[Sextan] PINEv4 Sextans Backtest FrameworkLevel: 5

Background

Backtesting of technical indicators and strategies is the most common way to understand a quantitative strategy. However, the complicated configuration and adaptation work of backtesting many quantitative tools makes many traders who do not understand the code daunted. Moreover, although I have written a lot of strategies,

However, I am still not very satisfied with the backtest configuration and writing efficiency. Therefore, I have been thinking about how to build a backtesting framework that can quickly and easily evaluate the backtesting performance of any indicator with a "long/short entry" indicator, that is, a "simple backtesting tool for dummies". The performance requirements should be stable, and the operation should be simple and convenient. It is best to "copy", "paste", and "a few mouse clicks" to complete the quick backtest and evaluation of a new indicator.

Luckily, I recently realized that TradingView provides an "Indicator on Indicator" feature, which is the perfect foundation for doing "hot swap" backtesting. My basic idea is to use a two-layer design. The first layer is the technical indicator signal source that needs to be embedded, which is only used to provide buy and sell signals of custom strategies; the second layer is the trading system, which is used to receive the output signals of the first layer, and filter the signals according to the agreed specifications. , Take Profit, Stop Loss, draw buy and sell signals and cost lines, define and send custom buy and sell alert messages to mobile phones, social software or trading interfaces. In general, this two-layer design is a flexible combination of "fixed and flexiable", which can meet the needs of most traders to quickly evaluate the performance of a certain technical indicator. The first layer here is flexible. Users can insert their own strategy codes according to my template, and they can draw buy and sell signals and output them to the second layer. The second layer is fixed, and the overall framework is solidified to ensure the stability and unity of the trading system. It is convenient to compare different or similar strategies under the same conditions. Finally, all trading signals are drawn on the chart, and the output strategy returns. test report.

The main function:

The first layer: "{Sextan} Your Indicator Source", the script provides a template for personalized strategy input, and the signal and definition interfaces ensure full compatibility with the second layer. Backtesting is performed stably in the backtesting framework of the layer. The first layer of this script is also relatively simple: enter your script in the highlighted custom script area, and after ensuring the final buy and sell signals long = bool condition, short = bool condition, the design of the first layer is considered complete. Input it into the PINE script editor of TradingView, save it and add it to the chart, you can see the pulse sequence in yellow (buy) and purple (sell) on the sub-picture, corresponding to the main picture, you can subjectively judge that the quality of the trading point of the strategy is good Bad.

The second layer: "{Sextan} PINEv4 Sextans Backtest Framework". This script is the standardized trading system strategy execution and alarm, used to generate the final report of the strategy backtest and some key indicators that I have customized that I find useful, such as: winning rate , Odds, Winning Surface, Kelly Ratio, Take Profit and Stop Loss Thresholds, Trading Frequency, etc. are evaluated according to the Kelly formula. To use the second layer, first load it into the TrainingView chart, no markers will appear on the chart, since you have not specified any strategy source signals, click on the gear-shaped setting next to the "{Sextan} PINEv4 Sextans BTFW" header button, you can open the backtest settings, the first item is to select your custom strategy source. Because we have added the strategy source to the chart in the previous step, you can easily find an option "{Sextan} Your Indicator Source: Signal" at the bottom of the list, this is the strategy source input we need, select and confirm , you can see various markers on the main graph, and quickly generate a backtesting profit graph and a list of backtesting reports. You can generate files and download the backtesting reports locally. You can also click the gear on the backtest chart interface to customize some conditions of the backtest, including: initial capital amount, currency type, percentage of each order placed, amount of pyramid additions, commission fees, slippage, etc. configuration. Note: The configuration in the interface dialog overrides the same configuration implemented by the code in the backtest script.

How to output charts:

The first layer: "{Sextan} Your Indicator Source", the output of this script is the pulse value of yellow and purple, yellow +1 means buy, purple -1 means sell.

The second layer: PINEv4 Sextans Backtest Framework". The output of this script is a bit complicated. After all, it is the entire trading system with a lot of information:

1. Blue and red arrows. The blue upward arrow indicates long position, the red downward arrow indicates short position, and the horizontal bar at the end of the purple arrow indicates take profit or stop loss exit.

2. Red and green lines. This is the holding cost line of the strategy, green represents the cost of holding a long position, and red represents the cost of holding a short position. The cost line is a continuous solid line and the price action is relatively close.

3. Green and yellow long take profit and stop loss area and green and yellow long take profit and stop loss fork. Once a long position is held, there is a conditional order for take profit and stop loss. The green horizontal line is the long take profit ratio line, and the yellow is the long stop loss ratio line; the green cross indicates the long take profit price, and the yellow cross indicates the long position. Stop loss price. It's worth noting that the prongs and wires don't necessarily go together. Because of the optimization of the algorithm, for a strong market, the take profit will occur after breaking the take profit line, and the profit will not be taken until the price falls.

4. The purple and red short take profit and stop loss area and the purple red short stop loss fork. Once a short position is held, there will be a take profit and stop loss conditional order, the red is the short take profit ratio line, and the purple is the short stop loss ratio line; the red cross indicates the short take profit price, and the purple cross indicates the short stop loss price.

5. In addition to the above signs, there are also text and numbers indicating the profit and loss values of long and short positions. "L" means long; "S" means short; "XL" means close long; "XS" means close short.

TradingView Strategy Tester Panel:

The overview graph is an intuitive graph that plots the blue (gain) and red (loss) curves of all backtest periods together, and notes: the absolute value and percentage of net profit, the number of all closed positions, the winning percentage, the profit factor, The maximum trading loss, the absolute value and ratio of the average trading profit and loss, and the average number of K-lines held in all trades.

Another is the performance summary. This is to display all long and short statistical indicators of backtesting in the form of a list, such as: net profit, gross profit, Sharpe ratio, maximum position, commission, times of profit and loss, etc.

Finally, the transaction list is a table indexed by the transaction serial number, showing the signal direction, date and time, price, profit and loss, accumulated profit and loss, maximum transaction profit, transaction loss and other values.

Remarks

Finally, I will explain that this is just the beginning of this model. I will continue to optimize the trading system of the second layer. Various optimization feedback and suggestions are welcome. For valuable feedback, I am willing to provide some L4/L5 technical indicators as rewards for free subscription rights.

Subscription

To encourage more people use this framework and avoid some abuse this one, I would like to set

100 Tradingview Coins per Monthly Subscription.

100X10 Tradingview Coins per Yearly Subscription.

Search in scripts for "backtest"

[fareid] Quick Backtest Framework█ OVERVIEW

This Framework allows Pine Coders to quickly code Study() based signal/strategy and validate its viability before proceed to code with more advance/complex customized rules for entry, exit, trailstop, risk management etc..

This is somewhat an upgraded version of my earlier personal template with different strategy used, cleaner code

and additional features.

█ USE CASES

- You have an idea for trade signal and need a quick way to verify its potential before writing lengthy/complicated code

- You found a study script for trading signal in public library and want to validate it profitability with minimum effort before including it in your trading playbook

█ FEATURES

- Alert: Ready to use alert function based on signals from your custom indicator.

- Visual Backtest: Auto-plot entry, stop-loss and take profit for simple strategy performance analysis

- Backtest Statistic: Provide basic key metrics based on backtest strategy

- BTE External Signal Protocol: Ready to use code that will supply required state to PineCoders Backtesting & Trading Engine if you wish to have more advance and sophisticated backtesting engine

Notes: All of the above features have On/Off toggle

█ Description & How To Use

This Framework consist of 5 Modules but you only need to edit the first 2 Modules:

Module1: Indicator

Module2: Framework Input Protocol

Module3: Alert

Module4: Backtest

Module5: Backtest & Trading Engine

Tips: The source-code includes collapsible block by module for easy navigating

Module1: Indicator:

-----------------------------------------------------------------------------------

Main Module. Place custom indicator input parameter/calculation/indicator plotting here

Sample Strategy: Double MACD Crossover

MACD Signal: 1st MACD Cross above signal line indicate Buy Signal

1st MACD Cross below signal line indicate Sell Signal

MACD Filter: 2nd MACD is above 0 line indicate Uptrend

2nd MACD is below 0 line indicate Downtrend

Module2: Framework Input Protocol:

-----------------------------------------------------------------------------------

Use this module to connect main indicator/signal calculated in Module1 to the rest of the framework's module

4 variables needed to be defined here:

1. Uptrend

2. Dntrend

3. BuySignal

4. SellSignal

i'm not sure how to place a code snippet here to show you example so in the source code i already put a comment in Module2 on which part u need to edit. I hope its pretty simple to use.

