Institutional Option Writing Strategies1. Understanding Option Writing

In simple terms, option writing involves selling call or put options to another party.

A call option writer agrees to sell an asset at a specified strike price if the buyer exercises the option.

A put option writer agrees to buy the asset at the strike price if exercised.

The writer receives the option premium upfront. If the option expires worthless, the writer keeps the entire premium as profit. Institutions, with their deep capital bases and risk management tools, leverage this structure to earn steady income streams while controlling exposure to extreme price moves.

2. Institutional Objectives Behind Option Writing

Institutions pursue option writing strategies for several key reasons:

Income Generation: Writing options generates regular cash inflows through premiums, especially during low-volatility market phases.

Portfolio Enhancement: Option writing can supplement portfolio returns without requiring additional capital allocation.

Hedging and Risk Management: Institutions may write options to hedge against downside or upside risks in their existing equity or fixed-income portfolios.

Volatility Harvesting: Many institutional traders exploit the difference between implied volatility (reflected in option prices) and realized volatility (actual market movement). When implied volatility is higher, writing options becomes more profitable.

3. Core Institutional Writing Strategies

Institutions employ a range of structured option writing techniques. Below are some of the most common and powerful institutional approaches:

A. Covered Call Writing

Description:

This is one of the most widely used strategies by institutional investors holding long positions in equities or indices. A call option is written against an existing holding.

Example:

If a fund owns 1 million shares of Reliance Industries and expects the price to remain stable or rise moderately, it might sell call options at a higher strike price.

Objective:

Earn option premiums while retaining upside potential (limited to the strike price).

Improve portfolio yield in sideways markets.

Institutional Use Case:

Large mutual funds, ETFs, and pension funds employ systematic covered call writing programs (e.g., the CBOE BuyWrite Index) to generate incremental yield.

B. Cash-Secured Put Writing

Description:

Here, an institution writes put options on securities it is willing to buy at lower prices.

Example:

If an institutional investor wants to purchase Infosys at ₹1,400 while the current market price is ₹1,500, it may sell a ₹1,400 put option. If the price drops, the institution buys the shares effectively at a discounted rate (strike price minus premium).

Objective:

Acquire desired stocks at a lower effective price.

Earn premiums if the option expires worthless.

Institutional Use Case:

Hedge funds and asset managers use this as a buy-entry strategy to accumulate equities in a disciplined manner.

C. Short Straddles and Strangles

Description:

These are non-directional premium harvesting strategies.

A short straddle involves selling both a call and a put at the same strike price.

A short strangle involves selling out-of-the-money (OTM) calls and puts at different strike prices.

Objective:

Profit from time decay and low realized volatility, as the position benefits when the underlying remains range-bound.

Institutional Use Case:

Market-making firms and volatility funds often employ delta-neutral short volatility trades, dynamically hedging exposure with futures or underlying assets to capture theta (time decay).

D. Covered Put Writing (or Reverse Conversion)

Description:

Institutions short the underlying asset and sell a put option simultaneously. This is effectively a synthetic short call position.

Objective:

Generate income from premium while holding a bearish outlook.

Institutional Use Case:

Used by proprietary desks to benefit from short-term bearish sentiment in overvalued stocks or indices.

E. Iron Condors and Iron Butterflies

Description:

These are advanced multi-leg strategies combining short straddles/strangles with long options for limited risk exposure.

Example:

An iron condor involves selling a short strangle and buying further OTM options as protection.

Objective:

Collect premium in range-bound markets while capping potential losses.

Institutional Use Case:

Quantitative hedge funds and volatility arbitrage desks often implement automated iron condor portfolios to capture small, consistent returns.

4. Risk Management in Institutional Option Writing

Unlike retail traders who often underestimate risk, institutions deploy rigorous frameworks to manage exposure. Some key practices include:

Delta Hedging: Institutions continuously adjust their underlying asset positions to maintain a neutral delta, reducing directional risk.

Value-at-Risk (VaR) Modeling: Quantitative models assess potential losses from adverse market movements.

Portfolio Diversification: Writing options across multiple securities, expirations, and strikes reduces concentration risk.

Volatility Analysis: Institutions track implied vs. realized volatility spreads to identify favorable conditions for selling options.

Position Limits: Regulatory and internal risk limits prevent overexposure to specific assets or strikes.

Dynamic Adjustments: Algorithms monitor changing market conditions to rebalance or exit positions.

5. Quantitative and Algorithmic Enhancements

Modern institutions integrate machine learning, data analytics, and algorithmic trading into their option writing programs. Some methods include:

Statistical Arbitrage Models: Exploit mispricing between options and underlying securities.

Volatility Forecasting: AI-driven models predict short-term volatility to optimize strike and expiration selection.

Automated Execution: Algorithms manage large-scale multi-leg option portfolios efficiently.

Gamma Scalping: Automated hedging against volatility swings ensures steady theta profits.

These advanced systems allow institutions to operate with precision and scalability impossible for manual traders.

6. Market Conditions Favorable for Option Writing

Institutional writers thrive under certain market conditions:

Stable or Sideways Markets: Time decay (theta) works in favor of sellers.

High Implied Volatility: Premiums are inflated, offering better reward-to-risk ratios.

Interest Rate Stability: Predictable macroeconomic conditions help maintain market equilibrium.

However, during periods of high market uncertainty—such as financial crises or unexpected geopolitical shocks—institutions may reduce or hedge their short volatility exposure aggressively.

7. Regulatory and Compliance Considerations

Institutions are subject to stringent SEBI, CFTC, and exchange-level regulations when engaging in derivatives trading. They must maintain adequate margin requirements, adhere to risk disclosure norms, and report large open positions. Compliance systems automatically monitor exposure to ensure adherence to capital adequacy and position limits.

8. Advantages of Institutional Option Writing

Consistent Income Generation through premium collection.

Portfolio Stability by offsetting volatility.

Improved Capital Efficiency through margin optimization.

Systematic and Scalable execution via automation.

Enhanced Long-Term Returns through disciplined risk-managed exposure.

9. Risks and Challenges

Despite its appeal, option writing carries notable risks:

Unlimited Loss Potential: Particularly in uncovered call writing.

Volatility Spikes: Sudden market swings can cause large mark-to-market losses.

Liquidity Risk: Difficulties in adjusting large positions in fast-moving markets.

Margin Pressure: Rising volatility increases margin requirements, straining liquidity.

Execution Complexity: Requires sophisticated systems and continuous monitoring.

