Strong trending markets (2020-style bull runs, sustained bear markets)

Markets with clear directional bias

Instruments with consistent volatility patterns

Timeframes: 15m to Daily (optimal on 1H-4H)

Challenging Conditions:

Choppy, range-bound markets

Low volatility consolidation periods

Highly news-driven instruments with frequent gaps

Very low timeframes (1m-5m) prone to noise

Recommended AssetsCryptocurrency:

ATR Trend + RSI Pullback Strategy [Profit-Focused]This strategy is designed to catch high-probability pullbacks during strong trends using a combination of ATR-based volatility filters, RSI exhaustion levels, and a trend-following entry model.

Strategy Logic

Rather than relying on lagging crossovers, this model waits for RSI to dip into oversold zones (below 40) while price remains above a long-term EMA (default: 200). This setup captures pullbacks in strong uptrends, allowing traders to enter early in a move while controlling risk dynamically.

To avoid entries during low-volatility conditions or sideways price action, it applies a minimum ATR filter. The ATR also defines both the stop-loss and take-profit levels, allowing the model to adapt to changing market conditions.

Exit logic includes:

A take-profit at 3× the ATR distance

A stop-loss at 1.5× the ATR distance

An optional early exit if RSI crosses above 70, signaling overbought conditions

Technical Details

Trend Filter: 200 EMA – must be rising and price must be above it

Entry Signal: RSI dips below 40 during an uptrend

Volatility Filter: ATR must be above a user-defined minimum threshold

Stop-Loss: 1.5× ATR below entry price

Take-Profit: 3.0× ATR above entry price

Exit on Overbought: RSI > 70 (optional early exit)

Backtest Settings

Initial Capital: $10,000

Position Sizing: 5% of equity per trade

Slippage: 1 tick

Commission: 0.075% per trade

Trade Direction: Long only

Timeframes Tested: 15m, 1H, and 30m on trending assets like BTCUSD, NAS100, ETHUSD

This model is tuned for positive P&L across trending environments and volatile markets.

Educational Use Only

This strategy is for educational purposes only and should not be considered financial advice. Past performance does not guarantee future results. Always validate performance on multiple markets and timeframes before using it in live trading.

BB SPY Mean Reversion Investment StrategySummary

Mean reversion first, continuation second. This strategy targets equities and ETFs on daily timeframes. It waits for price to revert from a Bollinger location with candle and EMA agreement, then manages risk with ATR based exits. Uniqueness comes from two elements working together. One, an adaptive band multiplier driven by volatility of volatility that expands or contracts the envelope as conditions change. Two, a bias memory that re arms the same direction after any stop, target, or time exit until a true opposite signal appears. Add it to a clean chart, use the markers and levels, and select on bar close for conservative alerts. Shapes can move while the bar is open and settle on close.

Scope and intent

• Markets. Currently adapted for SPY, needs to be optimized for other assets

• Timeframes. Daily primary. Other frames are possible but not the default

• Default demo. SPY on daily

• Purpose. Trade mean reversion entries that can chain into a longer swing by splitting holds into ATR or time segments

Originality and usefulness

• Novelty. Adaptive band width from volatility of volatility plus a persistent bias array that keeps the original direction alive across sequential entries until an opposite setup is confirmed

• Failure modes mitigated. False starts in chop are reduced by candle color and EMA location. Missed continuation after a take profit or stop is addressed by the re arm engine. Oversized envelopes during quiet regimes are avoided by the adaptive multiplier

• Testability. Every module has Inputs and visible levels so users can see why a suggestion appears

• Portable yardstick. All risk and targets are expressed in ATR units

Method overview in plain language

The engine measures where price sits relative to Bollinger bands, confirms with candle color and EMA location, requires ADX for shorts(in our case long close since we use it currently as long only), and optionally requires a trend or mean reversion regime using band width percent rank and basis slope. Risk uses ATR for stop, target, and optional breakeven. A small array stores the last confirmed direction. While flat, the engine keeps a pending order in that direction. The array flips only when a true opposite setup appears.

Base measures

• Range basis. True Range smoothed over a user defined ATR Length

• Return basis. Not required

Components

• Bollinger envelope. SMA length and standard deviation multiplier. Entry is based on cross of close through the band with location bias

• Candle and EMA filter. Close relative to open and close relative to EMA align direction

• ADX gate for shorts. Requires minimum trend strength for short trades

• Adaptive multiplier. Band width scales using volatility of volatility so envelopes breathe with conditions

• Regime gate optional. Band width percent rank and basis slope identify trend or mean reversion regimes

• Risk manager. ATR stop, ATR target, optional breakeven, optional time exit

• Bias memory. Array stores last confirmed direction and re arms entries while flat

Fusion rule

Minimum satisfied gates count style. All required gates must be true. Optional gates are controlled in Inputs. Bias memory never overrides an opposite confirmed setup.

Signal rule

• Long setup when close crosses up through the lower band, the bar closes green, and close is above the long EMA

• Short setup when close crosses down through the upper band, the bar closes red, close is below the short EMA, and ADX is above the minimum

• While flat the model keeps a pending order in the stored direction until a true opposite setup appears

• IN LONG or IN SHORT describes states between entry and exit

What you will see on the chart

• Markers for Long and Short setups

• Exit markers from ATR or time rules

• Reference levels for entry, stop, and target

• Bollinger bands and optional adaptive bands

Inputs with guidance

Setup

• Signal timeframe. Uses the chart timeframe

• Invert direction optional. Flips long and short

Logic

• BB Length. Typical 10 to 50. Higher smooths more

• BB Mult. Typical 1.0 to 2.5. Higher widens entries

• EMA Length long. Typical 10 to 50

• EMA Length short. Typical 5 to 30

• ADX Minimum for short. Typical 15 to 35

Filters

• Regime Type. none or trend or mean reversion

• Rank Lookback. Typical 100 to 300

• Basis Slope Length and Threshold. Larger values reduce false trends

Risk

• ATR Length. Typical 10 to 21

• ATR Stop Mult. Typical 1.0 to 3.0

• ATR Take Profit Mult. Typical 2.0 to 5.0

• Breakeven Trigger R. Move stop to entry after the chosen multiple

• Time Exit. Minimum bars and extension when profit exceeds a fraction of ATR

Bias and rearm

• Bias flips kept. Array depth

• Keep rearm when flat. Maintain a pending order while flat

UI

• Show markers and levels. Clean defaults

Usage recipes

Alerts update in real time and can change while the bar forms. Select on bar close for conservative workflows.

Properties visible in this publication

• Initial capital 25000

• Base currency USD

• If any higher timeframe calls are enabled, request.security uses lookahead off

• Commission 0.03 percent

• Slippage 3 ticks

• Default order size method Percent of equity with value 5

• Pyramiding 0

• Process orders on close On

• Bar magnifier Off

• Recalculate after order is filled Off

• Calc on every tick Off

Realism and responsible publication

No performance claims. Costs and fills vary by venue. Shapes can move intrabar and settle on close. Strategies use standard candles only.

Honest limitations and failure modes

High impact releases and thin liquidity can break assumptions. Gap heavy symbols may require larger ATR. Very quiet regimes can reduce contrast in the mean reversion signal. If stop and target can both be touched inside one bar, outcome follows the TradingView order model for that bar path.