Module3: Alert Module Description:

-----------------------------------------------------------------------------------

As long as the variables in Module2 properly defined, the alert module is ready to use without any further modification.

Input:

Enable Alert --> Enable TV's alert and plot signal to chart

Alert Type --> Set to take Buy only, Sell only or Both alert

Module4: Backtest Module Description:

-----------------------------------------------------------------------------------

As long as the variables in Module2 properly defined, the backtest module is ready to use without any further modification.

Input:

Backtest Stat --> Enable Backtest Statistic Label

Backtest Visual --> Enable Backtest visual simulation

Backtest Type --> Set to take Buy only or Sell only or both

SL Type -->

ATR : Set SL in ATR times Multiplier below entry price

Fixed : Set SL in fixed point below entry point (in 'Dollar'). e.g. for Stocks -> 0.5 equals to 50cent while for EURUSD currency -> 0.005 equal to 50 pips

HiLo Bar: Set SL at highest/lowest wick of previous bar plus/minus Fixed point. e.g. EURUSD HiLo=3 and Fixed Point = 0.0005, buy trade will place SL 5 Pips below lowest of previous 3 bar

SL ATR Multi --> Set Lookback Period used for SL's ATR calculation

SL ATR Multi --> Set ATR Multiplier for SL

SL Fixed --> Set Fixed Level for SL

SL Bar --> Set Number of previous bar to check for SL placement

TP RR Ratio --> Set TP based on RR multiplier. e.g. 2 means TP level will be twice further from entry point compared to Entry-SL distance.

Notes: The point is for preliminary testing, so it only supports 1 trade at a time and no Trailing Stop

Module5: Backtest & Trading Engine Description:

-----------------------------------------------------------------------------------

As long as the variables in Module2 properly defined, the Pinecoders BTE module is ready to use without any further modification.

Input:

External Signal Protocol --> Set ESP State to send to "Backtesting & Trading Engine "

Signal With Filter --> Use this to send entry signal that already filtered by this study indicator (without stoploss level)

Signal Without Filter --> Use this to send raw entry signal that are NOT YET FILTERED by this study indicator (without stoploss level)

Signal and Stop With Filter --> Use this to send entry signal WITH StopLoss that already filtered by this study indicator (with stoploss level)

Signal and Stop Without Filter --> Use this to send raw entry signal WITH StopLoss that are NOT YET FILTERED by this study indicator (with stoploss level)

Notes: Backtesting & Trading Engine already have built-in Filter, Entries and Stop Level. e.g. Unselect all their filter state if only want to use custom filter and make sure send Signal with Filter (with or without SL level)

█ DISCLAIMER:

This framework main objective is to create my personal indicator template so that i just have to modify the indicator module for preliminary testing in future.

The sample strategy included are for educational purpose only. Use at your own risk

credit: LucF/PineCoders for a lot of his scripts that i use as a guide to complete this

AstraAlgo BacktesterOVERVIEW

The AstraAlgo Backtester allows traders to simulate and evaluate trading strategies directly on TradingView. By simulating trades across different timeframes and markets, it provides valuable insights into win rates, drawdowns, and overall strategy effectiveness.

HOW TO GAIN ACCESS

Subscribe at www.astraalgo.com and provide your TradingView username. Access is usually granted within a few hours, and you’ll receive email confirmation once activated.

FEATURES

Signal Modes

Signal Modes are the core of the AstraAlgo Backtester, generating simulated trade signals based on historical price data. Users can choose between Off, Basic, Advanced, or Custom modes to evaluate strategies under different conditions and refine their trading approach.

Adjustable Backtesting

Parameters for historical simulations can be customized to test different market conditions and trading scenarios. This allows traders to measure strategy performance, including win rate, profit/loss, and risk/reward ratios, helping refine and optimize strategies before live execution.

Bar Coloring

Bar Coloring highlights bullish and bearish bars on historical charts, allowing traders to visually assess trend direction and trade outcomes during backtesting. This makes it easier to analyze momentum and strategy effectiveness at a glance.

Astra Cloud

Astra Cloud overlays dynamic support and resistance levels on historical price data. These zones adapt automatically to past market movements, helping traders identify areas where trades would have reacted, aiding strategy evaluation and optimization.

CONTACT US

For any questions or assistance, contact us at support@astraalgo.com or visit www.astraalgo.com.

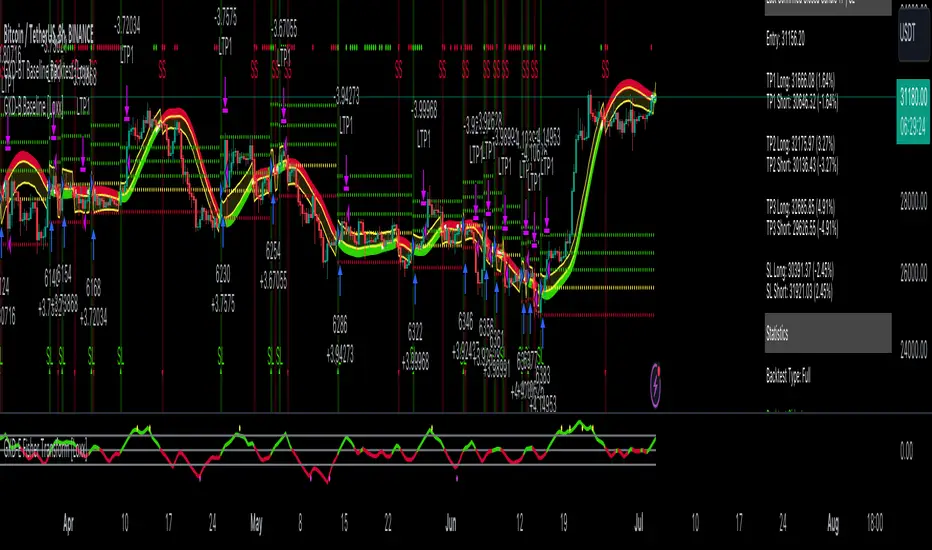

GKD-BT Baseline Backtest [Loxx]The Giga Kaleidoscope GKD-BT Baseline Backtest is a backtesting module included in Loxx's "Giga Kaleidoscope Modularized Trading System."

█ GKD-BT Baseline Backtest

The GKD-BT Baseline Backtest allows traders to backtest the Regular and Stepped baselines used in the GKD trading system. This module includes 65+ moving averages and 15+ types of volatility to choose from.

Additionally, this backtest module provides the option to test the GKD-B indicator with 1 to 3 take profits and 1 stop loss. The Trading backtest allows for the use of 1 to 3 take profits, while the Full backtest is limited to 1 take profit. The Trading backtest also offers the capability to apply a trailing take profit.

In terms of the percentage of trade removed at each take profit, this backtest module has the following hardcoded values:

Take profit 1: 50% of the trade is removed

Take profit 2: 25% of the trade is removed

Take profit 3: 25% of the trade is removed

Stop loss: 100% of the trade is removed

After each take profit is achieved, the stop loss level is adjusted. When take profit 1 is reached, the stop loss is moved to the entry point. Similarly, when take profit 2 is reached, the stop loss is shifted to take profit 1. The trailing take profit feature comes into play after take profit 2 or take profit 3, depending on the number of take profits selected in the settings. The trailing take profit is always activated on the final take profit when 2 or more take profits are chosen.

The backtest also offers the capability to restrict by a specific date range, allowing for simulated forward testing based on past data. Additionally, users have the option to display or hide a trading panel that provides relevant information about the backtest, statistics, and the current trade. It is also possible to activate alerts and toggle sections of the trading panel on or off. On the chart, historical take profit and stop loss levels are represented by horizontal lines overlaid for reference.

This backtest also includes an optional GKD-E Exit indicator that can be used to test early exits.

The GKD system utilizes volatility-based take profits and stop losses. Each take profit and stop loss is calculated as a multiple of volatility. You can change the values of the multipliers in the settings as well.

