T7 JNSARUpdated code for the T7 JNSAR system earlier published here -

Following updates made to the code

1. Buy / Sell arrows now appear when the corresponding conditions are met.

2. Support for Heikin-Ashi Candles added

3. Different Backtesting Position Sizing Algorithms added for evaluation

Also am republishing the trading rules here again with some modification

1. Go Long when the daily close is above the JNSAR line. Go Short when the daily close is below the JNSAR line. JNSAR line is the varying green line overlayed over the price chart. Once a signal comes at market close enter in the direction of the signal @ market price @ next day market open.

2. Trade only Nifty Index. This system was developed and backtested only for NIFTY Index. So trade in its Futures or Options, as you may deem fit. My recommendation is to choose futures for simplicity. If you want to reduce the trading cost and go with options, trade with deep in the money options, preferably 2 strikes far from the spot price.

3. Trade all signals. Markets trend only 30-35% of the time and hence the system is only accurate to that extend. But system tends to make enough money, in this small trending window, to keep the overall profitability in good health. But one never knows when a big trend may come and when it comes its absolutely imperative that you take it. To ensure that, trade all signals and don't be choosy about what signals you are going to trade. Also I wouldn't recommend using your own analysis to trade this system. Too many drivers will crash the car.

4. Like all trend following systems, this system will have many whipsaws during flat markets along with large trade and account drawdowns. Also some months and even years may not be profitable. But to trade this system profitably, it is necessary to take these in one's stride and keep trading. As the backtester results from 1990 to 2016 proves, this system is profitable overall thus far. Take confidence from that objective fact.

5. Trade with only that amount of money you can afford to loose. Initial capital that you need to have to trade one lot of NIFTY should be atleast - (Margin Money required to take and hold 1 lot position + maximum drawdown amount per lot)*1.2. Be prepared to add more if need be, but the above formula will give a rough idea of what you need to have to start trading and be in the game always.

6. Place an After Market Order @ Market Price with your broker after market close so that you get to execute the trade next trading day @ Market open to capture near similar price as the daily open price seen on the chart. This execution mode will give you the best chance to minimise the slippage and mimic the backtester results as closely as practically possible.

7. Follow all the 6 rules above religiously, as if your life depends on it. If you cant, then don't trade this system; You will certainly loose money.

Happy Trading !!! As always am looking out for your valuable feedback.

Search in scripts for "backtest"

CryptoFlux Dynamo [JOAT]CryptoFlux Dynamo: Velocity Scalping Strategy

This Pine Script v6 strategy is designed for cryptocurrency markets operating on 5-minute and faster timeframes. It combines volatility regime detection, multi-path signal confirmation, and adaptive risk management to identify momentum-based trading opportunities in perpetual futures markets.

Core Design Principles

The strategy addresses three challenges specific to cryptocurrency trading:

24/7 market operation without session boundaries requires continuous monitoring and execution logic

Volatility regimes shift rapidly, demanding adaptive stop and target calculations

Tick-level responsiveness is critical for capturing momentum moves before they complete

Strategy Architecture

1. Signal Generation Stack

The strategy uses multiple technical indicators calibrated for cryptocurrency momentum:

MACD with parameters 8/21/5 (fast/slow/signal) optimized for crypto acceleration phases

EMA ribbon using 8/21/34 periods with slope analysis to assess trend structure

Volume impulse detection combining SMA baseline, standard deviation, and z-score filtering

RSI (21 period) and MFI (21 period) for momentum confirmation

Bollinger Bands and Keltner Channels for squeeze detection

2. Volatility Regime Classification

The strategy normalizes ATR as a percentage of price and classifies market conditions into three regimes:

Compression (< 0.8% ATR): Reduced position sizing, tighter stops (1.05x ATR), lower profit targets (1.6x ATR)

Expansion (0.8% - 1.6% ATR): Standard risk parameters, balanced risk-reward (1.55x stop, 2.05x target)

Velocity (> 1.6% ATR): Wider stops (2.1x ATR), amplified targets (2.8x ATR), tighter trailing offsets

ATR is calculated over 21 periods and smoothed with a 13-period EMA to reduce noise from wicks.

3. Multi-Path Entry System

Four independent signal pathways contribute to a composite strength score (0-100):

Trend Break (30 points): Requires EMA ribbon alignment, positive slope, and structure breakout above/below recent highs/lows

Momentum Surge (30 points): MACD histogram exceeds adaptive baseline, MACD line crosses signal, RSI/MFI above/below thresholds, with volume impulse confirmation

Squeeze Release (25 points): Bollinger Bands compress inside Keltner Channels, then release with momentum bias

Micro Pullback (15 points): Shallow retracements within trend structure that reset without breaking support/resistance

Additional scoring modifiers:

Volume impulse: +5 points when present, -5 when absent

Regime bonus: +5 in velocity, -2 in compression

Cycle bias: +5 when aligned, -5 when counter-trend

Trades only execute when the composite score reaches the minimum threshold (default: 55) and all filters agree.

4. Risk Management Framework

Position sizing is calculated from:

RiskCapital = Equity × (riskPerTradePct / 100)

StopDistance = ATR × StopMultiplier(regime)

Quantity = min(RiskCapital / StopDistance, MaxExposure / Price)

The strategy includes:

Risk per trade: 0.65% of equity (configurable)

Maximum exposure: 12% of equity (configurable)

Regime-adaptive stop and target multipliers

Adaptive trailing stops based on ATR and regime

Kill switch that disables new entries after 6.5% drawdown

Momentum fail-safe exits when MACD polarity flips or ribbon structure breaks

5. Additional Filters

Cycle Oscillator : Measures price deviation from 55-period EMA. Requires cycle bias alignment (default: ±0.15%) before entry

BTC Dominance Filter : Optional filter using CRYPTOCAP:BTC.D to reduce long entries during risk-off periods (rising dominance) and short entries during risk-on periods

Session Filter : Optional time-based restriction (disabled by default for 24/7 operation)

Strategy Parameters

All default values used in backtesting:

Core Controls

Enable Short Structure: true

Restrict to Session Window: false

Execution Session: 0000-2359:1234567 (24/7)

Allow Same-Bar Re-Entry: true

Optimization Constants

MACD Fast Length: 8

MACD Slow Length: 21

MACD Signal Length: 5

EMA Fast: 8

EMA Mid: 21

EMA Slow: 34

EMA Slope Lookback: 8

Structure Break Window: 9

Regime Intelligence

ATR Length: 21

Volatility Soothing: 13

Low Vol Regime Threshold: 0.8% ATR

High Vol Regime Threshold: 1.6% ATR

Cycle Bias Length: 55

Cycle Bias Threshold: 0.15%

BTC Dominance Feed: CRYPTOCAP:BTC.D

BTC Dominance Confirmation: true

Signal Pathways

Volume Baseline Length: 34

Volume Impulse Multiplier: 1.15

Volume Z-Score Threshold: 0.5

MACD Histogram Smoothing: 5

MACD Histogram Sensitivity: 1.15

RSI Length: 21

RSI Momentum Trigger: 55

MFI Length: 21

MFI Momentum Trigger: 55

Squeeze Length: 20

Bollinger Multiplier: 1.5

Keltner Multiplier: 1.8

Squeeze Release Momentum Gate: 1.0

Micro Pullback Depth: 7

Minimum Composite Signal Strength: 55

Risk Architecture

Risk Allocation per Trade: 0.65%

Max Exposure: 12% of Equity

Base Risk/Reward Anchor: 1.8

Stop Multiplier • Low Regime: 1.05

Stop Multiplier • Medium Regime: 1.55

Stop Multiplier • High Regime: 2.1

Take Profit Multiplier • Low Regime: 1.6

Take Profit Multiplier • Medium Regime: 2.05

Take Profit Multiplier • High Regime: 2.8

Adaptive Trailing Engine: true

Trailing Offset Multiplier: 0.9

Quantity Granularity: 0.001

Kill Switch Drawdown: 6.5%

Strategy Settings

Initial Capital: $100,000

Commission: 0.04% (0.04 commission_value)

Slippage: 1 tick

Pyramiding: 1 (no position stacking)

calc_on_every_tick: true

calc_on_order_fills: true

Visualization Features

The strategy includes:

EMA ribbon overlay (8/21/34) with customizable colors

Regime-tinted background (compression: indigo, expansion: purple, velocity: magenta)

Dynamic bar coloring based on signal strength divergence

Signal labels for entry points

On-chart dashboard displaying regime, ATR%, signal strength, position status, stops, targets, and risk metrics

Recommended Usage

Timeframes

The strategy is optimized for 5-minute charts. It can operate on 3-minute and 1-minute timeframes for faster scalping, or 15-minute for swing confirmation. When using higher timeframes, consider:

Increasing structure lookback windows

Raising RSI trigger thresholds above 58 to filter noise

Extending volume baseline length

Markets

Designed for high-liquidity cryptocurrency perpetual futures:

BTC/USDT, BTC/USD perpetuals

ETH perpetuals

Major L1 tokens with sufficient volume

For thinner order books, increase volume impulse multiplier and adjust quantity granularity to match exchange minimums.

