30 Min Pivot Enhanced# 30 Min Pivot Enhanced

The **30 Min Pivot Enhanced** indicator detects pivot reversals and potential buy/sell signals on the 30-minute timeframe. It combines streak-based trend exhaustion with pivot breakouts and optional flush (capitulation) candle detection.

## Core Logic

- Trend streaks: pivots form after consecutive same-color candles (`trendLength`)

- Flush detection: oversized red candles (ATR based) flagged as potential exhaustion

- Pivot candidates:

- Bullish → after a red streak (or flush) followed by a green candle

- Bearish → after a green streak followed by a red candle

- Confirmation: price must break pivot high/low within `maxBarsAfterPivot`

## Inputs

- Consecutive Trend Candles → streak length required for pivot

- Maximum Bars After Pivot → confirmation window

- Show Pivot Lines → toggle pivot levels on chart

- Flush Detection → ATR-based capitulation detection

- Flush Lookback → how many bars to keep flush valid

- Enable Buy/Sell Alerts → toggle trade alerts

## Visuals

- Buy pivots → green "P Buy" labels under price

- Sell pivots → red pivot lines at lows (if enabled)

- Flush markers → optional debug labels showing capitulation bars

## Alerts

- Buy Alert → price breaks above pivot high

- Sell Alert → price breaks below pivot low

---

Best for traders watching **30-minute reversal plays**, especially where exhaustion or flush candles precede a breakout.

Indicators and strategies

Dynamic Swing Anchored VWAP STRAT (Zeiierman/PineIndicators)Dynamic Swing Anchored VWAP STRATEGY — Zeiierman × PineIndicators (Pine Script v6)

A pivot-to-pivot Anchored VWAP strategy that adapts to volatility, enters long on bullish structure, and closes on bearish structure. Built for TradingView in Pine Script v6.

Full credits to zeiierman.

Repainting notice: The original indicator logic is repainting. Swing labels (HH/HL/LH/LL) are finalized after enough bars have printed, so labels do not occur in real time. It is not possible to execute at historical label points. Treat results as educational and validate with Bar Replay and paper trading before considering any discretionary use.

Concept

The script identifies swing highs/lows over a user-defined lookback ( Swing Period ). When structure flips (most recent swing low is newer than the most recent swing high, or vice versa), a new regime begins.

At each confirmed pivot, a fresh Anchored VWAP segment is started and updated bar-by-bar using an EWMA-style decay on price×volume and volume.

Responsiveness is controlled by Adaptive Price Tracking (APT) . Optionally, APT auto-adjusts with an ATR ratio so that high volatility accelerates responsiveness and low volatility smooths it.

Longs are opened/held in bullish regimes and closed when the regime turns bearish. No short positions are taken by design.

How it works (under the hood)

Swing detection: Uses ta.highestbars / ta.lowestbars over prd to update swing highs (ph) and lows (pl), plus their bar indices (phL, plL).

Regime logic: If phL > plL → bullish regime; else → bearish regime. A change in this condition triggers a re-anchor of the VWAP at the newest pivot.

Adaptive VWAP math: APT is converted to an exponential decay factor ( alphaFromAPT ), then applied to running sums of price×volume and volume, producing the current VWAP estimate.

Rendering: Each pivot-anchored VWAP segment is drawn as a polyline and color-coded by regime. Optional structure labels (HH/HL/LH/LL) annotate the swing character.

Orders: On bullish flips, strategy.entry("L") opens/maintains a long; on bearish flips, strategy.close("L") exits.

Inputs & controls

Swing Period (prd) — Higher values identify larger, slower swings; lower values catch more frequent pivots but add noise.

Adaptive Price Tracking (APT) — Governs the VWAP’s “half-life.” Smaller APT → faster/closer to price; larger APT → smoother/stabler.

Adapt APT by ATR ratio — When enabled, APT scales with volatility so the VWAP speeds up in turbulent markets and slows down in quiet markets.

Volatility Bias — Tunes the strength of APT’s response to volatility (above 1 = stronger effect; below 1 = milder).

Style settings — Colors for swing labels and VWAP segments, plus line width for visibility.

Trade logic summary

Entry: Long when the swing structure turns bullish (latest swing low is more recent than the last swing high).

Exit: Close the long when structure turns bearish.

Position size: qty = strategy.equity / close × 5 (dynamic sizing; scales with account equity and instrument price). Consider reducing the multiplier for a more conservative profile.

Recommended workflow

Apply to instruments with reliable volume (equities, futures, crypto; FX tick volume can work but varies by broker).

Start on your preferred timeframe. Intraday often benefits from smaller APT (more reactive); higher timeframes may prefer larger APT (smoother).

Begin with defaults ( prd=50, APT=20 ); then toggle “Adapt by ATR” and vary Volatility Bias to observe how segments tighten/loosen.

Use Bar Replay to watch how pivots confirm and how the strategy re-anchors VWAP at those confirmations.

Layer your own risk rules (stops/targets, max position cap, session filters) before any discretionary use.

Practical tips

Context filter: Consider combining with a higher-timeframe bias (e.g., daily trend) and using this strategy as an entry timing layer.

First pivot preference: Some traders prefer only the first bullish pivot after a bearish regime (and vice versa) to reduce whipsaw in choppy ranges.

Deviations: You can add VWAP deviation bands to pre-plan partial exits or re-entries on mean-reversion pulls.

Sessions: Session-based filters (RTH vs. ETH) can materially change behavior on futures and equities.

Extending the script (ideas)

Add stops/targets (e.g., ATR stop below last swing low; partial profits at k×VWAP deviation).

Introduce mirrored short logic for two-sided testing.

Include alert conditions for regime flips or for price-VWAP interactions.

Incorporate HTF confirmation (e.g., only long when daily VWAP slope ≥ 0).

Throttle entries (e.g., once per regime flip) to avoid over-trading in ranges.

Known limitations

Repainting: Swing labels and pivot confirmations depend on future bars; historical labels can look “perfect.” Treat them as annotations, not executable signals.

Execution realism: Strategy includes commission and slippage fields, yet actual fills differ by venue/liquidity.

No guarantees: Past behavior does not imply future results. This publication is for research/education only and not financial advice.

Defaults (backtest environment)

Initial capital: 10,000

Commission value: 0.01

Slippage: 1

Overlay: true

Max bars back: 5000; Max labels/polylines set for deep swing histories

Quick checklist

Add to chart and verify that the instrument has volume.

Use defaults, then tune APT and Volatility Bias with/without ATR adaptation.

Observe how each pivot re-anchors VWAP and how regime flips drive entries/exits.

Paper trade across several symbols/timeframes before any discretionary decisions.

Attribution & license

Original indicator concept and logic: Zeiierman — please credit the author.

Strategy wrapper and publication: PineIndicators .

License: CC BY-NC-SA 4.0 (Attribution-NonCommercial-ShareAlike). Respect the license when forking or publishing derivatives.

Bank Strategy v2# Multi-Signal Confirmation Strategy (MSCS)

## Overview

The Multi-Signal Confirmation Strategy is a comprehensive technical analysis indicator that combines multiple confirmation signals to generate high-probability buy and sell opportunities. This indicator is designed to reduce false signals by requiring multiple technical confirmations before generating trading alerts.

