BT MA BandsThe BT MA Bands indicator is built around a central moving average (MA) with upper and lower bands derived from it, similar to Bollinger Bands but focused on exponential moving averages (EMAs) for smoother responsiveness.

The core idea is to visualize trend strength, volatility squeezes, and potential reversal points through dynamic bands that expand/contract based on price deviation. It includes trend-based color fills, entry/exit signals, an optional ATR (Average True Range) overlay for additional volatility bands, and flexible MA source options to adapt to different market conditions.

Inputs

MA Type and Length: Choose from EMA (default), SMA, WMA, or HMA. Default length is 20 periods, but adjustable (e.g., 10-50) for short-term scalping or longer swings.

Deviation Multiplier: Sets the band width as a multiple of the standard deviation from the MA (default: 2.0). Higher values create wider bands for trending markets; lower for ranging ones.

Source Data: Select price source for the MA calculation—close (default), open, high, low, (high+low)/2, or weighted (hlc3/hlcc4) to emphasize different aspects of price action.

ATR Toggle and Multiplier: Optional ATR-based outer bands (default off). When enabled, multiplier (default: 1.5) adds volatility sensitivity, helping filter noise in choppy conditions.

Signal Sensitivity: Threshold for generating buy/sell alerts (e.g., 0-100 scale; default 50) based on band crossovers or squeezes.

Style Options: Enable/disable fills, signals, and colors for personalization.

Visual Elements

Central MA Line: A solid line (e.g., blue by default) representing the chosen moving average, acting as the baseline.

Upper and Lower Bands: Dotted or dashed lines (green/red defaults) that flank the MA, widening during volatility and narrowing in consolidations.

Color-Changing Fills: The area between bands fills with color shifts—bullish (green) when price is above the MA and bands are expanding, bearish (red) when below and contracting, or neutral (gray) during flat trends.

Entry Signals: Arrow plots (up green for bullish, down red for bearish) appear on the chart when price crosses the bands or a squeeze resolves, with optional text labels like "Buy" or "Sell."

ATR Overlay (if enabled): Additional dashed outer bands in a lighter color (e.g., purple) to highlight extreme volatility zones.

How to Use It in Trading

Trend Identification: Use the central MA and band fills to gauge direction—price above the MA with green fills signals an uptrend (favor longs); below with red indicates downtrends (favor shorts). Narrow bands suggest a "squeeze" setup, often preceding big moves.

Entry Points:

Bullish Entries: Enter long when price breaks above the upper band on a bullish signal arrow, especially after a squeeze. Confirm with volume spike or RSI >50 on timeframes like 5m-1h for quick trades.

Bearish Entries: Enter short on a break below the lower band with a bearish arrow, post-squeeze. Ideal on 4h+ frames for swings, paired with MACD crossovers.

Exits and Risk Management: Exit longs when price hits the lower band or a bearish signal fires; vice versa for shorts. Set stops just beyond the opposite band (e.g., below lower for longs). Target 1.5-3x risk-reward, using ATR bands for trailing stops in volatile markets.

General Tips: Best in trending environments; avoid during news events causing false breakouts. Backtest parameters on historical data, and combine with other indicators like RSI or volume for confluence. It's great for spotting reversals but not infallible—always apply position sizing and monitor for band "walks" (price hugging one band) as continuation signals.

ATR

BT LigmaThe BT Ligma indicator combines momentum-based signals with volatility filters to identify potential trend reversals and high-probability entry points.

It uses a set of Exponential Moving Averages (EMAs) – typically a fast EMA (e.g., 9-period) crossing over a slower one (e.g., 21-period) – to generate baseline buy/sell signals. These are enhanced by a proprietary "Ligma Spread" filter, which measures the dynamic spread between short-term price action and a volatility envelope (similar to Bollinger Bands but customized with ATR multipliers). This filter helps weed out false signals in choppy markets by requiring a minimum spread threshold before confirming a trade alert.

BT Ligma allows a user to select up to 3 EMAs, the MA calculation method, and signal individual candles that cross EMA 1 & 2, or all 3 bands in the same bar.

Version 1.4, includes refined alert logic, including audio/visual notifications and optional trailing stops based on EMA alignments.

To use it effectively for trade entries:

Long (Buy) Entries: Look for a bullish EMA crossover (fast EMA above slow) combined with a positive Ligma Spread expansion (indicating increasing momentum). Enter when the signal fires on a close above the recent swing high, ideally on a timeframe like 15m or 1h for scalping/day trading. Pair this with volume confirmation or RSI above 50 to avoid overbought traps.

Short (Sell) Entries: Wait for a bearish EMA crossover (fast below slow) with a contracting or negative Ligma Spread (signaling potential downside volatility). Enter on a close below the recent swing low, using higher timeframes (e.g., 4h) for swing trades to capture larger moves.

General Tips: Always apply risk management – set stops below/above the slow EMA, target 2-3x risk-reward ratios, and avoid trading during low-liquidity periods. Backtest on historical data to tweak parameters, and combine with fundamentals like news events for better context.

Institutional Edge Pro v1.0 - 9.3/10 ConfidenceEducational 5-layer confirmation system combining institutional order flow concepts, trend analysis, and risk management principles. Features Order Block detection, adaptive stop losses (EMA 9x21), and probability scoring. For educational purposes only.

## ⚡ KEY FEATURES

### 🔍 5-Layer Confirmation System

- **Layer 0:** Market Regime Detection (30% weight) - ADX, Choppiness Index, Volatility, Volume

- **Layer 1:** Golden/Death Cross Trend Filter (20% weight) - EMA 50/200 with gradient confirmation

- **Layer 1.5:** Fast Death Cross Stop Loss - EMA 9/21 dynamic exits

- **Layer 2:** Smart Order Block Detection (20% weight) - Institutional footprint tracking

- **Layer 3:** Probabilistic Confirmations (20% weight) - RSI, MACD, Volume, Structure, Volatility

- **Layer 4:** Dynamic Risk Management (10% weight) - ATR-based adaptive stops

### 📊 Visual Dashboard

- **Regime Score:** 0-100 market health indicator

- **Trend Status:** Real-time BULL/BEAR/NONE classification

- **Trend Quality:** Freshness metric (degrades over time)

- **Order Block Status:** Active OB tracking with validation

- **Probability Scores:** Live Long/Short setup probabilities

Clean Industry DataClean Industry Data – Overview

Clean Industry Data is a utility tool designed to give traders an instant, structured view of key fundamental and volatility metrics directly on the chart. The script displays a compact, customizable information panel containing:

Industry & Sector

Market Cap and Free-Float Market Cap

Free-Float Percentage

Average Daily Rupee Volume

Relative Volume (R.Vol) based on daily volume

% from 10 / 21 / 50 EMAs (calculated on daily closes)

ADR (14-day) with threshold-based indicators

ATR (current timeframe) with colour-coded risk cues

All volume-based statistics are anchored to daily data, ensuring the values remain consistent across all timeframes. The display table supports flexible positioning, custom background/text colours, and adjustable text size.

This script is ideal for traders who want a quick, accurate snapshot of a stock’s liquidity, volatility, and broader classification — without digging through multiple menus or external sources.

ATM PROThe world’s strongest indicator that combines multiple indicators together, providing you with entry points, targets, and stop-loss levels with extreme accuracy. You can adjust its inputs to suit Forex and crypto pairs according to your needs. It contains these tools, and you can modify them based on your requirements.

المؤشر الاقوى عالميا الذي جمع عدة مؤشرات معا , من خلاله سيعطيك نقاط ( دخول واهداف وايقاف خسارة ) بدقة متناهية وتستطيع ان تعدل المدخلات ليتناسب مع ازواج الفوركس والكريبتو بشكل يتناسب مع ما تحتاجه

يحتوي على هذه الادوات ويمكنك تعديلها حسب متطلباتك

SHORT EMA

LONG EMA

TREND EMA

MACD SHORT

MACD LONG

MACD SIGNAL

RSI LENGTH

ATR LENGTH

VOLUME MULTIPLIER

ATR TARGET 1.2.3.4.5

STOP LOSS MULTIPLIER

BY ATM TEAM

Simple Price ChannelSimple Price Channel

This indicator plots a basic volatility-based channel around a moving average.

Features:

Midline using Simple Moving Average (SMA)

Upper & lower bands using ATR or true range

Channel fill for easy trend visualisation

This script is designed for educational and analytical purposes only.

It does not provide signals, alerts, or financial advice.

BT Aggressionv0.3.1 Beta Release

The BT Aggression Indicator is a high-resolution market sentiment and aggression tool for futures trading. It combines volume delta, volatility normalization, and dynamic smoothing to give traders real-time insight into market pressure.

Detailed description in future release.

