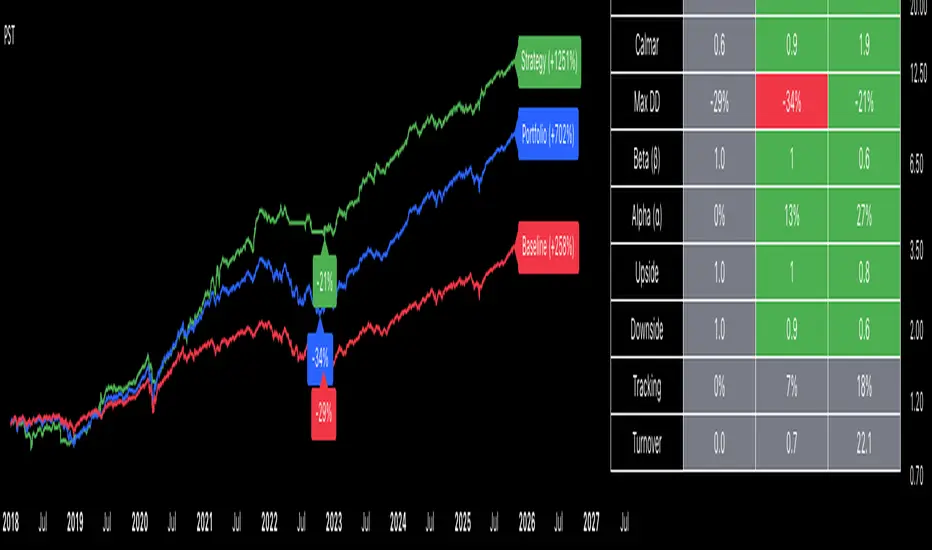

SPY 200SMA +4% Entry -3% Exit TQQQ/QLD/GLDM THREE PHASE STRATEGYWanted to take a look at all of the individual trades and provide a series of options to balance performance and risk. This post is expanding on my previous one - www.reddit.com

Here is the data and the backtesting splitting the strategy into three primary phases with multiple options and exact trade dates to help people easily backtest other combinations - docs.google.com (Three Tabs with the three phases)

If you just want my personal recommendations this would be what I will be using -

PHASE 1 (Strategy BUY signal triggers when SPY price crosses +4% over the SPY 200SMA) = 100% TQQQ

If trade lasts 366 days (Long Term Cap Gains) go to PHASE 2

If SPY price crosses below -3% SPY 200SMA go to PHASE 3

PHASE 2 (PHASE 1 lasts 366 days) = Deleverage and diversify into 50% QLD & 50% GLDM

PHASE 3 (Strategy SELL signal triggers when SPY price crosses -3% below the SPY 200SMA) = Defensive posture with 50% SGOV & 50% GLDM

As market degrades start selling SGOV and buying QQQ until 50% QQQ & 50% GLDM

TradingView Script for the THREE PHASE STRATEGY (imgur.com):

//

@version=

5

strategy("SPY 200SMA +4% Entry -3% Exit Strategy",

overlay=true,

default_qty_type=strategy.percent_of_equity,

default_qty_value=100)

// === Inputs ===

smaLength = input.int(200, title="SMA Period", minval=1)

entryThreshold = input.float(0.04, title="Entry Threshold (%)", step=0.01)

exitThreshold = input.float(0.03, title="Exit Threshold (%)", step=0.01)

startYear = input.int(1995, "Start Year")

startMonth = input.int(1, "Start Month")

startDay = input.int(1, "Start Day")

// === Time filter ===

startTime = timestamp(startYear, startMonth, startDay, 0, 0)

isAfterStart = time >= startTime

// === Calculations ===

sma200 = ta.sma(close, smaLength)

upperThreshold = sma200 * (1 + entryThreshold)

lowerThreshold = sma200 * (1 - exitThreshold)

// === Strategy Logic ===

enterLong = close > upperThreshold

exitLong = close < lowerThreshold

if isAfterStart

if enterLong and strategy.position_size == 0

strategy.entry("Buy", strategy.long)

if exitLong and strategy.position_size > 0

strategy.close("Buy")

// === 366-Day Marker Logic (Uninterrupted) ===

var

int

targetTime = na

// 1. Capture entry time only when a brand new position starts

if strategy.position_size > 0 and strategy.position_size == 0

targetTime := time + (366 * 24 * 60 * 60 * 1000)

// 2. IMPORTANT: If position is closed or a sell signal hits, reset the timer to "na"

if strategy.position_size == 0

targetTime := na

// 3. Trigger only if we are still in the trade and hit the timestamp

isAnniversary = not na(targetTime) and time >= targetTime and time < targetTime

// === Visuals ===

p_sma = plot(sma200, title="200 SMA", color=color.rgb(255, 0, 242))

p_upper = plot(upperThreshold, title="Entry Threshold (+4%)", color=color.rgb(0, 200, 0))

p_lower = plot(lowerThreshold, title="Exit Threshold (-3%)", color=color.rgb(255, 0, 0))

fill(p_sma, p_upper, color=color.new(color.green, 80), title="Entry Zone")

// Draw marker only if 366 days passed without a sell

if isAnniversary

label.new(bar_index, high, "366 DAYS - PHASE 2", style=label.style_label_down, color=color.yellow, textcolor=color.black, size=size.small)

// === Entry/Exit Labels ===

newOpen = strategy.position_size > 0 and strategy.position_size == 0

newClose = strategy.position_size == 0 and strategy.position_size > 0

if newOpen

label.new(x=bar_index, y=low * 0.97, text="BUY - PHASE 1", xloc=xloc.bar_index, yloc=yloc.price, color=color.lime, style=label.style_label_up, textcolor=color.black, size=size.small)

if newClose

label.new(x=bar_index, y=high * 1.03, text="SELL - PHASE 3", xloc=xloc.bar_index, yloc=yloc.price, color=color.red, style=label.style_label_down, textcolor=color.white, size=size.small)

200 SMA SPY Trading Range Bands Script:

//

@version=

5

indicator("200 SMA SPY Trading Range Bands", overlay=true)

// === Settings ===

smaLength = input.int(200, title="SMA Length")

mult1 = input.float(1.09, title="Multiplier 1 (9% Over)")

mult2 = input.float(1.15, title="Multiplier 2 (15% Over)")

// === Calculations ===

smaValue = ta.sma(close, smaLength)

line9Over = smaValue * mult1

line15Over = smaValue * mult2

// === Plotting ===

plot(smaValue, title="200 SMA", color=color.gray, linewidth=1, style=plot.style_linebr)

plot(line9Over, title="9% Over 200 SMA", color=color.rgb(255, 145, 0), linewidth=1)

plot(line15Over, title="15% Over 200 SMA", color=color.rgb(38, 1, 1), linewidth=2)

Backtest

Structura Candles Volume 1 v1.0█ OVERVIEW

Structura Candles Volume 1 is an advanced candlestick pattern recognition indicator based on the research methodology of Thomas N. Bulkowski's "Encyclopedia of Candlestick Charts." This indicator identifies 19 statistically-validated candlestick patterns and provides real-time backtesting against your current chart.

█ METHODOLOGY

Unlike traditional candlestick indicators that rely on theoretical pattern behavior, this script implements Bulkowski's empirical approach:

- Trend Detection: 10-period EMA to define short-term trend context

- Tall Candle Filter: 146% of 22-day average height threshold (statistically significant candles)

- Breakout Confirmation: Tracks whether price breaks above pattern high or below pattern low within a user-defined window

- Non-Repainting: Signals only confirm on bar close

█ PATTERNS INCLUDED

LONG Signals (Bullish):

- Three-Line Strike Bearish (84% reversal rate per Bulkowski)

- Engulfing Bullish

- Morning Star / Morning Doji Star

- Belt Hold Bullish

- Abandoned Baby Bullish

- Rising Window

- Three Inside Up

- Three Outside Up

SHORT Signals (Bearish):

- Engulfing Bearish

- Three Black Crows

- Evening Star / Evening Doji Star

- Abandoned Baby Bearish

- Two Black Gapping

- Falling Window

- Belt Hold Bearish

- Three Inside Down

- Three Outside Down

█ FEATURES

- Real-time pattern detection with LONG/SHORT direction

- Dynamic win rate calculation based on YOUR chart's historical performance

- Comparison to Bulkowski's book statistics

- Label colors update based on outcome:

🟡 Yellow = Pending (awaiting breakout)

🟢 Green = WIN (correct breakout direction)

🔴 Red = LOSS (wrong breakout direction)

⚪ Gray = Timeout (excluded from statistics)

- Separated LONG vs SHORT performance dashboard

- Adjustable breakout timeout window

█ HOW TO USE

1. When a pattern appears, the label shows direction (LONG/SHORT) and historical win rate

2. Wait for bar close confirmation (✓ CONFIRMED status)

3. Monitor subsequent bars for breakout above pattern high (bullish) or below pattern low (bearish)

4. Use the dashboard to identify which patterns perform best on your specific instrument

█ IMPORTANT DISCLAIMER

- Past performance does not guarantee future results

- The "Book WR" values are from Bulkowski's historical research on US equities and may differ across instruments, timeframes, and market conditions

- This indicator is for educational and analytical purposes only

- Always use proper risk management and do your own analysis before trading

- The win rates displayed are based on the breakout methodology, not actual trade profitability

█ SETTINGS

- Max Bars to Breakout: How long to wait for pattern confirmation (default: 10)

- Pattern Toggles: Enable/disable individual patterns

- Bulkowski Parameters: Adjust trend EMA, height threshold, and doji tolerance

█ ACCESS

This is an invite-only script. For access, please send a direct message.