## Key Features

### 🎯 **Multi-Confirmation System**

- Requires 2-5 confirmations before signal generation

- Reduces false signals and improves signal quality

- Customizable confirmation threshold

### 📊 **Technical Analysis Components**

1. **Trend Analysis** - Multiple moving average types (SMA, EMA, WMA, RMA)

2. **Liquidity Detection** - Identifies key support/resistance levels

3. **Manipulation Patterns** - Detects false moves and liquidity hunts

4. **Order Blocks** - Recognizes institutional order flow patterns

5. **Imbalances** - Identifies price gaps and imbalances

6. **Volume Analysis** - Detects significant volume spikes

### 🔍 **Signal Types**

#### Bullish Confirmations:

- Price above moving average (bullish trend)

- Support level liquidity hunt

- False move down pattern

- Bullish engulfing pattern

- Bullish gap/imbalance

- Volume spike confirmation

#### Bearish Confirmations:

- Price below moving average (bearish trend)

- Resistance level liquidity hunt

- False move up pattern

- Bearish engulfing pattern

- Bearish gap/imbalance

- Volume spike confirmation

## How to Use

### 📋 **Settings Configuration**

1. **Signal Configuration:**

- Set minimum confirmations (2-5 signals)

- Enable/disable status table display

2. **Visual Display:**

- Toggle liquidity levels visibility

- Show/hide manipulation zones

- Optional moving average line display

3. **Moving Average Settings:**

- Choose MA period (1-500, default: 200)

- Select MA type (SMA, EMA, WMA, RMA)

### 🎯 **Entry Management**

- Automatic entry level calculation (25% retracement from signal candle)

- Entry timeout after 10 bars to avoid stale signals

- Clear entry confirmation markers on chart

### 📈 **Visual Elements**

- **Green Triangle Up**: Buy signal generated

- **Red Triangle Down**: Sell signal generated

- **Yellow Lines**: Entry levels awaiting execution

- **"ENTRY" Labels**: Entry level triggered

- **Dashed Lines**: Key liquidity levels

- **Colored Boxes**: Manipulation zones (FM = False Move)

## Alert System

The indicator provides four types of alerts:

1. **Buy Signal Generated** - When bullish confirmations meet threshold

2. **Sell Signal Generated** - When bearish confirmations meet threshold

3. **Buy Entry Triggered** - When price reaches calculated buy entry level

4. **Sell Entry Triggered** - When price reaches calculated sell entry level

## Status Information Panel

The indicator includes a comprehensive status table showing:

- Current market trend direction

- Number of bullish confirmations active

- Number of bearish confirmations active

- Required confirmation threshold

- Current position status (awaiting buy/sell/none)

## Best Practices

### ✅ **Recommended Usage**

- Use higher timeframes (4H, Daily) for stronger signals

- Combine with proper risk management and position sizing

- Wait for entry level confirmation before taking trades

- Consider market context and overall trend direction

### ⚠️ **Risk Management**

- This indicator is for educational and analytical purposes

- Always use proper stop-loss and take-profit levels

- Do not risk more than you can afford to lose

- Backtest thoroughly before live trading

### 🔧 **Optimization Tips**

- Adjust confirmation requirements based on market volatility

- Higher confirmations = fewer but higher quality signals

- Lower confirmations = more signals but potentially more noise

- Test different MA periods for your specific market/timeframe

## Technical Specifications

- **Pine Script Version**: v5

- **Overlay**: Yes (displays on price chart)

- **Maximum Bars Back**: 100 (optimized for performance)

- **Repainting**: No (signals are final once bar closes)

## Educational Disclaimer

This indicator is designed for educational and informational purposes only. It should not be used as the sole basis for trading decisions. Always conduct your own analysis, consider multiple factors, and implement proper risk management strategies. Past performance does not guarantee future results.

Live Trade Table [NuengChill]signal for live trade score

when you live trade you can add signal as you trade

table

1. trade number

2. type Buy or sell waiting

3. entry price

4. TP1 , TP2

5. SL

6. win/ Lose result

7. statue => Active , SL hit , TP hit , TP2 hit

Bank Strategy v1 Pro # Bank Strategy v1 Pro - Advanced Institutional Trading System

## Overview

Bank Strategy v1 Pro is a sophisticated institutional-grade trading indicator designed for professional traders who understand advanced market microstructure concepts. This system implements the precise methodologies used by institutional traders to identify high-probability reversal opportunities through liquidity manipulation patterns.

## Core Methodology

### 🏦 **Institutional Trading Framework**

This strategy is built upon the fundamental principle that institutional players (banks, hedge funds, market makers) create specific patterns when accumulating or distributing positions. The indicator identifies these patterns through:

- **Liquidity Manipulation Sequences** - Detection of deliberate stop-loss hunting

- **False Move (FU) Patterns** - Identification of engineered price movements

- **Order Block Analysis** - Recognition of institutional accumulation/distribution zones

- **Imbalance Trading** - Exploitation of price inefficiencies

- **Market Structure Context** - Trend-based signal filtering

### 📊 **Advanced Signal Components**

#### 1. **Liquidity Zone Identification**

- Automated detection of swing highs/lows where retail stops accumulate

- Dynamic liquidity level tracking with 30-bar extension

- Real-time monitoring of liquidity sweeps and hunts

#### 2. **False Move (FU) Pattern Recognition**

- **Bullish FU**: High manipulation → Close below previous low (bearish trap)

- **Bearish FU**: Low manipulation → Close above previous high (bullish trap)

- Institutional reversal confirmation after liquidity grab

#### 3. **Order Block Detection**

- Bullish Engulfing: Strong institutional buying after bearish candle

- Bearish Engulfing: Strong institutional selling after bullish candle

- 20-bar forward projection for order block validity

#### 4. **Price Imbalance Analysis**

- Bullish Imbalance: Gap up indicating buying pressure

- Bearish Imbalance: Gap down indicating selling pressure

- 15-bar tracking with automatic labeling

## Signal Generation Logic

### 🎯 **Entry Criteria**

**Buy Signal Requirements:**

- Bearish FU pattern detected (liquidity grab below previous low)

- Price above 200 SMA (bullish market context)

- Liquidity lows available for targeting

- Signal confirmation enabled

**Sell Signal Requirements:**

- Bullish FU pattern detected (liquidity grab above previous high)

- Price below 200 SMA (bearish market context)

- Liquidity highs available for targeting

- Signal confirmation enabled

### 📈 **Advanced Entry Management**

- **Entry Level**: 50% retracement of manipulation candle body

- **Stop Loss**: 20% extension below/above manipulation range

- **Take Profit**: Configurable risk-reward ratio (1:1 to 1:5)

- **Timeout**: 15-bar automatic signal expiry

## Professional Features

### 🔧 **Customizable Parameters**

- **Signal Control**: Independent buy/sell signal toggles

- **Visual Elements**: Modular display of order blocks, imbalances, liquidity zones

- **Risk Management**: Adjustable risk-reward ratios up to 1:5

- **Market Structure**: Configurable swing length (3-20 periods)

- **MA Filter**: Optional 200 SMA trend context

### 📊 **Real-Time Status Monitoring**

Professional status table displaying:

- Current market trend direction

- Liquidity availability status

- Active entry waiting status

- Risk-reward configuration

- System health indicators

### 🚨 **Professional Alert System**

- **Signal Alerts**: Instant notification of buy/sell opportunities

- **Entry Alerts**: Confirmation when entry levels are reached

- **Custom Messages**: Detailed alert descriptions for trade management

## Advanced Visual Analysis

### 🎨 **Color-Coded Elements**

- **Green Boxes**: Bullish order blocks (institutional buying zones)

- **Red Boxes**: Bearish order blocks (institutional selling zones)

- **Blue/Orange Boxes**: Price imbalances requiring fill

- **Purple Boxes**: FU patterns with directional labels

- **Dotted Lines**: Key liquidity levels with labels

- **Yellow Lines**: Pending entry levels

### 📍 **Professional Labeling**

- Clear identification of all pattern types

- Directional bias indicators

- Entry confirmation markers

- Liquidity level annotations

## Risk Management Framework

### ⚠️ **Professional Trading Guidelines**

- **Timeframe Recommendation**: 4H+ for institutional signal reliability

- **Position Sizing**: Risk no more than 1-2% per signal

- **Confirmation**: Wait for entry level hits before position entry

- **Context**: Always consider overall market structure and sentiment

### 🛡️ **Built-in Protections**

- Automatic signal timeout prevents stale entries

- Trend context filtering reduces counter-trend risks

- Liquidity requirement ensures sufficient market depth

- Risk-reward enforcement maintains positive expectancy

## Performance Optimization

### ⚡ **Technical Specifications**

- **Pine Script v5**: Latest version compatibility

- **Resource Limits**: Optimized for 500 bars, 200 lines, 100 boxes, 200 labels

- **Processing**: Efficient array management for liquidity tracking

- **Memory**: Automatic cleanup of expired signals and objects

### 🎯 **Signal Quality**

- High-probability setups through multi-factor confirmation

- Institutional pattern recognition reduces retail noise

- Trend context filtering improves win rate

- Professional entry timing reduces slippage

## Educational Framework

### 📚 **Institutional Concepts**

This indicator teaches professional trading concepts:

- Market microstructure understanding

- Institutional order flow analysis

- Liquidity-based trading strategies

- Professional risk management techniques

### 🎓 **Skill Development**

- Pattern recognition training

- Market structure analysis

- Trade timing optimization

- Risk management discipline

## Disclaimer

This indicator is designed for professional traders with experience in institutional trading concepts. It requires understanding of market microstructure, liquidity dynamics, and professional risk management. Past performance does not guarantee future results. Always implement proper risk management and consider multiple analysis factors before making trading decisions.

