McClellan Oscillator for DAX (GER30) [aftabmk modified]About McClellan Oscillator

Developed by Sherman and Marian McClellan, the McClellan Oscillator is a breadth indicator derived from Net Advances, the number of advancing issues less the number of declining issues. Subtracting the 39-day exponential moving average of Net Advances from the 19-day exponential moving average of Net Advances forms the oscillator.

As the formula reveals, the McClellan Oscillator is a momentum indicator that works similar to MACD .

McClellan Oscillator signals can be generated with breadth thrusts, centerline crossovers, overall levels and divergences.

About my version

This version here is a modification, though:

- It can only be used on the DAX index (DAX 30 or GER 30)

- It only considers the DAX 30 stocks

- The data window will provide a summary about rising and declining stocks

- The data window will output the last change for each of the 30 stocks

BUG

I am only publishing this version because I am not sure if my current version is saved when I leave tradingview.com without publishing the script.

This version still contains a bug - the if/else clauses do not correctly recognize declining stocks. So the oscillator should not be used as it is.

Working on it these days. Feel free to provide feedback!

Stuff I am working on

- Coloring the area green/red according to the value

- Fixing this bug/making this script more efficient

DISCLAIMER

This script was mainly written for educational purposes (training myself how to write custom indicatotors).

As you can see, the code is really messy.

Credits

Based on the simple version of aftabmk

You can find the original version by searching for McClellan Oscillator for nifty 50.

Search in scripts for "收集一只股票30个交易日的成交量、开盘价、最高价和最低价和收盘价"

Gann RetracementThe indicator is based on W. D. Gann's method of retracement studies. Gann looked at stock retracement action in terms of Halves (1/2), Thirds (1/3, 2/3), Fifths (1/5, 2/5, 3/5, and 4/5) and more importantly the Eighths (1/8, 2/8, 3/8, 4/8, 5/8, 6/8, and 7/8). Needless to say, {2, 3, 5, 8} are the only Fibonacci numbers between 1 to 10. These ratios can easily be visualized in the form of division of a Circle as follows :

Divide the circle in 12 equal parts of 30 degree each to produce the Thirds :

30 x 4 = 120 is 1/3 of 360

30 x 8 = 240 is 2/3 of 360

The 30 degree retracement captures fundamental geometric shapes like a regular Triangle (120-240-360), a Square (90-180-270-360), and a regular Hexagon (60-120-180-240-300-360) inscribed inside of the circle.

Now, divide the circle in 10 equal parts of 36 degree each to produce the Fifths :

36 x 2 = 72 is 1/5 of 360

36 x 4 = 144 is 2/5 of 360

36 x 6 = 216 is 3/5 of 360

36 x 8 = 288 is 4/5 of 360

where, (72-144-216-288-360) is a regular Pentagon.

Finally, divide the circle in 8 equal parts of 45 degree each to produce the Eighths :

45 x 1 = 45 is 1/8 of 360

45 x 2 = 90 is 2/8 of 360

45 x 3 = 135 is 3/8 of 360

45 x 4 = 180 is 4/8 of 360

45 x 5 = 225 is 5/8 of 360

45 x 6 = 270 is 6/8 of 360

45 x 7 = 315 is 7/8 of 360

where, (45-90-135-180-225-270-315-360) is a regular Octagon.

How to Use this indicator ?

The indicator generates Gann retracement levels between any two significant price points, such as a high and a low.

Input :

Swing High (significant high price point, such as a top)

Swing Low (significant low price point, such as a bottom)

Degree (degree of retracement)

Output :

Gann retracement levels (color coded as follows) :

Swing High and Swing Low (BLUE)

50% retracement (ORANGE)

Retracements between Swing Low and 50% level (RED)

Retracements between 50% level and Swing High (LIME)

Bollinger Bands %B + ATR This indicator is best suitable for the 30-minutes interval OIL charts, due to ATR accuracy.

BB%B is great for showing oversold/overbought market conditions and offers excellent entry/exit opportunities for Day Trading (30 minutes chart), as well as reliable convergence/divergence patterns. ATR is conveniently combined and shows potential market volatility levels for the day when used in 30-minutes charts, thus demarcating your day trade exit point.

To use the ATR on this indicator: Just read the ATR value of the lowest (for a new bull trend) or the highest (for a new bear trend) candlestick of the newly formed trend leg. Let's suppose the ATR reads 0.2891, then you project a move of 2.891 points towards the given trend direction using the ruler tool (30-minutes charts). That's all, and there you have your take profit target!

Good Luck!!!

ADX strategy (considering ADX and +DI only )I have been checking the strategies on ADX indicator.

I have found that +DI crossing above ADX line under threshold 30 and exit on crossdown when ADX above 30 has better results than just following crossovers of +DI and -DI , ADX crossing above 30 .

BUY Rule

========

fast ema is above slow ema (default 13 and 55 , you can change these values in settings)

+DI cross above ADX well beloe threshold level (default 30)

Exit reule

========

when +DI cross down ADX , well above on threshold level

Stop Loss

=========

Default is set to 8%

Take a look and let me know how your symbol works with this strategy

Note : Bar color changes to yellow when the BUY condition is met.

Bar color and Background color shows to blue --- if Long position is active

fast ema and long ema doesnt print on the chart -- please add manually to the chart

Warning : for the use of educational purposes only

EulerMethod: DeltaEN

Shows the Integral Volume Delta (IVD)

It is a detailed OBV. Each bar sums up the volume for bars of a shorter timeframe.

For example, inside a 1M bar, every 12h bar is added up, and inside a 1h bar, every 1min bar is added. Thus, a conditional volume delta inside the bar is obtained.

The indicator for each bar shows the volume of purchases (positive), sales (negative) and the difference — IVD

The delta histogram is thicker than the volume histograms

Settings detalisation

M — 6 hours, 12 hours and 1 day for the M timeframe (720 by default)

W — 4 hours, 6 hours and 12 hours for the W timeframe (240 by default)

D — 30 minutes, 1 hour and 2 hours for the D timeframe (60 by default)

H — 1 minute, 5 minutes and 15 minutes for timeframes [1h, D) (default is 1)

For timeframes of 15m and less, the calculation is carried out by minute bars

VSA mode

The classic OBV adds volume to the cumulative sum under the condition Сlose (n) > Close (n-1) and subtracts it under the condition Close (n) < Close (n-1)

When VSA mode is disabled, all volumes are summed up under these conditions.

When the VSA approximation is turned on, the volume per bar of detail is divided by the factor (Close - Low) / (High - Low)

That is, it takes into account the spread per bar and closing relative to the spread. VSA is enabled by default

A/D mode

Shows the cumulative Accumulation / Distribution Index

The delta of the detail bar is multiplied by (High + Low + Close) / 3 bars, the result is added to the cumulative sum

No additional price conversions required due to integral summation

Index line view is customizable

EM Delta does not receive intermediate values in real time.

To see the result, wait until the bar closes or switch to a smaller timeframe

RU

Показывает Интегральную Дельту Объёма (ИДО)

Представляет собой детализированный OBV. В каждом баре суммируется объём за бары меньшего таймфрейма.

Например, внутри 1М-бара суммируется каждый 12h-бар, а внутри 1h — каждый 1m-бар. Таким образом получается условная дельта объёма внутри бара

Индикатор на каждый бар показывает объём покупок (положительный), объём продаж (отрицательный) и разницу — ИДО

Гистограмма дельты толще гистограмм объёмов

Настройки детализации внутри бара

M — 6 часов, 12 часов и 1 день для таймфрейма M (по-умолчанию 720)

W — 4 часа, 6 часов и 12 часов для таймфрейма W (по-умолчанию 240)

D — 30 минут, 1 час и 2 часа для таймфрейма D (по-умолчанию 60)

H — 1 минута, 5 минут и 15 минут для таймфреймов [1h, D) (по-умолчанию 1)

Для таймфреймов 15m и меньше расчёт ведётся по минутным барам

Режим VSA

Классический OBV прибавляет объём к кумулятивной сумме при условии Сlose(n) > Close(n-1) и отнимает при условии Close(n) < Close(n-1)

При отключении режима VSA все объёмы суммируются по этим условиям

При включённой VSA-аппроксимации объём за бар детализации делится по фактору (Close - Low) / (High - Low)

То есть учитывает спред за бар и закрытие относительно спреда. По-умолчанию режим VSA включен

Режим A/D

Показывает кумулятивный индекс Накопления/Распределения

Дельта бара детализации умножается на (High + Low + Close) / 3 бара, результат прибавляется к кумулятивной сумме

Дополнительные преобразования цены не требуются ввиду интегрального суммирования

Вид линии индекса настраивается

EM Delta не получает промежуточные значения в реальном времени.

Чтобы увидеть результат, дождитесь закрытия бара или перейдите на меньший таймфрейм

Crypto Trading Hours UTC based on Berlin time (UTC +2)Although crypto markets trade 24/7, there are spikes in volume according to the general hours at which different parts of the world do the majority of their trading.

This Script highlights the US, European and Asian markets when they are most active. The normal market hours are always from 08:00 to 16:30 local time.

