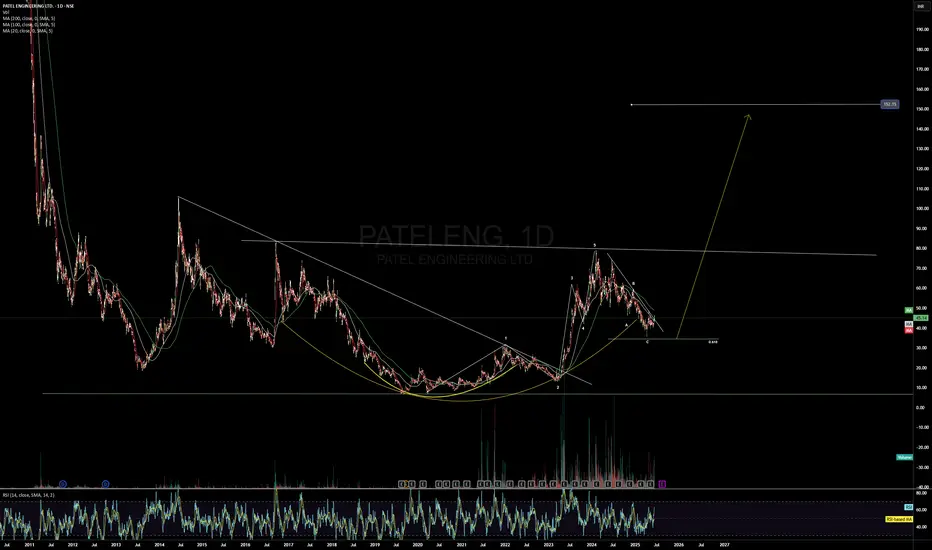

Patel Engineering - Multibagger with a turn around story ? Patel Engineering,

Looks like a turn around story in the making. After a rounded bottom it completed wave 1 at about 70 and now completed wave 2 around 35 in April.

Now its all set for the next impulse move ( wave 3 ) with a breakout happening. that should give multi bagger gains.

Details in chart.

Another possibility is that it might continue with the correction, by forming a flat pattern in which case a target of 60 to 70 is a given.

Some concerns are:

Promoters have pledged 88.7% of their holding.

Promoter holding has decreased over last 3 years: -18.5%

This is an effort in understanding Elliot Wave pattern and is for education purpose and not a stock recommendation.

Turnaround

ACE turning aroundLooks like ACE is done falling and is showing early signs of a turnaround after receiving its first sizeable defence order from the ministry of defence.

JYOTI STRUCTURES - Turnaround ?Jyoti Structures Limited (JSL) is an India-based engineering, procurement, and construction (EPC) company in the field of power transmission & distribution networks up to 765 Kilo Volts (kV) & 800 kV alternating current (AC) and high voltage direct current (HVDC) transmission lines and 765 kV Substations.

JSL offers a range of services including design & engineering, tower testing, manufacturing, construction & commissioning, sub-station design and engineering, and rural electrification.

JSL specializes in delivering turnkey projects involving designing, testing, manufacturing, erecting, and commissioning transmission lines, sub-stations, and power distribution projects in India and abroad.

JSL was one of the first 12 large accounts referred by the Reserve Bank of India under India’s new Insolvency and Bankruptcy Code 2016 (IBC). This was a significant event in the company’s history, marking a period of financial distress.

More recently, JSL has been working to improve its financial situation. In March 2024, the board of JSL approved the offer and issuance of fully paid-up equity shares of face value of ₹2 each to raise ₹175 crore through a rights issue. The rights issue price was set at ₹15 per equity share, including a premium of ₹13 per equity share. The rights issue period was scheduled to open on March 28, 2024, with a closing date on April 10, 2024.

The net proceeds from the issue were proposed to be utilized towards the payment of NCLT approved resolution plan dues. This move was seen as a part of the company’s efforts to resolve its financial issues and move towards a more stable financial future.