Regimes with extreme one sided trend and very low volatility can reduce mean reversion edges. Results vary by symbol and venue. Past results never guarantee future outcomes.

Open source reuse and credits

None.

Backtest realism

Costs are realistic for liquid equities. Sizing does not exceed five percent per trade by default. Any departure should be justified by the user.

If you got any questions please le me know

PSAR with ATR Trailing Stop + SMA Filter📈 Strategy Overview: PSAR + 6×ATR Trailing Stop with SMA Filter

This strategy is built around the principle of “Cut the losers, let the winners run” — a disciplined, trend-following approach that combines the Parabolic SAR indicator with dynamic risk management and a Simple Moving Average (SMA) trend filter.

🔍 Strategy Logic

Trend Filter Trades are only taken in the direction of the prevailing trend, defined by a user-selected SMA (default: 100).

✅ Long trades only when price is above the SMA

✅ Short trades only when price is below the SMA

Entry Signal: A trade is triggered when the Parabolic SAR flips to the opposite side of the price bars, signaling a potential trend reversal.

Stop Loss: The stop loss is dynamically set at 6×ATR from the entry price. This adapts to market volatility and is recalculated every bar — effectively acting as a trailing stop.

Exit Logic: There is no fixed take profit. The trade remains open until the trailing stop is hit — allowing winners to run and losers to be cut quickly.

Risk Management: Each trade risks 0.5% of total equity, ensuring consistent position sizing and capital preservation.

📊 Visual Elements

PSAR dots mark trend direction changes

SMA line shows the broader trend filter

Trailing stop crosses (with 50% opacity) indicate the current stop level without cluttering the chart

⚙️ Customizable Inputs

PSAR parameters: Start, Increment, Maximum

ATR length and multiplier

SMA length

Risk percentage per trade

This strategy is ideal for traders who want to stay aligned with the trend, automate disciplined exits, and avoid emotional decision-making. Clean, simple, and powerful.

Wishing you calm and successful trades!

Hyper SAR Reactor Trend StrategyHyperSAR Reactor Adaptive PSAR Strategy

Summary

Adaptive Parabolic SAR strategy for liquid stocks, ETFs, futures, and crypto across intraday to daily timeframes. It acts only when an adaptive trail flips and confirmation gates agree. Originality comes from a logistic boost of the SAR acceleration using drift versus ATR, plus ATR hysteresis, inertia on the trail, and a bear-only gate for shorts. Add to a clean chart and run on bar close for conservative alerts.

Scope and intent

• Markets: large cap equities and ETFs, index futures, major FX, liquid crypto

• Timeframes: one minute to daily

• Default demo: BTC on 60 minute

• Purpose: faster yet calmer PSAR that resists chop and improves short discipline

• Limits: this is a strategy that places simulated orders on standard candles

Originality and usefulness

• Novel fusion: PSAR AF is boosted by a logistic function of normalized drift, trail is monotone with inertia, entries use ATR buffers and optional cooldown, shorts are allowed only in a bear bias

• Addresses false flips in low volatility and weak downtrends

• All controls are exposed in Inputs for testability

• Yardstick: ATR normalizes drift so settings port across symbols

• Open source. No links. No solicitation

Method overview

Components

• Adaptive AF: base step plus boost factor times logistic strength

• Trail inertia: one sided blend that keeps the SAR monotone

• Flip hysteresis: price must clear SAR by a buffer times ATR

• Volatility gate: ATR over its mean must exceed a ratio

• Bear bias for shorts: price below EMA of length 91 with negative slope window 54

• Cooldown bars optional after any entry

• Visual SAR smoothing is cosmetic and does not drive orders

Fusion rule

Entry requires the internal flip plus all enabled gates. No weighted scores.

Signal rule

• Long when trend flips up and close is above SAR plus buffer times ATR and gates pass

• Short when trend flips down and close is below SAR minus buffer times ATR and gates pass

• Exit uses SAR as stop and optional ATR take profit per side

Inputs with guidance

Reactor Engine

• Start AF 0.02. Lower slows new trends. Higher reacts quicker

• Max AF 1. Typical 0.2 to 1. Caps acceleration

• Base step 0.04. Typical 0.01 to 0.08. Raises speed in trends

• Strength window 18. Typical 10 to 40. Drift estimation window

• ATR length 16. Typical 10 to 30. Volatility unit

• Strength gain 4.5. Typical 2 to 6. Steepness of logistic

• Strength center 0.45. Typical 0.3 to 0.8. Midpoint of logistic

• Boost factor 0.03. Typical 0.01 to 0.08. Adds to step when strength rises

• AF smoothing 0.50. Typical 0.2 to 0.7. Adds inertia to AF growth

• Trail smoothing 0.35. Typical 0.15 to 0.45. Adds inertia to the trail

• Allow Long, Allow Short toggles

Trade Filters

• Flip confirm buffer ATR 0.50. Typical 0.2 to 0.8. Raise to cut flips

• Cooldown bars after entry 0. Typical 0 to 8. Blocks re entry for N bars

• Vol gate length 30 and Vol gate ratio 1. Raise ratio to trade only in active regimes

• Gate shorts by bear regime ON. Bear bias window 54 and Bias MA length 91 tune strictness

Risk

• TP long ATR 1.0. Set to zero to disable

• TP short ATR 0.0. Set to 0.8 to 1.2 for quicker shorts

Usage recipes

Intraday trend focus

Confirm buffer 0.35 to 0.5. Cooldown 2 to 4. Vol gate ratio 1.1. Shorts gated by bear regime.

Intraday mean reversion focus

Confirm buffer 0.6 to 0.8. Cooldown 4 to 6. Lower boost factor. Leave shorts gated.

Swing continuation

Strength window 24 to 34. ATR length 20 to 30. Confirm buffer 0.4 to 0.6. Use daily or four hour charts.

Properties visible in this publication

Initial capital 10000. Base currency USD. Order size Percent of equity 3. Pyramiding 0. Commission 0.05 percent. Slippage 5 ticks. Process orders on close OFF. Bar magnifier OFF. Recalculate after order filled OFF. Calc on every tick OFF. No security calls.

Realism and responsible publication

No performance claims. Past results never guarantee future outcomes. Shapes can move while a bar forms and settle on close. Strategies execute only on standard candles.

Honest limitations and failure modes

High impact events and thin books can void assumptions. Gap heavy symbols may prefer longer ATR. Very quiet regimes can reduce contrast and invite false flips.

Open source reuse and credits

Public domain building blocks used: PSAR concept and ATR. Implementation and fusion are original. No borrowed code from other authors.

Strategy notice

Orders are simulated on standard candles. No lookahead.

Entries and exits

Long: flip up plus ATR buffer and all gates true

Short: flip down plus ATR buffer and gates true with bear bias when enabled

Exit: SAR stop per side, optional ATR take profit, optional cooldown after entry

Tie handling: stop first if both stop and target could fill in one bar

Twisted Forex's Doji + Area StrategyTitle

Twisted Forex’s Doji + Area Strategy

Description

What this strategy does

This strategy looks for doji candles forming inside or near supply/demand areas . Areas are built from swing pivots and sized with ATR, then tracked for retests (“confirmations”). When a doji prints close to an area and quality checks pass, the strategy places a trade with the stop beyond the doji and a configurable R:R target.