Position Sizing Calculator (Real-Time) - Futures Edition█ SUMMARY

The following indicator is a Position Sizing Calculator based on Average True Range (ATR), originally developed by market technician J. Welles Wilder Jr., intended for real-time trading.

This script utilizes the user's account size, acceptable risk percentage, and a stop-loss distance based on ATR to dynamically calculate the appropriate position size for each trade in real time.

█ BACKGROUND

Developed for use on the Micro E-mini Nasdaq-100 futures (MNQ), this script provides traders with continuously updated dynamic position sizes. It enables traders to instantly determine the exact number of contracts to use when entering a trade while staying within their acceptable risk tolerance.

This real-time position sizing tool helps traders make well-informed decisions when planning trade entries and calculating maximum stop-loss levels, ultimately enhancing risk management.

█ USER INPUTS

Trading Account Size: Total dollar value of the user's trading account.

Acceptable Risk (%): Maximum percentage of the trading account that the user is willing to risk per trade.

ATR Multiplier for Stop-Loss: Multiplier used to determine the distance of the stop-loss from the current price, based on the ATR value.

ATR Length: The length of the lookback period used to calculate the ATR value.

Show Target Risk Row: Toggle to hide/show the Target Risk Row

SL Levels Display: Option to see Both, Long Only, Short Only, or None of the Stop Loss Level Values.

Contract Point Value ($): Point value per contract. Tooltip highlights common values.

Tick Size: Minimum Price Movement (Default set to 0.25)

Minimum Contracts: Override the Minimum Contracts per trade to a user selected value.

(May Exceed User's Target Risk)

TR-ATR-DATR+MAs shows the Range of selected Candle + 3 Moving Averages

True Range

Avg True Range

Daily Range

QuantMotions - TPR Sentinel LineTPR Sentinel Line is an advanced adaptive Support/Resistance system that combines multi-layered trend analysis with a directional Time-Price Ratio (TPR) engine. The indicator dynamically builds a stabilized support or resistance line that adjusts to market volatility, trend strength, ATR expansion and contraction, and real-time slope changes.

This creates a high-precision, self-adjusting trend barrier that acts as support in uptrends, resistance in downtrends, and a neutral anchor during sideways phases.

Key Features

✔ Adaptive Trend Base

- A composite trend model blending:

- Kijun-style midpoint

- Donchian midline

- SMA & EMA smoothing

This creates a stable baseline that reacts smoothly but reliably to structural trend shifts.

✔ Directional TPR Calculation

The indicator measures slope across short, medium, and long trend windows, normalizes it with ATR, and determines:

- Trend direction

- Trend strength

- Momentum quality

✔ Dynamic Support/Resistance Line

Depending on trend direction:

- In uptrends → the line becomes adaptive support

- In downtrends → the line becomes adaptive resistance

- In neutral phases → the line centers around the smoothed trend base

A built-in lag factor prevents unrealistic jumps and keeps the level stable.

✔ Automatic Support/Resistance Zones

The indicator expands the main line into upper and lower zones based on ATR and trend strength, creating a dynamic volatility envelope around the trend structure.

✔ Signals & Alerts

- Support bounce

- Resistance rejection

- Breakouts above/below the dynamic line

These events help identify high-probability continuation or reversal moments.

✔ Information Panel

A real-time status table displays:

- Trend direction

- Trend strength

- Current S/R level

🎯 Ideal For

- Precision entries on pullbacks

- Detecting trend shifts earlier

- Identifying strong or weak trend phases

- Adaptive take-profit and stop-loss zones

- Filtering false breakouts

💡 Summary

TPR Sentinel Line gives you a living, breathing support/resistance structure that evolves with the market.

Instead of relying on static levels, you get a continuously adapting trend barrier that reflects real strength, real volatility, and real momentum.

A powerful tool for traders who want structure, clarity, and trend confidence.

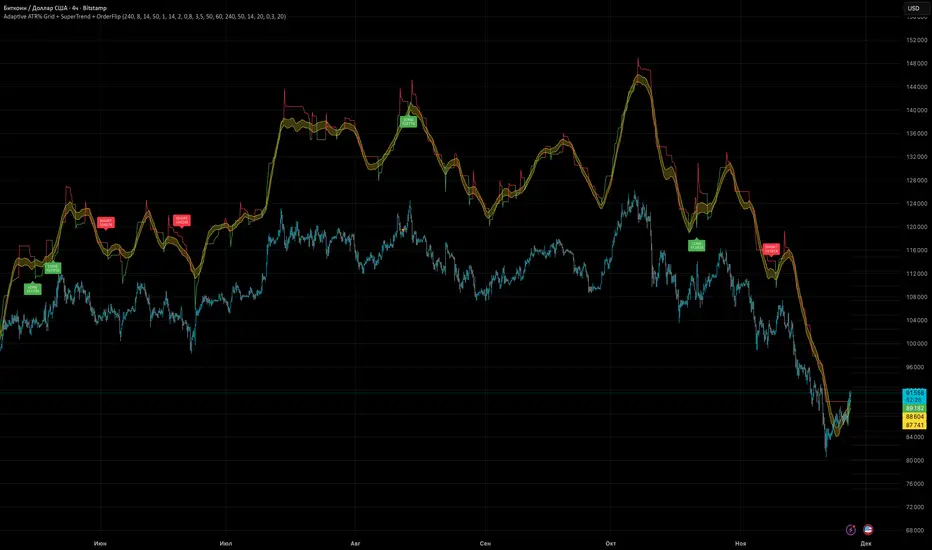

Adaptive ATR% Grid + SuperTrend + OrderFlipDescription:

This indicator combines multiple technical analysis tools to identify key price levels and trading signals:

ATR% Grid – automatic plotting of support and resistance levels based on current price and volatility (ATR). Useful for identifying potential targets and entry/exit zones.

SuperTrend – a classic trend indicator with an adaptive ATR multiplier that adjusts based on average volatility.

OrderFlip – identifies price reversal points relative to a moving average with ATR-based sensitivity, optionally filtered by OBV and DMI.

MTF Confirmation – multi-timeframe trend verification using EMA to reduce false signals.

Signal Labels – "LONG" and "SHORT" labels appear on the chart with an offset from the price for better visibility.

JSON Alerts – ready-to-use format for automated alerts, including price, SuperTrend direction, Fair Zone, and ATR%.

Features:

Fully compatible with Pine Script v6

Lines and signals are fixed on the chart, do not shift with new bars

Configurable grid, ATR, SuperTrend, and filter parameters

Works with MTF analysis and classic indicators (OBV/DMI)

Usage:

Best used with additional indicators and risk management strategies. ATR% Grid is ideal for both positional trading and intraday setups.

перевод на русский

Описание:

Этот индикатор объединяет несколько методов технического анализа для выявления ключевых уровней цены и сигналов на покупку/продажу:

Сетка ATR% (ATR% Grid) – автоматическое построение уровней поддержки и сопротивления на основе текущей цены и волатильности (ATR). Позволяет видеть потенциальные цели и зоны входа/выхода.

SuperTrend – классический трендовый индикатор с адаптивным множителем ATR, который корректируется на основе средней волатильности.

OrderFlip – определение моментов разворота цены относительно скользящей средней с учетом ATR, с возможностью фильтрации по OBV и DMI.

MTF-подтверждение – проверка направления тренда на нескольких таймфреймах с помощью EMA, чтобы снизить ложные сигналы.

Сигнальные метки – на графике появляются "LONG" и "SHORT" с отступом от цены для наглядности.

JSON Alerts – готовый формат для автоматических уведомлений, включающий цену, направление SuperTrend, Fair Zone и ATR%.

Особенности:

Поддержка Pine Script v6

Линии и сигналы закреплены на графике, не двигаются при обновлении свечей

Настраиваемые параметры сетки, ATR, SuperTrend и фильтров

Совместимость с MTF-анализом и классическими индикаторами OBV/DMI

Рекомендации:

Используйте в сочетании с другими индикаторами и стратегиями управления риском. Сетка ATR% отлично подходит для позиционной торговли и интрадей.

ATR% Grid – automatic plotting of support and resistance levels based on current price and volatility (ATR). Useful for identifying potential targets and entry/exit zones.

SuperTrend – a classic trend indicator with an adaptive ATR multiplier that adjusts based on average volatility.

EDGE MTF ATR Bias Matrix EDGE MTF ATR BIAS MATRIX - User Guide & Documentation

═════════════════════════════════════════════════════════════

OVERVIEW

The EDGE MTF ATR Bias Matrix is a multi-timeframe directional bias indicator

that displays dynamic support and resistance levels across six timeframes in a

compact corner panel. It uses ATR-based trailing bands to determine trend

direction and highlights key levels you should be watching for potential

entries, exits, or reversals.