Axis-Pro System | Trend Structure + Fibonacci Pullbacks Axis-Pro System is a comprehensive Trend Following strategy designed to trade high-probability pullbacks. Unlike indicators that merely chase price, this system patiently waits for market structure alignment before seeking an entry.

The system is built on the premise of "Quality over Quantity", utilizing volatility and structure filters to avoid choppy markets (ranges) and false breakouts.

🧠 Strategy Logic

The system makes decisions based on a strict 4-step hierarchy:

Higher Timeframe (HTF) Bias:

Analyzes the trend on a higher timeframe to ensure we are trading in the direction of the dominant flow.

Structure & BOS (Break of Structure):

Identifies clear impulses that break previous highs or lows. Once a BOS is confirmed, the system "arms" the trade and waits.

Fibonacci Zone Pullback:

It does not chase the breakout. Instead, it waits for a pullback into the "Discount Zone" (Golden Zone, configurable between 0.382 and 0.618) to improve the Risk/Reward ratio.

Validation & Trigger:

Uses an ATR expansion check to filter out low-volatility periods.

Requires candle confirmation and alignment with fast EMAs before pulling the trigger.

🛡️ Risk Management

The system incorporates advanced position management using a split execution model (50/50):

Dynamic Stop Loss: Automatically calculated using an ATR multiplier or the recent Swing High/Low (whichever offers better protection).

TP1 (Take Profit 1): Closes 50% of the position at a fixed R-multiple (e.g., 1.5R) to lock in profit and moves the Stop Loss to Break-Even.

TP2 (Runner): The remaining 50% is left to run for higher targets (e.g., 3.0R) or until the trend bends, maximizing gains during strong moves.

Trailing Stop: Optional feature to trail price with a fast EMA once the first target is hit.

⚙️ Settings & Features

The script is highly customizable for different assets (Crypto, Forex, Indices):

Date Range Filter: Includes a date selector to perform precise Backtesting on specific periods (e.g., testing specifically during a Bear Market vs. Bull Market).

Auto Trendlines: Automatically draws relevant trendlines for visual support.

Quality Filters: Options to toggle the EMA 200 filter and breakout buffers.

⚠️ Disclaimer

This strategy is a tool for analysis and backtesting purposes. Past performance does not guarantee future results. It is highly recommended to test the strategy on a Demo account first and adjust parameters according to the volatility of the specific asset being traded. Always use responsible risk management.

EMA Extension + Reversion StatisticsEMA Extension + Reversion Statistics

Description

This indicator is a statistical mean-reversion tool designed to quantify how far price has extended from its baseline trend (the Mean EMA) and calculate the historical probability of a reversion event.

Unlike standard oscillators that use arbitrary fixed numbers (like RSI > 70), this script uses a historical rolling window (default 10 years) of daily data to determine exactly what constitutes a "High" or "Extreme" deviation for the specific asset you are charting.

It answers two critical questions:

Is the price statistically overextended? (Are we in the top 2% of historical deviations?)

If I fade this move, what is the historical win rate? (e.g., "When price is this extended, it touches the 9 EMA within 5 days 82% of the time.")

Key Features

Dynamic Volatility Bands: Plots "High" (default 80th percentile) and "Extreme" (default 98th percentile) extension bands based on historical daily closes.

Real-Time Win Rates: An on-screen dashboard displays the historical success rate of three different mean-reversion strategies whenever price hits these bands.

Time-Independent Logic: The statistics are calculated on the Daily timeframe regardless of the chart you are viewing. This allows you to scalp on lower timeframes (like the 5m or 15m) while seeing the statistical pressure from the Daily chart.

Rolling Lookback: Uses an array-based memory system to calculate percentiles over a user-defined lookback period.

The 3 Reversion Strategies

The dashboard calculates the "Win Rate" for three specific scenarios. Note specifically which ones require a Close versus just a Touch:

Touch EMA (9):

Goal: Price must TOUCH the Target EMA (default 9 EMA) at any point during the day. Wicks count.

Constraint: Must happen within the defined "Max Days" (default 5).

Close Inside Band:

Goal: Price must CLOSE back inside the deviation band. A wick inside is not enough; the candle body must confirm the move.

Constraint: Must happen within the defined "Max Days" (default 2).

Touch Mean (20):

Goal: Price must TOUCH the Baseline Band EMA (default 20 EMA) at any point during the day.

Constraint: Must happen within the defined "Max Days" (default 10).

Fully Customizable Settings

This script is designed to be flexible for different trading styles, asset classes, and timeframes. You can adjust the statistical model to fit your specific needs by clicking the Settings (Gear Icon) on the indicator and navigating to the Inputs tab.

What You Can Customize:

Lookback Period (Years):

Default: 10 Years.

You can increase this for a more robust long-term model or decrease it for assets with less history (like newer crypto pairs).

Moving Averages (EMAs):

Change the Band EMA (Default: 20) if you prefer a slower baseline like the 50 EMA.

Change the Target EMA (Default: 9) if you scalp to a faster average like the 5 or 8 EMA.

Time Constraints (Max Days):

Define your own "Time Stop." If you believe a reversion trade isn't valid if it takes longer than 3 days, simply change the Max Days input from 5 to 3. The win rates will instantly update to reflect this stricter rule.

Dashboard Visibility:

Show Dashboard: Toggle the table on or off.

Table Position: Move the table to any corner of the chart (Top Right, Bottom Left, etc.) to fit your workspace.

Strategy Mode: Switch between viewing "Show All 3" strategies at once or focusing on a single strategy to keep your chart clean.

Visual Guide

Red Stepline: The "Extreme" deviation band. Historically, price rarely stays here long.

Orange Stepline: The "High" deviation band. Standard overbought/oversold zone.

Dashboard Colors:

Red Text: Stats relative to the Extreme Band.

Orange Text: Stats relative to the High Band.

Dashboard Data:

Dev: Shows the current deviation of price from the EMA in percent.

Columns: The percentages shown (e.g., "85%") represent the historical Win Rate of that strategy triggering from that specific band.

Disclaimer

This indicator is for educational and informational purposes only and does not constitute financial advice. The "Win Rates" displayed are based on historical data and do not guarantee future performance. Trading futures, options, and securities involves significant risk and is not suitable for every investor. You may lose more than your initial investment. Always trade with a risk management plan.

Backtest Pro - The TradingView Backtesting EngineBacktest your indicators — no strategy code required. Backtest Pro is the next-generation backtesting engine for smarter testing. Simply link your signals, set your stops, and start testing.

With its upgraded UI/UX and fundamentally improved stop system, Backtest Pro replaces the legacy PSE (Practical Strategy Engine) and sets a new standard for TradingView backtesting. It delivers more accurate intrabar trailing stops, flexible stop types (Points, ATR Multiplier, %), and a smoother workflow for greater precision and control.

Once loaded on your chart, Backtest Pro appears as BT Pro as the script title and in the Strategy Tester, alerts, and chart labels.

Beyond the core stop and pyramiding logic, Backtest Pro also introduces:

A clearer Data Window for reviewing trade details.

Improved signal labels in the Strategy Tester’s List of Trades for easier log analysis.

Updated chart labels that align better with TradingView’s native style and make signals easy to interpret. Together, these improvements make Backtest Pro the most practical and user-friendly way to backtest indicator-based trading signals in TradingView.

Copyright © 2025 CoinOperator

________________________________________________________________________________

🚀 Why Traders Choose Backtest Pro

Answer in minutes what used to take days of manual testing.

Backtest Pro is a drop-in, ready-to-use backtesting engine that links to your indicator with just a few simple connection lines. It provides more accurate intrabar trailing stops, multiple stop types (Points, ATR Multiplier, %), and a smoother workflow for greater precision and control.