How areas (zones) are built

• Swings are detected with a user-set pivot length.

• Each swing spawns a horizontal area centered at the pivot price with half-height = zoneHalfATR × ATR .

• Duplicates are de-duplicated by center distance (ATR-scaled).

• Areas fade when broken beyond a buffer or after an optional age (expiry).

• Retests are recorded when price touches and then bounces away from the area; repeated reactions increase the zone’s “strength”.

Signal logic (summary)

Doji detection: strict or loose body criteria with optional minimum wick fractions and ATR-scaled minimum range.

Proximity: price must be inside/near a supply or demand area (proxATR × ATR).

Side resolution: overlap is resolved by (a) which side price penetrates more, (b) fast/slow EMA trend, or (c) nearest distance. Optional “previous candle flip” can bias long after a bearish candle and short after a bullish one.

Optional 1-bar confirmation: the bar after the doji must close away from the area by confirmATR × ATR .

Quality filter (Off/Soft/Strict): four checks—(i) wick rejection past the edge, (ii) doji closes in an edge “band” of the area, (iii) fresh touch (cooldown), (iv) approach impulse over a short lookback. In Strict , thresholds auto-tighten.

Orders & exits

• Long: stop below doji low minus buffer; Short: above doji high plus buffer.

• Target = rrMultiple × risk distance .

• Pyramiding is off by default.

Position sizing

You can size from the script or from Strategy Properties:

• Script-driven (default): set Position sizing = “Risk % of equity” and choose riskPercent (e.g., 1.0%). The script applies safe floors/rounding (FX micro-lots by default) so quantity never rounds to zero.

• Properties-driven : toggle Use TV Properties → Order size ON, then pick “Percent of equity” in Properties (e.g., 1%). The header includes safe defaults so trades still place.

Key inputs to explore

• Zone building : pivotLen, zoneHalfATR, minDepartureATR, expiryBars, breakATR, leftBars, dedupeATR.

• Doji & proximity : strictDoji, dojiBodyFrac, minWickFrac, minRangeATR, proxATR, minBarsBetween.

• Overlap resolution : usePenetration, useTrend (EMA 21/55), “previous candle flip”, needNextBarConf & confirmATR.

• Quality : qualityMode (Off/Soft/Strict), minQualPass/kStrict, wickPenATR, edgeBandFrac, approachLookback, approachMinATR, freshTouchBars.

• Zone strength gating : minStrengthSoft / minStrengthStrict.

• HTF confluence (optional) : useHTFTrend (HTF EMA 34/89) and/or useHTFZoneProx (HTF swing bands).

Tips to make it cleaner / higher quality

• Turn needNextBarConf ON and use confirmATR = 0.10–0.15 .

• Increase approachMinATR (e.g., 0.35–0.45) to require a stronger pre-touch impulse.

• Raise minStrengthSoft/Strict (e.g., 4–6) so only well-reacted zones can signal.

• Use signalsOnlyConfirmed ON if you prefer trades only from zones with retests (the script falls back gracefully when none exist yet).

• Nudge proxATR to 0.5–0.6 to demand tighter proximity to the level.

• Optional: enable useHTFTrend to filter counter-trend setups.

Default settings used in this publication

• Initial capital: 100,000 (illustrative).

• Slippage: 1 tick; Commission: 0% (you can raise commission if you prefer—spread is partly modeled by slippage).

• Sizing: Risk % of equity via inputs; riskPercent = 1.0% ; FX uses micro-lot floors by default.

• Quality: Off by default (Soft/Strict available).

• HTF trend gate: Off by default.

Backtesting notes

For a meaningful sample size, test on liquid symbols/timeframes that yield 100+ trades (e.g., majors on 5–15m over 1–2 years). Backtests are modelled and broker costs/spread vary—validate on your feed and forward-test.

How to read the chart

Shaded bands are supply (above) and demand (below). Brighter bands are the nearest K per side (visual aid). BUY/SELL labels mark entries; colored dots show entry/SL/TP levels. You can hide zones or unconfirmed zones for a cleaner view.

Disclaimer

This is educational material, not financial advice. Trading involves risk. Always test and size responsibly.

Trend-Following & Breakout — Index Quant Strategy (NASDAQ)📈 Trend-Following & Breakout — Index Quant Strategy (NASDAQ & S&P 500)

Type: Invite-only strategy

Markets: NASDAQ 100 (NAS100 / US100 / NQ), S&P 500 (US500 / SPX), and other major equity indices.

🧠 Concept: Continuous trend model combining EWMAC (trend-following) and Donchian (breakout) signals, scaled by forecast strength and portfolio risk.

⚙️ Execution: Rebalances only on decision-bar closes, using hysteresis and a no-trade band to reduce churn.

📊 Default bias: Long-only — aligned with equity index drift.

🧩 How it works

• EWMAC Trend: Difference between fast and slow EMAs, normalized by an EWMA of absolute returns.

• Donchian Breakout: Distance beyond a 200-bar channel (Strict mode) or relative z-score position within it.

• Forecast combination: Weighted sum of trend and breakout points, clamped to ± capPoints.

• Hysteresis: Prevents quick sign flips near zero forecast.

• Risk scaling: Maps forecast strength to position size using equity × risk budget × ATR-based stop distance.

• Rebalance: Executes only if the required quantity change exceeds the Δqty threshold; can optionally block increases on Sundays (for CFDs).

⚙️ Default parameters

Deployed on NQ / US100 / NAS100 on Daily Timeframe

• Decision timeframe = 360 min (other options from 1 min to 1 week).

• Trend (EWMAC): Fast = 64, Slow = 256, Vol Norm = 32, Weight = 0.8.

• Breakout (Donchian): Length = 200, Mode = Strict, Weight = 0.2.

• Forecast scaling: ptsPerSigma = 1.0, capPoints = 10.

• Risk % per rebalance = 4 % of equity.

• ATR stop: ATR(14) × 1.0.

• No-trade band (Δqty) = 4 units.

• Hysteresis = 2 forecast points.

• Bias = Long-only (Neutral / Long-bias 50 % optional).

• Skip Sunday increases = false (default).

📋 Backtest properties (documented)

• Initial capital = 100 000 USD.

• Commission = 0.20 % per trade.

• Pyramiding = 10.

• Calc on every tick = false.

• Point value = 1 (for NAS100 CFD).

• No financing or slippage modeled.

• If using CFDs, account for overnight funding.

• On futures (NQ / ES), carry is implicit.

📊 Typical behaviour

• Many small scratches, a few large winners.

• Performs best during multi-week / multi-month trends.

• Underperforms in tight or volatile ranges.

• Average hold ≈ 30 – 90 days in historical tests.

💡 Risk and performance guide (illustrative)

Sharpe ≈ 1.25

Sortino ≈ 1.10 – 1.30

Max drawdown ≈ –18 % to –25 %

Annual volatility ≈ 24 – 28 %

CAGR ≈ 50 – 60 % (at 4 % risk)

Edge ratio ≈ 5 (MFE / MAE)

Historical backtests only — past performance does not guarantee future results.

