Prometheus Markov ChainThe Prometheus Markov Chain Indicator is a custom-built tool designed to predict potential future price movements using a Markov Chain approach. A Markov Chain is a statistical model that assumes the probability of moving to a future state depends solely on the current state. In this indicator, states represent price movement classifications—bullish, bearish, or neutral—and are determined based on historical price changes (percentage returns). The indicator builds a transition matrix to calculate probabilities of transitioning from one state to another, enabling traders to identify patterns and forecast likely price actions.

Core Functionality and Transition Matrix

The transition matrix is the backbone of the Markov Chain. It captures the frequency of transitions between states in the historical price data and normalizes these counts into probabilities. For example, if the price was in a bearish state and transitioned to a bullish state 3 out of 10 times, the probability of transitioning from bearish to bullish would be 0.3. The matrix is created dynamically using the stateFunc function to classify states, which can use either dynamic thresholds (highest and lowest returns over a lookback period) or a user-defined percent return threshold. Below is the snippet that updates the transition matrix:

transitionMatrix = matrix.new(dimension, dimension, 0.0)

for i = 0 to array.size(vec) - 2

fromState = array.get(vec, i)

toState = array.get(vec, i + 1)

transitionMatrix.set(fromState, toState, transitionMatrix.get(fromState, toState) + 1)

for i = 0 to dimension - 1

rowSum = 0.0

for j = 0 to dimension - 1

rowSum += transitionMatrix.get(i, j)

for j = 0 to dimension - 1

prob = transitionMatrix.get(i, j) / rowSum

transitionMatrix.set(i, j, prob)

This snippet iterates through historical price movements, counts state transitions, and then normalizes each row of the matrix so that the sum of probabilities for all possible transitions from a given state equals 1.

How the Indicator Predicts Future States

After constructing the transition matrix, the indicator calculates the current state of the price based on the latest percentage return and then uses the matrix to compute probabilities for transitioning to other states. The state with the highest probability is predicted as the next state, which is displayed on the chart using color-coded labels: green for bullish and red for bearish. The following snippet demonstrates how the current state and predictions are calculated:

current_chng = (close - close ) / close

var int current_state = na

if not use_custom_thresh

highest_chng = ta.highest(current_chng, int(size) * 2)

lowest_chng = ta.lowest(current_chng, int(size) * 2)

current_state := stateFunc(current_chng, highest_chng, lowest_chng)

else

current_state := stateFunc(current_chng, custom_thresh)

predicted_probs = array.new(dimension, 0.0)

for j = 0 to dimension - 1

array.set(predicted_probs, j, transitionMatrix.get(current_state, j))

The indicator evaluates which state has the highest transition probability (highest_prob) and places corresponding labels on the chart. For example, if the next state is predicted to be bullish, a green "Bullish" label is placed below the current bar. This predictive functionality helps traders anticipate potential reversals or continuations in price trends based on historical behavior patterns.

Usage:

Here we see the indicator at work on $PLTR. The states predicted are bullish then bearish. In this example we then see price move in a way that verifies those predictions.

On this 4 Hour NASDAQ:AMZN chart we see predictions play out in a short trade style. States quickly move from one to another but not without giving traders a way to take advantage.

This is the perspective we aim to provide. We encourage traders to not follow indicators blindly. No indicator is 100% accurate. This one can give you a different perspective market state. We encourage any comments about desired updates or criticism!

Search in scripts for "one一季度财报"

PSP Indicator [Elbaz]Precision Swing Point or PSP is a unique technical analysis tool designed to compare the price action of three tickers that are in sync.

It highlights moments when the price structure diverges between the markets, identifying ideal entry points for trades - We would like to enter a trade when we found PSP and one of the tickers took the wick while others didn't.

This strategy provides an edge by focusing on periods of desynchronization between the indices, where one index may be showing strength while another is lagging. The idea is to find the moments where the candle colors (bullish or bearish) differ across the markets, then wait for one of the tickers to "take" the wick of the PSP while other didn't and enter a trade.

Once a divergence is detected, the indicator plots an arrow on the chart, signaling a potential trade entry. To minimize risk, a good place to put stop loss will at the end of the wick of the PSP — the high or low wick of the candle where the divergence occurs.

The PSP Indicator allows for several custom inputs:

- Tickers: Customize the tickers to compare. The default values are S&P 500 E-mini, NASDAQ E-mini, and Dow Jones E-mini, if you trade Crypto you might want to use BTC, ETH, TOTAL3.

- Lookback Period: The lookback input defines how far back the indicator should evaluate to calculate the price structure point.

- Highlight Bar Times: Users can specify particular times during the trading day to highlight, such as the market open or significant news events. This helps traders focus on key trading windows.

Adaptive Linear Regression ChannelOverview

The Adaptive Linear Regression Channel Script is an advanced, multi-functional trading tool crafted to help traders pinpoint market trends, identify potential reversals, assess volatility, and establish dynamic levels for profit-taking and position exits. By incorporating key concepts such as linear regression , standard deviation , and other volatility measures like the ATR , the script offers a comprehensive view of market behavior beyond traditional deviation metrics.

This dynamic model continuously adapts to changing market conditions, adjusting in real-time to provide clear visualizations of trends, channels, and volatility levels. This adaptability makes the script invaluable for both trend-following and counter-trend strategies, giving traders the flexibility to respond effectively to different market environments.

Background

What is Linear Regression?

Definition : Linear regression is a statistical technique used to model the relationship between a dependent variable (target) and one or more independent variables (predictors).

In its simplest form (simple linear regression), the relationship between two variables is represented by a straight line (the regression line).

y = mx + b

where :

- y is the target variable (price)

- m is the slope

- x is the independent variable (time)

- b is the intercept

Slope of the Regression Line

Definition: The slope (m) measures the rate at which the dependent variable (y) changes as the independent variable (x) changes.

Interpretation:

- A positive slope indicates an uptrend.

- A negative slope indicates a downtrend.

Uses in Trading:

- Identifying the strength and direction of market trends.

- Assessing the momentum of price movements.

R-squared (Coefficient of Determination)

Definition: A measure of how well the regression line fits the data, ranging from 0 to 1.

Calculation :

R2 = 1− (SS tot/SS res)

where:

- SSres is the sum of squared residuals.

- SStot is the total sum of squares.

Interpretation:

- Higher R2 indicates a better fit, meaning the model explains a larger proportion of the variance in the data.

Uses in Trading:

- Higher R-squared values give traders confidence in trend-based signals.

- Low R-squared values may suggest that the market is more random or volatile.

Standard Deviation

Definition: Standard Deviation quantifies the dispersion of data points in a dataset relative to the mean. A low standard deviation indicates that data points tend to be close to the mean, while a high standard deviation indicates that the data points are spread out over a larger range of values.

Calculation

σ=√∑(xi−μ)2/N

Where

- σ is the standard deviation.

- ∑ is the summation symbol, indicating that the expression that follows should be summed over all data points.

- xi, this represents the i-th data point in the dataset.

- μ\mu, this represents the mean(average) of all the data points in the dataset.

- (xi−μ)2, this is the squared difference between each data point and the mean.

- N is the total number of data points in the dataset.

- **Interpretation**

- A higher standard deviation indicates greater volatility.

- Useful for identifying overbought/oversold conditions in markets.

Key Features

Dynamic Linear Regression Channels:

The script automatically generates adaptive regression channels that expand or contract based on the current market volatility. This real-time adjustment ensures that traders are always working with the most relevant data, making it easier to spot key support and resistance levels.

The channel width itself serves as an indicator of market volatility, expanding during periods of heightened uncertainty and contracting during more stable phases. Additionally, the channel width is trained on previous channel widths , allowing the script to adapt and provide a more accurate view of volatility trends of the asset. Traders can also customize the script to train on less historical data , enabling a more recent view of volatility , which is particularly useful in fast-moving or changing markets.

Dynamic Profits and Stops:

What is it?

Dynamic profit levels allow traders to adjust take-profit targets based on real-time market conditions. Unlike static levels, which remain fixed regardless of market changes, these adaptive levels leverage past volatility data to create more flexible profit-taking strategies.