Whether you’re running a quick test or fine-tuning complex strategies, Backtest Pro helps you reach clearer insights faster.

________________________________________________________________________________

👤 Who Backtest Pro Is For

Backtest Pro is designed for traders who already have a trading methodology or entry/exit logic and want professional-grade validation and risk analysis.

Backtest Pro is not a signal service and does not provide discretionary trade recommendations. All entries and exits — including alerts used for automation — are generated solely from user-defined logic.

You bring the logic — Backtest Pro provides the structure, metrics, and discipline.

Backtest Pro helps swing traders, day traders, and strategy developers streamline the backtesting process without sacrificing depth or accuracy. It offers flexible stop management, enhanced Data Window metrics, refined Strategy Tester labeling, and clean on-chart visuals to support consistent evaluation.

Backtest Pro supports trading and backtesting on futures (continuous contracts), forex, crypto, stocks, ETFs, and commodity/index CFDs (tradable if offered by your broker).

________________________________________________________________________________

⚡ Quick Start

Add Backtest Pro to your chart. It appears as BT Pro as the script title and in the Strategy Tester, alerts, and chart labels.

Add a few connector lines to your indicator, then link your custom entry and exit signals.

Adjust position sizing, stops, and pyramiding.

Run the TradingView Strategy Tester for instant results.

________________________________________________________________________________

🔄 From PSE to Backtest Pro

Backtest Pro builds on the foundation of the PSE (Practical Strategy Engine), evolving it into a more refined tool. While PSE introduced flexible stop handling, Backtest Pro enhances the experience with:

More accurate intrabar trailing stops

Expanded stop type options (Points, ATR Multiplier, %)

Upgraded Data Window for easier review

Clearer trade signals in the Strategy Tester

Cleaner, more consistent chart labels

Wash Sale Prevention is Now Optional. If enabled, it only applies to assets of types stock and fund.

🛠 INPUTS TAB SETTING

📅 Trading Window

Enable Trading Window to define the date/time when trading is allowed. Disable to trade the entire market data.

Partition the time when trading is allowed to see if your indicator settings work well across the different ranges. Your resulting metrics should be acceptable across all four (4) ranges: entire range, 1st half, IQR, and 2nd half.

Show Trading Window Lines – Enable to draw vertical lines at the start and end of the trading window for clear visual definition of when trading is allowed.

💰 Position Sizing (Money Management)

Separating the equity risk into initial position and pyramid position allows for greater ability to maximize profits within your acceptable drawdown.

Note : Position sizing is determined on the anticipated fill price which is affected by the maximum of slippage and selected price gap (discussed in the Execution Rules section). Max Equity per Position (%) : This setting applies to each position within a trade group . Limits the position size and will not exceed this amount. Set as desired. Default is 20% for non-leverage trading. For leveraged trading, adjust accordingly. Example: for 3× leverage, enter 300 (3 × 100 = 300).

Max Equity Drawdown Warning (%) : Triggers an alert if the strategy’s equity drawdown exceeds this threshold. Select the method to use for this warning. If BT Pro, then it is based on peak equity at bar-close. If TradingView, then it is based on the built-in variable strategy.max_drawdown_percent. Helps you manage strategy-level risk tolerance.

Scaled Pyramiding : Adjusts position size incrementally for each pyramid entry—either decreasing or increasing exposure relative to the prior entry.

Start Position: The entry number at which scaling begins. For example, 3 means scaling starts on the 2nd pyramid (the 3rd entry overall).

Chg(%): The percentage change applied to each subsequent pyramid entry.

Max(%): The maximum cumulative reduction allowed when scaling downward. Ignored for upward scaling because increases are already capped by Max Equity per Position (%).

⚖️ Execution Rules

Trade Direction : Select either Both , Long Only, or Short Only.

Alert Failed to Trade – Enable to alert you when a trade did not happen due to low equity or low order size. Applicable only for the first position of a trade group.

Cooldown Period : Controls how long the engine waits after an exit before allowing a new trade group. Backtest Pro also applies a small built-in safeguard to prevent unrealistic same-bar flips: ● 1 bar minimum for same-direction entries

● 2 bars minimum for direction changes

Prevent Wash Sales : Enable if you want the Backtest Pro to enforce a minimum cooldown period of 30 days for trade groups that result in a loss. Only applies to assets of types stock and fund.

Pyramid Conditions with Price Gaps : Dwn Gap and Up Gap refer to price gaps. A price gap is the difference between the closing price of the previous candle and the opening price of the current candle, and their value is shown in the Data Window. Selection options include: disabled (the default), median, avg, p80 (for 80th percentile), and p90 (for 90th percentile). The values reflect ~500 most recent bars from the cursor position. Disabled sets the Dwn Gap and Up Gap to zero in the below logic. Pyramids require a tailing stop loss, TSL. The price gaps are used in conditions for pyramids:

To ensure the previous position is protected when opening a pyramid position. A new pyramid position will not open until its trailing stop loss protects the prior position.

To prevent a pyramid position from becoming a loss when too close to a take profit level, TP (if enabled), due to commission cost.

The logic for #1 and #2 is as follows:

For a Long Pyramid: TSL: Stop Price - max(DwnGap, slippage) > LastEntryPrice

TP (if enabled): Long take profit > close + max(UpGap, slippage) AND gain > commission cost

For a Short Pyramid:

TSL: Stop Price + max(UpGap, slippage) < LastEntryPrice

TP (if enabled): Short take profit < close - max(DwnGap, slippage) AND gain > commission cost

Show All Gap Stats in Data Window

Enable to show all price gap statistics in the Data Window to review market conditions.

Disable for the Backtest Pro to run most efficiently.

Note: Statistics selected in Dwn Gap and Up Gap settings are always shown, regardless of this option.

🛑 Exit Strategy (Risk Management)

Backtest Pro supports multiple stop loss styles, giving traders the tools to backtest strategies in TradingView with precision:

The Exit Strategy applies a common protective stop across the entire trade group.

Pyramids require a trailing stop loss. A new pyramid position will not open until its trailing stop loss protects the prior position.

Plot Stop Level : You can plot the stop level either as of bar close (the default) or as of bar open. This only affects the visual plot. The underlying logic does not change. The trades will be the same regardless of the setting.

ATR Length : The ATR Length is used with the ATR multiplier and is common to stop loss, SL, trailing stop loss, TSL, take profit, TP, and the time-based exit option. It is the number of bars (periods) used in ATR calculation.

Price-Based Exits Stop Loss and Trailing Stop Loss options are Points, ATR Multiplier, and %.

The Trailing Stop Loss is activated from entry of the initial position of a trade group.

Take Profit options are Points, ATR Multiplier, %, and R-Multiple. How Trailing Stops Work in the Backtest Pro All trailing stop inputs (Points, ATR Multiplier, or %) are converted at the first entry into a fixed currency offset.

That offset is reactive intrabar and applied as the trailing distance from the most favorable price (highest for longs, lowest for shorts) since the first entry in the trade group.

Even if “%” is selected as the input method, the engine uses the fixed currency offset.

The trailing stop offset (points) is displayed in the Data Window for reference, allowing you to enter that offset directly at your broker if needed.

⚠️ Caution: Always enter a points-based trailing stop at your broker—never a percentage-based trailing stop. Volatility-Based Exit While in a trade, ATR values are accumulated each bar. The position exits once the total exceeds ATR Multiplier × ATR at entry if the Reward/Risk is below the set threshold.

Dividends are not included in reward (i.e., profit).

👉 These flexible stop types solve one of the biggest limitations of the legacy PSE and make Backtest Pro a true TradingView backtesting engine.

📑 Trade Signal Labels in Strategy Tester

Backtest Pro uses standardized trade labels in the Strategy Tester → List of Trades. These labels make it easy to understand the reason behind each entry or exit at a glance. Entry : Standard entry signal when conditions are met.

Stop : Stop-loss exit triggered at your defined stop level.

Pyr-Entry : Pyramid entry, adds to an existing position.

Trail-Stop : Trailing stop exit based on offset logic. Note : If the stop level has been adjusted to equal the trailing stop level, the Strategy Tester may display Stop instead of Trail-Stop. The exit displayed is the one Pine Script evaluates first, but the actual exit behavior remains correct.

Exit : Standard exit signal.

Delay-Exit : One-bar delayed exit, prevents immediate exit when position entry and exit signal occur on the same bar.

TP : Take Profit exit, closes position at your profit target.

RR-Exit : Reward/Risk exit — position closes when ATR accumulation exceeds the set threshold and R/R is below target.