🌍 Intended markets and timeframes

Optimized for NASDAQ 100 and S&P 500; also effective on similar indices (DAX, Dow Jones, FTSE).

Best on Daily or higher timeframes.

Aligns with long-term index drift — suitable for long-bias systematic trend portfolios.

⚠️ Limitations

• Backtests exclude CFD funding costs.

• Trend models will have losing streaks in range-bound markets.

• Designed for experienced traders seeking systematic exposure.

🔑 Requesting access

Send a private TradingView message to with the text:

“Request access to Trend-Following & Breakout — Index Quant Strategy.”

Access is granted only on explicit request.

For further information, see my TradingView Signature.

🆕 Release notes (v1.0)

• Initial release (360 min TF): EWMAC 64/256 + Donchian 200 Strict.

• Risk 4 %, ATR × 1.0, Long-only bias, hysteresis 2 pts, Δqty ≥ 4.

• Developed for NASDAQ 100 and S&P 500 indices.

• Implements continuous risk-scaled positioning and no-trade band logic.

🧾 Originality statement

This strategy is original work built entirely from TradingView built-ins (EMA, ATR, Highest, Lowest).

It does not reuse open-source invite-only code.

Any future reuse of open scripts will be done with explicit permission and credit.

Universal Breakout Strategy [KedArc Quant]Description:

A flexible breakout framework where you can test different logics (Prev Day, Bollinger, Volume, ATR, EMA Trend, RSI Confirm, Candle Confirm, Time Filter) under one system.

Choose your breakout mode, and the strategy will handle entries, exits, and optional risk management (ATR stops, take-profits, daily loss guard, cooldowns).

An on-chart info table shows live mode values (like Prev High/Low, Bollinger levels, RSI, etc.) plus P&L stats for quick analysis.

Use it to compare which breakout style works best on your instrument and timeframe, whether intraday, swing, or positional trading

🔑 Why it’s useful

* Flexibility: Switch between breakout strategies without loading different indicators.

* Clarity: On-chart info table displays current mode, relevant indicator levels, and live strategy P&L stats.

* Testing efficiency: Quickly A/B test different breakout styles under the same backtest environment.

* Transparency: Every trade is rule-based and displayed with entry/exit markers.

🚀 How it helps traders

* Lets you experiment with breakout strategies quickly without loading multiple scripts.

* Helps identify which breakout method fits your instrument & timeframe.

* Gives clear on-chart visual + statistical feedback for confident decision-making.

⚙️ Input Configuration

* Breakout Mode → choose which strategy to test:

* *Prev Day* → breakouts of yesterday’s High/Low.

* *Bollinger* → Upper/Lower BB pierce.

* *Volume* → Breakout confirmed with volume above average.

* *ATR Stop* → Wide range breakout using ATR filter.

* *Time Filter* → Breakouts inside defined session hours.

* *EMA Trend* → Breakouts only in EMA fast > slow alignment.

* *RSI Confirm* → Breakouts with RSI confirmation (e.g. >55 for longs).

* *Candle Confirm* → Breakouts validated by bullish/bearish candle.

* Lookback / ATR / Bollinger inputs → adjust sensitivity.

* Intrabar mode → option to evaluate breakouts using bar highs/lows instead of closes.

* Table options → show/hide info table, show/hide P&L stats, choose corner placement.

📈 Entry & Exit Logic

* Entry → occurs when breakout condition of chosen mode is met.

* Exit → default exits via opposite signals or optional stop/target if enabled.

* Session filter → optional auto-flat at session end.

* P&L management → optional daily loss guard, cooldown between trades, and ATR-based stop/take profit.

❓ FAQ — Choosing the best setup

Q: Which strategy should I use for which chart?

* *Prev Day Breakouts*: Best on indices, FX, and liquid futures with strong daily levels.

* *Bollinger*: Works well in range-bound environments, or crypto pairs with volatility compression.

* *Volume*: Good on equities where breakout strength is tied to volume spikes.

* *ATR Stop*: Suits volatile instruments (commodities, crypto).

* *EMA Trend*: Useful in trending markets (stocks, indices).

* *RSI Confirm*: Adds momentum filter, better for swing trades.

* *Candle Confirm*: Ideal for scalpers needing visual confirmation.

* *Time Filter*: For intraday traders who want signals only in high-liquidity sessions.

Q: What timeframe should I use?

* Intraday traders → 5m to 15m (Time Filter, Candle Confirm).

* Swing traders → 1H to 4H (EMA Trend, RSI Confirm, ATR Stop).

* Position traders → Daily (Prev Day, Bollinger).

* Breakout

A trade entry condition triggered when price crosses above a resistance level (for longs) or below a support level (for shorts).

* Prev Day High/Low

Formula:

Prev High = High of (Day )

Prev Low = Low of (Day )

* Bollinger Bands

Formula:

Basis = SMA(Close, Length)

Upper Band = Basis + (Multiplier × StdDev(Close, Length))

Lower Band = Basis – (Multiplier × StdDev(Close, Length))

* Volume Confirmation

A breakout is only valid if:

Volume > SMA(Volume, Length)

* ATR (Average True Range)

Measures volatility.

Formula:

ATR = SMA(True Range, Length)

where True Range = max(High–Low, |High–Close |, |Low–Close |)

* EMA (Exponential Moving Average)

Weighted moving average giving more weight to recent prices.

Formula:

EMA = (Price × α) + (EMA × (1–α))

with α = 2 / (Length + 1)

* RSI (Relative Strength Index)

Momentum oscillator scaled 0–100.

Formula:

RSI = 100 – (100 / (1 + RS))

where RS = Avg(Gain, Length) ÷ Avg(Loss, Length)

* Candle Confirmation

Bullish candle: Close > Open AND Close > Close

Bearish candle: Close < Open AND Close < Close

Win Rate (%)

Formula:

Win Rate = (Winning Trades ÷ Total Trades) × 100

* Average Trade P&L

Formula:

Avg Trade = Net Profit ÷ Total Trades

📊 Performance Notes

The Universal Breakout Strategy is designed as a framework rather than a single-asset optimized system. Results will vary depending on the chart, timeframe, and asset chosen.

On the current defaults (15-minute, INR-denominated example), the backtest produced 132 trades over the selected period. This provides a statistically sufficient sample size.

Win rate (~35%) is relatively low, but this is balanced by a positive reward-to-risk ratio (~1.8). In practice, a lower win rate with larger wins versus smaller losses is sustainable.

The average P&L per trade is close to breakeven under default settings. This is expected, as the strategy is not tuned for a single symbol but offered as a universal breakout framework.

Commissions (0.1%) and slippage (1 tick) are included in the simulation, ensuring realistic conditions.

Risk management is conservative, with order sizing set at 1 unit per trade. This avoids over-leveraging and keeps exposure well under the 5-10% equity risk guideline.

👉 Traders are encouraged to:

Experiment with inputs such as ATR period, breakout length, or Bollinger parameters.

Test across different timeframes and instruments (equities, futures, forex, crypto) to find optimal setups.

Combine with filters (trend direction, volatility regimes, or volume conditions) for further refinement.

⚠️ Disclaimer This script is provided for educational purposes only.