US market opens at 8:00 Silicon Valley local time, and closes at 16:30 New York local time.

European market opens at 8:00 London local time, and closes at 16:30 Frankfurt local time.

Asian market opens at 8:00 Hong Kong local time, and closes at 16:30 Sydney local time.

Supertrend MTF LAG ISSUEThis script based on

we all use Super trend but it main issue is the lag as it buy too late or sell too late

using Deavaet study of Heat map MTF we can do a little trick

if you look on his study you can see that major signal for example will happen in the time frame before it happen at larger time frame

so in this example if signal at MTF 30 min and signal at MTF 60 min happen at the same time at 2 hours or 4 hours candles then this signal are more likely to be true then random signal at each time frame specific.

since we use shorter time frame on larger time frame we can remove the lag issue that make supertrend not so effective

In this example I set the signal to be MTF 30 +60 om 2 hour TF , can be good also for 4 hour candles..

So you get the signal to close inside the larger candle

now if you want to make on even shorter TF then change the code to 15 and 30 MTF on candles on 1 hour

or 1 and 5 min on 30 min or 15 min

Panchang Time//This indicator is required in NimblrTA and can be used to define timeslots for the trend confirmation

study("Panchang Time", overlay=true)

timeinrange(res, sess) => time(res, sess) != 0

premarket = #C0C0C0

regular = #0000FF

regularslot2 = #00CCFF

postmarket = #5000FF

notrading = na

sessioncolor = timeinrange("30", "0915-0930") ? premarket : timeinrange("30", "0915-0930") ? regular : timeinrange("30", "0931-1200") ? regularslot2 : timeinrange("30", "1201-1305") ? postmarket : notrading

bgcolor(sessioncolor, transp=90)

extended session - Regular Opening-Range- JayyOpening Range and some other scripts updated to plot correctly (see comments below.) There are three variations of the fibonacci expansion beyond the opening range and retracements within the opening range of the US Market session - I have not put in the script for the other markets yet.

The three scripts have different uses and strengths:

The extended session script (with the script here below) will plot the opening range whether you are using the extended session or the regular session. (that is to say whether "ext" in the lower right hand corner is highlighted or not.). While in the extended session the opening range has some plotting issues with periods like 13 minutes or any period that is not divisible into 330 mins with a round number outcome (eg 330/60 =5.5. Therefore an hour long opening range has problems in the extended session.

The pre session script is only for the premarket. You can select any opening range period you like. I have set the opening range to be the full premarket session. If you select a different session you will have to unselect "pre open to 9:30 EST for Opening Range?" in the format section. The script defaults to 15 minutes in the "period Of Pre Opening Range?". To go back to the 4 am to 9:30 pre opening range select "pre open to 9:30 EST for Opening Range?" there is no automatic 330 minute selection.

The past days offset script only works in 5 min or 15 minute period. It will show the opening range from up to 20 days past over the current days price action. Use this for the regular session only. 0 shows the current day's opening range. Use the positive integers for number of days back ie 1, 2, 3 etc not -1, -2, -3 etc. The script is preprogrammed to use the current day (0).

Scripts updated to plot correctly: One thing they all have in common is a way of they deal with a somewhat random problem that shifts the plots 4 hours in one direction or the other ie the plot started at 9:30 EST or 1:30PM EST. This issue started to occur approximately June 22, 2015 and impacts any script that tried to use "session" times to manage a plot in my scripts. The issue now seems to have been resolved during this past week.

Just in case the problem reoccurs I have added a "Switch session plot?" to each script. If the plot looks funny check or uncheck the "Switch session plot?" and see the difference. Of course if a new issue crops up it will likely require a different fix.

I have updated all of the scripts shown on this chart. If you are using a script of mine that suffers from the compiler issue then you will find an update on this chart. You can get any and all of the scripts by clicking on the small sideways wishbone on the left middle of the chart. You will see a dialogue box. Then click "make it mine". This will import all of the scripts to your computer and you can play around with them all to decide what you want and what you don't want. This is the easiest way to get all of the scripts in one fell swoop. It is also the easiest way for me to make all of the scripts available. I do not have all of the plots visible since it is too messy and one of the scripts (pre OR) is only for the regular session. To view the scripts click on the blue eye to the right of the script title to show it on this script. If you can only use the regular session. The scripts will all (with the exception of the pre OR) work fine.

If for any reason this script seems flakey refresh the page r try a slightly different period. I have noticed that sometimes randomly the script loves to return to the 5 min OR. This is a very new issue transient issue. As always if you see an issue please let me know.

Cheers Jayy

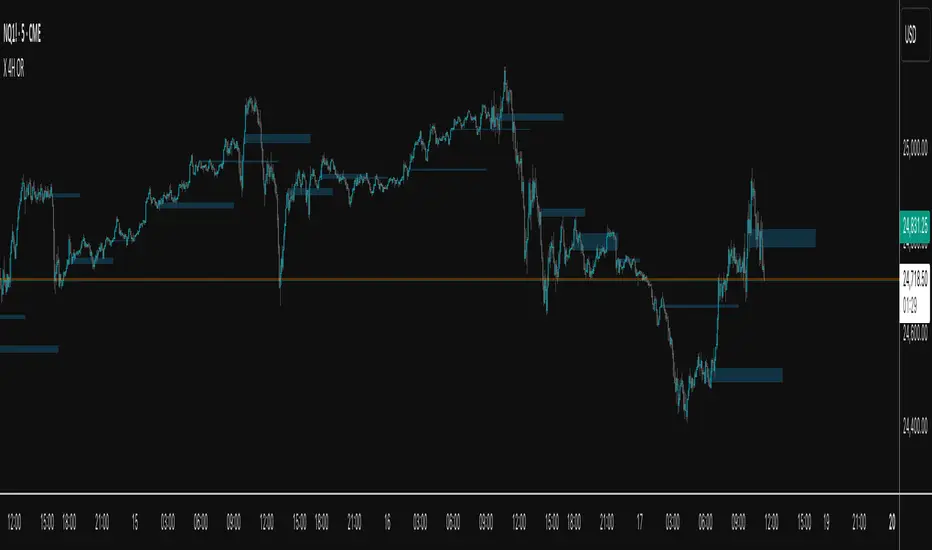

X 4H ORThis indicator plots the 30-second opening range (high/low) for six New-York–time anchors—2am, 6am, 10am, 2pm, 6pm, and 10pm—and extends each box to a fixed end time (e.g., 2am→9am, 6am→1pm, etc.). It samples true 30-second data regardless of the chart timeframe, so the captured highs/lows are precise.

What it does

Builds the first 30s OR for each selected anchor and draws a time-anchored box for that session.

Archives every day’s boxes (up to a cap) so you can study how price interacts with past ranges.

Adds per-anchor show toggles to display the latest box for that anchor.

Adds a global History toggle to show/hide all archived boxes without deleting them (clean view vs. context view).

Uses borderless, color-coded fills per anchor to avoid edge distortion while keeping levels easy to read.

Why it’s useful

Quickly spot session inflection zones where liquidity, breakouts, or reversals cluster.

Compare how current price trades relative to recent session ranges for bias and risk framing.

Perform lightweight post-session review/backtesting on OR breaks, retests, and range rotations.

Keep charts decluttered on demand (latest only), or flip on history for deeper context.

ORBs, EMAs, AVWAPThis Pine Script (version 6) is a multi-session trading indicator that combines Opening Range Breakouts (ORBs), Exponential Moving Averages (EMAs), and an Anchored VWAP (AVWAP) system — all in one overlay script for TradingView.

Here’s a clear breakdown of its structure and functionality:

🕒 1. Session Logic and ORB Calculation

Purpose: Identify and plot the high and low of the first 30 minutes (default) for the Tokyo, London, and New York trading sessions.

Session Anchors (NY time):

Tokyo → 20:00

London → 03:00

New York → 09:30

(All configurable in inputs.)

ORB Duration: Default is 30 minutes (orbDurationMin), also user-configurable.

Resets:

London and NY ORBs reset at the start of each new New York trading day (17:00 NY time).

Tokyo ORB resets independently using a stored timestamp.

Process:

For each session:

While the time is within the ORB window, the script captures the session’s high and low.

Once the window closes, those levels remain plotted until reset.

Plot Colors:

Tokyo → Yellow (#fecc02)

London → Gray (#8c9a9c)

New York → Magenta (#ff00c8)

These form visible horizontal lines marking the prior session ranges — useful for breakout or retest trading setups.

📈 2. EMA System

Purpose: Provide trend and dynamic support/resistance guidance.

It calculates and plots four EMAs:

EMA Period Color Purpose

EMA 9 Short-term Green Fast signal

EMA 20 Short-term Red Confirms direction

EMA 113 Medium Aqua Trend filter

EMA 200 Long-term Orange Macro trend baseline

Each EMA is plotted directly on the price chart for visual confluence with ORB and VWAP levels.

⚖️ 3. Anchored VWAP (AVWAP)

Purpose: Display a volume-weighted average price anchored to specific timeframes or events, optionally with dynamic deviation or percentage bands.

