CMOfilt BacktestThis indicator plots a CMO which ignores price changes which are less

than a threshold value. CMO was developed by Tushar Chande. A scientist,

an inventor, and a respected trading system developer, Mr. Chande developed

the CMO to capture what he calls "pure momentum". For more definitive

information on the CMO and other indicators we recommend the book The New

Technical Trader by Tushar Chande and Stanley Kroll.

The CMO is closely related to, yet unique from, other momentum oriented

indicators such as Relative Strength Index, Stochastic, Rate-of-Change, etc.

It is most closely related to Welles Wilder`s RSI, yet it differs in several ways:

- It uses data for both up days and down days in the numerator, thereby directly

measuring momentum;

- The calculations are applied on unsmoothed data. Therefore, short-term extreme

movements in price are not hidden. Once calculated, smoothing can be applied to the

CMO, if desired;

- The scale is bounded between +100 and -100, thereby allowing you to clearly see

changes in net momentum using the 0 level. The bounded scale also allows you to

conveniently compare values across different securities.

You can change long to short in the Input Settings

Please, use it only for learning or paper trading. Do not for real trading.

Strategy!

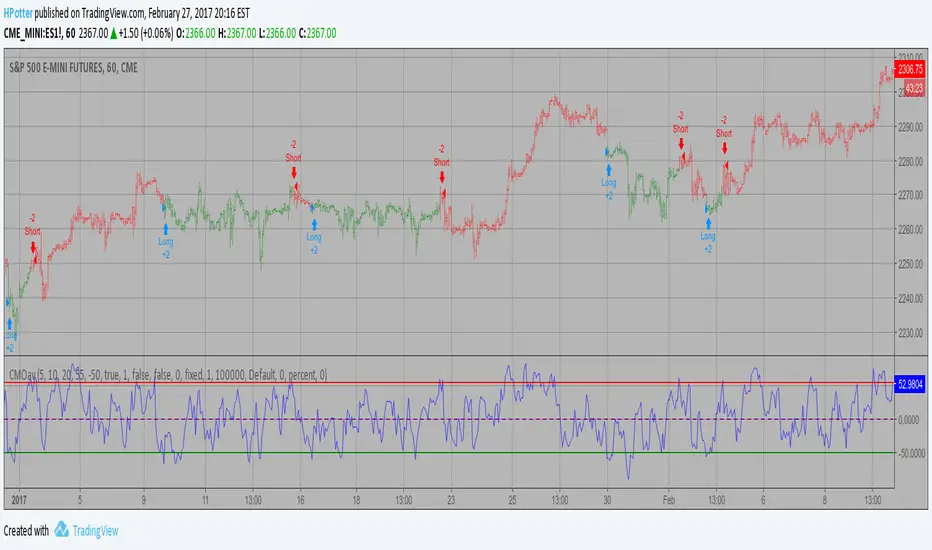

CMOav Backtest This indicator plots average of three different length CMO's. This indicator

was developed by Tushar Chande. A scientist, an inventor, and a respected

trading system developer, Mr. Chande developed the CMO to capture what he

calls "pure momentum". For more definitive information on the CMO and other

indicators we recommend the book The New Technical Trader by Tushar Chande

and Stanley Kroll.

You can change long to short in the Input Settings

Please, use it only for learning or paper trading. Do not for real trading.

Highest High and Lowest Low channel Backtest Highest High and Lowest Low channel Strategy

You can change long to short in the Input Settings

Please, use it only for learning or paper trading. Do not for real trading.

CMOabsav Backtest This indicator plots the absolute value of CMO averaged over three

different lengths. This indicator plots a classical-looking oscillator,

which is really an averaged value based on three different periods.

You can change long to short in the Input Settings

Please, use it only for learning or paper trading. Do not for real trading.

Gold/Silver 30m Only Strategy Buy/Sell SignalsIn my free time I felt like coding this strategy, and after backtesting it, it appears that the 30m time frame is the most profitable.

I only have been working on it for gold, but it should work similarly for silver as well.

This includes no pyramiding, and with pyramiding orders of 5, this strategy is upwards of 100% profitable.

Buy order - when price is above the 162 day EMA and RSI is less than 35

Sell order - when price is below the 162 day EMA and RSI is greater than 65

I will probably be adjusting it to increase the profitability and %success rate.

CMOabs Backtest This indicator plots the absolute value of CMO. CMO was developed by Tushar

Chande. A scientist, an inventor, and a respected trading system developer,

Mr. Chande developed the CMO to capture what he calls "pure momentum". For

more definitive information on the CMO and other indicators we recommend the

book The New Technical Trader by Tushar Chande and Stanley Kroll.