Limitations and Compromises

Backtesting Considerations

TradingView strategy backtesting does not replicate broker execution. Actual fills, slippage, and commissions may differ

The strategy uses calc_on_every_tick=true and calc_on_order_fills=true to reduce bar-close distortions, but real execution still depends on broker infrastructure

At least 200 historical bars are required to stabilize regime classification, volume baselines, and cycle context

Market Structure Dependencies

BTC dominance feed ( CRYPTOCAP:BTC.D ) may lag during low-liquidity periods or weekends. Consider disabling the filter if data quality degrades

Volume impulse detection assumes consistent order book depth. During extreme volatility or exchange issues, volume signatures may be unreliable

Regime classification based on ATR percentage assumes normal volatility distributions. During black swan events, regime thresholds may not adapt quickly enough

Parameter Sensitivity

Default parameters are tuned for BTC/ETH perpetuals on 5-minute charts. Different assets or timeframes require recalibration

The composite signal strength threshold (55) balances selectivity vs. opportunity. Higher values reduce false signals but may miss valid setups

Risk per trade (0.65%) and max exposure (12%) are conservative defaults. Aggressive scaling increases drawdown risk

Execution Constraints

Same-bar re-entry requires broker support for rapid order placement

Quantity granularity must match exchange contract minimums

Kill switch drawdown (6.5%) may trigger during normal volatility cycles, requiring manual reset

Performance Expectations

This strategy is a framework for momentum-based cryptocurrency trading. Performance depends on:

Market conditions (trending vs. ranging)

Exchange execution quality

Parameter calibration for specific assets

Risk management discipline

Backtest results shown in publications reflect specific market conditions and parameter sets. Past performance does not indicate future results. Always forward test with paper trading or broker simulation before deploying live capital.

Code Structure

The strategy is organized into functional sections:

Configuration groups for parameter organization

Helper functions for position sizing and normalization

Core indicator calculations (MACD, EMA, ATR, RSI, MFI, volume analytics)

Regime classification logic

Multi-path signal generation and composite scoring

Entry/exit orchestration with risk management

Visualization layer with dashboard and chart elements

The source code is open and can be modified to suit your trading requirements. Everyone is encouraged to understand the logic before deploying and to test thoroughly in their target markets.

Modification Guidelines

When adapting this strategy:

Document any parameter changes in your publication

Test modifications across different market regimes

Validate position sizing logic for your exchange's contract specifications

Consider exchange-specific limitations (funding rates, liquidation mechanics, order types)

Conclusion

This strategy provides a structured approach to cryptocurrency momentum trading with regime awareness and adaptive risk controls. It is not a guaranteed profit system, but rather a framework that requires understanding, testing, and ongoing calibration to market conditions.

You should thoroughly understand the logic, test extensively in their target markets, and manage risk appropriately. The strategy's effectiveness depends on proper parameter tuning, reliable execution infrastructure, and disciplined risk management.

Disclaimer

This script and its documentation are for educational and informational purposes only. They do not constitute financial advice, investment recommendations, or trading advice of any kind. Trading cryptocurrencies and derivatives involves substantial risk of loss and is not suitable for all investors. Past performance, whether real or indicated by backtesting, does not guarantee future results.

This strategy is provided "as is" without any warranties or guarantees of profitability

You should not rely solely on this strategy for making trading decisions

Always conduct your own research and analysis before making any financial decisions

Consider consulting with a qualified financial advisor before engaging in trading activities

The authors and contributors are not responsible for any losses incurred from using this strategy

Cryptocurrency trading can result in the loss of your entire investment

Only trade with capital you can afford to lose

Use this strategy at your own risk. The responsibility for any trading decisions and their consequences lies entirely with you.

Elliott Wave Full Fractal System v2.0Elliott Wave Full Fractal System v2.0 – Q.C. FINAL (Guaranteed R/R)

Elliott Wave Full Fractal System is a multi-timeframe wave engine that automatically labels Elliott impulses and ABC corrections, then builds a rule-based, ATR-driven risk/reward framework around the “W3–W4–W5” leg.

“Guaranteed R/R” here means every order is placed with a predefined stop-loss and take-profit that respect a minimum Reward:Risk ratio – it does not mean guaranteed profits.

Core Idea

This strategy turns a full fractal Elliott Wave labelling engine into a systematic trading model.

It scans fractal pivots on three wave degrees (Primary, Intermediate, Minor) to detect 5-wave impulses and ABC corrections.

A separate “Trading Degree” pivot stream, filtered by a 200-EMA trend filter and ATR-based dynamic pivots, is then used to find W4 pullback entries with a minimum, user-defined Reward:Risk ratio.

Default Properties & Risk Assumptions

The backtest uses realistic but conservative defaults:

// Default properties used for backtesting

strategy(

"Elliott Wave Full Fractal System - Q.C. FINAL (Guaranteed R/R)",

overlay = true,

initial_capital = 10000, // realistic account size

default_qty_type = strategy.percent_of_equity,

default_qty_value = 1, // 1% risk per trade

commission_type = strategy.commission.cash_per_contract,

commission_value = 0.005, // example stock commission

slippage = 0 // see notes below

)

Account size: 10,000 (can be changed to match your own account).

Position sizing: 1% of equity per trade to keep risk per idea sustainable and aligned with TradingView’s recommendations.

Commission: 0.005 cash per contract/share as a realistic example for stock trading.

Slippage: set to 0 in code for clarity of “pure logic” backtesting. Real-life trading will experience slippage, so users should adjust this according to their market and broker.

Always re-run the backtest after changing any of these values, and avoid using high risk fractions (5–10%+) as that is rarely sustainable.

1. Full Fractal Wave Engine

The script builds and maintains four pivot streams using ATR-adaptive fractals:

Primary Degree (Macro Trend):

Captures the large swings that define the major trend. Labels ①–⑤ and ⒶⒷⒸ using blue “Circle” labels and thicker lines.

Intermediate Degree (Trading Degree):

Captures the medium swings (swing-trading horizon). Uses teal labels ( (1)…(5), (A)(B)(C) ).

Minor Degree (Micro Structure):

Tracks short-term swings inside the larger waves. Uses red roman numerals (i…v, a b c).

ABC Corrections (Optional):

When enabled, the engine tries to detect standard A–B–C corrective structures that follow a completed 5-wave impulse and plots them with dashed lines.

Each degree uses a dynamic pivot lookback that expands when ATR is above its EMA, so the system naturally requires “stronger” pivots in volatile environments and reacts faster in quiet conditions.

2. Theory Rules & Strict Mode

Normal Mode: More permissive detection. Designed to show more wave structures for educational / exploratory use.

Strict Mode: Enforces key Elliott constraints:

Wave 3 not shorter than waves 1 and 5.

No invalid W4 overlap with W1 (for standard impulses).

ABC Logic: After a confirmed bullish impulse, the script expects a down-up-down corrective pattern (A,B,C). After a bearish impulse, it looks for up-down-up.

3. Trend Filter & Pivots

EMA Trend Filter: A configurable EMA (default 200) is used as a non-wave trend filter.

Price above EMA → Only long setups are considered.

Price below EMA → Only short setups are considered.

ATR-Adaptive Pivots: The pivot engine scales its left/right bars based on current ATR vs ATR EMA, making waves and trading pivots more robust in volatile regimes.

4. Dynamic Risk Management (Guaranteed R/R Engine)

The trading engine is designed around risk, not just pattern recognition:

ATR-Based Stop:

Stop-loss is placed at:

Entry ± ATR × Multiplier (user-configurable, default 2.0).

This anchors risk to current volatility.

Minimum Reward:Risk Ratio:

For each setup, the script:

Computes the distance from entry to stop (risk).

Projects a take-profit target at risk × min_rr_ratio away from entry.

Only accepts the setup if risk is positive and the required R:R ratio is achievable.

Result: Every order is created with both TP and SL at a predefined distance, so each trade starts with a known, minimum Reward:Risk profile by design.

“Guaranteed R/R” refers exclusively to this order placement logic (TP/SL geometry), not to win-rate or profitability.

5. Trading Logic – W3–W4–W5 Pattern

The Trading pivot stream (separate from visual wave degrees) looks for a simple but powerful pattern:

Bullish structure:

Sequence of pivots forms a higher-high / higher-low pattern.

Price is above the EMA trend filter.

A strong “W3” leg is confirmed with structure rules (optionally stricter in Strict mode).

Entry (Long – W4 Pullback):

The “height” of W3 is measured.

Entry is placed at a configurable Fibonacci pullback (default 50%) inside that leg.

ATR-based stop is placed below entry.

Take-profit is projected to satisfy min Reward:Risk.

Bearish structure:

Mirrored logic (lower highs/lows, price below EMA, W3 down, W4 retrace up, W5 continuation down).

Once a valid setup is found, the script draws a colored box around the entry zone and a label describing the type of signal (“LONG SETUP” or “SHORT SETUP”) with the suggested limit price.

6. Orders & Execution

Entry Orders: The strategy uses limit orders at the computed W4 level (“Sniper Long” or “Sniper Short”).

Exits: A single strategy.exit() is attached to each entry with:

Take-profit at the projected minimum R:R target.

