what is database trading and how to do it ???Trading data is a sub-category of financial market data. It provides real-time information about stock and market prices as well as historical trends for assets such as equities, fixed-income products, currencies and derivatives.

A Proven Process for Trading Economic Data

Step 1: Establishing the Baseline. Start by understanding the macroeconomic context. ...

Step 2: Analyzing the Surprise Factor. Beyond median forecasts, consider the range of expectations. ...

Step 3: Considering Pre-Positioning and the Bigger Picture.

Fundamental-analysis

how to pcr in the option chain analysis???PCR is computed by dividing open interest in a put contract on a particular day by open call interest on the very same day. Here PCR is computed by dividing the put trading volume by the call trading volume on a specific day. Here, Put volume indicates the total put options initiated over a specific time-frame.

The PCR ratio is calculated by dividing the total open interest of outstanding put options by the total open interest of outstanding call options for a specific security or market. The open interest represents the total number of options contracts that have not been exercised or expired.

How to use Option-Chain in stock market???An option chain has two sections: calls and puts. A call option gives the right to buy a stock while a put gives the right to sell a stock. The price of an options contract is called the premium, which is the upfront fee that an investor pays for purchasing the option.An option chain has two sections: calls and puts. A call option gives the right to buy a stock while a put gives the right to sell a stock. The price of an options contract is called the premium, which is the upfront fee that an investor pays for purchasing the option.

trent ltd"#TRENT - The Countdown Begins!

• Entry - 5300

Stop-Loss - 5000

Target - 6000

✦ Momentum building, ready for ignition!

Trent is forecast to grow earnings and revenue by 24% and 25.4% per annum respectively. EPS is expected to grow by 23.9% per annum. Return on equity is forecast to be 32.5% in 3 years.

How to trade profitabily in stock markets???Use strategies like scalping or momentum trading, aiming for small, consistent gains across several trades. Set realistic profit targets and strict stop-losses to limit risk. Always start with a small capital, trade with proper risk management, and avoid over-leveraging to protect your investments.

Scalping is one of the most popular strategies. It involves selling almost immediately after a trade becomes profitable. The price target is whatever figure means that you'll make money on the trade. Fading involves shorting stocks after rapid moves upward.

CRISIL Ltd.CRISIL a good stock to buy

looking good on weekly

keep in radar....

Past 10 year's financial track record analysis by Moneyworks4me indicates that CRISIL Ltd is a good quality company.

India's premier ratings agency having rated 35,000+ large and medium-scale entities. This is the most profitable business of company and accounts for 51% of total profits while contributing only 28% of revenues

Schneider Electric Infrastructure Ltd.#schneider double bottom pattern formed

target - 800 £

entry - 630 £

stop loss - 590 £

time frame - 2 months

technicals - bullish

this is not any financial advise

Tata consumer products ltdTata Consumer Products Ltd. has an average target of 1152.17. The consensus estimate represents an upside of 12.83% from the last price of 1021.20. View 22 reports from 7 analysts offering long-term price targets for Tata Consumer Products Ltd..

For the quarter, Revenue from operations grew by 9% (8% in constant currency) as compared to corresponding quarter of the previous year, with strong performance in India business, which grew 10%. Profit before exceptional items and tax at Rs 509 Crores is higher by12%.

EPL Ltd# Swing Trade Alert

# Stock Name - EPL

# CUP Break out possible and stock moving to previous support

# sustain above 250 will go for buy

EPL Limited (formerly Essel Propack Limited) is a global tube-packaging company owned by The Blackstone Group headquartered in Mumbai. It is a specialty packaging manufacturer of laminated plastic tubes for the FMCG and Pharma space.

How to use RSI in technical analysis ???To use the RSI indicator, check if the value is above 70 to show an asset is overbought, or below 30 to show it is oversold. Traders can use these signals to find possible trading opportunities.

Low RSI levels, typically below 30 (red line), indicate oversold conditions—generating a potential buy signal. Conversely, high RSI levels, typically above 70 (green line), indicate overbought conditions—generating a potential sell signal

Successful trades often occur when the RSI crosses above 30 (indicating a buy signal) or below 70 (indicating a sell signal). Adjusting the RSI period to 9 can make it more sensitive to price changes and be suitable for more active trading strategies

zensar technologies Ltd#ZENSARTECH

Stock has taken good support near 880 levels. After crossing 920 levels, more move is possible.

Time period: Swing/Positional call

Target 920/985

Stop loss 882

I am just representing my views

For educational purposes only.

Zensar Technologies is forecast to grow earnings and revenue by 13.6% and 11.6% per annum respectively. EPS is expected to grow by 13.4% per annum. Return on equity is forecast to be 17.4% in 3 years.

