Probability Grid [LuxAlgo]The Probability Grid tool allows traders to see the probability of where and when the next reversal would occur, it displays a 10x10 grid and/or dashboard with the probability of the next reversal occurring beyond each cell or within each cell.

🔶 USAGE

By default, the tool displays deciles (percentiles from 0 to 90), users can enable, disable and modify each percentile, but two of them must always be enabled or the tool will display an error message alerting of it.

The use of the tool is quite simple, as shown in the chart above, the further the price moves on the grid, the higher the probability of a reversal.

In this case, the reversal took place on the cell with a probability of 9%, which means that there is a probability of 91% within the square defined by the last reversal and this cell.

🔹 Grid vs Dashboard

The tool can display a grid starting from the last reversal and/or a dashboard at three predefined locations, as shown in the chart above.

🔶 DETAILS

🔹 Raw Data vs Normalized Data

By default the tool displays the normalized data, this means that instead of using the raw data (price delta between reversals) it uses the returns between each reversal, this is useful to make an apples to apples comparison of all the data in the dataset.

This can be seen in the left side of the chart above (BTCUSD Daily chart) where normalize data is disabled, the percentiles from 0 to 40 overlap and are indistinguishable from each other because the tool uses the raw price delta over the entire bitcoin history, with normalize data enabled as we can see in the right side of the chart we can have a fair comparison of the data over the entire history.

🔹 Probability Beyond or Within Each Cell

Two different probability modes are available, the default mode is Probability Beyond Each Cell, the number displayed in each cell is the probability of the next reversal to be located in the area beyond the cell, for example, if the cell displays 20%, it means that in the area formed by the square starting from the last reversal and ending at the cell, there is an 80% probability and outside that square there is a 20% probability for the location of the next reversal.

The second probability mode is the probability within each cell, this outlines the chance that the next reversal will be within the cell, as we can see on the right chart above, when using deciles as percentiles (default settings), each cell has the same 1% probability for the 10x10 grid.

🔶 SETTINGS

Swing Length: The maximum length in bars used to identify a swing

Maximum Reversals: Maximum number of reversals included in calculations

Normalize Data: Use returns between swings instead of raw price

Probability: Choose between two different probability modes: beyond and inside each cell

Percentiles: Enable/disable each of the ten percentiles and select the percentile number and line style

🔹 Dashboard

Show Dashboard: Enable or disable the dashboard

Position: Choose dashboard location

Size: Choose dashboard size

🔹 Style

Show Grid: Enable or disable the grid

Size: Choose grid text size

Colors: Choose grid background colors

Show Marks: Enable/disable reversal markers

Forecast

Forward-Backward Exponential Oscillator [LuxAlgo]The Forward-Backward Exponential Oscillator is a normalized oscillator able to estimate directional shifts by making use of a unique "Forward-Backward Filtering" calculation method for Exponential Moving Averages (EMAs).

This unique method provides a smooth normalized representation of the price with reduced lag.

🔶 USAGE

The oscillator consists of 2 series of values derived from normalizing the sum of each EMA's change across the selected user lookback window (length), one less reactive computed forward (in grey), and the other re-calculated backward for each bar (in blue).

Given this "Forward-Backwards" calculation method, we are able to produce a more reactive oscillator compared to the same operation done on a simple double-smoothed EMA.

The interaction between these 2 values (Forward Value and Backward Value) can highlight shifts in market momentum over time.

When the Forward Value is above the Backward Value, the price is seen moving up, and likewise, when the Forward EMA is below, the Backward EMA price is seen moving down.

The indicator specifically displays the difference between values through a histogram located at the 50 mark on the oscillator.

🔹 Projection

We project the approximated future values of the forward value in front of the current line. This helps show the data that is being used for the creation of the Forward Value.

🔹 Length & Smoothing

The Smoothing Input controls the length of the EMAs which are analyzed.

The Length Input controls the lookback for the sum of changes from the EMAs.

Displayed below is a comparison of varying input sizes and their results.

As seen above:

A larger length input will result in slower, gradual movement by the oscillator since the summed values are from a larger lookback.

A higher smoothing setting will result in smoother EMAs, leading to a smoother oscillator output that is less contaminated by noisy variations.

Note: The length of the projection is tied to the "length" input, to get a longer projection, a larger length is required.

🔶 DETAILS

Forward-backward filtering is a method applied to LTI (linear time-invariant) filters to provide a filter response with zero-phase shift, this has the visible effect of shifting a regular causal filter response to the right, making it appear has have effectively 0 lag.

The name of this operation indicates that the filter is first calculated forward over a series of values (like regular moving averages), then calculated backward, using the previous output as input for the filter, effectively applying the filter twice.

While this operation effectively allows us to obtain a zero-lag response when applied to an EMA, it is subject to repainting, as this indicator only returns the normalized sum of changes of the forward-backward EMA, which does not introduce any repainting behaviors in the final output of the oscillator.

🔶 SETTINGS

Length: Change the calculation lookback length for the oscillator.

Smoothing: Alter the smoothness of the back-end EMA calculations.

Source: Change the source input used for the indicator.

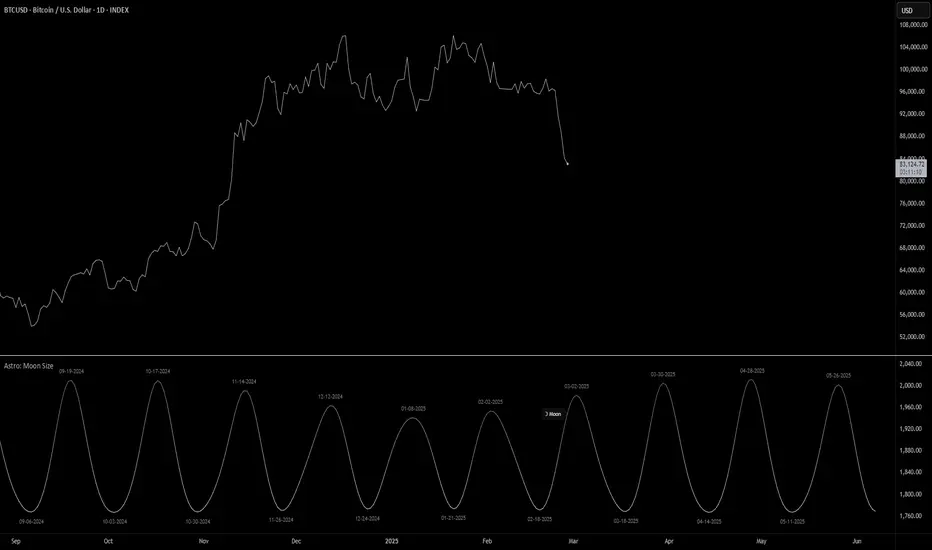

Astro: Moon SizeThe Astro: Moon Size indicator, built using AstroLib , calculates the distance and visualizes the apparent size of the Moon based on astronomical positioning. This script is tailored for the 1D timeframe and provides insights into lunar perigees (closest approach) and apogees (farthest distance), making it useful for astrologically-informed trading strategies.

New Astro Indicators Feature:

By setting the Julian Date to X number of days in the future, and offsetting the plot by X number of bars accordingly, it is now possible to visualize future projections of TradingView indicators that reference the AstroLib . This feature has been long requested and is far overdue, so thank you to everyone who pushed for this feature release. Enjoy, time travelers from the future!!

Key Features:

Moon Size Calculation: Uses Julian Date (J2000) conversion and AstroLib functions to determine the Moon's apparent distance.

Future Projection: Displays the Moon's distance from 28 up to 500 days ahead, with color gradients indicating proximity/size.

Pivot Identification: Marks local maxima (apogees) and minima (perigees) with labeled date stamps for easy reference.

Dynamic Labeling: Adapts label positioning and size based on the Moon's current trend and relative size.

Usage Notes:

⚠️ Timeframe Restriction: For now, the script only functions on the 1D timeframe and will prompt an error otherwise.

⚠️ Asset Restriction: This script is meant to be loaded on charts for assets that trade 24/7, like BTCUSD historical index.

