Multi-Symbol Volatility Tracker with Range DetectionMulti-Symbol Volatility Tracker with Range Detection

🎯 Main Purpose:

This indicator is specifically designed for scalpers to quickly identify symbols with high volatility that are currently in ranging conditions . It helps you spot the perfect opportunities for buying at lows and selling at highs repeatedly within the same trading session.

📊 Table Data Explanation:

The indicator displays a comprehensive table with 5 columns for 4 major symbols (GOLD, SILVER, NASDAQ, SP500):

SYMBOL: The trading instrument being analyzed

VOLATILITY: Color-coded volatility levels (NORMAL/HIGH/EXTREME) based on ATR values

Last Candle %: The percentage range of the most recent 5-minute candle

Last 5 Candle Avg %: Average percentage range over the last 5 candles

RANGE: Shows "YES" (blue) or "NO" (gray) indicating if the symbol is currently ranging

🔍 How to Identify Trading Opportunities:

Look for symbols that combine these characteristics:

RANGE column shows "YES" (highlighted in blue) - This means the symbol is moving sideways, perfect for range trading

VOLATILITY shows "HIGH" or "EXTREME" - Ensures there's enough movement for profitable scalping

Higher candlestick percentages - Indicates larger candle ranges, meaning more profit potential per trade

⚡ Optimal Usage:

Best Timeframe: Works optimally on 5-minute charts where the ranging patterns are most reliable for scalping

Trading Strategy: When you find a symbol with "YES" in the RANGE column, switch to that symbol and look for opportunities to buy near the lows and sell near the highs of the ranging pattern

Risk Management: Higher volatility symbols offer more profit potential but require tighter risk management

⚙️ Settings:

ATR Length: Adjusts the Average True Range calculation period (default: 14)

Range Sensitivity: Fine-tune range detection sensitivity (0.1-2.0, lower = more sensitive)

💡 Pro Tips:

The indicator updates in real-time, so monitor for symbols switching from "NO" to "YES" in the RANGE column

Combine HIGH/EXTREME volatility with RANGE: YES for the most profitable scalping setups

Use the candlestick percentages to gauge potential profit per trade - higher percentages mean more movement

The algorithm uses advanced statistical analysis including standard deviation, linear regression slopes, and range efficiency to accurately detect ranging conditions

Perfect for day traders and scalpers who want to quickly identify which symbols offer the best ranging opportunities for consistent buy-low, sell-high strategies.

Volatility

Stiffness IndexStiffness Index Indicator

Overview

The Stiffness Index is a technical analysis indicator created by Markos Katsanos and first introduced in the November 2018 issue of Technical Analysis of Stocks & Commodities magazine. This indicator attempts to recognize strong price trends by counting the number of times price was above the 100-day moving average during the indicator period.

Core Philosophy

The premise is the fewer number of times price penetrates the MA, the stronger the trend. The philosophy behind this indicator is that traders should trade when the trend is at its strongest point - when the trend is at its "stiffest". Based on the observation that in strong long-lasting uptrends, price seldom penetrates the 100-bar simple moving average, this indicator helps assess the quality and strength of an uptrend.

How It Works

The Stiffness Index operates through several key components:

1. Moving Average Baseline: Uses a 100-period moving average as the primary reference level

2. Volatility Threshold: Includes a volatility threshold to eliminate minor movements - typically 0.2 standard deviations to reject minimal penetrations above the moving average

3. Counting Mechanism: Calculates the stiffness coefficient as the ratio of the number of times the price has closed above the moving average during the indicator period to the length of that period

4. Smoothing: Applies additional smoothing to the final result for cleaner signals

Key Components

Input Parameters

- Period 1 (100): The moving average period for the baseline calculation

- MA Method 1: Type of moving average for the baseline (SMA, EMA, SMMA, LWMA)

- Summation Period (60): The lookback period for counting closes above the moving average

- Period 2 (3): Smoothing period for the final signal line

- MA Method 2: Smoothing method for the signal line

- Threshold Level (80): Reference level for identifying strong trends

Visual Elements

- Blue Signal Line: The main stiffness reading showing trend strength

- Dotted Line: Adjustable threshold level for reference

Interpretation and Trading Applications

Signal Readings

- High Values (Above Threshold): Indicates a "stiff" trend where price consistently stays above the moving average with minimal penetrations

- Low Values (Below Threshold): Suggests a weaker trend with frequent penetrations of the moving average

- Original threshold levels mentioned in research range from 75-95

Trading Strategy

The original strategy suggests entering long positions when the stiffness reading reaches 90 or higher, with exits when the reading drops below 50. Some implementations use a threshold of 75 for entry confirmation.

Key Characteristics

- Designed primarily for stocks and instruments with upward bias

- Trades infrequently - typically about once per year when using strict parameters

- Best suited for trend-following strategies in strongly trending markets

Advantages

- Trend Quality Assessment: Quantifies the "stiffness" or quality of trends

- Volatility Filtering: Built-in volatility threshold reduces false signals from minor price movements

- Objective Measurement: Provides a numerical assessment of trend strength

- Customizable: Multiple parameters allow adaptation to different markets and timeframes

Best Practices

- Use in conjunction with baseline trend indicators for confirmation

- Most effective in markets with strong directional bias

- Consider the low frequency of signals when developing trading strategies

- May not be suitable for instruments that "twitch up and down" frequently

*Note: This indicator is specifically designed to identify and trade the strongest trending periods, which naturally results in fewer but potentially higher-quality trading opportunities.*

Options Max Pain Calculator [BackQuant]Options Max Pain Calculator

A visualization tool that models option expiry dynamics by calculating "max pain" levels, displaying synthetic open interest curves, gamma exposure profiles, and pin-risk zones to help identify where market makers have the least payout exposure.