How does it work?

The script determines these levels using previously stored deviation values. These deviations are categorized into quantiles (like Q1, Q2, Q3, etc.) to classify current market conditions. As new deviation data is recorded, the profit levels are adjusted dynamically to reflect changes in market volatility. This approach helps to refine profit targets, especially when using regression channels with standard deviation rather than traditional ATR bands.

Why is it valuable?

By utilizing adaptive profit levels, traders can optimize their exits based on the current volatility landscape. For instance, when volatility increases, the dynamic levels expand, allowing trades to capture larger price movements. Conversely, during low volatility, profit targets tighten to lock in gains sooner, reducing exposure to market reversals. This flexibility is especially beneficial when combined with adaptive regression channels that respond to changes in standard deviation.

Slope-Based Trend Analysis:

One of the core elements of this script is the slope of the regression line , which helps define the direction and strength of the trend. Positive slopes indicate bullish momentum, while negative slopes suggest bearish conditions. The slope's steepness gives traders insight into the market's momentum, allowing them to adjust their strategies based on the strength of the trend.

Additionally, the script uses the slope to create a color gradient , which visually represents the intensity of the market's momentum. The gradient peaks at one color to show the maximum bullish momentum experienced in the past, while another color represents the maximum bearish momentum experienced in the past. This color-coded visualization makes it easier for traders to quickly assess the market's strength and direction at a glance.

Volatility Heatmap:

The integrated heatmap provides an intuitive, color-coded visualization of market volatility. The heatmap highlights areas where price action is expanding or contracting, giving traders a clear view of where volatility is rising or falling. By mapping out deviations from the regression line, the heatmap makes it easier to spot periods of high volatility that could lead to major market moves or potential reversals.

Deviation Concepts:

The script tracks price deviations from the regression line when a new range is formed, providing valuable insights when the price significantly deviates from the expected trend. These deviations are key in identifying potential breakout points or trend shifts .

This helps traders understand when the market is overextended or when a pullback may be imminent, allowing them to make more informed trading decisions.

Adaptive Model Properties:

Unlike static indicators, this script adapts over time . As the market changes, it stores historical data related to channel widths , slope dynamics , and volatility levels , adjusting its analysis accordingly to stay relevant to current market conditions.

Traders have the ability to train the model on all available data or specify a set number of bars to focus on more recent market activity. This flexibility allows for more tailored analysis , ensuring that traders can work with data that best fits their trading style and time horizon.

This continuous learning approach ensures that traders always have the most up-to-date insight into the market's structure.

Table

The table displays key metrics in real time to provide deeper insights into market behavior:

1. Deviation & Slope : Shows the current deviation if set to standard deviation or atr if set to atr(values used to calculated the channel widths) and the trend slope, helping to gauge market volatility and trend direction.

2. Rate of Change : For both deviation/atr and slope, the table also calculates the rate of change of their rates—essentially capturing the acceleration or deceleration of trends and volatility. This helps identify shifts in market momentum early.

3. R-squared : Indicates the strength and reliability of the trend fit. A higher value means the regression line better explains the price movements.

4. Quantiles : Uses historical deviation data to categorize current market conditions into quartiles (e.g., Q1, Q2, Q3). This helps classify the market's current volatility level, allowing traders to adjust strategies dynamically.

By combining these metrics, the table offers a comprehensive, real-time snapshot of market conditions, enabling more informed and adaptive trading decisions.

Settings

Here’s a breakdown of the script's settings for easy reference:

Linear Regression Settings

Show Dynamic Levels :Toggle to display dynamic profit levels on the chart.

Deviation Type :Select the method for calculating deviation—options include ATR (Average True Range) or Standard Deviation.

Timeframe :Sets the specific timeframe for the regression analysis (default is the chart’s timeframe).

Period :Defines the number of bars used for calculating the regression line (e.g., 50 bars).

Deviation Multiplier :Multiplier used to adjust the width of the deviation channel around the regression line.

Rate of Change :Sets the period for calculating the rate of change of the slope (used for momentum analysis).

Max Bars Back :Limits the number of historical bars to analyze (0 means all available data).

Slope Lookback :Number of bars used to calculate the slope gradient for trend detection.

Slope Gradient Display :Toggle to enable gradient coloring based on slope direction.

Slope Gradient Colors :Set colors for positive and negative slopes, respectively.

Slope Fill :Adjusts the transparency of the slope gradient fill.

Volatility Gradient Display :Toggle to enable gradient coloring based on volatility levels.

Volatility Gradient Colors :Set colors for low and high volatility, respectively.

Volatility Fill :Adjusts the transparency of the volatility gradient fill.

Table Settings

Show Table :Toggle to display the metrics table on the chart.

Table Position :Choose where to position the table (e.g., top-right, middle-center, etc.).

Font Size :Set the size of the text in the table. Options include Tiny, Small, Normal, Large, and Huge.

Forex Heatmap█ OVERVIEW

This indicator creates a dynamic grid display of currency pair cross rates (exchange rates) and percentage changes, emulating the Cross Rates and Heat Map widgets available on our Forex page. It provides a view of realtime exchange rates for all possible pairs derived from a user-specified list of currencies, allowing users to monitor the relative performance of several currencies directly on a TradingView chart.

█ CONCEPTS

Foreign exchange

The Foreign Exchange (Forex/FX) market is the largest, most liquid financial market globally, with an average daily trading volume of over 5 trillion USD. Open 24 hours a day, five days a week, it operates through a decentralized network of financial hubs in various major cities worldwide. In this market, participants trade currencies in pairs , where the listed price of a currency pair represents the exchange rate from a given base currency to a specific quote currency . For example, the "EURUSD" pair's price represents the amount of USD (quote currency) that equals one unit of EUR (base currency). Globally, the most traded currencies include the U.S. dollar (USD), Euro (EUR), Japanese yen (JPY), British pound (GBP), and Australian dollar (AUD), with USD involved in over 87% of all trades.

Understanding the Forex market is essential for traders and investors, even those who do not trade currency pairs directly, because exchange rates profoundly affect global markets. For instance, fluctuations in the value of USD can impact the demand for U.S. exports or the earnings of companies that handle multinational transactions, either of which can affect the prices of stocks, indices, and commodities. Additionally, since many factors influence exchange rates, including economic policies and interest rate changes, analyzing the exchange rates across currencies can provide insight into global economic health.

█ FEATURES

Requesting a list of currencies

This indicator requests data for every valid currency pair combination from the list of currencies defined by the "Currency list" input in the "Settings/Inputs" tab. The list can contain up to six unique currency codes separated by commas, resulting in a maximum of 30 requested currency pairs.

For example, if the specified "Currency list" input is "CAD, USD, EUR", the indicator requests and displays relevant data for six currency pair combinations: "CADUSD", "USDCAD", "CADEUR", "EURCAD", "USDEUR", "EURUSD". See the "Grid display" section below to understand how the script organizes the requested information.

Each item in the comma-separated list must represent a valid currency code. If the "Currency list" input contains an invalid currency code, the corresponding cells for that currency in the "Cross rates" or "Heat map" grid show "NaN" values. If the list contains empty items, e.g., "CAD, ,EUR, ", the indicator ignores them in its data requests and calculations.

NOTE: Some uncommon currency pair combinations might not have data feeds available. If no available symbols provide the exchange rates between two specified currencies, the corresponding table cells show "NaN" results.

Realtime data

The indicator retrieves realtime market prices, daily price changes, and minimum tick sizes for all the currency pairs derived from the "Currency list" input. It updates the retrieved information shown in its grid display after new ticks become available to reflect the latest known values.

NOTE: Pine scripts execute on realtime bars only when new ticks are available in the chart's data feed. If no new updates are available from the chart's realtime feed, it may cause a delay in the data the indicator receives.

Grid display

This indicator displays the requested data for each currency pair in a table with cells organized as a grid. Each row name corresponds to a pair's base currency , and each column name corresponds to a quote currency . The cell at the intersection of a specific row and column shows the value requested from the corresponding currency pair.

