Regression Fit Bollinger Bands [Spiritualhealer117]This indicator is best suited for mean reversion trading, shorting at the upper band and buying at the lower band, but it can be used in all the same ways as a standard bollinger band.

It differs from a normal bollinger band because it is centered around the linear regression line, as opposed to the moving average line, and uses the linear regression of the standard deviation as opposed to the standard deviation.

This script was an experiment with the new vertical gradient fill feature.

Search in scripts for "band"

EMA Bollinger Bands with customized std dev and moving averageTo use EMA with band you need to set input parameter named as "TypeOfMa" to 1.

If you set TypeOfMa = 1 then it will use EMA average for Bollinger bands.

If you set TypeOfMa = 0 then it will use MA average for Bollinger bands.

SymFlex Band - MAD, RSI Momentum, ATR Volatility"I wanted to design a hybrid band tool that adapts to different market conditions (volatility, momentum, trend) all in one."

"When the RSI band expands asymmetrically and the price closes outside it, this often signals a momentum climax or exhaustion zone."

"Ideal for traders looking to combine volatility breakout and mean reversion logic without switching indicators."

SymFlex Band is a flexible, multi-source band indicator that combines three dynamic metrics:

✅ MAD Band – Median Absolute Deviation-based range band

✅ RSI Momentum Band – Adaptive envelope using RSI deviation and trend bias

✅ ATR Band – Classic Average True Range-based volatility band

📌 Features

-Selectable band types (individually toggled)

-Configurable moving average for center line (EMA, SMA, TEMA, DEMA, Zero-lag variants)

-Dynamic distance and breakout tracking

-Automatic nearest band detection

-Real-time correlation table between bands

This tool helps identify price location relative to statistically adaptive bands, making it easier to detect breakout conditions, mean-reversion zones, and trend-following opportunities.

🚫 Note: This version is an indicator only. Strategy logic and entry triggers have been removed for publication clarity.

🔍 Use Case Suggestions:

Use MAD for range-dominant assets

Use RSI Band for momentum-driven setups

Use ATR when volatility-based positioning is key

Combine all three to get a full perspective of price behavior

Smoothed VWAP Bands🎯 Best Smoothing Setting for Scalping (What You Should Use)

Style σ Smoothing Result

Fast scalping (1min) EMA 14 Very responsive, still filters noise

Balanced intraday (1–5min) EMA 20 Best overall reliability

Slow confirmation (5–15min) EMA 30 Eliminates nearly all fakeouts

✅ What We Are Actually Smoothing

You are NOT smoothing VWAP itself.

You are smoothing the standard deviation (σ) that creates the VWAP bands:

✔ What this does:

* Computes the raw standard deviation (σ) of price relative to VWAP

* Smooths that σ using EMA smoothing

* Builds ±1 and ±2 bands using the smoothed σ

* You get clean, stable bands that filter fakeouts

✔ Result:

* Bands do NOT twitch in chop

* Fakeouts are filtered

* Real breakouts show obvious expansion

Outside the Bollinger Bands Alerting Indicator Overview

The Outside the Bollinger Bands Alerting Indicator is a comprehensive technical analysis tool that combines multiple proven

indicators into a single, powerful system designed to identify high-probability reversal patterns at Bollinger Band extremes. This

indicator goes beyond simple band touches to detect sophisticated pattern formations that often signal strong directional moves.

Key Features & Capabilities

🎯 Advanced Pattern Recognition

Bollinger Band Breakout Patterns

- Detects "pierce-and-reject" formations where price breaks through a Bollinger Band but immediately reverses back inside

- Identifies failed breakouts that often lead to strong moves in the opposite direction

- Combines multiple confirmation signals: engulfing candle patterns, MACD momentum, and ATR volatility filters

- Visual alerts with symbols positioned below (bullish) or above (bearish) candles

Tweezer Top & Bottom Patterns

- Identifies consecutive candles with nearly identical highs (tweezer tops) or lows (tweezer bottoms)

- Requires at least one candle to breach the respective Bollinger Band

- Confirms reversal with directional close requirements

- Customizable tolerance settings for pattern sensitivity

- Visual alerts with ❙❙ symbols for easy identification

📊 Multi-Indicator Integration

Bollinger Bands Indicator

- Dual-band configuration with outer (2.0 std dev) and inner (1.5 std dev) bands that can be adjusted to suit your own parameters

- Configurable MA types: SMA, EMA, SMMA (RMA), WMA, VWMA

- Customizable length, source, and offset parameters

- Color-coded band fills for visual clarity

Moving Average Suite

- EMA 9, 21, 50, and 200 (individually toggleable)

- Special "SMA 3 High" for help visualizing and detecting Bollinger Band break-outs

- Dynamic color coding based on price relationship

Optional Ichimoku Cloud overlay

- Complete Ichimoku implementation with customizable periods

- Dynamic cloud coloring based on trend direction

- Toggleable overlay that doesn't interfere with other indicators

🚨 Comprehensive Alert System

Real-Time JSON Alerts

- Sends structured data on every confirmed bar close

- Includes all indicator values: BB levels, EMAs, MACD, RSI

- Contains signal states and crossover conditions

- Perfect for automated trading systems and webhooks

{"timestamp":1753118700000,"symbol":"ETHUSD","timeframe":"5","price":3773.3,"bollinger_bands":{"upper":3826.95,"basis":3788.32,"lower":3749.68},"emas":{"ema_9":3780.45,"ema_21":3788.92,"ema_50":3800.79,"ema_200":3787.74,"sma_3_high":3789.45},"macd":{"macd":-10.1932,"signal":-11.3266,"histogram":1.1334},"rsi":{"rsi":40.5,"rsi_ma":39.32,"level":"neutral"}}

Specific Alert Conditions

- MACD histogram state changes (rising to falling, falling to rising)

- RSI overbought/oversold crossovers

- All pattern detections (BB Bounce, Tweezer patterns)

- Bollinger Band breakout alerts

🎨 Visual Elements

Pattern Identification

- ♻ symbols for Bollinger Band breakout patterns (green for bullish, red for bearish)

- ❙❙ symbols for tweezer patterns (green below for bottoms, red above for tops)

- Color-coded band fills for trend visualization

Chart Overlay Options

- All moving averages with distinct colors

- Bollinger Bands with inner and outer boundaries

- Optional Ichimoku cloud with trend-based coloring

Trading Applications

Reversal Trading

- Identify high-probability reversal points at extreme price levels

- Use failed breakout patterns for entry signals

- Combine multiple timeframes for enhanced accuracy

Trend Analysis

- Monitor moving average relationships for trend direction

- Use Ichimoku cloud for trend strength assessment

- Track momentum with MACD and RSI integration

Risk Management

- ATR-based volatility filtering reduces false signals

- Multiple confirmation requirements improve signal quality

- Real-time alerts enable prompt decision making

Suggested Use

- Use on multiple timeframes for confluence

- Combine with support/resistance levels for enhanced accuracy

- Set up alerts for hands-free monitoring

- Customize settings based on market volatility and trading style

- Consider volume confirmation for stronger signals

Volatility Zones (VStop + Bands) — Fixed (v2)📝 What this indicator is

This script is called “Volatility Zones (VStop + Bands)”.