Think of it as your "compass" — at a glance, you can see which direction the

market is pointing on the 5m, 15m, 30m, 1H, 4H, and Daily timeframes, along

with the critical price level to watch on each.

─────────────────────────────────────────────────────────────

HOW IT WORKS

The indicator uses a dual-band trailing stop system on each timeframe:

INNER BAND (Tighter/Faster)

• Calculated as: HL2 ± (Inner Multiplier × ATR)

• Default multiplier: 3.0

• Reacts more quickly to price changes

• Defines the "active" trend direction

OUTER BAND (Wider/Slower)

• Calculated as: HL2 ± (Outer Multiplier × ATR)

• Default multiplier: 6.0

• Provides a buffer zone / "cloud" between signals

• Represents major support/resistance levels

The two bands create a "cloud" structure:

• When Inner > Outer → Bullish Cloud (uptrend structure)

• When Inner < Outer → Bearish Cloud (downtrend structure)

Signal Logic:

▲ BULLISH (Green): Price is ABOVE the inner band in a bullish cloud

▼ BEARISH (Red): Price is BELOW the inner band in a bearish cloud

◆ NEUTRAL (Gray): Price is inside the cloud or at an inflection point

─────────────────────────────────────────────────────────────

READING THE PANEL

The panel displays three columns:

TF │ Level │ Δ

────────┼───────────

Daily │ 4,125.50 │

4H │ 4,118.25 │ 3.25

1H │ 4,115.00 │

30m │ 4,112.75 │ 1.50

15m │ 4,110.50 │

5m │ 4,108.25 │ 0.75

COLUMN 1 - TF (Timeframe)

The timeframe being analyzed

COLUMN 2 - Level

The key support/resistance level to watch

• Color indicates bias: Green = Bullish, Red = Bearish, Gray = Neutral

• This is the trailing band level that price is respecting

COLUMN 3 - Δ (Delta/Proximity)

Distance from current price to the key level

• Only appears when price is within the Proximity Threshold

• Yellow color draws attention to nearby levels

• Helps you spot imminent tests of support/resistance

─────────────────────────────────────────────────────────────

WHAT TO LOOK FOR

1. CONFLUENCE OF BIAS

When multiple timeframes show the same color (all green or all red), the

directional bias is strong. Trade with the trend.

Example: Daily, 4H, 1H, and 30m all GREEN = Strong bullish environment

→ Look for long entries on pullbacks to the displayed levels

2. DIVERGENCE BETWEEN TIMEFRAMES

When higher timeframes disagree with lower timeframes, expect choppy

conditions or potential reversals.

Example: Daily RED but 15m and 5m GREEN = Short-term bounce in downtrend

→ Approach longs with caution; these may be counter-trend trades

3. PROXIMITY ALERTS (Δ Column)

When you see a value in the Δ column, price is close to that timeframe's

key level. This is where you should pay attention for:

• Bounces (level holds = continuation)

• Breaks (level fails = potential reversal or acceleration)

4. LEVEL CLUSTERING

When multiple timeframe levels are near each other, that zone becomes

significant. Price often reacts strongly at these areas.

Example: If 1H shows 4,115 and 30m shows 4,114, that 4,114-4,115 zone

is a high-probability reaction area.

5. TREND ALIGNMENT FOR ENTRIES

For highest-probability trades:

• Ensure at least the 1H and 4H (or Daily) agree on direction

• Use lower timeframe (5m/15m) levels for entry timing

• Place stops beyond the next timeframe's level

─────────────────────────────────────────────────────────────

CONFIGURABLE SETTINGS

═══ Color Theme ═══

Bullish Default: Green (#4CAF50, 30% transparency)

Color used when bias is bullish

Bearish Default: Red (#F44336, 0% transparency)

Color used when bias is bearish

Neutral Default: Gray (#ECEFF1, 30% transparency)

Color used when price is in the cloud/neutral zone

═══ Display Settings ═══

Panel Location Default: Top Right

Choose where the panel appears on your chart

Options: Top Left, Top Center, Top Right,

Bottom Left, Bottom Center, Bottom Right

Sort Highest Default: ON (checked)

TF First When ON: Daily at top, 5m at bottom

When OFF: 5m at top, Daily at bottom

Choose based on your trading style preference

Proximity Default: 10.5

Threshold How close price must be to a level before the Δ column

shows the distance

• For index futures (ES, NQ): 10-15 points works well

• For forex: 0.0010-0.0050 (10-50 pips)

• For stocks: Adjust based on typical ATR

• Set to 0 to disable proximity alerts

Text Size Default: Small

Options: Tiny, Small, Normal, Large

Adjust based on your screen size and preference

═══ Algorithm Parameters ═══

ATR Lookback Default: 10

Number of bars used to calculate ATR

• Lower values (5-8): More reactive to recent volatility

• Higher values (14-20): Smoother, less reactive

Range: 1-50

Inner Band Default: 3.0

Multiplier Controls the tighter/faster trailing band

• Lower values: Tighter stops, more signals, more whipsaws

• Higher values: Wider stops, fewer signals, smoother trends

Range: 0.5-10.0 (step 0.5)

Outer Band Default: 6.0

Multiplier Controls the wider/slower trailing band

• Should always be larger than Inner Multiplier

• Creates the "buffer zone" between trend states

• Larger values = bigger neutral zones

Range: 1.0-20.0 (step 0.5)

─────────────────────────────────────────────────────────────

RECOMMENDED CONFIGURATIONS

FOR SCALPING (Fast/Aggressive):

• ATR Lookback: 7

• Inner Multiplier: 2.0

• Outer Multiplier: 4.0

• Proximity Threshold: 5.0

FOR DAY TRADING (Balanced):

• ATR Lookback: 10 (default)

• Inner Multiplier: 3.0 (default)

• Outer Multiplier: 6.0 (default)

• Proximity Threshold: 10.5 (default)

FOR SWING TRADING (Smooth/Patient):

• ATR Lookback: 14

• Inner Multiplier: 4.0

• Outer Multiplier: 8.0

• Proximity Threshold: 20.0

─────────────────────────────────────────────────────────────

TIPS FOR BEST RESULTS

1. Use this indicator as a BIAS tool, not an entry signal

It tells you which direction to favor — you still need price action,

order flow, or another method to time entries.

2. Respect higher timeframe bias

Even if 5m and 15m turn bullish, if Daily is bearish, those longs are

counter-trend. Size smaller and take profits quicker.

3. Watch for color changes on your trading timeframe

A flip from green to gray (or red) is an early warning that momentum

may be shifting.

4. The displayed levels are dynamic

They trail price during trends but lock in during pullbacks. This is

by design — the levels only move in the direction of the trend.

5. Combine with volume or momentum

This indicator shows structure. Pair it with volume analysis or a

momentum oscillator to confirm strength of moves.

─────────────────────────────────────────────────────────────

TIMEFRAMES ANALYZED

The indicator automatically pulls data from these fixed timeframes regardless

of what chart timeframe you're viewing:

• 5 Minute (5m) — Micro structure, scalp timing

• 15 Minute (15m) — Intraday swings

• 30 Minute (30m) — Intraday trend

• 1 Hour (1H) — Day trading bias

• 4 Hour (4H) — Swing trading bias

• Daily (1D) — Overall trend direction

─────────────────────────────────────────────────────────────

TROUBLESHOOTING

Panel not showing?

→ Make sure you're viewing on a timeframe equal to or lower than 5m

→ Check that the panel location isn't obscured by other indicators

All levels showing gray/neutral?

→ This can happen during ranging/consolidating markets

→ The multipliers may need adjustment for the instrument's volatility

Levels seem too far from price?

→ Reduce the Inner and Outer Multipliers

→ The defaults work well for index futures but may need tuning for

lower-volatility instruments

Proximity column never shows values?

→ Increase the Proximity Threshold setting

→ Current default (10.5) may be too tight for your instrument

DEMA ATR Strategy [PrimeAutomation]⯁ OVERVIEW

The DEMA ATR Strategy combines trend-following logic with adaptive volatility filters to identify strong momentum phases and manage trades dynamically.

It uses a Double Exponential Moving Average (DEMA) anchored to ATR volatility bands, creating a self-adjusting trend baseline.

When the adjusted DEMA shifts direction, the strategy enters positions and scales out profit in phases based on ATR-driven targets.

This system adapts to volatility, filters noise, and seeks sustained directional moves.

⯁ KEY FEATURES

DEMA-Volatility Hybrid Filter

Uses Double EMA with ATR expansion/compression logic to form a dynamic trend baseline.

Directional Shift Entries

Entries occur when the adjusted DEMA flips trend (bullish crossover or bearish crossunder vs its past value).

Noise Reduction Mechanism

ATR range caps extreme moves and prevents false flips during choppy volatility spikes.