Stop-loss at ATR-based level.

One Trade at a Time: New setups are only used when there is no open position (strategy.opentrades == 0) to keep the logic clear and risk contained.

7. Visual Guide on the Chart

Wave Labels:

Primary: ①,②,③,④,⑤, ⒶⒷⒸ

Intermediate: (1)…(5), (A)(B)(C)

Minor: i…v, a b c

Trend EMA: Single blue EMA showing the dominant trend.

Setup Boxes:

Green transparent box → long entry zone.

Red transparent box → short entry zone.

Labels: “LONG SETUP / SHORT SETUP” labels mark the proposed limit entry with price.

8. How to Use This Strategy

Attach the strategy to your chart

Choose your market (stocks, indices, FX, crypto, futures, etc.) and timeframe (for example 1h, 4h, or Daily). Then add the strategy to the chart from your Scripts list.

Start with the default settings

Leave all inputs on their defaults first. This lets you see the “intended” behaviour and the exact properties used for the published backtest (account size, 1% risk, commission, etc.).

Study the wave map

Zoom in and out and look at the three wave degrees:

Blue circles → Primary degree (big picture trend).

Teal (1)…(5) → Intermediate degree (swing structure).

Red i…v → Minor degree (micro waves).

Use this to understand how the engine is interpreting the Elliott structure on your symbol.

Watch for valid setups

Look for the coloured boxes and labels:

Green box + “LONG SETUP” label → potential W4 pullback long in an uptrend.

Red box + “SHORT SETUP” label → potential W4 pullback short in a downtrend.

Only trades in the direction of the EMA trend filter are allowed by the strategy.

Check the Reward:Risk of each idea

For each setup, inspect:

Limit entry price.

ATR-based stop level.

Projected take-profit level.

Make sure the minimum Reward:Risk ratio matches your own rules before you consider trading it.

Backtest and evaluate

Open the Strategy Tester:

Verify you have a decent sample size (ideally 100+ trades).

Check drawdowns, average trade, win-rate and R:R distribution.

Change markets and timeframes to see where the logic behaves best.

Adapt to your own risk profile

If you plan to use it live:

Set Initial Capital to your real account size.

Adjust default_qty_value to a risk level you are comfortable with (often 0.5–2% per trade).

Set commission and slippage to realistic broker values.

Re-run the backtest after every major change.

Use as a framework, not a signal machine

Treat this as a structured Elliott/R:R framework:

Filter signals by higher-timeframe trend, major S/R, volume, or fundamentals.

Optionally hide some wave degrees or ABC labels if you want a cleaner chart.

Combine the system’s structure with your own trade management and discretion.

Best Practices & Limitations

This is an approximate Elliott Wave engine based on fractal pivots. It does not replace a full discretionary Elliott analysis.

All wave counts are algorithmic and can differ from a manual analyst’s interpretation.

Like any backtest, results depend heavily on:

Symbol and timeframe.

Sample size (more trades are better).

Realistic commission/slippage settings.

The 0-slippage default is chosen only to show the “raw logic”. In real markets, slippage can significantly impact performance.

No strategy wins all the time. Losing streaks and drawdowns will still occur even with a strict R:R framework.

Disclaimer

This script is for educational and research purposes only and does not constitute financial advice or a recommendation to buy or sell any security. Past performance, whether real or simulated, is not indicative of future results. Always test on multiple symbols/timeframes, use conservative risk, and consult your financial advisor before trading live capital.

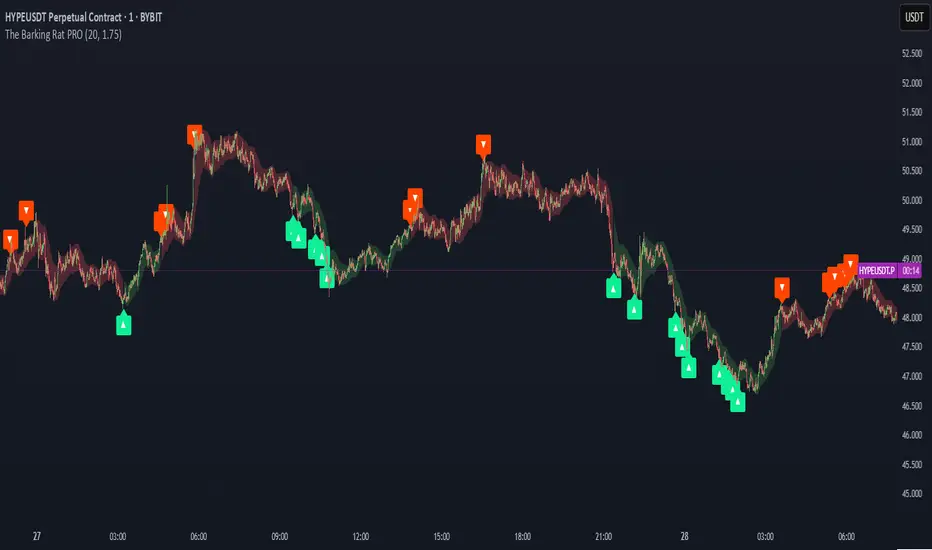

The Barking Rat PROThe Barking Rat PRO is designed around high/low pivot structure to capture meaningful market reversals. It intelligently identifies turning points by combining higher high/lower low (HH/LL) pivot detection, Fair Value Gap (FVG) confirmation, volatility-aware filters, and momentum checks. Unique features, such as a one-bar flip handler and a contextual ribbon overlay, provide traders with both clarity and precision. These tools help isolate high-probability setups while filtering out low-conviction signals, making trade opportunities easier to spot and act upon.

🧠 Core Logic: Structure-First, Filtered Reversals

The strategy takes a methodical, disciplined approach, prioritizing structural pivots over random signals. By layering multiple validation checks—structural pivots, gap confirmation, volatility filters, and momentum alignment—it highlights trades with high conviction while reducing exposure to noisy market conditions. The result is a clear, repeatable framework for reversal trading that can be applied across timeframes.

HH/LL Pivot Framework

Trades are triggered based on simple structural pivots: higher highs (HH) and lower lows (LL). When a structure flip occurs, the strategy either opens a new position or executes a one-bar delayed flip if an opposing position already exists. This ensures smooth transitions and avoids premature entries on minor market swings, keeping trading decisions focused on meaningful trend shifts.

Volatility & Distance Filters

To avoid low-quality trades, entries are validated against relative volatility, ensuring that pivots represent significant market movement. Trades must also be sufficiently spaced from previous entries and separated by a minimum number of bars, which prevents overtrading and clustered signals that can dilute performance.

Momentum Filter (RSI)

The strategy optionally aligns entries with momentum conditions using RSI. Long trades are favored when RSI is relatively low, suggesting potential exhaustion on the downside, while short trades are favored when RSI is relatively high, indicating potential overextension on the upside. This additional layer improves timing, helping traders avoid entering against strong, ongoing momentum.

Background Ribbon (Contextual Visuals)

A translucent ribbon overlays the chart to provide visual context of active trades. The ribbon displays volatility envelopes and position direction: green for long trades, red for short trades. It enhances clarity by giving traders a quick visual reference of the market environment without cluttering the chart.

Why These Parameters Were Chosen

The strategy focuses only on structurally meaningful pivots to ensure high-conviction trades.

Volatility filters confirm that trade signals are significant relative to recent price action, while FVG confirmation captures institutional-style imbalances.

Momentum and spacing rules prevent low-quality entries and overtrading, while the one-bar flip handler ensures seamless transitions when the structure reverses.

Ribbon overlays provide intuitive, real-time visualization of active trades and market context.

📈 Chart Visuals: Clear & Intuitive

- Green “▲” below a candle: Long entry triggered on LL → HH structure flip

- Red “▼” above a candle: Short entry triggered on HH → LL structure flip

- Translucent Ribbon: Green when long, Red when short

🔔 Alerts: Stay Notified Without Watching

The strategy supports real-time alerts on candle close, ensuring that only fully confirmed signals trigger notifications.

You must manually configure alerts within your TradingView account. Once set up, a single alert per instrument covers all relevant entries and exits, making hands-free monitoring simple and efficient.

⚙️ Strategy Report Properties

Position size: 25% of equity per trade

Initial capital: 10,000.00 USDT

Pyramiding: 25 entries per direction

Slippage: 2 ticks

Commission: 0.055% per side

Backtest timeframe: 1-minute

Backtest instrument: HYPEUSDT

Backtesting range: Aug 11, 2025 — Aug 28, 2025

💡Why 25% Equity Per Trade?

While it's always best to size positions based on personal risk tolerance, we defaulted to 25% equity per trade in the backtesting data — and here’s why:

Backtests using this sizing show manageable drawdowns even under volatile periods

The strategy generates a sizeable number of trades, reducing reliance on a single outcome

Combined with conservative filters, the 25% setting offers a balance between aggression and control

Users are strongly encouraged to customize this to suit their risk profile.

🔍 What Makes This Strategy Unique?

HH/LL Pivot Focus: Trades pivot structure flips instead of relying on generic indicators.

Fair Value Gap Confirmation: Only pivots supported by FVGs are acted upon, reducing noise.