Features:

Anchor Options:

Time-based: Session, Week, Month, Quarter, Year, Decade, Century

Event-based: Earnings, Dividends, Splits

VWAP resets when the chosen anchor condition is met (e.g., new month, new earnings event, etc.).

Bands:

Up to three levels of symmetric upper/lower bands.

Choose between Standard Deviation or Percentage-based widths.

Display Toggles:

Each band’s visibility is optional.

VWAP can be hidden on 1D+ timeframes (hideonDWM option).

Color Scheme:

VWAP: Fuchsia (magenta-pink) line

Bands: Green / Olive / Teal with light-filled zones

⚙️ 4. Technical Highlights

Uses ta.vwap() with built-in band calculations.

Handles instruments with or without volume (errors if missing volume).

Uses time-zone aware timestamps (timestamp(NY_TZ, …)).

Uses timeframe.change() to detect new anchors for the VWAP.

Employs persistent variables (var) to maintain session state across bars.

💡 In Practice

This indicator is designed for multi-session intraday traders who:

Trade Tokyo, London, or NY open breakouts or retests.

Use EMA stacking and crossovers for trend confirmation.

Use Anchored VWAP as a fair-value or mean-reversion reference.

Need clear visual structure across different market sessions.

It provides strong session separation, trend context, and volume-weighted price reference — making it ideal for discretionary or semi-systematic trading strategies focused on liquidity zones and session momentum.

RSI VWAP v1 [JopAlgo]RSI VWAP v1.1 made stronger by volume-aware!

We know there's nothing new and the original RSI already does an excellent job. We're just working on small, practical improvements – here's our take: The same basic idea, clearer display, and a single, specially developed rolling line: a VWAP of the RSI that incorporates volume (participation) into the calculation.

Do you prefer the pure classic?

You can still use Wilder or Cutler engines –

but the star here is the VW-RSI + rolling line.

This RSI also offers the possibility of illustrating a possible

POC (Point of Control - or the HAL or VAL) level.

However, the indicator does NOT plot any of these levels itself.

We have included an illustration in the chart for this!

We hope this version makes your decision-making easier.

What you’ll see

The RSI line with a 50 midline and optional bands: either static 70/30 or adaptive μ±k·σ of the Rolling Line.

One smoothing concept only: the Rolling Line (light blue) = VWAP of RSI.

Shadow shading between RSI and the Rolling Line (green when RSI > line, red when RSI < line).

A lighter tint only on the parts of that shadow that sit above the upper band or below the lower band (quick overbought/oversold context).

Simple divergence lines drawn from RSI pivots (green for regular bullish, red for regular bearish). No labels, no buy/sell text—kept deliberately clean.

What’s new, and why it helps

VW-RSI engine (default):

RSI can be computed from volume-weighted up/down moves, so momentum reflects how much traded when price moved—not just the direction.

Rolling Line (VWAP of RSI) with pure VWAP adaptation:

Low volume: blends toward a faster VWAP so early, thin starts aren’t missed.

Volume spikes: blends toward a slower VWAP so a single heavy bar doesn’t whip the curve.

You can reveal the Base Rolling (pre-adaptation) line to see exactly how much adaptation is happening.

Adaptive bands (optional):

Instead of fixed 70/30, use mean ± k·stdev of the Rolling Line over a lookback. Levels breathe with the market—useful in strong trends where static bounds stay pinned.

Minimal, readable panel:

One smoothing, one story. The shadow tells you who’s in control; the lighter highlight shows stretch beyond your lines.

How to read it (fast)

Bias: RSI above 50 (and a rising Rolling Line) → bullish bias; below 50 → bearish bias.

Trigger: RSI crossing the Rolling Line with the bias (e.g., above 50 and crossing up).

Stretch: Near/above the upper band, avoid chasing; near/below the lower band, avoid panic—prefer a cross back through the line.

Divergence lines: Use as context, not as standalone signals. They often help you wait for the next cross or avoid late entries into exhaustion.

Settings that actually matter

RSI Engine: VW-RSI (default), Wilder, or Cutler.

Rolling Line Length: the VWAP length on RSI (higher = calmer, lower = earlier).

Adaptive behavior (pure VWAP):

Speed-up on Low Volume → blends toward fast VWAP (factor of your length).

Dampen Spikes (volume z-score) → blends toward slow VWAP.

Fast/Slow Factors → how far those fast/slow variants sit from the base length.

Bands: choose Static 70/30 or Adaptive μ±k·σ (set the lookback and k).

Visuals: show/hide Base Rolling (ref), main shadow, and highlight beyond bands.

Signal gating: optional “ignore first bars” per day/session if you dislike open noise.

Starter presets

Scalp (1–5m): RSI 9–12, Rolling 12–18, FastFactor ~0.5, SlowFactor ~2.0, Adaptive on.

Intraday (15m–1H): RSI 10–14, Rolling 18–26, Bands k = 1.0–1.4.

Swing (4H–1D): RSI 14–20, Rolling 26–40, Bands k = 1.2–1.8, Adaptive on.

Where it shines (and limits)

Best: liquid markets where volume structure matters (majors, indices, large caps).

Works elsewhere: even with imperfect volume, the shadow + bands remain useful.

Limits: very thin/illiquid assets reduce the benefit of volume-weighting—lengthen settings if needed.

Attribution & License

Based on the concept and baseline implementation of the “Relative Strength Index” by TradingView (Pine v6 built-in).

Released as Open-source (MPL-2.0). Please keep the license header and attribution intact.

Disclaimer

For educational purposes only; not financial advice. Markets carry risk. Test first, use clear levels, and manage risk. This project is independent and not affiliated with or endorsed by TradingView.

Fish OrbThis indicator marks and tracks the first 15-minute range of the New York session open (default 9:30–9:45 AM ET) — a critical volatility period for futures like NQ (Nasdaq).

It helps you visually anchor intraday price action to that initial opening range.

Core Functionality

1. Opening Range Calculation

It measures the High, Low, and Midpoint of the first 15 minutes after the NY market opens (default 09:30–09:45 ET).

You can change the window or timezone in the inputs.

2. Visual Overlays

During the 15-minute window:

A teal shaded box highlights the open range period.

Live white lines mark the current High and Low.

A red line marks the midpoint (mid-range).

These update in real-time as each bar forms.

3. Post-Window Behavior

When the 15-minute window ends:

The High, Low, and Midpoint are locked in.

The indicator draws persistent horizontal lines for those values.

4. Historical Days

You can keep today + a set number of previous days (configurable via “Previous Days to Keep”).

Older days automatically delete to keep charts clean.

5. Line Extension Control

Each day’s lines extend to the right after they form.

You can toggle “Stop Lines at Next NY Open”:

ON: Yesterday’s lines stop exactly at the next NY session open (09:30 ET).

OFF: Lines extend indefinitely across the chart.

MNQ TopStep 50K | Ultra Quality v3.0MNQ TopStep 50K | Ultra Quality v3.0 - Publish Summary

📊 Overview

A professional-grade trading indicator designed specifically for MNQ futures traders using TopStep funded accounts. Combines 7 technical confirmations with 5 advanced safety filters to deliver high-quality trade signals while managing drawdown risk.

🎯 Key Features

Core Signal System

7-Point Confirmation: VWAP, EMA crossovers, 15-min HTF trend, MACD, RSI, ADX, and Volume

Signal Grading: Each signal is rated A+ through D based on 7 quality factors

Quality Threshold: Adjustable minimum grade requirement (A+, A, B, C, D)

Advanced Safety Filters (Customizable)

Mean Reversion Filter - Prevents chasing extended moves beyond VWAP bands

ATR Spike Filter - Avoids trading during extreme volatility events

EMA Spacing Filter - Ensures proper trend separation (optional)

Momentum Filter - Requires consecutive directional bars (optional)

Multi-Timeframe Confirmation - Aligns with 15-min trend (optional)

TopStep Risk Management

Real-time drawdown tracking

Position sizing calculator based on remaining cushion

Daily loss limit monitoring

Consecutive loss protection

Max trades per day limiter

Visual Components

VWAP with 1σ, 2σ, 3σ bands

EMA 9/21 with cloud fill

15-min EMA 50 for HTF trend

Comprehensive metrics dashboard

Risk management panel

Filter status panel

Detailed trade labels with entry, stops, and targets

⚙️ Default Settings (Balanced for Regular Signals)

Technical Indicators

Fast EMA: 9 | Slow EMA: 21 | HTF EMA: 50 (15-min)

MACD: 10/22/9

RSI: 14 period | Thresholds: 52 (buy) / 48 (sell)

ADX: 14 period | Minimum: 20

ATR: 14 period | Stop: 2x | TP1: 2x | TP2: 3x

Volume: 1.2x average required

Session Settings

Default: 9:30 AM - 11:30 AM ET (adjustable)

Avoids first 15 minutes after market open

Customizable trading hours

Safety Filters (Default Configuration)

✅ Mean Reversion: Enabled (2.5σ max from VWAP)

✅ ATR Spike: Enabled (2.0x threshold)

❌ EMA Spacing: Disabled (can enable for quality)