Tech Mahindra Ltd.#TECHM on a breakout.

Entry: 1160

SL: 1120

Target: 1315/ 1425/1570/1700/1800

Check BIO for any help.

Comment stocks below for review.

Happy Trading!!!

Tech Mahindra is forecast to grow earnings and revenue by 23.9% and 7.7% per annum respectively. EPS is expected to grow by 23.8% per annum. Return on equity is forecast to be 29.3% in 3 years

UltraTech Cement Ltd."#ULTRACEMCO - Building Up Strength!

Entry: 11600

Stop-Loss: 11300

Target: 12000

Support solid as concrete-next stop, sky!

UltraTech Cement Ltd. has an average target of 12000.The consensus estimate represents an upside of 9.46% from the last price of 11640.60. View 43 reports from 12 analysts offering long-term price targets for UltraTech Cement Ltd..

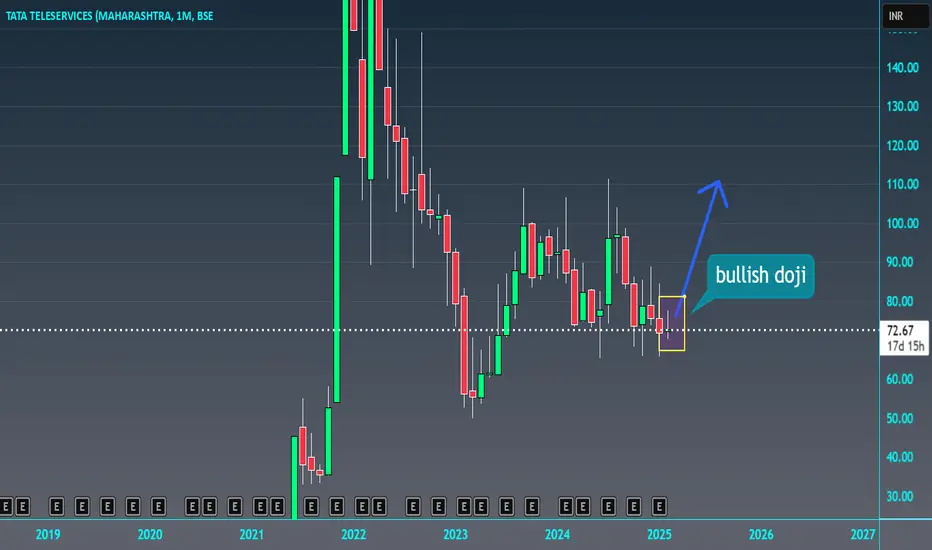

Tata Teleservices (Maharashtra) Ltd#TTML PERFECT REVERSAL CANDIDATE

TARGET - 82

ENTRY - 72

STOP LOSS - 70

TIME FRAME - MONTHLY

TECHNICALS - BULLISH DOJI CANDLE FORMED

THIS IS NOT ANY FINANCIAL ADVISE

As on 7th Feb 2025 TTML SHARE Price closed @ 72.04 and we RECOMMEND Strong Sell for LONG-TERM with Stoploss of 80.87 & Sell for SHORT-TERM with Stoploss of 76.08 we also expect STOCK to react on Following IMPORTANT LEVELS.

Mahamaya Steel Industries Ltd#MAHASTEEL

Daily chart..

Resistance at 225

Support at 180

Keep on Radar..

Shri Ramanand Agrawal

The Company has been promoted by Shri Ramanand Agrawal and his family members. Agrawal family is a well-known industrialist family from Raipur. The Company came out with a public issue in the year 1994 which was oversubscribed. MSIL is a profit making and dividend paying Company.

Transrail Lighting Limited#TRANSRAILL Buy near IPO price and hold it for 1:2.5 Profit.

Entry: 605

SL: 565

Target: 700

Check BIO for any help.

Comment stocks for review below.

Happy Trading!!!

Transrail Lighting IPO represents an opportunity to invest in a well-established company with robust financials, a diverse service portfolio, and a strong presence in a high-growth sector. Its strategic expansion plans and proven operational efficiency position it as a strong contender for long-term growth

Gulf Oil Lubricants India Ltd#GULFOILLUB

Daily chart..

Resistance at 1270

Support at 950

Keep an eye on it..

Market cap: $0.65 Billion USD

As of February 2025 Gulf Oil Lubricants has a market cap of $0.65 Billion USD. This makes Gulf Oil Lubricants the world's 6383th most valuable company by market cap according to our data.