[COG] WeatherForecaster🌤️ Just like a weather forecast that adjusts as new data emerges, this TMA Pivot Points Forecaster adapts to evolving market conditions!

Description:

This indicator combines the power of a Triple Moving Average (TMA) with pivot point analysis to identify potential market turning points and trend directions. Like a meteorologist using various atmospheric data to predict weather patterns, this tool analyzes price action through multiple lenses to forecast potential market movements.

Key Features:

- Dynamic TMA Line: Acts as our "atmospheric pressure system," showing the underlying market direction

- Adaptive Pivot Points: Like weather stations, these pivots identify key market levels where the "climate" might change

- Smart Entry Signals: ☀️ and 🌧️ icons appear when conditions align for potential trades

- Timeframe-Adaptive: Automatically adjusts sensitivity across different timeframes

- Customizable Visuals: Adjust colors and styles to match your trading environment

Settings Include:

✓ TMA Length and Slope Sensitivity

✓ Pivot Point Parameters

✓ Visual Customization Options

✓ Toggle Entry Signals

✓ Toggle Pivot Lines

Note: Like weather forecasts that update with new data, this indicator recalculates as market conditions evolve. Past signals may adjust as more price action develops. Always use proper risk management and combine with other analysis tools.

Usage Guide:

The indicator works best when used as part of a complete trading system. Here's how to interpret the signals:

📈 Bullish Conditions:

- TMA Line turns green: Indicates upward momentum

- "Buy above 🌋" level appears: Potential resistance turned support level

- ☀️ Signal: Indicates favorable buying conditions

📉 Bearish Conditions:

- TMA Line turns red: Indicates downward momentum

- "Sell below 🌋" level appears: Potential support turned resistance level

- 🌧️ Signal: Indicates favorable selling conditions

⏺️ Ranging Conditions:

- TMA Line turns yellow: Market in consolidation

- 💤 Signal: Suggests waiting for clearer direction

Best Practices:

1. Higher timeframes (4H, Daily) tend to produce more reliable signals

2. Use the pivot lines as potential entry/exit reference points

3. Adjust the TMA length based on your trading style:

• Shorter lengths (20-30) for more active trading

• Longer lengths (50-60) for trend following

Settings Explained:

TMA Settings:

- TMA Length: Determines the smoothing period (default: 30)

- Slope Threshold: Controls trend sensitivity (default: 0.015)

Pivot Settings:

- Left/Right Bars: Controls pivot point calculation

- Line Length: Adjusts the visual length of pivot lines

- Line Style & Colors: Customize the visual appearance

Disclaimer:

Past performance does not guarantee future results. This indicator, like any technical tool, provides possibilities rather than certainties. Please test thoroughly on your preferred timeframes and markets before using with real capital.

Bollinger Bands Reversal Strategy Analyzer█ OVERVIEW

The Bollinger Bands Reversal Overlay is a versatile trading tool designed to help traders identify potential reversal opportunities using Bollinger Bands. It provides visual signals, performance metrics, and a detailed table to analyze the effectiveness of reversal-based strategies over a user-defined lookback period.

█ KEY FEATURES

Bollinger Bands Calculation

The indicator calculates the standard Bollinger Bands, consisting of:

A middle band (basis) as the Simple Moving Average (SMA) of the closing price.

An upper band as the basis plus a multiple of the standard deviation.

A lower band as the basis minus a multiple of the standard deviation.

Users can customize the length of the Bollinger Bands and the multiplier for the standard deviation.

Reversal Signals

The indicator identifies potential reversal signals based on the interaction between the price and the Bollinger Bands.

Two entry strategies are available:

Revert Cross: Waits for the price to close back above the lower band (for longs) or below the upper band (for shorts) after crossing it.

Cross Threshold: Triggers a signal as soon as the price crosses the lower band (for longs) or the upper band (for shorts).

Trade Direction

Users can select a trade bias:

Long: Focuses on bullish reversal signals.

Short: Focuses on bearish reversal signals.

Performance Metrics

The indicator calculates and displays the performance of trades over a user-defined lookback period ( barLookback ).

Metrics include:

Win Rate: The percentage of trades that were profitable.

Mean Return: The average return across all trades.

Median Return: The median return across all trades.

These metrics are calculated for each bar in the lookback period, providing insights into the strategy's performance over time.

Visual Signals

The indicator plots buy and sell signals on the chart:

Buy Signals: Displayed as green triangles below the price bars.

Sell Signals: Displayed as red triangles above the price bars.

Performance Table

A customizable table is displayed on the chart, showing the performance metrics for each bar in the lookback period.

The table includes:

Win Rate: Highlighted with gradient colors (green for high win rates, red for low win rates).

Mean Return: Colored based on profitability (green for positive returns, red for negative returns).

Median Return: Colored similarly to the mean return.

Time Filtering

Users can define a specific time window for the indicator to analyze trades, ensuring that performance metrics are calculated only for the desired period.

Customizable Display

The table's font size can be adjusted to suit the user's preference, with options for "Auto," "Small," "Normal," and "Large."

█ PURPOSE

The Bollinger Bands Reversal Overlay is designed to:

Help traders identify high-probability reversal opportunities using Bollinger Bands.

Provide actionable insights into the performance of reversal-based strategies.

Enable users to backtest and optimize their trading strategies by analyzing historical performance metrics.

█ IDEAL USERS

Swing Traders: Looking for reversal opportunities within a trend.

Mean Reversion Traders: Interested in trading price reversals to the mean.

Strategy Developers: Seeking to backtest and refine Bollinger Bands-based strategies.

Performance Analysts: Wanting to evaluate the effectiveness of reversal signals over time.

ForecastPro by BinhMyco1. Overview:

This Pine Script implements a custom forecasting tool on TradingView, labeled "BinhMyco." It provides a method to predict future price movements based on historical data and a comparison with similar historical patterns. The script supports two types of forecasts: **Prediction** and **Replication**, where the forecasted price can be either based on price peaks/troughs or an average direction. The script also calculates a confidence probability, showing how closely the forecasted data aligns with historical trends.

2. Inputs:

- Source (`src`): The input data source for forecasting, which defaults to `open`.

- Length (`len`): The length of the training data used for analysis (fixed at 200).

- Reference Length (`leng`): A fixed reference length for comparing similar historical patterns (set to 70).

- Forecast Length (`length`): The length of the forecast period (fixed at 60).

- Multiplier (`mult`): A constant multiplier for the forecast confidence cone (set to 4.0).

- Forecast Type (`typ`): Type of forecast, either **Prediction** or **Replication**.

- Direction Type (`dirtyp`): Defines how the forecast is calculated — either based on price **peaks/troughs** or an **average direction**.

- Forecast Divergence Cone (`divcone`): A boolean option to enable the display of a confidence cone around the forecast.

3. Color Constants:

- Green (`#00ffbb`): Color used for upward price movements.

- Red (`#ff0000`): Color used for downward price movements.

- Reference Data Color (`refcol`): Blue color for the reference data.

- Similar Data Color (`simcol`): Orange color for the most similar data.

- Forecast Data Color (`forcol`): Yellow color for forecasted data.

4. Error Checking:

- The script checks if the reference length is greater than half the training data length, and if the forecast length exceeds the reference length, raising errors if either condition is true.

5. Arrays for Calculation:

- Correlation Array (`c`): Holds the correlation values between the data source (`src`) and historical data points.

- Index Array (`index`): Stores the indices of the historical data for comparison.

6. Forecasting Logic:

- Correlation Calculation: The script calculates the correlation between the historical data (`src`) and the reference data over the given reference length. It then identifies the point in history most similar to the current data.

- Forecast Price Calculation: Based on the type of forecast (Prediction or Replication), the script calculates future prices either by predicting based on similar bars or by replicating past data. The forecasted prices are stored in the `forecastPrices` array.

- Forecast Line Drawing: The script draws lines to represent the forecasted price movements. These lines are color-coded based on whether the forecasted price is higher or lower than the current price.