What is Max Pain?

Max Pain is the theoretical expiration price where the total dollar value of outstanding options would be minimized. At this price level, option holders collectively experience maximum losses while option writers (typically market makers) have minimal payout obligations. This creates a natural gravitational pull as expiration approaches.

Core Features

Visual Analysis Components:

Max Pain Line: Horizontal line showing the calculated minimum pain level

Strike Level Grid: Major support and resistance levels at key option strikes

Pin Zone: Highlighted area around max pain where price may gravitate

Pain Heatmap: Color-coded visualization showing pain distribution across prices

Gamma Exposure Profile: Bar chart displaying net gamma at each strike level

Real-time Dashboard: Summary statistics and risk metrics

Synthetic Market Modeling**

Since Pine Script cannot access live options data, the indicator creates realistic synthetic open interest distributions based on configurable market parameters including volume patterns, put/call ratios, and market maker positioning.

How It Works

Strike Generation:

The tool creates a grid of option strikes centered around the current price. You can control the range, density, and whether strikes snap to realistic market increments.

Open Interest Modeling:

Using your inputs for average volume, put/call ratios, and market maker behavior, the indicator generates synthetic open interest that mirrors real market dynamics:

Higher volume at-the-money with decay as strikes move further out

Adjustable put/call bias to reflect current market sentiment

Market maker inventory effects and typical short-gamma positioning

Weekly options boost for near-term expirations

Pain Calculation:

For each potential expiry price, the tool calculates total option payouts:

Call options contribute pain when finishing in-the-money

Put options contribute pain when finishing in-the-money

The strike with minimum total pain becomes the Max Pain level

Gamma Analysis:

Net gamma exposure is calculated at each strike using standard option pricing models, showing where hedging flows may be most intense. Positive gamma creates price support while negative gamma can amplify moves.

Key Settings

Basic Configuration:

Number of Strikes: Controls grid density (recommended: 15-25)

Days to Expiration: Time until option expiry

Strike Range: Price range around current level (recommended: 8-15%)

Strike Increment: Spacing between strikes

Market Parameters:

Average Daily Volume: Baseline for synthetic open interest

Put/Call Volume Ratio: Market sentiment bias (>1.0 = bearish, <1.0 = bullish) It does not work if set to 1.0

Implied Volatility: Current option volatility estimate

Market Maker Factors: Dealer positioning and hedging intensity

Display Options:

Model Complexity: Simple (line only), Standard (+ zones), Advanced (+ heatmap/gamma)

Visual Elements: Toggle individual components on/off

Theme: Dark/Light mode

Update Frequency: Real-time or daily calculation

Reading the Display

Dashboard Table (Top Right):

Current Price vs Max Pain Level

Distance to Pain: Percentage gap (smaller = higher pin risk)

Pin Risk Assessment: HIGH/MEDIUM/LOW based on proximity and time

Days to Expiry and Strike Count

Model complexity level

Visual Elements:

Red Line: Max Pain level where payout is minimized

Colored Zone: Pin risk area around max pain

Dotted Lines: Major strike levels (green = support, orange = resistance)

Color Bar: Pain heatmap (blue = high pain, red = low pain/max pain zones)

Horizontal Bars: Gamma exposure (green = positive, red = negative)

Yellow Dotted Line: Gamma flip level where hedging behavior changes

Trading Applications

Expiration Pinning:

When price is near max pain with limited time remaining, there's increased probability of gravitating toward that level as market makers hedge their positions.

Support and Resistance:

High open interest strikes often act as magnets, with max pain representing the strongest gravitational pull.

Volatility Expectations:

Above gamma flip: Expect dampened volatility (long gamma environment)

Below gamma flip: Expect amplified moves (short gamma environment)

Risk Assessment:

The pin risk indicator helps gauge likelihood of price manipulation near expiry, with HIGH risk suggesting potential range-bound action.

Best Practices

Setup Recommendations

Start with Model Complexity set to "Standard"

Use realistic strike ranges (8-12% for most assets)

Set put/call ratio based on current market sentiment

Adjust implied volatility to match current levels

Interpretation Guidelines:

Small distance to pain + short time = high pin probability

Large gamma bars indicate key hedging levels to monitor

Heatmap intensity shows strength of pain concentration

Multiple nearby strikes can create wider pin zones

Update Strategy:

Use "Daily" updates for cleaner visuals during trading hours

Switch to "Every Bar" for real-time analysis near expiration

Monitor changes in max pain level as new options activity emerges

Important Disclaimers

This is a modeling tool using synthetic data, not live market information. While the calculations are mathematically sound and the modeling realistic, actual market dynamics involve numerous factors not captured in any single indicator.

Max pain represents theoretical minimum payout levels and suggests where natural market forces may create gravitational pull, but it does not guarantee price movement or predict exact expiration levels. Market gaps, news events, and changing volatility can override these dynamics.

Use this tool as additional context for your analysis, not as a standalone trading signal. The synthetic nature of the data makes it most valuable for understanding market structure and potential zones of interest rather than precise price prediction.

Technical Notes

The indicator uses established option pricing principles with simplified implementations optimized for Pine Script performance. Gamma calculations use standard financial models while pain calculations follow the industry-standard definition of minimized option payouts.

All visual elements use fixed positioning to prevent movement when scrolling charts, and the tool includes performance optimizations to handle real-time calculation without timeout errors.

StdDev Supertrend {CHIPA}StdDev Supertrend ~ C H I P A is a supertrend style trend engine that replaces ATR with standard deviation as the volatility core. It can operate on raw prices or log return volatility, with optional smoothing to control noise.