It is an ATR-based volatility indicator that combines dynamic volatility bands, a Volatility Stop line (VStop), and volatility spike detection into a single tool.

Unlike moving average–based indicators, this tool does not rely on averages of price direction. Instead, it measures the market’s true volatility and reacts to expansions or contractions in price ranges.

________________________________________

⚙️ How it is built

The indicator uses several volatility-based components:

1. Average True Range (ATR)

o ATR is calculated over a user-defined length.

o It measures how much price typically moves in a given number of bars, making it the foundation of this indicator.

2. Volatility Bands

o Upper band = close + ATR × factor

o Lower band = close - ATR × factor

o The area between them is shaded.

o This gives traders an immediate visual sense of market volatility width — wide bands = high volatility, narrow bands = quiet market.

3. Volatility Stop (VStop)

o A stateful trailing stop based on ATR.

o It tracks the highest (or lowest) price in the current trend and places a stop offset by ATR × multiplier.

o When price crosses this stop, the indicator flips trend direction.

o This creates a dynamic stop-and-reverse mechanism that adapts to volatility.

4. Trend Zones

o When the trend is bullish, the stop is green and the chart background is shaded softly green.

o When bearish, the stop is red and the background is shaded softly red.

o This makes the market’s directional bias visually clear at all times.

5. Flip Signals (Buy/Sell Arrows)

o Whenever the VStop flips, arrows appear:

Green BUY arrows below price when the trend turns bullish.

Red SELL arrows above price when the trend turns bearish.

o These are also tied to built-in alerts for automation.

6. Volatility Spike Detection

o The script compares current ATR to its recent average.

o If ATR suddenly expands above a threshold, a small yellow “VOL” marker appears at the top of the chart.

o This highlights potential breakout phases or unusual volatility events.

7. Stop Labels

o At every trend flip, a small label appears at the bar, showing the exact stop level.

o This makes it easy to use the stop as a reference for risk management.

________________________________________

📊 How it works in practice

• When price is above the VStop line, the market is considered in an uptrend.

• When price is below the VStop line, the market is in a downtrend.

• The bands expand/contract with volatility, helping traders gauge risk and position sizing.

• Flip arrows signal when trend direction changes.

• Volatility spikes warn traders that the market is entering a higher-risk phase, often before strong moves.

________________________________________

🎯 How it may help traders

• Trend following → Helps traders identify whether the market is trending up or down.

• Stop placement → Provides a dynamic stop level that adjusts to volatility.

• Volatility awareness → Shaded bands and spike markers show when the market is likely to become unstable.

• Trade timing → Flip arrows and labels help identify potential entry or exit points.

• Risk management → Wide bands indicate higher risk; narrow bands suggest safer, tighter ranges.

________________________________________

🌍 In what markets it is useful

Because the indicator is based purely on volatility, it works across all asset classes and timeframes:

• Stocks & ETFs → Helps identify breakouts and long-term trends.

• Forex → Very useful in spot FX where volatility shifts frequently.

• Crypto → ATR reacts strongly to high volatility, helping traders adapt stops dynamically.

• Futures & Commodities → Great for tracking trending commodities and managing risk.

Scalpers, swing traders, and position traders can all benefit by adjusting the ATR length and multipliers to suit their trading style.

________________________________________

💡 Originality of this script

This is not just a mashup of existing indicators. It integrates:

• ATR-based Volatility Bands for context,

• A stateful Volatility Stop (adapted and rewritten cleanly),

• Flip arrows and labels for actionable trading signals,

• Volatility spike detection to highlight regime shifts.

The result is a comprehensive volatility-aware trading tool that goes beyond just plotting ATR or trend stops.

________________________________________

🔔 Alerts

• Buy Flip → triggers when the trend changes bullish.

• Sell Flip → triggers when the trend changes bearish.

Traders can connect these alerts to automated strategies, bots, or notification systems.

Rolling Volatility BandsMake sure to view it from the 1D candlestick chart.

The Rolling Volatility Bands indicator provides a statistically-driven approach to visualizing expected daily price movements using true volatility calculations employed by professional options traders. Unlike traditional Bollinger Bands which use price standard deviation around a moving average, this indicator calculates actual daily volatility from log returns over customizable rolling periods (20-day and 60-day), then annualizes the volatility using the standard √252 formula before projecting forward-looking probability bands. The 1 Standard Deviation bands represent a ~68% probability zone where price is expected to trade the following day, while the 2 Standard Deviation bands capture ~95% of expected movements. This methodology mirrors how major exchanges calculate expected moves for earnings and FOMC events, making it invaluable for options strategies like iron condors during low-volatility periods (narrow bands) or directional plays when volatility expands. The indicator works on any timeframe while always utilizing daily candle data via security() calls, ensuring consistent volatility calculations regardless of your chart resolution, and includes real-time annualized volatility percentages plus daily expected range statistics for comprehensive market analysis.

Official USD Staggered Bands - ArgentinaOfficial USD Staggered Bands - Argentina

The Central Bank, under the administration of Javier Milei (La Libertad Avanza), announced on Friday, April 11, 2025, a series of measures to eliminate the so-called "exchange rate restriction."

In this new phase, the dollar's exchange rate on the Free Exchange Market (MLC) will be able to fluctuate within a band between $1,000 and $1,400 , the limits of which will be expanded at a rate of 1% monthly.

The lines evolve daily, increasing as the public administration predicts. This way, you can know the likelihood of a Central Bank intervention to correct the variation and return the peso to a price within the band.

The script runs under the ticker USDARS

AI Breakout Bands (Zeiierman)█ Overview

AI Breakout Bands (Zeiierman) is an adaptive trend and breakout detection system that combines Kalman filtering with advanced K-Nearest Neighbor (KNN) smoothing. The result is a smart, self-adjusting band structure that adapts to dynamic market behavior, identifying breakout conditions with precision and visual clarity.

At its core, this indicator estimates price behavior using a two-dimensional Kalman filter (position + velocity), then enhances the smoothing process with a nonlinear, similarity-based KNN filter. This unique blend enables it to handle noisy markets and directional shifts with both speed and stability — providing breakout traders and trend followers a reliable framework to act on.