## Compatibility

- **Markets**: Forex, Indices, Cryptocurrencies, Commodities

- **Timeframes**: Optimized for 1H and above (4H+ recommended)

- **Platform**: TradingView Pine Script v5

- **Features**: Full alert integration, customizable display options

CQ_Historical Candle Color Changer🎯 Purpose

This indicator visually distinguishes candles based on how old they are—specifically within a user-defined range (e.g., 1 to 7 days old). It helps traders quickly isolate recent price action from older data, making it easier to interpret overlays like moving averages, volume profiles, or momentum indicators.

⚙️ Key Features

- User-Defined Age Range: Set minimum and maximum age in days (e.g., highlight candles that are 1–7 days old).

- Custom Colors: Choose highlight colors for candles within the range.

- Timeframe Awareness: Works across any chart timeframe (1m, 1h, 1D, etc.), calculating candle age based on actual time elapsed.

- Non-Intrusive Display: Candles outside the range retain their default appearance, preserving overall chart readability.

📐 How It Works

- The script calculates the age of each candle by comparing its timestamp to the current time.

- If the candle falls within the user-defined age range, it’s recolored using the selected style.

- Candles older or newer than the range are left untouched.

🧠 Use Cases

- Trend Isolation: Focus on recent price action without losing sight of broader context.

RSI OB/OSRSI OB/OS Signals indicator

The RSI OB/OS Signals indicator is an analysis and training tool that uses simple statistical learning (rolling correlations and z-scoring) to produce a smoothed, adaptive RSI weighting and signal line intended to highlight probable short-term RSI movements. The script does not attempt black-box machine-learning model export instead, it uses transparent building blocks — returns, RSI, ATR percentage, volume change (log), and raw volume — as predictors to estimate the likely next-bar RSI, then converts that estimate into a bounded “weight” and a smoothed signal line. The objective is educational: show how simple correlation-based weighting of standardized features can serve as an RSI augmentation and help traders identify higher-probability bullish or bearish RSI cross conditions, while making all internal reasoning visible and explainable.

At its core the indicator performs three conceptual steps each bar: first it computes a set of per-bar features aligned to the target (prior bar RSI) — specifically prior-bar log returns, prior-bar RSI, ATR as percent of price, the log change in volume and the prior-bar raw volume.

Second it standardizes these predictors through rolling z-scoring and computes rolling Pearson correlations between each standardized predictor and the target RSI over a user-configurable learning window. These correlations act as signed linear weights: predictors with higher absolute correlation are treated as more informative for that window.

Third it forms a linear prediction by summing correlation × z(feature) across the top correlated predictors, then maps that standardized prediction back to RSI scale using the rolling mean and standard deviation of the target. The mapped prediction is finally converted to a bounded “rsiWeight,” smoothed by a signal moving average, and used to produce bullish/bearish events on crossovers of preconfigured thresholds.

VWAP, buy/sell volume breakdown and simple tracking of the price move since the last signal are also displayed to help traders interpret the quality of signals.

The components are chosen for clear, complementary roles rather than as a random mashup. Prior-bar RSI embodies short-term momentum and is the natural prediction target.

Log returns add price-direction information; ATR percent encodes the intrabar volatility regime (helpful because RSI behaviour differs in high vs low volatility); the volume log-change and raw volume provide a participation signal indicating whether structural moves are supported by real activity. Standardizing predictors and using rolling correlations lets the script adapt its emphasis to the current regime: when volume changes correlate strongly with subsequent RSI moves, the algorithm will weight that predictor more heavily; when returns correlate more, weight shifts accordingly. Because the method is linear, transparent and computed on rolling windows you can reproduce and reason about the weight changes — a key requirement for educational clarity and TradingView compliance.

How to read and use the indicator practically: treat the smoothed rsiWeight line (ma_rsi) and its threshold crossings as an RSI-augmentation alert — not as a standalone automated buy/sell system. A practical workflow is: first inspect the dashboard and confirm the underlying drivers (which predictors show strong z-scores and which had high rolling correlation in the learning window); second check VWAP position and volume split to ensure that the price move is supported; third only consider signals that coincide with your higher-timeframe bias or structural support/resistance.

For example, a bullish crossover (ma_rsi crossing above −0.5) that occurs while VWAP is below price, buy volume share is elevated, and ATR is moderate is a higher-quality setup than the same crossing on thin volume and extreme ATR.

Use ATR or recent swing structure for stop placement and predefine risk per trade. Because the indicator tracks max points since the last signal, you can also use that metric as a simple intraday performance monitor.

Parameter tuning guidance: the learning window (learnLen) controls how quickly the correlation weights adapt; a short window (e.g., 10–20) makes the predictor weights responsive to regime shifts but also noisier; a longer window (e.g., 40–80) smooths weights and emphasizes longer-term relationships.

The rsiLen (target RSI length) should match your intended horizon — 14 is standard and balances responsiveness and smoothness. sigLen controls the smoothing of the predicted RSI weight: lower values make the signal line more reactive (useful for scalping), higher values produce smoother signals (useful for swing trades).

For low-liquidity instruments increase learnLen and sigLen to reduce false alarms; for high-speed intra-day work shorten them. Volume heuristics (volume thresholds) are instrument dependent — calibrate volume formatting and volumetric thresholds for equities versus futures or crypto.

Limitations and failure modes are explicit and important: the feature-selection approach is linear and based on Pearson correlation — it cannot capture nonlinear dependencies or temporal lags beyond the single lag studied, so it may miss relationships that require higher-order features.

The volume split used (close>open vs closeopen vs close

VIDYA with trend centered SDs with Chandelier Exit By KidevThis multi-tool overlay combines adaptive averaging, volatility envelopes, and structural swing detection into a single, configurable indicator.

Features

• Selectable MA75 — choose SMA / EMA / WMA / VWMA / HMA as the 75-length baseline.

• MA Trend Mode — optional up/side/down regime coloring driven by MA slope (configurable colors).

• VIDYA (Variable Index Dynamic Average) — adaptive moving average with cross (C>V / CV / C

Confluence Engine Confluence Engine is a practical, non-repainting decision aid that scores market conditions from −100…+100 by combining six proven modules: Trend, Momentum, Volatility, Volume, Structure, and an HTF confirmation. It’s designed for crypto, forex, indices, and stocks, and it fires entries only on confirmed bar closes.

What’s inside

Trend: EMA 20/50/200 alignment plus a Supertrend/KAMA toggle (you choose the baseline).

Momentum: RSI + MACD with confirmed-pivot divergence detection.

Volatility: ATR% and Bollinger Band width vs its average to favor expansion over chop.

Volume: OBV-style cumulative flow slope + volume surge vs SMA×multiplier.

Market Structure: Confirmed pivots, BOS (break of structure) and CHOCH (change of character).