Multi-Level Take Profits

Targets scale out positions at 1×, 2×, and 3× ATR multiples in the trade direction.

Volatility-Adaptive Targets

ATR multiplier ensures profit targets expand/contract based on market conditions.

Single-Direction Exposure

No pyramiding; the strategy flips position only when trend shifts.

Automated Trade Finalization

When all profit targets trigger, the position is fully closed.

⯁ STRATEGY LOGIC

Trend Direction:

DEMA baseline is modified using ATR upper/lower envelopes.

• If the adjusted DEMA rises above previous value → Bullish

• If it falls below previous value → Bearish

Entry Rules:

• Enter Long when bullish shift occurs and no long position exists

• Enter Short when bearish shift occurs and no short position exists

Take Profit Logic:

3 partial exits for each trade based on ATR:

• TP1 = ±1× ATR

• TP2 = ±2× ATR

• TP3 = ±3× ATR

Profit distribution: 30% / 30% / 40%

Exit Conditions:

• Exit when all TPs hit (full scale-out if sum of all TPs 100%)

• Opposite trend signal closes current trade and opens new one

⯁ WHEN TO USE

Trending environments

Medium–high volatility phases

Swing trading and intraday trend plays

Markets that respect momentum continuation (crypto, indices, FX majors)

⯁ CONCLUSION

This strategy blends DEMA trend recognition with ATR-based volatility adaptation to generate cleaner directional entries and structured take-profit exits. It is designed to capture momentum phases while avoiding noise-driven false signals, delivering a disciplined and scalable trend-following approach.

OTT Volatility [RunRox]📊 OTT Volatility is an indicator developed by the RunRox team to pinpoint the most optimal time to trade across different markets.

OTT stands for Optimal Trade Time Volatility and is designed primarily for markets without a fixed trading session, such as cryptocurrencies that trade 24/7. At the same time, it works equally well on any other market.

🔶 The concept is straightforward. The indicator takes a specified number of historical periods (Samples) and statistically evaluates which hours of the day or which days show the highest volatility for the selected asset.

As a result, it highlights time windows with elevated volatility where traders can focus on searching for trade setups and building positions.

🔶 As the core volatility metric, the indicator uses ATR (Average True Range) to measure intraday volatility. Then it calculates the average ATR value over the last N Samples, creating a statistically stable estimate of typical volatility for the selected asset.

🔶 Statistically, during these highlighted periods the market shows higher-than-average volatility.

This means that in these time windows price is more likely to be subject to stronger moves and potential manipulation, making them attractive for active trade execution and position management.

⚠️ However, historical behavior does not guarantee future results.

These periods should be treated only as zones where volatility has a higher probability of being above normal, not as a promise of movement.

As shown in the screenshot above, the indicator also projects potential future volatility based on historical data. This helps you better plan your trading hours and align your activity with periods where volatility is statistically expected to be higher or lower.

🔶 Current Volatility – as shown in the screenshot above, you can also monitor the real-time volatility of the market without any statistical averaging.

On top of that, you can overlay the current volatility on top of the statistical volatility levels, which makes it easy to see whether the market is now trading in a high- or low-volatility regime relative to its usual behavior.

4 display modes – you can choose any visualization style that fits your trading workflow:

Absolute – displays the raw volatility values.

Relative – shows volatility relative to its typical levels.

Average Centered – centers volatility around its average value.

Trim Low Value – filters out low-volatility noise and highlights only more significant moves.

This indicator helps you define the most effective trading hours on any market by relying on historical volatility statistics.

Use it to quickly see when your market tends to be more active and to structure your trading sessions around those periods.

✅ We hope this tool becomes a useful part of your trading toolkit and helps you improve the quality of your decisions and timing.

Kalman Trend Sniper# KALMAN TREND SNIPER

## ORIGINALITY STATEMENT

The Kalman Trend Sniper combines adaptive trend detection with precision entry validation to identify high-probability trading opportunities. Unlike static moving averages that use fixed parameters, this indicator adapts to changing market volatility through ATR-based gain adjustment and distinguishes trending from ranging markets using ADX regime detection.

The indicator's unique contribution is its three-phase entry validation system: signals must hold for three bars, undergo a pullback test to the signal level, and receive confirmation through price action before generating an entry. This structured approach helps traders enter established trends at favorable retracement levels rather than chasing momentum.

---

## TECHNICAL METHODOLOGY

### Kalman Filter Implementation

This indicator implements an Alpha-Beta variant of the Kalman filter, a recursive algorithm that estimates trend from noisy price data:

1. Prediction: kf = kf + velocity

2. Error calculation: error = price - kf

3. Correction: kf = kf + gain * error

4. Velocity update: velocity = velocity + (gain * error) / 2

The gain parameter determines filter responsiveness. Higher gain values track price more closely but increase noise sensitivity, while lower values provide smoother output but lag price changes.

### Adaptive Gain Mechanism

The indicator adjusts gain dynamically based on volatility:

Volatility Factor = Current ATR / Long-term ATR

Adaptive Gain = Base Gain * (0.7 + 0.6 * Volatility Factor)

This ATR ratio increases responsiveness during high-volatility periods and reduces sensitivity during consolidations, addressing the fixed-parameter limitation of traditional moving averages. The volatility factor is bounded between configurable minimum and maximum values to prevent extreme adjustments.

### Regime Detection

The indicator uses the Average Directional Index (ADX) to distinguish market conditions:

- Trending markets (ADX above threshold): Full gain applied, signals generated

- Ranging markets (ADX below threshold): Gain reduced 25%, fewer signals

This regime awareness helps reduce whipsaw signals during sideways consolidation periods.

### Signal Line Validation System

When the Kalman line changes direction in trending conditions, the indicator draws a horizontal signal line at the low (for long signals) or high (for short signals) of the signal candle. This line represents a potential support or resistance level.

The validation system then monitors three phases:

Phase 1 - Hold Period: Price must remain above (long) or below (short) the signal line for three consecutive bars. This requirement filters weak signals where price immediately violates the signal level.

Phase 2 - Test: After the hold period, the system waits for price to pull back and touch the signal line, with configurable tolerance for volatile instruments.

Phase 3 - Confirmation: Within eight bars of the test, a confirmation candle must close above (long) or below (short) the test candle's body, demonstrating renewed momentum. If confirmation does not occur within eight bars, the validation attempt expires.

Successful validation generates an R label at the entry point. This three-phase structure helps identify entries where trend direction and support/resistance validation align.

---

## USAGE INSTRUCTIONS

### Signal Interpretation

Triangle Signals:

- Upward triangle (teal): Kalman line turns bullish in trending market (ADX above threshold)

- Downward triangle (red): Kalman line turns bearish in trending market

Signal Lines (horizontal):

- Teal line: Potential long support level at signal candle low

- Red line: Potential short resistance level at signal candle high

- Gray line: First opposite-color candle after signal (initial reversal pressure)

R Labels (optional, disabled by default):

- Green R below price: Validation complete for long entry

- Red R above price: Validation complete for short entry

Stop Levels:

- Red dots: Long stop level (Kalman line minus ATR multiplier)

- Teal dots: Short stop level (Kalman line plus ATR multiplier)

### Dashboard Information

The dashboard displays real-time indicator state:

- Trend: Current Kalman direction (BULL/BEAR)

- Regime: Market classification (Trending when ADX exceeds threshold, Ranging otherwise)

- Gain: Current adaptive gain value

- Vol Factor: Volatility ratio (current ATR / long-term ATR)

- ADX: Trend strength (higher values indicate stronger trends)

- Z-Score: Standard deviation distance from Kalman line (when enabled)

- Stop Dist: Current ATR-based stop distance

- Lines: Number of active signal lines displayed

- R-Status: Validation system state (Idle / Waiting / Testing)

### Trading Applications

Trend Following Approach:

1. Wait for triangle signal in trending market (ADX above threshold)

2. Enter immediately at signal candle close or wait for pullback

3. Place stop at displayed stop level

4. Trail stop using Kalman line as dynamic support/resistance

Validation Entry Approach (conservative):

1. After triangle signal, observe three-bar hold period

2. Wait for pullback to signal line (test phase)

3. Enter on R label confirmation

4. Place stop below/above signal line

5. Provides higher probability entries but reduces trade frequency

Z-Score Mean Reversion (when enabled):

1. Watch for Z-Score exceeding entry threshold (default +/-2.0)

2. Consider counter-trend entries when price touches Kalman line

3. Target return to Kalman line (Z-Score near zero)

4. Use Z-Score threshold as stop level for extreme continuation

### Optimal Conditions

The indicator performs optimally in clearly trending markets where ADX consistently exceeds the threshold. Performance degrades in sideways, choppy conditions.