Whether you're identifying volatility expansions, capturing trend continuations, or spotting early breakout conditions, AI Breakout Bands gives you a mathematically grounded, visually adaptive roadmap of real-time market structure.

█ How It Works

⚪ Kalman Filter Engine

The Kalman filter models price movement as a state system with two components:

Position (price)

Velocity (trend direction)

It recursively updates predictions using real-time price as a noisy observation, balancing responsiveness with smoothness.

Process Noise (Position) controls sensitivity to sudden moves.

Process Noise (Velocity) controls smoothing of directional flow.

Measurement Noise (R) defines how much the filter "trusts" live price data.

This component alone creates a responsive yet stable estimate of the market’s center of gravity.

⚪ Advanced K-Neighbor Smoothing

After the Kalman estimate is computed, the script applies a custom K-Nearest Neighbor (KNN) smoother.

Rather than averaging raw values, this method:

Finds K most similar past Kalman values

Weighs them by similarity (inverse of absolute distance)

Produces a smoother that emphasizes structural similarity

This nonlinear approach gives the indicator an AI feature — reacting fast when needed, yet staying calm in consolidation.

█ How to Use

⚪ Trend Recognition

The line color shifts dynamically based on slope direction and breakout confirmation.

Bullish conditions: price above the mid band with positive slope

Bearish conditions: price below the mid band with negative slope

⚪ Breakout Signals

Price breaking above or below the bands may signal momentum acceleration.

Combine with your own volume or momentum confirmation for stronger entries.

Bands adapt to market noise, helping filter out low-quality whipsaws.

█ Settings

Process Noise (Position): Controls Kalman filter’s sensitivity to price changes.

Process Noise (Velocity): Controls smoothing of directional component.

Measurement Noise (R): Defines how much trust is placed in price data.

K-Neighbor Length: Number of historical Kalman values considered for smoothing.

Slope Calculation Window: Number of bars used to compute trend slope of the smoothed Kalman.

Band Lookback (MAE): Rolling period for average absolute error.

Band Multiplier: Multiplies MAE to determine band width.

-----------------

Disclaimer

The content provided in my scripts, indicators, ideas, algorithms, and systems is for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or a solicitation to buy or sell any financial instruments. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

Smooth Fibonacci BandsSmooth Fibonacci Bands

This indicator overlays adaptive Fibonacci bands on your chart, creating dynamic support and resistance zones based on price volatility. It combines a simple moving average with ATR-based Fibonacci levels to generate multiple bands that expand and contract with market conditions.

## Features

- Creates three pairs of upper and lower Fibonacci bands

- Smoothing option for cleaner, less noisy bands

- Fully customizable colors and line thickness

- Adapts automatically to changing market volatility

## Settings

Adjust the SMA and ATR lengths to match your trading timeframe. For short-term trading, try lower values; for longer-term analysis, use higher values. The Fibonacci factors determine how far each band extends from the center line - standard Fibonacci ratios (1.618, 2.618, and 4.236) are provided as defaults.

## Trading Applications

- Use band crossovers as potential entry and exit signals

- Look for price bouncing off bands as reversal opportunities

- Watch for price breaking through multiple bands as strong trend confirmation

- Identify potential support/resistance zones for placing stop losses or take profits

Fibonacci Bands combines the reliability of moving averages with the adaptability of ATR and the natural market harmony of Fibonacci ratios, offering a robust framework for both trend and range analysis.

Dynamic RSI Regression Bands (Zeiierman)█ Overview

The Dynamic RSI Regression Bands (Zeiierman) is a regression channel tool that dynamically resets based on RSI overbought and oversold conditions. It adapts to trend shifts in real time, creating a highly responsive regression framework that visualizes market sentiment and directional momentum with every RSI-triggered event.

Unlike static regression models, this indicator recalibrates its slope and deviation bands only after the RSI crosses predefined thresholds, helping traders pinpoint new phases of momentum, exhaustion, or reversal.

You’re not just measuring the trend — you’re tracking when and where the trend deserves to be re-evaluated.

█ The Assumption:

"A major momentum shift (RSI crossing OB/OS) signals a potential regime change, and thus, the trend model should be recalibrated from that point."

Instead of using a fixed-length regression (which assumes trend relevance over a static window), this script resets the regression calculation every time RSI crosses into extreme territory. The underlying idea is that extreme RSI levels often represent emotional peaks in market behavior and are statistically likely to be followed by a new price structure.

█ How It Works

⚪ RSI-Based Channel Reset

RSI is monitored continuously

If RSI crosses above the Overbought level, the indicator resets and starts a new regression channel

If RSI crosses below the Oversold level, the same reset logic applies

These events act as “anchor points” for dynamic trend analysis

⚪ Regression Channel Logic

A custom linear regression is calculated from the RSI reset point forward

The lookback grows with each bar after the reset, up to a user-defined max

Regression lines are drawn from the reset point to the current bar

⚪ Standard Deviation Bands

Upper and lower bands are plotted around the regression line using the standard deviation

These serve as dynamic volatility envelopes, great for spotting breakouts or reversals

⚪ Rejection Markers

If price hits the upper/lower band and then closes back inside it, a rejection marker is plotted

Helps visualize failed breakouts and areas of absorption or reversal pressure

█ How to Use

⚪ Detect Trend Shifts

Use the RSI resets to identify when the trend might be starting fresh.

⚪ Watch the Bands for Volatility Extremes

Use the outer bands as soft areas of potential reversal or momentum breakout.

⚪ Spot Rejections for Potential Entry Signals

If price moves outside a band but then quickly returns inside, it often means the breakout failed, and price may reverse.

█ Settings Explained

RSI Length – How many bars RSI uses. Shorter = faster.

OB / OS Levels – Crossing these triggers a regression reset.

Base Regression Length – Max number of bars regression can use post-reset.

StdDev Multiplier – Controls band width from the regression line.

Min Bars After Reset – Ensures channel doesn’t form immediately; waits for structure.

Show Reset Markers – Triangles mark where RSI crossed OB/OS.

Show Rejection Markers – Circles mark where the price rejected the channel edge.

-----------------

Disclaimer

The content provided in my scripts, indicators, ideas, algorithms, and systems is for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or a solicitation to buy or sell any financial instruments. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

Dynamic Momentum Bands | AlphaAlgosDynamic Momentum Bands | AlphaAlgos

Overview

The Dynamic Momentum Bands indicator is an advanced technical analysis tool that combines multiple analytical techniques to provide a comprehensive view of market momentum and trend dynamics. By integrating RSI (Relative Strength Index), volatility analysis, and adaptive moving averages, this indicator offers traders a nuanced perspective on market conditions.