7. Divergence Cone (Optional):

- If the **divcone** option is enabled, the script calculates and draws a confidence cone around the forecasted prices. The upper and lower bounds of the cone are calculated using a standard deviation factor, providing a visual representation of forecast uncertainty.

8. Probability Table:

- A table is displayed on the chart, showing the probability of the forecast being accurate. This probability is calculated using the correlation between the current data and the most similar historical pattern. If the probability is positive, the table background turns green; if negative, it turns red. The probability is presented as a percentage.

9. Key Functions:

- `highest_range` and `lowest_range`: Functions to find the highest and lowest price within a range of bars.

- `ftype`: Determines the forecast type (Prediction or Replication) and adjusts the forecasting logic accordingly.

- `ftypediff`: Computes the difference between the forecasted and actual prices based on the selected forecast type.

- `ftypelim`, `ftypeleft`, `ftyperight`: Additional functions to adjust the calculation of the forecast based on the forecast type.

10. Conclusion:

The "ForecastPro" script is a unique tool for forecasting future price movements on TradingView. It compares historical price data with similar historical trends to generate predictions. The script also offers a customizable confidence cone and displays the probability of the forecast's accuracy. This tool provides traders with valuable insights into future price action, potentially enhancing decision-making in trading strategies.

---

This script provides advanced functionality for traders who wish to explore price forecasting, and can be customized to fit various trading styles.

Three Step Future-Trend [BigBeluga]Three Step Future-Trend by BigBeluga is a forward-looking trend analysis tool designed to project potential future price direction based on historical periods. This indicator aggregates data from three consecutive periods, using price averages and delta volume analysis to forecast trend movement and visualize it on the chart with a projected trend line and volume metrics.

🔵 Key Features:

Three Period Analysis: Calculates price averages and delta volumes from three specified periods, creating a consolidated view of historical price movement.

Future Trend Line Projection: Plots a forward trend line based on the calculated averag of three periods, helping traders visualize potential future price movement.

Avg Delta Volume and Future Price Label: Shows a delta average Volume a long with a Future Price label at the end of the projected trend line, indicating the possible future delta volume and future Price.

Volume Data Table: Displays a detailed table showing delta and total volume for each of the three periods, allowing quick volume comparison to support the projected trend.

This indicator provides a dynamic way to anticipate market direction by blending price and volume data, giving traders insights into both volume and trend strength in upcoming periods.

High/Low Location Frequency [LuxAlgo]The High/Low Location Frequency tool provides users with probabilities of tops and bottoms at user-defined periods, along with advanced filters that offer deep and objective market information about the likelihood of a top or bottom in the market.

🔶 USAGE

There are four different time periods that traders can select for analysis of probabilities:

HOUR OF DAY: Probability of occurrence of top and bottom prices for each hour of the day

DAY OF WEEK: Probability of occurrence of top and bottom prices for each day of the week

DAY OF MONTH: Probability of occurrence of top and bottom prices for each day of the month

MONTH OF YEAR: Probability of occurrence of top and bottom prices for each month

The data is displayed as a dashboard, which users can position according to their preferences. The dashboard includes useful information in the header, such as the number of periods and the date from which the data is gathered. Additionally, users can enable active filters to customize their view. The probabilities are displayed in one, two, or three columns, depending on the number of elements.

🔹 Advanced Filters

Advanced Filters allow traders to exclude specific data from the results. They can choose to use none or all filters simultaneously, inputting a list of numbers separated by spaces or commas. However, it is not possible to use both separators on the same filter.

The tool is equipped with five advanced filters:

HOURS OF DAY: The permitted range is from 0 to 23.

DAYS OF WEEK: The permitted range is from 1 to 7.

DAYS OF MONTH: The permitted range is from 1 to 31.

MONTHS: The permitted range is from 1 to 12.

YEARS: The permitted range is from 1000 to 2999.

It should be noted that the DAYS OF WEEK advanced filter has been designed for use with tickers that trade every day, such as those trading in the crypto market. In such cases, the numbers displayed will range from 1 (Sunday) to 7 (Saturday). Conversely, for tickers that do not trade over the weekend, the numbers will range from 1 (Monday) to 5 (Friday).

To illustrate the application of this filter, we will exclude results for Mondays and Tuesdays, the first five days of each month, January and February, and the years 2020, 2021, and 2022. Let us review the results:

DAYS OF WEEK: `2,3` or `2 3` (for crypto) or `1,2` or `1 2` (for the rest)

DAYS OF MONTH: `1,2,3,4,5` or `1 2 3 4 5`

MONTHS: `1,2` or `1 2`

YEARS: `2020,2021,2022` or `2020 2021 2022`

🔹 High Probability Lines

The tool enables traders to identify the next period with the highest probability of a top (red) and/or bottom (green) on the chart, marked with two horizontal lines indicating the location of these periods.

🔹 Top/Bottom Labels and Periods Highlight

The tool is capable of indicating on the chart the upper and lower limits of each selected period, as well as the commencement of each new period, thus providing traders with a convenient reference point.

🔶 SETTINGS

Period: Select how many bars (hours, days, or months) will be used to gather data from, max value as default.

Execution Window: Select how many bars (hours, days, or months) will be used to gather data from

🔹 Advanced Filters

Hours of day: Filter which hours of the day are excluded from the data, it accepts a list of hours from 0 to 23 separated by commas or spaces, users can not mix commas or spaces as a separator, must choose one

Days of week: Filter which days of the week are excluded from the data, it accepts a list of days from 1 to 5 for tickers not trading weekends, or from 1 to 7 for tickers trading all week, users can choose between commas or spaces as a separator, but can not mix them on the same filter.

Days of month: Filter which days of the month are excluded from the data, it accepts a list of days from 1 to 31, users can choose between commas or spaces as separator, but can not mix them on the same filter.

Months: Filter months to exclude from data. Accepts months from 1 to 12. Choose one separator: comma or space.

Years: Filter years to exclude from data. Accepts years from 1000 to 2999. Choose one separator: comma or space.

🔹 Dashboard

Dashboard Location: Select both the vertical and horizontal parameters for the desired location of the dashboard.

Dashboard Size: Select size for dashboard.

🔹 Style

High Probability Top Line: Enable/disable `High Probability Top` vertical line and choose color

High Probability Bottom Line: Enable/disable `High Probability Bottom` vertical line and choose color

Top Label: Enable/disable period top labels, choose color and size.

Bottom Label: Enable/disable period bottom labels, choose color and size.

Highlight Period Changes: Enable/disable vertical highlight at start of period

Future Trend Channel [ChartPrime]The Future Trend Channel indicator is a dynamic tool for identifying trends and projecting future prices based on channel formations. The indicator uses SMA (Simple Moving Average) and volatility calculations to plot channels that visually represent trends. It also detects moments of lower momentum, indicated by neutral color changes in the channels, and projects future price levels for up to 50 bars ahead.

⯁ KEY FEATURES AND HOW TO USE

⯌ Dynamic Trend Channels :

The indicator draws channels when a trend is identified. It uses a combination of SMA and volatility to determine the direction and strength of the trend. Each channel is visualized with a specific color, where green indicates an uptrend and orange represents a downtrend.

Example of channels during uptrend and downtrend:

⯌ Momentum-Based Color Shifts :

The indicator adapts its channel colors based on momentum changes. When the starting point (Y1) of a channel is higher than its ending point (Y2) during an uptrend, the channel turns neutral, indicating lower momentum and a possible ranging market. The same applies in a downtrend, where the channel turns neutral if Y1 is lower than Y2.

Example of neutral momentum channels:

⯌ Future Price Projection :

At the end of each channel, the indicator generates a projected future price based on the midpoint of the channel. By default, this projection is made 50 bars into the future, but users can adjust the number of bars to their preference.

Example of future price projection:

⯌ Diamond Signals for Valid Trends :

Lime-colored diamonds appear when an uptrend channel is confirmed, while orange diamonds indicate valid downtrend channels. These signals confirm the presence of a strong trend and help identify valid entry and exit points. Neutral channels, which indicate lower momentum, do not show diamond signals.