The CMO is closely related to, yet unique from, other momentum oriented indicators

such as Relative Strength Index, Stochastic, Rate-of-Change, etc. It is most closely

related to Welles Wilder`s RSI, yet it differs in several ways:

- It uses data for both up days and down days in the numerator, thereby directly

measuring momentum;

- The calculations are applied on unsmoothed data. Therefore, short-term extreme

movements in price are not hidden. Once calculated, smoothing can be applied to

the CMO, if desired;

- The scale is bounded between +100 and -100, thereby allowing you to clearly see

changes in net momentum using the 0 level. The bounded scale also allows you to

conveniently compare values across different securities.

You can change long to short in the Input Settings

Please, use it only for learning or paper trading. Do not for real trading.

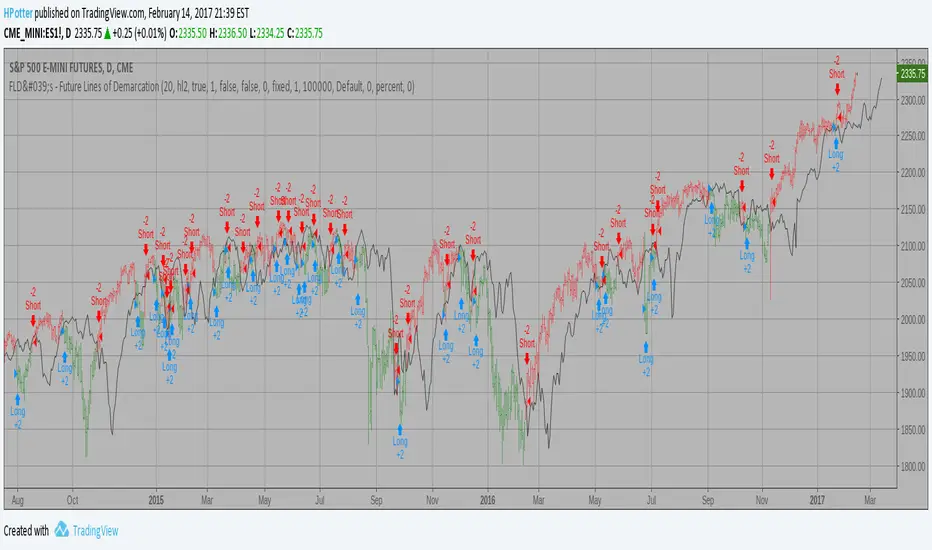

FLD's - Future Lines of Demarcation Backtest An FLD is a line that is plotted on the same scale as the price and is in fact the

price itself displaced to the right (into the future) by (approximately) half the

wavelength of the cycle for which the FLD is plotted. There are three FLD's that can be

plotted for each cycle:

An FLD based on the median price.

An FLD based on the high price.

An FLD based on the low price.

CMO & WMA Backtest This indicator plots Chande Momentum Oscillator and its WMA on the

same chart. This indicator plots the absolute value of CMO.

The CMO is closely related to, yet unique from, other momentum oriented

indicators such as Relative Strength Index, Stochastic, Rate-of-Change,

etc. It is most closely related to Welles Wilder?s RSI, yet it differs

in several ways:

- It uses data for both up days and down days in the numerator, thereby

directly measuring momentum;

- The calculations are applied on unsmoothed data. Therefore, short-term

extreme movements in price are not hidden. Once calculated, smoothing

can be applied to the CMO, if desired;

- The scale is bounded between +100 and -100, thereby allowing you to clearly

see changes in net momentum using the 0 level. The bounded scale also allows

you to conveniently compare values across different securities.

CMO (Chande Momentum Oscillator) Strategy Backtest This indicator plots Chande Momentum Oscillator. This indicator was

developed by Tushar Chande. A scientist, an inventor, and a respected

trading system developer, Mr. Chande developed the CMO to capture what

he calls "pure momentum". For more definitive information on the CMO and

other indicators we recommend the book The New Technical Trader by Tushar

Chande and Stanley Kroll.

The CMO is closely related to, yet unique from, other momentum oriented

indicators such as Relative Strength Index, Stochastic, Rate-of-Change,

etc. It is most closely related to Welles Wilder`s RSI, yet it differs

in several ways:

- It uses data for both up days and down days in the numerator, thereby

directly measuring momentum;

- The calculations are applied on unsmoothed data. Therefore, short-term

extreme movements in price are not hidden. Once calculated, smoothing

can be applied to the CMO, if desired;

- The scale is bounded between +100 and -100, thereby allowing you to

clearly see changes in net momentum using the 0 level. The bounded scale

also allows you to conveniently compare values across different securities.