HTF Filter: Closed higher-timeframe context via request.security(..., barmerge.gaps_on, barmerge.lookahead_off).

Why it does not repaint

Signals are computed and plotted on closed bars only.

Pivots/divergences use confirmed pivot points (no forward look).

HTF series are fetched with lookahead_off and use the last closed HTF bar in realtime.

No future bar references are used for entries or alerts.

How to use (3 steps)

Pick a timeframe pair: use a 4–6× HTF multiplier (5m→30m, 15m→1h, 1h→4h, 4h→1D, 1D→1W).

Trade with the HTF: take longs only when the HTF filter is bullish; shorts only when bearish.

Prefer expansion: act when BB width > its average and ATR% is elevated; skip most signals in compression.

Suggested presets (start here)

Crypto (BTC/ETH): 15m→1h, 1h→4h. stLen=10, stMult=3.0, bbLen=20, surgeMul=1.8–2.2, thresholds +40 / −40 (intraday can try +35 / −35).

Forex majors: 15m→1h, 1h→4h. stLen=10–14, stMult=2.5–3.0, surgeMul=1.5–1.8, thresholds +35 / −35 (swing: +45 / −45).

US equities (liquid): 5m→30m/1h, 15m→1h/2h. stMult=3.0–3.5, surgeMul=1.6–2.0, thresholds +45 / −45 to reduce chop.

Indices (ES/NQ): 5m→30m, 15m→1h. Defaults are fine; start at +40 / −40.

Gold/Oil: 15m→1h, 1h→4h. Thresholds +35 / −35, surgeMul=1.6–1.9.

Inputs (plain English)

Use Supertrend (off = KAMA): choose the trend baseline.

EMA Fast/Mid/Slow: 20/50/200 by default for classic stack.

RSI/MACD + divergence pivots: momentum and exhaustion context.

ATR Length & BB Length: volatility regime detection.

Volume SMA & Surge Multiplier: defines “meaningful” volume spikes.

Pivot left/right & “Confirm BOS/CHOCH on Close”: structure strictness.

Enable HTF & Higher Timeframe: confirms the lower timeframe direction.

Thresholds (+long / −short): when the score crosses these, you get signals.

Signals & alerts (IDs preserved)

Entry shapes plot at bar close when the score crosses thresholds.

Alerts you can enable:

CONFLUENCE LONG — long entry signal

CONFLUENCE SHORT — short entry signal

BULLISH BIAS — score turned positive

BEARISH BIAS — score turned negative

Best practices

Focus on signals with HTF agreement and volatility expansion; require volume participation (surge or rising OBV slope) for higher quality.

Raise thresholds (+45/−45 or +50/−50) to reduce whipsaws in choppy sessions.

Lower thresholds (+35/−35) only if you also require volatility/volume filters.

Performance & scope

Works across crypto/FX/equities/indices; no broker data or special feeds required.

No repainting by design; signals/alerts are computed on closed bars.

As with any tool, results vary by regime; always combine with risk management.

Disclosure

This script is for educational purposes only and is not financial advice. Trading involves risk. Test on historical data and paper trade before using live.

Contract Interest Turnover T3 [T69]Overview

--------

Contract Interest Turnover (CIT) estimates how “churny” a crypto derivatives market is by comparing the amount traded in a bar to the base stock of outstanding contracts (open interest). It normalizes both Volume and Open Interest (OI) by Price (Close), then plots a Turnover Rate = (Volume/Close) ÷ (OI/Close) as colored columns. Higher values = faster contract recycling (strong momentum / hype potential).

Features

--------

- Auto-fetch OI: Pulls OI via request.security(_OI, …) when the exchange/symbol exposes an OI stream on TradingView.

- Price-normalized comparison: Converts both Volume and OI into comparable notional terms by dividing each by Close.

- Turnover columns with threshold: Color the columns green once Turnover ≥ your set threshold; gray otherwise.

- Status-line readouts: Displays normalized Volume and OI values for quick sanity checks.

- Crypto-aware timeframe: Uses chart TF for crypto; forces daily OI when not crypto to avoid noisy intraday pulls.

How to Use

----------

1. Add the script on a perpetual/futures symbol that has OI on TradingView (e.g., BTC perps where an _OI feed exists).

2. Watch the Turnover Rate bars: spikes above your threshold flag sessions where contracts are actively flipping.

3. Interpret spikes as a signal of movement or activity — it does not specify price direction, only that the market is engaged and contracts are being traded more intensely than usual.

Configuration

-------------

- Interest Turnover Threshold (default 1.0): colors columns green when Turnover ≥ threshold. Tune per market’s typical churn profile.

Under the Hood (Formulas & Logic)

---------------------------------

- Fetch OI

oiClose ← request.security(ticker.standard(syminfo.tickerid) + "_OI", timeframe, close) with ignore_invalid_symbol = true.

If none is found, the script throws a clear runtime error.

- Normalize to price

vol_norm = volume / close

oi_norm = oiClose / close

This converts both to a common notional basis so their ratio is meaningful even as price changes.

- Turnover Rate

turnover = vol_norm / oi_norm

Interpretation: fraction/multiples of the outstanding contract base traded in the bar. Color = green if turnover ≥ threshold.

Why Open Interest ≈ “Float” Proxy

---------------------------------

In stocks, float ≈ shares the public can trade. In derivatives, there are no “shares,” so Open Interest acts as the live stock of active contracts. It’s the best proxy for “what’s available in play” because it counts open positions that persist across bars. Using Volume ÷ OI mirrors stock float-turnover logic: how fast the tradable base is being recycled each period.

Why Normalize by Price

----------------------

Derivatives volume and OI may be reported in contracts, not notional value. One contract’s economic weight changes with price (especially on inverse contracts). Dividing both Volume and OI by Close:

- Puts them on a comparable notional footing.

- Prevents false spikes purely from price moves.

- Makes Turnover comparable across time even as price trends.

Advanced Tips

-------------

- Calibrate threshold: Start from the 80th–90th percentile of the last 60–90 bars of Turnover; set the threshold a touch below that to surface early heat.

- Add OI-delta: Layer an OI change histogram (current − prior) to separate new positioning from pure churn.

- Linear vs inverse: For linear (USDT-margined) contracts, the normalization still works and keeps visuals consistent; for inverse, it’s essential.

Limitations

-----------

- Data availability: Works only if your symbol exposes an _OI feed on TradingView; otherwise it errors out.

- Exchange conventions: Volume units differ by venue (contracts, coin, notional). Normalization mitigates, but cross-symbol comparisons still need caution.

- Intrabar gaps: OI is typically end-of-bar; rapid intrabar shifts won’t appear until the bar closes.

Notes

-----

- Designed primarily for crypto derivatives. For non-crypto, the script blanks OI to avoid misleading plots and uses a daily TF when needed.

Credit

------

- Concept & data: Built for TradingView data feeds.

- Acknowledgment: Credit to TradingView default indicator as requested.

- Source: This write-up reflects the logic present in your uploaded script.

Disclaimer

----------

Markets move; indicators simplify. Use with position sizing, hard stops, and catalyst awareness. The Turnover Rate flags activity, not direction.

Custom Strategy Builder [CLAMENZA] i changed this indicator to make the market session lines thicker and font bigger as well.

Gimme!Gimme! make yo profit go Boom ! . Got trand wo, got singal wo but, need to learn wo. Small step we go mind set before compound for sure. Gimme Gimme Gimme Gimme ya ya tata.

TEWMA Supertrend - [JTCAPITAL]TEWMA Supertrend is a modified way to use Triple Exponential Weighted Moving Average inside Supertrend logic for Trend-Following

The indicator works by calculating in the following steps:

1. Calculate the Triple Exponential Moving Average with Weighted Moving Average as input.

2. Calculate the ATR over the Supertrend Length

3. Use the Triple Exponential Weighted Moving Average, and add the multiplier times the ATR for the upper limit, and subtract the multiplier times the ATR for the lower limit.