For example, the cell at the intersection of a "EUR" row and "USD" column shows the data retrieved for the "EURUSD" currency pair, and the cell at the "USD" row and "EUR" column shows data for the inverse pair ("USDEUR").

Note that the main diagonal cells in the table, where rows and columns with the same names intersect, are blank. The exchange rate from one currency to itself is always 1, and no Forex symbols such as "EUREUR" exist.

The dropdown input at the top of the "Settings/Inputs" tab determines the type of information displayed in the table. Two options are available: "Cross rates" and "Heat map" . Both modes color their cells for light and dark themes separately based on the inputs in the "Colors" section.

Cross rates

When a user selects the "Cross rates" display mode, the table's cells show the latest available exchange rate for each currency pair, emulating the behavior of the Cross Rates widget. Each cell's value represents the amount of the quote currency (column name) that equals one unit of the base currency (row name). This display allows users to compare cross rates across currency pairs, and their inverses.

The background color of each cell changes based on the most recent update to the exchange rate, allowing users to monitor the direction of short-term fluctuations as they occur. By default, the background turns green (positive cell color) when the cross rate increases from the last recorded update and red (negative cell color) when the rate decreases. The cell's color reverts to the chart's background color after no new updates are available for 200 milliseconds.

Heat map

When a user selects the "Heat map" display mode, the table's cells show the latest daily percentage change of each currency pair, emulating the behavior of the Heat Map widget.

In this mode, the background color of each cell depends on the corresponding currency pair's daily performance. Heat maps typically use colors that vary in intensity based on the calculated values. This indicator uses the following color coding by default:

• Green (Positive cell color): Percentage change > +0.1%

• No color: Percentage change between 0.0% and +0.1%

• Bright red (Negative cell color): Percentage change < -0.1%

• Lighter/darker red (Minor negative cell color): Percentage change between 0.0% and -0.1%

█ FOR Pine Script™ CODERS

• This script utilizes dynamic requests to iteratively fetch information from multiple contexts using a single request.security() instance in the code. Previously, `request.*()` functions were not allowed within the local scopes of loops or conditional structures, and most `request.*()` function parameters, excluding `expression`, required arguments of a simple or weaker qualified type. The new `dynamic_requests` parameter in script declaration statements enables more flexibility in how scripts can use `request.*()` calls. When its value is `true`, all `request.*()` functions can accept series arguments for the parameters that define their requested contexts, and `request.*()` functions can execute within local scopes. See the Dynamic requests section of the Pine Script™ User Manual to learn more.

• Scripts can execute up to 40 unique `request.*()` function calls. A `request.*()` call is unique only if the script does not already call the same function with the same arguments. See this section of the User Manual's Limitations page for more information.

• Typically, when requesting higher-timeframe data with request.security() using barmerge.lookahead_on as the `lookahead` argument, the `expression` argument should use the history-referencing operator to offset the series, preventing lookahead bias on historical bars. However, the request.security() call in this script uses barmerge.lookahead_on without offsetting the `expression` because the script only displays results for the latest historical bar and all realtime bars, where there is no future information to leak into the past. Instead, using this call on those bars ensures each request fetches the most recent data available from each context.

• The request.security() instance in this script includes a `calc_bars_count` argument to specify that each request retrieves only a minimal number of bars from the end of each symbol's historical data feed. The script does not need to request all the historical data for each symbol because it only shows results on the last chart bar that do not depend on the entire time series. In this case, reducing the retrieved bars in each request helps minimize resource usage without impacting the calculated results.

Look first. Then leap.

Market Stats Panel [Daveatt]█ Introduction

I've created a script that brings TradingView's watchlist stats panel functionality directly to your charts. This isn't just another performance indicator - it's a pixel-perfect (kidding) recreation of TradingView's native stats panel.

Important Notes

You might need to adjust manually the scaling the firs time you're using this script to display nicely all the elements.

█ Core Features

Performance Metrics

The panel displays key performance metrics (1W, 1M, 3M, 6M, YTD, 1Y) in real-time, with color-coded boxes (green for positive, red for negative) for instant performance assessment.

Display Modes

Switch seamlessly between absolute prices and percentage returns, making it easy to compare assets across different price scales.

Absolute mode

Percent mode

Historical Comparison

View year-over-year performance with color-coded lines, allowing for quick historical pattern recognition and analysis.

Data Structure Innovation

Let's talk about one of the most interesting challenges I faced. PineScript has this quirky limitation where request.security() can only return 127 tuples at most. £To work around this, I implemented a dual-request system. The first request handles indices 0-63, while the second one takes care of indices 64-127.

This approach lets us maintain extensive historical data without compromising script stability.

And here's the cool part: if you need to handle even more years of historical data, you can simply extend this pattern by adding more request.security() calls.

Each additional call can fetch another batch of monthly open prices and timestamps, following the same structure I've used.

Think of it as building with LEGO blocks - you can keep adding more pieces to extend your historical reach.

Flexible Date Range

Unlike many scripts that box you into specific timeframes, I've designed this one to be completely flexible with your date selection. You can set any start year, any end year, and the script will dynamically scale everything to match. The visual presentation automatically adjusts to whatever range you choose, ensuring your data is always displayed optimally.

█ Customization Options

Visual Settings

The panel's visual elements are highly customizable. You can adjust the panel width to perfectly fit your workspace, fine-tune the line thickness to match your preferences, and enjoy the pre-defined year color scheme that makes tracking historical performance intuitive and visually appealing.

Box Dimensions

Every aspect of the performance boxes can be tailored to your needs. Adjust their height and width, fine-tune the spacing between them, and position the entire panel exactly where you want it on your chart. The goal is to make this tool feel like it's truly yours.

█ Technical Challenges Solved

Polyline Precision

Creating precise polylines was perhaps the most demanding aspect of this project.

The challenge was ensuring accurate positioning across both time and price axes, while handling percentage mode scaling with precision.

The script constantly updates the current year's data in real-time, seamlessly integrating new information as it comes in.

Axis Management

Getting the axes right was like solving a complex puzzle. The Y-axis needed to scale dynamically whether you're viewing absolute prices or percentages.

The X-axis required careful month labeling that stays clean and readable regardless of your selected timeframe.

Everything needed to align perfectly while maintaining proper spacing in all conditions.

█ Final Notes

This tool transforms complex market data into clear, actionable insights. Whether you're day trading or analyzing long-term trends, it provides the information you need to make informed decisions. And remember, while we can't predict the future, we can certainly be better prepared for it with the right tools at hand.

A word of warning though - seeing those red numbers in a beautifully formatted panel doesn't make them any less painful! 😉

---

Happy Trading! May your charts be green and your stops be far away!

Daveatt

Quick scan for cycles🙏🏻

The followup for

As I told before, ML based algorading is all about detecting any kind of non-randomness & exploiting it (cuz allegedly u cant trade randomness), and cycles are legit patterns that can be leveraged

But bro would u really apply Fourier / Wavelets / 'whatever else heavy' on every update of thousands of datasets, esp in real time on HFT / nearly HFT data? That's why this metric. It works much faster & eats hell of a less electicity, will do initial rough filtering of time series that might contain any kind of cyclic behaviour. And then, only on these filtered datasets u gonna put Periodograms / Autocorrelograms and see what's going there for real. Better to do it 10x times less a day on 10x less datasets, right?

I ended up with 2 methods / formulas, I called em 'type 0' and 'type 1':

- type 0: takes sum of abs deviations from drift line, scales it by max abs deviation from the same drift line;

- type 1: takes sum of abs deviations from drift line, scales it by range of non-abs deviations from the same drift line.

Finnaly I've chosen type 0 , both logically (sum of abs dev divided by max abs dev makes more sense) and experimentally. About that actually, here are both formulas put on sine waves with uniform noise:

^^ generated sine wave with uniform noise

^^ both formulas on that wave

^^ both formulas on real data

As you can see type 0 is less affected by noise and shows higher values on synthetic data, but I decided to put type 1 inside as well, in case my analysis was not complete and on real data type 1 can actually be better since it has a lil higher info gain / info content (still not sure). But I can assure u that out of all other ways I've designed & tested for quite a time I tell you, these 2 are really the only ones who got there.