Past performance does not guarantee future results.

Trading involves risk, and users should exercise caution and use proper risk management when applying this strategy.

BOCS Channel Scalper Strategy - Automated Mean Reversion System# BOCS Channel Scalper Strategy - Automated Mean Reversion System

## WHAT THIS STRATEGY DOES:

This is an automated mean reversion trading strategy that identifies consolidation channels through volatility analysis and executes scalp trades when price enters entry zones near channel boundaries. Unlike breakout strategies, this system assumes price will revert to the channel mean, taking profits as price bounces back from extremes. Position sizing is fully customizable with three methods: fixed contracts, percentage of equity, or fixed dollar amount. Stop losses are placed just outside channel boundaries with take profits calculated either as fixed points or as a percentage of channel range.

## KEY DIFFERENCE FROM ORIGINAL BOCS:

**This strategy is designed for traders seeking higher trade frequency.** The original BOCS indicator trades breakouts OUTSIDE channels, waiting for price to escape consolidation before entering. This scalper version trades mean reversion INSIDE channels, entering when price reaches channel extremes and betting on a bounce back to center. The result is significantly more trading opportunities:

- **Original BOCS**: 1-3 signals per channel (only on breakout)

- **Scalper Version**: 5-15+ signals per channel (every touch of entry zones)

- **Trade Style**: Mean reversion vs trend following

- **Hold Time**: Seconds to minutes vs minutes to hours

- **Best Markets**: Ranging/choppy conditions vs trending breakouts

This makes the scalper ideal for active day traders who want continuous opportunities within consolidation zones rather than waiting for breakout confirmation. However, increased trade frequency also means higher commission costs and requires tighter risk management.

## TECHNICAL METHODOLOGY:

### Price Normalization Process:

The strategy normalizes price data to create consistent volatility measurements across different instruments and price levels. It calculates the highest high and lowest low over a user-defined lookback period (default 100 bars). Current close price is normalized using: (close - lowest_low) / (highest_high - lowest_low), producing values between 0 and 1 for standardized volatility analysis.

### Volatility Detection:

A 14-period standard deviation is applied to the normalized price series to measure price deviation from the mean. Higher standard deviation values indicate volatility expansion; lower values indicate consolidation. The strategy uses ta.highestbars() and ta.lowestbars() to identify when volatility peaks and troughs occur over the detection period (default 14 bars).

### Channel Formation Logic:

When volatility crosses from a high level to a low level (ta.crossover(upper, lower)), a consolidation phase begins. The strategy tracks the highest and lowest prices during this period, which become the channel boundaries. Minimum duration of 10+ bars is required to filter out brief volatility spikes. Channels are rendered as box objects with defined upper and lower boundaries, with colored zones indicating entry areas.

### Entry Signal Generation:

The strategy uses immediate touch-based entry logic. Entry zones are defined as a percentage from channel edges (default 20%):

- **Long Entry Zone**: Bottom 20% of channel (bottomBound + channelRange × 0.2)

- **Short Entry Zone**: Top 20% of channel (topBound - channelRange × 0.2)

Long signals trigger when candle low touches or enters the long entry zone. Short signals trigger when candle high touches or enters the short entry zone. This captures mean reversion opportunities as price reaches channel extremes.

### Cooldown Filter:

An optional cooldown period (measured in bars) prevents signal spam by enforcing minimum spacing between consecutive signals. If cooldown is set to 3 bars, no new long signal will fire until 3 bars after the previous long signal. Long and short cooldowns are tracked independently, allowing both directions to signal within the same period.

### ATR Volatility Filter:

The strategy includes a multi-timeframe ATR filter to avoid trading during low-volatility conditions. Using request.security(), it fetches ATR values from a specified timeframe (e.g., 1-minute ATR while trading on 5-minute charts). The filter compares current ATR to a user-defined minimum threshold:

- If ATR ≥ threshold: Trading enabled

- If ATR < threshold: No signals fire

This prevents entries during dead zones where mean reversion is unreliable due to insufficient price movement.

### Take Profit Calculation:

Two TP methods are available:

**Fixed Points Mode**:

- Long TP = Entry + (TP_Ticks × syminfo.mintick)

- Short TP = Entry - (TP_Ticks × syminfo.mintick)

**Channel Percentage Mode**:

- Long TP = Entry + (ChannelRange × TP_Percent)

- Short TP = Entry - (ChannelRange × TP_Percent)

Default 50% targets the channel midline, a natural mean reversion target. Larger percentages aim for opposite channel edge.

### Stop Loss Placement:

Stop losses are placed just outside the channel boundary by a user-defined tick offset:

- Long SL = ChannelBottom - (SL_Offset_Ticks × syminfo.mintick)

- Short SL = ChannelTop + (SL_Offset_Ticks × syminfo.mintick)

This logic assumes channel breaks invalidate the mean reversion thesis. If price breaks through, the range is no longer valid and position exits.

### Trade Execution Logic:

When entry conditions are met (price in zone, cooldown satisfied, ATR filter passed, no existing position):

1. Calculate entry price at zone boundary

2. Calculate TP and SL based on selected method

3. Execute strategy.entry() with calculated position size

4. Place strategy.exit() with TP limit and SL stop orders

5. Update info table with active trade details

The strategy enforces one position at a time by checking strategy.position_size == 0 before entry.

### Channel Breakout Management:

Channels are removed when price closes more than 10 ticks outside boundaries. This tolerance prevents premature channel deletion from minor breaks or wicks, allowing the mean reversion setup to persist through small boundary violations.

### Position Sizing System:

Three methods calculate position size:

**Fixed Contracts**:

- Uses exact contract quantity specified in settings

- Best for futures traders (e.g., "trade 2 NQ contracts")

**Percentage of Equity**:

- position_size = (strategy.equity × equity_pct / 100) / close

- Dynamically scales with account growth

**Cash Amount**:

- position_size = cash_amount / close

- Maintains consistent dollar exposure regardless of price

## INPUT PARAMETERS:

### Position Sizing:

- **Position Size Type**: Choose Fixed Contracts, % of Equity, or Cash Amount

- **Number of Contracts**: Fixed quantity per trade (1-1000)

- **% of Equity**: Percentage of account to allocate (1-100%)

- **Cash Amount**: Dollar value per position ($100+)

### Channel Settings:

- **Nested Channels**: Allow multiple overlapping channels vs single channel

- **Normalization Length**: Lookback for high/low calculation (1-500, default 100)

- **Box Detection Length**: Period for volatility detection (1-100, default 14)

### Scalping Settings:

- **Enable Long Scalps**: Toggle long entries on/off

- **Enable Short Scalps**: Toggle short entries on/off

- **Entry Zone % from Edge**: Size of entry zone (5-50%, default 20%)

- **SL Offset (Ticks)**: Distance beyond channel for stop (1+, default 5)

- **Cooldown Period (Bars)**: Minimum spacing between signals (0 = no cooldown)

### ATR Filter:

- **Enable ATR Filter**: Toggle volatility filter on/off

- **ATR Timeframe**: Source timeframe for ATR (1, 5, 15, 60 min, etc.)