Recommended timeframes:

- 1-5 minute charts: Use Crypto_1M preset (faster adaptation)

- 15-60 minute charts: Use Crypto_15M preset (balanced)

- Hourly charts: Use Forex preset (smoother)

- Daily charts: Use Stocks_Daily preset (long-term trends)

Market conditions:

- High volatility (Vol Factor above 1.5): Expect faster adaptation, wider stops needed

- Normal volatility (Vol Factor 0.7-1.5): Standard behavior

- Low volatility (Vol Factor below 0.7): Expect slower adaptation, tighter stops possible

---

## PARAMETER DOCUMENTATION

### Kalman Filter Settings

Preset Mode: Select optimized configuration for specific markets

- Custom: Manual parameter control

- Crypto_1M: Base Gain 0.05, ATR 7 (fast response for 1-5 minute crypto charts)

- Crypto_15M: Base Gain 0.03, ATR 14 (balanced for 15-60 minute crypto charts)

- Forex: Base Gain 0.02, ATR 14 (standard for forex pairs)

- Stocks_Daily: Base Gain 0.01, ATR 20 (smooth for daily stock charts)

Base Gain (0.001-0.2): Core Kalman filter responsiveness parameter. Higher values increase sensitivity to price changes. Low values (0.01-0.02) provide smooth output with fewer whipsaws but slower trend changes. High values (0.06-0.08) offer fast response with more signals but increased whipsaw risk.

Adaptive (checkbox): When enabled, automatically adjusts gain based on ATR ratio. Recommended to keep enabled for dynamic volatility adaptation.

ATR (5-50): Short-term Average True Range period for current volatility measurement. Default 14 is industry standard. Lower values respond faster to volatility changes.

Long ATR (20-200): Long-term ATR period for baseline volatility comparison. Default 50 provides stable reference. The ratio between ATR and Long ATR determines adaptive adjustment magnitude.

Regime Filter (checkbox): Enables ADX-based trending/ranging detection. When enabled, reduces gain by 25 percent during ranging markets to minimize false signals.

ADX Period (7-30): Period for ADX calculation. Default 14 is standard. Lower values respond faster to trend strength changes.

Threshold (15-40): ADX level distinguishing trending from ranging markets. Default 25. Above threshold: trending (generate signals normally). Below threshold: ranging (reduce sensitivity).

Min Vol / Max Vol (0.3-3.0): Bounds for volatility factor adjustment. Prevents extreme gain changes during unusual volatility spikes or quiet periods. Default minimum 0.5, maximum 2.0.

Stop ATR x (1.0-3.0): Multiplier for ATR-based stop loss distance. Default 2.0 places stops two ATRs from Kalman line. Use 1.5 for tight stops (intraday), 2.5-3.0 for wide stops (swing trading).

Show Signals (checkbox): Displays triangle signals when Kalman changes direction in trending markets. Disable to use indicator purely as dynamic support/resistance without signals.

Z-Score (checkbox): Enables mean-reversion signal generation based on statistical deviation from Kalman line.

Period (10-100): Lookback period for Z-Score standard deviation calculation. Default 20 bars. Longer periods produce smoother, less sensitive readings.

Entry (1.5-3.5): Standard deviation threshold for Z-Score signals. Default 2.0 generates signals at plus/minus two standard deviations (approximately 95th percentile moves).

Bull / Bear Colors: Customize Kalman line colors for uptrend (default teal) and downtrend (default red).

Fill (checkbox): Shows semi-transparent fill between price and Kalman line for visual trend emphasis.

### Signal Line System Settings

Signal Lines (checkbox): Displays horizontal signal lines at low (long) or high (short) of signal candles. These function as dynamic support/resistance levels.

Reverse Lines (checkbox): Shows gray horizontal lines at first opposite-colored candle after signal. Helps identify initial resistance points in new trends.

Max Lines (0-20): Maximum number of signal lines to display simultaneously. Older lines are removed as new signals appear. Use 1-2 for clean charts, 3-5 for recent support/resistance history.

Style (Solid/Dotted/Dashed): Visual style for signal and reverse lines. Dotted provides subtle appearance, solid is most prominent.

Line % / Label % (0-100): Transparency percentage for lines and labels. Zero is fully opaque, 100 is invisible.

R Labels (checkbox): Shows R labels when validation confirmation occurs. Default disabled. Enable if you want visual confirmation of successful pullback entries.

Tolerance % (0-1.0): Price deviation tolerance for test candle detection. Zero requires exact touch. 0.5 allows 0.5 percent deviation for volatile instruments.

### Dashboard Settings

Show Dashboard (checkbox): Toggles visibility of information panel. Disable for clean chart presentation.

Position: Choose dashboard location from nine positions (Top/Middle/Bottom combined with Left/Center/Right).

---

## LIMITATIONS AND WARNINGS

This indicator is a technical analysis tool that processes historical price data. It does not predict future price movements.

Inherent limitations:

1. Lagging nature: Like all trend indicators, the Kalman filter lags price. Signals occur after trend changes begin, not before.

2. Ranging markets: Generates fewer signals and reduced performance when ADX falls below threshold. Not optimized for sideways consolidation.

3. Whipsaw risk: In choppy, indecisive markets near ADX threshold, signals may reverse quickly despite regime filtering.

4. Parameter sensitivity: Inappropriate Base Gain settings can cause over-trading (too high) or missed trends (too low).

5. Validation requirement: The three-phase confirmation system provides higher accuracy but significantly reduces trade frequency. Not all trends produce valid pullback entries.

Not suitable for:

- Scalping strategies requiring instant signals (Kalman filter has intentional smoothing)

- Ultra-high frequency trading (indicator updates once per bar close)

- Markets with extreme overnight gaps (stops may be exceeded)

- Strategies requiring signals on Heikin Ashi, Renko, Kagi, Point and Figure, or Range charts

Risk management requirements:

This indicator provides trend direction and signal levels but does not incorporate position sizing, risk management, or account balance considerations. Users must implement appropriate position sizing, maximum daily loss limits, and portfolio diversification. Past performance does not indicate future results.

Optimal usage:

- Works optimally in clearly trending markets where ADX consistently exceeds threshold

- Performance degrades in sideways, choppy conditions

- Designed for swing trading and position trading timeframes (15-minute and above)

- Requires confirmation from price action or additional technical analysis

---

## NO REPAINT GUARANTEE

This indicator operates on bar close confirmation only. All signals, signal lines, and validation labels appear exclusively when candles close. Historical signals remain exactly where they appeared. This makes the indicator suitable for automated trading and reliable backtesting. What you see in historical data matches what appeared in real-time.

---

## ALERTS

The indicator provides eight alert conditions:

1. Kalman Buy Signal: Fires when upward triangle appears (bullish trend change in trending market)

2. Kalman Sell Signal: Fires when downward triangle appears (bearish trend change in trending market)

3. Trend Change to Bullish: Fires whenever Kalman line changes to bullish (regardless of ADX)

4. Trend Change to Bearish: Fires whenever Kalman line changes to bearish (regardless of ADX)

5. SCT-R Long Retest Confirmed: Fires when green R label appears for long validation

6. SCT-R Short Retest Confirmed: Fires when red R label appears for short validation

7. SCT Test Long Detected: Fires when test candle appears for long signal (before confirmation)

8. SCT Test Short Detected: Fires when test candle appears for short signal (before confirmation)

Alert messages include context about bar close confirmation and current price levels.

---

## CALCULATION TRANSPARENCY

While complete proprietary optimization methodology is not disclosed, the core technical approach is fully explained: Alpha-Beta Kalman filter with ATR-based adaptive gain adjustment and ADX regime detection. The signal line validation system uses a three-phase structure (hold, test, confirmation) with configurable parameters. Users can understand indicator functionality and make informed decisions about application.

---

## DISCLAIMER

This indicator is provided as a technical analysis tool. It does not constitute financial advice, trading recommendations, or performance guarantees. All trading decisions carry risk. Users are responsible for their own trading decisions and risk management. Past results do not indicate future performance.

Hash Supertrend [Hash Capital Research]Hash Supertrend Strategy by Hash Capital Research

Overview

Hash Supertrend is a professional-grade trend-following strategy that combines the proven Supertrend indicator with institutional visual design and flexible time filtering.

The strategy uses ATR-based volatility bands to identify trend direction and executes position reversals when the trend flips.This implementation features a distinctive fluorescent color system with customizable glow effects, making trend changes immediately visible while maintaining the clean, professional aesthetic expected in quantitative trading environments.