Now about dem thresholds and how to use it.

Both type 0 and type 1 can be modelled with Beta distribution, and based on it and on some obvious & tho non mainstream statistical modelling techniques, I got these thresholds, so these are not optimized overfitted values, but natural ones. Each type has 3 thresholds (from lowest to highest):

- typical value (turned off by default). aka basis ;

- typical deviation from typical value, aka deviation ;

- maximum modelled deviation from typical value (idk whow to call it properly for now, this is my own R&D), aka extension .

So when the metric is above one of these thresholds (which one is up to you, you'll read about it in a sec), it means that there might be a strong enough periodic signal inside the data, and the data got to be put through proper spectral analysis tools to confirm / deny it.

If you look at the pictures above again, you'll see gray signal, that's uniform noise. Take a look at it and see where does it sit comparing to the thresholds. Now you just undertand that picking up a threshold is all about the amount of false positives you care to withstand.

If you take basis as threshold, you'll get tons of false positives (that's why it's even turned off by default), but you'll almost never miss a true positive. If you take deviation as threshold, it's gonna be kinda balanced approach. If you take extension as threshold, you gonna miss some cycles, and gonna get only the strongest ones.

More true positives -> more false positives, less false positives -> less true positives, can't go around that mane

Just to be clear again, I am not completely sure yet, but I def lean towards type 0 as metric, and deviation as threshold.

Live Long and Prosper

P.S.: That was actually the main R&D of the last month, that script I've released earlier came out as derivative.

P.S.: These 2 are the first R&Ds made completely in " art-space", St. Petersburg. Come and see me, say wassup🤘🏻

Pine Execution MapPine Script Execution Map

Overview:

This is an educational script for Pine Script developers. The script includes data structure, functions/methods, and process to capture and print Pine Script execution map of functions called while pine script execution.

Map of execution is produced for last/latest candle execution.

The script also has example code to call execution map methods and generate Pine Execution map.

Use cases:

Pine script developers can get view of how the functions are called

This can also be used while debugging the code and know which functions are called vs what developer expect code to do

One can use this while using any of the open source published script and understand how public script is organized and how functions of the script are called.

Code components:

User defined type

type EMAP

string group

string sub_group

int level

array emap = array.new()

method called internally by other methods to generate level of function being executed

method id(string tag) =>

if(str.startswith(tag, "MAIN"))

exe_level.set(0, 0)

else if(str.startswith(tag, "END"))

exe_level.set(0, exe_level.get(0) - 1)

else

exe_level.set(0, exe_level.get(0) + 1)

exe_level.get(0)

Method called from main/global scope to record execution of main scope code. There should be only one call to this method at the start of global scope.

method main(string tag) =>

this = EMAP.new()

this.group := "MAIN"

this.sub_group := tag

this.level := "MAIN".id()

emap.push(this)

Method called from main/global scope to record end of execution of main scope code. There should be only one call to this method at the end of global scope.

method end_main(string tag) =>

this = EMAP.new()

this.group := "END_MAIN"

this.sub_group := tag

this.level := 0

emap.push(this)

Method called from start of each function to record execution of function code

method call(string tag) =>

this = EMAP.new()

this.group := "SUB"

this.sub_group := tag

this.level := "SUB".id()

emap.push(this)

Method called from end of each function to record end of execution of function code

method end_call(string tag) =>

this = EMAP.new()

this.group := "END_SUB"

this.sub_group := tag

this.level := "END_SUB".id()

emap.push(this)

Pine code which generates execution map and show it as a label tooltip.

if(barstate.islast)

for rec in emap

if(not str.startswith(rec.group, "END"))

lvl_tab = str.repeat("", rec.level+1, "\t")

txt = str.format("=> {0} {1}> {2}", lvl_tab, rec.level, rec.sub_group)

debug.log(txt)

debug.lastr()

Snapshot 1:

This is the output of the script and can be viewed by hovering mouse pointer over the blue color diamond shaped label

Snapshot 2:

How to read the Pine execution map

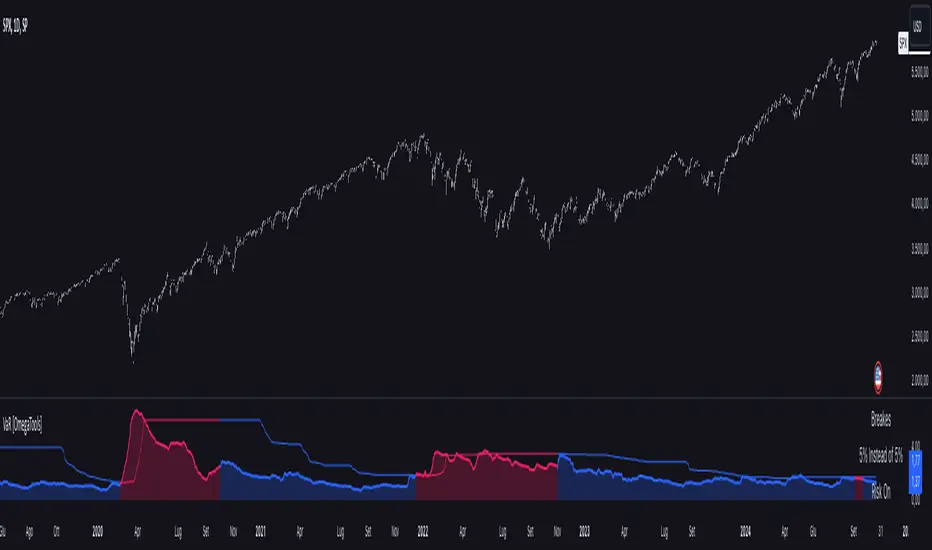

Value at Risk [OmegaTools]The "Value at Risk" (VaR) indicator is a powerful financial risk management tool that helps traders estimate the potential losses in a portfolio over a specified period of time, given a certain level of confidence. VaR is widely used by financial institutions, traders, and risk managers to assess the probability of portfolio losses in both normal and volatile market conditions. This TradingView script implements a comprehensive VaR calculation using several models, allowing users to visualize different risk scenarios and adjust their trading strategies accordingly.

Concept of Value at Risk

Value at Risk (VaR) is a statistical technique used to measure the likelihood of losses in a portfolio or financial asset due to market risks. In essence, it answers the question: "What is the maximum potential loss that could occur in a given portfolio over a specific time horizon, with a certain confidence level?" For instance, if a portfolio has a one-day 95% VaR of $10,000, it means that there is a 95% chance the portfolio will not lose more than $10,000 in a single day. Conversely, there is a 5% chance of losing more than $10,000. VaR is a key risk management tool for portfolio managers and traders because it quantifies potential losses in monetary terms, allowing for better-informed decision-making.

There are several ways to calculate VaR, and this indicator script incorporates three of the most commonly used models:

Historical VaR: This approach uses historical returns to estimate potential losses. It is based purely on past price data, assuming that the past distribution of returns is indicative of future risks.

Variance-Covariance VaR: This model assumes that asset returns follow a normal distribution and that the risk can be summarized using the mean and standard deviation of past returns. It is a parametric method that is widely used in financial risk management.

Exponentially Weighted Moving Average (EWMA) VaR: In this model, recent data points are given more weight than older data. This dynamic approach allows the VaR estimation to react more quickly to changes in market volatility, which is particularly useful during periods of market stress. This model uses the Exponential Weighted Moving Average Volatility Model.

How the Script Works

The script starts by offering users a set of customizable input settings. The first input allows the user to choose between two main calculation modes: "All" or "OCT" (Only Current Timeframe). In the "All" mode, the script calculates VaR using all available methodologies—Historical, Variance-Covariance, and EWMA—providing a comprehensive risk overview. The "OCT" mode narrows the calculation to the current timeframe, which can be particularly useful for intraday traders who need a more focused view of risk.

The next input is the lookback window, which defines the number of historical periods used to calculate VaR. Commonly used lookback periods include 21 days (approximately one month), 63 days (about three months), and 252 days (roughly one year), with the script supporting up to 504 days for more extended historical analysis. A longer lookback period provides a more comprehensive picture of risk but may be less responsive to recent market conditions.