- **ATR Length**: Smoothing period (1-100, default 14)

- **Min ATR Value**: Threshold for trade enablement (0.1+, default 10.0)

### Take Profit Settings:

- **TP Method**: Choose Fixed Points or % of Channel

- **TP Fixed (Ticks)**: Static distance in ticks (1+, default 30)

- **TP % of Channel**: Dynamic target as channel percentage (10-100%, default 50%)

### Appearance:

- **Show Entry Zones**: Toggle zone labels on channels

- **Show Info Table**: Display real-time strategy status

- **Table Position**: Corner placement (Top Left/Right, Bottom Left/Right)

- **Color Settings**: Customize long/short/TP/SL colors

## VISUAL INDICATORS:

- **Channel boxes** with semi-transparent fill showing consolidation zones

- **Colored entry zones** labeled "LONG ZONE ▲" and "SHORT ZONE ▼"

- **Entry signal arrows** below/above bars marking long/short entries

- **Active TP/SL lines** with emoji labels (⊕ Entry, 🎯 TP, 🛑 SL)

- **Info table** showing position status, channel state, last signal, entry/TP/SL prices, and ATR status

## HOW TO USE:

### For 1-3 Minute Scalping (NQ/ES):

- ATR Timeframe: "1" (1-minute)

- ATR Min Value: 10.0 (for NQ), adjust per instrument

- Entry Zone %: 20-25%

- TP Method: Fixed Points, 20-40 ticks

- SL Offset: 5-10 ticks

- Cooldown: 2-3 bars

- Position Size: 1-2 contracts

### For 5-15 Minute Day Trading:

- ATR Timeframe: "5" or match chart

- ATR Min Value: Adjust to instrument (test 8-15 for NQ)

- Entry Zone %: 20-30%

- TP Method: % of Channel, 40-60%

- SL Offset: 5-10 ticks

- Cooldown: 3-5 bars

- Position Size: Fixed contracts or 5-10% equity

### For 30-60 Minute Swing Scalping:

- ATR Timeframe: "15" or "30"

- ATR Min Value: Lower threshold for broader market

- Entry Zone %: 25-35%

- TP Method: % of Channel, 50-70%

- SL Offset: 10-15 ticks

- Cooldown: 5+ bars or disable

- Position Size: % of equity recommended

## BACKTEST CONSIDERATIONS:

- Strategy performs best in ranging, mean-reverting markets

- Strong trending markets produce more stop losses as price breaks channels

- ATR filter significantly reduces trade count but improves quality during low volatility

- Cooldown period trades signal quantity for signal quality

- Commission and slippage materially impact sub-5-minute timeframe performance

- Shorter timeframes require tighter entry zones (15-20%) to catch quick reversions

- % of Channel TP adapts better to varying channel sizes than fixed points

- Fixed contract sizing recommended for consistent risk per trade in futures

**Backtesting Parameters Used**: This strategy was developed and tested using realistic commission and slippage values to provide accurate performance expectations. Recommended settings: Commission of $1.40 per side (typical for NQ futures through discount brokers), slippage of 2 ticks to account for execution delays on fast-moving scalp entries. These values reflect real-world trading costs that active scalpers will encounter. Backtest results without proper cost simulation will significantly overstate profitability.

## COMPATIBLE MARKETS:

Works on any instrument with price data including stock indices (NQ, ES, YM, RTY), individual stocks, forex pairs (EUR/USD, GBP/USD), cryptocurrency (BTC, ETH), and commodities. Volume-based features require data feed with volume information but are optional for core functionality.

## KNOWN LIMITATIONS:

- Immediate touch entry can fire multiple times in choppy zones without adequate cooldown

- Channel deletion at 10-tick breaks may be too aggressive or lenient depending on instrument tick size

- ATR filter from lower timeframes requires higher-tier TradingView subscription (request.security limitation)

- Mean reversion logic fails in strong breakout scenarios leading to stop loss hits

- Position sizing via % of equity or cash amount calculates based on close price, may differ from actual fill price

- No partial closing capability - full position exits at TP or SL only

- Strategy does not account for gap openings or overnight holds

## RISK DISCLOSURE:

Trading involves substantial risk of loss. Past performance does not guarantee future results. This strategy is for educational purposes and backtesting only. Mean reversion strategies can experience extended drawdowns during trending markets. Stop losses may not fill at intended levels during extreme volatility or gaps. Thoroughly test on historical data and paper trade before risking real capital. Use appropriate position sizing and never risk more than you can afford to lose. Consider consulting a licensed financial advisor before making trading decisions. Automated trading systems can malfunction - monitor all live positions actively.

## ACKNOWLEDGMENT & CREDITS:

This strategy is built upon the channel detection methodology created by **AlgoAlpha** in the "Smart Money Breakout Channels" indicator. Full credit and appreciation to AlgoAlpha for pioneering the normalized volatility approach to identifying consolidation patterns. The core channel formation logic using normalized price standard deviation is AlgoAlpha's original contribution to the TradingView community.

Enhancements to the original concept include: mean reversion entry logic (vs breakout), immediate touch-based signals, multi-timeframe ATR volatility filtering, flexible position sizing (fixed/percentage/cash), cooldown period filtering, dual TP methods (fixed points vs channel percentage), automated strategy execution with exit management, and real-time position monitoring table.

Trendline Breakout Strategy [KedArc Quant] Description

A single, rule-based system that builds two trendlines from confirmed swing pivots and trades their breakouts, with optional retest, trend-regime gates (EMA / HTF EMA), and ATR-based risk. All parts serve one decision flow: structure → breakout → gated entry → managed risk.

What it does (for traders)

Draws Up line (teal) through the last two Higher Lows and Down line (red) through the last two Lower Highs, then extends them forward.

Long when price breaks above red; Short when price breaks below teal.

Optional Retest entry: after a break, wait for a pullback toward the broken line within an ATR-scaled buffer.

Uses ATR stop and R-multiple target so risk is consistent across symbols/timeframes.

Labels HL1/HL2/LH1/LH2 so non-coders can verify which pivots built each line.

Why these components are combined

Pure breakout systems on trendlines suffer from three practical issues:

False breaks in chop → solved by trend-regime gates (EMA / HTF EMA) that only allow trades aligned with the prevailing trend.

Uneven volatility across markets/timeframes → solved by ATR-based stop/target, normalizing distance so R-multiples are comparable.

First break whipsaws near wedge apices → mitigated by the optional retest rule that demands a pullback/hold before entry.

These modules are not separate indicators with their own signals. They are support roles inside one method.

The pivot engine defines structure, the breakout detector defines signal, the regime gates decide if we’re allowed to take that signal, and the ATR module sizes risk.

Together they make the trendline breakout usable, testable, and explainable.

How it works (mechanism; each component explained)

1) Pivot engine (structure, non-repainting)

Swings are confirmed with ta.pivotlow/high(L, R). A pivot only exists after R bars (no look-ahead), so once plotted, the line built from those pivots will not repaint.

2) Trendline builder (geometry)

Teal line updates when two consecutive pivot lows satisfy HL2.price > HL1.price (and HL2 occurs after HL1).

Red line updates when two consecutive pivot highs satisfy LH2.price < LH1.price.

Lines are extended right and their current value is read every bar via line.get_price().

