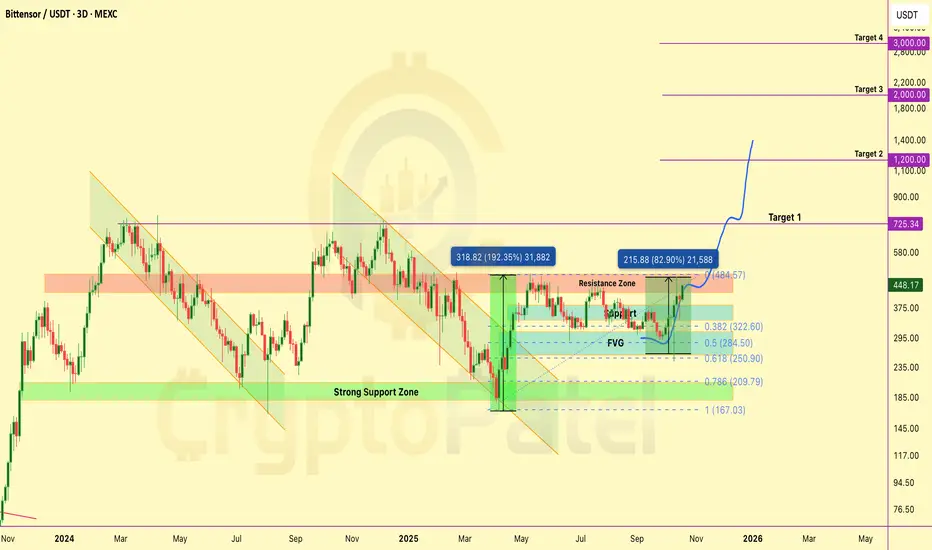

SCHAEFFLER Price Action 2 set upsSchaeffler India traded positively on October 21, 2025, closing near ₹3,930 after rising around 1.4% intraday. The day’s range was between ₹3,875 and ₹3,949, reflecting moderate volatility and a short-term recovery from recent consolidation near ₹3,850. The stock’s market capitalization stands around ₹61,300 crore, with a PE ratio close to 59.7 and a PB ratio near 11.3, indicating sustained valuation at a premium relative to the broader market.

Technically, Schaeffler has been moving in a neutral-to-bullish pattern. The RSI sits around 50–55, suggesting balanced momentum without overbought pressure. MACD remains slightly negative but flattening near the signal line, hinting that selling momentum is easing. Key support lies around ₹3,850 and ₹3,780, while resistance is seen at ₹3,980–₹4,050. A decisive breakout above ₹4,050 may reestablish bullish momentum toward ₹4,150–₹4,200.

Overall, the short-term outlook is mildly positive with improving stability in price structure. Sustaining above ₹3,900 will be crucial to continue upward momentum, while any dip below ₹3,850 could invite profit-taking or retesting of deeper supports around ₹3,750. Medium-term investors may await a clearer breakout above ₹4,050 before expecting stronger trend continuation.

Bullishsetup

GSLSU: Trend Reversal Signals The stock of GSLSU has been in a sustained downtrend since May, revisiting its discount zone multiple times. However, recent price action suggests a possible shift in sentiment. On Friday, October 17, the daily chart printed an inverted hammer candlestick, a pattern often interpreted by technical analysts as a potential bullish reversal signal—especially when supported by volume and other indicators.

The inverted hammer on the daily timeframe may indicate buying interest at lower levels. This pattern gains significance when it appears after a prolonged downtrend and is accompanied by increased volume. The bullish signal is further supported by a rise in trading volume and a daily close above the 20-day, 50-day, and 100-day EMAs, suggesting short-term strength and potential trend reversal.

In the most recent trading session, the stock found support at the 100-day EMA and rebounded, reinforcing the validity of this level as a short-term base. The RSI has moved above 65, indicating increasing bullish momentum. This level is often seen as a sign of strengthening trend, though not yet in overbought territory.

If the stock sustains its upward movement, the next potential resistance level may be around ₹136 , based on previous price action. The discount zone near ₹84 may serve as a key support level. Traders often monitor such zones for invalidation of bullish setups or potential re-entry points.

Disclaimer: This analysis is intended for educational and informational purposes only. It does not constitute investment advice or a recommendation to buy, sell, or hold any financial instrument. Market participants should conduct their own research and consult with a licensed financial advisor before making any investment decisions.

JkTyre Inverted Head & Shoulder PatternHi All…

Greetings!