To utilize this strategy, follow these steps:

1. (Required) Import the value "Input into NEW GKD-BT Backtest" from the GKD-B Baseline indicator into the GKD-BT Baseline Backtest field "Import GKD-B Baseline"

2. (Optional) Import the value "Input into NEW GKD-BT Backtest" from the GKD-E Exit indicator into the GKD-BT Baseline Backtest field "Import GKD-E Exit". You can toggle the Exit on or off using the "Activate GKD-E Exit" option.

Baselines that are compatible with this backtest module:

GKD-B Baseline

GKD-B Stepped Baseline

Volatility Types Included

17 types of volatility are included in this indicator

Close-to-Close

Parkinson

Garman-Klass

Rogers-Satchell

Yang-Zhang

Garman-Klass-Yang-Zhang

Exponential Weighted Moving Average

Standard Deviation of Log Returns

Pseudo GARCH(2,2)

Average True Range

True Range Double

Standard Deviation

Adaptive Deviation

Median Absolute Deviation

Efficiency-Ratio Adaptive ATR

Mean Absolute Deviation

Static Percent

█ Giga Kaleidoscope Modularized Trading System

Core components of an NNFX algorithmic trading strategy

The NNFX algorithm is built on the principles of trend, momentum, and volatility. There are six core components in the NNFX trading algorithm:

1. Volatility - price volatility; e.g., Average True Range, True Range Double, Close-to-Close, etc.

2. Baseline - a moving average to identify price trend

3. Confirmation 1 - a technical indicator used to identify trends

4. Confirmation 2 - a technical indicator used to identify trends

5. Continuation - a technical indicator used to identify trends

6. Volatility/Volume - a technical indicator used to identify volatility/volume breakouts/breakdown

7. Exit - a technical indicator used to determine when a trend is exhausted

8. Metamorphosis - a technical indicator that produces a compound signal from the combination of other GKD indicators*

*(not part of the NNFX algorithm)

What is Volatility in the NNFX trading system?

In the NNFX (No Nonsense Forex) trading system, ATR (Average True Range) is typically used to measure the volatility of an asset. It is used as a part of the system to help determine the appropriate stop loss and take profit levels for a trade. ATR is calculated by taking the average of the true range values over a specified period.

True range is calculated as the maximum of the following values:

-Current high minus the current low

-Absolute value of the current high minus the previous close

-Absolute value of the current low minus the previous close

ATR is a dynamic indicator that changes with changes in volatility. As volatility increases, the value of ATR increases, and as volatility decreases, the value of ATR decreases. By using ATR in NNFX system, traders can adjust their stop loss and take profit levels according to the volatility of the asset being traded. This helps to ensure that the trade is given enough room to move, while also minimizing potential losses.

Other types of volatility include True Range Double (TRD), Close-to-Close, and Garman-Klass

What is a Baseline indicator?

The baseline is essentially a moving average, and is used to determine the overall direction of the market.

The baseline in the NNFX system is used to filter out trades that are not in line with the long-term trend of the market. The baseline is plotted on the chart along with other indicators, such as the Moving Average (MA), the Relative Strength Index (RSI), and the Average True Range (ATR).

Trades are only taken when the price is in the same direction as the baseline. For example, if the baseline is sloping upwards, only long trades are taken, and if the baseline is sloping downwards, only short trades are taken. This approach helps to ensure that trades are in line with the overall trend of the market, and reduces the risk of entering trades that are likely to fail.

By using a baseline in the NNFX system, traders can have a clear reference point for determining the overall trend of the market, and can make more informed trading decisions. The baseline helps to filter out noise and false signals, and ensures that trades are taken in the direction of the long-term trend.

What is a Confirmation indicator?

Confirmation indicators are technical indicators that are used to confirm the signals generated by primary indicators. Primary indicators are the core indicators used in the NNFX system, such as the Average True Range (ATR), the Moving Average (MA), and the Relative Strength Index (RSI).

The purpose of the confirmation indicators is to reduce false signals and improve the accuracy of the trading system. They are designed to confirm the signals generated by the primary indicators by providing additional information about the strength and direction of the trend.

Some examples of confirmation indicators that may be used in the NNFX system include the Bollinger Bands, the MACD (Moving Average Convergence Divergence), and the MACD Oscillator. These indicators can provide information about the volatility, momentum, and trend strength of the market, and can be used to confirm the signals generated by the primary indicators.

In the NNFX system, confirmation indicators are used in combination with primary indicators and other filters to create a trading system that is robust and reliable. By using multiple indicators to confirm trading signals, the system aims to reduce the risk of false signals and improve the overall profitability of the trades.

What is a Continuation indicator?

In the NNFX (No Nonsense Forex) trading system, a continuation indicator is a technical indicator that is used to confirm a current trend and predict that the trend is likely to continue in the same direction. A continuation indicator is typically used in conjunction with other indicators in the system, such as a baseline indicator, to provide a comprehensive trading strategy.

What is a Volatility/Volume indicator?

Volume indicators, such as the On Balance Volume (OBV), the Chaikin Money Flow (CMF), or the Volume Price Trend (VPT), are used to measure the amount of buying and selling activity in a market. They are based on the trading volume of the market, and can provide information about the strength of the trend. In the NNFX system, volume indicators are used to confirm trading signals generated by the Moving Average and the Relative Strength Index. Volatility indicators include Average Direction Index, Waddah Attar, and Volatility Ratio. In the NNFX trading system, volatility is a proxy for volume and vice versa.

By using volume indicators as confirmation tools, the NNFX trading system aims to reduce the risk of false signals and improve the overall profitability of trades. These indicators can provide additional information about the market that is not captured by the primary indicators, and can help traders to make more informed trading decisions. In addition, volume indicators can be used to identify potential changes in market trends and to confirm the strength of price movements.

What is an Exit indicator?

The exit indicator is used in conjunction with other indicators in the system, such as the Moving Average (MA), the Relative Strength Index (RSI), and the Average True Range (ATR), to provide a comprehensive trading strategy.

The exit indicator in the NNFX system can be any technical indicator that is deemed effective at identifying optimal exit points. Examples of exit indicators that are commonly used include the Parabolic SAR, the Average Directional Index (ADX), and the Chandelier Exit.

The purpose of the exit indicator is to identify when a trend is likely to reverse or when the market conditions have changed, signaling the need to exit a trade. By using an exit indicator, traders can manage their risk and prevent significant losses.

In the NNFX system, the exit indicator is used in conjunction with a stop loss and a take profit order to maximize profits and minimize losses. The stop loss order is used to limit the amount of loss that can be incurred if the trade goes against the trader, while the take profit order is used to lock in profits when the trade is moving in the trader's favor.

Overall, the use of an exit indicator in the NNFX trading system is an important component of a comprehensive trading strategy. It allows traders to manage their risk effectively and improve the profitability of their trades by exiting at the right time.

What is an Metamorphosis indicator?

The concept of a metamorphosis indicator involves the integration of two or more GKD indicators to generate a compound signal. This is achieved by evaluating the accuracy of each indicator and selecting the signal from the indicator with the highest accuracy. As an illustration, let's consider a scenario where we calculate the accuracy of 10 indicators and choose the signal from the indicator that demonstrates the highest accuracy.

The resulting output from the metamorphosis indicator can then be utilized in a GKD-BT backtest by occupying a slot that aligns with the purpose of the metamorphosis indicator. The slot can be a GKD-B, GKD-C, or GKD-E slot, depending on the specific requirements and objectives of the indicator. This allows for seamless integration and utilization of the compound signal within the GKD-BT framework.

How does Loxx's GKD (Giga Kaleidoscope Modularized Trading System) implement the NNFX algorithm outlined above?

Loxx's GKD v2.0 system has five types of modules (indicators/strategies). These modules are:

1. GKD-BT - Backtesting module (Volatility, Number 1 in the NNFX algorithm)

2. GKD-B - Baseline module (Baseline and Volatility/Volume, Numbers 1 and 2 in the NNFX algorithm)

3. GKD-C - Confirmation 1/2 and Continuation module (Confirmation 1/2 and Continuation, Numbers 3, 4, and 5 in the NNFX algorithm)

4. GKD-V - Volatility/Volume module (Confirmation 1/2, Number 6 in the NNFX algorithm)

5. GKD-E - Exit module (Exit, Number 7 in the NNFX algorithm)

6. GKD-M - Metamorphosis module (Metamorphosis, Number 8 in the NNFX algorithm, but not part of the NNFX algorithm)

(additional module types will added in future releases)

Each module interacts with every module by passing data to A backtest module wherein the various components of the GKD system are combined to create a trading signal.