4. Define Buy and Sell conditions based on the price closing above or below the upper and lower limits.

--Buy and sell conditions--

- The buy and sell conditions are defined by the price going above/below the upper and lower limits, calculated by (TEWMA +/- multi * ATR).

- When this goes on the opposite direction of the current trend, the trend changes. If this goes in the same direction of the current trend, the line follows the price by moving up.

- When price gets closer to the limits the limits do not change. The upper limit only moves when the upper decreases, and the lower limit only moves when the lower increases.

- The ATR gets subtracted from the lows or added onto the highs to eliminate false signals in choppy markets, while enforcing fast entries and exits.

--Features and Parameters--

- Allows the usage of different sources

- Allows the changing of the length of the ATR

- Allows the changing of the length of the TEWMA

- Allows the changing of the multiplier to increase or decrease ATR usage

--Details--

This script is using TEWMA as input for the modified Supertrend. Using a TEWMA and getting a higher multiplier to the ATR is meant to decrease false signals. Which can be a problem when using a normal Supertrend. Using the TEWMA also ensures fast entries and exits from fast market moves after a calm period. Ensuring you don't stay left behind.

Be aware that lowering the multiplier for the ATR will allow for faster entries and exits but also allow for more false signals. It is recommended to change the parameters to fit your liking and to adjust to the timeframe you are working on.

Enjoy!

Weekly Fibonacci Pivot Levelsthis indicator in simple ways, draw the weekly fibo zones based on calculations

weekly zones are drawn automatically based on previous week, and are updated once a new week is opened

you can use it the way you like or adapt to your trading strategy

i really use it at extremes and when a divergence is occurring in these zones

Euler-Lagrange Bands [AGP] Ver.1.0Euler-Lagrange Bands : A Modern Approach to Volatility and Trend Analysis

indicator is an innovative technical analysis tool that uses a Kalman Filter to create dynamic and price-sensitive volatility bands. Unlike traditional Bollinger Bands or Keltner Channels, which rely on moving averages, this approach applies advanced engineering and mathematical principles to intelligently smooth price data. This reduces market noise and provides a clearer view of an asset's boundaries and its fair value.

Key Features

Dynamic and Smoothed Bands: The upper and lower bands adapt in real time to market volatility, offering a fluid and precise channel for identifying overbought and oversold zones.

"Fair Value" Midpoint: The indicator calculates and displays a midpoint that serves as a "fair value" reference. This is crucial for assessing whether the current price is over- or undervalued.

Multidimensional Analysis: It integrates with RSI and volume analysis to provide a comprehensive market view. The floating RSI and volume labels change color, offering quick and effective visual alerts.

Clear Visual Signals: The indicator draws shapes on the chart to mark band crosses, potential reversals, and trend confirmations. Additionally, the candlestick color changes to indicate whether the price is above or below the midpoint.

Real-Time Information Panel: A table in the top corner displays the exact values of the bands and the midpoint, giving you all the crucial information at a glance without cluttering the chart. The table's cell colors also change to alert you to price crosses.

Logic and Adjustments

The elb_process_noise and elb_measurement_noise values are fixed in this code to optimize band performance.

The only parameter the user can change from the indicator's settings in TradingView is length_periods, which allows for adjusting the bands' lookback period without altering the algorithm's sophisticated filtering logic.

The default values have been selected to provide an optimal balance between the indicator's stability and responsiveness, aiming to avoid false signals and ensure accurate market tracking.

How to Use It

This indicator is ideal for traders looking for a more sophisticated alternative to conventional volatility bands. It can be used to:

Identify an asset's price range.

Detect potential reversals when the price reaches or crosses the bands.

Confirm trend strength with volume and RSI analysis.

Make decisions based on the price's relationship to its "Fair Value."

Disclaimer

WARNING: This indicator is provided for educational and technical analysis purposes only. It does not constitute, and should not be interpreted as, financial advice. The buying and selling of financial instruments involve significant risk, and losses may exceed deposits. The past performance of any indicator or strategy is not a guarantee of future results. Users must conduct their own research, exercise due diligence, and consider their personal financial situation before making any investment decisions. The code's creator is not responsible for any losses or damages that may arise from the use of this indicator.

TCI Key Institutional Levels v2.0This script is a modified version of the Smart Money Concepts (SMC) framework originally published by LuxAlgo here: Smart Money Concepts – LuxAlgo

.

All credit and ownership of the original code goes to LuxAlgo.

Original indicator Credits:

The purpose of this publication is not to copy-paste the LuxAlgo indicator, but to present a modified version adapted in line with the concepts taught by Trading Cafe India (TCI).

These modifications include adjustments and refinements to better reflect the methodology followed by TCI, while still acknowledging the foundation laid by LuxAlgo.

⚠️ Important Notes:

This script is not an official LuxAlgo product.

This script is not an official TCI product.

This pretty much aligns with the TCI theory.

It is an independent, educational adaptation created for users who wish to see SMC concepts in the context of TCI-style modifications.

The modifications are original contributions and the script has been republished with the intention of providing additional learning value to the TradingView community.

By publishing this indicator, I fully respect and acknowledge the original author (LuxAlgo), while making clear that the changes applied are my own interpretation of SMC principles influenced by TCI’s teachings.

🔧 Key Functionalities & Modifications

Market Structure Labels

The standard Break of Structure (BOS) is now presented as Breaker, aligning with TCI’s interpretation.

The standard Change of Character (CHoCH) is now presented as Trap, reflecting how false moves and liquidity traps are often observed in Indian indices like Nifty & Bank Nifty.

Order Block & Liquidity Concepts

Retains core order block, supply-demand, and liquidity zone logic from the SMC framework.

Visuals and labels have been adjusted for easier interpretation by intraday traders in Indian markets.

Custom Adaptation for Indian Audience

Naming conventions and alerts have been optimized so beginners and experienced traders in India can relate to the terminology taught by TCI.

Chart annotations have been simplified to reduce clutter, making it more practical for real-time option trading and scalping strategies.

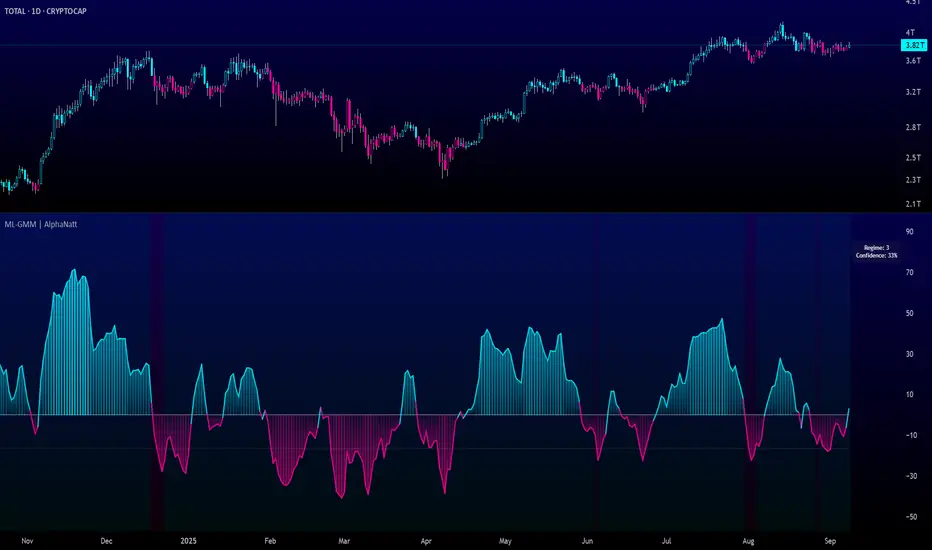

Machine Learning Gaussian Mixture Model | AlphaNattMachine Learning Gaussian Mixture Model | AlphaNatt

A revolutionary oscillator that uses Gaussian Mixture Models (GMM) with unsupervised machine learning to identify market regimes and automatically adapt momentum calculations - bringing statistical pattern recognition techniques to trading.