Key Features

Adaptive band calculation based on price momentum

Integrated RSI-driven volatility scaling

Multiple moving average type options (EMA, SMA, VWMA)

Smooth, gradient-based band visualization

Optional price bar coloring for trend identification

Technical Methodology

The indicator employs a sophisticated approach to market analysis:

1. Momentum Calculation

Calculates RSI using a customizable length

Uses RSI to dynamically adjust band volatility

Scales band width based on distance from the 50 RSI level

2. Band Construction

Applies a selected moving average type to the price source

Calculates deviation using ATR (Average True Range)

Smooths band edges for improved visual clarity

Configuration Options

Core Settings:

Price Source: Choose the price data used for calculations

RSI Length: Customize the RSI calculation period (1-50)

Band Length: Adjust the moving average period (5-100)

Volatility Multiplier: Fine-tune band width

Band Type: Select between EMA, SMA, and VWMA

Visual Settings:

Bar Coloring: Toggle color-coded price bars

Gradient-based band visualization

Smooth color transitions for trend representation

Trend Identification

The indicator provides trend insights through:

Color-coded bands (blue for bullish, pink for bearish)

Smooth gradient visualization

Optional price bar coloring

Trading Applications

Trend Following:

- Use band position relative to price as trend indicator

- Identify momentum shifts through color changes

- Utilize gradient zones for trend strength assessment

Volatility Analysis:

Observe band width changes

Detect potential breakout or consolidation periods

Use RSI-driven volatility scaling for market context

Best Practices

Adjust RSI length to match trading timeframe

Experiment with different moving average types

Use in conjunction with other technical indicators

Consider volatility multiplier for different market conditions

This indicator is provided for informational purposes only. Always use proper risk management when trading. Past performance is not indicative of future results. Not financial Advise

Accurate Bollinger Bands mcbw_ [True Volatility Distribution]The Bollinger Bands have become a very important technical tool for discretionary and algorithmic traders alike over the last decades. It was designed to give traders an edge on the markets by setting probabilistic values to different levels of volatility. However, some of the assumptions that go into its calculations make it unusable for traders who want to get a correct understanding of the volatility that the bands are trying to be used for. Let's go through what the Bollinger Bands are said to show, how their calculations work, the problems in the calculations, and how the current indicator I am presenting today fixes these.

--> If you just want to know how the settings work then skip straight to the end or click on the little (i) symbol next to the values in the indicator settings window when its on your chart <--

--------------------------- What Are Bollinger Bands ---------------------------

The Bollinger Bands were formed in the 1980's, a time when many retail traders interacted with their symbols via physically printed charts and computer memory for personal computer memory was measured in Kb (about a factor of 1 million smaller than today). Bollinger Bands are designed to help a trader or algorithm see the likelihood of price expanding outside of its typical range, the further the lines are from the current price implies the less often they will get hit. With a hands on understanding many strategies use these levels for designated levels of breakout trades or to assist in defining price ranges.

--------------------------- How Bollinger Bands Work ---------------------------

The calculations that go into Bollinger Bands are rather simple. There is a moving average that centers the indicator and an equidistant top band and bottom band are drawn at a fixed width away. The moving average is just a typical moving average (or common variant) that tracks the price action, while the distance to the top and bottom bands is a direct function of recent price volatility. The way that the distance to the bands is calculated is inspired by formulas from statistics. The standard deviation is taken from the candles that go into the moving average and then this is multiplied by a user defined value to set the bands position, I will call this value 'the multiple'. When discussing Bollinger Bands, that trading community at large normally discusses 'the multiple' as a multiplier of the standard deviation as it applies to a normal distribution (gaußian probability). On a normal distribution the number of standard deviations away (which trades directly use as 'the multiple') you are directly corresponds to how likely/unlikely something is to happen:

1 standard deviation equals 68.3%, meaning that the price should stay inside the 1 standard deviation 68.3% of the time and be outside of it 31.7% of the time;

2 standard deviation equals 95.5%, meaning that the price should stay inside the 2 standard deviation 95.5% of the time and be outside of it 4.5% of the time;

3 standard deviation equals 99.7%, meaning that the price should stay inside the 3 standard deviation 99.7% of the time and be outside of it 0.3% of the time.

Therefore when traders set 'the multiple' to 2, they interpret this as meaning that price will not reach there 95.5% of the time.

---------------- The Problem With The Math of Bollinger Bands ----------------

In and of themselves the Bollinger Bands are a great tool, but they have become misconstrued with some incorrect sense of statistical meaning, when they should really just be taken at face value without any further interpretation or implication.

In order to explain this it is going to get a bit technical so I will give a little math background and try to simplify things. First let's review some statistics topics (distributions, percentiles, standard deviations) and then with that understanding explore the incorrect logic of how Bollinger Bands have been interpreted/employed.

---------------- Quick Stats Review ----------------

.

(If you are comfortable with statistics feel free to skip ahead to the next section)

.

-------- I: Probability distributions --------

When you have a lot of data it is helpful to see how many times different results appear in your dataset. To visualize this people use "histograms", which just shows how many times each element appears in the dataset by stacking each of the same elements on top of each other to form a graph. You may be familiar with the bell curve (also called the "normal distribution", which we will be calling it by). The normal distribution histogram looks like a big hump around zero and then drops off super quickly the further you get from it. This shape (the bell curve) is very nice because it has a lot of very nifty mathematical properties and seems to show up in nature all the time. Since it pops up in so many places, society has developed many different shortcuts related to it that speed up all kinds of calculations, including the shortcut that 1 standard deviation = 68.3%, 2 standard deviations = 95.5%, and 3 standard deviations = 99.7% (these only apply to the normal distribution). Despite how handy the normal distribution is and all the shortcuts we have for it are, and how much it shows up in the natural world, there is nothing that forces your specific dataset to look like it. In fact, your data can actually have any possible shape. As we will explore later, economic and financial datasets *rarely* follow the normal distribution.