Entry Signals:

Long Entry: Price crosses above the Supertrend line (trend flips bullish)

Short Entry: Price crosses below the Supertrend line (trend flips bearish)

Controls the lookback period for volatility calculation

Lower values (7-10): More sensitive to price changes, generates more signals

Higher values (12-14): Smoother response, fewer signals but potentially delayed entries

Recommended range: 7-14 depending on market volatility

Factor (Default: 3.0)

Restricts trading to specific hours

Useful for avoiding low-liquidity sessions, overnight gaps, or known choppy periods

When disabled, strategy trades 24/7

Start Hour (Default: 9) & Start Minute (Default: 30)

Define when the trading session begins

Uses exchange timezone in 24-hour format

Example: 9:30 = 9:30 AM

End Hour (Default: 16) & End Minute (Default: 0)

Controls the vibrancy of the fluorescent color system

1-3: Subtle, muted colors

4-6: Balanced, moderate saturation

7-10: Bright, highly saturated fluorescent appearance

Affects both the Supertrend line and trend zones

Glow Effect (Default: On)

Adds luminous halo around the Supertrend line

Creates a multi-layered visual with depth

Particularly effective during strong trends

Glow Intensity (Default: 5.0)

Displays tiny fluorescent dots at entry points

Green dot below bar: Long entry

Red dot above bar: Short entry

Provides clear visual confirmation of executed trades

Show Trend Zone (Default: On)

Strong trending markets (2020-style bull runs, sustained bear markets)

Markets with clear directional bias

Instruments with consistent volatility patterns

Timeframes: 15m to Daily (optimal on 1H-4H)

Challenging Conditions:

Choppy, range-bound markets

Low volatility consolidation periods

Highly news-driven instruments with frequent gaps

Very low timeframes (1m-5m) prone to noise

Recommended AssetsCryptocurrency:

Average True Range % infoATR% is a modified version of the classic Average True Range indicator that displays price volatility as a percentage of the instrument's value, rather than in absolute values. This allows you to easily compare the volatility of different assets (e.g., Bitcoin vs Tesla stock) regardless of their price.

Main Features

1. ATR% Chart

The red line shows the average volatility from the last N candles (default 14), expressed as a percentage. For example:

ATR% = 2.5% means that the average daily move is approximately 2.5% of the asset's value

Higher values = greater volatility (higher profit potential, but also greater risk)

Lower values = lower volatility (calmer market)

2. Volatility Trend Analysis

The indicator automatically detects whether volatility is rising, falling, or stable:

Up arrow (↑) - volatility is rising (price becomes more "nervous")

Down arrow (↓) - volatility is falling (market is calming down)

Horizontal arrow (⮆) - volatility is stable (within ±3% of the moving average)

3. Information Table

In the upper right corner of the chart you will see Current ATR% value and Trend arrow with color coding:

- Green = rising volatility

- Red = falling volatility

- Gray = stable volatility

Parameters to Configure

Indicator Length (default: 14) - How many candles back to include in calculations:

Lower values (5-10): more sensitive to sudden changes, reacts faster

Higher values (20-30): more smoothed, shows long-term volatility picture

Trend Length (default: 10) - Period to analyze whether volatility is rising/falling:

Lower values: faster trend change signals

Higher values: more reliable, but slower signals

Sample Interpretations

ATR% Volatility Asset Type/Situation

< 1% Very low Stable blue-chip stocks, calm market

1-3% Low-medium Typical stocks, normal conditions

3-5% Medium-high Volatile stocks, cryptocurrencies at rest

5-10% High Cryptocurrencies, penny stocks

> 10% Extremely high Market panic, crash, pump & dump

Đại Ka 3 ATR BandsĐại Ka 3 ATR Bands – The ultimate single-slot indicator that replaces three separate ATR plots.

Designed specifically for ICT/SMC traders in 2025:

• Light red band (±0.5 ATR) → fake moves, Judas Swing, Turtle Soup zone

• Gray band (±1.0 ATR) → normal price action

• Light green band (±2.0 ATR) → real displacement zone → Silver Bullet, SFT, high-probability entries

How to use:

– Price stuck inside red band → expect reversal/fakeout

– Price breaks and closes outside green band + volume spike → enter aggressively in that direction (85%+ win-rate inside Killzones)

Default ATR(14), subtle fills for instant visual filtering of real vs fake moves.

Perfect companion for Order Blocks, FVG, Breaker Blocks and NY/London Killzones.

Free forever – coded with love by Đại Ka & Vietnamese ICT crew.

Momentum Tide [Alpha Extract]A sophisticated momentum-based trend identification system that measures normalized price deviation from an EMA baseline using ATR scaling and hyperbolic tangent smoothing for precise trend state classification. Utilizing advanced signal processing with configurable neutral bands and slope sensitivity adjustments, this indicator delivers institutional-grade momentum analysis with continuous strength measurement and visual trend confirmation. The system's three-state classification (bullish, bearish, neutral) combined with dynamic color intensity scaling provides comprehensive market momentum assessment across varying volatility conditions.

🔶 Advanced Baseline Deviation Framework

Implements EMA-based baseline calculation with ATR-normalized deviation measurement to create volatility-adjusted momentum signals. The system calculates raw price deviation from the baseline, scales by ATR and slope sensitivity factor, then applies exponential smoothing for stable signal generation with reduced noise and false transitions.

// Core Momentum Calculation

Baseline = ta.ema(close, Baseline_Length)

ATR_Value = ta.atr(ATR_Length)

Raw_Deviation = (close - Baseline) / (ATR_Value * Slope_Scaler)

Signal = ta.ema(Raw_Deviation, Signal_Smoothing)

🔶 Hyperbolic Tangent Normalization Engine

Features sophisticated tanh transformation that clamps raw deviation signals into normalized -1 to +1 range for consistent interpretation across all market conditions. The system applies safe exponential calculations with value capping to prevent overflow while maintaining signal sensitivity, creating bounded momentum readings suitable for systematic threshold analysis.

// Tanh Normalization

Clamped_Signal = tanh(Signal) // Bounded to

Strength = abs(Clamped_Signal) // Momentum intensity

🔶 Three-State Classification System

Implements intelligent trend state determination using configurable neutral band thresholds to reduce whipsaw signals during ranging conditions. The system classifies market as bullish (+1) when momentum exceeds upper neutral band, bearish (-1) below lower neutral band, and neutral (0) within the band, providing clear directional bias with built-in consolidation recognition.

🔶 Dynamic Color Intensity Architecture

Provides advanced visual feedback through momentum strength-based color intensity modulation, where stronger trends display more opaque colors and weaker trends show increased transparency. The system dynamically adjusts color alpha values based on absolute momentum strength, creating intuitive visual representation of trend conviction across baseline, candles, and bars.

🔶 Trend Strength Meter Visualization

Features innovative horizontal gradient meter displaying real-time momentum position across bear-to-bull spectrum with 24-segment resolution. The system creates smooth color transitions from bearish red through neutral gray to bullish green, with arrow indicator showing precise momentum location for instant trend strength assessment without cluttering the price chart.

🔶 Intelligent Flip Detection System

Generates transition markers when trend state changes from neutral/bearish to bullish or neutral/bullish to bearish, with duplicate signal suppression to prevent marker clustering. The system tracks previous signal states and only plots new markers on genuine trend reversals, providing clean entry signal visualization for systematic trading approaches.

snapshot

🔶 Configurable Neutral Band Framework

Implements adjustable neutral zone width using ATR percentage parameters to optimize signal frequency for different trading styles and market conditions. Wider bands reduce flip frequency for position trading while tighter bands increase sensitivity for active trading strategies, enabling customization without code modification.

🔶 Slope Sensitivity Adjustment

Features slope scaler parameter that modulates ATR normalization factor, controlling signal smoothness versus responsiveness trade-off. Higher values create smoother momentum readings with fewer transitions while lower values increase snappiness for faster reaction to price changes, allowing optimization across different volatility regimes and timeframes.

🔶 Comprehensive Visual Integration

Provides multi-dimensional trend visualization through color-coded baseline overlay, momentum-synchronized candle coloring, and bar color modification with configurable display toggles. The system includes optional flip markers and strength meter with position control for complete chart integration without visual overload.

🔶 Performance Optimization Framework

Utilizes efficient calculation methods with optimized table management for strength meter updates and minimal computational overhead for real-time momentum processing. The system includes intelligent state tracking and safe mathematical operations to prevent errors during extreme market conditions while maintaining consistent performance.

🔶 Why Choose Momentum Tide ?

This indicator delivers sophisticated momentum-based trend analysis through normalized deviation measurement and intelligent three-state classification. Unlike traditional momentum oscillators that operate in separate windows, Momentum Tide integrates directly with price action through baseline overlay and candle coloring while providing the analytical depth of bounded momentum measurement. The system's combination of tanh normalization, configurable neutral bands, dynamic color intensity, and innovative strength meter makes it essential for traders seeking adaptive trend-following approaches with clear visual feedback across cryptocurrency, forex, and equity markets. The three-state system naturally filters ranging periods while the momentum strength measurement enables position sizing and confidence assessment for systematic trading strategies.