Today I’m sharing with you JkTyre Daily Chart. Yesterday there has been a good break out in the stock. The stock has made a Inverted Head & Shoulder Pattern and has crossed its Neckline. I think it would a good time to invest in the stock. Hoping for the stock to reach the TGT’s of 420 448 478.

In the coming time I think it should give good returns.

Thanking You

Important Things

1. This is only for educational purposes only.

2. Never over trade.

3. Always keep Stop Loss.

4. Trade in limited quantity.

5. Taking a small loss is better than wiping up your whole capital.

I hope you found this idea helpful.

Please like and comment.

Share with Your Friends.

Keep Learning,

Happy & Safe Trading

Disclaimer – These ideas shared by me to all are my personal analysis / views. I'm not a SEBI registered technical analyst.

FORCEMOT Price Action PyramiddingForce Motors Ltd closed at ₹17,565 on October 17, 2025, gaining about 5.67% over the previous day amid strong volume and broad sector momentum. The stock traded between a high of ₹17,830 and a low of ₹16,624 during the session. This rise extends a rebound from mid-October levels after multiple sessions of consolidation near ₹16,000.

The near-term structure appears bullish, with momentum indicators showing strength; RSI has climbed above the neutral 50 mark, reflecting renewed buyer interest. The next resistance levels are positioned around ₹17,950–₹18,200, while immediate support lies at ₹17,000 followed by ₹16,500. Sustained closes above ₹18,200 could lead to further upside toward ₹18,800–₹19,000.

Fundamentally, Force Motors maintains a market capitalization of about ₹23,100 crore with a trailing P/E around 26.7 and P/B near 7.0, implying continued valuation expansion supported by strong earnings growth. The broader uptrend from late August lows remains intact, and short-term dips toward support zones may attract buying interest if overall market sentiment stays favorable.

NIFTY Price Action for long term set upThe Nifty 50 closed at 25,709.85 on October 19, 2025, gaining about 124.55 points or 0.49% in the last trading session. The index opened at 25,546.85, dipped to a low of 25,508.60, and recovered to touch an intraday high of 25,781.50 before closing near the upper end of the range. Market momentum was supported by strong performances from Asian Paints, Mahindra & Mahindra, and Bharti Airtel, while IT counters like Infosys and HCL Tech lagged.

In terms of technical structure, the immediate support zone lies near 25,500–25,550, while resistance is seen around 25,780–25,900. A sustained close above 25,900 may open the door toward 26,000–26,050 in the short term, whereas a break below 25,500 could trigger profit-booking down to 25,350.

The overall market breadth remains moderately positive, with sectors like banking, auto, and FMCG continuing to lead. The medium-term structure remains bullish as long as Nifty sustains above its 20-day moving average (~25,400). Traders are advised to maintain a positive bias, buying on dips near support zones while keeping trailing stops below 25,450.

$TAO: +80% IN 14 DAYS - INSTITUTIONAL ACCUMULATION PLAYGETTEX:TAO : +80% IN 14 DAYS - INSTITUTIONAL ACCUMULATION PLAY

Performance Update:

Entry execution: +80% unrealized gains

Institutional bid confirmed (Grayscale allocation)

Position Framework:

Entry Zones:

Primary: $180-$200 ✅

Secondary: $250-$300 ✅

Profit Targets: → $750 → $1,200 → $2,000 (6.6x → $3,000 (10x)

Technical Structure:

▶️ Chart formation: Bullish continuation pattern

▶️ Dip behavior: 30-40% retracements absorbed by institutional buying

▶️ Capital flow: Grayscale strategic allocation confirms smart money positioning

Long-term Thesis:

▶️ Every correction = accumulation opportunity

▶️ Strong hands buying weakness = supply compression

▶️ Institutional backing + technical strength = asymmetric upside

Volatility is the entry mechanism, not the exit signal.

