What a professional trader think. ?For every trade we have a reason, when the trade works, we naturally think our reason was right but here is a catch, there is no way to determine the intentions of all traders. Yet the typical trader executes his methodology as if he is being told what those intentions are the professionals does not. Disconnect any reason from the results of a trade because it is impossible to get an exact reason why the trade worked or failed. Many will disagree with me on this but believe me there are traders (Mota Bhais) even a single order from them can drag a shooting price down back to floor or even hell, and they to do it occasionally. Just see the past charts you will get what I am trying to say.

Prices are random guys, yes believe me or not it applies to every trade you take.

Let me ask you a question.

What trading skills required to experience a winning trade.?

- Do you need an edge.?

- Do you need a plan.?

- Do you need the discipline to execute the plan.?

- Do you need a good reason to enter a trade.?

Answer: Nothing just a click of your mouse, yes that's it.

but what if you want it to make your consistent source of income.?

Now here comes the difference only few traders get those correct belief system which keep them above others.

Pro trader belief

1) On a random outcome, I do not have to know what is going to happen next.

2) There is a random distribution between wins and losses.

3) There is no point to find a reason why price movement happened, it is the task of media let them take care of that.

4) There is no connection of my last trade to the current one, so it is very foolish to trade for loss recovery. There is nothing like loss recovery, every trade is unique.

5) On a particular trade I can fail or win but I have to think with a large number of trades, on overall profitability, over a long term.

6) My work is to execute the plan with full efficiency rest is not in my hand.

7) I do not predict price move it is not my task I focus on process.

Nobody wants to Chang the way they think. I am also not telling you to make a v curve you just need to adjust something within, and everything get sorted by itself.

Thanks for reading this out.

Community ideas

123 Reversal Bearish Pattern TradingSetup

The 123-chart pattern is a three-wave formation, where every move reaches a pivot point. This is where the name of the pattern comes from, the 1-2-3 pivot points.

The structure of 123 chart pattern

The pattern appears after three price movements, which form three pivot points and a confirmation level.

Pivot point 1.

This is a turning point that the price formed during the trend. If a price breaks the previous trendline after it formed pivot point 1, the pattern will be more reliable.

Pivot point 2.

The next turning point is very likely to form outside of the previous trendline or channel. This is a good indication that the trend might be ready to end and reverse.

Pivot point 3.

Pivot point 3 is crucial for 123 reversal chart patterns. The point must not exceed the pivot point 1 (in the worst case it might be on the same level) for the pattern to be valid.

Confirmation level

The confirmation level is our entry point in the market. It is located at the same level as pivot point 2. When price breaks through this level open the trade.

Target level

To set the target trader needs to connect 1 and 3 pivot points with a line. The size of your 123 pattern equals the vertical distance between Line 2 (which is a horizontal line at the level of 2 pivot point) and the midpoint of Line 1.

123 chart pattern stop loss setup

It is highly important to use stop loss when trading the 123 chart pattern. The stop loss should be set under pivot point 3 in the bullish trend reversal, and above in the bearish one. In the condition of high market volatility, the price might get pushed beyond the 2 pivot point for a while. That’s why it will be a good idea to set stop-loss slightly beyond the 3 pivot point, as this will prevent stop loss from being activated.

123 Reversal Pattern Trading23 reversal setup is a basic on-chart formation, that warns about upcoming trend reversal.

Setup

The 123-chart pattern is a three-wave formation, where every move reaches a pivot point. This is where the name of the pattern comes from, the 1-2-3 pivot points.

123 pattern works in both directions. In the first case, a bullish trend turns into a bearish one. And the second picture presents the opposite, a bearish trend turns into a bullish one.

The structure of 123 chart pattern

The pattern appears after three price movements, which form three pivot points and a confirmation level.

Pivot point 1.

This is a turning point that the price formed during the trend. If a price breaks the previous trendline after it formed pivot point 1, the pattern will be more reliable.

Pivot point 2.

The next turning point is very likely to form outside of the previous trendline or channel. This is a good indication that the trend might be ready to end and reverse.

Pivot point 3.

Pivot point 3 is crucial for 123 reversal chart patterns. The point must not exceed the pivot point 1 (in the worst case it might be on the same level) for the pattern to be valid.

Confirmation level

The confirmation level is our entry point in the market. It is located at the same level as pivot point 2. When price breaks through this level open the trade.

Target level

To set the target trader needs to connect 1 and 3 pivot points with a line. The size of your 123 pattern equals the vertical distance between Line 2 (which is a horizontal line at the level of 2 pivot point) and the midpoint of Line 1.

123 chart pattern stop loss setup

It is highly important to use stop loss when trading the 123 chart pattern. The stop loss should be set under pivot point 3 in the bullish trend reversal, and above in the bearish one. In the condition of high market volatility, the price might get pushed beyond the 2 pivot point for a while. That’s why it will be a good idea to set stop-loss slightly beyond the 3 pivot point, as this will prevent stop loss from being activated.

The target level of 123 continuation pattern

The target of the “continuation 123 pattern” measures the same way as usual. The only exception is that in this case, you should take pivot point 3 as a starting one of your target.

We are just 35% up from 2008 high To understand the Dollex, let us take a hypothetical situation. Assume that the Sensex was at 40,000 in January and has now grown to 50,000 in December. That is a phenomenal 25% appreciation in the Sensex and if you are an Indian investor you would be extremely happy. However, if you are a foreign portfolio investor or FPI, you also worry about the rupee/dollar exchange rate. That is because, for the foreign investor to realize the 25% gains on the Nifty, the rupee must have remained stable. However, if during this period the rupee had depreciated by 15% from Rs.70/$ to Rs.80.50/$, then the returns of the foreign investor would have been substantially lower. This currency impact is captured by the Dollex.

Now let us use this example to understand what is Dollex? The Dollex captures these dollar-adjusted returns. Let us break up the above illustration. In the above case, Sensex returns would be 25% {(50,000-40,000) / 40,000}. That is quite straight forward and that is the returns that your Sensex would show. Here is how Dollex would be calculated. Dollar infusion in January = 40,000/70 = $571.43. At the time of redemption, it is 50,000/80.50 =$621.12. In this case, the Dollex Returns would be 621.12/571.43 = 8.7%. That is a tad shocking. How did 25% returns become just 8.7%? That is because during this interim period, the rupee had depreciated by 15% resulting in the dollar returns reducing substantially. This dollar impact is captured by the Dollex. We shall look at the S&P BSE Dollex 30 in greater detail.

What are ratios to analyse any banking stocksHAPPY REPUBLIC DAY 🇮🇳

Today we will study ratios for analysing any banking/ non- banking stock.

Key Ratios are -

1. Net Interest Margin (NIM)

2. Provision Non Performing Assets (PNPA)

3. Loan to Assets Ratio

4. Return on Assets Ratio (ROA)

5. Capital Adequacy Ratio

6. Gross NPA

7. Net NPA

8. CASA Ratio

9. Cost to Income ratio

---------------------------------------------------------------------

1. Net Interest Margin (NIM)

1. Net Interest Margin = ( Investment Income –

Interest Expenses ) / Average Earning Assets.

