4C Options Expected Move (Weekly + 0DTE)This indicator plots the calculated Expected Move for BOTH Weekly and Zero Dated Expiration (0DTE) Daily options, for a quick visual reference.

Please Note: This indicator is different from our original "4C Expected Move (Weekly Options)" indicator, as it now packages the ability to ALSO plot 0DTE options expected moves along with Weekly expected moves. Many other newer features have also been implemented.

Background Information

The Expected Move (EM) is the amount that a stock is predicted to increase or decrease from its current price, based on the current level of options pricing and implied volatility.

This range can be viewed as possible support and resistance, or, once price gets outside of the range, institutional hedging actions can accelerate the move in that direction.

It can be useful to know what the weekly EM range is for a stock to understand the probabilities of the overall distance, direction and volatility for the week.

About the Indicator

This indicator plots the calculated Expected Move for BOTH Weekly and Zero Dated Expiration (0DTE) options, for a quick visual reference.

For the weekly EM, the range is based on the Weekly close of the prior week.

For the Daily EM based on 0DTE options, the range is based on the Daily close of the prior day.

The indicator will automatically start a new weekly EM plot at the beginning of the week, and a new daily EM at the beginning of each day.

The EM values must be updated weekly and/or daily.

Features

Plots the EM for the week

Plots the EM for the day, for symbols that offer daily expiration options

Plots the 2 Standard Deviation EM for both the weekly and daily EM

Labels with calculated values are plotted near the levels for quick visual aid

Settings

Can toggle weekly EM on/off

Can toggle Daily EM on/off

Can toggle 2 Standard Deviation lines on/off

Can toggle labels for all EM on/off

Robust line settings

Can adjust label location left/right based on personal preference

Can enter symbol into settings as a reference

Handy instructions in the settings

How To Set Up The Indicator

To use this indicator you must have access to a broker with options data (not available on Tradingview).

Usually, you can look at the stock's option chain to find the weekly expected move.

You will have to do your own research to find where this information is displayed depending on your broker. You may also need to find the information elsewhere if your broker does not have this information.

You can also do your calculation of the EM using the following formula (please do your own research):

Expected Move = Option Price x Implied Volatility x Square Root of Time

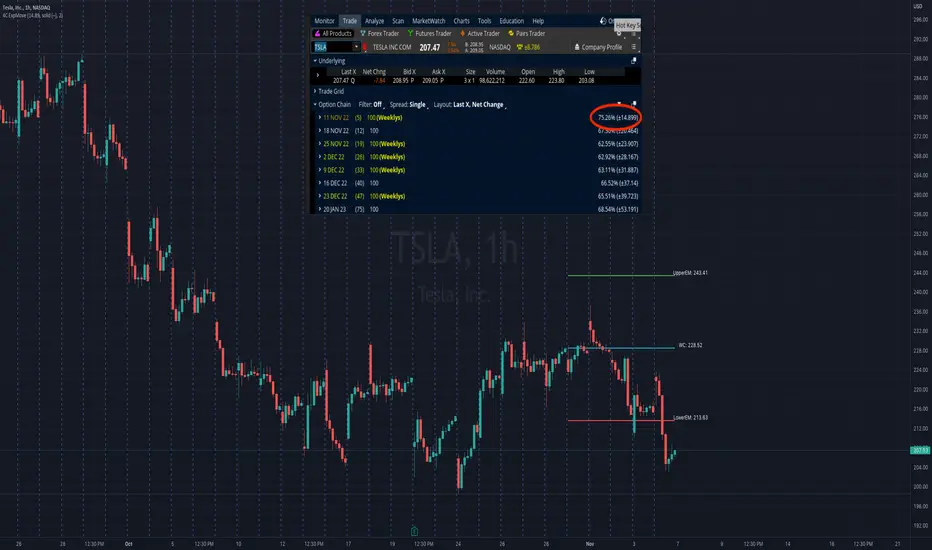

See screenshot example below

This is the Thinkorswim platform's option chain, and the Implied Volatility % and the calculated EM are on the right side of the option chain.

The Expected Move is circled in blue. Use the +- number in parentheses, NOT the % value.

For the weekly EM, input the number that corresponds to the weekly option into the indicator. This must be done on a weekly basis, and It is typically best to use the EM for the next week expiration that is generated AFTER the Friday close and/or before the Monday open of the upcoming week.

For the daily EM, input the number that corresponds to the daily 0DTE option into the indicator. This must be done on a daily basis, and it is typically best to use the EM value for the 0DTE option that is generated the night before (after market close), or before the market opens for that 0DTE. .

Pine Script® indicator