That is, the Baseline indicator passes its data to Volatility/Volume. The Volatility/Volume indicator passes its values to the Confirmation 1 indicator. The Confirmation 1 indicator passes its values to the Confirmation 2 indicator. The Confirmation 2 indicator passes its values to the Continuation indicator. The Continuation indicator passes its values to the Exit indicator, and finally, the Exit indicator passes its values to the Backtest strategy.

This chaining of indicators requires that each module conform to Loxx's GKD protocol, therefore allowing for the testing of every possible combination of technical indicators that make up the six components of the NNFX algorithm.

What does the application of the GKD trading system look like?

Example trading system:

Backtest: GKD-BT Baseline Backtest as shown on the chart above

Baseline: Hull Moving Average as shown on the chart above

Volatility/Volume: Hurst Exponent

Confirmation 1: Sherif's HiLo

Confirmation 2: uf2018

Continuation: Coppock Curve

Exit: Fisher Transform as shown on the chart above

Metamorphosis: Baseline Optimizer

Each GKD indicator is denoted with a module identifier of either: GKD-BT, GKD-B, GKD-C, GKD-V, GKD-M, or GKD-E. This allows traders to understand to which module each indicator belongs and where each indicator fits into the GKD system.

█ Giga Kaleidoscope Modularized Trading System Signals

Standard Entry

1. GKD-C Confirmation gives signal

2. Baseline agrees

3. Price inside Goldie Locks Zone Minimum

4. Price inside Goldie Locks Zone Maximum

5. Confirmation 2 agrees

6. Volatility/Volume agrees

1-Candle Standard Entry

1a. GKD-C Confirmation gives signal

2a. Baseline agrees

3a. Price inside Goldie Locks Zone Minimum

4a. Price inside Goldie Locks Zone Maximum

Next Candle

1b. Price retraced

2b. Baseline agrees

3b. Confirmation 1 agrees

4b. Confirmation 2 agrees

5b. Volatility/Volume agrees

Baseline Entry

1. GKD-B Baseline gives signal

2. Confirmation 1 agrees

3. Price inside Goldie Locks Zone Minimum

4. Price inside Goldie Locks Zone Maximum

5. Confirmation 2 agrees

6. Volatility/Volume agrees

7. Confirmation 1 signal was less than 'Maximum Allowable PSBC Bars Back' prior

1-Candle Baseline Entry

1a. GKD-B Baseline gives signal

2a. Confirmation 1 agrees

3a. Price inside Goldie Locks Zone Minimum

4a. Price inside Goldie Locks Zone Maximum

5a. Confirmation 1 signal was less than 'Maximum Allowable PSBC Bars Back' prior

Next Candle

1b. Price retraced

2b. Baseline agrees

3b. Confirmation 1 agrees

4b. Confirmation 2 agrees

5b. Volatility/Volume agrees

Volatility/Volume Entry

1. GKD-V Volatility/Volume gives signal

2. Confirmation 1 agrees

3. Price inside Goldie Locks Zone Minimum

4. Price inside Goldie Locks Zone Maximum

5. Confirmation 2 agrees

6. Baseline agrees

7. Confirmation 1 signal was less than 7 candles prior

1-Candle Volatility/Volume Entry

1a. GKD-V Volatility/Volume gives signal

2a. Confirmation 1 agrees

3a. Price inside Goldie Locks Zone Minimum

4a. Price inside Goldie Locks Zone Maximum

5a. Confirmation 1 signal was less than 'Maximum Allowable PSVVC Bars Back' prior

Next Candle

1b. Price retraced

2b. Volatility/Volume agrees

3b. Confirmation 1 agrees

4b. Confirmation 2 agrees

5b. Baseline agrees

Confirmation 2 Entry

1. GKD-C Confirmation 2 gives signal

2. Confirmation 1 agrees

3. Price inside Goldie Locks Zone Minimum

4. Price inside Goldie Locks Zone Maximum

5. Volatility/Volume agrees

6. Baseline agrees

7. Confirmation 1 signal was less than 7 candles prior

1-Candle Confirmation 2 Entry

1a. GKD-C Confirmation 2 gives signal

2a. Confirmation 1 agrees

3a. Price inside Goldie Locks Zone Minimum

4a. Price inside Goldie Locks Zone Maximum

5a. Confirmation 1 signal was less than 'Maximum Allowable PSC2C Bars Back' prior

Next Candle

1b. Price retraced

2b. Confirmation 2 agrees

3b. Confirmation 1 agrees

4b. Volatility/Volume agrees

5b. Baseline agrees

PullBack Entry

1a. GKD-B Baseline gives signal

2a. Confirmation 1 agrees

3a. Price is beyond 1.0x Volatility of Baseline

Next Candle

1b. Price inside Goldie Locks Zone Minimum

2b. Price inside Goldie Locks Zone Maximum

3b. Confirmation 1 agrees

4b. Confirmation 2 agrees

5b. Volatility/Volume agrees

Continuation Entry

1. Standard Entry, 1-Candle Standard Entry, Baseline Entry, 1-Candle Baseline Entry, Volatility/Volume Entry, 1-Candle Volatility/Volume Entry, Confirmation 2 Entry, 1-Candle Confirmation 2 Entry, or Pullback entry triggered previously

2. Baseline hasn't crossed since entry signal trigger

4. Confirmation 1 agrees

5. Baseline agrees

6. Confirmation 2 agrees

WhaleCrew BacktesterBacktesting indicators is easy , just add the following line of code to your script:

plot(longEntry ? 1 : shortEntry ? -1 : longTP ? 0.5 : shortTP ? -0.5 : 0, color=na, editable=false, title='Backtest')

These numbers are defined as constants in the backtester source-code.

After adding this indicator to your chart:

1. Open Settings

2. Select supported indicator to backtest

3. Select if you want to enter Longs and/or Shorts

4. Open the 'Strategy Tester' at the bottom to check the performance

Remember:

past performance is not indicative of future results

repainting indicators will create wrong/unrealistic results

Manual Backtest - Flat the ChartThis script is an utility tool for manual backtesting.

The main problem in backtesting a discretionary strategy is the bias of knowing the future result of the market, in this way all the market will be crushed into a flat line, this way you can avoid bias.

The way to use this indicator is easy and made by 4 step:

Step 1 : add to an asset you won't backtest and put the auto scale on

Step 2 : go to the asset you will backtest and scroll left until the date you want to start

Step 3 : use the replay function of tradingview (15 min chart won't go back more than 18 month)

Step 4: toggle off the indicator or remove from the chart (untill next asset to backtest)

That's not a complex indicator but is what you need to do a fair backtesting

TV signal for DCA backtestThis script allows you to backtest Trading View's "Technical Ratings" (Buy, Strong buy, Sell, Strong Sell) using Gavin's backtest script.

To use it add the backtest script to the chart together with this script and then from the back test settings connect the external indicator. You should select "TV Signal" as the source.

Backtesting works best on the 5m chart, but you can still change this script from its settings to higher timeframes.

Encoding

Buy is 1

Strong Buy is 2

Sell is -1

Strong Sell is -2

In the backtest script you can decide which rating you want to use for open deal and which one for close deal.

For example, if you were backtesting a long bot you could enter a long position when TV signal is Buy (1) and close the deal when TV signal is Sell (-1).

You have the full flexibility to decide which technical rating to use for your backtesting.

Enjoy!

*Auto Backtest & Optimize EngineFull-featured Engine for Automatic Backtesting and parameter optimization. Allows you to test millions of different combinations of stop-loss and take profit parameters, including on any connected indicators.

⭕️ Key Futures

Quickly identify the optimal parameters for your strategy.

Automatically generate and test thousands of parameter combinations.

A simple Genetic Algorithm for result selection.

Saves time on manual testing of multiple parameters.

Detailed analysis, sorting, filtering and statistics of results.

Detailed control panel with many tooltips.

Display of key metrics: Profit, Win Rate, etc..

Comprehensive Strategy Score calculation.