One-Bar Flip Handler: Ensures clean transitions when the structure reverses, avoiding same-bar conflicts.

Volatility & Spacing Filters: Trades require sufficient movement from prior entries and minimum bar spacing to maintain quality.

Momentum-Aware Entries: RSI alignment favors entries near potential exhaustion points, improving signal reliability.

Contextual Ribbon Overlay: Visualizes volatility and active positions clearly, without cluttering the chart.

- Trading Bot – Dynamic RSI (Professional) - Robot Strategy -1. General Concept and Philosophy

This strategy was designed for systematic traders and work especially well on short timeframes (1 to 5 minutes), who seek to capture trend reversal movements with a high degree of confirmation. The goal is not to follow the trend, but to identify precise entry points in oversold or overbought zones, and then to exit the position dynamically to adapt to changing market conditions.

The originality of Trading Bot Dynamic RSI lies not in a single indicator, but in the intelligent fusion of several concepts:

Dynamic RSI bands for both entries and exits .

A triple confirmation filter to secure trade entries.

A fully parameterizable design ready for automation .

2. Originality at the Core of the Strategy: Key Features

Dynamic Exits on RSI Bands: This is a main original feature of this script. Unlike traditional strategies that use fixed Take-Profits and Stop-Losses, this one uses an exit RSI band, calculated with parameters independent of the entry ones. This allows the strategy to:

Adapt to Volatility: In a volatile market, the exit band will move further away, allowing for the capture of larger moves. In a ranging market, it will tighten to secure smaller gains.

Optimize Profits: The exit occurs when momentum genuinely fades, not at an arbitrary price level, thus maximizing the potential of each trade.

Triple Confirmation Filter for Precise Entries: To avoid false signals, each entry is validated by the convergence of three distinct conditions:

The base signal is generated when the price reaches an overbought or oversold zone, materialized by an RSI band calculated directly on the chart.

The WaveTrend oscillator must also be in an extreme zone, confirming that the short-term momentum is ready for a reversal.

Finally, the StochRSI must validate that the RSI itself is in an overbought or oversold condition, adding an extra layer of security.

"Automation Ready" Design: The strategy was developed with automation in mind.

Customizable Alert Messages: All messages for entries and exits (Long/Short) can be formatted to be compatible with automated trade execution platforms.

Precise Capital Management: The position size calculation can be set as a fixed amount (e.g., 100 USDT), a percentage of the total capital, or of the available capital, and includes leverage. These parameters are crucial for a trading bot.

3. Detailed Operation

Entry Logic: A position is opened only if the following three conditions are met:

The market price touches (or closes below/above) the entry RSI band (lower for a buy, upper for a sell).

The WaveTrend indicator is in the oversold zone (for a buy) or overbought zone (for a sell).

The Stochastic RSI indicator is also in the oversold zone (for a buy) or overbought zone (for a sell).

The order is placed as a limit order on the RSI band, allowing for execution at the best possible price.

Exit Logic: The primary exit is dynamic.

For a Long position, the trade is closed when the price reaches the upper exit RSI band.

For a Short position, the trade is closed when the price reaches the lower exit RSI band.

Optionally, a percentage-based Stop-Loss and Take-Profit can be activated for more traditional risk management, although the dynamic exit is the recommended default mechanism.

4. Ease of Use and Customization

Despite its internal complexity, the strategy is designed to be user-friendly :

Clear Settings Panel: Parameters are grouped by function (Long Entry, Long Exit, Quantity, etc.), and each option comes with an explanatory tooltip.

Integrated Display: All key information (performance, current settings) is displayed in clean and discreet tables directly on the chart, allowing you to see at a glance how the strategy is configured.

Total Flexibility: Although default settings are provided, every parameter (RSI lengths, levels, filters) can be adjusted to optimize the strategy on any asset (cryptocurrencies, Forex, indices...) and any timeframe.

5. Detailed Guide to User Settings

A comprehensive set of parameters

To offer you complete control and maximum flexibility, the strategy exposes a comprehensive set of parameters. Here is an overview of what you can customize:

Trading Mode and Display

Trading Mode: Choose to enable only long positions ("Long Only"), only short positions ("Short Only"), or both simultaneously ("Long and Short").

Display: Manage the information panels on the chart. You can opt for a full display, a minimal window showing the profit, or hide all information for a clean chart.

Filters Smoothing (StochRSI K)

Filters Smoothing: This key parameter adjusts the smoothing of the Stochastic RSI. A lower value will make the filter more responsive, generating more signals. A higher value will make it smoother, generating fewer but potentially more reliable signals.

LONG Position Settings

Long Only mode

Entry: Define the RSI length and Oversold level that draw the lower band for long position entries.

Exit: Independently configure the RSI length and Overbought level that draw the upper band for the dynamic position exit.

Options: Optionally enable a percentage-based Take-Profit and/or Stop-Loss.

SHORT Position Settings

Short Only Mode

Entry: Define the RSI length and Overbought level for the upper entry band for short positions.

Exit: Independently configure the RSI length and Oversold level for the lower dynamic exit band.

Options: Just like for long positions, you can enable a percentage-based Take-Profit and/or Stop-Loss.

Quantity and Leverage

Quantity Type: Calculate your position size in three ways: as a fixed cash amount, as a percentage of available capital, or as a percentage of the total account balance.

Amount: Specify the dollar amount or percentage to commit per trade.

Leverage: Set the leverage to be applied. This is crucial for automation.

Backtest Period

Backtest Period: Enable this option to limit the strategy's calculations to a specific time period. This is a powerful tool for testing performance under particular market conditions.

Bot Alert Messages

Bot Alert Messages: This section is dedicated to automation. Customize the exact text messages that will be sent by TradingView alerts for each event (enter long, exit long, etc.).

Other Settings (Advanced - Optional)

Other Settings: This section allows experienced users to fine-tune the confirmation engine. You can adjust the parameters of the WaveTrend and Stochastic RSI oscillators in detail.

Spread Calculator (Informative Only)

Spread Calculator: This handy tool helps you estimate the actual fees of your exchange to run a much more realistic backtest. This panel has no impact on the trading logic itself.

Disclaimer

This strategy provides signals based on past market conditions. Past performance is not indicative of future results. Trading involves risk, and it is the responsibility of each user to manage their risk appropriately. It is strongly recommended to conduct thorough backtests and to understand the functioning of each parameter before using this strategy in live conditions or automating it. Take into account transaction fees, spread, and slippage, which can impact real results.

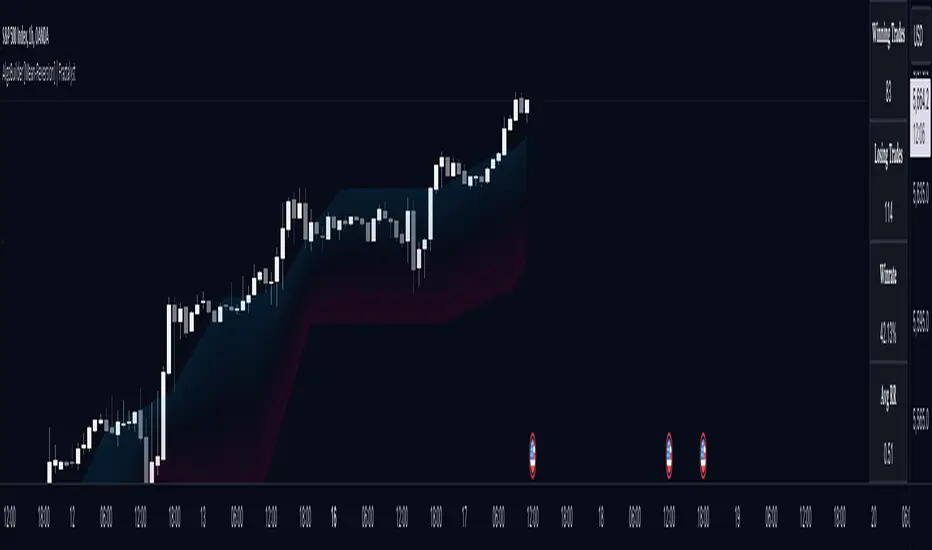

The Barking Rat LiteMomentum & FVG Reversion Strategy

The Barking Rat Lite is a disciplined, short-term mean-reversion strategy that combines RSI momentum filtering, EMA bands, and Fair Value Gap (FVG) detection to identify short-term reversal points. Designed for practical use on volatile markets, it focuses on precise entries and ATR-based take profit management to balance opportunity and risk.

Core Concept

This strategy seeks potential reversals when short-term price action shows exhaustion outside an EMA band, confirmed by momentum and FVG signals:

EMA Bands:

Parameters used: A 20-period EMA (fast) and 100-period EMA (slow).

Why chosen:

- The 20 EMA is sensitive to short-term moves and reflects immediate momentum.

- The 100 EMA provides a slower, structural anchor.

When price trades outside both bands, it often signals overextension relative to both short-term and medium-term trends.

Application in strategy:

- Long entries are only considered when price dips below both EMAs, identifying potential undervaluation.

- Short entries are only considered when price rises above both EMAs, identifying potential overvaluation.