Key features include:

Supertrend trailing rails built from a stddev scaled envelope that flips the regime only when price closes through the opposite rail.

Returns-based mode that scales volatility by log returns for more consistent behavior across price regimes.

Optional smoothing on the volatility input to tune responsiveness versus stability.

Directional gap fill between price and the active trend line on the main chart; opacity adapts to the distance (vs ATR) so wide gaps read stronger and small gaps stay subtle.

Secondary pane view of the rails with the same adaptive fade, plus an optional candle overlay for context.

Clean alerts that fire once when state changes

Use cases: medium-term trend following, stop/flip systems, and visual regime confirmation when you prefer stddev-based distance over ATR.

Note: no walk-forward or robustness testing is implied; parameter choices and risk controls are on you.

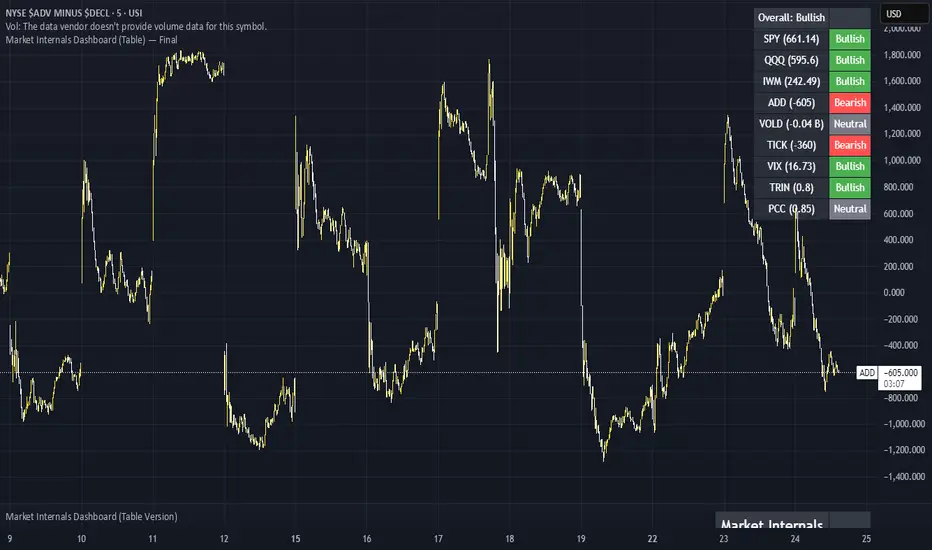

Market Internals Dashboard (Table) v5 - FixedHas a Dashboard for Market Internals and 3 Indices, very helpful

Institutional Levels (CNN) - [PhenLabs]📊Institutional Levels (Convolutional Neural Network-inspired)

Version : PineScript™v6

📌Description

The CNN-IL Institutional Levels indicator represents a breakthrough in automated zone detection technology, combining convolutional neural network principles with advanced statistical modeling. This sophisticated tool identifies high-probability institutional trading zones by analyzing pivot patterns, volume dynamics, and price behavior using machine learning algorithms.

The indicator employs a proprietary 9-factor logistic regression model that calculates real-time reaction probabilities for each detected zone. By incorporating CNN-inspired filtering techniques and dynamic zone management, it provides traders with unprecedented accuracy in identifying where institutional money is likely to react to price action.

🚀Points of Innovation

● CNN-Inspired Pivot Analysis - Advanced binning system using convolutional neural network principles for superior pattern recognition

● Real-Time Probability Engine - Live reaction probability calculations using 9-factor logistic regression model

● Dynamic Zone Intelligence - Automatic zone merging using Intersection over Union (IoU) algorithms

● Volume-Weighted Scoring - Time-of-day volume Z-score analysis for enhanced zone strength assessment

● Adaptive Decay System - Intelligent zone lifecycle management based on touch frequency and recency

● Multi-Filter Architecture - Optional gradient, smoothing, and Difference of Gaussians (DoG) convolution filters

🔧Core Components

● Pivot Detection Engine - Advanced pivot identification with configurable left/right bars and ATR-normalized strength calculations

● Neural Network Binning - Price level clustering using CNN-inspired algorithms with ATR-based bin sizing

● Logistic Regression Model - 9-factor probability calculation including distance, width, volume, VWAP deviation, and trend analysis

● Zone Management System - Intelligent creation, merging, and decay algorithms for optimal zone lifecycle control

● Visualization Layer - Dynamic line drawing with opacity-based scoring and optional zone fills

🔥Key Features

● High-Probability Zone Detection - Automatically identifies institutional levels with reaction probabilities above configurable thresholds

● Real-Time Probability Scoring - Live calculation of zone reaction likelihood using advanced statistical modeling

● Session-Aware Analysis - Optional filtering to specific trading sessions for enhanced accuracy during active market hours

● Customizable Parameters - Full control over lookback periods, zone sensitivity, merge thresholds, and probability models

● Performance Optimized - Efficient processing with controlled update frequencies and pivot processing limits

● Non-Repainting Mode - Strict mode available for backtesting accuracy and live trading reliability

🎨Visualization

● Dynamic Zone Lines - Color-coded support and resistance levels with opacity reflecting zone strength and confidence scores

● Probability Labels - Real-time display of reaction probabilities, touch counts, and historical hit rates for active zones

● Zone Fills - Optional semi-transparent zone highlighting for enhanced visual clarity and immediate pattern recognition

● Adaptive Styling - Automatic color and opacity adjustments based on zone scoring and statistical significance