Bull And Bear Balance Strategy Backtest This new indicator analyzes the balance between bullish and

bearish sentiment.

One can cay that it is an improved analogue of Elder Ray indicator.

To get more information please see "Bull And Bear Balance Indicator"

by Vadim Gimelfarb.

This modified strategy backtest from HPotter

Bill Williams Averages. 3Lines Backtest This indicator calculates 3 Moving Averages for default values of

13, 8 and 5 days, with displacement 8, 5 and 3 days: Median Price (High+Low/2).

The most popular method of interpreting a moving average is to compare

the relationship between a moving average of the security's price with

the security's price itself (or between several moving averages).

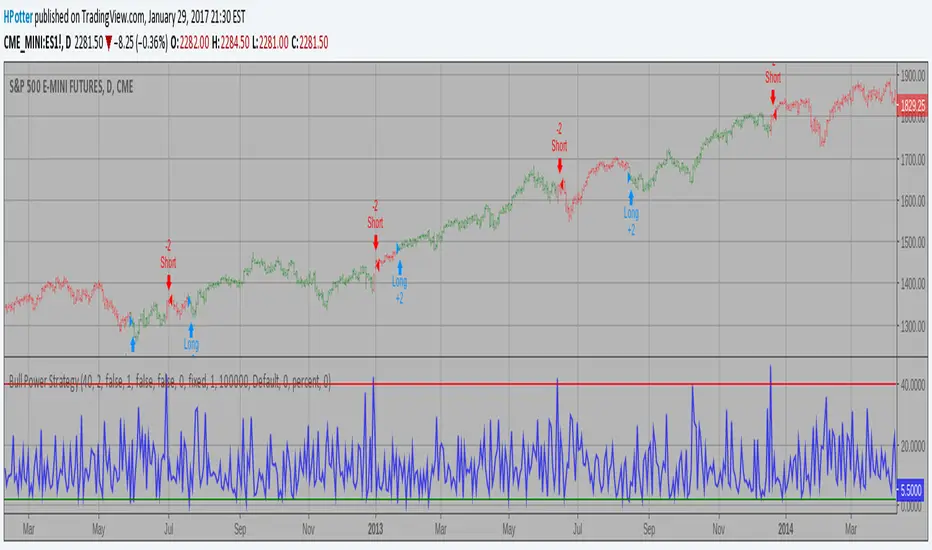

Bull Power Strategy Backtest Bull Power Indicator

To get more information please see "Bull And Bear Balance Indicator"

by Vadim Gimelfarb.

Bear Power Strategy Backtest Bear Power Indicator

To get more information please see "Bull And Bear Balance Indicator"

by Vadim Gimelfarb.

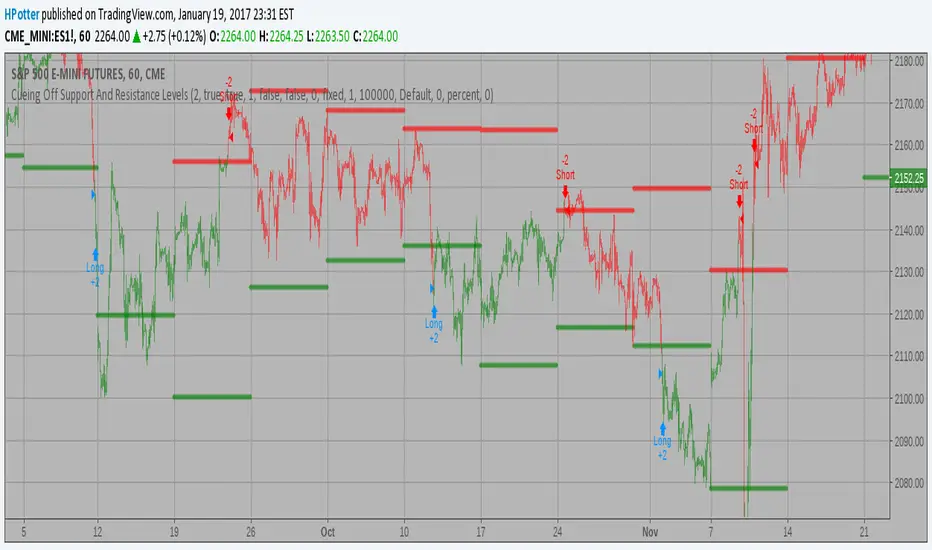

Cueing Off Support And Resistance Levels Backtest Cueing Off Support And Resistance Levels, by Thom Hartle

modified by HPotter for trade signals.