In-depth analysis of the performance of different types of stop-losses.

Possibility to use to calculate the best Stop-Take parameters for your position.

Ability to test your own functions and signals.

Customizable visualization of results.

Flexible Stop-Loss Settings:

• Auto ━ Allows you to test all types of Stop Losses at once(listed below).

• S.VOLATY ━ Static stop based on volatility (Fixed, ATR, STDEV).

• Trailing ━ Classic trailing stop following the price.

• Fast Trail ━ Accelerated trailing stop that reacts faster to price movements.

• Volatility ━ Dynamic stop based on volatility indicators.

• Chandelier ━ Stop based on price extremes.

• Activator ━ Dynamic stop based on SAR.

• MA ━ Stop based on moving averages (9 different types).

• SAR ━ Parabolic SAR (Stop and Reverse).

Advanced Take-Profit Options:

• R:R: Risk/Reward ━ sets TP based on SL size.

• T.VOLATY ━ Calculation based on volatility indicators (Fixed, ATR, STDEV).

Testing Modes:

• Stops ━ Cyclical stop-loss testing

• Pivot Point Example ━ Example of using pivot points

• External Example ━ Built-in example how test functions with different parameters

• External Signal ━ Using external signals

⭕️ Usage

━ First Steps:

When opening, select any point on the chart. It will not affect anything until you turn on Manual Start mode (more on this below).

The chart will immediately show the best results of the default Auto mode. You can switch Part's to try to find even better results in the table.

Now you can display any result from the table on the chart by entering its ID in the settings.

Repeat steps 3-4 until you determine which type of Stop Loss you like best. Then set it in the settings instead of Auto mode.

* Example: I flipped through 14 parts before I liked the first result and entered its ID so I could visually evaluate it on the chart.

Then select the stop loss type, choose it in place of Auto mode and repeat steps 3-4 or immediately follow the recommendations of the algorithm.

Now the Genetic Algorithm at the bottom right will prompt you to enter the Parameters you need to search for and select even better results.

Parameters must be entered All at once before they are updated. Enter recommendations strictly in fields with the same names.

Repeat steps 5-6 until there are approximately 10 Part's left or as you like. And after that, easily pour through the remaining Parts and select the best parameters.

━ Example of the finished result.

━ Example of use with Takes

You can also test at the same time along with Take Profit. In this example, I simply enabled Risk/Reward mode and immediately specified in the TP field Maximum RR, Minimum RR and Step. So in this example I can test (3-1) / 0.1 = 20 Takes of different sizes. There are additional tips in the settings.

━

* Soon you will start to understand how the system works and things will become much easier.

* If something doesn't work, just reset the engine settings and start over again.

* Use the tips I have left in the settings and on the Panel.

━ Details:

Sort ━ Sorting results by Score, Profit, Trades, etc..

Filter ━ Filtring results by Score, Profit, Trades, etc..

Trade Type ━ Ability to disable Long\Short but only from statistics.

BackWin ━ Backtest Window Number of Candle the script can test.

Manual Start ━ Enabling it will allow you to call a Stop from a selected point. which you selected when you started the engine.

* If you have a real open position then this mode can help to save good Stop\Take for it.

1 - 9 Сheckboxs ━ Allow you to disable any stop from Auto mode.

Ex Source - Allow you to test Stops/Takes from connected indicators.

Connection guide:

//@version=6

indicator("My script")

rsi = ta.rsi(close, 14)

buy = not na(rsi) and ta.crossover (rsi, 40) // OS = 40

sell = not na(rsi) and ta.crossunder(rsi, 60) // OB = 60

Signal = buy ? +1 : sell ? -1 : 0

plot(Signal, "🔌Connector🔌", display = display.none)

* Format the signal for your indicator in a similar style and then select it in Ex Source.

⭕️ How it Works

Hypothesis of Uniform Distribution of Rare Elements After Mixing.

'This hypothesis states that if an array of N elements contains K valid elements, then after mixing, these valid elements will be approximately uniformly distributed.'

'This means that in a random sample of k elements, the proportion of valid elements should closely match their proportion in the original array, with some random variation.'

'According to the central limit theorem, repeated sampling will result in an average count of valid elements following a normal distribution.'

'This supports the assumption that the valid elements are evenly spread across the array.'

'To test this hypothesis, we can conduct an experiment:'

'Create an array of 1,000,000 elements.'

'Select 1,000 random elements (1%) for validation.'

'Shuffle the array and divide it into groups of 1,000 elements.'

'If the hypothesis holds, each group should contain, on average, 1~ valid element, with minor variations.'

* I'd like to attach more details to My hypothesis but it won't be very relevant here. Since this is a whole separate topic, I will leave the minimum part for understanding the engine.

Practical Application

To apply this hypothesis, I needed a way to generate and thoroughly mix numerous possible combinations. Within Pine, generating over 100,000 combinations presents significant challenges, and storing millions of combinations requires excessive resources.

I developed an efficient mechanism that generates combinations in random order to address these limitations. While conventional methods often produce duplicates or require generating a complete list first, my approach guarantees that the first 10% of possible combinations are both unique and well-distributed. Based on my hypothesis, this sampling is sufficient to determine optimal testing parameters.

Most generators and randomizers fail to accommodate both my hypothesis and Pine's constraints. My solution utilizes a simple Linear Congruential Generator (LCG) for pseudo-randomization, enhanced with prime numbers to increase entropy during generation. I pre-generate the entire parameter range and then apply systematic mixing. This approach, combined with a hybrid combinatorial array-filling technique with linear distribution, delivers excellent generation quality.

My engine can efficiently generate and verify 300 unique combinations per batch. Based on the above, to determine optimal values, only 10-20 Parts need to be manually scrolled through to find the appropriate value or range, eliminating the need for exhaustive testing of millions of parameter combinations.

For the Score statistic I applied all the same, generated a range of Weights, distributed them randomly for each type of statistic to avoid manual distribution.

Score ━ based on Trade, Profit, WinRate, Profit Factor, Drawdown, Sharpe & Sortino & Omega & Calmar Ratio.

⭕️ Notes

For attentive users, a little tricks :)

To save time, switch parts every 3 seconds without waiting for it to load. After 10-20 parts, stop and wait for loading. If the pause is correct, you can switch between the rest of the parts without loading, as they will be cached. This used to work without having to wait for a pause, but now it does slower. This will save a lot of time if you are going to do a deeper backtest.

Sometimes you'll get the error “The scripts take too long to execute.”

For a quick fix you just need to switch the TF or Ticker back and forth and most likely everything will load.

The error appears because of problems on the side of the site because the engine is very heavy. It can also appear if you set too long a period for testing in BackWin or use a heavy indicator for testing.

Manual Start - Allow you to Start you Result from any point. Which in turn can help you choose a good stop-stick for your real position.

* It took me half a year from idea to current realization. This seems to be one of the few ways to build something automatic in backtest format and in this particular Pine environment. There are already better projects in other languages, and they are created much easier and faster because there are no limitations except for personal PC. If you see solutions to improve this system I would be glad if you share the code. At the moment I am tired and will continue him not soon.

Also You can use my previosly big Backtest project with more manual settings(updated soon)

Descriptive Backtesting Framework (DBF)As the name suggests, this is a backtesting framework made to offer full backtesting functionality to any custom indicator in a visually descriptive way.

Any trade taken will be very clear to visualize on the chart and the equity line will be updated live allowing us to use the REPLAY feature to view the strategy performing in real time.

Stops and Targets will also get draw on the chart with labels and tooltips and there will be a table on the top right corner displaying lots of descriptive metrics to measure your strategy's performance.

IF YOU DECIDE TO USE THIS FRAMEWORK, PLEASE READ **EVERYTHING** BELOW

HOW TO USE IT

Step 1 - Insert Your Strategy Indicators:

Inside this framework's code, right at the beginning, you will find a dedicated section where you can manually insert any set of indicators you desire.

Just replace the example code in there with your own strategy indicators.

Step 2 - Specify The Conditions To Take Trades:

After that, there will be another section where you need to specify your strategy's conditions to enter and exit trades.

When met, those conditions will fire the trading signals to the trading engine inside the framework.

If you don't wish to use some of the available signals, please just assign false to the signal.