📖Usage Guidelines

● Lookback Bars - Default 500, Range 100-1000, Controls the historical data window for pivot analysis and zone calculation

● Pivot Left/Right - Default 3, Range 1-10, Defines the pivot detection sensitivity and confirmation requirements

● Bin Size ATR units - Default 0.25, Range 0.1-2.0, Controls price level clustering granularity for zone creation

● Base Zone Half-Width ATR units - Default 0.25, Range 0.1-1.0, Sets the minimum zone width in ATR units for institutional level boundaries

● Zone Merge IoU Threshold - Default 0.5, Range 0.1-0.9, Intersection over Union threshold for automatic zone merging algorithms

● Max Active Zones - Default 5, Range 3-20, Maximum number of zones displayed simultaneously to prevent chart clutter

● Probability Threshold for Labels - Default 0.6, Range 0.3-0.9, Minimum reaction probability required for zone label display and alerts

● Distance Weight w1 - Controls influence of price distance from zone center on reaction probability

● Width Weight w2 - Adjusts impact of zone width on probability calculations

● Volume Weight w3 - Modifies volume Z-score influence on zone strength assessment

● VWAP Weight w4 - Controls VWAP deviation impact on institutional level significance

● Touch Count Weight w5 - Adjusts influence of historical zone interactions on probability scoring

● Hit Rate Weight w6 - Controls prior success rate impact on future reaction likelihood predictions

● Wick Penetration Weight w7 - Modifies wick penetration analysis influence on probability calculations

● Trend Weight w8 - Adjusts trend context impact using ADX analysis for directional bias assessment

✅Best Use Cases

● Swing Trading Entries - Enter positions at high-probability institutional zones with 60%+ reaction scores

● Scalping Opportunities - Quick entries and exits around frequently tested institutional levels

● Risk Management - Use zones as dynamic stop-loss and take-profit levels based on institutional behavior

● Market Structure Analysis - Identify key institutional levels that define current market structure and sentiment

● Confluence Trading - Combine with other technical indicators for high-probability trade setups

● Session-Based Strategies - Focus analysis during high-volume sessions for maximum effectiveness

⚠️Limitations

● Historical Pattern Dependency - Algorithm effectiveness relies on historical patterns that may not repeat in changing market conditions

● Computational Intensity - Complex calculations may impact chart performance on lower-end devices or with multiple indicators

● Probability Estimates - Reaction probabilities are statistical estimates and do not guarantee actual market outcomes

● Session Sensitivity - Performance may vary significantly between different market sessions and volatility regimes

● Parameter Sensitivity - Results can be highly dependent on input parameters requiring optimization for different instruments

💡What Makes This Unique

● CNN Architecture - First indicator to apply convolutional neural network principles to institutional-level detection

● Real-Time ML Scoring - Live machine learning probability calculations for each zone interaction

● Advanced Zone Management - Sophisticated algorithms for zone lifecycle management and automatic optimization

● Statistical Rigor - Comprehensive 9-factor logistic regression model with extensive backtesting validation

● Performance Optimization - Efficient processing algorithms designed for real-time trading applications

🔬How It Works

● Multi-timeframe pivot identification - Uses configurable sensitivity parameters for advanced pivot detection

● ATR-normalized strength calculations - Standardizes pivot significance across different volatility regimes

● Volume Z-score integration - Enhanced pivot weighting based on time-of-day volume patterns

● Price level clustering - Neural network binning algorithms with ATR-based sizing for zone creation

● Recency decay applications - Weights recent pivots more heavily than historical data for relevance

● Statistical filtering - Eliminates low-significance price levels and reduces market noise

● Dynamic zone generation - Creates zones from statistically significant pivot clusters with minimum support thresholds

● IoU-based merging algorithms - Combines overlapping zones while maintaining accuracy using Intersection over Union

● Adaptive decay systems - Automatic removal of outdated or low-performing zones for optimal performance

● 9-factor logistic regression - Incorporates distance, width, volume, VWAP, touch history, and trend analysis

● Real-time scoring updates - Zone interaction calculations with configurable threshold filtering

● Optional CNN filters - Gradient detection, smoothing, and Difference of Gaussians processing for enhanced accuracy

💡Note

This indicator represents advanced quantitative analysis and should be used by traders familiar with statistical modeling concepts. The probability scores are mathematical estimates based on historical patterns and should be combined with proper risk management and additional technical analysis for optimal trading decisions.

Irrationality Index by CRYPTO_ADA_BTC"The market can be irrational longer than you can stay solvent" ~ John Maynard Keynes

This indicator, the Irrationality Index, measures how far the current market price has deviated from a smoothed estimate of its "fair value," normalized for recent volatility. It provides traders with a visual sense of when the market may be behaving irrationally, without giving direct buy or sell signals.

How it works:

1. Fair Value Calculation

The indicator estimates a "fair value" for the asset using a combination of a long-term EMA (exponential moving average) and a linear regression trend over a configurable period. This fair value serves as a smoothed baseline for price, balancing trend-following and mean-reversion.

2. Volatility-Adjusted Z-Score

The deviation between price and fair value is measured in standard deviations of recent log returns:

Z = (log(price) - log(fairValue)) / volatility

This standardization accounts for different volatility environments, allowing comparison across assets.

3. Irrationality Score (0–100)

The Z-score is transformed using a logistic mapping into a 0–100 scale:

- 50 → price near fair value (rational zone)

- >75 → high irrationality, price stretched above fair value

- >90 → extreme irrationality, unsustainable extremes

- <25 → high irrationality, price stretched below fair value

- <10 → extreme bearish irrationality

4. Price vs Fair Value (% deviation)

The indicator plots the percentage difference between price and fair value:

pctDiff = (price - fairValue) / fairValue * 100

- Positive values → Percentage above fair value (optimistic / overvalued)

- Negative values → Percentage below fair value (pessimistic / undervalued)

Visuals:

- Irrationality (%) Line (0–100) shows irrationality level.