Institutions mitigate these risks through diversified, hedged, and dynamically managed portfolios.

10. Conclusion

Institutional option writing strategies represent a disciplined, risk-controlled approach to generating consistent returns in both bullish and neutral markets. Unlike speculative option buyers, institutional writers rely on probability, volatility analysis, and quantitative precision to achieve a long-term edge.

Through methods like covered calls, put writing, iron condors, and straddles, institutions systematically capture time decay and volatility premiums. Supported by advanced risk models and algorithmic execution, these strategies transform options from speculative instruments into powerful tools for income generation and portfolio optimization.

When executed with prudence and robust risk management, institutional option writing can serve as a cornerstone of stable, repeatable performance in modern financial markets.

Chart Patterns

Risk in Option Trading: Segments of Financial Markets1. Introduction to Options and Risk

Options are derivative instruments that give traders the right but not the obligation to buy (call option) or sell (put option) an underlying asset at a specified price (strike price) within a set time frame. While this flexibility can amplify profits, it can also magnify losses if the market moves unfavorably.

Unlike simple stock trading where risk is typically limited to the capital invested, option trading can expose traders to theoretically unlimited losses, depending on the strategy used. This complexity makes understanding option-related risks critical for both retail and institutional investors.

2. Types of Risks in Option Trading

Option trading involves several interconnected types of risk. The major categories include market risk, volatility risk, time decay (theta) risk, liquidity risk, and operational risk. Let’s explore each in detail.

A. Market Risk (Directional Risk)

Market risk, also known as directional risk, refers to the possibility of losing money due to adverse price movements in the underlying asset.

For Call Options: The risk arises if the price of the underlying asset fails to rise above the strike price before expiry. In this case, the option expires worthless, and the premium paid is lost.

For Put Options: The risk occurs if the price of the underlying fails to fall below the strike price, leading to a total loss of the premium.

For Option Sellers: The market risk is even higher. A call writer (seller) faces theoretically unlimited losses if the underlying price keeps rising, while a put writer can suffer heavy losses if the price falls drastically.

For example, if a trader sells a naked call on a stock trading at ₹1,000 with a strike price of ₹1,050 and the stock rallies to ₹1,200, the seller faces huge losses as they may have to deliver shares at ₹1,050 while buying them at ₹1,200 in the market.

B. Volatility Risk (Vega Risk)

Volatility is one of the most important factors influencing option prices. It reflects how much the underlying asset’s price fluctuates. Vega measures the sensitivity of an option’s price to changes in implied volatility.

High Volatility: Increases the premium of both call and put options because the probability of large price swings rises.

Low Volatility: Decreases option premiums as the likelihood of significant price movement reduces.

Traders holding long options (buyers) benefit from rising volatility since it inflates option prices. Conversely, sellers (writers) are hurt when volatility rises, as they may need to buy back the options at a higher premium.

The challenge arises when volatility changes unexpectedly. Even if the direction of the underlying asset moves favorably, a fall in volatility can reduce the option’s value — leading to losses despite being "right" about the price movement.

C. Time Decay Risk (Theta Risk)

Time decay (Theta) is a silent killer for option buyers. Options lose value as they approach expiration because the probability of a significant price move declines with time.

For Buyers: Each passing day erodes the option’s extrinsic value, even if the market doesn’t move. If the underlying asset doesn’t move as expected within a limited time, the option can expire worthless.

For Sellers: Time decay works in their favor. They benefit as the option’s value decreases over time, allowing them to buy it back at a lower price or let it expire worthless.

For instance, if an investor buys a call option for ₹100 with one week to expiry and the underlying asset stays flat, the option may fall to ₹40 simply due to time decay, even though the price hasn’t changed.

D. Liquidity Risk

Liquidity risk refers to the difficulty of entering or exiting a position without significantly affecting the market price. In illiquid options (those with low trading volumes and wide bid-ask spreads), traders may have to buy at a higher price and sell at a lower one, reducing profitability.

A wide bid-ask spread can erode returns and make stop-loss strategies ineffective. For example, an option quoted at ₹10 (bid) and ₹15 (ask) has a ₹5 spread — meaning a trader buying at ₹15 might only be able to sell at ₹10 immediately, losing ₹5 instantly.

This is particularly common in options of less popular stocks or far out-of-the-money strikes.

E. Leverage Risk

Options provide built-in leverage. With a small investment, traders can control a large notional value of the underlying asset. While this magnifies potential gains, it also amplifies losses.

For example, if a ₹50 premium option controls 100 shares, the total exposure is ₹5,000. A 50% move in the option’s value results in a ₹2,500 change, equating to a 50% gain or loss on the entire investment. Such leverage can be disastrous without proper risk management.

F. Assignment and Exercise Risk

For option sellers, there is always the risk of assignment, meaning they might be forced to deliver (in the case of calls) or buy (in the case of puts) the underlying asset before expiration if the buyer chooses to exercise early.

In American-style options, early exercise can happen anytime before expiration, catching the seller off guard. This can lead to unexpected margin requirements or losses, especially around dividend dates or earnings announcements.

G. Margin and Leverage Risk for Sellers

Selling options requires maintaining a margin deposit. If the market moves against the position, brokers can issue a margin call demanding additional funds. Failure to meet it can result in forced liquidation at unfavorable prices.

Because potential losses for naked option writers are theoretically unlimited, many traders face catastrophic losses when they fail to manage margin requirements properly.

H. Event and Gap Risk

Market-moving events such as earnings announcements, policy changes, or geopolitical developments can lead to sudden price gaps. These gaps can cause significant losses, especially for short-term traders or option sellers.

For example, if a company reports poor earnings overnight and its stock opens 20% lower the next day, all short put sellers will face massive losses instantly, often before they can react.

I. Psychological and Behavioral Risks

Option trading requires discipline, emotional control, and quick decision-making. Greed, fear, and overconfidence can lead traders to take excessive risks or hold losing positions too long. The complexity of options also tempts traders to overtrade, increasing transaction costs and exposure.

3. Managing Risks in Option Trading

While risks are inherent, they can be managed effectively with proper strategies and discipline:

Position Sizing: Never risk more than a small percentage of total capital on a single trade.

Stop-Loss Orders: Use stop-loss mechanisms to limit downside risk.

Hedging: Combine long and short options to reduce exposure (e.g., spreads or straddles).

Diversification: Avoid concentrating positions in one stock or sector.

Monitor Greeks: Regularly track Delta, Theta, Vega, and Gamma to understand sensitivity to market factors.