OIL's Net Zero commitment encompasses a range of initiatives, including adopting cleaner energy sources, investing in renewable energy projects and implementing advanced technologies to minimize greenhouse gas emissions for which about Rs. 25,000 Cr is envisaged to be invested by 2040.

Road Map for A New TraderRoadmap to being a successful trader

Step 1: Decide on your trading pattern. ...

Step 2: Select the most appropriate stock trading broker for You. ...

Step 3: Choose the best stocks for your investment. ...

Step 4: Determine your risk tolerance. ...

Step 5: Learn to be patient.

The forex market is often considered an ideal market for learning technical analysis due to several factors: Diverse market conditions: Forex trading offers a wide range of currency pairs and diverse market conditions, providing ample opportunities to practice technical analysis skills.

Option TradingWhen you trade options, you're essentially placing a bet on if a stock will decrease, increase or remain the same in value; how much it will deviate from its current price; and in what time those changes will occur. Based on those parameters, you can choose to enter into a contract to buy or sell a company's stock.

Options are highly sensitive to market volatility. Significant price swings can lead to substantial gains or losses. A trader might buy a put option expecting a stock to drop. If the stock instead surges in price due to unforeseen events, the value of the put option plummets.

What is the Producer Price Index (PPI) ?

🔍 Definition: Producer Price Index (PPI)

📍 Measures the average price change over time received by domestic producers for their goods and services.

📍 Indicates inflation trends at the wholesale level.

🚨 C ompilation:

📍 Based on thousands of price indexes categorized by industry and product types.

📌 Data Collection:

✅Relies on ~100,000 monthly price quotes provided voluntarily by 25,000 producer establishments.

⚠️ Release Timing:

📍 Published monthly by the U.S. Bureau of Labor Statistics (BLS) during

the s econd week of the month .

📌 Economic Significance:

🟢 Rising PPI: Suggests increasing production costs, potential inflationary pressures.

🔵 Falling PPI: Implies reduced cost pressures and possible deflationary signals.

🔥 How Many Moment Expected in Gold : 100-150 PIPS

( EASY TO TRADE BECAUSE FOLLOW TECHNICAL)

📚 Learn more about trading strategies and market insights!

💡 Follow for more educational content to boost your trading knowledge. 🚀

#TATA Consumer ltdTata Consumer

Structure break+ trend continuation are the sign of bullish reversal.

Perfect chart

1107/1234

Im waiting for entry point

as of February 6, 2025, Tata Consumer Products Limited (TATACONSUM) is trading at ₹1,069.85.

echnical indicators suggest a bullish trend for the stock.nalysts have set a median target price of ₹1,190.32 over the next 12 months, indicating potential upside.citeturn0search3

he company has demonstrated consistent financial performance, with a consolidated total income of ₹4,495.16 crore for the quarter ending December 31, 2024, reflecting a 5.51% increase from the previous quarter and a 16.35% rise compared to the same quarter the previous year.

given these factors, the stock's outlook appears positive.

*Please note that this information is for educational purposes only and should not be considered financial advice. Always consult with a qualified financial advisor before making investment decisions.*

How to draw support and resistance?Drawing **support and resistance** levels is a key aspect of technical analysis. These levels represent areas where the price tends to reverse or stall, providing key insights into market behavior. Here's how to draw them in brief:

### 1. **Support**

- **Definition**: A price level where a downtrend is expected to pause or reverse as demand increases. It's the floor of the price action.

- **How to Draw**:

- Look for areas where the price has bounced higher multiple times in the past. These are points where buyers have stepped in.

- Draw a horizontal line at the lowest price points in these areas.

- Strong support is confirmed when the price touches the same level multiple times without breaking it.

### 2. **Resistance**

- **Definition**: A price level where an uptrend is expected to pause or reverse as selling pressure increases. It's the ceiling of the price action.

- **How to Draw**:

- Identify areas where the price has consistently faced downward pressure or reversed. This is where sellers have entered the market.

- Draw a horizontal line at the highest price points in these areas.

- Strong resistance is confirmed when the price fails to break above it multiple times.

### 3. **Key Points to Remember**

- **Multiple Touches**: The more times the price touches a level without breaking through, the stronger the support or resistance.

- **Broken Levels**: Once a support level is broken, it often becomes resistance (and vice versa).

- **Use Trendlines**: In addition to horizontal levels, you can also draw diagonal trendlines to connect higher lows (support) or lower highs (resistance) in trending markets.

These levels help traders anticipate potential price reversals or continuations, making them essential for developing trading strategies.

Pansari Developers ltdpansari jackpot share

target - 250

entry - 210

stop loss - 190

time frame - weeks

technicals - bullish

this is not any financial advise