DO NOT DELETE THE SIGNAL VARIABLES

Step 3 - Specify Entry/Exit Prices, Stops & Targets:

Finally you'll reach the last section where you'll be able to specify entry/exit prices as well as add stops and targets.

On most cases, it's easier and more reliable to just use the close price to enter and exit trades.

If you decide to use the open price instead, please remember to change step 2 so that trades are taken on the open price of the next candle and not the present one to avoid the look ahead bias.

Stops and targets can be set in any way you want.

Also, please don't forget to update the spread. If your broker uses commissions instead of spreads or a combination of both, you'll need to manually incorporate those costs in this step.

And that's it! That's all you have to do.

Below this section you'll now see a sign warning you about not making any changes to the code below.

From here on, the framework will take care of executing the trades and calculating the performance metrics for you and making sure all calculations are consistent.

VISUAL FEATURES:

Price candles get painted according to the current trade.

They will be blue during long trades, purple on shorts and white when no trade is on.

When the framework receives the signals to start or close a trade, it will display those signals as shapes on the upper and lower limits of the chart:

DIAMOND: represents a signal to open a trade, the trade direction is represented by the shape's color;

CROSS: means a stop loss was triggered;

FLAG: means a take profit was triggered;

CIRCLE: means an exit trade signal was fired;

Hovering the mouse over the trade labels will reveal:

Asset Quantity;

Entry/Exit Prices;

Stops & Targets;

Trade Profit;

Profit As Percentage Of Trade Volume;

**Please note that there's a limit as to how many labels can be drawn on the chart at once.**

If you which to see labels from the beginning of the chart, you'll probably need to use the replay feature.

PERFORMANCE TABLE:

The performance table displays several performance metrics to evaluate the strategy.

All the performance metrics here are calculated by the framework. It does not uses the oficial pine script strategy tester.

All metrics are calculated in real time. If using the replay feature, they will be updated up to the last played bar.

Here are the available metrics and their definition:

INITIAL EQUITY: the initial amount of money we had when the strategy started, obviously...;

CURRENT EQUITY: the amount of money we have now. If using the replay feature, it will show the current equity up to the last bar played. The number on it's right side shows how many times our equity has been multiplied from it's initial value;

TRADE COUNT: how many trades were taken;

WIN COUNT: how many of those trades were wins. The percentage at the right side is the strategy WIN RATE;

AVG GAIN PER TRADE: the average percentage gain per trade. Very small values can indicate a fragile strategy that can behave in unexpected ways under high volatility conditions;

AVG GAIN PER WIN: the average percentage gain of trades that were profitable;

AVG GAIN PER LOSS: the average percentage loss on trades that were not profitable;

EQUITY MAX DD: the maximum drawdown experienced by our equity during the entire strategy backtest;

TRADE MAX DD: the maximum drawdown experienced by our equity after one single trade;

AVG MONTHLY RETURN: the compound monthly return that our strategy was able to create during the backtested period;

AVG ANNUAL RETURN: this is the strategy's CAGR (compound annual growth rate);

ELAPSED MONTHS: number of months since the backtest started;

RISK/REWARD RATIO: shows how profitable the strategy is for the amount of risk it takes. Values above 1 are very good (and rare). This is calculated as follows: (Avg Annual Return) / mod(Equity Max DD). Where mod() is the same as math.abs();

AVAILABLE SETTINGS:

SPREAD: specify your broker's asset spread

ENABLE LONGS / SHORTS: you can keep both enable or chose to take trades in only one direction

MINIMUM BARS CLOSED: to avoid trading before indicators such as a slow moving average have had time to populate, you can manually set the number of bars to wait before allowing trades.

INITIAL EQUITY: you can specify your starting equity

EXPOSURE: is the percentage of equity you wish to risk per trade. When using stops, the strategy will automatically calculate your position size to match the exposure with the stop distance. If you are not using stops then your trade volume will be the percentage of equity specified here. 100 means you'll enter trades with all your equity and 200 means you'll use a 2x leverage.

MAX LEVERAGE ALLOWED: In some situations a short stop distance can create huge levels of leverage. If you want to limit leverage to a maximum value you can set it here.

SEVERAL PLOTTING OPTIONS: You'll be able to specify which of the framework visuals you wish to see drawn on the chart.

FRAMEWORK **LIMITATIONS**:

When stop and target are both triggered in the same candle, this framework isn't able to enter faster timeframes to check which one was triggered first, so it will take the pessimistic assumption and annul the take profit signal;

This framework doesn't support pyramiding;

This framework doesn't support both long and short positions to be active at the same time. So for example, if a short signal is received while a long trade is open, the framework will close the long trade and then open a short trade;

FINAL CONSIDERATIONS:

I've been using this framework for a good time and I find it's better to use and easier to analyze a strategy's performance then relying on the oficial pine script strategy tester. However, I CANNOT GUARANTEE IT TO BE BUG FREE.

**PLEASE PERFORM A MANUAL BACKTEST BEFORE USING ANY STRATEGY WITH REAL MONEY**

LuxAlgo - Backtester (OSC)The OSC Backtester is an innovative strategy script that allows users to create a wide variety of strategies using various unique oscillators.

By utilizing our 'Step' and 'Match' algorithms, users can create custom and complex strategy entries from each of the supported oscillators and included conditions, as well as any external sources, allowing users to create entries from a sequence of conditions and/or multiple matching conditions.

We included a complete alert system that will send a notification for each action taken by the strategy and we also allow users to set custom messages for each action taken by a strategy.

🔶 Features

🔹 Step & Match Algorithm

More complex entry rules can be created by using multiple conditions together, this is done thanks to the Step dropdown setting on the right of each condition.

The Step setting is directly related to the Step & Match algorithm and works in two ways:

When two or more conditions have the same step number, both conditions are evaluated. Used to test matching conditions.

When two or more conditions have different step numbers, each conditions will be evaluated in order, testing for the first step and switching to the next step once the previous one is true. When the final step is true the strategy will open a market order. Used to create sequence of conditions.

This operation is complementary, as you can create a sequence of conditions with one step consisting of two or more matching conditions as long as they have the same step number.

🔹 Fully Customizable Entries From Various Oscillators And Conditions

We allow the users to set entries using our unique HyperWave, Smart Money Flow, and their derived conditions as entries.

The Hyper Wave is a normalized adaptive oscillator aiming to reflect price trends without returning a high amount of noise.

The Smart Money Flow aims to detect trends based on market activity, by doing a comparative analysis between current volume and historical volume. A Smart Money Flow above 50 suggest market participants are bullish, else bearish. Derived from this oscillator we have Overflow indications, this indicator detects when market is overbought or oversold based on participants activity.

Other entries include proprietary reversal signals, real-time divergence detection, oscillator confluence (indicating how aligned each oscillator is), as well as entries using external sources.

🔹 Complete Alert System

Users can get alerted for any action executed by a strategy, from opening positions to closing them.

The message field in the Alert Messages setting section allows for the strategy to send a custom alert message depending on the action taken by the strategy, if no messages are set the strategy will send default messages.

🔶 Usage

Users can create a wide variety of strategies from this script, whether they are trend-following or contrarian traders.

Let's see a contrarian (revesal-based) strategy example using the following entry conditions:

Long: Hyperwave bullish divergence and oversold Hyperwave (lower than 20).

Short: Hyperwave bearish divergence and overbought Hyperwave (greater than 20).

We can also introduce take-profit and stop-loss exit conditions based on external indicators, allowing more control over exits in our strategy. For example:

Long: Hyperwave crossing over 50 while money flow is bearish.

Short: Hyperwave crossing under 50 while money flow is bullish.

Exit Long on a profit (long exit tp): Hyperwave crossing 80.

Exit Short on a profit (short exit tp): Hyperwave crossing 20.

While this strategy script can be used as a standalone, we recommend using other indicators creatively to assist with entries and exits as well as TP/SLs.

Our Step & Match algorithm can magnify interoperability, allowing for way more complete strategies through complex conditions, let's demonstrate this using the following entries:

Long: Any bullish reversal occurring after the price crosses over the lowest upper reversal zone of the Signals & Overlays™.

Short: Any bearish reversal occurring after the price crosses under the highest lower reversal zone of the Signals & Overlays™.

Long TP/SL: 5 ATR's away from the entry price.

Short TP/SL: 5 ATR's away from the entry price.