Avoid Naked Positions: Prefer covered calls or cash-secured puts over naked options.

Stay Informed: Be aware of corporate events, macroeconomic announcements, and volatility trends.

Paper Trade First: Beginners should practice with virtual trades before using real money.

4. Conclusion

Option trading offers immense profit potential but carries significant risk due to leverage, volatility, and time sensitivity. The same features that make options powerful tools for speculation or hedging can also make them dangerous for uninformed traders.

Successful option traders understand that managing risk is more important than chasing returns. By combining knowledge of market dynamics, disciplined strategies, and proper risk management, traders can navigate the complex world of options effectively and sustainably.

Premium Charts Tips for Successful Option Trading

Master the basics before applying advanced strategies.

Analyze market trends, OI data, and IV regularly.

Use proper risk management—never risk more than 1–2% of capital per trade.

Avoid trading near major events (earnings, RBI policy) unless experienced.

Keep learning through backtesting and continuous strategy refinement.

Part 12 Trading Masster ClassOption Trading in India

In India, options are traded on exchanges like the NSE (National Stock Exchange) and BSE (Bombay Stock Exchange). The most active instruments include NIFTY, BANKNIFTY, and FINNIFTY indices, as well as popular stocks like Reliance, TCS, and HDFC Bank.

Indian traders have access to weekly and monthly expiries, providing short-term opportunities. SEBI regulates derivatives trading to ensure transparency and protect investors. Margin requirements, contract sizes, and position limits are predefined to manage systemic risk.

Part 11 Trading Masster ClassRole of Implied Volatility (IV) and Open Interest (OI)

Implied Volatility (IV): Indicates expected market volatility. Rising IV increases option premiums. Traders buy options during low IV and sell during high IV.

Open Interest (OI): Reflects the number of outstanding option contracts. Rising OI with price indicates strong trend confirmation, while divergence signals reversals.

These metrics help traders assess market sentiment and build informed positions.

Part 10 Trade Like InstitutionsOption Buying vs. Option Selling

Option Buyers have limited risk (premium paid) and unlimited potential profit. However, time decay works against them as Theta reduces the option’s value daily.

Option Sellers (Writers) have limited profit (premium received) but potentially unlimited risk. Sellers benefit from time decay and stable markets.

In the Indian market, most professional traders and institutions prefer option selling due to the high success rate when markets remain range-bound.

Pat 9 Tradig Master ClassThe Greeks in Options

The Greeks measure the sensitivity of an option’s price to various factors:

Delta: Measures how much the option’s price changes for a ₹1 move in the underlying asset.

Gamma: Measures the rate of change of delta; it helps traders understand how delta will change as the market moves.

Theta: Measures time decay—how much the option loses value each day as expiration approaches.

Vega: Measures sensitivity to volatility changes.

Rho: Measures sensitivity to interest rate changes.

Understanding these helps traders manage risk and create balanced strategies.

Part 8 Trading Master ClassOption Pricing

Option prices depend on several factors, collectively described by the Black-Scholes model. The main components are:

Underlying price: The current price of the stock or index.

Strike price: Determines whether the option is ITM, ATM, or OTM.

Time to expiration: Longer duration means higher premium, as there’s more time for the market to move favorably.

Volatility: Higher volatility increases premium since price movements are more unpredictable.

Interest rates and dividends: These have smaller effects but are still part of option pricing.

The relationship between these factors is known as the “Greeks.”

Part 7 Trading Master ClassBasic Terminology

To understand option trading, one must know a few key terms:

Strike Price: The price at which the underlying asset can be bought (call) or sold (put).

Premium: The price paid by the buyer to the seller for the option contract.

Expiration Date: The date on which the option contract expires. In India, options typically expire every Thursday (for weekly options) or the last Thursday of the month (for monthly options).

In-the-Money (ITM): A call option is ITM when the market price is above the strike price; a put option is ITM when the market price is below the strike price.

Out-of-the-Money (OTM): A call is OTM when the market price is below the strike, and a put is OTM when the market price is above the strike.

At-the-Money (ATM): When the market price and strike price are roughly equal.

Part 6 Learn Institutional Trading What Are Options?

An option is a financial derivative whose value is based on an underlying asset—such as stocks, indices, or commodities. The two main types of options are:

Call Option: Gives the holder the right to buy an asset at a specific price (called the strike price) before or on the expiration date.

Put Option: Gives the holder the right to sell an asset at a specific strike price before or on the expiration date.

The buyer of an option pays a premium to the seller (writer) for this right. The seller, in return, assumes an obligation—if the buyer exercises the option, the seller must fulfill the contract terms.

Option Buying vs Option Selling in the Indian Market1. Understanding Options in Brief

An option is a financial derivative contract that gives the buyer the right, but not the obligation, to buy or sell an underlying asset (such as Nifty, Bank Nifty, or stocks) at a predetermined price (strike price) before or on a specific date (expiry date).

Call Option (CE): Gives the buyer the right to buy the asset.

Put Option (PE): Gives the buyer the right to sell the asset.

The seller (also known as the writer) of an option, on the other hand, has the obligation to fulfill the contract if the buyer decides to exercise it.

2. Option Buying – The Right Without Obligation

Definition:

When a trader buys an option, they pay a premium to acquire the right to buy (Call) or sell (Put) the underlying asset. This is a leveraged position where the maximum loss is limited to the premium paid.

Example:

Suppose Nifty is trading at 22,000 and a trader buys a 22,000 CE at ₹150. If Nifty rises to 22,400 by expiry, the option may be worth ₹400, giving a profit of ₹250 (₹400 - ₹150).

If Nifty falls or remains below 22,000, the option expires worthless, and the buyer loses ₹150 (premium).

Advantages of Option Buying:

Limited Risk: The maximum loss is limited to the premium paid.

Unlimited Profit Potential: Profits can be substantial if the underlying asset moves sharply in the expected direction.

Leverage: Traders can control large positions with a small amount of capital.

Hedging Tool: Option buyers can hedge existing stock or portfolio positions against adverse movements.

Simplicity: Easier to understand for beginners as risks are predefined.

Disadvantages of Option Buying:

Time Decay (Theta): The value of options erodes as expiry approaches if the price does not move favorably.

Low Probability of Success: Most options expire worthless; hence, consistent profitability is difficult.

Implied Volatility (IV) Risk: A drop in volatility can reduce option prices even if the direction is correct.

Requires Precise Timing: The move in the underlying must be quick and significant to overcome time decay.

