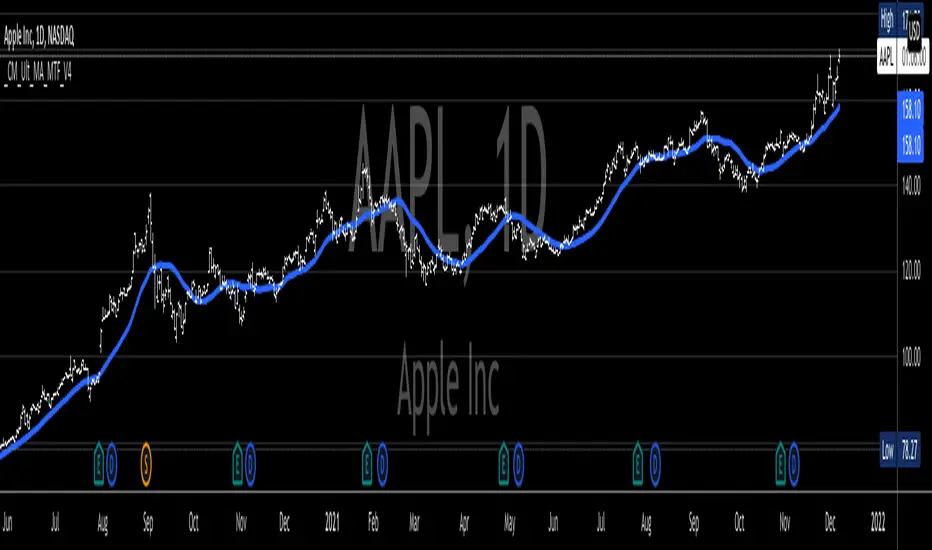

Tilson Bull-Bear-MarkerThe Tilson Bull-Bear marker is using 2 Tilson moving averages and their divergence to identify bull and bear trends and reversals (potential entry or exit points).

How to use it:

Fast T3 (thick line) above thin line / solid blue fill color = ongoing bull trend

Slow T3 (thin line) above thick line / solid red fill color = ongoing bear trend

Shrinking or expanding divergence between the lines = trend is getting hotter or cooling down

Fast T3 (thick line) changes color from blue to red = potential trend reversal from bullish to bearish

Fast T3 (thick line) changes color from red to blue = potential trend reversal from bearish to bullish

(No financial advise, for testing purposes only)

Pine Script® indicator