📊 Performance Metrics & Reporting

Include Dividends in Profit

Adjusts ROI, CAGR, Reward/Risk, Avg Invest/Trade-Grp, and Equity.

Assumes dividends are taken as cash (not reinvested). They are applied to Equity on the ex-date instead of the payment date.

Only applies if the security issues dividends and the chart is 1D or lower timeframe; otherwise ignored.

Include Dividends in Profit Factor

Applies only when Include Dividends in Profit is enabled.

Adds dividend income to both gross profits and gross losses when calculating Profit Factor, so PF reflects total return (trading + dividends).

Affects Avg Trade-Grp Loss, Equity Loss from ECL, and Equity Loss from ECL (%).

Show Dividends

Displays the payout in currency/share, as well as the total amount based on the number of shares of the position(s) currently held by the trade group. For long positions you earned the dividends. For short positions you owe the dividends.

Show Metrics Table

The on-chart Metrics Table displays a compact set of key statistics for quick reference and mobile use. Full and expanded metrics are available in the Data Window on desktop or browser. Section groupings may differ between the table and Data Window to optimize readability and presentation in each context.

📊 Data Window

Note : Accessible via a button on the right-hand toolbar of the chart interface. Unlike the Metrics Table, Data Window values update dynamically as you move your cursor across bars. All metrics are based on trade groups.

Trade Information

Enter Price

Stop Price

Favorable Extreme : only shows if trailing stop loss is enabled on Inputs tab. The most favorable price (highest for longs, lowest for shorts) since the first entry in the trade group.

TSL Offset Points : only shows if trailing stop loss is enabled on Inputs tab.

Take Profit : only shows if take profit is enabled on Inputs tab.

Leverage information applies to trade groups.

Fail Pos / Margin (%) : Shows zero if the failed position size was <1, or the margin % that failed to meet the requirement in the Properties tab. A flag appears above the bar where a failed trade occurred. Only applies to the first position of a trade group. Hover over the flag to view the value in the Data Window.

Notional Value : total trade group position size x latest entry price x point value. The equity must be > notional value x margin requirement for a trade to occur.

Current Margin (%) : must be greater than margin requirement set on the Properties tab in order for a trade to occur.

Margin Call Price : when enabled on the Style tab is displayed on both the chart and the Data Window as shown below.

Performance Net Profit (%) : Will include dividends if 'Include Dividends in Profit' is enabled. Only shows in Data Window if 'Include Dividends in Profit' is enabled.

ROI (%) and CAGR (%) : Based on Avg Invest/Trade-Grp. Adjusted for dividends if enabled.

Reward/Risk (profit/risked, expectancy per amount risked): Adjusted for dividends if enabled. Color is green if above breakeven, red if below, and yellow if within ±0.1 tolerance.

Profit Factor (PF) : By default, dividends are not counted in win/loss classification.

Win % : Uses same coloring scheme as Reward/Risk except uses a ±2% tolerance for yellow. Breakeven point is the balance between Reward/Risk and Win %, showing whether the system can be profitable. For example, for a low Win % a high Reward/Risk is needed for the system to be potentially profitable. Equity & Growth

Equity : Your current equity.

Dividend Sum : The amount of total dividends accumulated since entering the market. Only shows in Data Window if 'Include Dividends in Profit' is enabled. Risk & Drawdown

Maximum Drawdown (MDD)

Measures the largest peak-to-trough decline in account equity over the entire backtest.

A new peak is recorded whenever equity reaches a new high; the system then tracks the lowest equity seen until a new peak forms.

This method uses bar-close equity including both realized and unrealized P&L. Therfore, it may not match TradingView’s displayed drawdown values which use a different method.

Maximum Drawdown %

Expresses MDD as a percentage of the equity peak from which the decline occurred.

This normalizes drawdown across different account sizes and assets, making strategy-to-strategy risk comparisons more meaningful.

Maximum Consecutive Losses applies to trade groups.

Equivalent Consecutive Losses (ECL) : Based on Win % and Nbr of Trade-Grp’s.

Simulates a realistic losing streak with intermittent small wins.

Lowered by increasing Win %.

Equity Loss from ECL : Equity drawdown estimated from ECL.

Equity Loss from ECL (%) : Same, expressed as a percentage.

Avg Trade-Grp Loss Trade Structure

Backtesting Years : The trading window in years.

Nbr of Trade-Grp’s : Count of trade groups.

Nbr of Positions : The count of positions shown on the chart.

The TV list of trades in the Strategy Tester may indicate more than what is actually shown on the chart.

Avg Invest/Trade-Grp : Avg money invested per trade group. Adjusted for dividends if enabled.

Avg Trade-Grp Days : The average number of days for trade groups.

Time in Market (%) : The percentage of time in a trade based on the trading window.

Cnt 1st EE Same-Bar is the count of first positions in a trade group that enter and exit on the same bar. Labels appear above for easy reference. Helps assess optimal stop-loss settings.

Cnt Pyr EE Same-Bar is the count of pyramid positions in a trade group that enter and exit on the same bar. Labels appear above for easy reference. Helps assess optimal stop-loss settings. Up Gaps / Dwn Gap (Ticks) ( Show All Gap Stats in Data Window enabled )

Median gap

Avg gap

80 percentile

90 percentile

Price Gap (Ticks) ( Show All Gap Stats in Data Window disabled )

Dwn Gap : Shows selected option if not disabled.

Up Gap : Shows selected option if not disabled.

Data Quality

Tick Resolution measures how many minimum price increments (ticks) fit into the current asset’s price. It is calculated as: Tick Resolution = Price / Minimum Tick Size. This value indicates the precision available for order placement and stop calculations.

Green – High resolution (>= 1000). The strategy’s stop and profit calculations will operate with normal accuracy.

Yellow – Moderate resolution (100-999). Stop levels are still functional but may exhibit minor rounding effects.

Red – Low resolution (< 100). This can distort trailing stops, stop losses, or take profits due to coarse rounding by TradingView’s broker emulator.

⚠️ Caution : When Tick Resolution is in the red zone, results from backtests may differ significantly from live trading because price precision is too low for reliable simulation.

💡 Tip : If low tick resolution is present at the beginning of the chart’s market data (often with very old price history), use the Trading Window to restrict backtesting to later periods where the asset price has risen and tick resolution is higher.

👁 Visualization

Highlight Traded Background

Trade groups are shown in background color of green for long positions and red for short positions. Set as desired.

Show Losing Trade Groups

Losing trade groups are indicated at the exit with label text in the color blue. Used to easily find consecutive losses affecting your strategy’s performance. The dividend payment, if any, is not considered in the calculation of a win or loss.

Show Position Values

Enable to show the currency value of each position in gold color.

Show Max Drawdown (Peak & Trough) Enable to show the peak and trough labels on the price chart. Based on equity at bar close. Use to easily identify the bar associated with the peak and trough of equity.

Select label size for your preference.

Alert on Expiring GTC Orders

Backtest Pro includes an optional alert that warns you when a Good-Til-Canceled (GTC) order is approaching expiration. This feature is designed as a safety net, helping you avoid unprotected trades caused by broker-imposed GTC expirations. This alert is sent a few days before a 60-day time period you’re if still in an open position.

By default, the alert is enabled, offering protection for traders who may not actively monitor order expiry rules.

Professional users who already track expirations can disable the feature in the settings to streamline alerts.

🔌 Signal Connection

Click the dropdown and select the entry and exit signal to establish a connection to your indicator.

Separate Entry and Exit Signal Connections.

Backtest Pro requires separate entry and exit signals. Indicators that already produce distinct events integrate cleanly and make strategies easier to read, debug, and maintain.

If your indicator currently uses a combined signal (e.g., buy = 1, sell = –1, flat = 0), that structure can create overlap or conflicts during backtesting.

Don’t worry — later in this manual, you’ll learn exactly how to adapt your indicator so it outputs clear entry and exit signals compatible with Backtest Pro.

🔌 Configure Your Indicator for Entry and Exit Signals

This section explains how to structure your indicator’s entry and exit signals so they can connect seamlessly with the Backtest Pro engine.

Define your own conditions for when to enter or exit positions using any technical logic you prefer. You can configure exits independently of entries or make them dependent on them—for example, exiting only when the opposite entry condition occurs.

Below are a few examples of how you might define Long and Short Entry Signals before connecting them to Backtest Pro.

________________________________________________________________________________

Examples of Long Entry Signals

ind_sig_long = oscillator > UpperLimit

ind_sig_long = ta.crossover(ta.sma(close, 14), ta.sma(close, 28))

ind_sig_long = MACD_hist > 0 Examples of Short Entry Signals

ind_sig_short = oscillator < LowerLimit

ind_sig_short = ta.crossunder(ta.sma(close, 14), ta.sma(close, 28))

ind_sig_short = MACD_hist < 0 ________________________________________________________________________________

Combining and Refining Your Signals

If your indicator uses multiple internal conditions, you can combine them using logical operators or threshold rules before connecting to the Backtest Pro engine.