- Background Colors: Yellow= high bullish irrationality, Green= extreme bullish irrationality, Orange= high bearish irrationality, Red= extreme bearish irrationality.

- Price - FairValue (%) plot: price deviation vs fair value (%), Colored green above 0 and red below 0.

- Label: display actual price, estimated fair value, and Z-score for the latest bar.

- Alerts: configurable thresholds for high and extreme irrationality.

How to read it:

- 50 → Market trading near fair value.

- >75 / >90 → Price may be irrationally high; risk of pullback increases.

- <25 / <10 → Price may be irrationally low; potential rebound zones, but trends can continue.

- Price - FairValue (%) plot → visual guide for % price stretch relative to fair value.

Notes / Warnings:

- Measures relative deviation, not fundamental value!

- High irrationality scores do not automatically indicate trades; markets can remain can be irrational longer than you can stay solvent .

- Best used with other tools: momentum, volume, divergence, and multi-timeframe analysis.

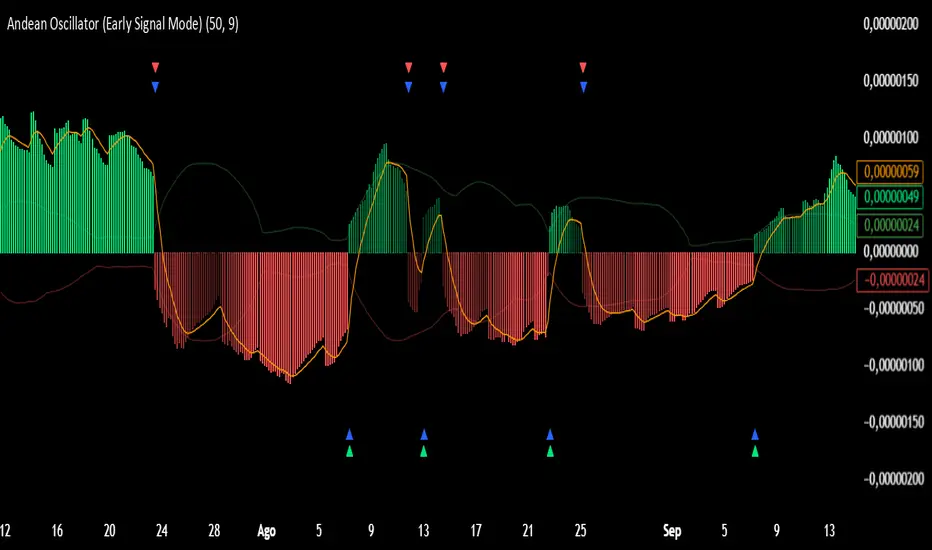

Andean Oscillator (Version 3.0 Sr.K)Andean Oscillator (Version 3.0 Sr.K)

This indicator is a momentum-based oscillator that measures the balance between bullish and bearish pressure.

🔧 How it works:

It calculates two adaptive envelopes around price and derives a "bullish" and "bearish" component.

The oscillator value is simply Bull - Bear, showing which side dominates.

A signal line (EMA of the oscillator) smooths the raw value.

Optionally, ±1σ levels are plotted to highlight statistically strong moves.

📊 What you see:

Histogram: Positive bars = bullish momentum, negative bars = bearish.

Orange Line: Signal line (EMA) used to confirm or anticipate reversals.

Zero Line: The equilibrium point. Crosses of this level signal a shift in market bias.

Green / Red Triangles: Buy and sell signals, either when crossing zero or crossing the signal line (depending on selected mode).

⚡ Early Signal Mode:

When enabled, signals trigger earlier — at the crossover between the oscillator and its signal line — allowing traders to enter potential reversals before a full zero-cross confirmation.

✅ Use cases:

Identify momentum shifts before price reversals.

Spot potential long/short setups with reduced lag.

Combine with price action or support/resistance for confirmation.

⚠️ Note: This is a tool for discretionary/manual trading. It does not open or close trades automatically. Always confirm with your own analysis and risk management.

VWAP + Range Breakout (Pre-Signal for Manual Entry)WHAT IT DOES

This tool highlights potential breakout opportunities when price sweeps the previous day’s high or low and aligns with VWAP and short-term range levels. It provides both pre-signals (early warnings) and confirmed signals (breakout closed) so traders can prepare before momentum accelerates.

Works on all timeframes and across markets (indices, forex, crypto). Especially useful during active London and New York sessions.

---

KEY FEATURES

Daily sweep logic: previous day high/low as liquidity reference

VWAP with cumulative calculation

Adjustable range breakout levels

Optional SMA trend filter

Session filter (London / NY trading hours)

Pre-Signal markers (early alert before breakout)

Confirmed LONG/SHORT signals after breakout close

Alerts for Pre-Long, Pre-Short, and Confirmed entries

---

HOW TO USE

1. Wait for price to sweep the previous day high/low.

2. Look for alignment with VWAP and the defined range breakout levels.

3. Use trend/session filters for higher accuracy.

4. Combine with your own risk management rules.

---

SETTINGS TIPS

Adjust range lookback for different timeframes (shorter for fast intraday, longer for higher timeframes).

Enable/disable session filters depending on your market.

Use SMA trend filter to stay aligned with higher-timeframe bias.

---

WHO IT’S FOR

Scalpers, intraday, and swing traders who want early signals when liquidity is taken and price is preparing for a breakout.