Example of trend confirmation signals:

⯌ Customizable Settings :

Users can adjust the channel length (how far back the trend is analyzed) and the width (which determines the channel boundaries based on volatility). The future price projection can also be customized to forecast further or fewer bars into the future.

⯁ USER INPUTS

Trend Length : Sets the number of bars used to calculate the trend channels.

Channel Width : Adjusts the width of the channels, based on volatility (ATR multiplier).

Up and Down Colors : Allows customization of the colors used for uptrend and downtrend channels.

Future Bars : Sets the number of bars used for future price projection.

⯁ CONCLUSION

The Future Trend Channel indicator is a versatile tool for identifying and trading trends. With its ability to detect momentum shifts and project future prices, it provides traders with key insights for making more informed decisions. The use of diamond signals for trend validation adds an extra layer of confirmation, helping traders act with greater confidence during volatile or trending markets.

Dual price forecast with Projection Zone [FXSMARTLAB]The Dual Price Forecast with Projection Zone indicator is built to simulate potential future price paths based on historical price movements over two defined lookback periods. By running multiple trials (or simulations) on these historical price movements, the indicator achieves a more robust forecast, incorporating the inherent variability of price behavior.

Key Components and Calculation Details

1. Lookback Periods and Historical Price Movements

Lookback Period 1 and Lookback Period 2 specify the range of past data used to generate each projection. For each period, the indicator calculates the price variations (differences between the closing and opening prices) and stores these in arrays.

These historical price variations capture the volatility and price patterns within each period, serving as templates for future price behavior.

2. Trials: Purpose and Function

The trials are a critical element in the projection calculation. Each trial represents a single simulation of possible future price movements, derived from a random reordering of the historical price variations in each lookback period.

By running multiple trials , the indicator explores various sequences of historical movements, simulating different possible future paths. Each trial adds to the projection’s robustness by capturing a unique potential price path based on past behavior.

Running these multiple trials allows the indicator to account for randomness in price behavior, making the projections more comprehensive by covering a range of scenarios rather than relying on a single deterministic forecast.

3. Reverse Option

The reverse option allows the indicator to invert the direction of price movements within each lookback period. When enabled, historical uptrends are treated as downtrends, and vice versa.

This feature is particularly valuable in scenarios where traders expect a potential reversal in market direction. By enabling the reverse option, the indicator can simulate what might happen if past trends inverted, providing an alternative forecast path that considers possible market reversals.

This allows traders to assess both continuation and reversal scenarios, giving them a more balanced view of potential future price paths and helping them prepare for either market direction.

4. Generating the Average Projection Path

Once the trials are complete, the indicator calculates an average projected price path for each lookback period by averaging the results of all trials. This average represents the most likely price trend based on historical data and provides a smoothed projection that mitigates extreme outliers.

By averaging across all trial paths, the indicator generates a more reliable and balanced forecast line, smoothing out the fluctuations that might appear if only one trial or a small number of trials were used.

5. Projection Zone Visualization

The indicator plots the two average projection paths (one for each lookback period) as Projection 1 and Projection 2, each in a user-defined color.

The Projection Zone is the area between these two lines, filled with a semi-transparent color. This zone visually represents the potential range of future price movement, highlighting where prices are likely to oscillate if historical trends persist.

The Projection Zone effectively functions as a potential support and resistance boundary, providing traders with a visual reference for possible price fluctuations within a specific range.

6. Display of Lookback Zones

To give context to the projections, the indicator can also display colored lookback zones on the chart. These zones correspond to Lookback Period 1 and Lookback Period 2 and are color-coded to match their respective projection lines.

These zones allow traders to see the sections of historical data used in the calculation, helping them understand which past price behaviors influenced the current projections.

Benefits of the Indicator

The "Dual Price Forecast with Projection Zone" indicator provides a multi-scenario forecast based on past price dynamics. Its use of trials ensures that projections are not based on a single deterministic path but on a range of possible scenarios that better reflect the inherent randomness in financial markets.

By generating a probabilistic forecast within a defined zone, the indicator helps traders to:

Anticipate potential price ranges and areas of support/resistance based on historical trends.

Understand the influence of different timeframes (short-term and long-term lookbacks) on future price behavior.

Make informed decisions by visualizing the likely variability of future prices within a controlled projection zone.

Prepare for both continuation and reversal scenarios, thanks to the reverse option. This feature is especially useful in markets where trends may change direction, as it allows traders to explore what might happen

Similar Price ActionDescription:

The indicator tries to find an area of N candles in history that has the most similar price action to the latest N candles. The maximum search distance is limited to 5000 candles. It works by calculating a coefficient for each candle and comparing it with the coefficient of the latest candle, thus searching for two closest values. The indicator highlights the latest N candles, as well as the most similar area found in the past, and also tries to predict future price based on the latest price and price directly after the most similar area that was found in the past.

Inputs:

- Length -> the area we are searching for is comprised of this many candles

- Lookback -> maximum distance in which a similar area can be found

- Function -> the function used to compare latest and past prices

Notes:

- The indicator is intended to work on smaller timeframes where the overall price difference is not very high, but can be used on any

[DarkTrader] Intersection Level & PredictionLinear Regression Function Reference by @RicardoSantos :

The Intersection Level Calculation process identifies critical price levels where significant market reactions are expected. It starts by analyzing historical price action and technical indicators to pinpoint key support and resistance levels.

Price Forecast Min represents the predicted lowest price level that the asset might reach, while Price Forecast Max indicates the anticipated highest price level. These projections are calculated using statistical methods and historical price patterns, allowing traders to anticipate potential support and resistance zones. By providing these forecasts, traders can better manage their risk and set more informed entry and exit points based on projected price movements.

Example Of Prediction (Before & After)

Predicting Future Price Movements :

Once the intersection levels are identified, the indicator uses various predictive models to forecast what price might do next when it approaches these levels. Here’s a breakdown of how it achieves this :

Price Reaction Analysis: The indicator assesses how price has historically reacted to similar intersection levels. For instance, if price has reversed from a certain support level multiple times, the indicator can predict a potential reversal or bounce when price approaches that level again.

Trend Continuation or Reversal: It examines the strength of the current trend by analyzing momentum indicators, volume, and the angle or direction of trendlines. Based on this, it can predict whether price is likely to break through an intersection level, signaling trend continuation, or bounce off it, indicating a potential reversal.

Confluence of Factors: The prediction mechanism becomes more accurate when multiple factors converge at the same intersection level. For example, if a trendline, moving average, and support zone all intersect at the same price point, the indicator predicts a stronger likelihood of significant price movement.

Market Volatility and Momentum: The indicator also considers current market volatility and momentum in its prediction. For example, if price approaches an intersection level with high momentum, it might predict a breakout, whereas low momentum might suggest consolidation or a weaker price reaction.

In this indicator, I utilize Linear Regression to forecast price movements by analyzing historical data trends. Linear Regression involves fitting a straight line to past price data, enabling me to model and project future price levels based on identified trends. This method calculates a trend line that best represents the historical price behavior, providing a foundation for predicting future price points. By extending this trend line, I can estimate where prices might move, incorporating a range to account for potential deviations. This approach helps in identifying both minimum and maximum forecasted prices, offering valuable insights into potential market directions.

Trend Forecasting - The Quant Science🌏 Trend Forecasting | ENG 🌏

This plug-in acts as a statistical filter, adding new information to your chart that will allow you to quickly verify the direction of a trend and the probability with which the price will be above or below the average in the future, helping you to uncover probable market inefficiencies.

🧠 Model calculation

The model calculates the arithmetic mean in relation to positive and negative events within the available sample for the selected time series. Where a positive event is defined as a closing price greater than the average, and a negative event as a closing price less than the average. Once all events have been calculated, the probabilities are extrapolated by relating each event.

Example

Positive event A: 70

Negative event B: 30

Total events: 100

Probabilities A: (100 / 70) x 100 = 70%

Probabilities B: (100 / 30) x 100 = 30%

Event A has a 70% probability of occurring compared to Event B which has a 30% probability.

🔍 Information Filter

The data on the graph show the future probabilities of prices being above average (default in green) and the probabilities of prices being below average (default in red).

The information that can be quickly retrieved from this indicator is:

1. Trend: Above-average prices together with a constant of data in green greater than 50% + 1 indicate that the observed historical series shows a bullish trend. The probability is correlated proportionally to the value of the data; the higher and increasing the expected value, the greater the observed bullish trend. On the other hand, a below-average price together with a red-coloured data constant show quantitative data regarding the presence of a bearish trend.

2. Future Probability: By analysing the data, it is possible to find the probability with which the price will be above or below the average in the future. In green are classified the probabilities that the price will be higher than the average, in red are classified the probabilities that the price will be lower than the average.

🔫 Operational Filter .

The indicator can be used operationally in the search for investment or trading opportunities given its ability to identify an inefficiency within the observed data sample.

⬆ Bullish forecast

For bullish trades, the inefficiency will appear as a historical series with a bullish trend, with high probability of a bullish trend in the future that is currently below the average.

⬇ Bearish forecast

For short trades, the inefficiency will appear as a historical series with a bearish trend, with a high probability of a bearish trend in the future that is currently above the average.

📚 Settings

Input: via the Input user interface, it is possible to adjust the periods (1 to 500) with which the average is to be calculated. By default the periods are set to 200, which means that the average is calculated by taking the last 200 periods.

Style: via the Style user interface it is possible to adjust the colour and switch a specific output on or off.

🇮🇹Previsione Della Tendenza Futura | ITA 🇮🇹

Questo plug-in funge da filtro statistico, aggiungendo nuove informazioni al tuo grafico che ti permetteranno di verificare rapidamente tendenza di un trend, probabilità con la quale il prezzo si troverà sopra o sotto la media in futuro aiutandoti a scovare probabili inefficienze di mercato.

🧠 Calcolo del modello

Il modello calcola la media aritmetica in relazione con gli eventi positivi e negativi all'intero del campione disponibile per la serie storica selezionata. Dove per evento positivo si intende un prezzo alla chiusura maggiore della media, mentre per evento negativo si intende un prezzo alla chiusura minore della media. Calcolata la totalità degli eventi le probabilità vengono estrapolate rapportando ciascun evento.

Esempio

Evento positivo A: 70

Evento negativo B: 30

Totale eventi : 100

Formula A: (100 / 70) x 100 = 70%

Formula B: (100 / 30) x 100 = 30%

Evento A ha una probabilità del 70% di realizzarsi rispetto all' Evento B che ha una probabilità pari al 30%.

🔍 Filtro informativo

I dati sul grafico mostrano le probabilità future che i prezzi siano sopra la media (di default in verde) e le probabilità che i prezzi siano sotto la media (di default in rosso).

Le informazioni che si possono rapidamente reperire da questo indicatore sono:

1. Trend: I prezzi sopra la media insieme ad una costante di dati in verde maggiori al 50% + 1 indicano che la serie storica osservata presenta un trend rialzista. La probabilità è correlata proporzionalmente al valore del dato; tanto più sarà alto e crescente il valore atteso e maggiore sarà la tendenza rialzista osservata. Viceversa, un prezzo sotto la media insieme ad una costante di dati classificati in colore rosso mostrano dati quantitativi riguardo la presenza di una tendenza ribassista.

2. Probabilità future: analizzando i dati è possibile reperire la probabilità con cui il prezzo si troverà sopra o sotto la media in futuro. In verde vengono classificate le probabilità che il prezzo sarà maggiore alla media, in rosso vengono classificate le probabilità che il prezzo sarà minore della media.

🔫 Filtro operativo

L' indicatore può essere utilizzato a livello operativo nella ricerca di opportunità di investimento o di trading vista la capacità di identificare un inefficienza all'interno del campione di dati osservato.

⬆ Previsione rialzista

Per operatività di tipo rialzista l'inefficienza apparirà come una serie storica a tendenza rialzista, con alte probabilità di tendenza rialzista in futuro che attualmente si trova al di sotto della media.

⬇ Previsione ribassista

Per operatività di tipo short l'inefficienza apparirà come una serie storica a tendenza ribassista, con alte probabilità di tendenza ribassista in futuro che si trova attualmente sopra la media.

📚 Impostazioni

Input: tramite l'interfaccia utente Input è possibile regolare i periodi (da 1 a 500) con cui calcolare la media. Di default i periodi sono impostati sul valore di 200, questo significa che la media viene calcolata prendendo gli ultimi 200 periodi.

Style: tramite l'interfaccia utente Style è possibile regolare il colore e attivare o disattivare un specifico output.

Moving Average Cross Probability [AlgoAlpha]Moving Average Cross Probability 📈✨

The Moving Average Cross Probability by AlgoAlpha calculates the probability of a cross-over or cross-under between the fast and slow values of a user defined Moving Average type before it happens, allowing users to benefit by front running the market.

✨ Key Features:

📊 Probability Histogram: Displays the Probability of MA cross in the form of a histogram.

🔄 Data Table: Displays forecast information for quick analysis.

🎨 Customizable MAs: Choose from various moving averages and customize their length.

🚀 How to Use:

🛠 Add Indicator: Add the indicator to favorites, and customize the settings to suite your trading style.

📊 Analyze Market: Watch the indicator to look for trend shifts early or for trend continuations.

🔔 Set Alerts: Get notified of bullish/bearish points.

✨ How It Works:

The Moving Average Cross Probability Indicator by AlgoAlpha determines the probability by looking at a probable range of values that the price can take in the next bar and finds out what percentage of those possibilities result in the user defined moving average crossing each other. This is done by first using the HMA to predict what the next price value will be, a standard deviation based range is then calculated. The range is divided by the user defined resolution and is split into multiple levels, each of these levels represent a possible value for price in the next bar. These possible predicted values are used to calculate the possible MA values for both the fast and slow MAs that may occur in the next bar and are then compared to see how many of those possible MA results end up crossing each other.

Stay ahead of the market with the Moving Average Cross Probability Indicator AlgoAlpha! 📈💡

Median Analyst ConsensusThe Median Analyst Consensus Indicator provides an unbiased, easy-to-interpret view of market sentiment by leveraging TradingView's comprehensive financial data library. This tool displays the median 12-month price target and the percentage difference from the current price directly on your charts.

Key Features

1. Accurate Market Sentiment: By consolidating analyst ratings and price targets from multiple reputable sources like Bloomberg, Refinitiv (formerly Thomson Reuters), S&P Capital IQ, and Morningstar, this indicator displays the median analyst consensus. Using the median ensures outlier ratings don't skew the overall sentiment, providing a more robust representation.

2. Simplicity at a Glance: View the median 12-month price target and percentage difference from the current price directly on your chart. No need to juggle multiple reports - key insights are surfaced within your normal trading workflow.

3. Data-Driven Transparency: If no analyst data is available for a particular asset, the indicator will not display, ensuring you only see reliable information. The number of contributing analysts is also shown for context.

Why the Median?

The median is favored over the mean to minimize the impact of outlier ratings that could distort the consensus view. By taking the middle value across all analyst projections, the median provides a more stable, outlier-resistant measure of market sentiment.

Powered by TradingView Data

This indicator taps into TradingView's financial data library, which aggregates analyst ratings, estimates, and recommendations from leading institutional data providers. TradingView sources this data from firms like FactSet, Bloomberg, Refinitiv, S&P Capital IQ, and Morningstar, ensuring a comprehensive and trusted view of analyst sentiment.

The library provides variables like:

syminfo.recommendations_buy

syminfo.recommendations_sell

syminfo.target_price_median

syminfo.recommendations_buy_strong

syminfo.recommendations_sell_strong

The indicator calculates and displays the median of these analyst inputs.

Usage

The indicator displays:

The median 12-month price target across analysts

The percentage difference between the price target and current price

The number of contributing analyst estimates

If no analyst data is available, the indicator does not display, ensuring full transparency.

The Median Analyst Consensus Indicator provides an unbiased, easy-to-interpret view of market sentiment by leveraging TradingView's comprehensive financial data library. This tool offers a new perspective on potential trade opportunities directly on your charts.

Disclaimer

While the data is sourced from reputable providers, analyst forecasts should not be construed as investment recommendations. This indicator aims to synthesize market opinions, but investment decisions are solely your responsibility. As with any analytical tool, you should conduct your own research and risk assessments before executing any trades.

Nasan Moving Average with ForecastThe "Nasan Moving Average with Forecast" indicator is a technical analysis forecasting tool that combines the principles of historical data analysis and random walk theory. It calculates a customized moving average (Nasan Moving Average) by integrating price data and statistical measures and projects future price points by generating forecast values within calculated volatility bounds, creating a dynamic and insightful visualization of potential market movements. This indicator to blend past market behavior with probabilistic future trends to enhance forecasting.

Input Parameters:

len: Differencing length (default 21, Use a minimum of 5 and for lower time frames less than 15 min use values between 300 -3000)

len1: Correction Factor Length 1 (default 21, this determines the length of the MA you want , eg. 10 MA, 50 MA, 100 MA, )

len2: Correction Factor Length 2 (default 9, this works best if it is ~ </=1/2 of len1 )

len3: Smoothing Length (default 5, I would not change this and only use if I want to introduce lag where you want to use it for cross over strategies).

forecast_points: Number of points to forecast (default 30).

m: Multiplier for standard deviation (default 2.5).

bl: Block length for calculating max/min values (default 100).

use_calculated_max_min: Boolean to decide whether to use calculated max/min values.

Nasan Moving Average Calculation:

Calculates the simple moving average (mean) and standard deviation (sd) of the typical price (hlc3).

Computes intermediate variables (a, b, c, etc.) based on log transformation and cumulative sum.

Applies weighted moving averages (wma) to these intermediate variables to smooth them and derive the final value c6.

Plots c6 as the Nasan Moving Average if the bar is confirmed. To learn more see Nasan Moving Average.

Forecast Points Calculation:

Calculates maximum (max_val) and minimum (min_val) values for the forecast, either using a fixed value or based on standard deviation and a multiplier.

Initializes an array to store forecast values and creates polyline objects for plotting.

If the current bar is one of the last three bars and confirmed:

Clears and reinitializes the polyline.

Initializes the first forecast value from the cumulative sum c.

Generates subsequent forecast values using a random value within the range .

Updates the forecast array and plots the forecast points as an orange curved polyline.

Plotting Max/Min Values:

Plots max_val and min_val as green and red lines, respectively, to indicate the bounds of the forecast range.

Components of the Forecasting Model

Historical Dependence:

Nasan Moving Average Calculation: The script calculates a custom moving average (c6) that incorporates historical price data (hlc3), standard deviations (sd), and weighted moving averages (wma). This part of the code processes historical data to create a smoothed representation of the price trend.

Max/Min Value Calculation: The maximum (max_val) and minimum (min_val) values for the forecast can be calculated based on the historical standard deviation of a transformed variable b over a block length (bl). This introduces historical volatility into the bounds for the forecast.

Random Walk Model:

Random Value Generation: Within the forecast points calculation, a random value (random_val) is generated for each forecast point within the range . This random value introduces stochasticity into the model, characteristic of a random walk process.

Cumulative Sum for Forecasting: The script uses a cumulative sum (prev_f + random_val) to generate the next forecast point (next_f). This is a typical approach in random walk models where each new point is based on the previous point plus some random noise.

Explanation of the Forecast Model

Random Walk Characteristics: Each new forecast point is generated by adding a random value to the previous point, making the model a random walk with drift, where the drift is influenced by historical correction factors (c1, c4).

Historical and Statistical Dependence: The bounds of the random values and the initial conditions are derived from historical data, ensuring that the forecast respects historical volatility and trends.

The forecasting model in the script is a hybrid approach: It uses a random walk to generate future points, characterized by adding random values to the previous forecasted value.

The historical and statistical dependence is incorporated through initial conditions, scaling factors, and bounds derived from historical price data and its statistical properties.

This combination ensures that the forecasts are not purely stochastic but are grounded in historical price behavior, making the model more robust and potentially more accurate in reflecting market conditions.

Price Reversal Probability + Price Forecast [TradeDots]The TradeDots Price Reversal Probability + Price Forecast Indicator helps traders discern market direction and identify potential trading opportunities.

📝 HOW IT WORKS

The indicator provides two types of reversal signals:

Bullish Reversal: Marked with a green label, indicating an expected upward market reversal.

Bearish Reversal: Marked with a red label, indicating an expected downward market reversal.

⭐️ Computation

This tool identifies significant reversal patterns using a mathematical model on a designated window of candlesticks to calculate price action changes. It incorporates candlestick data and price indicators, such as the Open, Close, High, Low of candlesticks and Average True Range (ATR), to detect similar occurrences in real-time.

Potential market turning points are marked with reversal labels and percentage changes , calculated using pivot high or low price data from the last reversal patterns of the opposite side.

For example, a green label on the chart indicates a bullish reversal pattern, showing the market is expected to reverse upward. However, signals are based on historical price actions and are not 100% accurate. If the price breaks down from the bullish reversal pivot low, the original signal will turn half transparent until the next reversal pattern is detected.

The algorithm groups consecutive bullish reversal patterns until a bearish reversal pattern appears. The last bullish label occurrence indicates the maximum number of bullish patterns required to confirm a reversal in the group. This information is stored to apply Bayesian statistical models and probability models to generate market insights.

⭐️ Statistical Analysis

Reversal signals are categorized into bullish and bearish groups, with each group storing consecutive reversal signals.

In the indicator table, each new reversal is labeled sequentially (e.g., "🟢 #1" for the first bullish reversal after a bearish signal). The number increases for each new signal on the same side and resets when a reversal signal on the opposite side appears.

The indicator provides two forecasts: the probability of reversal and the expected price change if the pattern is successful or unsuccessful.

⭐️ Probability of Reversal

By counting the number of consecutive reversal patterns on one side before a reversal pattern on the opposite side appears, we can calculate the probability of reversal of each signal throughout the entire price action history.

Using Bayes’ Theorem, the probability increases with each consecutive pattern. The values are displayed in the first two columns of the indicator table, with the current condition highlighted in orange.

⭐️ Price Forecast

The price forecast uses the pivot point of the last reversal pattern of the opposite side as a reference for calculating the percentage change.

For example, for a group of bullish patterns, the pivot high of the most recent bearish pattern is taken. A percentage is calculated with the pivot low of all bullish patterns in the same group. Repeating this model throughout the entire historical price action patterns gives the average price percentage difference between all bearish and bullish patterns.

Whenever a new reversal pattern is detected, a price can be forecasted using the percentage difference from the statistical model. The target price is calculated and displayed in the third and fourth columns of the indicator table.

Assisting Traders To Make Data-Informed Trading Decisions

All included features in this indicator:

Labeling of bullish and bearish reversal patterns

Success probability of each reversal pattern

Price targets of each reversal pattern

Visual aid for pattern confirmation

More (check the changelog below for current features)

🛠️ HOW TO USE

⭐️ Reversal Signals

There are two types of reversal signals identified by the algorithm that detects reversal patterns using price action analysis with candlestick data and price indicators. When the price breaks out from the labeled pivot, the label will turn half transparent.

Bullish reversal signals: Labeled in green. The number represents the price of the candlestick "low," and the percentage value indicates the price difference from the previous bearish reversal pattern's candlestick "high."

Bearish reversal signals: Labeled in red. The number represents the price of the candlestick "high," and the percentage value indicates the price difference from the previous bullish reversal pattern's candlestick "low."

⭐️ Probability Table

The probability table shows the likelihood of reversal for each number of occurrences of bullish and bearish reversal signals, displayed in the first two columns.

It also shows the target prices for both bullish and bearish conditions for each number of reversal patterns.

⭐️ Price Targets

By combining the probability of reversal and the price forecast, price targets for new reversal patterns are calculated. These insights help traders align their strategies with price action analysis and statistics by simply observing the candlestick chart in real-time.

Bullish Price Target: The average percentage price and probability that the next bearish reversal signal might hit.

Bearish Price Target: The average percentage price and probability that the next bullish reversal signal might hit.

⭐️ Market Trend Panel

The market trend panel is a small table that indicates the market trend using a 200 Exponential Moving Average (EMA) alongside reversal signals. A bullish reversal pattern above the moving average indicates a "bullish" market, while a bearish reversal pattern below it indicates a "bearish" market. If the price fluctuates around the moving average, it is identified as "choppy."

The panel also shows the risk and reward for each trade by taking the closing bullish and bearish targets from the most recent reversal pattern's price reference. Lastly, it displays the probability of reversal, consistent with the number highlighted in the probability table.

⭐️ Other Visual Aid

Other visual aids visualize the market trend and potential direction for users on the candlestick chart.

Background colors reflect the current market trend (green = bullish, red = bearish, blue = choppy).

A white plotted line represents the moving average for categorizing market trends.

❗️LIMITATIONS

Price targets represent only the mean of percentage differences. Therefore, the price could reverse before hitting either side of the price target.

When the market is in extreme price action or a new market pattern, the price targets may not be forecasted accurately and might move out of the model's range.

This model works best for assets with less price variation and a near-Gaussian distribution in returns. It may be less accurate for assets with random price movements.

CONCLUSION

This indicator uses fundamental statistics and mathematical models to generate reversal probabilities and price forecasts. It does not have the ability to predict the future with certainty. Traders should combine this indicator with other confirmation strategies to make informed investment decisions.

See Author's instructions below to get instant access to this indicator.

RISK DISCLAIMER

Trading entails substantial risk, and most day traders incur losses. All content, tools, scripts, articles, and education provided by TradeDots serve purely informational and educational purposes. Past performances are not definitive predictors of future results.

NOTES*

Calculations are based on historical data and do not guarantee future results.

Reversals exceeding ten consecutive occurrences are rare (likely <1% of total occurrences).

Users SHOULD NOT blindly follow the price targets as their trading strategy.

If you encounter a timeout with this indicator, reapply it to your chart.

LDPM Crossover Scanner AddonThe LDPM Crossover Scanner is designed to be used in conjunction with the Liquidity Dependent Price Movement Algorithm and is included with LDPM access.

The LDPM Crossover Scanner displays the LDPM status for up to 10 equity's. When conditions are bearish, per LDPM, the equity will light up on the scanner; otherwise, the equity will not light up.

When used in aggregate, this becomes a particularly useful way to measure up-coming market moves (especially when the crossover scanner showcases equities with significant beta to the chart's underlying!).

Johnny's Trend Lines, Supports and ResistancesInspired and based on ismailcarlik's Trend Lines, Supports and Resistances.

Additions include an overall upgrade to Pinescript v5, changes in the way resistance and support levels are calculated, improved visual queues, and additional customization options.

This indicator is meticulously crafted to provide traders with visual tools for identifying trend lines, support, and resistance levels, enhancing the decision-making process in trading activities.

Features and Functionality

Trend Lines: The indicator allows users to enable or disable trend lines, adjust the number of points to check for establishing a trend, and set parameters for trend validation, including the maximum violation and exceptions for the last bars.

Support and Resistance: It offers tools to identify and visualize key support and resistance levels based on recent pivot points. This includes adjustable parameters for the maximum violations allowed and the exclusion of recent bars from the analysis.

Pivot Points: Users can define the pivot length for calculating highs and lows, which helps in marking significant pivot points that are instrumental in trend analysis.

Alerts and Notifications: The indicator is equipped with customizable alerts for trend line breaches and pivot point formations, which can be set to trigger at different frequencies based on user preference.

How It Works

Input Flexibility: Users can adjust various settings like the length of trend lines and pivot points, enabling or disabling specific features like marking pivots, and managing alert settings directly from the indicator’s input panel.

Dynamic Analysis: By analyzing the price action relative to the calculated trend lines and pivot points, the indicator dynamically identifies potential trend reversals, continuations, and significant price levels.

Visualization: It plots trend lines and marks support and resistance levels directly on the chart, with options to extend these lines and add labels for better clarity. Violated trend lines can be visually differentiated by changing their style and width.

Practical Application

Trend Line Strategy: Traders can use the trend lines to determine the strength of the current market trend and to spot potential reversal points.

Support and Resistance Strategy: By marking where the price has historically faced resistance or found support, traders can plan entry and exit points, set stop-loss orders, or identify breakout opportunities.

Pivot Points Strategy: Pivot points serve as vital indicators for intraday trading or long-term trend analysis, providing insights into potential support and resistance levels.

Customization and Alerts

Custom Alerts: Traders can set alerts for when the price crosses trend lines or when new support or resistance levels are formed, helping them stay informed of critical market movements without having to continuously monitor the charts.

Visual Customization: Users can personalize the appearance of trend lines and labels, choosing from a variety of colors and styles to match their chart setup or preferences.

"Johnny's Trend Lines, Supports and Resistances" is an essential tool for traders who rely on technical analysis, offering detailed insights and real-time updates on market conditions, trend strength, and potential price barriers.

Pivot Profit Target [Mxwll]Introducing the Pivot Profit Target!

This script identifies recent pivot highs/lows and calculates the expected minimum distance for the next pivot, which acts as an approximate profit target.

The image above details the indicator's output.

The image above shows a table consisting of projection statistics.

How to use

The Pivot Profit Targets can be used to approximate a profit target for your trade.

Identify where your entry is relative to the most recent pivot, and assess whether the minimum expected distance for the most recent pivot has been exceeded. Treat the zones as an approximation.

If your trade aligns with the most recent pivot - treat the minimum expected distance zone as a potential profit target area. Of course, price might stop short or continue beyond the projection area!

That's it! Just a short and sweet script; thank you!

Edge AI Forecast [Edge Terminal]This indicator inputs the previous 150 closing prices in a simple two-layer neural network, normalizes the network inputs using a sigmoid function, uses a feedforward calculation to send it to the second layer, shows the MSE loss curve and uses both automatic and manual backpropagation (user input) to find the most likely forecast values and uses the analog forecasting algorithm to adjust and optimize the data furthermore to display potential prices on the chart.

Here's how it works:

The idea behind this script is to train a simple neural network to predict the future x values based on the sample data. For this, we use 2 types of data, Price and Volume.

The thinking behind this is that price alone can’t be used in this case because it doesn’t provide enough meaningful pattern data for the network but price and volume together can change the game. We’re planning to use more different data sets and expand on this in the future.

To avoid a bad mix of results, we technically have two neural networks, each processing a different data type, one for volume data and one for price data.

The actual prediction is decided by the way price and volume of the closing price relate to each other. Basically, the network passes the price and volume and finds the best relation between the two data set outputs and predicts where the price could be based on the upcoming volume of the latest candle.

The network adjusts the weights and biases using optimization algorithms like gradient descent to minimize the difference between the predicted and actual stock prices, typically measured by a loss function, (in this case, mean squared error) which you can see using the error rate bubble.

This is a good measure to see how well the network is performing and the idea is to adjust the settings inputs such as learning rate, epochs and data source to get the lowest possible error rate. That’s when you’re getting the most accurate prediction results.

For each data set, we use a multi-layer network. In a multi-layer neural network, the outputs of neurons in one layer serve as inputs to neurons in the next layer. Initially, the input layer of the neural network receives the historical data. Each input neuron represents a feature, such as previous stock prices and trading volumes over a specific period.

The hidden layers perform feature extraction and transformation through a series of weighted connections and activation functions. Each neuron in a hidden layer computes a weighted sum of the inputs from the previous layer, applies an activation function to the sum, and passes the result to the next layer using the feedforward (activation) function.

For extraction, we use a normalization function. This function takes a value or data (such as bar price) and divides it up by max scale which is the highest possible value of the bar. The idea is to take a normalized number, which is either below 1 or under 2 for simple use in the neural network layers.

For the activation, after computing the weighted sum, the neuron applies an activation function a(x). To introduce non-linearity into the model to pass it to the next layer. We use sigmoid activation functions in this case. The main reason we use sigmoid function is because the resulting number is between 0 to 1 and is better for models where we have to predict the probability as an output.

The final output of the network is passed as an input to the analog forecasting function. This is an algorithm commonly used in weather prediction systems. In this case, this is used to make predictions by comparing current values and assuming the patterns might repeat in the future.

There are many different ways to build an analog forecasting function but in our case, we’re used similarity measurement model:

X, as the current situation or set of current variables.

Y, as the outcome or variable of interest.

Si as the historical situations or patterns, where i ranges from 1 to n.

Vi as the vector of variables describing historical situation Si.

Oi as the outcome associated with historical situation Si.

First, we define a similarity measure sim(X,Vi) that quantifies the similarity between the current situation X and historical situation Si based on their respective variables Vi.

Then we select the K most similar historical situations (KNN Machine learning) based on the similarity measure sim(X,Vi). We denote the rest of the selected historical situations as {Si1, Si2,...Sik).

Then we examine the outcomes associated with the selected historical situations {Oi1, Oi2,...,Oik}.

Then we use the outcomes of the selected historical situations to forecast the future outcome Y^ using weighted averaging.

Finally, the output value of the analog forecasting is standardized using a standardization function which is the opposite of the normalization function. This function takes a normalized number and turns it back to its original value by multiplying it by the max scale (highest value of the bar). This function is used when the final number is produced by the network output at the end of the analog forecasting to turn the final value back into a price so it can be displayed on the chart with PineScript.

Settings:

Data source: Source of the neural network's input data.

Sample Bars: How many historical bars do you want to input into the neural network

Prediction Bars: How many bars you want the script to forecast

Show Training Rate: This shows the neural network's error rate for the optimization phase

Learning Rate: how many times you want the script to change the model in response to the estimated error (automatic)

Epochs: the network cycle or how many times you want to run the data through the network from the first layer to the last one.

Usage:

The sample bars input determines the number of historical bars to be used as a reference for the network. You need to change the Epochs and Learning Rate inputs for each asset and chart timeframe to get the lowest error rate.

On the surface, the highest possible epoch and learning rate should produce the most effective results but that's not always the case.

If the epochs rate is too high, there is a chance we face overfitting. Essentially, you might be over processing good data which can make it useless.

On the other hand, if the learning rate is too high, the network may overshoot the optimal solution and diverge. This is almost like the same issue I mentioned above with a high epoch rate.

Access:

It took over 4 months to develop this script and we’re constantly improving it so it took a lot of manpower to develop this script. Also when it comes to neural networks, Pine Script isn’t the most optimal language to build a neural network in, so we had to resort to a few proprietary mathematical formulas to ensure this runs smoothly without giving out an error for overprocessing, specially when you have multiple neural networks with many layers.

The optimization done to make this script run on Pine Script is basically state of the art and because of this, we would like to keep the code closed source at the moment.

On the other hand we don’t want to publish the code publicly as we want to keep the trading edge this script gives us in a closed loop, for our own small group of members so we have to keep the code closed. We only accept invites from expert traders who understand how this script and algo trading works and the type of edge it provides.

Additionally, at the moment we don’t want to share the code as some of the parts of this network, specifically the way we hand the data from neural network output into the analog method formula are proprietary code and we’d like to keep it that way.

You can contact us for access and if we believe this works for your trading case, we will provide you with access.

RSI AcceleratorThe Relative Strength Index (RSI) is like a fitness tracker for the underlying time series. It measures how overbought or oversold an asset is, which is kinda like saying how tired or energized it is.

When the RSI goes too high, it suggests the asset might be tired and due for a rest, so it could be a sign it's gonna drop. On the flip side, when the RSI goes too low, it's like the asset is pumped up and ready to go, so it might be a sign it's gonna bounce back up. Basically, it helps traders figure out if a stock is worn out or revved up, which can be handy for making decisions about buying or selling.

The RSI Accelerator takes the difference between a short-term RSI(5) and a longer-term RSI(14) to detect short-term movements. When the short-term RSI rises more than the long-term RSI, it typically refers to a short-term upside acceleration.

The conditions of the signals through the RSI Accelerator are as follows:

* A bullish signal is generated whenever the Accelerator surpasses -20 after having been below it.

* A bearish signal is generated whenever the Accelerator breaks 20 after having been above it.

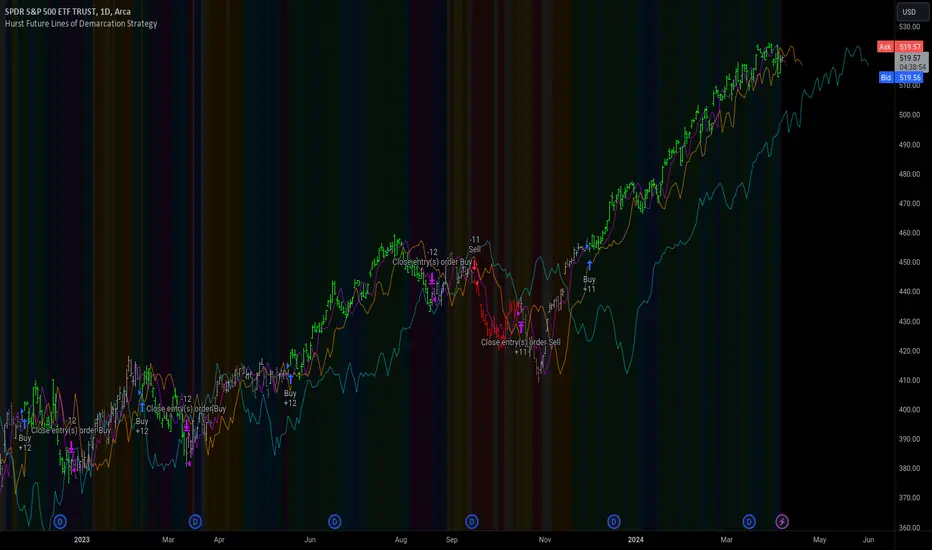

Hurst Future Lines of Demarcation StrategyJ. M. Hurst introduced a concept in technical analysis known as the Future Line of Demarcation (FLD), which serves as a forward-looking tool by incorporating a simple yet profound line into future projections on a financial chart. Specifically, the FLD is constructed by offsetting the price half a cycle ahead into the future on the time axis, relative to the Hurst Cycle of interest. For instance, in the context of a 40 Day Cycle, the FLD would be represented by shifting the current price data 20 days forward on the chart, offering an idea of future price movement anticipations.

The utility of FLDs extends into three critical areas of insight, which form the backbone of the FLD Trading Strategy:

A price crossing the FLD signifies the confirmation of either a peak or trough formation, indicating pivotal moments in price action.

Such crossings also help determine precise price targets for the upcoming peak or trough, aligned with the cycle of examination.

Additionally, the occurrence of a peak in the FLD itself signals a probable zone where the price might experience a trough, helping to anticipate of future price movements.

These insights by Hurst in his "Cycles Trading Course" during the 1970s, are instrumental for traders aiming to determine entry and exit points, and to forecast potential price movements within the market.

To use the FLD Trading Strategy, for example when focusing on the 40 Day Cycle, a trader should primarily concentrate on the interplay between three Hurst Cycles:

The 20 Day FLD (Signal) - Half the length of the Trade Cycle

The 40 Day FLD (Trade) - The Cycle you want to trade

The 80 Day FLD (Trend) - Twice the length of the Trade Cycle

Traders can gauge trend or consolidation by watching for two critical patterns:

Cascading patterns, characterized by several FLDs running parallel with a consistent separation, typically emerge during pronounced market trends, indicating strong directional momentum.

Consolidation patterns, on the other hand, occur when multiple FLDs intersect and navigate within the same price bandwidth, often reversing direction to traverse this range multiple times. This tangled scenario results in the formation of Pause Zones, areas where price momentum is likely to temporarily stall or where the emergence of a significant trend might be delayed.