1. Combine multiple conditions

Use logical and / or to merge your conditions into one signal:

Entry_Long = ind_sig_long1 and ind_sig_long2 // both must be true

Entry_Short = ind_sig_short1 or ind_sig_short2 // either may be true ________________________________________________________________________________

2. Require a minimum number of confirming conditions

You can also define a threshold for how many entry conditions must be true before triggering a signal. This can help ensure stronger confirmation.

minNbr_Entries = input.int(defval=1, title='Min Number of Entry Conditions')

// Convert boolean signals to numeric form

longCount = (ind_sig_long1 ? 1 : 0) + (ind_sig_long2 ? 1 : 0)

shortCount = (ind_sig_short1 ? 1 : 0) + (ind_sig_short2 ? 1 : 0)

// Require at least minNbr_Entries to confirm signal

Entry_Long = longCount >= minNbr_Entries

Entry_Short = shortCount >= minNbr_Entries

Do likewise for your Exit conditions to ensure consistency in trade confirmation.

________________________________________________________________________________

Defining Exits

Independent of Entries

Exit_Long = ta.crossunder(ta.rsi(close, 14), 70)

Exit_Short = ta.crossover(ta.rsi(close, 14), 30) Dependent on Entries

Exit_Long = Entry_Short // exit longs when short entry triggers

Exit_Short = Entry_Long // exit shorts when long entry triggers ________________________________________________________________________________

Final Signals to Connect to Backtest Pro

entry_signal = Entry_Long ? 1 : Entry_Short ? -1 : 0

exit_signal = Exit_Long ? 1 : Exit_Short ? -1 : 0

plot(entry_signal, title="entry_signal", color = color.blue, display=display.data_window)

plot(exit_signal, title="exit_signal", color = color.red, display=display.data_window) ________________________________________________________________________________

Notes

You can easily expand this structure to handle three or more conditions by adding them to the count expression.

If your indicator already provides a single entry_signal, you can connect it directly to Backtest Pro without modification.

Always ensure your final Entry_Long, Entry_Short, Exit_Long, and Exit_Short variables are boolean (true / false).

🔒 Connecting Closed-Source Indicators

If your indicator is closed-source (meaning you cannot view or modify its internal code), you’ll need to work with the plotted values it provides.

Create a connection indicator that reads those plotted values and converts them into clear entry and exit signals using the logic described above.

This connection indicator acts as a bridge between the closed-source indicator and Backtest Pro, allowing you to translate its behavior into standardized signal logic that the engine can process.

⚙️ PROPERTIES TAB SETTING

Initial Capital : Set as desired.

Base Currency : Leave as Default. The Backtest Pro is designed to use the instrument’s native currency, so changing this is not necessary.

Order Size : Essentially disabled. Position sizing is handled in the Inputs tab and is based on a percentage of equity.

Pyramiding : Set as desired.

Commission : Enter as a percentage of position value. The Backtest Pro is designed to work only with commission expressed this way.

Verify Price for Limit Orders : Set as desired.

Slippage : Set as desired. See the Dwn/Up Gap values in Data Window to get an idea of possible values to use.

Margin (Leverage Trading):

The Backtest Pro supports both leveraged and non-leveraged trading (default is no leverage).

Note : The following two settings apply at the trade group level . For example, to trade with 5× leverage, enter 20 (1 ÷ 5 × 100 = 20).

Margin for Long Positions : Set as desired. Default is 100%.

Margin for Short Positions : Set as desired. Default is 100%.

Recalculate After Order Is Filled (default is enabled)

Enabling this allows the Backtest Pro to function correctly and to recalculate immediately after an order is filled , which makes it possible to:

Enter and exit on the same bar (because the strategy sees the fill instantly).

Trigger alerts immediately after the fill , instead of waiting for the next bar close.

You may see the following Caution! message in the TradingView Strategy Tester:

This warning occurs because the strategy parameter calc_on_order_fills = true . You can safely close the caution message and know the Backtest Pro will produce realistic backtest results.

Recalculate On every tick : Disable.

Fill Orders

Using Bar Magnifier : Recommended if your TradingView plan supports it. Improves intrabar accuracy, but the strategy can still run without it.

On Bar Close : Must remain disabled. Enabling this prevents the Backtest Pro from working as intended.

⚠️ Caution : Enabling On Bar Close forces all orders to be evaluated only at bar close. This disables intrabar logic, prevents same-bar entries and exits, and breaks trailing stop / pyramid behavior. For the Backtest Pro to work as intended, On Bar Close must remain disabled .

Using Standard OHLC : Recommended if running the strategy on Heikin Ashi charts. Otherwise, set as desired. The default is enabled.

📢 Using The Alert Dialog Box Message Field

When setting alerts, include alert() function calls with order fills to allow notifications for drawdown exceeded, Failed to Trade (if enabled), and to be warned of expiring GTC orders (if enabled).

Example Message for Order Fill Alerts

(This is just an example. Consult TV manual for possible placeholders to use.)

Position: Current = {{strategy.market_position}}, Previous = {{strategy.prev_market_position}}

{{strategy.order.action}} {{strategy.order.contracts}} shares at price = {{strategy.order.price}} on {{exchange}}:{{ticker}} (TF: {{interval}})

Equity_Multiplier = {{strategy.order.contracts}} x {{strategy.order.price}} ÷ {{plot("Equity")}}

{{strategy.order.alert_message}}

Note :

Use a known account equity multiplied by Equity_Multiplier to determine the total currency amount required for position sizing—especially when managing multiple accounts with different equity levels.

What {{strategy.order.alert_message}} Includes

This placeholder automatically inserts the additional information generated for each order fill alert (blank for exits):

Stop Price (on first entries is based on bar close prior to order fill bar)

TSL Offset (Pts) distance from Favorable Extreme (for pyramid entries)

TP (on first entries is based on bar close prior to order fill bar)

Price Gap (Pts) based on your gap selection and slippage entered

Example Message for Bot Trading Alerts

(You must consult your specific bot for configuring the alert message. This is just an example.)

"action": "{{strategy.order.action}}",

“price”: {{strategy.order.price}}

"amount": {{strategy.order.contracts}},

"botId": "1234"

[Backtest Crypto] RSIThis script is designed for testing strategies based on the RSI oscillator.

Script settings:

Test range selection

Strategy type selection: reversal strategy (30/70); trend trading (from 40 / from 60); divergence trading; attempt to implement automatic range/trend detection.

Indicator settings.

Trade management: risk-to-reward ratio selection, stop-loss defined as min/max for a certain number of candles (you can set a desired number), option to partially lock in a position by moving the stop-loss to breakeven, trailing stop.

Stop-loss margin (%).

Option to limit the stop-loss by ATR to prevent it from becoming too large during volatile movements.

===============================================================

Скрипт предназначен для тестирования стратегий, основанных на осциляторе RSI.

Настройки скрипта:

Выбор диапазона тестирования

Выбор типа стратегии: разворотная стратегия (30/70); Торговля по тренду (от 40 / от 60); торговля дивергенций; попытка реализовать автоматическое определение ренжа/тренда.

Настройки индикаторов.

Сопровождение сделки: выбор соотношения риска к прибыли, стоп-лосс определяется как мин/мах за определенное количество свечей (можно устанавливать желаемое количество), возможность частичной фиксации позиции с переносом стоп-лосса в безубыток, трейлинг-стоп.

Запас стоп-лосса %.

Возможность ограничения стоп-лосса по ATR, чтобы при волатильных движениях он не был слишком большим.

Backtest any Indicator [Target Mode] StrategyUniversal Backtester Strategy with Sequential Logic

This strategy serves as a highly versatile, universal backtesting engine designed to test virtually any indicator-based trading system without requiring custom code for every new idea. It transforms standard indicator comparisons into a robust trading strategy with advanced features like sequential entry steps, dynamic target modes, and automated webhook alerts.

The core philosophy of this script is flexibility. Whether you are testing simple crossovers (e.g., MA Cross) or complex multi-stage setups (e.g., RSI overbought followed by a MACD flip), this tool allows you to configure logic via the settings panel and immediately see backtested results with professional-grade risk management.

Core Logic: Source vs. Target Mode

The fundamental building block of this strategy is the "Comparator" engine. Instead of hard-coding specific indicators, the script allows users to define logic slots (L1-L5 for Longs, S1-S5 for Shorts).