---

NOTES

For educational purposes only. No financial advice.

This script is open-source; redistribution follows TradingView rules.

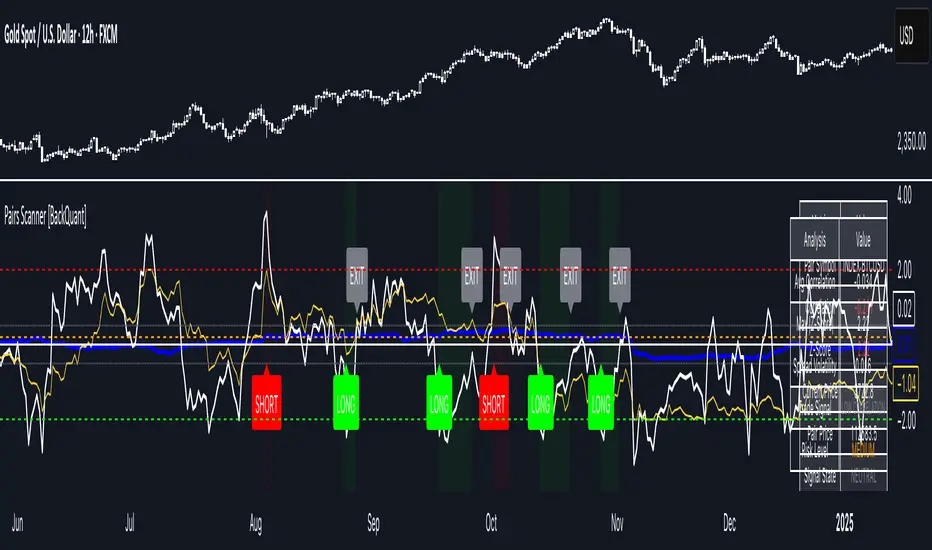

Pairs Trading Scanner [BackQuant]Pairs Trading Scanner

What it is

This scanner analyzes the relationship between your chart symbol and a chosen pair symbol in real time. It builds a normalized “spread” between them, tracks how tightly they move together (correlation), converts the spread into a Z-Score (how far from typical it is), and then prints clear LONG / SHORT / EXIT prompts plus an at-a-glance dashboard with the numbers that matter.

Why pairs at all?

Markets co-move. When two assets are statistically related, their relationship (the spread) tends to oscillate around a mean.

Pairs trading doesn’t require calling overall market direction you trade the relative mispricing between two instruments.

This scanner gives you a robust, visual way to find those dislocations, size their significance, and structure the trade.

How it works (plain English)

Step 1 Pick a partner: Select the Pair Symbol to compare against your chart symbol. The tool fetches synchronized prices for both.

Step 2 Build a spread: Choose a Spread Method that defines “relative value” (e.g., Log Spread, Price Ratio, Return Difference, Price Difference). Each lens highlights a different flavor of divergence.

Step 3 Validate relationship: A rolling Correlation checks if the pair is moving together enough to be tradable. If correlation is weak, the scanner stands down.

Step 4 Standardize & score: The spread is normalized (mean & variability over a lookback) to form a Z-Score . Large absolute Z means “stretched,” small means “near fair.”

Step 5 Signals: When the Z-Score crosses user-defined thresholds with sufficient correlation , entries print:

LONG = long chart symbol / short pair symbol,

SHORT = short chart symbol / long pair symbol,

EXIT = mean reversion into the exit zone or correlation failure.

Core concepts (the three pillars)

Spread Method Your definition of “distance” between the two series.

Guidance:

Log Spread: Focuses on proportional differences; robust when prices live on different scales.

Price Ratio: Classic relative value; good when you care about “X per Y.”

Return Difference: Emphasizes recent performance gaps; nimble for momentum-to-mean plays.

Price Difference: Straight subtraction; intuitive for similar-scale assets (e.g., two ETFs).

Correlation A rolling score of co-movement. The scanner requires it to be above your Min Correlation before acting, so you’re not trading random divergence.

Z-Score “How abnormal is today’s spread?” Positive = chart richer than pair; negative = cheaper. Thresholds define entries/exits with transparent, statistical context.

What you’ll see on the chart

Correlation plot (blue line) with a dashed Min Correlation guide. Above the line = green zone for signals; below = hands off.

Z-Score plot (white line) with colored, dashed Entry bands and dotted Exit bands. Zero line for mean.

Normalized spread (yellow) for a quick “shape read” of recent divergence swings.

Signal markers :

LONG (green label) when Z < –Entry and corr OK,

SHORT (red label) when Z > +Entry and corr OK,

EXIT (gray label) when Z returns inside the Exit band or correlation drops below the floor.

Background tint for active state (faint green for long-spread stance, faint red for short-spread stance).

The two built-in dashboards

Statistics Table (top-right)

Pair Symbol Your chosen partner.

Correlation Live value vs. your minimum.

Z-Score How stretched the spread is now.

Current / Pair Prices Real-time anchors.

Signal State NEUTRAL / LONG / SHORT.

Price Ratio Context for ratio-style setups.

Analysis Table (bottom-right)

Avg Correlation Typical co-movement level over your window.

Max |Z| The recent extremes of dislocation.

Spread Volatility How “lively” the spread has been.

Trade Signal A human-readable prompt (e.g., “LONG A / SHORT B” or “NO TRADE” / “LOW CORRELATION”).

Risk Level LOW / MEDIUM / HIGH based on current stretch (absolute Z).

Signals logic (plain English)

Entry (LONG): The spread is unusually negative (chart cheaper vs pair) and correlation is healthy. Expect mean reversion upward in the spread: long chart, short pair.