❌ Momentum: Disabled (can enable for quality)

❌ MTF Confirmation: Disabled (can enable for quality)

Risk Controls

Minimum Signal Quality: C (adjustable to A+ for fewer/better signals)

Min Bars Between Signals: 10

Max Trades Per Day: 5

Stop After Consecutive Losses: 2

📈 Expected Performance

With Default Settings:

Signals per week: 10-15 trades

Estimated win rate: 55-60%

Risk-Reward: 1:2 (TP1) and 1:3 (TP2)

With Aggressive Settings (Min Quality = D, All Filters Off):

Signals per week: 20-25 trades

Estimated win rate: 50-55%

With Conservative Settings (Min Quality = A, All Filters On):

Signals per week: 3-5 trades

Estimated win rate: 65-70%

🚀 How to Use

Basic Setup:

Add indicator to MNQ 5-minute chart

Adjust TopStep account settings in inputs

Set your risk per trade percentage (default: 0.5%)

Configure trading session hours

Set minimum signal quality (Start with C for balanced results)

Signal Interpretation:

Green Triangle (BUY): Long signal - all confirmations aligned

Red Triangle (SELL): Short signal - all confirmations aligned

Label Details: Shows entry, stop loss, take profit levels, position size, and signal grade

Signal Grade: A+ = Elite (6-7 points) | A = Strong (5) | B = Good (4) | C = Fair (3)

Dashboard Monitoring:

Top Right: Technical metrics and market conditions

Top Left: Filter status (which filters are passing/blocking)

Bottom Right: TopStep risk metrics and position sizing

⚡ Customization Tips

For More Signals:

Lower "Minimum Signal Quality" to D

Decrease ADX threshold to 18-20

Lower RSI thresholds to 50/50

Reduce Volume multiplier to 1.1x

Disable additional filters

For Higher Quality (Fewer Signals):

Raise "Minimum Signal Quality" to A or A+

Increase ADX threshold to 25-30

Enable all 5 advanced filters

Tighten VWAP distance to 2.0σ

Increase momentum requirement to 3-4 bars

For TopStep Compliance:

Adjust "Max Total Drawdown" and "Daily Loss Limit" to match your account

Update "Already Used Drawdown" daily

Monitor the Risk Panel for cushion remaining

Use recommended contract sizing

🛡️ Risk Disclaimer

IMPORTANT: This indicator is for educational and informational purposes only.

Past performance does not guarantee future results

All trading involves substantial risk of loss

Use proper risk management and position sizing

Test thoroughly in paper trading before live use

The indicator does not guarantee profitable trades

Adjust settings based on your risk tolerance and trading style

Always comply with your broker's and TopStep's rules

MNQ TopStep 50K | Ultra Quality v3.0MNQ TopStep 50K | Ultra Quality v3.0 - Publish Summary📊 OverviewA professional-grade trading indicator designed specifically for MNQ futures traders using TopStep funded accounts. Combines 7 technical confirmations with 5 advanced safety filters to deliver high-quality trade signals while managing drawdown risk.🎯 Key FeaturesCore Signal System

7-Point Confirmation: VWAP, EMA crossovers, 15-min HTF trend, MACD, RSI, ADX, and Volume

Signal Grading: Each signal is rated A+ through D based on 7 quality factors

Quality Threshold: Adjustable minimum grade requirement (A+, A, B, C, D)

Advanced Safety Filters (Customizable)

Mean Reversion Filter - Prevents chasing extended moves beyond VWAP bands

ATR Spike Filter - Avoids trading during extreme volatility events

EMA Spacing Filter - Ensures proper trend separation (optional)

Momentum Filter - Requires consecutive directional bars (optional)

Multi-Timeframe Confirmation - Aligns with 15-min trend (optional)

TopStep Risk Management

Real-time drawdown tracking

Position sizing calculator based on remaining cushion

Daily loss limit monitoring

Consecutive loss protection

Max trades per day limiter

Visual Components

VWAP with 1σ, 2σ, 3σ bands

EMA 9/21 with cloud fill

15-min EMA 50 for HTF trend

Comprehensive metrics dashboard

Risk management panel

Filter status panel

Detailed trade labels with entry, stops, and targets

⚙️ Default Settings (Balanced for Regular Signals)Technical Indicators

Fast EMA: 9 | Slow EMA: 21 | HTF EMA: 50 (15-min)

MACD: 10/22/9

RSI: 14 period | Thresholds: 52 (buy) / 48 (sell)

ADX: 14 period | Minimum: 20

ATR: 14 period | Stop: 2x | TP1: 2x | TP2: 3x

Volume: 1.2x average required

Session Settings

Default: 9:30 AM - 11:30 AM ET (adjustable)

Avoids first 15 minutes after market open

Customizable trading hours

Safety Filters (Default Configuration)

✅ Mean Reversion: Enabled (2.5σ max from VWAP)

✅ ATR Spike: Enabled (2.0x threshold)

❌ EMA Spacing: Disabled (can enable for quality)

❌ Momentum: Disabled (can enable for quality)

❌ MTF Confirmation: Disabled (can enable for quality)

Risk Controls

Minimum Signal Quality: C (adjustable to A+ for fewer/better signals)

Min Bars Between Signals: 10

Max Trades Per Day: 5

Stop After Consecutive Losses: 2

📈 Expected PerformanceWith Default Settings:

Signals per week: 10-15 trades

Estimated win rate: 55-60%

Risk-Reward: 1:2 (TP1) and 1:3 (TP2)

With Aggressive Settings (Min Quality = D, All Filters Off):

Signals per week: 20-25 trades

Estimated win rate: 50-55%

With Conservative Settings (Min Quality = A, All Filters On):

Signals per week: 3-5 trades

Estimated win rate: 65-70%

🚀 How to UseBasic Setup:

Add indicator to MNQ 5-minute chart

Adjust TopStep account settings in inputs

Set your risk per trade percentage (default: 0.5%)

Configure trading session hours

Set minimum signal quality (Start with C for balanced results)

Signal Interpretation:

Green Triangle (BUY): Long signal - all confirmations aligned

Red Triangle (SELL): Short signal - all confirmations aligned

Label Details: Shows entry, stop loss, take profit levels, position size, and signal grade

Signal Grade: A+ = Elite (6-7 points) | A = Strong (5) | B = Good (4) | C = Fair (3)

Dashboard Monitoring:

Top Right: Technical metrics and market conditions

Top Left: Filter status (which filters are passing/blocking)

Bottom Right: TopStep risk metrics and position sizing

⚡ Customization TipsFor More Signals:

Lower "Minimum Signal Quality" to D

Decrease ADX threshold to 18-20

Lower RSI thresholds to 50/50

Reduce Volume multiplier to 1.1x

Disable additional filters

For Higher Quality (Fewer Signals):

Raise "Minimum Signal Quality" to A or A+

Increase ADX threshold to 25-30

Enable all 5 advanced filters

Tighten VWAP distance to 2.0σ

Increase momentum requirement to 3-4 bars

For TopStep Compliance:

Adjust "Max Total Drawdown" and "Daily Loss Limit" to match your account

Update "Already Used Drawdown" daily

Monitor the Risk Panel for cushion remaining

Use recommended contract sizing

🛡️ Risk DisclaimerIMPORTANT: This indicator is for educational and informational purposes only.

Past performance does not guarantee future results

All trading involves substantial risk of loss

Use proper risk management and position sizing

Test thoroughly in paper trading before live use

The indicator does not guarantee profitable trades

Adjust settings based on your risk tolerance and trading style

Always comply with your broker's and TopStep's rules

Stochastic Enhanced [DCAUT]█ Stochastic Enhanced

📊 ORIGINALITY & INNOVATION

The Stochastic Enhanced indicator builds upon George Lane's classic momentum oscillator (developed in the late 1950s) by providing comprehensive smoothing algorithm flexibility. While traditional implementations limit users to Simple Moving Average (SMA) smoothing, this enhanced version offers 21 advanced smoothing algorithms, allowing traders to optimize the indicator's characteristics for different market conditions and trading styles.

Key Improvements:

Extended from single SMA smoothing to 21 professional-grade algorithms including adaptive filters (KAMA, FRAMA), zero-lag methods (ZLEMA, T3), and advanced digital filters (Kalman, Laguerre)

Maintains backward compatibility with traditional Stochastic calculations through SMA default setting

Unified smoothing algorithm applies to both %K and %D lines for consistent signal processing characteristics

Enhanced visual feedback with clear color distinction and background fill highlighting for intuitive signal recognition

Comprehensive alert system covering crossovers and zone entries for systematic trade management

Differentiation from Traditional Stochastic:

Traditional Stochastic indicators use fixed SMA smoothing, which introduces consistent lag regardless of market volatility. This enhanced version addresses the limitation by offering adaptive algorithms that adjust to market conditions (KAMA, FRAMA), reduce lag without sacrificing smoothness (ZLEMA, T3, HMA), or provide superior noise filtering (Kalman Filter, Laguerre filters). The flexibility helps traders balance responsiveness and stability according to their specific needs.

