DYCL RSI Breakout - D timeframeDYCL Dynamic cables daily chart. After exiting parallel channel, DYCL made double top formation and fell 41% breaking down neckline during Jan-Mar '25 correction despite good Q3 result YoY.

Now Daily chart displaying double bottom formation in price chart and RSI.

Mar 18 shows bullish harami and Mar 19 shows inverted hammer. Bullish patterns in daily chart. So far volume isn't satisfactory. May 17 (this week) Weekly chart shows hammer pattern, but RSI is taking nose dive. Let's see if daily chart makes the weekly chart better in upcoming days.

Considering demand in cables, DYCL is a good bet. I don't think recent entry of big player (Ultratech cement) to cable industry would affect much atleast for next year.

Cables

Polycab - Descending Broadening WedgeCables have good demand. Polycab making bullish breakout from descending broadening wedge pattern and the subsequent targets are 5528.50, 5929.85, 6403.60 and the weekly pivot is at 6494.00. Around this level is 61.8% fib level 6427.55 so there is more supply (selling) in this point.

Power Cables - Price, RSI breakout after all time support Cables - Power Custom Index D chart. After bearish shark harmonic pattern custom index took all time support and taking bullish reversal. RSI breakout. And trendline breakout as well in price chart.

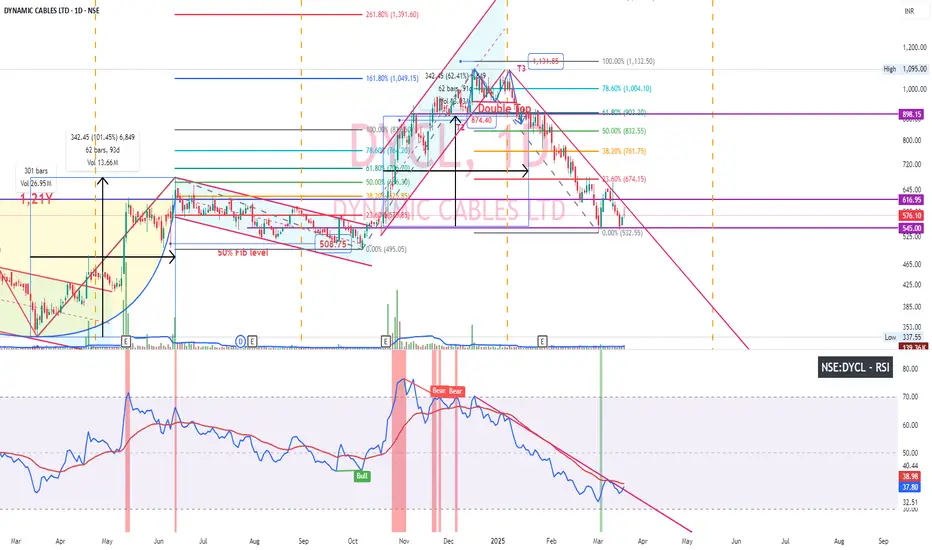

Dynamic cables Triangle Breakout RoaringTriangle pattern breakout. After hitting T2 1131.85, Will head to 1391.60 which is 261.8% Fib level

Cables - Power Potential breakoutCables looking good. Huge demand in cables for next 5 years across multiple sectors. Every player in the industry will get a pie of that demand. RSI daily chart double bottom looking for breakout. Price chart made trendline breakout.

Cables next rallyIndustry is experiencing robust demand environment and Polycab is well-positioned to capitalize on this favourable market dynamics.

India Ratings has improved the outlook on Polycab's credit rating to “positive” from the earlier “on watch with negative implication”

Polycab's in the process of calibrating new mid-term guidance and will be releasing the new guidance during the course of this financial year

RDSS Govt scheme will give good orderbook

Polycab working on 4 areas

Improving our reach

Product development

Brand positioning

Influencer management

Every quarter, Polycab adding new geography to supply its inventory

Working on 1000 to 1100cr capex to cater increased demand in next few years. 280Cr capex already done.

Capacity utilization in Q1 70-75%

In power transmission distribution sector, component of cable supply is high than other sectors. Cables 75% and wires 25% contribution.

Wire contribution would increase in upcoming quarters between 4 to 8 as real estate projects are in progress.

Framed index with Kei, Polycab, RRkabel, Fincables. Fib target is double of current. Target 29987.45 of this index.

Demand in cablesInfrastructure, Railways, Power all these sectors/Industries are bullish and have demand. Cables top player polycab has informed there will be enough demand that everyone will get a good pie in cables industry. Among cables, fundamentals of Dynamic cables is good and also making cup & handle pattern. This company too has huge potential for growth.

Cables breaking outPolycab leader of cables. Custom index created among Kei, Polycab, RRKables, Fincables.

Polycab - Wires & Cables demand in multiple sectorsConcall

Polycab...3K Cr Capex over 3Y. A bit towards backward integration(improves efficiency) & FMEG segment

Seen 30-40% volume growth in Q4 & last year. Industry at 22% growth

No material impact in pricing pressure despite rise in commodities(copper & Aluminium) pricing. Mgmt seems to have witnessed this

G8 demand in Infrastructure, Power, Renewable energy, EV, Railways sectors...and so capacity expansion.

Seems to be an article published mentioning power deficit in India in June

12-13% consistent margins achievable over long time

Distributors playing key role in sales.. Cuz only 10% customers directly buying from company. 89-90% sales is thro' distributors...

RDSS govt project open orders close to Rs. 50 Bn

FY 23 closed with 18K Cr revenue. Previously set target was 20K Cr top line by FY 26. But this will be revised(increased) by this FY

Polycab consolidationIf you look at Quarterly chart, We could see a pattern that after an year consolidation, 100% rise has happened. Could we expect Dec '23 - Dec '24 as consolidation period. Historically, 1st quarter of polycab hasn't performed except last year which was a surprise. Let's see what happens this year. Higher low hasn't formed yet in weekly chart.

Polycab - Valuations at its peakPolycab stellar performer among wires & cables. Polycab's guidance value is to achieve 20K Cr revenue(top-line) sales by 2026. And it appears they'll achieve ahead of timeline. Company expects volume growth to continue in the second half as well. As of 2023, 14K Cr sales.

Jefferies adjusted its price target for Polycab India from INR4,835 to INR6,220 and maintained its "buy" rating

Been riding this since 2021.

Earnings are growing good every quarter.

Revenue(8 to 16K Cr),

Net profit(766 to 1622),

EPS(50 to 100)

All these roughly doubled in 3Y since 2020.

Whereas Price grown 7 times. 740 to around 5K

Further in terms of valuations

PE (Price to Earnings ratio) Last 5Y avg is 31.426 Current 46.40

PB (Price to Book ratio) Last 5Y avg is 6.332 Current 11.45

PS (Price to Sales ratio) Last 5Y avg is 2.8. Current 4.7

I'll patiently wait for price near 50% Fib level which is 3350. 2600 is fair value.

Pivot R2 is at 3533.

Historical fall is 35% from ATH. So 35% from ATH is 3570.

Previous resistance breakout is at 3618 which could act as support.

So +/- 5 to 8% above 50% fib level.

I'll start watching from 3620 and accumulate gradually over fall & reversal.

Disclaimer: Entered and averaged up Since Mid 2021 till Mar 2023. Holding.

Buy Universal cable on dips.As can be seen the stock is going strongly moving upwards and is going fast. Advisable to buy on dips. Look for consolidation moves sideways for a couple of weeks to add a bigger position.