2. Positive Net Interest Margin shows that bank is earning more money in the form of interest than its cost of funding investments.

3. There are several factors that affect bank NIM. One of the most significant is interest rates. When interest rates are high, banks are able to earn more from loans and investments, which increases their NIM. When interest rates low, banks earning will loans and investments decrease, which lead lower NIM.

4. In summary, Net Interest Margin is important measure of bank's profitability and its ability to generate income from its existing assets. NIM is affected by interest rates and competition. Banks with a high NIM are generally considered strong financial position and better to grow and invest in new opportunities.

Let's look at example

Bank in India has total assets of ₹1,00,000 crore consist of loans and investments. The bank has total deposits of ₹80,000 crore and it pays interest rate of 4% on savings accounts and 6% on Fix Deposit The bank total interest income for the period is ₹2,400 crore which is earned by loans and investments. The bank total interest expense for period is ₹1,600 crore, which is paid to depositors.

To check the NIM we take the bank net interest income (NII) of ₹800 crore (₹2,400 crore in interest income - ₹1,600 crore interest expense) and divide by the bank average earning assets of ₹90,000 crore (average of total assets and total deposits).

NIM = NII / Average Earning Assets

NIM = ₹800 crore / ₹90,000 crore

NIM = 0.89%

Bank NIM is 0.89% every ₹100 of assets the bank is earning ₹0.89 of net interest income. This NIM is a measure of the bank efficiency in generating income from assets and can be used to compare it with other banks and over time.

NIM in India will be lower than developed countries due to lower lending rates and high competition among bank.

-=-=-=-=

2. Provision Non Performing Assets (PNPA)

1. An asset, including a leased asset, becomes non performing when it ceases to generate income for the bank.

2. Provision for Non Performing Assets (NPA). The amount keep aside by bank, to cover it's potential losses from loans and other credit related assets that have been non performing.These provisions are made when a bank expects that some of its borrowers will default on their loans, and the bank needs to set aside funds to cover the potential loss.

3. In summary, Provision for Non Performing Assets (NPA) Banks are required to make provisions for NPA on a regular basis, quarterly basis, amount of provisions is disclosed in the financial statements. Provision for NPA is an important measure of a bank's financial health, Help bank to absorb the impact of loan defaults and manage credit risk.

Provisions for NPA is closely watched by investors, analysts, and regulators, it helps them to assess the bank's credit risk.

Let's look at example

Bank total loans of ₹50,000 crore. ₹2,000 crore classified Non performing Assets (NPA) borrowers defaulted their payments more than 90 days. Bank required to set aside certain percentage of the NPA loans as PNPA as per the Reserve Bank of India's guidelines. The current PNPA provisioning ratio is 15%.

To get PNPA we multiply the NPA loans of ₹2,000 crore with the PNPA provisioning ratio of 15%.

PNPA = NPA loans x PNPA provisioning ratio

PNPA = INR 2,000 crore x 15%

PNPA = INR 300 crore

-=-=-=-=

3. Loan to Assets Ratio

1. Loan to Assets ratio can help investors obtain complete analysis of bank's operations. Banks that have relatively higher Loan to Assets ratio banks with lower levels of Loan to Assets ratios derive a relatively larger portion of their total incomes from more diversified, noninterest earning sources, such as asset management or trading. Banks with lower Loan to Assets ratios may fare better when interest rates are low or credit is tight.

2. In summary, Loan to Asset ratio is financial metric compares bank total loans to total assets. It's used to measure bank leverage assess the level of risk associated with lending activities. Higher Loan to Assets ratio indicates that a bank is more heavily reliant on lending and is more leveraged and risky, while a lower ratio indicates that the bank is less risky.

Let's look at example

Bank has total assets ₹1,00,000 crore, total loans ₹70,000 crore. to get Loan to Assets Ratio we divide the total loans by the total assets.

Loan to Asset Ratio = Total Loans / Total Assets

Loan to Asset Ratio = ₹70,000 crore / ₹1,00,000 crore. Loan to Asset Ratio = 0.7.

Bank's Loan to Assets Ratio is 0.7 / 70% (0.7*100) bank assets in form of loans. A higher Ratio indicates that bank is heavily invested in lending activities, which can be sign of more aggressive lending strategy. it's also increases the risk of default. Than higher risk of NPA. Banks required to maintain minimum level of Capital Adequacy Ratio as per the Reserve Bank of India's (RBI) guidelines.

-=-=-=-=

4. Return on Assets Ratio (ROA)

1. Return on Assets = Net Income / Total Assets

2. The higher ratio means assets are well managed and low ratio means resources didn't used effectively compared to the industry and competitors.

3. In summary, ROA is financial ratio measures profitability of company in relation to total assets. It is calculated by dividing the company's

net income by its total assets. This ratio is useful to compare the performance of company with its peers in the same industry. It is an important metric used to evaluate a company's overall efficiency and performance but it's important to keep in mind that high ROA not necessarily mean that company have strong financial position.

Let's look at example

Bank has total assets of ₹100 billion and net income of ₹5 billion. To get ROA we divide the net income by total assets.

ROA = Net Income / Total Assets

ROA = ₹5 billion / ₹100 billion

ROA = 0.05 or 5%.

Bank ROA is 5% For every ₹100 billion of assets, the bank generates ₹5 billion of net income. Higher ROA show that bank is profitable and efficient in utilizing assets. It's important to note this ratio is sensitive to the size of the bank It's better to compare the ROA of a bank with other banks of similar size.

-=-=-=-=

5. Capital Adequacy Ratio

1. The Capital Adequacy Ratio helps make sure banks have enough capital to protect depositors money.

2. Banks are required to maintain a certain level of Capital Adequacy Ratio as per the regulations set by central bank to ensure that they have sufficient capital to meet the potential losses and continue their operations even in adverse situations.

3. It helps maintain the stability of the financial system by ensuring that banks can withstand in unexpected situation.

Let's look at example

In India, the Reserve Bank of India (RBI) sets the minimum Capital Adequacy Ratio for banks at 9%. which means that they must hold capital worth at least 9% of their total risk-weighted assets.

Bank in India with total assets of ₹100 billion and risk-weighted assets of ₹80 billion must maintain minimum capital of ₹7.2 billion (9% of ₹80 billion) to meet the Capital Adequacy Ratio requirement set by the RBI.

It's important to note that, the Banks with a higher Capital Adequacy Ratio are considered to have a better ability to absorb unexpected losses.

-=-=-=-=

6. Gross NPA

1. Gross Non Performing Assets (GNPA) is refer to the total value of loans or advances that have been classified as Non Performing Assets. These are loans or advances the borrower has defaulted on repayment or interest for certain time. loan is classified as an NPA if the borrower has not made any payment for period of 90 days or more.