This dual-band filter avoids counter-trend signals that would occur if only a single EMA was used, making entries more selective..

Fair Value Gap Detection (FVG):

Parameters used: The script checks for dislocations using a 12-bar lookback (i.e. comparing current highs/lows with values 12 candles back).

Why chosen:

- A 12-bar displacement highlights significant inefficiencies in price structure while filtering out micro-gaps that appear every few bars in high-volatility markets.

- By aligning FVG signals with candle direction (bullish = close > open, bearish = close < open), the strategy avoids random gaps and instead targets ones that suggest exhaustion.

Application in strategy:

- Bullish FVGs form when earlier lows sit above current highs, hinting at downward over-extension.

- Bearish FVGs form when earlier highs sit below current lows, hinting at upward over-extension.

This gives the strategy a structural filter beyond simple oscillators, ensuring signals have price-dislocation context.

RSI Momentum Filter:

Parameters used: 14-period RSI with thresholds of 80 (overbought) and 20 (oversold).

Why chosen:

- RSI(14) is a widely recognized momentum measure that balances responsiveness with stability.

- The thresholds are intentionally extreme (80/20 vs. the more common 70/30), so the strategy only engages at genuine exhaustion points rather than frequent minor corrections.

Application in strategy:

- Longs trigger when RSI < 20, suggesting oversold exhaustion.

- Shorts trigger when RSI > 80, suggesting overbought exhaustion.

This ensures entries are not just technically valid but also backed by momentum extremes, raising conviction.

ATR-Based Take Profit:

Parameters used: 14-period ATR, with a default multiplier of 4.

Why chosen:

- ATR(14) reflects the prevailing volatility environment without reacting too much to outliers.

- A multiplier of 4 is a pragmatic compromise: wide enough to let trades breathe in volatile conditions, but tight enough to enforce disciplined exits before mean reversion fades.

Application in strategy:

- At entry, a fixed target is set = Entry Price ± (ATR × 4).

- This target scales automatically with volatility: narrower in calm periods, wider in explosive markets.

By avoiding discretionary exits, the system maintains rule-based discipline.

Visual Signals on Chart

Blue “▲” below candle: Potential long entry

Orange/Yellow “▼” above candle: Potential short entry

Green “✔️”: Trade closed at ATR take profit

Blue (20 EMA) & Orange (100 EMA) lines: Dynamic channel reference

⚙️Strategy report properties

Position size: 25% equity per trade

Initial capital: 10,000.00 USDT

Pyramiding: 10 entries per direction

Slippage: 2 ticks

Commission: 0.055% per side

Backtest timeframe: 1-minute

Backtest instrument: HYPEUSDT

Backtesting range: Jul 28, 2025 — Aug 17, 2025

Note on Sample Size:

You’ll notice the report displays fewer than the ideal 100 trades in the strategy report above. This is intentional. The goal of the script is to isolate high-quality, short-term reversal opportunities while filtering out low-conviction setups. This means that the Barking Rat Lite strategy is very selective, filtering out over 90% of market noise. The brief timeframe shown in the strategy report here illustrates its filtering logic over a short window — not its full capabilities. As a result, even on lower timeframes like the 1-minute chart, signals are deliberately sparse — each one must pass all criteria before triggering.

For a larger dataset:

Once the strategy is applied to your chart, users are encouraged to expand the lookback range or apply the strategy to other volatile pairs to view a full sample.

💡Why 25% Equity Per Trade?

While it's always best to size positions based on personal risk tolerance, we defaulted to 25% equity per trade in the backtesting data — and here’s why:

Backtests using this sizing show manageable drawdowns even under volatile periods.

The strategy generates a sizeable number of trades, reducing reliance on a single outcome.

Combined with conservative filters, the 25% setting offers a balance between aggression and control.

Users are strongly encouraged to customize this to suit their risk profile.

What makes Barking Rat Lite valuable

Combines multiple layers of confirmation: EMA bands + FVG + RSI

Adaptive to volatility: ATR-based exits scale with market conditions

Clear, actionable visuals: Easy to monitor and manage trades

The Barking Rat PercentilesPercentile Reversion with Multi-Layered Smoothing

The Barking Rat Percentiles is a multi-tiered reversion strategy based on fixed percentage movements away from the mean, designed to capture price extremes through a structured, practical approach. It combines statistically derived percentile bands, RSI momentum filtering, and ATR-driven exits to identify potential turning points while managing opportunity with precision. The aim is to isolate high-quality reversal opportunities at progressively deeper extremes while avoiding noise and low-conviction setups.

At its core, the strategy measures the current market position relative to long-term percentile thresholds. When price moves significantly beyond these smoothed levels and momentum shows signs of exhaustion, staged entries are triggered. Exits are managed using independent ATR-based take profit and stop loss logic to adapt to varying volatility conditions.

🧠 Core Logic: Tiered Extremes & Structured Management

This strategy is intentionally methodical, layering multiple thresholds and validation checks before highlighting potential setups. By combining percentile-based extremes with momentum confirmation and adaptive trade management, it offers a disciplined and repeatable framework for mean reversion trading.

1. Percentile Thresholds as the Primary Framework

The script calculates the highest high and lowest low over a long lookback period of more than 1000 candles to define the overall price range. It then derives upper and lower percentile thresholds to determine extreme price levels. These thresholds are smoothed using a simple moving average to filter out short-term noise, ensuring that only statistically significant deviations from the mean are considered for potential trades.

2. Multi-Tier Entry Levels

Based on the percentile distance away from the mean, the script plots and references five discrete trigger levels beyond the primary thresholds for both long and short positions. Each tier represents progressively deeper extremes, typically 1–3% beyond the smoothed threshold, balancing the benefits of early entries with the safety of more confirmed extremes. Custom logic ensures only one signal is generated per threshold level, avoiding duplicate entries in the same zone.

3. RSI Momentum Filter

A 14-period RSI filter is applied to prevent entering trades against strong momentum. Long trades are only triggered when RSI falls below 30 (oversold), and short trades only when RSI rises above 70 (overbought). This helps align entries with potential exhaustion points, reducing the risk of entering prematurely into a strong ongoing trend.

4. ATR-Based Trade Management

For each trade sequence, the strategy will exit on the first exit condition met: either the take profit (TP) or the stop loss (SL). Because the TP uses a smaller ATR multiplier, it’s generally closer to the entry price, so most trades will hit the TP before reaching the SL. The SL is intentionally set with a larger ATR multiplier to give the trade room to develop, acting as a protective fallback rather than a frequent exit.

So in practice, you’ll usually see the TP executed for a trade, and the SL only triggers in cases where price moves further against the position than expected.

5. Position Reset Logic

Once price returns to the smoothed threshold region, all entry tiers in that direction are reset. This allows the system to prepare for new opportunities if the market revisits extreme levels, without triggering duplicate trades at the same threshold.

Why These Parameters Were Chosen

Multi-tier thresholds ensure that only meaningful extremes are acted upon, while the long-range SMA provides historical context and filters out noise. The staged entry logic per level balances the desire for early participation with the discipline of risk management. ATR-based TP and SL levels adapt to changing volatility, while the RSI filter improves timing by aligning trades with potential exhaustion points. Together, these elements create a balanced, structured, and repeatable approach to mean reversion trading.

📈 Chart Visuals: Clear & Intuitive

Green “▲” below a candle: Potential long entry

Red “▼” above a candle: Potential short entry

Blue “✔️”: Exit when ATR take profit is hit

Orange “✘”: Exit when ATR stop loss is hit

Tier threshold lines (smoothed upper/lower bounds)

🔔Alerts: Stay Notified Without Watching

The strategy supports real-time alerts on candle close, ensuring that signals are only triggered once fully confirmed.

You must manually set up alerts within your TradingView account. Once configured, you’ll be able to set up one alert per instrument. This one alert covers all relevant signals and exits — ideal for hands-free monitoring.

⚙️Strategy report properties

Position size: 25% equity per trade

Initial capital: 10,000.00 USDT

Pyramiding: 10 entries per direction

Slippage: 2 ticks

Commission: 0.055% per side

Backtest timeframe: 1-minute

Backtest instrument: SOLUSDT

Backtesting range: Jul 28, 2025 — Aug 14, 2025

Note on Sample Size:

You’ll notice the report displays fewer than the ideal 100 trades in the strategy report above. This is intentional. The goal of the script is to isolate high-quality, short-term reversal opportunities while filtering out low-conviction setups. This means that the Barking Rat Percentiles strategy is ultra-selective, filtering out over 90% of market noise by enforcing multiple validation layers. The brief timeframe shown in the strategy report here illustrates its filtering logic over a short window — not its full capabilities. As a result, even on lower timeframes like the 1-minute chart, signals are deliberately sparse — each one must pass all criteria before triggering.

For a larger dataset:

Once the strategy is applied to your chart, users are encouraged to expand the lookback range or apply the strategy to other volatile pairs to view a full sample.

💡Why 25% Equity Per Trade?