NFA & DYOR

HDFC Bank cmp 1002.55 by Daily and Weekly Chart viewHDFC Bank cmp 1002.55 by Daily and Weekly Chart view

- Darvas Box Setup : Stock has been trading within price range 940 to ATH 1018.85 since mid of April 2025

- Stock chart has made Bullish Rounding Bottoms on both timeframes providing a technically logical upside target of +/- 1100 in the near future

Nifty Index spot 25709.85 by Weekly Chart viewNifty Index spot 25709.85 by Weekly Chart view

- Support Zone 25235 to 25535 Price Band

- Resistance Zone 26025 to ATH 26277.35 Price Band

- Crystal Clear Bullish Cup & Handle formed around Support Zone

- Lets hope for the best to happen based on this Nifty 50 Index Chart setup

- Sharing this beautiful Nifty Index Chart setup, courtesy by a curious Co-Learners observation 😊👍🏽🤞🏽

CRISIL Price actionCRISIL Limited traded mildly negative on October 18, 2025, closing near ₹4,695 after slipping about 0.7% intraday from an open around ₹4,770. The day’s range was between ₹4,694 and ₹4,781, maintaining consolidation below its recent resistance zone near ₹4,800. The stock’s 52-week range stands between ₹3,894 and ₹6,955, showing it remains in a mid-range retracement from its highs earlier in the year.

The current trailing 12-month EPS is approximately ₹99.3, giving a P/E ratio near 47, which aligns with its longer-term valuation band. The 50-day moving average (~₹4,965) and 200-day MA (~₹5,115) remain above current levels, indicating medium-term bearish momentum. Volumes were subdued, suggesting a lack of strong directional conviction.

Overall, CRISIL’s short-term trend is sideways-to-weak, facing resistance around ₹4,780–₹4,820 and finding interim support near ₹4,670 followed by ₹4,600. Sustained closes above ₹4,820 could revive buying momentum, while a break below ₹4,600 may invite further correction toward ₹4,450. The technical bias remains neutral until there’s a decisive move outside this consolidation band.

WESTLIFE Price Action Investing set upWestlife Foodworld traded in a downtrend as of October 18, 2025. The closing price was around ₹600, after an intraday range between ₹611.65 and ₹588.05. The broader trend over the last month has been negative, with the stock down about 13% in the last 30 days and nearly 31% off its yearly high of ₹898. Short-term support is near ₹588 and resistance is around ₹645.

The daily average traded price was approximately ₹600.59 and volumes were healthy at over 7 lakh shares. The stock is trading well below its 50-day moving average of ₹707.82, reinforcing the bearish short-term sentiment. Over recent weeks, continued selling pressure and weak technical momentum have prevailed, with no reversal signals as yet.

Technically, as long as the price stays below ₹645–₹650, the near-term outlook remains weak. Sustained closes above ₹650 could trigger a short-covering move, while breach of ₹588 may accelerate downside. Medium-term investors should watch for trend stabilization and base-building above the recent lows before any fresh entry.

RAMAPHO Price Action Rama Phosphates Ltd (RAMAPHO) closed at ₹168.05 on October 17, 2025, down 4% for the day, with a market cap of about ₹595 crore. The stock has seen a 52-week high of ₹188.90 (October 2025) and a low of ₹80.85 (March 2025), maintaining high volatility with a 20% daily price band set by the exchange.

Recent trading volumes remain strong, with 380,240 shares traded and a value of ₹6.39 crore on the latest trading day. The September 2025 quarter results showed net sales of ₹245.93 crore and a net profit of ₹17.28 crore, translating to an EPS of 4.88, indicating continued operational strength.

Technically, RAMAPHO has corrected from recent all-time highs but is backed by strong fundamentals—a TTM P/E of 14.09, P/B of 1.64, and a return on equity (ROE) of 4.72%. Comparisons with sector peers suggest the stock remains attractively valued relative to its earnings and book value, and optimism holds among some market watchers for medium-term upside toward the ₹500 level if earnings growth sustains.

Dividend activity and bulk deals in recent weeks have contributed to price swings, and investors should watch for ex-dividend dates and upcoming financial announcements for additional momentum triggers.

Bank Nifty spot 57713.35 by the Daily Chart view- Weekly updateBank Nifty spot 57713.35 by the Daily Chart view- Weekly update

- Bank Nifty created a New Lifetime High Milestone touching 57830.20

- Resistance Zone 56950 to 57350 then ATH 57628.40 for Bank Nifty

- Falling Resistance Trendline Breakout seems to be well sustained for now

- Rising Support Channel stood ground and providing steady positive support

- Current Support Zone 56950 to 57350 for Bank Nifty was earlier the Resistance Zone

- Bullish Rising W pattern done and has been well sustained by current trending momentum

- Bullish Rounding Bottom formed by Support Zone neckline inclusive of W pattern actively effective

Delta Corp | Support Zone Rebound | Long term analysisThis chart presents a technical study of Delta Corp Ltd. focusing on the historical price behavior around a strong support zone near ₹78 and the potential for a rebound toward the long-term descending trendline.