📐 MATHEMATICAL FOUNDATION

Core Stochastic Calculation:

The Stochastic Oscillator measures the position of the current close relative to the high-low range over a specified period:

Step 1: Raw %K Calculation

%K_raw = 100 × (Close - Lowest Low) / (Highest High - Lowest Low)

Where:

Close = Current closing price

Lowest Low = Lowest low over the %K Length period

Highest High = Highest high over the %K Length period

Result ranges from 0 (close at period low) to 100 (close at period high)

Step 2: Smoothed %K Calculation

%K = MA(%K_raw, K Smoothing Period, MA Type)

Where:

MA = Selected moving average algorithm (SMA, EMA, etc.)

K Smoothing = 1 for Fast Stochastic, 3+ for Slow Stochastic

Traditional Fast Stochastic uses %K_raw directly without smoothing

Step 3: Signal Line %D Calculation

%D = MA(%K, D Smoothing Period, MA Type)

Where:

%D acts as a signal line and moving average of %K

D Smoothing typically set to 3 periods in traditional implementations

Both %K and %D use the same MA algorithm for consistent behavior

Available Smoothing Algorithms (21 Options):

Standard Moving Averages:

SMA (Simple): Equal-weighted average, traditional default, consistent lag characteristics

EMA (Exponential): Recent price emphasis, faster response to changes, exponential decay weighting

RMA (Rolling/Wilder's): Smoothed average used in RSI, less reactive than EMA

WMA (Weighted): Linear weighting favoring recent data, moderate responsiveness

VWMA (Volume-Weighted): Incorporates volume data, reflects market participation intensity

Advanced Moving Averages:

HMA (Hull): Reduced lag with smoothness, uses weighted moving averages and square root period

ALMA (Arnaud Legoux): Gaussian distribution weighting, minimal lag with good noise reduction

LSMA (Least Squares): Linear regression based, fits trend line to data points

DEMA (Double Exponential): Reduced lag compared to EMA, uses double smoothing technique

TEMA (Triple Exponential): Further lag reduction, triple smoothing with lag compensation

ZLEMA (Zero-Lag Exponential): Lag elimination attempt using error correction, very responsive

TMA (Triangular): Double-smoothed SMA, very smooth but slower response

Adaptive & Intelligent Filters:

T3 (Tilson T3): Six-pass exponential smoothing with volume factor adjustment, excellent smoothness

FRAMA (Fractal Adaptive): Adapts to market fractal dimension, faster in trends, slower in ranges

KAMA (Kaufman Adaptive): Efficiency ratio based adaptation, responds to volatility changes

McGinley Dynamic: Self-adjusting mechanism following price more accurately, reduced whipsaws

Kalman Filter: Optimal estimation algorithm from aerospace engineering, dynamic noise filtering

Advanced Digital Filters:

Ultimate Smoother: Advanced digital filter design, superior noise rejection with minimal lag

Laguerre Filter: Time-domain filter with N-order implementation, adjustable lag characteristics

Laguerre Binomial Filter: 6-pole Laguerre filter, extremely smooth output for long-term analysis

Super Smoother: Butterworth filter implementation, removes high-frequency noise effectively

📊 COMPREHENSIVE SIGNAL ANALYSIS

Absolute Level Interpretation (%K Line):

%K Above 80: Overbought condition, price near period high, potential reversal or pullback zone, caution for new long entries

%K in 70-80 Range: Strong upward momentum, bullish trend confirmation, uptrend likely continuing

%K in 50-70 Range: Moderate bullish momentum, neutral to positive outlook, consolidation or mild uptrend

%K in 30-50 Range: Moderate bearish momentum, neutral to negative outlook, consolidation or mild downtrend

%K in 20-30 Range: Strong downward momentum, bearish trend confirmation, downtrend likely continuing

%K Below 20: Oversold condition, price near period low, potential bounce or reversal zone, caution for new short entries

Crossover Signal Analysis:

%K Crosses Above %D (Bullish Cross): Momentum shifting bullish, faster line overtakes slower signal, consider long entry especially in oversold zone, strongest when occurring below 20 level

%K Crosses Below %D (Bearish Cross): Momentum shifting bearish, faster line falls below slower signal, consider short entry especially in overbought zone, strongest when occurring above 80 level

Crossover in Midrange (40-60): Less reliable signals, often in choppy sideways markets, require additional confirmation from trend or volume analysis

Multiple Failed Crosses: Indicates ranging market or choppy conditions, reduce position sizes or avoid trading until clear directional move

Advanced Divergence Patterns (%K Line vs Price):

Bullish Divergence: Price makes lower low while %K makes higher low, indicates weakening bearish momentum, potential trend reversal upward, more reliable when %K in oversold zone

Bearish Divergence: Price makes higher high while %K makes lower high, indicates weakening bullish momentum, potential trend reversal downward, more reliable when %K in overbought zone

Hidden Bullish Divergence: Price makes higher low while %K makes lower low, indicates trend continuation in uptrend, bullish trend strength confirmation

Hidden Bearish Divergence: Price makes lower high while %K makes higher high, indicates trend continuation in downtrend, bearish trend strength confirmation

Momentum Strength Analysis (%K Line Slope):

Steep %K Slope: Rapid momentum change, strong directional conviction, potential for extended moves but also increased reversal risk

Gradual %K Slope: Steady momentum development, sustainable trends more likely, lower probability of sharp reversals

Flat or Horizontal %K: Momentum stalling, potential reversal or consolidation ahead, wait for directional break before committing

%K Oscillation Within Range: Indicates ranging market, sideways price action, better suited for range-trading strategies than trend following

🎯 STRATEGIC APPLICATIONS

Mean Reversion Strategy (Range-Bound Markets):

Identify ranging market conditions using price action or Bollinger Bands

Wait for Stochastic to reach extreme zones (above 80 for overbought, below 20 for oversold)

Enter counter-trend position when %K crosses %D in extreme zone (sell on bearish cross above 80, buy on bullish cross below 20)

Set profit targets near opposite extreme or midline (50 level)

Use tight stop-loss above recent swing high/low to protect against breakout scenarios

Exit when Stochastic reaches opposite extreme or %K crosses %D in opposite direction

Trend Following with Momentum Confirmation:

Identify primary trend direction using higher timeframe analysis or moving averages

Wait for Stochastic pullback to oversold zone (<20) in uptrend or overbought zone (>80) in downtrend

Enter in trend direction when %K crosses %D confirming momentum shift (bullish cross in uptrend, bearish cross in downtrend)

Use wider stops to accommodate normal trend volatility

Add to position on subsequent pullbacks showing similar Stochastic pattern

Exit when Stochastic shows opposite extreme with failed cross or bearish/bullish divergence

Divergence-Based Reversal Strategy:

Scan for divergence between price and Stochastic at swing highs/lows

Confirm divergence with at least two price pivots showing divergent Stochastic readings

Wait for %K to cross %D in direction of anticipated reversal as entry trigger

Enter position in divergence direction with stop beyond recent swing extreme

Target profit at key support/resistance levels or Fibonacci retracements

Scale out as Stochastic reaches opposite extreme zone

Multi-Timeframe Momentum Alignment:

Analyze Stochastic on higher timeframe (4H or Daily) for primary trend bias

Switch to lower timeframe (1H or 15M) for precise entry timing

Only take trades where lower timeframe Stochastic signal aligns with higher timeframe momentum direction

Higher timeframe Stochastic in bullish zone (>50) = only take long entries on lower timeframe

Higher timeframe Stochastic in bearish zone (<50) = only take short entries on lower timeframe

Exit when lower timeframe shows counter-signal or higher timeframe momentum reverses

Zone Transition Strategy:

Monitor Stochastic for transitions between zones (oversold to neutral, neutral to overbought, etc.)

Enter long when Stochastic crosses above 20 (exiting oversold), signaling momentum shift from bearish to neutral/bullish

Enter short when Stochastic crosses below 80 (exiting overbought), signaling momentum shift from bullish to neutral/bearish

Use zone midpoint (50) as dynamic support/resistance for position management

Trail stops as Stochastic advances through favorable zones

Exit when Stochastic fails to maintain momentum and reverses back into prior zone

📋 DETAILED PARAMETER CONFIGURATION

%K Length (Default: 14):

Lower Values (5-9): Highly sensitive to price changes, generates more frequent signals, increased false signals in choppy markets, suitable for very short-term trading and scalping

Standard Values (10-14): Balanced sensitivity and reliability, traditional default (14) widely used,适合 swing trading and intraday strategies

Higher Values (15-21): Reduced sensitivity, smoother oscillations, fewer but potentially more reliable signals, better for position trading and lower timeframe noise reduction

Very High Values (21+): Slow response, long-term momentum measurement, fewer trading signals, suitable for weekly or monthly analysis

%K Smoothing (Default: 3):

Value 1: Fast Stochastic, uses raw %K calculation without additional smoothing, most responsive to price changes, generates earliest signals with higher noise

Value 3: Slow Stochastic (default), traditional smoothing level, reduces false signals while maintaining good responsiveness, widely accepted standard

Values 5-7: Very slow response, extremely smooth oscillations, significantly reduced whipsaws but delayed entry/exit timing