The related article is copyrighted material from Stocks & Commodities.

You can change long to short in the Input Settings

Please, use it only for learning or paper trading. Do not for real trading.

Z-Score Strategy Backtest The author of this indicator is Veronique Valcu. The z-score (z) for a data

item x measures the distance (in standard deviations StdDev) and direction

of the item from its mean (U):

z = (x-StdDev) / U

A value of zero indicates that the data item x is equal to the mean U, while

positive or negative values show that the data item is above (x>U) or below

(x Values of +2 and -2 show that the data item is two standard deviations

above or below the chosen mean, respectively, and over 95.5% of all data

items are contained within these two horizontal references (see Figure 1).

We substitute x with the closing price C, the mean U with simple moving

average (SMA) of n periods (n), and StdDev with the standard deviation of

closing prices for n periods, the above formula becomes:

Z_score = (C - SMA(n)) / StdDev(C,n)

The z-score indicator is not new, but its use can be seen as a supplement to

Bollinger bands. It offers a simple way to assess the position of the price

vis-a-vis its resistance and support levels expressed by the Bollinger Bands.

In addition, crossings of z-score averages may signal the start or the end of

a tradable trend. Traders may take a step further and look for stronger signals

by identifying common crossing points of z-score, its average, and average of average.

You can change long to short in the Input Settings

Please, use it only for learning or paper trading. Do not for real trading.

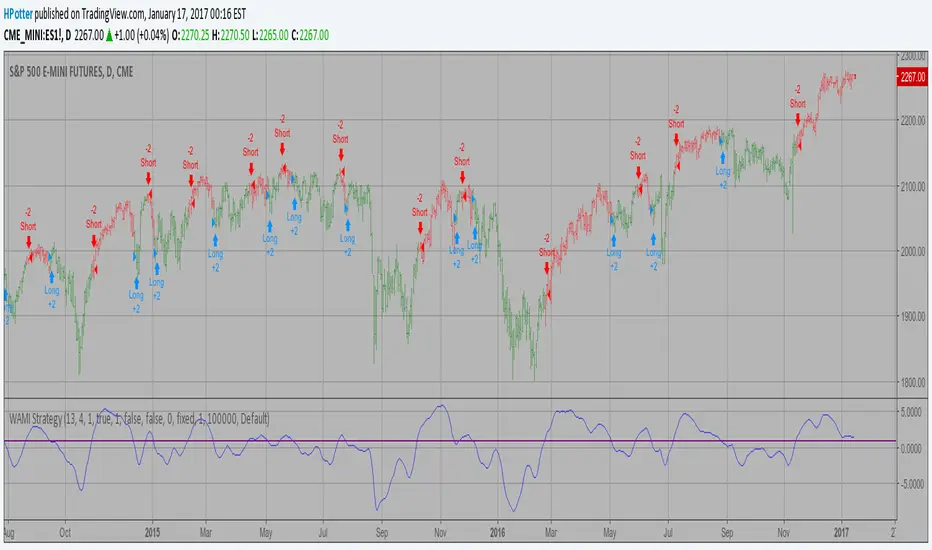

WAMI Strategy Backtest The WAMI-based trading lies in the application and iteration of the

optimization process until the indicated trades on past market data

give consistent, profitable results. It is rather difficult process

based on Fourier analysis.

You can to change Trigger parameter for to get best values of strategy.

You can change long to short in the Input Settings

Please, use it only for learning or paper trading. Do not for real trading.

Trend Trader Strategy Backtest This is plots the indicator developed by Andrew Abraham

in the Trading the Trend article of TASC September 1998

You can change long to short in the Input Settings

Please, use it only for learning or paper trading. Do not for real trading.

Strategy Stochastic Crossover Backtest This back testing strategy generates a long trade at the Open of the following

bar when the %K line crosses below the %D line and both are above the Overbought level.

It generates a short trade at the Open of the following bar when the %K line

crosses above the %D line and both values are below the Oversold level.

You can change long to short in the Input Settings

Please, use it only for learning or paper trading. Do not for real trading.

Strategy RSI Backtest The RSI is a very popular indicator that follows price activity.