🔍 Overview :

Support Zone Identification: The ₹78–₹79 level has acted as a multi-year horizontal support, with multiple past price reactions and bounces from this region.

Trendline Resistance: A long-term downward sloping trendline from the 2021 peak serves as a key resistance. Historically, price has respected this line, making it a crucial level to monitor for any rebound attempt.

Indicators Used:

RSI (Relative Strength Index) shows the stock is currently in the oversold zone (<40). Past oversold readings near this support level have led to bullish reversals.

MACD currently shows bearish momentum but is approaching a zone where reversals have previously occurred.

Volume remains modest, but any increase near support may indicate accumulation.

📈 Trade Study Hypothesis:

If the support holds, the price may potentially rebound toward the trendline (currently near the ₹110–₹120 range), offering a medium-term technical play. A strong bullish signal would be a breakout above the trendline with volume confirmation.

⚠️ Note:

This idea is intended purely for educational and analytical purposes. It is not a recommendation to buy, sell, or hold any security. Always perform your own due diligence or consult a financial advisor before making investment decisions.

Data Patterns cmp 2825 by Daily Chart viewData Patterns cmp 2825 by Daily Chart view

* Support Zone 2585 to 2685 Price Band

* Resistance Zone 2935 to 3065 Price Band

* Stock has made a near tight and contracting VCP pattern

* Falling Resistance Trendline Breakout in the making process

* Darvas Box pattern with price trending between 2375 to 2935

* Bullish Rounding Bottom formed by the Resistance Zone neckline

* Volumes spiking intermittently by good numbers over past few weeks

MSTCLTD Price ActionMSTC Limited (MSTCLTD) is currently trading in the ₹511–₹544 range, having closed around ₹543 on October 16, 2025. The stock recently rebounded over 5% within two sessions after experiencing a multi-day decline. Typical intraday volatility fluctuates between 2% and 3%.

Short-term technical indicators are mixed, with daily moving averages showing mild bearishness, while weekly momentum indicators are turning slightly bullish. On a monthly basis, trend signals remain bearish and Bollinger Bands suggest mild negative pressure over broader timeframes. Key support is noted near ₹540, immediate resistance is around ₹548, and there is major volume support at approximately ₹540.5. If the price breaks below ₹518, it may invite further declines; conversely, moving above ₹548–₹551 could enable a rally toward ₹560 or higher.

Fundamentally, MSTC is a small-cap company with a market capitalization just under ₹3,850 crore. Latest financials show flat sales and subdued long-term growth, though multi-year returns have outperformed benchmark indices over three and five years. Current share price trades at a substantial premium to its estimated intrinsic value, resulting in a stretched valuation compared to historical averages. The company maintains consistent dividend payouts, with the latest declared at ₹4.5 per share in April 2025.

Overall, MSTCLTD is showing short-term optimism due to a price rebound, but technical setups and high valuations suggest caution. Sustained upward movement will depend on fundamental improvement and supportive broader market conditions.

BTC SWING PLAY LONGChart Overview and Data

• Asset: BITCOIN/TETHERUS PERPETUAL CONTRACT.

• Time Frame: The chart shows data up to "16 Oct" (likely the date the screenshot was taken). The primary candles visible span from approximately June to October of the current year, with the x-axis extending into 2026, suggesting a daily (1D) or weekly (WEEK) candlestick view, though the top-left corner indicates "1D - WEEK", which might mean the current view is Daily (1D) within a larger Weekly (WEEK) analysis context.

• Price: The current price is approximately $107,705.3, and the asset is down $3,007.6 (-2.72%) for the period shown.

• Trading Action: There are prominent SELL and BUY buttons at the top left, with current bid/ask prices of $107,691.3 (SELL) and $107,691.4 (BUY).

Technical Analysis Elements

Candlestick Pattern

• The chart uses candlesticks to represent price action over time.

• The recent price action (around August to October) shows a period of consolidation or a slight uptrend that has recently seen a significant drop, as indicated by the large red candlestick currently forming (the one far to the right).

Indicators and Lines

• Moving Averages: Several moving average lines (blue and purple, and possibly a thinner red line) are overlaid on the candlesticks, typically used to identify trend direction.

• Support and Resistance:

• Support Zones (Red Boxes/Lines): Several horizontal red lines and a large red-shaded area beneath the current price action indicate potential support levels where traders expect buying interest to emerge. Key price points marked by red lines are around $106,973, $103,204, $101,297, and the "Low" at $98,125.2. Further support is indicated by the lowest red line at $89,076.1.

• Resistance/Target Zone (Yellow/Green Box): A prominent yellow horizontal line at $126,220.2 (labeled "High") acts as a significant resistance level or a potential upside target. The large green-shaded area above the current price, extending up to $161,047.0, appears to represent a profit target or a long-term trading objective for a potential long position.

Trade Setup Indication

• The chart appears to be illustrating a potential short trade setup, or a breakdown scenario, given:

• The large red-shaded area below the current price, which could be a projected target zone for a short position.

• The significant price drop in the last candle, breaking below recent support.

• Small arrows and boxes near the consolidation area (around July/August) also suggest previous or ongoing trade indications.

Axis and Additional Information

• Y-Axis: Represents the price of BTCUSDT, ranging from approximately $84,800 up to $161,047.

• X-Axis: Represents time, spanning from approximately July to April 2026.

• Volume: A smaller chart pane at the bottom shows volume data, represented by red and green vertical bars, which helps gauge the strength behind price movements.

#CARRARO - Large Base BreakOut Script: CARRARO

Key highlights: 💡⚡

📈 VCP BreakOut in Daily Time Frame

📈 Volume spike during Breakout

📈 Large Base BreakOut

📈 MACD Bounce

📈 Can go for a swing trade

BUY ONLY ABOVE 514 DCB

⏱️ C.M.P 📑💰- 507

🟢 Target 🎯🏆 – 24%

⚠️ Stoploss ☠️🚫 – 12%

⚠️ Important: Market conditions are Okish, Position size 50% per Trade. Protect Capital Always

⚠️ Important: Always Exit the trade before any Event.

⚠️ Important: Always maintain your Risk:Reward Ratio as 1:2, with this RR, you only need a 33% win rate to Breakeven.

✅Like and follow to never miss a new idea!✅

Disclaimer: I am not SEBI Registered Advisor. My posts are purely for training and educational purposes.

Eat🍜 Sleep😴 TradingView📈 Repeat 🔁

Observing Key Structural Patterns in Manaksia Coated MetalsThe daily chart of Manaksia Coated Metals & Industries Ltd (NSE) displays a confluence of notable technical formations. There is a clearly defined demand zone (highlighted in green) that has provided support for multiple sessions, as well as a supply area (marked at the upper region), signifying previous resistance.

A visually tight Volatility Contraction Pattern (VCP) is present, where price swings narrow progressively, indicating potential accumulation and increasing trader interest. The chart also reveals an inverted head and shoulders pattern, depicted using blue and red lines, which is often recognized as a classic reversal formation in technical analysis.

No attempt is made to forecast price movement; the Chart purely reflects observed market structure and patterns.

Disclaimer

This post is for educational and observational purposes only. It does not constitute financial advice or a trading recommendation. Always conduct your own research and consult a certified financial advisor before making investment decisions.

ACE Price Action with probable 18R trade set up- Current Price: Around ₹1,081 as of October 2025.

- Market Capitalization: Approximately ₹12,870 Crores.

- 52-week Range: The stock traded between ₹917 and ₹1,600 in the past year.

- PE Ratio: Roughly 31, indicating moderate to high valuation relative to earnings.

- EPS: Around ₹34.4 (TTM).

- Price-to-Book Ratio: About 8, suggesting a premium valuation relative to its book value.

- Dividend Yield: Low, approximately 0.19%.

- Revenue and Profit: Latest annual revenue near ₹3,245 Crores and net profit around ₹423 Crores.

- Price Trend: The stock has faced some downside pressure recently with a 19% decline over the last year but historical performance showing strong growth over 3-5 years.

- Volatility: The stock is moderately volatile, about 3.2 times more than the Nifty index.

- Sector: ACE operates in the heavy machinery and industrial equipment sector, showing good profitability and efficiency metrics with consistent earnings growth.

Overall, ACE trades at a premium valuation reflecting growth expectations but recent price corrections indicate some caution in the market. The company shows good fundamentals with strong earnings growth potential balanced against sector cyclicality and market volatility.

VIMTALABS: Probable pyramid entries

- Current Price: Around ₹715 as of early October 2025, with daily price fluctuations between approximately ₹700 and ₹723.

- 52-week Range: The stock has traded from a low near ₹270 to a high around ₹903, showing strong growth over the past year.

- Market Capitalization: About ₹3,180 Crores.

- Valuation: PE ratio stands near 45, indicating a moderately high valuation relative to earnings.

- Earnings: EPS is about ₹15.9.

- Moving Averages: The 50-day average price is roughly ₹719, and the 200-day average is near ₹545, indicating medium-term momentum in an uptrend.

- Dividend Yield: Very low at around 0.14%, consistent with growth-oriented companies.

- Volume: Recent trading volumes average about 60 lakh shares daily, indicating good liquidity.

- Price Trend: The stock has experienced some volatility but sustained gains overall, with occasional pullbacks and rebounds, reflecting investor confidence in the company’s niche testing and laboratory services sector.

- The stock price structure indicates a bullish phase supported by improving fundamentals and positive market sentiment.

Overall, Vimta Labs shows strong upward price momentum with a solid growth profile, trading at a premium that reflects optimism about its expanding testing services business.

HERITGFOOD Re-entry set upHeritage Foods Limited (HERITGFOOD)

- Current Price: Approximately ₹496 as of mid-October 2025, with a day range between ₹485.7 and ₹497.7.

- 52-week Range: The stock has traded between ₹355.55 (low) and ₹658 (high) in the past year.

- Market Capitalization: About ₹4,607 Crores.

- Valuation: PE ratio stands around 27, indicating moderate valuation given its dairy sector positioning.

- Earnings: EPS of about ₹18.34.

- Moving Averages: The 50-day average price is approximately ₹483, and the 200-day average is near ₹443, showing a recent upward trend with solid support.

- Dividend Yield: Roughly 0.5%, reflecting modest income for shareholders.

- Volume: Daily traded volumes average around 16,000 shares.

- Performance Trends: Over recent years, the company has grown sales significantly, with a healthy profit recovery and improving operating margins. The stock price has demonstrated a mid-term rising trend with potential upsides based on recent positive momentum.

- Market Sentiment: Moderate volatility with periodic volume increases correlating with price advances.

Overall, Heritage Foods exhibits stable financials with steady profitability and moderate valuation in the food processing sector, trading near its short-term highs with a cautiously optimistic outlook for further gains.

MAHSCOOTER Price ActionAs of August 29, 2025, Maharashtra Scooters Limited is trading around ₹15,722, having posted a gain of nearly 5.5% over the past month and 18.5% in three months. The stock has maintained a strong uptrend for over a year, nearly doubling from its 52-week low of ₹8,822 to a high of ₹16,315 during this period. Notably, its market capitalization is about ₹17,968 crore, ranking it highly in the holding company segment.

Technically, the price momentum is positive, trading close to resistance levels near ₹16,000. The short-term moving averages show mild volatility, but long-term signals remain bullish. Despite a very high price-to-earnings ratio above 73, investor interest is supported by consistent profitability, strong control over operating costs, and robust dividend payouts.

Financially, March quarter results reflect steady net sales growth with improved margins. The company continues to benefit from its stake in group entities and maintains a solid cash position with minimal debt. Although growth is modest, valuation remains expensive—a sign that further gains may be limited unless fundamentals accelerate or sector sentiment grows even more bullish. Risk levels are relatively low with support seen around ₹14,340, and the stock remains a hold for existing investors while aggressive new buying may need fresh earnings triggers.

ADANIPORTS Pice Action- The stock is trading around ₹1,438 as of mid-October 2025, with a day range from approximately ₹1,396 to ₹1,442.

- On a 52-week basis, the stock fluctuated between a low of about ₹995 and a high near ₹1,494, currently trading closer to its upper range.

- Market capitalization is around ₹3.1 lakh Crores, making it one of the largest port infrastructure companies in India.

- The PE ratio is about 27.5, reflecting a moderate valuation for a growing infrastructure sector leader.

- Book value per share is about ₹288, so the stock trades at approximately 5 times book value.

- Dividend yield is low, near 0.5%, consistent with reinvestment into growth.

- Recent quarterly results showed a 6.5% rise in net profit and a strong 31% increase in revenue year over year.

- The stock has demonstrated steady sales and profit growth over the past five years with roughly 23% CAGR in profits.

- Return on capital employed (ROCE) is approximately 13.8%, with return on equity (ROE) close to 18.8%, signaling efficient use of capital.

- The stock has shown volatility with daily price swings around 2%, reflecting sensitivity to macroeconomic factors and sector developments.

Overall, ADANIPORTS remains a strong performer in the infrastructure sector with solid fundamentals, consistent growth, and trading at a fair valuation reflecting its leadership in port and logistics services.