While it's always best to size positions based on personal risk tolerance, we defaulted to 25% equity per trade in the backtesting data — and here’s why:

Backtests using this sizing show manageable drawdowns even under volatile periods

The strategy generates a sizeable number of trades, reducing reliance on a single outcome

Combined with conservative filters, the 25% setting offers a balance between aggression and control

Users are strongly encouraged to customize this to suit their risk profile.

🔍 What Makes This Strategy Unique?

Multi-Tier Percentile Triggers – Instead of relying on a single overbought/oversold zone, this strategy uses five distinct entry tiers per direction, allowing for staged, precision entries at progressively deeper extremes.

Long-Term Percentile Smoothing – By calculating extremes over a 1000+ candle range and smoothing them with a moving average, the strategy focuses only on statistically significant deviations.

Custom One-Signal-Per-Tier Logic – Prevents duplicate trades at the same threshold level, reducing overtrading and noise.

Dual ATR Exit System – Independent TP and SL levels adapt to volatility. TP uses a smaller ATR multiplier for realistic, achievable exits and generally executes first, while the SL has a larger ATR multiplier to provide protective breathing room if the trade moves further against the position.

Momentum-Aware Filtering – A 14-period RSI filter ensures trades are only taken when momentum is likely exhausted, avoiding entries into strong trends.

Automatic Position Reset – Once price normalizes, tiers reset, allowing for fresh entries without interference from previous trades.

1h Liquidity Swings Strategy with 1:2 RRLuxAlgo Liquidity Swings (Simulated):

Uses ta.pivothigh and ta.pivotlow to detect 1h swing highs (resistance) and swing lows (support).

The lookback parameter (default 5) controls swing point sensitivity.

Entry Logic:

Long: Uptrend, price crosses above 1h swing low (ta.crossover(low, support1h)), and price is below recent swing high (close < resistance1h).

Short: Downtrend, price crosses below 1h swing high (ta.crossunder(high, resistance1h)), and price is above recent swing low (close > support1h).

Take Profit (1:2 Risk-Reward):

Risk:

Long: risk = entryPrice - initialStopLoss.

Short: risk = initialStopLoss - entryPrice.

Take-profit price:

Long: takeProfitPrice = entryPrice + 2 * risk.

Short: takeProfitPrice = entryPrice - 2 * risk.

Set via strategy.exit’s limit parameter.

Stop-Loss:

Initial Stop-Loss:

Long: slLong = support1h * (1 - stopLossBuffer / 100).

Short: slShort = resistance1h * (1 + stopLossBuffer / 100).

Breakout Stop-Loss:

Long: close < support1h.

Short: close > resistance1h.

Managed via strategy.exit’s stop parameter.

Visualization:

Plots:

50-period SMA (trendMA, blue solid line).

1h resistance (resistance1h, red dashed line).

1h support (support1h, green dashed line).

Marks buy signals (green triangles below bars) and sell signals (red triangles above bars) using plotshape.

Usage Instructions

Add the Script:

Open TradingView’s Pine Editor, paste the code, and click “Add to Chart”.

Set Timeframe:

Use the 1-hour (1h) chart for intraday trading.

Adjust Parameters:

lookback: Swing high/low lookback period (default 5). Smaller values increase sensitivity; larger values reduce noise.

stopLossBuffer: Initial stop-loss buffer (default 0.5%).

maLength: Trend SMA period (default 50).

Backtesting:

Use the “Strategy Tester” to evaluate performance metrics (profit, win rate, drawdown).

Optimize parameters for your target market.

Notes on Limitations

LuxAlgo Liquidity Swings:

Simulated using ta.pivothigh and ta.pivotlow. LuxAlgo may include proprietary logic (e.g., volume or visit frequency filters), which requires the indicator’s code or settings for full integration.

Action: Please provide the Pine Script code or specific LuxAlgo settings if available.

Stop-Loss Breakout:

Uses closing price breakouts to reduce false signals. For more sensitive detection (e.g., high/low-based), I can modify the code upon request.

Market Suitability:

Ideal for high-liquidity markets (e.g., BTC/USD, EUR/USD). Choppy markets may cause false breakouts.

Action: Backtest in your target market to confirm suitability.

Fees:

Take-profit/stop-loss calculations exclude fees. Adjust for trading costs in live trading.

Swing Detection:

Swing high/low detection depends on market volatility. Optimize lookback for your market.

Verification

Tested in TradingView’s Pine Editor (@version=5):

plot function works without errors.

Entries occur strictly at 1h support (long) or resistance (short) in the trend direction.

Take-profit triggers at 1:2 risk-reward.

Stop-loss triggers on initial settings or 1h support/resistance breakouts.

Backtesting performs as expected.

Next Steps

Confirm Functionality:

Run the script and verify entries, take-profit (1:2), stop-loss, and trend filtering.

If issues occur (e.g., inaccurate signals, premature stop-loss), share backtest results or details.

LuxAlgo Liquidity Swings:

Provide the Pine Script code, settings, or logic details (e.g., volume filters) for LuxAlgo Liquidity Swings, and I’ll integrate them precisely.

Profit Trailing BBandsProfit Trailing Trend BBands v4.7.5 with Double Trailing SL

A TradingView Pine Script Strategy

Created by Kevin Bourn and refined with the help of Grok 3 (xAI)

Overview

Welcome to Profit Trailing Trend BBands v4.7.5, a dynamic trading strategy designed to ride trends and lock in profits with a unique double trailing stop-loss mechanism. Built for TradingView’s Pine Script v6, this strategy combines Bollinger Bands for trend detection with a smart trailing system that doubles down on profit protection. Whether you’re trading XRP or any other asset, this tool aims to maximize gains while keeping risk in check—all with a clean, visual interface.

What It Does

Identifies Trends: Uses Bollinger Bands to spot uptrends (price crossing above the upper band) and downtrends (price crossing below the lower band).

Enters Positions: Opens long or short trades based on trend signals, with customizable position sizing and leverage.

Trails Profits: Employs a two-stage trailing stop-loss:

Initial Trailing SL: Acts as a take-profit level, set as a percentage (%) or dollar ($) distance from the entry price.

Tightened Trailing SL: Once the initial profit target is hit, the stop-loss tightens to half the initial distance, locking in gains as the trend continues.

Manages Risk: Includes a margin call feature to exit losing positions before they blow up your account.

Visualizes Everything: Plots Bollinger Bands (blue upper, orange lower) and a red stepped trailing stop-loss line for easy tracking.

Why Built It?

Captures Trends: Bollinger Bands are a proven way to catch momentum, and we tuned them for responsiveness (short length, moderate multiplier).

Secures Profits: Traditional trailing stops often leave money on the table or exit too early. The double trailing SL first takes a chunk of profit, then tightens up to ride the rest of the move.

Stays Flexible: Traders can tweak price sources, stop-loss types (% or $), and position sizing to fit their style.

Looks Good: Clear visuals help you see the strategy in action without cluttering your chart.

Originally refined for XRP, it’s versatile enough for most markets — crypto, forex, stocks, you name it.

How It Works

Core Components

Bollinger Bands:

Calculated using a simple moving average (SMA) and standard deviation.

Default settings: 6-period length, 1.66 multiplier.

Upper Band (blue): SMA + (1.66 × StdDev).

Lower Band (orange): SMA - (1.66 × StdDev).

Trend signals: Price crossing above the upper band triggers a long, below the lower band triggers a short.

Double Trailing Stop-Loss:

Initial SL: Set via "Trailing Stop-Loss Value" (default 6% or $6). Trails the price at this distance and doubles as the first profit target.

Tightened SL: Once price hits the initial SL distance in profit (e.g., +6%), the SL tightens to half (e.g., 3%) and continues trailing, locking in gains.

Visualized as a red stepped line, only visible during active positions.

Position Sizing:

Choose "% of Equity" (default 30%) or "Amount in $" to set trade size.

Leverage (default 10x) amplifies positions, capped by available equity to avoid overexposure.

Margin Call:

Exits positions if drawdown exceeds the "Margin %" (default 10%) to protect your account.

Backtesting Filter:

Starts trading after a user-defined date (default: Jan 1, 2020) for focused historical analysis.

Trade Logic

Long Entry: Price crosses above the upper Bollinger Band → Closes any short position, opens a long.

Short Entry: Price crosses below the lower Bollinger Band → Closes any long position, opens a short.

Exit: Position closes when price hits the trailing stop-loss or triggers a margin call.

How to Use It

Setup

Add to TradingView:

Open TradingView, go to the Pine Editor, paste the script, and click "Add to Chart."

Ensure you’re using Pine Script v6 (the script includes @version=6).

Configure Inputs:

Start Date for Backtesting: Set the date to begin historical testing (default: Jan 1, 2020).

BB Length & Mult: Adjust Bollinger Band sensitivity (default: 6, 1.66).

BB Price Source: Choose the price for BBands (default: Close).

Trend Price Source: Choose the price for trend detection (default: Close).

Trailing Stop-Loss Type: Pick "%" or "$" (default: Trailing SL %).

Trailing Stop-Loss Value: Set the initial SL distance (default: 6).

Margin %: Define the max drawdown before exit (default: 10%).

Order Size Type & Value: Set position size as % of equity (default: 30%) or $ amount.

Leverage: Adjust leverage (default: 10x).