The confidence level is another important setting in the script. This represents the probability that the loss will not exceed the VaR estimate. Standard confidence levels are 90%, 95%, and 99%. A higher confidence level results in a more conservative risk estimate, meaning that the calculated VaR will reflect a more extreme loss scenario.

In addition to these core settings, the script allows users to customize the visual appearance of the indicator. For example, traders can choose different colors for "Bullish" (Risk On), "Bearish" (Risk Off), and "Neutral" phases, as well as colors for highlighting "Breaks" in the data, where returns exceed the calculated VaR. These visual cues make it easy to identify periods of heightened risk at a glance.

The actual VaR calculation is broken down into several models, starting with the Historical VaR calculation. This is done by computing the logarithmic returns of the asset's closing prices and then using linear interpolation to determine the percentile corresponding to the desired confidence level. This percentile represents the potential loss in the asset over the lookback period.

Next, the script calculates Variance-Covariance VaR using the mean and standard deviation of the historical returns. The standard deviation is multiplied by a z-score corresponding to the chosen confidence level (e.g., 1.645 for 95% confidence), and the resulting value is subtracted from the mean return to arrive at the VaR estimate.

The EWMA VaR model uses the EWMA for the sigma parameter, the standard deviation, obtaining a specific dynamic in the volatility. It is particularly useful in volatile markets where recent price behavior is more indicative of future risk than older data.

For traders interested in intraday risk management, the script provides several methods to adjust VaR calculations for lower timeframes. By using intraday returns and scaling them according to the chosen timeframe, the script provides a dynamic view of risk throughout the trading day. This is especially important for short-term traders who need to manage their exposure during high-volatility periods within the same day. The script also incorporates an EWMA model for intraday data, which gives greater weight to the most recent intraday price movements.

In addition to calculating VaR, the script also attempts to detect periods where the asset's returns exceed the estimated VaR threshold, referred to as "Breaks." When the returns breach the VaR limit, the script highlights these instances on the chart, allowing traders to quickly identify periods of extreme risk. The script also calculates the average of these breaks and displays it for comparison, helping traders understand how frequently these high-risk periods occur.

The script further visualizes the risk scenario using a risk phase classification system. Depending on the level of risk, the script categorizes the market as either "Risk On," "Risk Off," or "Risk Neutral." In "Risk On" mode, the market is considered bullish, and the indicator displays a green background. In "Risk Off" mode, the market is bearish, and the background turns red. If the market is neither strongly bullish nor bearish, the background turns neutral, signaling a balanced risk environment.

Traders can customize whether they want to see this risk phase background, along with toggling the display of the various VaR models, the intraday methods, and the break signals. This flexibility allows traders to tailor the indicator to their specific needs, whether they are day traders looking for quick intraday insights or longer-term investors focused on historical risk analysis.

The "Risk On" and "Risk Off" phases calculated by this Value at Risk (VaR) script introduce a novel approach to market risk assessment, offering traders an advanced toolset to gauge market sentiment and potential risk levels dynamically. These risk phases are built on a combination of traditional VaR methodologies and proprietary logic to create a more responsive and intuitive way to manage exposure in both normal and volatile market conditions. This method of classifying market conditions into "Risk On," "Risk Off," or "Risk Neutral" is not something that has been traditionally associated with VaR, making it a groundbreaking addition to this indicator.

How the "Risk On" and "Risk Off" Phases Are Calculated

In typical VaR implementations, the focus is on calculating the potential losses at a given confidence level without providing an overall market outlook. This script, however, introduces a unique risk classification system that takes the output of various VaR models and translates it into actionable signals for traders, marking whether the market is in a Risk On, Risk Off, or Risk Neutral phase.

The Risk On and Risk Off phases are primarily determined by comparing the current returns of the asset to the average VaR calculated across several different methods, including Historical VaR, Variance-Covariance VaR, and EWMA VaR. Here's how the process works:

1. Threshold Setting and Effect Calculation: The script first computes the average VaR using the selected models. It then checks whether the current returns (expressed as a negative value to signify loss) exceed the average VaR value. If the current returns surpass the calculated VaR threshold, this indicates that the actual market risk is higher than expected, signaling a potential shift in market conditions.

2. Break Analysis: In addition to monitoring whether returns exceed the average VaR, the script counts the number of instances within the lookback period where this breach occurs. This is referred to as the "break effect." For each period in the lookback window, the script checks whether the returns surpass the calculated VaR threshold and increments a counter. The percentage of periods where this breach occurs is then calculated as the "effect" or break percentage.

3. Dual Effect Check (if "Double" Risk Scenario is selected): When the user chooses the "Double" risk scenario mode, the script performs two layers of analysis. First, it calculates the effect of returns exceeding the VaR threshold for the current timeframe. Then, it calculates the effect for the lower intraday timeframe as well. Both effects are compared to the user-defined confidence level (e.g., 95%). If both effects exceed the confidence level, the market is deemed to be in a high-risk situation, thus triggering a Risk Off phase. If both effects fall below the confidence level, the market is classified as Risk On.

4. Risk Phases Determination: The final risk phase is determined by analyzing these effects in relation to the confidence level:

- Risk On: If the calculated effect of breaks is lower than the confidence level (e.g., fewer than 5% of periods show returns exceeding the VaR threshold for a 95% confidence level), the market is considered to be in a relatively safe state, and the script signals a "Risk On" phase. This is indicative of bullish conditions where the potential for extreme loss is minimal.

- Risk Off: If the break effect exceeds the confidence level (e.g., more than 5% of periods show returns breaching the VaR threshold), the market is deemed to be in a high-risk state, and the script signals a "Risk Off" phase. This indicates bearish market conditions where the likelihood of significant losses is higher.

- Risk Neutral: If the break effect hovers near the confidence level or if there is no clear trend indicating a shift toward either extreme, the market is classified as "Risk Neutral." In this phase, neither bulls nor bears are dominant, and traders should remain cautious.

The phase color that the script uses helps visualize these risk phases. The background will turn green in Risk On conditions, red in Risk Off conditions, and gray in Risk Neutral phases, providing immediate visual feedback on market risk. In addition to this, when the "Double" risk scenario is selected, the background will only turn green or red if both the current and intraday timeframes confirm the respective risk phase. This double-checking process ensures that traders are only given a strong signal when both longer-term and short-term risks align, reducing the likelihood of false signals.

A New Way of Using Value at Risk

This innovative Risk On/Risk Off classification, based on the interaction between VaR thresholds and market returns, represents a significant departure from the traditional use of Value at Risk as a pure risk measurement tool. Typically, VaR is employed as a backward-looking measure of risk, providing a static estimate of potential losses over a given timeframe with no immediate actionable feedback on current market conditions. This script, however, dynamically interprets VaR results to create a forward-looking, real-time signal that informs traders whether they are operating in a favorable (Risk On) or unfavorable (Risk Off) environment.

By incorporating the "break effect" analysis and allowing users to view the VaR breaches as a percentage of past occurrences, the script adds a predictive element that can be used to time market entries and exits more effectively. This **dual-layer risk analysis**, particularly when using the "Double" scenario mode, adds further granularity by considering both current timeframe and intraday risks. Traders can therefore make more informed decisions not just based on historical risk data, but on how the market is behaving in real-time relative to those risk benchmarks.

This approach transforms the VaR indicator from a risk monitoring tool into a decision-making system that helps identify favorable trading opportunities while alerting users to potential market downturns. It provides a more holistic view of market conditions by combining both statistical risk measurement and intuitive phase-based market analysis. This level of integration between VaR methodologies and real-time signal generation has not been widely seen in the world of trading indicators, marking this script as a cutting-edge tool for risk management and market sentiment analysis.

I would like to express my sincere gratitude to @skewedzeta for his invaluable contribution to the final script. From generating fresh ideas to applying his expertise in reviewing the formula, his support has been instrumental in refining the outcome.

Macros ICT KillZones [TradingFinder] Times & Price Trading Setup🔵 Introduction

ICT Macros, developed by Michael Huddleston, also known as ICT (Inner Circle Trader), is a powerful trading tool designed to help traders identify the best trading opportunities during key time intervals like the London and New York trading sessions.