🔶 Strategy Properties (Important)

This script backtest is done on daily EURGBP, using the following backtesting properties:

Balance (default): 10 000 (default base currency)

Order Size: 10% of the equity

Comission: 3.4 pips (average spread for EURGBP)

Slippage: 3 tick

Stop Loss: 0.02 points away from entry price

We use these properties to ensure a realistic preview of the backtesting system, do note that default properties can be different for various reasons described below:

Order Size: 1 contract by default, this is to allow the strategy to run properly on most instruments such as futures.

Comission: Comission can vary depending on the market and instrument, there is no default value that might return realistic results.

We strongly recommend all users to ensure they adjust the Properties within the script settings to be in line with their accounts & trading platforms of choice to ensure results from the strategies built are realistic.

🔶 How To Access

You can see the Author's Instructions below to learn how to get access.

Strategy BackTest Display Statistics - TraderHalaiThis script was born out of my quest to be able to display strategy back test statistics on charts to allow for easier backtesting on devices that do not natively support backtest engine (such as mobile phones, when I am backtesting from away from my computer). There are already a few good ones on TradingView, but most / many are too complicated for my needs.

Found an excellent display backtest engine by 'The Art of Trading'. This script is a snippet of his hard work, with some very minor tweaks and changes. Much respect to the original author.

Full credit to the original author of this script. It can be found here: www.tradingview.com

I decided to modify the script by simplifying it down and make it easier to integrate into existing strategies, using simple copy and paste, by relying on existing tradingview strategy backtester inputs. I have also added 3 additional performance metrics:

- Max Run Up

- Average Win per trade

- Average Loss per trade

As this is a work in progress, I will look to add in more performance metrics in future, as I further develop this script.

Feel free to use this display panel in your scripts and strategies.

Thanks and enjoy :)

ETF Builder & Backtest System [TradeDots]Create, analyze, and monitor your own custom “ETF-like” portfolio directly on TradingView. This script merges up to 10 different assets with user-defined weightings into a single composite chart, allowing you to see how your personalized portfolio would have performed historically. It is an original tool designed to help traders and investors quickly gauge risk and return profiles without leaving the TradingView platform.

📝 HOW IT WORKS

1. Custom Portfolio Construction

Multiple Assets : Combine up to 10 different stocks, ETFs, cryptocurrencies, or other symbols.

User-Defined Weights : Allocate each asset a percentage weight (e.g., 15% in AAPL, 10% in MSFT, etc.).

Single Composite Value : The script calculates a weighted “ETF-style” price, effectively simulating a merged portfolio curve on your chart.

2. Performance Tracking & Return Analysis

Automatic History Capture : The indicator records each asset’s starting price when it first appears in your chosen date range.

Rolling Updates : As time progresses, all asset prices are continually evaluated and the portfolio value is updated in real time.

Buy & Hold Returns : See how each asset—and the overall portfolio—performed from the “start” date to the most recent bar.

Annualized Return : Automatically calculates CAGR (Compound Annual Growth Rate) to help visualize performance over varying timescales.

3. Table & Visual Output

Performance Table : A comprehensive table displays individual asset returns, annualized returns, and portfolio totals.

Normalized Chart Plot : The composite ETF value is scaled to 100 at the start date, making it easy to compare relative growth or decline.

Optional Time Filter : You can define a specific date range (Start/End Dates) to focus on a particular period or to limit historical data.

⚙️ KEY FEATURES

1. Flexible Asset Selection

Choose any symbols from multiple asset classes. The script will only run calculations when data is available—no need to worry about missing quotes.

2. Dynamic Table Reporting

Start Price for each asset

Percentage Weight in the portfolio

Total Return (%) and Annualized Return (%)

3. Simple Backtesting Logic

This script takes a straightforward Buy & Hold perspective. Once the start date is reached, the portfolio remains static until the end date, so you can quickly assess hypothetical growth.

4. Plot Customization

Toggle the main “ETF” plot on/off.

Alter the visual style for tables and text.

Adjust the time filter to limit or extend your performance measurement window.

🚀 HOW TO USE IT

1. Add the Script

Search for “ETF Builder & Backtest System ” in the Indicators & Strategies tab or manually add it to your chart after saving it in your Pine Editor.

2. Configure Inputs

Enable Time Filter : Choose whether to restrict the analysis to a particular date range.

Start & End Date : Define the period you want to measure performance over (e.g., from 2019-12-31 to 2025-01-01).

Assets & Weights : Enter each symbol and specify a percentage weight (up to 10 assets).

Display Options : Pick where you want the Table to appear and choose background/text colors.

3. Interpret the Table & Plots

Asset Rows : Each asset’s ticker, weighting, start price, and performance metrics.

ETF Total Row : Summarizes total weighting, composite starting value, and overall returns.

Normalized Plot : Tracks growth/decline of the combined portfolio, starting at 100 on the chart.

4. Refine Your Strategy

Compare how different weights or a new mix of assets would have performed over the same period.

Assess if certain assets contribute disproportionately to your returns or volatility.

Use the results to guide allocations in your real trading or paper trading accounts.

❗️LIMITATIONS

1. Buy & Hold Only

This script does not handle rebalancing or partial divestments. Once the portfolio starts, weights remain fixed throughout the chosen timeframe.

2. No Reinvestment Tracking

Dividends or other distributions are not factored into performance.

3. Data Availability

If historical data for a particular asset is unavailable on TradingView, related results may display as “N/A.”

4. Market Regimes & Volatility

Past performance does not guarantee similar future behavior. Markets can change rapidly, which may render historical backtests less predictive over time.

⚠️ RISK DISCLAIMER

Trading and investing carry significant risk and can result in financial loss. The “ETF Builder & Backtest System ” is provided for informational and educational purposes only. It does not constitute financial advice.

Always conduct your own research.

Use proper risk management and position sizing.

Past performance does not guarantee future results.

This script is an original creation by TradeDots, published under the Mozilla Public License 2.0.

Use this indicator as part of a broader trading or investment approach—consider fundamental and technical factors, overall market context, and personal risk tolerance. No trading tool can assure profits; exercise caution and responsibility in all financial decisions.

[MT] Strategy Backtest Template| Initial Release | | EN |

An update of my old script, this script is designed so that it can be used as a template for all those traders who want to save time when programming their strategy and backtesting it, having functions already programmed that in normal development would take you more time to program, with this template you can simply add your favorite indicator and thus be able to take advantage of all the functions that this template has.

🔴Stop Loss and 🟢Take Profit:

No need to mention that it is a Stop Loss and a Take Profit, within these functions we find the options of: fixed percentage (%), fixed price ($), ATR, especially for Stop Loss we find the Pivot Points, in addition to this, the price range between the entry and the Stop Loss can be converted into a trailing stop loss, instead, especially for the Take Profit we have an option to choose a 1:X ratio that complements very well with the Pivot Points.

📈Heikin Ashi Based Entries:

Heikin Ashi entries are trades that are calculated based on Heikin Ashi candles but their price is executed to Japanese candles, thus avoiding false results that occur in Heikin candlestick charts, this making in certain cases better results in strategies that are executed with this option compared to Japanese candlesticks.

📊Dashboard:

A more visual and organized way to see the results and necessary data produced by our strategy, among them we can see the dates between which our operations are made regardless if you have activated some time filter, usual data such as Profit, Win Rate, Profit factor are also displayed in this panel, additionally data such as the total number of operations, how many were gains and how many losses, the average profit and loss for each operation and finally the maximum profits and losses followed, which are data that will be very useful to us when we elaborate our strategies.

Feel free to use this template to program your own strategies, if you find errors or want to request a new feature let me know in the comments or through my social networks found in my tradingview profile.

| Update 1.1 | | EN |

➕Additions: '

Time sessions filter and days of the week filter added to the time filter section.

Option to add leverage to the strategy.

5 Moving Averages, RSI, Stochastic RSI, ADX, and Parabolic Sar have been added as indicators for the strategy.

You can choose from the 6 available indicators the way to trade, entry alert or entry filter.

Added the option of ATR for Take Profit.

Ticker information and timeframe are now displayed on the dashboard.

Added display customization and color customization of indicator plots.

Added customization of display and color plots of trades displayed on chart.

📝Changes:

Now when activating the time filter it is optional to add a start or end date and time, being able to only add a start date or only an end date.