-------- II: Percentiles --------

After you have made the histogram of your dataset you have built the "probability distribution" of your own dataset that is specific to all the data you have collected. There is a whole complicated framework for how to accurately calculate percentiles but we will dramatically simplify it for our use. The 'percentile' in our case is just the number of data points we are away from the "middle" of the data set (normally just 0). Lets say I took the difference of the daily close of a symbol for the last two weeks, green candles would be positive and red would be negative. In this example my dataset of day by day closing price difference is:

week 1:

week 2:

sorting all of these value into a single dataset I have:

I can separate the positive and negative returns and explore their distributions separately:

negative return distribution =

positive return distribution =

Taking the 25th% percentile of these would just be taking the value that is 25% towards the end of the end of these returns. Or akin the 100%th percentile would just be taking the vale that is 100% at the end of those:

negative return distribution (50%) = -5

positive return distribution (50%) = +4

negative return distribution (100%) = -10

positive return distribution (100%) = +20

Or instead of separating the positive and negative returns we can also look at all of the differences in the daily close as just pure price movement and not account for the direction, in this case we would pool all of the data together by ignoring the negative signs of the negative reruns

combined return distribution =

In this case the 50%th and 100%th percentile of the combined return distribution would be:

combined return distribution (50%) = 4

combined return distribution (100%) = 10

Sometimes taking the positive and negative distributions separately is better than pooling them into a combined distribution for some purposes. Other times the combined distribution is better.

Most financial data has very different distributions for negative returns and positive returns. This is encapsulated in sayings like "Price takes the stairs up and the elevator down".

-------- III: Standard Deviation --------

The formula for the standard deviation (refereed to here by its shorthand 'STDEV') can be intimidating, but going through each of its elements will illuminate what it does. The formula for STDEV is equal to:

square root ( (sum ) / N )

Going back the the dataset that you might have, the variables in the formula above are:

'mean' is the average of your entire dataset

'x' is just representative of a single point in your dataset (one point at a time)

'N' is the total number of things in your dataset.

Going back to the STDEV formula above we can see how each part of it works. Starting with the '(x - mean)' part. What this does is it takes every single point of the dataset and measure how far away it is from the mean of the entire dataset. Taking this value to the power of two: '(x - mean) ^ 2', means that points that are very far away from the dataset mean get 'penalized' twice as much. Points that are very close to the dataset mean are not impacted as much. In practice, this would mean that if your dataset had a bunch of values that were in a wide range but always stayed in that range, this value ('(x - mean) ^ 2') would end up being small. On the other hand, if your dataset was full of the exact same number, but had a couple outliers very far away, this would have a much larger value since the square par of '(x - mean) ^ 2' make them grow massive. Now including the sum part of 'sum ', this just adds up all the of the squared distanced from the dataset mean. Then this is divided by the number of values in the dataset ('N'), and then the square root of that value is taken.

There is nothing inherently special or definitive about the STDEV formula, it is just a tool with extremely widespread use and adoption. As we saw here, all the STDEV formula is really doing is measuring the intensity of the outliers.

--------------------------- Flaws of Bollinger Bands ---------------------------

The largest problem with Bollinger Bands is the assumption that price has a normal distribution. This is assumption is massively incorrect for many reasons that I will try to encapsulate into two points:

Price return do not follow a normal distribution, every single symbol on every single timeframe has is own unique distribution that is specific to only itself. Therefore all the tools, shortcuts, and ideas that we use for normal distributions do not apply to price returns, and since they do not apply here they should not be used. A more general approach is needed that allows each specific symbol on every specific timeframe to be treated uniquely.

The distributions of price returns on the positive and negative side are almost never the same. A more general approach is needed that allows positive and negative returns to be calculated separately.

In addition to the issues of the normal distribution assumption, the standard deviation formula (as shown above in the quick stats review) is essentially just a tame measurement of outliers (a more aggressive form of outlier measurement might be taking the differences to the power of 3 rather than 2). Despite this being a bit of a philosophical question, does the measurement of outlier intensity as defined by the STDEV formula really measure what we want to know as traders when we're experiencing volatility? Or would adjustments to that formula better reflect what we *experience* as volatility when we are actively trading? This is an open ended question that I will leave here, but I wanted to pose this question because it is a key part of what how the Bollinger Bands work that we all assume as a given.

Circling back on the normal distribution assumption, the standard deviation formula used in the calculation of the bands only encompasses the deviation of the candles that go into the moving average and have no knowledge of the historical price action. Therefore the level of the bands may not really reflect how the price action behaves over a longer period of time.

------------ Delivering Factually Accurate Data That Traders Need------------

In light of the problems identified above, this indicator fixes all of these issue and delivers statistically correct information that discretionary and algorithmic traders can use, with truly accurate probabilities. It takes the price action of the last 2,000 candles and builds a huge dataset of distributions that you can directly select your percentiles from. It also allows you to have the positive and negative distributions calculated separately, or if you would like, you can pool all of them together in a combined distribution. In addition to this, there is a wide selection of moving averages directly available in the indicator to choose from.

Hedge funds, quant shops, algo prop firms, and advanced mechanical groups all employ the true return distributions in their work. Now you have access to the same type of data with this indicator, wherein it's doing all the lifting for you.

------------------------------ Indicator Settings ------------------------------

.

---- Moving average ----

Select the type of moving average you would like and its length

---- Bands ----

The percentiles that you enter here will be pulled directly from the return distribution of the last 2,000 candles. With the typical Bollinger Bands, traders would select 2 standard deviations and incorrectly think that the levels it highlights are the 95.5% levels. Now, if you want the true 95.5% level, you can just enter 95.5 into the percentile value here. Each of the three available bands takes the true percentile you enter here.

---- Separate Positive & Negative Distributions----

If this box is checked the positive and negative distributions are treated indecently, completely separate from each other. You will see that the width of the top and bottom bands will be different for each of the percentiles you enter.

If this box is unchecked then all the negative and positive distributions are pooled together. You will notice that the width of the top and bottom bands will be the exact same.

---- Distribution Size ----

This is the number of candles that the price return is calculated over. EG: to collect the price return over the last 33 candles, the difference of price from now to 33 candles ago is calculated for the last 2,000 candles, to build a return distribution of 2000 points of price differences over 33 candles.

NEGATIVE NUMBERS(<0) == exact number of candles to include;

EG: setting this value to -20 will always collect volatility distributions of 20 candles

POSITIVE NUMBERS(>0) == number of candles to include as a multiple of the Moving Average Length value set above;

EG: if the Moving Average Length value is set to 22, setting this value to 2 will use the last 22*2 = 44 candles for the collection of volatility distributions

MORE candles being include will generally make the bands WIDER and their size will change SLOWER over time.

I wish you focus, dedication, and earnest success on your journey.