2. A high ratio of GNPA to total loans indicates a higher level of credit risk and potentially weaker financial condition for the bank.

Let's look at example

Bank has total loans of ₹100 billion and ₹20 billion are classified Non Performing Assets (NPA). The bank Gross Non Performing Assets (GNPA) would be INR 20 billion.

we see the ratio of GNPA to total loans we get 0.2 (₹20 billion / ₹100 billion). This ratio of 20% indicates that 20% of the bank loans are classified as NPA. This high ratio may indicate the bank is facing high level of credit risk it could be cause for concern.

It's important to note that Gross NPA ratio is used in conjunction with other financial indicators to understand overall financial health of bank and single indicator may not enough to make a conclusion.

-=-=-=-=

7. Net NPA

1. Any financial security owned by a bank is considered an asset. The interest we pay on loans is the primary source of income for banks these loans are classified as assets for bank's.

when borrowers can't repay the amount these assets are classified as Non Performing Assets (NPA) because they are not generating any income for the bank's.

2.If loan provided by bank is overdue more than 90 days from the borrower end comes under NPA. If loan amount is unpaid more than 1 year from due date then it's a doubtful debt and if it’s unpaid more than 3 years then loss of an asset or default account.

Net Non-Performing Asset = Gross NPA – Provisions.

Gross NPA = Total Gross NPA/Total Loans given.

Impact of NPA

Due to higher NPA rates, banks will suffer significant revenue losses that will potentially affect their brand image. insufficient funds, banks will have to increase the interest rates on loans to maintain their profit margin.

Let's look at example

Bank has total loans of ₹100 billion and ₹20 billion are classified as Non Performing Assets (NPA). The bank is required to make provisions for ₹10 billion against these NPA. The bank Gross Non-Performing Assets (GNPA) would be ₹20 billion and Net Non Performing Assets (Net NPA) would be ₹10 billion (₹20 billion - ₹10 billion).

If we see the ratio of Net NPA to total loans we get 0.1 (INR 10 billion / INR 100 billion). This ratio of 10% indicates that 10% of the bank's loans classified as NPA after making necessary provisioning. This ratio gives a clearer picture of bank's financial health than just Gross NPA ratio as it takes into account the provisions made against NPA.

-=-=-=-=

8. CASA Ratio

1. CASA (Current Account and Saving Account) it is measure the proportion of bank deposits that are in the form of current and savings accounts.

2. The ratio is calculated by dividing the total value of current and savings account deposits by the total deposits. It is typically expressed as percentage. Higher CASA ratio indicates that bank have larger proportion of stable deposits. This is because banks can use these deposits to fund their lending activities at a lower cost which improves bank's net interest margin.

Let's look at example

Bank has total deposits of ₹200 billion and ₹150 billion in form of current and savings accounts. The bank CASA ratio would be 75%.

This ratio indicates that three fourth of the bank deposits are in the form of current and savings accounts which are considered the stable form of deposits. This high ratio is considered positive sign. Stable deposits can used to fund lending activities lower cost.

High CASA ratio the bank will have access to cheaper funding which will improve it's net interest margin. This means that the bank will be able to offer loans at a lower rate of interest. which will make it more competitive in the market and attract more customers. And bank will also have more stable funding which will make it less vulnerable to market fluctuations and interest rate changes.

Asset quality, capital adequacy play important roles in assessing a bank's overall financial condition.

-=-=-=-=

9. Cost to Income ratio

1. Cost to Income Ratio (CIR) measure company efficiency by comparing it's operating expenses to it's revenue. calculated by dividing the total operating expenses by the total revenue and expressed in percentage.

2. Lower (CIR) indicates that company more efficient in managing expenses and able to generate more income for every unit of expenses. while higher (CIR) indicates that company less efficient in managing it's expenses and is generating less income for every unit of expenses.

Let's look at example

Bank A with a high CIR.

Bank has total operating expenses of ₹10 billion and total revenue of ₹15 billion. The bank's CIR is 67% (₹10 billion / ₹15 billion). High CIR indicates that the bank is not very efficient in managing its expenses and is generating less income for every unit of expenses. The bank may need to review its cost structure and implement measures to reduce expenses in order to increase its efficiency and profitability.

Bank B with a low CIR:

A bank has total operating expenses of ₹5 billion and total revenue of ₹15 billion. The bank CIR is 33% (₹5 billion / ₹15 billion). This low CIR indicates that the bank is efficient in managing its expenses and is able to generate more income for every unit of expenses. The bank able to invest in growth opportunities and increase profitability.

I hope you found this helpful.

Please like and comment.

Keep Learning,

Thank you for reading!

If you are not 'INSIDE' you are 'OUTSIDE' In the stock market, if you are not inside, you are outside.

I expect all those reading this article wants to be inside the market.

So, if you want to participate in the market then you must develop a deep insight into

the key market players i.e. your competitors who drive day to day movement of the market.

Key Market Players:-

The following are the three types of market participants.

->Retail - general public also called clients

->High Net Worth Investors - commonly known as HNI clients.

->Proprietary Trading - also called 'Pro' are firms.

->Institutions - referred to as trading organizations.

Let's dive into the details of each of them listed above .

Retail Investors :- They are the general public who invest or trade in the market individually with very

small capital as compared to other participants. They are at the bottom of the market food chain when considered individually

but in recent few years, the retail participants as a whole have seen a significant rise in numbers.

High Net Worth Investors: - They are also an individual but with big sums in their pockets. They have a deeper access to

the markets, inside news, and all. They don't participate in day-to-day trading.

Proprietary Traders :- Also known as 'Pro 'are those firms/banks which also trade in the daily market with the firm's funds.

They are at the middle of the market food chain i.e. above retail but below institutions. Actively participate

in daily market movements.

Institutional Investors :- They are organizations taking part actively in market movements. They are at the top of the market food chain.

They can be further divided into two groups:

->FII (Foreign Institutional Investors): Institutions whose origin is outside India but still they invest in Indian markets. Actively participate

in daily market movements.

->DII (Domestic Institutional Investors): Institutions whose origin is India. They are inactive in the derivatives segment.

Among the participants listed above Retail, Pro & FII are actively involved in the daily market trading and encourage

derivatives segment.

We all have seen everyone in markets talking about FIIs that are bearish/bullish on markets but why?

The above figure is of FII+Pro & Client correlation with nifty, this describes the reason why the positions of FII are significant.

We can draw the following conclusion:-

1. Majority of the time FII is correct to predict the market movement.

2. Clients generally build position against FII and max times have an opposite correlation with market movements.

Now, have a look at how the FII and client positions affect the market movement

The above figure justifies the correlation.

We can draw the following conclusions:-

1. Maximum time FII are net short in nifty whereas clients are net long in nifty.

2. When FII cover their shorts and deploys the longs we see an uptrend but at the same time, the client unwinds long

and deploys shorts which are generally against the trend i.e. client likes to drive in opposite direction.

3. And when FII positions converge with the Client there is previous trend exhaustion and the arrival of a sideways market or

sometimes a new trend.

