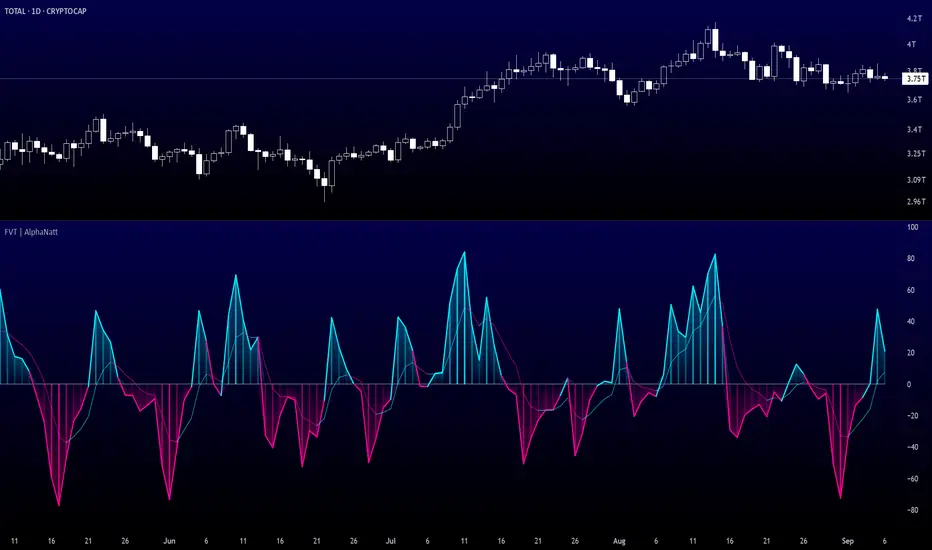

Fisher Volume Transform | AlphaNattFisher Volume Transform | AlphaNatt

A powerful oscillator that applies the Fisher Transform - converting price into a Gaussian normal distribution - while incorporating volume weighting to identify high-probability reversal points with institutional participation.

"The Fisher Transform reveals what statistics professors have known for decades: when you transform market data into a normal distribution, turning points become crystal clear."

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🎲 THE MATHEMATICS

Fisher Transform Formula:

The Fisher Transform converts any bounded dataset into a Gaussian distribution:

y = 0.5 × ln((1 + x) / (1 - x))

Where x is normalized price (-1 to 1 range)

Why This Matters:

Market extremes become statistically identifiable

Turning points are amplified and clarified

Removes the skew from price distributions

Creates nearly instantaneous signals at reversals

Volume Integration:

Unlike standard Fisher Transform, this version weights price by relative volume:

High volume moves get more weight

Low volume moves get filtered out

Identifies institutional participation

Reduces false signals from retail chop

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

💎 KEY ADVANTAGES

Statistical Edge: Transforms price into normal distribution where extremes are mathematically defined

Volume Confirmation: Only signals with volume support

Early Reversal Detection: Fisher Transform amplifies turning points

Clean Signals: Gaussian distribution reduces noise

No Lag: Mathematical transformation, not averaging

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

⚙️ SETTINGS OPTIMIZATION

Fisher Period (5-30):

5-9: Very sensitive, many signals

10: Default - balanced sensitivity

15-20: Moderate smoothing

25-30: Major reversals only

Volume Weight (0.1-1.0):

0.1-0.3: Minimal volume influence

0.5-0.7: Balanced price/volume

0.7: Default - strong volume weight

0.8-1.0: Volume dominant

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📊 TRADING SIGNALS

Primary Signals:

Zero Cross Up: Bullish momentum shift

Zero Cross Down: Bearish momentum shift

Signal Line Cross: Early reversal warning

Extreme Readings (±75): Potential reversal zones

Visual Interpretation:

Cyan zones: Bullish momentum

Magenta zones: Bearish momentum

Gradient intensity: Strength of move

Histogram: Raw momentum power

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🎯 OPTIMAL USAGE

Best Market Conditions:

Range-bound markets (reversals clear)

High volume periods

Major support/resistance levels

Divergence hunting

Trading Strategies:

1. Extreme Reversal:

Enter when oscillator exceeds ±75 and reverses

2. Zero Line Momentum:

Trade crosses of zero line with volume confirmation

3. Signal Line Strategy:

Early entry on signal line crosses

4. Divergence Trading:

Price makes new high/low but Fisher doesn't

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

Developed by AlphaNatt | Quantitative Trading Systems

Version: 1.0

Classification: Statistical Transform Oscillator

Not financial advice. Always DYOR.

M-oscillator

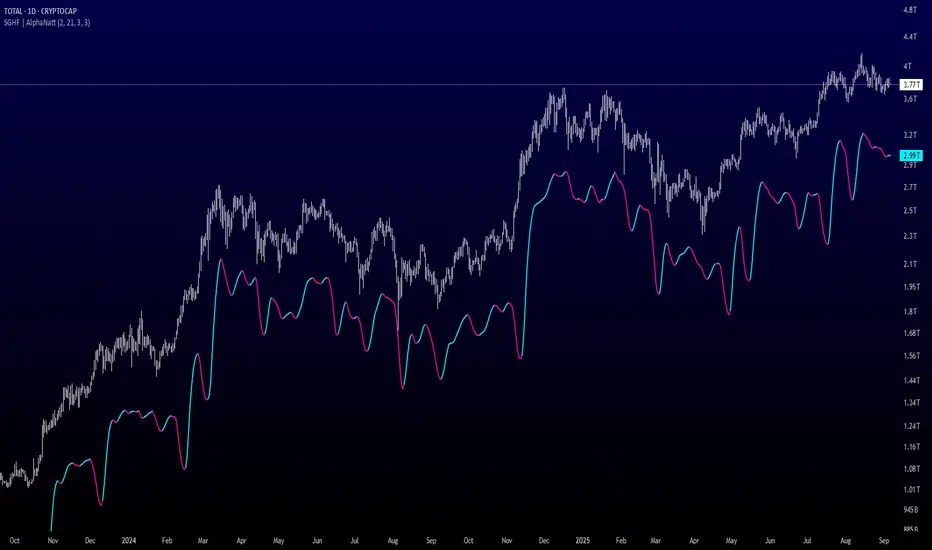

Savitzky-Golay Hampel Filter | AlphaNattSavitzky-Golay Hampel Filter | AlphaNatt

A revolutionary indicator combining NASA's satellite data processing algorithms with robust statistical outlier detection to create the most scientifically advanced trend filter available on TradingView.

"This is the same mathematics that processes signals from the Hubble Space Telescope and analyzes data from the Large Hadron Collider - now applied to financial markets."

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🚀 SCIENTIFIC PEDIGREE

Savitzky-Golay Filter Applications:

NASA: Satellite telemetry and space probe data processing

CERN: Particle physics data analysis at the LHC

Pharmaceutical: Chromatography and spectroscopy analysis

Astronomy: Processing signals from radio telescopes

Medical: ECG and EEG signal processing

Hampel Filter Usage:

Aerospace: Cleaning sensor data from aircraft and spacecraft

Manufacturing: Quality control in precision engineering

Seismology: Earthquake detection and analysis

Robotics: Sensor fusion and noise reduction

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🧬 THE MATHEMATICS

1. Savitzky-Golay Filter

The SG filter performs local polynomial regression on data points:

Fits a polynomial of degree n to a sliding window of data

Evaluates the polynomial at the center point

Preserves higher moments (peaks, valleys) unlike moving averages

Maintains derivative information for true momentum analysis

Originally published in Analytical Chemistry (1964)

Mathematical Properties:

Optimal smoothing in the least-squares sense

Preserves statistical moments up to polynomial order

Exact derivative calculation without additional lag

Superior frequency response vs traditional filters

2. Hampel Filter

A robust outlier detector based on Median Absolute Deviation (MAD):

Identifies outliers using robust statistics

Replaces spurious values with polynomial-fitted estimates

Resistant to up to 50% contaminated data

MAD is 1.4826 times more robust than standard deviation

Outlier Detection Formula:

|x - median| > k × 1.4826 × MAD

Where k is the threshold parameter (typically 3 for 99.7% confidence)

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

💎 WHY THIS IS SUPERIOR

vs Moving Averages:

Preserves peaks and valleys (critical for catching tops/bottoms)

No lag penalty for smoothness

Maintains derivative information

Polynomial fitting > simple averaging

vs Other Filters:

Outlier immunity (Hampel component)

Scientifically optimal smoothing

Preserves higher-order features

Used in billion-dollar research projects

Unique Advantages:

Feature Preservation: Maintains market structure while smoothing

Spike Immunity: Ignores false breakouts and stop hunts

Derivative Accuracy: True momentum without additional indicators

Scientific Validation: 60+ years of academic research

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

⚙️ PARAMETER OPTIMIZATION

1. Polynomial Order (2-5)

2 (Quadratic): Maximum smoothing, gentle curves

3 (Cubic): Balanced smoothing and responsiveness (recommended)

4-5 (Higher): More responsive, preserves more features

2. Window Size (7-51)

Must be odd number

Larger = smoother but more lag

Formula: 2×(desired smoothing period) + 1

Default 21 = analyzes 10 bars each side

3. Hampel Threshold (1.0-5.0)

1.0: Aggressive outlier removal (68% confidence)

2.0: Moderate outlier removal (95% confidence)

3.0: Conservative outlier removal (99.7% confidence) (default)

4.0+: Only extreme outliers removed

4. Final Smoothing (1-7)

Additional WMA smoothing after filtering

1 = No additional smoothing

3-5 = Recommended for most timeframes

7 = Ultra-smooth for position trading

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📊 TRADING STRATEGIES

Signal Recognition:

Cyan Line: Bullish trend with positive derivative

Pink Line: Bearish trend with negative derivative

Color Change: Trend reversal with polynomial confirmation

1. Trend Following Strategy

Enter when price crosses above cyan filter

Exit when filter turns pink

Use filter as dynamic stop loss

Best in trending markets

2. Mean Reversion Strategy

Enter long when price touches filter from below in uptrend

Enter short when price touches filter from above in downtrend

Exit at opposite band or filter color change

Excellent for range-bound markets

3. Derivative Strategy (Advanced)

The SG filter preserves derivative information

Acceleration = second derivative > 0

Enter on positive first derivative + positive acceleration

Exit on negative second derivative (momentum slowing)

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📈 PERFORMANCE CHARACTERISTICS

Strengths:

Outlier Immunity: Ignores stop hunts and flash crashes

Feature Preservation: Catches tops/bottoms better than MAs

Smooth Output: Reduces whipsaws significantly

Scientific Basis: Not curve-fitted or optimized to markets

Considerations:

Slight lag in extreme volatility (all filters have this)

Requires odd window sizes (mathematical requirement)

More complex than simple moving averages

Best with liquid instruments

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🔬 SCIENTIFIC BACKGROUND

Savitzky-Golay Publication:

"Smoothing and Differentiation of Data by Simplified Least Squares Procedures"

- Abraham Savitzky & Marcel Golay

- Analytical Chemistry, Vol. 36, No. 8, 1964

Hampel Filter Origin:

"Robust Statistics: The Approach Based on Influence Functions"

- Frank Hampel et al., 1986

- Princeton University Press

These techniques have been validated in thousands of scientific papers and are standard tools in:

NASA's Jet Propulsion Laboratory

European Space Agency

CERN (Large Hadron Collider)

MIT Lincoln Laboratory

Max Planck Institutes

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

💡 ADVANCED TIPS

News Trading: Lower Hampel threshold before major events to catch spikes

Scalping: Use Order=2 for maximum smoothness, Window=11 for responsiveness

Position Trading: Increase Window to 31+ for long-term trends

Combine with Volume: Strong trends need volume confirmation

Multiple Timeframes: Use daily for trend, hourly for entry

Watch the Derivative: Filter color changes when first derivative changes sign

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

⚠️ IMPORTANT NOTICES

Not financial advice - educational purposes only

Past performance does not guarantee future results

Always use proper risk management

Test settings on your specific instrument and timeframe

No indicator is perfect - part of complete trading system

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🏆 CONCLUSION

The Savitzky-Golay Hampel Filter represents the pinnacle of scientific signal processing applied to financial markets. By combining polynomial regression with robust outlier detection, traders gain access to the same mathematical tools that:

Guide spacecraft to other planets

Detect gravitational waves from black holes

Analyze particle collisions at near light-speed

Process signals from deep space

This isn't just another indicator - it's rocket science for trading .

"When NASA needs to separate signal from noise in billion-dollar missions, they use these exact algorithms. Now you can too."

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

Developed by AlphaNatt

Version: 1.0

Release: 2025

Pine Script: v6

"Where Space Technology Meets Market Analysis"

Not financial advice. Always DYOR

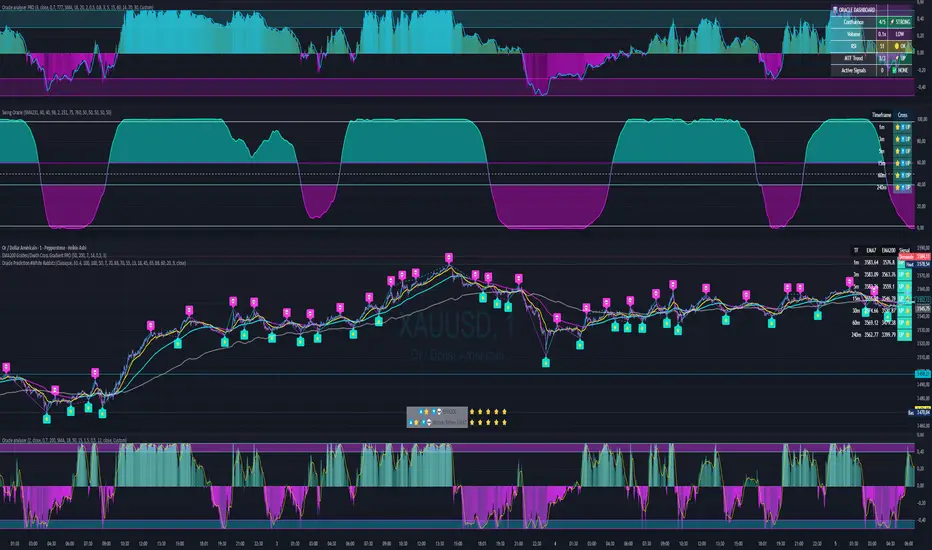

Swing Oracle Stock// (\_/)

// ( •.•)

// (")_(")

📌 Swing Oracle Stock – Professional Cycle & Trend Detection Indicator

The Swing Oracle Stock is an advanced market analysis tool designed to highlight price cycles, trend shifts, and key trading zones with precision. It combines trendline dynamics, normalized oscillators, and multi-timeframe confirmation into a single comprehensive indicator.

🔑 Key Features

NDOS (Normalized Dynamic Oscillator System):

Measures price strength relative to recent highs and lows to detect overbought, neutral, and oversold zones.

Dynamic Trendline (EMA8 or SMA231):

Flexible source selection for adapting to different trading styles (scalping vs. swing).

Multi-Timeframe H1 Confirmation:

Adds higher-timeframe validation to improve signal reliability.

Automated Buy & Sell Signals:

Triggered only on significant crossovers above/below defined levels.

Weekly Cycles (7-day M5 projection):

Tracks recurring time-based market cycles to anticipate reversal points.

Intuitive Visualization:

Colored zones (high, low, neutral) for quick market context.

Optional background and candlestick coloring for better clarity.

Multi-Timeframe Cross Table:

Automatically compares SMA50 vs. EMA200 across multiple timeframes (1m → 4h), showing clear status:

⭐️⬆️ UP = bullish trend confirmation

💀⬇️ Drop = bearish trend confirmation

📊 Built-in Statistical Tools

Normalized difference between short and long EMA.

Projected normalized mean levels plotted directly on the main chart.

Dynamic analysis of price distance from SMA50 to capture market “waves.”

🎯 Use Cases

Spot trend reversals with multi-timeframe confirmation.

Identify powerful breakout and breakdown zones.

Time entries and exits based on trend + cycle confluence.

Enhance market timing for swing trades, scalps, or long-term positions.

⚡ Swing Oracle Stock brings together cycle detection, oscillator normalization, and multi-timeframe confirmation into one streamlined indicator for traders who want a professional edge.

Momentum Index [BigBeluga]The Momentum Index is an innovative indicator designed to measure the momentum of price action by analyzing the distribution of positive and negative momentum values over a defined period. By incorporating delta-based calculations and smoothing techniques, it provides traders with a clear and actionable representation of market momentum dynamics.

🔵 Key Features:

Delta-Based Momentum Analysis:

Calculates the momentum of price by comparing its current state to its value from a defined number of bars back.

Inside a loop, it evaluates whether momentum values are above or below zero, producing a delta value that reflects the net momentum direction and intensity.

Double EMA Smoothing:

Smooths the raw delta-based momentum values with a double EMA filter, reducing noise and providing a clearer trend signal.

tmi(len) =>

sum = 0.0

sum1 = 0.0

above = 0.0

below = 0.0

src_ = src - src

for i = 0 to len

sum := sum + (src_ > nz(src_ ) ? 1 : -1)

sum1 := sum1 + (sum > 0 ? 1 : -1)

sum1 := emaEma(sum1, 10)

for i = 1 to len

above := above + (sum1 > 0 ? 1 : 0)

below := below + (sum1 > 0 ? 0 : 1)

Directional Momentum Signals:

Generates momentum shift signals and displays them on both the oscillator and the main chart:

- △ Aqua Triangles: Represent upward momentum shifts.

- ▽ Red Triangles: Represent downward momentum shifts.

Dynamic Gradient Display:

Highlights momentum zones with gradient fills:

- Aqua shades for positive momentum (above zero).

- Red shades for negative momentum (below zero).

Dashboard Display:

A dashboard summarizing the count of momentum values above and below zero for the defined period (Sentiment Length e.g. 100), helping traders assess market sentiment at a glance.

🔵 How It Works:

The indicator takes price momentum as its source and evaluates the number of momentum values above and below zero within a defined period.

The delta calculation aggregates this information, providing a net representation of the prevailing market momentum.

A double EMA filter is applied to the delta values, smoothing the momentum line and enhancing signal clarity.

Momentum shifts are highlighted with visual signals on the oscillator and price chart, while the gradient display provides a visual representation of intensity.

🔵 Use Cases:

Momentum Tracking: Identify whether market momentum is predominantly bullish or bearish.

Signal Confirmation: Use chart-based signals to confirm potential trend reversals or continuation.

Analyze Market Strength: Leverage the dashboard to quickly assess the distribution of momentum over the chosen period.

Overbought/Oversold Conditions: Utilize gradient zones to detect areas of momentum extremes and possible price exhaustion.

Momentum Index offers a refined approach to analyzing momentum dynamics, combining delta-based calculations with smoothing techniques and intuitive visuals, making it an essential tool for traders looking to anticipate market movements effectively.

Artharjan ADXArtharjan ADX (AADX) by Rrahul Desai @Artharjan

📌 Overview

The Artharjan ADX (AADX) is an advanced implementation of the Average Directional Index (ADX) with customizable moving averages, momentum thresholds, and visually intuitive grading of bullish and bearish strength.

Unlike the standard ADX indicator that only shows trend strength, AADX adds graded bullish/bearish conditions, alerts, smoothed DI signals, histogram visualizations, and background color fills to help traders quickly interpret market conditions.

It is designed for traders who want early detection of trend strength, clean visual cues, and automated alert triggers for both bullish and bearish momentum setups.

⚙️ Key Features

🔹 Customizable Calculations

DI Length (default 13) – controls sensitivity of directional indicators.

+/- DI Smoothing – smooths DI signals with user-selected MA.

Multiple Moving Average Types – SMA, EMA, WMA, RMA, VWMA, ALMA, Hull, SWMA, SMMA, TMA.

ADX Smoothing – define how smooth/fast the ADX reacts.

🔹 Flexible Display

Toggle between line plots or histogram view.

Adjustable plot thickness.

Option to plot averages of ADX, +DI, -DI for confirmation.

Configurable background fills:

ADX above/below momentum threshold.

ADX rising/falling color shading.

Trend-grade based color intensity.

🔹 Momentum & Thresholds

Momentum Level (default 25) → defines “strong trend” zone.

Crossover Threshold (default 15) → helps detect early DI crossovers.

Color-coded histogram bars for +DI vs -DI difference:

Above/below zero.

Rising/falling momentum.

🔹 Bullish & Bearish Grading System

The indicator assigns grades from 1 to 5 for both bullish and bearish setups, based on DI and ADX conditions:

Bullish Grades

Grade 1 → Very Weak Bullish

Grade 2 → Weak Bullish

Grade 3 → Moderate Bullish

Grade 4 → Strong Bullish

Grade 5 → Very Strong Bullish

Bearish Grades

Grade 1 → Very Weak Bearish

Grade 2 → Weak Bearish

Grade 3 → Moderate Bearish

Grade 4 → Strong Bearish

Grade 5 → Very Strong Bearish

Labels are automatically plotted above bars to indicate the active grade.

🔹 Alerts

Bullish Alert → when +DI crosses above its average below the threshold OR bullish conditions are met.

Bearish Alert → when -DI crosses above its average below the threshold OR bearish conditions are met.

These alerts make it possible to automate trading signals for scalping, intraday, and swing trading.

📊 Use Cases

Trend Strength Measurement

Spot when markets shift from range-bound to trending.

Confirm the reliability of breakouts with strong ADX readings.

Bullish vs Bearish Control

Compare +DI vs -DI strength to gauge trend direction.

Identify trend reversals early with DI slope changes.

Momentum Confirmation

Use ADX rising + DI grades to validate trade entries.

Filter false breakouts with weak ADX.

Trade Grading System

Enter aggressively on Grade 4–5 signals.

Stay cautious on Grade 1–2 signals.

Automated Alerts & Screening

Combine AADX alerts with strategy rules.

Build scanners to highlight strong ADX setups across multiple stocks.

🎯 Trader’s Advantage

More powerful than standard ADX → Adds slope, grading, alerts, and visualization.

Adaptable to any style → Works for intraday scalping, swing trading, and positional analysis.

Visual clarity → Color fills, histograms, and labels simplify decision-making.

Customizable smoothing → Adjusts to fast or slow markets.

✅ Closing Note

The Artharjan ADX (AADX) transforms the traditional ADX into a complete trend and momentum analyzer. It helps traders detect, confirm, and act on directional strength with clarity and confidence.

With Thanks,

Rrahul Desai

@Artharjan

High For Loop | MisinkoMasterThe High For Loop is a new Trend Following tool designed to give traders smooth and fast signals without being too complex, overfit or repainting.

It works by finding how many bars have a higher high than the current high, how many have a lower high, and scores it based on that. This provides users with easy and accurate signals, allowing for gaining a large edge in the market.

It is pretty simple but you can still play around with it pretty well and improve uppon your strategies.

For any backtests using strategies, I left many comments and tried to make it as easy as possible to backtest.

Enjoy G´s

MA-Median For Loop | MisinkoMasterThe MA-Median For Loop is a new Trend Following tool that gives the user smooth yet responsive trend signals, allowing you to see clear and accurate trends by combining the Moving Average & Median in a For Loop concept.

How does it work?

1. Select user defined inputs

=> Adjust it to your liking, everyone can set it to their liking.

2. Calculate the MA and the Median

=> Simple, but important

3. Calculate the For Loop

=> For every bar back where the median or ma of that bar is higher than the current median or ma subtract 0.5 from the trend score, and for every bar back where the current median/ma is higher than the previous one add 0.5 to the trend score.

This simple yet effective approach enhances speed, decreases noise, and produces accurate signals everyone can utilize to get an edge in the market

Enjoy G´s

Cardwell RSI by TQ📌 Cardwell RSI – Enhanced Relative Strength Index

This indicator is based on Andrew Cardwell’s RSI methodology , extending the classic RSI with tools to better identify bullish/bearish ranges and trend dynamics.

In uptrends, RSI tends to hold between 40–80 (Cardwell bullish range).

In downtrends, RSI tends to stay between 20–60 (Cardwell bearish range).

Key Features :

Standard RSI with configurable length & source

Fast (9) & Slow (45) RSI Moving Averages (toggleable)

Cardwell Core Levels (80 / 60 / 40 / 20) – enabled by default

Base Bands (70 / 50 / 30) in dotted style

Optional custom levels (up to 3)

Alerts for MA crosses and level crosses

Data Window metrics: RSI vs Fast/Slow MA differences

How to Use :

Monitor RSI behavior inside Cardwell’s bullish (40–80) and bearish (20–60) ranges

Watch RSI crossovers with Fast (9) and Slow (45) MAs to confirm momentum or trend shifts

Use levels and alerts as confluence with your trading strategy

Default Settings :

RSI Length: 14

MA Type: WMA

Fast MA: 9 (hidden by default)

Slow MA: 45 (hidden by default)

Cardwell Levels (80/60/40/20): ON

Base Bands (70/50/30): ON

Sequential Pattern Strength [QuantAlgo]🟢 Overview

The Sequential Pattern Strength indicator measures the power and sustainability of consecutive price movements by tracking unbroken sequences of up or down closes. It incorporates sequence quality assessment, price extension analysis, and automatic exhaustion detection to help traders identify when strong trends are losing momentum and approaching potential reversal or continuation points.

🟢 How It Works

The indicator's key insight lies in its sequential pattern tracking system, where pattern strength is measured by analyzing consecutive price movements and their sustainability:

if close > close

upSequence := upSequence + 1

downSequence := 0

else if close < close

downSequence := downSequence + 1

upSequence := 0

The system calculates sequence quality by measuring how "perfect" the consecutive moves are:

perfectMoves = math.max(upSequence, downSequence)

totalMoves = math.abs(bar_index - ta.valuewhen(upSequence == 1 or downSequence == 1, bar_index, 0))

sequenceQuality = totalMoves > 0 ? perfectMoves / totalMoves : 1.0

First, it tracks price extension from the sequence starting point:

priceExtension = (close - sequenceStartPrice) / sequenceStartPrice * 100

Then, pattern exhaustion is identified when sequences become overextended:

isExhausted = math.abs(currentSequence) >= maxSequence or

math.abs(priceExtension) > resetThreshold * math.abs(currentSequence)

Finally, the pattern strength combines sequence length, quality, and price movement with momentum enhancement:

patternStrength = currentSequence * sequenceQuality * (1 + math.abs(priceExtension) / 10)

enhancedSignal = patternStrength + momentum * 10

signal = ta.ema(enhancedSignal, smooth)

This creates a sequence-based momentum indicator that combines consecutive movement analysis with pattern sustainability assessment, providing traders with both directional signals and exhaustion insights for entry/exit timing.

🟢 Signal Interpretation

Positive Values (Above Zero): Sequential pattern strength indicating bullish momentum with consecutive upward price movements and sustained buying pressure = Long/Buy opportunities

Negative Values (Below Zero): Sequential pattern strength indicating bearish momentum with consecutive downward price movements and sustained selling pressure = Short/Sell opportunities

Zero Line Crosses: Pattern transitions between bullish and bearish regimes, indicating potential trend changes or momentum shifts when sequences break

Upper Threshold Zone: Area above maximum sequence threshold (2x maxSequence) indicating extremely strong bullish patterns approaching exhaustion levels

Lower Threshold Zone: Area below negative threshold (-2x maxSequence) indicating extremely strong bearish patterns approaching exhaustion levels

Top and Bottom Probability

The top and bottom probability oscillator is an educational indicator that estimates the probability of a local top or bottom using four ingredients:

price extension since the last RSI overbought/oversold,

time since that OB/OS event,

RSI divergence strength,

Directional Momentum Velocity (DMV) — a normalized, signed trend velocity.

It plots RSI, two probability histograms (Top %, Bottom %), and an optional 0–100 velocity gauge.

How to read it

RSI & Levels: Standard RSI with OB/OS lines (70/30 by default).

Prob Top (%): Red histogram, 0–100. Higher values suggest increasing risk of a local top after an RSI overbought anchor.

Prob Bottom (%): Green histogram, 0–100. Higher values suggest increasing chance of a local bottom after an RSI oversold anchor.

Velocity (0–100): Optional line. Above 50 = positive/upward DMV; below 50 = negative/downward DMV. DMV pushes Top risk when trending down and Bottom chance when trending up.

These are composite, scale-free scores, not certainties or trade signals.

What the probabilities consider

Price Delta: How far price has moved beyond the last OB (for tops) or below the last OS (for bottoms). More extension → higher probability.

Time Since OB/OS: Longer time since the anchor → higher probability (until capped by the “Time Normalization (bars)” input).

Oscillator Divergence: RSI pulling away from its last OB/OS reading in the opposite direction implies weakening momentum and increases probability.

Directional Momentum Velocity (DMV):

Computes a regression slope of hlc3 vs. bar index, normalized by ATR, then squashed with tanh.

Downward DMV boosts Top probability; upward DMV boosts Bottom probability.

Toggle the velocity plot and adjust its sensitivity with Velocity Lookback, ATR Length, and Velocity Gain.

All four terms are blended with user-set weights. If Normalize Weights is ON, weights are rescaled to sum to 1.

Inputs (most useful)

RSI Length / OB / OS: Core RSI setup.

Time Normalization (bars): Sets how quickly the “time since OB/OS” term ramps from 0→1.

Weights:

Price Delta, Time Since OB/OS, Osc Divergence, Directional Velocity.

Turn Normalize Weights ON to keep the blend consistent when you experiment.

Settings:

Velocity Lookback: Window for slope estimation (shorter = more reactive).

ATR Length: Normalizes slope so symbols/timeframes are comparable.

Velocity Gain: Steepens or softens the tanh curve (higher = punchier extremes).

Show Velocity (0–100): Toggles the DMV display.

Tip: If you prefer momentum measured on RSI rather than price, in the DMV block replace hlc3 with rsi (concept stays identical).

Practical tips

Use Top/Bottom % as context, not triggers. Combine with structure (S/R), trend filters, and risk management.

On strong trends, expect the opposite probability (e.g., Top % during an uptrend) to stay suppressed longer.

Calibrate weights: e.g., raise Osc Divergence on mean-reversion symbols; raise Velocity in trending markets.

For lower noise: lengthen Velocity Lookback and ATR Length, or reduce Velocity Gain.

Ultra Volume DetectorNative Volume — Auto Levels + Ultra Label

What it does

This indicator classifies volume bars into four categories — Low, Medium, High, and Ultra — using rolling percentile thresholds. Instead of fixed cutoffs, it adapts dynamically to recent market activity, making it useful across different symbols and timeframes. Ultra-high volume bars are highlighted with labels showing compacted values (K/M/B/T) and the appropriate unit (shares, contracts, ticks, etc.).

Core Logic

Dynamic thresholds: Calculates percentile levels (e.g., 50th, 80th, 98th) over a user-defined window of bars.

Categorization: Bars are colored by category (Low/Med/High/Ultra).

Ultra labeling: Only Ultra bars are labeled, preventing chart clutter.

Optional MA: A moving average of raw volume can be plotted for context.

Alerts: Supports both alert condition for Ultra events and dynamic alert() messages that include the actual volume value at bar close.

How to use

Adjust window size: Larger windows (e.g., 200+) provide stable thresholds; smaller windows react more quickly.

Set percentiles: Typical defaults are 50 for Medium, 80 for High, and 98 for Ultra. Lower the Ultra percentile to see more frequent signals, or raise it to isolate only extreme events.

Read chart signals:

Bar colors show the category.

Labels appear only on Ultra bars.

Alerts can be set up for automatic notification when Ultra volume occurs.

Why it’s unique

Adaptive: Uses rolling statistics, not static thresholds.

Cross-asset ready: Adjusts units automatically depending on instrument type.

Efficient visualization: Focuses labels only on the most significant events, reducing noise.

⚠️ Disclaimer: This tool is for educational and analytical purposes only. It does not provide financial advice. Always test and manage risk before trading live

PulseMA Oscillator Normalized v2█ OVERVIEW

PulseMA Oscillator Normalized v2 is a technical indicator designed for the TradingView platform, assisting traders in identifying potential trend reversal points based on price dynamics derived from moving averages. The indicator is normalized for easier interpretation across various market conditions, and its visual presentation with gradients and signals facilitates quick decision-making.

█ CONCEPTS

The core idea of the indicator is to analyze trend dynamics by calculating an oscillator based on a moving average (EMA), which is then normalized and smoothed. It provides insights into trend strength, overbought/oversold levels, and reversal signals, enhanced by gradient visualizations.

Why use it?

Identifying reversal points: The indicator detects overbought and oversold levels, generating buy/sell signals at their crossovers.

Price dynamics analysis: Based on moving averages, it measures how long the price stays above or below the EMA, incorporating trend slope.

Visual clarity: Gradients, fills, and colored lines enable quick chart analysis.

Flexibility: Configurable parameters, such as moving average lengths or normalization period, allow adaptation to various strategies and markets.

How it works?

Trend detection: Calculates a base exponential moving average (EMA with PulseMA Length) and measures how long the price stays above or below it, multiplied by the slope for the oscillator.

Normalization: The oscillator is normalized based on the minimum and maximum values over a lookback period (default 150 bars), scaling it to a range from -100 to 100: (oscillator - min) / (max - min) * 200 - 100. This ensures values are comparable across different instruments and timeframes.

Smoothing: The main line (PulseMA) is the normalized oscillator (oscillatorNorm). The PulseMA MA line is a smoothed version of PulseMA, calculated using an SMA with the PulseMA MA length. As PulseMA MA is smoothed, it reacts more slowly and can be used as a noise filter.

Signals: Generates buy signals when crossing the oversold level upward and sell signals when crossing the overbought level downward. Signals are stronger when PulseMA MA is in the overbought or oversold zone (exceeding the respective thresholds for PulseMA MA).

Visualization: Draws lines with gradients for PulseMA and PulseMA MA, levels with gradients, gradient fill to the zero line, and signals as triangles.

Alerts: Built-in alerts for buy and sell signals.

Settings and customization

PulseMA Length: Length of the base EMA (default 20).

PulseMA MA: Length of the SMA for smoothing PulseMA MA (default 20).

Normalization Lookback Period: Normalization period (default 150, minimum 10).

Overbought/Oversold Levels: Levels for the main line (default 100/-100) and thresholds for PulseMA MA, indicating zones where PulseMA MA exceeds set values (default 50/-50).

Colors and gradients: Customize colors for lines, gradients, and levels; options to enable/disable gradients and fills.

Visualizations: Show PulseMA MA, gradients for overbought/oversold/zero levels, and fills.

█ OTHER SECTIONS

Usage examples

Trend analysis: Observe PulseMA above 0 for an uptrend or below 0 for a downtrend. Use different values for PulseMA Length and PulseMA MA to gain a clearer trend picture. PulseMA MA, being smoothed, reacts more slowly and can serve as a noise filter to confirm trend direction.

Reversal signals: Look for buy triangles when PulseMA crosses the oversold level, especially when PulseMA MA is in the oversold zone. Similarly, look for sell triangles when crossing the overbought level with PulseMA MA in the overbought zone. Such confirmation increases signal reliability.

Customization: Test different values for PulseMA Length and PulseMA MA on a given instrument and timeframe to minimize false signals and tailor the indicator to market specifics.

Notes for users

Combine with other tools, such as support/resistance levels or other oscillators, for greater accuracy.

Test different settings for PulseMA Length and PulseMA MA on the chosen instrument and timeframe to find optimal values.

Commodity Channel Index DualThe CCI Dual is a custom TradingView indicator built in Pine Script v5, designed to help traders identify potential buy and sell signals using two Commodity Channel Index (CCI) oscillators. It combines a shorter-period CCI (default: 14) for quick momentum detection with a longer-period CCI (default: 50) for confirmation, focusing on mean-reversion opportunities in overbought or oversold conditions.

This setup is particularly suited for volatile markets like cryptocurrencies on higher timeframes (e.g., 3-day charts), where it highlights reversals by requiring both CCIs to cross out of extreme zones within a short window (default: 3 bars).

The indicator plots the CCIs, customizable bands (inner: 100, OB/OS: 175, outer: 200), dynamic fills for visual emphasis, background highlights for signals, and alert conditions for notifications.

How It Works

The indicator calculates two CCIs based on user-defined lengths and source (default: close price):

CCI Calculation: CCI measures price deviation from its average, using the formula: CCI = (Typical Price - Simple Moving Average) / (0.015 * Mean Deviation). The short CCI reacts faster to price changes, while the long CCI provides smoother, trend-aware confirmation.

Overbought/Oversold Levels: Customizable thresholds define extremes (Overbought at +175, Oversold at -175 by default). Bands are plotted at inner (±100), mid (±175 dashed), and outer (±200) levels, with gray fills for the outer zones.

Dynamic Fills: The longer CCI is used to shade areas beyond OB/OS levels in red (overbought) or green (oversold) for quick visual cues.

Signals:

Buy Signal: Triggers when both CCIs cross above the Oversold level (-175) within the signal window (3 bars). This suggests a potential upward reversal from an oversold state.

Sell Signal: Triggers when both cross below the Overbought level (+175) within the window, indicating a possible downward reversal.

Visuals and Alerts: Buy signals highlight the background green, sells red. Separate alertconditions allow setting TradingView alerts for buys or sells independently.

Customization: Adjust lengths, levels, and window via inputs to fit your timeframe or asset—e.g., higher OB/OS for crypto volatility.

This logic reduces noise by requiring dual confirmation, but like all oscillators, it can produce false signals in strong trends where prices stay extended.

To mitigate false signals (e.g., in trending markets), layer the CCI Dual with MACD (default: 12,26,9) and RSI (default: 14) for multi-indicator confirmation:

With MACD: Only take CCI buys if the MACD line is above the signal line (or histogram positive), confirming bullish momentum. For sells, require MACD bearish crossover. This filters counter-trend signals by aligning with trend strength—e.g., ignore CCI sells if MACD shows upward momentum.

With RSI: Confirm CCI oversold buys only if RSI is below 30 and rising (or shows bullish divergence). For overbought sells, RSI above 70 and falling. This adds overextension validation, reducing whipsaws in crypto trends.

I made this customizable for you to find what works best for your asset you are trading. I trade the 6 hour and 3 day timeframe mainly on major cryptocurrency pairs. I hope you enjoy this script and it serves you well.

ZLEMA Trend Index 2.0ZTI — ZLEMA Trend Index 2.0 (0–1000)

Overview

Price Mapped ZTI v2.0 - Enhanced Zero-Lag Trend Index.

This indicator is a significant upgrade to the original ZTI v1.0, featuring enhanced resolution from 0-100 to 0-1000 levels for dramatically improved price action accuracy. The Price Mapped ZTI uses direct price-to-level mapping to eliminate statistical noise and provide true proportional representation of market movements.

Key Innovation: Instead of statistical normalization, this version maps current price position within a user-defined lookback period directly to the ZTI scale, ensuring perfect correlation with actual price movements. I believe this is the best way to capture trends instead of directly on the charts using a plethora of indicators which introduces bad signals resulting in drawdowns. The RSI-like ZTI overbought and oversold lines filter valid trends by slicing through the current trading zone. Unlike RSI that can introduce false signals, the ZTI levels 1 to 1000 is faithfully mapped to the lowest to highest price in the current trading zone (lookback period in days) which can be changed in the settings. The ZTI line will never go off the beyond the ZTI levels in case of extreme trend continuation as the trading zone is constantly updated to reflect only the most recent bars based on lookback days.

Core Features

✅ 10x Higher Resolution - 0-1000 scale provides granular movement detection

✅ Adjustable Trading Zone - Customizable lookback period from 1-50 days

✅ Price-Proportional Mapping - Direct correlation between price position and ZTI level

✅ Zero Statistical Lag - No rolling averages or standard deviation calculations

✅ Multi-Strategy Adaptability - Single parameter adjustment for different trading styles

Trading Zone Optimization

📊 Lookback Period Strategies

Short-term (1-3 days):

Ultra-responsive to recent price action

Perfect for scalping and day trading

Tight range produces more sensitive signals

Medium-term (7-14 days):

Balanced view of recent trading range

Ideal for swing trading

Captures meaningful support/resistance levels

Long-term (21-30 days):

Broader market context

Excellent for position trading

Smooths out short-term market noise

⚡ Market Condition Adaptation

Volatile Markets: Use shorter lookback (3-5 days) for tighter ranges

Trending Markets: Use longer lookback (14-21 days) for broader context

Ranging Markets: Use medium lookback (7-10 days) for clear boundaries

🎯 Timeframe Optimization

1-minute charts: 1-2 day lookback

5-minute charts: 2-5 day lookback

Hourly charts: 7-14 day lookback

Daily charts: 21-50 day lookback

Trading Applications

Scalping Setup (2-day lookback):

Super tight range for quick reversals

ZTI 800+ = immediate short opportunity

ZTI 200- = immediate long opportunity

Swing Trading Setup (10-day lookback):

Meaningful swing levels captured

ZTI extremes = high-probability reversal zones

More stable signals, reduced whipsaws

Advanced Usage

🔧 Real-Time Adaptability

Trending days: Increase to 14+ days for broader perspective

Range-bound days: Decrease to 3 days for tighter signals

High volatility: Shorter lookback for responsiveness

Low volatility: Longer lookback to avoid false signals

💡 Multi-Timeframe Approach

Entry signals: Use 7-day ZTI on main timeframe

Trend confirmation: Use 21-day ZTI on higher timeframe

Exit timing: Use 3-day ZTI for precise exits

🌐 Session Optimization

Asian session: Shorter lookback (3-5 days) for range-bound conditions

London/NY session: Longer lookback (7-14 days) for trending conditions

How It Works

The indicator maps the current price position within the specified lookback period directly to a 0-1000 scale and plots it using ZLEMA (Zero Lag Exponential Moving Average) which has the least lag of the available popular moving averages:

Price at recent high = ZTI at 1000

Price at recent low = ZTI at 1

Price at mid-range = ZTI at 500

This creates perfect proportional representation where every price movement translates directly to corresponding ZTI movement, eliminating the false signals common in traditional oscillators.

This single, versatile indicator adapts to any market condition, timeframe, or trading style through one simple parameter adjustment, making it an essential tool for traders at every level.

Credits

ZLEMA techniques widely attributed to John Ehlers.

Disclaimer

This tool is for educational purposes only and is not financial advice. Backtest and forward‑test before live use, and always manage risk.

Please note that I set this as closed source to prevent source code cloning by others, repackaging and republishing which results in multiple confusing choices of the same indicator.

B@dshah Indicator🚀 Advanced Multi-Indicator Trading System

A comprehensive trading indicator that combines multiple technical analysis tools for high-probability signal generation:

📊 CORE FEATURES:

- EMA Trend Analysis (Fast/Slow crossovers)

- RSI Momentum Detection

- MACD Signal Confirmation

- Bollinger Bands (Squeeze & Mean Reversion)

- Fibonacci Retracement Levels

- Volume & ATR Filtering

- Multi-Confluence Scoring System (0-10 scale)

🎯 SIGNAL QUALITY:

- Non-repainting signals (confirmed at bar close)

- Minimum 60% strength threshold for trades

- Dynamic TP/SL based on market structure

- Real-time win rate tracking

- Signal strength percentage display

⚙️ UNIQUE FEATURES:

- BB Squeeze detection for volatility breakouts

- Fibonacci level confluence analysis

- Smart position sizing recommendations

- Visual TP/SL lines with outcome tracking

- Comprehensive statistics table

🔔 ALERTS INCLUDED:

- Buy/Sell signals with strength ratings

- TP/SL hit notifications

- BB squeeze/expansion alerts

- Fibonacci level touches

Best used on 1H+ timeframes for optimal results.

Perfect for swing trading and position entries.

Quad Stochastic OscillatorThis is my take on the "Quad Rotation Strategy". It's a simple but powerful indicator once you know what to look for. I combined the four different periods into one script, which makes seeing the rotation, and other cues, easier. I suggest changing the %K line to dotted or off, so it doesn't clutter the view.

Capiba RSI + Ichimoku + VolatilidadeThe "Capiba RSI + Ichimoku + Volatility" indicator is a powerful, all-in-one technical analysis tool designed to provide traders with a comprehensive view of market dynamics directly on their price chart. This multi-layered indicator combines a custom Relative Strength Index (RSI), the trend-following Custom Ichimoku Cloud, and dynamic volatility lines to help identify high-probability trading setups.

How It Works

This indicator functions by overlaying three distinct, yet complementary, analysis systems onto a single chart, offering a clear and actionable perspective on a wide range of market conditions, from strong trends to periods of consolidation.

1. Custom RSI & Momentum Signals

The core of this indicator is a refined version of the Relative Strength Index (RSI). It calculates a custom Ultimate RSI that is more sensitive to price movements, offering a quicker response to potential shifts in momentum. The indicator also plots a moving average of this RSI, allowing for the generation of clear trading signals. Use RMAs.

Bar Coloring: The color of the price bars on your chart dynamically changes to reflect the underlying RSI momentum.

Blue bars indicate overbought conditions, suggesting trend and a potential short-term reversal.

Yellow bars indicate oversold conditions, hinting at a potential bounce.

Green bars signal bullish momentum, where the Custom RSI is above both 50 and its own moving average.

Red bars indicate bearish momentum, as the Custom RSI is below both 50 and its moving average.

Trading Signals: The indicator plots visual signals directly on the chart in the form of triangles to highlight key entry and exit points. A green triangle appears when the Custom RSI crosses above its moving average (a buy signal), while a red triangle marks a bearish crossunder (a sell signal).

2. Custom Ichimoku Cloud for Trend Confirmation

This component plots a standard Ichimoku Cloud directly on the chart, providing a forward-looking view of trend direction, momentum, and dynamic support and resistance levels.

The cloud’s color serves as a strong visual cue for the prevailing trend: a green cloud indicates a bullish trend, while a red cloud signals a bearish trend.

The cloud itself acts as a dynamic support or resistance zone. For example, in an uptrend, prices are expected to hold above the cloud, which provides a strong support level for the market.

3. Dynamic Volatility Lines

This final layer is a dynamic volatility channel that automatically plots the highest high and lowest low from a user-defined period. These lines create a visual representation of the recent price range, helping traders understand the current market volatility.

Volatility Ratio: A label is displayed on the chart showing a volatility ratio, which compares the current price range to a historical average. A high ratio indicates increasing volatility, while a low ratio suggests a period of price consolidation or lateral movement, a valuable insight for day traders.

The indicator is highly customizable, allowing you to adjust parameters like RSI length, overbought/oversold levels, Ichimoku periods, and volatility lookback periods to suit your personal trading strategy. It is an ideal tool for traders who rely on a combination of momentum, trend, and volatility to make well-informed decisions.

Full Stochastic (TC2000-style EMA 5,3,3)Full Stochastic (TC2000-style EMA 5,3,3) computes a Full Stochastic oscillator matching TC2000’s settings with Average Type = Exponential.

Raw %K is calculated over K=5, then smoothed by an EMA with Slowing=3 to form the Full %K, and %D is an EMA of Full %K with D=3.

Plots:

%K in black, %D in red, with 80/20 overbought/oversold levels in green.

This setup emphasizes momentum shifts while applying EMA smoothing at both stages to reduce noise and maintain responsiveness. Inputs are adjustable to suit different symbols and timeframes.

Money Flow | Lyro RSMoney Flow | Lyro RS

The Money Flow is a momentum and volume-driven oscillator designed to highlight market strength, exhaustion, and potential reversal points. By combining smoothed Money Flow Index readings with volatility, momentum, and RVI-based logic, it offers traders a deeper perspective on money inflow/outflow, divergences, and overbought/oversold dynamics.

Key Features

Smoothed Money Flow Line

EMA-smoothed calculation of the MFI for noise reduction.

Clear thresholds for overbought and oversold zones.

Normalized Histogram

Histogram plots show bullish/bearish money flow pressure.

Color-coded cross logic for quick trend assessment.

Relative Volatility Index (RVI) Signals

Detects overbought and oversold conditions using volatility-adjusted RVI.

Plots ▲ and ▼ markers at exhaustion points.

Momentum Strength Gauge

Calculates normalized momentum strength from ROC and volume activity.

Displays percentage scale of current momentum force.

Divergence Detection

Bullish divergence: Price makes lower lows while money flow makes higher lows.

Bearish divergence: Price makes higher highs while money flow makes lower highs.

Plotted as diamond markers on the oscillator.

Signal Dashboard (Table Overlay)

Displays real-time status of Money Flow signals, volatility, and momentum.

Color-coded readouts for instant clarity (Long/Short/Neutral + Momentum Bias).

How It Works

Money Flow Calculation – Applies EMA smoothing to MFI values.

Normalization – Scales oscillator between relative high/low values.

Trend & Signals – Generates bullish/bearish signals based on midline and histogram cross logic.

RVI Integration – Confirms momentum exhaustion with overbought/oversold markers.

Divergences – Identifies hidden market imbalances between price and money flow.

Practical Use

Trend Confirmation – Use midline crossovers with histogram direction for money flow bias.

Overbought/Oversold Reversals – Watch RVI ▲/▼ markers for exhaustion setups.

Momentum Tracking – Monitor momentum percentage to gauge strength of current trend.

Divergence Alerts – Spot early reversal opportunities when money flow diverges from price action.

Customization

Adjust length, smoothing, and thresholds for different markets.

Enable/disable divergence detection as needed.

Personalize visuals and dashboard display for cleaner charts.

⚠️ Disclaimer

This indicator is a tool for technical analysis and does not provide guaranteed results. It should be used alongside other methods and proper risk management. The creator is not responsible for financial decisions made using this script.

Radial Basis Kernel RSI for LoopRadial Basis Kernel RSI for Loop

What it is

An RSI-style oscillator that uses a radial basis function (RBF) kernel to compute a similarity-weighted average of gains and losses across many lookback lengths and kernel widths (γ). By averaging dozens of RSI estimates—each built with different parameters—it aims to deliver a smoother, more robust momentum signal that adapts to changing market conditions.

How it works

The script measures up/down price changes from your chosen Source (default: close).

For each combination of RSI length and Gamma (γ) in your ranges, it builds an RSI where recent bars that look most similar (by price behavior) get more weight via an RBF kernel.

It averages all those RSIs into a single value, then smooths it with your selected Moving Average type (SMA, EMA, WMA, HMA, DEMA) and a light regression-based filter for stability.

Inputs you can tune

Min/Max RSI Kernel Length & Step: Range of RSI lookbacks to include in the ensemble (e.g., 20→40 by 1) or (e.g., 30→50 by 1).

Min/Max Gamma & Step: Controls the RBF “width.” Lower γ = broader similarity (smoother); higher γ = more selective (snappier).

Source: Price series to analyze.

Overbought / Oversold levels: Defaults 70 / 30, with a midline at 50. Shaded regions help visualize extremes.

MA Type & Period (Confluence): Final smoothing on the averaged RSI line (e.g., DEMA(44) by default).

Red “OB” labels when the line crosses down from extreme highs (~80) → potential overbought fade/exit areas.

Green “OS” labels when the line crosses up from extreme lows (~20) → potential oversold bounce/entry areas.

How to use it

Treat it like RSI, but expect fewer whipsaws thanks to the ensemble and kernel weighting.

Common approaches:

Look for crosses back inside the bands (e.g., down from >70 or up from <30).

Use the 50 midline for directional bias (above = bullish momentum tilt; below = bearish).

Combine with trend filters (e.g., your chart MA) for higher-probability signals.

Performance note: This is really heavy and depending on how much time your subscription allows you could experience this timing out. Increasing the step size is the easiest way to reduce the load time.

Works on any symbol or timeframe. Like any oscillator, best used alongside price action and risk management rather than in isolation.

Custom RVGI with Zero Lineits only traditional RVGI available in trading view and its not my own. I just adding zero line for visible comfort. I am not the creater or owner of this RVGI.

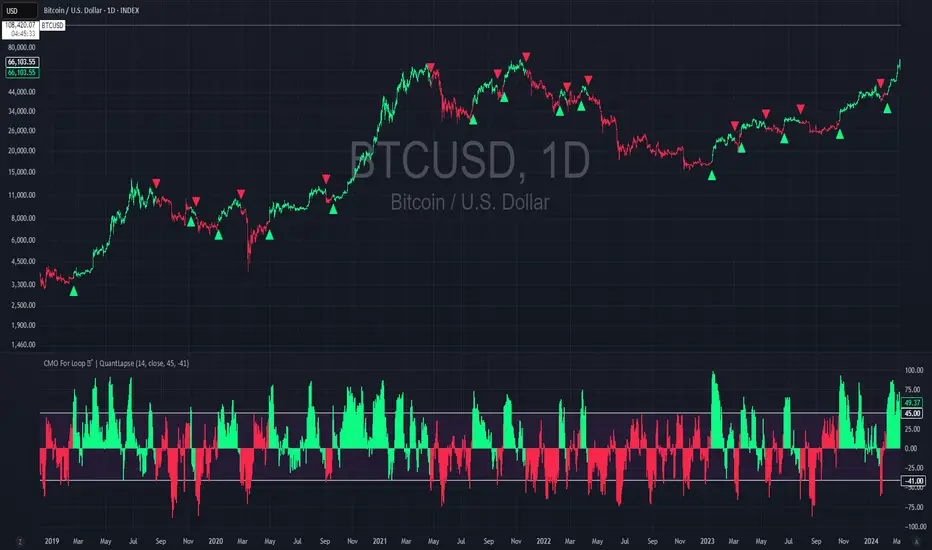

CMO For Loop | QuantLapseCMO For Loop Indicator

The CMO For Loop indicator, inspired by Alex Orekhov's, "Chande Momentum Oscillator," and indicator originally made by Tushar Chande, the CMO designed as a fast and responsive tool to capture quick price movements in financial markets. This oscillator leverages Momentum to measure price deviations, providing a concise yet powerful framework for identifying potential trade entry and exit points. What makes this

"enhanced" CMO indicator special is its ability to identify trending periods more accurately. By using thresholds, this allows the script to enter accurate long and short conditions extremely quickly.

Intended Uses:

Used to capture long-term trends:

Used to identify quick reversals:

Recommended Uses

Best suited for higher timeframes (8H+) to improve accuracy of signals.

Designed for strategies that require fast entries and exits.

Can also be applied to scalping approaches.

Not Recommended For

Should not be used as a mean reversion tool.

Should not be interpreted as a valuation indicator (overbought/oversold levels).

Key Features

Rapid Market Reaction

Built to prioritize speed over smoothing, making it ideal for traders who want to take advantage of quick price shifts in trending or highly volatile markets.

Flexible Thresholds

Users can customize the upper and lower CMO levels to trigger long or short conditions, allowing the indicator to adapt to different assets and trading styles.

Embracing the Noise

Signals may appear frequently, but this is intentional. The tool is optimized for traders who thrive on fast rotations, using the “noise” to catch short-lived yet impactful moves.

Clear Visual Feedback

Plots key oscillator levels and provides dynamic, color-coded candles and shapes that make it easy to identify bias and react quickly.

How It Works

Oscillator Calculation

The CMO (Chande Momentum Oscillator) is derived from comparing the source price’s deviations relative to its momentum. This approach emphasizes trend-driven price shifts.

Signal Triggers

When the oscillator rises above the upper threshold, a long bias is triggered and remains until the CMO drops below the lower threshold.

When the oscillator falls below the lower threshold, a short bias is triggered and remains until the CMO crosses back above the upper threshold.

No bias is active when the oscillator is between thresholds.

Visual Signals

Green candles = long bias

Red candles = short bias

Gray candles = neutral/no signal

Triangles mark points of change in signal direction.

Confluence StackPlease read the instructions below. The code was mostly written using AI so may contain errors. Happy trading all and good luck. ATB Richard

INTENDED USE

This indicator is designed for technical traders who want to move beyond simple buy/sell signals and gain a deeper understanding of the underlying market dynamics. It is ideal for trend followers, swing traders, and anyone looking to confirm the quality of a trend.

WHO IS THIS FOR?

Traders who want to differentiate between strong, sustainable trends and weak, unreliable moves.

Analysts looking to identify high-conviction setups backed by multiple factors (e.g., momentum confirmed by volume).

Discretionary traders who need a quick, visual tool to gauge market sentiment and avoid choppy conditions.

WHY USE IT?

Traditional indicators often give conflicting signals. The Confluence Stack solves this by aggregating multiple perspectives into one clear visual. It helps you answer not just "Is the market going up?" but "WHY is it going up, and how strong is the conviction?". This allows for more informed decision-making and helps filter out low-probability trades.

DISCLAIMER AND LICENSE

This script is for educational purposes only and is not a recommendation to buy or sell any financial instrument. All trading and investment decisions are the sole responsibility of the user. Trading involves significant risk.

This source code is subject to the terms of the Mozilla Public License 2.0 at www.mozilla.org

HOW TO USE THIS INDICATOR

This indicator is designed to show the 'character' of a market move by grouping signals into distinct categories. Instead of seeing many individual signals, you see the strength of the underlying forces driving the price.

1. READ THE HEIGHT (Strength of Confluence)

The total height of the stack shows the strength of agreement. A tall stack means many signals are aligned, indicating a high-conviction move. A short stack means weak agreement and a choppy, indecisive market.

2. READ THE COLOR (Character of the Move)

The colors tell you WHY the market is moving.

BLUE (Momentum): A stack of mostly blue shades indicates a trend driven by pure momentum. This is the 'speed' of the market.

RSI (Relative Strength Index): Measures the magnitude of recent price gains versus losses. A smooth measure of trend strength.

Stochastic Oscillator: Measures the current closing price's position within the recent high-low range. More sensitive to immediate price action.

CCI (Commodity Channel Index): Measures the price's deviation from its moving average. Excels at identifying cyclical turns.

MACD (Moving Average Convergence Divergence): A trend-following momentum indicator showing the relationship between two moving averages. Excellent for identifying the start and end of trends.

YELLOW (Volume): The appearance of yellow shades confirms the move is supported by high market participation. This is the 'fuel' for the trend.

Volume Ratio: A custom signal that triggers when buy or sell volume is unusually high compared to its recent average.

CRV (Candle Range Volume): A custom signal that looks for candles with significant price range and volume.

OBV (On-Balance Volume): A cumulative indicator that adds volume on up days and subtracts it on down days. It shows the long-term flow of money.

FUCHSIA (Volatility): A fuchsia block signals a volatility breakout. This adds a sense of urgency and confirms the price is moving with exceptional force.

Bollinger Bands: A signal triggers when the price closes outside of the upper or lower standard deviation bands.

ORANGE (Price Action): An orange block is a pure price structure signal. It's a raw statement of intent from the market.

Price Gap: A signal that triggers when there's a gap up or gap down between candles.

3. READ THE TRANSITION (Shift in Sentiment)

The most important signal from the stacks is the flip from one side of the zero line to the other.

Flipping from Negative to Positive: A bearish stack disappears and is replaced by a bullish stack. This indicates market sentiment is shifting from bearish to bullish.

Flipping from Positive to Negative: A bullish stack disappears and is replaced by a bearish stack. This warns of a potential top or the start of a new downtrend.

4. FILTER FOR NOISE (Plot Threshold)

In choppy markets, the stack can flicker with low signal counts (e.g., +1 or -1). To focus only on high-conviction moves, go to the indicator settings and increase the "Plot Threshold". A setting of 2 or 3 will hide all stacks that don't have at least 2 or 3 agreeing signals, effectively filtering out market noise and keeping your chart clean.

5. CUSTOMIZE YOUR SIGNALS (Enable/Disable)

This indicator is fully customizable. In the settings, you can enable or disable each of the 9 indicators individually. For example, if you are a pure momentum trader, you could disable all Volume, Volatility, and Price Action signals to focus only on the blue stacks. Tailor it to fit your specific trading style.

EXAMPLE INTERPRETATIONS

Strong, Confirmed Trend: A tall stack of mostly blue (Momentum) and yellow (Volume) indicates a high-quality trend backed by both speed and market participation.

Momentum-Only Trend: A tall stack of only blue is a strong momentum move, but the lack of yellow (Volume) is a warning that the move may lack the "fuel" to be sustained.

Choppy/Indecisive Market: A short, mixed-color stack flickering around the zero line means the market is choppy with no clear conviction. It's often best to stay out.

Volatility Breakout: A new stack that appears suddenly with a fuchsia (Bollinger Bands) block on its first bar suggests a volatility-driven breakout is initiating.

Exhaustion Move: An orange (Price Gap) block appearing at the peak of a tall, long-standing stack can signal an exhaustion gap, potentially marking the end of the trend.

Weakening Conviction (Divergence): If price makes a new high but the positive stack is visibly shorter than the stack at the previous price high, it suggests underlying conviction is weakening.