For traders aiming to capitalize on market volatility, liquidity shifts, and Fair Value Gaps (FVG), understanding and using these critical time zones can significantly improve trading outcomes.

In today’s highly competitive financial markets, identifying the moments when the market is seeking buy-side or sell-side liquidity, or filling price imbalances, is essential for maximizing profitability.

The ICT Macros indicator is built on the renowned ICT time and price theory, which enables traders to track and leverage key market dynamics such as breaks of highs and lows, imbalances, and liquidity hunts.

This indicator automatically detects crucial market times and optimizes strategies for traders by highlighting the specific moments when price movements are most likely to occur. A standout feature of ICT Macros is its automatic adjustment for Daylight Saving Time (DST), ensuring that traders remain synced with the correct session times.

This means you can rely on accurate market timing without the need for manual updates, allowing you to focus on capturing profitable trades during critical timeframes.

🔵 How to Use

The ICT Macros indicator helps you capitalize on trading opportunities during key market moments, particularly when the market is breaking highs or lows, filling Fair Value Gaps (FVG), or addressing imbalances. This indicator is particularly beneficial for traders who seek to identify liquidity, market volatility, and price imbalances.

🟣 Sessions

London Sessions

London Macro 1 :

UTC Time : 06:33 to 07:00

New York Time : 02:33 to 03:00

London Macro 2 :

UTC Time : 08:03 to 08:30

New York Time : 04:03 to 04:30

New York Sessions

New York Macro AM 1 :

UTC Time : 12:50 to 13:10

New York Time : 08:50 to 09:10

New York Macro AM 2 :

UTC Time : 13:50 to 14:10

New York Time : 09:50 to 10:10

New York Macro AM 3 :

UTC Time : 14:50 to 15:10

New York Time : 10:50 to 11:10

New York Lunch Macro :

UTC Time : 15:50 to 16:10

New York Time : 11:50 to 12:10

New York PM Macro :

UTC Time : 17:10 to 17:40

New York Time : 13:10 to 13:40

New York Last Hour Macro :

UTC Time : 19:15 to 19:45

New York Time : 15:15 to 15:45

These time intervals adjust automatically based on Daylight Saving Time (DST), helping traders to enter or exit trades during key market moments when price volatility is high.

Below are the main applications of this tool and how to incorporate it into your trading strategies :

🟣 Combining ICT Macros with Trading Strategies

The ICT Macros indicator can easily be used in conjunction with various trading strategies. Two well-known strategies that can be combined with this indicator include:

ICT 2022 Trading Model : This model is designed based on identifying market liquidity, structural price changes, and Fair Value Gaps (FVG). By using ICT Macros, you can identify the key time intervals when the market is seeking liquidity, filling imbalances, or breaking through important highs and lows, allowing you to enter or exit trades at the right moment.

Silver Bullet Strategy : This strategy, which is built around liquidity hunting and rapid price movements, can work more accurately with the help of ICT Macros. The indicator pinpoints precise liquidity times, helping traders take advantage of market shifts caused by filling Fair Value Gaps or correcting imbalances.

🟣 Capitalizing on Price Volatility During Key Times

Large market algorithms often seek liquidity or fill Fair Value Gaps (FVG) during the intervals marked by ICT Macros. These periods are when price volatility increases, and traders can use these moments to enter or exit trades.

For example, if sell-side liquidity is drained and the market fills an imbalance, the price might move toward buy-side liquidity. By identifying these moments, which may also involve breaking a previous high or low, you can leverage rapid market fluctuations to your advantage.

🟣 Identifying Liquidity and Price Imbalances

One of the important uses of ICT Macros is identifying points where the market is seeking liquidity and correcting imbalances. You can determine high or low liquidity levels in the market before each ICT Macro, as well as Fair Value Gaps (FVG) and price imbalances that need to be filled, using them to adjust your trading strategy. This capability allows you to manage trades based on liquidity shifts or imbalance corrections without needing a bias toward a specific direction.

🔵 Settings

The ICT Macros indicator offers various customization options, allowing users to tailor it to their specific needs. Below are the main settings:

Time Zone Mode : You can select one of the following options to define how time is displayed:

UTC : For traders who need to work with Universal Time.

Session Local Time : The local time corresponding to the London or New York markets.

Your Time Zone : You can specify your own time zone (e.g., "UTC-4:00").

Your Time Zone : If you choose "Your Time Zone," you can set your specific time zone. By default, this is set to UTC-4:00.

Show Range Time : This option allows you to display the time range of each session on the chart. If enabled, the exact start and end times of each interval are shown.

Show or Hide Time Ranges : Toggle on/off for visual clarity depending on user preference.

Custom Colors : Set distinct colors for each session, allowing users to personalize their chart based on their trading style.These settings allow you to adjust the key time intervals of each trading session to your preference and customize the time format according to your own needs.

🔵 Conclusion

The ICT Macros indicator is a powerful tool for traders, helping them to identify key time intervals where the market seeks liquidity or fills Fair Value Gaps (FVG), corrects imbalances, and breaks highs or lows. This tool is especially valuable for traders using liquidity-based strategies such as ICT 2022 or Silver Bullet.

One of the key features of this indicator is its support for Daylight Saving Time (DST), ensuring you are always in sync with the correct trading session timings without manual adjustments. This is particularly beneficial for traders operating across different time zones.

With ICT Macros, you can capitalize on crucial market opportunities during sensitive times, take advantage of imbalances, and enhance your trading strategies based on market volatility, liquidity shifts, and Fair Value Gaps.

RSI Fakeout Filter with SMA Confirmation [CHE] Introducing: RSI Fakeout Detection

Are you tired of being caught in fakeouts that can lead to frustrating losses? The RSI Fakeout Detection is here to enhance your trading strategy by filtering out false signals and providing you with more reliable entries. This innovative indicator is designed to help traders identify when market momentum, as indicated by the RSI, does not align with price movement – a key indicator of potential fakeouts!

What Does It Do?

The RSI Fakeout Detection focuses on one key goal: avoiding false signals. By monitoring when the RSI exceeds a customizable threshold (indicating strength) but the price remains below a moving average like the SMA, this indicator highlights situations where the market may seem strong, but the price action doesn't support that momentum. In other words, it saves you from those tricky fake breakouts.

Key Benefits:

1. Reduce Risk, Increase Confidence: Get an extra layer of protection against fakeouts by receiving signals only when both RSI and price confirm the market's true direction. Avoid entering false breakouts and trade with more confidence.

2. Dynamic Analysis of SMA Lengths: It doesn’t just rely on one SMA. The indicator automatically analyzes and sorts through different SMA lengths to find the most reliable one for your specific market condition, ensuring that you get the best possible signal.

3. Tailored for You: With customizable RSI thresholds, a choice of multiple moving average types (SMA, EMA, Bollinger Bands, and more), and vibrant color-coded visuals, this tool is built to fit your unique trading style and preferences.

4. Spot Fakeouts with Ease: Visual cues make it easy to see when the market might be tricking you. Labels, plotted lines, and a toggleable disclaimer keep everything transparent and easy to understand.

5. Friendly and Intuitive: Whether you’re new to trading or a seasoned pro, the RSI Fakeout Detection is designed to be simple and effective. The labels and plots are clear, the alerts are timely, and it seamlessly integrates into your chart without cluttering it.

Why Choose RSI Fakeout Detection?

- Accuracy and Precision: By combining RSI and SMA analysis, this indicator minimizes the risk of following false trends and entering trades too early.

- Save Time and Reduce Guesswork: No more spending hours trying to figure out which SMA length works best – the RSI Fakeout Detection does it for you!

- Peace of Mind: Avoiding fakeouts means fewer bad trades, which can lead to more consistent performance and less stress.

Transform the way you trade, and step into a more confident trading future with RSI Fakeout Detection . Whether you’re day trading or swing trading, this tool will give you an edge by helping you filter out the noise and make more informed decisions.