As of now the index is clearly explained but what about stocks how much significant is FII in stocks?

To answer the above question let's take an example of a very famous stock ITC:-

The above figure says that FII has increased holding in the interval of Jun2022 - Sep2022 from 12.7% to 44.5%

and by the time client has decreased the holding from 44.5% to 14.8%.

Does the change in position affect the stock price of ITC? let's have a look

Now it's clear that FII have ultimate power because when they started to increase their holding in ITC

the price shoot up during this time Public who were holding it for the last 2yrs exited when ITC has just begun to move.

Hope the readers had understood the mightiness of FII and the oppositeness of the Public and also have got a deep insight

about their competitors .

Also, thanks to @biswapatra for requesting me to write an article on this topic. You can also suggest an topic on which you

want to have analysis.

Concept Volume: How to plan your trade with help of volumeConcept Volume:

(1): We have got a clear uptrend till now (pls check the example shared) until a good volume (red) candle comes out of nowhere, as mentioned - (1).

This is the first sign of weakness in the trend, long positions need to be trailed after that, one should avoid creating long positions. & high of this zone could be monitored serious turning point zone.

Here, in Aarti Industries we have seen a clear breakout. Though the trend is intact & till now we have only encountered a single speed breaker, we should consider this as a sign of caution.

(2): candle completed the week of 4th Oct. 21, is the blow-off top. After the big move-up, we have got an extremely low volume Doji.

How could be possible to have a Doji after a good move-up? (acceleration than a pause in the momentum)

(3) After approaching again at the psychological resistance, this got rejected forming an engulfing. But before this why this reversal happened let us find it.

Check the following candle-

18 Oct 21: good volume spread & good volume candle,

25 Oct 21: low volume spread & low volume candle, why? If the trend is intact it should not happen

1 Nov 21: a Doji-type candle with ultra-low volume. Are bears no more interested in taking the stock further down?

15 Nov 21: First avg. volume green candle after 5 red candles. High is marked as a psychological resistance.

Now, check 28 Feb candle, it has finally broken the support (maximum traders enter here, considering the good opportunity to go short & it is ideally a good one but if entered, it has tested the patience)

also, check how could be possible that this breakout candle has a low volume than the last one, in the trend?

All of this is basically an anomaly.

From here, the trend got reversed making 5 green candles that retraced the red ones till their resistance level as mentioned (4).

From 11 April 22 we have got 5 candles, in the trend and aligned with the volume

Now, if you notice the three candles formed after 30 May 22, you see the pattern is not aligned with the volume (the market is going down but the volume is decreasing along with the size of the candle---AN ANAMOLY)

CASE STUDY

(aarti industries)

A sense of debtIn the previous two posts, we explored how assets are grouped in a company's balance sheet.

Part 1: Balance sheet: taking the first steps

Part 2: Assets I prioritize

Now let's deal with Liabilities and Stockholders' equity. Let me remind you that these are the sources of funds that give a company assets. And indeed, with what funds can a company have assets? Either with its own funds (stockholders' equity), or with funds borrowed (liabilities). For simplicity, we will call them Debts and Equity.

Debts can vary in maturity, so we've divided them into two categories in the balance sheet: Current liabilities and Non-current liabilities .

Current liabilities include:

- Current debts are debts that need to be paid back within a year after they are incurred. Do you remember our master took a loan from the bank to make a large batch of boots? That loan will be recorded in this item (assuming the loan is up to one year in repayment).

- Accounts payable (debts to suppliers of goods and services). You can borrow money not only from the bank, but also from your suppliers, for example. In other words he is giving you raw materials now, but is ready to accept payment later. Such debts are reflected in this item.

- Accrued liabilities (Provisions for future expenses on unpaid bills in the form of wages, rent, taxes). The word "debt" is in many ways synonymous with the word "liability." A company may have many such liabilities: payment of wages, rent and taxes. In essence, these are also debts to be paid during the year. For convenience, cash reserves are set aside for them. They are spent at the moment when the payment is due. Such reserves are recorded in this item.

- Other current liabilities . Debts or liabilities with a maturity of up to one year that are not included in the categories above are shown here.

Non-current liabilities include:

- Long term debt - these are debts that need to be paid back more than one year after they are incurred. If our master had borrowed from the bank for two years, such a loan would fall into this category.

- Deferred taxes liabilities (Provision for taxes to be paid in a future period). Tax rates are subject to change, and new taxes may come into effect in a year or more. But even now, the company can set aside money for future taxes.

- Other long term liabilities . Here are debts or liabilities with a maturity of more than one year that are not included in the categories above.

In short, debts are loans taken by the company, provisions for tax liabilities, and debts to suppliers.

The amount of debt is a very important indicator in the fundamental analysis of a company. On the one hand, the mere presence of debt is not scary, because it demonstrates that banks trust the company and give it loans for development. On the other hand, a substantial amount of debt can cause serious problems and losses in the period of weak sales of goods or services. Banks are unlikely to suspend interest charges on loans if a company is doing poorly. This means the company will incur expenses in the form of interest on loans that are not offset by revenue. Also a reminder that if a company goes bankrupt, the owners of the stock get the assets of that company only after all debts have been settled . If the debts are so large that they exceed the value of all the property, the shareholders get nothing. For these reasons, I select companies with small debt loads.

What liabilities do I focus on?

- Current debt;

- Accounts payable;

- Long term debt.

For me, these are the items that most clearly reflect the company's debt situation.

In the next post, we will conclude our study of the balance sheet and look at the basic source of assets, which is Equity. See you soon!

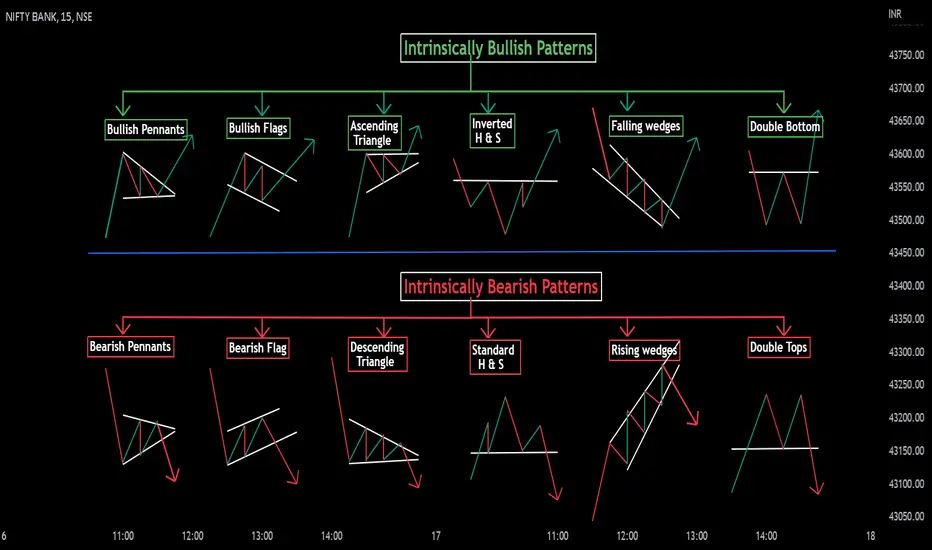

Interpretation Of Chart Patterns According To Market Phase.NSE:BANKNIFTY1!