Entry (SHORT): The spread is unusually positive (chart richer vs pair) and correlation is healthy. Expect mean reversion downward in the spread: short chart, long pair.

Exit: The spread relaxes back toward normal (inside your exit band), or correlation deteriorates (relationship no longer trusted).

A quick, repeatable workflow

1) Choose your pair in context (same sector/theme or known macro link). Think: “Do these two plausibly co-move?”

2) Pick a spread lens that matches your narrative (ratio for relative value, returns for short-term performance gaps, etc.).

3) Confirm correlation is above your floor no corr, no trade.

4) Wait for a stretch (Z beyond Entry band) and a printed LONG / SHORT .

5) Manage to the mean (EXIT band) or correlation failure; let the scanners’ state/labels keep you honest.

Settings that matter (and why)

Spread Method Defines the “mispricing” you care about.

Correlation Period Longer = steadier regime read, shorter = snappier to regime change.

Z-Score Period The window that defines “normal” for the spread; it sets the yardstick.

Use Percentage Returns Normalizes series when using return-based logic; keep on for mixed-scale assets.

Entry / Exit Thresholds Set your stretch and your target reversion zone. Wider entries = rarer but stronger signals.

Minimum Correlation The gatekeeper. Raising it favors quality over quantity.

Choosing pairs (practical cheat sheet)

Same family: two index ETFs, two oil-linked names, two gold miners, two L1 tokens.

Hedge & proxy: stock vs. sector ETF, BTC vs. BTC index, WTI vs. energy ETF.

Cross-venue or cross-listing: instruments that are functionally the same exposure but price differently intraday.

Reading the cues like a pro

Divergence shape: The yellow normalized spread helps you see rhythm fast spike and snap-back versus slow grind.

Corr-first discipline: Don’t fight the “Min Correlation” line. Good pairs trading starts with a relationship you can trust.

Exit humility: When Z re-centers, let the EXIT do its job. The edge is the journey to the mean, not overstaying it.

Frequently asked (quick answers)

“Long/Short means what exactly?”

LONG = long the chart symbol and short the pair symbol.

SHORT = short the chart symbol and long the pair symbol.

“Do I need same price scales?” No. The spread methods normalize in different ways; choose the one that fits your use case (log/ratio are great for mixed scales).

“What if correlation falls mid-trade?” The scanner will neutralize the state and print EXIT . Relationship first; trade second.

Field notes & patterns

Snap-back days: After a one-sided session, return-difference spreads often flag cleaner intraday mean reversions.

Macro rotations: Ratio spreads shine during sector re-weights (e.g., value vs. growth ETFs); look for steady corr + elevated |Z|.

Event bleed-through: If one symbol reacts to news and its partner lags, Z often flags a high-quality, short-horizon re-centering.

Display controls at a glance

Show Statistics Table Live state & key numbers, top-right.

Show Analysis Table Context/risk read, bottom-right.

Show Correlation / Spread / Z-Score Toggle the sub-charts you want visible.

Show Entry/Exit Signals Turn markers on/off as needed.

Coloring Adjust Long/Short/Neutral and correlation line colors to match your theme.

Alerts (ready to route to your workflow)

Pairs Long Entry Z falls through the long threshold with correlation above minimum.

Pairs Short Entry Z rises through the short threshold with correlation above minimum.

Pairs Trade Exit Z returns to neutral or the relationship fails your correlation floor.

Correlation Breakdown Rolling correlation crosses your minimum; relationship caution.

Final notes

The scanner is designed to keep you systematic: require relationship (correlation), quantify dislocation (Z-Score), act when stretched, stand down when it normalizes or the relationship degrades. It’s a full, visual loop for relative-value trading that stays out of your way when it should and gets loud only when the numbers line up.

Smart Money LITE — Daily Sweep → HQ Signals (VWAP • FVG • CHoCH) 🔗 PRO VERSION (VWAP + FVG + CHoCH — full confirmations, all timeframes):

chartedgepro.gumroad.com/l/rmnbhw

Daily liquidity sweep → confluence signals with VWAP, FVG & CHoCH. Works on all timeframes & markets (Indices, Forex, Crypto).

WHAT IT DOES

Smart Money LITE+ highlights high-quality LONG/SHORT signals only after daily liquidity is swept (previous day high/low) with confluence from VWAP, FVG and structure (BOS/CHoCH).

Works on all timeframes and across markets: indices, forex, crypto.

KEY FEATURES (Lite)

• Daily sweep logic (PDH/PDL) + previous day zones

• VWAP + deviation bands (optional) and proximity filter

• 3-bar FVG boxes (visual) with adjustable extension

• ATR/volatility filter, optional HTF trend filter

• Anti-spam cooldown, clean LONG/SHORT labels

• Alerts: HQ LONG / HQ SHORT

HOW TO USE

1. Wait for price to sweep PDH/PDL → indicator opens “signal window”.

2. Look for confluence: VWAP touch/proximity + CHoCH or BOS in direction.

3. Enter with proper risk management (stop beyond swing/zone, partials).

SETTINGS TIPS

• Enable “Require VWAP Confluence?” for strictest setups.

• Use “HTF Trend Filter?” to align with higher-timeframe EMA trend.

• Adjust “After sweep (bars)” to define signal validity window.

• FVGs are visual in Lite — advanced filtering and confirmation are in Pro.

WHO IT'S FOR

Scalpers, intraday, and swing traders looking for objective, visual signals based on liquidity sweeps and VWAP/FVG confluence.

PRO VERSION (full confirmations)

Adds advanced FVG/iFVG logic, more confluence filters, dynamic risk tools and extended alert packages — optimized for all timeframes.