Each slot operates on a flexible comparison logic:

Source: The primary indicator you are testing (e.g., Close Price, RSI, Volume).

Operator: The condition to check (Equal/Cross, Greater Than, Less Than).

Target Mode:

Value Mode: Compares the Source against a fixed number (e.g., RSI > 70).

Source Mode: Compares the Source against another dynamic indicator (e.g., Close > SMA 200).

This "Target Mode" switch allows the strategy to adapt to almost any technical analysis concept, from oscillator levels to moving average trends.

Advanced Entry System: Sequential Steps (1-5)

Unlike standard backtesters that usually require all conditions to happen simultaneously (AND logic), this strategy implements a State Machine for sequential execution. Each of the 5 entry slots (L1-L5 / S1-S5) is assigned a "Step" number.

The logic flows as follows:

Stage 1: The strategy waits for all conditions assigned to "Step 1" to be true.

Latch & Wait: Once Step 1 is met, the strategy "remembers" this and advances to Stage 2. It waits for a subsequent bar to satisfy Step 2 conditions.

Trigger: The actual trade entry is only executed once the highest assigned step is completed.

Example Use Case:

Step 1: Price closes below the Lower Bollinger Band (Dip).

Step 2: RSI crosses back above 30 (Confirmation).

Execution: Buy Signal triggers on the Step 2 confirmation candle.

This creates a realistic "Setup -> Trigger" workflow common in professional trading, preventing premature entries.

Exit Logic & Risk Management

The strategy employs a dual-layer exit system to maximize profit retention and protect capital.

1. Signal-Based Exits (OR Logic) There are 5 configurable exit slots (LX1-LX5 / SX1-SX5). Unlike entries, these operate on "OR" logic. If any enabled exit condition is met (e.g., RSI becomes overbought OR Price crosses below EMA), the position is closed immediately.

2. Hard Stop & Take Profit

Fixed %: Users can set a hard percentage-based Stop Loss and Take Profit.

Trailing Stop: A toggleable "Trailing?" feature allows the Stop Loss to dynamically trail the price.

Longs: The SL moves up as the price makes new highs.

Shorts: The SL moves down as the price makes new lows.

Automated Alerts & Webhooks

This script is built with automation in mind. It includes a dedicated makeJson() function that constructs a JSON payload compatible with most trading bots (e.g., 3Commas, TradersPost, Tealstreet).

Alert Modes Supported: | Alert Type | Description | | :--- | :--- | | Order Fills Only | Triggers standard TradingView strategy alerts when the broker emulator fills an order. | | Alert() Function | Triggers specific JSON payloads defined in the code ("action": "buy", "ticker": "MNQ", etc.). |

The script automatically calculates the alert quantity based on your equity percentage settings, ensuring the payload matches your backtest sizing.

Dashboard & Visuals

To aid in rapid analysis, the strategy includes visual tools directly on the chart:

Performance Table: A dashboard (top-right) displays real-time stats including Net Profit, Win Rate, Profit Factor, and Max Drawdown.

Trade Markers: Custom labels (goLong, exLong) show exactly where trades opened and closed, including the trade number and profit percentage.

SL/TP Visualization: Dynamic step-lines (Orange for SL, Lime for TP) show exactly where your protection levels are sitting, helping you visually verify if your stops are too tight or too loose.

Logic Flow Signals & Backtest [bercutiatia]To understand the advanced logic of the tool, it is essential that you carefully read each topic and check the visual examples in this presentation.

--

Who is the Logic Flow Signals & Backtest tool recommended for?

Ideal for traders looking to increase the reliability and level of their operations. Recommended for those who want to create rigorous confluences, validate strategies with backtesting, and transform emotional management into systematic and measurable processes.

How can the Logic Flow Signals & Backtest tool help me?

High-confidence signals! You combine TradingView indicators and create a single robust signal, eliminating the frustration of having to spend hours in front of the chart and still clicking at the wrong time. This ensures that your entry is validated by logic, not emotional impulse.

--

Logic Flow Signals & Backtest is a versatile and powerful tool designed to test and validate your trading ideas with indicators from the TradingView community.

Extreme flexibility: Allows you to combine indicators available on TradingView (EMAs, RSI, MACD, SMC, etc.) to create custom entry and exit logics.

Sequential Logic: Goes far beyond simple crossovers. You can define rules where signal A must occur before signal B — and, if desired, before signal C or D — to validate an entry. Add time, order, and context filters, creating truly intelligent sequential logic that generates a single final alert only when all conditions align.

With Stages (Stage 1, Stage 2, etc.), your entries follow the exact sequence you define. And the best part: you no longer need to spend hours in front of the chart waiting for confluences. Simply set up your stages once, create an alert in TradingView, and the system will automatically notify you when the ideal combination of signals occurs.

Sequence Invalidation: Offers the option to define conditions that, if they occur, immediately cancel an ongoing entry sequence, helping to avoid entries in unfavorable scenarios.

Explaining the first image example (chart below):

LONG INDICATOR 1 (Stage 1): The market confirms a change in character (CHoCH Bullish). The system enters an alert state awaiting the confluence of the next indicators.

LONG INDICATOR 2 and 3 (Stage 2): Entry is only released when the SMA17 crosses above the SMA72 (indicator 2), but with one condition: The SMA72 must be ABOVE the SMA305 (indicator 3); Without this alignment of indicator 3, the signal of indicator 2 does not occur.

LONG INDICATOR 4 (Invalidation Rule): If at any point in the sequence the SMA72 crosses below the SMA305, the setup is immediately canceled and no entry signal is generated. The sequence restarts with indicator 1.

EXIT LONG (Hybrid Exit TP + SIGNAL): The trade seeks a TP target of 1000 ticks, but has a technical "Trailing Stop": if the trend reverses (Exit Long Indicator 1 = SMA72 crosses below the SMA305) before the target, the position is closed to protect capital.

SHORT INDICATOR 1 (Stage 1): Identification of weakness in the market with a Bearish CHoCH.

SHORT INDICATOR 2 and 3 (Stage 2): Entry is only released when the SMA17 crosses below the SMA72 (indicator 2), but with a strict condition: The SMA72 must be BELOW the SMA305 (indicator 3); Without this STATE of indicator 3, the signal from indicator 2 does not occur.

SHORT INDICATOR 4 (Invalidation Rule): If at any point in the sequence the SMA72 crosses above the SMA305, the setup is immediately canceled and no entry signal is generated. The sequence starts again with indicator 1.

EXIT SHORT (Hybrid Exit TP + SIGNAL): The trade seeks a target of 1000 ticks, but has a technical "Trailing Stop": if the downtrend reverses (Exit Short Indicator 1 = SMA72 crosses above the SMA305) before the target, the position is closed to protect capital.

In this strategy, we use the external indicators: Multiple MTF MA and Smart Money Concepts (Advanced)

--

Stage Duration: In STAGE DURATION , you control the maximum time (in candles) allowed for each transition between stages to occur. If the time limit expires before the next stage is reached, the sequence is reset. Keep it at 0 to disable the time limit.

The "Stage Duration" function is available in four separate blocks on the settings panel:

- LONG - STAGE DURATION: Controls the time limit (in candles) between Long entry stages (for example from Stage 1 to Stage 2).

- LONG EXIT - STAGE DURATION: Controls the time limit between Long exit stages.

- SHORT - STAGE DURATION: Controls the time limit between Short entry stages.

- SHORT EXIT - STAGE DURATION: Controls the time limit between Short exit stages.

Explaining the second image example (chart below):

Stage 1 (INDICATOR 1): New Fair Value Gap (FVG) Bullish Confirmed.

- Meaning: The move starts with a bullish FVG (Fair Value Gap), indicating a confirmed imbalance where buyers were much more aggressive than sellers.

Stage 2 (INDICATOR 2): EMA10 crossing above the EMA50.

- Meaning: Immediately after the FVG trigger, the fast moving average (10 periods) crosses the intermediate moving average (50 periods). This confirms that the initial FVG impulse was not an isolated event but the beginning of a short-term trend.

Stage 3: In this final stage, we require two simultaneous confirmations to validate the entry:

- INDICATOR 3: The EMA10 crosses above the EMA100, indicating that the movement has enough strength to break through larger barriers.

- INDICATOR 4: The RSI must be above its own moving average (SMA14). This ensures the asset is gaining momentum at the exact moment the averages are broken, avoiding entries in "tired" markets.

Stage Duration: The most important feature of this setup is the restricted time window.

- Rule: From Stage 1 to 2, and from Stage 2 to 3, the maximum interval to accept confluences is only 3 candles.