3) Breakout detector (signal)

On every bar, compute:

crossover(close, redLine) ⇒ Long breakout

crossunder(close, tealLine) ⇒ Short breakdown

4) Regime gates (trend filters, not separate signals)

EMA gate: allow longs only if close > EMA(len), shorts only if close < EMA(len).

HTF EMA gate (optional): same rule on a higher timeframe to avoid fighting the larger trend.

These do not create entries; they simply permit or block the breakout signal.

5) Retest module (optional confirmation)

After a breakout, record the line price. A valid retest occurs if price pulls back within an ATR-scaled buffer toward that broken line and then closes back in the breakout direction.

This reduces first-tick fakeouts.

6) Risk module (position exit)

Initial stop = ATR(len) × atrMult from entry.

Target = tpR × (ATR × atrMult) (e.g., 2R).

This keeps results consistent across instruments/timeframes.

Entries & exits

Long entry

Base: close breaks above red and passes EMA/HTF gates.

Retest (if enabled): after the break, price pulls back near the broken red line (within the ATR buffer) and holds; then enter.

Short entry

Mirror logic with teal (break below & gates), optionally with a retest.

Exit

strategy.exit places ATR stop & R-multiple target automatically.

Optional “flip”: close if the opposite base signal triggers.

How to use it (step-by-step)

Timeframe: 1–15m for intraday, 1–4h for swing.

Start defaults: Pivot L/R = 5, EMA len = 200, ATR len = 14, ATR mult = 2, TP = 2R, Retest = ON.

Tune sensitivity:

Faster lines (more trades): set L/R = 3–4.

Fewer counter-trend trades: enable HTF EMA (e.g., 60-min or Daily).

Visual audit: labels HL1/HL2 & LH1/LH2 show which pivots built each line—verify by eye.

Alerts: use Long breakout, Short breakdown, and Retest alerts to automate.

Originality (why it merits publication)

Trades the visualization: many “auto-trendline” tools only draw lines; this one turns them into testable, alertable rules.

Integrated design: each component has a defined role in the same pipeline—no unrelated indicators bolted together.

Transparent & non-repainting: pivot confirmation removes look-ahead; labels let non-coders understand the setup that produced each signal.

Notes & limitations

Lines update only after pivot confirmation; that lag is intentional to avoid repainting.

Breakouts near an apex can whipsaw; prefer Retest and/or HTF gate in choppy regimes.

Backtests are idealized; forward-test and size risk appropriately.

⚠️ Disclaimer

This script is provided for educational purposes only.

Past performance does not guarantee future results.

Trading involves risk, and users should exercise caution and use proper risk management when applying this strategy.

Gann Fan Strategy [KedarArc Quant]Description

A single-concept, rule-based strategy that trades around a programmatic Gann Fan.

It anchors to a swing (or a manual point), builds 1×1 and related fan lines numerically, and triggers entries when price interacts with the 1×1 (breakout or bounce). Management is done entirely with the fan structure (next/previous line) plus optional ATR trailing.

What TV indicators are used

* Pivots: `ta.pivothigh/ta.pivotlow` to confirm swing highs/lows for anchor selection.

* ATR: `ta.atr` only to scale the 1×1 slope (optional) and for an optional trailing stop.

* EMA: `ta.ema` as a trend filter (e.g., only long above the EMA, short below).

No RSI/MACD/Stoch/Heikin/etc. The logic is one coherent framework: Gann price–time geometry, with ATR as a scale and EMA as a risk filter.

How it works

1. Anchor

* Auto: chooses the most recent *confirmed* pivot (you control Left/Right).

* Manual: set a price and bar index and the fan will hold that point (no re-anchoring).

* Optional Re-anchor when a newer pivot confirms.

2. 1×1 Slope (numeric, not cosmetic)

* ATR mode: `1×1 = ATR(Length) × Multiplier` (adapts to volatility).

* Fixed mode: `ticks per bar` (constant slope).

Because slope is numeric, it doesn’t change with chart zoom, unlike the drawing tool.

3. Fan Lines

Builds classic ratios around the 1×1: 1/8, 1/4, 1/3, 1/2, 1/1, 2/1, 3/1, 4/1, 8/1.

4. Signals

* Breakout: cross of price over/under the 1×1 in the EMA-aligned direction.

* Bounce (optional): touch + reversal across the 1×1 to reduce whipsaw.

5. Exits & Risk

* Take-profit at the next fan line; Stop at the previous fan line.

* If a level is missing (right after re-anchor), a fallback Risk-Reward (RR) is used.

* Optional ATR trailing stop.

Why this is unique

* True numeric fan: The 1×1 slope is calculated from ATR or fixed ticks—not from screen geometry—so it is scale-invariant and reproducible across users/timeframes.

* Deterministic anchor logic: Uses confirmed pivots (with your L/R settings). No look-ahead; anchors update only when the right bars complete.

* Fan-native trade management: Both entries and exits come from the fan structure itself (with a minimal ATR/EMA assist), keeping the method pure.

* Two entry archetypes: Breakout for momentum days; Bounce for range days—switchable without changing the core model.

* Manual mode: Lock a session’s bias by anchoring to a chosen swing (e.g., day’s first major low/high) and keep the fan constant all day.

Inputs (quick guide)

* Auto Anchor (Left/Right): pivot sensitivity. Higher values = fewer, stronger anchors.

* Re-anchor: refresh to newer pivots as they confirm.

* Manual Anchor Price / Bar Index: fixes the fan (turn Auto off).

* Scale 1×1 by ATR: on = adaptive; off = use ticks per bar.

* ATR Length / ATR Multiplier: controls adaptive slope; start around 14 / 0.25–0.35.

* Ticks per bar: exact fixed slope (match a hand-drawn fan by computing slope ÷ mintick).

* EMA Trend Filter: e.g., 50–100; trades only in EMA direction.

* Use Bounce: require touch + reverse across 1×1 (helps in chop).

* TP/SL at fan lines; Fallback RR for missing levels; ATR Trailing Stop optional.

* Transparency/Plot EMA: visual preferences.

Tips

* Range days: larger pivots (L/R 8–12), Bounce ON, ATR Multiplier \~0.30–0.40, EMA 100.

* Trend days: L/R 5–6, Breakout, Multiplier \~0.20–0.30, EMA 50, ATR trail 1.0–1.5.

* Match the TV Gann Fan drawing: turn ATR scale OFF, set ticks per bar = `(Δprice between anchor and 1×1 target) / (bars) / mintick`.

Repainting & testing notes

* Pivots require Right bars to confirm; anchors are set after confirmation (no look-ahead).

* Signals use the current bar close with TradingView strategy mechanics; real-time vs. bar-close can differ slightly, as with any strategy.

* Re-anchoring legitimately moves the structure when new pivots confirm—by design.

⚠️ Disclaimer

This script is provided for educational purposes only.

Past performance does not guarantee future results.

Trading involves risk, and users should exercise caution and use proper risk management when applying this strategy.

Mutanabby_AI | ATR+ | Trend-Following StrategyThis document presents the Mutanabby_AI | ATR+ Pine Script strategy, a systematic approach designed for trend identification and risk-managed position entry in financial markets. The strategy is engineered for long-only positions and integrates volatility-adjusted components to enhance signal robustness and trade management.