"Markets don't follow a single distribution - they're a mixture of different regimes. This oscillator identifies which regime we're in and adapts accordingly."

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🤖 THE MACHINE LEARNING

Gaussian Mixture Models (GMM):

Unlike K-means clustering which assigns hard boundaries, GMM uses probabilistic clustering :

Models data as coming from multiple Gaussian distributions

Each market regime is a different Gaussian component

Provides probability of belonging to each regime

More sophisticated than simple clustering

Expectation-Maximization Algorithm:

The indicator continuously learns and adapts using the E-M algorithm:

E-step: Calculate probability of current market belonging to each regime

M-step: Update regime parameters based on new data

Continuous learning without repainting

Adapts to changing market conditions

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🎯 THREE MARKET REGIMES

The GMM identifies three distinct market states:

Regime 1 - Low Volatility:

Quiet, ranging markets

Uses RSI-based momentum calculation

Reduces false signals in choppy conditions

Background: Pink tint

Regime 2 - Normal Market:

Standard trending conditions

Uses Rate of Change momentum

Balanced sensitivity

Background: Gray tint

Regime 3 - High Volatility:

Strong trends or volatility events

Uses Z-score based momentum

Captures extreme moves

Background: Cyan tint

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

💡 KEY INNOVATIONS

1. Probabilistic Regime Detection:

Instead of binary regime assignment, provides probabilities:

30% Regime 1, 60% Regime 2, 10% Regime 3

Smooth transitions between regimes

No sudden indicator jumps

2. Weighted Momentum Calculation:

Combines three different momentum formulas

Weights based on regime probabilities

Automatically adapts to market conditions

3. Confidence Indicator:

Shows how certain the model is (white line)

High confidence = strong regime identification

Low confidence = transitional market state

Line transparency changes with confidence

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

⚙️ PARAMETER OPTIMIZATION

Training Period (50-500):

50-100: Quick adaptation to recent conditions

100: Balanced (default)

200-500: Stable regime identification

Number of Components (2-5):

2: Simple bull/bear regimes

3: Low/Normal/High volatility (default)

4-5: More granular regime detection

Learning Rate (0.1-1.0):

0.1-0.3: Slow, stable learning

0.3: Balanced (default)

0.5-1.0: Fast adaptation

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📊 TRADING STRATEGIES

Visual Signals:

Cyan gradient: Bullish momentum

Magenta gradient: Bearish momentum

Background color: Current regime

Confidence line: Model certainty

1. Regime-Based Trading:

Regime 1 (pink): Expect mean reversion

Regime 2 (gray): Standard trend following

Regime 3 (cyan): Strong momentum trades

2. Confidence-Filtered Signals:

Only trade when confidence > 70%

High confidence = clearer market state

Avoid transitions (low confidence)

3. Adaptive Position Sizing:

Regime 1: Smaller positions (choppy)

Regime 2: Normal positions

Regime 3: Larger positions (trending)

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🚀 ADVANTAGES OVER OTHER ML INDICATORS

vs K-Means Clustering:

Soft clustering (probabilities) vs hard boundaries

Captures uncertainty and transitions

More mathematically robust

vs KNN (K-Nearest Neighbors):

Unsupervised learning (no historical labels needed)

Continuous adaptation

Lower computational complexity

vs Neural Networks:

Interpretable (know what each regime means)

No overfitting issues

Works with limited data

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📈 PERFORMANCE CHARACTERISTICS

Best Market Conditions:

Markets with clear regime shifts

Volatile to trending transitions

Multi-timeframe analysis

Cryptocurrency markets (high regime variation)

Key Strengths:

Automatically adapts to market changes

No manual parameter adjustment needed

Smooth transitions between regimes

Probabilistic confidence measure

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🔬 TECHNICAL BACKGROUND

Gaussian Mixture Models are used extensively in:

Speech recognition (Google Assistant)

Computer vision (facial recognition)

Astronomy (galaxy classification)

Genomics (gene expression analysis)

Finance (risk modeling at investment banks)

The E-M algorithm was developed at Stanford in 1977 and is one of the most important algorithms in unsupervised machine learning.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

💡 PRO TIPS

Watch regime transitions: Best opportunities often occur when regimes change

Combine with volume: High volume + regime change = strong signal

Use confidence filter: Avoid low confidence periods

Multi-timeframe: Compare regimes across timeframes

Adjust position size: Scale based on identified regime

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

⚠️ IMPORTANT NOTES

Machine learning adapts but doesn't predict the future

Best used with other confirmation indicators

Allow time for model to learn (100+ bars)

Not financial advice - educational purposes

Backtest thoroughly on your instruments

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🏆 CONCLUSION

The GMM Momentum Oscillator brings institutional-grade machine learning to retail trading. By identifying market regimes probabilistically and adapting momentum calculations accordingly, it provides:

Automatic adaptation to market conditions

Clear regime identification with confidence levels

Smooth, professional signal generation

True unsupervised machine learning

This isn't just another indicator with "ML" in the name - it's a genuine implementation of Gaussian Mixture Models with the Expectation-Maximization algorithm, the same technology used in:

Google's speech recognition

Tesla's computer vision

NASA's data analysis

Wall Street risk models

"Let the machine learn the market regimes. Trade with statistical confidence."

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

Developed by AlphaNatt | Machine Learning Trading Systems

Version: 1.0

Algorithm: Gaussian Mixture Model with E-M

Classification: Unsupervised Learning Oscillator

Not financial advice. Always DYOR.

AI-Weighted RSI (Zeiierman)█ Overview

AI-Weighted RSI (Zeiierman) is an adaptive oscillator that enhances classic RSI by applying a correlation-weighted prediction layer. Instead of looking only at RSI values directly, this indicator continuously evaluates how other price- and volume-based features (returns, volatility, volume shifts) correlate with RSI, and then weights them accordingly to project the next RSI state.

The result is a smoother, forward-looking RSI framework that adapts to market conditions in real time.

By leveraging feature correlation instead of static formulas, AI-Weighted RSI behaves like a lightweight learning model, adjusting its emphasis depending on which features are most aligned with RSI behavior during the current regime.

█ How It Works

⚪ Feature Extraction

Each bar, the script computes features: log returns, RSI itself, ATR% (volatility), volume, and volume log-change.

⚪ Correlation Screening

Over a rolling learning window, it measures the correlation of each feature against RSI. The strongest relationships are ranked and selected.

⚪ Adaptive Weighting

Features are standardized (z-scored), then combined using their signed correlations as weights, building a rolling, adaptive prediction of RSI.

⚪ Prediction to RSI Weight

The predicted RSI is mapped back into a “weight” scale (±2 by default). Above 0 = bullish bias, below 0 = bearish bias, with color-graded fills to visualize overbought/oversold pressure.

⚪ Signal Line

A smoothing option (signal length) overlays a moving average of the AI-Weighted RSI for clearer trend confirmation.

█ Why AI-Weighted RSI

⚪ Adaptive to Market Regime

Because the model re-evaluates correlations continuously, it naturally shifts which features dominate, sometimes volatility explains RSI best, sometimes volume, sometimes returns.

⚪ Forward-Looking Bias

Instead of simply reflecting RSI, the model provides a projection, helping anticipate shifts in momentum before RSI itself flips.

█ How to Use

⚪ Directional Bias

Read the RSI relative to 0. Above = bullish momentum bias, below = bearish.

⚪ Overbought / Oversold Zones

Shaded fills beyond +0.5 or -0.5 highlight extremes where RSI pressure often exhausts.

⚪ Divergences

When price makes new highs/lows but AI-Weighted RSI fails to confirm, it often signals weakening momentum.

█ Settings

RSI Length: Lookback for the core RSI calculation.

Signal Length: Smoothing applied to the AI-Weighted RSI output.

Learning Window: Bars used for correlation learning and z-scoring.