- Why this is vital? If the market took 20 candles to align these conditions, it would indicate weakness or indecision. By demanding that everything happens within a maximum of 3 candles per step, the setup filters only the moves where buying pressure is urgent and aggressive, increasing the probability of an explosive move in favor of the trade.

Asymmetric Risk Management: To complement a high-probability and high-pressure setup, we use aggressive risk management:

- Stop Loss (Technical/Short): 200 Ticks. If the buying pressure fails quickly, we exit early with a small loss.

- Take Profit (Long Target): 1000 Ticks. We aim to ride the impulse "leg" that the setup identified.

- Risk/Reward: 5:1. This means a single winning trade covers five losing trades, making the strategy mathematically viable in the long term.

In this strategy, we use the external indicators: Multiple MTF MA , Smart Money Concepts (Advanced) and Relative Strength Index (RSI) .

--

Multiple Operating Modes

It is not limited to sequences. It can operate by confluence (where all signals must be valid at the same time), by single trigger (only one signal is required), or by "OR" logic (any one of the defined signals).

- If you use only Stage 1 in more than one indicator session, the entry will only occur if all enabled conditions are true simultaneously.

- Any condition defined as OR can trigger the entry by itself.

- If only one condition block is enabled, the single indicator will function as a simple signal.

Multiple and Simultaneous Exits

It allows for the configuration of exits by both indicators and TP/SL targets. The strategy will close the trade as soon as any of these conditions are met first (indicator signal, profit target, or loss limit

Integrated Risk Management

It includes Stop Loss and Take Profit exits by percentage and ticks, which are easy to configure and essential for risk management. The strategy calculates the exact TP and SL prices based on your entry price and monitors the market on every tick.

Explaining the Third Image Example (Chart Below)

The move was validated by a 4-step logical sequence (Stage 1) and managed by a hybrid exit system.

Short Indicator 1, 2, and 3: The price (Close) crossed below the SMA200, SMA72, and SMA17 averages simultaneously.

- What this means: When a single candle has the strength to break below the short-term (17), mid-term (72), and long-term (200) averages, it indicates a high probability for the price to seek lower levels.

To reinforce Indicators 1 through 3, we added an extra layer of confirmation.

Short Indicator 4: The Positive Volume Index (PVI) needed to be below its own long-term average (EMA300).

- Why this is important: PVI below the average confirms that selling volume is dominant, validating that the break of the averages was not just noise.

Triple Exit Management (Maximum Security)

The great advantage of this tool is the ability to manage risk dynamically. In this trade, we configured three simultaneous exit conditions, where the first one to be met closes the position:

1. Financial Target (TP): A fixed Take Profit of 15%.

2. Exit Short Indicator 1 (Technical Exit 1): If the average (SMA72) crosses above the average (SMA200), the trade is closed.

3. Exit Short Indicator 2 (Technical Exit 2): If the PVI crosses above the EMA300, indicating an entry of buying strength, the trade is closed.

"OR" Logic: The tool monitors these conditions in real-time. Whichever occurs first triggers the exit, ensuring you lock in profit (TP) or protect your capital at the first sign from the indicators.

In this strategy, we use the external indicators: Multiple MTF MA and Positive Volume Index .

--

Reversal Mode (Stop and Reverse)

The Reversal Mode (Stop and Reverse) allows a new signal in the opposite direction (e.g., a SELL signal) to automatically close an existing position (e.g., BUY) and open a new one (sell). This "stop and reverse" function can be enabled or disabled in the settings, giving you full control over whether the strategy should only exit (awaiting a new signal) or immediately reverse the position.

Explaining the Fourth Image Example (Chart Below)

In this example, we demonstrate a setup focused on capturing every market "flip," keeping the trader positioned 100% of the time ("Always-in"), a technique widely used in automation.

- Long Entry: Occurs immediately upon confirming a bullish change of character (New CHoCH Bullish).

- Short Entry: Occurs immediately upon confirming a bearish change of character (New CHoCH Bearish).

- Exit (The Differentiator): We are not using fixed TP or SL here. The exit is triggered by Automatic Reversal.

The Power of "Exit by Opposite Signal"

Notice the labels on the chart: "Close Short" followed immediately by a "Long." This happens because the Allow Reversal function is enabled in the tool's settings.

When the market generates a buy signal, the tool understands that the sell thesis has been invalidated. It simultaneously sends an order to close the Short position and open a new Long position.

When to use this exit rule?

- Capturing Long Trends / Directional Movements: Ideal for volatile assets where you want to ride the trend until the market structure effectively changes.

- Operational Simplification: Eliminates the need to guess profit targets and acts as a loss limiter when the price moves against your position. The market dictates when to enter and when to exit.

Hybrid Flexibility:

The strongest point of Logic Flow is that you don't have to choose just one method. Reversal can be used in two ways:

1. Individually (as in the image): Reversal is the only form of exit. You stay in the move until the opposite signal.

2. Combined (Hybrid): You can enable Reversal and configure a safety Stop Loss + technical Take Profit (Exit Long/Short Indicator).

- Example: If the price hits your TP/SL first, you exit. If the market turns before the TP, the Reversal takes you out of the trade and generates a new trend alert.

In this strategy, we use the external indicators: Smart Money Concepts .

--

Backtesting: Far beyond creating logic and generating signals, Logic Flow Signals stands out due to its Integrated Backtest.

Backtesting serves as a reality check for the trader. It takes the strategy out of the realm of "imagination" and puts it to the test against historical data.

Here are the 4 main practical uses:

1. Verifying Feasibility (Proof of Concept): The most obvious use is to answer: "Does this idea make money?". Many strategies look visually perfect on the chart, but when you run the backtest, you discover that brokerage fees or frequent "stops" consume all the profit.

2. Knowing the "Worst-Case Scenario" (Drawdown): Maximum Drawdown: It shows you what the largest accumulated drop the strategy has ever experienced was. By identifying a Drawdown that exceeds the desired risk tolerance, the backtest allows for parameter optimization in search of a more efficient balance between risk and return.

3. Fine-Tuning (Optimization): It allows you to make changes such as: Increasing the profit target, changing the stop, removing an indicator, changing the chart timeframe, among other actions. You can test various variations instantly to find the most efficient configuration.

4. Expectation Management and Discipline: Backtesting does not eliminate fear nor guarantee that the future will repeat the past, but it serves as a reference map.

The Real Role: Aligning expectation with reality.

In the image below, you can check out how a backtest result is generated:

To understand the backtest results shown above, check the chart and the detailed operational logic below:

This operational example seeks to identify altcoins that are demonstrating an explosive decorrelation relative to Bitcoin. The logic is: we want to buy only the assets that are outperforming the market leader, precisely at the moment when speculative money (Open Interest) heavily enters the market.

For the buy signal (Long) to be triggered, three conditions must be simultaneously true (Stage 1):

Long Indicator 1 (Altcoin Strength): The asset's RSI must be above the 70 level (Overbought), indicating extremely strong bullish momentum.

Long Indicator 2 (Bitcoin Weakness): Bitcoin's RSI must be below the 50 level. This confirms that the Altcoin's rally is genuine and independent.

Long Indicator 3 (Money Flow): The Open Interest (open contracts) must be above the Extreme level of the OI DELTA indicator. This validates that new money is aggressively entering the asset to sustain the rally.

Risk Management: In this example, we configured an aggressive target to capture the altcoin volatility:

- Take Profit: 100%

- Stop Loss: 20%

- Risk/Reward: 5:1

In this strategy, we use the external indicators: RSI Crypto Strength (Asset vs BTC) and Open Interest Delta .

--

Configuring an Indicator Block

Each block (BUY INDICATOR 1, BUY INDICATOR 2, ...) allows you to define a complete condition.

- Enable (Activate): Simply turns this indicator block on or off.

- Source A: The first value you want to analyze.

example: The Closing Price (Close), Opening Price (Open), or another TradingView indicator.

- Condition: How 'Source A' will be compared.

example: Crossover/Crossunder, Greater Than, Less Than, Cross Up.

- Comparison Type: The option that defines whether you will compare 'Source A' with a fixed number or with another indicator.

- Fixed Value: Used if you selected "Fixed Value".

example: For an RSI greater than 70 condition, Source A would be the RSI, the Condition would be Greater Than, and the Fixed Value would be 70.

- Source B: Used if you selected "Source B".

example: For a condition where the EMA10 crosses above the EMA200, Source A would be the EMA10, the Condition would be 'Cross Up', and Source B would be the EMA200.

--

Configurable Alert Signals

Configurable Alert Signals: The tool allows for the creation of fully customized alerts for different types of events, such as entries, signal-based exits, take profit, and stop loss. These alerts can be used for both strategy automation and manual, real-time notifications.