Recommendation: Default value 3 suits most trading scenarios, active short-term traders may use 1, conservative long-term positions use 5+

%D Smoothing (Default: 3):

Lower Values (1-2): Signal line closely follows %K, frequent crossover signals, useful for active trading but requires strict filtering

Standard Value (3): Traditional setting providing balanced signal line behavior, optimal for most trading applications

Higher Values (4-7): Smoother signal line, fewer crossover signals, reduced whipsaws but slower confirmation, better for trend trading

Very High Values (8+): Signal line becomes slow-moving reference, crossovers rare and highly significant, suitable for long-term position changes only

Smoothing Type Algorithm Selection:

For Trending Markets:

ZLEMA, DEMA, TEMA: Reduced lag for faster trend entry, quick response to momentum shifts, suitable for strong directional moves

HMA, ALMA: Good balance of smoothness and responsiveness, effective for clean trend following without excessive noise

EMA: Classic choice for trending markets, faster than SMA while maintaining reasonable stability

For Ranging/Choppy Markets:

Kalman Filter, Super Smoother: Superior noise filtering, reduces false signals in sideways action, helps identify genuine reversal points

Laguerre Filters: Smooth oscillations with adjustable lag, excellent for mean reversion strategies in ranges

T3, TMA: Very smooth output, filters out market noise effectively, clearer extreme zone identification

For Adaptive Market Conditions:

KAMA: Automatically adjusts to market efficiency, fast in trends and slow in congestion, reduces whipsaws during transitions

FRAMA: Adapts to fractal market structure, responsive during directional moves, conservative during uncertainty

McGinley Dynamic: Self-adjusting smoothing, follows price naturally, minimizes lag in trending markets while filtering noise in ranges

For Conservative Long-Term Analysis:

SMA: Traditional choice, predictable behavior, widely understood characteristics

RMA (Wilder's): Smooth oscillations, reduced sensitivity to outliers, consistent behavior across market conditions

Laguerre Binomial Filter: Extremely smooth output, ideal for weekly/monthly timeframe analysis, eliminates short-term noise completely

Source Selection:

Close (Default): Standard choice using closing prices, most common and widely tested

HLC3 or OHLC4: Incorporates more price information, reduces impact of sudden spikes or gaps, smoother oscillator behavior

HL2: Midpoint of high-low range, emphasizes intrabar volatility, useful for markets with wide intraday ranges

Custom Source: Can use other indicators as input (e.g., Heikin Ashi close, smoothed price), creates derivative momentum indicators

📈 PERFORMANCE ANALYSIS & COMPETITIVE ADVANTAGES

Responsiveness Characteristics:

Traditional SMA-Based Stochastic:

Fixed lag regardless of market conditions, consistent delay of approximately (K Smoothing + D Smoothing) / 2 periods

Equal treatment of trending and ranging markets, no adaptation to volatility changes

Predictable behavior but suboptimal in varying market regimes

Enhanced Version with Adaptive Algorithms:

KAMA and FRAMA reduce lag by up to 40-60% in strong trends compared to SMA while maintaining similar smoothness in ranges

ZLEMA and T3 provide near-zero lag characteristics for early entry signals with acceptable noise levels

Kalman Filter and Super Smoother offer superior noise rejection, reducing false signals in choppy conditions by estimations of 30-50% compared to SMA

Performance improvements vary by algorithm selection and market conditions

Signal Quality Improvements:

Adaptive algorithms help reduce whipsaw trades in ranging markets by adjusting sensitivity dynamically

Advanced filters (Kalman, Laguerre, Super Smoother) provide clearer extreme zone readings for mean reversion strategies

Zero-lag methods (ZLEMA, DEMA, TEMA) generate earlier crossover signals in trending markets for improved entry timing

Smoother algorithms (T3, Laguerre Binomial) reduce false extreme zone touches for more reliable overbought/oversold signals

Comparison with Standard Implementations:

Versus Basic Stochastic: Enhanced version offers 21 smoothing options versus single SMA, allowing optimization for specific market characteristics and trading styles

Versus RSI: Stochastic provides range-bound measurement (0-100) with clear extreme zones, RSI measures momentum speed, Stochastic offers clearer visual overbought/oversold identification

Versus MACD: Stochastic bounded oscillator suitable for mean reversion, MACD unbounded indicator better for trend strength, Stochastic excels in range-bound and oscillating markets

Versus CCI: Stochastic has fixed bounds (0-100) for consistent interpretation, CCI unbounded with variable extremes, Stochastic provides more standardized extreme readings across different instruments

Flexibility Advantages:

Single indicator adaptable to multiple strategies through algorithm selection rather than requiring different indicator variants

Ability to optimize smoothing characteristics for specific instruments (e.g., smoother for crypto volatility, faster for forex trends)

Multi-timeframe analysis with consistent algorithm across timeframes for coherent momentum picture

Backtesting capability with algorithm as optimization parameter for strategy development

Limitations and Considerations:

Increased complexity from multiple algorithm choices may lead to over-optimization if parameters are curve-fitted to historical data

Adaptive algorithms (KAMA, FRAMA) have adjustment periods during market regime changes where signals may be less reliable

Zero-lag algorithms sacrifice some smoothness for responsiveness, potentially increasing noise sensitivity in very choppy conditions

Performance characteristics vary significantly across algorithms, requiring understanding and testing before live implementation

Like all oscillators, Stochastic can remain in extreme zones for extended periods during strong trends, generating premature reversal signals

USAGE NOTES

This indicator is designed for technical analysis and educational purposes to provide traders with enhanced flexibility in momentum analysis. The Stochastic Oscillator has limitations and should not be used as the sole basis for trading decisions.

Important Considerations:

Algorithm performance varies with market conditions - no single smoothing method is optimal for all scenarios

Extreme zone signals (overbought/oversold) indicate potential reversal areas but not guaranteed turning points, especially in strong trends

Crossover signals may generate false entries during sideways choppy markets regardless of smoothing algorithm

Divergence patterns require confirmation from price action or additional indicators before trading

Past indicator characteristics and backtested results do not guarantee future performance

Always combine Stochastic analysis with proper risk management, position sizing, and multi-indicator confirmation

Test selected algorithm on historical data of specific instrument and timeframe before live trading

Market regime changes may require algorithm adjustment for optimal performance

The enhanced smoothing options are intended to provide tools for optimizing the indicator's behavior to match individual trading styles and market characteristics, not to create a perfect predictive tool. Responsible usage includes understanding the mathematical properties of selected algorithms and their appropriate application contexts.

Session-Conditioned Regime ATRWhy this exists

Classic ATR is great—until the open. The first few bars often inherit overnight gaps and 24-hour noise that have nothing to do with the intraday regime you actually trade. That inflates early ATR, scrambles thresholds, and invites hyper-recency bias (“today is crazy!”) when it’s just the open being the open.

This tool was built to:

Separate session reality from 24h noise. Measure volatility only inside your defined session (e.g., NYSE 09:30–16:00 ET).

Judge candles against the current regime, not the last 2–3 bars. A rolling statistic from the last N completed sessions defines what “typical” means right now.

Label “large” and “small” objectively. Bars are colored only when True Range meaningfully departs from the session regime—no gut feel, no open-bar distortion (gap inclusion optional).

Overview

Purpose: objectively identify unusually big or small candles within the active trading session, compared to the recent session regime.

Use cases: volatility filters, entry/exit confirmation, session bias detection, adaptive sizing.

This indicator replaces generic ATR with a session-conditioned, regime-aware measure. It colors candles only when their True Range (TR) is abnormally large/small versus the last N completed sessions of the same session window.

How it works

Session gating: Only bars inside the selected session are evaluated (presets for NYSE, CME RTH, FX NY; custom supported).

Per-bar TR: TR = max(high, prevRef) − min(low, prevRef).

prevRef is the prior close for in-session bars.

First bar of the session can include the overnight gap (optional; default off).

Regime statistic: For any bar in session k, aggregate all in-session TRs from the previous N completed sessions (k−N … k−1), then compute Median (default) or Mean.

Today’s anchor: Running statistic from today’s session start → current bar (for context and the on-chart ratio).

Color logic:

Big if TR ≥ bigMult × RegimeStat

Small if TR ≤ smallMult × RegimeStat

Colored states: big bull, big bear, small bull, small bear.

Non-triggering bars retain the chart’s native colors.

Panel (top-right by default)

Regime ATR (Nd): session-conditioned statistic over the past N completed sessions.

Today ATR (anchored): running statistic for the current session.

Ratio (Today/Regime): intraday volatility vs regime.

Sample size n: number of bars used in the regime calculation.

Inputs

Session Preset: NYSE (09:30–16:00 ET), CME RTH (08:30–15:00 CT), FX NY (08:00–17:00 ET), Custom (session + IANA timezone).

Regime Window: number of completed sessions (default 5).

Statistic: Median (robust) or Mean.

Include Open Gap: include overnight gap in the first in-session bar’s TR (default off).

Big/Small thresholds: multipliers relative to RegimeStat (defaults: Big=1.5×, Small=0.67×).