3. Option Selling – The Power of Probability

Definition:

Option sellers (writers) receive a premium by selling (writing) options. They are obligated to fulfill the contract if the buyer exercises it. Sellers profit when the market remains stable or moves against the option buyer’s position.

Example:

If a trader sells a Nifty 22,000 CE at ₹150 and Nifty remains below 22,000 till expiry, the seller keeps the entire ₹150 premium as profit. However, if Nifty rises to 22,400, the seller incurs a loss of ₹250 (₹400 - ₹150).

Advantages of Option Selling:

High Probability of Profit: Since most options expire worthless, sellers statistically have better odds.

Benefit from Time Decay: Sellers gain as the option premium reduces with each passing day.

Volatility Advantage: When volatility drops, option prices fall, benefiting sellers.

Range-Bound Profitability: Sellers can profit even in sideways markets, unlike buyers who need strong price movement.

Disadvantages of Option Selling:

Unlimited Risk: Losses can be theoretically unlimited, especially for uncovered (naked) positions.

Margin Requirement: Sellers must maintain significant margin with brokers, reducing leverage.

Emotional Stress: Constant monitoring is needed as rapid moves in the market can cause heavy losses.

Complex Strategies Required: Often, sellers use spreads or hedges to control risk, which requires advanced knowledge.

4. Market Behavior and Strategy Selection

Option Buyers Thrive When:

The market makes sharp and fast movements in a particular direction.

Implied volatility is low before the trade and increases later.

There is a news event or earnings announcement expected to cause large swings.

The trend is strong and directional (e.g., breakout setups).

Example Strategies for Buyers:

Long Call or Long Put

Straddle or Strangle (when expecting volatility)

Call Debit Spread or Put Debit Spread

Option Sellers Succeed When:

The market remains range-bound or moves slowly.

Implied volatility is high at the time of entry and drops later.

Time decay favors them as expiry nears.

The trader expects no major event or breakout.

Example Strategies for Sellers:

Short Straddle / Short Strangle

Iron Condor

Credit Spreads (Bull Put Spread, Bear Call Spread)

Covered Call Writing

5. Role of Implied Volatility (IV) and Time Decay

In the Indian market, IV and Theta play crucial roles in deciding profitability.

For Buyers:

They need an increase in IV (expectation of higher movement). Rising IV inflates option premiums, helping buyers.

For Sellers:

They gain when IV drops (post-event or consolidation), as option prices fall.

Time Decay (Theta) always works against buyers and in favor of sellers. For example, in the last week before expiry, options lose value rapidly if the underlying does not move significantly.

6. Regulatory and Practical Considerations in India

Margins: SEBI’s framework requires SPAN + Exposure margin, making naked selling capital-intensive.

Liquidity: Nifty, Bank Nifty, and FinNifty have high liquidity, making both buying and selling viable.

Taxation: Option profits are treated as business income for both buyers and sellers.

Brokerage and Slippage: Active option sellers often face higher transaction costs due to large volumes.

Retail Participation: Most retail traders prefer buying options due to low capital requirements, while professional traders prefer selling for steady income.

7. Real-World Insights

Around 70–80% of retail traders in India buy options, but most lose money due to time decay and poor timing.

Professional traders and institutions prefer option writing using hedged strategies to generate consistent returns.

Successful traders often combine both — buying for directional plays and selling for income generation.

8. Which Is Better – Buying or Selling?

There’s no one-size-fits-all answer. It depends on market conditions, trading capital, and risk appetite.

If you have small capital, prefer buying options with strict stop-loss and a clear directional view.

If you have large capital and can manage risk with spreads or hedges, selling options can provide consistent returns.

Combining both (for example, selling options in high volatility and buying in low volatility) can create balance.

Conclusion

The debate between option buying and option selling in the Indian market revolves around risk vs. probability. Option buyers enjoy limited risk and unlimited profit potential but low success rates. Option sellers face higher risk but benefit from time decay and probability in their favor.

In essence:

Buy options when expecting a big, fast move.

Sell options when expecting a range-bound or stable market.

A disciplined approach, risk management, and understanding of volatility are the keys to succeeding in either strategy. In the dynamic Indian derivatives market, mastering both sides of the trade — when to buy and when to sell — transforms an ordinary trader into a consistently profitable one.

Implied Volatility and Open Interest Analysis1. Understanding Implied Volatility (IV)

Implied Volatility is a metric derived from the market price of options that reflects the market’s expectations of future volatility in the price of the underlying asset. Unlike historical volatility, which measures past price fluctuations, IV is forward-looking—it tells us how much the market expects the asset to move in the future.

Key Characteristics of IV:

Expressed in percentage terms, showing the expected annualized movement in the underlying asset.

Does not predict direction—only the magnitude of expected price swings.

Higher IV means the market expects larger price movements (high uncertainty or fear).

Lower IV means smaller expected price movements (stability or complacency).

Factors Influencing Implied Volatility:

Market sentiment: During uncertainty or events like elections, budgets, or economic announcements, IV tends to rise.

Supply and demand for options: Heavy buying of options increases IV, while heavy selling reduces it.

Time to expiration: Longer-duration options usually have higher IV due to greater uncertainty over time.

Earnings or corporate events: Stocks often show rising IV ahead of quarterly earnings announcements.

2. Interpreting Implied Volatility

High IV Environment:

When IV is high, option premiums are expensive. This generally indicates:

Traders expect significant movement (up or down).

Fear or uncertainty is present in the market.

Volatility sellers (option writers) might see an opportunity to sell overpriced options.

For example, before major events like the Union Budget or RBI policy meeting, IV in Nifty options typically spikes due to the anticipated market reaction.

Low IV Environment:

When IV is low, option premiums are cheaper. This usually means:

The market expects calm or limited movement.

Traders may be complacent.

Volatility buyers might see an opportunity to buy options cheaply before an expected rise in volatility.

Implied Volatility Rank (IVR) and IV Percentile:

IV Rank compares current IV to its range over the past year.

Example: An IV Rank of 80 means current IV is higher than 80% of the past year’s readings.

IV Percentile shows the percentage of time IV has been below current levels.

Both help traders decide if options are cheap or expensive relative to history.

3. Understanding Open Interest (OI)

Open Interest represents the total number of outstanding option or futures contracts that are currently open (not yet closed, exercised, or expired). It indicates the total participation or liquidity in a particular strike or contract.

For example, if a trader buys 1 Nifty 22000 Call and another trader sells it, OI increases by one contract. If later that position is closed, OI decreases by one.

Key Aspects of OI:

Rising OI with rising prices = new money entering the market (bullish).

Rising OI with falling prices = fresh short positions (bearish).

Falling OI with rising or falling prices = unwinding of positions (profit booking or exit).

Stable OI = sideways or consolidating market.

4. How to Read Open Interest Data

OI and Price Relationship:

Price Trend OI Trend Market Interpretation

↑ Price ↑ OI Long build-up (bullish)

↓ Price ↑ OI Short build-up (bearish)

↑ Price ↓ OI Short covering (bullish)

↓ Price ↓ OI Long unwinding (bearish)

For example, if Nifty futures rise by 150 points and OI increases, traders are opening new long positions, suggesting bullishness. But if prices rise while OI falls, short positions are being covered.

5. Using OI in Option Chain Analysis

In options trading, OI is especially useful for identifying support and resistance zones.

High Call OI indicates a potential resistance level because sellers expect the price to stay below that strike.

High Put OI indicates a potential support level because sellers expect the price to stay above that strike.

For instance:

If Nifty has maximum Call OI at 22500 and maximum Put OI at 22000, traders consider this as a range of consolidation (22000–22500).

A breakout above 22500 or breakdown below 22000 with sharp OI changes can signal a shift in trend.

6. Combining IV and OI for Better Insights

Using IV and OI together gives a more complete picture of the market’s mindset.

Scenario 1: Rising IV + Rising OI

Indicates strong speculative activity.

Traders expect big moves, either due to events or upcoming volatility.

Suitable for straddle or strangle buyers.

Scenario 2: Falling IV + Rising OI

Implies calm market conditions with new positions being built.

Traders expect limited movement.

Suitable for option writing strategies (like Iron Condor, Short Straddle).

Scenario 3: Rising IV + Falling OI

Suggests short covering or unwinding due to fear.

Market participants are closing existing positions amid uncertainty.

Scenario 4: Falling IV + Falling OI

Indicates profit booking after a volatile phase.

Usually happens in post-event consolidation.

7. Practical Example: Nifty Option Chain Analysis

Suppose the Nifty 50 index is trading around 22,300.

Strike Call OI Put OI IV (Call) IV (Put)

22,000 4.8 L 6.2 L 15% 16%

22,300 5.5 L 5.1 L 17% 18%

22,500 7.8 L 3.9 L 20% 17%

Here:

Maximum Call OI at 22,500 → Resistance zone.

Maximum Put OI at 22,000 → Support zone.

IV is rising across strikes → traders expect upcoming volatility.

If price moves above 22,500 and Call writers exit (OI drops), while new Put OI builds, it signals a bullish breakout.

8. Role of IV and OI in Strategy Selection

High IV Strategies (Volatile Market):

Buy Straddle or Strangle (expecting large movement)

Calendar Spread

Long Vega strategies

Low IV Strategies (Stable Market):

Iron Condor

Short Straddle

Covered Call

Credit Spreads

OI data helps traders identify which strikes to select for these strategies and where the market might reverse or consolidate.

9. Limitations of IV and OI Analysis

While powerful, both metrics have limitations:

IV can be misleading before major events; it reflects expectations, not certainty.

OI data is end-of-day in many cases, so intraday traders might miss rapid shifts.

Sharp OI changes might also result from rollovers or hedging adjustments, not directional bias.

Hence, traders must use IV and OI along with price action, volume, and trend indicators for confirmation.

10. Conclusion

Implied Volatility and Open Interest form the foundation of options market sentiment analysis.

IV tells us what the market expects to happen in terms of movement magnitude.

OI tells us how much participation or commitment traders have in the current trend.

Together, they reveal a deeper layer of market psychology—identifying whether traders are fearful, greedy, hedging, or speculating.

For successful trading, combining price action + IV + OI enables traders to forecast volatility cycles, confirm trends, and time their entries or exits effectively.

In essence, mastering IV and OI analysis empowers traders to read the invisible hand of market sentiment—a crucial skill for anyone in the derivatives market.

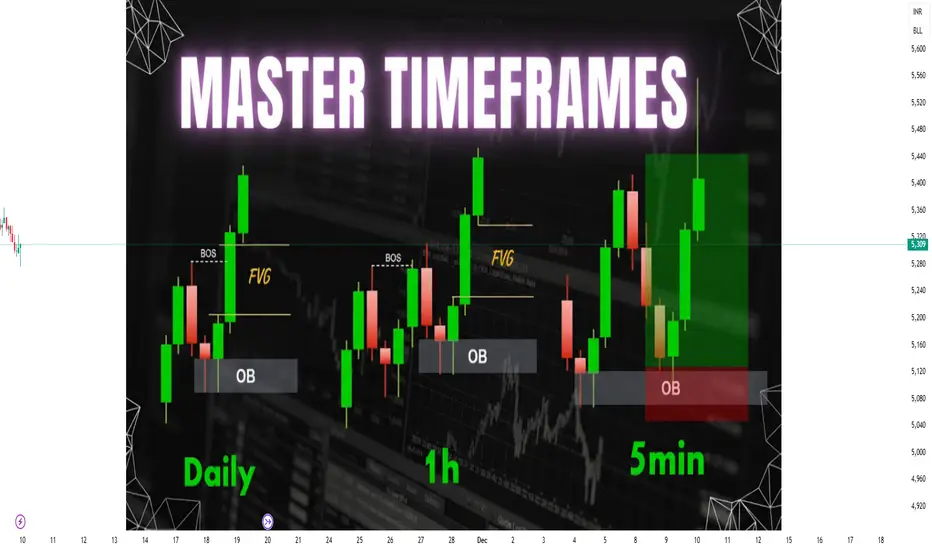

Multi-Timeframe Analysis (Intraday, Swing, Positional)1. Understanding Multi-Timeframe Analysis

Multi-Timeframe Analysis refers to the process of observing the same security across different timeframes to identify trend alignment, potential reversal zones, and optimal trading opportunities. Every timeframe provides unique insights:

Higher Timeframe: Defines the major trend and key support/resistance zones.

Intermediate Timeframe: Helps identify swing trends within the larger move.

Lower Timeframe: Provides precise entry and exit signals.

For example, a trader analyzing Nifty 50 might observe:

Daily Chart (Positional) for the overall trend direction.

Hourly Chart (Swing) for intermediate momentum.

15-Minute Chart (Intraday) for entry confirmation.

This top-down approach ensures that trades are placed in harmony with the broader market movement rather than against it.

2. The Logic Behind Multi-Timeframe Analysis

Financial markets are fractal in nature, meaning patterns repeat on various time scales. A breakout on a 5-minute chart might just be a retracement on a 1-hour chart, while a downtrend on a daily chart could appear as a bullish trend on a 15-minute chart.

MTA helps traders:

Identify dominant trends (macro view).

Spot short-term countertrends (micro adjustments).

Time entries with high probability setups.

Essentially, it synchronizes multiple layers of information to produce well-informed trading decisions.

3. Types of Traders and Timeframes

Each trader category operates within different time horizons:

A. Intraday Traders

Objective: Capture small price moves within a single trading day.

Timeframes Used: 1-minute, 5-minute, 15-minute, and 1-hour charts.

Holding Period: A few minutes to several hours.

Example: A trader identifies a bullish breakout on the 15-minute chart, confirms strength on the 5-minute chart, and exits before the market close.

B. Swing Traders

Objective: Ride short to medium-term trends lasting several days or weeks.

Timeframes Used: 1-hour, 4-hour, and daily charts.

Holding Period: 2 to 15 days typically.

Example: A bullish pattern on the daily chart confirmed by a 4-hour breakout helps the trader capture a multi-day price rally.

C. Positional Traders

Objective: Trade major trends that can last from weeks to months.

Timeframes Used: Daily, weekly, and monthly charts.

Holding Period: Several weeks to many months.

Example: A trader identifies a long-term uptrend on the weekly chart and holds positions through short-term fluctuations.

Each trader uses MTA to align smaller trends within the context of larger ones.

4. The Top-Down Approach

The Top-Down Approach is a systematic method of conducting multi-timeframe analysis. It involves starting with the highest relevant timeframe and drilling down to lower timeframes for precision.

Step 1: Identify the Major Trend (Higher Timeframe)

Use weekly or daily charts to determine the broader market direction.

Apply moving averages, trendlines, or price structure (higher highs and higher lows).

Example: On the weekly chart, Nifty 50 is in an uptrend.

Step 2: Confirm Momentum (Intermediate Timeframe)

Switch to a 4-hour or 1-hour chart to check if the momentum supports the higher timeframe trend.

Look for consolidation, breakouts, or pullbacks.

Step 3: Refine Entry and Exit (Lower Timeframe)

Use 15-minute or 5-minute charts to time entries and exits.

Identify short-term support, resistance, and candlestick patterns for precision.

This method ensures alignment between long-term direction and short-term trade execution, minimizing false signals and improving accuracy.

5. Example of Multi-Timeframe Analysis in Action

Let’s illustrate with an example:

Weekly Chart (Positional View): Shows a strong uptrend with price above 50-day moving average.

Daily Chart (Swing View): Reveals a bullish flag pattern forming after a rally.

Hourly Chart (Intraday View): Displays a breakout above the flag resistance with volume confirmation.

A positional trader may initiate a long position based on weekly strength, while a swing trader enters after the daily flag breakout. An intraday trader could use the hourly chart to time the exact breakout candle entry.

All three traders align their strategies to the same trend but operate on different time horizons.

6. Tools and Indicators Used in Multi-Timeframe Analysis

Several tools enhance the effectiveness of MTA:

Moving Averages (MA): Identify trend direction and alignment across timeframes (e.g., 20 EMA, 50 SMA).

Relative Strength Index (RSI): Helps confirm momentum consistency.

MACD: Detects shifts in momentum and crossovers aligning with major trends.

Support and Resistance Levels: Define crucial zones visible across charts.

Trendlines and Channels: Show structure of price swings.

Candlestick Patterns: Confirm entry signals on smaller timeframes.

Combining these tools across multiple frames builds confluence—an essential component of successful trading.

7. Advantages of Multi-Timeframe Analysis

Trend Confirmation:

Confirms whether short-term movements align with the long-term trend, improving accuracy.

Reduced False Signals:

Helps filter noise from smaller charts that may mislead traders.

Enhanced Entry Timing:

Allows traders to enter trades at precise moments when all timeframes agree.

Better Risk Management:

By aligning with larger trends, traders can define stop-loss and target levels more logically.

Adaptability Across Strategies:

Suitable for scalping, swing trading, or long-term investing.

8. Challenges in Multi-Timeframe Analysis

While MTA is powerful, it also presents certain difficulties:

Information Overload: Analyzing multiple charts can cause confusion or analysis paralysis.

Conflicting Signals: Short-term and long-term charts may show opposite trends, requiring trader judgment.

Execution Complexity: Managing entries and exits across multiple timeframes demands discipline and experience.

Emotional Bias: Traders may get biased by one timeframe and ignore contradictory evidence.

Therefore, consistency in analysis and clear trading rules are vital to prevent confusion.

9. Tips for Effective Multi-Timeframe Trading

Always start with higher timeframes before moving down.

Use a ratio of 1:4 or 1:6 between timeframes (e.g., daily → 4-hour → 1-hour).

Focus on key support/resistance levels visible across multiple frames.

Avoid overcomplicating; two or three timeframes are usually enough.

Maintain a trading journal to note observations from each timeframe.

Use alerts or automated tools to monitor price behavior when multiple charts are involved.

10. Conclusion

Multi-Timeframe Analysis is not just a technique but a strategic framework that enhances decision-making across trading styles—whether intraday, swing, or positional. By combining insights from different timeframes, traders gain a holistic view of the market, identify high-probability setups, and reduce the risk of false entries.

For intraday traders, MTA refines timing; for swing traders, it offers trend confirmation; and for positional traders, it ensures long-term alignment. When executed with discipline, proper analysis, and risk control, Multi-Timeframe Analysis becomes one of the most reliable methods to trade profitably in volatile markets like India’s NSE and BSE.

AI and Machine Learning in Stock Market Forecasting1. Introduction to AI and Machine Learning in Finance

Artificial Intelligence refers to the simulation of human intelligence in machines that can learn, reason, and make decisions. Machine Learning, a subset of AI, involves algorithms that improve automatically through experience. In finance, AI and ML are used to analyze market data, forecast trends, and automate trading strategies.

Unlike traditional statistical models that rely on fixed mathematical relationships, ML models adapt dynamically to changing market conditions. This adaptability makes them particularly useful in forecasting stock prices, where patterns are non-linear, complex, and influenced by multiple interacting variables.

2. Traditional Methods vs. AI-Based Forecasting

Traditional stock market forecasting techniques — such as fundamental analysis, technical analysis, and econometric models — depend heavily on historical data and human interpretation. These models often assume linear relationships and static patterns, which may not hold true in volatile markets.

In contrast, AI and ML models can process:

Large volumes of structured and unstructured data

Non-linear dependencies

Real-time information updates

For example, a traditional regression model may struggle to account for sudden market shocks, whereas an ML algorithm can learn from data anomalies and adapt to new market behaviors through continuous learning.

3. Machine Learning Techniques in Stock Market Forecasting

AI-driven forecasting utilizes various ML algorithms, each suited for different kinds of financial predictions:

a. Supervised Learning

Supervised learning algorithms are trained using labeled historical data — for example, past stock prices and associated indicators — to predict future values. Common models include:

Linear and Logistic Regression

Support Vector Machines (SVM)

Random Forests

Gradient Boosting Machines (XGBoost, LightGBM)

These algorithms can forecast future price movements, classify stocks as “buy,” “hold,” or “sell,” and identify potential risks.

b. Unsupervised Learning

In unsupervised learning, algorithms detect hidden patterns in data without labeled outcomes. Techniques like K-Means Clustering and Principal Component Analysis (PCA) are used to:

Identify stock groupings with similar behavior

Detect anomalies or unusual trading activities

Segment markets based on volatility or performance trends

c. Deep Learning

Deep Learning models, particularly Recurrent Neural Networks (RNNs) and Long Short-Term Memory (LSTM) networks, are highly effective in time-series forecasting.

These models capture temporal dependencies — such as how past price movements influence future prices — and are capable of handling sequential data efficiently.

For instance, an LSTM model can analyze years of price history, trading volume, and sentiment data to forecast the next day’s closing price.

d. Reinforcement Learning

Reinforcement Learning (RL) is a powerful AI approach where algorithms learn optimal trading strategies through trial and error. The system receives rewards for profitable trades and penalties for losses, gradually learning to maximize returns.

RL is increasingly used in algorithmic trading systems that make autonomous buy/sell decisions based on real-time market data.

4. Data Sources for AI-Based Forecasting

AI and ML models rely on diverse data sources to generate accurate predictions:

Historical Market Data: Price, volume, volatility, and returns over time.

Fundamental Data: Earnings, balance sheets, and macroeconomic indicators.

Alternative Data: News sentiment, social media trends, Google searches, and even satellite imagery.

Technical Indicators: Moving averages, RSI, MACD, and Bollinger Bands.

By integrating structured (numerical) and unstructured (text, images) data, AI models can capture market sentiment and detect emerging trends that traditional models may overlook.

5. Applications of AI and ML in Stock Forecasting

a. Price Prediction

Machine learning models are used to forecast short-term and long-term price movements. Algorithms such as LSTMs and Random Forests analyze time-series data to predict next-day or next-week stock prices.

b. Sentiment Analysis

Natural Language Processing (NLP), a branch of AI, interprets financial news, analyst reports, and social media content to gauge market sentiment.

For example, a surge in negative news sentiment about a company may signal an upcoming drop in its stock price.

c. Portfolio Optimization

AI systems analyze correlations among different assets and optimize portfolios to maximize returns while minimizing risk. Tools like Markowitz’s modern portfolio theory can be enhanced by machine learning models that adapt dynamically to market volatility.

d. High-Frequency Trading (HFT)

In high-frequency trading, AI algorithms execute thousands of trades per second based on micro-movements in prices. ML models process real-time market data streams and make ultra-fast trading decisions with minimal human intervention.

e. Risk Management and Anomaly Detection

AI systems monitor trading patterns to identify abnormal behavior, potential fraud, or risk exposure. These models help financial institutions comply with regulations and safeguard investor assets.

6. Benefits of AI and ML in Forecasting

Accuracy and Efficiency: AI models can analyze vast datasets quickly and produce precise forecasts.

Adaptability: They adjust to evolving market dynamics without manual recalibration.

Automation: Reduces human error and enables algorithmic trading.

Sentiment Integration: Incorporates behavioral and psychological aspects of markets.

Continuous Learning: Models improve over time as they process more data.

AI thus empowers traders, analysts, and institutions to make data-driven decisions and respond rapidly to market changes.

7. Challenges and Limitations

Despite their promise, AI and ML in stock forecasting face certain limitations:

Data Quality Issues: Inaccurate or biased data can mislead models.

Overfitting: ML models may perform well on training data but fail in real-world scenarios.

Black-Box Nature: Many AI models lack transparency in how they generate predictions, posing trust issues.

Market Unpredictability: Events like political crises, pandemics, or natural disasters can disrupt models trained on historical data.

Ethical and Regulatory Concerns: Use of AI-driven trading can lead to market manipulation or flash crashes if not monitored.

Hence, human oversight remains essential even in AI-based systems.

8. Future of AI and ML in Financial Forecasting

The future of AI in finance lies in hybrid models — combining human expertise with machine intelligence. Emerging technologies such as Quantum Computing, Explainable AI (XAI), and Federated Learning will further enhance forecasting capabilities.

Moreover, integration of blockchain data, real-time global sentiment, and predictive analytics will make AI-driven models more robust and transparent.

In the coming years, AI systems are expected to play a central role not just in forecasting but also in risk management, compliance automation, and personalized investment advice through robo-advisors.

9. Conclusion

AI and Machine Learning have transformed the way investors, institutions, and analysts approach the stock market. From pattern recognition and sentiment analysis to autonomous trading and portfolio optimization, these technologies offer powerful tools for understanding and predicting market behavior.

While challenges such as data quality, overfitting, and transparency remain, continuous advancements in AI research promise more reliable and interpretable forecasting systems. Ultimately, the combination of human insight and AI-driven analytics represents the future of intelligent investing — where data, algorithms, and human judgment work hand in hand to navigate the ever-changing financial markets.

The Psychology Behind Winning TradesThe Psychology Behind Winning Trades 🧠💹✨

Introduction – Hook:

📊 “Why do some traders consistently win 💰 while others struggle 💔?”

It’s rarely the strategy—it’s the mindset behind the trade! 🧠🌟

Your emotions, thoughts, and biases control your decisions, even with perfect technical skills. 🎯

1️⃣ What is Trading Psychology?