As we all know market moves in phases

What are those phases?

A primary bull or bear trend consists of two phases, specifically

Accumulation phase: if the market rises after consolidating, we say that the consolidation represents accumulation (buying activity).

Distribution phase: if the market declines after consolidating, we say that the consolidation represents distribution (selling activity)

The main issue arises when a trader tries to know whether this consolidation is accumulation or distribution.

So how can we overcome that issue?

As a trader, we have to try to look for evidence that suggests whether accumulation or distribution is taking place during consolidation and out of that evidence we will discuss how we can use chart patterns to identify the phase.

Chart patterns belong to one of two groups, that is, reversal or continuation.

Chart patterns have intrinsic and extrinsic biases.

What is the intrinsic bias of chart patterns?

Intrinsic bias means the inherent bullish or bearish sentiment associated with a chart pattern.

For example,1. An ascending triangle pattern has an inherently bullish bias.

2. A head and shoulder pattern has an inherently bearish bias.

3. A descending triangle pattern has an inherently bearish bias.

## A symmetrical triangle and rectangle/horizontal range pattern have an intrinsically neutral bias

What is the extrinsic bias of chart patterns?

Extrinsic bias refers to as location-based sentiment of a chart pattern.

Like a pattern forming at some location which is historically a strong resistance zone (Market top) so if an ascending triangle forms at that location then its extrinsic bias will be bearish.

Example 1: An descending triangle is an intrinsically bearish pattern, but if it is forming at a strong support location then the extrinsic bias will be bullish.

Example 2: An ascending triangle is intrinsically bullish, that is, it has a bullish bias. Regardless of where this pattern occurs with respect to past price action, it will always be inherently a bullish indication, but If this bullish pattern is found at the price level of some historically significant market top/Resistance, then we say that it is extrinsically bearish, cause the pattern is located at a significant resistance.

Factors determining the extrinsic bias of the pattern

• Direction of the preceding trend.

• Location with respect to historical extremes in price.

• Location with respect to the phase of an underlying market cycle

• Location with respect to other support and resistance barriers to price.

• Bullish or bearish divergent formations.

How can we use this extrinsic and intrinsic bias?

When extrinsic bias and intrinsic bias both are in agreement then the possibility of a reversal at market tops or bottoms is significant.

Similarly, for trends, when the intrinsic bias of the chart pattern is in agreement with the directionality of the trend, i.e., the trend sentiment, the potential for a continuation is usually greater.

For example, The inverse head and shoulder pattern have an intrinsically bullish bias, and it is also forming at a strong support location then its extrinsic bias is also bullish.

Like, If both are in alignment then we can say that this is an accumulation phase and a long entry can be initiated.

##When attempting to determine the reliability of potential reversals during the accumulation and distribution phases, or continuations during the trend phase, it is important to look for agreement between the intrinsic and extrinsic biases. If Any disagreement is seen as an indication that a reversal or continuation may be inherently weak.

##Intrinsically neutral formations, their extrinsic bias or sentiment is derived from the trend sentiment. For example, a symmetrical triangle will adopt an extrinsically bullish bias in an uptrend and an extrinsically bearish bias in a downtrend.

By considering these Factors while trading chart patterns in different market phases will give an in-depth insight and helps in making more informed and rational decisions.

I hope you found this helpful.

Please like and comment.

Keep Learning,

Happy Trading!

Assets I prioritizeIn the previous post Balance sheet: taking the first steps , we began parsing the balance sheet of the imaginary workshop and focused on assets. Today, I suggest looking at what types of tangible and intangible property are classified as current assets and what types are classified as non-current assets.

Current assets contain the following items:

- Cash and cash equivalents - in our case we can include a safe with money, which, in general, corresponds to the company's cash in its current bank accounts.

- Net receivables - here we would include the IOU from a friend. That is everything that clients owe the company for goods or services.

- Inventory - this includes a bag with leather, rubber and thread. That is all raw materials, from which goods are made, as well as stocks of finished goods in warehouses.

- Other current assets - this can include other current assets that do not belong to the previous items.

Non-current assets include the following items:

- Net property, plant and equipment - we include a garage, table, chair, sewing machine and tools. Depreciation is deducted from the original cost of the property when reporting it. Depreciation is the cost to repair and renew the property.

- Equity and other investments - in our example, this would include oil company stocks (and in general, any company investment in stocks or bonds of other companies).

- Goodwill - let's say our company wants to buy another company and is willing to pay $11 million for it. The assets of the other company are $10 million, and the debts that our company will have to pay for the other company are $2 million. So the assets net of debt are $8 million. After the purchase, the assets and debts of that company will become the assets and debts of our company. So, the difference between the purchase amount of $11 million and the net assets of $8 million is a goodwill equal to $3 million. For our workshop, this item is not relevant, as it didn't buy any company. Nevertheless, remember that goodwill is the difference between the purchase price of another company and its net assets.

- Intangible assets - this can include the value of the customer base in the master's phone book, as well as any other assets that have no tangible basis (such as purchased trademarks).

- Other long term assets - this item includes other non-current assets that don't belong to the previous items.

Once we understand which asset belongs to which item, its value (or rather, the sum of the values of all assets belonging to this item) is written in the balance sheet. For example, let's say we've determined that the Inventory item includes leather, rubber, and thread. The accountant adds up the value of the leather, rubber, and thread and writes the total amount in monetary terms against the Inventory item. This is how the numbers appear in the balance sheet.

Now let's discuss which balance sheet items we should pay attention to during the fundamental analysis of assets. I have formulated the following rule for myself: pay attention to the assets that are directly related to the sale of the company's goods or services .

If a company does not sell its goods or services well, its bank account balance will shrink, huge inventories of unsold goods and raw materials will accumulate in its warehouses, and accounts receivable (customers debt) will grow. The fact is that when sales are bad, the company is ready to lend out goods as debt.

If sales are going well, then, on the contrary, the money in the account will grow, and accounts receivable and inventory will start to shrink. All other assets can influence sales only indirectly, so I don't consider them.

Thus, I have identified my priority assets :

- Cash and cash equivalents;

- Net receivables;

- Inventory.

As you can see, they are all quick current assets. Non-current assets only indirectly affect sales, so they are not a priority benchmark for me.

In the next post, we'll start looking at the right side of our disclosed book, called the Balance sheet. That's where the company's liabilities and equity belong. See you next time!

The Ikigai of Profitable TradingYou're mistaken if you think that being a profitable trader revolves around cracking the code to defeat the market and being able to predict it's every move.