Strategic Design and Methodological Basis

The Mutanabby_AI | ATR+ strategy is constructed upon a foundation of established technical analysis principles, with a focus on objective signal generation and realistic trade execution.

Heikin Ashi for Trend Filtering: The core price data is processed via Heikin Ashi (HA) methodology to mitigate transient market noise and accentuate underlying trend direction. The script offers three distinct HA calculation modes, allowing for comparative analysis and validation:

Manual Calculation: Provides a transparent and deterministic computation of HA values.

ticker.heikinashi(): Utilizes TradingView's built-in function, employing confirmed historical bars to prevent repainting artifacts.

Regular Candles: Allows for direct comparison with standard OHLC price action.

This multi-methodological approach to trend smoothing is critical for robust signal generation.

Adaptive ATR Trailing Stop: A key component is the Average True Range (ATR)-based trailing stop. ATR serves as a dynamic measure of market volatility. The strategy incorporates user-defined parameters (

Key Value and ATR Period) to calibrate the sensitivity of this trailing stop, enabling adaptation to varying market volatility regimes. This mechanism is designed to provide a dynamic exit point, preserving capital and locking in gains as a trend progresses.

EMA Crossover for Signal Generation: Entry and exit signals are derived from the interaction between the Heikin Ashi derived price source and an Exponential Moving Average (EMA). A crossover event between these two components is utilized to objectively identify shifts in momentum, signaling potential long entry or exit points.

Rigorous Stop Loss Implementation: A critical feature for risk mitigation, the strategy includes an optional stop loss. This stop loss can be configured as a percentage or fixed point deviation from the entry price. Importantly, stop loss execution is based on real market prices, not the synthetic Heikin Ashi values. This design choice ensures that risk management is grounded in actual market liquidity and price levels, providing a more accurate representation of potential drawdowns during backtesting and live operation.

Backtesting Protocol: The strategy is configured for realistic backtesting, employing fill_orders_on_standard_ohlc=true to simulate order execution at standard OHLC prices. A configurable Date Filter is included to define specific historical periods for performance evaluation.

Data Visualization and Metrics: The script provides on-chart visual overlays for buy/sell signals, the ATR trailing stop, and the stop loss level. An integrated information table displays real-time strategy parameters, current position status, trend direction, and key price levels, facilitating immediate quantitative assessment.

Applicability

The Mutanabby_AI | ATR+ strategy is particularly suited for:

Cryptocurrency Markets: The inherent volatility of assets such as #Bitcoin and #Ethereum makes the ATR-based trailing stop a relevant tool for dynamic risk management.

Systematic Trend Following: Individuals employing systematic methodologies for trend capture will find the objective signal generation and rule-based execution aligned with their approach.

Pine Script Developers and Quants: The transparent code structure and emphasis on realistic backtesting provide a valuable framework for further analysis, modification, and integration into broader quantitative models.

Automated Trading Systems: The clear, deterministic entry and exit conditions facilitate integration into automated trading environments.

Implementation and Evaluation

To evaluate the Mutanabby_AI | ATR+ strategy, apply the script to your chosen chart on TradingView. Adjust the input parameters (Key Value, ATR Period, Heikin Ashi Method, Stop Loss Settings) to observe performance across various asset classes and timeframes. Comprehensive backtesting is recommended to assess the strategy's historical performance characteristics, including profitability, drawdown, and risk-adjusted returns.

I'd love to hear your thoughts, feedback, and any optimizations you discover! Drop a comment below, give it a like if you find it useful, and share your results.

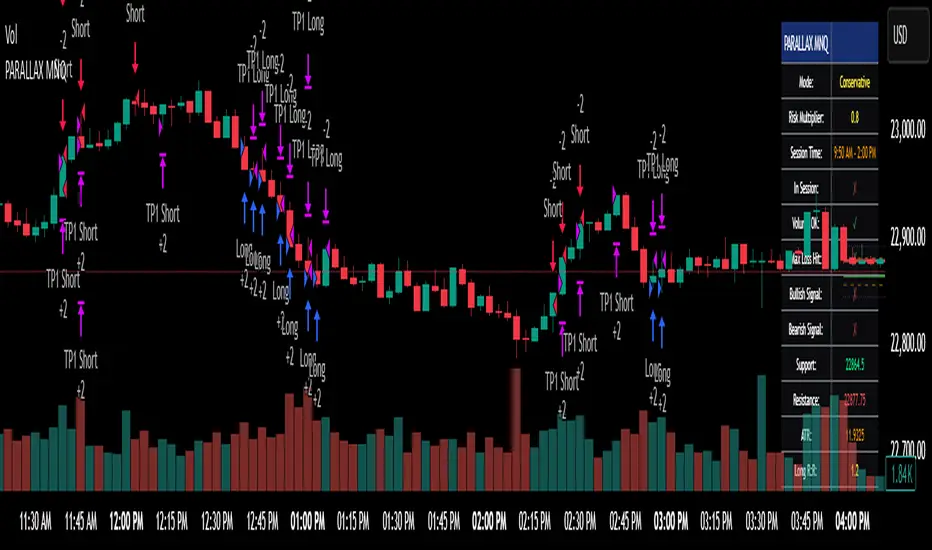

Parallax Momentum MNQ Strategy# 📈 Parallax Momentum MNQ Strategy

## Overview

The Parallax Momentum MNQ Strategy is a sophisticated support/resistance breakout system specifically designed for Micro Nasdaq futures (MNQ) trading (also works on minis). This strategy combines dynamic level detection with momentum confirmation to identify high-probability entry opportunities while maintaining strict risk management protocols.

## 🎯 Key Features

### Core Strategy Logic

- **Dynamic Support/Resistance Detection**: Automatically identifies key levels using configurable lookback periods

- **Momentum Confirmation**: Volume-based filtering ensures trades align with market momentum

- **ATR-Based Risk Management**: Adaptive stop losses and take profits based on market volatility

- **Dual Entry System**: Both long and short opportunities with limit order execution

### Risk Management

- **ATR-Adaptive Stops**: Stop losses and take profits automatically adjust to market volatility

- **Reward-to-Risk Ratios**: Configurable R:R ratios with default 2:1 minimum

- **Maximum Loss Protection**: Optional daily loss limits to prevent overtrading

- **Session Time Filtering**: Trade only during specified market hours

### Strategy Modes

- **Conservative Mode**: 0.8x risk multiplier for cautious trading

- **Balanced Mode**: Standard 1.0x risk multiplier (default)

- **Aggressive Mode**: 1.2x risk multiplier for active trading

## 📊 Visual Features

### Dashboard Display

- Real-time strategy status and performance metrics

- Current support/resistance levels and ATR values

- Live risk-to-reward ratios for potential trades

- Win rate, profit factor, and drawdown statistics

- Adjustable dashboard size and positioning

### Chart Indicators

- Support and resistance lines with labels

- ATR-based levels (+/-1 ATR and +/-2 ATR)

- Dynamic visual updates as levels change

- Configurable line extensions and styling

## ⚙️ Configuration Options

### Entry Filters

- **Volume Filter**: Optional volume confirmation above SMA

- **Session Time Filter**: 12-hour format time restrictions