The message field is highly flexible: it accepts dynamic placeholders, JSON structure, UUID identifiers, or any custom text, allowing integration with other external tools and systems via webhook.

Configuring Your Messages:

- LONG/SHORT - ALERTS: Defines the message for new entries.

- LONG/SHORT INDICATOR EXIT - ALERTS: Defines the message for signal-based exits (e.g., moving average cross).

- REVERSAL - ALERTS: Defines the message for when a position is closed by an opposite signal (stop-and-reverse).

- LONG/SHORT TP/SL EXIT - ALERTS: Defines the message for exits triggered by take profit (TP) or stop loss (SL), via percentage or ticks.

A Single Alert to Control Everything

You don't need to create separate alerts for "Buy," "Sell," or "Exits." On a single screen, you can create strategies by defining entries, signal-based exits, profit targets, or stop limits.

Alert Times (Operating Window)

In the Alert Times section, you can define a specific time (and time zone) for the strategy to generate entry or exit signals.

--

To create your alert, simply follow these steps:

- Condition: Select the script name: "Logic Flow Signals & Backtest".

- Message: Insert only the placeholder: {{strategy.order.alert_message}}

Once this single alert is active, it will "listen" to all orders executed by the strategy.

This means you can have your Long-Term, Short-Term, Signal-Based Exits, and TP/SL strategies active simultaneously. When any of these events are plotted on the chart, the script will send the customized message (which you wrote in the fields) to your single alert.

--

Advanced period filters: Allow you to test the strategy in specific date ranges, over the last X days, or over the last X bars, facilitating performance analysis in different market environments.

--

Status Panel: Displays a clear summary of all active rules and settings directly on the chart, facilitating the visualization and confirmation of the running logic.

Additionally, it has a settings box where you can activate or deactivate the panel, choose its position (such as at the bottom or side), and adjust its size.

--

The Thumbnail strategy uses the following external indicators: Multiple MTF MA and Breakout Finder .

--

Final Considerations:

The Logic Flow Signals & Backtest tool is a versatile and powerful system, designed to test and apply trading ideas based on multiple indicators from TradingView.

Its differential is being a customization environment: the script does not have integrated graphical indicators, as the objective is precisely to allow the user to combine and integrate multiple existing indicators in the TradingView community to build unique entry and exit logics.

It offers flexibility and precision, but the true value emerges when the trader integrates the tool into a consistent trading plan, with efficient risk management (Stop Loss and Take Profit), leverage control, and a professional mindset.

Important: Risk of Repainting (Unstable Data): Avoid indicators that 'repaint' (those that change their values in past bars after the closing of new candles). The backtest will be invalidated, and the actual performance of the strategy will fail.

Legal Warning and Didactic Purpose:

It is fundamental to understand that all visual examples, charts, and texts contained in this description do not constitute financial advice, buy or sell recommendations, nor a promise of easy or guaranteed gains.

This is an advanced support tool, not an automatic profit system. Use the integrated backtesting to evaluate the historical behavior of strategies before real execution and understand how different market conditions impact your results. The sole purpose of this material is to demonstrate the logical and execution capacity of the script, serving as a didactic guide for you to test and validate your own ideas.

Conclusion and Risk Warning:

Success in financial markets comes not only from a set of charting indicators, but from the trader's understanding, practice, and discipline. Our objective is to provide a robust, customizable, and intuitive solution, created to enhance your technical analysis and broaden your strategic vision, without replacing critical thinking and conscious decision-making.

Finally, remember: past results do not guarantee future performance. The real differentiator lies in continuous learning, testing, and evolution.

PA Builder [PrimeAutomation]1. PA Builder – Overview

PA Builder is not a fixed strategy; it’s a framework for building strategies. Instead of giving traders one rigid system, it provides a toolbox where entries, exits, filters, risk parameters, and automation rules can all be defined and combined. The core philosophy is confluence: the idea that a trade should only be taken when multiple independent signals agree. The Builder is built around this principle. Every module; trend, reactors, bands, reversals, volume, structure, divergences, externals can be treated as one layer of confidence. The stronger the alignment across layers, the higher the quality of the setup in theory.

In practice, this means PA Builder encourages traders to think in terms of “confluence,” not single indicators. Trend and positioning define whether you should even be looking for longs or shorts. Timing tools such as bands, reversals and candlestick structures determine when inside that broader bias you want to engage. Confirmation tools like volume and flow tell you whether capital is actually supporting the move. Filter systems then ensure that even if everything looks good locally, you still respect higher-timeframe or opposing warnings. The Builder’s philosophy is simple: enter less often, but only when conditions are genuinely in your favour.

2. Core Entry Signal Components

The entry logic in PA Builder is built on a set of signal engines that can be combined in many ways. Trend Signals form a natural foundation. They use low-lag low-pass filters, borrowed from audio signal processing, to extract directional bias from price without the classic delay of classical moving averages. The sensitivity parameter controls how reactive this engine is: lower values favour cleaner trends and fewer whipsaws, while higher values are better suited to short-term intraday trading where speed matters more than smoothness. Many traders start by requiring that Trend Signals show “all bullish” or “all bearish” before allowing any entries in that direction.

Trend signals firing short positions

On top of this directional backbone, the Dynamic Reactor behaves as an adaptive baseline. It accelerates in volatile phases and slows down during consolidation, effectively acting as a moving reference point for both trend and price position. A typical use of this module is to insist that, for long trades, the price sits above a bullish reactor; for shorts, below a bearish one. At the higher-timeframe level, the Quantum Reactor provides a VWAP-style reference that can be anchored to larger candles than the chart you are trading. A common configuration is to trade on a 15-minute chart while requiring that price is above the 4-hour Quantum Reactor for longs or below it for shorts. The “fast” and “slow” options determine how quickly this reference adapts to new information.

Timing is then refined with tools like Quantum Bands, reversals and candle structure analysis. Quantum Bands identify extremes within the current environment. In an uptrend, a tag of the lower band can be treated as a pullback rather than a breakdown; in a downtrend, the upper band acts like a shorting zone. Many traders combine “trend up and above higher-timeframe reactor” with “price temporarily below lower band” to construct a mean-reversion entry inside a larger uptrend. Reversal detection modules examine recent bars to find turning points, with shorter lookbacks capturing fast flips and longer lookbacks tracking deeper structural changes. Candle structure logic goes beyond classical candlestick names and instead focuses on whether price action confirms follow-through or reversion behaviour, with options like “2X” modes that wait for two successive confirmations before acting.

Before and after filtering using reactor applied.

Additional confirmation layers come from Volume Matrix, Money Flow, OSC True7 and divergence detection. Volume and flow tools answer whether actual capital is participating in the move or whether price is drifting on thin activity. OSC True7 categorises the state of the trend into intuitive buckets, strong, healthy, neutral, or exhausted, making it easier to avoid chasing extremes. Divergences between price and momentum can be used either as entry triggers in contrarian systems or as hard filters that block trades when warning signs are present. Finally, two external indicator inputs make it possible to integrate RSI, MACD, custom indicators or even other strategies into the Builder, either as simple thresholds or as comparative logic between two external sources (for example, requiring a fast EMA to be above a slow EMA before allowing longs).

3. Exit System & Trade Management

The exit systems in PA Builder are designed to be as vital as the entry logic. It assumes exits are not an afterthought, but half of the edge. Instead of forcing a single take profit point, the system uses a three-tier structure where you can assign different portions of the position to different targets. A common pattern is to scale out a small portion early (for example at one ATR), another portion at an intermediate level, and keep the largest slice for a deeper move. This creates a natural balance: you book something early to reduce emotional stress, while leaving room to participate in the full potential of a trend.

Targets can be defined using ATR multiples or risk-to-reward ratios that are directly tied to the initial stop distance. Using ATR keeps exits proportional to current volatility. A two ATR target in a quiet environment is very different in absolute price distance from the same multiple in a high-volatility environment, yet conceptually it represents the same “size” move. Risk-to-reward exits build on this by ensuring that if you risk one unit (1R), the reward targets are set at predefined multiples of that risk. This enforces positive expectancy at the structural level: the strategy cannot generate entries with inherently negative payoffs.

Once price begins to move in your favour, trailing logic takes over if you choose to enable it. Trailing can begin immediately from entry or only after a target has been hit. Many users prefer to let TP1 and TP2 behave as fixed profit points and then apply a trailing stop or trailing take profit to the final remainder. That way, routine winners are banked mechanically, while occasional explosive moves can be ridden for as long as the market allows. The breakeven module supports this behaviour by automatically moving stops to entry (or slightly through entry into profit) after a specified condition such as TP1 being hit. This transforms the risk profile mid trade: once breakeven has been secured, remaining size can be managed with much less psychological pressure.