Trading is about probabilities and about how well you're able to maintain the balance of the ikigai of trading (my words) which are 3 equally important things namely - an edge, risk management and psychology.

Master your mind to master the charts.

DM | FOLLOW | SHARE

Dow theory - 3 kinds of trend1. Primary trend (9months to 2 years)

2. Secondary trend (6 weeks to 9 months)

3. Minor trend (few days to few weeks)

> Black line is the primary trend

> Green lines are an example of a secondary trend.

> Blue lines are minor trend.

Always trade with harmony of a primary trend.

Note : only for learning.

Why Traders Fail: Need for a Balanced ApproachWhy do people fail at trading?

It is true that the success rate in trading is very less. You will find only a couple of good traders in a city. In my opinion it is due to the imbalance between two extreme emotions or personalities. One cannot understand or succeed unless a balance is created between them. All that is needed to create the balance throughout this adventure is your Time and meaningful effort.

Here are some of those extremities that need to be recognized and balanced.

🚀 Lack of awareness Vs Hyperawareness

There are people who enter in trading without knowing this business. They would throw their hard-earned money in the market just because someone else is making money here. These people have very short trading career as they lose all their money in a couple of trades. At least knowing about trading will make them shy away from high risk scenarios and hence help in surviving for long.

On the other hand, there are people who have acquainted themselves to the markets to such a level that they want to know everything. They would like to learn each and every indicator and apply it on their charts, until they are left with a chaotic system which is bound to fail.

Market is an ocean. You can’t know everything but can try to master a few things.

🚀 Fear of Loss Vs Greed

Let me say that most of the people entering this business belong somewhere in the middle class. They always have dearth of money. So, they trade with less money and are afraid of losing it. They would either book very small profits or exit too early from good trades. But unfortunately, they won’t show this haste in losing trades. So, they book 1 point and lose 2.

On the other hand, there are risk takers who have money but they are greedy. They would often book heavy losses or do not book healthy profits on time. They would only fume when their profitable trades turn into losses.

Having less or more is not the question but discipline of booking profits and losses is the answer.

🚀 Stubbornness Vs Springy

People would hold on to a trade or system infinitely. They would not believe in cutting small losses or mend their system for improvements.

On the contrary, there are those who would keep on hopping on to one system or the other like a spring . They would book small profit/loss in one stock and buy another with higher risk.

Improvement and patience are the key to success in trading.

🚀 Dependent Vs Egoist

Each one of us would have bought stocks on the basis of tips from our broker, business channels or friends. Some of us would have moved on knowing the reality of tipsters while the others would still be clinging on to them. The latter would never learn a lesson before losing their entire capital.

On the contrary, an egoist would only be overconfident in what he is doing. Having your ears closed in trading is a great thing but lack of flexibility is another. If the whole world says that the ship is going to sink, you can not just sit on its deck waiting for a miracle.

Be an independent but flexible thinker.

Thanks for reading.

SYSTEM 1.27Give the system a test run EU and GU , and don't forget to express your appreciation once you secure funding ! ..If you don't have any system yet, It could be the missing piece of the puzzle you've been searching for, I can assure you that during the backtesting process, you will discover many new and interesting insights.

Bollinger Bands Secret Part 1In this tutorial we have learned about Bollinger Band trading concept.

When the price is above the 20 MA always think about buying the call/futures or selling the put options.

When the price is below the 20 MA always think about buying the put and selling the futures/call options.

If the 20 MA is flat - Sideways Market

If the 20 MA is upwards - Bullish (Trending market )

If the 20 MA is downwards - Bearish (Trending market )

If the Bollinger Band is compressing then the market is ready for a blast in the either side (upwards/downwards)

What Is the RSI Indicator & RSI DivergenceRSI - Relative Strength Index Indicator:

The Relative Strength Index (RSI) is a momentum indicator used in technical analysis that measures the magnitude of recent price changes to evaluate overbought or oversold conditions in the price of a stock or other asset. The RSI is displayed as an oscillator (a line graph that moves between two extremes) and can have a reading from 0 to 100. It is important to note that the RSI does not indicate whether a stock is a buy or a sell; rather, it provides insight into the current trend of the stock.

The RSI is a versatile indicator that can be used by traders of all levels and can be adapted for any style of trading. For example, a trader may use the RSI to identify support or resistance levels, or to spot divergences that can be used to predict future price movements. The RSI can also be used to locate potential trading opportunities by looking for overbought or oversold conditions. Furthermore, the RSI can be used in combination with other indicators, such as moving averages, to gain a better understanding of the market’s overall trend.

Formula of RSI:

The RSI is calculated using a formula that compares the magnitude of recent gains against recent losses over a specified period. The formula for the RSI is:

RSI = 100 - (100 / (1 + (Average of Upward Price Movements / Average of Downward Price Movements)))

What is periods in RSI:

Periods in RSI (Relative Strength Index) are the number of time periods used to calculate the RSI. The most commonly used period for RSI is 14, but other periods such as 7, 9, and 25 are also used. This number represents the number of time periods that are used to calculate the RSI, so a period of 14 would mean the RSI is being calculated using the last 14 time periods.

RSI divergence:

RSI divergences are a type of technical analysis used to identify potential trend reversals in the markets. They are based on the Relative Strength Index (RSI) and are used to spot potential trend reversals before they occur.

A divergence occurs when the price of an asset makes a higher high, but the RSI makes a lower high. This suggests that the current rally is losing momentum and may reverse course. Similarly, a lower low in the price and a higher low in the RSI may signal an impending rally.

Divergences are best used in conjunction with other technical indicators and analysis to confirm price action. It is also important to keep in mind that divergences do not always lead to reversals and may simply signal a period of consolidation before the price continues its current trend.

Divergence Cheat Sheet / Types of Divergence:

Structural Confluence of Elliot and HarmonicsConfluence doesnt mean some indicators and price action .. confluence conditions can be seen everywhere from structure to entry

The above structure shows you confluence with 2 major concepts in trading world HARMONICS and ELLIOT, shows you the possible areas where you could see confluence of both

The 3rd wave could some times be BAT pattern or DEEP CRAB pattern in impulse, when it comes to elliot correction you will prob'ly see ABCD pattern in formation.

This will give you an idea of how to identify the confluence when you are looking for swing trading

Always keep in mind that there will be internal small patterns within the big pattern do not get confused while doing multi TF analysis thinking which pattern to follow, always follow the higher TF pattern.

Our take on AI-generated Pine Script™The fact that GPT can generate Pine Script™ code has garnered much attention lately. While the perspective of making natural language requests to an AI to generate code is understandably attractive, it is unfortunately not something traders should use as a substitute for learning to program or finding a freelancer who will program for them if they are not interested in learning to code.

Simply put, the core of the problem lies in the fact that code generated by software like GPT is unreliable. Only someone who already knows Pine can analyze it and make the inevitable changes required for it to work as intended.