Happy trading :)

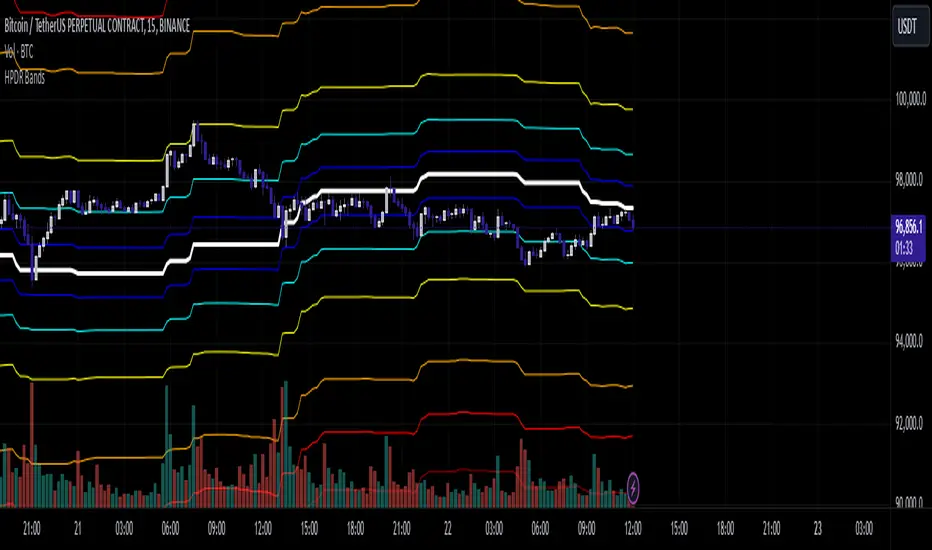

HPDR Bands IndicatorThe HPDR Bands indicator is a customizable tool designed to help traders visualize dynamic price action zones. By combining historical price ranges with adaptive bands, this script provides clear insights into potential support, resistance, and midline levels. The indicator is well-suited for all trading styles, including trend-following and range-bound strategies.

Features:

Dynamic Price Bands: Calculates price zones based on historical highs and lows, blending long-term and short-term price data for responsive adaptation to current market conditions.

Probability Enhancements: Includes a probability plot derived from the relative position of the closing price within the range, adjusted for volatility to highlight potential price movement scenarios.

Fibonacci-Like Levels: Highlights key levels (100%, 95%, 88%, 78%, 61%, 50%, and 38%) for intuitive visualization of price zones, aiding in identifying high-probability trading opportunities.

Midline Visualization: Displays a midline that serves as a reference for price mean reversion or breakout analysis.

How to Use:

Trending Markets: Use the adaptive upper and lower bands to gauge potential breakout or retracement zones.

Range-Bound Markets: Identify support and resistance levels within the defined price range.

Volatility Analysis: Observe the probability plot and its sensitivity to volatility for informed decision-making.

Important Notes:

This script is not intended as investment advice. It is a tool to assist with market analysis and should be used alongside proper risk management and other trading tools.

The script is provided as-is and without warranty. Users are encouraged to backtest and validate its suitability for their specific trading needs.

Happy Trading!

If you find this script helpful, consider sharing your feedback or suggestions for improvement. Collaboration strengthens the TradingView community, and your input is always appreciated!

Jurik Price Bands and Range Box [BigBeluga]Jurik Price Bands and Range Box

The Jurik Price Bands and Range Box - BigBeluga indicator is an advanced technical analysis tool that combines Jurik Moving Average (JMA) based price bands with a dynamic range box. This versatile indicator is designed to help traders identify trends, potential reversal points, and price ranges over a specified period.

🔵 KEY FEATURES

● Jurik Price Bands

Utilizes Jurik Moving Average for smoother, more responsive bands

//@function Calculates Jurik Moving Average

//@param src (float) Source series

//@param len (int) Length parameter

//@param ph (int) Phase parameter

//@returns (float) Jurik Moving Average value

jma(src, len, ph) =>

var float jma = na

var float e0 = 0.0

var float e1 = 0.0

var float e2 = 0.0

phaseRatio = ph < -100 ? 0.5 : ph > 100 ? 2.5 : ph / 100 + 1.5

beta = 0.45 * (len - 1) / (0.45 * (len - 1) + 2)

alpha = math.pow(beta, phaseRatio)

e0 := (1 - alpha) * src + alpha * nz(e0 )

e1 := (src - e0) * (1 - beta) + beta * nz(e1 )

e2 := (e0 + phaseRatio * e1 - nz(jma )) * math.pow(1 - alpha, 2) + math.pow(alpha, 2) * nz(e2 )

jma := e2 + nz(jma )

jma

Consists of an upper band, lower band, and a smooth price line

Bands adapt to market volatility using Jurik MA on ATR

Helps identify potential trend reversal points and overextended market conditions

● Dynamic Range Box

Displays a box representing the price range over a specified period

Calculates high, low, and mid-range prices

Option for adaptive mid-range calculation based on average price

Provides visual representation of recent price action and volatility

● Price Position Indicator

Shows current price position relative to the mid-range

Displays percentage difference from mid-range

Color-coded for quick trend identification

● Dashboard

Displays key information including current price, range high, mid, and low

Shows trend direction based on price position relative to mid-range

Provides at-a-glance market context

🔵 HOW TO USE

● Trend Identification

Use the middle of the Range Box as the primary trend reference point

Price above the middle of the Range Box indicates an uptrend

Price below the middle of the Range Box indicates a downtrend

The bar on the right shows the percentage distance of the close from the middle of the box

This percentage indicates both trend direction and strength

Refer to the dashboard for quick trend direction confirmation

● Potential Reversal Points

Upper and lower Jurik Bands can indicate potential trend reversal points

Price reaching or exceeding these bands may suggest overextended conditions

Watch for price reaction at these levels for possible trend shifts or pullbacks

Range Box high and low can serve as additional reference points for price action

● Range Analysis

Use Range Box to gauge recent price volatility and trading range

Mid-range line can act as a pivot point for short-term price movements

Percentage difference from mid-range helps quantify price position strength

🔵 CUSTOMIZATION

The Jurik Price Bands and Range Box indicator offers several customization options:

Adjust Range Box length for different timeframe analysis

Toggle between standard and adaptive mid-range calculation

Standard:

Adaptive:

Modify Jurik MA length and deviation for band calculation

Toggle visibility of Jurik Bands

By fine-tuning these settings, traders can adapt the indicator to various market conditions and personal trading strategies.

The Jurik Price Bands and Range Box indicator provides a multi-faceted approach to market analysis, combining trend identification, potential reversal point detection, and range analysis in one comprehensive tool. The use of Jurik Moving Average offers a smoother, more responsive alternative to traditional moving averages, potentially providing more accurate signals.

This indicator can be particularly useful for traders looking to understand market context quickly, identify potential reversal points, and assess current market volatility. The combination of dynamic bands, range analysis, and the informative dashboard provides traders with a rich set of data points to inform their trading decisions.