Best regards,

Chervolino

Disclaimer:

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Custom Pattern DetectionOverview

Chart Patterns is a major tool for many traders. Pattern formation at specific location on the chart is used for investment/trading decisions.

This indicator is designed in a way to allow investors/traders to define patterns of their choice based on certain input parameters and then detect defined pattern on the chart.

Investors/traders can use their own creativity to create and detect patterns.

This indicator works in 2 modes

Create Pattern: One can define a pattern and verify sample pattern formation visually

Detect Pattern: Detect and mark patterns on the chart

Settings

Create Custom Pattern:

Show Custom Pattern – This will mark the pattern lines on the chart so that one can verify how pattern appears based on the input’s parameters provided for lines XA, AB, BC, CD, DE, EF

Offset – Used while pattern creation. Offset is horizonal distance between 2 lines.

XA Points – Used to draw XA line when sample pattern is drawn. XA points can be a negative or position number.

XA line is drawn based on Offset and XA Points. E.g. Offset = 5 and XA Points = -20. In this line would be drawn from last candle high to high – 20 (these are y1 and y2 points of a line). While drawing line distance of 5 candles would be placed between 2 line points (these are x1 and x2 points of a line). In XA line X forms start point and A forms end point of the line.

Line AB – Line AB is drawn from point X. To derive the end point of AB, average Fib% is derived based on From Fib% and To Fib% parameters. Finally end point is derived by applying Fib Retracement on Line XA based on average Fib%.

Line AB to Line EF – These points are derived as explained in Line AB.

The indicator can be used to define/create patterns up to 6 legs/lines. The line would be named as XA -> AB -> BC -> CD -> DE -> EF.

If one wish to create pattern consisting 3 legs then it can be achieved by unchecking/deselecting Line CD, DE and EF or by checking only Line AB and BC.

Based on the parameters above indicator draws a sample pattern after last candle/bar on the chart. Sample pattern helps to visually see how pattern will appear on the chart.

Pattern Identification

Indicator derive the swing high/low points based on the Pivot lookback and use as reference points while detecting patterns.

Use of From Fib% and To Fib% - While detecting pattern, retracement price points are derived for From Fib% and To Fib%. Price points between from Fib% and To Fib% are treated as valid retracement points.

How to configure and use indicator for detecting patterns

Sample Pattern 1

Sample Pattern 2

Sample Pattern 3

Sample Pattern 4

Shifted Symbol Overlay with OffsetThe Shifted Symbol Overlay Indicator is a custom TradingView indicator designed to overlay the price data of one stock or asset over another, allowing for direct visual comparison. This is particularly useful for comparing the performance of two assets over different time periods. The indicator enables you to shift the data from one asset either forward or backward in time, making it easier to compare historical data from one stock with more recent data from another. The indicator supports shifting both to the right (future periods) and to the left (earlier periods), helping traders and analysts explore correlations or divergences between two financial instruments.

The indicator also includes a normalization option that adjusts the scale of the two assets, so you can compare them even if they have vastly different price levels. This is useful when you're interested in relative performance rather than the absolute price values.

Absolute ZigZagThis ZigZag Indicator is a bit unique in it's kind.

It uses my own Absolute ZigZag Lib to calculate the pivots:

Instead of using percentages or looking more than 1 bar left or right, this Zigzag library calculates pivots by just looking at the current bar highs and lows and the ones of one bar earlier. This is a very fast and accurate way of calculating pivots.

The library also features a solution for bars that have both a higher high and a higher low like seen below.

You can also use your own colors for the labels and the lines:

You can also quickly select a one-colored theme without changing all colors at once:

Tian Di Grid Merge Version 6.0

Strategy Introduction:

1. We know that the exchange can only set a maximum of 100 grids. However, our grid strategy can set a maximum of 350 grids.

2. We have added the modes of proportional and differential warehousing.

3. It should be noted that we have not set any filtering conditions, which means that when the price falls below the grid, we will execute a buy action at the closing price, and when the price falls above the grid, we will execute a sell action;

4. We suggest limiting the trading time cycle to 5 meters, as sometimes errors may appear on TV due to the dense grid or the inability to draw so many grids;

5. Please ensure that the minimum spacing between each grid is not less than 0.1%, as this is extremely difficult to profit from, and on the other hand, it may not function due to excessively dense spacing;

6. The maximum number of grids is 350, and the minimum number is currently 3;

matters needing attention:

Don't choose to go long or short together, and don't choose to go even short or short;

Closing position setting: It is recommended to select it to avoid order accumulation;

Unable to trade: If unable to trade normally, switch to a 1m cycle;

Number of cells: Calculate it yourself, 350 is just the maximum number of cells that can be adjusted;

Grid spacing: minimum 0.1%, below which no profit can be made;

Position value: default is 100u, which is the amount already leveraged;

Multiple investment: The order amount for each order is the same, and there is no need for multiple investment;

Open both long and short positions: You can open multiple positions for one account and open one position for one account. Do not open both long and short positions for the same target at the same time

Pressure Zones with MA [SYNC & TRADE]Description:

The "Pressure Zones with MA " indicator is designed to analyze the pressure of buyers and sellers on the market, as well as to identify areas of increased activity. When designing it, the main task was to see manipulations on the market, when the power of sellers or the power of buyers is in a sideways trend or falling, and the opposite is growing.

Here is a good example. The power of sellers is in a narrow sideways trend, and sales are increasing very aggressively. The power of buyers is in a gray block with the inscription "range". Then we see the fading of the power of sellers and buyers furiously pounce on the asset that has fallen in price.

Here are the main aspects of its operation and use:

First, turn off the moving averages in the indicator settings, on the "style" tab. Choose your favorite asset, which you understand well and know all its ups and downs. I want you to see a clean chart, so that you can be imbued with a new idea, you need to watch it. This is a proprietary indicator and I understand that it does not have the inscription “buy” / “sell”, but believe me, if you pay attention, you will see its strength. I usually add functionality later, but the light code and visualization remain preferable in the first version.

Purpose:

The indicator helps to determine the strength of buyers and sellers in the market.

It visualizes zones where the pressure of buyers or sellers prevails.

Additionally displays moving averages (MA) for data smoothing.

Main components:

Buyer strength chart (blue line)

Seller strength chart (red line)

Moving averages for buyer and seller strength

Threshold line for defining zones

Indicator settings:

Period: defines the base period for calculations (default 89)

Threshold: sets the level for defining pressure zones (from 0 to 2, default 0.8)

MA type for purchases and sales: select the type of moving average (SMA, EMA, RMA, WMA, VWMA, HMA)

MA length for purchases and sales: period for calculating moving averages

Colors for uptrends and downtrends of MA

Moving averages:

Help smooth out data and identify trends

The direction of the MA (up or down) further confirms the current trend

The color of the MA changes depending on the direction (blue for up, red for down)

Now you can turn them on and see how they help in understanding where one or another force is weakening. It is in this case that we see the intersection of forces and the sellers' force is moving aggressively upward. Also, according to the moving average, we see the weakening of the sellers' force. The buyers' force was in the sideways range and then switched on to buy out and also according to the moving average, it is clear where the main interest in purchases disappeared.

Use:

Observe the strength of buyers and sellers relative to each other. They can move simultaneously in one direction, this is regarded as balance

can move in different directions and this will strengthen the upward force of sellers or buyers

You may also notice that the movement of one of the forces will be in a narrow range and the second will grow strongly - this is manipulation or trading without resistance.

You can also play with the threshold line, but it is not the main thing here. I disabled this function in the code.

// Display zones

//bgcolor(buy_zone ? color.new(color.blue, 90) : na)

//bgcolor(sell_zone ? color.new(color.red, 90) : na)

If you want to enable it, copy it instead

// Display zones

bgcolor(buy_zone ? color.new(color.blue, 90) : na)

bgcolor(sell_zone ? color.new(color.red, 90) : na)

Pay attention to the intersection of forces.

Use crossovers of force lines and their moving averages as potential signals

Combine the indicator signals with other technical analysis tools for confirmation

Limitations:

Requires customization of parameters for a specific trading instrument and timeframe

The indicator should not be used as the only tool for making trading decisions

Remember that this indicator provides additional information for market analysis, but is not a guarantee of successful trades. Always combine it with other analysis methods and follow risk management rules.