👉 chartedgepro.gumroad.com/l/rmnbhw

NOTES

• For educational purposes only. No financial advice.

• “Lite” is open-source; redistribution of code follows TradingView rules.

Transaction Value Alert (4Cr+)Transactions with a value of INR 4 crore or above on a one-minute candle indicate FII or DII activity and confirms momentum and is an excellent indicator for the intraday trading

Japan Yen Carry Trade to Risk Ratio Sharpe Ratio By UncleBFMStep-by-Step Calculation in the ScriptFetch Rates:Pulls rates dynamically using request.security() from user-specified symbols (e.g., TVC:JP10Y for yen, TVC:US10Y for target). If unavailable (NA), uses fallback inputs (e.g., 0.25% for yen, 4.50% for target).

Converts rates to decimals: (target_rate - yen_rate) / 100.

Calculate Carry:Carry = (Target Rate - Yen Rate) / 100

Example: If US 10Y yield is 4.50% and Japan 10Y is 0.25%, carry = (4.50 - 0.25) / 100 = 0.0425 (4.25% annual yield).

Calculate Daily Log Returns:Log Returns = ln(Close / Close ), where Close is the current price of the pair (e.g., USDJPY) and Close is the previous day's price.

This measures daily percentage changes in a way suitable for volatility calculations.

Calculate Annualized Volatility:Volatility = Standard Deviation of Log Returns over a lookback period (default 63 days, ~3 months) × √252.

Example: If the standard deviation of USDJPY log returns is 0.005 (0.5% daily), annualized volatility = 0.005 × √252 ≈ 0.0794 (7.94%).

Compute the Ratio:Ratio = Carry / Volatility

Example: Using above, 0.0425 / 0.0794 ≈ 0.535.

If volatility is zero, the ratio is set to NA to avoid division errors.

Plot:Plots the ratio as a line, with optional thresholds (e.g., 0.2 for "high attractiveness") to guide interpretation.

NotesDynamic Rates: Using bond yields (e.g., TVC:JP10Y) or policy rates (e.g., ECONOMICS:JPINTR) makes the indicator responsive to historical and current rate changes, unlike static inputs.

Context: BIS reports use similar ratios to assess carry trade viability. For USDJPY in 2025, with Fed rates around 4.5% and BoJ at 0.25–0.5%, the carry is positive but sensitive to volatility spikes (e.g., during 2024 unwind events).

Usage: Apply to a yen pair chart (e.g., USDJPY, AUDJPY). Adjust symbols for the target currency (e.g., TVC:AU10Y for AUD). The ratio helps compare carry trade profitability across pairs or over time.

FlowSpike ES — BB • RSI • VWAP + AVWAP + News MuteThis indicator is purpose-built for E-mini S&P 500 (ES) futures traders, combining volatility bands, momentum filters, and session-anchored levels into a streamlined tool for intraday execution.

Key Features:

• ES-Tuned Presets

Automatically optimized settings for scalping (1–2m), daytrading (5m), and swing trading (15–60m) timeframes.

• Bollinger Band & RSI Signals

Entry signals trigger only at statistically significant extremes, with RSI filters to reduce false moves.

• VWAP & Anchored VWAPs

Session VWAP plus anchored VWAPs (RTH open, weekly, monthly, and custom) provide high-confidence reference levels used by professional order-flow traders.

• Volatility Filter (ATR in ticks)

Ensures signals are only shown when the ES is moving enough to offer tradable edges.

• News-Time Mute

Suppresses signals around scheduled economic releases (customizable windows in ET), helping traders avoid whipsaw conditions.

• Clean Alerts

Long/short alerts are generated only when all conditions align, with optional bar-close confirmation.

Why It’s Tailored for ES Futures:

• Designed around ES tick size (0.25) and volatility structure.

• Session settings respect RTH hours (09:30–16:00 ET), the period where most liquidity and institutional flows concentrate.

• ATR thresholds and RSI bands are pre-tuned for ES market behavior, reducing the need for manual optimization.

⸻

This is not a generic indicator—it’s a futures-focused tool created to align with the way ES trades day after day. Whether you scalp the open, manage intraday swings, or align to weekly/monthly anchored flows, FlowSpike ES gives you a clear, rules-based signal framework.

Simplified Wave Trend Overbought/OversoldThis is just a variation of the popular wave trend that I find to be nicer to look at.

SMC BOS - Structure Breaks & Median Continuation ProjectionsThis tool shows what usually happens after a Break of Structure (BOS).

It scans past BOS events on your chart, finds the ones most similar to the latest break (using ATR to filter by volatility), and then plots the median continuation path.

Optional percentile bands (P10–P90) display the possible range of outcomes around the median.

Key features:

• Automatic detection of bullish and bearish BOS events

• Library of past BOS with adjustable size and spacing

• ATR-based similarity and recency weighting

• Median continuation projections with optional percentile bands

• Customizable colors, signals, and stats table

• Works on any market and timeframe

Use cases:

• See how price typically behaves after a BOS

• Support SMC analysis with data-driven projections

• Improve trade planning by visualizing likely continuations

• Apply across crypto, forex, stocks, and futures

Originality:

Instead of only marking BOS, this script learns from history and projects forward the median path of the most similar past cases, adjusted for volatility. It turns BOS signals into practical continuation scenarios.

Instructions:

Add the indicator to your chart. When a BOS is detected, the projection is drawn automatically.

Use the settings to adjust the library, ATR weighting, projection style, percentile bands, and the display of signals or stats.

For questions or customization, contact Julien Eche (Julien_Eche) on TradingView.