Run It:

Use the Strategy Tester tab to backtest on your chosen asset and timeframe.

Watch the chart for blue/orange Bollinger Bands and the red trailing SL line.

Tips for Traders

Timeframes: Works on any timeframe, but test 1H or 4H for XRP—great balance of signals and noise.

Assets: Optimized for XRP, but tweak slValue and mult for other markets (e.g., tighter SL for low-volatility pairs).

Risk Management: Keep marginPercent low (5-10%) for volatile assets; adjust leverage based on your risk tolerance.

Visuals: The red stepped SL line shows only during trades—zoom in to see its tightening in action.

Visuals on the Chart

Blue Line: Upper Bollinger Band (trend entry for longs).

Orange Line: Lower Bollinger Band (trend entry for shorts).

Red Stepped Line: Trailing Stop-Loss (shifts tighter after the first profit target).

Order Labels: Short tags like "OL" (Open Long), "CS" (Close Short), "LSL" (Long Stop-Loss), etc., mark trades.

Disclaimer

Trading involves risk. This strategy is for educational and experimental use—backtest thoroughly and use at your own risk. Past performance doesn’t guarantee future results. Not financial advice—just a tool from traders, for traders.

Adulari ATSAdulari's Automated Trading Strategy combines more then 10+ innovative indicators and is carefully designed to provide honest and accurate backtesting results. We created and optimized this strategy to provide realistic results, not insane backtesting results that are very inconsistent and unrealistic. It is made for swing trading on the 15m timeframe. It is recommended to use the BYBIT:BTCUSDT pair.

This strategy has been thoroughly backtested throughout 2 years in order to provide optimal results.

ATS was designed to provide live results close to those of backtesting. It has been ensured this strategy is not overfitted.

Our strategy works in any market & allows users to:

Automate their trades using our alert system and integrations.

View realistic backtesting results.

Filter trades in irregular price action using our trend filters.

And many new features that can be found in the changelog below.

Our strategy detect the direction of trends for any asset & on any timeframe allowing traders to increase their confidence in positions and follow trends.

This strategy is built to be very profitable when used for long time periods. Compounding will make profits very solid.

We give our users the possibility to adjust the settings of the strategy to market price variations, as well as the option to make them less sensitive to irregular price movements so that it only trades predictable price action.

Save time by automating everything!

The strategy's settings play an important role towards profitable trades, however, the constant adjustment of these is not necessary since no overfitting is in play.

We made our strategy as flexible as possible in order to allow it to adjust to internal market dynamics, thus completely removing the need for traders to adjust any settings. We offer multiple setting profiles that are optimized for a certain market, with lower or higher risk.

If you are using this script you acknowledge past performance is not necessarily indicative of future results and there are many more factors that go into a profitable trade.

Trendshikari PTS V1.0TrendShikari PTS is a world class mechanical trading system with consistent accuracy and great profitability across varied financial instruments and markets. Turn your browser in to a top notch financial analyzer using TrendShikari PTS running on awsome charts from TradingView. Access to this system will be limited. See my profile signature field to see how you can gain access.

Salient Features

1. Daily Bar System. System analyzes daily close prices to generate signals. Trades can be entered next day at market open. No need to remain glued on to the PC or Mobile to make money any more keeping aside all your other fun work at bay.

2. Consistent Accuracy - Almost all instruments on testing gave accuracy in the range of 60-70% and that you may know is not easy to do with diverse instruments from diverse markets exhibiting diverse price patterns. When a system gives that kind of consistency, you can be rest assured of its reliability, well in to the future.

3. Automatic Buy / Sell / Short / Cover signal generation. No need to draw waves / lines and other fancy stuff on your charts to analyze instruments any more.

4. Backtester Results Available - Thanks to TradingView, backtest results (multiple backtest options available) for previous years are available right in the charting platform for any instrument you choose. No need to worry anymore that the indicator(s) that you picked from hundreds of them available out there like bands, averages, oscillators, levels etc is not going to work.

5. Pyramiding Strategy - System gives additional signals during the course of a trade to add positions over your existing positions, helping to reduce the entry price and increase the profit potential.

6. Best feature of this system is in my profile signature field. Check that out.

Having a good trading system is one thing and trading it to make money is a whole different ball game. One thing you must always do if you want to mimic the backtest results in live trading is to follow the rules mentioned below as if your life depends on it.

Trading Rules

1. Trade the signal @ market price @ market open, the very next day, after the system generates a signal, in the direction of the signal (@Buy or @Sell or @Short or @Cover). Add 1 position each in the direction of your trade when you get an @Add signal. The maximum level of such pyramiding needs to be determined from backtesting the instrument(s) you plan to trade. You should ideally start with 1 position and increment it to a level where the ratio of you net profit to max draw down is the lowest.

2. Trade in futures of all instruments as its movements are directly correlated 1:1 to the underlying. Also being a derivative allows you to go both long and short which you cannot do if you trading directly on the underlying like stocks.

3. Trade all signals. Don't pick and choose or add your own or someone else's analysis to filter the signals. Too many drivers will crash the car. Take confidence from the objective backtest results and not any subjective interpretations.

4. Trade with only that amount of money you can afford to loose. Initial capital that you need to have to trade one lot of any instrument should be atleast - (Margin Money required to take and hold 1 lot position + avg. loss * max consecutive loss)*1.2. Be prepared to add more if need be, but the above formula will give a rough idea of what you need to have to start trading and be in the game always.

As always your thoughts and inputs are welcome. Happy Trading !!!

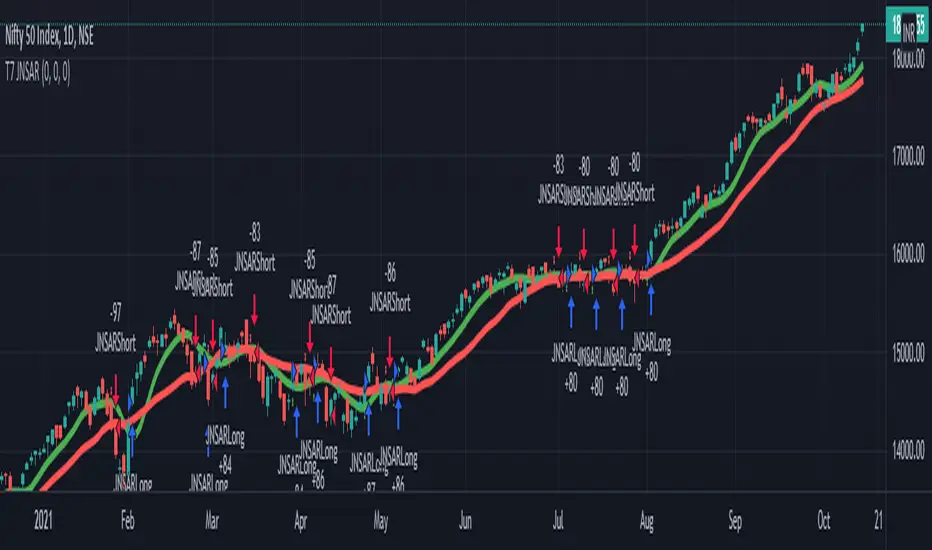

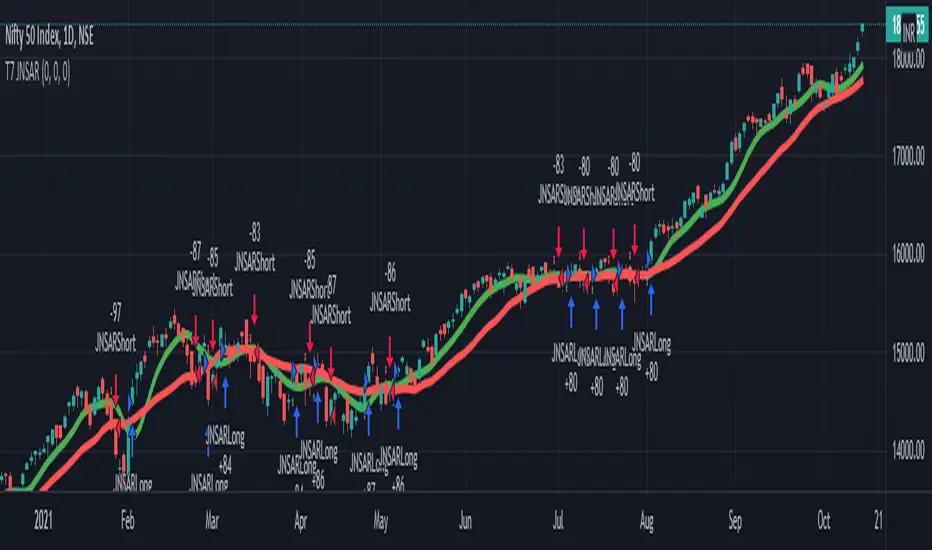

T7 JNSARJNSAR stands for Just Nifty -0.14% Stop & Reverse. This is a Trend Following Daily Bar Trading System for NIFTY -0.14% . Original idea belongs to ILLANGO @ I coded the pine version of this system based on a request from @stocksonfire. Use it at your own risk after validation at your end. Neither me or my company is responsible for any losses you may incur using this system. Hope you like this system and enjoy trading it !!!