Operation plots have been changed from plot() to line creation with line.new().

Indicator plots can now be controlled from the "plots" section.

Acceptable and deniable range of profit, winrate and profit factor can now be chosen from the "plots" section to be displayed on the dashboard.

Aesthetic changes in the section separations within the settings section and within the code itself.

The function that made the indicators give inputs based on heikin ashi candles has been changed, see the code for more information.

⚙️Fixes:

Dashboard label now projects correctly on all timeframes including custom timeframes.

Removed unnecessary lines and variables to take up less code space.

All code in general has been optimized to avoid the use of variables, unnecessary lines and avoid unnecessary calculations, freeing up space to declare more variables and be able to use fewer lines of code.

| Lanzamiento Inicial | | ES |

Una actualización de mi antiguo script, este script está diseñado para que pueda ser usado como una plantilla para todos aquellos traders que quieran ahorrar tiempo al programar su estrategia y hacer un backtesting de ella, teniendo funciones ya programadas que en el desarrollo normal te tomaría más tiempo programar, con esta plantilla puedes simplemente agregar tu indicador favorito y así poder aprovechar todas las funciones que tiene esta plantilla.

🔴Stop Loss y 🟢Take Profit:

No hace falta mencionar que es un Stop Loss y un Take Profit, dentro de estas funciones encontramos las opciones de: porcentaje fijo (%), precio fijo ($), ATR, en especial para Stop Loss encontramos los Pivot Points, adicionalmente a esto, el rango de precio entre la entrada y el Stop Loss se puede convertir en un trailing stop loss, en cambio, especialmente para el Take Profit tenemos una opción para elegir un ratio 1:X que se complementa muy bien con los Pivot Points.

📈Entradas Basadas en Heikin Ashi:

Las entradas Heikin Ashi son operaciones que son calculados en base a las velas Heikin Ashi pero su precio esta ejecutado a velas japonesas, evitando así́ los falsos resultados que se producen en graficas de velas Heikin, esto haciendo que en ciertos casos se obtengan mejores resultados en las estrategias que son ejecutadas con esta opción en comparación con las velas japonesas.

📊Panel de Control:

Una manera más visual y organizada de ver los resultados y datos necesarios producidos por nuestra estrategia, entre ellos podemos ver las fechas entre las que se hacen nuestras operaciones independientemente si se tiene activado algún filtro de tiempo, datos usuales como el Profit, Win Rate, Profit factor también son mostrados en este panel, adicionalmente se agregaron datos como el número total de operaciones, cuantos fueron ganancias y cuantos perdidas, el promedio de ganancias y pérdidas por cada operación y por ultimo las máximas ganancias y pérdidas seguidas, que son datos que nos serán muy útiles al elaborar nuestras estrategias.

Siéntete libre de usar esta plantilla para programar tus propias estrategias, si encuentras errores o quieres solicitar una nueva función házmelo saber en los comentarios o a través de mis redes sociales que se encuentran en mi perfil de tradingview.

| Actualización 1.1 | | ES |

➕Añadidos:

Filtro de sesiones de tiempo y filtro de días de la semana agregados al apartado de filtro de tiempo.

Opción para agregar apalancamiento a la estrategia.

5 Moving Averages, RSI, Stochastic RSI, ADX, y Parabolic Sar se han agregado como indicadores para la estrategia.

Puedes escoger entre los 6 indicadores disponibles la forma de operar, alerta de entrada o filtro de entrada.

Añadido la opción de ATR para Take Profit.

La información del ticker y la temporalidad ahora se muestran en el dashboard.

Añadido personalización de visualización y color de los plots de indicadores.

Añadido personalización de visualización y color de los plots de operaciones mostradas en grafica.

📝Cambios:

Ahora al activar el filtro de tiempo es opcional añadir una fecha y hora de inicio o fin, pudiendo únicamente agregar una fecha de inicio o solamente una fecha de fin.

Los plots de operaciones han cambiados de plot() a creación de líneas con line.new().

Los plots de indicadores ahora se pueden controlar desde el apartado "plots".

Ahora se puede elegir el rango aceptable y negable de profit, winrate y profit factor desde el apartado "plots" para mostrarse en el dashboard.

Cambios estéticos en las separaciones de secciones dentro del apartado de configuraciones y dentro del propio código.

Se ha cambiado la función que hacía que los indicadores dieran entradas en base a velas heikin ashi, mire el código para más información.

⚙️Arreglos:

El dashboard label ahora se proyecta correctamente en todas las temporalidades incluyendo las temporalidades personalizadas.

Se han eliminado líneas y variables innecesarias para ocupar menos espacio en el código.

Se ha optimizado todo el código en general para evitar el uso de variables, líneas innecesarias y evitar los cálculos innecesarios, liberando espacio para declarar más variables y poder utilizar menos líneas de código.

TTP Grid BacktesterThis pine script strategy allows to backtest Grid bots.

This initial version offers the following features:

- Set the top and bottom limits of the grid

- Plots the average position price, realised and unrealised profits

- Set the value to invest

- This script is a strategy so you can check each individual buy/sell, stats and all included with strategies

What does it do:

- Depending where is located the initial close price relative to the grid (above, below, inside) it will buy for as many levels are above the price.

- It will disable a level that recently filled an order (in the way grids bot do)

- When the grid starts it will disable the closest grid level

- It places limit orders in the active levels and many levels can be filled in a single candle

- You can activate recalculate on each order filled, which will allow to fill further needed orders if the price swings up and down crossing multiple times multiple grid levels but I have found that doing this can compromise the accuracy of the price used on those levels (there are minor gaps between the filled price and the original level price)

How to use it:

- When you add this strategy to the chart you will be asked to select the top and bottom limits of the grid

- Notice you can always select the strategy in the chart and drag and drop the limits to adjust the grid

- Once the grid is in place, you can use either lower chart timeframes for higher accuracy of the stats, or higher timeframes if you want to privilege longer periods of testing

How to set the correct "initial capital"

In order to prevent getting wrong stats you need to make sure you are using the correct initial capital. If you put less than what you are actually using your results will be over inflated. If you set an initial capital below what the bot requires, your results will be smaller than they should.

- If you want to use exactly 100% of the capital for the grid use then first select what amount per level you want to use. Set this value in the settings of the indicator (if you are trading BTCUSD pair, how much BTC you want to use per level, 0.01 for example).

- Once you have set this value, then open the TradingView "Data Window" to be able to visualise the calculation of cash required to run the grid that the strategy is giving you. In our example with BTCUSD this value will be given in USD.

- Enter this amount in the "Properties" tab, "Initial Capital". If you enter the exact amount you will be using all for the grid usage.

- The grid first action will be to buy 0.01 for each level that is above the current price in the first candle of the chart. If there are no levels above it won't do any initial investment.

- The rest of the cash will be use to buy levels below if the price goes to the lower range of the grid later

Intention of this script

I built this script to help me understand better how grid bots work.

Understanding the flow of realised vs unrealised profits in a grid can help me understand why sometimes even if you are in red on unrealised profits, you can still compensate with realised profits and many other tricky scenarios with grids.

Sometimes I'm running a grid bot and would like to simulate how much better (or worst) it would have been to run it using different limits.

Future work and ideas

Initially I'm focusing on confirming that the grid behaves correctly and that the stats are as accurate as possible.

That is the first priority.

Once I feel more confident with the accuracy I will consider adding some of the following ideas (not in any particular order):

- Table with stats including: price of each level, times the level filled an order, times it was use for selling/buying, etc. Time it took to become in realised profit. Comparison against profits from buy & hold.

- Trailing TP/SL

- Entry/exit price

- Trading time window: only trade between the specified dates/times

- Alerts

Zendog Backtest-DCA-Bot-3commasHi everyone,

This is a strategy that serves as a basic Backtester for 3commas DCA bots.

You can plugin your own studies into the Backtester, play around with their parameters as well with the DCA parameters and see how they can provide best result on historical data.

Features:

- Meaningful statistics that actually group orders under the same deal.

(base order + safety orders are the same deal, but Tradingview Strategy Tester shows them as separate trades)

See how many safety orders were used for each deal.

- Deal start condition: built in RSI-7 or external indicator

(main purpose of this strategy is to connect your own studies, so using external indicator is recommended)

- Base order and safety orders configs similar to 3commas