It calculates an average of the positive net changes, and an average

of the negative net changes in the most recent bars, and it determines

the ratio between these averages. The result is expressed as a number

between 0 and 100. Commonly it is said that if the RSI has a low value,

for example 30 or under, the symbol is oversold. And if the RSI has a

high value, 70 for example, the symbol is overbought.

You can change long to short in the Input Settings

Please, use it only for learning or paper trading. Do not for real trading.

Percent change bar chart Strategy Backtest This histogram displays price or % change from previous bar.

Can be applied to any time frame.

This strategy buy if value above 0 and sell if value below 0.

You can change long to short in the Input Settings

Please, use it only for learning or paper trading. Do not for real trading.

Stochastic RSI StrategyThis is an an adaption of Binary option 1 minute by Maxim Chechel to a strategy. I have had success with this on FCT/BTC on Poloniex.

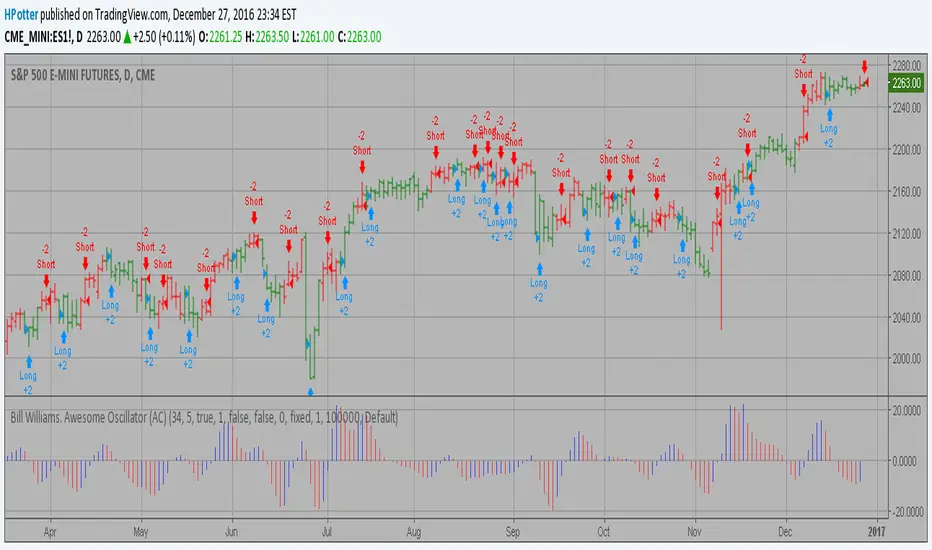

Bill Williams. Awesome Oscillator (AO) Backtest This indicator is based on Bill Williams` recommendations from his book

"New Trading Dimensions". We recommend this book to you as most useful reading.

The wisdom, technical expertise, and skillful teaching style of Williams make

it a truly revolutionary-level source. A must-have new book for stock and

commodity traders.

The 1st 2 chapters are somewhat of ramble where the author describes the

"metaphysics" of trading. Still some good ideas are offered. The book references

chaos theory, and leaves it up to the reader to believe whether "supercomputers"

were used in formulating the various trading methods (the author wants to come across

as an applied mathemetician, but he sure looks like a stock trader). There isn't any

obvious connection with Chaos Theory - despite of the weak link between the title and

content, the trading methodologies do work. Most readers think the author's systems to

be a perfect filter and trigger for a short term trading system. He states a goal of

10%/month, but when these filters & axioms are correctly combined with a good momentum

system, much more is a probable result.

There's better written & more informative books out there for less money, but this author

does have the "Holy Grail" of stock trading. A set of filters, axioms, and methods which are

the "missing link" for any trading system which is based upon conventional indicators.

This indicator plots the oscillator as a histogram where periods fit for buying are marked

as blue, and periods fit for selling as red. If the current value of AC (Awesome Oscillator)

is over the previous, the period is deemed fit for buying and the indicator is marked blue.

If the AC values is not over the previous, the period is deemed fir for selling and the indicator

is marked red.

You can change long to short in the Input Settings

Please, use it only for learning or paper trading. Do not for real trading.

Bill Williams. Awesome Oscillator (AC) Backtest This indicator plots the oscillator as a histogram where blue denotes

periods suited for buying and red . for selling. If the current value

of AO (Awesome Oscillator) is above previous, the period is considered

suited for buying and the period is marked blue. If the AO value is not

above previous, the period is considered suited for selling and the

indicator marks it as red.

You can change long to short in the Input Settings

Please, use it only for learning or paper trading. Do not for real trading.