Trading psychology is the study of how emotions and mental habits affect trading decisions. 🌈🧘♂️

It’s about understanding:

How fear 😨, greed 😍, or impatience ⏳ impacts your trades

Why you sometimes ignore your rules 📝

How discipline 💪 can make the difference between profit 🏆 and loss 💸

💡 Tip: Even the best strategies fail if your mind isn’t in control. 🧠✨

2️⃣ Common Psychological Traps & How They Appear in Trades

Trap Emoji Effect Example in Trading

Fear 😨 Exiting too early Closing a winning trade because you’re scared of losing profits 💔

Greed 😍 Holding losing trades Waiting for a loss to “come back” and losing more money 💸

FOMO 🏃♂️💨 Jumping impulsively Entering trades last minute because everyone else is trading 🚀

Revenge Trading 😤🔥 Emotional loss-chasing Trying to recover losses by taking bigger, risky trades 💣

💡 Insight: Recognizing these emotions is the first step to controlling them. 🌟

3️⃣ How to Master Your Trading Mind

1️⃣ Pre-Trade Preparation 🧘♀️✅

Check your emotional state before trading 🕊️

Confirm your trade plan is clear 📋✨

2️⃣ During the Trade ✋🎯

Stick to your rules, don’t let emotions take over 💪🔥

Avoid impulsive exits or entries ⏱️❌

3️⃣ Post-Trade Reflection 📖🖊️

Keep a Trading Journal: note emotions, mistakes & wins ✨📓

Review trades to improve your mindset over time 📈🌟

4️⃣ Pro Tips for Winning Psychology

🔥 Mindset Checklist:

Am I trading calmly? 😌💭

Am I following my plan? 📋✅

Am I chasing losses or profits emotionally? ⚖️💡

💡 Daily Mindset Practice: Meditation 🧘♂️, journaling ✍️, or reviewing trades 📊 can help you stay disciplined under pressure 💎🌟

5️⃣ Why It Matters

Trading without psychology = strategy leaks money 💸💨

Emotional control = consistency, higher win rates, confidence 🏆💪

Professionals don’t just trade charts—they trade themselves 🧠✨

6️⃣ Engagement Section

👇 Question for your audience:

“What’s the biggest psychological trap YOU’ve faced in trading? Share your story below! 💬💭💖”

Banknifty Premium ChartWhat is Option Premium?

It’s the cost of an option contract.

When you buy an option, you pay the premium upfront.

Example: If you buy a Call Option of Reliance ₹2800 at ₹50 premium — you pay ₹50 × lot size.

Who Receives It?

The option seller (writer) receives the premium income immediately when they sell (write) the option.

Explain: Candle PatternWhat is a Candlestick Pattern?

A candlestick pattern represents the price movement of an asset (like a stock) during a specific time frame. It shows open, high, low, and close prices in one candle.

Structure of a Candle

Each candle has:

Body: The range between open and close price.

Wick (or shadow): The lines above and below the body showing high and low prices.

Color: Green (bullish – price up) or Red (bearish – price down).

Part 4 Learn Institutional TradingAdvantages of Option Trading

Leverage:

Options allow control over large quantities of an asset with a small investment (premium). This magnifies potential profits.

Limited Risk for Buyers:

When buying options, the maximum loss is limited to the premium paid.

Hedging Capability:

Options can offset potential losses in the underlying portfolio.

Flexibility:

Options can be combined in various strategies to suit market outlooks—bullish, bearish, or neutral.

Multiple Strategies:

Options offer numerous strategies like straddles, strangles, spreads, collars, and iron condors, giving traders the ability to profit in different market conditions.

Part 3 Learn Institutional Trading Purpose of Option Trading

Option trading serves three main purposes:

Hedging (Risk Management):

Investors use options to protect their portfolios against adverse price movements. For instance, if you hold a stock, buying a put option acts as insurance—allowing you to sell the stock at a predetermined price even if the market crashes.

Speculation:

Traders use options to bet on future market direction. Options allow traders to gain exposure with limited capital, as the premium is usually a fraction of the asset’s full price.

Income Generation:

Investors can sell (write) options to earn premiums. For example, selling covered calls against owned stocks generates additional income, even if the stock price remains stable.

Part 2 Ride The Big Moves How Option Prices Are Determined

Option prices are influenced by several factors. The most common model used to calculate the theoretical value of an option is the Black-Scholes Model. The key factors that affect option prices include:

Underlying Asset Price: The higher the price of the asset, the higher the value of a call option and the lower the value of a put option.

Strike Price: The difference between the strike and current market price affects the intrinsic value of the option.

Time to Expiration: The more time left until expiration, the higher the premium (because there’s more time for the option to become profitable).

Volatility: Higher volatility increases option premiums since the chance of large price movement rises.

Interest Rates and Dividends: These can slightly influence option values, especially for longer-term options.

Part 1 Ride The Big Moves How Option Trading Works

Option trading involves four basic positions:

Buy Call (Long Call): The trader expects the underlying asset’s price to rise.

Sell Call (Short Call): The trader expects the price to stay the same or fall.

Buy Put (Long Put): The trader expects the underlying asset’s price to fall.

Sell Put (Short Put): The trader expects the price to stay the same or rise.

For example, if a trader buys a call option on a stock with a strike price of ₹100 and pays a premium of ₹5, they have the right to buy the stock at ₹100 even if it rises to ₹120. In this case, their profit per share would be ₹15 (₹120 - ₹100 - ₹5). However, if the stock remains below ₹100, they would not exercise the option and would lose only the premium of ₹5.

Part 2 Support and Reistance Key Terminology in Option Trading

Before diving deeper, it’s important to understand the essential terms used in option trading:

Strike Price: The fixed price at which the holder can buy (call) or sell (put) the underlying asset.

Premium: The price paid by the option buyer to the seller for the contract.

Expiration Date: The date on which the option contract expires. After this date, the option becomes worthless if not exercised.

In-the-Money (ITM): A call option is ITM when the underlying price is above the strike price; a put option is ITM when the underlying price is below the strike price.

Out-of-the-Money (OTM): A call option is OTM when the underlying price is below the strike price; a put option is OTM when the underlying price is above the strike price.

At-the-Money (ATM): When the underlying asset price equals the strike price.

Underlying Asset: The financial instrument (stock, index, currency, or commodity) on which the option is based.

Part 1 Support and Resistance What Are Options?

An option is a financial contract between two parties: the buyer (also called the holder) and the seller (also called the writer). The buyer pays a premium to the seller in exchange for the right to buy or sell the underlying asset at a specified strike price before or on a specified expiration date.

There are two main types of options:

Call Option – gives the buyer the right to buy the underlying asset at the strike price.

Put Option – gives the buyer the right to sell the underlying asset at the strike price.