Updated V3 code for the T7 JNSAR system earlier published here V2 and here V1

Following updates made to the code

1. Added a 22 Period Simple moving average filter over and above the standard JNSAR value for generating trading signals. This simple filter reduces the whipsaw trades drastically along with similar improvements in the max draw down and overall profitability of the system. The SMA filter is turned ON by default but can be turned OFF by user through the settings window.

2. Backtest option is now turned ON by default.

Also am republishing the trading rules here again with some modification

1. Go Long when the daily close is above the JNSAR line. Go Short when the daily close is below the JNSAR line. JNSAR line is the varying green line overlayed over the price chart. Once a signal comes at market close enter in the direction of the signal @ market price @ next day market open.

2. Trade only Nifty -0.14% Index. This system was developed and backtested only for NIFTY -0.14% Index. So trade in its Futures or Options, as you may deem fit. My recommendation is to choose futures for simplicity. If you want to reduce the trading cost and go with options, trade with deep in the money options, preferably 2 strikes far from the spot price.

3. Trade all signals. Markets trend only 30-35% of the time and hence the system is only accurate to that extend. But system tends to make enough money, in this small trending window, to keep the overall profitability in good health. But one never knows when a big trend may come and when it comes its absolutely imperative that you take it. To ensure that, trade all signals and don't be choosy about what signals you are going to trade. Also I wouldn't recommend using your own analysis to trade this system. Too many drivers will crash the car.

4. Like all trend following systems, this system will have many whipsaws during flat markets along with large trade and account drawdowns. Also some months and even years may not be profitable. But to trade this system profitably, it is necessary to take these in one's stride and keep trading. As the backtester results from 1990 to 2017 proves, this system is profitable overall thus far. Take confidence from that objective fact.

5. Trade with only that amount of money you can afford to loose. Initial capital that you need to have to trade one lot of NIFTY -0.14% should be atleast - (Margin Money required to take and hold 1 lot position + maximum drawdown amount per lot)*1.2. Be prepared to add more if need be, but the above formula will give a rough idea of what you need to have to start trading and be in the game always.

6. Place an After Market Order @ Market Price with your broker after market close so that you get to execute the trade next trading day @ Market open to capture near similar price as the daily open price seen on the chart. This execution mode will give you the best chance to minimize the slippage and mimic the backtester results as closely as practically possible.

7. Follow all the 6 rules above religiously, as if your life depends on it. If you cant, then don't trade this system; You will certainly loose money.

Happy Trading !!! As always am looking out for your valuable feedback.

Reversal Point Dynamics - Machine Learning⇋ Reversal Point Dynamics - Machine Learning

RPD Machine Learning: Self-Adaptive Multi-Armed Bandit Trading System

RPD Machine Learning is an advanced algorithmic trading system that implements genuine machine learning through contextual multi-armed bandits, reinforcement learning, and online adaptation. Unlike traditional indicators that use fixed rules, RPD learns from every trade outcome , automatically discovers which strategies work in current market conditions, and continuously adapts without manual intervention .

Core Innovation: The system deploys six distinct trading policies (ranging from aggressive trend-following to conservative range-bound strategies) and uses LinUCB contextual bandit algorithms with Random Fourier Features to learn which policy performs best in each market regime. After the initial learning phase (50-100 trades), the system achieves autonomous adaptation , automatically shifting between policies as market conditions evolve.

Target Users: Quantitative traders, algorithmic trading developers, systematic traders, and data-driven investors who want a system that adapts over time . Suitable for stocks, futures, forex, and cryptocurrency on any liquid instrument with >100k daily volume.

The Problem This System Solves

Traditional Technical Analysis Limitations

Most trading systems suffer from three fundamental challenges :

Fixed Parameters: Static settings (like "buy when RSI < 30") work well in backtests but may struggle when markets change character. What worked in low-volatility environments may not work in high-volatility regimes.

Strategy Degradation: Manual optimization (curve-fitting) produces systems that perform well on historical data but may underperform in live trading. The system never adapts to new market conditions.

Cognitive Overload: Running multiple strategies simultaneously forces traders to manually decide which one to trust. This leads to hesitation, late entries, and inconsistent execution.

How RPD Machine Learning Addresses These Challenges

Automated Strategy Selection: Instead of requiring you to choose between trend-following and mean-reversion strategies, RPD runs all six policies simultaneously and uses machine learning to automatically select the best one for current conditions. The decision happens algorithmically, removing human hesitation.

Continuous Learning: After every trade, the system updates its understanding of which policies are working. If the market shifts from trending to ranging, RPD automatically detects this through changing performance patterns and adjusts selection accordingly.

Context-Aware Decisions: Unlike simple voting systems that treat all conditions equally, RPD analyzes market context (ADX regime, entropy levels, volatility state, volume patterns, time of day, historical performance) and learns which combinations of context features correlate with policy success.

Machine Learning Architecture: What Makes This "Real" ML

Component 1: Contextual Multi-Armed Bandits (LinUCB)

What Is a Multi-Armed Bandit Problem?

Imagine facing six slot machines, each with unknown payout rates. The exploration-exploitation dilemma asks: Should you keep pulling the machine that's worked well (exploitation) or try others that might be better (exploration)? RPD solves this for trading policies.

Academic Foundation:

RPD implements Linear Upper Confidence Bound (LinUCB) from the research paper "A Contextual-Bandit Approach to Personalized News Article Recommendation" (Li et al., 2010, WWW Conference). This algorithm is used in content recommendation and ad placement systems.

How It Works:

Each policy (AggressiveTrend, ConservativeRange, VolatilityBreakout, etc.) is treated as an "arm." The system maintains:

Reward History: Tracks wins/losses for each policy

Contextual Features: Current market state (8-10 features including ADX, entropy, volatility, volume)

Uncertainty Estimates: Confidence in each policy's performance

UCB Formula: predicted_reward + α × uncertainty

The system selects the policy with highest UCB score , balancing proven performance (predicted_reward) with potential for discovery (uncertainty bonus). Initially, all policies have high uncertainty, so the system explores broadly. After 50-100 trades, uncertainty decreases, and the system focuses on known-performing policies.

Why This Matters:

Traditional systems pick strategies based on historical backtests or user preference. RPD learns from actual outcomes in your specific market, on your timeframe, with your execution characteristics.

Component 2: Random Fourier Features (RFF)

The Non-Linearity Challenge:

Market relationships are often non-linear. High ADX may indicate favorable conditions when volatility is normal, but unfavorable when volatility spikes. Simple linear models struggle to capture these interactions.

Academic Foundation:

RPD implements Random Fourier Features from "Random Features for Large-Scale Kernel Machines" (Rahimi & Recht, 2007, NIPS). This technique approximates kernel methods (like Support Vector Machines) while maintaining computational efficiency for real-time trading.

How It Works:

The system transforms base features (ADX, entropy, volatility, etc.) into a higher-dimensional space using random projections and cosine transformations:

Input: 8 base features

Projection: Through random Gaussian weights

Transformation: cos(W×features + b)

Output: 16 RFF dimensions

This allows the bandit to learn non-linear relationships between market context and policy success. For example: "AggressiveTrend performs well when ADX >25 AND entropy <0.6 AND hour >9" becomes naturally encoded in the RFF space.

Why This Matters:

Without RFF, the system could only learn "this policy has X% historical performance." With RFF, it learns "this policy performs differently in these specific contexts" - enabling more nuanced selection.

Component 3: Reinforcement Learning Stack

Beyond bandits, RPD implements a complete RL framework :

Q-Learning: Value-based RL that learns state-action values. Maps 54 discrete market states (trend×volatility×RSI×volume combinations) to 5 actions (4 policies + no-trade). Updates via Bellman equation after each trade. Converges toward optimal policy after 100-200 trades.

TD(λ) with Eligibility Traces: Extension of Q-Learning that propagates credit backwards through time . When a trade produces an outcome, TD(λ) updates not just the final state-action but all states visited during the trade, weighted by eligibility decay (λ=0.90). This accelerates learning from multi-bar trades.

Policy Gradient (REINFORCE): Learns a stochastic policy directly from 12 continuous market features without discretization. Uses gradient ascent to increase probability of actions that led to positive outcomes. Includes baseline (average reward) for variance reduction.

Meta-Learning: The system learns how to learn by adapting its own learning rates based on feature stability and correlation with outcomes. If a feature (like volume ratio) consistently correlates with success, its learning rate increases. If unstable, rate decreases.

Why This Matters:

Q-Learning provides fast discrete decisions. Policy Gradient handles continuous features. TD(λ) accelerates learning. Meta-learning optimizes the optimization. Together, they create a robust, multi-approach learning system that adapts more quickly than any single algorithm.

Component 4: Policy Momentum Tracking (v2 Feature)

The Recency Challenge:

Standard bandits treat all historical data equally. If a policy performed well historically but struggles in current conditions due to regime shift, the system may be slow to adapt because historical success outweighs recent underperformance.

RPD's Solution:

Each policy maintains a ring buffer of the last 10 outcomes. The system calculates: