AI & Machine Learning Models in Market Prediction1. Overview of AI and Machine Learning in Finance

1.1 Artificial Intelligence in Finance

AI refers to computer systems designed to perform tasks that normally require human intelligence. In finance, AI can perform tasks like risk assessment, fraud detection, sentiment analysis, and predictive modeling. Its ability to simulate human-like decision-making is particularly valuable in trading, where speed, accuracy, and adaptability are crucial.

1.2 Machine Learning as a Subset of AI

Machine Learning is a subset of AI that focuses on algorithms that learn from data. Unlike traditional statistical methods, ML models improve their predictive accuracy as they are exposed to more data. ML can be categorized into:

Supervised Learning: The model learns from labeled historical data to predict future outcomes (e.g., stock prices).

Unsupervised Learning: The model identifies hidden patterns in unlabeled data (e.g., market clustering, anomaly detection).

Reinforcement Learning: The model learns by trial and error to maximize rewards, often used in algorithmic trading.

2. Types of Machine Learning Models Used in Market Prediction

2.1 Regression Models

Regression analysis predicts continuous outcomes, such as stock prices, interest rates, or commodity values. Common models include:

Linear Regression: Models the relationship between a dependent variable and one or more independent variables.

Ridge and Lasso Regression: Improve linear regression by adding regularization to prevent overfitting.

Polynomial Regression: Captures non-linear relationships in market data.

2.2 Classification Models

Classification models are used when outcomes are categorical, such as predicting whether a stock will go up or down. Examples include:

Logistic Regression

Support Vector Machines (SVM)

Random Forests

Gradient Boosting Machines

2.3 Time Series Models

Financial data is inherently sequential. Time series models exploit temporal dependencies to forecast future trends:

ARIMA (Auto-Regressive Integrated Moving Average)

SARIMA (Seasonal ARIMA)

Prophet (by Facebook)

LSTM (Long Short-Term Memory networks): A type of neural network ideal for capturing long-term dependencies in sequential data.

2.4 Deep Learning Models

Deep learning involves multi-layer neural networks capable of modeling complex, non-linear relationships in market data:

Convolutional Neural Networks (CNNs): Typically used for image recognition but applied to visualized market data like candlestick charts.

Recurrent Neural Networks (RNNs): Designed for sequential data, with LSTM and GRU as advanced versions.

Transformers: Advanced models that handle large datasets and multiple features, increasingly used in financial forecasting.

2.5 Reinforcement Learning

Reinforcement Learning (RL) models are particularly popular in algorithmic trading. In RL:

The agent (trading algorithm) interacts with an environment (market).

It receives feedback (reward or penalty) based on its actions.

Over time, it learns strategies to maximize cumulative rewards.

Applications include high-frequency trading, portfolio optimization, and dynamic hedging strategies.

3. Data Sources for AI Market Prediction

AI models require large and diverse datasets. Key sources include:

Historical Market Data: Prices, volumes, and volatility indices.

Economic Indicators: GDP, inflation, employment rates.

Company Fundamentals: Financial statements, earnings reports, and debt levels.

Alternative Data: Social media sentiment, news articles, Google Trends, satellite imagery.

High-Frequency Data: Tick-by-tick data used in HFT algorithms.

Data quality is critical: noisy, incomplete, or biased data can significantly reduce model accuracy.

4. Features and Variables in Market Prediction

Feature engineering transforms raw data into meaningful input variables. Common features include:

Technical Indicators: Moving averages, RSI, MACD, Bollinger Bands.

Sentiment Scores: Derived from social media or news sentiment analysis.

Macroeconomic Variables: Interest rates, commodity prices, geopolitical events.

Market Microstructure: Order book depth, bid-ask spreads, and trade volume.

Feature selection helps reduce dimensionality, improve computation efficiency, and avoid overfitting.

5. Advantages of AI and ML in Market Prediction

Speed and Efficiency: Can analyze millions of data points in seconds.

Pattern Recognition: Detects complex non-linear patterns invisible to human analysts.

Adaptability: Models can adjust to new market conditions.

Risk Management: Improves predictive accuracy, helping mitigate losses.

Automation: Enables algorithmic trading and continuous market monitoring.

6. Challenges and Limitations

Data Quality and Availability: Poor or biased data reduces model effectiveness.

Overfitting: Models may perform well on historical data but fail in real-time markets.

Market Unpredictability: Black swan events and irrational market behavior are difficult to model.

Interpretability: Complex models like deep neural networks are often “black boxes.”

Regulatory Compliance: Financial regulations may restrict the use of certain AI models.

7. Case Studies and Applications

7.1 Stock Price Prediction

Companies use LSTM networks and hybrid models combining technical indicators and sentiment analysis to forecast stock movements. Some hedge funds leverage AI for short-term price predictions.

7.2 Algorithmic and High-Frequency Trading

AI-driven HFT systems execute thousands of trades per second using reinforcement learning and predictive analytics to exploit market inefficiencies.

7.3 Portfolio Optimization

AI models can rebalance portfolios dynamically, considering risk, expected returns, and correlations between assets, often outperforming traditional mean-variance optimization.

7.4 Risk Assessment and Fraud Detection

Machine learning models assess credit risk, detect unusual trading patterns, and flag potential fraud in real-time.

8. Future Trends

Explainable AI (XAI): Increasing demand for transparent models that can explain decisions to regulators and investors.

Integration with Alternative Data: Enhanced predictive power through social media, news sentiment, and satellite imagery.

Quantum Computing: Potential to accelerate complex computations and improve prediction accuracy.

AI-Driven Macroeconomic Forecasting: Integration of global economic, political, and environmental data for holistic market prediction.

Conclusion

AI and Machine Learning have transformed financial market prediction, offering unprecedented speed, accuracy, and adaptability. By leveraging historical and real-time data, these technologies can identify complex patterns, optimize trading strategies, and improve risk management. However, challenges such as data quality, overfitting, interpretability, and market unpredictability remain.

As AI continues to evolve, combining explainable models, alternative data, and advanced computational techniques will redefine the future of market analysis, making financial decision-making more informed and strategic.

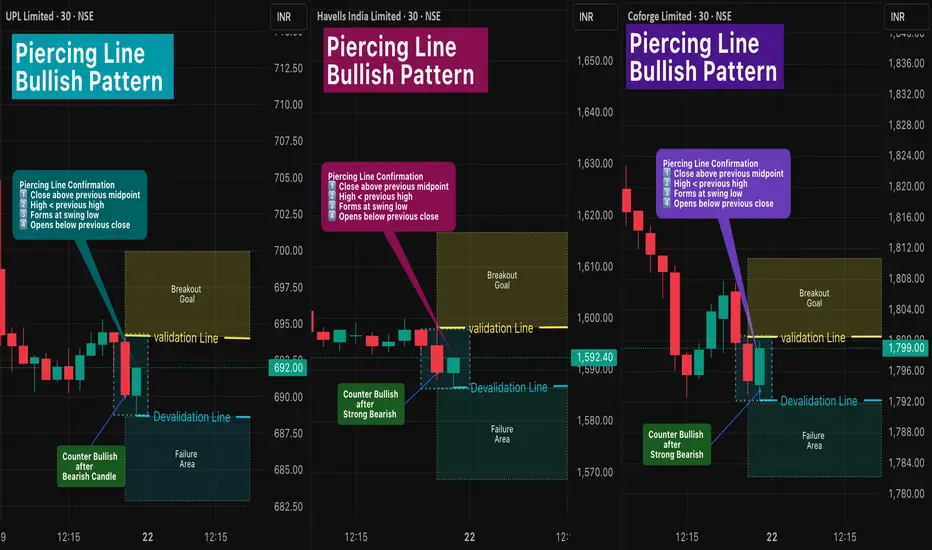

Chart Patterns

Piercing Line Bullish Pattern 🔎 Intro / Overview

The Piercing Line Pattern is a two-candle bullish reversal setup that forms after a downtrend.

- Sellers lose control → Buyers step in strongly.

- Entry and exit are rule-based using Validation and Devalidation lines to restrict false signals.

- Stop-loss is based on swing low, and Target is 1R (equal to risk distance).

This setup can be applied across any symbols and any timeframe (Just make sure it is after Downtrend or at Swing Low).

📊 Example symbols in this idea:

NSE:UPL · NSE:HAVELLS · NSE:COFORGE

___________________________________________________________

📌 How to Use

✅ Piercing Line Pattern – Confirmation Rules

1️⃣ Close Above Midpoint → The second candle must close above the midpoint of the first bearish candle.

2️⃣ Lower High Condition → The second candle’s high should be lower than the previous candle’s high, showing controlled recovery rather than immediate breakout.

3️⃣ Swing Low Context → The pattern forms after a swing low or decline, signaling potential reversal from bearish to bullish.

4️⃣ Gap/Open Condition → The second candle should open below the prior candle’s close, reflecting initial selling pressure before buyers take over.

When Pattern Confirm - Entry Rules -

📌 Validation → Close above the Pattern High .

📌 Devalidation → Close below Swing Low before validation.

When all conditions align, the Piercing Line confirms a bullish reversal opportunity.

__________________________________

🎯 Trading Plan

- Entry → Candle closes above the Validation line (Pattern high).

- Failure → If candle closes below Devalidation line before validation.

- Stoploss → Swing Low.

- Target → Equal to stoploss distance (1R).

___________________________________________________________

📊 Chart Explanation

All Patterns shown in 30-min timeframe :

1️⃣ NSE:UPL (UPL Limited)

- Entry @ 694.20 → Breakout Goal confirmed only on candle close above this level.

- Devalidation Level: If price closes below 688.70 , the Pattern shifts to the Failure Area.

2️⃣ NSE:HAVELLS (Havells India Limited)

- Entry @ 1598.20 → Breakout Goal confirmed only on candle close above this level.

- Devalidation Level: If price closes below 1586.50 , the Pattern shifts to the Failure Area.

3️⃣ NSE:COFORGE (Coforge Limited)

- Entry @ 1800.50 → Breakout Goal confirmed only on candle close above this level.

- Devalidation Level: If price closes below 1792.10 , the Pattern shifts to the Failure Area. .

📊 All three Patterns are live and active in the same timeframe.

___________________________________________________________

👀 Observation

- Piercing Line is most effective near swing lows after a clear downtrend.

- Strict validation/devalidation rules help avoid false entries.

- Works well across multiple symbols when conditions align.

___________________________________________________________

❗ Why It Matters?

- Defines entries and exits clearly with rule-based validation.

- Provides a structured framework to trade reversals confidently.

___________________________________________________________

🎯 Conclusion

The Piercing Line Pattern is a disciplined bullish reversal signal.

By combining Validation and Devalidation Rules, traders gain clarity and protection against false trades.

🔥 Patterns don’t predict. Rules protect. 🚀

___________________________________________________________

⚠️ Disclaimer

📘 For educational purposes only.

🙅 Not SEBI registered.

❌ Not a buy/sell recommendation.

🧠 Purely a learning resource.

📊 Not Financial Advice.

Part 1 Master Candlestick PatternIntroduction

Options trading has always attracted traders and investors because of its flexibility, leverage, and the ability to profit in both rising and falling markets. Unlike simple stock buying, where you purchase shares and wait for them to rise, options allow you to speculate, hedge, or even create income-generating strategies. But this flexibility comes at a cost: risk.

In fact, while options provide opportunities for huge rewards, they also carry risks that can wipe out capital quickly if not managed properly. Many new traders get lured by the promise of quick profits and ignore the hidden dangers. The truth is, every option trade is a balance between potential gain and potential loss — and understanding the nature of these risks is the first step to trading responsibly.

In this guide, we’ll explore all major types of risk in options trading — from market risk and time decay to volatility traps, liquidity issues, and even psychological mistakes.

1. Market Risk – The Most Obvious Enemy

Market risk is the possibility of losing money due to unfavorable price movements in the underlying asset. Since options derive their value from stocks, indices, currencies, or commodities, any sharp move against your position can create losses.

For call buyers: If the stock fails to rise above the strike price plus premium, you lose money.

For put buyers: If the stock doesn’t fall below the strike price minus premium, the option expires worthless.

For sellers (writers): The risk is even greater. A short call can lead to unlimited losses if the stock keeps rising, and a short put can cause heavy losses if the stock collapses.

👉 Example:

Suppose you buy a call option on Reliance Industries with a strike price of ₹3,000 at a premium of ₹50. If the stock stays around ₹2,950 at expiry, your entire premium (₹50 per share) is lost. Conversely, if you had sold that same call, and the stock shot up to ₹3,300, you’d lose ₹250 per share — far more than the premium you collected.

Lesson: Market risk is unavoidable. Every trade needs a pre-defined exit plan.

2. Leverage Risk – The Double-Edged Sword

Options provide huge leverage. You control a large notional value of stock by paying a small premium. But this magnifies both profits and losses.

A 5% move in the stock could mean a 50% change in the option’s premium.

A trader who overuses leverage can blow up their capital in just a few trades.

👉 Example:

With just ₹10,000, you buy out-of-the-money (OTM) Bank Nifty weekly options. If the market moves in your favor, you might double your money in a day. But if it goes the other way, you could lose everything — and very fast.

Lesson: Leverage is powerful, but without discipline, it’s deadly.

3. Time Decay Risk – The Silent Killer (Theta Risk)

Options are wasting assets. Every day that passes reduces their time value, especially as expiry nears. This is called Theta decay.

Option buyers suffer from time decay. Even if the stock doesn’t move, the option premium keeps falling.

Option sellers benefit from time decay, but only if the market stays within their expected range.

👉 Example:

You buy an at-the-money (ATM) Nifty option one week before expiry at ₹100. Even if Nifty stays flat, that option could drop to ₹40 by expiry simply because of time decay.

Lesson: If you are an option buyer, timing is everything. If you are a seller, time decay works in your favor, but risk still exists from sudden moves.

4. Volatility Risk – The Invisible Factor (Vega Risk)

Volatility is the heartbeat of options pricing. Higher volatility means higher premiums because there’s a greater chance of large price moves. But this creates Vega risk.

If you buy options during high volatility (like before elections, results, or big events), you may pay inflated premiums. Once the event passes and volatility drops, the option’s value can collapse, even if the stock moves as expected.

Sellers face the opposite problem. Selling options in low volatility periods is dangerous because any sudden jump in volatility can cause premiums to spike, leading to losses.

👉 Example:

Before Union Budget announcements, Nifty options trade at very high premiums. If you buy expecting a big move, but the budget turns out uneventful, volatility drops sharply, and the option loses value instantly.

Lesson: Never ignore implied volatility (IV) before entering an option trade.

Divergence Secrets1. Understanding Options: The Foundation

Options are derivative instruments that derive their value from an underlying asset, such as stocks, indices, commodities, or currencies. They grant the buyer the right—but not the obligation—to buy or sell the underlying asset at a predetermined price within a specified period. There are two primary types of options:

Call Option: Provides the right to buy the underlying asset at a specified price (strike price) before or at expiration.

Put Option: Provides the right to sell the underlying asset at a specified price before or at expiration.

Key Terms:

Strike Price: The price at which the underlying asset can be bought or sold.

Expiration Date: The date on which the option contract expires.

Premium: The cost paid by the buyer to acquire the option.

In-the-Money (ITM): When exercising the option is profitable.

Out-of-the-Money (OTM): When exercising the option is not profitable.

Options provide leverage, enabling traders to control large positions with a relatively small capital outlay, creating unique opportunities for profit in both bullish and bearish markets.

2. Market Opportunities in Options Trading

Options trading opportunities are vast, ranging from directional plays to hedging strategies. The unique characteristics of options allow market participants to exploit price volatility, market inefficiencies, and changing investor sentiment.

2.1. Directional Opportunities

Traders can use options to profit from price movements in underlying assets:

Bullish Outlook: Buying call options allows traders to benefit from rising stock prices with limited risk.

Bearish Outlook: Buying put options provides an opportunity to profit from falling prices without short-selling.

Example: If a stock trading at ₹1,500 is expected to rise to ₹1,650 in two months, a trader could buy a call option with a strike price of ₹1,520. The profit potential is theoretically unlimited, while the maximum loss is limited to the premium paid.

2.2. Hedging Opportunities

Options provide risk mitigation for portfolios, protecting against adverse price movements:

Protective Puts: Investors holding stocks can buy put options to hedge against potential declines.

Covered Calls: Investors owning shares can sell call options to generate income, reducing portfolio volatility.

Example: An investor holding 100 shares of a stock priced at ₹2,000 may buy a put option at a ₹1,950 strike price. If the stock falls to ₹1,800, losses in the stock are offset by gains in the put option.

2.3. Income Generation

Options can be used to generate consistent income through premium collection:

Cash-Secured Puts: Selling put options on stocks an investor wants to acquire can generate premium income.

Covered Call Writing: Selling call options on held stock can earn income while potentially selling the stock at a target price.

2.4. Volatility-Based Opportunities

Options prices are highly sensitive to implied volatility, creating opportunities even when the market direction is uncertain:

Long Straddles: Buying both call and put options at the same strike price allows traders to profit from significant price swings, irrespective of direction.

Long Strangles: Similar to straddles but with different strike prices, strangles are cost-effective strategies for volatile markets.

Part 2 Support and Resistance1. How Option Pricing Works

Option pricing is determined primarily by two components:

1.1 Intrinsic Value

The intrinsic value of an option is the difference between the current market price of the underlying asset and the option’s strike price:

For a call option: Intrinsic Value = Max(0, Current Price – Strike Price)

For a put option: Intrinsic Value = Max(0, Strike Price – Current Price)

1.2 Time Value

The time value accounts for the possibility that the option’s price may increase before expiration. Factors influencing time value include:

Time to Expiry: Longer durations increase the likelihood of profitable movement.

Volatility: Higher volatility increases the potential for price swings, making options more expensive.

Interest Rates and Dividends: These factors can adjust the expected returns of the underlying asset and, consequently, the option premium.

1.3 The Black-Scholes Model

The Black-Scholes model is a widely used formula for estimating theoretical option prices. It considers factors like:

Current stock price

Strike price

Time to expiration

Volatility

Risk-free interest rate

This model forms the foundation of modern option pricing, though practical trading often considers market sentiment and liquidity as well.

2. Types of Option Styles

Options come in several styles, each dictating when the option can be exercised:

American Options: Can be exercised any time before expiration.

European Options: Can only be exercised on the expiration date.

Exotic Options: Include complex derivatives such as barrier options, Asian options, and lookback options, often used by institutional investors.

3. Uses of Options

Option trading serves multiple purposes in financial markets:

3.1 Hedging

Investors use options to protect their portfolios from adverse price movements:

Protective Put: Buying a put option to insure a long stock position.

Covered Call: Selling a call option on a stock already owned to earn additional premium income.

3.2 Speculation

Traders can use options to profit from anticipated price movements without owning the underlying asset:

Buying call options for bullish expectations.

Buying put options for bearish expectations.

Using leverage, a small investment can yield substantial returns if predictions are correct.

3.3 Income Generation

Selling options allows traders to collect premiums regularly:

Cash-Secured Puts: Selling put options while holding enough cash to buy the underlying asset if exercised.

Covered Calls: Generates income by selling calls against owned stock.

3.4 Arbitrage

Institutional traders use options to exploit price discrepancies between markets, combining options and underlying assets for risk-free profits.

Leveraged & Margin Trading1. Understanding Margin and Leverage

1.1. Margin Trading

Margin trading is a practice where traders borrow funds from a broker to trade financial instruments beyond the capital they own. Essentially, the trader puts up a portion of the trade’s value as a “margin,” while the broker provides the remainder.

Initial Margin: The amount a trader must deposit to open a position.

Maintenance Margin: The minimum account balance required to keep the position open. Falling below this can trigger a margin call.

Example:

If an investor wants to buy $10,000 worth of stock but only has $2,000, they can borrow the remaining $8,000 from the broker. Here, $2,000 is the initial margin.

2. How Margin Trading Works

2.1. Opening a Margin Account

Margin trading requires a margin account with a brokerage. Unlike a standard cash account:

Brokers assess creditworthiness and risk tolerance.

Regulatory bodies often impose minimum equity requirements.

Margin accounts allow borrowing for long and short positions.

2.2. Margin Call and Liquidation

A margin call occurs when the trader’s equity falls below the maintenance margin. Brokers demand additional funds or liquidate positions to cover losses.

Example:

Initial equity: $5,000

Maintenance margin: 25%

Position value drops, equity falls below $1,250 → margin call issued.

2.3. Interest and Costs

Borrowing funds incurs interest. Traders must account for:

Daily or monthly interest rates on borrowed funds.

Fees for overnight or extended positions.

Potential hidden costs in leveraged ETFs or derivatives.

3. Types of Leverage and Margin Instruments

3.1. Equity Margin Trading

Allows buying more shares than one can afford.

Popular in stock markets like the NYSE, NSE, and NASDAQ.

Often subject to regulatory limits, e.g., max 2x leverage for retail investors.

3.2. Forex Leverage

Forex brokers often provide high leverage (50:1 to 500:1) due to low volatility per pip.

Extremely high risk due to rapid market movements.

Margin is expressed as a percentage (e.g., 2% margin = 50x leverage).

3.3. Derivatives and Futures

Futures contracts inherently involve leverage.

Traders only deposit a fraction of the contract value as margin.

Profit/loss calculated daily (“mark-to-market”).

3.4. CFD (Contract for Difference) Trading

CFDs let traders speculate on asset price movements without owning the asset.

Leverage is widely used, amplifying gains and losses.

4. Benefits of Leveraged & Margin Trading

Amplified Returns: Small price movements can generate substantial profits.

Capital Efficiency: Traders can deploy limited capital across multiple positions.

Hedging Opportunities: Use leverage to hedge existing portfolios.

Short-Selling: Margin accounts enable profiting from falling markets.

Access to Advanced Markets: Leverage allows participation in markets with high nominal value (commodities, derivatives).

5. Risks and Challenges

5.1. Magnified Losses

Leverage increases exposure to adverse price movements.

Small losses can quickly exceed initial capital, leading to debt.

5.2. Margin Calls and Forced Liquidation

Margin calls can trigger automatic liquidation at unfavorable prices.

Timing and liquidity are critical to avoid catastrophic losses.

5.3. Interest and Fees

Borrowing costs reduce net gains.

Long-term leveraged positions can become expensive.

5.4. Psychological Pressure

High leverage induces stress, emotional trading, and overconfidence.

Traders may exit positions prematurely or double down recklessly.

6. Strategies in Leveraged & Margin Trading

6.1. Trend Following

Use leverage to maximize profits in strong trending markets.

Combine technical analysis, moving averages, and momentum indicators.

6.2. Scalping and Intraday Trading

Small positions with tight stop-losses reduce exposure.

High-frequency trades magnified through margin can yield substantial intraday gains.

6.3. Hedging and Portfolio Protection

Leveraged instruments hedge existing investments.

Options and futures contracts allow downside protection.

6.4. Swing Trading

Capture medium-term price swings.

Leverage allows traders to scale positions while maintaining capital efficiency.

7. Risk Management in Leveraged Trading

7.1. Setting Stop-Loss Orders

Essential to limit downside.

Automated stop-losses prevent emotional decision-making.

7.2. Position Sizing

Calculate leverage based on volatility and account size.

Avoid risking more than a small percentage of total capital per trade.

7.3. Diversification

Spread exposure across multiple assets.

Reduces risk of catastrophic losses from a single position.

7.4. Monitoring Margin Levels

Keep track of maintenance margin requirements.

Avoid last-minute margin calls by maintaining buffer equity.

8. Regulatory and Ethical Considerations

Regulators impose limits on retail leverage to protect investors.

Brokers must disclose risks clearly.

Leveraged trading carries ethical responsibility—reckless use can lead to systemic market instability.

9. Practical Examples

9.1. Stock Margin Trade

Buy 500 shares at $50 each = $25,000

Own capital: $5,000

Borrowed: $20,000 (5:1 leverage)

Scenario A: Price rises 10% → $27,500 value

Profit = $2,500 → 50% return on own capital

Scenario B: Price falls 10% → $22,500 value

Loss = $2,500 → 50% loss on own capital, risk of margin call

9.2. Forex Leverage

EUR/USD position: $100,000

Own capital: $2,000 → 50:1 leverage

100 pips movement → profit/loss = $1,000 (50% of equity)

9.3. Futures Contracts

Oil futures: 1 contract = 1,000 barrels, $80/barrel → $80,000

Margin: 10% → $8,000 deposit

Price increase to $85 → $5,000 profit → 62.5% return on margin

10. Psychological Aspects

Leverage magnifies emotions: greed, fear, and overconfidence.

Discipline is crucial—traders must stick to pre-defined risk strategies.

Education and simulation trading can build confidence before risking real capital.

11. Leveraged ETFs

Exchange-Traded Funds designed to multiply returns of an underlying index.

Examples: 2x or 3x daily returns of S&P 500.

Ideal for short-term strategies; long-term holding can lead to compounding decay.

12. Leveraged Trading in Crypto Markets

Cryptocurrency exchanges offer extreme leverage (up to 100x).

High volatility makes margin calls frequent.

Traders must combine technical analysis, position sizing, and stop-losses rigorously.

13. Common Misconceptions

Leverage guarantees profit: False—losses are amplified too.

Higher leverage = better returns: False—risk management is more important than high leverage.

Margin trading is only for experts: False—but education is crucial.

14. Best Practices

Always calculate maximum potential loss before opening positions.

Use leverage conservatively, especially in volatile markets.

Diversify trades across assets and strategies.

Keep an emergency equity buffer to avoid forced liquidation.

Continuously review and adjust risk exposure.

15. Conclusion

Leveraged and margin trading are potent tools in modern financial markets. They provide opportunities to magnify returns, access sophisticated trading strategies, and enhance portfolio efficiency. However, they come with inherent risks: magnified losses, margin calls, psychological stress, and the potential for total capital erosion.

Success in leveraged trading depends on education, risk management, discipline, and strategic execution. Understanding the mechanics of margin accounts, leverage ratios, and market dynamics is essential. When used prudently, leverage can be a powerful ally; when mismanaged, it can become a trader’s downfall.

In essence, leveraged and margin trading are not merely about borrowing money—they are about amplifying strategic thinking, market insights, and disciplined execution. Traders who respect both the power and the peril of leverage are often those who succeed in the long run.

Geopolitical Risks and Their Impact on Global MarketsIntroduction

Geopolitical risks encompass a broad spectrum of political, economic, and military events that can disrupt the global economic landscape. These risks, ranging from armed conflicts and trade wars to policy shifts and regime changes, have profound implications for financial markets, investment strategies, and economic stability. Understanding the nature of these risks and their potential impacts is crucial for investors, policymakers, and businesses operating in an increasingly interconnected world.

1. Nature and Sources of Geopolitical Risks

Geopolitical risks arise from various sources, each with unique characteristics and potential consequences:

Armed Conflicts and Wars: Military engagements, such as the ongoing Russia-Ukraine conflict, can lead to significant disruptions in global supply chains, especially in energy and commodities markets. For instance, attacks on critical infrastructure can cause immediate price spikes and long-term supply shortages.

Trade Wars and Sanctions: Economic measures like tariffs, export controls, and sanctions can alter trade flows and affect the profitability of multinational corporations. The U.S.-China trade tensions are a prime example, influencing global supply chains and market sentiments.

Political Instability and Regime Changes: Shifts in political power, especially in key economies, can lead to policy uncertainties that affect investor confidence and market stability. Changes in leadership can result in abrupt policy shifts, impacting sectors such as energy, finance, and technology.

Cybersecurity Threats: Increasing reliance on digital infrastructure makes economies vulnerable to cyberattacks, which can disrupt financial systems, trade, and national security.

Environmental and Resource Conflicts: Competition for scarce resources, exacerbated by climate change, can lead to geopolitical tensions, particularly in regions dependent on natural resources.

2. Mechanisms of Market Impact

Geopolitical events influence markets through several channels:

Market Volatility: Uncertainty surrounding geopolitical events can lead to increased volatility in stock and bond markets. Investors often react swiftly to news, leading to sharp price movements.

Commodity Price Fluctuations: Conflicts in resource-rich regions can disrupt supply chains, leading to price increases in commodities like oil, gas, and metals. For example, tensions in the Middle East often result in spikes in oil prices due to concerns over supply disruptions.

Currency Instability: Geopolitical risks can affect investor confidence in a country's currency, leading to depreciation or volatility. Countries directly involved in conflicts may see their currencies weaken due to capital outflows.

Capital Flows and Investment Patterns: Heightened risks can lead to shifts in investment strategies, with investors seeking safe-haven assets like gold, government bonds, or stable currencies. Emerging markets may experience capital outflows as investors seek safer investments.

Supply Chain Disruptions: Conflicts and trade restrictions can interrupt the flow of goods and services, leading to shortages and increased costs for businesses and consumers.

3. Case Studies of Geopolitical Events and Market Reactions

Russia-Ukraine Conflict: The invasion of Ukraine by Russia in 2022 led to significant disruptions in global energy markets. Sanctions imposed on Russia resulted in soaring oil and gas prices, affecting global inflation rates and energy security.

U.S.-China Trade War: The imposition of tariffs between the U.S. and China in 2018-2019 disrupted global supply chains, affecting industries from electronics to agriculture. Markets experienced heightened volatility as investors adjusted to the changing trade landscape.

Brexit: The United Kingdom's decision to leave the European Union introduced uncertainties regarding trade agreements, regulatory standards, and economic relations, leading to fluctuations in the British pound and stock market volatility.

Middle East Tensions: Periodic conflicts and tensions in the Middle East, particularly involving Iran, have led to spikes in oil prices due to concerns over supply disruptions, impacting global markets.

4. Quantifying Geopolitical Risk

Measuring geopolitical risk is challenging due to its multifaceted nature. However, several indices and models have been developed to assess and quantify these risks:

Geopolitical Risk Index (GPR): Developed by Caldara and Iacoviello (2022), this index quantifies geopolitical tensions based on news coverage and policy uncertainty. It provides a historical perspective on the frequency and intensity of geopolitical events.

BlackRock Geopolitical Risk Indicator (BGRI): This indicator tracks market attention to geopolitical risks by analyzing brokerage reports and financial news stories. It helps investors gauge the level of concern in the market regarding specific geopolitical events.

Market-Driven Scenarios (MDS): Employed by institutions like BlackRock, MDS frameworks estimate the potential impact of geopolitical events on global assets by analyzing historical parallels and expert insights.

5. Investor Strategies in the Face of Geopolitical Risks

Investors can adopt several strategies to mitigate the impact of geopolitical risks:

Diversification: Spreading investments across various asset classes, sectors, and geographies can reduce exposure to specific geopolitical events.

Hedging: Utilizing financial instruments like options, futures, and currency swaps can help protect portfolios from adverse market movements.

Focus on Fundamentals: Investing in companies with strong fundamentals, such as robust balance sheets and resilient business models, can provide stability during turbulent times.

Monitoring Geopolitical Developments: Staying informed about global events and understanding their potential implications can help investors make timely and informed decisions.

Scenario Planning: Developing and regularly updating risk scenarios can prepare investors for potential geopolitical shocks and guide strategic responses.

6. Implications for Policymakers and Businesses

Policymakers and businesses must recognize the significance of geopolitical risks and take proactive measures:

Policy Formulation: Governments should develop policies that enhance economic resilience, promote diversification, and reduce dependence on volatile regions.

Crisis Management Plans: Establishing frameworks to respond to geopolitical crises can help mitigate their impact on national security and economic stability.

Public-Private Collaboration: Cooperation between governments and businesses can lead to more effective risk management strategies and resource allocation during crises.

Investment in Technology and Infrastructure: Strengthening digital infrastructure and cybersecurity can reduce vulnerabilities to cyber threats and enhance economic resilience.

Conclusion

Geopolitical risks are an inherent aspect of the global economic landscape, with the potential to influence markets, investment strategies, and economic policies. While these risks cannot be entirely eliminated, understanding their sources, mechanisms, and potential impacts allows investors, businesses, and policymakers to develop strategies to mitigate their effects. By adopting proactive risk management approaches and staying informed about global developments, stakeholders can navigate the complexities of geopolitical risks and maintain stability in an interconnected world.

Futures & Hedging Techniques1. Understanding Futures Contracts

1.1 Definition and Basics

A futures contract is a standardized agreement between two parties to buy or sell an underlying asset at a predetermined price on a specific future date. Futures are traded on regulated exchanges and cover a wide range of assets, including commodities (oil, gold, wheat), financial instruments (bonds, stock indices), and currencies.

Key characteristics:

Standardization: Contract size, expiration date, and quality of the underlying asset are predefined.

Leverage: Futures allow traders to control a large position with a relatively small margin, magnifying both gains and losses.

Obligation: Unlike options, both parties are obligated to fulfill the contract unless it is closed before expiration.

1.2 Types of Futures Contracts

Futures contracts can be broadly classified into:

Commodity Futures: Contracts for physical goods like crude oil, natural gas, metals, or agricultural products.

Financial Futures: Contracts based on financial instruments such as stock indices (e.g., S&P 500), government bonds, or currencies.

Currency Futures: Agreements to exchange a specific amount of one currency for another at a future date.

Interest Rate Futures: Contracts based on the future level of interest rates, often used to hedge bond positions.

2. The Concept of Hedging

2.1 What is Hedging?

Hedging is a risk management strategy used to offset potential losses in an investment by taking an opposite position in a related asset. It acts as a financial "insurance policy," protecting against price volatility.

Example:

A wheat farmer expects to harvest 10,000 bushels in three months. To protect against a price drop, he sells wheat futures. If prices fall, gains from the futures contract offset losses in the cash market.

2.2 Hedging vs. Speculation

Hedgers: Aim to reduce risk and protect profit margins.

Speculators: Take on risk to profit from price movements.

Hedgers use futures primarily, while speculators are attracted to leverage and profit potential.

3. Hedging Techniques

3.1 Long Hedge

A long hedge is used when an investor or business anticipates purchasing an asset in the future and wants to protect against price increases. It involves buying futures contracts.

Example:

An airline company expects to buy jet fuel in three months. To hedge against rising fuel prices, it buys fuel futures. If fuel prices increase, gains from the futures offset higher cash market costs.

3.2 Short Hedge

A short hedge is applied when the investor or business owns the asset and wants protection against price declines. It involves selling futures contracts.

Example:

A farmer expecting to sell corn in six months may sell corn futures. If market prices drop, gains from futures contracts compensate for lower cash sales prices.

3.3 Cross Hedging

Cross hedging occurs when the exact underlying asset is not available for hedging, so a related asset's futures contract is used. This method carries basis risk, as the hedge may not perfectly offset price changes.

Example:

A steel manufacturer might use iron ore futures to hedge against steel price fluctuations when no steel futures are available.

3.4 Rolling Hedges

Futures contracts have expiration dates. To maintain continuous hedging, traders roll over contracts from a near-month to a later-month contract, locking in protection over a longer horizon.

4. Advanced Hedging Strategies

4.1 Delta Hedging

Primarily used in options trading, delta hedging involves adjusting positions to remain neutral against price movements of the underlying asset. Though complex, it can minimize directional risk.

4.2 Ratio Hedging

This involves using a proportionate number of futures contracts to hedge a position. Over-hedging or under-hedging can be applied based on risk appetite.

4.3 Hedging with Options on Futures

Options provide asymmetric protection:

Buying put options hedges against price declines.

Buying call options hedges against price increases.

This approach limits losses while retaining upside potential.

5. Real-World Applications of Futures and Hedging

5.1 Commodities

Agriculture: Farmers hedge crops to lock in prices and stabilize income.

Energy: Airlines and utilities hedge oil, gas, and electricity prices to manage operational costs.

Metals: Industrial manufacturers hedge metals like copper and aluminum to control production expenses.

5.2 Financial Markets

Equities: Portfolio managers hedge against market downturns using index futures.

Interest Rates: Banks hedge bond portfolios against interest rate fluctuations using Treasury futures.

Currency Exposure: Multinational companies hedge foreign currency transactions to mitigate exchange rate risk.

5.3 Corporate Finance

Corporations employ hedging to:

Protect profit margins.

Secure predictable cash flows.

Reduce volatility in earnings reports.

6. Advantages and Limitations

6.1 Advantages

Risk Management: Reduces exposure to adverse price movements.

Liquidity: Futures markets are highly liquid.

Price Discovery: Transparent pricing aids decision-making.

Standardization: Contracts are uniform and regulated.

6.2 Limitations

Basis Risk: Imperfect hedging can leave residual risk.

Margin Calls: Leverage can lead to unexpected losses.

Market Volatility: Extreme events may cause margin strain.

Complexity: Advanced hedging requires financial expertise.

7. Practical Tips for Effective Hedging

Identify Exposures: Determine what risks need hedging—commodity prices, interest rates, currencies.

Choose the Right Instrument: Use futures, options, or combinations to optimize coverage.

Calculate Hedge Ratios: Apply statistical methods for precision.

Monitor Positions: Markets are dynamic; regular evaluation is critical.

Understand Costs: Consider transaction costs, margin requirements, and potential losses.

8. Case Studies

Case Study 1: Airline Fuel Hedge

A major airline facing volatile fuel prices purchased crude oil futures. When prices surged 12% in three months, the gains from futures offset the higher fuel costs, stabilizing operational expenses.

Case Study 2: Wheat Farmer

A farmer expecting to sell wheat in 90 days sold futures contracts. Prices fell by 8%, but the futures gain neutralized losses, ensuring predictable revenue.

Case Study 3: Multinational Corporation

A tech firm receiving payments in euros hedged using currency futures. Adverse EUR/USD fluctuations could have reduced earnings, but gains from futures mitigated the impact.

9. Emerging Trends in Futures and Hedging

Algorithmic Hedging: AI and quantitative models optimize hedge ratios in real-time.

ESG Hedging: Companies hedge exposure to carbon credits or renewable energy costs.

Cryptocurrency Futures: Digital assets now offer hedging tools for crypto portfolios.

Globalization: Increasing cross-border trade creates diverse hedging needs in multiple currencies and commodities.

10. Conclusion

Futures and hedging techniques are indispensable tools in modern finance. They allow market participants to manage risk, protect profits, and plan for uncertainties. While futures provide standardized, leveraged instruments for price speculation and risk management, hedging techniques enable businesses and investors to achieve stability amid market volatility.

Mastering these concepts requires a combination of theoretical knowledge, practical experience, and an understanding of market behavior. With careful planning, risk assessment, and strategy execution, futures and hedging can transform uncertainty into a manageable, predictable component of financial decision-making.

High-Frequency Trading (HFT)1. The Evolution of Trading Technology

1.1 From Manual to Electronic Trading

Before HFT, financial markets relied primarily on human traders, floor brokers, and telephonic transactions. Orders were manually placed, reviewed, and executed—a process that was time-consuming and prone to errors.

The 1980s and 1990s witnessed a revolution in trading technology with the emergence of electronic trading platforms. Nasdaq became one of the first fully electronic markets, offering automated order execution, real-time price quotes, and faster transaction speeds. This shift laid the groundwork for algorithmic trading and, eventually, HFT.

1.2 Algorithmic Trading

Algorithmic trading refers to using pre-programmed instructions to execute trades based on market data. Algorithms can react to price movements, volumes, and news faster than any human. HFT is essentially an extreme form of algorithmic trading where execution speed is the primary advantage.

2. Core Characteristics of High-Frequency Trading

HFT differs from conventional trading in several key aspects:

2.1 Ultra-Low Latency

Latency is the time delay between market data reception and order execution. HFT firms invest heavily in technology to reduce latency to microseconds. They co-locate their servers near exchange data centers to gain nanoseconds in execution speed.

2.2 Massive Order Volumes

HFT strategies often involve placing thousands to millions of orders daily. Most orders are canceled within fractions of a second, a practice called “order-to-trade ratio management.”

2.3 Short Holding Periods

HFT trades rarely hold positions longer than a few seconds. Some strategies may close trades in milliseconds. Profits rely on exploiting tiny price discrepancies that exist only briefly.

2.4 Reliance on Market Data

HFT depends on real-time market data, including order books, trade histories, and economic news. Algorithms analyze this data continuously to identify patterns and opportunities invisible to human traders.

3. High-Frequency Trading Strategies

HFT strategies can be broadly categorized based on their objectives and techniques.

3.1 Market Making

Market-making HFT firms provide liquidity by continuously quoting bid and ask prices. They profit from the bid-ask spread, earning small but frequent gains on each trade. Their activity reduces price volatility and enhances market efficiency.

3.2 Statistical Arbitrage

Statistical arbitrage involves exploiting price inefficiencies across related assets. For instance, HFT algorithms may detect mispricings between futures and underlying stocks, executing trades that profit when the discrepancy corrects.

3.3 Event-Driven Strategies

Event-driven HFT reacts to news events, economic data releases, or corporate announcements. Algorithms scan news feeds and social media in real time, executing trades within microseconds of market-moving information.

3.4 Momentum Ignition

Some HFT strategies attempt to trigger rapid price movements by placing a series of orders designed to provoke reactions from other traders. This technique is controversial and often falls under regulatory scrutiny.

3.5 Latency Arbitrage

Latency arbitrage exploits time differences in price reporting between different exchanges. Firms can buy an asset on one exchange and sell it milliseconds later on another where the price has not yet adjusted.

4. Technological Infrastructure

HFT requires cutting-edge technology. Firms invest millions in the following areas:

4.1 Hardware

Ultra-Fast Servers: HFT firms use servers with high processing power to minimize computation time.

FPGAs (Field-Programmable Gate Arrays): Custom hardware accelerates data processing, reducing latency.

High-Speed Networking: Direct fiber-optic lines and microwave communication are employed to reduce transmission time between exchanges.

4.2 Software

Low-Latency Algorithms: Optimized to execute in microseconds.

Real-Time Analytics: Processes incoming market data instantly to make trade decisions.

Risk Management Systems: Monitor exposures, automatically adjusting or canceling orders to prevent significant losses.

4.3 Co-Location

Many exchanges offer co-location services, allowing HFT servers to be physically close to exchange servers. Proximity can reduce latency by fractions of a millisecond, which is crucial in a speed-sensitive environment.

5. Market Impact

5.1 Liquidity Enhancement

HFT provides liquidity by constantly placing buy and sell orders, reducing spreads and improving market depth. This allows other market participants to execute trades more efficiently.

5.2 Price Discovery

HFT accelerates the incorporation of new information into asset prices. By rapidly reacting to market signals, HFT helps markets reflect underlying values more accurately.

5.3 Volatility Concerns

Critics argue that HFT can exacerbate market volatility. During periods of market stress, algorithms may simultaneously withdraw liquidity, leading to flash crashes or sudden price swings.

5.4 Unequal Playing Field

HFT firms enjoy advantages unavailable to retail traders, including co-location, proprietary data feeds, and ultra-fast hardware. Critics contend that this undermines market fairness.

6. Regulation of High-Frequency Trading

Global regulators have increasingly focused on HFT due to its complexity and potential risks. Key regulatory measures include:

6.1 Market Surveillance

Exchanges and regulators monitor HFT activity to detect manipulative practices, such as quote stuffing (placing excessive orders to slow down competitors) and spoofing (placing orders with no intent to execute).

6.2 Minimum Resting Times

Some markets have introduced minimum order resting times, requiring orders to remain on the book for a short period to reduce excessive cancellations.

6.3 Trade Reporting and Transparency

Regulators require HFT firms to provide detailed trade reporting, ensuring oversight and traceability of rapid trading activity.

7. Advantages and Criticisms

7.1 Advantages

Increased Liquidity: HFT enhances market efficiency by providing continuous buy and sell orders.

Lower Spreads: Narrow bid-ask spreads benefit all market participants.

Efficient Price Discovery: Speeds up reflection of information in market prices.

Innovation in Trading Technology: Drives advancements in software and hardware.

7.2 Criticisms

Market Manipulation Risk: Certain strategies can manipulate prices temporarily.

Systemic Risk: Highly automated systems can exacerbate crashes.

Unequal Access: Retail traders cannot compete on speed or technology.

Short-Term Focus: HFT focuses on minuscule, fleeting opportunities rather than long-term value creation.

8. Case Studies and Notable Events

8.1 The Flash Crash of 2010

On May 6, 2010, U.S. stock markets experienced a sudden, dramatic drop, with the Dow Jones falling nearly 1,000 points in minutes. HFT algorithms amplified the crash by rapidly selling and withdrawing liquidity, illustrating the risks of ultra-fast trading.

8.2 HFT in Global Markets

HFT is not limited to U.S. exchanges. European and Asian markets have also witnessed significant HFT activity, with local regulations adapting to manage associated risks. In some regions, HFT has contributed positively to liquidity and price efficiency, demonstrating the dual nature of its impact.

9. The Future of High-Frequency Trading

9.1 Technological Advancements

HFT will continue to evolve with innovations such as quantum computing, AI-driven predictive analytics, and next-generation networking technologies. These may further reduce latency and enhance decision-making.

9.2 Regulation and Ethical Considerations

Regulators will likely impose stricter rules to prevent systemic risk and maintain fairness. The industry may need to balance speed-driven profits with broader market stability.

9.3 Integration with Other Trading Forms

HFT may increasingly interact with other forms of algorithmic trading, including options, futures, and cryptocurrency markets, creating complex, interconnected trading ecosystems.

Conclusion

High-Frequency Trading represents a pinnacle of technological integration into financial markets. It has reshaped the landscape, providing liquidity, speeding up price discovery, and introducing new risks. While it benefits markets in terms of efficiency and narrower spreads, it also raises concerns about fairness, volatility, and systemic risk. Understanding HFT requires recognizing its dual nature: a tool of innovation and speed that must be managed carefully to prevent unintended consequences.

As global markets become more interconnected, HFT will remain a critical area of study for traders, regulators, and technologists alike. Its future will be defined by the interplay between technological innovation, market dynamics, and regulatory oversight.

Part 8 Trading Master Class1. Introduction to Option Trading

Financial markets are constantly evolving, offering traders and investors a wide variety of tools to manage risk, speculate on price movements, or generate income. One of the most fascinating and versatile financial instruments is the option.

Unlike buying a share of a company directly, which gives you ownership, an option gives you rights, not obligations. This small distinction makes options powerful. They can amplify profits, reduce risks, and allow traders to play multiple angles of the market.

Option trading might sound complicated at first, but once you understand the foundation, it’s like learning a new language – everything starts connecting.

2. The Basics: What Are Options?

An option is a contract between two parties – a buyer and a seller – that gives the buyer the right, but not the obligation, to buy or sell an underlying asset at a predetermined price within a set time frame.

The underlying asset could be a stock, an index, a commodity (like gold or crude oil), or even currencies.

The predetermined price is called the strike price.

The time frame is defined by the expiry date.

In simple words:

Options are like a reservation ticket. You pay a small amount now (premium) to lock in the ability to buy/sell later, but you don’t have to use it if you don’t want to.

3. Types of Options: Call and Put

There are two main types:

Call Option: Gives the buyer the right to buy the underlying asset at the strike price.

Example: You buy a call option for Reliance at ₹2500. If Reliance goes to ₹2700, you can still buy it at ₹2500, making profit.

Put Option: Gives the buyer the right to sell the underlying asset at the strike price.

Example: You buy a put option for Infosys at ₹1500. If Infosys falls to ₹1300, you can still sell it at ₹1500.

Think of calls as a bet on prices going up, and puts as a bet on prices going down.

4. Key Terminologies in Options

To understand option trading, you must master its unique vocabulary:

Strike Price: The pre-agreed price at which you can buy/sell the underlying.

Expiry Date: The date on which the option contract expires.

Premium: The price you pay to buy the option.

In-the-Money (ITM): Option has intrinsic value. (E.g., stock is above strike for calls, below strike for puts).

Out-of-the-Money (OTM): Option has no intrinsic value.

At-the-Money (ATM): Stock price and strike price are nearly the same.

Option Writer: The seller of the option, who takes the opposite side.

Lot Size: The minimum quantity you can trade in an option contract.

Part 7 Trading Master Class1. Introduction to Options Trading

Options trading is one of the most versatile and complex areas of financial markets. It offers traders and investors the ability to hedge, speculate, or generate income. Unlike stocks, which represent ownership in a company, options are financial contracts giving the buyer the right, but not the obligation, to buy or sell an underlying asset at a predetermined price within a specified time frame.

Options are derivatives, meaning their value derives from an underlying asset such as equities, indices, commodities, or currencies. They are widely used by institutional traders, retail investors, and hedgers to manage risk and leverage positions efficiently.

2. Types of Options

There are two primary types of options:

Call Options

Gives the holder the right to buy an underlying asset at a specified price (strike price) before or on the expiry date.

Used by traders who expect the price of the asset to rise.

Put Options

Gives the holder the right to sell an underlying asset at a specified price before or on expiry.

Used by traders who expect the price of the asset to fall.

Key Terms in Options Trading

Strike Price (Exercise Price): The predetermined price at which the asset can be bought or sold.

Expiry Date: The date by which the option must be exercised.

Premium: The cost of buying the option.

Intrinsic Value: The actual value if exercised immediately (difference between market price and strike price).

Time Value: Extra value reflecting the possibility of future price movement before expiry.

3. How Options Work

Options can be exercised in two styles:

American Style Options: Can be exercised anytime before expiry.

European Style Options: Can only be exercised on the expiry date.

Example:

You buy a call option for stock XYZ with a strike price of ₹1,000, expiring in 1 month.

Current market price is ₹1,050, and the premium paid is ₹50.

If the stock rises to ₹1,200, you can exercise the option and make a profit:

Profit = (Stock Price − Strike Price − Premium) = 1,200 − 1,000 − 50 = ₹150 per share.

Part 6 Learn Institutional Trading 1. Introduction to Options Trading

Options trading is one of the most versatile and complex areas of financial markets. It offers traders and investors the ability to hedge, speculate, or generate income. Unlike stocks, which represent ownership in a company, options are financial contracts giving the buyer the right, but not the obligation, to buy or sell an underlying asset at a predetermined price within a specified time frame.

Options are derivatives, meaning their value derives from an underlying asset such as equities, indices, commodities, or currencies. They are widely used by institutional traders, retail investors, and hedgers to manage risk and leverage positions efficiently.

2. Types of Options

There are two primary types of options:

Call Options

Gives the holder the right to buy an underlying asset at a specified price (strike price) before or on the expiry date.

Used by traders who expect the price of the asset to rise.

Put Options

Gives the holder the right to sell an underlying asset at a specified price before or on expiry.

Used by traders who expect the price of the asset to fall.

Key Terms in Options Trading

Strike Price (Exercise Price): The predetermined price at which the asset can be bought or sold.

Expiry Date: The date by which the option must be exercised.

Premium: The cost of buying the option.

Intrinsic Value: The actual value if exercised immediately (difference between market price and strike price).

Time Value: Extra value reflecting the possibility of future price movement before expiry.

3. How Options Work

Options can be exercised in two styles:

American Style Options: Can be exercised anytime before expiry.

European Style Options: Can only be exercised on the expiry date.

Example:

You buy a call option for stock XYZ with a strike price of ₹1,000, expiring in 1 month.

Current market price is ₹1,050, and the premium paid is ₹50.

If the stock rises to ₹1,200, you can exercise the option and make a profit:

Profit = (Stock Price − Strike Price − Premium) = 1,200 − 1,000 − 50 = ₹150 per share.

Part 4 Learn Institutional Trading1. Uses of Options

Options trading is not just speculation; it serves multiple purposes:

Hedging (Risk Management):

Investors use options to protect against unfavorable price movements.

Example: A stock investor buys a put option to limit losses if the stock price drops.

Speculation:

Traders use options to bet on price direction with limited capital and potentially high returns.

Income Generation:

Selling options (writing calls or puts) can generate consistent income through premiums.

Covered calls are a popular income strategy where you hold the stock and sell a call option against it.

Arbitrage Opportunities:

Advanced traders exploit mispricing between options and underlying assets to make risk-free profits.

2. Option Strategies

Options provide flexibility through a variety of strategies, which range from simple to highly complex:

Basic Strategies

Long Call: Buy call option anticipating price increase.

Long Put: Buy put option anticipating price decrease.

Covered Call: Hold stock and sell a call to earn premium.

Protective Put: Buy a put for stock you own to limit downside risk.

Intermediate Strategies

Straddle: Buy call and put at the same strike and expiry to profit from volatility.

Strangle: Buy call and put with different strikes to benefit from large price moves.

Bull Spread: Combine two calls (different strikes) to profit from moderate upward movement.

Bear Spread: Combine two puts to profit from moderate downward movement.

Advanced Strategies

Butterfly Spread: Limit risk and reward for minimal cost, suitable for low volatility expectations.

Iron Condor: Sell an out-of-the-money call and put while buying further out-of-the-money options to cap risk.

Calendar Spread: Exploit differences in time decay by trading options with the same strike but different expiries.

3. Greeks in Options Trading

Options traders use Greeks to measure sensitivity of option prices to different variables:

Delta: Measures price change in option relative to underlying asset.

Gamma: Measures change in delta as asset price changes.

Theta: Measures time decay of the option’s premium.

Vega: Measures sensitivity to volatility.

Rho: Measures sensitivity to interest rates.

Understanding Greeks helps traders manage risk, hedge positions, and optimize strategies.

4. Risks in Options Trading

Options trading carries significant risk, especially for sellers/writers:

For Buyers:

Risk limited to premium paid.

Potential for total loss if option expires worthless.

For Sellers:

Risk can be unlimited for uncovered (naked) options.

Margin requirements can be high.

Time Decay Risk:

Options lose value as expiry approaches, especially OTM options.

Volatility Risk:

Unexpected changes in market volatility can affect option premiums dramatically.

Proper risk management, position sizing, and understanding of market conditions are crucial.

5. Practical Tips for Options Trading

Start Small: Begin with a few contracts until you understand mechanics and risk.

Focus on Liquid Options: Trade options with high volume to ensure tight spreads and easy entry/exit.

Use Stop-Loss: Protect capital by predefining risk limits.

Understand Time Decay: Avoid holding OTM options for too long without movement in underlying.

Diversify Strategies: Combine hedging, speculation, and income strategies.

Part 2 Ride The Big MovesHow Options Work

Options trading works through a combination of buying and selling call and put contracts. Here's an example:

Suppose you buy a call option for a stock currently trading at ₹1,000, with a strike price of ₹1,050, expiring in one month. You pay a premium of ₹20. If the stock rises to ₹1,100:

You can exercise the option to buy the stock at ₹1,050 and sell it at ₹1,100, making a profit of ₹50 per share minus the ₹20 premium, resulting in a net gain of ₹30 per share.

If the stock price stays below ₹1,050, the option expires worthless, and your loss is limited to the premium paid (₹20).

Similarly, with a put option, if the stock falls below the strike price, you can sell it at the higher strike price, profiting from the difference.

Advantages of Options Trading

Leverage: Options allow traders to control a large position with a relatively small investment, magnifying potential profits.

Risk Management: Investors use options to hedge against unfavorable price movements in their portfolios. For instance, buying put options on a stock you own can protect against a decline in its price.

Flexibility: Options provide various strategies to profit from upward, downward, or even sideways movements in the market.

Income Generation: Writing options, especially covered calls, can generate additional income from an existing portfolio.

Risks of Options Trading

Despite their advantages, options come with risks:

Limited Time: Options expire, so timing is crucial. An option can lose all its value if the underlying asset doesn’t move as anticipated before expiration.

Complexity: Options strategies, especially involving multiple legs (like spreads, straddles, and butterflies), can be complex and require careful planning.

Leverage Risk: While leverage can amplify profits, it also magnifies losses. A wrong bet can lead to losing the entire premium or more if you’re selling options.

Popular Options Strategies

Options traders use various strategies depending on market outlook and risk tolerance:

Covered Call: Selling a call option on a stock you already own to earn premium income.

Protective Put: Buying a put option on a stock you own to guard against downside risk.

Straddle: Buying a call and put option with the same strike price and expiration to profit from volatility in either direction.

Spread Strategies: Combining multiple options to limit risk while maintaining profit potential, such as bull spreads or bear spreads.

Part 1 Ride The Big MovesIntroduction to Options Trading

Options trading is a dynamic segment of the financial markets that allows investors to hedge risk, speculate on price movements, and enhance returns. Unlike stocks, which represent ownership in a company, options are financial derivatives—contracts whose value is derived from an underlying asset, such as stocks, indices, commodities, or currencies. By offering flexibility and leverage, options have become a popular tool for both professional traders and retail investors.

What Are Options?

An option is a contract that gives the buyer the right—but not the obligation—to buy or sell an underlying asset at a predetermined price, called the strike price, before or on a specific date known as the expiration date. The seller, or writer, of the option has the obligation to fulfill the contract if the buyer chooses to exercise it.

There are two main types of options:

Call Options – These give the holder the right to buy the underlying asset at the strike price. Investors purchase call options when they expect the price of the underlying asset to rise.

Put Options – These give the holder the right to sell the underlying asset at the strike price. Investors buy put options when they expect the price of the underlying asset to fall.

Key Terms in Options Trading

Understanding options requires familiarity with some key concepts:

Premium: The price paid by the buyer to the seller for the option. This is influenced by factors like the underlying asset price, strike price, time to expiration, volatility, and interest rates.

Strike Price: The price at which the buyer can buy (call) or sell (put) the underlying asset.

Expiration Date: The date on which the option expires. After this, the option becomes worthless if not exercised.

In-the-Money (ITM): A call option is ITM if the underlying price is above the strike price, and a put option is ITM if the underlying price is below the strike price.

Out-of-the-Money (OTM): A call option is OTM if the underlying price is below the strike price, and a put option is OTM if it’s above the strike price.

At-the-Money (ATM): When the underlying price is equal to the strike price.

Risk-Free Trading and Strategies1. Understanding Risk and the Risk-Free Concept

1.1 Definition of Risk in Trading

In trading, risk is defined as the probability of losing part or all of the invested capital due to market fluctuations. Market risks arise from several sources:

Price Risk: The chance that asset prices move against the trader’s position.

Interest Rate Risk: Fluctuations in interest rates affecting bond prices or currency valuations.

Liquidity Risk: Difficulty in executing a trade without impacting the asset’s price.

Counterparty Risk: The risk that the other party in a financial transaction may default.

1.2 The Risk-Free Rate

The risk-free rate is a foundational concept in finance. It represents the theoretical return an investor would receive from an investment with zero risk of financial loss. Government-issued securities, such as U.S. Treasury bills or Indian Government Bonds, are commonly used as proxies for risk-free assets because the probability of default is extremely low. All other investments are measured relative to this baseline using risk premiums, which compensate investors for taking additional risk.

1.3 The Myth of “Risk-Free Trading”

It is crucial to acknowledge that true risk-free trading does not exist in speculative markets. Even sophisticated strategies designed to minimize risk can fail due to unexpected market conditions, operational errors, or systemic shocks. However, financial markets offer near risk-free opportunities, often through arbitrage, hedging, or government-backed instruments.

2. Theoretical Foundations of Risk-Free Trading

2.1 Arbitrage Theory

Arbitrage is a cornerstone of risk-free trading. Arbitrage involves buying and selling the same asset simultaneously in different markets to profit from price discrepancies. Theoretically, arbitrage is considered “risk-free” because it exploits mispricing rather than market direction.

Example:

Suppose a stock trades at ₹100 on the National Stock Exchange (NSE) in India and $1.25 equivalent on an international exchange. A trader can:

Buy the cheaper stock in India.

Sell the same stock in the international market.

Lock in a risk-free profit equal to the price difference after accounting for transaction costs.

While arbitrage appears risk-free, practical execution involves risks, such as transaction delays, market volatility during execution, and high transaction costs.

2.2 Covered Interest Rate Parity

Covered Interest Rate Parity (CIRP) is a near risk-free strategy in the foreign exchange market. It exploits differences in interest rates between two countries while hedging currency risk through forward contracts.

How it Works:

Borrow funds in the currency with a lower interest rate.

Convert the borrowed funds into a higher interest rate currency.

Invest in a risk-free asset in the higher interest rate currency.

Use a forward contract to convert the proceeds back to the original currency at a predetermined rate.

This approach ensures a locked-in return with minimal exposure to currency fluctuations.

2.3 The Role of Hedging

Hedging is another critical element in risk-free trading. Hedging involves taking offsetting positions to reduce or neutralize market risk. Traders use derivatives like options, futures, and swaps to protect their portfolios from adverse price movements.

Common Hedging Strategies:

Protective Put: Buying a put option to limit downside on a stock holding.

Covered Call: Owning a stock while selling a call option to earn premium income while limiting upside.

Delta Neutral Strategy: Combining options and stock positions to minimize sensitivity to price changes.

Hedging reduces risk but does not entirely eliminate it. It is most effective in volatile markets where potential losses can be significant.

3. Practical Risk-Free Trading Strategies

Although no market strategy is entirely risk-free, several practical methods allow traders to approach near-zero risk levels.

3.1 Arbitrage Trading

Arbitrage remains the closest form of “risk-free trading.” Various types exist:

3.1.1 Stock Arbitrage

Exploits price discrepancies of the same stock across different exchanges.

Requires quick execution and sufficient capital.

3.1.2 Triangular Forex Arbitrage

Involves three currencies and takes advantage of discrepancies in cross-exchange rates.

For example, converting USD → EUR → GBP → USD to earn a risk-free profit.

3.1.3 Futures Arbitrage

Exploits the difference between spot and futures prices of the same asset.

Requires precise timing and understanding of carrying costs.

Pros: Low-risk, market-neutral.

Cons: Short-lived opportunities, requires technology and low transaction costs.

3.2 Hedged Trading with Derivatives

Options and futures provide tools for risk mitigation.

Protective Put Strategy:

Buy a put option for a stock already owned.

Limits maximum loss while allowing unlimited upside potential.

Covered Call Strategy:

Hold a stock and sell a call option.

Earn premium income, which offsets potential losses in small downturns.

Example:

Own 100 shares of a company at ₹1,000 each.

Sell a call option with a strike of ₹1,050 for ₹20 premium.

If stock rises above ₹1,050, you sell at ₹1,050 but keep ₹20 premium.

If stock falls, the premium offsets part of the loss.

3.3 Risk-Free Bonds and Government Securities

Investing in government securities is the most straightforward risk-free strategy. Examples include:

Treasury Bills (T-Bills): Short-term government debt with fixed returns.

Government Bonds: Longer-term instruments with predictable interest payments.

Fixed Deposits (FDs): Bank-backed deposits with guaranteed returns.

Pros: Extremely low risk and predictable returns.

Cons: Low returns compared to equities; susceptible to inflation risk.

3.4 Market-Neutral ETFs

Some ETFs employ long-short strategies to minimize market exposure.

Long-short ETFs: Buy undervalued stocks (long) and short overvalued stocks.

Market-neutral ETFs: Target returns independent of overall market movements.

These instruments provide a way for retail investors to engage in near-risk-free strategies without complex derivative setups.

3.5 Statistical Arbitrage

Statistical arbitrage uses historical correlations and mathematical models to trade pairs or baskets of securities.

How it Works:

Identify highly correlated assets.

Go long on underperforming and short on overperforming securities.

Profit as the spread converges.

This is a market-neutral strategy but requires sophisticated software, data analysis, and continuous monitoring.

4. Principles of Minimizing Risk

Even with strategies labeled “risk-free,” the following principles are essential:

Diversification: Spread capital across multiple assets to reduce exposure to a single market event.

Hedging: Protect positions using derivatives to offset adverse moves.

Position Sizing: Avoid over-leveraging, as even low-risk trades can become high-risk with excessive capital.

Liquidity Awareness: Trade only in liquid markets where positions can be exited quickly.

Cost Management: Transaction fees, spreads, and taxes can erode profits, converting low-risk strategies into potential losses.

5. Common Misconceptions

“Risk-free trading exists in all markets” → False. Only government-backed instruments are truly risk-free.

“High returns with zero risk is achievable” → Impossible; higher returns always involve higher risk.

“Hedging eliminates risk” → Hedging reduces risk but cannot remove systemic or operational risk.