-----------------

Disclaimer

The content provided in my scripts, indicators, ideas, algorithms, and systems is for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or a solicitation to buy or sell any financial instruments. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

Deadband Hysteresis Supertrend [BackQuant]Deadband Hysteresis Supertrend

A two-stage trend tool that first filters price with a deadband baseline, then runs a Supertrend around that baseline with optional flip hysteresis and ATR-based adverse exits.

What this is

A hybrid of two ideas:

Deadband Hysteresis Baseline that only advances when price pulls far enough from the baseline to matter. This suppresses micro noise and gives you a stable centerline.

Supertrend bands wrapped around that baseline instead of raw price. Flips are further gated by an extra margin so side changes are more deliberate.

The goal is fewer whipsaws in chop and clearer regime identification during trends.

How it works (high level)

Deadband step — compute a per-bar “deadband” size from one of four modes: ATR, Percent of price, Ticks, or Points. If price deviates from the baseline by more than this amount, move the baseline forward by a fraction of the excess. If not, hold the line.

Centered Supertrend — build upper and lower bands around the baseline using ATR and a user factor. Track the usual trailing logic that tightens a band while price moves in its favor.

Flip hysteresis — require price to exceed the active band by an extra flip offset × ATR before switching sides. This adds stickiness at the boundary.

Adverse exit — once a side is taken, trigger an exit if price moves against the entry by K × ATR .

If you would like to check out the filter by itself:

What it plots

DBHF baseline (optional) as a smooth centerline.

DBHF Supertrend as the active trailing band.

Candle coloring by trend side for quick read.

Signal markers 𝕃 and 𝕊 at flips plus ✖ on adverse exits.

Inputs that matter

Price Source — series being filtered. Close is typical. HL2 or HLC3 can be steadier.

Deadband mode — ATR, Percent, Ticks, or Points. This defines the “it’s big enough to matter” zone.

ATR Length / Mult (DBHF) — only used when mode = ATR. Larger values widen the do-nothing zone.

Percent / Ticks / Points — alternatives to ATR; pick what fits your market’s convention.

Enter Mult — scales the deadband you must clear before the baseline moves. Increase to filter more noise.

Response — fraction of the excess applied to baseline movement. Higher responds faster; lower is smoother.

Supertrend ATR Period & Factor — traditional band size controls; higher factor widens and flips less often.

Flip Offset ATR — extra ATR buffer required to flip. Useful in choppy regimes.

Adverse Stop K·ATR — per-trade danger brake that forces an exit if price moves K×ATR against entry.

UI — toggle baseline, supertrend, signals, and bar painting; choose long and short colors.

How to read it

Green regime — candles painted long and the Supertrend running below price. Pullbacks toward the baseline that fail to breach the opposite band often resume higher.

Red regime — candles painted short and the Supertrend running above price. Rallies that cannot reclaim the band may roll over.

Frequent side swaps — reduce sensitivity by increasing Enter Mult, using ATR mode, raising the Supertrend factor, or adding Flip Offset ATR.

Use cases

Bias filter — allow entries only in the direction of the current side. Use your preferred triggers inside that bias.

Trailing logic — treat the active band as a dynamic stop. If the side flips or an adverse K·ATR exit prints, reduce or close exposure.

Regime map — on higher timeframes, the combination baseline + band produces a clean up vs down template for allocation decisions.

Tuning guidance

Fast markets — ATR deadband, modest Enter Mult (0.8–1.2), response 0.2–0.35, Supertrend factor 1.7–2.2, small Flip Offset (0.2–0.5 ATR).

Choppy ranges — widen deadband or raise Enter Mult, lower response, and add more Flip Offset so flips require stronger evidence.

Slow trends — longer ATR periods and higher Supertrend factor to keep you on side longer; use a conservative adverse K.

Included alerts

DBHF ST Long — side flips to long.

DBHF ST Short — side flips to short.

Adverse Exit Long / Short — K·ATR stop triggers against the current side.

Strengths

Deadbanded baseline reduces micro whipsaws before Supertrend logic even begins.

Flip hysteresis adds a second layer of confirmation at the boundary.

Optional adverse ATR stop provides a uniform risk cut across assets and regimes.

Clear visuals and minimal parameters to adjust for symbol behavior.

Putting it together

Think of this tool as two decisions layered into one view. The deadband baseline answers “does this move even count,” then the Supertrend wrapped around that baseline answers “if it counts, which side should I be on and where do I flip.” When both parts agree you tend to stay on the correct side of a trend for longer, and when they disagree you get an early warning that conditions are changing.

When the baseline bends and price cannot reclaim the opposite band , momentum is usually continuing. Pullbacks into the baseline that stall before the far band often resolve in trend.

When the baseline flattens and the bands compress , expect indecision. Use the Flip Offset ATR to avoid reacting to the first feint. Wait for a clean band breach with follow through.

When an adverse K·ATR exit prints while the side has not flipped , treat it as a risk event rather than a full regime change. Many users cut size, re-enter only if the side reasserts, and let the next flip confirm a new trend.

Final thoughts

Deadband Hysteresis Supertrend is best read as a regime lens. The baseline defines your tolerance for noise, the bands define your trailing structure, and the flip offset plus adverse ATR stop define how forgiving or strict you want to be at the boundary. On strong trends it helps you hold through shallow shakeouts. In choppy conditions it encourages patience until price does something meaningful. Start with settings that reflect the cadence of your market, observe how often flips occur, then nudge the deadband and flip offset until the tool spends most of its time describing the move you care about rather than the noise in between.

KeyLevel - AOCKeyLevel - AOC

✨ Features📈 Session Levels: Tracks high, low, and open prices for Asian, London, and New York sessions.📅 Multi-Timeframe Levels: Plots previous day, week, month, quarter, and yearly open/high/low levels.⚙️ Preset Modes: Choose Scalp, Intraday, or Swing presets for tailored level displays.🎨 Customizable Visuals: Adjust colors, line styles, and label abbreviations for clarity.🖼️ Legend Table: Displays a color-coded legend for quick reference to session and period levels.🔧 Flexible Settings: Enable/disable specific sessions or levels and customize UTC offsets.

🛠️ How to Use

Add to Chart: Apply the "KeyLevel - AOC" indicator on TradingView.

Configure Inputs:

Preset: Select Scalp, Intraday, or Swing, or use custom settings.

Session Levels: Toggle Asian, London, NY sessions and their open/high/low lines.

Period Levels: Enable/disable previous day, week, month, quarter, or yearly levels.

Visuals: Adjust colors, line widths, and label abbreviations.

Legend: Show/hide the legend table for level identification.

Analyze: Monitor key levels for support/resistance and session-based price action.

Track Trends: Use levels to identify breakouts, reversals, or consolidation zones.

🎯 Why Use It?

Dynamic Levels: Tracks critical price levels across multiple timeframes for comprehensive analysis.

Session Focus: Highlights key session price points for intraday trading strategies.

Customizable: Tailor displayed levels and visuals to match your trading style.

User-Friendly: Clear lines, labels, and legend table simplify price level tracking.

📝 Notes

Ensure timeframe compatibility (e.g., avoid daily charts for session levels).

Use M5 or higher timeframes for accurate session tracking; some levels disabled on M5.

Combine with indicators like RSI or MACD for enhanced trading signals.

Adjust UTC offset if session times misalign with your broker’s timezone.

Volatility Cone Forecaster Lite [PhenLabs]📊 Volatility Cone Forecaster

Version: PineScript™v6

📌Description

The Volatility Cone Forecaster (VCF) is an advanced indicator designed to provide traders with a forward-looking perspective on market volatility. Instead of merely measuring past price fluctuations, the VCF analyzes historical volatility data to project a statistical “cone” that outlines a probable range for future price movements. Its core purpose is to contextualize the current market environment, helping traders to anticipate potential shifts from low to high volatility periods (and vice versa). By identifying whether volatility is expanding or contracting relative to historical norms, it solves the critical problem of preparing for significant market moves before they happen, offering a clear statistical edge in strategy development.