As with all technical indicators, it's recommended to use the Jurik Price Bands and Range Box in conjunction with other forms of analysis and within the context of a well-defined trading strategy. While this indicator provides valuable insights, it should be considered alongside other factors such as overall market conditions, volume, and fundamental analysis when making trading decisions.

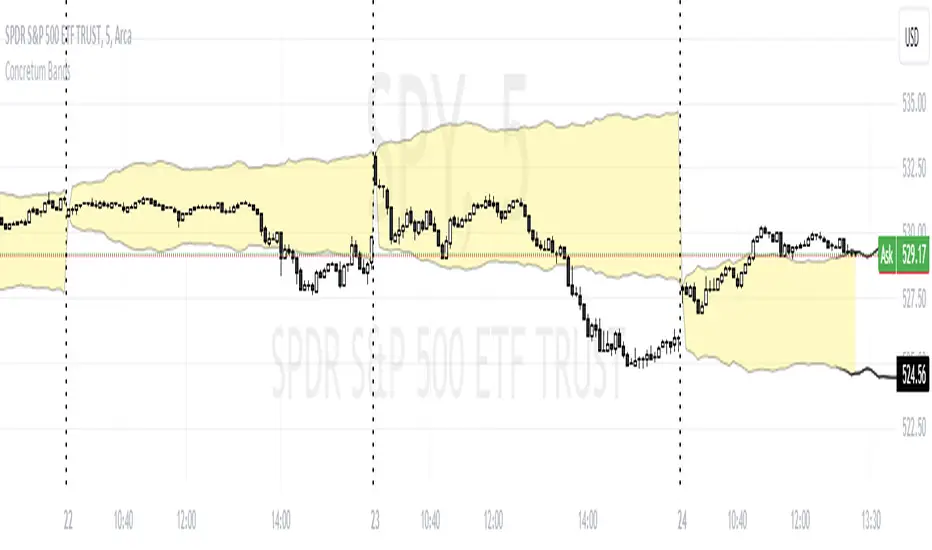

Concretum BandsDefinition

The Concretum Bands indicator recreates the Upper and Lower Bound of the Noise Area described in the paper "Beat the Market: An Effective Intraday Momentum Strategy for S&P500 ETF (SPY)" published by Concretum founder Zarattini, along with Barbon and Aziz, in May 2024.

Below we provide all the information required to understand how the indicator is calculated, the rationale behind it and how people can use it.

Idea Behind

The indicator aims to outline an intraday price region where the stock is expected to move without indicating any demand/supply imbalance. When the price crosses the boundaries of the Noise Area, it suggests a significant imbalance that may trigger an intraday trend.

How the Indicator is Calculated

The bands at time HH:MM are computed by taking the open price of day t and then adding/subtracting the average absolute move over the last n days from market open to minute HH:MM . The bands are also adjusted to account for overnight gaps. A volatility multiplier can be used to increase/decrease the width of the bands, similar to other well-known technical bands. The bands described in the paper were computed using a lookback period (length) of 14 days and a Volatility Multiplier of 1. Users can easily adjust these settings.

How to use the indicator

A trader may use this indicator to identify intraday moves that exceed the average move over the most recent period. A break outside the bands could be used as a signal of significant demand/supply imbalance.

Multi Time Frame Composite BandsMulti Time Frame Composite Bands utilizes Fibonacci numbers (5, 8, 13, 21, 34) as period lengths for calculations. The indicator calculates a composite high line (C_high) by averaging the highest prices over Fibonacci periods, incorporating moving averages (SMA) of high prices for added refinement and smoothing. Similarly, a composite low line (C_low) is calculated by averaging the lowest prices with moving averages of low prices. The midline, obtained from the mean of C_high and C_low.

This band can function as volatility bands unlike traditional volatility indicators like Bollinger Bands , ATR bands it does not use traditional measures of volatility such standard deviation , ATR. This hugs closely to the price and during trending markets the some part of the candles stay outside the band and when the entire candle digress outside the band a price correction or reversal can be anticipated. This can be considered as a smoothed Donchian channel.

TrueLevel BandsTrueLevel Bands is a powerful trading indicator that employs linear regression and standard deviation to create dynamic, envelope-style bands around the price action of a financial instrument. These bands are designed to help traders identify potential support and resistance levels, trend direction, and volatility.

The TrueLevel Bands indicator consists of multiple envelope bands, each constructed using different timeframes or lengths, and a multiple (mult) factor. The multiple factor determines the width of the bands by adjusting the number of standard deviations from the linear regression line.

Key Features of TrueLevel Bands

1. Multi-Timeframe Analysis: Unlike traditional moving average-based indicators, TrueLevel Bands allow traders to incorporate multiple timeframes into their analysis. This helps traders capture both short-term and long-term market dynamics, offering a more comprehensive understanding of price behavior.

2. Customization: The TrueLevel Bands indicator offers a high level of customization, allowing traders to adjust the lengths and multiple factors to suit their trading style and preferences. This flexibility enables traders to fine-tune the indicator to work optimally with various instruments and market conditions.

3. Adaptive Volatility: By incorporating standard deviation, TrueLevel Bands can automatically adjust to changing market volatility. This feature enables the bands to expand during periods of high volatility and contract during periods of low volatility, providing traders with a more accurate representation of market dynamics.

4. Dynamic Support and Resistance Levels: TrueLevel Bands can help traders identify dynamic support and resistance levels, as the bands adjust in real-time according to price action. This can be particularly useful for traders looking to enter or exit positions based on support and resistance levels.

5. The "Global Trend Line" refers to the average of the bands used to indicate the overall trend.

Why TrueLevel Bands are Different from Classic Moving Averages

TrueLevel Bands differ from conventional moving averages in several ways:

1. Linear Regression: While moving averages are based on simple arithmetic means, TrueLevel Bands use linear regression to determine the centerline. This offers a more accurate representation of the trend and helps traders better assess potential entry and exit points.

2. Envelope Style Bands: Unlike moving averages, which are single lines, TrueLevel Bands form envelope-style bands around the price action. This provides traders with a visual representation of potential support and resistance levels, trend direction, and volatility.

3. Multi-Timeframe Analysis: Classic moving averages typically focus on a single timeframe. In contrast, TrueLevel Bands incorporate multiple timeframes, enabling traders to capture a broader understanding of market dynamics.

4. Adaptive Volatility: Traditional moving averages do not account for changing market volatility, whereas TrueLevel Bands automatically adjust to volatility shifts through the use of standard deviation.