Colors: four independent colors for big/small × bull/bear.

Panel position & text size.

Hidden outputs: expose RegimeStat, TodayStat, Ratio, and Z-score to other scripts.

Alerts

RegimeATR: BIG bar — triggers when a bar meets the “Big” condition.

RegimeATR: SMALL bar — triggers when a bar meets the “Small” condition.

Hidden outputs (for strategies/screeners)

RegimeATR_stat, TodayATR_stat, Today_vs_Regime_Ratio, BarTR_Zscore.

Notes & limitations

No look-ahead: calculations only use information available up to that bar. Historical colors reflect what would have been known then.

Warm-up: colors begin once there are at least N completed sessions; before that, regime is undefined by design.

Changing inputs (session window, multipliers, median/mean, gap toggle) recomputes the full series using the same rolling regime logic per bar.

Designed for standard candles. Styling respects existing chart colors when no condition triggers.

Practical tips

For a broader or tighter notion of “unusual,” adjust Big/Small multipliers.

Prefer Median in markets prone to outliers; use Mean if you want Z-score alignment with the panel’s regime mean/std.

Use the Ratio readout to spot compression/expansion days quickly (e.g., <0.7× = compressed session, >1.3× = expanded).

Roadmap

More session presets:

24h continuous (crypto, index CFDs).

23h/Globex futures (CME ETH with a 60-minute maintenance break).

Regional equities (LSE, Xetra, TSE), Asia/Europe/NY overlaps for FX.

Half-day/holiday templates and dynamic calendars.

Multi-regime comparison: track multiple overlapping regimes (e.g., RTH vs ETH for futures) and show separate stats/ratios.

Robust stats options: trimmed mean, MAD/Huber alternatives; optional percentile thresholds instead of fixed multipliers.

Subpanel visuals: rolling TodayATR and Ratio plots; optional Z-score ribbon.

Screener/strategy hooks: export boolean series for BIG/SMALL, plus a lightweight strategy template for backtesting entries/exits conditioned on regime volatility.

Performance/QOL: per-symbol presets, smarter warm-up, and finer control over sample caps for ultra-low TF charts.

Changelog

v0.9b (Beta)

Session presets (NYSE/CME RTH/FX NY/Custom) with timezone handling.

Panel enhancements: ratio + sample size n.

Four-state bar coloring (big/small × bull/bear).

Alerts for BIG/SMALL bars.

Hidden Z-score stream for downstream use.

Gap-in-TR toggle for the first in-session bar.

Disclaimer

For educational purposes only. Not investment advice. Validate thresholds and session settings across symbols/timeframes before live use.

Session First 5-Min High/LowHere's a professional description for your indicator:

Session First 5-Min High/Low Marker

This indicator automatically identifies and marks the high and low price levels established during the first 5 minutes of major trading sessions, helping traders identify key intraday support and resistance zones.

Key Features:

Tracks three major trading sessions in IST (Indian Standard Time):

Asian Session: 5:30 AM - 5:35 AM

London Session: 12:30 PM - 12:35 PM

New York Session: 5:30 PM - 5:35 PM

Draws horizontal lines at the highest and lowest prices reached during each session's opening 5-minute window

Color-coded for easy identification (Yellow for Asian, Blue for London, Red for New York)

Lines extend across the chart to help track price reactions throughout the day

Clean, minimal design with optional labels

Best Used For:

Identifying key intraday support and resistance levels

Session breakout trading strategies

Understanding institutional order flow at market opens

Works on 1-minute timeframe for precise tracking

Customizable Settings:

Toggle line extensions on/off

Adjust line width (1-5)

Change colors for each session

Show/hide session labels

Perfect for day traders and scalpers who trade around major session openings and want to identify high-probability support/resistance zones established during peak liquidity periods.

This description explains what the indicator does, its practical applications, and its key features in a way that's clear for TradingView users.RetryClaude can make mistakes. Please double-check responses.

Session Volume Spike DetectorSession Volume Spike Detector (Buy/Sell, Dual Windows, MTF + Edge/Cooldown)

What it does

Detects statistically significant buy/sell volume spikes inside two DST-aware Mountain Time sessions and projects 1m / 5m / 10m signals onto any chart timeframe (even 1s). Spikes are confirmed at the close of their native bar and are edge-triggered with optional cooldowns to prevent duplicate alerts.

How spikes are detected

Volume ≥ SMA × multiplier

Optional jump vs recent highest volume

Optional Z-Score gate for significance

Separate Buy/Sell logic using your Direction Mode (Prev Close or Candle Body)

Multi-Timeframe (MTF) display

Shows 1m, 5m, 10m arrows on your current chart

Each HTF fires once on its bar close (no repaint after close)

Sessions (DST-aware, MT)

Morning: 05:30–08:30

Midday: 11:00–13:30

Spikes only count inside these windows.

Inputs & styling

Thresholds: SMA length, multipliers, recent lookback, Z-Score toggle/level

Toggles for which TFs to display (chart TF, 1m, 5m, 10m)

Per-TF colors + cooldowns (seconds) for Any TF, 1m, 5m, 10m

Alerts (edge + cooldown)

MTF Volume Spike (Any TF) — fires on the first qualifying spike across enabled TFs

1m / 5m / 10m Volume Spike — per-TF alerts, Buy or Sell

Recommended: set alert Trigger = Once per bar close. Cooldowns tame “triggered too often” warnings.

Great with

FVG zones, bank/insto levels, session range breaks, and trend filters. Use the MTF arrows as a participation/pressure tell to confirm or fade moves.

Notes

Works on any symbol/timeframe; best viewed on 1m or sub-minute charts.

HTF spikes appear on the bar close of 1m/5m/10m respectively.

No dynamic plot titles; Pine v6-safe.

Short summary (≤250 chars):

MTF volume-spike detector for intraday sessions (DST-aware, MT). Projects 1m/5m/10m buy/sell spikes onto any chart, with edge-triggered alerts and per-TF cooldowns to prevent duplicates. Ideal for spotting institutional participation.

Session Volume Spike Detector (MTF Arrows)Overview

The Session Volume Spike Detector is a precision multi-timeframe (MTF) tool that identifies sudden surges in buy or sell volume during key market windows. It highlights high-impact institutional participation by comparing current volume against its historical baseline and short-term highs, then plots directional markers on your chart.

This version adds MTF awareness, showing spikes from 1-minute, 5-minute, and 10-minute frames on a single chart. It’s ideal for traders monitoring microstructure shifts across multiple time compressions while staying on a fast chart (like 1-second or 1-minute).

Key Features

Dual Session Windows (DST-aware)

Automatically tracks Morning (05:30–08:30 MT) and Midday (11:00–13:30 MT) activity, adjusted for daylight savings.

Directional Spike Detection

Flags Buy spikes (green triangles) and Sell spikes (magenta triangles) using dynamic volume gates, Z-Score normalization, and recent-bar jump filters.

Multi-Timeframe Projection

Displays higher-timeframe (1m / 5m / 10m) spikes directly on your active chart for continuous visual context — even on sub-minute intervals.

Adaptive Volume Logic

Each spike is validated against:

Volume ≥ SMA × multiplier

Volume ≥ recent-high × jump factor

Optional Z-Score threshold for statistical significance

Session-Only Filtering

Ensures spikes are only plotted within specified trading sessions — ideal for futures or intraday equity traders.

Configurable Alerts

Built-in alert conditions for:

Any timeframe (MTF aggregate)

Individual 1m, 5m, or 10m windows

Alerts trigger only when a new qualifying spike appears at the close of its bar.

Use Cases

Detect algorithmic or institutional activity bursts inside your trading window.

Track confluence of volume surges across multiple timeframes.

Combine with FVGs, bank levels, or range breakouts to identify probable continuation or reversal zones.

Build custom automation or alert workflows around statistically unusual participation spikes.

Recommended Settings

Use on 1-minute chart for full MTF display.

Adjust the SMA length (default 20) and Z-Score threshold (default 3.0) to suit market volatility.

For scalping or high-frequency environments, disable the 10m layer to reduce visual clutter.

Credits

Developed by Jason Hyde

© 2025 — All rights reserved.

Designed for clarity, precision, and MTF-synchronized institutional volume detection.

Williams Alligator Spread Oscillator (WASO)Short description (About box)

Williams Alligator Spread Oscillator (WASO) converts Bill Williams’ Alligator into a 0–100 oscillator that measures the average distance between Lips/Teeth/Jaw relative to ATR. High = expansion/trend (default), low = compression/range — making sideways markets easier to spot. Includes adaptive normalization, configurable thresholds, background shading, and alerts.

Full description (Description field)

What it does

The Williams Alligator Spread Oscillator (WASO) transforms Bill Williams’ Alligator into a single, adaptive 0–100 scale. It computes the average pairwise distance among the Alligator lines (Lips/Teeth/Jaw), normalizes it by ATR and a rolling min–max window, and smooths the result. This makes the signal robust across symbols and timeframes and explicitly improves detection of sideways (ranging) conditions by highlighting compression regimes.