This indicator moves beyond lagging measures by employing percentile analysis to rank the current volatility state. This allows traders to understand not just what volatility is, but how significant it is compared to the recent past. The VCF is built for discretionary traders, system developers, and options strategists who need a sophisticated understanding of market dynamics to manage risk and identify high-probability opportunities.

🚀Points of Innovation

Forward-Looking Volatility Projection: Unlike standard indicators that only show historical data, the VCF projects a statistical cone of future volatility.

Percentile-Based Regime Analysis: Ranks current volatility against historical data (e.g., 90th, 75th percentiles) to provide objective context.

Automated Regime Detection: Automatically identifies and labels the market as being in a ‘High’, ‘Low’, or ‘Normal’ volatility regime.

Expansion & Contraction Signals: Clearly indicates whether volatility is currently increasing or decreasing, signaling shifts in market energy.

Integrated ATR Comparison: Plots an ATR-equivalent volatility measure to offer a familiar point of reference against the statistical model.

Dynamic Visual Modeling: The cone visualization directly on the price chart provides an intuitive guide for future expected price ranges.

🔧Core Components

Realized Volatility Engine: Calculates historical volatility using log returns over multiple user-defined lookback periods (short, medium, long) for a comprehensive view.

Percentile Analysis Module: A custom function calculates the 10th, 25th, 50th, 75th, and 90th percentiles of volatility over a long-term lookback (e.g., 252 days).

Forward Projection Calculator: Uses the calculated volatility percentiles to mathematically derive and draw the upper and lower bounds of the future volatility cone.

Volatility Regime Classifier: A logic-based system that compares current volatility to the historical percentile bands to classify the market state.

🔥Key Features

Customizable Lookback Periods: Adjust short, medium, and long-term lookbacks to fine-tune the indicator’s sensitivity to different market cycles.

Configurable Forward Projection: Set the number of days for the forward cone projection to align with your specific trading horizon.

Interactive Display Options: Toggle visibility for percentile labels, ATR levels, and regime coloring to customize the chart display.

Data-Rich Information Table: A clean, on-screen table displays all key metrics, including current volatility, percentile rank, regime, and trend.

Built-in Alert Conditions: Set alerts for critical events like volatility crossing the 90th percentile, dropping below the 10th, or switching between expansion and contraction.

🎨Visualization

Volatility Cone: Shaded bands projected onto the future price axis, representing the probable price range at different statistical confidence levels (e.g., 75th-90th percentile).

Color-Coded Volatility Line: The primary volatility plot dynamically changes color (e.g., red for high, green for low) to reflect the current volatility regime, providing instant context.

Historical Percentile Bands: Horizontal lines plotted across the indicator pane mark the key percentile levels, showing how current volatility compares to the past.

On-Chart Labels: Clear labels automatically display the current volatility reading, its percentile rank, the detected regime, and trend (Expanding/Contracting).

📖Usage Guidelines

Setting Categories

Short-term Lookback: Default: 10, Range: 5-50. Controls the most sensitive volatility calculation.

Medium-term Lookback: Default: 21, Range: 10-100. The primary input for the current volatility reading.

Long-term Lookback: Default: 63, Range: 30-252. Provides a baseline for long-term market character.

Percentile Lookback Period: Default: 252, Range: 100-1000. Defines the period for historical ranking; 252 represents one trading year.

Forward Projection Days: Default: 21, Range: 5-63. Determines how many bars into the future the cone is projected.

✅Best Use Cases

Breakout Trading: Identify periods of deep consolidation when volatility falls to low percentile ranks (e.g., below 25th) and begins to expand, signaling a potential breakout.

Mean Reversion Strategies: Target trades when volatility reaches extreme high percentile ranks (e.g., above 90th), as these periods are often unsustainable and lead to contraction.

Options Strategy: Use the cone’s projected upper and lower bounds to help select strike prices for strategies like iron condors or straddles.

Risk Management: Widen stop-losses and reduce position sizes when the indicator signals a transition into a ‘High’ volatility regime.

⚠️Limitations

Probabilistic, Not Predictive: The cone represents a statistical probability, not a guarantee of future price action. Extreme, unpredictable news events can drive prices outside the cone.

Lagging by Nature: All calculations are based on historical price data, meaning the indicator will always react to, not pre-empt, market changes.

Non-Directional: The indicator forecasts the *magnitude* of future moves, not the *direction*. It should be paired with a directional analysis tool.

💡What Makes This Unique

Forward Projection: Its primary distinction is projecting a data-driven, statistical forecast of future volatility, which standard oscillators do not do.

Contextual Analysis: It doesn’t just provide a number; it tells you what that number means through percentile ranking and automated regime classification.

🔬How It Works

1. Data Calculation:

The indicator first calculates the logarithmic returns of the asset’s price. It then computes the annualized standard deviation of these returns over short, medium, and long-term lookback periods to generate realized volatility readings.

2. Percentile Ranking:

Using a 252-day lookback, it analyzes the history of the medium-term volatility and determines the values that correspond to the 10th, 25th, 50th, 75th, and 90th percentiles. This builds a statistical map of the asset’s volatility behavior.

3. Cone Projection:

Finally, it takes these historical percentile values and projects them forward in time, calculating the potential upper and lower price bounds based on what would happen if volatility were to run at those levels over the next 21 days.

💡Note:

The Volatility Cone Forecaster is most effective on daily and weekly charts where statistical volatility models are more reliable. For lower timeframes, consider shortening the lookback periods. Always use this indicator as part of a comprehensive trading plan that includes other forms of analysis.

Supertrend Channel Histogram OscillatorThis histogram is based on the script "Supertrend Channels "

The idea of the indicator is to visually represent the interaction of price with several different supertrend channels of various lengths in an oscillator in order to make it much more clear to the trader how the longer trends are interacting with shorter trends of the price movement of an asset. I got this idea from the "Kurutoga Cloud" and "Kurutoga Histogram" by D7R which is based on the centerlines of 3 Donchian Channels, however after I started using the Supertrend Channel by LuxAlgo I found that it was a more reliable price range channel than a standard Donchian Channel and I made this indicator to accompany it.

This indicator plots a positive value above 0 when the price is above the centerline of the supertrend channel and a negative value below 0 when the price is below the centerline.

The first supertrend's length and multiple can be adjusted in the settings.

The given supertrend input is then doubled and quadrupled in both length and multiplication so that a supertrend histogram with the values of 3, 3 will be accompanied by 2 additional supertrend histograms with the values of 6, 6 and 12, 12.

The larger price trend histograms are clearly visible behind the short term supertrend channel's histogram, giving traders a balanced view of short and long term trends interacting. The less visible columns of the larger trend remain above or below the 0 line behind the more visible short term channel trend, helping to spot pullbacks within a larger trend.

Additionally, when the 3 separate histograms are all positive or all negative but the histogram columns are separating from each other this can indicate a potential trend exhaustion leading to reversal or pullback about to happen.

The overbought and oversold lines at 50 and -50 are representative primarily of the short term trend with above 50 or below -50 indicating that the price is pushing the boundary and potentially beginning a new short term supertrend in the opposite direction. If values do not noticably exceed these levels, then the current short term trend movement can be viewed as a pullback within a larger trend, with continuation potentially to follow.

I have had troubles converting the original code to v6 so this will be published here in v5 of pinescript to be used in conjunction with the original. I was intending to create a companion indicator for this oscillator that represents 3 supertrends with corresponding 2x and 4x calculations based on LuxAlgo's script, but I can't seem to get it to work correctly in v5.

For best visualization of the trends 3 LuxAlgo Supertrend channels with 2x and 4x values should be used in conjunction with each other to fully visualize the histogram.

Used in conjunction with other indicators this can be a very effective strategy to capture larger trend moves and pullbacks within trends, as well as warn of potential price trend exhaustion.