Would you rely on a code you cannot trust to trade your money? Those who can answer "yes" to that question are gamblers — not traders — and they most probably won't be reading this publication anyway. Because you are reading this, we assume that you are, or hope to become a trader, in which case elementary risk management would dictate that you consider GPT-generated Pine code with suspicion and not use it to make your trading decisions.

Some of the typical problems you can expect of GPT-generated Pine Script™ code are that its logic will not do what you asked it to do and that it will frequently fail to compile because its syntax is malformed, among other reasons because it mixes up different versions of Pine.

Consequently, we have decided not to allow requests to fix GPT-related code in the Q&A forums where PineCoders answer programming questions. We believe this is the best way to support our community's all-important volunteers who contribute their valuable time and knowledge to help Pine programmers facing programming challenges. Our Q&A forums are not indicator-writing services for traders who do not code in Pine. For that, traders can use our list of Trusted Pine Script™ Programmers for Hire to find a reliable freelancer they will pay to do the work for them.

Our Q&A forums for Pine Script™ programmers are:

• Stack Overflow

• "PineCoders Pine Script™ Q&A" room on Telegram

• "Pine Script™ Q&A" chat on TradingView

If you are interested in learning Pine Script™, start here .

Whether you program or not, do not miss the opportunity to explore our 100,000-strong Community Scripts published by TradingViewers who so graciously share their work with our community.

Disclaimer

This publication is not intended as a dismissal of GPT-3. Originally designed to process requests to generate text, the successive versions of GPT have turned out to be increasingly adept at producing relatively good-quality text, so much so that it is often difficult for humans to detect that a program wrote it. See on the chart above, for example, its own text on the subject we explore in this publication, or this paper it wrote about itself. We can certainly foresee many uses for GPT-generated text, although it does bring to light challenging ethical questions.

Look first. Then leap.

Balance sheet: taking the first stepsToday we are going to start learning about fundamental analysis of companies. In my opinion, this is the basic skill you should have when picking stocks to invest in.

Once again, the main principle of the strategy I follow is to pick outstanding companies and buy their stocks at a discounted price.

You may have noticed that first-class products are occasionally discounted in stores, but not for long, because such products are quickly swept off the shelves, and almost the next day the price is again without a discount. Exactly the same strategy is applicable to the stock market. Now, fundamental analysis is a method for picking outstanding companies (that is, companies with strong fundamentals).

How can we tell if a company has a strong foundation or not? There is only one way - by analyzing its financial statements. Every listed company has to disclose this information publicly on its website. In other words, we don't have to extract that information - it is publicly available. You can also find it on TradingView and see the data in dynamics.

What is the content of this information? The company publishes three reports : balance sheet, income statement and cash flow statement.

The balance sheet, like the order book , can be presented as an open book. The left side of the book lists the company's assets and their valuation in monetary terms, and the right side lists the company's liabilities and equity , and their valuation in monetary terms.

What are company assets? These are everything that belongs to the company: buildings, equipment, trademark, shares of other companies, cash in the cash register. In general, all tangible and intangible property of a company are assets.

What are liabilities and equity of a company? These are the sources of funds that gave rise to the assets. For example, if you bought a computer for $1000 with your savings, then the computer is an asset, and your own savings are equity. If a friend lent you $100, and you put the money in your pocket, the money in your pocket is an asset, and the debt to your friend is a liability. Based on these examples, you can make an imaginary balance sheet:

As you can see, the entry in the balance sheet is the name of the asset, liability or equity and their monetary value. Assets, liabilities and equity are inextricably linked, so the sum of assets is always equal to the sum of liabilities and equity .

If we were to write every asset in this way on the balance sheet of a large company, it would turn into an endless book of hundreds of pages. However, if we look at the balance sheets of huge corporations, they can fit on a single sheet of paper. This is due to the fact that over time invented to group the same type of balance sheet items. Let's look at how the company's balance sheet items are grouped:

Don't be frightened. Now we will try to digest this table with the help of an example we are already familiar with. Let's think back to our master cobbler , specifically to the period when he was just starting out.

Let's assume what exactly he had at that time: a garage, a table, a chair, a sewing machine, tools, a bag with leather and rubber, thread, a safe with money, a phone book with clients' contact information, a IOU from his friend, and oil company stocks.

I have now listed the assets of our master, or should I say, of his workshop. I should note that what is listed here is exactly what is directly related to his business. Even the money in the safe, the debt from his friend, and the oil company shares came about because of the existence of the business. Let's say the master's apartment or the bicycle he rides in the park are not assets, because they don't belong to the workshop. They belong to the master, but not to his business.

Let's categorize the workshop's assets into groups. There are two big groups: Current assets and Non-current assets .

How should you distinguish them? The general rule is this: Current assets are what a company's product is made of, and what can turn into money in the near future, so they can be called quick assets . Non-current assets are where and with what we create the product, and what can turn into money not so soon (so they can be called long-term assets ).

So, here we go:

- A garage, a table, a chair are where we create a product, so a long-term (non-current) asset.

- A sewing machine, tools - this is what we use to create a product - a long-term (non-current) asset.

- A bag with leather and rubber and thread is what a product is made from - a quick (current) asset.

- A safe with money is already real money - a quick (current) asset.

- A phone book with customer numbers - it's hard to sell it to someone quickly, such assets are also called intangible assets and are placed in long-term (non-current) assets.

- IOU from a friend, i.e. a friend bought boots from a master, but can pay only after receiving his salary - a quick (current) asset.

- Shares of an oil company - let's assume that a customer once paid for the boots with them - a long-term (non-current) asset.

So, we've just categorized the master's assets into two groups: current assets (quick assets) and non-current assets (long-term assets). In the next post, we'll break down the components of these two large groups. See you then!

Trading is a waste of time Trading is a waste of time - until you do this!

Welcome back for another exciting video, an educational video, and an eye-opening video for a lot of traders, and I have given it a very, very interesting title that is Trading a Waste of Time.

Let's find out in this short video. Recently reading a book called The Best Loser Wins.

It's written by Tom Hoggard , he goes by the name of Trader Tom on YouTube .And I urge you to check him out. There are some things that I have learned from his book and I'd like to share it with you.

The particular data is of 2019 and these brokers are all located in European Union and, by law they are required to post the failure rates , how many clients are losing money in their market in their accounts.

Out of a hundred clients, 89 clients were in a loss. And the situation is same for almost each and every broking houses.

So eventually the brokers are making money, but the clients are not.

Whenever as a beginner or even a seasoned trader, we are looking at these data and we believe that we are not in this statistical data. We are in the winning percentage in the remaining 10%, but it's not like that for the markets. We are just a statistic. Right? And even if you look at the top 10 broking forms in the world, the majority of people are in a loss.

So that really makes us ask this question. Is trading really a waste of time? Are we just wasting our time in trading? And a lot of people, it's a very fine detail and a lot of people might agree with me that, in the initial stages it's really hard to be consistent in making money, right?

And I'll discuss the reason with you because this particular reason is not discussed.

The social media of Twitter, YouTube, it has all created an image where if you're not doubling your money every month, then you are a loser in the market.