AMBALALSA - MONTHLY BREAKOUT WITH TURNAROUND POTENTIALHi Friends,

Today I'll like to share a very interesting company Ambalal Sarabhai Enterprises Ltd

Fundamentals:

MCap - 548Cr

Mcap/Sales - 3.16

Promoter Holding - 30.8%

PE - 96

On the onset, everything looks bad about this company except PRICE ACTION & FY23 AR (Especially Director's Report)

Some Key factors in the report

- Strategy of moving business to focussed subsidiaries has been successful

- Asence Pharma has started a new Oncology and Synthetic API plant

- Synbiotics is manufacturing an antifungal active ingredient - Amphotericin B

- Sarabhai M Chemicals has started manufacturing Vitamin C coated products

- Vovantis Labs has setup a state of art manufacturing facility to expand business

- CoSara DIagnostics has the exclusive manufacturing rights in India for the complete menu of its US partner - Co-Diagnostics

So many turnaround factors which is clearly indicated by Price Action

Technicals

On a monthly chart, PA has formed a CUP and HANDLE with breakout. This is a powerful indication of confirming the fundamentals stated above.

This pick is for those who like turnaround candidates (dark horse)

Hope you'll like this idea,

Thanks,

Stock-n-Shine

GTLINFRA is give good Price Moves.GTLINFRA is give good Price Moves. and its last 3-4 Qtr results was good . Most probability its break consolidation face and resistance. lets see next Moves.

Educational Purpose only.

HCC-Is it a U-turn multibagger?HCC is one of the oldest infra stock of India showing some change in fundamentals which is visible clearly on chart.

A weekly closing above 50 can open big targets for stock. A risky bet for multibagger returns.

Swing Stock Ideas with Good Level of BuyingStock Name

Wardwizard innovation

Revenue is Provide Good Side For this stock

and recent Development also Towards

CMP is 54

Target is 66-76-87

Getting a smell of "Turnaround candidate"Long term ---> Need to closely monitor coming results also

Chemical sector also waking up! Potential wealth creator in Long term if they can do what they comment.

BHEL : Will turning fundamentals lead to an unpredictable move ?NSE:BHEL quoted profits after many quarters. The rising demand from real estate will support the growth and earning of Bharat heavy electronics in near future. Investors can add this FALLEN ANGEL in their Portfolio.

- Strong balance sheet

- Good Promoter holding (63.17%)

The idea shared is for educational purpose only.

This tech hardware CMO could be the next turnaround story!NSE:OPTIEMUS

Technicals:

- Stock price has cleared 3 resistance zones in 3 days and broken out of a long consolidation

- Stock is nearing its all time high resistance zone with strength

- Stock price is showing high relative strength compared to NIFTY

Fundamentals:

- YoY data are bleak with low growth numbers

- However quarterly financials are encouraging with growing sales, margins and earnings

Business:

- Company produces wearables for brands such as Noise and Harman which are well known Gen Z brands

- They will commission new factory for wearables in Noida by December-end as part of its strategy to expand capacity to meet growing demand for smartwatches and truly wireless stereo (TWS) earbuds

- They intend to expand into batteries, displays, and microphone contract manufacturing

Source: Screener.in, Tickertape.in, LiveMint

Disclaimer: Not a recommendation. Only for research and education purposes.

KPIT TECHNOLOGIES CONSOLIDATION BREAKOUT COMMING AFTER FALLkpit technologies after correction in entire it sector is ready for another up move. it is bouncing between its 200 and 100 day moving average , which means a big move is about to come . it is also forming a small symmetrical triangle formation whose breakout is about to happen. if you see then the candles at the bottom or during this base formation have been very small , which means after correction there is some halt in selling and probability is that the buyers may come into picture now. so this stock looks extremely bullish also because of broad based it sector rally , and by the way this stock is fundamentally very good because of electric vehicle sector.

Higher Top Higher Bottom pattern on Nifty 15min chartNifty 15min chart is showing a higher top higher bottom pattern. A turnaround may have started.

Jindal Drilling Multi -Year Falling Channel BreakoutAlmost a 10 year falling channel breakout has happened in jindal drilling. Usually falling channel breakout gives a huge targets and is also in this case. The target could be somewhat 440 and the CMP is 142.