Reward-Risk Visual Zones (RRZ)Reward–Risk Visual Zones (RRZ) – Structure-Driven Risk Mapping Engine

Most indicators tell you when to trade.

RRZ is designed to answer a different question:

“Is this setup worth the risk before I take the trade?”

RRZ is not a mashup of unrelated indicators.

It is a 3-stage risk engine that builds a complete trade “story” around each swing:

1. Market structure pivot → defines the trade idea

2. ATR volatility unit → defines the risk size

3. Projected reward → compares reward vs that risk and filters bad setups

The output is a visual trade map : entry, target, stop, and R:R, printed directly on chart at each qualified swing.

1. Market Structure Layer – Where trades are anchored

RRZ doesn’t fire signals from MA/RSI crossovers.

It begins with s wing structure :

• Uses ta.pivotlow() and ta.pivothigh() with user-controlled left/right sensitivity:

• Pivot Sensitivity (L) controls how wide a swing must be to qualify as a structural pivot.

• Pivot Confirmation (R) controls how fast/slow a pivot is confirmed (1 = almost real-time, larger values = safer but later).

• A confirmed swing low becomes the candidate anchor for a long R:R zone.

• A confirmed swing high becomes the candidate anchor for a short R:R zone.

Each pivot is stored with its exact price and bar index , so the rest of the logic is always anchored to a real swing instead of a random candle.

2. Volatility Layer – Turning ATR into a “risk unit”

Once a pivot is confirmed, RRZ measures local volatility using ATR:

• ATR length is configurable via ATR Length.

• ATR is not used as a trailing stop or overlay.

In RRZ it plays one specific role:

“One ATR = one unit of structural risk from this swing.”

From that:

Long scenario:

• Entry = pivot low

• Stop = Entry − 1 × ATR

Short scenario:

• Entry = pivot high

• Stop = Entry + 1 × ATR

This standardizes risk across different volatility regimes:

a 2R move in a quiet market and a 2R move in a volatile market are both “2 × ATR” from the structure.

3. Reward Projection Layer – Evaluating if the trade is worth it

RRZ then estimates how far price can realistically travel away from the pivot, given recent behaviour:

For longs (from swing low):

• Projects reward using the highest high in a rolling lookahead window (e.g., last 20 bars).

• Reward = HighestHigh – PivotLow

• Risk = ATR

• R:R = Reward / ATR

For shorts (from swing high):

• Projects reward using the lowest low in the window.

• Reward = PivotHigh – LowestLow

• Risk = ATR

• R:R = Reward / ATR

The user can set a minimum R:R filter via Min R:R Threshold.

• If R:R ≥ threshold → zone is tagged as “ GOOD R:R ” and highlighted in green (long) or red (short).

• If R:R < threshold → optionally still shown as “ LOW R:R ” in orange (so you can visually see “tempting but not worth it” trades).

This transforms a raw pivot + ATR into a quantified decision:

“From this swing, volatility says my stop is 1× ATR. Do I even have 2× ATR of room in my favour?”

4. Execution Map – How components work together on chart

Instead of just printing numbers, RRZ builds a full execution template for every qualifying swing:

• Entry line at the pivot price

• Target line at the reward projection price

• Stop line at pivot ± ATR

• A structured label including:

• LONG / SHORT direction

• “GOOD R:R” or “LOW R:R”

• Numerical R:R (e.g., 2.3 : 1)

• Entry, Target, Stop, current Close

A Cooldown Bars parameter prevents overlapping spam:

• After an R:R zone is created (long or short), the script waits X bars before considering another zone in the same direction.

• This keeps charts readable and focuses attention on the most recent high-quality swings.

RRZ also includes line style controls (solid/dashed/dotted) and separate colours for entry, target, and stop, so traders can quickly read the chart even without opening settings.

5. How to Use RRZ in a Trading Plan

RRZ is not a magic “buy/sell” button.

It is designed to sit on top of your existing strategy as a risk filter.

Typical workflows:

SMC / price-action traders:

• Use your own logic for BOS/CHoCH, order blocks, or liquidity sweeps.

• Use RRZ only where structure aligns and the zone shows GOOD R:R ≥ 2.0.

• Avoid setups where RRZ marks LOW R:R even if the pattern looks good.

System traders / swing traders:

• Use RRZ to standardize risk across assets and timeframes.

• Filter out trades where potential reward does not justify the stop, based on current ATR.

Beginners:

• Learn to stop taking trades where the target is too close and the stop is too wide.

• Visually understand how structural swings and volatility interact.

RRZ works across Forex, Crypto, Indices, and Stocks on intraday and higher timeframes.

Once a pivot is confirmed and a zone is plotted, its lines and labels do not repaint.

⸻

6. Why this invite-only script is more than a basic mashup

RRZ does use classic building blocks (pivots, ATR), but the value is in the way they are stitched into a single risk framework:

• It doesn’t run multiple separate indicators on chart.

Everything is computed inside one engine with a single purpose: structure-based R:R evaluation.

• ATR is not just “slapped on” as a stop line; it is treated as the core risk unit in the R:R calculation pipeline.

• Every zone is a coherent trade idea: from swing, to risk unit, to projected reward, to filtered label, to execution lines.

• The script is designed specifically to help traders do the one thing that almost no free indicator prioritizes:

“Say NO to low R:R trades automatically.”

This is what distinguishes RRZ from generic ATR-stop scripts or simple pivot overlays.

⸻

Important

• No performance promises.

• No marketing claims (“guaranteed”, “high win rate”, etc.).

• Purely a risk mapping & visualization tool.

HTF BIAS FILTER🧭HTF Bias Filter Indicator: 5 in 1 indicator

Technical Overview

The Bias Filter is a comprehensive multi-timeframe tool designed to confirm directional bias using five key indicators before entering a trade. It plots higher-timeframe Moving Averages directly on the chart and provides an immediate status summary via a static dashboard.

The more confluence on the dashboard, the greater the probability of the direction of the trade.

1. 📊 Display Components

A. Plotted Lines

The indicator uses the request.security function to draw Moving Averages from higher timeframes onto your current chart:

1H EMA 21 (Purple): The 21-period Exponential Moving Average calculated on the 1-Hour (60 min) chart. Plotted using a step-line style.

4H EMA 50 (Red): The 50-period Exponential Moving Average calculated on the 4-Hour (240 min) chart. Plotted using a step-line style.

B. Directional Dashboard

A fixed-position summary table is anchored to the bottom-right corner of the chart, providing a quick glance at the current status of all five filters.

2. 🎨 Colour Logic

Each of the five indicators is assigned a colour based on its current directional signal. The more indicators that show the same colour (confluence), the stronger the signal and the higher the likelihood of a high-probability trade.

🟢 Green indicators are signaling UP/BUY (Bullish momentum or trend).

🔴 Red indicators are signaling DOWN/SELL (Bearish momentum or trend).

⚫ Gray indicators are signaling Mixed or flat directions (neutral or undecided).

Note: The dashboard's main header color is determined by a strict confluence logic (All four 4H filters must align for Green/Red), while individual indicator colors follow the simple rules above.

3. 📋 Indicator Breakdown and Logic

The dashboard provides the direction of five different filters.

3.1. Higher-Timeframe (HTF) Trend Indicators

These two signals determine the immediate slope and direction of the primary Moving Averages:

4H EMA 50:

Timeframe: 4-Hour (240 min)

Logic: Compares the current EMA value to the value two bars ago on the 4H chart.

Output: UP ↑, DOWN ↓, or FLAT ⏸

1H EMA 21:

Timeframe: 1-Hour (60 min)

Logic: Compares the current EMA value to the value two bars ago on the 1H chart.

Output: UP ↑, DOWN ↓, or FLAT ⏸

3.2. 4-Hour Confluence Filters

These three indicators provide supplementary confirmation on Volume, Price Position, and Momentum, all calculated on the 4-Hour (240 min) chart:

4H OBV (Smoothed):

Timeframe: 4-Hour (240 min)

Logic: Direction is based on the current value of the 21-bar smoothed On-Balance Volume (OBV) compared to its value nine bars ago.

Output: UP ↑, DOWN ↓, or FLAT ⏸

4H ATR DIR (EMA Proxy):

Timeframe: 4-Hour (240 min)

Logic: Determines the price position by comparing the current Close price against the 4H EMA 50.

Output: BUY 🟢 (Close > EMA 50), SELL 🔴 (Close < EMA 50), or FLAT ⏸️ (Close = EMA 50).

4H RSI (14):

Timeframe: 4-Hour (240 min)

Logic: Momentum check comparing the 14-period Relative Strength Index (RSI) value against the 50 level.

Output: BUY 🟢 (RSI > 50), SELL 🔴 (RSI < 50), or FLAT ⏸️ (RSI = 50).