Описание:

Индикатор "Pressure Zones with MA " предназначен для анализа давления покупателей и продавцов на рынке, а также для определения зон повышенной активности. При его проектировании основная задача была увидеть манипуляции на рынке, когда сила продавцов или сила покупателей стоит в боковике или падает, а противоположная растет.

Вот хороший пример. Сила продавцов стоит в узком боковике, а продажи очень агрессивно усиливаются. Сила покупателей в сером блоке с надписью “range”. Потом мы видим затухание силы продавцов и покупателей яростно накидываются на подешевевший актив.

Вот основные аспекты его работы и использования:

Для начала отключите средние скользящие в настройках индикатора, на закладке “стиль”. Выберите свой любимый актив, в котором вы хорошо разбираетесь и знаете его все взлеты и падения. Я хочу чтобы вы увидели чистый график, для того чтобы вы могли проникнутся новой идеей нужно понаблюдать за ним. Это авторский индикатор и я понимаю что на нем нет надписи “купить” / “продать”, но поверьте уделив свое внимание вы увидите его силу. Я обычно потом добавляю функционал но легкий код и визуализация, в первом варианте остается предпочтительней.

Назначение:

Индикатор помогает определить силу покупателей и продавцов на рынке.

Он визуализирует зоны, где преобладает давление покупателей или продавцов.

Дополнительно отображает скользящие средние (MA) для сглаживания данных.

Основные компоненты:

График силы покупателей (синяя линия)

График силы продавцов (красная линия)

Скользящие средние для силы покупателей и продавцов

Пороговая линия для определения зон

Настройки индикатора:

Период (Period): определяет базовый период для расчетов (по умолчанию 89)

Порог (Threshold): устанавливает уровень для определения зон давления (от 0 до 2, по умолчанию 0.8)

Тип MA для покупок и продаж: выбор типа скользящей средней (SMA, EMA, RMA, WMA, VWMA, HMA)

Длина MA для покупок и продаж: период для расчета скользящих средних

Цвета для восходящего и нисходящего трендов MA

Скользящие средние:

Помогают сглаживать данные и выявлять тренды

Направление MA (вверх или вниз) дополнительно подтверждает текущий тренд

Цвет MA меняется в зависимости от направления (синий для восходящего, красный для нисходящего)

Теперь вы можете их включить и посмотреть как они помогают в понимании где ослабевает та или иная сила. Именно в этом случае мы видим пересечение сил и сила продавцов идет агрессивно вверх. Также по средней скользящей мы видим затухание силы продавцов. Сила покупателей стояла в боковике потом включилась на откуп и также по средней скользящей видно где пропал основной интерес к покупкам.

Использование:

Наблюдайте за силой покупателей и продавцов относительно друг друга. Они могут двигаться одновременно в одном направлении это расценивается как баланс

могут двигаться в разных направлениях и это будет усиливать восходящую силу продавцов или покупателей

также возможно вы заметите что движение одной из силы будет в узком диапазоне а вторая будет сильно расти - это манипуляция или торговля без сопротивления.

Также можете поиграть с пороговой линией, но она совершенно не главная здесь. В коде я отключил эту функцию.

// Display zones

//bgcolor(buy_zone ? color.new(color.blue, 90) : na)

//bgcolor(sell_zone ? color.new(color.red, 90) : na)

Если захотите включить скопируйте вместо нее

// Display zones

bgcolor(buy_zone ? color.new(color.blue, 90) : na)

bgcolor(sell_zone ? color.new(color.red, 90) : na)

Обращайте внимание на пересечение сил.

Используйте пересечения линий силы и их скользящих средних как потенциальные сигналы

Комбинируйте сигналы индикатора с другими инструментами технического анализа для подтверждения

Ограничения:

Требуется настройка параметров под конкретный торговый инструмент и таймфрейм

Не следует использовать индикатор как единственный инструмент для принятия торговых решений

Помните, что этот индикатор предоставляет дополнительную информацию для анализа рынка, но не является гарантией успешных сделок. Всегда сочетайте его с другими методами анализа и соблюдайте правила управления рисками.

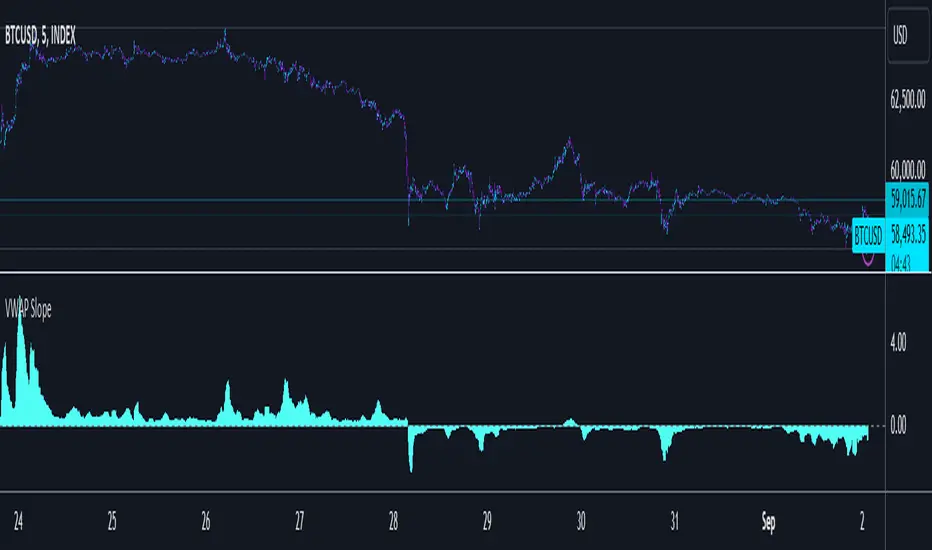

VWAP SlopePublishing one of the simplest yet one of my favorite concepts. Had to publish since I didn't really find any script for this on TV.

VWAP slope.

This is nothing fancy because it's just calculating "slope" with a very basic level formula

vwap_slope = (vwap - vwap ) / length

Above zero line, it's positive zone.

Below zero line, it's a negative zone.

The idea is to avoid choppy conditions and stay true to larger readings, sometimes when we have vwap directly on chart and when price interacts with it, we tend to take the lot of bad trades.

The intention here is to avoid just that.

This is also good at tracking failure of change in sentiments, this failure is very important, because one's failure occurs there is significant movement in the opposite direction of the failure.

Since there isn't much alteration to this idea, there is not much to talk about tbh.

Just remember, this is an educational idea and not assurance of future performance.

Regards.

DrawingLibrary "Drawing"

User Defined types and methods for basic drawing structure. Consolidated from the earlier libraries - DrawingTypes and DrawingMethods

method get_price(this, bar)

get line price based on bar

Namespace types: Line

Parameters:

this (Line) : (series Line) Line object.

bar (int) : (series/int) bar at which line price need to be calculated

Returns: line price at given bar.

method init(this)

Namespace types: PolyLine

Parameters:

this (PolyLine)

method tostring(this, sortKeys, sortOrder, includeKeys)

Converts DrawingTypes/Point object to string representation

Namespace types: chart.point

Parameters:

this (chart.point) : DrawingTypes/Point object

sortKeys (bool) : If set to true, string output is sorted by keys.

sortOrder (int) : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

includeKeys (array) : Array of string containing selective keys. Optional parmaeter. If not provided, all the keys are considered

Returns: string representation of DrawingTypes/Point

method tostring(this, sortKeys, sortOrder, includeKeys)

Converts DrawingTypes/LineProperties object to string representation

Namespace types: LineProperties

Parameters:

this (LineProperties) : DrawingTypes/LineProperties object

sortKeys (bool) : If set to true, string output is sorted by keys.

sortOrder (int) : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

includeKeys (array) : Array of string containing selective keys. Optional parmaeter. If not provided, all the keys are considered

Returns: string representation of DrawingTypes/LineProperties

method tostring(this, sortKeys, sortOrder, includeKeys)