Why it helps

Sideways detection made easier: Low WASO marks compressed regimes that commonly align with consolidation/range phases, helping you identify chop and plan breakout strategies.

Trend/expansion clarity: High WASO indicates the Alligator lines are widening relative to volatility, pointing to trending or expanding conditions.

You can flip the direction if you prefer “High = Range.”

How it is calculated (plain English)

Smooth price with RMA (SMMA-like) to get Jaw, Teeth, Lips.

Compute the average pairwise distance between these three lines.

Divide by ATR to remove price-scale effects.

Normalize with a rolling min–max window to map values to 0–100.

Optionally apply EMA smoothing to the oscillator.

Key settings

Jaw/Teeth/Lips Lengths: Alligator periods (SMMA-like via ta.rma).

ATR Length: Volatility benchmark for scaling.

Normalization Lookback: Longer = steadier; shorter = more responsive.

Smoothing (EMA): Evens out noise.

High Value = Large Spread (Trend): Toggle to invert semantics.

Upper/Lower Thresholds: 70/30 are practical starting points.

Signals / interpretation

Sideways / Compression (easier to spot):

Default direction: WASO below Lower Threshold (e.g., <30).

With inverted direction OFF: WASO above Upper Threshold (e.g., >70).

Trend / Expansion:

Default direction: WASO above Upper Threshold (e.g., >70).

With inverted direction OFF: WASO below Lower Threshold (e.g., <30).

Midline (50): Neutral zone; flips around 50 can hint at regime shifts.

Alerts included

Range Start (sideways/compression)

Trend Start (expansion/trend)

Notes & limitations

This implementation omits the classic forward shift of Alligator lines to keep signals usable on live bars.

If market behavior shifts (very quiet or very volatile), tune Lookback and ATR Length.

Combine WASO with breakout levels or momentum filters for entries/exits.

Credits & disclaimer

Inspired by Bill Williams’ Alligator.

For educational purposes only. Not financial advice.

Release Notes (v1.0):

Initial release of Williams-Alligator Spread Oscillator (WASO) with ATR-based scaling and adaptive 0–100 normalization.

Direction toggle (High = Trend by default), adjustable thresholds, background shading, and two alert conditions.

FirstStrike Long 200 - Daily Trend Rider [KedArc Quant]Strategy Description

FirstStrike Long 200 is a disciplined, long-only momentum strategy designed for daily "strike-first" entries in trending markets. It scans for RSI momentum above a customizable trigger (default 50), confirmed by EMA trend filters, and limits you to *exactly one trade per day* to avoid overtrading. It uses ATR for dynamic risk management (1.5x stop, 2:1 RR target) and optional trailing stops to ride winners. Backtested with realistic commissions and sizing, it prioritizes low drawdowns (<1% max in tests) over aggressive gains—ideal for swing traders seeking quality setups in bull runs.

Why It's Different from Other Strategies

Unlike generic RSI crossover bots or EMA ribbon mashups that spam signals and bleed in chop, FirstStrike enforces a "one-and-done" daily gate, blending precision momentum (RSI modes with grace/sustain) with robust filters (volume, sessions, rearm dips).

How It Helps Traders

- Reduces Emotional Trading: One entry/day forces discipline—miss a setup? Wait for tomorrow. Perfect for busy pros avoiding screen fatigue.

- Adapts to Regimes: Switch modes for trends ("Cross+Grace") vs. ranges ("Any bar")—boosts win rates 5-10% in backtests on high-beta names like .

- Risk-First Design: ATR scales stops to vol capping DD at 0.2% while targeting 2R winners. Trailing option locks +3-5% runs without early exits.

- Quick Insights: Labels/alerts flag entries with RSI values; bgcolor highlights signals for visual scanning. Helps spot "first-strike" edges in uptrends, filtering ~60% noise.

Why This Is Not a Mashup

This isn't a Frankenstein of off-the-shelf indicators—while it uses standard RSI/EMA/ATR (core Pine primitives), the innovation lies in:

- Custom Trigger Engine: Switchable modes (e.g., "Cross+Grace+Sustain" requires post-cross hold) prevent perpetual signals, unlike basic `ta.crossover()`.

- Daily Rearm Gate: Resets eligibility only after a dip (if enabled), tying momentum to mean-reversion—original logic not found in common scripts.

- Per-Day Isolation: `var` vars + `ta.change(time("D"))` ensure zero pyramiding/overlaps, beyond simple session filters.

All formulae are derived in-house for "first-strike" (early RSI pops in trends), not copied from public repos.

Input Configurations

Let's break down every input in the FirstStrike Long 200 strategy. These settings let you tweak the strategy like a dashboard—start with defaults for quick testing,

then adjust based on your asset or timeframe (5m for intraday). They're grouped logically to keep things organized, and most have tooltips in the script for quick reminders.

RSI / Trigger Group: The Heart of Momentum Detection

This is where the magic starts—the strategy hunts for "upward energy" using RSI (Relative Strength Index), a tool that measures if a stock is overbought (too hot) or oversold (too cold) on a 0-100 scale.

- RSI Length: How many bars (candles) back to calculate RSI. Default is 14, like a 14-day window for daily charts. Shorter (e.g., 9) makes it snappier for fast markets; longer (21) smooths out noise but misses quick turns.

- Trigger Level (RSI >= this): The key RSI value where the strategy says, "Go time!" Default 50 means enter when RSI crosses or holds above the neutral midline. Why is this trigger required? It acts as your "green light" filter—without it, you'd enter on every tiny price wiggle, leading to endless losers. RSI above this shows building buyer power, avoiding weak or sideways moves. It's essential for quality over quantity, especially in one-trade-per-day setups.

- Trigger Mode: Picks how strict the RSI signal must be. Options: "Cross only" (exact RSI crossover above trigger—super precise, fewer trades); "Cross+Grace" (crossover or within a grace window after—gives a second chance); "Cross+Grace+Sustain" (crossover/grace plus RSI holding steady for bars—best for steady climbs); "Any bar >= trigger" (looser, any bar above—more opportunities but riskier in chop). Start with "Any bar" for trends, switch to "Cross only" for caution.

- Grace Window (bars after cross): If mode allows, how many bars post-RSI-cross you can still enter if RSI dips but recovers. Default 30 (about 2.5 hours on 5m). Zero means no wiggle room—pure precision.

- Sustain Bars (RSI >= trigger): In sustain mode, how many straight bars RSI must stay above trigger. Default 3 ensures it's not a fluke spike.

- Require RSI Dip Below Rearm Before Any Entry?: A yes/no toggle. If on, the strategy "rearms" only after RSI dips below a low level (like a breather), preventing back-to-back signals in overextended rallies.

- Rearm Level (if requireDip=true): The dip threshold for rearming. Default 45—RSI must go below this to reset eligibility. Lower (30) for deeper pullbacks in volatile stocks.

For the trigger level itself, presets matter a lot—default 50 is neutral and versatile for broad trends. Bump to 55-60 for "strong momentum only" (fewer but higher-win trades, great in bull runs like tech surges); drop to 40-45 for "early bird" catches in recoveries (more signals but watch for fakes in ranges). The optimize hint (40-60) lets you test these in TradingView to match your risk—higher presets cut noise by 20-30% in backtests.

Trend / Filters Group: Keeping You on the Right Side of the Market

These EMAs (Exponential Moving Averages) act like guardrails, ensuring you only long in uptrends.

- EMA (Fast) Confirmation: Short-term EMA for price action. Default 20 periods—price must be above this for "recent strength." Shorter (10) reacts faster to intraday pops.

- EMA (Trend Filter): Long-term EMA for big-picture trend. Default 200 (classic "above the 200-day" rule)—price above it confirms bull market. Minimum 50 to avoid over-smoothing.

Optional Hour Window Group: Timing Your Strikes

Avoid bad hours like lunch lulls or after-hours tricks.

- Restrict by Session?: Yes/no for using exact market hours. Default off.

- Session (e.g., 0930-1600 for NYSE): Time string like "0930-1600" for open to close. Auto-skips pre/post-market noise.

- Restrict by Hour Range?: Fallback yes/no for simple hours. Default off.

- Start Hour / End Hour: Clock times (0-23). Defaults 9-15 ET—focus on peak volume.

Volume Filter Group: No Volume, No Party

Confirms conviction—big moves need big participation.

- Require Volume > SMA?: Yes/no toggle. Default off—only fires on above-average volume.

- Volume SMA Length: Periods for the average. Default 20—compares current bar to recent norm.

Risk / Exits Group: Protecting and Profiting Smartly

Dynamic stops based on volatility (ATR = Average True Range) keep things realistic.

- ATR Length: Bars for ATR calc. Default 14—measures recent "wiggle room" in price.

- ATR Stop Multiplier: How far below entry for stop-loss. Default 1.5x ATR—gives breathing space without huge risk

- Take-Profit R Multiple: Reward target as multiple of risk. Default 2.0 (2:1 ratio)—aims for twice your stop distance.

- Use Trailing Stop?: Yes/no for profit-locking trail. Default off—activates after entry.

- Trailing ATR Multiplier: Trail distance. Default 2.0x ATR—looser than initial stop to let winners run.