But in fact, trading is a very tough profession and it's really hard to make money and initial days protecting your money is one of the biggest tasks in surviving in the market.

Protecting yourself from ruin is one of the biggest achievements in trading.

So whenever we are starting our journey as a trader, where is our focus? What are the questions we are looking for? What are the things we are usually focused on? , we are on the internet looking for strategies, how to do scalping, how to do seing trading, how to use the indicators, the MACD and RSI, and how we can use different types of breakout indicators, right?

These are the focal points of. I remember when I started trading, these are the things I was looking for. A hundred percent strategy, no loss strategy. These are the things that I was looking for initially, but these are usually the wrong answers.

You know, in an area where 90% people are in a loss, then you need to ask yourself that.

Because it has never been easier to trade because you go back 10 to 15 years, it was not easy to trade. You had to call your broker. And now we have an online trading system where we can just buy and sell stocks at an instant, right?

That leads to high liquidity. And high liquidity usually means you can enter and. Very fast and you don't have to pay much for it. And you have all the tools available, especially a tool like Trading View, where you get each and every trading charts, indicators without paying a single penny.

So it has never ever been easier to trade. So why are we all still losing money? We are only creating brokerage for our broking firm.

This takes us to another and final topic is that in the year 2019, one Forex brokerage firm did an analysis of over 25,000 traders.

And over a span of 15 months or 16 months.

So that is a long period of time and over five crore trades were analyzed.

So it was a very big data to analyze and that would give us a clear picture.

So in that analysis it was recorded that out of hundred. , the traders were profitable in 60 of them and they lost money in 40 of them.

So this is a very good data, right? Your win, your hit ratio is very high in the total amount of trades.

So eventually the data is in your favor, but there's a small catch . When the traders are winning, they're winning 40 points.

And when they lose, they lose around 75 points. This is a recipe for disaster. This particular thing created a lot of problems for me in the initial trades during my initial career.

And this might be creating a lot of problems for people who are trading for the past one or two years in this high VIX environment because, you know, on paper, on week to week basis, you are winning And, and suddenly there's one particular day when you lose it all and that is the day when it drags your capital back to square one.

So this is the biggest reason why it's very difficult for people to manage their trades.

Cause it all comes down to how much you win when you win, and how much you lose when you lose.

This brings us to the concept of risk . right in this modern area, uh, where option selling and creating spreads and selling naked options has been a very famous thing to do for the past couple of years. That is what happens whenever you're selling options, you have a probability of one 68%.

That is a one standard deviation, right?

So out of hundred trades you are going to win in 68% of them. But what you do and how you come out of the remaining 30 trades when the situation is not going to go in your favor, that is all going to matter.

And that is the crux of thing that makes your journey as a successful trader.

Our position in the market is very, very small for the market to know that we even exist or not.

If you look at the data, if you just reverse the win and the loss points, even if you're winning only 50% of the times, then also your position is going to be in a net profit.

So that's it for the guys.

That makes this particular question really interesting. Is trading a waste of time?

You're wasting of time, or are you smart enough to realize this thing that the other traders are doing and are in a loss?

And what are you doing to improve this position and to improve your survival In this market.

So that's it for you guys. I hope I have provided some value in this video, and if you found the video helpful, don't forget to follow me @piyushrawtani Trading View. And if you have any queries, feel free to post it in the comments section.

Thank you very much and good night.

STUDY ( EOD )Understanding where the liquidity in the market is our edge, now note we are not anticipating a change in detraction, but a pullback after the swipe of liquidity at least 20-30 pips pullback, we take advantage of the pullback that why we go deeper to the ltf to look for entry, so we can get into the trade, and know where to get out

Trend Analysis and its Characteristics.MCX:GOLD1!

What is Trend and how to identify it?

A trend is the overall direction of a market or an asset's price.

an uptrend is defined using peak and trough analysis. An uptrend is represented by a series of successively higher highs (peaks) and lows (troughs), while a downtrend is represented by a series of successively lower highs and lows.

->One can identify it by determining peaks and troughs.

->By using trendlines

->Price remaining above or below an overlay indicator.

we can quickly identify the general direction of a market or an asset by looking at the price chart but what we have to learn is to identify the quality of the current trend and how we can do that, by gauging the strength of the trend.

Here are some significant points which help us in understanding the mood and quality of a trend.

The highest skill any trader can aspire to is the ability to read pure price action.

1. Cycle Amplitude

Look for decreasing cycle amplitude in uptrends and downtrends.

A decrease in cycle amplitude in an uptrend is an early indication that there may potentially be an underlying weakness in the uptrend.

In a similar fashion, a decrease in cycle amplitude in a downtrend is regarded as a bullish indication.

2. Cycle Period

A gradual reduction in the cycle period during an uptrend is an early indication that there may potentially be an underlying weakness in the uptrend and a gradual reduction in the cycle period during the downtrend is a bullish indication.

3.Average Bar Range

A decrease in the average bar range in an uptrend and downtrend is an early indication of potential weakness in the current trend.

-> you can track the bar range using the average true range (ATR) oscillator

4.Bar Retracement Symmetry

A change in the number of bars in a retracement is also an early indication of a potential change in trend behaviour.

5. Average Candlestick Real Body to Range Ratio

A gradual decrease in the real body to candlestick range is also an early indication of potential weakness in a Trend.

6. Angular Symmetry and Momentum

Any change in the Angle of trend is significant:-

i.) An upside acceleration in price is bullish whereas an upside deceleration in price is bearish

ii.) A downside acceleration in price is bearish whereas a downside deceleration in price is bullish.

#It should be noted that although an upside acceleration in price is bullish, the uptrend may not be self‐sustaining if the rate of ascent was excessive. Such rapid increases in price usually end in a blow-off or buying climax with prices subsequently collapsing. Similarly, downside acceleration in prices may also end in a selling climax.

7. Frequency and Depth of Trend-Based Oscillations

When a trend moves with reasonable retracements not too short and not too big, it indicates a healthy trend which has profit taking along the way as the trend unfolds.

Traders and investors tend not to react as emotionally and irrationally at higher prices where the risk of losing pent‐up and unrealized profit is greater.

8.Relative Measure of Consolidation Size and Duration

Trend interruptions are more significant if:

■ Price formations are of greater magnitude (taller chart patterns).

■ Price formations develop over a longer period (wider chart patterns).

Larger trend interruptions normally tend to lead to a greater probability of a reversal. In a strong uptrend, a larger head and shoulders formation would be deemed more bearish than a smaller formation. Similarly, a larger rounding bottom formation would be more bullish than a smaller one in a downtrend.

In short, size takes precedence over form. Moreover, the longer it takes for a consolidation to unfold, the greater will be its disruptive power with respect to the trend, should a reversal occur.

By considering these characteristics while analysing trend will give a in depth insight and helps in making more informed and rational decisions.

I Hope you found this helpful.

Please like and comment.

Keep Learning,

Happy Trading!