DLF 10 YEARS BREAKOUT [ COMMING OUT OF HIBERNATION]DLF Has given a big breakout after almost 10 years of consolidation.. Though the breakout happened earlier it got failed because of covid second wave. It has formed a big base at the bottom and usually the more bigger the base , the bigger is the upward move. Its like constructing a building , the bigger the base below the ground the stronger and taller is the building. Real estate sector is in boom. There are few reasons behind it. First of all RERA Act has reduced a lot of uncertainty and fraud in the sector.

The owner of the land are looking for bigger developers . Developers now have to open a escrow account for all transaction and make particular compliance certificates for

environmental, fire , legal etc. Skilled and educated people are now working and are being employed , where as earlier all unskilled people where working. The real estate sector is at almost rock bottom, so valuations are good. This sector can take time to move but looks really good both fundamentally and technically.

The Stock can take time to move Bearing the fact that there have been problem in this sector and company. But the targets are very high.

JCT Ltd: Turn around potential. Potential Multibagger.1. Current year sales trending at 600 crores. EBITDA at 28 crores.

2. Launched new line of anti-infective clothing which it believes will be in demand going forward

3. From yarn to fabric to stitching & sealing of PPE Suits,JCT Mills,Phagwara is doing it all in-house,following WHO guidelines.

4. JCT is making amazing PPE equipment ! They have risen from the ashes to fight the war against Covid ! They have a huge capacity.

5. The textiles ministry is in the process of obtaining approval of the Cabinet for the scheme of Mega Investment Textile Park. Under the scheme, seven Mega Textile Parks will be set up in the country over 3 years. JCT will be a direct beneficiary of this scheme.

TTK PRESTIGE - LONG

Potential Turnaround Stock - Positional Idea

TTK Prestige

LTP ~ INR 5984/-

Breakout At INR 6575/- Resistance At INR 7750/- Support At INR 5325/-

The stock from a technical standpoint is trading Above 3% to its 50DMA and comfortably placed above its 200DMA, around 10% above 200DMA.

50DSMA ~ 5774.40/- Trading above 50 Day SMA from 24th Dec 20

It needs to take support around the 50 DMA level to continue further upside move.

Stock is technically in a Mildly Bullish range

The technical trend has improved from Sideways on 24-Dec-20The stocks MACD and Bollinger Band technical factors are also Bullish

Say Yes to Yes BankBogged down by a few issues, Yes Bank is gamely soldiering on. With a strong banks consortium trying its best to pull it out, there could emerge a winner. Risk reward is very favourable. Any positive news flow can propel it and give 2x return at the very least. Accumulate...Break above 31 can prove decisive in the counter.

Coal India - above 133 - set for uptrend Incase if Market opens positive on Monday and price sustains above 133

can see clear turnaround in CoalIndia from lifetime low levels.

Watch it / Add to watch list for Monday

Turn round possibleUflex is in dntrend, but if 200 level sustains and mfi and adx shows divergence and strength may be a turnaround case, the company business seems good prospect. Huge Positive volumes at 200 138 and 106 can be seen earlier. Pls comment on my thoughts

ATGN LongFor the last five years the company has gone through a tough but the right transition from hardware to recurring software. For 20 years it reported Negative eps. The last 2 years it turned a slight profit and according to the conference call they expect it to continue. People havent looked at this stock in many years because of losses and no revenue growth. I think things are about to change as this last quarter the saas biz grew at over 40% topline but was masked by the decline in hardware which is now over. As revenue finally shows growth it will get recognized. Also the UC space has been consolidating MITL EGHT RING. I believe ATGN also has better technology in the financial UC space. Running an eps model for next year comes up w $0.18 assuming a 40x gives you a $7.20 target. Even if you use a conservative mult of 20x (1/2 its growth rate) you get a $3.60 stock. I'm sure more people on this site are better looking at technicals but in the 20 years this has only traded over 500k shares a few times so the stock is more than washed out w/ some very LT holders. Also its net asset value is .45 and that assumes 0 value for the business. Would love any feedback. I own a position in the company.