Uptrick: Dynamic Z-Score DivergenceIntroduction

Uptrick: Dynamic Z-Score Divergence is an oscillator that combines multiple momentum sources within a Z-Score framework, allowing for the detection of statistically significant mean-reversion setups, directional shifts, and divergence signals. It integrates a multi-source normalized oscillator, a slope-based signal engine, structured divergence logic, a slope-adaptive EMA with dynamic bands, and a modular bar coloring system. This script is designed to help traders identify statistically stretched conditions, evolving trend dynamics, and classical divergence behavior using a unified statistical approach.

Overview

At its core, this script calculates the Z-Score of three momentum sources—RSI, Stochastic RSI, and MACD—using a user-defined lookback period. These are averaged and smoothed to form the main oscillator line. This normalized oscillator reflects how far short-term momentum deviates from its mean, highlighting statistically extreme areas.

Signals are triggered when the oscillator reverses slope within defined inner zones, indicating a shift in direction while the signal remains in a statistically stretched state. These mean-reversion flips (referred to as TP signals) help identify turning points when price momentum begins to revert from extended zones.

In addition, the script includes a divergence detection engine that compares oscillator pivot points with price pivot points. It confirms regular bullish and bearish divergence by validating spacing between pivots and visualizes both the oscillator-side and chart-side divergences clearly.

A dynamic trend overlay system is included using a Slope Adaptive EMA (SA-EMA). This trend line becomes more responsive when Z-Score deviation increases, allowing the trend line to adapt to market conditions. It is paired with ATR-based bands that are slope-sensitive and selectively visible—offering context for dynamic support and resistance.

The script includes configurable bar coloring logic, allowing users to color candles based on oscillator slope, last confirmed divergence, or the most recent signal of any type. A full alert system is also built-in for key signals.

Originality

The script is based on the well-known concept of Z-Score valuation, which is a standard statistical method for identifying how far a signal deviates from its mean. This foundation—normalizing momentum values such as RSI or MACD to measure relative strength or weakness—is not unique to this script and is widely used in quantitative analysis.

What makes this implementation original is how it expands the Z-Score foundation into a fully featured, signal-producing system. First, it introduces a multi-source composite oscillator by combining three momentum inputs—RSI, Stochastic RSI, and MACD—into a unified Z-Score stream. Second, it builds on that stream with a directional slope logic that identifies turning points inside statistical zones.

The most distinctive additions are the layered features placed on top of this normalized oscillator:

A structured divergence detection engine that compares oscillator pivots with price pivots to validate regular bullish and bearish divergence using precise spacing and timing filters.

A fully integrated slope-adaptive EMA overlay, where the smoothing dynamically adjusts based on real-time Z-Score movement of RSI, allowing the trend line to become more reactive during high-momentum environments and slower during consolidation.

ATR-based dynamic bands that adapt to slope direction and offer real-time visual zones for support and resistance within trend structures.

These features are not typically found in standard Z-Score indicators and collectively provide a unique approach that bridges statistical normalization, structure detection, and adaptive trend modeling within one script.

Features

Z-Score-based oscillator combining RSI, StochRSI, and MACD

Configurable smoothing for stable composite signal output

Buy/Sell TP signals based on slope flips in defined zones

Background highlighting for extreme outer bands

Inner and outer zones with fill logic for statistical context

Pivot-based divergence detection (regular bullish/bearish)

Divergence markers on oscillator and price chart

Slope-Adaptive EMA (SA-EMA) with real-time adaptivity based on RSI Z-Score

ATR-based upper and lower bands around the SA-EMA, visibility tied to slope direction

Configurable bar coloring (oscillator slope, divergence, or most recent signal)

Alerts for TP signals and confirmed divergences

Optional fixed Y-axis scaling for consistent oscillator view

The full setup mode can be seen below:

Input Parameters

General Settings

Full Setup: Enables rendering of the full visual system (lines, bands, signals)

Z-Score Lookback: Lookback period for normalization (mean and standard deviation)

Main Line Smoothing: EMA length applied to the averaged Z-Score

Slope Detection Index: Used to calculate directional flips for signal logic

Enable Background Highlighting: Enables visual region coloring in

overbought/oversold areas

Force Visible Y-Axis Scale: Forces max/min bounds for a consistent oscillator range

Divergence Settings

Enable Divergence Detection: Toggles divergence logic

Pivot Lookback Left / Right: Defines the structure of oscillator pivot points

Minimum / Maximum Bars Between Pivots: Controls the allowed spacing range for divergence validation

Bar Coloring Settings

Bar Coloring Mode:

➜ Line Color: Colors bars based on oscillator slope

➜ Latest Confirmed Signal: Colors bars based on the most recent confirmed divergence

➜ Any Latest Signal: Colors based on the most recent signal (TP or divergence)

SA-EMA Settings

RSI Length: RSI period used to determine adaptivity

Z-Score Length: Lookback for normalizing RSI in adaptive logic

Base EMA Length: Base length for smoothing before adaptivity

Adaptivity Intensity: Scales the smoothing responsiveness based on RSI deviation

Slope Index: Determines slope direction for coloring and band logic

Band ATR Length / Band Multiplier: Controls the width and responsiveness of the trend-following bands

Alerts

The script includes the following alert conditions:

Buy Signal (TP reversal detected in oversold zone)

Sell Signal (TP reversal detected in overbought zone)

Confirmed Bullish Divergence (oscillator HL, price LL)

Confirmed Bearish Divergence (oscillator LH, price HH)

These alerts allow integration into automation systems or signal monitoring setups.

Summary

Uptrick: Dynamic Z-Score Divergence is a statistically grounded trading indicator that merges normalized multi-momentum analysis with real-time slope logic, divergence detection, and adaptive trend overlays. It helps traders identify mean-reversion conditions, divergence structures, and evolving trend zones using a modular system of statistical and structural tools. Its alert system, layered visuals, and flexible input design make it suitable for discretionary traders seeking to combine quantitative momentum logic with structural pattern recognition.

Disclaimer

This script is for educational and informational purposes only. No indicator can guarantee future performance, and trading involves risk. Always use risk management and test strategies in a simulated environment before deploying with live capital.

Time-Decay Liquidity Zones [BackQuant]Time-Decay Liquidity Zones

A dynamic liquidity map that turns single-bar exhaustion events into fading, color-graded zones, so you can see where trapped traders and unfinished business still matter, and when those areas have finally stopped pulling price.

What this is

This indicator detects unusually strong impulsive moves into wicks, converts them into supply or demand “zones,” then lets those zones decay over time. Each zone carries a strength score that fades bar by bar. Zones that stop attracting or rejecting price are gradually de-emphasized and eventually removed, while the most relevant areas stay bright and obvious.

Instead of static rectangles that live forever, you get a living liquidity map where:

Zones are born from objective criteria: volatility, wick size, and optional volume spikes.

Zones “age” using a configurable decay factor and maximum lifetime.

Zone color and opacity reflect current relative strength on a unified clear → green → red gradient.

Zones freeze when broken, so you can distinguish “active reaction areas” from “historical levels that have already given way”.

Conceptual idea

Large wicks with strong volatility often mark areas where aggressive orders met hidden liquidity and got absorbed. Price may revisit these areas to test leftover interest or to relieve trapped positions. However, not every wick matters for long. As time passes and more bars print, the market “forgets” some areas.

Time-Decay Liquidity Zones turns that idea into a rule-based system:

Find bars that likely reflect strong aggressive flows into liquidity.

Mark a zone around the wick using ATR-based thickness.

Assign a strength score of 1.0 at birth.

Each bar, reduce that score by a decay factor and remove zones that fall below a threshold or live too long.

Color all surviving zones from weak to strong using a single gradient scale and a visual legend.

How events are detected

Detection lives in the Event Detection group. The script combines range, wick size, and optional volume filters into simple rules.

Volatility filter

ATR Length — computes a rolling ATR over your chosen window. This is the volatility baseline.

Min range in ATRs — bar range (High–Low) must exceed this multiple of ATR for an event to be considered. This avoids tiny bars triggering zones.

Wick filters

For each bar, the script splits the candle into body and wicks:

Upper wick = High minus the max(Open, Close).

Lower wick = min(Open, Close) minus Low.

Then it tests:

Upper wick condition — upper wick must be larger than Min wick size in ATRs × ATR.

Lower wick condition — lower wick must be larger than Min wick size in ATRs × ATR.

Only bars with a sufficiently long wick relative to volatility qualify as candidate “liquidity events”.

Volume filter

Optionally, the script requires a volume spike:

Use volume filter — if enabled, volume must exceed a rolling volume SMA by a configurable multiplier.

Volume SMA length — period for the volume average.

Volume spike multiplier — how many times above the SMA current volume needs to be.