The TrueLevel Bands indicator is a powerful, versatile tool that offers traders a unique approach to technical analysis. With its ability to adapt to changing market conditions, provide multi-timeframe analysis, and dynamic support and resistance levels, TrueLevel Bands can serve as an invaluable asset to both novice and experienced traders looking to gain an edge in the markets.

Bollinger Band ribbonThis indicator plots 9 upper and lower lines with increasing length. Lines are 0.618 upper and lower level of Bollinger band.

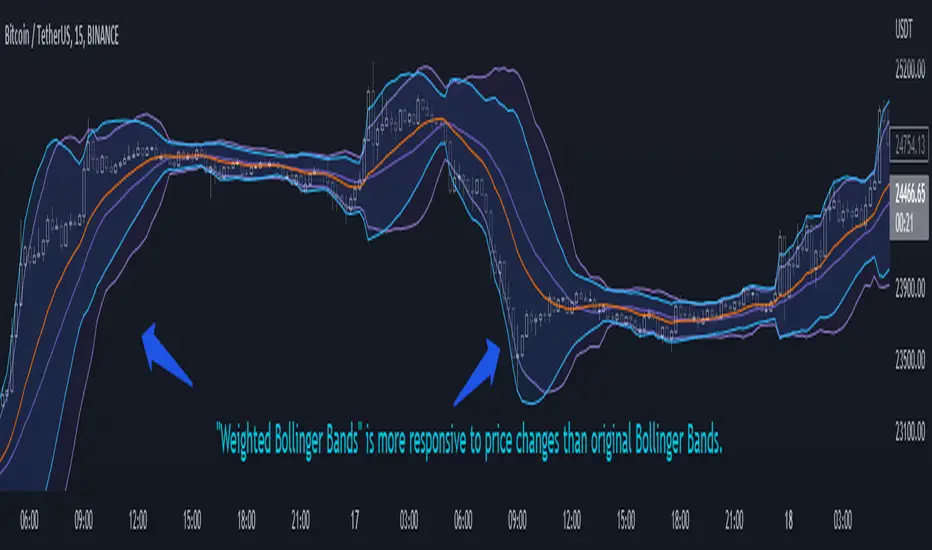

Weighted Bollinger Band (+ Logarithmic)ENG)

Weighted BB is more responsive to price changes than original Bollinger Bands.

the calculation formula uses a weighted method based on the current price.

Instead of using a standard deviation, I used a weighted standard deviation that weights the current price, and instead of a simple moving average, I used a weighted moving average.

Also included is a formula to log the Bollinger Bands for users who view charts on a logarithmic scale.

KOR)

원본 볼밴보다 가격변화에 대한 반응성이 높습니다.

계산식에는 현재가격에 가중을 주는 방식을 사용하였습니다.

표준편차를 사용하는 대신 저는 현재가격에 가중을 두는 가중표준편차를 사용하였고, 단순이동평균 대신 가중이동평균을 사용하였습니다.

또한 로그스케일로 차트를 보는 유저를 위해 볼린저밴드를 log화 하는 수식도 포함하였습니다.

Average Trend with Deviation BandsTL,DR: A trend indicator with deviation bands using a modified Donchian calculation

This indicator plots a trend using the average of the lowest and highest closing price and the lowest low and highest high of a given period. This is similar to Donchian channels which use an average of the lowest and highest value (of a given period). This might sound like a small change but imho it provides a better "average" when lows/highs and lowest/highest closing prices are considered in the average calculation as well.

I also added the option to show 2 deviation bands (one is deactivated by default but can be activated in the options menu). The deviation band uses the standard deviation (of the average trend) and can be used to determine if a price movement is still in a "normal" range or not. Based on my testing it is fine to use one band with a standard deviation of 1 but it is also possible to show a second band with a different deviation value if needed. The bands (and trendline) can also be used as dynamic support/resistance zones.

Trendline without deviation bands

Volume Weighted Hull Moving Average Bollinger Bands (VWHBB)Title: "Volume Weighted Hull Moving Average Bollinger Bands Indicator for TradingView"

Abstract: This script presents a TradingView indicator that displays Bollinger Bands based on the volume weighted Hull Moving Average (VEHMA) of a financial asset. The VEHMA is a technical analysis tool that combines the reduced lag of the Hull Moving Average (HMA) with volume weighting to provide a more sensitive indicator of market trends and dynamics. The Bollinger Bands are a volatility indicator that plot upper and lower bands around a moving average, which can help traders identify potential trend changes and overbought or oversold conditions. The script allows the user to customize the VEHMA length and Bollinger Band deviation parameters.

Introduction: Bollinger Bands are a popular technical analysis tool used to identify potential trend changes and overbought or oversold conditions in the market. They are constructed by plotting upper and lower bands around a moving average, with the width of the bands determined by the volatility of the asset. The VEHMA is a variant of the Hull Moving Average (HMA) that combines the reduced lag of the HMA with volume weighting to provide a more sensitive indicator of market trends and dynamics.

Methodology: The VEHMA is calculated using a weighted average of two exponential moving averages (EMAs), with the weighting based on the volume of the asset and the length of the moving average. The Bollinger Bands are calculated by plotting the VEHMA plus and minus a standard deviation of the asset's price over a specified period. The standard deviation is a measure of the volatility of the asset and helps to adjust the width of the bands based on market conditions.

Implementation: The script is implemented in TradingView's PineScript language and can be easily added to any chart on the platform. The user can customize the VEHMA length and Bollinger Band deviation parameters to suit their trading strategy. The VEHMA, Bollinger Bands, and fill colors are plotted on the chart to provide a visual representation of the indicator.

Conclusion: The VEHMA Bollinger Bands indicator is a useful tool for traders looking to identify potential trend changes and overbought or oversold conditions in the market. This script provides a convenient and customizable implementation of the indicator for use in TradingView.

Bollinger Bands Width and Bollinger Bands %BThis script shows both the Bollinger Band Width(BBW) and %B on the same indicator window.

Both the BBW and %B are introduced by John Bollinger(creator of Bollinger Bands) in 2010.

Default Parameter values: Length = 20, Source = Close, Mult = 2

Bollinger Bands Width (BBW): Color = (Default: Green )

- I consider stocks with "BBW >= 4" are at a volatile state and ready for price contraction, but this depends on the parameter values of your choice.

Bollinger Bands %B (%B): Color = (Default: Blue )

1. %B Above 10 = Price is Above the Upper Band

2. %B Equal to 10 = Price is at the Upper Band

3. %B Above 5 = Price is Above the Middle Line

4. %B Below 5 = Price is Below the Middle Line

5. %B Equal to 0 = Price is at the Lower Band

6. %B Below 0 = Price is Below the Lower Band